As filed with the Securities and Exchange Commission on October 30, 2007

Registration Statement No. 333-

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

HK ENERGY PARTNERS LP

(Exact name of registrant as specified in its charter)

| | | | |

| Delaware | | 1311 | | 26-1285390 |

(State or other jurisdiction of incorporation or organization) | | (Primary Standard Industrial Classification Code Number) | | (I.R.S. Employer Identification No.) |

1000 Louisiana, Suite 5810

Houston, Texas 77002

(832) 204-2700

(Address, including zip code, and telephone number,

including area code, of registrant’s principal executive offices)

Floyd C. Wilson

President and Chief Executive Officer

1000 Louisiana, Suite 5810

Houston, Texas 77002

(832) 204-2700

(Name, address, including zip code, and telephone number,

including area code, of agent for service)

Copies to:

| | |

William T. Heller IV Harry R. Beaudry Thompson & Knight LLP 333 Clay Street, Suite 3300 Houston, Texas 77002 (713) 654-8111 | | James M. Prince Vinson & Elkins L.L.P. 1001 Fannin Street, Suite 2500 Houston, Texas 77002 (713) 758-2222 |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are being offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

CALCULATION OF REGISTRATION FEE

| | | | |

| |

| Title of each Class of Securities to be Registered | | Proposed

Maximum

Aggregate Offering Price(1)(2) | | Amount of Registration Fee |

Common Units representing limited partner interests | | $212,750,000 | | $6,532 |

| |

| |

| (1) | Includes common units issuable upon exercise of the underwriters’ option to purchase additional common units. |

| (2) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o). |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This document is not an offer to sell these securities and we are not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion, dated October 30, 2007

PROSPECTUS

9,250,000 Common Units

Representing Limited Partner Interests

HK Energy Partners LP is a growth oriented Delaware limited partnership recently formed by Petrohawk Energy Corporation (NYSE: HK) to acquire, develop and exploit oil and natural gas properties. We are offering 9,250,000 common units representing limited partner interests. This is the initial public offering of our common units. No public market currently exists for our common units. We expect the initial offering price to be between $ and $ per common unit. We intend to apply to list our common units on The New York Stock Exchange under the symbol “HKE.”

Investing in our common units involves risks. Please read “Risk Factors” beginning on page 19.

These risks include the following:

| | • | | Unless we replace the oil and natural gas reserves we produce, our production and revenues will decline, which would adversely affect our cash flow from operations and our ability to make distributions to our unitholders. |

| | • | | If oil or gas prices decline significantly for a prolonged period, we may lower our distributions or not pay distributions at all. |

| | • | | Our development operations will require substantial capital expenditures, which will reduce our cash available for distribution. We may be unable to obtain needed capital or financing on satisfactory terms, which could lead to a decline in our production and reserves. |

| | • | | We intend to pay holders of our common units distributions of $0.35 per unit for each quarter (or $1.40 per unit annually) before we pay distributions to holders of our subordinated units. For the year ended December 31, 2006 and the twelve months ended June 30, 2007, we would not have had enough cash available to pay the full $0.35 per common unit quarterly distribution to the holders of the common units or the distribution to the holders of the subordinated units. |

| | • | | We may not have sufficient cash from operations following the establishment of cash reserves and payment of fees and expenses, including cost reimbursements to our general partner, to enable us to make cash distributions to holders of our common units and subordinated units at the minimum quarterly distribution rate under our cash distribution policy. |

| | • | | We may incur substantial debt in the future. This debt may restrict our ability to make distributions. |

| | • | | Our general partner and its affiliates control us and will have conflicts of interest with us. Our partnership agreement limits the fiduciary duties that our general partner owes to us, which may permit it to favor its own interests to your detriment, and limits the circumstances under which you may make a claim relating to conflicts of interest and the remedies available to you in that event. |

| | • | | If you are not an “Eligible Holder” (generally a United States citizen or entity), you will not be entitled to receive distributions or allocations of income or loss on your common units, and your common units will be subject to redemption at a price that may be below the current market price. |

| | • | | You may be required to pay taxes on income earned by us even though your cash distributions from us are less than your share of our income. |

| | | | | | |

| | | Per

Common

Unit | | Total |

| | |

Initial public offering price | | $ | | | $ | |

| | |

Underwriting discount | | $ | | | $ | |

| | |

Proceeds, before expenses, to HK Energy Partners LP | | $ | | | $ | |

We have granted the underwriters a 30-day option to purchase up to an additional 1,387,500 common units from us on the same terms and conditions as set forth above if the underwriters sell more than 9,250,000 common units in this offering.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Lehman Brothers, on behalf of the underwriters, expects to deliver the common units on or about , 2007.

LEHMAN BROTHERS | WACHOVIA SECURITIES |

, 2007

TABLE OF CONTENTS

i

ii

You should rely only on the information contained in this prospectus. We have not, and the underwriters have not, authorized anyone to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. We are not, and the underwriters are not, making an offer to sell these securities in any jurisdiction where an offer or sale is not permitted. You should assume that the information appearing in this prospectus is accurate as of the date on the front cover of this prospectus. Our business, financial condition, results of operations and prospects may have changed since that date.

Until , 200 (25 days after the date of this prospectus), all dealers that effect transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers’ obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

Our natural gas and crude oil proved reserve information as of June 30, 2007 included in this prospectus is based on a reserve report prepared by Netherland, Sewell & Associates, Inc., or NSAI, an independent engineering firm. A summary of this report is provided in Appendix C and is referred to in this prospectus as the “reserve report”.

iii

PROSPECTUS SUMMARY

This summary highlights selected information contained elsewhere in this prospectus. You should read the entire prospectus carefully, including the historical and pro forma financial statements and notes to those financial statements. The information presented in this prospectus assumes an initial public offering price of $20.00 per common unit and, unless otherwise noted, that the underwriters’ option to purchase additional common units is not exercised. You should read “Risk Factors” beginning on page 19 for more information about important factors that you should consider carefully before buying our common units. We include a glossary of some of the oil and natural gas terms used in this prospectus as Appendix B.

References in this prospectus to “HK Energy Partners,” “the partnership,” “we,” “our,” “us” or similar terms refer to HK Energy Partners LP and its subsidiaries. References in this prospectus to “HK GP” or “our general partner” refer to HK Energy Partners GP LP, our general partner. References in this prospectus to “HK Management” or “our management” refer to Petrohawk Management Company, LLC, the general partner of our general partner. References in this prospectus to “Petrohawk” refer to Petrohawk Energy Corporation, the ultimate parent company of our general partner, and its wholly owned subsidiaries, including HK Management. References in this prospectus to the “partnership properties” or “our properties” refer to the combination of oil and natural gas properties contributed and sold to us by subsidiaries of Petrohawk in connection with this offering. Unless otherwise noted, references in this prospectus to our properties on a “pro forma combined basis” refer to our properties as if they had been contributed and sold to us by Petrohawk on January 1, 2006.

HK Energy Partners LP

We are a growth oriented Delaware limited partnership formed in October 2007 by Petrohawk Energy Corporation (NYSE: HK) to acquire, develop and exploit oil and natural gas properties. Our properties are primarily located in the Permian Basin region in West Texas and southeastern New Mexico.

At June 30, 2007, our oil and natural gas properties had estimated net proved reserves of 145.3 Bcfe, of which approximately 72% were natural gas and 79% were proved developed. For the six months ended June 30, 2007, on a pro forma combined basis, our properties produced approximately 26.3 MMcfe/d. Our producing properties are located in mature fields that exhibit relatively long-lived production, with a reserve to production ratio of 15 years, based on our estimated proved reserves as of June 30, 2007 and our annualized production for the six months ended June 30, 2007.

