UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For fiscal year ended December 31, 2015

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report______________

For the transition period from __________ to ___________

Commission file number 001-34477

FINCERA INC.

(Exact name of the Registrant as specified in its charter)

N/A

(Translation of Registrant’s name into English)

Cayman Islands

(Jurisdiction of incorporation or organization)

27/F, Kai Yuan Finance Center, No. 5, East Main Street

Shijiazhuang, Hebei

People’s Republic of China

Tel: +86 311 8382 7688

Fax: +86 311 8381 9636

(Address of principal executive offices)

Yong Hui Li

27/F, Kai Yuan Finance Center, No. 5, East Main Street

Shijiazhuang, Hebei

People’s Republic of China

Tel: +86 311 8382 7688

Fax: +86 311 8381 9636

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of Each Class | | Name of each exchange on which registered |

| Ordinary Shares, par value $0.001 per share | | OTC QB |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

N/A

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

Indicate the number of outstanding shares of each of the Issuer’s classes of capital or ordinary shares as of the close of the period covered by the annual report: 23,550,993 ordinary shares, par value $0.001 per share, as of December 31, 2015.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ¨ Yes x No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.¨

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).x Yes ¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer or a non-accelerated filer.

| ¨ Large Accelerated filer | | x Accelerated filer | | ¨ Non-accelerated filer |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| x US GAAP | | ¨ International Financial | | ¨ Other |

| | | Reporting Standards as issued by | | |

| | | the International Accounting | | |

| | | Standards Board | | |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

¨ Item 17 ¨ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

¨ Yes x No

Table of Contents

CERTAIN INFORMATION

Unless otherwise indicated and except where the context otherwise requires, in this Annual Report on Form 20-F references to:

| | · | “Fincera”, “we,” “us”, “our” or “Company” refer to Fincera Inc. (together with its subsidiaries and affiliated entities); |

| | · | “ACG” refers to AutoChina Group Inc. (together with its subsidiaries and affiliated entities); |

| | · | “Auto Kaiyuan Companies” refers to Kaiyuan Logistics, Kaiyuan Auto Trade Co., Ltd. (“Kaiyuan Auto Trade”), and Hebei Xuhua Trading Co., Ltd.; |

| | · | “PRC” or “China” refer to the People’s Republic of China; |

| | · | “dollars” or “$” refer to the legal currency of the United States; and |

| | · | “Renminbi” or “RMB” refer to the legal currency of China. |

FORWARD-LOOKING STATEMENTS

We believe that some of the information in this Annual Report on Form 20-F constitutes forward-looking statements within the definition of the Private Securities Litigation Reform Act of 1995. You can identify these statements by forward-looking words such as “may,” “expect,” “anticipate,” “contemplate,” “believe,” “estimate,” “intends,” and “continue” or similar words. You should read statements that contain these words carefully because they discuss future expectations, contain projections of future results of operations or financial condition or state other “forward-looking” information.

We believe it is important to communicate our expectations to our security holders. However, there may be events in the future that we are not able to predict accurately or over which we have no control. The risk factors and cautionary language included in this Annual Report on Form 20-F provide examples of risks, uncertainties and events that may cause actual results to differ materially from the expectations described by us in such forward-looking statements, including among other things:

| | · | changing principles of generally accepted accounting principles; |

| | · | outcomes of government reviews, inquiries, investigations and related litigation; |

| | · | continued compliance with government regulations; |

| | · | legislation or regulatory environments, requirements or changes adversely affecting the financial industry in China; |

| | · | fluctuations in customer demand; |

| | · | management of rapid growth; |

| | · | general economic conditions; |

| | · | changes in government policy; |

| | · | the fluctuations in sales of commercial vehicles in China; |

| | · | China’s overall economic conditions and local market economic conditions; |

| | · | our ability to expand through strategic acquisitions and establishment of new locations; |

| | · | our business strategy and plans; |

| | · | the results of future financing efforts; and |

You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this Annual Report.

All forward-looking statements included herein attributable to us are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. Except to the extent required by applicable laws and regulations, we do not undertake any obligation to update these forward-looking statements to reflect events or circumstances after the date of this Annual Report or to reflect the occurrence of unanticipated events.

This Annual Report should be read in conjunction with our audited financial statements and the accompanying notes thereto, which are included in Item 18 of this Annual Report.

PART I

| ITEM 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

Not required.

| ITEM 2. | OFFER STATISTICS AND EXPECTED TIMETABLE |

Not required.

| A. | Selected financial data |

The following selected consolidated financial data as of December 31, 2015 and 2014 and for the years ended December 31, 2015, 2014 and 2013 have been derived from the audited consolidated financial statements of Fincera included in this Annual Report beginning on page F-1. The following summary consolidated financial data as of December 31, 2012 and 2011 and for the year ended December 31, 2012 and 2011 have been derived from the audited consolidated financial statements of Fincera. Such financial data is not included in this Annual Report. The consolidated financial data for all periods presented is retrospectively adjusted to reflect the merger under common control of Heat Planet Holdings Limited (“Heat Planet”) and its subsidiaries. Prior period amounts have been adjusted to exclude discontinued operations (refer to Note 3 for additional information). This information is only a summary and should be read together with the consolidated financial statements, the related notes, the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations of Fincera” and other financial information included in this Annual Report.

The consolidated financial statements are prepared and presented in accordance with generally accepted accounting principles in the United States, or “U.S. GAAP.” The results of operations of Fincera in any period may not necessarily be indicative of the results that may be expected for any future period. See “Risk Factors” included elsewhere in this Annual Report.

FINCERA INC. AND SUBSIDIARIES

Selected Consolidated Financial Data

(In thousands of U.S. Dollars, except per share amounts)

| | | As of December 31, | |

| | | 2015 | | | 2014 | | | 2013 | | | 2012 | | | 2011 | |

| | | | | | | | | | | | | | | | |

| Balance Sheet Data – | | | | | | | | | | | | | | | | | | | | |

| Cash and cash equivalents | | $ | 61,957 | | | $ | 26,027 | | | $ | 31,370 | | | $ | 75,777 | | | $ | 43,048 | |

| Restricted cash | | $ | 157 | | | $ | 988 | | | $ | 1,244 | | | $ | 160 | | | $ | 159 | |

| Total current assets | | $ | 654,237 | | | $ | 458,491 | | | $ | 469,625 | | | $ | 316,366 | | | $ | 434,852 | |

| Total assets | | $ | 750,315 | | | $ | 612,645 | | | $ | 553,119 | | | $ | 439,306 | | | $ | 554,466 | |

| Total current liabilities | | $ | 491,659 | | | $ | 325,783 | | | $ | 300,314 | | | $ | 210,946 | | | $ | 263,283 | |

| Total liabilities | | $ | 494,246 | | | $ | 349,593 | | | $ | 300,314 | | | $ | 210,946 | | | $ | 263,283 | |

| Total equity | | $ | 256,069 | | | $ | 263,052 | | | $ | 252,805 | | | $ | 228,360 | | | $ | 291,183 | |

| | | For the Years Ended December 31, | |

| | | 2015 | | | 2014 | | | 2013 | | | 2012 | | | 2011 | |

| | | | | | | | | | | | | | | | |

| Statement of Income Data – | | | | | | | | | | | | | �� | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| Income | | $ | 56,311 | | | $ | 5,375 | | | $ | 678 | | | $ | — | | | $ | — | |

