Table of Contents

As filed with the Securities and Exchange Commission on December 22, 2011

Registration No. 333-174801

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 4

to

Form S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

AVAYA HOLDINGS CORP.

(Exact name of registrant as specified in its charter)

| Delaware | 3661 | 26-1119726 | ||

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

211 Mount Airy Road

Basking Ridge, New Jersey 07920

(908) 953-6000

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Pamela F. Craven, Esq.

Chief Administrative Officer

Avaya Holdings Corp.

211 Mount Airy Road

Basking Ridge, New Jersey 07920

(908) 953-6000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With copies to:

Julie H. Jones, Esq. 800 Boylston St. | Daniel J. Zubkoff, Esq. Douglas S. Horowitz, Esq. Cahill Gordon & ReindelLLP 80 Pine Street New York, NY 10005 Telephone (212) 701-3000 Fax (212) 269-5420 |

Approximate date of commencement of proposed sale to public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||||||

| Non-accelerated filer | x | (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | ||||||

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

PROSPECTUS (Subject to Completion)

Issued December 22, 2011

Shares

COMMON STOCK

Avaya Holdings Corp. is offering shares of its common stock. This is the initial public offering of shares of our common stock and no public market currently exists for our shares. We expect the initial public offering price of our common stock to be between $ and $ per share.

After the completion of this offering, funds affiliated with our Sponsors (as defined herein) will continue to own a majority of the voting power of our outstanding common stock. As a result, we expect to be a “controlled company” within the meaning of the corporate governance standards of the New York Stock Exchange. See “Principal Stockholders.”

We have applied to list our common stock on the New York Stock Exchange under the symbol “AVYA.”

Investing in our common stock involves a high degree of risk. See “Risk Factors” beginning on page 16.

PRICE $ A SHARE

| Public Offering Price | Underwriting | Proceeds | ||||

Per Share | $ | $ | $ | |||

Total | $ | $ | $ |

We have granted the underwriters the right to purchase up to an additional shares of common stock for a period of 30 days.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares to purchasers on , 2012.

| MORGAN STANLEY | GOLDMAN, SACHS & CO. | J.P. MORGAN |

| CITI | DEUTSCHE BANK SECURITIES | |

BofA MERRILL LYNCH | BARCLAYS CAPITAL UBS INVESTMENT BANK | CREDIT SUISSE | ||

, 2012

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| Page | ||||

| 1 | ||||

| 16 | ||||

| 30 | ||||

| 32 | ||||

| 33 | ||||

| 34 | ||||

| 36 | ||||

| 38 | ||||

| 44 | ||||

Management’s Discussion and Analysis of Financial Condition and Results of Operations | 52 | |||

| 104 | ||||

| 127 | ||||

| 128 | ||||

| Page | ||||

| 138 | ||||

| 168 | ||||

| 173 | ||||

| 177 | ||||

| 186 | ||||

| 191 | ||||

Certain Material U.S. Federal Income Tax Considerations For Non-U.S. Holders Of Common Stock | 193 | |||

| 197 | ||||

| 204 | ||||

| 204 | ||||

| 204 | ||||

| F-1 | ||||

We have not authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectuses we file with the Securities and Exchange Commission, or the SEC. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus is current only as of its date.

Until , 2012 (25 days after the commencement of this offering), all dealers that buy, sell or trade shares of our common stock, whether or not participating in this offering, may be required to deliver a prospectus. This delivery requirement is in addition to the obligation of dealers to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

For investors outside the United States: we have not and the underwriters have not done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the shares of common stock and the distribution of this prospectus outside the United States.

When we use the terms “we,” “us,” “our,” “Avaya” or the “Company,” we mean Avaya Holdings Corp., a Delaware corporation, and its consolidated subsidiaries, including Avaya Inc., our principal U.S. operating subsidiary, taken as a whole, unless the context otherwise indicates.

Avaya Aura®, Avaya Flare® and Avaya web.alive™ and other trademarks or service marks of Avaya are the property of Avaya Holdings Corp. and/or its affiliates. This prospectus also contains additional tradenames, trademarks or service marks belonging to us and to other companies. We do not intend our use or display of other parties’ trademarks, tradenames or service marks to imply, and such use or display should not be construed to imply, a relationship with, or endorsement or sponsorship of us by, these other parties.

i

Table of Contents

This summary highlights information contained elsewhere in this prospectus. This summary does not contain all of the information you should consider before investing in our common stock. You should read this entire prospectus carefully, especially the “Risk Factors” section of this prospectus and our consolidated financial statements and related notes appearing at the end of this prospectus, before making an investment decision. This summary contains forward-looking statements that involve risks and uncertainties. Our actual results may differ significantly from the results discussed in the forward-looking statements as a result of certain factors, including those set forth in “Risk Factors” and “Special Note Regarding Forward-Looking Statements.”

Our Company

We are a leading global provider of next-generation business collaboration and communications solutions that bring people together with the right information at the right time in the right context, enabling business users to improve their efficiency and quickly solve critical business challenges. Our solutions are designed to enable business users to work together more effectively as a team internally or with their customers and suppliers, increasing innovation, improving productivity and accelerating decision-making and business outcomes.

We develop software and hardware products and offer related services that we market and sell directly and through our channel partners as part of our collaboration and communications solutions for large enterprises, small- and mid-sized businesses and government organizations. Our software delivers rich value-added applications for enterprise collaboration and communications, including messaging, telephony, voice, video and web conferencing, mobility and customer service. These applications operate on our own hardware, which includes a broad range of desk phones, servers and gateways, and LAN/WAN switching wireless access points and gateways, as well as on third-party devices, including desk phones, tablets and desktop PCs. In addition, our award-winning portfolio of services supports our products to help customers achieve enhanced business results both directly and indirectly through partners. Market opportunities associated with our business collaboration and communications solutions include spending on unified communications (which includes, among others, enterprise telephony and messaging), contact center applications and data networking equipment, as well as spending on support and maintenance services to implement and support these tools. These areas are expected to attract $77 billion of spending in 2011 in the aggregate, with unified communications accounting for $14 billion, contact center accounting for $3 billion, data networking accounting for $25 billion and maintenance, managed and professional services accounting for the remaining $35 billion.

We are highly focused on and structured to serve our core business collaboration and communications markets with fit-for-purpose products, targeted sales coverage and distributed software services and support models. We offer solutions in five key business collaboration and communications categories:

| • | Unified Communications Software, Infrastructure and Endpoints; |

| • | Real Time Video Collaboration; |

| • | Contact Center; |

| • | Data Networking; and |

| • | Applications, including their Integration and Enablement. |

Our next-generation business collaboration solutions are designed to be highly scalable, flexible and easy to manage. They can be deployed in numerous ways, including on a customer’s own premise, in the cloud and in a virtualized environment. We are committed to open standards-based solutions, using Session Initiation Protocol, or SIP, extensively throughout our portfolio. SIP is a signaling protocol used to establish voice, video or data communication sessions over an IP network. At the core of our next-generation business collaboration portfolio

1

Table of Contents

is Avaya Aura, our SIP-based software suite that brings together voice, video and data into a single, integrated communications and collaboration platform.

