Fees are charged regardless of a Fund’s returns and may result in depletion of assets.

The Funds are subject to the fees and expenses described herein which are payable irrespective of a Fund’s returns, as well as the effects of commissions, trading spreads, and embedded financing, borrowing costs and fees associated with swaps, forwards, futures contracts, and costs relating to the purchase of U.S. Treasury securities or similar high credit quality, short-term fixed-income or similar securities. Additional charges may include other fees as applicable. These fees and expenses have a negative impact on Fund returns.

For the Funds linked to a benchmark, changes implemented by the benchmark provider that affect the composition and valuation of the benchmark could negatively impact the performance of the Funds.

The Funds, other than the Currency Fund, are linked to benchmarks maintained by third-party providers that are unaffiliated with the Funds or the Sponsor. There can be no guarantee or assurance that the methodology used by the third-party provider to create the benchmark will result in a Fund achieving high, or even positive, returns. The policies implemented by each benchmark provider concerning the calculation or the composition of a benchmark could affect the value of a benchmark and, therefore, the value of such Funds’ Shares. A benchmark provider may change the composition of the benchmark, or make other methodological changes that could change the value of a benchmark. Additionally, a benchmark provider may alter, discontinue or suspend calculation or dissemination of a benchmark. Any of these actions could adversely affect the value of Shares of a Fund using that benchmark. There is no guarantee the methodology underlying the benchmark will be free from error. Benchmark providers have no obligation to consider Fund shareholder interests in calculating or revising a benchmark. Each of these factors could have a negative impact on the performance of the Funds.

Calculation of a benchmark may not be possible or feasible under certain events or circumstances that are beyond the reasonable control of the Sponsor, which in turn may adversely impact both the benchmark and/or the Shares, as applicable. Additionally, benchmark calculations are subject to error and may be disrupted by rollover disruptions, rebalancing disruptions and/or market emergencies, which may have a negative impact on the performance of the Funds.

