Table of Contents

Filed Pursuant to Rule 424(b)(3)

Registration No. 333-230151

PROSHARES TRUST II

Common Units of Beneficial Interest

Title of Securities to be Registered | Benchmark | Proposed Maximum Aggregate Offering Price Per Fund | ||||

ProShares VIX Short-Term Futures ETF (VIXY) | S&P 500® VIX Short-Term Futures Index | $ | 1,157,471,315 | |||

ProShares Ultra VIX Short-Term Futures ETF (UVXY) | S&P 500 ® VIX Short-Term Futures Index | $ | 6,661,218,948 | |||

ProShares Short VIX Short-Term Futures ETF (SVXY) | S&P 500® VIX Short-Term Futures Index | $ | 8,945,616,566 | |||

ProShares Trust II (the “Trust”) is a Delaware statutory trust organized into separate series. The Trust may from time to time offer to sell common units of beneficial interest (“Shares”) of any or all of the three series of the Trust listed above (each, a “Fund” and collectively, the “Funds”) or other series of the Trust. Shares represent units of fractional undivided beneficial interest in and ownership of a series of the Trust. Each Fund’s Shares will be offered on a continuous basis. The Shares of each Fund are listed for trading on NYSE Arca, Inc. (the “Exchange”) under the ticker symbol shown above next to each Fund’s name. Please note that the Trust has series other than the Funds.

The ProShares VIX Short-Term Futures ETF (the “Matching Fund”) seeks investment results, before fees and expenses, that match the performance of the S&P 500® VIX Short-Term Futures Index (the “Index”). The ProShares Short VIX Short-Term Futures ETF (the “Short Fund”) seeks daily investment results, before fees and expenses, that correspond toone-half the inverse(-0.5x) of the performance of the Index for a single day, not for any other period. The ProShares Ultra VIX Short-Term Futures ETF (the “Ultra Fund”) seeks daily investment results, before fees and expenses, that correspond to one andone-half times (1.5x) the performance of the Index for a single day, not for any other period. The Short Fund and the Ultra Fund are sometimes referred to herein as the “Geared Funds.” A “single day” is measured from the time a Fund calculates its net asset value (“NAV”) to the time of the Fund’s next NAV calculation. The NAV calculation time for the Funds typically is 4:15 p.m. (Eastern Time). Please see the section entitled“Summary—Creation and Redemption Transactions” for additional details on the NAV calculation time for the Funds.

The Funds seek to achieve their respective investment objectives through the appropriate amount of exposure to the VIX futures contracts included in the Index. Each Fund also has the ability to engage in swap transactions, forward contracts and other instruments in order to achieve its investment objective, in the manner and to the extent described herein.

The Funds are not benchmarked to the widely referenced CBOE Volatility Index, commonly known as the “VIX.” The Index and the VIX are two separate indices and can be expected to perform very differently. As such, the Funds can be expected to perform very differently from the VIX or one andone-half times (1.5x) orone-half the inverse(-0.5x) of the performance of the VIX.

INVESTING IN THE SHARES INVOLVES SIGNIFICANT RISKS. PLEASE REFER TO “RISK FACTORS” BEGINNING ON PAGE 6.

Table of Contents

THE FUNDS PRESENT SIGNIFICANT RISKS NOT APPLICABLE TO OTHER TYPES OF FUNDS, INCLUDING RISKS RELATING TO INVESTING IN AND SEEKING EXPOSURE TO VIX FUTURES CONTRACTS. THE FUNDS ARE NOT APPROPRIATE FOR ALL INVESTORS. THE ULTRA FUND USES LEVERAGE AND IS RISKIER THAN SIMILARLY BENCHMARKED EXCHANGE-TRADED FUNDS THAT DO NOT USE LEVERAGE. AN INVESTOR SHOULD ONLY CONSIDER AN INVESTMENT IN A GEARED FUND IF HE OR SHE UNDERSTANDS THE CONSEQUENCES OF SEEKING DAILY INVESTMENT RESULTS AND THE IMPACT OF COMPOUNDING ON GEARED FUND PERFORMANCE.

THE RETURN OF EACH OF THE ULTRA FUND AND THE SHORT FUND FOR A PERIOD LONGER THAN A SINGLE DAY IS THE RESULT OF ITS RETURN FOR EACH DAY COMPOUNDED OVER THE PERIOD AND USUALLY WILL DIFFER IN AMOUNT AND POSSIBLY EVEN DIRECTION FROM THE FUND’S STATED MULTIPLE TIMES THE RETURN OF THE INDEX FOR THE SAME PERIOD. THESE DIFFERENCES CAN BE SIGNIFICANT.

THE FUNDS’ INVESTMENTS MAY BE ILLIQUID AND/OR HIGHLY VOLATILE AND THE FUNDS MAY EXPERIENCE LARGE LOSSES FROM BUYING, SELLING OR HOLDING SUCH INVESTMENTS. AN INVESTOR IN ANY OF THE FUNDS COULD POTENTIALLY LOSE THE FULL PRINCIPAL VALUE OF HIS/HER INVESTMENT WITHIN A SINGLE DAY.

THE FUNDS GENERALLY ARE INTENDED TO BE USED ONLY FOR SHORT-TERM TIME HORIZONS. SHAREHOLDERS WHO INVEST IN THE FUNDS SHOULD ACTIVELY MANAGE AND MONITOR THEIR INVESTMENTS, AS FREQUENTLY AS DAILY.

An investor should only consider an investment in a Fund if he or she understands the consequences of seeking exposure to VIX futures contracts. The Funds are benchmarked to the S&P 500 VIX Short-Term Futures Index; the Funds are not benchmarked to the VIX. The S&P 500 VIX Short-Term Futures Index and the VIX are two separate indices and can be expected to perform very differently.

The VIX is anon-investable index that measures the implied volatility of the S&P 500. For these purposes, “implied volatility” is a measure of the expected volatility (i.e., the rate and magnitude of variations in performance) of the S&P 500 over the next 30 days. The VIX does not represent the actual volatility of the S&P 500. The VIX is calculated based on the prices of a constantly changing portfolio of S&P 500 put and call options. The S&P 500 VIX Short-Term Futures Index, the Index used by each Fund, consists of short-term VIX futures contracts. As such, the performance of the S&P 500 VIX Short-Term Futures Index can be expected to be very different from the actual volatility of the S&P 500, or the performance of the VIX, or one andone-half times (1.5x) orone-half the inverse(-0.5x) of the actual volatility of the S&P 500 or the performance of the VIX.

Unlike certain other asset classes that, in general, have historically increased in price over long periods of time, the volatility of the S&P 500 as measured by the VIX has historically reverted to a long-term average level over time. This means that the potential upside of an investment in a Fund may be limited. In addition, gains, if any, may be subject to significant and unexpected reversals. The Funds generally are intended to be used only for short-term investment horizons. Investors holding Shares of the Funds beyond short-term periods have an increased risk of losing all or a substantial portion of their investment.

The Ultra Fund seeks daily investment results, before fees and expenses, that correspond to one andone-half times (1.5x) the performance of the Index for a single day, not for any other period. The Short Fund seeks daily investment results, before fees and expenses, that correspond toone-half the inverse(-0.5x) of the performance of the Index for a single day, not for any other period. The return of each of the Ultra Fund and the Short Fund for a period longer than a single day is the result of its return for each day compounded over the period and usually will differ in amount and possibly even direction from the Fund’s stated multiple times the return of the Index for the same period. These differences can be significant. Daily compounding of the investment returns of each of the Ultra Fund and the Short Fund can dramatically and adversely affect its longer-term performance, especially during periods of high volatility. Volatility has a negative impact on Geared Fund performance and the volatility of the Index may be at least as important to the returns of the Ultra Fund and the Short Fund as the return of the Index. The Ultra Fund uses leverage and should produce

Table of Contents

returns for a single day that are more volatile than that of the Index. For example, the return for a single day of the Ultra Fund with its 1.5x multiple should be approximately one andone-half times as volatile for a single day as the return of a fund with an objective of matching the same Index.

Each Fund will distribute to shareholders a ScheduleK-1 that will contain information regarding the income and expenses of the Fund.

NEITHER THE TRUST NOR ANY FUND IS A MUTUAL FUND OR ANY OTHER TYPE OF INVESTMENT COMPANY AS DEFINED IN THE INVESTMENT COMPANY ACT OF 1940, AS AMENDED (THE “1940 ACT”), AND NEITHER IS SUBJECT TO REGULATION THEREUNDER. SHAREHOLDERS DO NOT HAVE THE PROTECTIONS ASSOCIATED WITH OWNERSHIP OF SHARES IN AN INVESTMENT COMPANY REGISTERED UNDER THE 1940 ACT. SEE RISK FACTOR ENTITLED “SHAREHOLDERS DO NOT HAVE THE PROTECTIONS ASSOCIATED WITH OWNERSHIP OF SHARES IN AN INVESTMENT COMPANY REGISTERED UNDER THE INVESTMENT COMPANY ACT OF 1940, AS AMENDED (THE “1940 ACT”)” IN PART ONE OF THIS PROSPECTUS FOR MORE INFORMATION.

Each Fund continuously offers and redeems Shares in blocks of 50,000 Shares (25,000 Shares with respect to the Matching Fund only) (each such block, a “Creation Unit”). Only Authorized Participants (as defined herein) may purchase and redeem Shares from a Fund and then only in Creation Units. An Authorized Participant is an entity that has entered into an Authorized Participant Agreement with the Trust and ProShare Capital Management LLC (the “Sponsor”). Shares are offered to Authorized Participants in Creation Units at each Fund’s respective NAV. Authorized Participants may then offer to the public, from time to time, Shares from any Creation Unit they create at aper-Share market price. The form of Authorized Participant Agreement and the related Authorized Participant Procedures Handbook set forth the terms and conditions under which an Authorized Participant may purchase or redeem a Creation Unit. Authorized Participants will not receive from any Fund, the Sponsor, or any of their affiliates, any fee or other compensation in connection with their sale of Shares to the public. An Authorized Participant may receive commissions or fees from investors who purchase Shares through their commission orfee-based brokerage accounts.

These securities have not been approved or disapproved by the United States Securities and Exchange Commission (the “SEC”) or any state securities commission nor has the SEC or any state securities commission passed upon the accuracy or adequacy of this Prospectus. Any representation to the contrary is a criminal offense.

THE COMMODITY FUTURES TRADING COMMISSION HAS NOT PASSED UPON THE MERITS OF PARTICIPATING IN THIS POOL NOR HAS THE COMMISSION PASSED ON THE ADEQUACY OR ACCURACY OF THIS DISCLOSURE DOCUMENT.

March 29, 2019

Table of Contents

The Shares are neither interests in nor obligations of the Sponsor, Wilmington Trust Company, or any of their respective affiliates. The Shares are not insured by the Federal Deposit Insurance Corporation or any other governmental agency.