Through our next-generation collaboration solutions, including Avaya Aura, we are reshaping our product portfolio to drive revenue growth and business model cash cycle time. Our portfolio of business collaboration and communications solutions is designed to deliver an intuitive and personalized user experience, seamlessly integrating various modes of communications and collaboration, including real-time voice, video, instant messaging and conferencing, and non real-time email, voicemail and social networking. These solutions target high growth market segments and we believe accelerate our sales cycle as customers more frequently upgrade their solutions to take advantage of our ongoing product innovation and to deploy our user experience across an array of endpoints, including our own and those of other vendors.

Over the past several years, we have invested significantly in research and development, introducing more than 70 new product offerings to the market since the beginning of fiscal year 2010. For example, in September 2010 we released our Avaya Flare Experience, a real-time, enterprise video communications and collaboration solution that can help to break down the barriers commonly seen in today’s communications and collaboration tools with a distinctive user interface for quick, easy access to voice and video, social media, presence, instant messaging, audio/video/web conferencing, a consolidated view of multiple directories and context history.

Our solutions address the needs of a diverse range of customers, including large multinational enterprises, small- and medium-sized businesses and government organizations. As of September 30, 2011, we had over 400,000 customers, including more than 90% of the Fortune 500 companies and one million customer locations worldwide. Our customers operate in a broad range of industries, including financial services, manufacturing, retail, transportation, energy, media and communications, healthcare, education and government, and include, among others, Morgan Stanley & Co. LLC, Progressive Casualty Insurance Company, Whirlpool Corporation, The Hewlett-Packard Company, Home Depot, Inc., United Air Lines, Inc., Marriott International, Inc., the Blue Cross and Blue Shield Association, Australia National University and the Federal Deposit Insurance Corporation, or the FDIC. We employ a flexible go-to-market strategy with direct and indirect presence in over 160 countries. As of September 30, 2011, we had approximately 9,100 channel partners and for fiscal year 2011, our product revenue from indirect sales represented approximately 76% of our total product revenue. We are expanding our sales coverage model, including both partners and direct sales, while supporting our customers’ channel preferences. In December 2009, we acquired the enterprise solutions business of Nortel Networks Corporation, or NES, which expanded our customer base, broadened and strengthened our indirect sales channel, enhanced our technology portfolio, established our presence in data networking and improved our ability to compete globally.

For fiscal years 2011 and 2010, we generated revenue of $5,547 million and $5,060 million, respectively. For fiscal year 2011, product revenue represented 54% of our total revenue and services revenue represented 46%. For fiscal year 2010, product revenue represented 51% of our total revenue and services revenue represented 49%. For fiscal year 2011, approximately 54% of our revenue was generated in the United States. For fiscal years 2011 and 2010, we had a net loss of $863 million and $871 million, respectively, and Adjusted EBITDA of $971 million and $795 million, respectively.

Adjusted EBITDA is a non-GAAP measure we use to measure our financial performance based on operational factors that management can impact in the short-term, namely our pricing strategies, volume, costs and expenses of the organization. See “Prospectus Summary—Summary Historical Financial Data” on pages 12 to 15 and “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Non-GAAP Financial Measures and Supplemental Disclosure—EBITDA and Adjusted EBITDA” for an explanation and reconciliation of net loss to Adjusted EBITDA.”

2

Table of Contents

Our Industry

Enterprises are increasingly focused on deploying collaboration solutions in order to increase productivity, reduce costs and complexity and gain competitive advantages. The requirements of enterprises have evolved over the past few years in response to the following trends and challenges:

Increasingly Mobile and Connected Workforce Needs Anytime/Anywhere Collaboration Tools.As enterprises move toward a more geographically dispersed, 24x7 workforce, they need tools to enable their users to quickly solve business challenges while improving their efficiency. To do this, enterprises need collaboration technology that can bring people together with the right information at the right time in the right context to make critical business decisions.

Proliferation of Devices and Applications and Consumerization of the Enterprise are Changing Users’ Expectations and Needs.The number and types of endpoints are growing rapidly and business users are also increasingly using consumer-focused products and applications for business tasks, particularly in the areas of collaboration and communications. In order to communicate seamlessly and securely across these devices, applications and endpoints, collaboration solutions must be integrated into the communications infrastructure and allow IT professionals to manage them effectively and reliably.

Customer Expectations of Contact Centers and Customer Service are Changing. The way customers communicate with the enterprise is rapidly changing, especially in contact centers where interactions have evolved from voice-centric to multimedia and multi-modal communications. Customers increasingly expect enterprises to know the history of their interactions regardless of whether they are communicating by phone or through email, social media or another method of communication.

Business Leaders are Increasingly Challenged to Deliver New Business Capabilities to Support Growth While Facing Tight IT Budgets. Business leaders continue to manage their overall spending closely due to continued macro-economic uncertainty. At the same time, business leaders are focused on strategic IT investments to gain competitive advantage and improve productivity, while expecting acceptable levels of return on their investments. As a result, they are seeking solutions that cost-effectively scale with their businesses.

Businesses Need Comprehensive, Scalable Solutions.To address these rapidly developing trends and needs, enterprises often have deployed tools that loosely tie various communication systems together with a single user interface, rather than fully integrating the underlying architectures. The resulting solutions often are difficult to deploy and manage, and may not provide businesses with the expected benefits, such as simultaneous conversations across different media. These solutions frequently employ proprietary, closed architectures, which do not integrate well with those of other vendors or enable integration of new consumer devices. This may require customers to abandon existing infrastructure and face additional complexity and costs to deploy new equipment or applications.

Our Solutions

We are a leader in business collaboration and communications and have created next-generation solutions that offer an innovative approach, delivering our customers fit-for-purpose, open solutions that we believe enable them to experience enhanced levels of productivity at a lower total cost of ownership than our competitors. The key benefits of our solutions include:

Innovative Real-Time, Multimedia, Multi-Platform Collaboration Tools that Promote Business Collaboration.Our next-generation business collaboration and communications solutions are designed to provide our customers with the software and infrastructure needed to bring people together with the right information at the right time in the right context regardless of the communications technology, devices or location.

3

Table of Contents

Fit-for-Purpose Solutions that Offer an Enhanced User Experience, Productivity Benefits and Lower Total Cost of Ownership.Our solutions are specifically designed to address the needs of today’s unified communications environment, seamlessly integrating various modes of communications and collaboration, including real-time voice, video, instant messaging and conferencing, and non real-time email, voicemail and social networking. We believe our solutions require less hardware and perform better than our competitors.

Open Standards-Based Architecture that Enables Flexible and Extensible Collaboration.Our open standards-based solutions, including Avaya Aura, accommodate customers with multi-vendor environments seeking to leverage their existing investments, supplement their existing solutions with specific collaboration products that they need, and rapidly create and deploy applications. These next-generation business collaboration solutions are designed to be highly scalable, flexible and easy to manage and can be deployed in numerous ways, including on a customer’s own premise, in the cloud and in a virtualized environment.

Enterprise-Class Solutions that are Scalable, Secure, Reliable and Backed by Our Award-Winning Services.Our product portfolio has been designed to be highly reliable, secure and scalable, and is backed by our award-winning global services. Avaya Global Services, or AGS, is a leading provider of maintenance services relating to business collaboration and communications solutions, offering services support tools to help our customers monitor, troubleshoot and manage their infrastructure. In addition, AGS delivers managed and professional services, providing the integration expertise necessary to help customers migrate from their current communications environment to next-generation business collaboration and communications environments.

Centralized Application Integration and Management that Makes it Easier to Integrate, Deploy and Manage. Our solutions provide enterprises with the ability to perform integration and management tasks as part of a central service rather than from individual platforms, reducing the amount of time required to perform integration activities and to support and manage unified communications services.

