UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| |

| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2018

Or

| |

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 001-34046

WESTERN GAS PARTNERS, LP

(Exact name of registrant as specified in its charter)

|

| | |

| Delaware | | 26-1075808 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

1201 Lake Robbins Drive The Woodlands, Texas | | 77380 |

| (Address of principal executive offices) | | (Zip Code) |

(832) 636-6000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

| | |

Title of Each Class Common Units Representing Limited Partner Interests | | Name of Each Exchange on Which Registered New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

| | | | | | | | |

Large accelerated filer þ | | Accelerated filer ¨ | | Non-accelerated filer ¨ | | Smaller reporting company ¨ | | Emerging growth company ¨ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

The aggregate market value of the registrant’s common units representing limited partner interests held by non-affiliates of the registrant was $4.9 billion on June 29, 2018, based on the closing price as reported on the New York Stock Exchange.

At February 18, 2019, there were 152,609,285 common units outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None

TABLE OF CONTENTS

|

| | |

| Item | | Page |

| | | |

| | | |

| 1 and 2. | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| 1A. | | |

| 1B. | | |

| 3. | | |

| 4. | | |

| | | |

| | | |

| | | |

| 5. | | |

| | | |

| | | |

| | | |

| 6. | | |

| 7. | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| 7A. | | |

| 8. | | |

| 9. | | |

| 9A. | | |

| 9B. | | |

|

| | |

| Item | | Page |

| | | |

| | | |

| 10. | | |

| 11. | | |

| 12. | | |

| 13. | | |

| 14. | | |

| | | |

| | | |

| | | |

| 15. | | |

| 16. | | |

COMMONLY USED TERMS AND DEFINITIONS

Unless the context otherwise requires, references to “we,” “us,” “our,” the “Partnership” or “Western Gas Partners, LP” refer to Western Gas Partners, LP and its subsidiaries. As used in this Form 10-K, the terms and definitions below have the following meanings:

Additional DBJV System Interest: Our additional 50% interest in the DBJV system acquired from a third party in March 2017.

AESC: Anadarko Energy Services Company.

Affiliates: Subsidiaries of Anadarko, excluding us, but including equity interests in Fort Union, White Cliffs, Rendezvous, the Mont Belvieu JV, TEP, TEG, FRP, Whitethorn and Cactus II.

AMH: APC Midstream Holdings, LLC.

AMM: Anadarko Marcellus Midstream, L.L.C.

Anadarko: Anadarko Petroleum Corporation and its subsidiaries, excluding us and our general partner.

Barrel or Bbl: 42 U.S. gallons measured at 60 degrees Fahrenheit.

Bbls/d: Barrels per day.

Board of Directors or Board: The board of directors of our general partner.

Btu: British thermal unit; the approximate amount of heat required to raise the temperature of one pound of water by one degree Fahrenheit.

Cactus II: Cactus II Pipeline LLC.

Chipeta: Chipeta Processing, LLC.

Chipeta LLC agreement: Chipeta’s limited liability company agreement, as amended and restated as of July 23, 2009.

Condensate: A natural gas liquid with a low vapor pressure mainly composed of propane, butane, pentane and heavier hydrocarbon fractions.

Cryogenic: The process in which liquefied gases are used to bring natural gas volumes to very low temperatures (below approximately -238 degrees Fahrenheit) to separate natural gas liquids from natural gas. Through cryogenic processing, more natural gas liquids are extracted than when traditional refrigeration methods are used.

DBJV: Delaware Basin JV Gathering LLC.

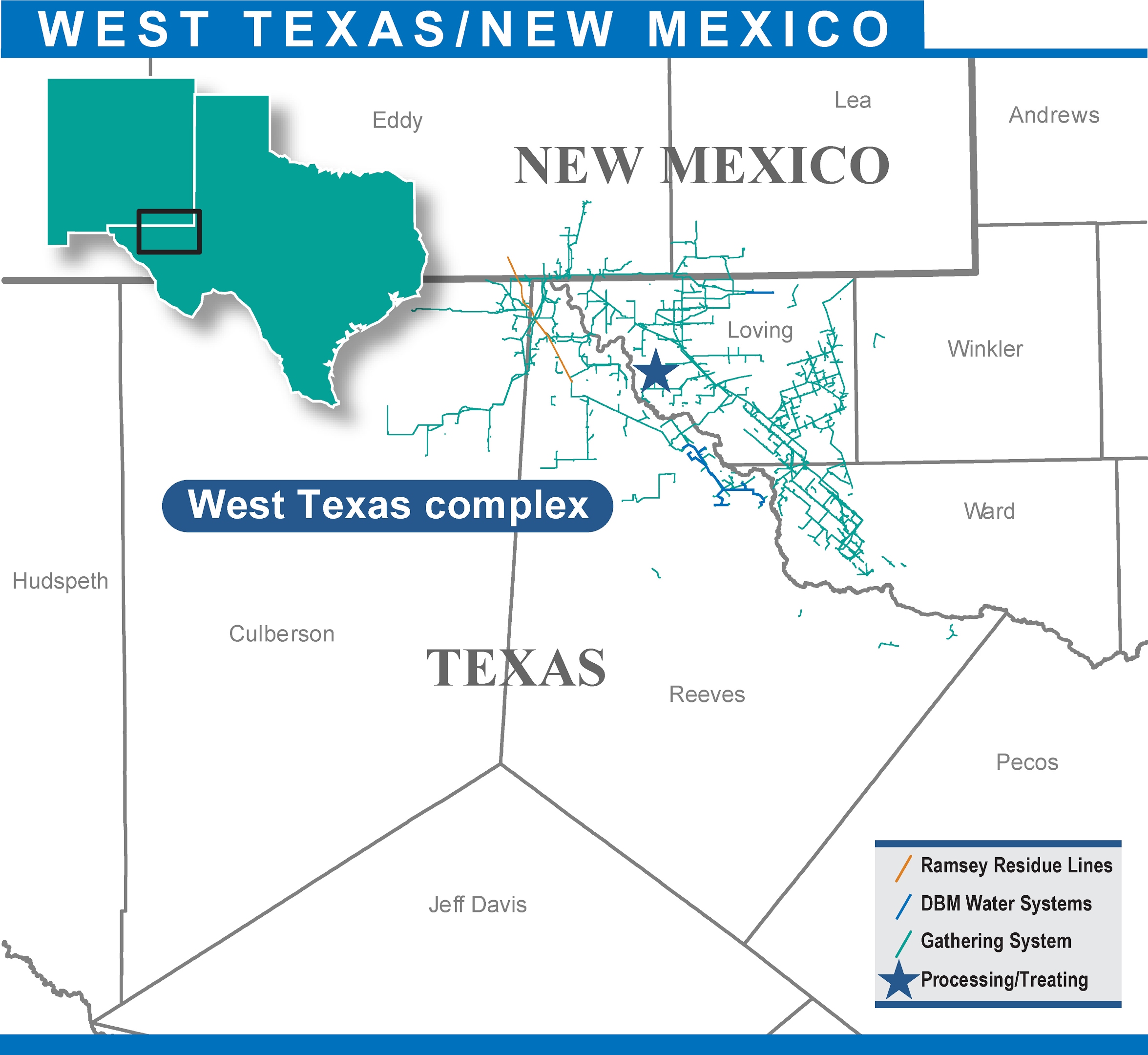

DBJV system: A gathering system and related facilities located in the Delaware Basin in Loving, Ward, Winkler and Reeves Counties in West Texas, part of the West Texas complex effective January 1, 2018.

DBM: Delaware Basin Midstream, LLC.

DBM complex: The cryogenic processing plants, gas gathering system, and related facilities and equipment in West Texas that serve production from Reeves, Loving and Culberson Counties, Texas and Eddy and Lea Counties, New Mexico, part of the West Texas complex effective January 1, 2018.

DBM water systems: Two produced water gathering and disposal systems in West Texas.

Delivery point: The point where hydrocarbons are delivered by a processor or transporter to a producer, shipper or purchaser, typically the inlet at the interconnection between the gathering or processing system and the facilities of a third-party processor or transporter.

DJ Basin complex: The Platte Valley system, Wattenberg system and Lancaster plant, all of which were combined into a single complex in the first quarter of 2014.

Drip condensate: Heavier hydrocarbon liquids that fall out of the natural gas stream and are recovered in the gathering system without processing.

Dry gas: A gas primarily composed of methane and ethane where heavy hydrocarbons and water either do not exist or have been removed through processing.

EBITDA: Earnings before interest, taxes, depreciation, and amortization. For a definition of “Adjusted EBITDA,” see How We Evaluate Our Operations under Part II, Item 7 of this Form 10-K.

End-use markets: The ultimate users/consumers of transported energy products.

Equity investment throughput: Our 14.81% share of average Fort Union throughput, 22% share of average Rendezvous throughput, 10% share of average White Cliffs throughput, 25% share of average Mont Belvieu JV throughput, 20% share of average TEP and TEG throughput, 33.33% share of average FRP throughput and 20% share of average Whitethorn throughput.

Exchange Act: The Securities Exchange Act of 1934, as amended.

FERC: The Federal Energy Regulatory Commission.

Fort Union: Fort Union Gas Gathering, LLC.

Fractionation: The process of applying various levels of higher pressure and lower temperature to separate a stream of natural gas liquids into ethane, propane, normal butane, isobutane and natural gasoline for end-use sale.

FRP: Front Range Pipeline LLC.

GAAP: Generally accepted accounting principles in the United States.

General partner: Western Gas Holdings, LLC.

Gpm: Gallons per minute, when used in the context of amine treating capacity.

Hydraulic fracturing: The injection of fluids into the wellbore to create fractures in rock formations, stimulating the production of oil or gas.

IDRs: Incentive distribution rights.

Imbalance: Imbalances result from (i) differences between gas and NGLs volumes nominated by customers and gas and NGLs volumes received from those customers and (ii) differences between gas and NGLs volumes received from customers and gas and NGLs volumes delivered to those customers.

IPO: Initial public offering.

Joule-Thompson (JT): A type of processing plant that uses the Joule-Thompson effect to cool natural gas by expanding the gas from a higher pressure to a lower pressure, which reduces the temperature.

LIBOR: London Interbank Offered Rate.

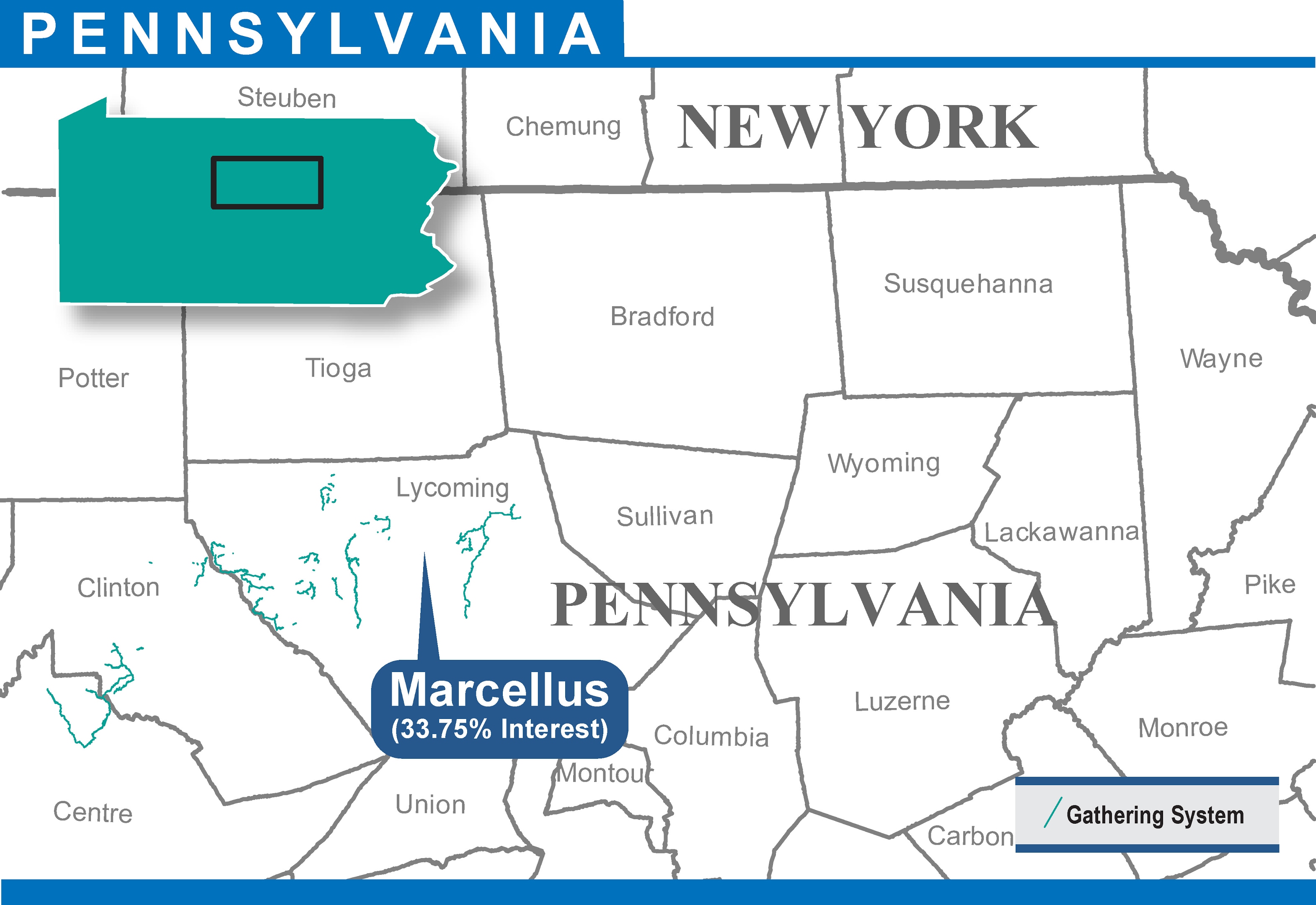

Marcellus Interest: Our 33.75% interest in the Larry’s Creek, Seely and Warrensville gas gathering systems and related facilities located in northern Pennsylvania.

