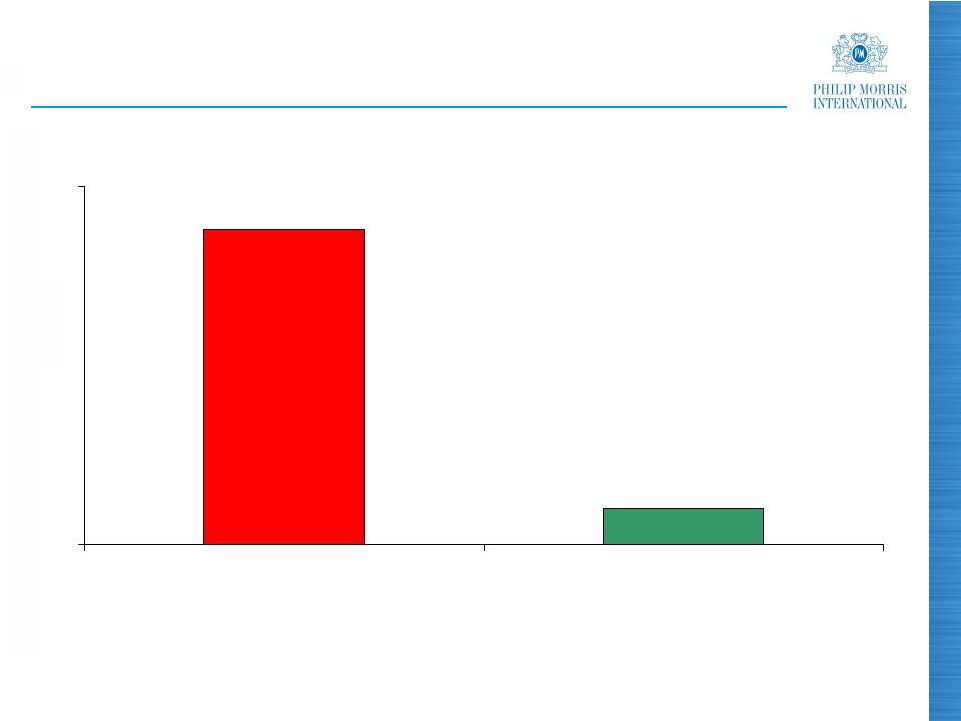

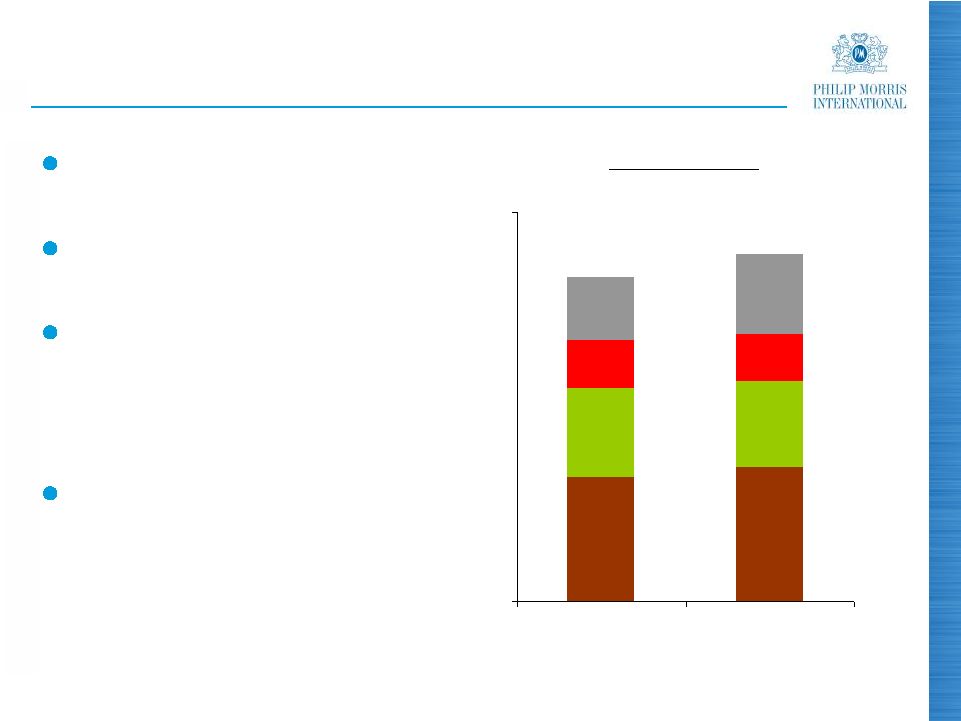

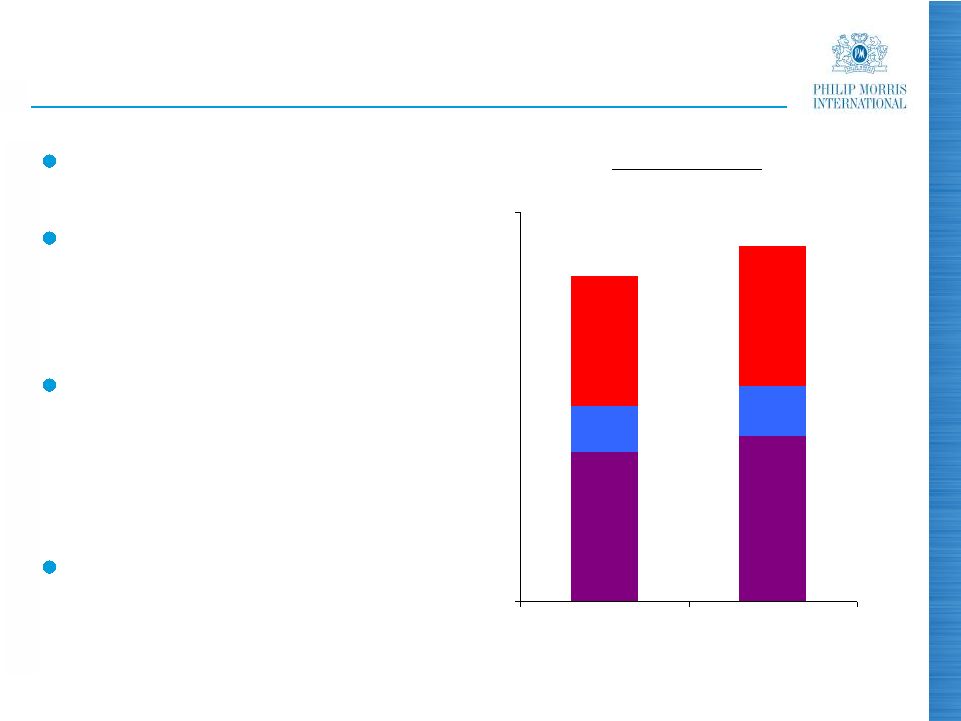

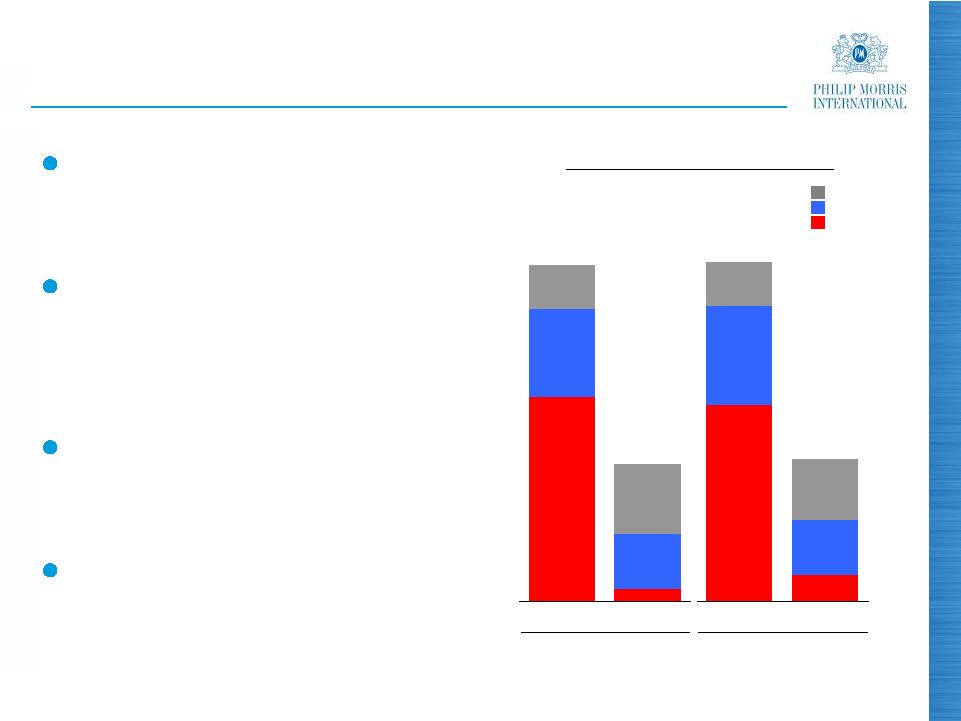

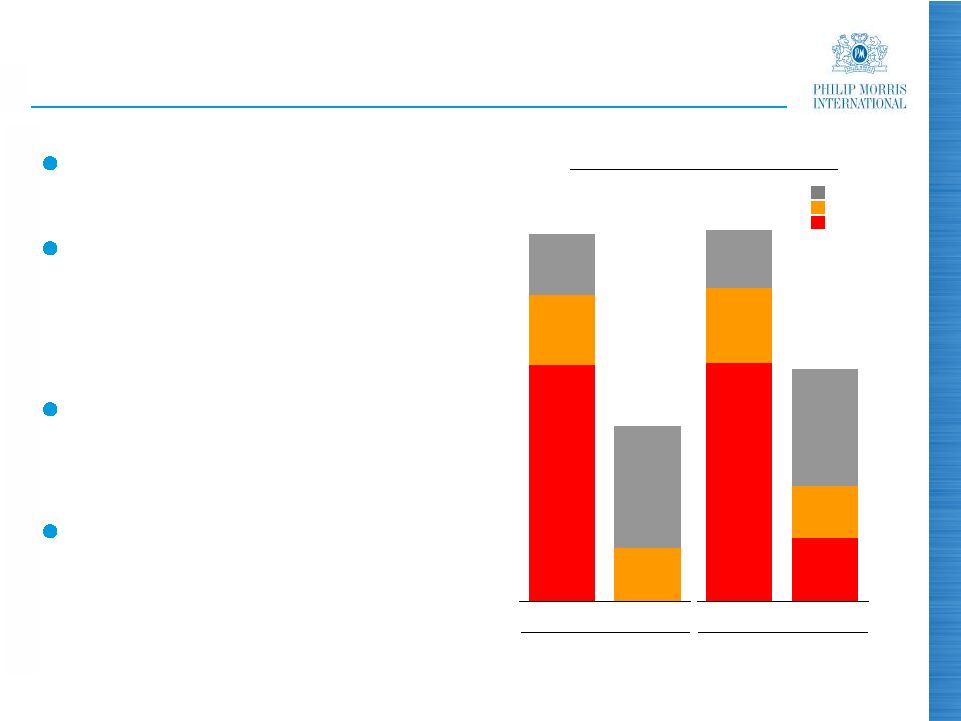

28 PHILIP MORRIS INTERNATIONAL INC. and Subsidiaries Reconciliation of Non-GAAP Measures Adjustments for the Impact of Currency and Acquisitions For the Quarters Ended September 30, ($ in millions) (Unaudited) Reported Net Revenues Less Excise Taxes Reported Net Revenues excluding Excise Taxes Less Currency Reported Net Revenues excluding Excise Taxes & Currency Less Acquisi- tions Reported Net Revenues excluding Excise Taxes, Currency & Acquisitions Reported