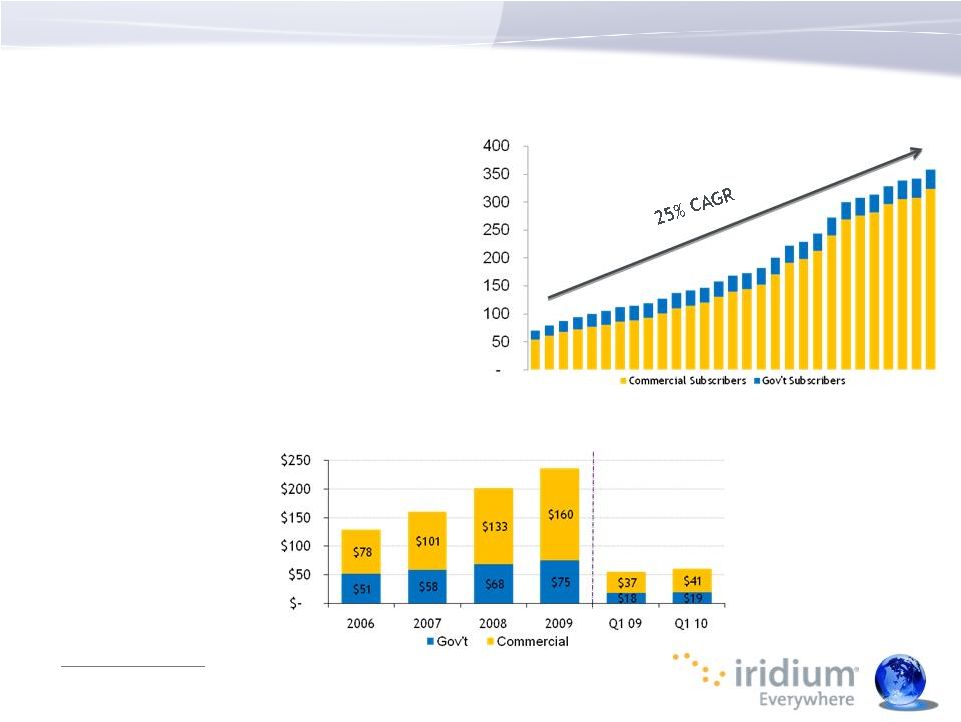

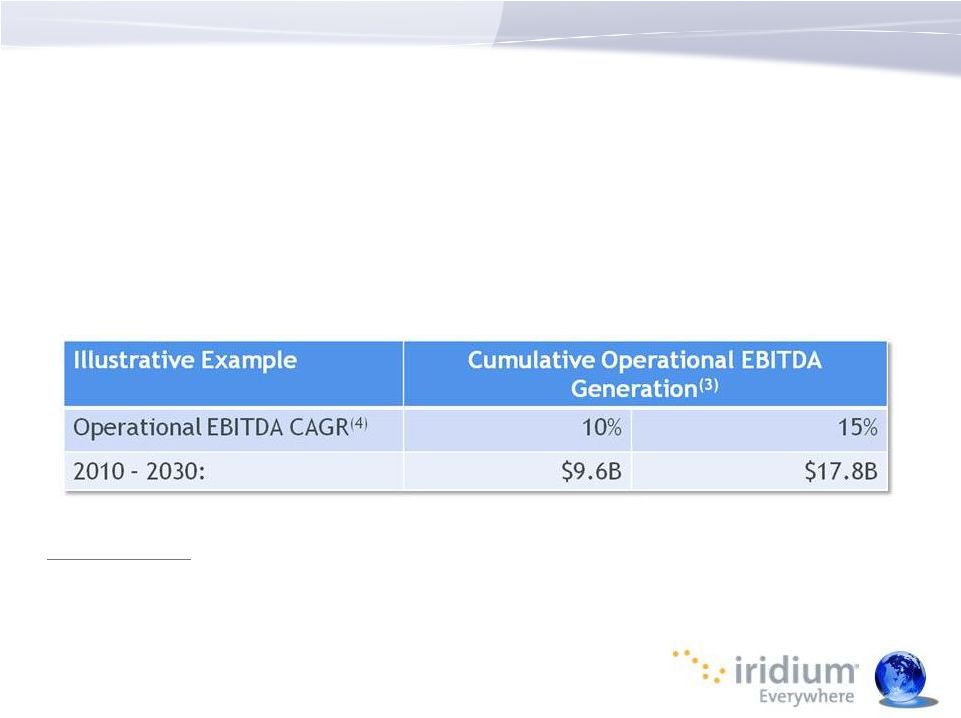

Basis of Presentation 3 3 • Reporting Entity For comparison purposes, we have presented the operating results of Iridium Holdings LLC and Iridium Communications Inc. on a combined basis for the year ended December 31, 2009 along with the Iridium Holdings LLC operating results for 2008. The combined 2009 presentation is a simple mathematical addition of the pre-acquisition results of operations of Iridium Holdings LLC for the period from January 1, 2009 to September 29, 2009 and the post-acquisition results of operations of Iridium Communications Inc. for the three months ended December 31, 2009. Please note that this presentation is different from the “combined” presentation that we include in the ‘Management’s Discussion and Analysis’ section of our Form 8-K filed on May 10, 2010, which combined the pre-acquisition results of operations of Iridium Holdings LLC for the period from January 1, 2009 to September 29, 2009 with the full year 2009 results of operations of Iridium Communications Inc., both pre- and post-acquisition. Iridium Communications Inc. had no material operating activities from the date of formation of GHL Acquisition Corp. until the acquisition. There are no other adjustments made in the combined presentation. This presentation is intended to facilitate the evaluation and understanding of the financial performance of the Iridium business on a year-to-year basis. Management believes this presentation is useful in providing the users of our financial information with an understanding of our results of operations because there were no material changes to the operations or customer relationships of Iridium as a result of the acquisition of Iridium Holdings LLC by GHL Acquisition Corp. • Non-GAAP Measures In addition to disclosing financial results that are determined in accordance with U.S. GAAP, we disclose Operational EBITDA, which is a non-GAAP financial measure, as a supplemental measure to help investors evaluate our fundamental operational performance. Operational EBITDA represents earnings before interest, income taxes, depreciation and amortization, Iridium NEXT revenue and expenses (for