MBbls/d: Thousand barrels per day.

Merger: The merger of Clarity Merger Sub, LLC, a wholly owned subsidiary of WGP, with and into the Partnership, with the Partnership continuing as the surviving entity and a subsidiary of WGP, which is expected to close in the first quarter of 2019.

Merger Agreement: The Contribution Agreement and Agreement and Plan of Merger, dated November 7, 2018, by and among WGP, the Partnership, Anadarko and certain of their affiliates, pursuant to which the parties thereto agreed to effect the Merger and certain other transactions.

MGR: Mountain Gas Resources, LLC.

MGR assets: The Red Desert complex and the Granger straddle plant.

MIGC: MIGC, LLC.

MLP: Master limited partnership.

MMBtu: Million British thermal units.

MMcf: Million cubic feet.

MMcf/d: Million cubic feet per day.

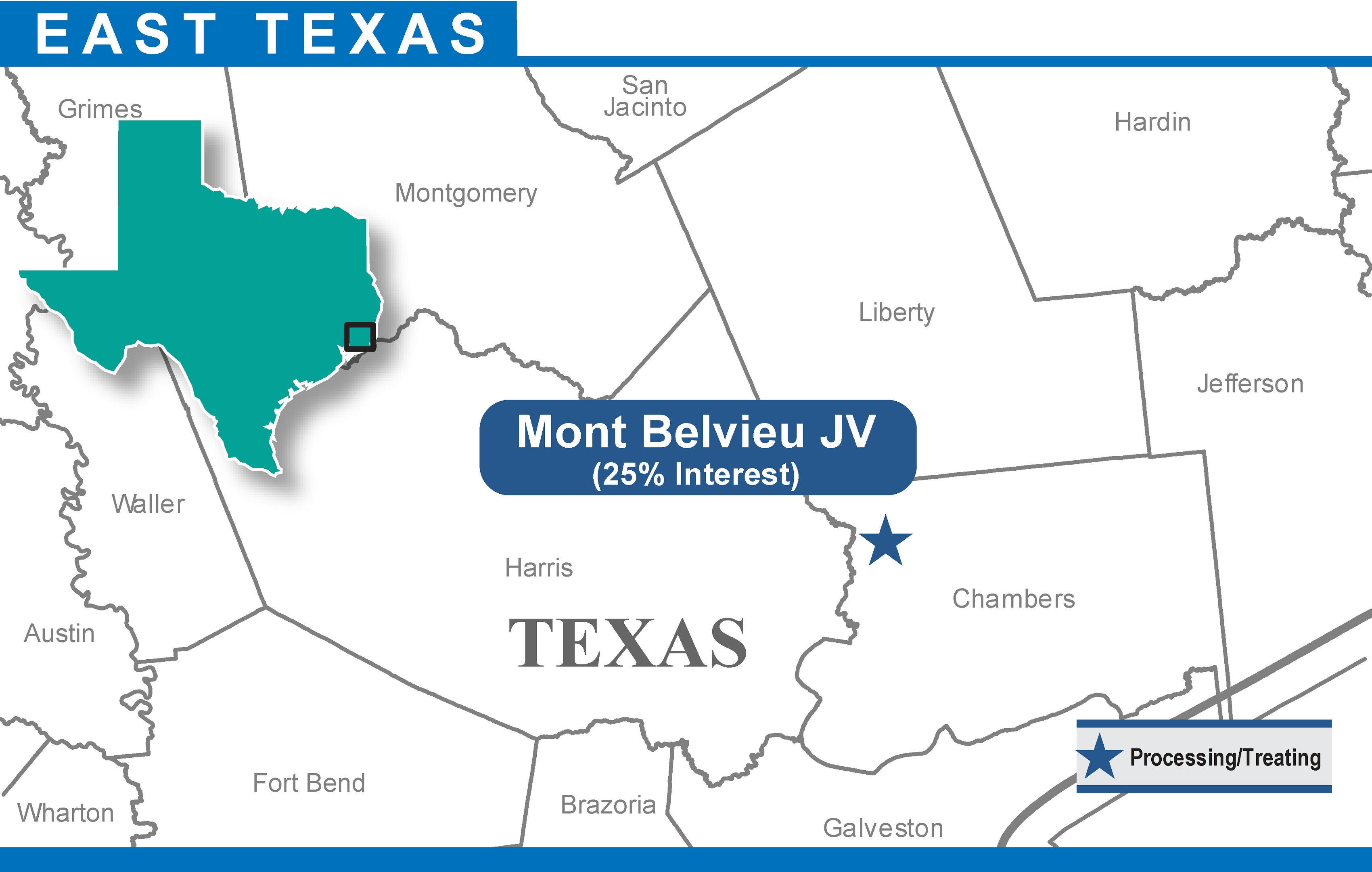

Mont Belvieu JV: Enterprise EF78 LLC.

Natural gas liquid(s) or NGL(s): The combination of ethane, propane, normal butane, isobutane and natural gasolines that, when removed from natural gas, become liquid under various levels of higher pressure and lower temperature.

Non-Operated Marcellus Interest: The 33.75% interest in the Liberty and Rome gas gathering systems and related facilities located in northern Pennsylvania that was transferred to a third party in March 2017 pursuant to the Property Exchange.

NYSE: New York Stock Exchange.

NYMEX: New York Mercantile Exchange.

OTTCO: Overland Trail Transmission, LLC.

PIK Class C units: Additional Class C units issued as quarterly distributions to the holder of our Class C units.

Play: A group of gas or oil fields that contain known or potential commercial amounts of petroleum and/or natural gas.

Produced water: Byproduct associated with the production of crude oil and natural gas that often contains a number of dissolved solids and other materials found in oil and gas reservoirs.

Property Exchange: Our acquisition of the Additional DBJV System Interest from a third party in exchange for the Non-Operated Marcellus Interest and $155.0 million of cash consideration, as further described in our Forms 8-K filed with the SEC on February 9, 2017, and March 23, 2017.

RCF: Our senior unsecured revolving credit facility.

Receipt point: The point where hydrocarbons are received by or into a gathering system, processing facility or transportation pipeline.

Red Desert complex: The Patrick Draw processing plant, the Red Desert processing plant, associated gathering lines, and related facilities.

Refrigeration: A method of processing natural gas by reducing the gas temperature with the use of an external refrigeration system.

Rendezvous: Rendezvous Gas Services, LLC.

Residue: The natural gas remaining after the unprocessed natural gas stream has been processed or treated.

SEC: U.S. Securities and Exchange Commission.

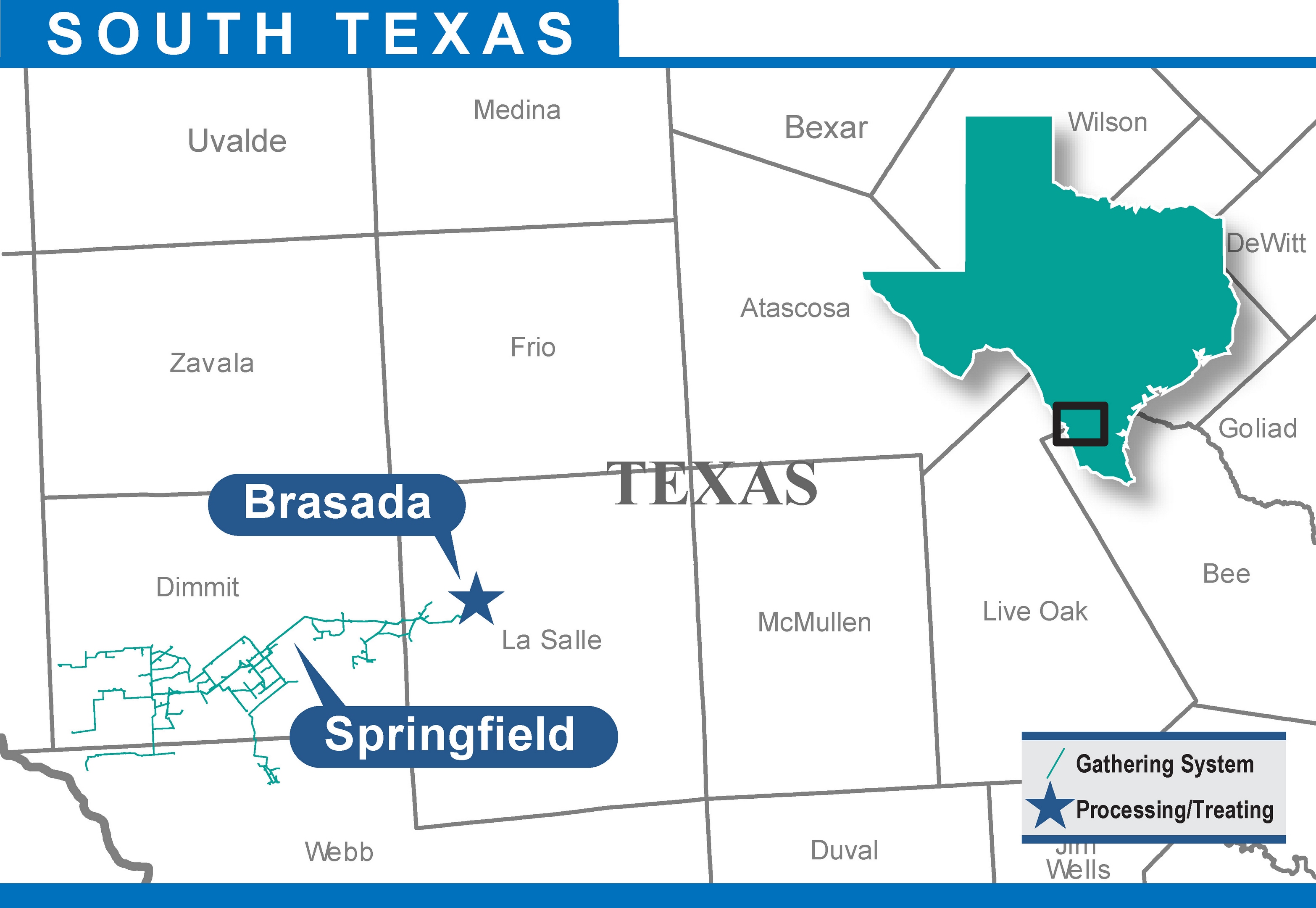

Springfield: Springfield Pipeline LLC.

Springfield gas gathering system: A gas gathering system and related facilities located in Dimmit, La Salle, Maverick and Webb Counties in South Texas.

Springfield oil gathering system: An oil gathering system and related facilities located in Dimmit, La Salle, Maverick and Webb Counties in South Texas.

