UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the Securities

Exchange Act of 1934

Filed by the Registrant o

Filed by a Party other than the Registrant x

Check the appropriate box:

o | Preliminary Proxy Statement |

o | Confidential, For Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

o | Definitive Proxy Statement |

o | Definitive Additional Materials |

x | Soliciting Material Pursuant to § 240.14a-12 |

THE COMMERCE GROUP, INC.

(Name of Registrant as Specified In Its Charter)

MAPFRE SA

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

x | No fee required. |

o | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

(1) | Title of each class of securities to which transaction applies: |

(2) | Aggregate number of securities to which transaction applies: |

(3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

(4) | Proposed maximum aggregate value of transaction: |

(5) | Total fee paid: |

o | Fee paid previously with preliminary materials. |

o | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

(1) | Amount Previously Paid: |

(2) | Form, Schedule or Registration Statement No.: |

(3) | Filing Party: |

(4) | Date Filed: |

-----------------------------------------------------------------------------------

Acquisition of The Commerce Group Inc.

31st October 2007

This document is purely informative. Its content does not constitute, nor can it be

interpreted as, an offer or an invitation to sell, exchange or buy, and it is not binding on

the issuer in any way. The information about the plans of the Company, its evolution, its

results and its dividends represents a simple forecast whose formulation does not

represent a guarantee with respect to the future performance of the Company or the

achievement of its targets or estimated results. The recipients of this information must

be aware that the preparation of these forecasts is based on assumptions and

estimates, which are subject to a high degree of uncertainty, and that, due to multiple

factors, future results may differ materially from expected results. Among such factors,

the following are worth highlighting: the evolution of the insurance market and of the

economic environment in general in those countries where the Company operates;

changes in the legal framework; changes in monetary policy; circumstances which may

affect the competitiveness of insurance products and services; changes in the

underlying tendencies on which the mortality and morbidity tables used in Life and

Health insurance are based; frequency and severity of claims insured, with respect to

reinsurance and general insurance, as well as to life insurance; variations in interest

rates and exchange rates; risks associated with the use of derivative instruments; the

impact of future acquisitions.

MAPFRE S.A. does not undertake to update or revise periodically the content of this

document.

Disclaimer

2

Executive Summary

MAPFRE has announced the signing of an agreement to acquire all shares of The Commerce Group

Inc. (“Commerce”) at a price of $36.70 per share. The Board of Commerce deems the offer to be fair

and will recommend the transaction to its shareholders. The transaction will be carried out through the

merger of a subsidiary of MAPFRE with Commerce, under U.S. regulations

Commerce fits MAPFRE’s growth strategy:

Leading position in motor insurance in Massachusetts

Licenses in 50 states and operations in 17 of them

Quality operations and consistent underwriting profits

Experienced management team with proven track record

Positive financial impact from the outset:

Total consideration of $2,207mn (€1,538mn), paid entirely in cash

Acquisition price implies P/E 2008 of 13.1x (First Call consensus) and P/BV (Q3 ‘07 ) of 1.65x

Premium to market of 17.9% vs. 30th October’s closing price, 22.5% vs. the 30-day average and of 20.4% vs. the

3-month average

Initial funding through a bridge loan. Long-term funding expected to come from an equity capital raising of €500mn,

the issuance of hybrid debt of up to €800mn and internal resources

Immediately EPS accretive

Upon completion, MAPFRE would retain Commerce´s management team and together both groups

would design a cautious growth strategy in a number of new states, including dedicated services for

the Hispanic community

3

Overview of Commerce

Strategic rationale for MAPFRE

Transaction details and financial impact

Appendix

4

Overview of The Commerce Group, Inc.

