January 15, 2015

U. S. Securities and Exchange Commission

Division of Corporation Finance

100 F Street, N.E.

Washington, D.C. 20549

| Attn: | Mr. Larry Spirgel, Assistant Director | |

| Mr. Robert Littlepage, Accounting Branch Chief | ||

| Mr. Dean Suehiro, Senior Staff Accountant | ||

| Mr. Robert Shapiro, Staff Accountant |

| RE: | Iridium Communications Inc. | |

| Form 10-K for the Year Ended December 31, 2013 | ||

| Filed March 4, 2014 | ||

| Form 10-Q for Fiscal Quarter Ended September 30, 2014 | ||

| Filed October 30, 2014 | ||

| File No. 001-33963 |

Gentlemen:

Iridium Communications Inc. (the “Company”) is responding to comments (the “Comments”) received from the staff of the Division of Corporation Finance (the “Staff”) of the U.S. Securities and Exchange Commission (the “Commission”) by letter dated December 11, 2014 with respect to the above-referenced filings (as applicable, the “Form 10-K” or the “Form 10-Q”). Set forth below are the Company’s responses to the Comments. The numbering of the paragraphs below corresponds to the numbering of the Comments, which for your convenience we have incorporated into this response letter. Page references in the text of this response letter correspond to the page numbers of the referenced filing with the Commission.

Form 10-K for the Fiscal Year Ended December 31, 2013

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Commerical Service Revenue, page 47

|  |

| 1. | Please tell us and disclose the nature of your change in your prepaid airtime policy effective in 2013. In addition, tell us the amount of the impact of this change on your prepaid revenues and total commercial service revenues. |

Response to Comment 1:

Response

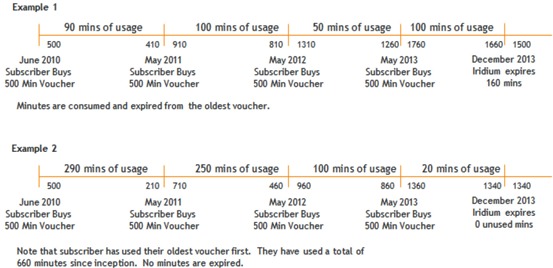

As originally communicated to the Company’s service providers in September 2012, the Company modified its policy regarding the expiration of prepaid airtime effective December 2013. Prior to December 2013, e-vouchers for prepaid airtime could be extended if the customer either purchased additional minutes or purchased a 30-day extension e-voucher. Effective December 2013, the Company amended the policy to create a maximum period through which prepaid e-vouchers can be extended. Extendable prepaid e-vouchers carrying a 12-month expiry period became subject to a 3-year maximum period of extension. Extendable prepaid e-vouchers carrying a 24-month expiry period became subject to a 4-year maximum period of extension. The terms of the 30-day extension e-vouchers remained unchanged under the amended policy but cannot extend the life of a e-voucher beyond the 3- or 4-year extension period as described above. Any e-vouchers held by customers with outstanding prepaid balances that were less than three or four years old, as the case may be, was not affected by this amended policy for 2013. Please see two examples below with timelines that demonstrate the purchase of a 500 minute 12 month e-voucher for 1) a customer with minutes that expired on December 17, 2013 and 2) a customer with minutes that did not expire on December 17, 2013; both examples are based on the amended policy:

| |

As a result of the change in the policy, the Company recognized non-recurring revenue of $3.6 million in December 2013 related to the expiration of prepaid minutes which were older than the established maximums detailed in the amended policy.

In future filings, when comparing the results of operations, the Company will continue to assess the impact of ongoing expirations under the new prepaid expiration policy occurring in the regular course of business. If the change, period over period, is considered to be significant, the Company will quantify and disclose the nature of the drivers of the increase (decrease) in commercial service revenue.

In addition, in response to the Staff’s comment and specifically related to the December 2013 policy change, the Company will provide additional disclosure, in future filings, to read substantially similar to the following Critical Accounting Policies included in Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations and Significant Accounting Policies included in the footnotes to its financial statements:

| |

Revenue Recognition

We sell prepaid services in the form of e-vouchers and prepaid cards. A liability is established equal to the cash paid upon purchase for the e-voucher or prepaid card. We recognize revenue from the prepaid services (i) upon the use of the e-voucher or prepaid card by the customer; (ii) upon the expiration of the right to access the prepaid service; or (iii) when it is determined that the likelihood of the prepaid card being redeemed by the customer is remote. The likelihood of redemption is based on historical redemption patterns. If future results are not consistent with these historical patterns, and therefore actual usage results are not consistent with our estimates or assumptions, we may be exposed to changes to earned and unearned revenue that could be material. In September 2012, we communicated a new expiration policy with respect to prepaid e-vouchers, effective December 2013. While the terms of prepaid e-vouchers can be extended by the purchase of additional e-vouchers, prepaid e-vouchers may not be extended beyond the new limits of three or four years, dependent on the initial expiry period when purchased. We do not offer refunds for unused prepaid services.