Our primary business objective is to generate stable cash flows through maintaining our current production levels and asset base over the long term in a manner that will allow us to make quarterly cash distributions to our unitholders at the minimum quarterly distribution rate of $0.35 per unit and, over time, to grow our production and asset base to increase our quarterly cash distribution rate. We intend to rely on the significant operating and acquisition experience of Petrohawk’s management team, acting for our general partner, to execute our growth strategy. Subsequent to the arrival of Petrohawk’s current management in May 2004, Petrohawk increased its proved reserves from approximately 219 Bcfe as of December 31, 2004 to approximately 1,076 Bcfe as of December 31, 2006 and increased its average daily production from approximately 29 MMcfe/d for the three month period ended December 31, 2004 to approximately 321 MMcfe/d for the six months ended June 30, 2007, primarily through strategic acquisitions of oil and natural gas properties and the drilling and exploitation of those properties.

We intend to pay a minimum quarterly cash distribution of $0.35 per unit, or $1.40 per unit annually, to holders of our common units. We will pay this distribution, which we refer to as our minimum quarterly

1

distribution, on all of our common units before paying quarterly distributions on our subordinated units, which constitute 25% of our limited and general partner interests. To achieve more predictable cash flows and to reduce our exposure to adverse fluctuations in the prices of oil and natural gas, we intend to implement an active hedging program covering a significant portion of our expected oil and natural gas production.

Our Properties

Our principal properties are located in the Permian Basin, which is one of the largest and most prolific oil and natural gas producing basins in the United States. The Permian Basin extends over 100,000 square miles in West Texas and southeastern New Mexico and has produced over 26 billion Bbls of oil and 85 Tcf of natural gas since its discovery in 1921. This basin is characterized by oil and natural gas fields with large accumulations of original hydrocarbons in place, long production histories, and multiple producing formations. Because of these inherent qualities, we believe properties in this region are well suited for our partnership and its business objectives.

Our producing properties in the Permian Basin are mature fields with relatively predictable production and with relatively low production declines. We intend to pursue relatively low risk development drilling and workover projects designed to partially offset our natural production decline rates in our existing fields. We expect to drill a total of 22 gross (7.1 net) wells and complete 37 (14 net) workovers on our properties during 2007 with annual budgeted spending of $14 million, of which 13 wells (1.7 net) have been drilled and 25 (7.6 net) workovers have been completed at a cost of approximately $7 million (net) as of June 30, 2007. For the year ending December 31, 2008, we anticipate drilling a total of 47 (12.1 net) wells and completing 44 (16.4 net) workovers with budgeted spending of approximately $16 million (net).

The following table is a summary of the proved reserves and production of our oil and natural gas properties as of June 30, 2007.

| | | | | | | | | | | | | | | | | |

Field | | As of June 30, 2007(1) | | 1st Half

2007

Average

Daily

Production | | Reserve-to- Production

Ratio(3) | | Estimated

Production

Decline

Rate(4) | |

| | Estimated Proved Reserves | | Percent

of Total Proved

Reserves | | | Percent Natural

Gas(2) | | | Estimated Proved Developed Reserves | | | |

| | | (Bcfe) | | | | | | | | (Bcfe) | | (MMcfe/d) | | (Years) | | | |

Texas | | | | | | | | | | | | | | | | | |

Waddell Ranch | | 42.3 | | 29.1 | % | | 46.1 | % | | 33.9 | | 5.9 | | 19.6 | | 10 | % |

Sawyer | | 38.3 | | 26.3 | % | | 99.1 | % | | 28.9 | | 10.6 | | 9.9 | | 12 | % |

TXL North | | 24.2 | | 16.7 | % | | 36.8 | % | | 20.0 | | 3.1 | | 21.4 | | 7 | % |

New Mexico | | | | | | | | | | | | | | | | | |

Jalmat | | 38.3 | | 26.4 | % | | 94.4 | % | | 30.4 | | 6.1 | | 17.2 | | 13 | % |

Oklahoma | | | | | | | | | | | | | | | | | |

Carpenter / Carpenter NE | | 2.2 | | 1.5 | % | | 99.7 | % | | 2.2 | | 0.6 | | 10.1 | | 12 | % |

| | | | | | | | | | | | | | | | | |

Total | | 145.3 | | 100.0 | % | | 72.1 | % | | 115.4 | | 26.3 | | 15.1 | | 11 | % |

| | | | | | | | | | | | | | | | | |

| (1) | Our natural gas and oil proved reserve information as of June 30, 2007 is based on a reserve report prepared by Netherland, Sewell & Associates, Inc., an independent engineering firm (“NSAI”). See Appendix C. |

| (2) | Calculated using natural gas equivalents of six Mcf of natural gas per Bbl of oil. NGLs are included in natural gas. |

| (3) | The reserve-to-production ratio is calculated by dividing our estimated net proved reserves as of June 30, 2007 by our annualized average daily production for the six months ended June 30, 2007. |

| (4) | Represents percentage decrease in annual production from our proved developed producing reserves in 2009 when compared to 2008 as estimated by NSAI. |

2

Texas Properties

Our Texas properties include our Waddell Ranch, Sawyer and TXL North fields. Our interests in these fields encompass approximately 111,000 gross (43,000 net) acres and are located in Crane, Sutton and Ector counties. The producing formations in our Texas properties range in depth from 3,000 to 11,000 feet and activity in these fields focuses primarily on infill development drilling. We have identified approximately 1,000 development drilling locations as well as approximately 110 workover and exploitation projects. In 2008, we plan to spend a total of $11 million on our Texas properties, including $9.4 million for drilling and completing 47 gross wells (12.1 net) and $1.6 million for 31 (4 net) workover and exploitation projects.

New Mexico Property

Our property in southeastern New Mexico consists of the Jalmat field. Our interests in this field encompass approximately 9,400 gross (8,900 net) acres located in Lea County. The producing formations in this field range in depth from 2,700 to 4,000 feet and activity in this field focuses primarily on workover projects. We have identified 45 exploitation projects that consist primarily of workover and redrill activities. In 2008, we plan to spend a total of $5 million on 13 (12.4 net) workover projects on our New Mexico property.

Business Strategy

Our primary business objective is to generate stable cash flows through maintaining our current production levels and asset base over the long term in a manner that will allow us to make quarterly cash distributions to our unitholders and, over time, to grow our production and asset base to increase our quarterly cash distribution rate. We intend to accomplish this objective by executing the following business strategies:

| | • | | Make accretive acquisitions of properties with long-lived, stable and predictable production profiles: |

| | • | | directly from Petrohawk through negotiated transactions; |

| | • | | by cooperating with Petrohawk in pursuit of attractive acquisition candidates; and |

| | • | | from third-parties independent of Petrohawk; |

| | • | | Maintain a multi-year inventory of relatively low risk drilling locations and exploitation projects; |

| | • | | Reduce the volatility in our cash flows through our commodity hedging activities; and |

| | • | | Leverage the technical and managerial expertise of Petrohawk to develop and exploit our existing assets and to grow through acquisitions. |

Competitive Strengths

We believe the following competitive strengths will enable us to achieve our primary business objective and successfully execute our strategies:

| | • | | Our substantial inventory of identified development drilling locations and exploitation projects; |

| | • | | Our oil and natural gas properties are characterized by long-lived reserves with relatively predictable production profiles; and |

| | • | | Our relationship with Petrohawk, which provides us with: |

| | • | | the opportunity to acquire assets directly from and jointly with Petrohawk; |

| | • | | the ability to leverage Petrohawk’s technical expertise to implement our acquisition, development and exploitation strategy; |

3

| | • | | access to the substantial acquisition, integration and operational experience of Petrohawk’s management team; and |

| | • | | the experience of Petrohawk’s management team in the oil and natural gas industry, including significant experience in the Permian Basin and other regions with properties characterized by stable and predictable production profiles and long-lived reserves. |

Hedging

An important part of our business strategy includes hedging a portion of our oil and natural gas production to reduce our exposure to fluctuations in the prices of oil and natural gas and achieve more predictable cash flows. As of October 25, 2007, Petrohawk has entered into swap agreements covering 3,660,000 MMBtu of natural gas and 275 MBbls of oil for each of calendar years 2008, 2009 and 2010. The hedged volumes represent approximately 56% of our forecasted total production of 9,405 MMcfe for the twelve months ending December 31, 2008 at weighted average prices of $8.25 per MMBtu for natural gas and $81.17 per Bbl for oil. Petrohawk will assign those derivative contracts to us at the closing of this offering. Petrohawk intends to enter into additional derivative financial instruments so that approximately 80% to 85% of our estimated net production of oil and natural gas from proved developed producing reserves will be covered by derivatives through December 31, 2010. The form of these derivatives is expected to be fixed-price swaps and puts. By removing a portion of price volatility associated with our future oil and natural gas production we have mitigated, but not eliminated, the potential effects of changing oil and natural gas prices on our cash flows from operations for those periods. For more information on our hedging arrangements, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations — How We Evaluate Our Operations — Derivative Instruments and Hedging Activities.”