The Commerce Group, Inc. (“Commerce”) began operating in 1971. Today it focuses on

writing personal automobile insurance and other property and casualty lines in 17 states,

which it distributes primarily through independent agents

Since 1990, it is the largest and most profitable personal auto writer in Massachusetts. It

ranks as the 20 th largest company nationwide in this line

Its operations are rated ‘A+ (Superior)’ by A.M. Best, ‘A2’ by Moody’s and ‘A’ by S&P

% of

Total

Written and

accepted

premiums

$1.96B

Total

12%

0.23

Outside

Massachusetts

88%

$1.72B

Massachusetts

’06 Breakdown of written and accepted premiums

Private Passenger

Auto Liability

50%

Auto Physical

Damage

29%

Other

8%

Commercial Auto

Liability

4%

Homeowners

9%

5

Geographic focus

Commerce has historically written business in Massachusetts, but has recently expanded in

16 other states

WA

OR

CA

MT

WY

CO

NM

ID

NV

UT

AZ

ND

SD

NE

KS

OK

TX

MN

IA

MO

AR

LA

FL

MI

WI

IL

TN

MS

AL

GA

SC

NC

VA

KY

NY

PA

OH

IN

WV

RI

ME

VT

NH

MA

CT

DE

MD

NJ

MI

AK

HI

American Commerce

Columbus, OH

State-Wide

Insurance Co.

Hempstead, NY

Commerce Insurance Co.

Webster, MA

Commerce West

Pleasanton, CA

Citation Insurance

Webster, MA

Heartland (3% of DPW)

Northeast (80% of DPW)

West (15% of DPW) (1)

Recent Expansion States (2% of DPW) (2)

(1) Pro forma for $170mm of premium from Stonewood Insurance Agency Agreement, anticipated to write $20mm by 06/2008, $50mm by

06/2009 and $100mm by 06/2010

(2) Pro forma for $41mm of premium from SWICO acquired April 2007

RI

6

Key Strengths: competitive position

Leading market position in the Massachusetts P&C business:

Strong brand recognition

Excellent agency relationships

Leading market shares:

# 1 in personal auto (31.5%)

# 1 in homeowners (9.8%)

# 2 in commercial auto (12.7%)

Above average position in affinity group marketing programs

Outstanding customer service

Unsurpassed economies of scale

Highly experienced management team with proven track record

In-depth understanding of the Massachusetts and U.S. regulatory and underwriting

environment

7

Key strengths: distribution through independent agents

Independent agents are Commerce’s main distribution channel

Relations with agents are excellent, as evidenced by their high degree of loyalty: nearly 60%

of all agents in Massachusetts have been with the group for over 10 years

Commerce ensures the interests of agents are aligned with its own through an effective profit

sharing system, which utilises a three-year rolling plan. To qualify for profit sharing, an

agent’s portfolio generally must have a three-year average loss ratio of 60% or better

Commerce devotes considerable attention and resources to providing a high level of service

to both the agents and their customers, thus enhancing satisfaction and retention

8

Key strengths: distribution through the AAA

Commerce enjoys a strategic relationship with numerous American Automobile

Association (AAA) clubs

In Massachusetts:

Commerce has exclusive distribution agreements with all three AAA clubs, whose members

receive a 5% discount on their premiums

In 2006, 50% of all personal auto DPW came from AAA members (42% written by Commerce’s

network of independent agents and 8% through AAA agencies)

The present agreements were renewed on 01.01.2007 for a period of 20 years

Outside of Massachusetts:

Commerce distributes its products through AAA clubs in eleven states

AAA Southern New England has a 5% shareholding in American Commerce

Growth opportunities are significant, as Commerce has currently penetrated less than 1% of a

membership base exceeding 100 million

9

Distribution network

10

Independent

Agents

AAA Agents

Brokers

Total

California

120

---

1,080

1,200

Massachusetts

792

3

---

795

Arizona

294

---

---

294

Oregon

200

1

---

201

New York

---

---

72

72

New Hampshire

55

---

---

55

Ohio

37

12

---

49

Indiana

35

1

---

36

Kentucky

25

2

---

27

Idaho

---

2

---

2

Tennessee

---

2

---

2

Connecticut

---

1

---

1

Oklahoma

---

1

---

1

Rhode Island

---

1

---

1

South Dakota

---

1

---

1

Washington

---

1

---

1

TOTAL

1,558

28

1,152

2,738

Commerce competitive position

Source: A.M. Best (2006)