This Prospectus has two parts: the offered series disclosure and the general pool disclosure. These parts are bound together and are incomplete if not distributed together to prospective participants.

COMMODITY FUTURES TRADING COMMISSION

RISK DISCLOSURE STATEMENT

YOU SHOULD CAREFULLY CONSIDER WHETHER YOUR FINANCIAL CONDITION PERMITS YOU TO PARTICIPATE IN A COMMODITY POOL. IN SO DOING, YOU SHOULD BE AWARE THAT COMMODITY INTEREST TRADING CAN QUICKLY LEAD TO LARGE LOSSES AS WELL AS GAINS. SUCH TRADING LOSSES CAN SHARPLY REDUCE THE NET ASSET VALUE OF THE POOL AND CONSEQUENTLY THE VALUE OF YOUR INTEREST IN THE POOL. IN ADDITION, RESTRICTIONS ON REDEMPTIONS MAY AFFECT YOUR ABILITY TO WITHDRAW YOUR PARTICIPATION IN THE POOL.

FURTHER, COMMODITY POOLS MAY BE SUBJECT TO SUBSTANTIAL CHARGES FOR MANAGEMENT, AND ADVISORY AND BROKERAGE FEES. IT MAY BE NECESSARY FOR THOSE POOLS THAT ARE SUBJECT TO THESE CHARGES TO MAKE SUBSTANTIAL TRADING PROFITS TO AVOID DEPLETION OR EXHAUSTION OF THEIR ASSETS. THIS DISCLOSURE DOCUMENT CONTAINS A COMPLETE DESCRIPTION OF EACH EXPENSE TO BE CHARGED TO THIS POOL, AT PAGE 49, AND A STATEMENT OF THE PERCENTAGE RETURN NECESSARY TO BREAK EVEN, THAT IS, TO RECOVER THE AMOUNT OF YOUR INITIAL INVESTMENT, AT PAGE 48.

THIS BRIEF STATEMENT CANNOT DISCLOSE ALL THE RISKS AND OTHER FACTORS NECESSARY TO EVALUATE YOUR PARTICIPATION IN THIS COMMODITY POOL. THEREFORE, BEFORE YOU DECIDE TO PARTICIPATE IN THIS COMMODITY POOL, YOU SHOULD CAREFULLY STUDY THIS DISCLOSURE DOCUMENT, INCLUDING A DESCRIPTION OF THE PRINCIPAL RISK FACTORS OF THIS INVESTMENT, AT PAGES 6 THROUGH 31.

YOU SHOULD ALSO BE AWARE THAT THIS COMMODITY POOL MAY TRADE FOREIGN FUTURES OR OPTIONS CONTRACTS. TRANSACTIONS ON MARKETS LOCATED OUTSIDE THE UNITED STATES, INCLUDING MARKETS FORMALLY LINKED TO A UNITED STATES MARKET, MAY BE SUBJECT TO REGULATIONS WHICH OFFER DIFFERENT OR DIMINISHED PROTECTION TO THE POOL AND ITS PARTICIPANTS. FURTHER, UNITED STATES REGULATORY AUTHORITIES MAY BE UNABLE TO COMPEL THE ENFORCEMENT OF THE RULES OF REGULATORY AUTHORITIES OR MARKETS INNON-UNITED STATES JURISDICTIONS WHERE TRANSACTIONS FOR THE POOL MAY BE EFFECTED.

SWAPS TRANSACTIONS, LIKE OTHER FINANCIAL TRANSACTIONS, INVOLVE A VARIETY OF SIGNIFICANT RISKS. THE SPECIFIC RISKS PRESENTED BY A PARTICULAR SWAP TRANSACTION NECESSARILY DEPEND UPON THE TERMS OF THE TRANSACTION AND YOUR CIRCUMSTANCES. IN GENERAL, HOWEVER, ALL SWAPS TRANSACTIONS INVOLVE SOME COMBINATION OF MARKET RISK, CREDIT RISK, COUNTERPARTY CREDIT RISK, FUNDING RISK, LIQUIDITY RISK, AND OPERATIONAL RISK.

HIGHLY CUSTOMIZED SWAPS TRANSACTIONS IN PARTICULAR MAY INCREASE LIQUIDITY RISK, WHICH MAY RESULT IN A SUSPENSION OF REDEMPTIONS. HIGHLY LEVERAGED TRANSACTIONS MAY EXPERIENCE SUBSTANTIAL GAINS OR LOSSES IN VALUE AS A RESULT OF RELATIVELY SMALL CHANGES IN THE VALUE OR LEVEL OF AN UNDERLYING OR RELATED MARKET FACTOR. IN EVALUATING THE RISKS AND CONTRACTUAL OBLIGATIONS ASSOCIATED WITH A PARTICULAR SWAP TRANSACTION, IT IS IMPORTANT TO CONSIDER THAT A SWAP TRANSACTION MAY, IN CERTAIN INSTANCES, BE MODIFIED OR TERMINATED ONLY BY MUTUAL CONSENT OF THE ORIGINAL PARTIES AND SUBJECT TO AGREEMENT ON INDIVIDUALLY NEGOTIATED TERMS. THEREFORE, IT MAY NOT BE POSSIBLE FOR THE COMMODITY POOL OPERATOR TO MODIFY, TERMINATE, OR OFFSET THE POOL’S OBLIGATIONS OR THE POOL’S EXPOSURE TO THE RISKS ASSOCIATED WITH A TRANSACTION PRIOR TO ITS SCHEDULED TERMINATION DATE.

-i-

Table of Contents

THIS PROSPECTUS DOES NOT INCLUDE ALL OF THE INFORMATION OR EXHIBITS IN THE REGISTRATION STATEMENT OF THE TRUST. INVESTORS CAN READ AND COPY THE ENTIRE REGISTRATION STATEMENT AT THE PUBLIC REFERENCE FACILITIES MAINTAINED BY THE SEC IN WASHINGTON, D.C.

THE TRUST WILL FILE QUARTERLY AND ANNUAL REPORTS WITH THE SEC. INVESTORS CAN READ AND COPY THESE REPORTS AT THE SEC PUBLIC REFERENCE FACILITIES IN WASHINGTON, D.C. PLEASE CALL THE SEC AT1-800-SEC-0330 FOR FURTHER INFORMATION.

THE FILINGS OF THE TRUST ARE POSTED AT THE SEC WEBSITE ATWWW.SEC.GOV.

-ii-

Table of Contents

REGULATORY NOTICES

NO DEALER, SALESMAN OR ANY OTHER PERSON HAS BEEN AUTHORIZED TO GIVE ANY INFORMATION OR TO MAKE ANY REPRESENTATION NOT CONTAINED IN THIS PROSPECTUS, AND, IF GIVEN OR MADE, SUCH OTHER INFORMATION OR REPRESENTATION MUST NOT BE RELIED UPON AS HAVING BEEN AUTHORIZED BY THE TRUST, ANY OF THE FUNDS, THE SPONSOR, THE AUTHORIZED PARTICIPANTS OR ANY OTHER PERSON.

THIS PROSPECTUS DOES NOT CONSTITUTE AN OFFER OR SOLICITATION TO SELL OR A SOLICITATION OF AN OFFER TO BUY, NOR SHALL THERE BE ANY OFFER, SOLICITATION, OR SALE OF THE SHARES IN ANY JURISDICTION IN WHICH SUCH OFFER, SOLICITATION, OR SALE IS NOT AUTHORIZED OR TO ANY PERSON TO WHOM IT IS UNLAWFUL TO MAKE ANY SUCH OFFER, SOLICITATION, OR SALE.

AUTHORIZED PARTICIPANTS MAY BE REQUIRED TO DELIVER A PROSPECTUS WHEN TRANSACTING IN SHARES. SEE “PLAN OF DISTRIBUTION” IN PART TWO OF THIS PROSPECTUS.

-iii-

Table of Contents

PROSHARES TRUST II

| Page | ||||

| 1 | ||||

| 1 | ||||

| 2 | ||||

| 3 | ||||

| 4 | ||||

| 4 | ||||

| 5 | ||||

| 5 | ||||

| 6 | ||||

| 6 | ||||

| 15 | ||||

| 18 | ||||

| 31 | ||||

| 32 | ||||

| 32 | ||||

| 33 | ||||

| 35 | ||||

| 35 | ||||

| 36 | ||||

PERFORMANCE OF THE OFFERED COMMODITY POOLS OPERATED BY THE COMMODITY POOL OPERATOR | 43 | |||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 47 | |||

| 48 | ||||

| 48 | ||||

| 50 | ||||

| 51 | ||||

| 52 | ||||

PERFORMANCE OF THE OTHER COMMODITY POOLS OPERATED BY THE COMMODITY POOL OPERATOR | 62 | |||

| 84 | ||||

| 84 | ||||

| 84 | ||||

| 86 | ||||

-iv-

Table of Contents

| 87 | ||||

| 88 | ||||

| 88 | ||||

| 89 | ||||

DESCRIPTION OF THE SHARES; THE FUNDS; CERTAIN MATERIAL TERMS OF THE TRUST AGREEMENT | 89 | |||

| 89 | ||||

| 89 | ||||

| 90 | ||||

| 90 | ||||

| 91 | ||||

| 94 | ||||

| 95 | ||||

| 95 | ||||

| 95 | ||||

Possible Repayment of Distributions Received by Shareholders | 95 | |||

| 95 | ||||

| 95 | ||||

| 96 | ||||

| 96 | ||||

| 97 | ||||

| 97 | ||||

| 97 | ||||

| 97 | ||||

| 98 | ||||

| 98 | ||||

| 98 | ||||

| 98 | ||||

THE SECURITIES DEPOSITORY; BOOK-ENTRY ONLY SYSTEM; GLOBAL SECURITY | 98 | |||

| 99 | ||||

| 99 | ||||

| 99 | ||||

| 100 | ||||

| 101 | ||||

| 101 | ||||

| 101 | ||||

| 102 | ||||

| 102 | ||||

| 102 | ||||

| 102 | ||||

| 103 | ||||

| 103 | ||||

| 104 | ||||

| 104 |

-v-

Table of Contents

| 104 | ||||

| 104 | ||||

| 105 | ||||

| 105 | ||||

| 105 | ||||

| 105 | ||||

| 106 | ||||

| 107 | ||||

| 107 | ||||

| 107 | ||||

| 107 | ||||

| 107 | ||||

| 107 | ||||

| 108 | ||||

| 109 | ||||

| 136 | ||||

| 136 | ||||

Litigation and Regulatory Disclosure Relating to Swap Counterparties | 137 | |||

| A-1 |

-vi-

Table of Contents

Investors should read the following summary together with the more detailed information in this Prospectus before investing in Shares of any of the Funds, including the information under the caption “Risk Factors,” and all exhibits to this Prospectus and the information incorporated by reference in this Prospectus, including the financial statements and the notes to those financial statements in the Trust’s Annual Report on Form10-K, as amended, and the Quarterly Reports on Form10-Q, and Current Reports, if any, on Form8-K. Please see the section entitled “Incorporation by Reference of Certain Documents” in Part Two of this Prospectus.