periods prior to the commencement of operations of Iridium NEXT), stock-based compensation expenses, transaction expenses associated with the acquisition, the impact of purchase accounting adjustments, and changes in the fair value of warrants. We also present Operational EBITDA expressed as a percentage of total revenues, or Operational EBITDA margin. Operational EBITDA does not represent, and should not be considered, an alternative to GAAP measurements such as net income, and our calculations thereof may not be comparable to similarly entitled measures reported by other companies. A reconciliation of Operational EBITDA to net (loss) income, its comparable GAAP financial measure, is in the attached table. By eliminating interest, income taxes, depreciation and amortization, Iridium NEXT revenue and expenses (for periods prior to the deployment of Iridium NEXT only), stock-based compensation expenses, transaction expenses associated with the acquisition, the impact of purchase accounting adjustments and changes in fair value of the warrants, we believe the result is a useful measure across time in evaluating our fundamental core operating performance. Management also uses Operational EBITDA to manage our business, including in preparing its annual operating budget, financial projections and compensation plans. We believe that Operational EBITDA is also useful to investors because similar measures are frequently used by securities analysts, investors and other interested parties in their evaluation of companies in similar industries. As indicated, Operational EBITDA does not include interest expense on borrowed money or the payment of income taxes or depreciation expense on our capital assets, which are necessary elements of our operations. It also excludes expenses in connection with the development, deployment and financing of Iridium NEXT. Since Operational EBITDA does not account for these and other expenses, its utility as a measure of our operating performance has material limitations. Due to these limitations, our management does not view Operational EBITDA in isolation and also uses other measurements, such as net income, revenues and operating profit, to measure operating performance. |