Personal auto

Commerce Group

1

31.5%

Safety Group

2

11.2

Arbella Insurance Group

3

9.6

Liberty Mutual Insurance Companies

4

7.7

MetLife Auto & Home Group

5

7.1

Travelers Insurance Companies

6

7.0

Plymouth Rock Companies

7

6.1

Amica Mutual Group

8

3.6

Hanover Insurance Grp Prop and Cas Cos

9

3.6

White Mountains Insurance Group

10

2.9

Allstate Insurance Group

11

2.3

USAA Group

12

2.1

Quincy Mutual Group

13

1.4

Main Street America Group

14

1.3

Homeowners

Commercial auto

Massachusetts

Rank

% of Market

1

9.8%

2

12.7%

11

3.2

3

11.0

7

5.2

4

10.5

5

6.7

9

3.6

10

3.2

--

0.0

3

8.2

1

13.5

16

2.1

6

6.0

13

3.0

44

0.1

9

3.3

5

7.9

14

2.6

8

3.8

27

1.1

--

0.0

15

2.5

--

0.0

6

5.9

36

0.2

21

1.5

16

1.4

Massachusetts

Rank

% of Market

Massachusetts

Rank

% of Market

11

Growth in market share in MA personal auto

Source: Commerce public filings & Equity Research

Since 1990, when it first became the largest writer of personal auto insurance in MA,

Commerce’ market share has risen from 11.5% to 31.5% in 2006

Commerce has significantly and consistently grown its MA personal auto business

(policies in thousands; premiums in $ million)

$733

$794

$809

$816

$868

$918

$1,046

$1,118

$1,172

$1,201

$1,253

553

600

609

615

654

693

791

834

870

889

929

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Commerce MA personal auto premiums written

Commerce MA personal auto policies in force

31.5%

30.0%

29.0%

27.6%

25.9%

23.2%

22.3%

21.3%

21.6%

21.8%

20.8%

16.3%

11.5%

12.4%

14.8%

16.0%

16.4%

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Commerce market share in MA

12

Key Strengths: underwriting results and claims handling

Commerce has been delivering consistently for over 15 years positive technical results

and significant reserve redundancies, thanks to:

Effective underwriting:

The largest proprietary underwriting database in the Massachusetts market with a high degree of

data reliability, providing superior risk selection and pricing capabilities

Strict underwriting guidelines

No meaningful environmental risks legacy issues

Quick and efficient handling of claims:

24-hour claim reporting service, which improves customer satisfaction by making the initial claim

handling much faster and ultimately reduces indemnity payments

Outsourced drive-in centres, close to repair shops, allowing quick adjustment and settlement of car

body damages. Additionally, Commerce has a panel of preferred body shops with guaranteed

prices and workmanship

Sophisticated software systems used for internal and external claims processing and field

communications that increase productivity while reducing expenses and indemnity payments

Significant internal resources devoted to fighting fraud, complemented by external investigators

Regular surveys among agents, customers and third-party claimants to monitor the quality of

claims handling

Low-cost structure, high degree of centralisation and unsurpassed economies of scale

13

MA internal personal auto acquisition costs (1)

Commerce enjoys a low cost structure enabling it to compete effectively

Source: Company public filings.

(1) Policy acquisition costs include the company's general fixed expenses (i.e. salaries, advertising, etc.) allocated to acquisition costs, excluding

actual commissions payable to the agents.