Our Relationship with Petrohawk

One of our principal strengths is our relationship with Petrohawk (NYSE: HK), a publicly traded independent oil and natural gas company. Petrohawk is engaged in the acquisition and development of oil and natural gas reserves from onshore fields in the United States and seeks to acquire a balanced, geographically diverse portfolio of long-lived, lower risk reserves along with shorter lived, higher margin reserves. As of December 31, 2006, and including the interests to be conveyed to us, Petrohawk’s total estimated proved reserves were 1,076 Bcfe, consisting of 24 MMBbls of oil and condensate and 930 Bcf of natural gas and NGLs located primarily in the Mid-Continent region (including 204 Bcfe in the Gulf Coast region that Petrohawk has signed a definitive agreement to divest). Upon completion of this offering, Petrohawk will have a significant interest in us through its ownership of 5,904,048 common units and 5,189,742 subordinated units, representing a 53.4% limited partner interest in us, a 2% general partner interest in us and all of our incentive distribution rights.

A principal component of our business strategy is to grow our proved reserves and production through the acquisition of oil and natural gas properties characterized by long-lived, stable and predictable production profiles and that have substantial opportunities for further development and exploitation. We intend to leverage the significant experience of Petrohawk’s management team to execute our growth strategy. Petrohawk has an established track record of successfully acquiring, developing, exploiting and operating oil and natural gas properties. Subsequent to the arrival of Petrohawk’s current management in May 2004, Petrohawk has increased its proved reserves from approximately 219 Bcfe as of December 31, 2004 to approximately 1,076 Bcfe as of December 31, 2006, and has increased its average daily production from approximately 29 MMcfe/d for the three months ended December 31, 2004 to approximately 321 MMcfe/d for the six months ended June 30, 2007, primarily through strategic acquisitions of oil and natural gas properties and the drilling and exploitation of those properties. After the contribution of the partnership properties to us, Petrohawk will continue to own and operate properties with estimated net proved reserves as of December 31, 2006 of 927 Bcfe (including 204 Bcfe in the Gulf Coast region that Petrohawk has signed a definitive agreement to divest), which include some properties with characteristics that are or, after additional capital is invested, may be well suited for our partnership.

4

Petrohawk views us as an integral part of its growth strategy. It may be in Petrohawk’s best interest to sell additional assets to us in the future. Nonetheless, no assurance can be provided as to which, if any, assets may be made available to us by Petrohawk as Petrohawk is not obligated to offer us assets for acquisition, or if we will choose to pursue the opportunity to acquire such assets if they are made available to us. Furthermore, Petrohawk evaluates acquisitions and divestitures and may elect to acquire or divest oil and natural gas properties in the future without offering us the opportunity to participate. After this offering, Petrohawk will continue to be free to act in a manner that is beneficial to its interests and may be detrimental to ours, which may include competing with us for future acquisition opportunities. Accordingly, while our relationship with Petrohawk and its subsidiaries is a significant strength, it also is a source of potential conflicts. See “Conflicts of Interest and Fiduciary Duties.”

5

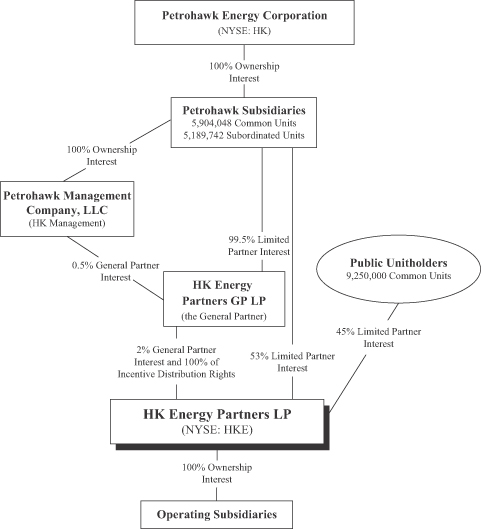

Organizational Chart

The following diagram depicts our organizational structure and ownership after giving effect to this offering and the related formation transactions, assuming that the underwriters’ option to purchase additional common units is not exercised.

| | | |

Public Common Units | | 45 | % |

Petrohawk | | | |

Common Units | | 28 | % |

Subordinated Units | | 25 | % |

General Partner Interests | | 2 | % |

6

Risk Factors

An investment in our common units involves risks associated with our business, regulatory and legal matters, our limited partnership structure and the tax characteristics of our common units. Please read carefully the risks under “Risk Factors” beginning on page 19.

Summary of Conflicts of Interest and Fiduciary Duties

Conflicts of Interest. Our general partner has a legal duty to manage us in a manner beneficial to our unitholders. This legal duty originates in statutes and judicial decisions and is commonly referred to as a “fiduciary duty.” However, because our general partner and its general partner, HK Management, are owned by Petrohawk, the officers and directors of HK Management also have fiduciary duties to manage our general partner in a manner beneficial to Petrohawk. As a result of this relationship, conflicts of interest may arise in the future between us and holders of our common units, on the one hand, and our general partner and its affiliates, including Petrohawk and its subsidiaries, on the other hand.

Partnership Agreement Modifications of Fiduciary Duties. Our partnership agreement limits the liability and reduces the fiduciary duties of our general partner to us and our unitholders. Our partnership agreement also restricts the remedies available to our unitholders for actions that might otherwise constitute a breach of our general partner’s fiduciary duties owed to our unitholders. Our partnership agreement also provides that Petrohawk and its affiliates may own assets or engage in businesses that compete with us. For example, Petrohawk or its affiliates may acquire, invest in or dispose of oil and natural gas exploration and production or other assets in the future without any obligation to offer us the opportunity to purchase or own interests in those assets, and Petrohawk may, at any time alter its strategy, including determining that we no longer constitute an integral component of Petrohawk’s growth. Petrohawk is also not under any obligation to make any acquisitions on our behalf. By purchasing a common unit, the purchaser agrees to be bound by the terms of our partnership agreement and, pursuant to the terms of our partnership agreement, each holder of common units consents to various actions contemplated in the partnership agreement and conflicts of interest that might otherwise be considered a breach of fiduciary or other duties under applicable state law.

For a more detailed description of the conflicts of interest and fiduciary duties of our general partner, see “Risk Factors — Risks Inherent in an Investment in Us” and “Conflicts of Interest and Fiduciary Duties.”

Formation Transactions and Partnership Structure

We are a Delaware limited partnership formed in October 2007. Our general partner, HK Energy Partners GP LP, has sole responsibility for conducting our business and managing our operations. The board of directors of Petrohawk Management Company, LLC, which is the general partner of HK Energy Partners GP LP, a wholly owned subsidiary of Petrohawk, will be responsible for directing the business and operations of our general partner. Our operations will be conducted through, and our operating assets will be owned by, our operating subsidiaries. We own, directly or indirectly, all of the ownership interests in our operating subsidiaries. We, our subsidiaries and our general partner do not have employees.