| | | | | | | | | | | | | | | | | | | | | |

| Income (loss) from continuing operations before income taxes | | | 350 | | | | (19,720 | ) | | | (10,468 | ) | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | |

| Income tax provision (benefit) | | | 274 | | | | (3,398 | ) | | | (1,702 | ) | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | |

| Income (loss) from continuing operations | | | 76 | | | | (16,322 | ) | | | (8,766 | ) | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | |

| Income from discontinued operations, net of taxes | | | 8,205 | | | | 26,488 | | | | 20,594 | | | | 23,549 | | | | (25,151 | ) |

| | | | | | | | | | | | | | | | | | | | | |

| Net income (loss) attributable to shareholders | | $ | 8,281 | | | $ | 10,166 | | | $ | 11,828 | | | $ | 23,549 | | | $ | (25,151 | ) |

| | | | | | | | | | | | | | | | | | | | | |

| Earnings (loss) per share – | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| Basic | | | | | | | | | | | | | | | | | | | | |

| Continuing operations | | $ | 0.003 | | | $ | (0.69 | ) | | $ | (0.37 | ) | | $ | 1.00 | | | $ | 1.11 | |

| Discontinued operations | | | 0.35 | | | | 1.12 | | | | 0.87 | | | | — | | | | (0.04 | ) |

| | | $ | 0.35 | | | $ | 0.43 | | | $ | 0.50 | | | $ | 1.00 | | | $ | 1.07 | ) |

| Diluted | | | | | | | | | | | | | | | | | | | | |

| Continuing operations | | $ | 0.003 | | | $ | (0.68 | ) | | $ | (0.37 | ) | | $ | 0.99 | | | $ | 1.11 | |

| Discontinued operations | | | 0.34 | | | | 1.11 | | | | 0.87 | | | | — | | | | (0.04 | ) |

| | | $ | 0.34 | | | $ | 0.43 | | | $ | 0.50 | | | $ | 0.99 | | | $ | 1.07 | |

| B. | Capitalization and Indebtedness |

Not required.

| C. | Reasons for the Offer and Use of Proceeds |

Not required.

An investment in our securities involves risk. The discussion of risks related to our business contained in this Annual Report on Form 20-F comprises material risks of which we are aware. If any of the events or developments described actually occurs, our business, financial condition or results of operations would likely suffer. The discussion of risks related to our business contained in this Annual Report on Form 20-F also includes forward-looking statements, and our actual results may differ substantially from those discussed in these forward-looking statements. See “Cautionary Note Regarding Forward-Looking Statements.”

You should carefully consider the following risk factors, together with all of the other information included in this Annual Report on Form 20-F.

Risks Relating to our Business

We have recently made significant changes to our business model, and our new model may not be successful.

We have undergone a strategic shift which involves growing our new internet-based businesses (launched in 2014 and 2015) and ceasing our legacy commercial vehicle sales, leasing and support business. There is no guarantee that our new businesses will be successful, profitable or provide an equal or greater return on investment as compared to the businesses we are winding down.

Our changing business model, limited operating history and the new and evolving nature of our industry makes evaluating our future prospects difficult.

China’s internet-based financial services industry is relatively new and may not develop as expected. Its regulatory framework is also evolving and may remain uncertain for the foreseeable future.

Our first two internet-based businesses, the CeraVest lending platform and the CeraPay payments platform, were launched at the end of 2014. In October 2015 we launched the TruShip ecommerce platform. We are also in the process of developing and launching additional internet-based businesses. Our new businesses have a limited operating history. Therefore, it is difficult to effectively assess our future prospects. There are many risks and challenges we are subject to including, but not limited to:

| | · | Transitioning to new business models; |

| | · | Navigating an evolving regulatory environment; |

| | · | achieving and maintaining our profitability and margins; |

| | · | acquiring and retaining customers; |

| | · | attracting, training and retaining qualified personnel; |

| | · | broadening our product offering; |

| | · | maintaining adequate control over our costs and expenses; |

| | · | maintaining the security of our platforms and the confidentiality of the information provided and utilized across our platforms; |

| | · | managing credit risk in our portfolio of loans; |

| | · | responding to competitive and changing market conditions. |

If we are unsuccessful in addressing any of the above risks, our business may be materially and adversely affected.

If we fail to adequately assess, monitor and control the credit risks of our customers, we could experience an increase in credit loss.

We are subject to the credit risk of our customers. We use various methods to screen potential customers and establish appropriate credit limits, but these methods cannot eliminate all potential credit risks and may not always prevent us from approving customer applications that are not credit worthy or are fraudulently completed. Changes in our industry and customer demand may result in periodic increases to customer credit limits and spending and, as a result, could lead to increased credit losses. We may also fail to detect changes to the credit risk of customers over time. Further, during a declining economic environment, we experience increased customer defaults and preference claims by bankrupt customers. If we fail to adequately manage our credit risks, our bad debt expense could be significantly higher than historic levels and adversely affect our business, operating results and financial condition.

Significant defaults by financing customers could materially and adversely our business and results of operations.

We are subject to credit risk associated with potential loan defaults. If a significant number of customers fail to make payments when due, we may not be able to fully recover the outstanding principal of loans we make, which could significantly affect our profitability.

A security breach or malicious attack could damage our reputation, expose us to the risks of litigation and liability, disrupt our business or otherwise harm our results of operations.

In the normal course of business, we collect, process and retain sensitive and confidential customer information. Despite the security measures we have in place, which includes performing security scans, penetration testing and server activity monitoring, our facilities and systems, and those of third-party service providers, could be vulnerable to security breaches, acts of vandalism, computer viruses, misplaced or lost data, programming or human errors or other similar events. Any security breach or malicious attack involving the misappropriation, loss or other unauthorized disclosure of confidential information, whether by us or by third-party service providers, could damage our reputation, expose us to the risks of litigation and liability, disrupt our business or otherwise harm our results of operations.

The laws and regulations governing the internet-based finance industry in China are developing and evolving and subject to changes. If our practice is deemed to violate any PRC laws or regulations, we could be forced to change our business practices or be subject to penalties.

Due to the relatively short history of the internet finance industry in China, the regulatory framework governing our industry is still developing. On July 18, 2015 the People’s Bank of China, together with nine other PRC regulatory agencies, jointly issued a series of policy measures applicable to the industry titled the Guidelines on Promoting the Healthy Development of Internet Finance, or the Guidelines. The Guidelines introduced formally for the first time the regulatory framework and some basic principles for administering the industry in China. The Guidelines call for active government support of China’s internet finance industry and clarify the division of responsibility among regulatory agencies. The Guidelines specify that the China Banking Regulatory Commission, or the CBRC, will have primary regulatory responsibility for the online peer-to-peer lending service industry in China while the People’s Bank of China (“PBOC”) will oversee the online payment businesses. The Guidelines only set out the basic principles for promoting and administering the internet-based finance industry, and were not accompanied by any implementing rules. The Guidelines instead urge the relevant regulatory agencies to adopt implementing rules at the appropriate time.