14.1

Amica

14.7

Liberty

13.5

White Mountain

Percent of earned premium

Direct Writers

7.3%

USAA

7.7%

All companies

12.0

Metropolitan

7.5

State Farm

11.8

Arbella

8.5

Plymouth Rock

8.1

Hanover

6.0

Safety

4.1

Travelers

3.3%

Commerce

Percent of earned premium

Agency companies

14

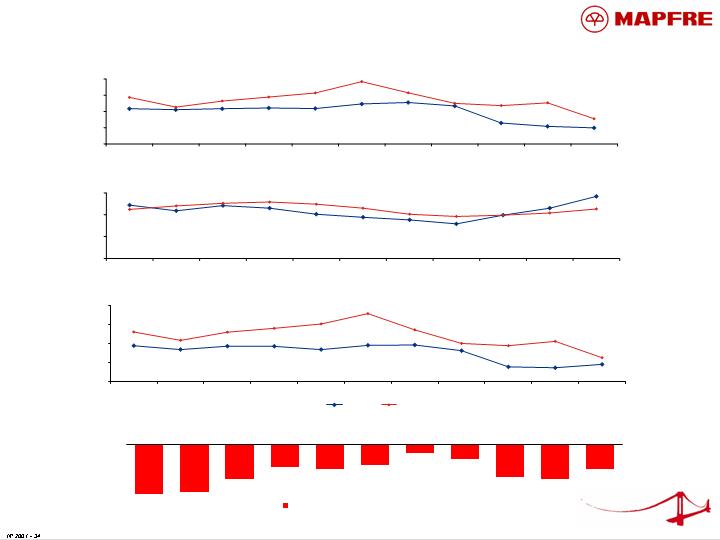

Strong, consistent historical underwriting results

Source: Commerce public filings, A.M. Best.

N.B. Combined ratios are on a statutory basis.

Combined Ratio

Loss and Loss Adjustment Expense Ratio

Expense Ratio

Reserve Redundancies

($83.8)

($87.8)

Additions to (reductions in) reserves for earlier losses ($ millions)

($35.3)

($39.9)

($61.4)

($42.4)

($14.4)

($43.7)

($61.4)

($57.0)

($25.2)

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

107.2%

101.2%

89.1%

87.3%

87.8%

96.3%

99.3%

99.1%

96.9%

98.6%

98.7%

96.9%

98.9%

92.6%

98.9%

100.1%

115.7%

110.3%

108.0%

106.0%

101.7%

106.1%

80

90

100

110

120

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Commerce

U.S. P&C Industry

59.9%

60.8%

62.9%

73.4%

75.5%

74.6%

71.8%

72.1%

71.7%

71.1%

71.7%

65.5%

75.3%

73.6%

75.0%

81.5%

88.4%

81.4%

78.9%

76.4%

72.7%

78.7%

50

60

70

80

90

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

22.9%

24.9%

27.2%

29.2%

26.5%

23.8%

24.4%

25.1%

26.5%

27.1%

25.9%

26.2%

26.3%

25.4%

24.9%

24.6%

25.1%

26.5%

27.4%

27.9%

27.6%

27.0%

15

20

25

30

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

15

Key Strengths: investment portfolio and returns

Commerce generates recurring investment yields from a portfolio made up primarily of high

quality fixed income investments:

Nearly 90% of ABS instruments are AAA-rated and an equal percentage is mortgage-backed

Sub-prime exposure is very limited ($28mn) and has caused losses of $4.7mn to date

12/31/06 Total : $3,071mn

Private sector: 52%

Public sector: 48%

16

Key Strengths: profitability and cash generation

Commerce has consistently recorded growing profits and above-industry-average returns

on the back of its recurring positive underwriting results and strong net financial income

Source: Commerce public filings, A.M. Best

($ in millions)

Cash generation is also strong, as evidenced by a cash flow from operating activities of

$344 million (18.8% of NPW)

($ in millions)