For ease of reference, any references throughout this Prospectus to various actions taken by any or all of the Funds are actually actions taken by the Trust on behalf of such Funds.

Definitions used in this Prospectus can be found in the Glossary of Defined Terms in Appendix A and throughout this Prospectus.

Important Information About the Funds

THE FUNDS PRESENT SIGNIFICANT RISKS NOT APPLICABLE TO OTHER TYPES OF FUNDS, INCLUDING RISKS RELATING TO INVESTING IN VIX FUTURES CONTRACTS. THE FUNDS ARE NOT APPROPRIATE FOR ALL INVESTORS. THE ULTRA FUND USES LEVERAGE AND IS RISKIER THAN SIMILARLY BENCHMARKED EXCHANGE-TRADED FUNDS THAT DO NOT USE LEVERAGE. AN INVESTOR SHOULD ONLY CONSIDER AN INVESTMENT IN A GEARED FUND IF HE OR SHE UNDERSTANDS THE CONSEQUENCES OF SEEKING DAILY INVESTMENT RESULTS AND THE IMPACT OF COMPOUNDING ON GEARED FUND PERFORMANCE.

THE RETURN OF A GEARED FUND FOR A PERIOD LONGER THAN A SINGLE DAY IS THE RESULT OF ITS RETURN FOR EACH DAY COMPOUNDED OVER THE PERIOD AND USUALLY WILL DIFFER IN AMOUNT AND POSSIBLY EVEN DIRECTION FROM THE GEARED FUND’S STATED MULTIPLE TIMES THE RETURN OF THE INDEX FOR THE SAME PERIOD. THESE DIFFERENCES CAN BE SIGNIFICANT.

THE FUNDS’ INVESTMENTS MAY BE ILLIQUID AND/OR HIGHLY VOLATILE AND THE FUNDS MAY EXPERIENCE LARGE LOSSES FROM BUYING, SELLING OR HOLDING SUCH INVESTMENTS. AN INVESTOR IN ANY OF THE FUNDS COULD POTENTIALLY LOSE THE FULL PRINCIPAL VALUE OF HIS/HER INVESTMENT WITHIN A SINGLE DAY.

SHAREHOLDERS WHO INVEST IN THE FUNDS SHOULD ACTIVELY MANAGE AND MONITOR THEIR INVESTMENTS, AS FREQUENTLY AS DAILY.

All Funds

An investor should only consider an investment in a Fund if he or she understands the consequences of seeking exposure to VIX futures contracts. The Funds are benchmarked to the S&P 500 VIX Short-Term Futures Index; the Funds are not benchmarked to the VIX. The S&P 500 VIX Short-Term Futures Index and the VIX are two separate Indices and can be expected to perform very differently.

The VIX is anon-investable index that measures the implied volatility of the S&P 500. For these purposes, “implied volatility” is a measure of the expected volatility (i.e., the rate and magnitude of variations in performance) of the S&P 500 over the next 30 days. The VIX does not represent the actual volatility of the S&P 500. The VIX is calculated based on the prices of a constantly changing portfolio of S&P 500 put and call options. The S&P 500 VIX Short-Term Futures Index, the Index used by each Fund, consists of short-term VIX futures contracts. As such, the performance of the S&P 500 VIX Short-Term Futures Index, and therefore the performance of the Funds, can be expected to be very different from the actual volatility of the

-1-

Table of Contents

S&P 500 or the performance of the VIX. As a result, the performance of the Funds also can be expected to be very different from the actual volatility of the S&P 500, the performance of the VIX or one andone-half times (1.5x) orone-half the inverse(-0.5x) of the actual volatility of the S&P 500 or the performance of the VIX.

Unlike certain other asset classes that, in general, have historically increased in price over long periods of time, the volatility of the S&P 500 as measured by the VIX has historically reverted to a long-term average level over time. This means that the potential upside of an investment in a Fund may be limited. In addition, gains, if any, may be subject to significant and unexpected reversals. Investors holding Shares of the Funds beyond short-term periods have an increased risk of losing all or a substantial portion of their investment. The Funds generally are intended to be used only for short-term investment horizons. Shareholders who invest in the Funds should actively manage and monitor their investments, as frequently as daily.

Geared Funds

The Ultra Fund seeks daily investment results, before fees and expenses, that correspond to one andone-half times (1.5x) the performance of the Index for a single day, not for any other period. The Short Fund seeks daily investment results, before fees and expenses, that correspond toone-half the inverse(-0.5x) of the performance of the Index for a single day, not for any other period. The return of a Geared Fund for a period longer than a single day is the result of its return for each day compounded over the period and usually will differ in amount and possibly even direction from the Geared Fund’s stated multiple times the return of the Index for the same period. These differences can be significant. Daily compounding of a Geared Fund’s investment returns can dramatically and adversely affect its longer-term performance, especially during periods of high volatility. Volatility has a negative impact on Geared Fund performance and may be at least as important to a Geared Fund’s return for a period as the return of the Geared Fund’s underlying Index. The Ultra Fund uses leverage and should produce returns for a single day that are more volatile than that of the Index. For example, the return for a single day of the Ultra Fund with its 1.5x multiple should be approximately one andone-half times as volatile for a single day as the return of a fund with an objective of matching the same Index.

Fund Name | Index | |

| ProShares VIX Short-Term Futures ETF | S&P 500® VIX Short-Term Futures Index | |

| ProShares Ultra VIX Short-Term Futures ETF | S&P 500® VIX Short-Term Futures Index | |

| ProShares Short VIX Short-Term Futures ETF | S&P 500® VIX Short-Term Futures Index |

The Funds are benchmarked to the S&P 500 VIX Short-Term Futures Index (the “Index”), an investable index of VIX futures contracts. The Funds are not benchmarked to the VIX. The VIX is anon-investable index that measures the implied volatility of the S&P 500. The market’s current expectation of the possible rate and magnitude of movements in an index is commonly referred to as the “implied volatility” of the index. For these purposes, “implied volatility” is a measure of the expected volatility of the S&P 500 over the next 30 days. The VIX does not represent the actual or the realized volatility of the S&P 500. The VIX is calculated based on the prices of a constantly changing portfolio of S&P 500 put and call options. The Index consists of short-term VIX futures contracts.

THE PERFORMANCE OF THE INDEX AND THE FUNDS CAN BE EXPECTED TO BE VERY DIFFERENT FROM THE ACTUAL VOLATILITY OF THE S&P 500 OR THE PERFORMANCE OF THE VIX OR ONE ANDONE-HALF TIMES (1.5X) ORONE-HALF THE INVERSE(-0.5X) OF THE ACTUAL VOLATILITY OF THE S&P 500 OR THE PERFORMANCE OF THE VIX.

The Matching Fund

The Matching Fund seeks investment results, before fees and expenses, that over time, match the performance of the Index.

-2-

Table of Contents

The Ultra Fund

The Ultra Fund seeks daily investment results, before fees and expenses, that correspond to one andone-half times (1.5x) the performance of the Index for a single day, not for any other period. A “single day” is measured from the time the Fund calculates its NAV to the time of the Fund’s next NAV calculation. The NAV calculation time for the Funds typically is 4:15 p.m. (Eastern Time).

The Ultra Fund seeks to engage in daily rebalancing to position its portfolio so that its exposure to the Index is consistent with its daily investment objective. The impact of changes to the value of the Index each day will affect whether the Ultra Fund’s portfolio needs to be rebalanced. For example, if the level of the Index has risen on a given day, net assets of the Ultra Fund should rise. As a result, long exposure will need to be increased. Conversely, if the level of the Index has fallen on a given day, net assets of the Ultra Fund should fall. As a result, long exposure will need to be decreased. The time and manner in which the Ultra Fund rebalances its portfolio may vary from day to day depending upon market conditions and other circumstances at the discretion of the Sponsor.

DAILY REBALANCING AND THE COMPOUNDING OF EACH DAY’S RETURN OVER TIME MEANS THAT THE RETURN OF THE ULTRA FUND FOR A PERIOD LONGER THAN A SINGLE DAY WILL BE THE RESULT OF EACH DAY’S RETURNS COMPOUNDED OVER THE PERIOD, WHICH WILL VERY LIKELY DIFFER FROM ONE ANDONE-HALF TIMES (1.5X) THE RETURN OF THE INDEX FOR THE SAME PERIOD. THESE DIFFERENCES CAN BE SIGNIFICANT. THE ULTRA FUND WILL LOSE MONEY IF THE INDEX’S PERFORMANCE IS FLAT OVER TIME, AND THE FUND CAN LOSE MONEY REGARDLESS OF THE PERFORMANCE OF THE INDEX, AS A RESULT OF DAILY REBALANCING, THE INDEX’S VOLATILITY, COMPOUNDING AND OTHER FACTORS.

The Short Fund

The Short Fund seeks daily investment results, before fees and expenses, that correspond toone-half the inverse(-0.5x) of the performance of the Index for a single day, not for any other period. The Short Fund does not seek to achieve its stated objective over a period greater than a single day. A “single day” is measured from the time the Fund calculates its NAV to the time of the Fund’s next NAV calculation. The NAV calculation time for the Funds typically is 4:15 p.m. (Eastern Time). Please see the section entitled“Summary—Creation and Redemption Transactions” for additional details on the NAV calculation time for the Funds.

The Short Fund seeks to engage in daily rebalancing to position its portfolio so that its exposure to the Index is consistent with its daily investment objective. The impact of changes to the value of the Index each day will affect whether the Short Fund’s portfolio needs to be rebalanced. For example, if the level of the Index has risen on a given day, net assets of the Short Fund should fall. As a result, inverse exposure will need to be decreased. Conversely, if the level of the Index has fallen on a given day, net assets of the Short Fund should rise. As a result, inverse exposure will need to be increased. The time and manner in which the Short Fund rebalances its portfolio may vary from day to day depending upon market conditions and other circumstances at the discretion of the Sponsor.