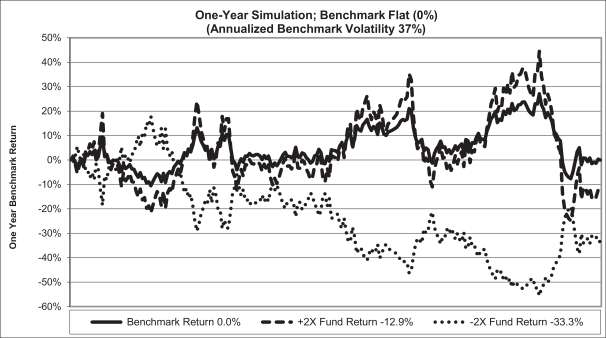

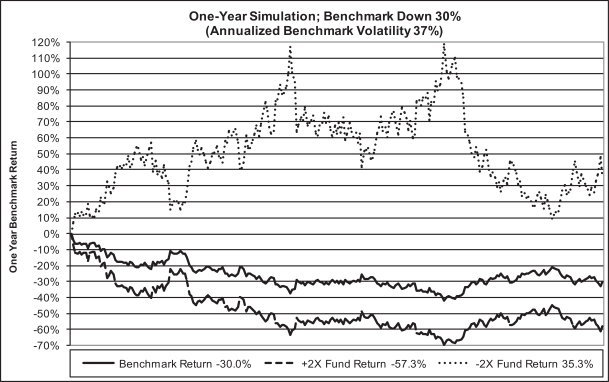

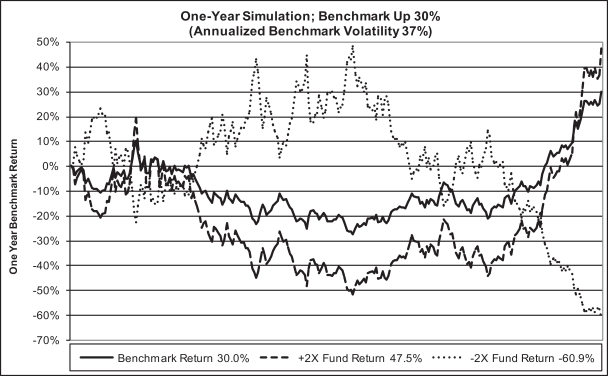

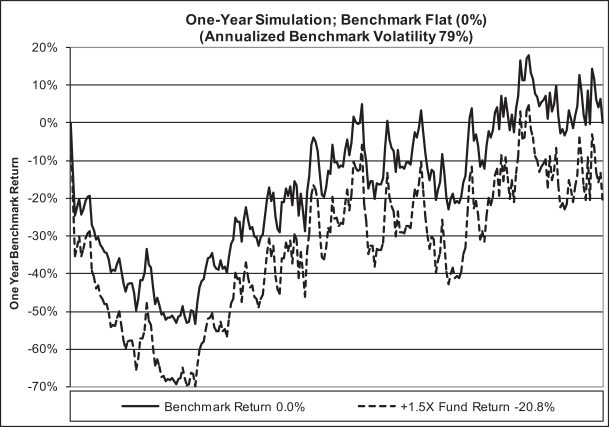

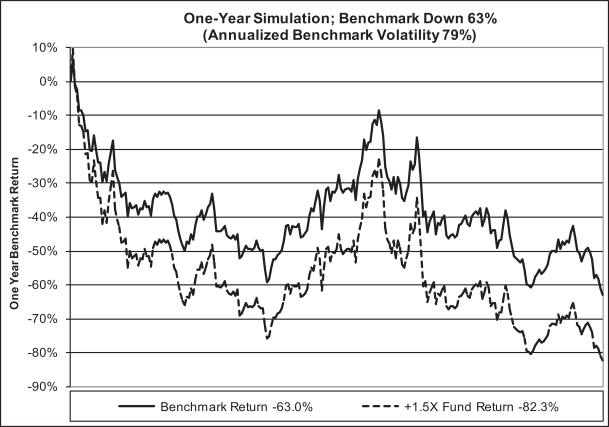

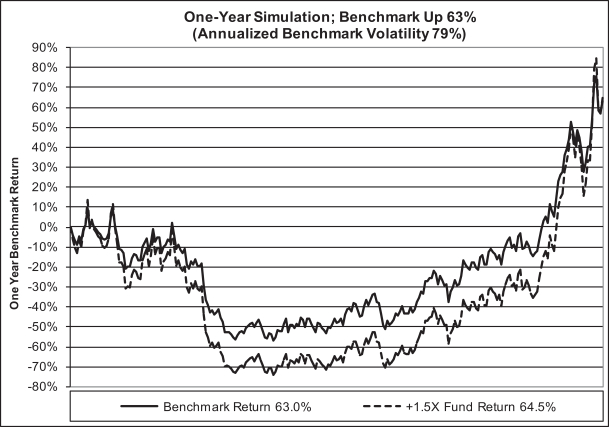

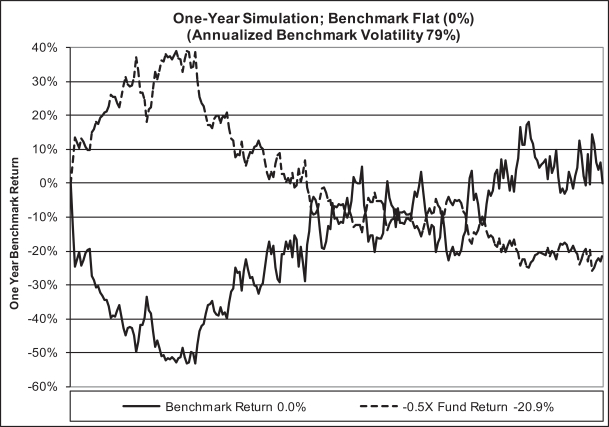

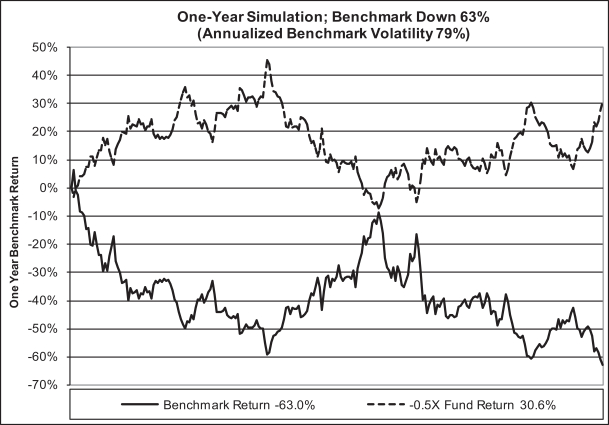

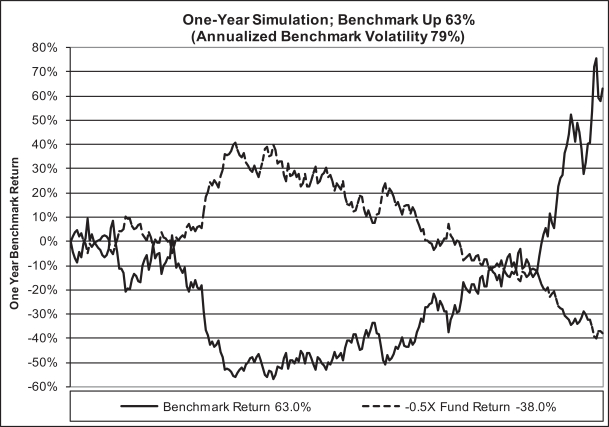

The particular benchmark used by a Fund may underperform other asset classes and may underperform other indices or benchmarks based upon the same underlying Reference Asset.

The Funds, other than the Currency Fund, are linked to benchmarks maintained by third-party providers unaffiliated with the Funds or the Sponsor. There can be no guarantee or assurance that the methodology used by the third-party provider to create the benchmark will result in a Fund achieving high, or even positive, returns. Further, there can be no guarantee that the methodology underlying the benchmark or the daily calculation of the benchmark will be free from error. It is also possible that the value of the benchmark or its underlying Reference Asset may be subject to intentional manipulation by third-party market participants The particular benchmark used by each Fund may underperform other asset classes and may underperform other indices or benchmarks based upon the same underlying Reference Asset. Each of these factors could have a negative impact on the performance of a Fund.

The Funds may be subject to counterparty risks.

Each Fund may use derivatives such as swap agreements and forward contracts (collectively referred to herein as “derivatives”) in the manner described herein as a means to achieve their respective investment objectives. The use of derivatives by a Fund exposes the Fund to counterparty risks.