17

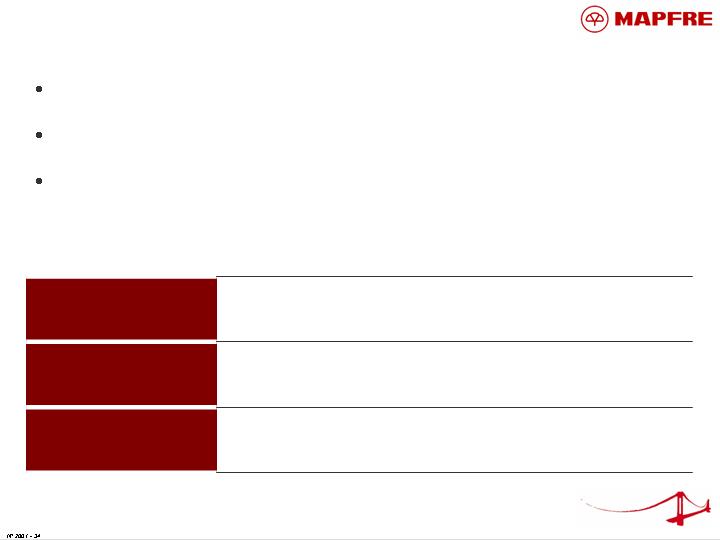

Key strengths: experienced management team

Source: Company public filings.

Appointed COO/EVP of non-MA operations in January 2007

17 years at California State Auto Association

COO and EVP of Non-MA

Operations

50

Lawrence Pentis

Appointed EVP of MA operations (responsible for underwriting,

product/pricing and marketing) in August 2006

Senior VP for Commerce Group in May 2001 until August 2006

Appointed General Counsel of Commerce Group in February 2000

Secretary of ACIC Holding and Commerce West

General Counsel and EVP of

MA Operations

44

James A. Ermilio

Appointed Senior VP of Policyholder Benefits in 1988 and appointed

EVP of country-wide policyholder benefits in August 2006

Became responsible for the Claims Operations of ACIC in August 2001

and of Commerce West and State-wide in 2007

Vice President – Mortgage Operations, 1981 – 1988

EVP, Policyholder benefits

(claims)

51

Arthur J. Remillard III

A Certified Public Accountant, was appointed CFO and Senior VP of

Commerce Group in February 2006

Treasurer and Chief Accounting Officer of Commerce Group from 1994

through 2006

Assistant Treasurer and Comptroller of Commerce Group from 1990 to

1994

CFO

46

Randall V. Becker

A Certified Public Accountant, was appointed CEO to replace Arthur

Remillard, Jr. in July 2006

Previously President and COO of Commerce Insurance since 2001

Appointed Executive Vice President of Commerce Group in 1989

CEO, President, Chairman of

the Board

63

Gerald Fels

Biography

Position

Age

Name

18

Overview of Commerce

Strategic rationale for MAPFRE

Transaction details and financial impact

Appendix

19

Consistency with MAPFRE´s current strategy

“Fit” of Commerce with MAPFRE

Criteria

Earnings per share accretive from the first year assuming the

announced financing mix

Return on Investment above MAPFRE’s cost of capital

The discontinuation of listing will increase Commerce’ EBT by about

$7mn/year

Operations that

increase earnings

per share in the

first three years

Commerce’s performance will be enhanced by the access to

MAPFRE’s:

Experience competing under different regulations, which will facilitate the

transition to the new regulatory environment in Massachusetts

Product knowledge across several countries in all P&C lines

Integrated and unified IT platform

Reinsurance solutions for the most appropriate protection of the portfolio

Companies whose

growth and

profitability can be

enhanced through

the application of

MAPFRE’s

expertise

US was indicated in the past as a target market for MAPFRE

Joint growth opportunities exist through:

The introduction of a specific offering for the Hispanic community (21.8 million

people in the states in which Commerce presently operates, equivalent to 14%

of their total population)

Business expansion in and outside of Massachusetts, including an increased

penetration of the AAA club members’ base

Markets or

segments that are

not fully penetrated

or developed by

MAPFRE

20

MAPFRE Insurance Company Of Florida

Company domiciled and licensed in Florida, currently writing commercial lines business and more

recently personal Auto. Rated ‘A-’ by A.M. Best

MAPFRE Insurance Company

Company domiciled and licensed in New Jersey, as well as in 34 other states. Rated ‘A-’ by A.M.