DAILY REBALANCING AND THE COMPOUNDING OF EACH DAY’S RETURN OVER TIME MEANS THAT THE RETURN OF THE SHORT FUND FOR A PERIOD LONGER THAN A SINGLE DAY WILL BE THE RESULT OF EACH DAY’S RETURNS COMPOUNDED OVER THE PERIOD, WHICH WILL VERY LIKELY DIFFER FROMONE-HALF THE INVERSE(-0.5X) OF THE RETURN OF THE INDEX FOR THE SAME PERIOD. THESE DIFFERENCES CAN BE SIGNIFICANT. THE SHORT FUND WILL LOSE MONEY IF THE INDEX’S PERFORMANCE IS FLAT OVER TIME, AND THE FUND CAN LOSE MONEY REGARDLESS OF THE PERFORMANCE OF THE INDEX, AS A RESULT OF DAILY REBALANCING, THE INDEX’S VOLATILITY, COMPOUNDING AND OTHER FACTORS.

Each of the Funds intends to invest in Financial Instruments to gain the appropriate exposure to the Index in the manner and to the extent described herein. “Financial Instruments” are instruments whose value is derived from the value of an underlying asset, rate or benchmark (such asset, rate or benchmark, a “Reference Asset”) and include futures contracts, swap agreements, forward contracts and other instruments. The Funds will not directly invest in the VIX.

-3-

Table of Contents

In seeking to achieve the Funds’ investment objectives, the Sponsor uses a mathematical approach to investing. Using this approach, the Sponsor determines the type, quantity and mix of Financial Instruments that the Sponsor believes, in combination, should produce daily returns consistent with the Funds’ objectives.

The Funds are not actively managed by traditional methods (e.g., by effecting changes in the composition of a portfolio on the basis of judgments relating to economic, financial and market conditions with a view toward obtaining positive results under all market conditions). Each Fund seeks to remain fully invested at all times in Financial Instruments and money market instruments that, in combination, provide exposure to the Index consistent with its investment objective, even during periods in which the Index is flat or moving in a manner which causes the value of a Fund to decline.

The Sponsor has the power to change a Fund’s investment objective, benchmark or investment strategy, and may liquidate a Fund, at any time, without shareholder approval, subject to applicable regulatory requirements.

ProShare Capital Management LLC, a Maryland limited liability company, serves as the Trust’s Sponsor and commodity pool operator. The principal office of the Sponsor and the Funds is located at 7501 Wisconsin Avenue, East Tower, 10th Floor, Bethesda, Maryland 20814. The telephone number of the Sponsor and each of the Funds is(240) 497-6400.

Purchases and Sales in the Secondary Market

The Shares of each Fund are listed on NYSE Arca, Inc. (the “Exchange”) under the ticker symbols shown on the front cover of this Prospectus. Secondary market purchases and sales of Shares are subject to ordinary brokerage commissions and charges.

Creation and Redemption Transactions

Only an Authorized Participant may purchase (i.e., create) or redeem Shares with the Funds. Authorized Participants may create and redeem Shares only in blocks of 50,000 Shares (25,000 Shares with respect to the Matching Fund only) (each such block, a “Creation Unit”) in the Funds. An “Authorized Participant” is an entity that has entered into an Authorized Participant Agreement with the Trust and the Sponsor. Creation Units are offered to Authorized Participants at each Fund’s NAV. Creation Units in a Fund are expected to be created when there is sufficient demand for Shares in such Fund that the market price per Share is at a premium to the NAV per Share. Authorized Participants will likely sell such Shares to the public at prices that are expected to reflect, among other factors, the trading price of the Shares of such Fund and the supply of and demand for the Shares at the time of sale. Similarly, it is expected that Creation Units in a Fund will be redeemed when the market price per Share of such Fund is at a discount to the NAV per Share. The Sponsor expects that the exploitation of such arbitrage opportunities by Authorized Participants and their clients will tend to cause the public trading price of the Shares to track the NAV per Share of a Fund over time. Retail investors seeking to purchase or sell Shares on any day effect such transactions in the secondary market at the market price per Share, rather than in connection with the creation or redemption of Creation Units.

A creation transaction, which is subject to acceptance by SEI Investments Distribution Co. (“SEI” or the “Distributor”), generally takes place when an Authorized Participant deposits a specified amount of cash (unless as provided otherwise in this Prospectus) in exchange for a specified number of Creation Units. Similarly, Shares can be redeemed only in Creation Units, generally for cash (unless as provided otherwise in this Prospectus). Except when aggregated in Creation Units, Shares are not redeemable. The prices at which creations and redemptions occur are based on the next calculation of the NAV after an order is received in proper form, as described in the Authorized Participant Agreement and the related Authorized Participant Procedures Handbook. The manner by which Creation Units are purchased and redeemed is governed by the terms of this Prospectus, the Authorized Participant Agreement and Authorized Participant Procedures Handbook. Creation and redemption orders are not effective until accepted by the Distributor and may be rejected or revoked. By placing a purchase order, an Authorized Participant agrees to deposit cash (unless as provided otherwise in this Prospectus) with the Bank of New York Mellon (“BNYM”, the “Custodian”, the “Transfer Agent” and the “Administrator”), acting in its capacity as custodian of the Funds.

-4-

Table of Contents

Creation and redemption transactions must be placed each day with SEI by the create/redeemcut-off time (stated below) to receive that day’s NAV, or earlier if, for example, the Exchange or other exchange material to the valuation or operation of such Fund closes before suchcut-off time. See the section entitled“Net Asset Value” for additional information about NAV calculations.

Create/Redeem Cut-off | NAV Calculation Time | |

| 2:00 p.m. (Eastern Time) | 4:15 p.m. (Eastern Time) |

A Fund will be profitable only if returns from the Fund’s investments exceed its “breakeven amount.” Estimated breakeven amounts are set forth in the table below. The estimated breakeven amounts represent the estimated amount of trading income that each Fund would need to achieve during one year to offset the Fund’s estimated fees, costs and expenses, net of any interest income earned by the Fund on its investments. Estimated amounts do not represent actual results, which may be different. It is not possible to predict whether a Fund will break even at the end of the first twelve months of an investment or any other period. See“Charges—Breakeven Table,” beginning on page 48, for more detailed tables showing Breakeven Amounts.

Fund Name | Breakeven Amount (% Per Annum of Average Daily NAV)* | Assumed Selling Price Per Share* | Breakeven Amount ($ for the Assumed Selling Price Per Share)* | |||||||||

ProShares Ultra VIX Short-Term Futures ETF | 0.99 | % | $ | 45.00 | 0.45 | |||||||

ProShares Short VIX Short-Term Futures ETF | 0.06 | % | $ | 50.00 | 0.03 | |||||||

ProShares VIX Short-Term Futures ETF** | 0.00 | % | $ | 30.00 | 0.00 | |||||||

| * | The breakeven analysis set forth in this table assumes that the Shares have a constant NAV equal to the amount shown. The amount approximates the NAV of such Shares on February 28, 2019, rounded to the nearest $5. The actual NAV of each Fund differs and is likely to change on a daily basis. The numbers in this chart have been rounded to the nearest 0.01. |

| ** | Fees and expenses are less than the anticipated interest income; therefore, the net trading gains that would be necessary to offset such expenses would be zero. |

Please note that each Fund will distribute to shareholders a ScheduleK-1 that will contain information regarding the income and expense items of the Fund. The ScheduleK-1 is a complex form and shareholders may find that preparing tax returns may require additional time or may require the assistance of an accountant or other tax preparer, at an additional expense to the shareholder.

-5-

Table of Contents

The Funds may be highly volatile and generally are intended for short-term investment purposes only.

Investing in the Funds involves significant risks not applicable to other types of investments. You could potentially lose the full principal value of your investment within a single day. Before you decide to purchase any Shares, you should consider carefully the risks described below together with all of the other information included in this Prospectus, as well as information found in documents incorporated by reference in this Prospectus.

These risk factors may be amended, supplemented or superseded from time to time by risk factors contained in any periodic report, prospectus supplement, post-effective amendment or in other reports filed with the SEC in the future.

Risks Specific to the Geared Funds

In addition to the risks described elsewhere in this“Risk Factors” section, the following risks apply to the Geared Funds.

The use of leveraged positions increases risk and could result in the total loss of an investor’s investment within a single day.

The Ultra Fund utilizes leverage in seeking to achieve its investment objective and will lose more money in market environments adverse to its investment objective than funds that do not employ leverage. The more the Ultra Fund invests in leveraged positions, the more this leverage will magnify any losses on those investments. The Ultra Fund’s investments in these positions generally requires a small investment relative to the amount of investment exposure assumed. As a result, such investments may give rise to losses that exceed the amount invested in those instruments. The use of leveraged positions increases risk and could result in the total loss of an investor’s investment within a single day.

For example, because the Ultra Fund includes a one andone-half times (1.5x) multiplier, asingle-day movement in the Index approaching 66.7% at any point in the day could result in the total loss or almost total loss of an investor’s investment if that movement is contrary to the investment objective of the UltraFund, even if the Index subsequently moves in an opposite direction, eliminating all or a portion of the movement. This would be the case with downwardsingle-day or intraday movements in the Index, even if the Index maintains a level greater than zero at all times.

Due to the compounding of daily returns, a Geared Fund’s returns over periods longer than a single day will likely differ in amount and possibly even direction from the Fund’s stated multiple times the return of the Index for such period.

Each of the Geared Funds is “geared” which means that each has an investment objective to seek daily investment results, before fees and expenses, that correspond to one andone-half times (1.5x) orone-half the inverse(-0.5x) of the performance of the Index for a single day. Each Geared Fund seeks investment results for a single day only, as measured from NAV calculation time to NAV calculation time, and not for any other period (see“Summary—Creation and Redemption Transactions” for the typical NAV calculation time of each Fund). The return of a Geared Fund for a period longer than a single day is the result of its return for each day compounded over the period and usually will differ from one andone-half times (1.5x) orone-half the inverse(-0.5x) of the return of the Index for the same period. Compounding is the cumulative effect of applying investment gains and losses and income to the principal amount invested over time. Gains or losses experienced over a given period will increase or reduce the principal amount invested from which the subsequent period’s returns are calculated. The effects of compounding will likely cause the performance of a Geared Fund to differ from the Geared Fund’s stated multiple times the return of the Index for the same period. The effect of compounding becomes more pronounced as index volatility and holding period increase. The impact of compounding will impact each shareholder differently depending on the period of time an investment in a Geared Fund is held and the volatility of the index during the holding period of an investment in the Geared Fund.

A Geared Fund will lose money if the Index’s performance is flat over time, and a Geared Fund can lose money regardless of the performance of the Index, as a result of daily rebalancing, the Index’s volatility, compounding and other factors. Longer holding periods, higher index volatility, inverse exposure and greater leverage each affect the impact of compounding on a Geared Fund’s returns. Daily compounding of a Geared Fund’s investment returns can dramatically and adversely affect performance, especially during periods of high volatility. Volatility has a negative impact on Geared Fund performance and the volatility of the Index may be at least as important to a Geared Fund’s return for a period as the return of the Index.

