Filed pursuant to Rule 424(b)(3)

Registration Statement No. 333-146364

Prospectus Supplement

Interests in

KAISER FEDERAL BANK

EMPLOYEES’ SAVINGS & PROFIT SHARING PLAN AND TRUST

Offering of Participation Interests in up to 277,900 Shares of

KAISER FEDERAL FINANCIAL GROUP, INC.

Common Stock

In connection with the conversion of K-Fed Mutual Holding Company from the mutual to the stock form of organization, Kaiser Federal Financial Group, Inc. is allowing its employees who are participants in the Kaiser Federal Bank Employees’ Savings & Profit Sharing Plan and Trust (the “Plan”) to invest all or a portion of their accounts in stock units representing an ownership interest in the common stock of Kaiser Federal Financial Group, Inc. (the “Common Stock”). Kaiser Federal Financial Group, Inc. has registered a number of participation interests through the Plan in order to enable the trustee of the Plan to purchase up to 277,900 shares of the Common Stock, assuming a purchase price of $10.00 per share. As a participant in the Plan, you may direct the trustee of the Plan to purchase Common Stock in the stock offering by transferring amounts currently allocated to your account under the Plan to the Employer Stock Fund (other than amounts you presently have invested in the Employer Stock Fund).

The prospectus of Kaiser Federal Financial Group, Inc., dated November 9, 2007, accompanies this prospectus supplement. It contains detailed information regarding the conversion and stock offering of Kaiser Federal Financial Group, Inc. Common Stock and the financial condition, results of operations and business of K-Fed Bancorp, Inc. This prospectus supplement provides information regarding the Plan. You should read this prospectus supplement together with the prospectus and keep both for future reference.

For a discussion of risks that you should consider, see “Risk Factors” in the prospectus.

The interests in the Plan and the offering of Common Stock have not been approved or disapproved by the Office of Thrift Supervision, the Securities and Exchange Commission or any other federal or state agency. Any representation to the contrary is a criminal offense.

The securities offered in this prospectus supplement and in the prospectus are not deposits or accounts and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

This prospectus supplement may be used only in connection with offers and sales by Kaiser Federal Financial Group, Inc. of interest or shares of Common Stock pursuant to the Plan. No one may use this prospectus supplement to re-offer or resell interests or shares of Common Stock acquired through the Plan.

You should rely only on the information contained in this prospectus supplement and the accompanying prospectus. Kaiser Federal Financial Group, Inc. and the Plan have not authorized anyone to provide you with information that is different.

This prospectus supplement does not constitute an offer to sell or solicitation of an offer to buy any securities in any jurisdiction to any person to whom it is unlawful to make an offer or solicitation in that jurisdiction. Neither the delivery of this prospectus supplement and the prospectus nor any sale of Common Stock shall under any circumstances imply that there has been no change in the affairs of Kaiser Federal Financial Group, Inc. or any of its subsidiaries or the Plan since the date of this prospectus supplement, or that the information contained in this prospectus supplement or incorporated by reference is correct as of any time after the date of this prospectus supplement.

The date of this prospectus supplement is November 9, 2007.

TABLE OF CONTENTS

|

|

i | |

i | |

Election to Purchase Common Stock in the Offering: Priorities | ii |

iii | |

iv | |

iv | |

iv | |

v | |

v | |

v | |

v | |

vi | |

vi | |

1 | |

1 | |

1 | |

2 | |

2 | |

2 | |

3 | |

3 | |

6 | |

11 | |

12 | |

12 | |

13 | |

13 | |

15 | |

Securities and Exchange Commission Reporting and Short-Swing Profit Liability | 15 |

16 | |

16 |

|

|

|

|

|

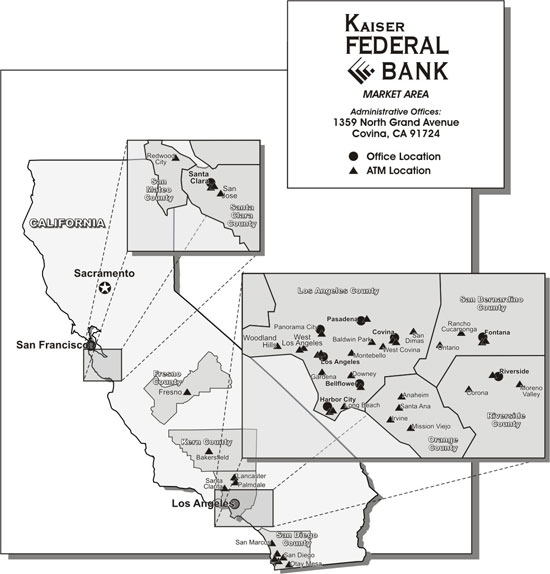

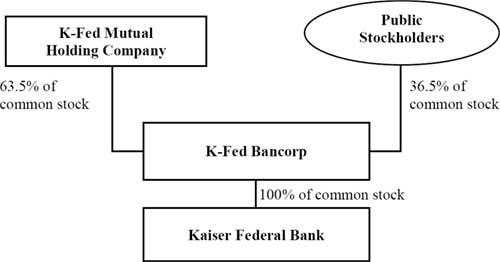

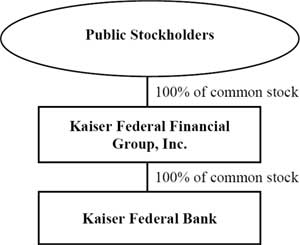

| As a result of the conversion, Kaiser Federal Financial Group, Inc. will replace K-Fed Bancorp as the parent company of Kaiser Federal Bank. In connection with the conversion and “second step” offering of shares of Kaiser Federal Financial Group, Inc. to the public, participants in the Kaiser Federal Bank Employees’ Savings & Profit Sharing Plan and Trust (the “Plan”) have the opportunity to purchase employer stock units (“stock units”) as an investment alternative in the Plan. Stock units represent indirect ownership of Kaiser Federal Financial Group, Inc. through the Plan. In the offering, a stock unit will consist of 100% Common Stock of Kaiser Federal Financial Group, Inc. After the offering, a stock unit will consist of approximately 95% shares of Kaiser Federal Financial Group, Inc. Common Stock and 5% cash. Given the $10 per unit price in the offering, at August 15, 2007, there were sufficient funds in the Plan (excluding funds invested in the existing Employer Stock Fund) to purchase up to approximately 277,900 shares of Kaiser Federal Financial Group, Inc. Common Stock in the offering. The shares of K-Fed Bancorp common stock currently held in the existing Employer Stock Fund in the Plan will be exchanged (within the Employer Stock Fund) for shares of Kaiser Federal Financial Group, Inc. Common Stock pursuant to an exchange ratio, as is more fully discussed in “The Conversion and Offering” section of the prospectus. Only employees of Kaiser Federal Bank may participate in the Plan. Your investment in the Common Stock of Kaiser Federal Financial Group, Inc. through the Plan in the offering is subject to the priorities listed below. Information with regard to the Plan is contained in this prospectus supplement and information with regard to the financial condition, results of operations and business of K-Fed Bancorp is contained in the accompanying prospectus. The address of the principal executive office of Kaiser Federal Financial Group, Inc. is 1359 North Grand Avenue, Covina, California 91724. | |||

|

|

| ||

|

| All elections to purchase stock units in the stock offering under the Plan and any questions about this prospectus supplement should be addressed to Mary Templin, Human Resources/Benefits Administrator, 1359 North Grand Avenue, Covina, California 91724, telephone number: (626)339-9663, extension 1252; fax: (626) 858-5745; email: m.templin@kffg.com. | ||

i

|

|

|

|

|

| In connection with the conversion and stock offering, you may elect to transfer, by whole percentages, all or part of your account balances in the Plan (other than the amounts you currently have invested in the existing Employer Stock Fund) to the new Employer Stock Fund, to be used to purchase Common Stock of Kaiser Federal Financial Group, Inc. issued in the offering. The trustee of the Employer Stock Fund will purchase Common Stock to be held as stock units in accordance with your directions. However, such directions are subject to purchase limitations in the plan of conversion and reorganization of K-Fed Mutual Holding Company. | |||

|

|

|

|

|

|

| The shares of Common Stock are being offered at $10 per share in a subscription offering and community offering. In the offering, the purchase priorities are as follows: | ||

|

|

|

|

|

|

| Subscription Offering: | ||

|

|

| ||

|

|

| (1) | Depositors of Kaiser Federal Bank with $50 or more as of the close of business on March 31, 2006, get first priority. |

|

|

| (2) | Kaiser Federal Bank and Kaiser Federal Financial Group, Inc.’s tax-qualified plans, including the employee stock ownership plan and 401(k) plan, get second priority. |