In connection with the closing of this offering:

| | • | | we will enter into a contribution agreement with certain wholly-owned subsidiaries of Petrohawk and our general partner pursuant to which: |

| | • | | our general partner and another subsidiary of Petrohawk will contribute all of the partnership properties to us; |

| | • | | we will issue 5,904,048 common units and 5,189,742 subordinated units to wholly owned subsidiaries of Petrohawk, representing an aggregate 53.4% limited partner interest in us as partial consideration for such contribution; |

| | • | | subsidiaries of Petrohawk will agree to indemnify us for certain environmental and tax liabilities and title defects, as well as relating to retained assets and liabilities, occurring or existing before the closing; |

7

| | • | | we will sell 9,250,000 common units to the public in this offering, representing a 44.6% limited partner interest in us, and will use the proceeds as described in “Use of Proceeds”; |

| | • | | we will issue to HK Energy Partners GP LP a 2% general partner interest in us and all of our incentive distribution rights, which will entitle our general partner to increasing percentages of the cash we distribute in excess of $0.4025 per unit per quarter (115% of the minimum quarterly distribution); |

| | • | | we expect to borrow $165.0 million in term debt under our credit facility which will be secured by $165.0 million of qualifying investment grade securities, and distribute the funds to our general partner and another subsidiary of Petrohawk as partial consideration for the partnership properties contributed to us; |

| | • | | we expect to borrow $58.1 million in revolving debt under our credit facility and distribute the funds to our general partner and another subsidiary of Petrohawk; |

| | • | | we will enter into an administrative services agreement with Petrohawk, HK Management and our general partner pursuant to which we will reimburse Petrohawk and its affiliates for the payment of certain operating expenses and for providing various general and administrative services to us. |

Management of HK Energy Partners LP

HK Energy Partners GP LP, our general partner, is an indirect, wholly owned subsidiary of Petrohawk and has sole responsibility for conducting our business and for managing our operations. Because our general partner is a limited partnership, its general partner, HK Management, will conduct our business and operations, and the board of directors and officers of HK Management will make decisions on our behalf. Petrohawk will elect all seven directors of HK Management, with at least three directors meeting the independence standards established by The New York Stock Exchange, one of whom will be elected to the board as of the closing of this offering. Services will be provided to HK Energy Partners GP LP and us by officers and other employees of Petrohawk and its subsidiaries. For more information about these individuals, see “Management — Directors and Executive Officers.”

At the closing of this offering, we intend to enter into an administrative services agreement with Petrohawk, HK Management and our general partner pursuant to which Petrohawk and its subsidiaries will perform administrative services for us such as accounting, business development, finance, land, legal, engineering, investor relations, management, marketing, information technology, insurance, government regulations, communications, regulatory, environmental and human resources. Petrohawk and its subsidiaries will not be liable to us for their performance of, or failure to perform, services under the administrative services agreement unless their acts or omissions constitute gross negligence or willful misconduct. Petrohawk and its subsidiaries will be reimbursed for their costs incurred in providing such services to us, including for salary, bonus, incentive compensation and other amounts paid by Petrohawk and its subsidiaries to persons who perform services for us or on our behalf. Our general partner is entitled to determine in good faith the expenses that are allocable to us. Petrohawk has informed us that it intends initially to structure the reimbursement of these costs in the form of a monthly billing of a portion of Petrohawk’s corporate and other expenses, representing an estimated allocable share of time spent by the officers and employees of Petrohawk and its subsidiaries on our operations. We expect that the annual reimbursement charge will be approximately $2.9 million and will be pro-rated for the initial period from the closing of this offering through December 31, 2008. Petrohawk has indicated that it expects that it will review at least annually with the board of directors of HK Management this reimbursement arrangement and any changes to the amount or methodology by which it is determined. In addition, we will incur additional third party expenses, such as those incurred as a result of our being a public company, which we expect to approximate $2.8 million annually. See “Certain Relationships and Related Transactions.”

As is common with publicly traded limited partnerships and in order to maximize operational flexibility, we will conduct our operations through subsidiaries. We will have several direct operating subsidiaries initially, which will conduct business through themselves and their subsidiaries.

8

Other Information

Our principal executive offices are located at 1000 Louisiana, Suite 5810, Houston, Texas 77002 and our telephone number is . We expect our internet address to be www. .com. We expect to make our periodic reports and other information filed with or furnished to the Securities and Exchange Commission, which we refer to as the SEC, available, free of charge, through our website, as soon as reasonably practicable after those reports and other information are electronically filed with or furnished to the SEC. Information on our website or any other website is not incorporated by reference into this prospectus and does not constitute a part of this prospectus.

9

The Offering

Common units offered to the public | 9,250,000 common units; 10,637,500 common units if the underwriters exercise their option to purchase additional common units in full. |

Units outstanding after this offering | 15,154,048 common units and 5,189,742 subordinated units, representing 73% and 25%, respectively, of our limited and general partner interests. The general partner will own a 2% general partner interest in us. |

| | If the underwriters exercise their option to purchase additional common units in full, 16,541,548 common units and 5,189,742 subordinated units, representing 75% and 23%, respectively, of our limited and general partner interests will be outstanding after this offering. |

Use of proceeds | We estimate that we will receive net proceeds of approximately $170.0 million from the sale of 9,250,000 common units offered by this prospectus, assuming an offering price of $20.00 per unit and after deducting underwriting discounts, a structuring fee and estimated offering expenses. We anticipate using the aggregate net proceeds of this offering to: |

| | • | | purchase $165.0 million of qualifying investment grade securities, which will be assigned as collateral to secure the term loan portion of our credit facility; and |

| | • | | fund $5.0 million of working capital. |

| | We also anticipate that we will borrow approximately $165.0 million in term debt and $58.1 million in revolving debt upon the closing of this offering, and we will distribute the aggregate amount of the net proceeds from such borrowings to subsidiaries of Petrohawk, which distribution will be made in partial consideration of the assets contributed to us upon the closing of this offering. |

| | If the underwriters’ option to purchase additional common units is exercised in full, we will use the net proceeds of approximately $25.8 million (also assuming an offering price of $20.00 per unit) to repay a portion of our anticipated borrowings under our revolving credit facility. |

Cash distributions | We intend to make minimum quarterly distributions of $0.35 per unit per quarter ($1.40 per unit on an annualized basis) to the extent we have sufficient cash from our operations after establishment of cash reserves and payment of fees and expenses, including payments to our general partner and its affiliates. Assuming that we become a publicly traded partnership before March 31, 2008, we will pay unitholders a prorated distribution for the period from the first day our common units are publicly traded to and including March 31, 2008. We expect to pay this cash distribution on or before May 15, 2008. We intend to retain substantial cash reserves to finance the capital expenditures necessary to maintain our existing levels of production and asset base over the long term. Our ability to pay cash distributions at this |