Net Revenues Less Excise Taxes Reported Net Revenues excluding Excise Taxes Reported Reported excluding Currency Reported excluding Currency & Acquisitions 8,155 $ 5,649 $ 2,506 $ 321 $ 2,185 $ - $ 2,185 $ European Union 7,045 $ 4,906 $ 2,139 $ 17.2% 2.2% 2.2% 4,921 2,711 2,210 89 2,121 13 2,108 EEMA 4,184 2,288 1,896 16.6% 11.9% 11.2% 5,143 2,344 2,799 248 2,551 2 2,549 Asia 3,629 1,796 1,833 52.7% 39.2% 39.1% 2,487 1,640 847 39 808 - 808 Latin America & Canada 2,078 1,332 746 13.5% 8.3% 8.3% 20,706 $ 12,344 $ 8,362 $ 697 $ 7,665 $ 15 $ 7,650 $ PMI Total 16,936 $ 10,322 $ 6,614 $ 26.4% 15.9% 15.7% Reported Operating Companies Income Less Currency Reported Operating Companies Income excluding Currency Less Acquisi- tions Reported Operating Companies Income excluding Currency & Acquisitions Reported Operating Companies Income Reported Reported excluding Currency Reported excluding Currency & Acquisitions 1,262 $ 105 $ 1,157 $ - $ 1,157 $ European Union 1,113 $ 13.4% 4.0% 4.0% 925 (32) 957 (13) 970 EEMA 856 8.1% 11.8% 13.3% 1,309 104 1,205 2 1,203 Asia 690 89.7% 74.6% 74.3% 255 - 255 - 255 Latin America & Canada 244 4.5% 4.5% 4.5% 3,751 $ 177 $ 3,574 $ (11) $ 3,585 $ PMI Total 2,903 $ 29.2% 23.1% 23.5% 2011 2010 % Change in Reported Operating Companies Income 2011 2010 % Change in Reported Net Revenues excluding Excise Taxes |