UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22123

Nuveen Municipal High Income Opportunity Fund 2

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive

Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Kevin J. McCarthy

Nuveen Investments

333 West Wacker Drive

Chicago, IL 60606

(Name and address of agent for service)

Registrant's telephone number, including area code: (312) 917-7700

Date of fiscal year end: October 31

Date of reporting period: October 31, 2012

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss. 3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

LIFE IS COMPLEX.

Nuveen makes things e-simple.

It only takes a minute to sign up for e-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Fund information is ready. No more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report and save it on your computer if you wish.

Free e-Reports right to your e-mail!

www.investordelivery.com

If you receive your Nuveen Fund distributions and statements from your financial advisor or brokerage account.

OR

www.nuveen.com/accountaccess

If you receive your Nuveen Fund distributions and statements directly from Nuveen.

Table of Contents

| Chairman’s Letter to Shareholders | 4 |

| Portfolio Managers’ Comments | 5 |

| Fund Leverage and Other Information | 12 |

| Common Share Dividend and Price Information | 15 |

| Performance Overviews | 17 |

| Shareholder Meeting Report | 23 |

| Report of Independent Registered Public Accounting Firm | 25 |

| Portfolios of Investments | 26 |

| Statement of Assets and Liabilities | 102 |

| Statement of Operations | 104 |

| Statement of Changes in Net Assets | 106 |

| Statement of Cash Flows | 109 |

| Financial Highlights | 112 |

| Notes to Financial Statements | 120 |

| Annual Investment Management Agreement Approval Process | 135 |

| Board Members and Officers | 145 |

| Reinvest Automatically, Easily and Conveniently | 150 |

| Glossary of Terms Used in this Report | 152 |

| Additional Fund Information | 155 |

Chairman’s

Letter to Shareholders

Dear Shareholders,

Investors have many reasons to remain cautious. The challenges in the Euro area continue to cast a shadow over global economies and financial markets. The political support for addressing fiscal issues is eroding as the economic and social impacts become more visible. Despite strong action by the European Central Bank, member nations appear unwilling to surrender sufficient sovereignty to unify the Euro area financial system or strengthen its banks. The gains made in reducing deficits, and the hard-won progress on winning popular acceptance of the need for economic austerity, are at risk. To their credit, European political leaders press on to find compromise solutions, but there is increasing concern that time is running out.

In the U.S., the extended period of increasing corporate earnings that enabled the equity markets to withstand the downward pressures coming from weakening job creation and slower economic growth appears to be coming to an end. The Fed remains committed to low interest rates and announced a third phase of quantitative easing (QE3) scheduled to continue until mid-2015. The recent election results have removed a major element of uncertainty in the U.S. political picture, but it remains to be seen whether the outcome will reduce the highly partisan atmosphere in Congress and enable progress on the many pressing fiscal and budgetary issues that must be resolved in the coming months.

During the last twelve months, U.S. investors have experienced a solid recovery in the domestic equity markets with increasing volatility as the “fiscal cliff” approaches. The experienced investment teams at Nuveen keep their eye on a longer time horizon and use their practiced investment disciplines to negotiate through market peaks and valleys to achieve long-term goals for investors. Experienced professionals pursue investments that will weather short-term volatility and at the same time, seek opportunities that are created by markets that overreact to negative developments. Monitoring this process is an important consideration for the Fund Board as it oversees your Nuveen Fund on your behalf.

As always, I encourage you to contact your financial consultant if you have any questions about your investment in a Nuveen Fund. On behalf of the other members of your Fund Board, we look forward to continuing to earn your trust in the months and years ahead.

Sincerely,

Robert P. Bremner

Chairman of the Board

December 20, 2012

| 4 | Nuveen Investments |

Portfolio Managers’ Comments

Nuveen Investment Quality Municipal Fund, Inc. (NQM)

Nuveen Select Quality Municipal Fund, Inc. (NQS)

Nuveen Quality Income Municipal Fund, Inc. (NQU)

Nuveen Premier Municipal Income Fund, Inc. (NPF)

Nuveen Municipal High Income Opportunity Fund (NMZ)

Nuveen Municipal High Income Opportunity Fund 2 (NMD)

Portfolio managers Chris Drahn, Tom Spalding, Daniel Close and John Miller discuss U.S. economic and municipal market conditions, key investment strategies and the twelvemonth performance of these six national Funds. Chris assumed portfolio management responsibility for NQM in January 2011, Tom has managed NQS and NQU since 2003, Dan assumed portfolio management responsibility for NPF in January 2011 and John has managed NMZ since its inception in 2003 and has been involved in the management of NMD since its inception in 2007. He assumed full portfolio management responsibility for NMD in 2010.

What factors affected the U.S. economy and municipal market during the twelve-month reporting period ended October 31, 2012?

During this period, the U.S. economy’s progress toward recovery from recession continued at a moderate pace. The Federal Reserve (Fed) maintained its efforts to improve the overall economic environment by holding the benchmark fed funds rate at the record low level of zero to 0.25% that it established in December 2008. Subsequent to the reporting period, the central bank decided during its December 2012 meeting to keep the fed funds rate at “exceptionally low levels” until either the unemployment rate reaches 6.5% or expected inflation goes above 2.5%. The Fed also affirmed its decision, announced in September 2012, to purchase $40 billion of mortgage-backed securities each month in an effort to stimulate the housing market. In addition to this new, open-ended stimulus program, the Fed plans to continue its program to extend the average maturity of its holdings of U.S. Treasury securities through the end of December 2012. The goals of these actions, which together will increase the Fed’s holdings of longer term securities by approximately $85 billion a month through the end of the year, are to put downward pressure on longer term interest rates, make broader financial conditions more accommodative and support a stronger economic recovery as well as continued progress toward the Fed’s mandates of maximum employment and price stability.

Certain statements in this report are forward-looking statements. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The forward-looking statements and other views expressed herein are those of the portfolio managers as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and the views expressed herein are subject to change at any time, due to numerous market and other factors. The Funds disclaim any obligation to update publicly or revise any forward-looking statements or views expressed herein.

Ratings shown are the highest rating given by one of the following national rating agencies: Standard & Poor’s, Moody’s Investor Services, Inc., or Fitch, Inc. Credit ratings are subject to change. AAA, AA, A, and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below investment grade ratings. Certain bonds backed by U.S. Government or agency securities are regarded as having an implied rating equal to the rating of such securities. Holdings designated N/R are not rated by these national rating agencies.

| Nuveen Investments | 5 |

In the third quarter 2012, the U.S. economy, as measured by the U.S. gross domestic product (GDP), grew at an annualized rate of 2.7%, up from 1.3% in the second quarter, marking 13 consecutive quarters of positive growth. The Consumer Price Index (CPI) rose 2.2% year-over-year as of October 2012, while the core CPI (which excludes food and energy) increased 2.0% during the period, staying just within the Fed’s unofficial objective of 2.0% or lower for this inflation measure. As of November 2012 (subsequent to this reporting period), the national unemployment rate was 7.7%, the lowest unemployment rate since December 2008 and below the 8.7% level recorded in November 2011. The slight decrease in unemployment from 7.9% in October 2012 was primarily due to workers who are no longer counted as part of the workforce. The housing market, long a major weak spot in the economic recovery, showed signs of improvement, with the average home price in the S&P/Case-Shiller Index of 20 major metropolitan areas rising 3.0% for the twelve months ended September 2012 (most recent data available at the time this report was prepared). This marked the largest annual percentage gain for the index since July 2010, although housing prices continued to be off approximately 30% from their mid-2006 peak. The outlook for the U.S. economy remained clouded by uncertainty about global financial markets as well as the impending “fiscal cliff,” the combination of tax increases and spending cuts scheduled to take effect beginning January 2013 and their potential impact on the economy.

Municipal bond prices generally rallied during this period, as strong demand and tight supply combined to create favorable market conditions for municipal bonds. Although the total volume of tax-exempt supply improved over that of the same period a year earlier, the issuance pattern remained light compared with long-term historical trends, and new money issuance was relatively flat. This supply/demand dynamic served as a key driver of performance. Concurrent with rising prices, yields continued to decline across most maturities, especially at the longer end of the municipal yield curve and the curve flattened. In addition to the lingering effects of the Build America Bonds (BAB) program, which expired at the end of 2010 but impacted issuance well into 2012, the low level of municipal issuance reflected the current political distaste for additional borrowing by state and local governments facing fiscal constraints and the prevalent atmosphere of municipal budget austerity. During this period, we saw an increased number of borrowers come to market seeking to take advantage of the low rate environment through refunding activity, with approximately 60% of municipal paper issued by borrowers that were calling existing debt and refinancing at lower rates.

Over the twelve months ended October 31, 2012, municipal bond issuance nationwide totaled $379.6 billion, an increase of 18.6% over the issuance for the twelve-month period ended October 31, 2011. As previously discussed, the majority of this increase was attributable to refunding issues, rather than new money issuance. During this period, demand for municipal bonds remained consistently strong, especially from individual investors (as evidenced in part by flows into mutual funds) and also from banks and crossover buyers such as hedge funds.

| 6 | Nuveen Investments |

What key strategies were used to manage these Funds during the twelve-month reporting period ended October 31, 2012?

In an environment characterized by tight supply, strong demand and lower yields, we continued to take a bottom-up approach to discovering sectors that appeared undervalued as well as individual credits that had the potential to perform well over the long term. During this period, NQM, NQS, NQU and NPF generally found value in broad based essential services bonds backed by taxes or other revenues. NQS and NQU added health care bonds and took advantage of attractive valuation levels to purchase tobacco credits, which resulted in a slight increase in our allocations of these bonds. NPF and NQM also bought health care, dedicated tax bonds, local general obligation (GO) credits, water and sewer and tollway bonds.