On December 28, 2015 the CBRC issued draft rules for online lending in China for public opinion. As previously communicated in the Guidelines, the draft rules state that online lending platforms are designated as information intermediaries for borrowers and lenders, and should not participate in the transaction in any other way. The official preface to the rules states that the main purpose of the regulations is to promote risk management and establish ground rules to limit the prevalence of unsound practices and illegal activity in the industry. The draft rules also set forth a list of 12 prohibited activities:

| · | Using the platform for self-financing or for financing of related parties. |

| · | Directly or indirectly accepting and managing lender funds. |

| · | Providing guarantees to lenders or promising guaranteed returns on principal and interest. |

| · | Marketing or recommending loan investments to users that have not completed identification verification after registering on the platform. |

| · | Directly making loans to borrowers, unless stated otherwise by applicable laws and regulations. |

| · | Structuring loans into investment products with liquidity timing that differs from the original loan term. |

| · | Selling bank wealth management products, mutual funds, insurance annuities and other financial products. |

| · | Unless stated otherwise by applicable laws and regulations, collaborating with other investment or brokerage businesses to bundle, sell or broker investment products. |

| · | Providing false loan information or creating unrealistic return expectations. |

| · | Facilitating loans for the purpose of making investments in the stock market. |

| · | Providing equity crowdfunding or project crowdfunding platform services. |

| · | Other activities forbidden by applicable laws and regulations. |

The rules granted an 18-month transition period during which platforms can work toward full compliance as more detailed measures are revealed. We may need to modify our business practices to conform to the eventual final regulations. Doing so may adversely affect our ability to attract, retain or profitability service customers and therefore have a material adverse effect on our business.

Also on December 28, 2015, the PBOC issued the final rules on online payments for third party payment platforms. There are three main areas covered by the rules: 1.) strict know your customer (“KYC”) checks to support anti-money laundering and counter-terrorism efforts; 2.) limits on daily transaction volume to force payment platforms to focus on providing small e-commerce transaction services; and 3.) tiered regulation for platforms based on a government rating system instead of a blanket approach. The final online payment rules are set to take effect on July 1, 2016. Although our CeraPay product offers online payment processing services, we are not a licensed third party payment service provider. Therefore, it is unclear whether the PBOC rules on online payments would apply to us. We may need to modify our business practices to conform to the eventual final regulations. Doing so may adversely affect our ability to attract, retain or profitability service customers and therefore have a material adverse effect on our business.

As of the date of this filing, we have not been subject to any material fines or other penalties under any PRC laws or regulations including those governing the peer-to-peer lending service industry or online payments industry in China. Although regulations to date do not set out the liabilities that will be imposed on the service providers who fail to comply with the principles and requirements contained thereunder, nor do other applicable rules, laws and regulations contain specific liability provisions applicable to us. However, if our practice is deemed to violate any rules, laws or regulations, we may face injunctions, including orders to cease illegal activities, and may be exposed to other penalties as determined by the relevant government authorities as well. If such situations occur, our business, financial condition and prospects would be materially and adversely affected. In addition, given the evolving regulatory environment in which we operate, we cannot rule out the possibility that the PRC government will institute a licensing regime covering our industry. If such a licensing regime were introduced, we cannot assure you that we would be able to obtain any newly required license in a timely manner, or at all, which could materially and adversely affect our business and impede our ability to continue our operations. We currently do not hold any licenses or permits related to online payments or online lending.

The internet-based finance industry in China is becoming increasingly competitive and such increasing competition may limit our growth.

The internet-based finance industry in China is intensely competitive and evolving rapidly. Although we currently focus on the transportation industry vertical, in which we have many years of experience operating, there are a large number of broader internet-based financial product offerings that may compete with our products. With respect to lending competition, we primarily compete with offline boutique financing providers and in some cases internet-based financing providers. With respect to investors, we primarily compete with other investment products and asset classes, such as equities, bonds, investment trust products, bank savings accounts, real estate and alternative asset classes. If we are unable to compete effectively, our business and results of operations could be harmed. In addition, if we begin lending to other industries, we will face more competition in those markets from more established lenders.

New competition may also reduce our growth prospects or level of profitability. Competitors may also attempt to copy or replicate our business model. This could have an adverse effect on our business.

We have incurred net losses in the past and the new internet-based business may incur net losses in the future.

Our revenues of legacy commercial vehicle sales, leasing and support business have declined as a result of our strategic shift towards internet-based businesses. We cannot assure you that our new internet-based businesses will be able to generate sufficient revenues to generate net income in the future.

Fraudulent activity on our internet-based financial product platforms could negatively impact our operating results, brand and reputation and cause the use of our products to decrease.

We are subject to the risk of fraudulent activity on our internet-based platforms, primarily from prospective borrowers. Borrowers could use fraudulent means to procure credit that they would otherwise not be extended. Our resources, technologies and fraud detection tools may be insufficient to accurately detect and prevent such fraud from occurring. Significant increases in fraudulent activity could negatively impact our brand and reputation, reduce the volume of transactions facilitated through our platform and lead us to take additional steps to reduce fraud risk, which could increase our costs. High profile fraudulent activity could even lead to regulatory intervention, and may divert our management’s attention and cause us to incur additional expenses and costs. Although we have not experienced any material business or reputational harm as a result of fraudulent activities in the past, we cannot rule out the possibility that any of the foregoing may occur causing harm to our business or reputation in the future. If any of the foregoing were to occur, our results of operations and financial conditions could be materially and adversely affected.

Misconduct, errors and failure to function by our employees and third-party service providers could harm our business and reputation.

We are exposed to many types of operational risks, including the risk of misconduct and errors by our employees and third-party service providers. Our business depends on our employees and third-party service providers to interact with potential borrowers and investors, process large numbers of transactions and support the loan collection process, all of which involve the use and disclosure of personal information. We could be materially adversely affected if transactions were redirected, misappropriated or otherwise improperly executed, if personal information was disclosed to unintended recipients or if an operational breakdown or failure in the processing of transactions occurred, whether as a result of human error, purposeful sabotage or fraudulent manipulation of our operations or systems. In addition, the manner in which we store and use certain personal information and interact with borrowers and investors through our internet-based finance platforms is governed by various PRC laws. It is not always possible to identify and deter misconduct or errors by employees or third-party service providers, and the precautions we take to detect and prevent this activity may not be effective in controlling unknown or unmanaged risks or losses. If any of our employees or third-party service providers take, convert or misuse funds, documents or data or fail to follow protocol when interacting with borrowers and investors, we could be liable for damages and subject to regulatory actions and penalties. We could also be perceived to have facilitated or participated in the illegal misappropriation of funds, documents or data, or the failure to follow protocol, and therefore be subject to civil or criminal liability.

Furthermore, as we rely on certain third-party service providers, such as third-party payment platforms and custodian banks, to conduct our business, if these third-party service providers failed to function properly, we cannot assure you that we would be able to find an alternative in a timely and cost-efficient manner or at all. Any of these occurrences could result in our diminished ability to operate our business, potential liability to borrowers and investors, inability to attract borrowers and investors, reputational damage, regulatory intervention and financial harm, which could negatively impact our business, financial condition and results of operations.

Increases in fees incurred by third-party service providers could adversely affect our profitability.

We rely on certain third-party service providers, such as third-party payment platforms and custodian banks, to conduct our business. If these third-party service providers were to increase the fees that they charge us, our profitability could be adversely affected. Furthermore, we may not be able offset any increase in expenses incurred. We could also incur additional expenses to find other suitable third-party service providers.