-6-

Table of Contents

The Ultra Fund uses leverage and should produce daily returns that are more volatile than that of the Index. For example, the return for a single day of the Ultra Fund with its 1.5x multiple should be approximately one andone-half times as volatile for a single day as the return of a fund with an objective of matching the performance of the Index.

The Geared Funds are not appropriate for all investors and present significant risks not applicable to other types of funds. The Ultra Fund uses leverage and is riskier than similarly benchmarked exchange-traded funds that do not use leverage. An investor should only consider an investment in a Geared Fund if he or she understands the consequences of seeking leveraged or inverse investment results for a single day. Shareholders who invest in the Geared Funds should actively manage and monitor their investments, as frequently as daily.

The hypothetical examples below illustrate how daily geared fund returns can behave for periods longer than a single day. Each involves a hypothetical fund XYZ that seeks one andone-half times (1.5x) the daily performance of index XYZ, before fees and expenses. On each day, fund XYZ performs in line with its objective (one andone-half times (1.5x) the index’s daily performance before fees and expenses). Notice that, in the first example (showing an overall index loss for the period), over the entireseven-day period, the fund’s total return is more than one andone-half times the loss of the period return of the index. For theseven-day period, index XYZ lost 3.26% while fund XYZ lost-5.08% (versus-4.89% (or 1.5 x-3.26%)).

| Index XYZ | Fund XYZ | |||||||||||||||

| Level | Daily Performance | Daily Performance | Net Asset Value | |||||||||||||

Start | 100.00 | $ | 100.00 | |||||||||||||

Day 1 | 97.00 | -3.00 | % | -4.50 | % | $ | 95.50 | |||||||||

Day 2 | 99.91 | 3.00 | % | 4.50 | % | $ | 99.80 | |||||||||

Day 3 | 96.91 | -3.00 | % | -4.50 | % | $ | 95.31 | |||||||||

Day 4 | 99.82 | 3.00 | % | 4.50 | % | $ | 99.60 | |||||||||

Day 5 | 96.83 | -3.00 | % | -4.50 | % | $ | 95.11 | |||||||||

Day 6 | 99.73 | 3.00 | % | 4.50 | % | $ | 99.39 | |||||||||

Day 7 | 96.74 | -3.00 | % | -4.50 | % | $ | 94.92 | |||||||||

|

|

|

| |||||||||||||

Total Return | -3.26 | % | -5.08 | % | ||||||||||||

|

|

|

| |||||||||||||

Similarly, in another example (showing an overall index gain for the period), over the entireseven-day period, the fund’s total return is less than one andone-half times (1.5x) that of the period return of the index. For theseven-day period, index XYZ gained 2.72% while fund XYZ gained 3.87% (versus 4.08% (or 1.5 x 2.72%)).

| Index XYZ | Fund XYZ | |||||||||||||||

| Level | Daily Performance | Daily Performance | Net Asset Value | |||||||||||||

Start | 100.00 | $ | 100.00 | |||||||||||||

Day 1 | 103.00 | 3.00 | % | 4.50 | % | $ | 104.50 | |||||||||

Day 2 | 99.91 | -3.00 | % | -4.50 | % | $ | 99.80 | |||||||||

Day 3 | 102.91 | 3.00 | % | 4.50 | % | $ | 104.29 | |||||||||

Day 4 | 99.82 | -3.00 | % | -4.50 | % | $ | 99.60 | |||||||||

Day 5 | 102.81 | 3.00 | % | 4.50 | % | $ | 104.08 | |||||||||

Day 6 | 99.73 | -3.00 | % | -4.50 | % | $ | 99.39 | |||||||||

Day 7 | 102.72 | 3.00 | % | 4.50 | % | $ | 103.87 | |||||||||

|

|

|

| |||||||||||||

Total Return | 2.72 | % | 3.87 | % | ||||||||||||

|

|

|

| |||||||||||||

-7-

Table of Contents

These effects are caused by compounding, which exists in all investments, but has a more significant impact in geared funds. In general, during periods of higher Index volatility, compounding will cause the Ultra Fund’s returns for periods longer than a single day to be less than one andone-half times (1.5x) the return of the Index (or less thanone-half the inverse(-0.5x) of the return of the Index for the Short Fund). This effect becomes more pronounced as volatility increases. Conversely, in periods of lower Index volatility (particularly when combined with higher index returns), the Ultra Fund’s returns over longer periods can be greater than one andone-half times (1.5x) the return of the Index (or greater thanone-half the inverse(-0.5x) of the return of the Index for the Short Fund). Actual results for a particular period are also dependent on the magnitude of the Index return in addition to the Index volatility.

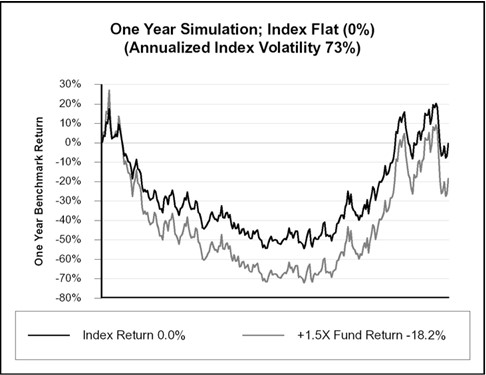

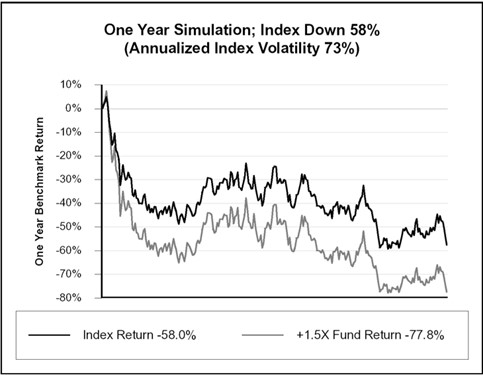

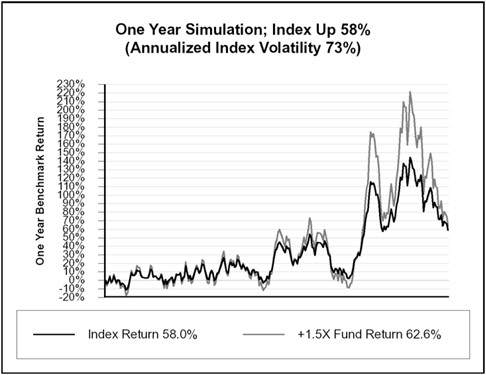

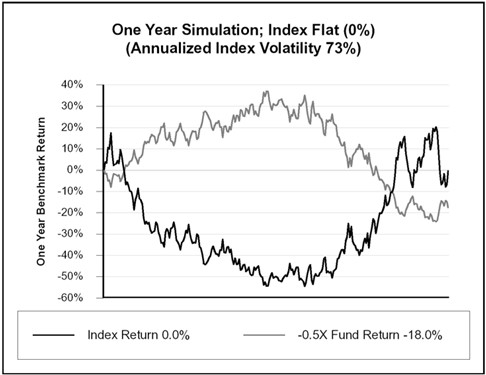

The graphs that follow illustrate this point. Each of the graphs shows a simulated hypotheticalone-year performance of an index compared with the performance of a geared fund that perfectly achieves its geared daily investment objective. The graphs demonstrate that, for periods greater than a single day, a geared fund is likely to underperform or overperform (but not match) the index performance (or the inverse of the index performance) times the multiple stated as the daily fund objective. Investors should understand the consequences of holding daily rebalanced funds for periods longer than a single day and should actively manage and monitor their investments, as frequently as daily. Aone-year period is used solely for illustrative purposes. Deviations from the index return (or the inverse of the index return) times the fund multiple can occur over periods as short as two days (each day as measured from NAV to NAV) and may also occur in periods of a single day or evenintra-day. To isolate the impact of daily leveraged exposure, these graphs assume: a) no fund expenses or transaction costs; b) borrowing/lending rates (to obtain required leveraged or inverse exposure) and cash reinvestment rates of zero percent; and c) the fund consistently maintaining perfect exposure (1.5x or-0.5x) as of the fund’s NAV time each day. If these assumptions were different, the fund’s performance would be different than that shown. If fund expenses, transaction costs and financing expenses greater than zero percent were included, the fund’s performance would also be different than shown. Each of the graphs also assumes a volatility rate of 73%, which is an approximate average of the five-year historical volatility rate of the Index as of December 31, 2018. An index’s volatility rate is a statistical measure of the magnitude of fluctuations in its returns.

HYPOTHETICAL PERFORMANCE RESULTS HAVE MANY INHERENT LIMITATIONS. NO REPRESENTATION IS BEING MADE THAT ANY INDEX OR FUND WILL OR IS LIKELY TO ACHIEVE GAINS OR LOSSES SIMILAR TO THOSE SHOWN OR WILL EXPERIENCE VOLATILITY SIMILAR TO THAT SHOWN. THE INFORMATION PROVIDED IN THE CHARTS BELOW IS FOR ILLUSTRATIVE PURPOSES ONLY.

-8-

Table of Contents

The graph above shows a scenario where the index, which exhibitsday-to-day volatility, is flat or trendless over the year (i.e., begins and ends the year at 0%), but the Ultra Fund (1.5x) is down.

The graph above shows a scenario where the index, which exhibitsday-to-day volatility, is down over the year, but the Ultra Fund (1.5x) is down less than one andone-half times the index.

-9-

Table of Contents

The graph above shows a scenario where the index, which exhibitsday-to-day volatility, is up over the year, but the Ultra Fund (1.5x) is up less than one andone-half times the index.

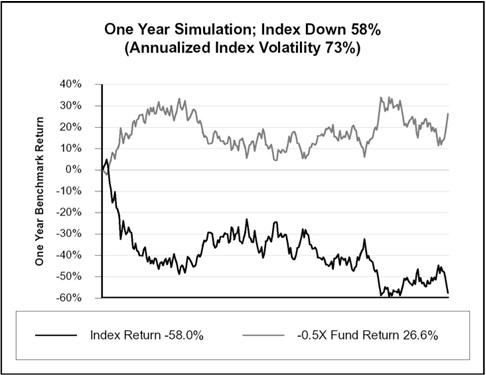

The graph above shows a scenario where the index, which exhibitsday-to-day volatility, is flat or trendless over the year (i.e., begins and ends the year at 0%), but the Short Fund(-0.5x) is down.

-10-

Table of Contents

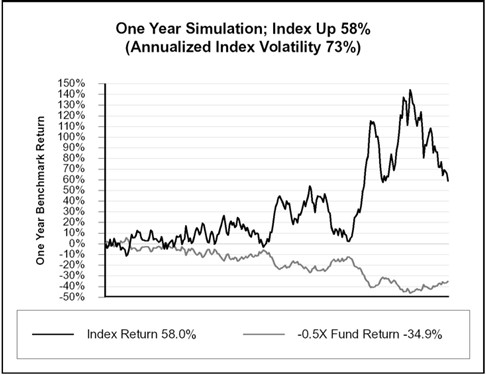

The graph above shows a scenario where the index, which exhibitsday-to-day volatility, is down over the year, but the Short Fund(-0.5x) is up less thanone-half the inverse of the index.