Springfield system: The Springfield gas gathering system and Springfield oil gathering system.

Stabilization: The process of separating very light hydrocarbon gases, methane and ethane in particular, from heavier hydrocarbon components. This process reduces the volatility of the liquids during transportation and storage.

Tailgate: The point at which processed natural gas and/or natural gas liquids leave a processing facility for end-use markets.

TEFR Interests: The interests in TEP, TEG and FRP.

TEG: Texas Express Gathering LLC.

TEP: Texas Express Pipeline LLC.

Wellhead: The point at which the hydrocarbons and water exit the ground.

WES LTIP: With respect to awards granted prior to October 17, 2017, the Western Gas Partners, LP 2008 Long-Term Incentive Plan (the “WES 2008 LTIP”), which was adopted by our general partner in connection with our IPO in 2008, and, with respect to awards granted after October 17, 2017, the Western Gas Partners, LP 2017 Long-Term Incentive Plan, which was approved by our common and Class C unitholders on October 17, 2017.

West Texas complex: The DBM complex and DBJV and Haley systems, all of which were combined into a single complex effective January 1, 2018.

WGP: Western Gas Equity Partners, LP.

WGP GP: Western Gas Equity Holdings, LLC, the general partner of WGP.

WGP LTIP: Western Gas Equity Partners, LP 2012 Long-Term Incentive Plan.

WGRI: Western Gas Resources, Inc.

White Cliffs: White Cliffs Pipeline, LLC.

Whitethorn LLC: Whitethorn Pipeline Company LLC.

364-day Facility: Our 364-day senior unsecured credit agreement.

$500.0 million COP: The continuous offering program that may be undertaken pursuant to the registration statement filed with the SEC in July 2017 for the issuance of up to an aggregate of $500.0 million of our common units.

PART I

Items 1 and 2. Business and Properties

GENERAL OVERVIEW

We are a growth-oriented Delaware MLP formed by Anadarko in 2007 to acquire, own, develop and operate midstream assets. We are engaged in the business of gathering, compressing, treating, processing and transporting natural gas; gathering, stabilizing and transporting condensate, NGLs and crude oil; and gathering and disposing of produced water. In addition, in our capacity as a processor of natural gas, we also buy and sell natural gas, NGLs and condensate on behalf of ourselves and as agent for our customers under certain of our contracts. We provide these midstream services for Anadarko, as well as for third-party customers. Our common units are publicly traded on the NYSE under the symbol “WES.”

WGP, a Delaware MLP formed by Anadarko in September 2012, owns our general partner and a significant limited partner interest in us. WGP’s common units are publicly traded on the NYSE under the symbol “WGP.” WGP GP is a wholly owned subsidiary of Anadarko.

Merger transactions. On November 7, 2018, WGP, the Partnership, Anadarko and certain of their affiliates entered into a Contribution Agreement and Agreement and Plan of Merger (as may be amended from time to time, the “Merger Agreement”), pursuant to which, among other things, Clarity Merger Sub, LLC, a wholly owned subsidiary of WGP, will merge with and into the Partnership, with the Partnership continuing as the surviving entity and a subsidiary of WGP (the “Merger”). Upon closing of the Merger, which is expected to occur in the first quarter of 2019, the common units of the Partnership will no longer be publicly traded and will cease to trade on the NYSE under the symbol “WES.” The common units of WGP will begin trading on the NYSE under the symbol “WES” and WGP will change its name to Western Midstream Partners, LP.

The Merger Agreement also provides that WGP, the Partnership and Anadarko will, and will cause their respective affiliates to, cause the following transactions, among others, to occur immediately prior to the Merger becoming effective in the order as follows: (1) Anadarko E&P Onshore LLC and WGR Asset Holding Company LLC (“WGRAH”) (the “Contributing Parties”) will contribute to the Partnership all of their interests in each of Anadarko Wattenberg Oil Complex LLC, Anadarko DJ Oil Pipeline LLC, Anadarko DJ Gas Processing LLC, Wamsutter Pipeline LLC, DBM Oil Services, LLC, Anadarko Pecos Midstream LLC, Anadarko Mi Vida LLC and APC Water Holdings 1, LLC (“APCWH”) to WGR Operating, LP, Kerr-McGee Gathering LLC and Delaware Basin Midstream, LLC (each wholly owned by the Partnership) in exchange for aggregate consideration of $1.814 billion in cash from the Partnership, minus the outstanding amount payable pursuant to an intercompany note (“APCWH Note Payable”) to be assumed by the Partnership in connection with the transaction, and 45,760,201 of our common units; (2) AMH will sell to the Partnership its interests in Saddlehorn Pipeline Company, LLC and Panola Pipeline Company, LLC in exchange for aggregate consideration of $193.9 million in cash; (3) the Partnership will contribute cash in an amount equal to the outstanding balance of the APCWH Note Payable immediately prior to the effective time to APCWH, and APCWH will pay such cash to Anadarko in satisfaction of the APCWH Note Payable; (4) Class C units will convert into our common units on a one-for-one basis; and (5) the Partnership and its general partner will cause the conversion of the IDRs and the 2,583,068 general partner units held by the general partner into a non-economic general partner interest in us and 105,624,704 of our common units. The 45,760,201 of our common units to be issued to the Contributing Parties, less 6,375,284 common units to be retained by WGRAH, will be converted into the right to receive an aggregate of 55,360,984 WGP common units upon the consummation of the Merger. See Note 13—Debt and Interest Expense in the Notes to Consolidated Financial Statements under Part II, Item 8 of this Form 10-K for additional information.

Available information. We electronically file our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and other documents with the SEC under the Exchange Act. From time to time, we may also file registration and related statements pertaining to equity or debt offerings.

We provide access free of charge to all of these SEC filings, as soon as reasonably practicable after filing or furnishing such materials with the SEC, on our website located at www.westerngas.com. The public may also obtain such reports from the SEC’s website at www.sec.gov.

Our Corporate Governance Guidelines, Code of Ethics for our Chief Executive Officer and Senior Financial Officers, Code of Business Conduct and Ethics and the charters of the Audit Committee and the Special Committee of our Board of Directors are also available on our website. We will also provide, free of charge, a copy of any of our governance documents listed above upon written request to our general partner’s corporate secretary at our principal executive office. Our principal executive offices are located at 1201 Lake Robbins Drive, The Woodlands, TX 77380-1046. Our telephone number is 832-636-6000.

OUR ASSETS AND AREAS OF OPERATION

As of December 31, 2018, our assets and investments consisted of the following:

|

| | | | | | | | | | | | |

| | | Owned and Operated | | Operated Interests | | Non-Operated Interests | | Equity Interests |

Gathering systems (1) | | 12 |

| | 2 |

| | 3 |

| | 2 |

|

| Treating facilities | | 14 |

| | 3 |

| | — |

| | 3 |

|

| Natural gas processing plants/trains | | 21 |

| | 3 |

| | — |

| | 2 |

|

| NGLs pipelines | | 2 |

| | — |

| | — |

| | 3 |

|

| Natural gas pipelines | | 5 |

| | — |

| | — |

| | — |

|

| Oil pipelines | | — |

| | 1 |

| | — |

| | 2 |

|

| |

(1) | Includes the DBM water systems. |

These assets and investments are located in the Rocky Mountains (Colorado, Utah and Wyoming), North-central Pennsylvania, Texas and New Mexico. The following table provides information regarding our assets by geographic region, as of and for the year ended December 31, 2018, excluding Mentone Train II at the West Texas complex and the Latham processing plant at the DJ Basin complex, which are currently under construction in West Texas and Colorado, respectively, (see Assets Under Development within these Items 1 and 2):

|

| | | | | | | | | | | | | | | | | | | | | | | |

| Area | | Asset Type | | Miles of Pipeline (1) | | Approximate Number of Active Receipt Points (1) | | Compression (HP) (1) (2) | | Processing or Treating Capacity (MMcf/d) (1) | | Processing, Treating or Disposal Capacity (MBbls/d) (1) | | Average Gathering, Processing, Treating and Transportation Throughput (MMcf/d) (3) | | Average Gathering, Treating, Transportation and Disposal Throughput (MBbls/d) (4) |

| Rocky Mountains | | Gathering, Processing and Treating | | 6,894 |

| | 3,584 |

| | 536,470 |

| | 3,250 |

| | 14 |

| | 2,228 |

| | — |

|

| | | Transportation | | 1,500 |

| | 57 |

| | — |

| | — |

| | — |

| | 79 |

| | 26 |

|

| Texas / New Mexico | | Gathering, Processing, Treating and Disposal | | 2,544 |

| | 1,114 |

| | 615,361 |

| | 1,370 |

| | 414 |

| | 1,485 |

| | 183 |

|

| | | Transportation | | 1,647 |

| | 19 |

| | — |

| | — |

| | — |

| | — |

| | 156 |

|

| North-central Pennsylvania | | Gathering | | 146 |

| | 59 |

| | 9,660 |

| | — |

| | — |

| | 100 |

| | — |

|

| Total | | | | 12,731 |

| | 4,833 |

| | 1,161,491 |

| | 4,620 |

| | 428 |

| | 3,892 |

| | 365 |

|

| |

(1) | All system metrics are presented on a gross basis and include owned, rented and leased compressors at certain facilities. Includes horsepower associated with liquid pump stations. Includes bypass capacity at the DJ Basin and West Texas complexes. |

| |

(2) | Excludes compression horsepower for transportation. |

| |

(3) | Includes 100% of Chipeta throughput, a 50.1% share of Springfield gas gathering throughput, a 22% share of Rendezvous throughput and a 14.81% share of Fort Union throughput. |

| |

(4) | Consists of throughput on the Chipeta NGL pipeline, an NGLs line at the Brasada complex and at the DBM water systems, a 50.1% share of Springfield oil gathering throughput, a 10% share of White Cliffs throughput, a 25% share of Mont Belvieu JV throughput, a 20% share of TEG and TEP throughput, a 33.33% share of FRP throughput and a 20% share of Whitethorn throughput. See Properties below for further descriptions of these systems. |

Our operations are organized into a single operating segment that engages in gathering, compressing, treating, processing and transporting natural gas; gathering, stabilizing and transporting condensate, NGLs and crude oil; and gathering and disposing of produced water. We provide these midstream services for Anadarko, as well as for third-party customers in the United States. See Part II, Item 8 of this Form 10-K for disclosure of revenues, profits and total assets for the years ended December 31, 2018, 2017 and 2016.

ACQUISITIONS AND DIVESTITURES

Whitethorn LLC acquisition. In June 2018, we acquired a 20% interest in Whitethorn LLC, which owns a crude oil and condensate pipeline that originates in Midland, Texas and terminates in Sealy, Texas (the “Midland-to-Sealy pipeline”) and related storage facilities (collectively referred to as “Whitethorn”). A third party operates Whitethorn and oversees the related commercial activities. In connection with our investment in Whitethorn, we will share proportionally in the commercial activities. We acquired our 20% interest via a $150.6 million net investment, which was funded with cash on hand and is accounted for under the equity method.

Cactus II acquisition. In June 2018, we acquired a 15% interest in Cactus II, which will own a crude oil pipeline operated by a third party (the “Cactus II pipeline”) connecting West Texas to the Corpus Christi area. The Cactus II pipeline is under construction and is expected to become operational in late 2019. We acquired our 15% interest from a third party via an initial net investment of $12.1 million, which represented our share of costs incurred up to the date of acquisition. The initial investment was funded with cash on hand and the interest in Cactus II is accounted for under the equity method.

Newcastle system divestiture. In December 2018, the Newcastle system, located in Northeast Wyoming, was sold to a third party for $3.2 million, resulting in a net gain on sale of $0.6 million recorded as Gain (loss) on divestiture and other, net in the consolidated statements of operations. We previously held a 50% interest in, and operated, the Newcastle system.

Presentation of Partnership assets. The term “Partnership assets” includes both the assets owned and the interests accounted for under the equity method by us as of December 31, 2018 (see Note 10—Equity Investments in the Notes to Consolidated Financial Statements under Part II, Item 8 of this Form 10-K). Because Anadarko controls us through its control of WGP, which owns the entire interest in our general partner, each acquisition of Partnership assets from Anadarko has been considered a transfer of net assets between entities under common control. As such, the Partnership assets we acquired from Anadarko were initially recorded at Anadarko’s historic carrying value, which did not correlate to the total acquisition price paid by us. Further, after an acquisition of assets from Anadarko, we are required to recast our financial statements to include the activities of such Partnership assets from the date of common control.