A severe or prolonged downturn in the Chinese or global economy could materially reduce our revenues.

Any prolonged slowdown in the Chinese or global economy may have a negative impact on our business, results of operations and financial condition. In particular, general economic factors and conditions in China or worldwide, including the general interest rate environment and unemployment rates, may affect borrower willingness to seek loans and investor ability and desire to invest in loans. Economic conditions in China are sensitive to global economic conditions. The global financial markets have experienced significant disruptions since 2008 and the United States, Europe and other economies have experienced periods of recession. The recovery from the lows of 2008 and 2009 has been uneven and there are new challenges, including the escalation of the European sovereign debt crisis from 2011 and the slowdown of China’s economic growth since 2012 which may continue. There is considerable uncertainty over the long-term effects of the expansionary monetary and fiscal policies adopted by the central banks and financial authorities of some of the world’s leading economies, including the United States and China. There have also been concerns over unrest in Ukraine, the Middle East and Africa, which have resulted in volatility in financial and other markets, as well as concerns about the economic effect of the tensions in the relationship between China and surrounding Asian countries. If present Chinese and global economic uncertainties persist, many of our investors may delay or reduce their investment in the loans facilitated through our platform.

Adverse economic conditions could also reduce the number of qualified borrowers seeking loans on our CeraVest platform, as well as their ability to make payments. Should any of these situations occur, the amount of loans facilitated through CeraVest and our net revenues will decline, and our business and financial conditions will be negatively impacted. Additionally, continued turbulence in the international markets may adversely affect our ability to access the capital markets to meet liquidity needs.

Our operations depend on the performance of the internet infrastructure and fixed telecommunications networks in China.

Almost all access to the internet in China is maintained through state-owned telecommunication operators under the administrative control and regulatory supervision of the Ministry of Industry and Information Technology, or the MIIT. We primarily rely on a limited number of telecommunication service providers to provide us with data communications capacity through local telecommunications lines and internet data centers to host our servers. We have limited access to alternative networks or services in the event of disruptions, failures or other problems with China’s internet infrastructure or the fixed telecommunications networks provided by telecommunication service providers. With the expansion of our business, we may be required to upgrade our technology and infrastructure to keep up with the increasing traffic on our platform. We cannot assure you that the internet infrastructure and the fixed telecommunications networks in China will be able to support the demands associated with the continued growth in internet usage.

In addition, we have no control over the costs of the services provided by telecommunication service providers. If the prices we pay for telecommunications and internet services rise significantly, our results of operations may be adversely affected. Furthermore, if internet access fees or other charges to internet users increase, our user traffic may decline and our business may be harmed.

Any significant disruption in service on our platform or in our computer systems, including events beyond our control, could prevent us from processing payments or posting loans on our marketplace, reduce the attractiveness of our online products and result in a loss of users.

In the event of an outage affecting our internet-based businesses and physical data loss, our ability to perform our servicing obligations, process payments, process applications or make loans available to investors would be materially and adversely affected. The satisfactory performance, reliability and availability of our platforms and our underlying network infrastructure are critical to our operations, customer service, reputation and our ability to retain existing and attract new borrowers and investors. Much of our system hardware is hosted in a leased facility located in Beijing that is maintained and serviced by our IT Staff. We also periodically make backups to servers located at a separate facility also located in Beijing. Some internal systems are hosted on servers at our headquarters in Shijiazhuang, which would also disrupt our operations if affected. Our operations depend on our ability to protect our systems against damage or interruption from natural disasters, power or telecommunications failures, air quality issues, environmental conditions, computer viruses or attempts to harm our systems, criminal acts and similar events. If there is a lapse in service or damage to our leased Beijing facilities or our offices in Shijiazhuang, we could experience interruptions in our service as well as delays and additional expense in arranging new facilities.

Any interruptions or delays in our service, whether as a result of third-party error, our error, natural disasters or security breaches, whether accidental or willful, could harm our relationships with our borrowers and investors and our reputation. Additionally, in the event of damage or interruption, our insurance policies may not adequately compensate us for any losses that we may incur. Our disaster recovery plan has not been tested under actual disaster conditions, and we may not have sufficient capacity to recover all data and services in the event of an outage. These factors could prevent us from processing or posting payments on loans, damage our brand and reputation, divert our employees’ attention, subject us to liability and cause borrowers and investors to abandon our marketplace, any of which could adversely affect our business, financial condition and results of operations.

Our internet-based businesses and internal systems rely on software that is highly technical, and if it contains undetected errors, our business could be adversely affected.

Our internet-based businesses and internal systems rely on software that is highly technical and complex. For example, our CeraVest and CeraPay platforms and internal systems depend on the ability of such software to store, retrieve, process and manage immense amounts of data. The software on which we rely has contained, and may now or in the future contain, undetected errors or bugs. Some errors may only be discovered after the code has been released for external or internal use. Errors or other design defects within the software on which we rely may result in a negative experience for our customers, delay introductions of new features or enhancements, result in errors or compromise our ability to protect customer data or our intellectual property. Any errors, bugs or defects discovered in the software on which we rely could result in harm to our reputation, loss of customers or liability for damages, any of which could adversely affect our business, results of operations and financial conditions.

Competition for employees is intense, and we may not be able to attract and retain the qualified and skilled employees needed to support our business.

We believe our success depends on the efforts and talent of our employees, including risk management, software engineering, financial and marketing personnel. Our future success depends on our continued ability to attract, develop, motivate and retain qualified and skilled employees. Competition for highly skilled technical, risk management and financial personnel is extremely intense. We may not be able to hire and retain these personnel at compensation levels consistent with our existing compensation and salary structure. Some of the companies with which we compete for experienced employees have greater resources than we have and may be able to offer more attractive terms of employment.

In addition, we invest significant time and expenses in training our employees, which increases their value to competitors who may seek to recruit them. If we fail to retain our employees, we could incur significant expenses in hiring and training their replacements, and the quality of our services and our ability to serve borrowers and investors could diminish, resulting in a material adverse effect to our business.

Increases in labor costs in the PRC may adversely affect our profitability.

The economy in China has experienced increases in inflation and labor costs in recent years. As a result, average wages in the PRC are expected to continue to increase. In addition, we are required by PRC laws and regulations to pay various statutory employee benefits, including pension, housing fund, medical insurance, work-related injury insurance, unemployment insurance and maternity insurance to designated government agencies for the benefit of our employees. The relevant government agencies may examine whether an employer has made adequate payments to the statutory employee benefits, and those employers who fail to make adequate payments may be subject to late payment fees, fines and/or other penalties. We expect that our labor costs, including wages and employee benefits, will continue to increase. Unless we are able to control our labor costs or pass on these increased labor costs to our users by increasing the fees of our services, our financial condition and results of operations may be adversely affected.

If we fail to promote and maintain our brand in an effective and cost-efficient way, our ability to grow our business may be impaired.