10

| | minimum quarterly distribution rate is subject to various restrictions and other factors described in more detail under “Our Cash Distribution Policy and Restrictions on Distributions.” |

| | Our partnership agreement requires us to distribute all of our cash on hand at the end of each quarter, beginning with the quarter ending March 31, 2008, less reserves established by our general partner. We refer to this cash as “available cash,” and we define its meaning in our partnership agreement attached as Appendix A. |

| | All of our cash distributions will be characterized as coming from either operating surplus or capital surplus. Operating surplus is defined in our partnership agreement and generally means amounts we receive from operating sources, such as sales of our oil and natural gas production, less operating expenditures, such as production costs and taxes and less estimated average maintenance capital expenditures, which are generally amounts we estimate we will spend in the future to maintain our existing production levels and asset base over the long term. Capital surplus generally means amounts we receive from non-operating sources such as sales of properties and issuances of debt or equity securities or borrowings, other than short term working capital borrowings. We distribute operating surplus differently than capital surplus. We do not expect to make any distributions of available cash from capital surplus. Our partnership agreement requires that we distribute all of our available cash from operating surplus each quarter in the following manner: |

| | • | | first, 98% to the holders of common units and 2% to our general partner, until each common unit has received a minimum quarterly distribution of $0.35 plus any arrearages from prior quarters; |

| | • | | second, 98% to the holders of subordinated units and 2% to our general partner, until each subordinated unit has received a minimum quarterly distribution of $0.35; |

| | • | | third, 98% to all unitholders, pro rata, and 2% to our general partner, until each unit has received an aggregate distribution of $0.4025; |

| | • | | fourth, 85% to all unitholders, pro rata, and 15% to our general partner, until each unit has received an aggregate distribution of $0.4375; and |

| | • | | thereafter, 75% to all unitholders, pro rata, and 25% to our general partner. |

| | On a pro forma basis for the year ended December 31, 2006 and the twelve months ended June 30, 2007, we would have generated available cash of approximately $9.5 million and $18.3 million, respectively. This amount of pro forma cash available for distribution |

11

| | would have been sufficient to allow us to pay approximately 44% and 84%, respectively, of the minimum quarterly distributions on our common units during these periods (48% and 86%, respectively, assuming the underwriters exercise in full their option to purchase additional common units). See “Our Cash Distribution Policy and Restrictions on Distributions — Unaudited Pro Forma Available Cash for the Year Ended December 31, 2006 and for the Twelve Months Ended June 30, 2007.” |

| | We believe that, based on the assumptions and factors included under “Our Cash Distribution Policy and Restrictions on Distributions — Assumptions and Considerations,” we will have sufficient cash available from operating surplus to make cash distributions for the four quarters ending December 31, 2008 at the minimum quarterly distribution rate of $0.35 per unit per quarter ($1.40 per common unit on an annualized basis) on all common units and subordinated units. See “Our Cash Distribution Policy and Restrictions on Distributions — Estimated Cash Available for Distribution for the Twelve Months Ending December 31, 2008.” |

Subordinated units | Following this offering, Petrohawk will beneficially own all of our subordinated units. The principal difference between our common units and subordinated units is that in any quarter during the subordination period, holders of the subordinated units are entitled to receive the minimum quarterly distribution from operating surplus of $0.35 per unit only after the common units have received the minimum quarterly distribution from operating surplus plus any arrearages in the payment of the minimum quarterly distribution from prior quarters and the general partner has received its 2% distribution. Accordingly, the holders of subordinated units may receive a smaller distribution than holders of common units or no distribution at all. Subordinated units will not accrue arrearages. |

| | The subordination period will generally end on the first business day after we have earned and paid from operating surplus at least $0.35 per quarter on each outstanding common unit and subordinated unit and paid to the general partner the related amount representing its general partner interest for any three consecutive, non-overlapping four-quarter periods ending on or after December 31, 2010. The subordination period also will end upon the removal of our general partner other than for cause if the units held by our general partner and its affiliates are not voted in favor of such removal. |

| | When the subordination period ends, all remaining subordinated units will convert into common units on a one-for-one basis, and the common units will no longer be entitled to arrearages. See “How We Will Make Distributions — Subordination Period.” |

12

General Partner’s right to reset the target distribution levels | Our general partner has the right, at a time when there are no subordinated units outstanding and it has received incentive distributions at the highest level to which it is entitled (23%), for each of the prior four consecutive fiscal quarters, to reset the initial cash target distribution levels at higher levels based on the distribution at the time of the exercise of the reset election. Following a reset election by our general partner, the minimum quarterly distribution amount will be reset to an amount equal to the average cash distribution amount per common unit for the two fiscal quarters immediately preceding the reset election (‘‘reset minimum quarterly distribution’’) and the target distribution levels will be reset to correspondingly higher levels based on the same percentage increases above the reset minimum quarterly distribution amount as in our current target distribution levels. |

| | In connection with resetting these target distribution levels, our general partner will be entitled to receive a number of Class B units equal to that number of common units whose aggregate quarterly cash distributions equaled the average of the distributions to our general partner on the incentive distribution rights in the prior two quarters. The Class B units will be entitled to the same cash distributions per unit as our common units and will be convertible into an equal number of common units at any time following the first anniversary of issuance. See “How We Will Make Cash Distributions — General Partner’s Right to Reset Target Distribution Levels.” |

Issuance of additional units | We can issue an unlimited number of units without the consent of our unitholders. See “Units Eligible for Future Sale” and “The Partnership Agreement — Issuance of Additional Securities.” |

Limited voting rights | Our general partner will manage and operate us. Unlike the holders of common stock in a corporation, you will have only limited voting rights on matters affecting our business. You will have no right to elect our general partner or its general partner, HK Management, or the directors of HK Management on an annual or other continuing basis. Our general partner may not be removed except by a vote of the holders of at least 66 2/3% of the outstanding units, including any units owned by our general partner and its affiliates, voting together as a single class. Upon consummation of this offering our general partner and its owners and their affiliates will own an aggregate of 55.4% of our common and subordinated units and general partner interests. This will give our general partner the practical ability to prevent its involuntary removal. See “The Partnership Agreement — Voting Rights.” |

Limited call right | If at any time more than 80% of the outstanding common units are owned by our general partner and its affiliates, our general partner has the right, but not the obligation, to purchase all of the remaining common units at a price not less than the then-current market price of |

13

| | the common units. See “The Partnership Agreement — Limited Call Right.” At the end of the subordination period, assuming no additional issuances of common units, our general partner and its affiliates will own 55.4% of the common units and general partner interests. |

Eligible Holders and redemption | Only Eligible Holders will be entitled to receive distributions or be allocated income or loss from us. Eligible Holders are: |

| | • | | individuals or entities subject to United States federal income taxation on the income generated by us; or |

| | • | | entities not subject to United States federal taxation on the income generated by us, so long as all of the entity’s owners are subject to such taxation. |

| | We have the right, which we may assign to any of our affiliates, but not the obligation, to redeem all of the common and subordinated units of any holder that is not an Eligible Holder or that has failed to certify or has falsely certified that such holder is an Eligible Holder. The purchase price for such redemption would be equal to the lower of the holder’s purchase price and the then-current market price of the units. The redemption price will be paid in cash or by delivery of a promissory note, as determined by our general partner. |

| | See “Description of the Common Units — Transfer of Common Units” and “The Partnership Agreement — Non-Eligible Holders; Redemption.” |

Estimated ratio of taxable income to distributions | We estimate that if you own the common units you purchase in this offering through the record date for distributions for the period ending December 31, 2010, you will be allocated, on a cumulative basis, an amount of federal taxable income for that period that will be % or less of the cash distributed to you with respect to that period. For example, if you receive an annual distribution of $1.40 per unit, we estimate that your average allocable federal taxable income per year will be no more than $ per unit. See “Material Tax Consequences — Tax Consequences of Unit Ownership — Ratio of Taxable Income to Distributions” for the basis of this estimate. |

Material tax consequences | For a discussion of other material federal income tax consequences that may be relevant to prospective unitholders who are individual citizens or residents of the United States, see “Material Tax Consequences.” |

Exchange listing | We intend to apply to list our common units on The New York Stock Exchange under the symbol “HKE.” |

14

Summary Historical and Pro Forma Financial Data

The following section presents summary historical financial data for HK Energy Partners LP Predecessor, the predecessor to HK Energy Partners LP, and pro forma financial data of HK Energy Partners LP, as of the dates and for the periods indicated.