Our Competitive Strengths

In addition to the strengths of our solutions, we believe the following competitive strengths position us well to capitalize on the opportunities presented by the market trends impacting our industry.

Leading Position Across Our Key End Markets.We are a leader in business collaboration and communications, with leading market share in worldwide unified communications, contact center infrastructure, voice maintenance services and enterprise messaging.

Large, Diverse and Global Customer Installed Base.Our solutions address the needs of a diverse range of customers from large multinational enterprises to small- and medium-sized businesses in a number of industries. We believe our large and diverse customer base provides us with recurring revenue and a continuing growth opportunity to further expand within our customer base.

History of Innovation with Large Pipeline of New Products and Differentiated Approach to Commercialization.As of September 30, 2011, we had approximately 5,600 patents and pending patent applications, including foreign counterparts. Since the beginning of fiscal year 2010, we have introduced more than 70 new offerings across our portfolio. We have a differentiated commercialization approach that we believe results in new products with broad appeal and accelerates the timeline for development and adoption.

Flexible Go-to-Market Strategy Expands Reach of Our Products and Services.We sell our solutions both directly and through an indirect sales channel, enabling us to reach customers across industries and globally. With the acquisition of NES, we significantly expanded our channel coverage and deepened our vertical expertise.

4

Table of Contents

Global End-to-End Services Capability Provides Large Recurring Revenue Stream. AGS provides us with a key advantage over many of our competitors whose customers must contract with third-party service providers, adding to the overall cost and complexity of the deployment of their solutions. In addition, our services contracts tend to be multi-year arrangements, have high renewal rates and have provided us with a large recurring revenue base and significant visibility into our customers’ future needs.

Experienced Management Team with Track Record of Execution. We have an experienced team of senior executives that has demonstrated an ability to identify critical trends in the technology and communications sectors and develop a comprehensive strategic vision to enable businesses to capitalize on those trends.

Our Growth Strategy

We intend to be the preeminent provider of business collaboration solutions with a commitment to open standards and innovative products, services and solutions. Key elements of our strategy include:

Leverage our Leading Market Positions to Drive the Adoption of our Next-Generation Collaboration Solutions. Our market leadership, global scale, extensive customer interaction and credibility with customers and prospects position us to drive and shape the evolution of enterprise communications toward greater business collaboration.

Capture Additional Market Share Across our Portfolio of Products and Services. Our open architecture integrates with competitor systems and provides a path for gradual transition, while still achieving cost savings and improved functionality. In addition, with the NES acquisition, we acquired a data networking portfolio, which we believe provides a compelling value proposition to both our large installed base and new customers. Although we have a modest market presence in data networking, we believe we have a strong portfolio from which to expand our customer base. There is also significant opportunity to sell new maintenance contracts to customers acquired in the NES acquisition.

Expand Margins and Profitability. Our increasing focus on higher-margin software revenue, efficiencies achieved through enhanced product design and services productivity, cost-savings initiatives and achieving greater economies of scale is designed to drive profitable growth worldwide and further increase our profit margins.

Continue to Develop Products and Services Around Our Next Generation Business Collaboration Solutions to Drive Revenue Growth and Shorter Sales Cycles. Through our continued focus on product innovation and substantial investment in research and development for new products and services in high-growth areas, we believe our customers are more likely to upgrade their business collaboration solutions more frequently. We believe our ability to develop innovative solutions is advanced by feedback gathered from our extensive customer relationships and our customer focus, which allow us to better meet our customers’ needs and anticipate market demand.

Continue to Invest in and Expand our Sales and Distribution Capabilities to Attack New Markets and Better Penetrate Existing Markets. Our continued investment in our channel partners and sales force is designed to help optimize their market focus, improve segmentation, enter new geographies and provide our channel partners with compelling business incentives and discounts, along with training, marketing programs and technical support through Avaya Connect, our business partner program. We also plan to leverage our sales and distribution channels to accelerate customer adoption and generate an increasing percentage of our revenue from our new high value software solutions and user experience-centric applications.

5

Table of Contents

Pursue Strategic Relationships and Develop Talent Globally. We plan to continue our global growth by continuing to establish relationships and alliances and selectively acquiring capability-enhancing businesses. We intend to support this growth by developing a workforce that has both exceptional technical and leadership capabilities.

Risks Associated with Our Company

Our business is subject to a number of risks of which you should be aware before making an investment

decision. These risks are discussed more fully in the “Risk Factors” section of this prospectus immediately following this prospectus summary. These risks include, but are not limited to, the following:

| • | Our revenues are dependent on general economic conditions and the willingness of enterprises to make capital investments. The impact of economic conditions on the willingness of enterprises to make capital investments, particularly in business collaboration technology and related services can significantly affect our operating results and we believe that enterprises continue to be cautious about sustained economic growth. |

| • | The market opportunity for advanced communications products and services, including our next-generation business collaboration solutions may not develop in the ways that we anticipate. The demand for our offerings can change quickly and in ways that we may not anticipate because the market in which we operate is characterized by rapid, and sometimes disruptive, technological developments, evolving industry standards, frequent new product introductions and enhancements, changes in customer requirements and a limited ability to accurately forecast future customer demand. |

| • | We are dependent on our intellectual property. As a leader in technology and innovation in business collaboration, we are dependent on the maintenance of our current intellectual property rights and the establishment of new intellectual property rights. If we are not able to protect our intellectual property rights or if those rights are invalidated or circumvented, our business may be adversely affected. |

| • | Our degree of leverage could adversely affect our ability to raise additional capital to fund our operations and limit our ability to react to changes in the economy or our industry. Our degree of leverage could have important consequences, including making it more difficult for us to make payments on our indebtedness and increasing our vulnerability to general economic and industry conditions. |

| • | We face formidable competition from numerous established firms that provide both traditional enterprise voice communications solutions as well as providers of technology related to business collaboration and contact center solutions. In addition to the competition we face from traditional enterprise voice communications solutions and providers of technology related to business collaboration and contact center solutions, we expect competition to intensify and expand to include companies that do not currently compete directly against us. |

| • | The Sponsors have significant influence over corporate transactions. Following the completion of this offering, funds affiliated with TPG Capital, or TPG, and Silver Lake Partners, or Silver Lake, which are collectively referred to as our Sponsors, will have the ability to control the outcome of matters submitted for stockholder approval and may have interests that differ from those of our other stockholders. |

| • | We expect to be a “controlled company” within the meaning of the rules of the New York Stock Exchange. After completion of this offering, the Sponsors will continue to control a majority of the voting power of our outstanding common stock. As a result, we will qualify for, and intend to rely on, exemptions from certain corporate governance requirements. |

6

Table of Contents

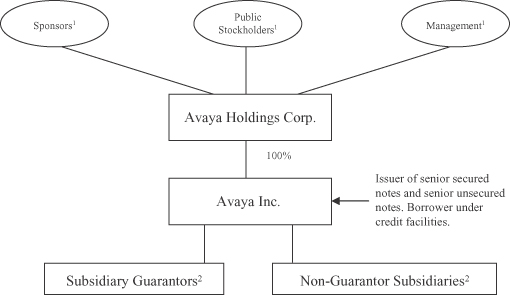

Company Information and Corporate Structure

Our principal executive offices are located at 211 Mt. Airy Road, Basking Ridge, NJ 07920. Our telephone number is (908) 953-6000. Our website address is www.avaya.com. Information contained in, and that can be accessed through, our website is not incorporated into and does not form a part of this prospectus.