In NMZ and NMD, our purchases largely focused on areas such as health care, community development districts (CDDs) and charter schools as well as a few special turnaround situations, that is, individual credits that we believed offered stability and appreciation potential at exceptionally attractive and compelling prices and yields, especially in relation to their underlying credit quality. Some examples of our purchases during this period included bonds issued for Cardinal Health System, Indiana, in NMD; Mariposa East Public Improvement District, New Mexico, in NMZ; Ave Maria CDD, Florida, in NMD; Renaissance Charter School, Florida, in NMZ and Carden Traditional Schools, Arizona, in NMD. Both Funds also purchased bonds issued by the Illinois Finance Authority for the Fullerton Village Project at DePaul University, Chicago. We purchased these student housing revenue bonds at a deep discount based on our belief that the recovery demonstrated by this dorm project over the past three years will continue.

In general during this period, all of the Funds emphasized bonds with longer maturities. This enabled us to take advantage of more attractive yields at the longer end of the municipal yield curve and also provided some protection for the Funds’ duration and yield curve positioning. In terms of quality, NQM and NPF did purchase lower rated bonds when we found attractive opportunities, as we believed these bonds continued to offer relative value. NQS and NQU generally focused on higher quality bonds with the goal of positioning these two Funds slightly more defensively. NMZ and NMD entered this period with allocation levels below the 50% maximum allowable in non-rated and sub-investment grade bonds and we continued to invest in these categories during the period. Our opportunities to purchase bonds with longer maturities and lower credit quality were somewhat constrained during this period by the structure of bonds typically issued as part of refinancing deals, which tend to be characterized by shorter maturities and higher credit quality.

We also took advantage of short-term opportunities created by the supply/demand dynamics in the municipal market. While demand for tax-exempt paper remained consistently strong throughout the period, supply fluctuated widely. We found that

| Nuveen Investments | 7 |

periods of substantial supply provided good short-term buying opportunities not only because of the increased number of issues available, but also because some investors became more hesitant in their buying as supply grew, causing spreads to widen temporarily. At times when supply was more plentiful, we were proactive in focusing on anticipating cash flows from bond calls and maturing bonds and closely monitored opportunities for reinvestment.

Cash for new purchases during this period was generated primarily by the proceeds from an increased number of bond calls resulting from the growth in refinancings. During this period, we worked to redeploy these proceeds as well as those from maturing bonds to keep the Funds as fully invested as possible. In NPF, we also sold selected pre-refunded bonds to generate additional cash. Overall, selling was relatively limited because the bonds in our portfolios generally offered higher yields than those available in the current marketplace.

As of October 31, 2012, all six of these Funds continued to use inverse floating rate securities. We employ inverse floaters for a variety of reasons, including duration management, income enhancement and total return enhancement. As part of our duration management strategies, NMZ and NMD also made moderate use of interest rate swaps and forward interest rate swaps to reduce price volatility risk to movements in U.S. interest rates relative to the Funds’ benchmark. During this period, interest rates declined and therefore these swaps had a mildly negative impact on performance. These swaps remained in place at period end.

How did the Funds perform during the twelve-month reporting period ended October 31, 2012?

Individual results for these Funds, as well as relevant index and peer group information, are presented in the accompanying table.

Average Annual Total Returns on Common Share Net Asset Value

For periods ended 10/31/12

| Fund | 1-Year | 5-Year | 10-Year |

| NQM | 18.37% | 8.46% | 7.02% |

| NQS | 19.50% | 8.37% | 7.36% |

| NQU | 19.63% | 7.96% | 7.15% |

| NPF | 14.98% | 7.14% | 6.26% |

| S&P Municipal Bond Index* | 9.56% | 5.83% | 5.35% |

| Lipper General & Insured Leveraged Municipal Debt Funds Classification Average* | 18.77% | 7.73% | 6.99% |

| NMZ | 24.55% | 6.23% | N/A |

| NMD | 24.56% | N/A | N/A |

| S&P Municipal Bond High Yield Index* | 17.01% | 5.38% | 7.20% |

| Lipper High-Yield Municipal Debt Funds Classification Average* | 20.08% | 6.80% | 6.87% |

| Past performance is not predictive of future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. | |

| For additional information, see the Performance Overview page for your Fund in this report. | |

| * | Refer to the Glossary of Terms Used in this Report for definitions. Indexes and Lipper averages are not available for direct investment. |

| 8 | Nuveen Investments |

For the twelve months ended October 31, 2012, the total returns on common share net asset value (NAV) for NQM, NQS, NQU and NPF exceeded the return for the S&P Municipal Bond Index. NQS and NQU outperformed the average return for the Lipper General & Insured Leveraged Municipal Debt Funds Classification Average and NQM and NPF lagged this Lipper average. For the same period, NMZ and NMD outperformed the return for the S&P Municipal Bond High Yield Index as well as the average return for the Lipper High-Yield Municipal Debt Funds Classification Average.

Key management factors that influenced the Funds’ returns during this period included duration and yield curve positioning, the use of derivatives in NMZ and NMD, credit exposure and sector allocation. In addition, the use of regulatory leverage was an important positive factor affecting the Funds’ performance over this period. Leverage is discussed in more detail later in this report.

In an environment of declining rates and a flattening yield curve, municipal bonds with longer maturities generally outperformed those with shorter maturities during this period. Overall, credits at the longest end of the municipal yield curve posted the strongest returns, while bonds at the shortest end produced the weakest results. For this period, duration and yield curve positioning was a major positive contributor to the performance of these Funds, with the net impact varying according to each Fund’s individual weightings along the yield curve. Overall, NQU, NMZ and NMD were the most advantageously positioned in terms of duration and yield curve during this period. All of the Funds benefited from their holdings of long duration bonds, many of which had zero percent coupons, which generally outperformed the market. This was especially true in NQM, NQS and NQU, all of which were overweight in zero coupon bonds. While the Funds were overweight in the longer parts of the yield curve that performed well, NPF also was overweight in bonds with shorter maturities, particularly pre-refunded bonds, which constrained its participation in the market rally.

Although both NMZ and NMD benefited from their longer durations, these Funds used interest rate swaps and forward interest rate swaps to reduce duration and moderate interest rate risk. Because the interest rate swaps were used to hedge against a potential rise in interest rates, the swaps performed poorly as interest rates fell, negatively impacting the Funds’ total return performance for the period. This was offset by the Funds’ overall duration and yield curve positioning and the strong performance of their municipal bond holdings.

Credit exposure was another important factor in the Funds’ performance during these twelve months, as lower quality bonds generally outperformed higher quality bonds. This outperformance was due in part to the greater demand for lower rated bonds as investors looked for investment vehicles offering higher yields. As investors became more comfortable taking on additional investment risk, credit spreads, or the difference in yield spreads between U.S. Treasury securities and comparable investments such as municipal bonds, narrowed through a variety of rating categories. As a result of this spread compression, all of these Funds benefited from their holdings of lower rated

| Nuveen Investments | 9 |

credits. Both NMZ and NMD had heavy weightings in credits rated BBB or lower as well as non-rated bonds, which also generally performed well. For the period, NPF had the heaviest weighting of bonds rated AAA and the smallest weighting of BBB bonds, which detracted from its performance.

During this period, revenue bonds as a whole outperformed the general municipal market. Holdings that generally made positive contributions to the Funds’ returns included health care (together with hospitals), transportation (especially toll roads), education and water and sewer bonds. All of these Funds had strong weightings in health care, which added to their performance, although NPF’s allocation to this sector was smaller than that of the other five Funds. Tobacco credits backed by the 1998 master tobacco settlement agreement also performed extremely well, helped in part by their longer effective durations. These bonds also benefited from market developments, including increased demand for higher yielding investments by investors who had become less risk averse. In addition, based on recent data showing that cigarette sales had fallen less steeply than anticipated, the 46 states participating in the agreement stand to receive increased payments from the tobacco companies. As of October 31, 2012, NQM, NPF and especially NQS and NQU were overweight in tobacco bonds, which benefited their performance as tobacco credits rallied. Although NMZ and NMD were underexposed to the tobacco sector relative to the S&P Municipal Bond High Yield index, their weightings were strong enough to make a substantial positive contribution to performance.

In addition to a focus on health care, NMZ and NMD emphasized bonds in the real estate sector, including CDDs and charter school subsectors of the high yield segment of the municipal market. During this period, these Funds were rewarded with strong performance from CDD holdings including Pine Island, Beacon Lakes and Westchester, all in Florida, as they experienced growth in assessed property valuations and debt service coverage. NMZ also benefited from improvement in its holding of bonds issued for the conference center project in downtown Vancouver, Washington. Both Funds have relatively modest exposures to American Airlines facilities in several locations. While the airline filed for bankruptcy in November 2011, these holdings were deemed to be secured interests, which are backed by security interests in property and take precedence over unsecured claims and they performed well for the Funds.

In contrast, pre-refunded bonds, which are often backed by U.S. Treasury securities, were the poorest performing market segment during this period. The underperfor-mance of these bonds can be attributed primarily to their shorter effective maturities and higher credit quality. As of October 31, 2012, NPF held the heaviest weighting of pre-refunded bonds, which detracted from its performance during this period. As higher quality credits with shorter durations, pre-refunded bonds generally do not fit the profiles of longer term, higher yielding Funds such as NMZ and NMD, and these two Funds had negligible exposure to pre-refunded bonds. GO bonds and housing and utilities (e.g., resource recovery, public power) credits also lagged the performance of the general municipal market for this period. These Funds tended to have relatively lighter exposures to GOs, which lessened the impact of these holdings.

| 10 | Nuveen Investments |

NMZ and NMD also were impacted by a few small, isolated credit disappointments. In NMZ, these included the Southgate Suites Hotel project in New Orleans, Northern Berkshire Community Services bonds issued by the Massachusetts Health and Educational Facilities Authority and the EnerTech Regional Biosolids project in California. NMD also held the Southgate project bonds as well as credits issued for the Roberts Hotel project in Jackson, Mississippi. We continued to own these securities because we have seen some recent improvements in performance, and we believed their further downside risk was limited. Overall, the impact of these distressed holdings was minimized by the Funds’ duration and yield curve positioning, credit allocations, and the strong performance of their other holdings.