Best

Road America Motor Club

Acquired by MAPFRE Asistencia in 2003. Founded in 1978, provides a variety of B2B services

related to roadside assistance and ancillary services to the OEM, telecom and insurance industries

More than 19 million customers

Two state-of-the-art call center facilities in Columbus, GA and Miami, FL

Overall capacity for more than 2 million services annually

Coverage of Canada (Road Canada) and Puerto Rico

Federal Assist, subsidiary of MAPFRE Asistencia specialised in providing Medical Travel Assistance,

Medical Case Management and Home Repairs Assistance since 1993

Furthermore, MAPFRE operates in the Associated Commonwealth of Puerto Rico through MAPFRE

Puerto Rico, the oldest and third-largest insurer in the island, writing P&C, Life and Health insurance.

Rated ‘A’ by A.M. Best

MAPFRE current operations in the US

21

U.S. personal auto markets

MA has attractive demographics for personal auto insurance

Source: NAIC, Bureau of Economic Analysis, U.S. Census Bureau, Insurance Information Institute, National Auto Dealers Association and AIPSO. Data as of 2005.

840

843

845

845

849

926

931

945

962

983

991

1,028

1,059

1,063

1,113

1,122

1,182

$1,184

Average

Premium for personal

auto insurance

96.9

86.3

91.8

93.5

98.6

92.5

121.7

91.7

97.3

105.5

92.5

98.4

87.7

104.0

92.3

85.7

87.0

96.3%

Combined Ratio

Washington

Hawaii

California

Texas

Pennsylvania

Arizona

Michigan

Maryland

Alaska

Nevada

Connecticut

Delaware

Rhode Island

Florida

Massachusetts

New York

District of Columbia

New Jersey

State

4,225,106

770,475

24,523,124

NA

8,281,032

3,661,581

6,323,287

3,779,282

392,662

1,631,401

2,403,762

589,277

673,359

10,879,575

4,146,762

9,100,868

216,217

5,132,615

Number of Cars

Insured

35,730

8.5

2.1

34,818

5.7

1.9

37,283

34.2

2.5

33,160

34.7

1.9

34,810

3.7

1.8

30,384

27.9

1.6

32,719

3.6

1.8

41,587

5.3

1.9

36,636

4.6

2.5

37,420

23.2

1.3

47,701

10.0

2.1

37,080

5.7

2.0

35,757

9.4

1.8

34,712

19.1

1.9

43,601

6.7

2.0

40,916

13.5

1.5

53,594

6.8

0.8

$43,318

14.1%

1.8

Per Capita

personal Income

% of Population

Hispanic

Vehicles Per

Housing Unit

22

Impact on MAPFRE’s business mix

MAPFRE Standalone(1)

Impact on

Geographic

Mix

MAPFRE Pro Forma

On the basis of

Premiums

Impact on

Product Mix

(1) Pro forma including recent acquisitions

Spain

58%

UNIDAD

AMERICA

19%

MAPFRE RE

11%

MAPFRE

ASISTENCIA

2%

MAPFRE INTL.

10%

Spain

53%

UNIDAD

AMERICA

17%

MAPFRE RE

10%

MAPFRE

ASISTENCIA

2%

MAPFRE INTL.

9%

EE.UU.

9%

Non-life

80%

Life

20%

Non-life

81%

Life

19%

23

Impact on MAPFRE’s business profile

MAPFRE’s business profile will be strengthened by the integration of Commerce:

Addition of an established and solid platform to develop a business in the U.S.

Enhanced geographical, business cycle and currency diversification

Considerable strengthening of management resources and skills in North America

24

Overview of Commerce

Strategic rationale for MAPFRE

Transaction details and financial impact

Appendix

25

Transaction highlights

Expected Timetable

Commerce operations to remain in Massachusetts

Management retention in place

Operations

2Q 2008

Estimated closing

Initial funding through a bridge loan

Expected long-term funding through an equity capital raising of €500mn, hybrid debt issuance

of up to €800mn and internal resources

Financing

Total consideration of $2,207mn (€1,538mn), $36.70 per share

Acquisition price implies P/E 2008 of 13.1x (First Call consensus) and P/BV (Q3 ‘07) of 1.65x

Premium to market of 17.9% vs. 30th October’s closing price, 22.5% vs. the 30-day average

and of 20.4% vs. the 3-month average

Pricing

All cash consideration

Structure

Acquisition of 100% of The Commerce Group Inc.