Avaya Holdings Corp., formerly known as Sierra Holdings Corp., was incorporated under the laws of the State of Delaware on June 1, 2007 by affiliates of the Sponsors. The Sponsors, through a subsidiary holding company, acquired Avaya Inc., our principal U.S. operating subsidiary, and each of its subsidiaries in a merger transaction that was completed on October 26, 2007, which we refer to in this prospectus as the Merger. Since Avaya Inc.’s obligation to file periodic and current reports with the SEC ended on October 1, 2010, it has voluntarily filed such reports with the SEC to comply with the terms of the indentures governing its senior secured and unsecured notes. Avaya Holdings Corp. is a holding company with no stand-alone operations and has no material assets other than its ownership interest in Avaya Inc. and its subsidiaries. All of Avaya Holdings Corp.’s operations are conducted through its various subsidiaries, which are organized and operated according to the laws of their jurisdiction of incorporation, and consolidated by Avaya Holdings Corp.

As of September 30, 2011, our total outstanding indebtedness was $6,157 million (excluding capital lease obligations and $9 million of debt discount due upon settlement of our indebtedness), of which $5,148 million was attributable to financing associated with the Merger and $1,009 million was attributable to financing associated with the acquisition of NES. For a complete discussion of our financing see Note 9, “Financing Arrangements,” to our consolidated financial statements included elsewhere in this prospectus.

The following chart shows our organizational structure immediately following the consummation of this offering:

| (1) | Represents %, % and % of the total voting power in our company, respectively. |

| (2) | Substantially all of our domestic 100% owned subsidiaries as of September 30, 2011 guarantee our notes and our credit facilities. Other subsidiaries, including non-U.S. subsidiaries, do not guarantee our notes or our credit facilities. See “Description of Certain Outstanding Indebtedness” for more information. |

7

Table of Contents

THE OFFERING

Common stock we are offering | Shares | |

Common stock to be outstanding after this offering | Shares | |

Option to purchase additional shares offered to underwriters | Shares | |

Use of proceeds | We intend to use the net proceeds received by us in connection with this offering for the following purposes: | |

• to repay a portion of our long-term indebtedness; | ||

• to redeem all of our outstanding Series A Preferred Stock; and | ||

• to pay certain amounts in connection with the termination of our management services agreement with affiliates of our Sponsors pursuant to its terms. | ||

See “Use of Proceeds.” | ||

Risk factors | You should carefully read the “Risk Factors” section of this prospectus beginning on page 16 for a discussion of factors to consider carefully before deciding whether to purchase shares of our common stock. | |

Proposed NYSE symbol | “AVYA” | |

As of September 30, 2011, we had 487,401,790 shares of common stock outstanding. This excludes the following numbers of shares of our common stock issuable in connection with the exercise of warrants outstanding as of September 30, 2011 and equity awards under our Amended and Restated 2007 Equity Incentive Plan, or the 2007 Plan:

| • | 100,000,000 shares of common stock issuable upon the exercise of warrants held by affiliates of our Sponsors, which warrants are subject to the lock-up agreements described under “Underwriters” and exercisable at any time prior to December 18, 2019 at an exercise price of $3.25 per share, see “Description of Capital Stock—Warrants” and “Principal Stockholders”; |

| • | 429,761 shares of common stock issuable on the exercise of options that were awarded to executive officers prior to the Merger and were permitted to be rolled over into equity awards issued by us upon consummation of the Merger, or Continuation Options, each with an exercise price of $1.25 per share; |

| • | 972,341 shares of common stock issuable on the distribution of units that were awarded to executive officers prior to the Merger and were permitted to be rolled over into equity awards issued by us upon consummation of the Merger, or Continuation Units; |

| • | 43,595,906 shares of common stock issuable upon the exercise of options with exercise prices ranging from $3.00 to $5.00 per share and a weighted average exercise price of $3.11 per share; |

| • | 1,560,000 shares of common stock issuable on the vesting and distribution of restricted stock units, or RSUs; and |

8

Table of Contents

| • | 4,674,875 additional shares of common stock as of September 30, 2011 reserved for future grants under the 2007 Plan. |

This also excludes additional shares of common stock reserved for future equity incentive plans to be effective upon the completion of this offering.

Unless otherwise indicated, all information in this prospectus:

| • | assumes the adoption of our amended and restated certificate of incorporation and our amended and restated bylaws to be effective upon the closing of this offering; |

| • | assumes no exercise by the underwriters of their option to purchase up to additional shares of our common stock in this offering; and |

| • | reflects, for all prior periods, a for of our common stock to be effected prior to the consummation of this offering. |

9

Table of Contents

SUMMARY HISTORICAL FINANCIAL DATA

The following table sets forth our summary historical consolidated financial data at the dates and for the periods indicated. Avaya Holdings Corp. was incorporated on June 1, 2007 by affiliates of the Sponsors. Avaya Holdings Corp., through a subsidiary holding company, entered into a merger agreement with Avaya Inc., or the Predecessor, pursuant to which the holding company merged with and into Avaya Inc., with Avaya Inc. continuing as the surviving entity and a wholly owned subsidiary of Avaya Holdings Corp., in a transaction that was completed on October 26, 2007. Avaya Holdings Corp. is a holding company and has no material assets or stand-alone operations other than its ownership in Avaya Inc. and its subsidiaries. The summary historical consolidated financial data set forth below are those of Avaya Holdings Corp. and its consolidated subsidiaries, or the Successor, from its inception on June 1, 2007 through September 30, 2011 and those of its predecessor, Avaya Inc., for all prior periods through the closing date of the Merger.

The Predecessor summary historical consolidated financial data set forth below as of and for the year ended September 30, 2007 and for the period October 1, 2007 through October 26, 2007 have been derived from our Predecessor’s audited consolidated financial statements and related notes, which are not included in this prospectus. The Successor summary historical consolidated financial data set forth below as of and for the years ended September 30, 2009, 2010 and 2011 have been derived from our audited consolidated financial statements and related notes included elsewhere in this prospectus. The Successor summary historical consolidated financial data set forth below for the year ended September 30, 2008 have been derived from our audited consolidated financial statements and related notes, which are not included in this prospectus. The Successor summary historical consolidated financial data set forth below as of and for the period June 1, 2007 through September 30, 2007 has been derived from our consolidated financial statements, which are not included in this prospectus. The Successor had no operations prior to the Merger. As part of the Merger on October 26, 2007, we entered into various financing arrangements and, as a result, had a different capital structure following the Merger. Accordingly, the results of operations for periods subsequent to the Merger will not necessarily be comparable to prior periods.

The following summary should be read together with our consolidated financial statements and the related notes appearing elsewhere in this prospectus and the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” section of this prospectus.