The statement of operations data for our predecessor for the years ended December 31, 2004, 2005 and 2006 and the balance sheet data as of December 31, 2005 and 2006 set forth below are derived from our audited carve out financial statements and the notes thereto included elsewhere in this document. The statement of operations data for our predecessor for the six months ended June 30, 2007 and 2006 and the balance sheet data as of June 30, 2007 are derived from our unaudited carve out financial statements included elsewhere in this document and, in the opinion of management, include all adjustments (consisting only of normal recurring accruals) necessary for a fair presentation of the financial position and results of operations as of the dates and for the periods indicated. The carve out financial statements of our predecessor are comprised of oil and natural gas assets, liabilities and operations located in the Permian Basin of West Texas and New Mexico currently owned by Petrohawk, which we refer to as the partnership properties, and which we will acquire upon completion of this offering. Due to the factors described in “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” our future results of operations may not be comparable to HK Energy Partners LP Predecessor’s historical results. The results for periods of less than a full year are not necessarily indicative of the results to be expected for any interim period or for a full year.

The summary pro forma statement of operations data presented for the year ended December 31, 2006 and as of and for the six months ended June 30, 2007 for HK Energy Partners LP give pro forma effect to the following as if all transactions had been completed on January 1, 2006:

| | • | | the acquisition by Petrohawk of KCS Energy, Inc. on July 12, 2006; |

| | • | | our entrance into the contribution agreement, pursuant to which: |

| | • | | our general partner and another subsidiary of Petrohawk will contribute all of the partnership properties to us; |

| | • | | we will issue 5,904,048 common units and 5,189,742 subordinated units to wholly owned subsidiaries of Petrohawk, representing an aggregate 53.4% limited partner interest in us as partial consideration for such contribution; |

| | • | | we will sell 9,250,000 common units to the public in this offering, representing a 44.6% limited partner interest in us, and will use the proceeds as described in “Use of Proceeds”; and |

| | • | | we will issue to HK Energy Partners GP LP a 2% general partner interest in us and all of our incentive distribution rights, which will entitle our general partner to increasing percentages of the cash we distribute in excess of $0.4025 per unit per quarter (115% of the minimum quarterly distribution); |

| | • | | expected borrowings of $165.0 million in term debt under our credit facility, which will be secured by $165.0 million of qualifying investment grade securities, and distribution of the funds to our general partner and another subsidiary of Petrohawk as partial consideration for the partnership properties contributed to us; |

| | • | | expected borrowings of $58.1 million in revolving debt under our credit facility and distribution of the funds to our general partner and another subsidiary of Petrohawk as partial consideration for the partnership properties contributed to us; |

| | • | | the entrance by us into an administrative services agreement with Petrohawk, HK Management and our general partner pursuant to which we will reimburse Petrohawk and its affiliates $5.7 million in allocated general and administrative costs, including $2.8 million in incremental costs related to being a publicly traded partnership. |

15

The unaudited pro forma balance sheet assumes the transactions listed above occurred on June 30, 2007. The summary pro forma financial data is derived from pro forma financial statements of HK Energy Partners LP included elsewhere in this prospectus.

You should read the following table in conjunction with “ — Formation Transactions and Partnership Structure,” “Use of Proceeds,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” the historical carve out financial statements of HK Energy Partners LP Predecessor, and the unaudited pro forma financial statements of HK Energy Partners LP included elsewhere in this prospectus. Among other things, those historical and pro forma financial statements include more detailed information regarding the basis of presentation for the following information.

The following table presents summary historical financial information for HK Energy Partners LP Predecessor as well as summary pro forma data for HK Energy Partners LP. Also included in this table is a non-GAAP financial measure, Adjusted EBITDA, which we use in our business. This measure is not calculated or presented in accordance with accounting principles generally accepted in the United States of America (“GAAP”). We explain this measure below and reconcile it to the most directly comparable financial measures calculated and presented in accordance with GAAP.

| | | | | | | | | | | | | | | | | | | | |

| | | HK Energy Partners LP Predecessor | | | Pro Forma HK Energy Partners LP | |

| | | Year Ended December 31,

2006 | | | Six Months Ended June 30, | | | Year Ended December 31,

2006 | | | Six Months Ended June 30, 2007 | |

| | | | 2006 | | | 2007 | | | |

| | | (in thousands except per unit data) | |

Operating revenues: | | | | | | | | | | | | | | | | | | | | |

Oil and natural gas | | $ | 59,578 | | | $ | 22,225 | | | $ | 37,272 | | | $ | 78,285 | | | $ | 37,272 | |

Operating expenses: | | | | | | | | | | | | | | | | | | | | |

Production: | | | | | | | | | | | | | | | | | | | | |

Lease operating | | | 8,694 | | | | 3,550 | | | | 5,536 | | | | 10,328 | | | | 5,536 | |

Workover and other | | | 198 | | | | 9 | | | | 38 | | | | 247 | | | | 38 | |

Taxes other than income | | | 5,606 | | | | 1,727 | | | | 3,664 | | | | 7,467 | | | | 3,664 | |

Gathering, transportation and other | | | 878 | | | | 158 | | | | 824 | | | | 1,483 | | | | 824 | |

Impairment expense | | | 53,190 | | | | — | | | | — | | | | 53,190 | | | | — | |

General and administrative | | | 4,683 | | | | 1,711 | | | | 2,873 | | | | 5,723 | | | | 2,861 | |

Depletion, depreciation and amortization | | | 23,740 | | | | 7,052 | | | | 13,034 | | | | 30,617 | | | | 13,034 | |

| | | | | | | | | | | | | | | | | | | | |

Total operating expenses | | | 96,989 | | | | 14,207 | | | | 25,969 | | | | 109,055 | | | | 25,957 | |

| | | | | | | | | | | | | | | | | | | | |

(Loss) income from operations | | | (37,411 | ) | | | 8,018 | | | | 11,303 | | | | (30,770 | ) | | | 11,315 | |

Interest expense and other | | | (18,953 | ) | | | (7,442 | ) | | | (11,882 | ) | | | (5,042 | ) | | | (2,521 | ) |

| | | | | | | | | | | | | | | | | | | | |

(Loss) income before income taxes | | $ | (56,364 | ) | | $ | 576 | | | $ | (579 | ) | | $ | (35,812 | ) | | $ | 8,794 | |

Income tax provision | | | (714 | ) | | | (576 | ) | | | (50 | ) | | | (714 | ) | | | (50 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net (loss) income | | $ | (57,078 | ) | | $ | — | | | $ | (629 | ) | | $ | (36,526 | ) | | $ | 8,744 | |

| | | | | | | | | | | | | | | | | | | | |

Pro forma net (loss) income per limited partner unit | | | | | | | | | | | | | | $ | (2.36 | ) | | $ | 0.57 | |

Adjusted EBITDA | | $ | 39,519 | | | $ | 15,070 | | | $ | 24,337 | | | $ | 53,037 | | | $ | 24,349 | |

Balance sheet data (at period end): | | | | | | | | | | | | | | | | | | | | |

Working capital | | | | | | | | | | | | | | | | | | $ | 171,747 | |

Total assets | | | | | | | | | | | | | | | | | | | 766,940 | |

Long-term debt | | | | | | | | | | | | | | | | | | | 223,120 | |

Owner’s equity | | | | | | | | | | | | | | | | | | | 531,513 | |

| | | | | |

Cash flow data: | | | | | | | | | | | | | | | | | | | | |

Net cash provided by (used in): | | | | | | | | | | | | | | | | | | | | |

Operating activities | | $ | 15,292 | | | $ | 7,223 | | | $ | 11,306 | | | | | | | | | |

Investing activities | | | (311,683 | ) | | | (6,311 | ) | | | (8,532 | ) | | | | | | | | |

Financing activities | | | 296,391 | | | | (912 | ) | | | (2,774 | ) | | | | | | | | |

16

Adjusted EBITDA

We use EBITDA, adjusted as described below, which we refer to in this prospectus as Adjusted EBITDA, as a supplemental measure of our performance that is not required by, or presented in accordance with, GAAP. We define Adjusted EBITDA as net income plus (i) impairment expense, (ii) depletion, depreciation, and amortization, (iii) interest expense and other and (iv) income taxes. We present Adjusted EBITDA because we consider it an important supplemental measure of our performance, and in particular because it excludes amounts that do not relate directly to our operating performance. Because the use of Adjusted EBITDA facilitates comparisons of our historical operating performance on a more consistent basis, we use this measure for business planning and analysis purposes, in assessing acquisition opportunities and in determining how potential external financing sources are likely to evaluate our business.