For those periods requiring recast, the consolidated financial statements for periods prior to our acquisition of the Partnership assets from Anadarko have been prepared from Anadarko’s historical cost-basis accounts and may not necessarily be indicative of the actual results of operations that would have occurred if we had owned the Partnership assets during the periods reported. For ease of reference, we refer to the historical financial results of the Partnership assets prior to our acquisitions from Anadarko as being “our” historical financial results.

STRATEGY

Our primary business objective is to continue to increase our cash distributions per unit over time. To accomplish this objective, we intend to execute the following strategy:

| |

| • | Capitalizing on organic growth opportunities. We expect to grow certain of our systems organically over time by meeting Anadarko’s and our other customers’ midstream service needs that result from their drilling activity in our areas of operation. We continually evaluate economically attractive organic expansion opportunities in existing or new areas of operation that allow us to leverage our infrastructure, operating expertise and customer relationships to meet new or increased demand of our services. |

| |

| • | Increasing third-party volumes to our systems. We continue to actively market our midstream services to, and pursue strategic relationships with, third-party customers with the intention of attracting additional volumes and/or expansion opportunities. |

| |

| • | Pursuing accretive acquisitions. We expect to continue to pursue accretive acquisitions of midstream assets. |

| |

| • | Managing commodity price exposure. We intend to continue limiting our direct exposure to commodity price changes and promote cash flow stability by pursuing a contract structure designed to mitigate exposure to a substantial majority of the commodity price uncertainty through the use of fee-based contracts. |

| |

| • | Maintaining investment grade metrics. We intend to operate at appropriate leverage and distribution coverage levels in line with other partnerships in our sector that maintain investment grade credit ratings. By maintaining investment grade credit metrics, in part through staying within leverage ratios appropriate for investment-grade partnerships, we believe that we will be able to pursue strategic acquisitions and large growth projects at a lower cost of fixed-income capital, which would enhance our accretion and overall return. |

COMPETITIVE STRENGTHS

We believe that we are well positioned to successfully execute our strategy and achieve our primary business objective because of the following competitive strengths:

| |

| • | Affiliation with Anadarko. We believe Anadarko is motivated to promote and support the successful execution of our business plan and utilize its relationships within the energy industry and the strength of its asset portfolio to pursue projects that help to enhance the value of our business. This includes the ability of Anadarko to secure equity investment opportunities for us in connection with the commitments it makes to other midstream companies. See Our Relationship with Anadarko Petroleum Corporation below. |

| |

| • | Substantial presence in basins with historically strong producer economics. Certain of our systems are in areas, such as the Delaware and DJ Basins, which have historically seen robust producer activity and are considered to have some of the most favorable producer returns for onshore North America. Our assets in these areas serve production where the hydrocarbons contain not only natural gas, but also crude oil, condensate and NGLs. |

| |

| • | Well-positioned and well-maintained assets. We believe that our asset portfolio, which is located in geographically diverse areas of operation, provides us with opportunities to expand and attract additional volumes to our systems from multiple productive reservoirs. Moreover, our portfolio consists of high-quality, well-maintained assets for which we have implemented modern processing, treating, measurement and operating technologies. |

| |

| • | Commodity price and volumetric risk mitigation. We believe a substantial majority of our cash flows are protected from direct fluctuations caused by commodity price volatility, as 89% of our wellhead natural gas volumes (excluding equity investments) and 100% of our crude oil and produced water throughput (excluding equity investments) were attributable to fee-based contracts for the year ended December 31, 2018. In addition, we mitigate volumetric risk by entering into contracts with cost of service structures and/or minimum volume commitments. For the year ended December 31, 2018, 64% of our natural gas throughput and 71% of our crude oil, NGLs and produced water throughput were supported by either minimum volume commitments with associated deficiency payments or cost of service commitments. |

| |

| • | Liquidity to pursue expansion and acquisition opportunities. We believe our operating cash flows, borrowing capacity, long-term relationships and reasonable access to debt and equity capital markets provide us with the liquidity to competitively pursue acquisition and expansion opportunities and to execute our strategy across capital market cycles. As of December 31, 2018, we had $1.3 billion in available borrowing capacity under the RCF. |

| |

| • | Consistent track record of accretive acquisitions. Since our IPO in 2008, our management team has successfully executed eleven related-party acquisitions and nine third-party acquisitions, with an aggregate acquisition value of $6.5 billion. Our management team has demonstrated its ability to identify, evaluate, negotiate, consummate and integrate strategic acquisitions and expansion projects, and it intends to use its experience and reputation to continue to grow the Partnership through accretive acquisitions, focusing on opportunities to improve throughput volumes and cash flows. |

We believe that we will effectively leverage our competitive strengths to successfully implement our strategy. However, our business involves numerous risks and uncertainties that may prevent us from achieving our primary business objective. For a more complete description of the risks associated with our business, read Risk Factors under Part I, Item 1A of this Form 10-K.

OUR RELATIONSHIP WITH ANADARKO PETROLEUM CORPORATION

Our operations and activities are managed by our general partner, which is indirectly controlled by Anadarko through WGP. Anadarko is among the largest independent oil and gas exploration and production companies in the world. Anadarko’s upstream oil and gas business explores for and produces natural gas, crude oil, condensate and NGLs.

We believe that one of our principal strengths is our relationship with Anadarko, and that Anadarko, through its significant indirect economic interest in us, will continue to be motivated to promote and support the successful execution of our business plan and to pursue projects that help to enhance the value of our business.

As of December 31, 2018, WGP held 50,132,046 of our common units, representing a 29.6% limited partner interest in us, and, through its ownership of our general partner, indirectly held 2,583,068 general partner units, representing a 1.5% general partner interest in us, and 100% of our IDRs. As of December 31, 2018, other subsidiaries of Anadarko collectively held 2,011,380 common units and 14,372,665 Class C units, representing an aggregate 9.7% limited partner interest in us. As of December 31, 2018, the public held 100,465,859 common units, representing the remaining 59.2% limited partner interest in us.

For the year ended December 31, 2018, production owned or controlled by Anadarko represented (i) 7% of our natural gas gathering, treating and transportation throughput (excluding equity investment throughput), (ii) 41% of our natural gas processing throughput (excluding equity investment throughput), and (iii) 73% of our crude oil, NGLs and produced water gathering, treating, transportation and disposal throughput (excluding equity investment throughput). In addition, Anadarko supports our operations by providing dedications and/or minimum volume commitments with respect to a substantial portion of its throughput. In executing our growth strategy, which includes acquiring and constructing additional midstream assets, we are able to leverage Anadarko’s significant industry expertise.

During 2018, we had commodity price swap agreements with Anadarko to mitigate exposure to the commodity price risk inherent in our percent-of-proceeds, percent-of-product and keep-whole contracts at the DJ Basin complex and the MGR assets. These commodity price swap agreements expired without renewal on December 31, 2018. See Note 6—Transactions with Affiliates in the Notes to Consolidated Financial Statements under Part II, Item 8 of this Form 10-K.

In connection with our IPO, we entered into an omnibus agreement with Anadarko and our general partner that governs our relationship with Anadarko regarding certain reimbursement and indemnification matters. Although we believe our relationship with Anadarko provides us with a significant advantage in the midstream sector, it is also a source of potential conflicts. For example, neither Anadarko nor WGP is restricted from competing with us. Given Anadarko’s significant indirect economic interest in us through its ownership of WGP, we believe it will be in Anadarko’s best economic interest for it to transfer additional assets to us over time. However, Anadarko continually evaluates acquisitions and divestitures and may elect to acquire, construct or dispose of midstream assets in the future without offering us the opportunity to participate in such transactions. Should Anadarko choose to pursue midstream asset sales, it is under no contractual obligation to offer assets or business opportunities to us, nor are we obligated to participate in any such opportunities. We cannot state with any certainty which, if any, opportunities to acquire additional assets from Anadarko may be made available to us or if we will elect, or will have the ability, to pursue any such opportunities. See Risk Factors under Part I, Item 1A and Certain Relationships and Related Transactions, and Director Independence under Part III, Item 13 of this Form 10-K for more information.

INDUSTRY OVERVIEW

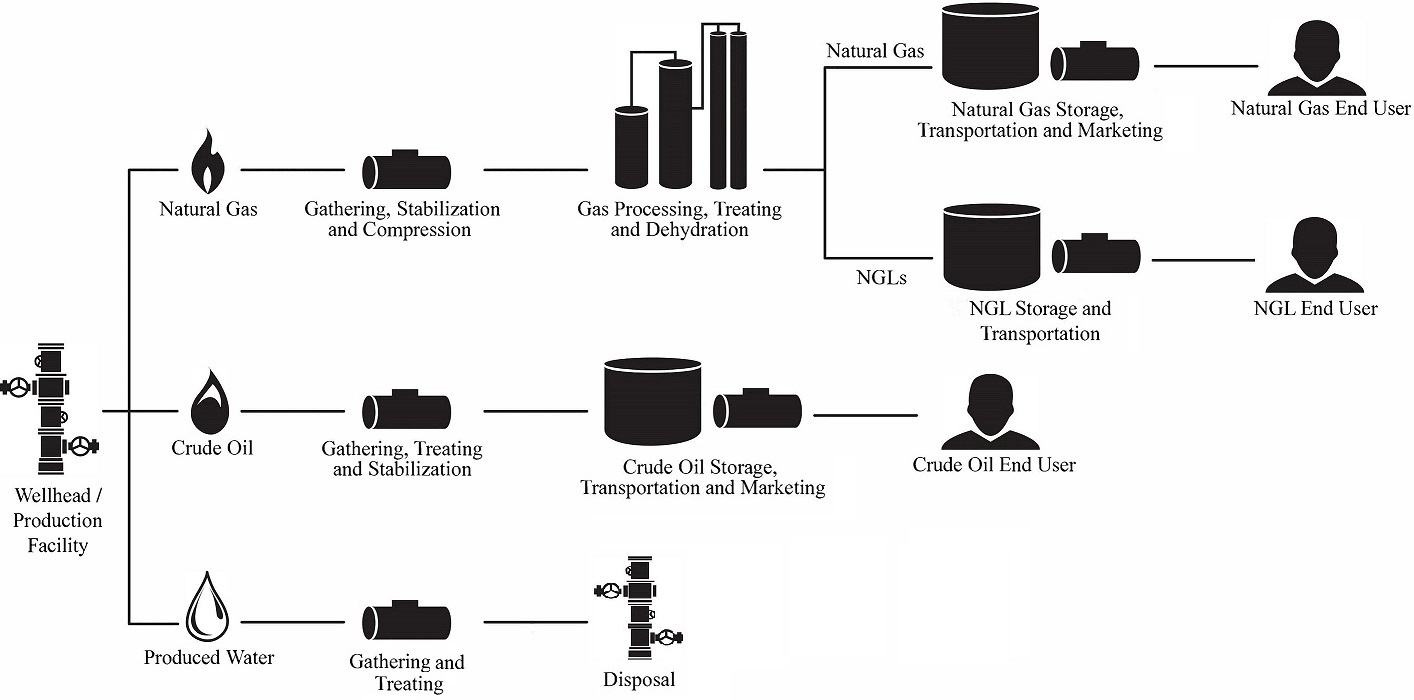

The midstream industry is the link between the exploration for and production of natural gas, NGLs, and crude oil and the delivery of the resulting hydrocarbon components to end-use markets. Operators within this industry create value at various stages along the midstream value chain by gathering production from producers at the wellhead or production facility, separating the produced hydrocarbons into various components and delivering these components to end-use markets, and where applicable, gathering and disposing of produced water.