10

Table of Contents

| Successor | Predecessor | |||||||||||||||||||||||||||||

| Fiscal year ended September 30, | Period from June 1, 2007 through September 30, 2007(2) | Period from October 1, 2007 through October 26, 2007 | Fiscal year ended September 30, 2007 | |||||||||||||||||||||||||||

| 2011 | 2010 | 2009 | 2008(1) | |||||||||||||||||||||||||||

| (in millions, except per share amounts) | ||||||||||||||||||||||||||||||

STATEMENT OF OPERATIONS DATA: | ||||||||||||||||||||||||||||||

REVENUE | ||||||||||||||||||||||||||||||

Products | $ | 2,976 | $ | 2,602 | $ | 1,923 | $ | 2,595 | $ | — | $ | 96 | $ | 2,875 | ||||||||||||||||

Services | 2,571 | 2,458 | 2,227 | 2,328 | — | 150 | 2,403 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||

| 5,547 | 5,060 | 4,150 | 4,923 | — | 246 | 5,278 | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||

COSTS | ||||||||||||||||||||||||||||||

Products: | ||||||||||||||||||||||||||||||

Costs (exclusive of amortization of intangible assets) | 1,314 | 1,243 | 872 | 1,256 | — | 56 | 1,295 | |||||||||||||||||||||||

Amortization of technology intangible assets | 257 | 291 | 248 | 231 | — | 1 | 20 | |||||||||||||||||||||||

Services | 1,344 | 1,354 | 1,164 | 1,403 | — | 100 | 1,512 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||

| 2,915 | 2,888 | 2,284 | 2,890 | — | 157 | 2,827 | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||

GROSS MARGIN | 2,632 | 2,172 | 1,866 | 2,033 | — | 89 | 2,451 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||

OPERATING EXPENSES | ||||||||||||||||||||||||||||||

Selling, general and administrative | 1,845 | 1,721 | 1,272 | 1,456 | — | 111 | 1,552 | |||||||||||||||||||||||

Research and development | 461 | 407 | 309 | 376 | — | 29 | 444 | |||||||||||||||||||||||

Amortization of intangible assets | 226 | 218 | 207 | 187 | — | 4 | 48 | |||||||||||||||||||||||

Impairment of long-lived assets | — | 16 | 2 | 10 | — | — | — | |||||||||||||||||||||||

Impairment of indefinite-lived intangible assets | — | — | 60 | 130 | — | — | — | |||||||||||||||||||||||

Goodwill impairment | — | — | 235 | 899 | — | — | — | |||||||||||||||||||||||

Restructuring charges, net | 189 | 171 | 160 | — | — | 1 | 36 | |||||||||||||||||||||||

In-process research and development charge | — | — | 12 | 112 | — | — | — | |||||||||||||||||||||||

Acquistion-related costs | 5 | 20 | 29 | — | — | — | — | |||||||||||||||||||||||

Merger-related costs | — | — | — | 1 | — | 57 | 105 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||

| 2,726 | 2,553 | 2,286 | 3,171 | — | 202 | 2,185 | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||

OPERATING (LOSS) INCOME | (94 | ) | (381 | ) | (420 | ) | (1,138 | ) | — | (113 | ) | 266 | ||||||||||||||||||

Interest expense | (460 | ) | (487 | ) | (409 | ) | (377 | ) | — | — | (1 | ) | ||||||||||||||||||

Loss on extinguishment of debt | (246 | ) | — | — | — | — | — | — | ||||||||||||||||||||||

Other income, net | 5 | 15 | 14 | 27 | — | 1 | 43 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||

(LOSS) INCOME BEFORE INCOME TAXES | (795 | ) | (853 | ) | (815 | ) | (1,488 | ) | — | (112 | ) | 308 | ||||||||||||||||||

Provision for (benefit from) income taxes | 68 | 18 | 30 | (183 | ) | — | (24 | ) | 93 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||

NET (LOSS) INCOME | (863 | ) | (871 | ) | (845 | ) | (1,305 | ) | — | (88 | ) | 215 | ||||||||||||||||||

Less net income attributable to noncontrolling interests | — | 3 | 2 | 2 | — | — | 3 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||

NET (LOSS) INCOME ATTRIBUTABLE TO AVAYA HOLDINGS CORP. | (863 | ) | (874 | ) | (847 | ) | (1,307 | ) | — | (88 | ) | 212 | ||||||||||||||||||

Less: Accretion and accrued dividendson Series A preferred stock | (7 | ) | (62 | ) | — | — | — | — | — | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||

NET (LOSS) INCOME ATTRIBUTABLE TO AVAYA HOLDINGS CORP. COMMON STOCKHOLDERS | $ | (870 | ) | $ | (936 | ) | $ | (847 | ) | $ | (1,307 | ) | $ | — | $ | (88 | ) | $ | 212 | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||

SHARE DATA: | ||||||||||||||||||||||||||||||

Net (loss) income per share attributable to common stockholders—basic | $ | (1.78 | ) | $ | (1.92 | ) | $ | (1.74 | ) | $ | (2.87 | ) | $ | — | $ | (0.19 | ) | $ | 0.47 | |||||||||||

Weighted average shares outstanding—basic | 489.0 | 488.6 | 488.1 | 455.9 | — | 462.9 | 454.2 | |||||||||||||||||||||||

Net (loss) income per share attributable to common stockholders—diluted | (1.78 | ) | (1.92 | ) | (1.74 | ) | (2.87 | ) | — | (0.19 | ) | 0.46 | ||||||||||||||||||

Weighted average shares outstanding—diluted | 489.0 | 488.6 | 488.1 | 455.9 | — | 462.9 | 461.3 | |||||||||||||||||||||||

11

Table of Contents

| Successor | Predecessor | |||||||||||||||||||||||||||||

| Fiscal year ended September 30, | Period from June 1, 2007 through September 30, 2007(2) | Period from October 1, 2007 through October 26, 2007 | Fiscal year ended September 30, 2007 | |||||||||||||||||||||||||||

| 2011 | 2010 | 2009 | 2008(1) | |||||||||||||||||||||||||||

| (in millions) | ||||||||||||||||||||||||||||||

BALANCE SHEET DATA (at end of period): | ||||||||||||||||||||||||||||||

Cash and cash equivalents | $ | 415 | $ | 594 | $ | 582 | $ | 594 | $ | — | $ | 1,270 | ||||||||||||||||||

Intangible assets, net | 2,129 | 2,603 | 2,636 | 3,154 | — | 248 | ||||||||||||||||||||||||

Goodwill | 4,079 | 4,075 | 3,695 | 3,956 | — | 1,157 | ||||||||||||||||||||||||

Total assets | 8,561 | 9,276 | 8,665 | 10,010 | — | 5,933 | ||||||||||||||||||||||||

Total debt (excluding capital lease obligations) | 6,157 | 5,928 | 5,150 | 5,222 | — | — | ||||||||||||||||||||||||

Preferred stock, Series A | 137 | 130 | — | — | — | — | ||||||||||||||||||||||||

Total Avaya Holdings Corp. stockholders’ equity (deficiency) | (2,500 | ) | (1,543 | ) | (682 | ) | 1,063 | — | 2,586 | |||||||||||||||||||||

STATEMENT OF CASH FLOWS DATA: | ||||||||||||||||||||||||||||||

Net cash provided by (used in) | ||||||||||||||||||||||||||||||

Operating activities | $ | (300 | ) | $ | 42 | $ | 242 | $ | 304 | $ | — | $ | 133 | $ | 637 | |||||||||||||||

Investing activities | (101 | ) | (864 | ) | (155 | ) | (7,205 | ) | — | (16 | ) | (360 | ) | |||||||||||||||||

Financing activities | 228 | 853 | (101 | ) | 7,512 | — | 11 | 54 | ||||||||||||||||||||||