|

|

| (3) | Depositors of Kaiser Federal Bank with $50 or more on deposit as of the close of business on September 30, 2007, get third priority. |

|

|

| (4) | Depositors of Kaiser Federal Bank as of October 31, 2007 get fourth priority. |

|

|

|

|

|

|

| Community Offering: | ||

|

|

|

|

|

|

|

| (5) | Residents of Los Angeles, San Bernardino, Riverside and Santa Clara Counties, California, get fifth priority. |

|

|

|

|

|

|

|

| (6) | Public stockholders of K-Fed Bancorp as of November 14, 2007 get sixth priority. |

|

|

|

|

|

|

|

| (7) | Persons who do not qualify under any other priority listed above get last priority. |

|

|

| ||

|

| If you are an eligible depositor in the subscription offering, as listed above, you will separately receive offering materials in the mail, including a Stock Order Form. If you wish to purchase stock outside of the Plan, you must complete and submit the Stock Order Form and payment, using the reply envelope provided. | ||

|

|

| ||

|

| Additionally, or instead of placing an order outside of the Plan | ||

ii

|

|

|

|

|

|

| through a Stock Order Form, as a Plan participant, you may place an order for stock units through the Plan, using the enclosed Special Election Form, to be completed and submitted in the manner described on the next page. If you are a participant in the Plan who is eligible in priority one (depositor of Kaiser Federal Bank with $50 or more on deposit at March 31, 2006), your Special Election Form order will receive priority one treatment. If you are not eligible in priority one, your Special Election Form order will receive priority two treatment, as an order in a tax-qualified plan of Kaiser Federal Bank. | ||

|

|

|

|

|

|

| No later than the subscription offering period deadline, the amount that you elect to transfer from your existing account balances for the purchase of Common Stock in the offering will be removed from your existing accounts and transferred to an interest-bearing money market account in the Plan, pending the closing of the offering. | ||

|

|

|

|

|

|

| At the closing of the offering, the amount that you have transferred to purchase stock in the offering will be placed in the new Employer Stock Fund and allocated to your Plan account. | ||

|

|

|

|

|

|

| Once the offering is closed, any amounts that you elected to apply towards the purchase of stock units in the offering will appear in your new Employer Stock Fund balance when you access your account via the internet or by telephone. The formal closing of the offering is expected to be in late December, 2007 or January, 2008. Note that any amount that you have invested in the existing Employer Stock Fund will continue to exist, as Kaiser Federal Financial Group, Inc. stock units within the existing Employer Stock Fund until the existing Employer Stock Fund is eventually merged with the new Employer Stock Fund. See page 10 for additional information. | ||

|

|

|

|

|

|

| If you choose not to direct the investment of your account balances towards the purchase of any shares of Common Stock in the offering, your account balances will remain in the investment funds of the Plan as previously directed by you. | ||

|

|

|

|

|

| The new Employer Stock Fund will initially invest 100% in the Common Stock of Kaiser Federal Financial Group, Inc. After the closing of the stock offering, the new Employer Stock Fund will maintain a cash component for liquidity purposes. Liquidity is required in order to facilitate daily transactions such as investment transfers or distributions from the new Employer Stock Fund. Following the closing of the stock offering, the new Employer Stock Fund will consist of approximately 95% Common Stock and 5% | |||

iii

|

|

|

|

|

|

| cash. A unit of the new Employer Stock Fund (known as a “stock unit”) will be initially valued at $10. Newly issued stock units will consist of a percentage interest in both the Common Stock and cash held in the new Employer Stock Fund. Unit values (similar to the stock’s share price) and the number of units (similar to number of shares) will be used to communicate the dollar value of a participant’s account. Following the stock offering, each day, the stock unit value of the new Employer Stock Fund will be determined by dividing the total market value of the Employer Stock Fund at the end of the day by the total number of units held in the Employer Stock Fund by all participants as of the previous day’s end. The change in stock unit value reflects the day’s change in stock price, any cash dividends accrued and the interest earned on the cash component of the Employer Stock Fund, less any investment management fees. The market value and unit holdings of your account in the new Employer Stock Fund will be reported to you on your regular Plan participant statements. Note that any amount that you have invested in the existing Employer Stock Fund (which holds shares of Common Stock of K-Fed Bancorp and cash) will continue to be shown as being invested in the existing Employer Stock Fund until the existing Employer Stock Fund is eventually merged with the new Employer Stock Fund (which holds shares of Kaiser Federal Financial Group, Inc. Common Stock.) | ||

|

|

|

|

|

| As of August 15, 2007, the market value of the assets of the Plan, excluding the existing Employer Stock Fund, was approximately $2,779,000. | |||

|

|

|

|

|

| Accompanying this supplement is a Special Election Form on which you can elect to transfer all or a portion of your account balance in the Plan to the new Employer Stock Fund for the purchase of stock units in the offering (other than amounts you currently have invested in such fund). If you wish to use all or part of your account balance in the Plan to purchase Common Stock issued in the offering (other than amounts you currently have invested in the Employer Stock Fund), you should indicate that decision on the Special Election Form.If you do not wish to purchase stock units in the offering through the Plan, you should check Box 7 on page 2 of the Special Election Form and return the form to Mary Templin as instructed below. | |||

|

|

|

|

|

| If you wish to purchase Common Stock with your Plan account balances, your Special Election Form must bereceived by Mary Templin, Human Resources/Benefits Administrator, 1359 North Grand Avenue, Covina, California 91724, telephone number (626) 339-9663, extension 1252; fax (626) 858-5745; email: m.templin@kffg.com no later than 5:00 p.m. on December 4, 2007. | |||

iv

|

|

|

|

|

|

| To allow for processing, this deadline is prior to the subscription offering period deadline (which is December 11, 2007). If you have any questions with respect to the Special Election Form, please contact Mary Templin. | ||

|

|

|

|

|

| You may not revoke your Special Election Form once it has been delivered to Mary Templin. You will, however, continue to have the ability to transfer amounts not directed towards the purchase of stock in the offering among all of the other investment funds, including the existing Employer Stock Fund, on a daily basis. | |||

|

|

|

|

|

| Whether or not you choose to purchase stock in the offering through the Plan, you will at all times have complete access to those amounts in your account that you donot apply towards purchases in the offering. For example, you will be able to purchase other funds within the Plan with that portion of your account balance that you do not apply towards purchases in the offering during the offering period. Such purchases will be made at the prevailing market price in the same manner as you make such purchases now,i.e., through telephone transfers and internet access to your account. You can only purchase stock units in the offering through the Plan by returning your Special Election Form to Mary Templin by the due date. You cannot purchase stock units in the offering by means of telephone transfers or the internet. That portion of your Plan account balance that you elect to apply towards the purchase of stock units in the offering will be irrevocably committed to such purchase. | |||

|

|

|

|

|

| After the offering, you will again have complete access to any amount that you directed towards the purchase of shares of Common Stock in the offering. For example, after the offering closes, you may sell any shares that you purchased in the offering. Special restrictions may apply to transfers directed to and from the Employer Stock Fund by the participants who are subject to the provisions of section 16(b) of the Securities Exchange Act of 1934, as amended, relating to the purchase and sale of securities by officers, directors and principal shareholders of Kaiser Federal Financial Group, Inc. | |||

|

|

|

|

|

| The trustee will pay $10.00 per stock unit, which will be the same price paid by all other persons for a share of Common Stock in the offering. No sales commision will be charged for Common Stock purchased through stock units in the offering. | |||

|

|

|

|

|

|

| After the offering, the trustee will acquire Common Stock in open market transactions at the prevailing price. The trustee will pay transaction fees, if any, associated with the purchase, sale or transfer | ||

v

|

|

|

|

|

|

| of the Common Stock after the offering. | ||

|

|

|

|

|

| The trustee will hold the stock units in trust for the participants of the Plan. Stock units acquired by the trustee at your direction will be allocated to your account. Therefore, investment decisions of other participants should not affect the earnings allocated to your account. | |||

|

|

|

|

|

| The trustee generally will exercise voting rights attributable to all Common Stock held by the existing Employer Stock Fund and the new Employer Stock Fund, as directed by participants with accounts invested in the fund. When stockholders have a right to vote on a matter, you will be allocated voting instruction rights reflecting your proportionate interest in the existing or new Employer Stock Fund. The trustee will vote the Common Stock in the existing or new Employer Stock Fund affirmatively or negatively on each matter, in proportion to the voting instructions the trustee receives from participants. In connection with the conversion of K-Fed Mutual Holding Company, Plan participants who had shares of K-Fed Bancorp allocated to their accounts in the Plan on November 14, 2007, soon will receive a packet of material containing, among other things, a Proxy Statement-Prospectus, Confidential 401(k) Plan Voting Instruction Letter and Confidential 401(k) Plan Vote Authorization Form. The Confidential 401(k) Plan Voting Instruction Letter will provide instructions on completing the Confidential 401(k) Plan Vote Authorization Form so that the trustee can vote the shares of Common Stock attributable to your account at the Annual Stockholder Meeting on December 18, 2007. | |||