The following diagram illustrates the primary groups of assets found along the midstream value chain:

Natural Gas Midstream Services

Midstream companies provide services with respect to natural gas that are generally classified into the categories described below.

| |

| • | Gathering. At the initial stages of the midstream value chain, a network of typically smaller diameter pipelines known as gathering systems directly connect to wellheads or production facilities in the area. These gathering systems transport raw, or untreated, natural gas to a central location for treating and processing, if necessary. A large gathering system may involve thousands of miles of gathering lines connected to thousands of wells. Gathering systems are typically designed to be highly flexible to allow gathering of natural gas at different pressures and scalable to allow gathering of additional production without significant incremental capital expenditures. |

| |

| • | Stabilization. Stabilization is a process that separates the heavier hydrocarbons (which are also valuable commodities) that are sometimes found in natural gas, typically referred to as “liquids-rich” natural gas, from the lighter components by using a distillation process or by reducing the pressure and letting the more volatile components flash. |

| |

| • | Compression. Natural gas compression is a mechanical process in which a volume of natural gas at a given pressure is compressed to a desired higher pressure, which allows the natural gas to be gathered more efficiently and delivered into a higher pressure system, processing plant or pipeline. Field compression is typically used to allow a gathering system to operate at a lower pressure or provide sufficient discharge pressure to deliver natural gas into a higher pressure system. Since wells produce at progressively lower field pressures as they deplete, field compression is needed to maintain throughput across the gathering system. |

| |

| • | Treating and dehydration. To the extent that gathered natural gas contains water vapor or contaminants, such as carbon dioxide and hydrogen sulfide, it is dehydrated to remove the saturated water and treated to separate the carbon dioxide and hydrogen sulfide from the gas stream. |

| |

| • | Processing. The principal components of natural gas are methane and ethane, but most natural gas also contains varying amounts of heavier NGLs and contaminants, such as water and carbon dioxide, sulfur compounds, nitrogen or helium. Natural gas is processed to remove unwanted contaminants that would interfere with pipeline transportation or use of the natural gas and to separate those hydrocarbon liquids from the gas that have higher value as NGLs. The removal and separation of individual hydrocarbons through processing is possible due to differences in molecular weight, boiling point, vapor pressure and other physical characteristics. |

| |

| • | Fractionation. Fractionation is the process of applying various levels of higher pressure and lower temperature to separate a stream of NGLs into ethane, propane, normal butane, isobutane and natural gasoline for end-use sale. |

| |

| • | Storage, transportation and marketing. Once the raw natural gas has been treated or processed and the raw NGL mix has been fractionated into individual NGL components, the natural gas and NGL components are stored, transported and marketed to end-use markets. Each pipeline system typically has storage capacity located throughout the pipeline network or at major market centers to better accommodate seasonal demand and daily supply-demand shifts. We do not currently offer storage services. |

Crude Oil Midstream Services

Midstream companies provide services with respect to crude oil that are generally classified into the categories described below.

| |

| • | Gathering. Crude oil gathering assets provide the link between crude oil production gathered at the well site or nearby collection points and crude oil terminals, storage facilities, long-haul crude oil pipelines and refineries. Crude oil gathering assets generally consist of a network of small-diameter pipelines that are connected directly to the well site or central receipt points and deliver into large-diameter trunk lines. To the extent there are not enough volumes to justify construction of or connection to a pipeline system, crude oil can also be trucked from a well site to a central collection point. |

| |

| • | Stabilization. Crude oil stabilization assets process crude oil to meet vapor pressure specifications. Crude oil delivery points, including crude oil terminals, storage facilities, long-haul crude oil pipelines and refineries, often have specific requirements for vapor pressure and temperature, and for the amount of sediment and water that can be contained in any crude oil delivered to them. |

Produced Water Midstream Services

The services provided by us and other midstream companies with respect to produced water are generally classified into the categories described below.

| |

| • | Gathering. Produced water often accounts for the largest byproduct stream associated with production of crude oil and natural gas. Produced water gathering assets provide the link between well sites or nearby collection points and disposal facilities. |

| |

| • | Disposal. As a natural byproduct of crude oil and natural gas production, produced water must be recycled or disposed of in order to maintain production. Produced water disposal systems remove hydrocarbon products and other sediments from the produced water in compliance with applicable regulations and re-inject the produced water utilizing permitted disposal wells. |

Typical Contractual Arrangements

Midstream services, other than transportation, are usually provided under contractual arrangements that vary in the amount of commodity price risk they carry. Three typical contract types, or combinations thereof, are described below:

| |

| • | Fee-based. Under fee-based arrangements, the service provider typically receives a fee for each unit of (i) natural gas, NGLs, or crude oil gathered, treated, processed and/or transported, or (ii) produced water gathered and disposed of, at its facilities. As a result, the price per unit received by the service provider does not vary with commodity price changes, minimizing the service provider’s direct commodity price risk exposure. |

| |

| • | Percent-of-proceeds, percent-of-value or percent-of-liquids. Percent-of-proceeds, percent-of-value or percent-of-liquids arrangements may be used for gathering and processing services. Under these arrangements, the service provider typically remits to the producers either a percentage of the proceeds from the sale of residue gas and/or NGLs or a percentage of the actual residue gas and/or NGLs at the tailgate. These types of arrangements expose the service provider to commodity price risk, as the revenues from the contracts directly correlate with the fluctuating price of natural gas and/or NGLs. |

| |

| • | Keep-whole. Keep-whole arrangements may be used for processing services. Under these arrangements, a customer provides liquids rich gas volumes to the service provider for processing. The service provider is obligated to return the equivalent gas volumes to the customer subsequent to processing. Due to the use and loss of volumes in processing, the service provider must purchase additional volumes to compensate the customer. In these arrangements, the service provider receives all or a portion of the NGLs produced in consideration for the service provided. These type of arrangements can expose the service provider to high levels of commodity price exposure associated with the volumes purchased to keep the customer whole, as well as for the consideration received. |

See Note 1—Summary of Significant Accounting Policies in the Notes to Consolidated Financial Statements under Part II, Item 8 of this Form 10-K for information regarding recognition of revenue under our contracts.

PROPERTIES

The following sections describe in more detail the services provided by our assets in our areas of operation as of December��31, 2018.

GATHERING, PROCESSING AND TREATING

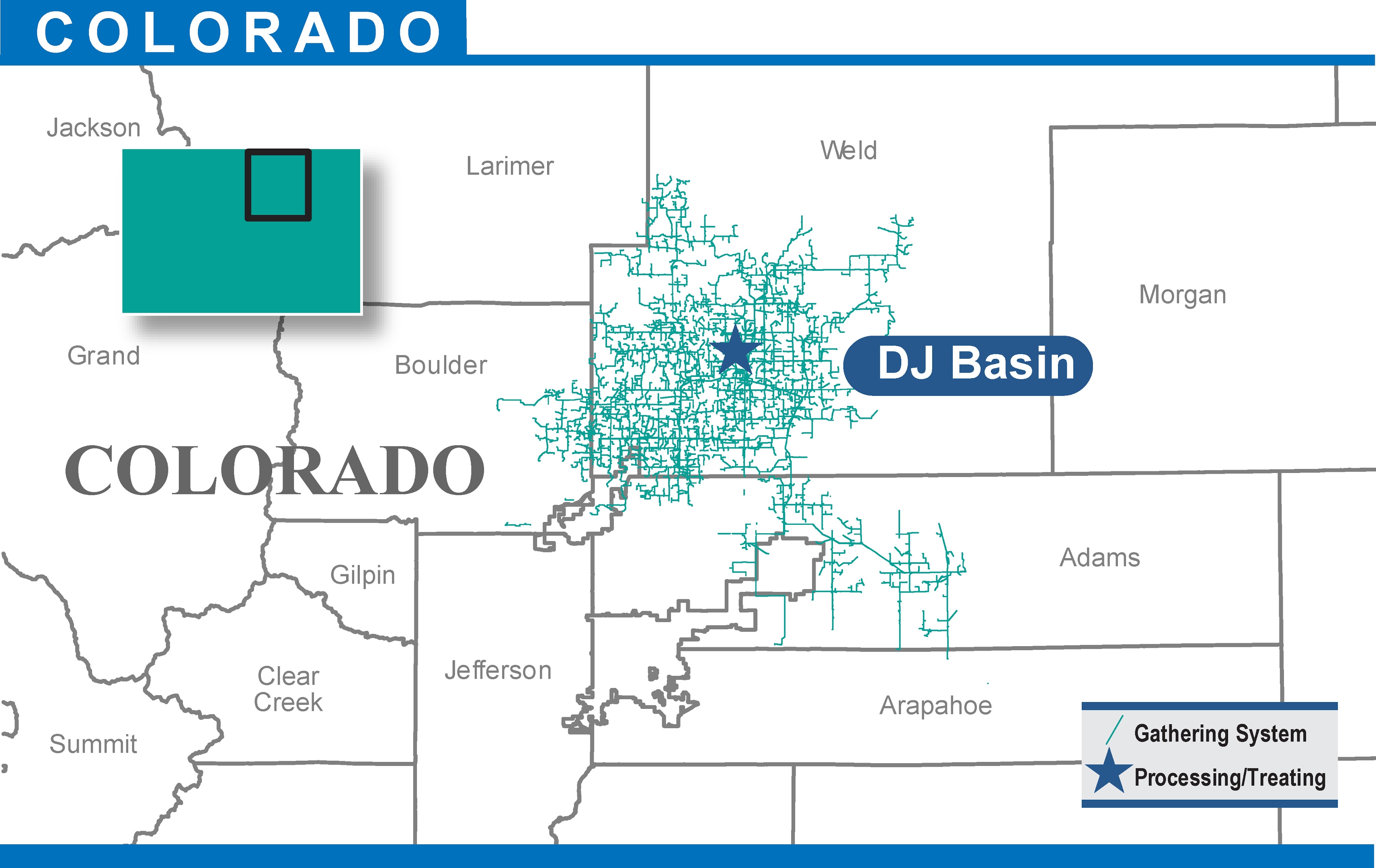

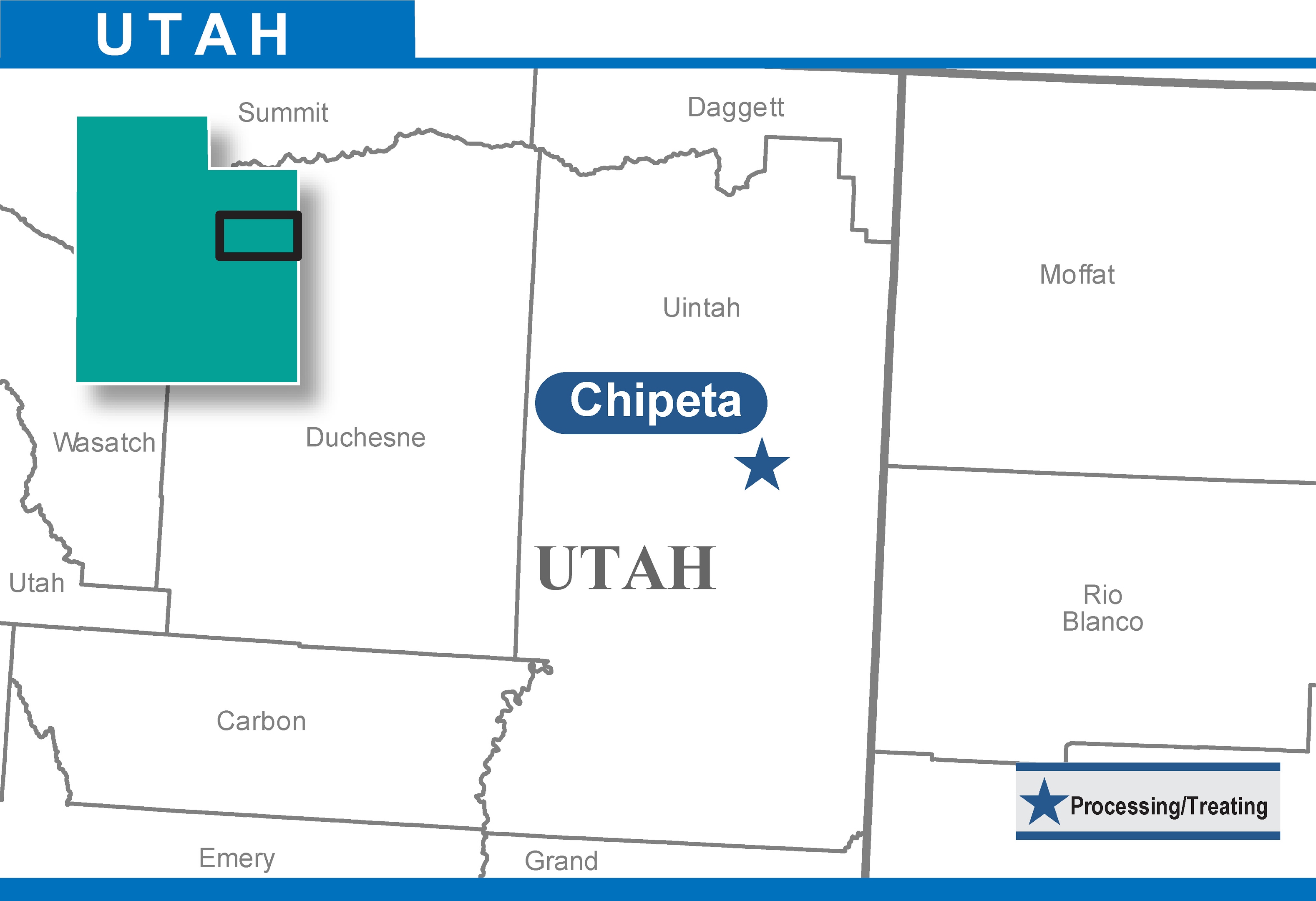

Overview - Rocky Mountains - Colorado and Utah

|

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Location | | Asset | | Type | | Processing / Treating Plants | | Processing / Treating Capacity (MMcf/d) (1) | | Processing / Treating Capacity (MBbls/d) | | Compressors | | Compression Horsepower | | Gathering Systems | | Pipeline Miles |