OTHER FINANCIAL DATA: | ||||||||||||||||||||||||||||||

EBITDA | $ | 313 | $ | 320 | $ | 240 | $ | (515 | ) | $ | — | $ | (94 | ) | $ | 557 | ||||||||||||||

Adjusted EBITDA(3) | 971 | 795 | 753 | 859 | — | (27 | ) | 832 | ||||||||||||||||||||||

Capital expenditures, net | 83 | 79 | 76 | 120 | — | 8 | 120 | |||||||||||||||||||||||

Capitalized software development costs | 42 | 43 | 43 | 74 | — | 7 | 93 | |||||||||||||||||||||||

| (1) | The summary historical consolidated financial data above as of and for the year ended September 30, 2008 reflect the results of Avaya Holdings Corp. for the entire fiscal year and includes the results of Avaya Inc. and its consolidated subsidiaries subsequent to October 26, 2007, the date of the Merger. |

| (2) | Avaya Holdings Corp. is a holding company formed on June 1, 2007 by affiliates of the Sponsors for the purpose of consummating the Merger. Avaya Holdings Corp. has no material assets or stand-alone operations other than its ownership in Avaya Inc. and its subsidiaries. The summary historical consolidated financial data above as of September 30, 2007 and for the period from June 1, 2007 through September 30, 2007 reflects the results of Avaya Holdings Corp., which did not have assets or operations prior to the Merger. |

| (3) | Adjusted EBITDA is calculated in accordance with Avaya Inc.’s debt agreements entered into in connection with the Merger. For the fiscal year ended September 30, 2007, Adjusted EBITDA is calculated in accordance with the debt agreements for comparative purposes. |

EBITDA is defined as net income (loss) before income taxes, interest and depreciation and amortization. EBITDA provides us with a measure of operating performance that excludes items that are outside the control of management, which can differ significantly from company to company depending on capital structure, the tax jurisdictions in which companies operate and capital investments. Under Avaya Inc.’s debt agreements, its ability to draw on its revolving credit facilities or engage in activities such as incurring additional indebtedness, making investments and paying dividends is tied in part to ratios based on Adjusted EBITDA. EBITDA and Adjusted EBITDA are non-GAAP measures. GAAP is a reference to generally accepted accounting principles in the United States of America. As defined in Avaya Inc.’s debt agreements, Adjusted EBITDA is a measure of EBITDA further adjusted to exclude certain charges and other adjustments permitted in calculating covenant compliance under Avaya Inc.’s debt agreements. We believe that including supplementary information concerning Adjusted EBITDA is appropriate to provide additional information to investors to demonstrate compliance with Avaya Inc.’s debt agreements and because it serves as a basis for determining management compensation. In addition, we believe Adjusted EBITDA provides more comparability between our historical results and results that reflect purchase accounting and our new capital structure following the Merger. Accordingly, Adjusted EBITDA measures our financial performance based on operational factors that management can impact in the short-term, namely the Company’s pricing strategies, volume, costs and expenses of the organization.

12

Table of Contents

EBITDA and Adjusted EBITDA have limitations as analytical tools. Adjusted EBITDA does not represent net income (loss) or cash flow from operations as those terms are defined by GAAP and does not necessarily indicate whether cash flows will be sufficient to fund cash needs. While Adjusted EBITDA and similar measures are frequently used as measures of operations and the ability to meet debt service requirements, these terms are not necessarily comparable to other similarly titled captions of other companies due to the potential inconsistencies in the method of calculation. Adjusted EBITDA does not reflect the impact of earnings or charges resulting from matters that we consider not to be indicative of our ongoing operations. In particular, the definition of Adjusted EBITDA in Avaya Inc.’s debt agreements allows us to add back certain non-cash charges that are deducted in calculating net income (loss). Avaya Inc.’s debt agreements also allows us to add back restructuring charges, Sponsor monitoring fees and other specific cash costs and expenses as defined in the agreements and that portion of our pension costs, other post-employment benefit costs, and non-retirement post-employment benefit costs representing the amortization of prior service costs and net actuarial gains/losses associated with these employment benefits. However, these are expenses that may recur, may vary and are difficult to predict. Further, Avaya Inc.’s debt agreements require that Adjusted EBITDA be calculated for the most recent four fiscal quarters. As a result, the measure can be disproportionately affected by a particularly strong or weak quarter. Further, it may not be comparable to the measure for any subsequent four-quarter period or any complete fiscal year.

13

Table of Contents

The unaudited reconciliation of net (loss) income, which is a GAAP measure, to EBITDA and Adjusted EBITDA is presented below:

| Successor |

| Predecessor | ||||||||||||||||||||||||||||

| Fiscal year ended September 30, | Period from June 1, 2007 through September 30, 2007(2) |

| Period from October 1, 2007 through October 26, 2007 | Fiscal year ended September 30, 2007 | ||||||||||||||||||||||||||

| 2011 | 2010 | 2009 | 2008(1) | |||||||||||||||||||||||||||

| (in millions) | ||||||||||||||||||||||||||||||

Net (loss) income | $ | (863 | ) | $ | (871 | ) | $ | (845 | ) | $ | (1,305 | ) | $ | — | $ | (88 | ) | $ | 215 | |||||||||||

Interest expense | 460 | 487 | 409 | 377 | — | — | 1 | |||||||||||||||||||||||

Interest income | (5 | ) | (5 | ) | (6 | ) | (20 | ) | — | (5 | ) | (49 | ) | |||||||||||||||||

Income tax expense (benefit) | 68 | 18 | 30 | (183 | ) | — | (24 | ) | 93 | |||||||||||||||||||||

Depreciation and amortization | 653 | 691 | 652 | 616 | — | 23 | 297 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

EBITDA | 313 | 320 | 240 | (515 | ) | — | (94 | ) | 557 | |||||||||||||||||||||

Impact of purchase accounting adjustments(3) | — | 5 | (1 | ) | 230 | — | — | — | ||||||||||||||||||||||

Restructuring charges, net | 189 | 171 | 160 | — | — | 1 | 36 | |||||||||||||||||||||||

Sponsors’ fees(4) | 7 | 7 | 7 | 6 | — | — | — | |||||||||||||||||||||||

Merger-related costs(5) | — | — | — | 1 | — | 57 | 105 | |||||||||||||||||||||||

Acquisition-related costs(6) | 5 | 20 | 29 | — | — | — | — | |||||||||||||||||||||||

Integration-related costs(7) | 132 | 208 | 5 | — | — | — | — | |||||||||||||||||||||||

Debt registration fees | — | 1 | — | — | — | — | — | |||||||||||||||||||||||

Loss on extinguishment of debt(8) | 246 | — | — | — | — | — | — | |||||||||||||||||||||||

Third-party fees expensed in connection with debt modification(9) | 9 | — | — | — | — | — | — | |||||||||||||||||||||||

Strategic initiative costs(10) | — | 6 | 21 | 27 | — | — | — | |||||||||||||||||||||||

Non-cash share-based compensation | 12 | 19 | 10 | 21 | — | — | 39 | |||||||||||||||||||||||

Write-down of held for sale assets to net realizable value | 1 | — | — | — | — | — | — | |||||||||||||||||||||||

Loss (gain) on sale of long-lived assets | 1 | (4 | ) | 1 | 1 | — | — | (8 | ) | |||||||||||||||||||||

Impairment of long-lived assets | — | 16 | 62 | 140 | — | — | 8 | |||||||||||||||||||||||