|

|

|

|

|

|

| If you are a participant who has voting rights (as discussed above), you will need to complete the Confidential 401(k) Plan Vote Authorization Form and return it in the self-addressed stamped envelope provided to you, if you want the trustee to vote in accordance with your voting instructions. | ||

|

|

|

|

|

vi

Kaiser Federal Bank adopted the Kaiser Federal Bank Retirement Savings Plan, dated December 31, 2002, and amended it into the Kaiser Federal Bank Employees’ Savings & Profit Sharing Plan and Trust, effective January 1, 2004 (referred to as the “Plan”). The Plan is a tax-qualified plan with a cash or deferred compensation feature established in accordance with the requirements under Section 401(a) and Section 401(k) of the Internal Revenue Code of 1986, as amended (the “Code”).

Kaiser Federal Bank intends that the Plan, in operation, will comply with the requirements under Section 401(a) and Section 401(k) of the Code. Kaiser Federal Bank will adopt any amendments to the Plan that may be necessary to ensure the continuing qualified status of the Plan under the Code and applicable Treasury Regulations.

Employee Retirement Income Security Act of 1974 (“ERISA”). The Plan is an “individual account plan” other than a “money purchase pension plan” within the meaning of ERISA. As such, the Plan is subject to all of the provisions of Title I (Protection of Employee Benefit Rights) and Title II (Amendments to the Code Relating to Retirement Plans) of ERISA, except to the funding requirements contained in Part 3 of Title I of ERISA which by their terms do not apply to an individual account plan (other than a money purchase plan). The Plan is not subject to Title IV (Plan Termination Insurance) of ERISA. The funding requirements contained in Title IV of ERISA are not applicable to participants or beneficiaries under the Plan.

Reference to Full Text of Plan.The following portions of this prospectus supplement summarize certain provisions of the Plan. They are not complete and are qualified in their entirety by the full text of the Plan. Copies of the Plan are available to all employees by filing a request with the Plan administrator c/o Kaiser Federal Bank, Attn: Mary Templin, Human Resources/Benefits Administrator, 1359 North Grand Avenue, Covina, California 91724; telephone number: (626) 339-9663, extension 1252; fax: (626) 858-5745; email: m.templin@kffg.com. You are urged to read carefully the full text of the Plan.

If you are a regular employee of Kaiser Federal Bank, you are eligible to become a participant in the Plan on January 1, April 1, July 1, or October 1 coinciding with or next following the date you attain age 21. You become eligible to receive employer contributions upon attainment of age 21 and completion of 12 consecutive months of service. The Plan Year is July 1 to June 30 (“Plan Year”).

As of August 15, 2007, there were approximately 144 employees, former employees and beneficiaries eligible to participate in the Plan.

401(k) Plan Contributions.You are permitted to defer on a pre-tax basis up to 15% of your monthly salary (expressed in terms of whole percentages), subject to certain restrictions imposed by the Code, and to have that amount contributed to the Plan on your behalf. For purposes of the Plan, “salary” means your total taxable compensation as reported on Form W-2 (exclusive of any compensation deferred from a prior year). In 2007, the annual salary of each participant taken into account under the Plan is limited to $225,000. (Limits established by the Internal Revenue Service are subject to increase pursuant to an annual cost-of-living adjustment, as permitted by the Code). You may elect to modify the amount contributed to the Plan by filing a new elective deferral agreement with the Plan administrator once per calendar quarter.

Employer Matching Contributions.Kaiser Federal Bank makes matching contributions of 50% of your contributions to the Plan, up to 10% of your salary.

Limitations on Employee Salary Deferrals. For the Plan Year beginning July 1, 2007, the amount of your before-tax contributions may not exceed $15,500 per year. Contributions in excess of this limit are known as excess deferrals. If you defer amounts in excess of this limitation, your gross income for federal income tax purposes will include the excess in the year of the deferral. In addition, unless the excess deferral is distributed within 2 ½ months after the end of the plan year for which the deferral was made, , it will be taxed again in the year distributed. In addition, income on the excess deferrals that are distributed within 2 ½ months after the end of the plan year for which the deferral was made will be treated, for federal income tax purposes, as earned and received by you in the tax year for which the excess deferral was made.

Catch-up Contributions.If you have made the maximum amount of regular before-tax contributions allowed by the Plan or other legal limits and you have attained at least age 50 (or will reach age 50 prior to the end of the Plan Year), you are also eligible to make an additional catch-up contribution. You may authorize your employer to withhold a specified dollar amount of your compensation for this purposes. For 2007, the maximum catch-up contribution is $5,000.

Vesting.At all times, you have a fully vested, nonforfeitable interest in the 401(k) deferrals you have made and any earnings related thereto. Employer contributions vest in accordance with the following schedule:

2

|

|

|

|

|

Completed |

|

| Vested |

|

|

|

| ||

Less than 2 |

|

| 0 |

|

2 but less than 3 |

|

| 20 | % |

3 but less than 4 |

|

| 40 | % |

4 but less than 5 |

|

| 60 | % |

5 but less than 6 |

|

| 80 | % |

6 or more |

|

| 100 | % |

Investment of Contributions and Account Balances

All amounts credited to your accounts under the Plan are held in the Plan trust (the “Trust”) which is administered by the trustee appointed by Kaiser Federal Bank’s Board of Directors.

Prior to the effective date of the offering, you were provided the opportunity to direct the investment of your account into one of the following funds:

|

|

1. | International Stock Fund |

2. | NASDAQ 100 Stock Fund |

3. | Russell 2000 Stock Fund |

4. | S&P MidCap Stock Fund |

5. | S&P/Growth Stock Fund |

6. | S&P/Value Stock Fund |

7. | S&P 500 Stock Fund |

8. | US REIT Index Fund |

9. | Long Treasury Index Fund |

10. | Aggregate Bond Index Fund |

11. | Stable Value Fund |

12. | Short Term Investment Fund |

13. | Income Plus Asset Allocation Fund |

14. | Growth and Income Asset Allocation Fund |

15. | Growth Asset Allocation Fund |

16. | SSgA Target Retirement 2015 Fund |

17. | SSgA Target Retirement 2025 Fund |

18. | SSgA Target Retirement 2035 Fund |

19. | SSgA Target Retirement 2045 Fund |

20. | Employer Stock Fund |

The following table provides performance data with respect to the investment funds available under the Plan through July 31, 2007:

3

FUND RETURNS THROUGH JULY 31, 20071

|

|

|

|

|

|

|

|

|

|

|

|

Stock Funds |

| Monthly |

| Year to |

| Last 12 |

| 5 Calendar |

| 10 Calendar |

|

|

|

|

|

|

| ||||||

INTERNATIONAL STOCK FUND1,2 |

| -1.5 | % | 8.8 | % | 23.2 | % | 18.6 | % | 6.5 | % |

Benchmark: MSCI EAFE Index |

| -1.5 | % | 9.1 | % | 23.9 | % | 19.9 | % | 7.4 | % |

NASDAQ 100 STOCK FUND3 |

| -0.1 | % | 9.7 | % | 27.3 | % | 14.5 | % | 5.2 | % |

Benchmark: NASDAQ 100 Index |

| -0.1 | % | 10.2 | % | 28.6 | % | 15.1 | % | 5.8 | % |

RUSSELL 2000 STOCK FUND4 |

| -6.9 | % | -1.1 | % | 11.6 | % | 15.3 | % | 7.2 | % |

Benchmark: Russell 2000 Index |

| -6.8 | % | -0.8 | % | 12.1 | % | 16.0 | % | 7.8 | % |

S&P MIDCAP STOCK FUND5 |

| -4.3 | % | 6.8 | % | 16.1 | % | 15.0 | % | 11.3 | % |

Benchmark: S&P MidCap 400 Index |

| -4.3 | % | 7.2 | % | 16.7 | % | 15.5 | % | 11.8 | % |

S&P/GROWTH STOCK FUND4 |

| -2.3 | % | 3.8 | % | 15.9 | % | 8.6 | % | 3.8 | % |

Benchmark: S&P 500/Citigroup Growth Index |

| -2.2 | % | 4.2 | % | 16.5 | % | 9.2 | % | 4.4 | % |

S&P/VALUE STOCK FUND4 |

| -4.0 | % | 2.8 | % | 15.0 | % | 13.8 | % | 6.5 | % |

Benchmark: S&P 500/Citigroup Value Index |

| -3.9 | % | 3.2 | % | 15.8 | % | 14.5 | % | 7.1 | % |

S&P 500 STOCK FUND5 |

| -3.1 | % | 3.3 | % | 15.5 | % | 11.2 | % | 5.4 | % |

Benchmark: S&P 500 Index |

| -3.1 | % | 3.6 | % | 16.1 | % | 11.8 | % | 6.0 | % |

US REIT INDEX FUND6 |

| -7.9 | % | -13.7 | % | -1.4 | % | 15.1 | % | N/A |

|

Benchmark: Dow Jones/Wilshire REIT Index |

| -7.8 | % | -13.4 | % | -0.6 | % | 18.6 | % | 12.7 | % |

Bond Funds |

|

|

|

|

|

|

|

|

|

|

|

LONG TREASURY INDEX FUND5 |

| 2.6 | % | 1.4 | % | 6.1 | % | 5.7 | % | 6.6 | % |

Benchmark: Lehman Bros Long Treasury Index |

| 2.7 | % | 1.8 | % | 6.8 | % | 6.3 | % | 7.2 | % |

AGGREGATE BOND INDEX FUND9 |

| 0.8 | % | 1.5 | % | 4.9 | % | 3.8 | % | n.a. |

|

Benchmark: Lehman Brothers Aggregate Bond Index |

| 0.8 | % | 1.8 | % | 5.6 | % | 4.4 | % | 5.8 | % |

Fixed Income Funds |

|

|

|

|

|

|

|

|

|

|

|

STABLE VALUE FUND7 |

| 0.3 | % | 2.2 | % | 3.9 | % | 4.0 | % | 4.9 | % |

Benchmark: Ryan Labs 3 Yr. GIC |

| 0.4 | % | 2.5 | % | 4.2 | % | 4.0 | % | 5.1 | % |

SHORT TERM INVESTMENT FUND5 |

| 0.4 | % | 2.9 | % | 5.0 | % | 2.6 | % | 3.7 | % |

Benchmark: Citigroup 3 Month Treasury Bill |

| 0.4 | % | 2.9 | % | 5.1 | % | 2.7 | % | 3.7 | % |

Asset Allocation Funds2,8 |

|

|

|

|

|

|

|

|

|

|

|

INCOME PLUS ASSET ALLOCATION FUND |

| -0.2 | % | 2.1 | % | 7.6 | % | 6.5 | % | 5.1 | % |

GROWTH AND INCOME ASSET ALLOCATION FUND |

| -1.4 | % | 3.0 | % | 11.2 | % | 9.5 | % | 5.7 | % |

GROWTH ASSET ALLOCATION FUND |

| -2.6 | % | 3.8 | % | 14.8 | % | 12.2 | % | 5.7 | % |

Target Retirement Funds10 |

|

|

|

|

|

|

|

|

|

|

|

SSgA TARGET RETIREMENT 2015 FUND |

| N/A |

| N/A |

| N/A |

| N/A |

| N/A |

|

SSgA TARGET RETIREMENT 2025 FUND |

| N/A |

| N/A |

| N/A |

| N/A |

| N/A |

|

SSgA TARGET RETIREMENT 2035 FUND |

| N/A |

| N/A |

| N/A |

| N/A |

| N/A |

|

SSgA TARGET RETIREMENT 2045 FUND |

| N/A |

| N/A |

| N/A |

| N/A |

| N/A |

|

EMPLOYER STOCK FUND |

| -15.1 | % | -28.2 | % | -11.54 | % | N/A |

| N/A |

|

4

Returns are shown net of fees. Dividends and interest are automatically reinvested. Past performance is no guarantee of future performance. Total expenses charged to each fund, as a percentage of each fund’s estimated average assets per year, are as follows: International Stock Fund 0.720%; Nasdaq 100 Stock Fund 0.594%; Russell 2000 Stock Fund 0.594%; S&P MidCap Stock Fund 0.594%; S&P Growth Stock Fund 0.594%; S&P Value Stock Fund 0.594%; S&P 500 Stock Fund 0.594%; Long Treasury Index Fund 0.670%; Aggregate Bond Index Fund 0.670%; REIT Fund 0.670%; Stable Value Fund 0.621%; Short Term Investment Fund 0.450%; Target Retirement Fund 0.92%. Unit values are determined as of the last business day of each month. Benchmark indices are not investment funds and have no fees. See following notes.

State Street Global Investors (SSgA) is the Investment Manager for all Funds and is the provider of benchmark index returns. Historical returns of the index funds reflect management by Barclays Global Investors (BGI) before November 4, 2005 and SSgA’s management thereafter.

1 Prior to September 30, 1999, this Fund was limited to no more than 25% exposure to Japan.

2 The Asset Allocation Funds and the International Stock Fund were first offered July 2, 1997. Returns prior to inception are simulated using the returns of market indices for, or actual funds of, the Fund’s investment components, and are net of fees.

3The Nasdaq 100 Stock Fund was first offered on May 1, 2002, while BGI’s underlying Nasdaq 100 Fund was initially offered on August 7, 2000. Returns prior to May 1, 2002 are based on returns of the then-existing BGI funds (when available) and on the (hypothetical) returns of the Nasdaq 100 Index for periods prior to the inception date of the BGI fund. All returns are net of fees.

4The Russell 2000, S&P 500/Growth and S&P 500/Value Stock Funds were first offered on January 4, 2000. Returns prior to January 4, 2000 are hypothetical and are based on the returns of the then-existing BGI funds, and are net of fees. Effective December 16, 2005, the S&P 500/Barra Growth and S&P 500/Barra Value indexes were reconstituted as the S&P 500/Citigroup Growth and S&P500/Citigroup Value Indexes. Additional information can be found atwww.styleindices.standardandpoors.com

5 The S&P MidCap, S&P 500, Long Treasury Index and Short Term Investment Funds were first offered on June 17, 1997. Results prior to that date are hypothetical, based on previous investment returns of the then-existing BGI funds, and are net of fees.

6 The US REIT Index Fund was first offered on January 1, 2005. Returns shown for periods prior to that date are hypothetical and are based on the returns of the then-existing BGI Fund for the MSCI US REIT Index, and are net of fees.

7The Stable Value Fund is a separately managed account; historical return data represents its actual performance.

8The Asset Allocation Funds are designed investment vehicles utilizing various asset classes represented by index funds, and, under BGI management, were managed on an exclusive basis. Only hypothetical results are available from January 1992 to July 2, 1997 (the inception date of the Asset Allocation Funds). Note that SSgA changed certain allocations and underlying indexes (see fund descriptions for information on same).

9 The Aggregate Bond Index Fund became available effective April 30, 2006. Results prior to that date are based on historical investment returns of the then-existing SSgA fund, and are net of PSI fees which would have been levied.

5

10 The Target Retirement Funds became available August 1, 2007. Results prior to that date are based on historical investment returns of the then-existing SSgA fund, and are net of all relevant fees which would have been levied.

Description of the Investment Funds

The following is a description of each of the funds:

|

|

| International Stock Fund.The fund seeks to match the performance of the Moran Stanley Capital International, Europe, Australia, Far East (MSCI EAFE) Index while providing daily liquidity. The MSCI EAFE Index is a float-adjusted developed markets international equity index which covers approximately 85% of each industry within each represented country and measures the performance of over 1,000 companies in 21 countries outside North and South America. The International Stock Fund typically invests in all the stocks in the MSCI EAFE Index in proportion to their weighting in the index. The strategy of investing in the same stocks as the index minimizes the need for trading and therefore results in lower expenses. |

|

|

| NASDAQ 100 Stock Fund. The fund seeks to match the performances of the NASDAQ 100 Index, which consists of 100 of the largest non-financial companies, both domestic and international, listed on the NASDAQ exchange; the size of the companies is determined by market cap and all major industry groups are included, with the exception of financial and investment companies. The NASDAQ 100 Stock Fund invests in all of the stocks in the NASDAQ 100 Index in proportion to their weighting in the index. The fund may also hold 2-5% of its value in futures contacts (an agreement to buy or sell a specific security by a specific date at an agreed upon price). The strategy of investing in the same stocks as the index minimizes the need for trading and therefore results in lower expenses. |

|

|

| Russell 2000 Stock Fund.The fund seeks to match the performance of the Russell 2000 Index, which is a float-adjusted small cap equity index covering approximately 8% of the U.S. equity market and measuring the performance of the 2,000 smallest companies in the broad market Russell 3000 Index, based on total market capitalization. The Russell 2000 Stock Fund attempts to invest in all 2,000 stocks in the Russell 2000 Index in proportion to their weighting in the index. The fund may also hold 2-5% of its value in futures contracts (an agreement to buy or sell a specific security by a specific date at an agreed upon price). The strategy of investing in the same stocks as the index minimizes the need for trading and therefore results in lower expenses. |

|

|

| S&P MidCap Stock Fund. The fund seeks to match the performance of the S&P MidCap 400 Index, which is a float-adjusted mid-cap equity index covering approximately 15% of U.S. equity market and measuring the performance of 400 leading companies in leading industries within the mid cap segment of the market as determined by S&P’s Index Committee. The S&P MidCap Stock Fund invests in all 400 stocks in the index in proportion to their weighting in the index. The fund may also hold 2-5% of its value in futures contracts (an agreement to buy or sell a specific security by a specific date at an agreed upon price). The strategy of investing in the same stocks as the index minimizes the need for trading and therefore results in lower expenses. |