Margin requirements for futures contracts and position limits imposed by exchanges and FCMs may limit a Fund’s ability to achieve sufficient exposure and prevent a Fund from achieving its investment objective.

The term “margin” refers to the minimum amount a Fund must deposit and maintain with its FCM to establish an open position in futures contracts. The minimum amount of margin required in connection with a particular futures contract is set by the clearinghouse that clears such contract and is subject to change at any time during the term of the contract. Futures contracts are customarily bought and sold on margins that represent a percentage of the aggregate purchase or sales price of the contract. “Initial” or “original” margin is the minimum amount of funds that must be deposited by each of the Funds with its FCM to initiate a futures position or to maintain an open position in a futures contract. “Maintenance” margin is the amount (generally less than initial margin) to which a Fund’s account may decline before the Fund must provide additional margin. A margin deposit is like a performance bond in that it helps assure a Fund’s performance of the futures contract that the Fund purchases or sells. Futures contracts are customarily bought and sold on margin that represents a very small percentage (ranging upward from less than 2%) of the purchase or sales price of the contract being traded. Because of such low margins, price fluctuations occurring in the futures markets may create profits and losses that are greater, in relation to the amount invested, than are customary in other forms of investments. An FCM may not accept lower, and generally require higher, amounts of margin from its clients than the minimum margin requirements established by the clearinghouses as a matter of policy to afford further protection for themselves.