Goodwill impairment | — | — | 235 | 899 | — | — | — | |||||||||||||||||||||||

Bank fees | — | — | — | — | — | — | 7 | |||||||||||||||||||||||

Net (income) loss of unrestricted subsidiaries, net of dividends received | — | (6 | ) | (4 | ) | (5 | ) | — | 2 | (6 | ) | |||||||||||||||||||

(Gain) loss on foreign currency transactions | (12 | ) | 1 | (8 | ) | (15 | ) | — | 1 | — | ||||||||||||||||||||

Pension/OPEB/nonretirement postemployment benefits and long-term disability costs(11) | 68 | 31 | (4 | ) | 69 | — | 6 | 94 | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

Adjusted EBITDA | $ | 971 | $ | 795 | $ | 753 | $ | 859 | $ | — | $ | (27 | ) | $ | 832 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

| (1) | The summary historical consolidated financial data above as of and for the year ended September 30, 2008 reflect the results of Avaya Holdings Corp. for the entire fiscal year and includes the results of Avaya Inc. and its consolidated subsidiaries subsequent to October 26, 2007, the date of the Merger. |

| (2) | Avaya Holdings Corp. is a holding company formed on June 1, 2007 by affiliates of the Sponsors for the purpose of consummating the Merger. Avaya Holdings Corp. has no material assets or stand-alone operations other than its ownership in Avaya Inc. and its subsidiaries. The summary historical consolidated financial data above as of September 30, 2007 and for the period from June 1, 2007 through September 30, 2007 reflects the results of Avaya Holdings Corp., which did not have assets or operations prior to the Merger. |

| (3) | For fiscal years 2011 and 2010, represents adjustments to eliminate the impact of certain purchase accounting adjustments recorded as a result of the acquisitions of NES and Konftel AB, or Konftel, and the Merger, including the recognition of the amortization of business partner commissions, which were eliminated in purchase accounting, the recognition of revenue and costs that were deferred in prior periods and eliminated in purchase accounting and the elimination of the impact of estimated fair value adjustments |

14

Table of Contents

| for certain assets and liabilities, such as inventory. For fiscal year 2009, represents the recognition of the amortization of business partner commissions which were eliminated in purchase accounting, partially offset by the recognition of revenues and costs that were deferred in prior years and eliminated in purchase accounting as a result of the Merger. For fiscal year 2008, represents adjustments to eliminate the impact of certain purchase accounting adjustments recorded as a result of the Merger, including: the recognition of the amortization of business partner commissions, which were eliminated in purchase accounting; elimination of certain deferred revenues and deferred costs and expenses; elimination of previously capitalized software development costs; write-off of in-process research and development, or IPRD, costs and adjustment to estimated fair values of certain assets and liabilities, such as inventory. |

| (4) | Sponsors’ fees represent monitoring fees payable to affiliates of the Sponsors pursuant to a management services agreement entered into at the time of the Merger. See “Certain Relationships and Related Party Transactions.” |

| (5) | Merger-related costs are costs directly attributable to the Merger and include investment banking, legal and other third-party costs. |

| (6) | Acquisition-related costs include legal and other costs related to the acquisition of NES and other acquisitions. |

| (7) | Integration-related costs primarily represent third-party consulting fees and other administrative costs associated with consolidating and coordinating the operations of Avaya and NES. These costs were incurred in connection with, among other things, the on-boarding of NES personnel, developing compatible IT systems and internal processes and developing and implementing a strategic operating plan to help enable a smooth transition with minimal disruption to NES customers. Integration-related costs also include fees paid to certain Nortel-controlled entities for logistics and other support functions being performed on a temporary basis pursuant to a transition services agreement. |

| (8) | Loss on extinguishment of debt represents the loss recognized in connection with the payment in full of the senior secured incremental term B-2 loans. The loss is based on the difference between the reacquisition price and the carrying value of the senior secured incremental term B-2 loans. See Note 9, “Financing Arrangements,” to our consolidated financial statements located elsewhere in this prospectus. |

| (9) | The third-party fees expensed in connection with the modification of the senior secured credit facility are discussed in Note 9, “Financing Arrangements,” to our consolidated financial statements located elsewhere in this prospectus. |

| (10) | Strategic initiative costs represent consulting fees in connection with management’s cost-savings actions, which commenced subsequent to the Merger. |

| (11) | Represents that portion of our pension costs, other post-employment benefit costs, non-retirement post-employment benefit costs representing the amortization of prior service costs and net actuarial gains/losses associated with these employment benefits. For the fiscal year ended September 30, 2011, the amount includes a curtailment charge of $7 million associated with workforce reductions in Germany. |

15

Table of Contents

Investing in our common stock involves a high degree of risk. You should carefully consider the following risk factors, as well as the other information in this prospectus, before deciding to invest in our common stock. The occurrence of any of the following risks could harm our business, financial condition, results of operations or prospects. In that case, the trading price of our common stock could decline, and you may lose all or part of your investment.

Risks Associated with Our Company

Our solutions may fail to keep pace with rapidly changing technology and evolving industry standards.

The market in which we operate is characterized by rapid, and sometimes disruptive, technological developments, evolving industry standards, frequent new product introductions and enhancements and changes in customer requirements. In addition, both traditional and new competitors are investing heavily in this market and competing for customers. As next-generation business collaboration technology continues to evolve, we must keep pace in order to maintain or expand our market leading position. We recently introduced a significant number of new product offerings and are increasingly focused on new high, value software solutions, as a revenue driver. If we are not able to successfully develop and bring these new solutions to market in a timely manner, achieve market acceptance of our solutions or identify new market opportunities for our solutions, our business and results of operations may be materially and adversely affected.

The market opportunity for business collaboration, unified communications solutions and other products and services may not develop in the ways that we anticipate.

The demand for our offerings can change quickly and in ways that we may not anticipate because the market in which we operate is characterized by rapid, and sometimes disruptive, technological developments, evolving industry standards, frequent new product introductions and enhancements, changes in customer requirements and a limited ability to accurately forecast future customer orders. Our operating results may be adversely affected if the market opportunity for our products and services does not develop in the ways that we anticipate.

We cannot predict whether:

| • | our solutions will attract and retain customers and channel partners or that we can execute our sales strategy successfully; |

| • | the demand for our products and services, including Avaya Aura and the Avaya Flare Experience, will grow as quickly as we anticipate or current or future competitors or new technologies will cause the market to evolve in a manner different than we expect; |

| • | other technologies will become more accepted or standard in our industry or will disrupt our SIP-based technology platform; or |

| • | we will be able to maintain a leadership or profitable position as this opportunity develops. |

We face formidable competition from numerous established firms that provide both traditional enterprise voice communications solutions as well as providers of technology related to business collaboration and contact center solutions; as these markets evolve, we expect competition to intensify and expand to include companies that do not currently compete directly against us.

We compete against providers of both traditional enterprise voice communications solutions as well as providers of technology related to business collaboration and contact center solutions. For example, we compete with Alcatel-Lucent, Genesys Telecommunications Laboratories, Inc., or Genesys, Aspect Software, Inc., or Aspect, Brocade Communications Systems, Inc., or Brocade, Cisco Systems, Inc., or Cisco, Juniper Networks,

16

Table of Contents

Inc., or Juniper, Microsoft Corporation, or Microsoft, NEC Corporation, or NEC, and Siemens Enterprise Communications Group, or SEN. Our video conferencing solutions both partner and compete with solutions offered by Polycom Inc., TANDBERG (now Cisco) and LifeSize (now a division of Logitech International S.A.). We also face competition in the small and medium enterprise market from many competitors, including Cisco, Alcatel-Lucent, NEC, Matsushita Electric Corporation of America, and Mitel Networks Corp., or Mitel, although the market for these products is more fragmented. We face competition in certain geographies with companies that have a particular strength and focus in particular countries or regions, such as Huawei Technologies Co., Ltd. in China and Intelbras S.A. in Latin America. Our services business competes with companies like those above in offering services, either directly or indirectly through their channel partners, with respect to their own product offerings, as well as with many value-added resellers, consulting and systems integration firms and network service providers.