APPROVED FUND REORGANIZATION

On December 13, 2012, (subsequent to the close of this reporting period), the reorganization of NMD into NMZ was approved by each Fund’s Board of Trustees. The reorganization is intended to create a single larger national Fund, which would potentially offer shareholders the following benefits:

| • | Lower Fund expense ratios (excluding the effects of leverage), as fixed costs are spread over a larger asset base; |

| • | Enhanced secondary market trading, as larger Funds potentially make it easier for investors to buy and sell Fund shares; |

| • | Lower per share trading costs through reduced bid/ask spreads due to a larger common share float; and |

| • | Increased Fund flexibility in managing the structure and cost of leverage over time. |

If shareholders approve the reorganization, and upon the closing of the reorganization, NMD will transfer its assets to NMZ in exchange for common shares of NMZ, and the assumption by NMZ of the liabilities of NMD. NMD will then be liquidated, dissolved and terminated in accordance with its Declaration of Trust. In addition, shareholders of NMD will become shareholders of NMZ. Holders of common shares will receive newly issued common shares of NMZ, the aggregate net asset value of which will be equal to the aggregate net asset value of the common shares of NMD held immediately prior to the reorganization (including for this purpose fractional NMZ shares to which shareholders would be entitled). Fractional shares will be sold on the open market and shareholders will receive cash in lieu of such fractional shares.

| Nuveen Investments | 11 |

Fund Leverage and

Other Information

IMPACT OF THE FUNDS’ LEVERAGE STRATEGIES ON PERFORMANCE

One important factor impacting the returns of all these Funds relative to the comparative indexes was the Funds’ use of leverage. The Funds use leverage because their managers believe that, over time, leveraging provides opportunities for additional income and total return for common shareholders. However, use of leverage also can expose common shareholders to additional volatility. For example, as the prices of securities held by a Fund decline, the negative impact of these valuation changes on common share net asset value and common shareholder total return is magnified by the use of leverage. Conversely, leverage may enhance common share returns during periods when the prices of securities held by a Fund generally are rising. Leverage made a positive contribution to the performance of these Funds over this reporting period.

THE FUNDS’ REGULATORY LEVERAGE

As of October 31, 2012, the following Funds have issued and outstanding Variable Rate Demand Preferred (VRDP) Shares as shown in the accompanying table.

VRDP Shares

| VRDP Shares Issued | |||

| Fund | at Liquidation Value | ||

| NQM | $ | 211,800,000 | |

| NQS | $ | 252,500,000 | |

| NQU | $ | 388,400,000 | |

| NPF | $ | 127,700,000 | |

(Refer to Notes to Financial Statements, Footnote 1 – General Information and Significant Accounting Policies for further details on VRDP Shares.)

Bank Borrowings

NMZ and NMD employ regulatory leverage through the use of bank borrowings. (Refer to Notes to Financial Statements, Footnote 8 — Borrowings Arrangements for further details on each Fund’s bank borrowings.)

| 12 | Nuveen Investments |

SUBSEQUENT LEVERAGING EVENTS

On December 21, 2012, subsequent to the close of this reporting period, both NMZ and NMD terminated their borrowings with the custodian bank and paid the full outstanding balance, including accrued interest and fees.

In conjunction with terminating these borrowings, NMZ and NMD issued $51 million and $36 million ($100,000 liquidation value per share) of Variable Rate MuniFund Term Preferred (VMTP) Shares, respectively, as a new form of leverage. Proceeds from the issuance of VMTP Shares were used to pay each Fund’s outstanding balance on its borrowings as described above. VMTP Shares were offered only to qualified institutional buyers, pursuant to Rule 144A under the Securities Act of 1933. VMTP Shares pay dividends weekly and will be set at a fixed spread to the Securities Industry and Financial Markets Association Municipal Swap Index (SIFMA).

RISK CONSIDERATIONS

Fund shares are not guaranteed or endorsed by any bank or other insured depository institution, and are not federally insured by the Federal Deposit Insurance Corporation. Past performance is no guarantee of future results. Fund common shares are subject to a variety of risks, including:

Investment and Market Risk. An investment in common shares is subject to investment risk, including the possible loss of the entire principal amount that you invest. Your investment in common shares represents an indirect investment in the municipal securities owned by the Fund, which generally trade in the over-the-counter markets. Your common shares at any point in time may be worth less than your original investment, even after taking into account the reinvestment of Fund dividends and distributions.

Price Risk. Shares of closed-end investment companies like these Funds frequently trade at a discount to their NAV. Your common shares at any point in time may be worth less than your original investment, even after taking into account the reinvestment of Fund dividends and distributions.

Leverage Risk. Each Fund’s use of leverage creates the possibility of higher volatility for the Fund’s per share NAV, market price, distributions and returns. There is no assurance that a Fund’s leveraging strategy will be successful.

Issuer Credit Risk. This is the risk that a security in a Fund’s portfolio will fail to make dividend or interest payments when due.

| Nuveen Investments | 13 |

Credit Risk. An issuer of a bond held by a Fund may be unable to make interest and principal payments when due. A failure by the issuer to make such payments is called a “default”. A default can cause the price of the issuer’s bonds to plummet. Even if the issuer does not default, the prices of its bonds can fall if the market perceives that the risk of default is increasing.

Low-Quality Bond Risk. NMZ and NMD concentrate a large portion of their investments in low-quality municipal bonds (sometimes called “junk bonds”), which have greater credit risk and generally are less liquid and have more volatile prices than higher quality securities.

Interest Rate Risk. Fixed-income securities such as bonds, preferred, convertible and other debt securities will decline in value if market interest rates rise.

Derivatives Risk. The Funds may use derivative instruments which involve a high degree of financial risk, including the risk that the loss on a derivative may be greater than the principal amount invested.

Inverse Floater Risk. The Funds may invest in inverse floaters. Due to their leveraged nature, these investments can greatly increase a Fund’s exposure to interest rate risk and credit risk. In addition, investments in inverse floaters involve the risk that the Fund could lose more than its original principal investment.

Reinvestment Risk. If market interest rates decline, income earned from a Fund’s portfolio may be reinvested at rates below that of the original bond that generated the income.

Call Risk or Prepayment Risk. Issuers may exercise their option to prepay principal earlier than scheduled, forcing a Fund to reinvest in lower-yielding securities.

Tax Risk. The tax treatment of Fund distributions may be affected by new IRS interpretations of the Internal Revenue Code and future changes in tax laws and regulations.

Below-Investment Grade Risk. Investments in securities below investment grade quality are predominantly speculative and subject to greater volatility and risk of default.

| 14 | Nuveen Investments |

Common Share Dividend

and Price Information

DIVIDEND INFORMATION

During the twelve-month reporting period ended October 31, 2012, the monthly dividends of NQM, NMZ and NMD remained stable throughout the period, while the dividends of NQS, NQU and NPF were each reduced once during the period.

Due to normal portfolio activity, common shareholders of the following Funds received capital gains or net ordinary income distributions in December 2011 as follows:

| Short-Term Capital Gains | ||||||

| Long-Term Capital Gains | and/or Ordinary Income | |||||

| Fund | (per share) | (per share) | ||||

| NQS | $ | 0.0759 | — | |||

| NQU | $ | 0.0335 | — | |||

| NMZ | — | $ | 0.0231 | |||

| NMD | — | $ | 0.0035 | |||

All of the Funds in this report seek to pay stable dividends at rates that reflect each Fund’s past results and projected future performance. During certain periods, each Fund may pay dividends at a rate that may be more or less than the amount of net investment income actually earned by the Fund during the period. If a Fund has cumulatively earned more than it has paid in dividends, it holds the excess in reserve as undistributed net investment income (UNII) as part of the Fund’s NAV. Conversely, if a Fund has cumulatively paid dividends in excess of its earnings, the excess constitutes negative UNII that is likewise reflected in the Fund’s NAV. Each Fund will, over time, pay all of its net investment income as dividends to shareholders. As of October 31, 2012, all of the Funds in this report had positive UNII balances for both tax and financial reporting purposes.

COMMON SHARE REPURCHASES AND PRICE INFORMATION

As of October 31, 2012, and since the inception of the Funds’ repurchase programs, NPF has cumulatively repurchased and retired its outstanding common shares as shown in the accompanying table. Since the inception of the Funds’ repurchase programs, NQM, NQS, NQU, NMZ and NMD have not repurchased any of their outstanding common shares.

| Common Shares | % of Outstanding | |

| Fund | Repurchased and Retired | Common Shares |

| NPF | 202,500 | 1.0% |

During the twelve-month reporting period, NPF did not repurchase any of its outstanding common shares.

| Nuveen Investments | 15 |

As of October 31, 2012, and during the twelve-month reporting period, the Funds’ common share prices were trading at (+) premiums and/or (-) discounts to their common share NAVs as shown in the accompanying table.

| 10/31/12 | Twelve-Month Average | |

| Fund | (+)Premium/(-)Discount | (+)Premium/(-)Discount |

| NQM | (+)0.24% | (+)0.04% |

| NQS | (+)2.89% | (+)1.90% |

| NQU | (-)2.11% | (-)1.69% |

| NPF | (-)1.21% | (-)2.11% |

| NMZ | (+)5.72% | (+)3.51% |

| NMD | (+)0.46% | (+)0.16% |

SHELF EQUITY PROGRAMS

NQS, NMZ and NMD have each filed registration statements with the Securities and Exchange Commission (SEC) authorizing the Funds to issue additional common shares, through an equity shelf offering program. Under these equity shelf programs, the Funds, subject to market conditions, may raise additional capital from time to time in varying amounts and offering methods at a net price at or above each Fund’s NAV per common share.

As of October 31, 2012, NQS, NMZ and NMD had cumulatively sold 490,341, 5,953,081 and 2,302,664 common shares, respectively, through their shelf equity programs.