Transaction Overview

Subject to the relevant regulatory authorisations and to the requisite approval of the merger

agreement by the holders of at least two-thirds of the shares of Commerce common stock

Approved by the Board of MAPFRE and recommended by the Board of Commerce

Conditions and other

26

Financial impact: value creation for MAPFRE shareholders

The acquisition of Commerce will be immediately additive to MAPFRE’s EPS

Projected returns exceed MAPFRE’s cost of capital

Funding mix aimed to protect present solvency position by combining equity issuance

with a rational use of the Group’s hybrid capacity

0.005

--

0.005

2007

0.008

0.007

Commerce

0.021

0.016

Previously announced

acquisitions (1)

0.031

0.025

Total

2008

2009

(1) Genel Sigorta, CCM, MCA, Bankinter Vida, shareholding in Cattolica

(Euros per share)

27

Transaction structure

1.

MAPFRE creates a Special Purpose Vehicle (SPV) and capitalises it with the financial

resources needed to acquire Commerce

2.

The merger between the SPV and Commerce is approved by the holders of at least two

thirds of Commerce common stock

3.

SPV and Commerce merge

4.

The resulting company buys back Commerce´s shares. In exchange, shareholders will

receive cash

28

Overview of Commerce

Strategic rationale for MAPFRE

Transaction details and financial impact

Appendix

29

Organisational structure

Source: Company financials.

N.B. Ratings represent S&P/Moody’s senior unsecured debt ratings at holding company and AM Best financial strength rating at insurance subsidiary.

(1) Pro forma for $170mn of premium from Stonewood Insurance Agency Agreement, anticipated to write $20mn by 06/2008, $50mn by 06/2009 and $100mn

by 06/2010.

(2) Announced in December 2006, completed in April 2007.

100%

Commerce

Insurance Co.

(Webster, MA)

A+

ACIC Holding Co.

(RI)

American Commerce

(Columbus, OH)

A+

Citation Insurance

(Webster, MA)

A+

100%

100%

95%

The Commerce Group, Inc.

(Webster, MA)

BBB/Baa2

AAA Southern New

England

5%

State-Wide Insurance (2)

(Hempstead, NY)

A+

Bay Finance Co.

(Webster, MA)

stopped doing business in

Aug. 2007

100%

NA

3

NA

MA, CT

--

1,846

# of Employees

’06 DPW ($mn)

Distribution

States

$95

795 Agents

MA

$1,544

795 Agents

MA, NH

$226 (1)

90

1,231 Agents

CA, OR, AZ

N/A

246

# of Employees

$168

738 Agents

WA, AZ, OK, RI, OR, OH, KY, IN,

TN, ID, SD,CT

’06 DPW ($mn)

Distribution

States

$38

145 Brokers, Direct

NY, NJ

A.M.Best FSR

Headquarters

A.M.Best FSR

Headquarters

Commerce West

(Pleasanton, CA)

A+

30

Commerce’s historical financials

Source: Company financials.