6

|

|

| S&P/Growth Stock Fund. The fund seeks to match the performance of the Standard & Poor’s 500/Citigroup Growth Index, which is constructed by including those stocks from the S&P 500 Index with higher price to book ratios. The index is market capitalization weighted and their constituents are mutually exclusive. The S&P/Growth Fund invests in all of the stocks in the S&P 500/Citigroup Growth Index in proportion to their weighting in the index. The fund may also hold 2-5% of its value in futures contracts (an agreement to buy or sell a specific security by a specific date at an agreed upon price). The strategy of investing in the same stocks as the index minimizes the need for trading and therefore results in lower expenses. |

|

|

| S&P/Value Stock Fund. The fund seeks to match the performance of the Standard & Poor’s 500/Citigroup Value Index, which is constructed by including those stocks from the S&P 500 Index with lower price to book ratios. The index is market capitalization weighted and their constituents are mutually exclusive. The S&P/Value Stock Fund invests in all of the stocks in the S&P500/Citigroup Value Index in proportion to their weighting in the index. The fund may also hold 2-5% of its value in futures contracts (an agreement to buy or sell a specific security by a specific date at an agreed upon price). The strategy of investing in the same stocks as the index minimizes the need for trading and therefore results in lower expenses. |

|

|

| S&P 500 Stock Fund. The fund seeks to match the performance of the Standard & Poor’s 500 Index, which is a float-adjusted large-cap equity index covering approximately 80% of U.S. equity market and measuring the performance of 500 leading companies in leading industries within the large cap segment of the market as determined by S&P’s Index Committee. The S&P Stock Fund invests in all 500 stocks in the S&P 500 Index in proportion to their weighting in the index. The fund may also hold 2-5% of its value in futures contracts (an agreement to buy or sell a specific security by a specific date at an agreed upon price). The strategy of investing in the same stocks as the index minimizes the need for trading and therefore results in lower expenses. |

|

|

| US REIT Index Fund. The fund seeks to match the performance of the Dow Jones/Wilshire REIT Index while providing daily liquidity. The Dow Jones/Wilshire REIT Index is a market capitalization weighted index which is comprises of 90 publicly traded Real Estate Investment Trusts (REITs). To be included in the index, a company must be an equity owner and operator of commercial (or residential) real estate and must generate at least 75% of its revenue from such assets; minimum requirements for market capitalization and liquidity also apply. The US REIT Index Fund typically invests in all securities in the Dow Jones/Wilshire REIT Index in proportion to their weighting in the index. As such, the fund seeks to maintain sector and security weightings that closely match the index. This replication process results in low turnover, accurate tracking and low costs. The fund invests primarily in equity shares of real estate investment trusts (REITs). REITs invest in loans secured by real estate and invest directly in real estate properties such as apartments, office buildings, and shopping malls. REITs generate income from rentals or lease payments and offer the potential for growth from property appreciation and the potential for capital gains from the sale of properties. |

7

|

|

| Long Treasury Index Fund. The fund seeks to match the total rate of return of the Lehman Brothers Long Treasury Bond Index. The fund invests primarily in U.S. Treasury securities with a maturity of 10 years or longer. The fund invests in a well diversified portfolio that is representative of the U.S. Long Treasury bond market. The fund buys and holds securities, trading only when there is a change to the composition of the index or when cash flow activity occurs in the fund. This process minimizes turnover and costs while maintaining accurate tracking. |

|

|

| Aggregate Bond Index Fund.The fund seeks to match the returns of the Lehman Brothers Aggregate Bond Index. The fund invests primarily in government, corporate, mortgage-backed and asset-backed securities. The fund invests in a well-diversified portfolio that is representative of the broad domestic bond market. |

|

|

| Stable Value Fund.The fund seeks to preserve the principal amount of your contributions while maintaining a rate of return comparable to other fixed income instruments. The fund invests in investment contracts issued by insurance companies, banks, and other financial institutions, as well as enhanced short-term investment products. Each issuer must meet the credit quality criteria in order to be approved by the investment manager. The fund is managed to a weighted average maturity of approximately 1.5-4.0 years and maintains an average AA credit quality. |

|

|

| Short Term Investment Fund. The fund seeks to maximize current income while preserving capital and liquidity through investing in a diversified portfolio of short-term securities. The fund’s yield reflects short-term interest rates. The fund seeks to maintain a diversified portfolio of short-term securities by investing in high-quality money market securities and other short-term debt investments. Most of the investments in the fund may have a range of maturity from overnight to 90 days; however, 20% of the value of the fund may be invested in assets with a maturity date in excess of 90 days, but not to exceed 13 months. All securities are required to meet strict guidelines for credit quality and must be rated at least A1 by Standard & Poor’s and P1 by Moody’s Investors Service. |

|

|

| Income Plus Asset Allocation Fund. The fund seeks to provide income from fixed income securities and some growth of principal from stock funds. The fund’s risk profile is somewhat conservative due to an emphasis on bond holdings. The fund has a target asset allocation of 25% equities and 75% fixed income achieved by investing in a mix of other funds as follows: 15% in the S&P 500 Index Fund; 5% in the Russell Small Cap Completeness Index Fund; 5% in the Daily EAFE Fund; and 75% in the Bond Market Index Fund. The fund will be managed to approximate this target portfolio mix. The fund will be rebalanced monthly or more often when justified by significant activity or changes in the market values of the underlying funds. These percentages may fluctuate away from the target weights between rebalancing. |

|

|

| Growth and Income Asset Allocation Fund. The fund seeks to provide income from fixed income securities and growth of principal from stock funds. The fund’s risk profile is moderate due to the presence of well-diversified stock and bond holdings. The fund has a |

8

target asset allocation of 55% equities and 45% fixed income achieved by investing in a mix of other funds as follows: 35% in the S&P 500 Index Fund; 10% in the Russell Small Cap Completeness Index Fund; 10% in the Daily EAFE Fund; and 45% in the Bond Market Index Fund. The fund will be managed to approximate this target portfolio mix. The fund will be rebalanced monthly or more often when justified by significant activity or changes in the market values of the underlying funds. These percentages may fluctuate away from the target weights between rebalancing.

Growth Asset Allocation Fund.The fund seeks to provide growth of principal from stock funds and some income from fixed income securities. The fund’s risk profile is somewhat aggressive due to its emphasis on stock holdings. The fund has a target asset allocation of 85% equities and 15% fixed income achieved by investing in a mix of other funds as follows: 55% in S&P 500 Index Fund; 15% in the Russell Small Cap Completeness Index Fund; 15% in the Daily EAFE Fund, and 15% in the Bond Market Index Fund.

SSgA Target Retirement 2015 Fund. The SSgA Target Retirement Funds are designed as “one-stop” investment solutions. The funds are invested in a broadly diversified portfolio of SSgA index funds, covering U.S. and international large cap, U.S. mid-cap and U.S. small cap stocks along with long-term and short-term bonds. The date in a fund’s name corresponds to an expected retirement date. You simply select the fund with a date closest to when you expect to retire and invest accordingly. The 2015 fund starts out with a stock and bond allocation suitable for the full time horizon – from now to the year 2015 and beyond. Professional managers then adjust the index fund mix annually, gradually decreasing the stock allocations while increasing the bond allocations as the retirement date approaches. Five years after the retirement date, the fund will maintain a fixed allocation of 35% stock funds and 65% bond funds. The fund has a target mix among equities and fixed income as follows: 33% in the S&P 500 Index Fund; 8% in the Daily MSCI EAFE Index Fund; 3.9% in the S&P MidCap 400 Index Fund; 2.6% in the Russell 2000 Index Fund; 37% in the Lehman Long Government Bond Fund; 10.5% in the Limited Duration Bond Fund; and 5% in the Short Term Investment Fund.