During the twelve-month reporting period, NQS, NMZ and NMD sold common shares through their shelf equity programs at a weighted average premium to NAV per common share as shown in the accompanying table.

| Common Shares | Weighted Average | |

| Sold through | Premium to NAV | |

| Fund | Shelf Offering | Per Share Sold |

| NQS | 490,341 | 1.71% |

| NMZ | 2,004,701 | 4.05% |

| NMD | 702,445 | 1.81% |

On October 29, 2012, NQM filed a preliminary prospectus with the SEC for an equity shelf offering, pursuant to which the Fund may issue additional common shares. New common shares of NQM will not be sold until the registration statement is effective.

(Refer to Notes to Financial Statements, Footnote 1 - General Information and Significant Accounting Policies for further details on the Funds’ Shelf Equity Programs.)

| 16 | Nuveen Investments |

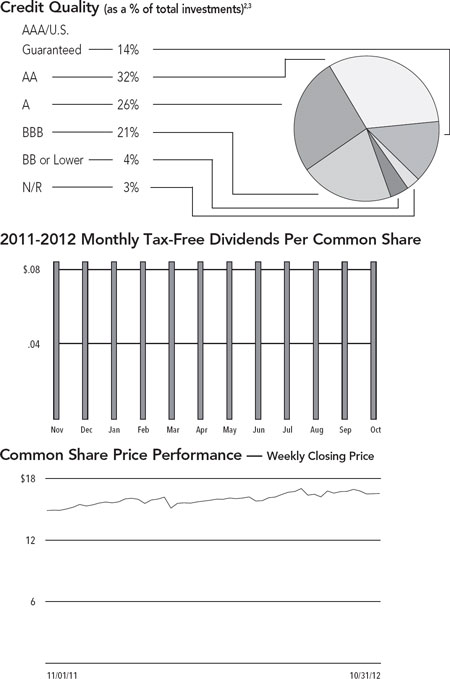

| NQM | Nuveen Investment | |

| Performance | Quality Municipal | |

| OVERVIEW | Fund, Inc. | |

| as of October 31, 2012 |

| Fund Snapshot | ||||

| Common Share Price | $ | 16.64 | ||

| Common Share Net Asset Value (NAV) | $ | 16.60 | ||

| Premium/(Discount) to NAV | 0.24 | % | ||

| Market Yield | 6.06 | % | ||

Taxable-Equivalent Yield1 | 8.42 | % | ||

| Net Assets Applicable to Common Shares ($000) | $ | 596,684 | ||

| Leverage | ||||

| Regulatory Leverage | 26.20 | % | ||

| Effective Leverage | 34.15 | % |

| Average Annual Total Returns | |||||||

| (Inception 6/21/90) | |||||||

| On Share Price | On NAV | ||||||

| 1-Year | 21.61 | % | 18.37 | % | |||

| 5-Year | 10.53 | % | 8.46 | % | |||

| 10-Year | 7.77 | % | 7.02 | % | |||

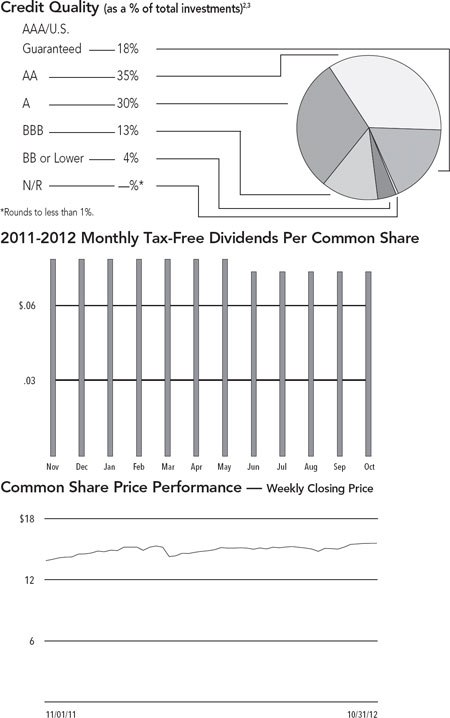

States3 | ||||

| (as a % of total investments) | ||||

| California | 17.2 | % | ||

| New York | 10.2 | % | ||

| Texas | 8.0 | % | ||

| Illinois | 8.0 | % | ||

| Florida | 5.6 | % | ||

| District of Columbia | 4.1 | % | ||

| Colorado | 3.4 | % | ||

| Ohio | 3.2 | % | ||

| Pennsylvania | 2.5 | % | ||

| Michigan | 2.5 | % | ||

| Minnesota | 2.4 | % | ||

| Tennessee | 2.3 | % | ||

| Arizona | 2.2 | % | ||

| Wisconsin | 2.1 | % | ||

| Massachusetts | 2.0 | % | ||

| New Jersey | 1.7 | % | ||

| Nebraska | 1.6 | % | ||

| Puerto Rico | 1.6 | % | ||

| Missouri | 1.5 | % | ||

| South Carolina | 1.4 | % | ||

| Georgia | 1.4 | % | ||

| Louisiana | 1.3 | % | ||

| Other | 13.8 | % |

Portfolio Composition3 | ||||

| (as a % of total investments) | ||||

| Health Care | 21.4 | % | ||

| Tax Obligation/Limited | 17.3 | % | ||

| Transportation | 11.2 | % | ||

| U.S. Guaranteed | 10.1 | % | ||

| Tax Obligation/General | 9.4 | % | ||

| Education and Civic Organizations | 8.7 | % | ||

| Water and Sewer | 8.4 | % | ||

| Utilities | 5.9 | % | ||

| Other | 7.6 | % |

| Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this Fund’s Performance Overview page. | |

| 1 | Taxable-Equivalent Yield represents the yield that must be earned on a fully taxable investment in order to equal the yield of the Fund on an after-tax basis. It is based on a federal income tax rate of 28%. When comparing this Fund to investments that generate qualified dividend income, the Taxable-Equivalent Yield is lower. |

| 2 | Ratings shown are the highest rating given by one of the following national rating agencies: Standard & Poor’s, Moody’s Investors Service, Inc. or Fitch, Inc. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Certain bonds backed by U.S. Government or agency securities are regarded as having an implied rating equal to the rating of such securities. Holdings designated N/R are not rated by these national rating agencies. |

| 3 | Holdings are subject to change. |

| Nuveen Investments | 17 |

| NQS | Nuveen Select | |

| Performance | Quality Municipal | |

| OVERVIEW | Fund, Inc. | |

| as of October 31, 2012 |

| Fund Snapshot | ||||

| Common Share Price | $ | 16.40 | ||

| Common Share Net Asset Value (NAV) | $ | 15.94 | ||

| Premium/(Discount) to NAV | 2.89 | % | ||

| Market Yield | 5.85 | % | ||

Taxable-Equivalent Yield1 | 8.13 | % | ||

| Net Assets Applicable to Common Shares ($000) | $ | 557,646 | ||

| Leverage | ||||

| Regulatory Leverage | 31.18 | % | ||

| Effective Leverage | 35.81 | % |

| Average Annual Total Returns | |||||||

| (Inception 3/21/91) | |||||||

| On Share Price | On NAV | ||||||

| 1-Year | 20.32 | % | 19.50 | % | |||

| 5-Year | 9.19 | % | 8.37 | % | |||

| 10-Year | 8.26 | % | 7.36 | % | |||

States3 | ||||

| (as a % of total investments) | ||||

| Texas | 13.4 | % | ||

| Illinois | 12.0 | % | ||

| California | 9.1 | % | ||

| Michigan | 5.8 | % | ||

| Ohio | 4.8 | % | ||

| Colorado | 4.4 | % | ||

| South Carolina | 3.9 | % | ||

| Florida | 3.4 | % | ||

| Arizona | 3.1 | % | ||

| Tennessee | 2.9 | % | ||

| Pennsylvania | 2.7 | % | ||

| Puerto Rico | 2.6 | % | ||

| New Jersey | 2.6 | % | ||

| Nevada | 2.1 | % | ||

| New York | 2.1 | % | ||

| Massachusetts | 2.0 | % | ||

| District of Columbia | 1.9 | % | ||

| Indiana | 1.9 | % | ||

| Virginia | 1.8 | % | ||

| Missouri | 1.7 | % | ||

| Washington | 1.6 | % | ||

| Other | 14.2 | % |

Portfolio Composition3 | ||||

| (as a % of total investments) | ||||

| Health Care | 22.5 | % | ||

| Tax Obligation/General | 16.5 | % | ||

| Tax Obligation/Limited | 16.0 | % | ||

| Transportation | 10.8 | % | ||

| U.S. Guaranteed | 9.0 | % | ||

| Consumer Staples | 7.5 | % | ||

| Utilities | 6.3 | % | ||

| Other | 11.4 | % |

| Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this Fund’s Performance Overview page. | |

| 1 | Taxable-Equivalent Yield represents the yield that must be earned on a fully taxable investment in order to equal the yield of the Fund on an after-tax basis. It is based on a federal income tax rate of 28%. When comparing this Fund to investments that generate qualified dividend income, the Taxable-Equivalent Yield is lower. |

| 2 | Ratings shown are the highest rating given by one of the following national rating agencies: Standard & Poor’s, Moody’s Investors Service, Inc. or Fitch, Inc. Credit ratings are subject to change. AAA, AA, A, and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Certain bonds backed by U.S.Government or agency securities are regarded as having an implied rating equal to the rating of such securities. Holdings designated N/R are not rated by these national rating agencies. |

| 3 | Holdings are subject to change. |

| 4 | The Fund paid shareholders a capital gains distribution in December 2011 of $0.0759 per share. |