Adjusted EBITDA is not a measurement of our financial performance under GAAP and should not be considered as an alternative to net income, operating income or any other performance measure derived in accordance with GAAP, as an alternative to cash flow from operating activities or as a measure of our liquidity. You should not assume that the Adjusted EBITDA amounts shown in this prospectus are comparable to Adjusted EBITDA amounts disclosed by other companies. In evaluating Adjusted EBITDA, you should be aware that it excludes expenses that we will incur in the future on a recurring basis.

Adjusted EBITDA has limitations as an analytical tool, and you should not consider it in isolation. Some of its limitations are:

| | • | | it does not reflect our cash expenditures for capital expenditures; |

| | • | | it does not reflect our interest expense, or the cash requirements necessary to service interest or principal payments on our indebtedness; and |

| | • | | although depletion, depreciation, and amortization are non-cash charges, the assets being depreciated and amortized will often have to be replaced in the future, and Adjusted EBITDA does not reflect the cost or cash requirements for such replacements. |

We compensate for these limitations by relying primarily on our GAAP results and using Adjusted EBITDA only supplementally. For more information, see our combined financial statements and the notes to those statements included elsewhere in this prospectus. The following table reconciles our net income before income taxes to our Adjusted EBITDA on a historical and pro forma basis as of the dates shown (in thousands):

| | | | | | | | | | | | | | | | | | |

| | | HK Energy Partners LP Predecessor | | | Pro Forma HK Energy Partners LP |

| | | Year Ended December 31, 2006 | | | Six Months Ended

June 30, | | | Year Ended December 31,

2006 | | | Six Months Ended June 30, 2007 |

| | | 2006 | | 2007 | | | |

| | | (in thousands) |

Net (loss) income | | $ | (57,078 | ) | | $ | — | | $ | (629 | ) | | $ | (36,526 | ) | | $ | 8,744 |

Impairment expense | | | 53,190 | | | | — | | | — | | | | 53,190 | | | | — |

Depletion, depreciation and amortization | | | 23,740 | | | | 7,052 | | | 13,034 | | | | 30,617 | | | | 13,034 |

Interest expense and other | | | 18,953 | | | | 7,442 | | | 11,882 | | | | 5,042 | | | | 2,521 |

Income tax provision | | | 714 | | | | 576 | | | 50 | | | | 714 | | | | 50 |

| | | | | | | | | | | | | | | | | | |

Adjusted EBITDA | | $ | 39,519 | | | $ | 15,070 | | $ | 24,337 | | | $ | 53,037 | | | $ | 24,349 |

| | | | | | | | | | | | | | | | | | |

17

Summary Reserve and Operating Data

The following tables show our estimated net proved oil and natural gas reserves based on reserve reports prepared by NSAI, our independent petroleum engineers, and certain summary unaudited information regarding production and sales of oil and natural gas with respect to such properties. You should refer to “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Business — Oil and Natural Gas Data — Oil and Natural Gas Reserves” in evaluating the material presented below.

| | | | | | |

| | | December 31, 2006(1) | | | June 30,

2007(1) | |

Reserve Data: | | | | | | |

Estimated net proved reserves: | | | | | | |

Oil (MMBbls) | | 6.8 | | | 6.8 | |

Natural gas (Bcf)(2) | | 107.7 | | | 104.7 | |

Total (Bcfe) | | 148.6 | | | 145.3 | |

Proved developed (Bcfe) | | 119.6 | | | 115.4 | |

Proved undeveloped (Bcfe) | | 29.0 | | | 29.9 | |

Proved developed reserves as % of total estimated net proved reserves | | 80 | % | | 79 | % |

% Natural gas(2) | | 72 | % | | 72 | % |

| (1) | Our estimates of proved reserves have been made in accordance with SEC guidelines using constant oil and natural gas prices and operating costs at the date indicated and are based on the December 31, 2006 West Texas Intermediate posted price of $57.75 per Bbl of oil and Henry Hub spot market price of $5.63 per MMBtu of gas and the June 30, 2007 West Texas Intermediate posted price of $67.25 per Bbl of oil and Henry Hub spot market price of $6.80 per MMBtu of gas. |

| (2) | Includes NGL volumes calculated using natural gas equivalents of six Mcf of natural gas per Bbl of oil or NGL. |

| | | | | | | | | |

| | | Year Ended December 31, 2006 | | Six Months Ended

June 30, 2007 |

| | | HK Energy Partners LP | | HK Energy

Partners LP | | HK Energy

Partners LP |

| | | Predecessor | | Pro Forma(1) | | Pro Forma(1) |

Production: | | | | | | | | | |

Oil (MBbl) | | | 356 | | | 361 | | | 171 |

Natural gas (MMcf)(2) | | | 5,646 | | | 7,951 | | | 3,746 |

Total production (MMcfe) | | | 7,780 | | | 10,116 | | | 4,772 |

Average daily production (MMcfe/d) | | | 21.3 | | | 27.7 | | | 26.3 |

| | | |

Average price per unit (excluding hedges): | | | | | | | | | |

Oil (per Bbl) | | $ | 58.95 | | $ | 59.03 | | $ | 54.88 |

Gas (per Mcf) | | | 6.72 | | | 7.08 | | | 7.38 |

| | | |

Average cost per Mcfe: | | | | | | | | | |

Lease operating expenses | | $ | 1.12 | | $ | 1.02 | | $ | 1.16 |

Other operating expenses(3) | | | 0.14 | | | 0.17 | | | 0.18 |

Taxes other than income | | | 0.72 | | | 0.74 | | | 0.77 |

| (1) | The unaudited pro forma combined statements of operations gives effect to the formation of the partnership, the contribution to the partnership by affiliates of Petrohawk of all of the partnership properties, and certain other transactions as if they had occurred on January 1, 2006. |

| (2) | Includes NGL volumes calculated using natural gas equivalents of six Mcf of natural gas per Bbl of NGL. |

| (3) | Includes workover and gathering, transportation and other expenses. |

18

RISK FACTORS

Limited partner interests are inherently different from capital stock of a corporation, although many of the business risks to which we are subject are similar to those that would be faced by a corporation engaged in similar businesses. You should consider carefully the following risk factors together with all of the other information included in this prospectus in evaluating an investment in our common units.

If any of the following risks were actually to occur, our business, financial condition or results of operations could be materially adversely affected. In that case, we might not be able to pay the minimum quarterly distribution on our common units, the trading price of our common units could decline and you could lose all or part of your investment.

Risks Related to Our Business

We may not have sufficient cash flow from operations to pay the minimum quarterly distribution on our common units following establishment of cash reserves and payment of fees and expenses, including reimbursement of expenses to our general partner and Petrohawk.