We believe that developing and maintaining awareness of our brand effectively is critical to attracting new and retaining existing borrowers and investors to our marketplace. Successful promotion of our brand and our ability to attract qualified borrowers and sufficient investors depend largely on the effectiveness of our marketing efforts and the success of the channels we use to promote our marketplace. Our efforts to build our brand have caused us to incur significant expenses, and it is likely that our future marketing efforts will require us to incur significant additional expenses. These efforts may not result in increased revenues in the immediate future or at all and, even if they do, any increases in revenues may not offset the expenses incurred. If we fail to successfully promote and maintain our brand while incurring substantial expenses, our results of operations and financial condition would be adversely affected, which may impair our ability to grow our business.

Any harm to our brand or reputation or any damage to the reputation of the online finance industry may materially and adversely affect our business and results of operations.

Enhancing the recognition and reputation of our brand is critical to our business and competitiveness. Factors that are vital to this objective include but are not limited to our ability to:

| · | maintain the quality and reliability of our platforms; |

| · | provide borrowers and investors with a superior experience in our marketplace; |

| · | enhance and improve our credit assessment and decision-making models; |

| · | effectively manage and resolve borrower and investor complaints; and |

| · | effectively protect personal information and privacy of borrowers and investors. |

Any malicious or innocent negative allegation made by the media or other parties about our company, including but not limited to our management, business, compliance with law, financial conditions or prospects, whether with merit or not, could severely hurt our reputation and harm our business and operating results. As the market for online finance in China is new and the regulatory framework for this market is also evolving, negative publicity about this industry may arise from time to time. Negative publicity about China’s online consumer finance marketplace industry in general may also have a negative impact on our reputation, regardless of whether we have engaged in any inappropriate activities.

In addition, certain factors that may adversely affect our reputation are beyond our control. Negative publicity about our partners, outsourced service providers or other counterparties and any failure by them to adequately protect the information of borrowers and investors, to comply with applicable laws and regulations or to otherwise meet required quality and service standards could harm our reputation. Furthermore, any negative development in the online finance industry, such as bankruptcies or failures of other finance marketplaces, and especially a large number of such bankruptcies or failures, or negative perception of the industry as a whole, such as that arises from any failure of other finance marketplaces to detect or prevent money laundering or other illegal activities, even if factually incorrect or based on isolated incidents, could compromise our image, undermine the trust and credibility we have established and impose a negative impact on our ability to attract new borrowers and investors. Negative developments in the online finance industry, such as widespread borrower defaults, fraudulent behavior and/or the closure of other online consumer finance marketplaces, may also lead to tightened regulatory scrutiny of the sector and limit the scope of permissible business activities that may be conducted by online consumer finance marketplaces like us. If any of the foregoing takes place, our business and results of operations could be materially and adversely affected.

Our reputation may be harmed if information supplied by borrowers is inaccurate, misleading or incomplete, including if the borrowers use the loan proceeds for purposes other than as originally provided.

Borrowers supply a variety of information to us before we grant them a loan. Although we take steps to verify the information we receive from borrowers, it is possible that we are unable to detect all instances where a borrower provides false or misleading information. Although we also take steps to ensure a borrower uses loan proceeds for specified purposes, it is possible that we are unable to detect all instances where a borrower may use loan proceeds for other purposes that may involve increased risk than as originally provided.

We may not be able to prevent others from unauthorized use of our intellectual property, which could harm our business and competitive position.

We regard our trademarks, domain names, know-how, proprietary technologies and similar intellectual property as critical to our success, and we rely on a combination of intellectual property laws and contractual arrangements, including confidentiality, invention assignment and non-compete agreements with our employees and others to protect our proprietary rights.

It is often difficult to register, maintain and enforce intellectual property rights in China. Statutory laws and regulations are subject to judicial interpretation and enforcement and may not be applied consistently due to the lack of clear guidance on statutory interpretation. Confidentiality, invention assignment and noncompete agreements may be breached by counterparties, and there may not be adequate remedies available to us for any such breach. Accordingly, we may not be able to effectively protect our intellectual property rights or to enforce our contractual rights in China. Preventing any unauthorized use of our intellectual property is difficult and costly and the steps we take may be inadequate to prevent the misappropriation of our intellectual property. In the event that we resort to litigation to enforce our intellectual property rights, such litigation could result in substantial costs and a diversion of our managerial and financial resources. We can provide no assurance that we will prevail in such litigation. In addition, our trade secrets may be leaked or otherwise become available to, or be independently discovered by, our competitors. To the extent that our employees or consultants use intellectual property owned by others in their work for us, disputes may arise as to the rights in related know-how and inventions. Any failure in protecting or enforcing our intellectual property rights could have a material adverse effect on our business, financial condition and results of operations.

We may be subject to intellectual property infringement claims, which may be expensive to defend and may disrupt our business and operations.

We cannot be certain that our operations or any aspects of our business do not or will not infringe upon or otherwise violate trademarks, patents, copyrights, know-how or other intellectual property rights held by third parties. We may be from time to time in the future subject to legal proceedings and claims relating to the intellectual property rights of others. In addition, there may be third-party trademarks, patents, copyrights, know-how or other intellectual property rights that are infringed by our products, services or other aspects of our business without our awareness. Holders of such intellectual property rights may seek to enforce such intellectual property rights against us in China, the United States or other jurisdictions. If any third-party infringement claims are brought against us, we may be forced to divert management’s time and other resources from our business and operations to defend against these claims, regardless of their merits.

Additionally, the application and interpretation of China’s intellectual property right laws and the procedures and standards for granting trademarks, patents, copyrights, know-how or other intellectual property rights in China are still evolving and are uncertain, and we cannot assure you that PRC courts or regulatory authorities would agree with our analysis. If we were found to have violated the intellectual property rights of others, we may be subject to liability for our infringement activities or may be prohibited from using such intellectual property, and we may incur licensing fees or be forced to develop alternatives of our own. As a result, our business and results of operations may be materially and adversely affected.

Store closings result in unexpected costs that could result in write downs and expenses relating to the closings.

From time to time, in the ordinary course of our business, we may close certain underperforming office branches, generally based on considerations of branch profitability, competition, strategic factors and other considerations. Closing an office branch could subject us to costs, including the write-down of leasehold improvements, equipment, furniture and fixtures. In addition, we could remain liable for future lease obligations.

The loss of any key members of the management team may impair our ability to identify and secure new contracts with customers or otherwise manage our business effectively.

Our success depends, in part, on the continued contributions of our senior management. In particular, Mr. Yong Hui Li, our Chief Executive Officer, has been appointed by the Board of Directors to oversee and supervise the strategic direction and overall performance of Fincera.

Fincera relies on its senior management to manage its business successfully. In addition, the relationships and reputation that members of our management team have established and maintained with our customers contribute to our ability to maintain good customer relations, which is important to the direct selling strategy that we adopt. Employment contracts entered into between us and our senior management cannot prevent our senior management from terminating their employment, and the death, disability or resignation of Mr. Yong Hui Li or any other member of our senior management team may impair our ability to maintain business growth and identify and develop new business opportunities or otherwise to manage our business effectively.

We rely on our information technology, billing and credit control systems, and any problems with these systems could interrupt our operations, resulting in reduced cash flow.

Fincera’s business cannot be managed effectively without its integrated information technology system. Accordingly, we run various “real time” integrated information technology management systems for our financing business.