| 18 | Nuveen Investments |

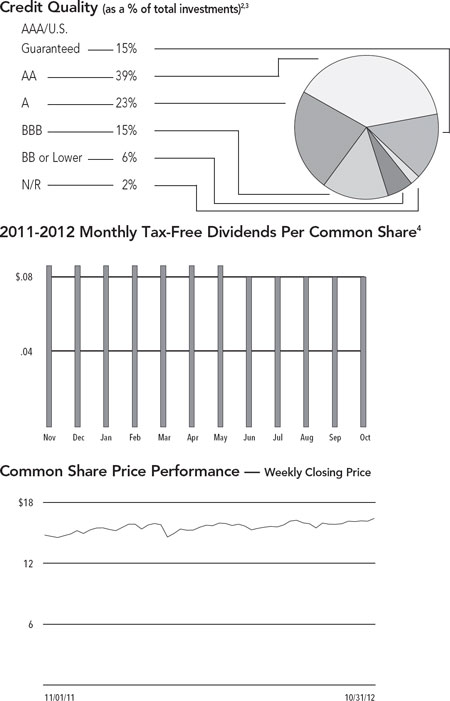

| NQU | Nuveen Quality | |

| Performance | Income Municipal | |

| OVERVIEW | Fund, Inc. | |

| as of October 31, 2012 |

| Fund Snapshot | ||||

| Common Share Price | $ | 15.81 | ||

| Common Share Net Asset Value (NAV) | $ | 16.15 | ||

| Premium/(Discount) to NAV | -2.11 | % | ||

| Market Yield | 5.62 | % | ||

Taxable-Equivalent Yield1 | 7.81 | % | ||

| Net Assets Applicable to Common Shares ($000) | $ | 878,070 | ||

| Leverage | ||||

| Regulatory Leverage | 30.67 | % | ||

| Effective Leverage | 34.55 | % |

| Average Annual Total Returns | |||||||

| (Inception 6/19/91) | |||||||

| On Share Price | On NAV | ||||||

| 1-Year | 21.16 | % | 19.63 | % | |||

| 5-Year | 9.73 | % | 7.96 | % | |||

| 10-Year | 7.68 | % | 7.15 | % | |||

States3 | ||||

| (as a % of total investments) | ||||

| California | 16.2 | % | ||

| Illinois | 9.7 | % | ||

| Texas | 7.0 | % | ||

| New York | 5.7 | % | ||

| Puerto Rico | 5.7 | % | ||

| Colorado | 4.5 | % | ||

| Ohio | 4.3 | % | ||

| Michigan | 4.1 | % | ||

| New Jersey | 3.6 | % | ||

| South Carolina | 3.1 | % | ||

| Louisiana | 2.7 | % | ||

| Pennsylvania | 2.6 | % | ||

| North Carolina | 2.5 | % | ||

| Massachusetts | 2.2 | % | ||

| Indiana | 2.1 | % | ||

| Nevada | 2.0 | % | ||

| Washington | 1.9 | % | ||

| Arizona | 1.8 | % | ||

| Missouri | 1.8 | % | ||

| Virginia | 1.7 | % | ||

| Other | 14.8 | % |

Portfolio Composition3 | ||||

| (as a % of total investments) | ||||

| Health Care | 20.0 | % | ||

| Tax Obligation/Limited | 17.2 | % | ||

| Transportation | 16.1 | % | ||

| Tax Obligation/General | 15.0 | % | ||

| U.S. Guaranteed | 9.1 | % | ||

| Consumer Staples | 7.3 | % | ||

| Utilities | 6.1 | % | ||

| Education and Civic Organizations | 5.7 | % | ||

| Other | 3.5 | % |

| Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this Fund’s Performance Overview page. | |

| 1 | Taxable-Equivalent Yield represents the yield that must be earned on a fully taxable investment in order to equal the yield of the Fund on an after-tax basis. It is based on a federal income tax rate of 28%. When comparing this Fund to investments that generate qualified dividend income, the Taxable-Equivalent Yield is lower. |

| 2 | Ratings shown are the highest rating given by one of the following national rating agencies: Standard & Poor’s, Moody’s Investors Service, Inc. or Fitch, Inc. Credit ratings are subject to change. AAA, AA, A, and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Certain bonds backed by U.S. Government or agency securities are regarded as having an implied rating equal to the rating of such securities. Holdings designated N/R are not rated by these national rating agencies. |

| 3 | Holdings are subject to change. |

| 4 | The Fund paid shareholders a capital gains distribution in December 2011 of $0.0335 per share. |

| Nuveen Investments | 19 |

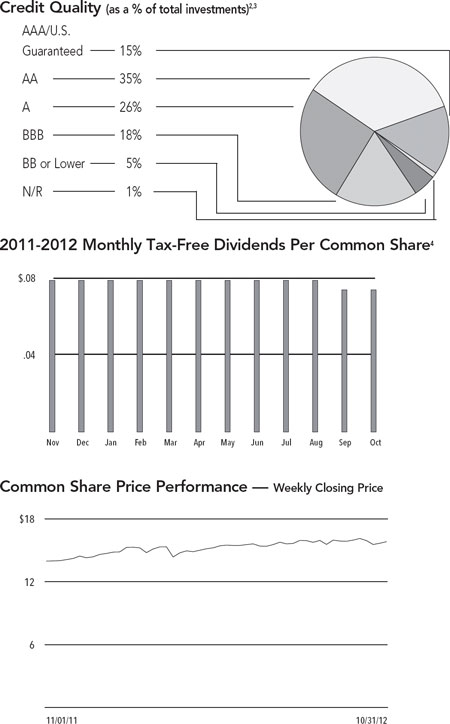

| NPF | Nuveen Premier | |

| Performance | Municipal Income | |

| OVERVIEW | Fund, Inc. | |

| as of October 31, 2012 |

| Fund Snapshot | ||||

| Common Share Price | $ | 15.46 | ||

| Common Share Net Asset Value (NAV) | $ | 15.65 | ||

| Premium/(Discount) to NAV | -1.21 | % | ||

| Market Yield | 5.71 | % | ||

Taxable-Equivalent Yield1 | 7.93 | % | ||

| Net Assets Applicable to Common Shares ($000) | $ | 311,279 | ||

| Leverage | ||||

| Regulatory Leverage | 29.09 | % | ||

| Effective Leverage | 36.45 | % |

| Average Annual Total Returns | |||||||

| (Inception 12/19/91) | |||||||

| On Share Price | On NAV | ||||||

| 1-Year | 18.11 | % | 14.98 | % | |||

| 5-Year | 9.60 | % | 7.14 | % | |||

| 10-Year | 7.06 | % | 6.26 | % | |||

States3 | ||||

| (as a % of total investments) | ||||

| California | 12.4 | % | ||

| Illinois | 11.8 | % | ||

| New York | 9.9 | % | ||

| Colorado | 5.7 | % | ||

| New Jersey | 4.9 | % | ||

| South Carolina | 4.6 | % | ||

| Louisiana | 4.5 | % | ||

| Michigan | 4.4 | % | ||

| Texas | 4.2 | % | ||

| Minnesota | 3.3 | % | ||

| North Carolina | 2.8 | % | ||

| Arizona | 2.7 | % | ||

| Massachusetts | 2.7 | % | ||

| Indiana | 2.1 | % | ||

| Ohio | 1.8 | % | ||

| Georgia | 1.8 | % | ||

| Pennsylvania | 1.5 | % | ||

| Nevada | 1.5 | % | ||

| Tennessee | 1.4 | % | ||

| Washington | 1.1 | % | ||

| Other | 14.9 | % |

Portfolio Composition3 | ||||

| (as a % of total investments) | ||||

| Tax Obligation/Limited | 21.2 | % | ||

| U.S. Guaranteed | 16.7 | % | ||

| Transportation | 13.8 | % | ||

| Health Care | 13.5 | % | ||

| Utilities | 9.2 | % | ||

| Water and Sewer | 8.3 | % | ||

| Tax Obligation/General | 7.3 | % | ||

| Other | 10.0 | % |

| Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this Fund’s Performance Overview page. | |

| 1 | Taxable-Equivalent Yield represents the yield that must be earned on a fully taxable investment in order to equal the yield of the Fund on an after-tax basis. It is based on a federal income tax rate of 28%. When comparing this Fund to investments that generate qualified dividend income, the Taxable-Equivalent Yield is lower. |

| 2 | Ratings shown are the highest rating given by one of the following national rating agencies: Standard & Poor’s, Moody’s Investors Service, Inc. or Fitch, Inc. Credit ratings are subject to change. AAA, AA, A, and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Certain bonds backed by U.S. Government or agency securities are regarded as having an implied rating equal to the rating of such securities. Holdings designated N/R are not rated by these national rating agencies. |