Our pro forma cash available for distribution for the year ended December 31, 2006 and the twelve months ended June 30, 2007, would have been sufficient to pay only 44% and 84%, respectively, of the minimum quarterly distributions on our common units for those periods. To make our cash distributions at our minimum quarterly distribution rate of $0.35 per common unit per quarter, or $1.40 per unit per year, we will require available cash of approximately $7.3 million per quarter, or $29.1 million per year, based on the total common and subordinated units and general partner interests outstanding immediately after completion of this offering. We may not have sufficient available cash from operating surplus each quarter to enable us to make cash distributions at the minimum quarterly distribution rate under our cash distribution policy. The amount of cash we can distribute on our common units principally depends upon the amount of cash we generate from our operations, which will fluctuate from quarter to quarter based on, among other things:

| | • | | the amount of oil and natural gas we produce; |

| | • | | the prices at which we sell our oil and natural gas production; |

| | • | | our ability to acquire additional oil and natural gas properties at economically attractive prices; |

| | • | | cash settlement of hedging positions; |

| | • | | the amount of cash reserves, which we expect to be substantial, established by our general partner for the proper conduct of our business and for capital expenditures to maintain our production levels over the long-term; |

| | • | | the level of our operating and administrative costs; |

| | • | | the level of our interest expense, which depends on the amount of our indebtedness and the interest payable thereon; and |

| | • | | timing and collectibility of receivables. |

In addition, the actual amount of cash we will have available for distribution will depend on other factors, some of which are beyond our control, including:

| | • | | the level of competition we face; |

| | • | | government regulation and taxation; |

| | • | | fluctuations in our working capital needs; |

| | • | | our ability to borrow funds and access capital markets; and |

| | • | | prevailing economic conditions. |

19

As a result of these factors, the amount of cash we distribute to our common unitholders may fluctuate significantly from quarter to quarter and may be less than the minimum quarterly distribution amount that we expect to distribute. For a description of additional restrictions and factors that may affect our ability to make cash distributions, see “Our Cash Distribution Policy and Restrictions on Distributions.”

The amount of cash we have available for distribution to holders of our common units depends primarily on our cash flow.

You should be aware that the amount of cash we have available for distribution depends primarily upon our cash flow, including financial reserves, working capital or other borrowing, and not solely on profitability, which will be affected by non-cash items. As a result, we may make cash distributions during periods when we record losses for financial accounting purposes and may not make cash distributions during periods when we record net income for financial accounting purposes.

Our estimate of the minimum Adjusted EBITDA necessary for us to make a distribution on all units at the minimum quarterly distribution rate for each of the four quarters ending December 31, 2008 is based on assumptions that are inherently uncertain and are subject to significant business, economic, financial, legal, regulatory and competitive risks and uncertainties that could cause actual results to differ materially from those estimated.

Our estimate of the minimum Adjusted EBITDA necessary for us to make a distribution on all units at the minimum quarterly distribution rate for each of the four quarters ending December 31, 2008, as set forth in “Our Cash Distribution Policy and Restrictions on Distributions,” is based on our management’s calculations, and we have not received an opinion or report on it from any independent accountants. This estimate is based on assumptions about development activities, production, oil and natural gas prices, settlements under commodity derivative contracts, capital expenditures, expenses, borrowings and other matters that are inherently uncertain and are subject to significant business, economic, financial, legal, regulatory and competitive risks and uncertainties that could cause actual results to differ materially from those estimated. If any of these assumptions prove to have been inaccurate, our actual results may differ materially from those set forth in our estimates, and we may be unable to pay all or part of the minimum quarterly distribution on our common units.

If oil or natural gas prices decline significantly, our cash flow from operations will decline and we may have to lower our distributions or may not be able to pay distributions at all.

Our revenue, profitability and cash flow depend upon the prices for oil and natural gas. The prices we receive for oil and natural gas production are volatile and a drop in prices can significantly affect our financial results and impede our growth, including our ability to maintain or increase our borrowing capacity, to repay current or future indebtedness and to obtain additional capital on attractive terms, all of which can affect our ability to pay distributions. Changes in oil and natural gas prices have a significant impact on the value of our reserves and on our cash flow. Prices for oil and natural gas may fluctuate widely in response to relatively minor changes in the supply and demand, market uncertainty and a variety of additional factors that are beyond our control, such as:

| | • | | the domestic and foreign supply of oil and natural gas; |

| | • | | the ability of members of the Organization of Petroleum Exporting Countries, or OPEC, and other producing countries to agree upon and maintain prices and production levels; |

| | • | | political instability, armed conflict or terrorist attacks, whether or not in oil or natural gas producing regions; |

| | • | | the level of consumer product demand; |

| | • | | the growth of consumer product demand in emerging markets, such as China; |

| | • | | labor unrest in oil and natural gas producing regions; |

20

| | • | | weather conditions, including hurricanes and other natural occurrences that affect the supply of and/or demand for oil and natural gas; |

| | • | | the price and availability of alternative fuels; |

| | • | | the price of foreign imports; and |

| | • | | worldwide economic conditions. |

In the past, the prices of oil and natural gas have been extremely volatile, and we expect this volatility to continue. For example, during the year ended December 31, 2006, the NYMEX oil price ranged from a high of $77.03 per Bbl to a low of $55.81 per Bbl. During 2006, the NYMEX Henry Hub natural gas price ranged from a high of $9.87 per MMBtu to a low of $3.63 per MMBtu. NYMEX closing oil and natural gas prices at December 31, 2006 were $57.75 per Bbl of oil and $5.63 per MMBtu of natural gas. At June 30, 2007, the NYMEX closing oil price had increased from December 31, 2006 to $70.68 per Bbl, while the NYMEX closing natural gas price had increased to $6.77 per MMBtu. At October 15, 2007, the NYMEX closing oil and natural gas prices for 2008 were $81.02 per Bbl of oil and $8.15 per MMBtu of natural gas. These volatile changes, particularly in natural gas prices, will also correspondingly affect the standardized measure of discounted future net cash flows of our net estimated proved reserves.

Lower oil or gas prices may not only decrease our revenues, but also reduce the amount of oil or gas that we can produce economically. This may result in our having to make substantial downward adjustments to our estimated proved reserves. If this occurs, or if our estimates of development costs increase, production data factors change or drilling results deteriorate, accounting rules may require us to write down, as a non-cash charge to earnings, the carrying value of our oil and natural gas properties for impairments. We are required to perform impairment tests on our assets whenever events or changes in circumstances lead to a reduction of the estimated useful life or estimated future cash flows that would indicate that the carry amount may not be recoverable or whenever management’s plans change with respect to those assets. We may incur impairment charges in the future, which could have a material adverse effect on our results of operations in the period taken and our ability to borrow funds under our credit facility, which may adversely affect our ability to make cash distributions to our unitholders.

Our credit facility will likely contain substantial restrictions and financial covenants that may restrict our business and financing activities and our ability to pay distributions.

The credit facility that we expect to enter into upon the closing of this offering, and any future financing agreements that we may enter into, will likely contain operating and financial restrictions and covenants that may restrict our ability to finance future operations or capital needs or to engage, expand or pursue our business activities or to pay distributions. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Capital Resources and Liquidity — Credit Facility.”

Our ability to comply with the restrictions and covenants in our credit facility in the future is uncertain and will be affected by the levels of cash flow from our operations and events or circumstances beyond our control. If market or other economic conditions deteriorate, our ability to comply with these covenants may be impaired. If we violate any of the restrictions, covenants, ratios or tests in our credit facility, a significant portion of our indebtedness may become immediately due and payable, our ability to make distributions will be inhibited and our lenders’ commitment to make further loans to us may terminate. We might not have, or be able to obtain, sufficient funds to make these accelerated payments. In addition, our obligations under our credit facility will be secured by substantially all of our assets, and if we are unable to repay our indebtedness under our credit facility, the lenders could seek to foreclose on our assets.

Our credit facility will likely limit the amounts we can borrow to a borrowing base amount, to be determined by the lenders in their sole discretion. Outstanding borrowings in excess of the borrowing base will be required to be repaid immediately, or we will be required to pledge other oil and natural gas properties as additional collateral.

21

Unless we replace the oil and natural gas reserves we produce, our revenues and production will decline, which would adversely affect our cash flow from operations and our ability to make distributions to our unitholders.