In addition, sophisticated billing and credit control systems are critical to our ability to increase revenue streams, avoid revenue loss and potential credit problems, and bill customers in a proper and timely manner. If adequate billing and credit control systems and programs are unavailable, or if upgrades are delayed or not introduced in a timely manner, or if we are unable to integrate such systems and software programs into our billing and credit systems, we may experience delayed billing which may negatively affect our cash flow and the results of operations.

In case of a failure of our data storage system, we may lose critical operational or billing data or important email correspondence with our customers and suppliers. Any such data stored in the core data center may be lost if there is a lapse or failure of the disaster recovery system in backing up these data, or if the periodic offline backup is insufficient in frequency or scope, which may result in reduced cash flow and reduce revenues.

Adverse economic conditions in Shijiazhuang, China that negatively impact the demand for office space may result in lower occupancy and rental rates for our property lease and management business, which would adversely affect its results of operations.

Generally speaking, economic growth and employment levels in a local market are important factors in determining how successful a local property lease and management business is. Since we only lease office space in one building that is located in Shijiazhuang, China, the economic conditions of this city are likely to be important factors in determining the occupancy levels and rental rates that our property lease and management business is able to achieve. Therefore, any deterioration in the economic conditions of Shijiazhuang may adversely affect the results of operations of our property lease and management business.

We face considerable competition in the leasing market and may be unable to renew existing leases or re-let space on terms similar to the existing leases, or we may spend significant capital in our efforts to renew and re-let space, which may adversely affect our results of operations.

In addition to seeking to increase our average occupancy by leasing current vacant space, we also concentrate our leasing efforts on renewing existing leases. Because we compete with a number of other developers, owners and operators of office and office-oriented, mixed-use properties, we may be unable to renew leases with our existing customers and, if our current customers do not renew their leases, we may be unable to re-let the space to new customers. To the extent that we are able to renew existing leases or re-let such space to new customers, heightened competition resulting from adverse market conditions may require us to utilize rent concessions and tenant improvements to a greater extent than we have historically. Further, changes in space utilization by our customers due to technology, economic conditions and business culture also affect the occupancy of our properties. As a result, customers may seek to downsize by leasing less space from us upon any renewal.

If our competitors offer space at rental rates below current market rates or below the rental rates we currently charge our customers, we may lose existing and potential customers, and we may be pressured to reduce our rental rates below those we currently charge in order to retain customers upon expiration of their existing leases. Even if our customers renew their leases or we are able to re-let the space, the terms and other costs of renewal or re-letting, including the cost of required renovations, increased tenant improvement allowances, leasing commissions, reduced rental rates and other potential concessions, may be less favorable than the terms of our current leases and could require significant capital expenditures. From time to time, we may also agree to modify the terms of existing leases to incentivize customers to renew their leases. If we are unable to renew leases or re-let space in a reasonable time, or if our rental rates decline or our tenant improvement costs, leasing commissions or other costs increase, our financial condition and results of operations of the property lease and management business could be materially adversely affected.

Bankruptcy or insolvency of tenants may decrease our revenue, net income and available cash.

The bankruptcy or insolvency of a major tenant could cause us to suffer lower revenues and operational difficulties, including leasing the remainder of the property. As a result, the bankruptcy or insolvency of a major tenant could result in decreased revenue, net income and funds available to pay our indebtedness.

Fincera’s ability to pay dividends and utilize cash resources of its subsidiaries is dependent upon the earnings of, and distributions by, Fincera’s subsidiaries and jointly-controlled enterprises, which could result in Fincera having little if any cash available for dividends.

Fincera is a holding company with substantially all of its business operations conducted through its subsidiaries. Fincera paid a special cash dividend in the amount of $0.25 per ordinary share in February 2012. Fincera does not currently intend to pay dividends in the near future. However, If Fincera did decide to pay dividends, Fincera’s ability to make future dividend payments would depend upon the receipt of dividends or distributions from its subsidiaries. The ability of its subsidiaries to pay dividends or other distributions may be subject to their earnings, financial position, cash requirements and availability, applicable laws and regulations and to restrictions on making payments to Fincera contained in financing or other agreements. These restrictions could reduce the amount of dividends or other distributions that Fincera receives from its subsidiaries, which could restrict its ability to fund its business operations and to pay dividends to its shareholders. Fincera’s future declaration of dividends may or may not reflect its historical declarations of dividends and will be at the absolute discretion of the Board of Directors.

Operating Fincera’s internet-based financial services requires a large amount of capital and its growth may require additional capital that may not be available on favorable terms or at all, which could limit our ability to continue our operations.

To the extent that the loans we extend to customers as part of our internet-based businesses are not fully funded by investors on our CeraVest platform, we must find a way to fund the shortfall ourselves. We have, in the past, entered into loan agreements in order to raise additional capital. Although we believe that our current cash, other loan facilities and financing arrangement with related parties will be sufficient to meet our present and reasonably anticipated cash needs, it may, in the future, require additional cash resources due to changed business conditions, implementation of our strategy to expand our branch network or other investments or acquisitions we may decide to pursue. If our own financial resources are insufficient to satisfy our capital requirements, we may seek to sell additional equity or debt securities or obtain additional credit facilities. The sale of additional equity securities could result in dilution to our shareholders. Our existing debt service obligations do not have any operating and financial covenants that would restrict our operations, however, the incurrence of indebtedness would result in increased debt service obligations and could require us to agree to operating and financial covenants that would restrict our operations. Financing may not be available in amounts or on terms acceptable to us, if at all. Any failure by Fincera to raise additional funds on terms favorable to us, or at all, could limit our ability to expand our business operations and could harm our overall business prospects.

A significant portion of our working capital is funded through loans from related parties of our Chairman and CEO, Mr. Yong Hui Li, that may be called by the lenders at any time, which could materially and adversely affect Fincera’s liquidity and Fincera’s ability to fund and expand its business.

As of December 31, 2015, we had outstanding borrowings from related parties of our Chairman and Chief Executive officer, Mr. Yong Hui Li, of approximately $48.2 million. These borrowings are interest bearing and for a perpetual term, but are callable at any time by the lenders. The lenders have not indicated to us if there is a maximum amount they are willing to lend to us, and there can be no assurance that they will lend us any more funds or that they will not call the loans for repayment. In the event such lenders determine to call these loans we will have to repay the loans from our cash reserves or financing provided by third-party financial institutions. There can be no assurance that we will have sufficient cash reserves or that we could secure additional financing from third parties on favorable terms or at all. If cash reserves or suitable financing were not available, we would have to divert working capital from growing our commercial leasing business, and we would not be able to expand our commercial leasing business as quickly as expected.

We may have difficulty adjusting our existing offerings to customers, including introducing new products and services, which could reduce our profits and growth.

As we have done in the past, we plan to continue adjusting our existing offerings to customers and to introduce new products and services such as our CeraVest and CeraPay businesses. Any inability to successfully modify our offerings or introduce new products and services that meet the demands of our customers could result in reduced profits and growth.

We do not have any business insurance coverage.

Insurance companies in China currently do not offer as extensive an array of insurance products as insurance companies in more developed economies. Currently, we do not have any business liability or disruption insurance to cover our operations. We have determined that the costs of insuring for these risks and the difficulties associated with acquiring such insurance on commercially reasonable terms make it impractical for us to have such insurance. Any uninsured business disruptions may result in our incurring substantial costs and the diversion of resources, which could have an adverse effect on our results of operations and financial condition.