An FCM may compute margin requirements multiple times per day and must do so at least once per day. When a Fund has an open futures contract position, it is subject to daily variation margin calls by an FCM that could be substantial in the event of adverse price movements. Because futures contracts require only a small initial investment in the form of a deposit or initial margin, they involve a high degree of leverage. A Fund with open positions is subject to maintenance or variation margin on its open positions. When the market value of a particular open futures contract position changes to a point where the margin on deposit does not satisfy maintenance margin requirements, a margin call is made by the FCM. If the margin call is not met within a reasonable time, the FCM may close out a Fund’s position which may impair the Fund from achieving its investment objective or result in reduced returns to the Fund’s investors. If a Fund has insufficient cash to meet daily variation margin requirements, it may need to sell Financial Instruments at a time when such sales are disadvantageous. Futures markets are highly volatile in general, and may become more volatile during periods of general market and/or economic volatility, and the use of or exposure to futures contracts may increase volatility of a Fund’s NAV.

The FCMs utilized by the Funds may impose margin requirements in addition to those imposed by the clearinghouse. Margin requirements are subject to change on any given day, and may be raised in the future on a single day or on multiple or successive days by either or both of the clearinghouse and the FCMs. High margin requirements could prevent a Fund from obtaining sufficient exposure to futures contracts and may adversely affect a Fund’s ability to achieve its investment objective. An FCM’s failure to return required margin to a Fund on a timely basis may cause the Fund to delay redemption settlement dates and/or restrict, postpone or limit the right of redemption.

Futures contracts are subject to liquidity risk. Certain of the FCMs utilized by the Funds have imposed their own “position limits”, or risk limits, on the Funds. Any such risk limits restrict the amount of exposure to futures contracts that a Fund can obtain through such FCMs. As a result, the Fund may need to transact through a number of FCMs to achieve its investment objective. If enough FCMs are not willing to transact with the Fund, or if the risk limits imposed by such FCMs do not provide sufficient exposure, the Fund may not be able to achieve its investment objective.

Margin requirements for uncleared swaps may limit a Fund’s ability to achieve sufficient exposure and prevent a Fund from achieving its investment objective.

The CFTC and banking regulators, as well as regulators outside the United States, have adopted collateral requirements applicable to swaps that are traded bilaterally and not cleared by a clearinghouse (“uncleared swaps”). Although a Fund is not directly subject to uncleared swap margin requirements, the Fund will become subject to these requirements by virtue of its counterparty’s status if such counterparty is registered as a swap dealer. Thus, when a Fund’s counterparty is subject to uncleared swap margin requirements, uncleared swaps between the Fund and that counterparty are subject to daily marked-to-market, or variation margin, requirements, and collateral is required to be exchanged between the Fund and the counterparty to account for any changes in the value of such swaps. The rules require registered swap dealers to collect from, and post to, a Fund variation margin (and initial margin, if the Fund exceeds a specified exposure threshold) for uncleared swap transactions.

The uncleared swap margin rules impose a number of requirements on counterparties to an uncleared swap that are registered swap dealers, including requirements related to the timing of margin transfers, the types of collateral that may be posted, the valuations of such collateral, and the calculation of margin requirements. The rules also require that a Fund post uncleared margin collateral to an independent bank custodian. These rules may result in significant operational burdens and costs to the Funds when they engage in uncleared swaps and may impair the Funds’ ability to achieve their investment objective or result in reduced returns to the Funds’ investors.

In addition to the variation margin requirements to which a Fund is subject when its uncleared swap counterparty is a registered swap dealer, regulators have adopted initial margin requirements applicable to uncleared swaps where at least one party is a registered swap dealer. The initial margin rules require parties to an uncleared swap to post, to a custodian that is independent from the swap counterparties, collateral (in addition to any variation margin) in an amount that is either (i) specified in a schedule in the rules or (ii) calculated by the swap dealer counterparty in accordance with a model that has been approved by the swap dealer’s regulator. Initial margin requirements are subject to a phased-in compliance period and, currently, these rules do not apply to any of the Funds. However, it is possible that in the future, these rules could apply to the Funds. In the event that the initial margin for uncleared swap rules apply to a Fund in the future, the rules would impose significant costs on the Fund’s ability to engage in uncleared swaps and may impair the Fund from achieving its investment objective or result in reduced returns to the Fund’s investors.