| 3 | Holdings are subject to change. |

| 20 | Nuveen Investments |

| NMZ | Nuveen Municipal | |

| Performance | High Income | |

| OVERVIEW | Opportunity Fund | |

| as of October 31, 2012 |

| Fund Snapshot | ||||

| Common Share Price | $ | 14.22 | ||

| Common Share Net Asset Value (NAV) | $ | 13.45 | ||

| Premium/(Discount) to NAV | 5.72 | % | ||

| Market Yield | 6.16 | % | ||

Taxable-Equivalent Yield2 | 8.56 | % | ||

| Net Assets Applicable to Common Shares ($000) | $ | 402,573 | ||

| Leverage | ||||

| Regulatory Leverage | 11.06 | % | ||

| Effective Leverage | 33.93 | % |

| Average Annual Total Returns | |||||||

| (Inception 11/19/03) | |||||||

| On Share Price | On NAV | ||||||

| 1-Year | 29.84 | % | 24.55 | % | |||

| 5-Year | 6.45 | % | 6.23 | % | |||

| Since Inception | 7.18 | % | 7.36 | % | |||

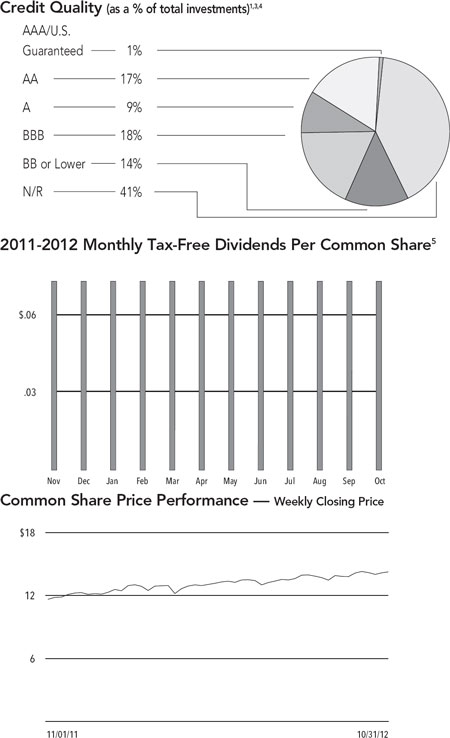

States1,4 | ||||

| (as a % of total investments) | ||||

| California | 13.9 | % | ||

| Florida | 11.2 | % | ||

| Texas | 8.2 | % | ||

| Illinois | 7.7 | % | ||

| Colorado | 6.5 | % | ||

| Arizona | 5.9 | % | ||

| Wisconsin | 3.7 | % | ||

| Indiana | 3.4 | % | ||

| Michigan | 3.2 | % | ||

| Ohio | 2.8 | % | ||

| Louisiana | 2.5 | % | ||

| Washington | 2.5 | % | ||

| Nebraska | 2.5 | % | ||

| New Jersey | 2.3 | % | ||

| North Carolina | 1.9 | % | ||

| Pennsylvania | 1.8 | % | ||

| Tennessee | 1.7 | % | ||

| New York | 1.7 | % | ||

| Missouri | 1.5 | % | ||

| Maryland | 1.1 | % | ||

| Other | 14.0 | % |

Portfolio Composition1,4 | ||||

| (as a % of total investments) | ||||

| Tax Obligation/Limited | 26.8 | % | ||

| Health Care | 19.9 | % | ||

| Education and Civic Organizations | 12.4 | % | ||

| Utilities | 7.6 | % | ||

| Transportation | 6.6 | % | ||

| Housing/Multifamily | 5.7 | % | ||

| Industrials | 4.0 | % | ||

| Consumer Staples | 3.5 | % | ||

| Other | 13.5 | % |

| Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this Fund’s Performance Overview page. | |

| 1 | Excluding investments in derivatives. |

| 2 | Taxable-Equivalent Yield represents the yield that must be earned on a fully taxable investment in order to equal the yield of the Fund on an after-tax basis. It is based on a federal income tax rate of 28%. When comparing this Fund to investments that generate qualified dividend income, the Taxable-Equivalent Yield is lower. |

| 3 | Ratings shown are the highest rating given by one of the following national rating agencies: Standard & Poor’s, Moody’s Investors Service, Inc. or Fitch, Inc. Credit ratings are subject to change. AAA, AA, A, and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Certain bonds backed by U.S. Government or agency securities are regarded as having an implied rating equal to the rating of such securities. Holdings designated N/R are not rated by these national rating agencies. |

| 4 | Holdings are subject to change. |

| 5 | The Fund paid shareholders a net ordinary income distribution in December 2011 of $0.0231 per share. |

| Nuveen Investments | 21 |

| NMD | Nuveen Municipal | |

| Performance | High Income | |

| OVERVIEW | Opportunity Fund 2 | |

| as of October 31, 2012 |

| Fund Snapshot | ||||

| Common Share Price | $ | 13.11 | ||

| Common Share Net Asset Value (NAV) | $ | 13.05 | ||

| Premium/(Discount) to NAV | 0.46 | % | ||

| Market Yield | 6.00 | % | ||

Taxable-Equivalent Yield2 | 8.33 | % | ||

| Net Assets Applicable to Common Shares ($000) | $ | 242,636 | ||

| Leverage | ||||

| Regulatory Leverage | 12.61 | % | ||

| Effective Leverage | 33.41 | % |

| Average Annual Total Returns | |||||||

| (Inception 11/15/07) | |||||||

| On Share Price | On NAV | ||||||

| 1-Year | 27.09 | % | 24.56 | % | |||

| Since Inception | 5.29 | % | 6.29 | % | |||

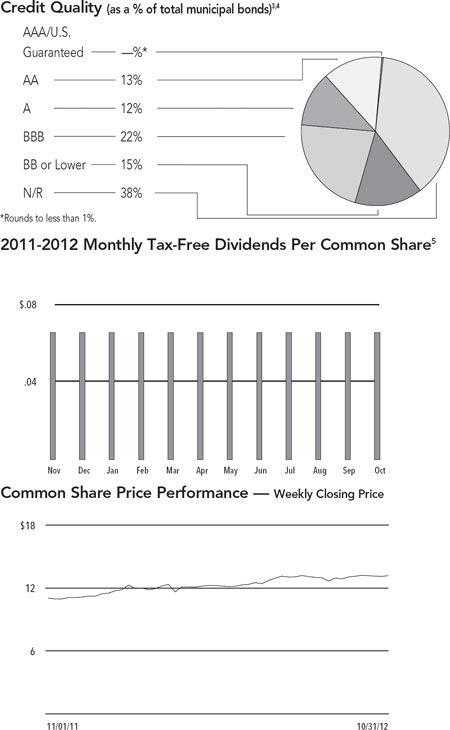

States4 | ||||

| (as a % of total municipal bonds) | ||||

| California | 16.3 | % | ||

| Illinois | 10.8 | % | ||

| Colorado | 9.2 | % | ||

| Florida | 8.1 | % | ||

| Texas | 6.3 | % | ||

| Arizona | 5.6 | % | ||

| Washington | 5.3 | % | ||

| Indiana | 3.2 | % | ||

| Louisiana | 2.9 | % | ||

| Utah | 2.8 | % | ||

| New Jersey | 2.8 | % | ||

| New York | 2.5 | % | ||

| Pennsylvania | 2.5 | % | ||

| Missouri | 2.2 | % | ||

| Nevada | 2.0 | % | ||

| Wisconsin | 2.0 | % | ||

| Connecticut | 1.7 | % | ||

| Other | 13.8 | % |

Portfolio Composition1,4 | ||||

| (as a % of total investments) | ||||

| Tax Obligation/Limited | 21.0 | % | ||

| Health Care | 19.5 | % | ||

| Education and Civic Organizations | 17.9 | % | ||

| Transportation | 7.9 | % | ||

| Utilities | 5.1 | % | ||

| Consumer Discretionary | 5.1 | % | ||

| Long-Term Care | 5.0 | % | ||

| Consumer Staples | 4.4 | % | ||

| Other | 14.1 | % |

| Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this Fund’s Performance Overview page. | |

| 1 | Excluding investments in derivatives. |

| 2 | Taxable-Equivalent Yield represents the yield that must be earned on a fully taxable investment in order to equal the yield of the Fund on an after-tax basis. It is based on a federal income tax rate of 28%. When comparing this Fund to investments that generate qualified dividend income, the Taxable-Equivalent Yield is lower. |

| 3 | Ratings shown are the highest rating given by one of the following national rating agencies: Standard & Poor’s, Moody’s Investors Service, Inc. or Fitch, Inc. Credit ratings are subject to change. AAA, AA, A, and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Certain bonds backed by U.S. Government or agency securities are regarded as having an implied rating equal to the rating of such securities. Holdings designated N/R are not rated by these national rating agencies. |

| 4 | Holdings are subject to change. |

| 5 | The Fund paid shareholders a net ordinary income distribution in December 2011 of $0.0035 per share. |

| 22 | Nuveen Investments |

| NQM | Shareholder Meeting Report | |

| NQS | ||

| NQU | The annual meeting of shareholders was held on July 31, 2012 in the Lobby Conference Room, 333 West Wacker Drive, Chicago, IL360606; at this meeting the shareholders were asked to vote on the election of Board Members. |

| NQM | NQS | NQU | |||||||||||||||||

| Common and | Common and | Common and | |||||||||||||||||

| Preferred | Preferred | Preferred | Preferred | Preferred | Preferred | ||||||||||||||

| shares voting | shares voting | shares voting | shares voting | shares voting | shares voting | ||||||||||||||

| together | together | together | together | together | together | ||||||||||||||

| as a class | as a class | as a class | as a class | as a class | as a class | ||||||||||||||