The graph above shows a scenario where the index, which exhibitsday-to-day volatility, is up over the year, but the Short Fund(-0.5x) is down more thanone-half the inverse of the index.

The historical five year average volatility of the Index was approximately 73% as of December 31, 2018.

Historical average volatility does not predict future volatility, which may be higher or lower than historical averages.

-11-

Table of Contents

Fund performance for periods greater than a single day can be estimated given any set of assumptions for the following factors: a) benchmark volatility; b) benchmark performance; c) period of time; d) financing rates associated with leveraged exposure; and e) other Fund expenses. The tables below illustrate the impact of two factors that affect a geared fund’s performance, index volatility and index return. Index volatility is a statistical measure of the magnitude of fluctuations in the returns of an index and is calculated as the standard deviation of the natural logarithms of one plus the index return (calculated daily), multiplied by the square root of the number of trading days per year (assumed to be 252). The table shows estimated fund returns for a number of combinations of index volatility and index return over aone-year period. To isolate the impact of daily leveraged orone-half inverse exposure, the graphs assume: a) no fund expenses or transaction costs; b) borrowing/lending rates of zero percent (to obtain required leveraged or inverse exposure) and cash reinvestment rates of zero percent; and c) the fund consistently maintaining perfect exposure (1.5x or-0.5x) as of the fund’s NAV time each day. If these assumptions were different, the fund’s performance would be different than that shown. If fund expenses, transaction costs and financing expenses were included, the fund’s performance would be different than shown. The first table below shows an example in which a geared fund has an investment objective to correspond (before fees and expenses) to one andone-half times (1.5x) the daily performance of an index. The geared fund could incorrectly be expected to achieve a 15% return on a yearly basis if the index return was 10%, absent the effects of compounding. However, as the table shows, with an index volatility of 40%, such a fund would return 8.7%. In the charts below, shaded areas represent those scenarios where a geared fund with the investment objective described will outperform (i.e., return more than) the index performance times the stated multiple in the fund’s investment objective; conversely, areas not shaded represent those scenarios where the fund will underperform (i.e., return less than) the index performance times the multiple stated as the daily fund objective.

-12-

Table of Contents

Estimated Fund Return Over One Year When the Fund’s Objective is to Seek Daily Investment Results, Before Fees and Expenses, that Correspond to One andOne-Half Times (1.5x) the Performance of an Index For a Single Day.

One Year Index Performance | One and One-Half Times (1.5x) One Year Index Performance | Index Volatility | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 0% | 5% | 10% | 15% | 20% | 25% | 30% | 35% | 40% | 45% | 50% | 55% | 60% | 65% | 70% | 75% | |||||||||||||||||||||||||||||||||||||||||||||||||||||

-60% | -90.0 | % | -74.7 | % | -74.7 | % | -74.8 | % | -74.9 | % | -75.1 | % | -75.3 | % | -75.5 | % | -75.8 | % | -76.2 | % | -76.6 | % | -77.0 | % | -77.4 | % | -77.9 | % | -78.4 | % | -78.9 | % | -79.5 | % | ||||||||||||||||||||||||||||||||||

-55% | -82.5 | % | -69.8 | % | -69.8 | % | -69.9 | % | -70.1 | % | -70.3 | % | -70.5 | % | -70.8 | % | -71.2 | % | -71.6 | % | -72.0 | % | -72.5 | % | -73.1 | % | -73.6 | % | -74.2 | % | -74.9 | % | -75.6 | % | ||||||||||||||||||||||||||||||||||

-50% | -75.0 | % | -64.6 | % | -64.7 | % | -64.8 | % | -64.9 | % | -65.2 | % | -65.5 | % | -65.8 | % | -66.2 | % | -66.7 | % | -67.2 | % | -67.8 | % | -68.4 | % | -69.1 | % | -69.8 | % | -70.6 | % | -71.4 | % | ||||||||||||||||||||||||||||||||||

-45% | -67.5 | % | -59.2 | % | -59.2 | % | -59.4 | % | -59.6 | % | -59.8 | % | -60.2 | % | -60.6 | % | -61.0 | % | -61.6 | % | -62.2 | % | -62.9 | % | -63.6 | % | -64.4 | % | -65.2 | % | -66.1 | % | -67.0 | % | ||||||||||||||||||||||||||||||||||

-40% | -60.0 | % | -53.5 | % | -53.6 | % | -53.7 | % | -53.9 | % | -54.2 | % | -54.6 | % | -55.1 | % | -55.6 | % | -56.2 | % | -56.9 | % | -57.7 | % | -58.5 | % | -59.4 | % | -60.3 | % | -61.3 | % | -62.4 | % | ||||||||||||||||||||||||||||||||||

-35% | -52.5 | % | -47.6 | % | -47.6 | % | -47.8 | % | -48.0 | % | -48.4 | % | -48.8 | % | -49.3 | % | -49.9 | % | -50.6 | % | -51.4 | % | -52.3 | % | -53.2 | % | -54.2 | % | -55.3 | % | -56.4 | % | -57.6 | % | ||||||||||||||||||||||||||||||||||

-30% | -45.0 | % | -41.4 | % | -41.5 | % | -41.7 | % | -41.9 | % | -42.3 | % | -42.8 | % | -43.4 | % | -44.1 | % | -44.8 | % | -45.7 | % | -46.7 | % | -47.7 | % | -48.8 | % | -50.0 | % | -51.3 | % | -52.6 | % | ||||||||||||||||||||||||||||||||||

-25% | -37.5 | % | -35.0 | % | -35.1 | % | -35.3 | % | -35.6 | % | -36.0 | % | -36.6 | % | -37.2 | % | -38.0 | % | -38.8 | % | -39.8 | % | -40.9 | % | -42.0 | % | -43.3 | % | -44.6 | % | -46.0 | % | -47.4 | % | ||||||||||||||||||||||||||||||||||

-20% | -30.0 | % | -28.4 | % | -28.5 | % | -28.7 | % | -29.0 | % | -29.5 | % | -30.1 | % | -30.8 | % | -31.7 | % | -32.6 | % | -33.7 | % | -34.8 | % | -36.1 | % | -37.5 | % | -38.9 | % | -40.5 | % | -42.1 | % | ||||||||||||||||||||||||||||||||||

-15% | -22.5 | % | -21.6 | % | -21.7 | % | -21.9 | % | -22.3 | % | -22.8 | % | -23.4 | % | -24.2 | % | -25.2 | % | -26.2 | % | -27.4 | % | -28.6 | % | -30.0 | % | -31.5 | % | -33.1 | % | -34.8 | % | -36.5 | % | ||||||||||||||||||||||||||||||||||

-10% | -15.0 | % | -14.6 | % | -14.7 | % | -14.9 | % | -15.3 | % | -15.9 | % | -16.6 | % | -17.5 | % | -18.5 | % | -19.6 | % | -20.9 | % | -22.3 | % | -23.8 | % | -25.4 | % | -27.1 | % | -29.0 | % | -30.9 | % | ||||||||||||||||||||||||||||||||||

-5% | -7.5 | % | -7.4 | % | -7.5 | % | -7.8 | % | -8.2 | % | -8.8 | % | -9.6 | % | -10.5 | % | -11.6 | % | -12.8 | % | -14.2 | % | -15.7 | % | -17.3 | % | -19.1 | % | -21.0 | % | -22.9 | % | -25.0 | % | ||||||||||||||||||||||||||||||||||

0% | 0.0 | % | 0.0 | % | -0.1 | % | -0.4 | % | -0.8 | % | -1.5 | % | -2.3 | % | -3.3 | % | -4.5 | % | -5.8 | % | -7.3 | % | -8.9 | % | -10.7 | % | -12.6 | % | -14.7 | % | -16.8 | % | -19.0 | % | ||||||||||||||||||||||||||||||||||

5% | 7.5 | % | 7.6 | % | 7.5 | % | 7.2 | % | 6.7 | % | 6.0 | % | 5.1 | % | 4.0 | % | 2.8 | % | 1.3 | % | -0.3 | % | -2.0 | % | -3.9 | % | -6.0 | % | -8.2 | % | -10.5 | % | -12.9 | % | ||||||||||||||||||||||||||||||||||

10% | 15.0 | % | 15.4 | % | 15.3 | % | 14.9 | % | 14.4 | % | 13.7 | % | 12.7 | % | 11.5 | % | 10.2 | % | 8.7 | % | 6.9 | % | 5.0 | % | 3.0 | % | 0.8 | % | -1.5 | % | -4.0 | % | -6.6 | % | ||||||||||||||||||||||||||||||||||

15% | 22.5 | % | 23.3 | % | 23.2 | % | 22.9 | % | 22.3 | % | 21.5 | % | 20.5 | % | 19.2 | % | 17.8 | % | 16.1 | % | 14.3 | % | 12.3 | % | 10.1 | % | 7.7 | % | 5.3 | % | 2.6 | % | -0.1 | % | ||||||||||||||||||||||||||||||||||

20% | 30.0 | % | 31.5 | % | 31.3 | % | 31.0 | % | 30.3 | % | 29.5 | % | 28.4 | % | 27.1 | % | 25.6 | % | 23.8 | % | 21.8 | % | 19.7 | % | 17.4 | % | 14.9 | % | 12.2 | % | 9.4 | % | 6.5 | % | ||||||||||||||||||||||||||||||||||

25% | 37.5 | % | 39.8 | % | 39.6 | % | 39.2 | % | 38.6 | % | 37.7 | % | 36.5 | % | 35.1 | % | 33.5 | % | 31.6 | % | 29.5 | % | 27.2 | % | 24.8 | % | 22.1 | % | 19.3 | % | 16.3 | % | 13.2 | % | ||||||||||||||||||||||||||||||||||

30% | 45.0 | % | 48.2 | % | 48.1 | % | 47.7 | % | 47.0 | % | 46.0 | % | 44.8 | % | 43.3 | % | 41.6 | % | 39.6 | % | 37.4 | % | 35.0 | % | 32.3 | % | 29.5 | % | 26.5 | % | 23.3 | % | 20.0 | % | ||||||||||||||||||||||||||||||||||

35% | 52.5 | % | 56.9 | % | 56.7 | % | 56.3 | % | 55.5 | % | 54.5 | % | 53.2 | % | 51.7 | % | 49.8 | % | 47.7 | % | 45.4 | % | 42.8 | % | 40.0 | % | 37.0 | % | 33.9 | % | 30.5 | % | 27.0 | % | ||||||||||||||||||||||||||||||||||