Income Statement

Key Balance Sheet Items and Ratios

For the Year Ending December 31

2004

2005

2006

YTD 3Q'06

YTD 3Q'07

Total Investments and cash

$2,527.7

$2,765.3

$3,070.8

$2,985.3

$2,846.6

Premiums Receivable

459.8

475.1

480.6

511.6

497.9

Total Assets

3,612.2

3,927.0

4,110.9

4,089.1

3,979.7

Unpaid Losses/Loss Adjustment Expense

990.3

989.2

971.9

957.0

1,011.9

Unearned Premiums

902.6

933.2

935.4

986.0

989.9

Bonds Payable

298.2

298.4

298.6

298.5

298.7

Stockholders Equity

1,116.2

1,305.1

1,503.3

1,477.0

1,339.9

Shareholder Dividends Paid

43.0

49.4

66.0

49.1

57.9

Key Performance Ratios:

Return on Average Equity, Ex. AOCI

21.7%

20.2%

17.1%

13.1%

12.0%

Operating Return on Average Equity, Ex. AOCI

20.4

18.9

16.4

12.8

10.7

Loss and LAE Ratio

62.9

60.8

59.9

59.8

64.9

Underwriting Expense Ratio

24.9

26.5

29.2

27.5

29.1

Combined Ratio

87.8

87.3

89.1

87.3

94.0

Debt to Cap

21.1

18.6

16.6

16.8

17.8

($ in millions)

For the Year Ending December 31

2004

2005

2006

YTD 3Q'06

YTD 3Q'07

Revenues:

Direct Premiums Written

$1,838.2

$1,874.2

$1,864.2

$1,445.0

$1,447.7

Premiums Assumed

128.2

132.1

99.0

78.4

78.6

Earned Premiums

1,638.8

1,709.9

1,760.7

1,302.9

1,363.6

Net Investment Income

119.4

124.0

153.0

104.1

119.8

Premium Finance and Service Fees

28.4

28.3

28.6

21.4

23.5

Net Realized Investment Gains

23.6

22.9

16.6

7.7

28.9

Total Revenue

1,806.6

1,884.4

1,949.5

1,436.0

1,535.8

Expenses:

Loss and Loss Adjustment Expenses

1,044.8

1,050.2

1,068.4

778.9

885.2

Policy Acquisition Costs

439.2

463.3

516.3

381.5

395.0

Interest Expense and Amortization of Bond Fees

18.3

18.3

18.3

13.7

13.7

Total Expenses

1,502.4

1,531.8

1,603.0

1,174.1

1,293.9

Earnings before Income Taxes and Minority Interest

304.2

352.6

346.4

261.9

241.8

Income Taxes

89.0

107.8

104.0

79.1

69.2

Earnings before Minority Interest

215.2

244.8

242.4

182.8

172.6

Change in Accounting Principles

0.0

0.0

0.0

0.0

0.0

Minority Interest in Earnings of Affiliates

(0.8)

(0.9)

(0.9)

(0.7)

(1.2)

Net Earnings

$214.4

$243.9

$241.5

$182.1

$171.4

Net premiums written

1,712.5

1,736.2

1,825.3

1,428.6

1,400.5

31

Investor Relations Department

Luigi Lubelli

Finance Director

+34-91-581-6071

Jesús Amadori Carrillo

+34-91-581-2086

Alberto Fernández-Sanguino

+34-91-581-2255

Beatriz Izard Pereda

+34-91-581-2061

Antonio Triguero Sánchez

+34-91-581-5211

Marisa Godino Alvarez

Secretaria

+34-91-581-2985

MAPFRE S.A.

Investor Relations Department

Carretera de Pozuelo, n° 52

28220 Majadahonda

relacionesconinversores@mapfre.com

32

In connection with the operation hereby disclosed, COMMERCE will file with the Stock

Exchange Commission (“SEC”), among other materials, a proxy statement. We urge investors

to read the proxy statement and these other materials when they become available because

they will contain important information about COMMERCE and the proposed acquisition.

Investors will be able to obtain free copies of the proxy statement (when available) as well as

other filed documents containing information about the Company on the SEC’s website at

http://www.sec.gov. Likewise, free copies of the COMMERCE's SEC filings are also available

at http://www.commerceinsurance.com (Investor Relations). MAPFRE and its directors and

executive officers may be deemed, under SEC rules, to be participants in the solicitation of

proxies. Information regarding such individuals is available at the web page

http://www.mapfre.com and will also be available in a Schedule 13D to be filed by MAPFRE

with the SEC.

Disclaimer

33