SSgA Target Retirement 2025 Fund. The SSgA Target Retirement Funds are designed as “one-stop” investment solutions. The funds are invested in a broadly diversified portfolio of SSgA index funds, covering U.S. and international large cap, U.S. mid-cap and U.S. small cap stocks along with long-term and short-term bonds. The date in a fund’s name corresponds to an expected retirement date. You simply select the fund with a date closest to when you expect to retire and invest accordingly. The 2025 fund starts out with a stock and bond allocation suitable for the full time horizon – from now to the year 2025 and beyond. Professional managers then adjust the index fund mix annually, gradually decreasing the stock allocations while increasing the bond allocations as the retirement date approaches. Five years after the retirement date, the fund will maintain a fixed allocation of 35% stock funds and 65% bond funds. The fund currently has a target mix among equities and fixed income as follows: 41.5% in the S&P 500 Index Fund; 16.5% in the Daily MSCI EAFE Index Fund; 6.5% in the S&P MidCap 400 Index Fund; 5% in the Russell 2000 Index Fund; 27% in the Long US Government Bond Fund; 3.5% in the Short Term Investment Fund.

9

SSgA Target Retirement 2035 Fund. The SSgA Target Retirement Funds are designed as “one-stop” investment solutions. The funds are invested in a broadly diversified portfolio of SSgA index funds, covering U.S. and international large cap, U.S. mid-cap and U.S. small cap stocks along with long-term and short-term bonds. The date in a fund’s name corresponds to an expected retirement date. You simply select the fund with a date closest to when you expect to retire and invest accordingly. The 2035 fund starts out with a stock and bond allocation suitable for the full time horizon – from now to the year 2035 and beyond. Professional managers then adjust the index fund mix annually, gradually decreasing the stock allocations while increasing the bond allocations as the retirement date approaches. Five years after the retirement date, the fund will maintain a fixed allocation of 35% stock funds and 65% bond funds. The fund has a target mix among equities and fixed income as follows: 45% in the S&P 500 Index Fund; 21.5% in the Daily MSCI EAFE Index Fund; 8.3% in the S&P MidCap 400 Index Fund; 8.2% in the Russell 2000 Index Fund; and 17% in the Long US Government Bond Fund.

SSgA Target Retirement 2045 Fund. The SSgA Target Retirement Funds are designed as “one-stop” investment solutions. The funds are invested in a broadly diversified portfolio of SSgA index funds, covering U.S. and international large cap, U.S. mid-cap and U.S. small cap stocks along with long-term and short-term bonds. The date in a fund’s name corresponds to an expected retirement date. You simply select the fund with a date closest to when you expect to retire and invest accordingly. The 2045 fund starts out with a stock and bond allocation suitable for the full time horizon – from now to the year 2045 and beyond. Professional managers then adjust the index fund mix annually, gradually decreasing the stock allocations while increasing the bond allocations as the retirement date approaches. Five years after the retirement date, the fund will maintain a fixed allocation of 35% stock funds and 65% bond funds. The fund has a target mix among equities and fixed income as follows: 45% in the S&P 500 Index Fund; 25% in the Daily MSCI EAFE Index Fund; 10% in the S&P MidCap 400 Index Fund; 10% in the Russell 2000 Index Fund; and 10% in the Long US Government Bond Fund.

|

An investment in any of the funds listed above is not a deposit of a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. As with any mutual fund investment, there is always a risk that you may lose money on your investment in any of the funds listed above. |

Employer Stock Fund. The Employer Stock Fund currently consists primarily of investments in common stock of K-Fed Bancorp (95% common stock and 5% cash). K-Fed Bancorp is a federally chartered majority-owned subsidiary of K-Fed Mutual Holding Company. Following the offering, K-Fed Bancorp, a federal corporation, will cease to exist, but will be succeeded by a new Maryland corporation with the name Kaiser Federal Financial Group, Inc., which will be 100% owned by its public shareholders, including Kaiser Federal Financial Group, Inc.’s tax-qualified plans. Shares of K-Fed Bancorp (a federal corporation) which were held in the existing Employer Stock Fund prior to the conversion and offering will be converted, upon the closing of the offering, into new shares of common stock of Kaiser Federal Financial Group, Inc. (a

10

Maryland corporation), in accordance with the exchange ratio, as described in the accompanying prospectus, in the section titled, “The Conversion and Offering.” For a period of time following the offering, the existing Employer Stock Fund will be maintained separately from the newly created Employer Stock Fund. The newly created Employer Stock Fund will initially consist of 100% Common Stock of Kaiser Federal Financial Group, Inc. Following the offering, the newly created Employer Stock Fund will consist of approximately 95% common stock of Kaiser Federal Financial Group, Inc. and 5% cash. During the first six months of 2008, the existing Employer Stock Fund will be merged with the newly created Employer Stock Fund.

The trustee will use all amounts reallocated to the Employer Stock Fund in the special election to acquire shares in the Common Stock offering. After the offering, the trustee will, to the extent practicable, use all amounts held by it in the new and existing Employer Stock Funds, including cash dividends paid on common stock held in the Employer Stock Funds, to purchase shares of Common Stock of Kaiser Federal Financial Group, Inc. It is expected that all purchases will be made at prevailing market prices. Under certain circumstances, the trustee may be required to limit the daily volume of shares purchased. Pending investment in Common Stock of Kaiser Federal Financial Group, Inc., amounts allocated towards the purchase of shares of Common Stock in the offering will be held in the Plan in an interest-bearing account.

For a discussion ofmaterial risks, you should consider the “Risk Factors” set forth in the attached prospectus.

Withdrawals and Distributions from the Plan

Applicable federal law requires the Plan to impose substantial restrictions on the right of a Plan participant to withdraw amounts held for his or her benefit under the Plan prior to the participant’s termination of employment with Kaiser Federal Bank. A substantial federal tax penalty may also be imposed on withdrawals made prior to the participant’s attainment of age 59 ½, regardless of whether such a withdrawal occurs during his or her employment with Kaiser Federal Bank or after termination of employment.

Withdrawals Prior to Termination of Employment. You may make voluntary withdrawals of your pre-tax elective deferrals only in the event of attainment of age 59 ½. You may also make withdrawals of your employee rollover contributions and the earnings thereon. You may make withdrawals of employer matching contributions and the earnings thereon only in the event of hardship or upon attainment of age 59 ½. In general, employer contributions credited on your behalf will not be available for in-service withdrawal until such employer contributions have been invested in the Plan for at least two years or you have been a participant in the Plan for at least five years.

Withdrawal upon Termination of Employment.You may make withdrawals from your account at any time after you terminate employment. You may also leave your account with the Plan and defer commencement of receipt of your vested balance until April 1 of the calendar year following the calendar year in which you attain age 70 ½. You may request a distribution of all or part of your account no more frequently than once per Plan Year. Distribution will be made in a lump sum or in installments (no less frequently than annually).

11

Withdrawal upon Disability.If you are disabled in accordance with the definition of disability under the Plan, you will be entitled to the same withdrawal rights as if you had terminated your employment.

Withdrawal upon Death. If you die while you are a participant in the Plan, the value of your entire account will be payable to your beneficiary. You may elect to have your beneficiary receive distribution in 5 annual installments (10 if your spouse is your beneficiary, provided that you spouse’s remaining life expectancy is at least 10 years). If such an election is not in effect at the time of your death, your beneficiary may elect to receive the benefit in the form of annual installments over a period not to exceed 5 years (10 years if your spouse is your beneficiary, provided that you spouse’s remaining life expectancy is at least 10 years) or make withdrawals as often as once per year, except that any balance remaining must be withdrawn by the 5th anniversary (10th anniversary if your spouse is your beneficiary, provided that you spouse’s remaining life expectancy is at least 10 years) of your death.

The Plan allows participants to obtain loans from their accounts.

The Trustee and Custodian. The trustee of the Plan is The Bank of New York. The Bank of New York serves as trustee for all the investments funds under the Plan except the Employer Stock Fund.