40% | 60.0 | % | 65.7 | % | 65.5 | % | 65.0 | % | 64.3 | % | 63.2 | % | 61.8 | % | 60.2 | % | 58.2 | % | 56.0 | % | 53.5 | % | 50.8 | % | 47.9 | % | 44.7 | % | 41.4 | % | 37.8 | % | 34.1 | % | ||||||||||||||||||||||||||||||||||

45% | 67.5 | % | 74.6 | % | 74.4 | % | 73.9 | % | 73.1 | % | 72.0 | % | 70.6 | % | 68.8 | % | 66.8 | % | 64.4 | % | 61.8 | % | 59.0 | % | 55.9 | % | 52.6 | % | 49.0 | % | 45.3 | % | 41.4 | % | ||||||||||||||||||||||||||||||||||

50% | 75.0 | % | 83.7 | % | 83.5 | % | 83.0 | % | 82.2 | % | 81.0 | % | 79.5 | % | 77.6 | % | 75.5 | % | 73.0 | % | 70.3 | % | 67.3 | % | 64.0 | % | 60.5 | % | 56.8 | % | 52.9 | % | 48.8 | % | ||||||||||||||||||||||||||||||||||

55% | 82.5 | % | 93.0 | % | 92.8 | % | 92.3 | % | 91.4 | % | 90.1 | % | 88.5 | % | 86.6 | % | 84.3 | % | 81.7 | % | 78.9 | % | 75.7 | % | 72.3 | % | 68.6 | % | 64.7 | % | 60.6 | % | 56.3 | % | ||||||||||||||||||||||||||||||||||

60% | 90.0 | % | 102.4 | % | 102.2 | % | 101.6 | % | 100.7 | % | 99.4 | % | 97.7 | % | 95.7 | % | 93.3 | % | 90.6 | % | 87.6 | % | 84.3 | % | 80.7 | % | 76.8 | % | 72.7 | % | 68.4 | % | 63.9 | % | ||||||||||||||||||||||||||||||||||

-13-

Table of Contents

Estimated Fund Return Over One Year When the Fund’s Objective is to Seek Daily Investment Results, Before Fees and Expenses, that Correspond toOne-Half the Inverse(-0.5x) of the Performance of an Index For a Single Day.

One Year Index Performance | One-Half the Invers (-0.5x) One Year Index Performance | Index Volatility | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 0% | 5% | 10% | 15% | 20% | 25% | 30% | 35% | 40% | 45% | 50% | 55% | 60% | 65% | 70% | 75% | |||||||||||||||||||||||||||||||||||||||||||||||||||||

-60% | 30.0 | % | 58.1 | % | 58.0 | % | 57.5 | % | 56.8 | % | 55.8 | % | 54.5 | % | 52.9 | % | 51.0 | % | 48.9 | % | 46.6 | % | 44.0 | % | 41.2 | % | 38.1 | % | 34.9 | % | 31.6 | % | 28.0 | % | ||||||||||||||||||||||||||||||||||

-55% | 27.5 | % | 49.1 | % | 48.9 | % | 48.5 | % | 47.8 | % | 46.9 | % | 45.6 | % | 44.1 | % | 42.4 | % | 40.4 | % | 38.2 | % | 35.7 | % | 33.1 | % | 30.2 | % | 27.2 | % | 24.0 | % | 20.7 | % | ||||||||||||||||||||||||||||||||||

-50% | 25.0 | % | 41.4 | % | 41.3 | % | 40.9 | % | 40.2 | % | 39.3 | % | 38.1 | % | 36.7 | % | 35.1 | % | 33.2 | % | 31.1 | % | 28.8 | % | 26.3 | % | 23.6 | % | 20.7 | % | 17.7 | % | 14.5 | % | ||||||||||||||||||||||||||||||||||

-45% | 22.5 | % | 34.8 | % | 34.7 | % | 34.3 | % | 33.7 | % | 32.8 | % | 31.7 | % | 30.4 | % | 28.8 | % | 27.0 | % | 25.0 | % | 22.8 | % | 20.4 | % | 17.8 | % | 15.1 | % | 12.2 | % | 9.2 | % | ||||||||||||||||||||||||||||||||||

-40% | 20.0 | % | 29.1 | % | 29.0 | % | 28.6 | % | 28.0 | % | 27.2 | % | 26.1 | % | 24.8 | % | 23.3 | % | 21.6 | % | 19.7 | % | 17.5 | % | 15.3 | % | 12.8 | % | 10.2 | % | 7.4 | % | 4.5 | % | ||||||||||||||||||||||||||||||||||

-35% | 17.5 | % | 24.0 | % | 23.9 | % | 23.6 | % | 23.0 | % | 22.2 | % | 21.2 | % | 19.9 | % | 18.5 | % | 16.8 | % | 15.0 | % | 12.9 | % | 10.7 | % | 8.4 | % | 5.9 | % | 3.2 | % | 0.4 | % | ||||||||||||||||||||||||||||||||||

-30% | 15.0 | % | 19.5 | % | 19.4 | % | 19.1 | % | 18.5 | % | 17.7 | % | 16.8 | % | 15.6 | % | 14.2 | % | 12.6 | % | 10.8 | % | 8.8 | % | 6.7 | % | 4.4 | % | 2.0 | % | -0.5 | % | -3.2 | % | ||||||||||||||||||||||||||||||||||

-25% | 12.5 | % | 15.5 | % | 15.4 | % | 15.0 | % | 14.5 | % | 13.8 | % | 12.8 | % | 11.6 | % | 10.3 | % | 8.7 | % | 7.0 | % | 5.1 | % | 3.1 | % | 0.9 | % | -1.4 | % | -3.9 | % | -6.5 | % | ||||||||||||||||||||||||||||||||||

-20% | 10.0 | % | 11.8 | % | 11.7 | % | 11.4 | % | 10.9 | % | 10.1 | % | 9.2 | % | 8.1 | % | 6.8 | % | 5.3 | % | 3.6 | % | 1.8 | % | -0.2 | % | -2.3 | % | -4.6 | % | -7.0 | % | -9.5 | % | ||||||||||||||||||||||||||||||||||

-15% | 7.5 | % | 8.5 | % | 8.4 | % | 8.1 | % | 7.6 | % | 6.9 | % | 6.0 | % | 4.9 | % | 3.6 | % | 2.1 | % | 0.5 | % | -1.2 | % | -3.2 | % | -5.2 | % | -7.4 | % | -9.7 | % | -12.2 | % | ||||||||||||||||||||||||||||||||||

-10% | 5.0 | % | 5.4 | % | 5.3 | % | 5.0 | % | 4.5 | % | 3.8 | % | 3.0 | % | 1.9 | % | 0.7 | % | -0.7 | % | -2.3 | % | -4.0 | % | -5.9 | % | -7.9 | % | -10.0 | % | -12.3 | % | -14.6 | % | ||||||||||||||||||||||||||||||||||

-5% | 2.5 | % | 2.6 | % | 2.5 | % | 2.2 | % | 1.7 | % | 1.1 | % | 0.2 | % | -0.8 | % | -2.0 | % | -3.4 | % | -4.9 | % | -6.6 | % | -8.4 | % | -10.4 | % | -12.4 | % | -14.6 | % | -16.9 | % | ||||||||||||||||||||||||||||||||||

0% | 0.0 | % | 0.0 | % | -0.1 | % | -0.4 | % | -0.8 | % | -1.5 | % | -2.3 | % | -3.3 | % | -4.5 | % | -5.8 | % | -7.3 | % | -8.9 | % | -10.7 | % | -12.6 | % | -14.7 | % | -16.8 | % | -19.0 | % | ||||||||||||||||||||||||||||||||||

5% | -2.5 | % | -2.4 | % | -2.5 | % | -2.8 | % | -3.2 | % | -3.9 | % | -4.7 | % | -5.6 | % | -6.8 | % | -8.1 | % | -9.5 | % | -11.1 | % | -12.9 | % | -14.7 | % | -16.7 | % | -18.8 | % | -21.0 | % | ||||||||||||||||||||||||||||||||||

10% | -5.0 | % | -4.7 | % | -4.7 | % | -5.0 | % | -5.5 | % | -6.1 | % | -6.9 | % | -7.8 | % | -8.9 | % | -10.2 | % | -11.6 | % | -13.2 | % | -14.9 | % | -16.7 | % | -18.6 | % | -20.7 | % | -22.8 | % | ||||||||||||||||||||||||||||||||||

15% | -7.5 | % | -6.7 | % | -6.8 | % | -7.1 | % | -7.5 | % | -8.1 | % | -8.9 | % | -9.8 | % | -10.9 | % | -12.2 | % | -13.6 | % | -15.1 | % | -16.7 | % | -18.5 | % | -20.4 | % | -22.4 | % | -24.5 | % | ||||||||||||||||||||||||||||||||||

20% | -10.0 | % | -8.7 | % | -8.8 | % | -9.1 | % | -9.5 | % | -10.1 | % | -10.8 | % | -11.7 | % | -12.8 | % | -14.0 | % | -15.4 | % | -16.9 | % | -18.5 | % | -20.2 | % | -22.1 | % | -24.0 | % | -26.1 | % | ||||||||||||||||||||||||||||||||||

25% | -12.5 | % | -10.6 | % | -10.6 | % | -10.9 | % | -11.3 | % | -11.9 | % | -12.6 | % | -13.5 | % | -14.6 | % | -15.8 | % | -17.1 | % | -18.6 | % | -20.1 | % | -21.9 | % | -23.7 | % | -25.6 | % | -27.6 | % | ||||||||||||||||||||||||||||||||||

30% | -15.0 | % | -12.3 | % | -12.4 | % | -12.6 | % | -13.0 | % | -13.6 | % | -14.3 | % | -15.2 | % | -16.2 | % | -17.4 | % | -18.7 | % | -20.1 | % | -21.7 | % | -23.4 | % | -25.1 | % | -27.0 | % | -29.0 | % | ||||||||||||||||||||||||||||||||||

35% | -17.5 | % | -13.9 | % | -14.0 | % | -14.3 | % | -14.7 | % | -15.2 | % | -15.9 | % | -16.8 | % | -17.8 | % | -18.9 | % | -20.2 | % | -21.6 | % | -23.2 | % | -24.8 | % | -26.5 | % | -28.4 | % | -30.3 | % | ||||||||||||||||||||||||||||||||||

40% | -20.0 | % | -15.5 | % | -15.6 | % | -15.8 | % | -16.2 | % | -16.7 | % | -17.4 | % | -18.3 | % | -19.3 | % | -20.4 | % | -21.7 | % | -23.0 | % | -24.5 | % | -26.2 | % | -27.9 | % | -29.7 | % | -31.6 | % | ||||||||||||||||||||||||||||||||||