Failure to make adequate contributions to various employee benefit plans as required by PRC regulations may subject us to penalties.

We are required under PRC laws and regulations to participate in various government sponsored employee benefit plans, including certain social insurance, housing funds and other welfare-oriented payment obligations, and contribute to the plans in amounts equal to certain percentages of salaries, including bonuses and allowances, of our employees up to a maximum amount specified by the local government from time to time at locations where we operate our businesses. The requirement of employee benefit plans has not been implemented consistently by the local governments in China given the different levels of economic development in different locations. We have not made adequate employee benefit payments in the past and we may be required to make up the contributions for these plans as well as to pay late fees and fines. If we are subject to late fees or fines in relation to the underpaid employee benefits, our profitability could be adversely affected.

If we cannot maintain our corporate culture as we grow, we could lose the innovation, collaboration and focus that contribute to our business.

We believe that a critical component of our success is our corporate culture, which we believe fosters innovation, encourages teamwork and cultivates creativity. As we continue to develop the infrastructure of a public company and continue to grow and change, we may find it difficult to maintain these valuable aspects of our corporate culture. Any failure to preserve our culture could negatively impact our future success, including our ability to attract and retain employees, encourage innovation and teamwork and effectively focus on and pursue our corporate objectives.

Our profitability will be adversely affected if we are unable to successfully collect receivables from our commercial vehicle sales, leasing and support business, which have been classified as discontinued operations.

We have discontinued our legacy truck leasing business by existing the leasing industry. This involves servicing the remaining leases and collecting the outstanding amounts due to us. If we are unable to effectively and efficiently collect these amounts, the profitability of this discontinued business segment will be reduced, which in turn will adversely affect our profitability.

Risks to Fincera’s Shareholders

Because FINRA did not allow our name change to be processed for trading purposes, you may have difficulty trading our stock.

In June 2015, we changed our name from AutoChina International Ltd. to Fincera Inc. to better suit our new internet-based business. However, FINRA did not allow our name change to be processed for trading purposes. This has resulted in a number of brokers advising us that they are unable to trade shares for their clients. Therefore, although our shares are still quoted under the symbol AUTCF, our shareholders may have difficulty trading our stock.

Because Fincera may not pay regular dividends on its ordinary shares, shareholders will generally benefit from an investment in Fincera’s ordinary shares only if the shares appreciate in value.

Although Fincera declared and paid a special cash dividend in the amount of $0.25 per ordinary share in February 2012 to its shareholders, Fincera has not declared any dividends since then and may not declare or pay any regular cash dividends on its ordinary shares in future. Fincera currently intends to retain future earnings, if any, for use in the operations and expansion of the business. As a result, Fincera does not anticipate paying regular cash dividends in the foreseeable future. Any future determination as to the declaration and payment of cash dividends will be at the discretion of Fincera’s Board of Directors and will depend on factors Fincera’s Board of Directors deems relevant, including among others, Fincera’s results of operations, financial condition and cash requirements, business prospects, and the terms of Fincera’s credit facilities and other financing arrangements. If no dividends are paid, realization of a gain on a shareholders’ investments will depend solely on the appreciation of the price of Fincera’s ordinary shares. There is no guarantee that Fincera’s ordinary shares will appreciate in value.

Our ordinary shares are quoted on the over the counter market, which may limit the liquidity and price of our ordinary shares more than if the ordinary shares were quoted or listed on a National Securities Exchange.

Our ordinary shares are currently quoted on the over the counter market, as opposed to being listed on a national securities exchange such as the Nasdaq Stock Market or the New York Stock Exchange. Quotation of our ordinary shares on the over the counter market limits the liquidity and price of our ordinary shares more than if the ordinary shares were quoted or listed on a national securities exchange. In addition, certain institutional investors may be prohibited from purchasing our ordinary shares because the ordinary shares are not listed on a national securities exchange.

Yong Hui Li, the Chairman and Chief Executive Officer of Fincera, is the beneficial owner of a substantial amount of Fincera’s ordinary shares and Mr. Li may take actions with respect to such shares which are not consistent with the interests of the other shareholders.

Yong Hui Li, the Chairman and Chief Executive Officer of Fincera, beneficially owns approximately 81.0% of the outstanding ordinary shares of Fincera as of the date of this Annual Report on Form 20-F, assuming that there are no other changes to the number of ordinary shares outstanding. Mr. Li may take actions with respect to such shares without the approval of other shareholders and which are not consistent with the interests of the other shareholders, including the election of the directors and other corporate actions of Fincera such as:

| | · | its merger with or into another company; |

| | · | a sale of substantially all of its assets; and |

| | · | amendments to its memorandum and articles of incorporation. |

The decisions of Mr. Li may conflict with Fincera’s interests or the interests of Fincera’s other shareholders.

Risks Related to Fincera’s Corporate Structure and Restrictions on its Industry

Contractual arrangements in respect of certain companies in the PRC may be subject to challenge by the relevant governmental authorities and may affect our investment and control over these companies and their operations.

Foreign ownership of internet-based businesses, such as distribution of online information, is subject to restrictions under current PRC laws and regulations. For example, foreign investors are not allowed to own more than 50% of the equity interests in a value-added telecommunication service provider (except e-commerce) and any such foreign investor must have experience in providing value-added telecommunications services overseas and maintain a good track record in accordance with the Guidance Catalog of Industries for Foreign Investment promulgated in 2007, as amended in 2011 and in 2015, respectively, and other applicable laws and regulations.

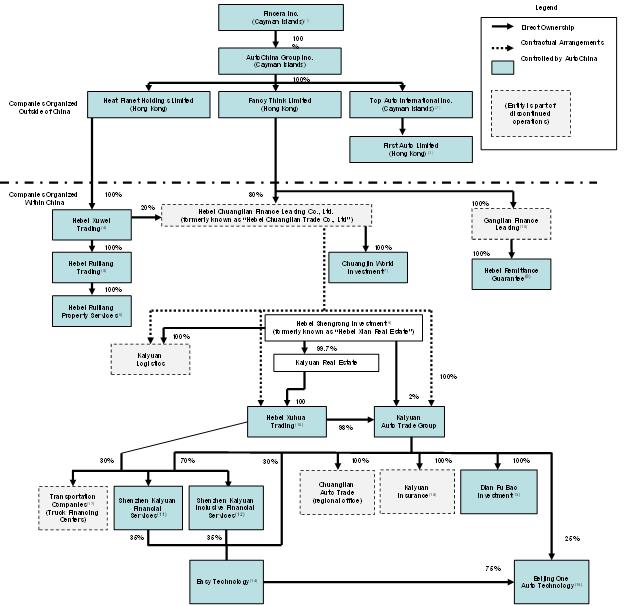

Since our wholly-owned subsidiary ACG is a Cayman Islands company and it holds the equity interests of its PRC subsidiaries indirectly through Fancy Think Limited, a Hong Kong company, our PRC subsidiaries are treated as foreign invested enterprises under PRC laws and regulations. To comply with PRC laws and regulations, we conduct our operations in China through a series of contractual arrangements, (the “Enterprise Agreements”), entered into with the Auto Kaiyuan Companies, Hebei Kaiyuan Real Estate Development Co., Ltd. (“Hebei Kaiyuan”) and Hebei Shengrong Investment Co., Ltd. (“Hebei Shengrong Investment”, under which with Hebei Kaiyuan are collectively known as the “AKC Shareholders”). Pursuant to the Enterprise Agreements, we, through our wholly-owned subsidiary ACG, have exclusive rights to obtain the economic benefits and assume the business risks of the Auto Kaiyuan Companies from their shareholders, and has control of the Auto Kaiyuan Companies. The Auto Kaiyuan Companies are considered variable interest entities, and Fincera is the primary beneficiary. ACG’s relationships with the Auto Kaiyuan Companies and the AKC Shareholders are governed by the Enterprise Agreements between Hebei Chuanglian Finance Leasing Co. Ltd. (“Chuanglian”), an indirect wholly-owned subsidiary of ACG, and each of the Auto Kaiyuan Companies, which are the operating companies of ACG in the PRC. The Auto Kaiyuan Companies hold and their subsidiaries hold the relevant business licenses to carry out the business.