Natural Disaster/Epidemic Risk.

Natural or environmental disasters, such as earthquakes, fires, floods, hurricanes, tsunamis and other severe weather-related phenomena generally, and widespread disease, including pandemics and epidemics (for example, the novel coronavirus COVID-19), have been and can be highly disruptive to economies and markets and have recently led, and may continue to lead, to increased market volatility and significant market losses. Such natural disaster and health crises could exacerbate political, social, and economic risks previously mentioned, and result in significant breakdowns, delays, shutdowns, social isolation, and other disruptions to important global, local and regional supply chains affected, with potential corresponding results on the operating performance of the Funds and their investments. A climate of uncertainty and panic, including the contagion of infectious viruses or diseases, may adversely affect global, regional, and local economies and reduce the availability of potential investment opportunities, and increases the difficulty of performing due diligence and modeling market conditions, potentially reducing the accuracy of financial projections. Under these circumstances, the Funds may have difficulty achieving their investment objectives which may adversely impact performance. Further, such events can be highly disruptive to economies and markets, significantly disrupt the operations of individual companies (including, but not limited to, the Funds’ Sponsor and third party service providers), sectors, industries, markets, securities and commodity exchanges, currencies, interest and inflation rates, credit ratings, investor sentiment, and other factors affecting the value of the Funds’ investments. These factors can cause substantial market volatility, exchange trading suspensions and closures and can impact the ability of the Funds to complete redemptions and otherwise affect Fund performance and Fund trading in the secondary market. A widespread crisis may also affect the global economy in ways that cannot necessarily be foreseen at the current time. How long such events will last and whether they will continue or recur cannot be predicted. Impacts from these events could have significant impact on a Fund’s performance, resulting in losses to your investment.

Risk that Current Assumptions and Expectations Could Become Outdated As a Result of Global Economic Shocks

The onset of the novel coronavirus (COVID-19) has caused significant shocks to global financial markets and economies, with many governments taking extreme actions to slow and contain the spread of COVID-19. These actions have had, and likely will continue to have, a severe economic impact on global economies as economic activity in some instances has essentially ceased. Financial markets across the globe are experiencing severe distress at least equal to what was experienced during the global financial crisis in 2008. In March 2020, U.S. equity markets entered a bear market in the fastest such move in the history of U.S. financial markets. Contemporaneous with the onset of the COVID-19 pandemic in the US, oil experienced shocks to supply and demand, impacting the price and volatility of oil. The global economic shocks being experienced as of the date hereof may cause the underlying assumptions and expectations of the Funds to become outdated quickly or inaccurate, resulting in significant losses.

Regulatory Treatment

Derivatives are generally traded inover-the-counter (“OTC”) markets and have only recently become subject to comprehensive regulation in the United States. Cash-settled forwards are generally regulated as “swaps”, whereas physically settled forwards are generally not subject to regulation or subject to the federal securities laws (in the case of securities).

Title VII of the Dodd-Frank Act (as defined below) (“Title VII”) created a regulatory regime for derivatives, with the Commodity Futures Trading Commission (the “CFTC”) responsible for the regulation of swaps and the SEC responsible for the regulation of “security-based swaps.” The SEC requirements have largely yet to be made effective, but the CFTC requirements are largely in place. The CFTC requirements have included rules for some of the types of transactions in which the Funds will engage, including mandatory clearinghouse and exchange trading for certain categories of swaps, reporting, and margin for uncleared swaps. Title VII also created new categories of regulated market participants, such as “swap dealers,” “security-based swap dealers,” “major swap participants,” and “major security-based swap participants” who are, or will be, subject to significant new capital, registration, recordkeeping, reporting, disclosure, business conduct and other regulatory requirements. The regulatory requirements under Title VII continue to be developed and there may be further modifications that could materially and adversely impact the Funds, the markets in which a Fund trades and the counterparties with which the Fund engages in derivatives transactions.

-16-