| Approval of the Board Members was reached as follows: | |||||||||||||||||||

| John P. Amboian | |||||||||||||||||||

| For | 32,175,102 | — | 31,102,870 | — | 46,695,420 | — | |||||||||||||

| Withhold | 686,791 | — | 758,582 | — | 1,500,493 | — | |||||||||||||

| Total | 32,861,893 | — | 31,861,452 | — | 48,195,913 | — | |||||||||||||

| Robert P. Bremner | |||||||||||||||||||

| For | 32,142,156 | — | 31,091,379 | — | 46,710,578 | — | |||||||||||||

| Withhold | 719,737 | — | 770,073 | — | 1,485,335 | — | |||||||||||||

| Total | 32,861,893 | — | 31,861,452 | — | 48,195,913 | — | |||||||||||||

| Jack B. Evans | |||||||||||||||||||

| For | 32,124,004 | — | 31,099,573 | — | 46,722,002 | — | |||||||||||||

| Withhold | 737,889 | — | 761,879 | — | 1,473,911 | — | |||||||||||||

| Total | 32,861,893 | — | 31,861,452 | — | 48,195,913 | — | |||||||||||||

| William C. Hunter | |||||||||||||||||||

| For | — | 1,568 | — | 1,725 | — | 2,500 | |||||||||||||

| Withhold | — | 150 | — | 299 | — | 384 | |||||||||||||

| Total | — | 1,718 | — | 2,024 | — | 2,884 | |||||||||||||

| David J. Kundert | |||||||||||||||||||

| For | 32,145,312 | — | 31,083,341 | — | 46,697,261 | — | |||||||||||||

| Withhold | 716,581 | — | 778,111 | — | 1,498,652 | — | |||||||||||||

| Total | 32,861,893 | — | 31,861,452 | — | 48,195,913 | — | |||||||||||||

| William J. Schneider | |||||||||||||||||||

| For | — | 1,568 | — | 1,725 | — | 2,500 | |||||||||||||

| Withhold | — | 150 | — | 299 | — | 384 | |||||||||||||

| Total | — | 1,718 | — | 2,024 | — | 2,884 | |||||||||||||

| Judith M. Stockdale | |||||||||||||||||||

| For | 32,130,096 | — | 31,057,469 | — | 46,620,935 | — | |||||||||||||

| Withhold | 731,797 | — | 803,983 | — | 1,574,978 | — | |||||||||||||

| Total | 32,861,893 | — | 31,861,452 | — | 48,195,913 | — | |||||||||||||

| Carole E. Stone | |||||||||||||||||||

| For | 32,159,466 | — | 31,060,119 | — | 46,628,162 | — | |||||||||||||

| Withhold | 702,427 | — | 801,333 | — | 1,567,751 | — | |||||||||||||

| Total | 32,861,893 | — | 31,861,452 | — | 48,195,913 | — | |||||||||||||

| Virginia L. Stringer | |||||||||||||||||||

| For | 32,162,753 | — | 31,059,951 | — | 46,628,982 | — | |||||||||||||

| Withhold | 699,140 | — | 801,501 | — | 1,566,931 | — | |||||||||||||

| Total | 32,861,893 | — | 31,861,452 | — | 48,195,913 | — | |||||||||||||

| Terence J. Toth | |||||||||||||||||||

| For | 32,186,833 | — | 31,093,851 | — | 46,688,565 | — | |||||||||||||

| Withhold | 675,060 | — | 767,601 | — | 1,507,348 | — | |||||||||||||

| Total | 32,861,893 | — | 31,861,452 | — | 48,195,913 | — | |||||||||||||

| Nuveen Investments | 23 |

| NPF | Shareholder Meeting Report (continued) | |

| NMZ | ||

| NMD |

| NPF | NMZ | NMD | |||||||||||

| Common and | Common and | Common and | |||||||||||

| Preferred | Preferred | Preferred | Preferred | ||||||||||

| shares voting | shares voting | shares voting | shares voting | ||||||||||

| together | together | together | together | ||||||||||

| as a class | as a class | as a class | as a class | ||||||||||

| Approval of the Board Members was reached as follows: | |||||||||||||

| John P. Amboian | |||||||||||||

| For | 17,984,464 | — | — | — | |||||||||

| Withhold | 451,439 | — | — | — | |||||||||

| Total | 18,435,903 | — | — | — | |||||||||

| Robert P. Bremner | |||||||||||||

| For | 17,917,046 | — | 25,663,131 | 16,294,149 | |||||||||

| Withhold | 518,857 | — | 971,211 | 351,464 | |||||||||

| Total | 18,435,903 | — | 26,634,342 | 16,645,613 | |||||||||

| Jack B. Evans | |||||||||||||

| For | 17,954,684 | — | 25,741,732 | 16,295,045 | |||||||||

| Withhold | 481,219 | — | 892,610 | 350,568 | |||||||||

| Total | 18,435,903 | — | 26,634,342 | 16,645,613 | |||||||||

| William C. Hunter | |||||||||||||

| For | — | 1,227 | — | — | |||||||||

| Withhold | — | 50 | — | — | |||||||||

| Total | — | 1,277 | — | — | |||||||||

| David J. Kundert | |||||||||||||

| For | 17,924,230 | — | — | — | |||||||||

| Withhold | 511,673 | — | — | — | |||||||||

| Total | 18,435,903 | — | — | — | |||||||||

| William J. Schneider | |||||||||||||

| For | — | 1,227 | 25,690,174 | 16,296,515 | |||||||||

| Withhold | — | 50 | 944,168 | 349,098 | |||||||||

| Total | — | 1,277 | 26,634,342 | 16,645,613 | |||||||||

| Judith M. Stockdale | |||||||||||||

| For | 17,898,852 | — | — | — | |||||||||

| Withhold | 537,051 | — | — | — | |||||||||

| Total | 18,435,903 | — | — | — | |||||||||

| Carole E. Stone | |||||||||||||

| For | 17,873,608 | — | — | — | |||||||||

| Withhold | 562,295 | — | — | — | |||||||||

| Total | 18,435,903 | — | — | — | |||||||||

| Virginia L. Stringer | |||||||||||||

| For | 17,898,922 | — | — | — | |||||||||

| Withhold | 536,981 | — | — | — | |||||||||

| Total | 18,435,903 | — | — | — | |||||||||

| Terence J. Toth | |||||||||||||

| For | 17,988,585 | — | — | — | |||||||||

| Withhold | 447,318 | — | — | — | |||||||||

| Total | 18,435,903 | — | — | — | |||||||||

| 24 | Nuveen Investments |

Report of Independent

Registered Public Accounting Firm

The Board of Directors/Trustees and Shareholders

Nuveen Investment Quality Municipal Fund, Inc.

Nuveen Select Quality Municipal Fund, Inc.

Nuveen Quality Income Municipal Fund, Inc.

Nuveen Premier Municipal Income Fund, Inc.

Nuveen Municipal High Income Opportunity Fund

Nuveen Municipal High Income Opportunity Fund 2

We have audited the accompanying statements of assets and liabilities, including the portfolios of investments, of Nuveen Investment Quality Municipal Fund, Inc., Nuveen Select Quality Municipal Fund, Inc., Nuveen Quality Income Municipal Fund, Inc., Nuveen Premier Municipal Income Fund, Inc., Nuveen Municipal High Income Opportunity Fund, and Nuveen Municipal High Income Opportunity Fund 2 (the “Funds”) as of October 31, 2012, and the related statements of operations and cash flows for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the periods indicated therein. These financial statements and financial highlights are the responsibility of the Funds’ management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. We were not engaged to perform an audit of the Funds’ internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Funds’ internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements and financial highlights, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of October 31, 2012, by correspondence with the custodian and brokers or by other appropriate auditing procedures where replies from brokers were not received. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial positions of Nuveen Investment Quality Municipal Fund, Inc., Nuveen Select Quality Municipal Fund, Inc., Nuveen Quality Income Municipal Fund, Inc., Nuveen Premier Municipal Income Fund, Inc., Nuveen Municipal High Income Opportunity Fund, and Nuveen Municipal High Income Opportunity Fund 2 at October 31, 2012, and the results of their operations and their cash flows for the year then ended, the changes in their net assets for each of the two years in the period then ended, and the financial highlights for each of the periods indicated therein, in conformity with U.S. generally accepted accounting principles.

Chicago, Illinois

December 27, 2012

| Nuveen Investments | 25 |

| Nuveen Investment Quality Municipal Fund, Inc. | ||

| NQM | Portfolio of Investments |

October 31, 2012

| Principal | Optional Call | |||||||

| Amount (000) | Description (1) | Provisions (2) | Ratings (3) | Value | ||||

| Alabama – 1.5% (1.0% of Total Investments) | ||||||||

| $ | 3,800 | Alabama Special Care Facilities Financing Authority, Revenue Bonds, Ascension Health, Series 2006C-2, 5.000%, 11/15/36 (UB) | 11/16 at 100.00 | AA+ | $ | 4,128,016 | ||

| Birmingham Special Care Facilities Financing Authority, Alabama, Revenue Bonds, Baptist Health System Inc., Series 2005A: | ||||||||

| 1,200 | 5.250%, 11/15/20 | 11/15 at 100.00 | Baa2 | 1,269,612 | ||||

| 800 | 5.000%, 11/15/30 | 11/15 at 100.00 | Baa2 | 811,912 | ||||

| 1,650 | Courtland Industrial Development Board, Alabama, Pollution Control Revenue Bonds, International Paper Company, Series 2005A, 5.000%, 6/01/25 | 6/15 at 100.00 | BBB | 1,690,013 | ||||

| 1,000 | Jefferson County, Alabama, Limited Obligation School Warrants, Education Tax Revenue Bonds, Series 2004A, 5.250%, 1/01/23 – AGM Insured | 1/14 at 100.00 | AA | 1,019,220 | ||||

| 8,450 | Total Alabama | 8,918,773 | ||||||

| Alaska – 0.7% (0.5% of Total Investments) | ||||||||

| Northern Tobacco Securitization Corporation, Alaska, Tobacco Settlement Asset-Backed Bonds, Series 2006A: | ||||||||

| 4,000 | 5.000%, 6/01/32 | 6/14 at 100.00 | B+ | 3,559,480 | ||||

| 500 | 5.000%, 6/01/46 | 6/14 at 100.00 | B+ | 426,185 | ||||

| 4,500 | Total Alaska | 3,985,665 | ||||||

| Arizona – 3.2% (2.2% of Total Investments) | ||||||||

| 650 | Apache County Industrial Development Authority, Arizona, Pollution Control Revenue Bonds, Tucson Electric Power Company, Series 20102A, 4.500%, 3/01/30 | 3/22 at 100.00 | BBB | 682,832 | ||||

| 2,500 | Arizona Sports and Tourism Authority, Senior Revenue Refunding Bonds, Multipurpose Stadium Facility Project, Series 2012A, 5.000%, 7/01/32 | 7/22 at 100.00 | A1 | 2,797,575 | ||||

| 1,000 | Arizona Tourism and Sports Authority, Tax Revenue Bonds, Multipurpose Stadium Facility Project, Series 2003A, 5.000%, 7/01/31 (Pre-refunded 7/01/13) – NPFG Insured | 7/13 at 100.00 | A1 (4) | 1,031,650 | ||||

| Glendale Industrial Development Authority, Arizona, Revenue Bonds, John C. Lincoln Health Network, Series 2005B: | ||||||||

| 200 | 5.250%, 12/01/24 | 12/15 at 100.00 | BBB+ | 211,206 | ||||

| 265 | 5.250%, 12/01/25 | 12/15 at 100.00 | BBB+ | 279,522 | ||||

| 2,500 | Mesa, Arizona, Utility System Revenue Bonds, Tender Option Bond Trust, Series 11032- 11034, 14.760%, 7/01/26 – AGM Insured (IF) | 7/17 at 100.00 | Aa2 | 2,940,400 | ||||

| 5,000 | Phoenix, Arizona, Civic Improvement Corporation, Senior Lien Airport Revenue Bonds, Series 2008, Trust 1132, 9.021%, 1/01/32 (IF) | 7/18 at 100.00 | AA– | 6,021,000 | ||||