In addition, because the business collaboration market continues to evolve and technology continues to develop rapidly, we may face competition in the future from companies that do not currently compete against us, but whose current business activities may bring them into competition with us in the future. In particular, this may be the case as business, information technology and communications applications deployed on converged networks become more integrated to support business collaboration. We may face increased competition from current leaders in information technology infrastructure, information technology, consumer products companies, personal and business applications and the software that connects the network infrastructure to those applications. With respect to services, we may also face competition from companies that seek to sell remotely hosted services or software as a service directly to the end customer. Competition from these potential market entrants may take many forms, including offering products and applications similar to those we offer as part of another offering. In addition, these technologies continue to move from a proprietary environment to an open standards-based environment.

Several of our existing competitors have, and many of our future competitors may have, greater financial, personnel, technical, research and development and other resources, more well-established brands or reputations and broader customer bases than we do and, as a result, these competitors may be in a stronger position to respond quickly to potential acquisitions and other market opportunities, new or emerging technologies and changes in customer requirements. Some of these competitors may have customer bases that are more geographically balanced than ours and, therefore, may be less affected by an economic downturn in a particular region. Other competitors may have deeper expertise in a particular stand-alone technology that develops more quickly than we anticipate. Competitors with greater resources also may be able to offer lower prices, additional products or services or other incentives that we cannot match or do not offer. Industry consolidations may also create competitors with broader and more geographic coverage and the ability to reach enterprises through communications service providers. Existing customers of data networking companies that compete against us may be inclined to purchase enterprise communications solutions from their current data networking or software vendors rather than from us. Also, as communications and data networks converge, we may face competition from systems integrators that traditionally have been focused on data network integration.

We cannot predict which competitors may enter our markets in the future, what form such competition may take or whether we will be able to respond effectively to the entry of new competitors into competition with us or the rapid evolution in technology and product development that has characterized our businesses. In addition, in order to effectively compete with any new market entrant, we may need to make additional investments in our business, use more capital resources than our business currently requires or reduce prices, any of which may materially and adversely affect our profitability.

Our revenues are dependent on general economic conditions and the willingness of enterprises to make capital investments.

One factor that significantly affects our operating results is the impact of economic conditions on the willingness of enterprises to make capital investments, particularly in business collaboration technology and

17

Table of Contents

related services. Given the current state of the economy, we believe that enterprises continue to be cautious about sustained economic growth and have tried to maintain or improve profitability through cost control and constrained capital spending, which places additional pressure on IT departments to demonstrate acceptable return on investment and may cause them to delay or reject capital projects, including implementing our solutions. Because it is not certain whether enterprises will increase spending on business collaboration technology significantly in the near term, we could experience continued pressure on our ability to increase our revenue. Our ability to grow revenue also may be affected by other factors, such as competitive pricing pressures, price erosion and our ability to effectively and consistently price new and existing offers in the marketplace. If these or other conditions limit our ability to grow revenue or cause our revenue to decline and we cannot reduce costs on a timely basis or at all, our operating results may be materially and adversely affected.

Our strategy depends in part on our ability to rely on our indirect sales channel.

We continue to take steps to sell our products and services into new and expanded geographic markets and to a broader customer base. An important element of our go-to-market strategy, therefore, involves our indirect sales channel, which includes our global network of alliance partners, distributors, dealers, value-added resellers, telecommunications service providers and system integrators. For example, although we expanded our indirect channel network and gained relationships with new channel partners through our acquisition of NES, in order to be successful we must further monetize the NES installed base by increasing the services attach rate for the Nortel customers we acquired. Our relationships with channel partners are important elements of our marketing and sales efforts and certain of our contractual agreements with our largest distributors and channel partners generally permit termination of the relationship by either party for convenience upon prior notice of 30 to 180 days. See “Our Business—Customers, Sales, Partners and Distribution—Sales, Partners and Distribution” for more information on Avaya Connect, our global business partner program, and the standard terms of our program agreements. Our financial results could be adversely affected if our contracts with channel partners were terminated, if our relationships with channel partners were to deteriorate, if our maintenance pricing or other services strategies conflict with those of our channel partners, if any of our competitors were to enter into strategic relationships with or acquire a significant channel partner or if the financial condition of our channel partners were to weaken. In addition, we may expend time, money and other resources on developing and maintaining channel relationships that are ultimately unsuccessful. There can be no assurance that we will be successful in maintaining, expanding or developing relationships with channel partners, including those obtained as a result of the acquisition of NES. If we are not successful, we may lose sales opportunities, customers and market share.

We are dependent on our intellectual property. If we are not able to protect our proprietary rights or if those rights are invalidated or circumvented, our business may be adversely affected.

We believe that developing new products and technology is critical to our success. As a leader in technology and innovation in business collaboration, we are dependent on the maintenance of our current intellectual property rights and the establishment of new intellectual property rights. We generally protect our intellectual property through patents, trademarks, trade secrets, copyrights, confidentiality and nondisclosure agreements and other measures. There can be no assurance that patents will be issued from pending applications that we have filed or that our patents will be sufficient to protect our key technology. Although we have been granted and have acquired many patents, have obtained other intellectual property rights and continue to file new patent applications and seek additional proprietary rights, there can be no assurances made that any of our patents, patent applications or our other intellectual property or proprietary rights will not be challenged, invalidated or circumvented. In addition, our business is global and the level of protection of our proprietary technology will vary by country, particularly in countries that do not have well developed judicial systems or laws that adequately protect intellectual property rights. Any actions taken in these countries may have results that are different than if such actions were taken under the laws of the U.S. Patent litigation and other challenges to our patents and other proprietary rights are costly and unpredictable and may prevent us from marketing and selling a product in a particular geographic area. Patent filings by third parties, whether made before or after the date of our filings, could render our intellectual property less valuable. Competitors and others may also misappropriate

18

Table of Contents

our intellectual property, disputes as to ownership of intellectual property may arise and our intellectual property may otherwise fall into the public domain. If we are unable to protect our proprietary rights, we may be at a disadvantage to others who did not incur the substantial time and expense we incurred to create our products. In addition, our efforts to enforce or protect our proprietary rights may be ineffective, could result in substantial costs and diversion of resources and could substantially harm operating results.

If we fail to retain or attract key employees, our business may be harmed.

The success of our business depends on the skill, experience and dedication of our employee base. If we are unable to retain and recruit sufficiently experienced and capable personnel, especially in the key areas of product development, sales, services and management, our business and financial results may suffer. Experienced and capable personnel in the technology industry remain in high demand, and there is continual competition for their talents among our competitors. When talented employees leave, we may have difficulty replacing them and our business may suffer. While we strive to maintain our competitiveness in the marketplace, there can be no assurance that we will be able to successfully retain and attract the personnel that we need to achieve our business objectives.

We rely on third-party providers for the manufacture, warehousing and distribution logistics associated with our products.