| Colorado | | DJ Basin complex (2) | | Gathering, Processing & Treating | | 10 |

| | 1,010 |

| | 14 |

| | 120 |

| | 302,187 |

| | 2 |

| | 3,215 |

|

| Utah | | Chipeta (3) | | Processing | | 3 |

| | 790 |

| | — |

| | 12 |

| | 74,875 |

| | — |

| | 2 |

|

| Total | | | | | | 13 |

| | 1,800 |

| | 14 |

| | 132 |

| | 377,062 |

| | 2 |

| | 3,217 |

|

| |

(1) | Includes 160 MMcf/d of bypass capacity at the DJ Basin complex. |

| |

(2) | The DJ Basin complex includes the Platte Valley, Fort Lupton, Fort Lupton JT, Hambert JT, which is currently inactive, and Lancaster Trains I and II processing plants and the Wattenberg gathering system. |

| |

(3) | We are the managing member of and own a 75% interest in Chipeta, which owns the Chipeta processing complex. |

DJ Basin gathering, treating and processing complex

| |

| • | Customers. As of December 31, 2018, throughput at the DJ Basin complex was from Anadarko and numerous third-party customers. For the year ended December 31, 2018, Anadarko’s production represented 65% of the DJ Basin complex throughput and the largest third-party customer provided 14% of the throughput. |

| |

| • | Supply. The DJ Basin complex is primarily supplied by the Wattenberg field. There were 2,122 active receipt points connected to the DJ Basin complex as of December 31, 2018. Anadarko holds interests in approximately 645,000 gross (460,000 net) acres within the DJ Basin and during the year ended December 31, 2018, turned 278 operated wells to sales in the DJ Basin. |

| |

| • | Delivery points. As of December 31, 2018, the DJ Basin complex had the following delivery points for gas not processed within the DJ Basin complex: |

| |

| ◦ | Anadarko’s Wattenberg plant inlet; and |

| |

| ◦ | Various interconnections with DCP Midstream LP’s (“DCP”) gathering and processing system. |

The DJ Basin complex is connected to the Colorado Interstate Gas Company LLC’s pipeline (“CIG pipeline”) and Xcel Energy’s residue pipelines for natural gas residue takeaway and to Overland Pass Pipeline Company LLC’s pipeline and FRP’s pipeline for NGLs takeaway. In addition, the NGLs fractionator at the Platte Valley plant and associated truck-loading facility provides access to local NGLs markets.

Chipeta processing complex

| |

| • | Customers. As of December 31, 2018, throughput at the Chipeta complex was from Anadarko and numerous third-party customers. For the year ended December 31, 2018, Anadarko’s production represented 74% of the Chipeta complex throughput and the largest third-party customer provided 15% of the throughput. |

| |

| • | Supply. The Chipeta complex is well positioned to access Anadarko and third-party production in the Uinta Basin where Anadarko holds interests in 244,000 gross acres. Chipeta’s inlet is connected to Anadarko’s Natural Buttes gathering system, the Dominion Energy Questar Pipeline, LLC system (“Questar pipeline”) and Three Rivers Gathering, LLC’s system, which is owned by Andeavor Logistics LP (“Andeavor”). |

| |

| • | Delivery points. The Chipeta plant delivers NGLs to Enterprise Products Partners LP’s (“Enterprise”) Mid-America Pipeline Company pipeline (“MAPL pipeline”), which provides transportation through Enterprise’s Seminole pipeline (“Seminole pipeline”) and TEP’s pipeline in West Texas and ultimately to the NGLs fractionation and storage facilities in Mont Belvieu, Texas. The Chipeta plant has residue gas delivery points through the following pipelines delivering to markets throughout the Rockies and Western United States: |

| |

| ◦ | Wyoming Interstate Company’s pipeline (“WIC pipeline”). |

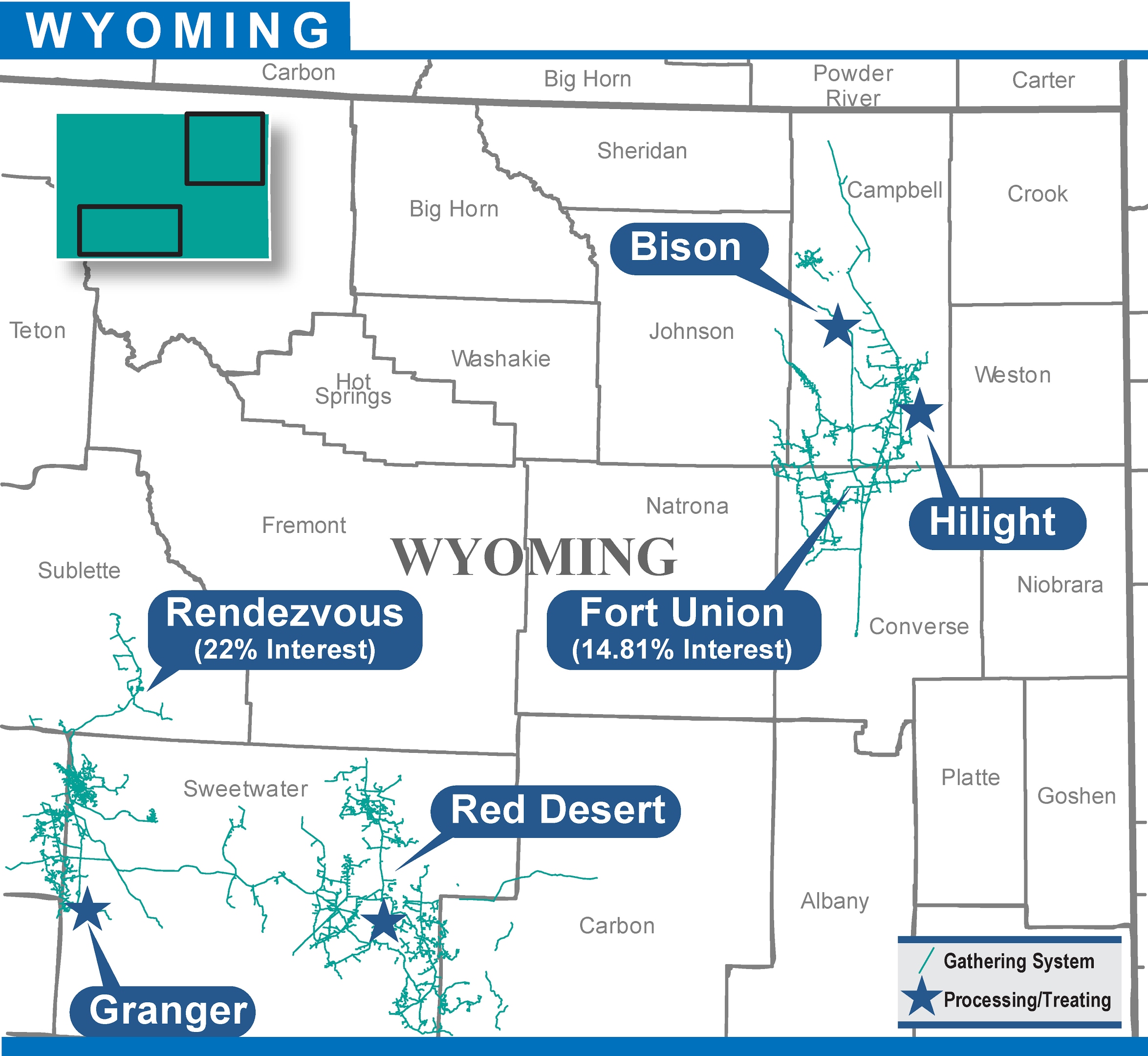

Overview - Rocky Mountains - Wyoming

|

| | | | | | | | | | | | | | | | | | | | | | |

| Location | | Asset | | Type | | Processing / Treating Plants | | Processing / Treating Capacity (MMcf/d) | | Compressors | | Compression Horsepower | | Gathering Systems | | Pipeline Miles |

| Northeast Wyoming | | Bison | | Treating | | 3 |

| | 450 |

| | 9 |

| | 14,645 |

| | — |

| | — |

|

| Northeast Wyoming | | Fort Union (1) | | Gathering & Treating | | 3 |

| | 295 |

| | 3 |

| | 5,454 |

| | 1 |

| | 315 |

|

| Northeast Wyoming | | Hilight | | Gathering & Processing | | 2 |

| | 60 |

| | 34 |

| | 36,554 |

| | 1 |

| | 1,232 |

|

| Southwest Wyoming | | Granger complex (2) | | Gathering & Processing | | 4 |

| | 520 |

| | 41 |

| | 44,967 |

| | 1 |

| | 738 |

|

| Southwest Wyoming | | Red Desert complex (3) | | Gathering & Processing | | 1 |

| | 125 |

| | 25 |

| | 50,303 |

| | 1 |

| | 1,054 |

|

| Southwest Wyoming | | Rendezvous (4) | | Gathering | | — |

| | — |

| | 5 |

| | 7,485 |

| | 1 |

| | 338 |

|

| Total | | | | | | 13 |

| | 1,450 |

| | 117 |

| | 159,408 |

| | 5 |

| | 3,677 |

|

| |

(1) | We have a 14.81% interest in Fort Union. |

| |

(2) | The Granger complex includes the “Granger straddle plant,” a refrigeration processing plant. |

| |

(3) | The Red Desert complex includes the Red Desert cryogenic processing plant, which is currently inactive, and the Patrick Draw cryogenic processing plant. |

| |

(4) | We have a 22% interest in the Rendezvous gathering system, which is operated by a third party. |

Northeast Wyoming

Bison treating facility

| |

| • | Customers. Throughput at the Bison treating facility was from two third-party customers as of December 31, 2018. The largest customer provided 75% of the throughput for the year ended December 31, 2018. In connection with Anadarko’s sale of its Powder River Basin coal-bed methane assets in 2015, Anadarko retained its throughput commitment to Bison through 2020. |

| |

| • | Supply and delivery points. The Bison treating facility treats and compresses gas from coal-bed methane wells in the Powder River Basin of Wyoming. The Bison treating facility is directly connected to Fort Union’s pipeline and the Bison pipeline operated by TransCanada Corporation. |

Fort Union gathering system and treating facility

| |

| • | Customers. Moriah Powder River, LLC holds a majority of the firm capacity on the Fort Union system. To the extent capacity on the system is not used by this customer, it is available to third parties under interruptible agreements. |

| |

| • | Supply. Substantially all of Fort Union’s gas supply is comprised of coal-bed methane volumes from the Powder River Basin near Gillette, Wyoming that are either produced or gathered by the customer noted above and their affiliates. These volumes are gathered and treated under contracts with minimum volume commitments. |

| |

| • | Delivery points. The Fort Union system delivers coal-bed methane gas to the hub in Glenrock, Wyoming, which has access to the following interstate pipelines: |

| |

| ◦ | Tallgrass Interstate Gas Transmission system’s pipeline (“TIGT pipeline”); and |

These pipelines serve gas markets in the Rocky Mountains and Midwest regions of the United States.