| 3,450 | Salt Verde Financial Corporation, Arizona, Senior Gas Revenue Bonds, Citigroup Energy Inc Prepay Contract Obligations, Series 2007, 5.000%, 12/01/37 | No Opt. Call | A– | 3,998,343 | ||||

| 958 | Watson Road Community Facilities District, Arizona, Special Assessment Revenue Bonds, Series 2005, 6.000%, 7/01/30 | 7/16 at 100.00 | N/R | 919,651 | ||||

| 16,523 | Total Arizona | 18,882,179 | ||||||

| Arkansas – 0.6% (0.4% of Total Investments) | ||||||||

| 3,290 | University of Arkansas, Pine Bluff Campus, Revenue Bonds, Series 2005A, 5.000%, 12/01/30 – AMBAC Insured | 12/15 at 100.00 | Aa2 | 3,612,157 | ||||

| California – 25.2% (17.2% of Total Investments) | ||||||||

| 1,500 | ABAG Finance Authority for Non-Profit Corporations, California, Cal-Mortgage Insured Revenue Bonds, Channing House, Series 2010, 6.000%, 5/15/30 | 5/20 at 100.00 | A– | 1,716,120 | ||||

| 2,250 | California Educational Facilities Authority, Revenue Bonds, University of Southern California, Series 2005, 4.750%, 10/01/28 (UB) | 10/15 at 100.00 | Aa1 | 2,471,783 | ||||

| 1,000 | California Educational Facilities Authority, Revenue Bonds, University of the Pacific, Series 2006, 5.000%, 11/01/30 | 11/15 at 100.00 | A2 | 1,052,420 |

| 26 | Nuveen Investments |

| Principal | Optional Call | |||||||

| Amount (000) | Description (1) | Provisions (2) | Ratings (3) | Value | ||||

California (continued) | ||||||||

| $ | 2,500 | California Health Facilities Financing Authority, Revenue Bonds, Cedars-Sinai Medical Center, Series 2005, 5.000%, 11/15/27 | 11/15 at 100.00 | AAA | $ | 2,714,500 | ||

| 4,285 | California Health Facilities Financing Authority, Revenue Bonds, Kaiser Permanante System, Series 2006, 5.000%, 4/01/37 | 4/16 at 100.00 | A+ | 4,523,417 | ||||

| 5,500 | California Health Facilities Financing Authority, Revenue Bonds, Sutter Health, Series 2007A, 5.000%, 11/15/42 (UB) | 11/16 at 100.00 | AA– | 5,889,675 | ||||

| 810 | California State Public Works Board, Lease Revenue Bonds, Various Capital Projects, Series 2009-I, 6.375%, 11/01/34 | 11/19 at 100.00 | A2 | 981,736 | ||||

| 1,500 | California State Public Works Board, Lease Revenue Bonds, Various Capital Projects, Series 2010A-1, 5.750%, 3/01/30 | 3/20 at 100.00 | A2 | 1,732,815 | ||||

| California State, General Obligation Bonds, Various Purpose Series 2010: | ||||||||

| 2,100 | 5.250%, 3/01/30 | 3/20 at 100.00 | A1 | 2,444,169 | ||||

| 3,000 | 5.500%, 3/01/40 | 3/20 at 100.00 | A1 | 3,467,850 | ||||

| California Statewide Communities Development Authority, Revenue Bonds, American Baptist Homes of the West, Series 2010: | ||||||||

| 900 | 6.000%, 10/01/29 | 10/19 at 100.00 | BBB+ | 999,639 | ||||

| 1,030 | 6.250%, 10/01/39 | 10/19 at 100.00 | BBB+ | 1,127,428 | ||||

| 1,055 | California Statewide Communities Development Authority, School Facility Revenue Bonds, Aspire Public Schools, Series 2010, 6.000%, 7/01/40 | 1/19 at 100.00 | BB+ | 1,087,737 | ||||

| California Statewide Community Development Authority, Revenue Bonds, Daughters of Charity Health System, Series 2005A: | ||||||||

| 1,000 | 5.250%, 7/01/30 | 7/15 at 100.00 | BBB | 1,041,420 | ||||

| 2,000 | 5.000%, 7/01/39 | 7/15 at 100.00 | BBB | 2,051,280 | ||||

| 1,390 | California Statewide Community Development Authority, Revenue Bonds, Sutter Health, Tender Option Bond Trust 3175, 13.471%, 5/15/14 (IF) | No Opt. Call | AA– | 1,956,939 | ||||

| 1,900 | Chula Vista, California, Industrial Development Revenue Bonds, San Diego Gas and Electric Company, Series 1996A, 5.300%, 7/01/21 | 6/14 at 102.00 | A+ | 2,013,335 | ||||

| 2,530 | Commerce Joint Power Financing Authority, California, Tax Allocation Bonds, Redevelopment Projects 2 and 3, Refunding Series 2003A, 5.000%, 8/01/28 – RAAI Insured | 8/13 at 100.00 | BBB | 2,540,727 | ||||

| 145 | Commerce Joint Power Financing Authority, California, Tax Allocation Bonds, Redevelopment Projects 2 and 3, Refunding Series 2003A, 5.000%, 8/01/28 (Pre-refunded 8/01/13) – RAAI Insured | 8/13 at 100.00 | N/R (4) | 150,192 | ||||

| 1,000 | Davis Redevelopment Agency, California, Tax Allocation Bonds, Davis Redevelopment Project, Subordinate Series 2011A, 7.000%, 12/01/36 | 12/21 at 100.00 | A+ | 1,223,570 | ||||

| 1,500 | Gavilan Joint Community College District, Santa Clara and San Benito Counties, California, General Obligation Bonds, Election of 2004 Series 2011D, 5.750%, 8/01/35 | 8/21 at 100.00 | Aa2 | 1,830,150 | ||||

| 2,000 | Glendale Redevelopment Agency, California, Central Glendale Redevelopment Project, Tax, Allocation Bonds Series 2010, 5.500%, 12/01/24 | 12/16 at 100.00 | A | 2,109,140 | ||||

| Golden State Tobacco Securitization Corporation, California, Tobacco Settlement Asset-Backed Bonds, Series 2007A-1: | ||||||||

| 3,000 | 5.000%, 6/01/33 | 6/17 at 100.00 | BB– | 2,571,990 | ||||

| 1,000 | 5.750%, 6/01/47 | 6/17 at 100.00 | BB– | 895,930 | ||||

| 610 | 5.125%, 6/01/47 | 6/17 at 100.00 | BB– | 494,344 | ||||

| 9,740 | Huntington Park Redevelopment Agency, California, Single Family Residential Mortgage Revenue Refunding Bonds, Series 1986A, 8.000%, 12/01/19 (ETM) | No Opt. Call | Aaa | 14,344,195 | ||||

| 400 | Jurupa Public Financing Authority, California, Superior Lien Revenue Bonds, Series 2010A, 5.000%, 9/01/33 | 9/20 at 100.00 | AA– | 435,488 | ||||

| 500 | Madera County, California, Certificates of Participation, Children’s Hospital Central California, Series 2010, 5.375%, 3/15/36 | 3/20 at 100.00 | A+ | 540,345 | ||||

| 6,215 | Marinez Unified School District, Contra Costa County, California, General Obligation Bonds, Series 2011, 0.000%, 8/01/31 | 8/24 at 100.00 | AA– | 6,931,154 |

| Nuveen Investments | 27 |

| Nuveen Investment Quality Municipal Fund, Inc. (continued) | ||

NQM | Portfolio of Investments |

October 31, 2012

| Principal | Optional Call | |||||||

| Amount (000) | Description (1) | Provisions (2) | Ratings (3) | Value | ||||

California (continued) | ||||||||

| $ | 2,700 | M-S-R Energy Authority, California, Gas Revenue Bonds, Series 2009A, 7.000%, 11/01/34 | No Opt. Call | A | $ | 3,933,144 | ||

| 1,030 | Natomas Union School District, Sacramento County, California, General Obligation Refunding Bonds, Series 1999, 5.950%, 9/01/21 – NPFG Insured | No Opt. Call | BBB+ | 1,183,697 | ||||

| 15,770 | Ontario Redevelopment Financing Authority, San Bernardino County, California, Revenue Refunding Bonds, Redevelopment Project 1, Series 1995, 7.400%, 8/01/25 – NPFG Insured | No Opt. Call | BBB | 19,528,306 | ||||

| 1,265 | Palomar Pomerado Health Care District, California, Certificates of Participation, Series 2009, 6.750%, 11/01/39 | 11/19 at 100.00 | Baa3 | 1,431,461 | ||||

| 1,875 | Palomar Pomerado Health Care District, California, Certificates of Participation, Series 2010, 5.250%, 11/01/21 | 11/20 at 100.00 | Baa3 | 2,060,100 | ||||

| 13,145 | Perris, California, GNMA Mortgage-Backed Securities Program Single Family Mortgage Revenue Bonds, Series 1988B, 8.200%, 9/01/23 (Alternative Minimum Tax) (ETM) | No Opt. Call | Aaa | 20,118,028 | ||||

| 2,500 | Petaluma, Sonoma County, California, Wastewater Revenue Bonds, Refunding Series 2011, 5.500%, 5/01/32 | 5/21 at 100.00 | AA– | 2,911,825 | ||||

| 3,415 | Rancho Mirage Joint Powers Financing Authority, California, Revenue Bonds, Eisenhower Medical Center, Series 2004, 5.875%, 7/01/26 (Pre-refunded 7/01/14) | 7/14 at 100.00 | Baa2 (4) | 3,730,375 | ||||

| San Diego County, California, Certificates of Participation, Burnham Institute, Series 2006: | ||||||||

| 250 | 5.000%, 9/01/21 | 9/15 at 102.00 | Baa2 | 263,648 | ||||

| 275 | 5.000%, 9/01/23 | 9/15 at 102.00 | Baa2 | 286,963 | ||||