Plan Administrator. Pursuant to the terms of the Plan, the Plan is administered by the Plan administrator. The address of the Plan administrator is Kaiser Federal Bank, Attention: Mary Templin, Human Resources/Benefits Administrator, 1359 North Grand Avenue, Covina, California 91724, telephone number (626) 339-9663, extension 1252. The Plan administrator is responsible for the administration of the Plan, interpretation of the provisions of the Plan, prescribing procedures for filing applications for benefits, preparation and distribution of information explaining the Plan, maintenance of Plan records, books of account and all other data necessary for the proper administration of the Plan, preparation and filing of all returns and reports relating to the Plan which are required to be filed with the U.S. Department of Labor and the Internal Revenue Service, and for all disclosures required to be made to participants, beneficiaries and others under Sections 104 and 105 of ERISA.

Reports to Plan Participants. The Plan administrator will furnish you a statement at least quarterly showing the balance in your account as of the end of that period, the amount of contributions allocated to your account for that period, and any adjustments to your account to reflect earnings or losses (if any).

It is the intention of Kaiser Federal Bank to continue the Plan indefinitely. Nevertheless, Kaiser Federal Bank may terminate the Plan at any time. If the Plan is terminated in whole or in part, then regardless of other provisions in the Plan, you will have a fully vested interest in your

12

accounts. Kaiser Federal Bank reserves the right to make any amendment or amendments to the Plan which do not cause any part of the trust to be used for, or diverted to, any purpose other than the exclusive benefit of participants or their beneficiaries; provided, however, that Kaiser Federal Bank may make any amendment it determines necessary or desirable, with or without retroactive effect, to comply with ERISA.

Merger, Consolidation or Transfer

In the event of the merger or consolidation of the Plan with another plan, or the transfer of the trust assets to another plan, the Plan requires that you would, if either the Plan or the other plan terminates, receive a benefit immediately after the merger, consolidation or transfer which is equal to or greater than the benefit you would have been entitled to receive immediately before the merger, consolidation or transfer, if the Plan had then terminated.

Federal Income Tax Consequences

The following is a brief summary of the material federal income tax aspects of the Plan. You should not rely on this summary as a complete or definitive description of the material federal income tax consequences relating to the Plan. Statutory provisions change, as do their interpretations, and their application may vary in individual circumstances. Finally, the consequences under applicable state and local income tax laws may not be the same as under the federal income tax laws. Please consult your tax advisor with respect to any distribution from the Plan and transactions involving the Plan.

As a “tax-qualified retirement plan,” the Code affords the Plan special tax treatment, including:

(1) the sponsoring employer is allowed an immediate tax deduction for the amount contributed to the Plan each year;

(2) participants pay no current income tax on amounts contributed by the employer on their behalf; and

(3) earnings of the Plan are tax-deferred, thereby permitting the tax-free accumulation of income and gains on investments.

Kaiser Federal Bank will administer the Plan to comply with the requirements of the Code as of the applicable effective date of any change in the law.

Lump-Sum Distribution. A distribution from the Plan to a participant or the beneficiary of a participant will qualify as a lump-sum distribution if it is made within one taxable year, on account of the participant’s death, disability or separation from service, or after the participant attains age 59 ½, and consists of the balance credited to participants under the Plan and all other profit sharing plans (and in some cases all other stock bonus plans), if any, maintained by Kaiser Federal Bank. The portion of any lump-sum distribution required to be included in your taxable income for federal income tax purposes consists of the entire amount of the lump-sum

13

distribution, less the amount of after-tax contributions, if any, you have made to this Plan and any other profit sharing plans maintained by Kaiser Federal Bank, which is included in the distribution.

Kaiser Federal Financial Group, Inc. Common Stock Included in Lump-Sum Distribution. If a lump-sum distribution includes Kaiser Federal Financial Group, Inc. Common Stock, the distribution generally will be taxed in the manner described above, except that the total taxable amount may be reduced by the amount of any net unrealized appreciation with respect to Kaiser Federal Financial Group, Inc. Common Stock, that is, the excess of the value of Kaiser Federal Financial Group, Inc. Common Stock at the time of the distribution over its cost or other basis of the securities to the trust. The tax basis of Kaiser Federal Financial Group, Inc. Common Stock, for purposes of computing gain or loss on its subsequent sale, equals the value of Kaiser Federal Financial Group, Inc. Common Stock at the time of distribution, less the amount of net unrealized appreciation. Any gain on a subsequent sale or other taxable disposition of Kaiser Federal Financial Group, Inc. Common Stock, to the extent of the amount of net unrealized appreciation at the time of distribution, will constitute long-term capital gain, regardless of the holding period of Kaiser Federal Financial Group, Inc. Common Stock. Any gain on a subsequent sale or other taxable disposition of Kaiser Federal Financial Group, Inc. Common Stock, in excess of the amount of net unrealized appreciation at the time of distribution, will be considered long-term capital gain. The recipient of a distribution may elect to include the amount of any net unrealized appreciation in the total taxable amount of the distribution, to the extent allowed by regulations to be issued by the Internal Revenue Service.

Distributions: Rollovers and Direct Transfers to Another Qualified Plan or to an IRA. You may roll over virtually all distributions from the Plan to another qualified plan or to an individual retirement account in accordance with the terms of the other plan or account.

Notice of Your Rights Concerning Employer Securities. There has been an important change in Federal law that provides specific rights concerning investments in employer securities, such as Kaiser Federal Financial Group, Inc. Common Stock. Because you may in the future have investments in Kaiser Federal Financial Group, Inc. Stock Fund under the Plan, you should take the time to read the following information carefully.

Your Rights Concerning Employer Securities. Beginning in 2007, the Plan must allow you to elect to move any portion of your account that is invested in the Kaiser Federal Financial Group, Inc. Stock Fund from that investment into other investment alternatives under the Plan. You may contact the Plan administrator shown above for specific information regarding this new right, including how to make this election. In deciding whether to exercise this right, you will want to give careful consideration to the information below that describes the importance of diversification. All of the investment options under the Plan are available to you if you decide to diversify out of the Kaiser Federal Financial Group, Inc. Stock Fund.

The Importance of Diversifying Your Retirement Savings. To help achieve long-term retirement security, you should give careful consideration to the benefits of a well-balanced and diversified investment portfolio. Spreading your assets among different types of investments can help you achieve a favorable rate of return, while minimizing your overall risk of losing money.

14

This is because market or other economic conditions that cause one category of assets, or one particular security, to perform very well often cause another asset category, or another particular security, to perform poorly. If you invest more than 20% of your retirement savings in any one company or industry, your savings may not be properly diversified. Although diversification is not a guarantee against loss, it is an effective strategy to help you manage investment risk.

In deciding how to invest your retirement savings, you should take into account all of your assets, including any retirement savings outside of the Plan. No single approach is right for everyone because, among other factors, individuals have different financial goals, different time horizons for meeting their goals, and different tolerance for risk. Therefore, you should carefully consider the rights described here and how these rights affect the amount of money that you invest in Kaiser Federal Financial Group, Inc. Common Stock through the Plan.

It is also important to periodically review your investment portfolio, your investment objectives, and the investment options under the Plan to help ensure that your retirement savings will meet your retirement goals.

Additional ERISA Considerations

As noted above, the Plan is subject to certain provisions of ERISA, including special provisions relating to control over the Plan’s assets by participants and beneficiaries. The Plan’s feature that allows you to direct the investment of your account balances is intended to satisfy the requirements of Section 404(c) of ERISA relating to control over plan assets by a participant or beneficiary. The effect of this is two-fold. First, you will not be deemed a “fiduciary” because of your exercise of investment discretion. Second, no person who otherwise is a fiduciary, such as Kaiser Federal Bank, the Plan administrator, or the Plan’s trustee is liable under the fiduciary responsibility provision of ERISA for any loss which results from your exercise of control over the assets in your Plan account.

Because you will be entitled to invest all or a portion of your account balance in the Plan in Kaiser Federal Financial Group, Inc. Common Stock, the regulations under Section 404(c) of ERISA require that the Plan establish procedures that ensure the confidentiality of your decision to purchase, hold, or sell employer securities, except to the extent that disclosure of such information is necessary to comply with federal or state laws not preempted by ERISA. These regulations also require that your exercise of voting and similar rights with respect to the Common Stock be conducted in a way that ensures the confidentiality of your exercise of these rights.