Hilight gathering system and processing plant

| |

| • | Customers. As of December 31, 2018, gas gathered and processed through the Hilight system was from numerous third-party customers. The four largest producers provided 72% of the system throughput for the year ended December 31, 2018. |

| |

| • | Supply. The Hilight gathering system serves the gas gathering needs of several conventional producing fields in Johnson, Campbell, Natrona and Converse Counties, Wyoming. |

| |

| • | Delivery points. The Hilight plant delivers residue into our MIGC transmission line (see Transportation within these Items 1 and 2). Hilight is not connected to an active NGLs pipeline, resulting in all fractionated NGLs being sold locally through truck and rail loading facilities. |

Southwest Wyoming

Granger gathering and processing complex

| |

| • | Customers. As of December 31, 2018, throughput at the Granger complex was from numerous third-party customers. The two largest third-party customers provided 78% of the Granger complex throughput for the year ended December 31, 2018. |

| |

| • | Supply. The Granger complex is supplied by the Moxa Arch and the Jonah and Pinedale Anticline fields. The Granger gas gathering system had 577 active receipt points as of December 31, 2018. |

| |

| • | Delivery points. The residue from the Granger complex can be delivered to the following major pipelines: |

| |

| ◦ | Berkshire Hathaway Energy’s Kern River pipeline (“Kern River pipeline”) via a connect with Andeavor’s Rendezvous pipeline (“Rendezvous pipeline”); |

| |

| ◦ | Dominion Energy Overthrust Pipeline; |

| |

| ◦ | The Williams Companies, Inc.’s Northwest Pipeline (“NWPL”); |

| |

| ◦ | our Mountain Gas Transportation LLC pipeline. |

The NGLs have market access to the MAPL pipeline, which terminates at Mont Belvieu, Texas, as well as to local markets.

Red Desert gathering and processing complex

| |

| • | Customers. As of December 31, 2018, throughput at the Red Desert complex was from Anadarko and numerous third-party customers. For the year ended December 31, 2018, 40% of the Red Desert complex throughput was from the two largest third-party customers and 2% was from Anadarko. |

| |

| • | Supply. The Red Desert complex gathers, compresses, treats and processes natural gas and fractionates NGLs produced from the eastern portion of the Greater Green River Basin, providing service primarily to the Red Desert and Washakie Basins. |

| |

| • | Delivery points. Residue from the Red Desert complex is delivered to the CIG and WIC pipelines, while NGLs are delivered to the MAPL pipeline, as well as to truck and rail loading facilities. |

Rendezvous gathering system

| |

| • | Customers. As of December 31, 2018, throughput on the Rendezvous gathering system was primarily from two shippers that have dedicated acreage to the system. |

| |

| • | Supply and delivery points. The Rendezvous gathering system provides high pressure gathering service for gas from the Jonah and Pinedale Anticline fields and delivers to our Granger plant, as well as Andeavor’s Blacks Fork gas processing plant, which connects to the Questar pipeline, NWPL and the Kern River pipeline via the Rendezvous pipeline. |

Overview - Texas and New Mexico

|

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Location | | Asset | | Type | | Processing / Treating Plants | | Processing / Treating Capacity (MMcf/d) (1) | | Processing / Treating / Disposal Capacity (MBbls/d) | | Compressors / Pumps (2) | | Compression Horsepower (2) | | Gathering Systems | | Pipeline Miles (3) |

| West Texas / New Mexico | | West Texas complex (4) | | Gathering, Processing & Treating | | 12 |

| | 1,170 |

| | 34 |

| | 246 |

| | 405,445 |

| | 3 |

| | 1,620 |

|

| West Texas | | DBM water systems | | Gathering & Disposal | | — |

| | — |

| | 120 |

| | 19 |

| | 7,250 |

| | 2 |

| | 46 |

|

| East Texas | | Mont Belvieu JV (5) | | Processing | | 2 |

| | — |

| | 170 |

| | — |

| | — |

| | — |

| | — |

|

| South Texas | | Brasada complex | | Gathering, Processing & Treating | | 3 |

| | 200 |

| | 15 |

| | 14 |

| | 30,450 |

| | 1 |

| | 57 |

|

| South Texas | | Springfield system (6) | | Gathering and Treating | | 3 |

| | — |

| | 75 |

| | 107 |

| | 172,216 |

| | 2 |

| | 821 |

|

| Total | | | | | | 20 |

| | 1,370 |

| | 414 |

| | 386 |

| | 615,361 |

| | 8 |

| | 2,544 |

|

| |

(1) | Includes 70 MMcf/d of bypass capacity at the West Texas complex. |

| |

(2) | Includes owned, rented and leased compressors and compression horsepower. |

| |

(3) | Includes 18 miles of transportation related to the Ramsey Residue Lines at the West Texas complex. |

| |

(4) | The West Texas complex includes the DBM complex and DBJV and Haley systems. Excludes 2,000 gpm of amine treating capacity. |

| |

(5) | We own a 25% interest in the Mont Belvieu JV, which owns two NGLs fractionation trains. A third party serves as the operator. |

| |

(6) | We own a 50.1% interest in the Springfield system and serve as the operator. |

West Texas gathering, treating and processing complex

| |

| • | Customers. As of December 31, 2018, throughput at the West Texas complex was from Anadarko and numerous third-party customers. For the year ended December 31, 2018, Anadarko’s production represented 30% of the West Texas complex throughput and the largest third-party customer provided 11% of the throughput. |

| |

| • | Supply. Supply of gas and NGLs for the complex comes from production from the Delaware Sands, Avalon Shale, Bone Spring, Wolfcamp and Penn formations in the Delaware Basin portion of the Permian Basin. Anadarko holds interests in approximately 590,000 gross (240,000 net) acres within the Delaware Basin. |

| |

| • | Delivery points. Avalon, Bone Spring and Wolfcamp gas is dehydrated, compressed and delivered to the Bone Spring Gas Processing plant (the “Bone Spring plant”), the Mi Vida Gas Processing plant (the “Mi Vida plant”) and within the West Texas complex for processing, while lean gas is delivered into Enterprise GC, L.P.’s pipeline for ultimate delivery into Energy Transfer LP’s (“ET”) Oasis pipeline (the “Oasis pipeline”). Residue gas from the Bone Spring and Mi Vida plants is delivered into the Oasis pipeline or Transwestern Pipeline Company LLC’s pipeline. Residue gas produced at the West Texas complex is delivered to ET’s Red Bluff Express pipeline and the Ramsey Residue Lines, which extend from the complex to the south and to the north, with both lines connecting with Kinder Morgan, Inc.’s interstate pipeline system. NGLs production is delivered into the Sand Hills pipeline, Lone Star NGL LLC’s pipeline and EPIC Y-Grade Pipeline, LP’s NGL pipeline. See Note 3—Acquisitions and Divestitures in the Notes to Consolidated Financial Statements under Part II, Item 8 of this Form 10-K. |

DBM produced water disposal systems. The DBM water systems consist of the River Reeves and Silvertip systems.

| |

| • | Customers. As of December 31, 2018, throughput at the DBM water systems was from Anadarko and four third-party producers. Anadarko’s production represented 98% of the throughput for the year ended December 31, 2018. |

| |

| • | Supply. The systems gather and dispose produced water for Anadarko and third-party producers. |

Mont Belvieu JV fractionation trains

| |

| • | Customers. The Mont Belvieu JV does not directly contract with customers, but rather is allocated volumes from Enterprise based on the available capacity of the other trains at Enterprise’s NGLs fractionation complex in Mont Belvieu, Texas. |

| |

| • | Supply and delivery points. Enterprise receives volumes at its fractionation complex in Mont Belvieu, Texas via a large number of pipelines that terminate there, including the Seminole pipeline, Skelly-Belvieu Pipeline Company, LLC’s pipeline, TEP and Enterprise’s Panola Pipeline, in which Anadarko has a 15% equity interest. Individual NGLs are delivered to end users either through customer-owned pipelines that are connected to nearby petrochemical plants or via export terminal. |

Brasada gathering, stabilization, treating and processing complex

| |

| • | Customers. Throughput at the Brasada complex was from one third-party customer as of December 31, 2018. |

| |

| • | Supply. Supply of gas and NGLs comes from throughput gathered by the Springfield system. |

| |

| • | Delivery points. The facility delivers residue gas into the Eagle Ford Midstream system operated by NET Midstream, LLC. It delivers stabilized condensate into Plains All American Pipeline and NGLs into the South Texas NGL Pipeline System operated by Enterprise. |

Springfield gathering system, stabilization facility and storage

| |

| • | Customers. Throughput at the Springfield system was from numerous third-party customers as of December 31, 2018. |

| |

| • | Supply. Supply of gas and oil comes from third-party production in the Eagleford shale. |

| |

| • | Delivery points. The gas gathering system delivers rich gas to our Brasada complex, the Raptor processing plant owned by Targa Resources Corp. and Sanchez Midstream Partners LP, and to processing plants operated by Enterprise, ET and Kinder Morgan, Inc. The oil gathering system has delivery points to Plains All American Pipeline, Kinder Morgan, Inc.’s Double Eagle Pipeline, Hilcorp Energy Company’s Harvest Pipeline and NuStar Energy L.P.’s Pipeline. |

Overview - North-central Pennsylvania

|

| | | | | | | | | | | | | | | | |

| Location | | Asset | | Type | | Compressors | | Compression Horsepower | | Gathering Systems | | Pipeline Miles |

| North-central Pennsylvania | | Marcellus (1) | | Gathering | | 7 |

| | 9,660 |

| | 3 |

| | 146 |

|

| |

(1) | We own a 33.75% interest in the Marcellus Interest gathering systems. |

Marcellus gathering systems

| |

| • | Customers. As of December 31, 2018, the Marcellus Interest gathering systems had multiple priority shippers. The largest producer provided 86% of the throughput for the year ended December 31, 2018. Capacity not used by priority shippers is available to third parties as determined by the operating partner, Alta Resources Development, LLC. |

| |

| • | Supply and delivery points. The Marcellus Interest gathering systems are well positioned to serve dry gas production from the Marcellus shale. The Marcellus Interest gathering systems have access to Transcontinental Gas Pipe Line Company, LLC’s pipeline. |