45% | -22.5 | % | -17.0 | % | -17.0 | % | -17.3 | % | -17.7 | % | -18.2 | % | -18.9 | % | -19.7 | % | -20.7 | % | -21.8 | % | -23.0 | % | -24.4 | % | -25.9 | % | -27.4 | % | -29.1 | % | -30.9 | % | -32.7 | % | ||||||||||||||||||||||||||||||||||

50% | -25.0 | % | -18.4 | % | -18.4 | % | -18.7 | % | -19.0 | % | -19.6 | % | -20.2 | % | -21.1 | % | -22.0 | % | -23.1 | % | -24.3 | % | -25.7 | % | -27.1 | % | -28.7 | % | -30.3 | % | -32.1 | % | -33.9 | % | ||||||||||||||||||||||||||||||||||

55% | -27.5 | % | -19.7 | % | -19.8 | % | -20.0 | % | -20.4 | % | -20.9 | % | -21.5 | % | -22.3 | % | -23.3 | % | -24.4 | % | -25.6 | % | -26.9 | % | -28.3 | % | -29.8 | % | -31.4 | % | -33.2 | % | -35.0 | % | ||||||||||||||||||||||||||||||||||

60% | -30.0 | % | -20.9 | % | -21.0 | % | -21.2 | % | -21.6 | % | -22.1 | % | -22.8 | % | -23.6 | % | -24.5 | % | -25.5 | % | -26.7 | % | -28.0 | % | -29.4 | % | -30.9 | % | -32.5 | % | -34.2 | % | -36.0 | % | ||||||||||||||||||||||||||||||||||

-14-

Table of Contents

The foregoing tables are intended to isolate the effect of index volatility and index performance on the return of leveraged or inverse funds. The Geared Funds’ actual returns may be greater or less than the returns shown above.

Correlation Risks Specific to the Geared Funds.

In order to achieve a high degree of correlation with the Index, each Geared Fund seeks to rebalance its portfolio daily to keep exposure consistent with its investment objective. Being materially under or overexposed to the Index may prevent a Geared Fund from achieving a high degree of correlation with the Index. Market disruptions or closures, large movements of assets into or out of a Geared Fund, regulatory restrictions, market volatility, accountability levels, position limits, and daily price fluctuation limits set by the exchanges and other factors will adversely affect a Geared Fund’s ability to adjust exposure to requisite levels. The target amount of portfolio exposure may be impacted by changes to the value of the Index each day. Other things being equal, more significant movement, up or down, will require more significant adjustments to a Fund’s portfolio. Because of this, it is unlikely that a Geared Fund will be perfectly exposed (i.e., 1.5x or-0.5x, as applicable) at the end of each day, and the likelihood of being materially under- or overexposed is higher on days when the index levels are volatile at or near the close of the trading day. These risks are particularly acute for the Geared Funds due to the high degree of volatility in VIX futures contracts.

Each Geared Fund seeks to rebalance its portfolio on a daily basis. The time and manner in which a Geared Fund rebalances its portfolio may vary from day to day at the discretion of the Sponsor depending upon market conditions and other circumstances. Unlike other funds that do not rebalance their portfolios as frequently, the Geared Funds may be subject to increased trading costs associated with daily portfolio rebalancings. The effects of these trading costs have been estimated and included in the Breakeven Table. See“Charges—Breakeven Table” below.

For general correlation risks applicable to each Fund, including the Matching Fund, please see the risk factor herein entitled “Several factors may affect a Fund’s ability to closely track the Index on a consistent basis.”

Changes to the Index and the Daily Rebalancing of the Geared Funds May Impact Trading in the Underlying Futures Contracts

Changes to the Index and daily rebalancing may cause the Geared Funds to adjust their portfolio positions. This trading activity will contribute to the trading volume of the underlying futures contracts and may adversely affect the market price of such underlying futures contracts.

Intraday Price/Performance Risk.

The intraday performance of Shares traded in the secondary market generally will be different from the performance of a Geared Fund when measured from one NAV calculation-time to the next. When Shares are bought intraday, the performance of such Shares relative to its index until the Geared Fund’s next NAV calculation time likely will be greater than or less than the Fund’s stated daily multiple times the performance of its index. These differences can be significant.

Risks Applicable to Investing in VIX Futures Contracts

VIX futures contracts can be highly volatile and the Funds may experience sudden and large losses when buying, selling or holding such instruments; you can lose all or a portion of your investment within a single day.

Investments linked to equity market volatility, including VIX futures contracts, can be highly volatile and may experience sudden, large and unexpected losses. For example, in 2018 the Index, which is comprised of VIX futures contracts, had its largest one-day move ever of approximately 96%. In the future, the Index could have even larger single-day or intraday moves, up or down, that could cause investors to lose all or a substantial portion of their investment in a short period of time. VIX futures contracts are unlike traditional futures contracts and are not based on a tradable reference asset. The VIX is not directly investable, and the settlement price of a VIX futures contract is based on the calculation that determines the level of the VIX. As a result, the behavior of a VIX futures contract may be different from a traditional futures contract whose settlement price is based on a specific tradable asset and may differ from an investor’s expectations. The market for VIX futures contracts may fluctuate widely based on a variety of factors including changes in overall market movements, political and economic events and policies, wars, acts of terrorism, natural disasters, changes in interest rates or inflation rates. High volatility may have an adverse impact on the performance of the Funds. The UltraFund’s leverage factor (1.5x) increases the potential for loss on an investment in this Fund. An investor in any of the Funds could potentially lose the full principal of his or her investment within a single day.

-15-

Table of Contents

Daily rebalancing of the futures contracts underlying the Index may impact trading in the underlying futures contracts.

The daily rebalancing of the futures contracts underlying the Index may impact trading in such futures contracts. For example, such trading may cause Futures Commission Merchants (“FCMs”) to adjust their hedges. The trading activity associated with such transactions will contribute to the existing trading volume of the underlying futures contracts and may adversely affect the market price of such underlying futures contracts and in turn the level of the Index.

The Funds generally are intended to be used as trading tools for short-term investment horizons and investors holding shares of the Fund over longer-term periods may be subject to increased risk of loss.

The Funds generally are intended to be used only for short-term investment horizons. An investor in the Funds can lose all or a substantial portion of his or her investment within a single day. The longer an investor’s holding period in these Funds, the greater the potential for loss.

The Funds are benchmarked to the Index. They are not benchmarked to the VIX; the performance of the Funds should be expected to vary from the performance of the VIX. As a result, the Index and each Fund should be expected to perform very differently from the VIX over all periods of time.

The performance of the Index is based on the value of the VIX short-term futures contracts (“VIX futures contracts”) that comprise the Index. While there is a relationship between the performance of the Index and future levels of the VIX, the performance of the Index is not directly linked to the performance of the VIX, to the realized volatility of the S&P500® or to the options that underlie the calculation of the VIX. As a result, the Index and each Fund should be expected to perform very differently from the VIX over all periods of time. In many cases, the Index (and thus the Funds) will underperform the VIX. Further, the performance of the Index and each Fund should not be expected to represent the realized volatility of the S&P500® or any multiple or inverse thereof.

The VIX seeks to measure the market’s current expectation of30-day volatility of the S&P 500® Index, as reflected by the prices of near-term S&P500® options. The market’s current expectation of the possible rate and magnitude of movements in an index is commonly referred to as the “implied volatility” of the index. Because S&P500® options derive value from the possibility that the S&P500® may experience movement before such options expire, the prices of near-term S&P 500® options are used to calculate the implied volatility of the S&P 500®.

Unlike many indexes, the VIX is not an investable index. It is not practical to invest in the VIX as it is comprised of a constantly changing portfolio of options on the S&P500®. Rather, the VIX is designed to serve as a market volatility forecast. The Funds are not benchmarked to the performance of the VIX or the realized volatility of the S&P500® and, in fact, can be expected to perform very differently from the VIX and the realized volatility of the S&P500® over all periods of time.

The prices of futures contracts based on anon-investable index such as the VIX may behave differently from the prices of futures contracts whose settlement price is based on a tradeable asset.

As noted, each Fund is benchmarked against an underlying index of VIX short-term futures contracts. The value of a VIX futures contract is based on the expected value of the VIX at a future point in time, specifically the expiration date of the VIX futures contract. Therefore, a VIX futures contract represents the forward implied volatility of the VIX, and therefore the forward implied volatility of the S&P500®, over the30-day period following the expiration of such contract. As a result, a change in the VIX today will not necessarily result in a corresponding movement in the price of VIX futures contracts since the price of the VIX futures contracts is based on expectations of the performance of the VIX at a future point in time. For example, a VIX futures contract purchased in March that expires in May, in effect, is a forward contract on what the level of the VIX, as a measure of30-day implied volatility of the S& P500®, will be on the May expiration date. The forward volatility reading of the VIX may not correlate directly to the current volatility reading of the VIX because the implied volatility of the S&P500® at a future expiration date may be different from the current implied volatility of the S&P500®. As a result, the Index and each Fund should be expected to perform very differently from the VIX over all periods of time.

The level of the VIX has historically reverted to a long-term mean (i.e., average) and any increase or decrease in the level of the VIX will likely continue to be constrained.

-16-

Table of Contents

In the past, the level of the VIX has typically reverted over the longer term to a historical mean, and its absolute level has been constrained within a band. As such, the potential upside of long or short exposure to VIX futures contracts may be limited as the performance of VIX reverts to its long-term average. In addition, any gains may be subject to significant and unexpected reversals as the VIX reverts to its long term mean.

When economic uncertainty or other market risks increase, or are expected to increase, and there is an associated increase in expected volatility, the price of VIX futures contracts has historically tended to increase. Similarly, when economic uncertainty or other market risks recede, or are expected to recede, and there is an associated decrease in expected volatility, the price of VIX futures contracts has historically tended to decrease. Historically, each of these patterns have tended to reverse. These reversals may be significant and unexpected and have a negative impact on the performance of a Fund.

Potential negative impact from rolling futures positions; there have been extended periods in the past where the strategies utilized by the Funds have caused significant and sustained losses.

Each Fund invests in or has exposure to VIX futures contracts and is subject to risks related to “rolling” such futures contracts, which is the process by which a Fund closes out a futures position prior to its expiration month and purchases an identical futures contract with a later expiration date. The Funds do not intend to hold futures contracts through expiration, but instead intend to “roll” their respective positions as they approach expiration. The contractual obligations of a buyer or seller holding a futures contract to expiration may be satisfied by settling in cash as designated in the contract specifications. As explained further below, the price of futures contracts further from expiration may be higher (a condition known as “contango”) or lower (a condition known as “backwardation”), which can impact the Funds’ returns.