Pursuant to these Enterprise Agreements, we are able to consolidate the financial results of the Auto Kaiyuan Companies, which are accounted for as VIEs of us under the prevailing accounting principles. There can be no assurance that the relevant governmental authority will not challenge the validity of these contractual arrangements or that the governmental authorities in the PRC will not promulgate laws or regulations to invalidate such arrangements in the future.

If Fincera’s ownership structure, contractual arrangements and businesses, or its PRC subsidiaries and Auto Kaiyuan Companies, are found to be in violation of any existing or future PRC laws or regulations, the relevant regulatory authorities would have broad discretion in dealing with such violations, including:

| | · | revoking the business and operating licenses of Fincera’s PRC subsidiaries or Auto Kaiyuan Companies, which business and operating licenses are essential to the operation of Fincera’s business; |

| | · | confiscating Fincera’s income or the income of its PRC subsidiaries or Auto Kaiyuan Companies; |

| | · | discontinuing or restricting our operations or the operations of Fincera’s PRC subsidiaries or Auto Kaiyuan Companies; |

| | · | imposing conditions or requirements with which Fincera, ACG, Fincera’s PRC subsidiaries or Auto Kaiyuan Companies may not be able to comply; |

| | · | requiring Fincera, Fincera’s PRC subsidiaries or Auto Kaiyuan Companies to restructure their relevant ownership structure, operations or contractual arrangements; |

| | · | restricting or prohibiting Fincera’s use of the proceeds from Fincera’s initial public offering to finance its business and operations in China; and |

| | · | taking other regulatory or enforcement actions that could be harmful to the business of the Auto Kaiyuan Companies. |

The Ministry of Commerce, or MOFCOM, published a discussion draft of the proposed Foreign Investment Law on January 19, 2015 which would replace the three existing laws regulating foreign investment in China (namely, the Sino-foreign Equity Joint Venture Enterprise Law, the Sinoforeign Cooperative Joint Venture Enterprise Law and the Wholly Foreign-invested Enterprise Law) together with their implementation rules and ancillary regulations. The draft Foreign Investment Law embodies an expected PRC regulatory trend to rationalize its foreign investment regulatory regime in line with prevailing international practice and the legislative efforts to unify the corporate legal requirements for both foreign and domestic investments. The draft Foreign Investment Law, if enacted as proposed, may materially impact the entire legal framework regulating the foreign investments in China and may also impact viability of our current corporate structure, corporate governance and business operations to some extent.

Among other things, the draft Foreign Investment Law expands the definition of foreign investment and introduces the principle of “actual control” in determining whether a company is considered a foreign-invested enterprise, or an FIE. As such, the jurisdiction of incorporation of an entity is not the ultimate determining factor as to whether or not it’s an FIE. The draft Foreign Investment Law specifically provides that entities established in China but “controlled” by foreign investors will be treated as FIEs, whereas an entity set up in a foreign jurisdiction would nonetheless be, upon market entry clearance by the MOFCOM or its local branches, treated as a PRC domestic investor provided that the entity is “controlled” by PRC entities and/or citizens. In this connection, “control” is broadly defined in the draft law to cover, among others, having the power to exert decisive influence, via contractual or trust arrangements, over the subject entity’s operations, financial matters or other key aspects of business operations. Once an entity is determined to be an FIE and its investment amount exceeds certain thresholds or its business operation falls within a “negative list”, to be separately issued by the State Counsel in the future, market entry clearance by the MOFCOM or its local braches would be required.

It is likely that we would not be considered as ultimately controlled by Chinese parties. To our knowledge, ultimate beneficial owners of our shares who are PRC nationals may not, in the aggregate, control more than 50% of our total voting power as of March 15, 2016. The draft Foreign Investment Law has not taken a position on what actions will be taken with respect to the existing companies with a VIE structure, whether or not these companies are controlled by Chinese parties, while it is soliciting comments from the public on this point by illustrating several possible options. Under these varied options, a company that has a VIE structure and conducts the business on the “negative list” at the time of enactment of the new Foreign Investment Law has either the option or obligation to disclose its corporate structure to the authorities, while the authorities, after reviewing the ultimate share control structure of the company, may either permit the company to continue to maintain the VIE structure (if the company is deemed ultimately controlled by PRC nationals), or require the company to dispose of its businesses and/or VIE structure based on circumstantial considerations. Moreover, it is uncertain whether online lending and online payments in which our variable interest entities operate, will be subject to the foreign investment restrictions or prohibitions set forth in the “negative list” to be issued. If the enacted version of the Foreign Investment Law and the final “negative list” mandate further actions, such as MOFCOM market entry clearance or certain restructuring of our corporate structure and operations, to be completed by companies with existing VIE structure like us, we face substantial uncertainties as to whether these actions can be timely completed, or at all, and our business and financial condition may be materially and adversely affected.

However, until “The foreign investment law” is enacted, which may take some time, the Company’s current VIE contractual arrangement structure will not be affected.

The draft Foreign Investment Law, if enacted as proposed, may also materially impact our corporate governance practice and increase our compliance costs. For instance, the draft Foreign Investment Law imposes stringent ad hoc and periodic information reporting requirements on foreign investors and the applicable FIEs. Aside from investment implementation report and investment amendment report that are required at each investment and alteration of investment specifics, an annual report is mandatory, and large foreign investors meeting certain criteria are required to report on a quarterly basis. Any company found to be non-compliant with these information reporting obligations may potentially be subject to fines and/or administrative or criminal liabilities, and the persons directly responsible may be subject to criminal liabilities.

The shareholders of the Auto Kaiyuan Companies may have potential conflicts of interest with Fincera, which may materially and adversely affect Fincera’s business and financial condition.

We, through our wholly-owned subsidiary ACG, have contractual arrangements with respect to operating the business with the Auto Kaiyuan Companies, and the shareholders of Auto Kaiyuan Companies are Hebei Kaiyuan and its parent company, Hebei Shengrong Investment, companies registered in the PRC and indirectly owned by our Chairman and CEO, Mr. Yong Hui Li. Although Auto Kaiyuan Companies, Hebei Kaiyuan and Hebei Shengrong Investment have given undertakings to act in the best interests of Fincera, Fincera cannot assure you that when conflicts arise, these individuals will act in Fincera’s best interests or that conflicts will be resolved in Fincera’s favor.