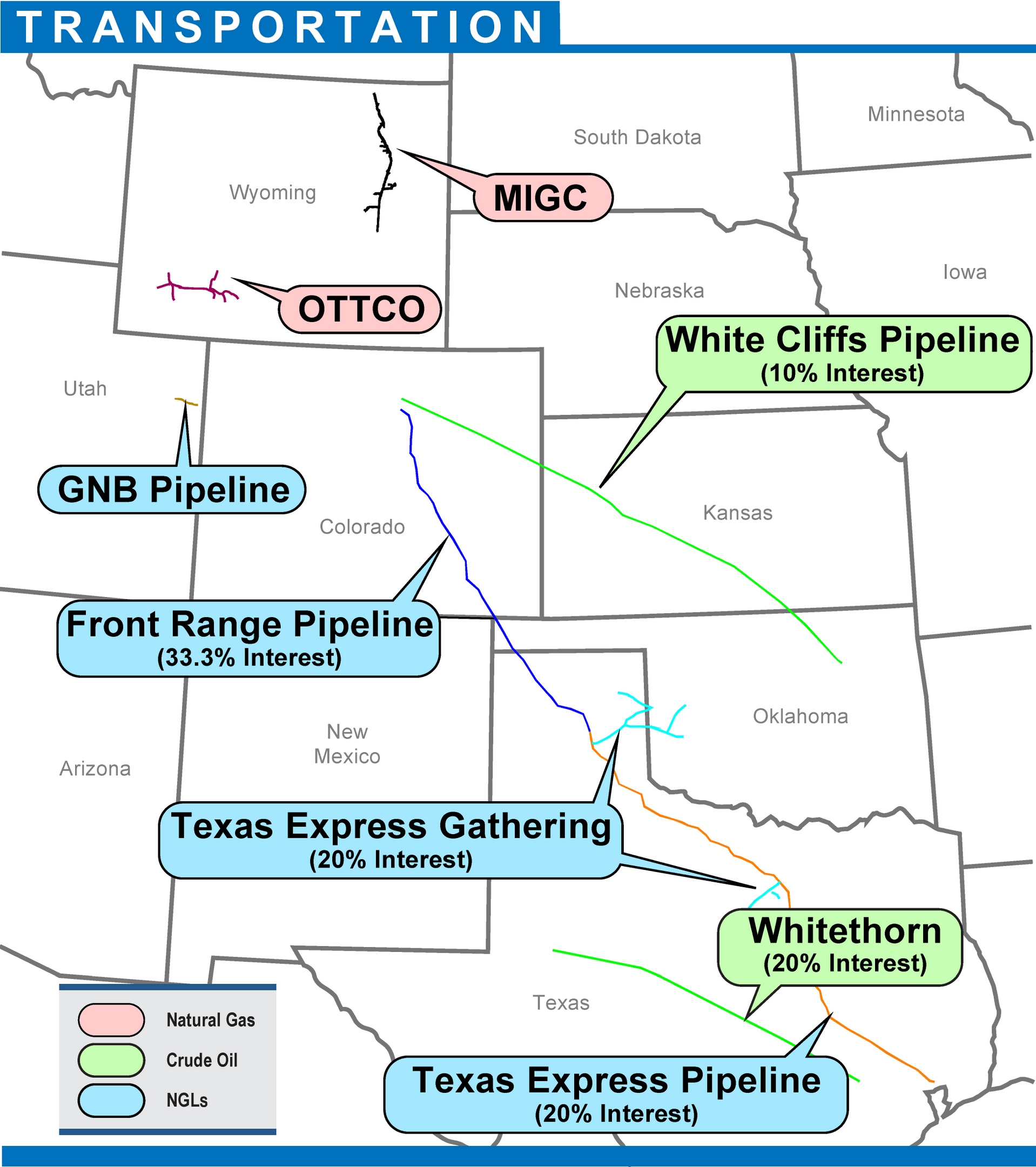

Overview

|

| | | | | | | |

| Location | | Asset | | Type | | Pipeline Miles |

| Colorado, Kansas, Oklahoma | | White Cliffs (1) (2) | | Oil | | 1,054 |

|

| Utah | | GNB NGL (1) | | NGLs | | 33 |

|

| Northeast Wyoming | | MIGC (1) | | Gas | | 239 |

|

| Southwest Wyoming | | OTTCO | | Gas | | 174 |

|

| Colorado, Oklahoma, Texas | | FRP (1) (3) | | NGLs | | 447 |

|

| Texas, Oklahoma | | TEG (3) | | NGLs | | 191 |

|

| Texas | | TEP (1) (3) | | NGLs | | 593 |

|

| Texas | | Whitethorn (4) | | Oil | | 416 |

|

| Total | | | | | | 3,147 |

|

| |

(1) | White Cliffs, GNB NGL, MIGC, FRP and TEP are regulated by FERC. |

| |

(2) | We own a 10% interest in the White Cliffs pipeline, which is operated by a third party. |

| |

(3) | We own a 20% interest in TEG and TEP and a 33.33% interest in FRP. All three systems are operated by third parties. |

| |

(4) | We own a 20% interest in Whitethorn, which is operated by a third party. |

Rocky Mountains - Colorado

White Cliffs pipeline

| |

| • | Customers. The White Cliffs pipeline had multiple committed shippers, including Anadarko, as of December 31, 2018. In addition, other parties may ship on the White Cliffs pipeline at FERC-based rates. The White Cliffs dual pipeline system provides crude oil takeaway capacity of approximately 190 MBbls/d from Platteville, Colorado to Cushing, Oklahoma. During 2019, one of the pipelines will be converted from crude service to NGL Y-grade service with an initial capacity of 90 MBbls/d. To achieve this, the pipeline will be taken out of service in early 2019 and is expected to come back online during the fourth quarter of 2019. |

| |

| • | Supply. The White Cliffs pipeline is supplied by production from the DJ Basin. At the point of origin, there is a storage facility adjacent to a truck-unloading facility. |

| |

| • | Delivery points. The White Cliffs pipeline delivery point is SemCrude’s storage facility in Cushing, Oklahoma, a major crude oil marketing center, which ultimately delivers to Gulf Coast and mid-continent refineries. |

Rocky Mountains - Utah

GNB NGL pipeline

| |

| • | Customers. Anadarko was the only shipper on the GNB NGL pipeline as of December 31, 2018. |

| |

| • | Supply. The GNB NGL pipeline receives NGLs from Chipeta’s gas processing facility and Andeavor’s Stagecoach/Iron Horse gas processing complex. |

| |

| • | Delivery points. The GNB NGL pipeline delivers NGLs to the MAPL pipeline, which provides transportation through the Seminole pipeline and TEP in West Texas, and ultimately to NGLs fractionation and storage facilities in Mont Belvieu, Texas. |

Rocky Mountains - Northeast Wyoming

MIGC transportation system

| |

| • | Customers. Anadarko was the largest firm shipper on the MIGC system, with 85% of the throughput for the year ended December 31, 2018. The remaining throughput on the MIGC system was from numerous third-party shippers. MIGC is certificated for 175 MMcf/d of firm transportation capacity. |

| |

| • | Supply. MIGC receives gas from various coal-bed methane gathering systems in the Powder River Basin and the Hilight system, as well as from WBI Energy Transmission, Inc. on the north end of the transportation system. |

| |

| • | Delivery points. MIGC volumes can be redelivered to the hub in Glenrock, Wyoming, which has access to the following interstate pipelines: |

Volumes can also be delivered to Cheyenne Light Fuel & Power and several industrial users.

Rocky Mountains - Southwest Wyoming

OTTCO transportation system

| |

| • | Customers. For the year ended December 31, 2018, 10% of OTTCO’s throughput was from Anadarko. The remaining throughput on the OTTCO transportation system was from two third-party shippers. Revenues on the OTTCO transportation system are generated from contracts that contain minimum volume commitments and volumetric fees paid by shippers under firm and interruptible gas transportation agreements. |

| |

| • | Supply and delivery points. Supply points to the OTTCO transportation system include approximately 30 wellheads, the Granger complex and ExxonMobil Corporation’s Shute Creek plant, which are supplied by the eastern portion of the Greater Green River Basin, the Moxa Arch and the Jonah and Pinedale Anticline fields. Primary delivery points include the Red Desert complex, two third-party industrial facilities and an inactive interconnection with the Kern River pipeline. |

Texas

TEFR Interests

| |

| • | Front Range Pipeline. FRP provides takeaway capacity from the DJ Basin in Northeast Colorado. FRP has receipt points at gas plants in Weld and Adams Counties, Colorado (including the Lancaster plant, which is within the DJ Basin complex and Anadarko’s Wattenberg plant) (see Rocky Mountains—Colorado and Utah within these Items 1 and 2). FRP connects to TEP near Skellytown, Texas. As of December 31, 2018, FRP had multiple committed shippers, including Anadarko. FRP provides capacity to other shippers at the posted FERC tariff rate. In 2018, we elected to participate in the expansion of FRP, which will increase capacity by 100 MBbls/d, to a targeted total capacity of 258 MBbls/d, with the expansion expected to be completed in 2019. |

| |

| • | Texas Express Gathering. TEG consists of two NGLs gathering systems that provide plants in North Texas, the Texas panhandle and West Oklahoma with access to NGLs takeaway capacity on TEP. TEG had one committed shipper as of December 31, 2018. In 2018, we participated in the expansion of the Texas/Oklahoma system of TEG, which has a total capacity of 100 MBbls/d and was completed in the second quarter of 2018. |

| |

| • | Texas Express Pipeline. TEP delivers to NGLs fractionation and storage facilities in Mont Belvieu, Texas. TEP is supplied with NGLs from other pipelines including FRP, the MAPL pipeline and TEG. As of December 31, 2018, TEP had multiple committed shippers, including Anadarko. TEP provides capacity to other shippers at the posted FERC tariff rates. In 2018, we elected to participate in the expansion of TEP, which will increase capacity by 90 MBbls/d, to a targeted total capacity of 348 MBbls/d, with the expansion expected to be completed in 2019. |

Whitethorn

Supply and delivery points. Whitethorn is supplied by production from the Permian Basin. Whitethorn transports crude oil and condensate from Enterprise’s Midland terminal to Enterprise’s Sealy terminal. From Sealy, shippers have access to Enterprise’s Rancho II pipeline, which extends to Enterprise’s ECHO terminal located in Houston, Texas. From ECHO, shippers have access to refineries in Houston, Texas City, Beaumont and Port Arthur, Texas, as well as Enterprise’s crude oil export facilities.

Assets Under Development

In addition to significant gathering expansion projects at the West Texas and DJ Basin complexes and the DBM water systems, we currently have the following significant projects scheduled for completion in 2019 in West Texas and Colorado. See Capital expenditures, under Part II, Item 7 of this Form 10-K.

| |

| • | Mentone Train II. We are currently constructing a second cryogenic processing train at the Mentone processing plant at the West Texas complex. Mentone Train II will have a capacity of 200 MMcf/d, and we expect this train to be completed in the first quarter of 2019. Upon completion of Mentone Train II, the West Texas complex will have a total processing capacity of 1,370 MMcf/d. |

| |

| • | Latham processing plant. We are currently constructing two cryogenic processing trains at a new processing plant located in Weld County, Colorado. Latham Trains I and II will each have a capacity of 200 MMcf/d. Latham Train I is expected to be completed in mid-2019 and Latham Train II is expected to be completed around year-end 2019. The Latham processing plant will be part of the DJ Basin complex, and upon completion of Latham Trains I and II, the DJ Basin complex will have a total processing capacity of 1,410 MMcf/d. |

| |

| • | Equity investments. We are currently contributing to the construction of the Cactus II pipeline, a crude oil pipeline connecting West Texas to the Corpus Christi area. The Cactus II pipeline will have a total capacity of 670 MBbls/d upon completion and is expected to become operational in late 2019. |

COMPETITION

The midstream services business is extremely competitive. Our competitors include other midstream companies, producers, and intrastate and interstate pipelines. Competition is primarily based on reputation, commercial terms, reliability, service levels, location, available capacity, capital expenditures and fuel efficiencies. However, Anadarko supports our operations by providing dedications and/or minimum volume commitments with respect to a substantial portion of its throughput. We believe that our assets located outside of the dedicated areas are geographically well positioned to retain and attract third-party volumes due to our competitive rates.

We believe the primary advantages of our assets are their proximity to established and/or future production, and the service flexibility they provide to producers. We believe we can efficiently, and at competitive and flexible contract terms, provide services that customers require to connect, gather and process their natural gas, and gather and dispose of their produced water.

Gathering Systems and Processing Plants

The following table summarizes the primary competitors for our gathering systems and processing plants as of December 31, 2018.

|

| | |

| Asset | | Competitor(s) |

| Bison facility | | Thunder Creek Gas Services, LLC and Fort Union (treating only) |

| Brasada complex | | Enterprise, ET, Targa Resources Partners LP, Kinder Morgan, Inc., Plains All American Pipeline and Howard Energy Partners |

| Chipeta complex | | Andeavor and Kinder Morgan, Inc. |

| DBM water systems | | NGL Water Solutions, LLC, Mesquite SWD, Inc., Oilfield Water Logistics, LLC and Hillstone Environmental Partners, LLC |

| DJ Basin complex | | DCP, AKA Energy Group, LLC, Rocky Mountain Midstream LLC and Cureton Midstream, LLC |

| Fort Union system | | Bison treating facility (carbon dioxide treating services only), MIGC, Thunder Creek Gas Services, LLC and TransCanada Corporation |

| Granger complex | | Williams Field Services Company, LLC, Enterprise/Jonah Gas Gathering Company and Andeavor |

| Hilight system | | ONEOK Gas Gathering Company, Thunder Creek Gas Services, LLC, Crestwood Midstream Partners LP, Tallgrass Energy Partners, LP and Evolution Midstream |

| Marcellus Interest gathering systems | | ET and National Fuel Gas Midstream Corporation |

| Mont Belvieu JV | | Targa Resources Partners LP, Phillips 66, Lone Star NGL LLC and ONEOK Partners, LP |

| Red Desert complex | | Williams Field Services Company, LLC and Andeavor |

| Rendezvous system | | No significant direct competition |

| Springfield system | | Enterprise, ET, Targa Resources Partners LP, Kinder Morgan, Inc., Plains All American Pipeline, Southcross Energy Partners, L.P., Williams Field Services Company, LLC and Howard Energy Partners |

| West Texas complex | | ET, Targa Resources Partners LP, Enterprise GC, L.P., EagleClaw Midstream Ventures, LLC, Enlink Midstream Partners, LP, Vaquero Midstream LLC, MPLX LP, Crestwood Midstream Partners LP and Noble Midstream Partners LP |

Transportation