Securities and Exchange Commission Reporting and Short-Swing Profit Liability

Section 16 of the Securities Exchange Act of 1934, as amended, imposes reporting and liability requirements on officers, directors, and persons beneficially owning more than 10% of public companies such as Kaiser Federal Financial Group, Inc. Section 16(a) of the Securities Exchange Act of 1934 requires the filing of reports of beneficial ownership. Within 10 days of becoming an officer, director or person beneficially owning more than 10% of the shares of Kaiser Federal Financial Group, Inc. Common Stock, a Form 3 reporting initial beneficial

15

ownership must be filed with the Securities and Exchange Commission. Changes in beneficial ownership, such as purchases, sales and gifts generally must be reported periodically, either on a Form 4 within two business days after the change occurs, or annually on a Form 5 within 45 days after the close of Kaiser Federal Financial Group, Inc.’s fiscal year. Discretionary transactions in and beneficial ownership of the Common Stock through the Kaiser Federal Financial Group, Inc. Stock Fund of the Plan by officers, directors and persons beneficially owning more than 10% of the Common Stock of Kaiser Federal Financial Group, Inc. generally must be reported to the Securities and Exchange Commission by such individuals.

In addition to the reporting requirements described above, Section 16(b) of the Securities Exchange Act of 1934, as amended, provides for the recovery by Kaiser Federal Financial Group, Inc. of profits realized by an officer, director or any person beneficially owning more than 10% of Kaiser Federal Financial Group, Inc.’s Common Stock resulting from non-exempt purchases and sales of Kaiser Federal Financial Group, Inc. Common Stock within any six-month period.

The Securities and Exchange Commission has adopted rules that provide exemptions from the profit recovery provisions of Section 16(b) for all transactions in employer securities within an employee benefit plan, provided certain requirements are met. These requirements generally involve restrictions upon the timing of elections to acquire or dispose of employer securities for the accounts of Section 16(b) persons.

Except for distributions of Common Stock due to death, disability, retirement, termination of employment or under a qualified domestic relations order, persons affected by Section 16(b) are required to hold shares of Common Stock distributed from the Plan for six months following such distribution and are prohibited from directing additional purchases within the Kaiser Federal Financial Group, Inc. Stock Fund for six months after receiving such a distribution.

Financial Information Regarding Plan Assets

Financial information representing the assets available for plan benefits at June 30, 2007 and June 30, 2006, and changes in net assets available for benefits for the years ended June 30, 2007 and June 30, 2006, are available upon written request to the Plan administrator at the address shown above.

The validity of the issuance of the Common Stock has been passed upon by Luse Gorman Pomerenk & Schick, A Professional Corporation, Washington, D.C., which firm acted as special counsel to Kaiser Federal Financial Group, Inc. in connection with Kaiser Federal Financial Group, Inc.’s stock offering.

16

PROSPECTUS

|

|

|

(Proposed Holding Company for Kaiser Federal Bank) |

Up to 14,950,000 Shares of Common Stock |

(Subject to Increase to up to 17,192,500 Shares) |

Kaiser Federal Financial Group, Inc., a Maryland corporation, is offering shares of common stock for sale in connection with the conversion of K-Fed Mutual Holding Company from the mutual to the stock form of organization. The shares of common stock we are offering represent the 63.5% ownership interest in K-Fed Bancorp currently owned by K-Fed Mutual Holding Company. In addition, at the conclusion of the conversion and offering, existing shares of K-Fed Bancorp common stock currently held by the public will be exchanged for shares of common stock of Kaiser Federal Financial Group, Inc. All shares of common stock are being offered for sale at a price of $10.00 per share. Purchasers will not pay a commission to purchase shares of common stock in the offering. K-Fed Bancorp’s common stock is currently traded on the Nasdaq Global Market under the trading symbol “KFED.” The closing price of K-Fed Bancorp’s common stock on November 9, 2007, was $11.39. We expect that Kaiser Federal Financial Group, Inc.’s shares of common stock will also trade on the Nasdaq Global Market under the trading symbol “KFFG.”

|

|

|

| If you are or were a depositor of Kaiser Federal Bank: | |

|

| |

| • | You have priority rights to purchase shares of our common stock if (1) you had at least $50.00 on deposit at Kaiser Federal Bank at the close of business on March 31, 2006; (2) you had at least $50.00 on deposit at Kaiser Federal Bank at the close of business on September 30, 2007; or (3) you are a depositor of Kaiser Federal Bank at the close of business on October 31, 2007. |

|

|

|

| If you are currently a stockholder of K-Fed Bancorp: | |

|

| |

| • | You may have the opportunity to purchase additional shares of our common stock in the offering after priority orders are filled. |

|

|

|

| • | Each of your shares of common stock will be exchanged at the conclusion of the offering for between 1.2469 and 1.6870 new shares (subject to adjustment to up to 1.9401 new shares) of common stock of Kaiser Federal Financial Group, Inc. to maintain approximately your existing percentage ownership in K-Fed Bancorp (excluding additional purchases of shares of common stock in the offering). |

|

|

|

| If you fit neither of the categories above, but are interested in purchasing shares of our common stock: | |

|

| |

| • | You may have the opportunity to purchase shares of common stock after priority orders in the preceding categories are filled. |

We are offering up to 14,950,000 shares of common stock for sale on a best efforts basis. We may sell up to 17,192,500 shares of common stock because of regulatory considerations, demand for the shares of common stock or changes in financial market conditions, without resoliciting purchasers. In addition to the shares we are selling in the offering, we also will simultaneously issue up to 8,582,229 shares of common stock to public stockholders of K-Fed Bancorp in exchange for their existing shares. The number of shares to be issued in the exchange may be increased to up to 9,869,563 shares of common stock, if we sell 17,192,500 shares of common stock in the offering. We must sell a minimum of 11,050,000 shares in the offering and issue 6,343,386 shares in the exchange in order to complete the offering and the exchange of existing shares of common stock.

The minimum number of shares of common stock you may order is 25. The offering is expected to expire at 12:00 Noon, Pacific Time, on December 11, 2007. We may extend this expiration date without notice to you until January 25, 2008, unless the Office of Thrift Supervision approves a later date, which may not be beyond December 18, 2009. Once submitted, orders are irrevocable unless the offering is terminated or is extended beyond January 25, 2008, or the number of shares of common stock to be sold is increased to more than 17,192,500 shares or decreased to less than 11,050,000 shares. If the subscription and community offerings are terminated, purchasers will have their funds returned promptly, with interest. If the offering is extended beyond January 25, 2008 or there is a change in the offering range, we will resolicit purchasers, and you will have the opportunity to maintain, change or cancel your order. If you do not provide us with a written indication of your intent, your order will be cancelled and your funds will be returned to you, with interest. Funds received prior to the completion of the offering up to the minimum of the offering range will be held in a segregated account at Kaiser Federal Bank. Funds received in excess of the minimum of the offering range may be maintained in a segregated account at Kaiser Federal Bank or, at our discretion, at another federally insured depository institution. However, in no event will we maintain more than one escrow account. All funds received will earn interest calculated at Kaiser Federal Bank’s passbook savings rate, which is currently 0.35% per annum. Keefe, Bruyette & Woods, Inc. will assist us in selling our shares of common stock on a best efforts basis in the subscription offering. We may also offer shares of common stock not subscribed for in the subscription offering in a community offering concurrent with or subsequent to the subscription offering as well as through a syndicated community offering through a syndicate of selected dealers managed by Keefe, Bruyette & Woods, Inc. Keefe, Bruyette & Woods, Inc. is not required to purchase any shares of the common stock that are being offered for sale.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| OFFERING SUMMARY |

|

|

|

|

|

|

| ||||||||

|

| Minimum |

| Midpoint |

| Maximum |

| Maximum as Adjusted |

| ||||||||

|

|

|

|

|

| ||||||||||||

Number of shares |

|

|

| 11,050,000 |

|

| 13,000,000 |

|

| 14,950,000 |

|

|

| 17,192,500 |

| ||

Gross offering proceeds |

| $ | 110,500,000 |

| $ | 130,000,000 |

| $ | 149,500,000 |

| $ | 171,925,000 |

| ||||

Estimated offering expenses excluding selling agent commissions and expenses |

| $ | 1,200,000 |

| $ | 1,200,000 |

| $ | 1,200,000 |

| $ | 1,200,000 |

| ||||

Selling agent commissions and expenses(1) |

| $ | 3,123,850 |

| $ | 4,132,000 |

| $ | 5,140,150 |

| $ | 6,299,523 |

| ||||

Net proceeds |

| $ | 106,176,150 |

| $ | 124,668,000 |

| $ | 143,159,850 |

| $ | 164,425,477 |

| ||||

Net proceeds per share |

| $ | 9.61 |

| $ | 9.59 |

| $ | 9.58 |

| $ | 9.56 |

| ||||

|

|

(1) | Please see “The Conversion and Offering—Marketing Arrangements” for a discussion of Keefe, Bruyette & Woods, Inc.’s compensation for this offering. |

This investment involves a degree of risk, including the possible loss of principal.

Please read “Risk Factors” beginning on page 20.