Notes to Consolidated Financial Statements

Note 2. Significant Accounting Policies and Basis of Presentation, pages 65 - 71

| 2. | Please disclose your accounting policy for your investment in Aireon accounted for under the equity method including the $10 million airtime credits and additional investment of up to $15 million as disclosed on page 75. We note your disclosures on pages 18, 20 and 42. Refer to ASC 323-10-50. |

Response to Comment 2:

The Company advises the staff the Company’s disclosure of its investment in Aireon LLC (“Aireon”) has been evaluated in accordance with ASC 323-10-50. The Company considered but elected not to disclose its equity method investment accounting policy with respect to Aireon due to the immaterial impact of the investment in Aireon on the consolidated financial statements and disclosures as of December 31, 2013. The investment balance in Aireon as of December 31, 2013 was $4.1 million. Additionally, as of June 30, 2014, the Company has suspended the recognition of losses from Aireon’s operations as

| |

the related investment balance had been reduced to zero. The Company will continue to evaluate the impact of its investment in Aireon on the consolidated financial statements and consider related disclosures.

Aireon was initially formed on December 16, 2011. The Company holds common ownership interests in Aireon and, beginning in 2012, Aireon has issued preferred ownership interests to parties unrelated to the Company. The Company initially evaluated, and continues to evaluate at each reporting period, the investment in Aireon in accordance with the consolidation guidance of ASC 810,Consolidation. In its evaluation of Aireon, the Company concluded that Aireon is a variable interest entity for which the Company is not the primary beneficiary and that Iridium does not have a controlling financial interest in Aireon.

The Company further assessed whether or not it has the ability to exercise significant influence, in accordance with ASC 323-10, over Aireon. Given the Company’s ownership interest, its representation on Aireon’s Board of Directors and various other rights, the Company concluded it was appropriate to account for the investment in Aireon under the equity method in accordance with ASC 323-10. Accordingly, the Company recorded its proportionate share of Aireon’s losses until the investment balance was reduced to zero.

With respect to the reference to $10.0 million of airtime credits, in October 2012, Aireon entered into an agreement with the Company pursuant to which the Company would sell to Aireon, under certain circumstances, various Iridium services and Aireon could, in turn, transfer the right to those services to a third party. In addition, Aireon had previously entered into an agreement with a third party for the development of Aireon’s hosted payload and related infrastructure. Under the terms of the related agreements, should Aireon fail to make payment of its related obligation to the third party in a timely manner, Aireon may satisfy up to $10.0 million of that obligation with the prepaid services purchased from the Company. To date, Aireon has successfully met its obligations to the third party. Therefore, Aireon has not purchased any prepaid services. Accordingly, there has been no accounting or other impact for this arrangement.

With respect to the reference to an additional investment of up to $15.0 million, the Company requested that its lenders provide permission to the Company to invest up to an additional $15.0 million into Aireon. However, the Company is

| |

not obligated to make any additional investment in Aireon and the Company has not made any such additional investment in Aireon. Thus, the Company has not recorded any investment other than its initial $12.5 million investment.

Property and Equipment, page 68

| 3. | As previously requested, please disclose the estimated useful lives for satellites and building improvements. |

Response to Comment 3:

In a previous response to comments from the Staff on May 31, 2013, the Company addressed the estimated useful life of the satellites with the following response:

“As discussed above and disclosed with the ‘depreciation expense’ discussion within the Significant Accounting Policies and Basis of Presentation note to our financial statements, the estimated useful lives of our Block 1 satellites are consistent with the expected deployment of Iridium NEXT. We will further clarify this information for the readers of our financial statements by providing the following updated Property and Equipment disclosures in the notes to our financial statements beginning with our Form 10-Q for the quarter ending June 30, 2013: |

Property and Equipment Property and equipment is carried at cost less accumulated depreciation. |

Depreciation is calculated using the straight-line method over the following estimated useful lives: |

Satellites | estimated useful life | |

Ground system | 5-7 years | |

Equipment | 3-5 years | |

Internally developed software and purchased software | 3-7 years | |

Building | 39 years | |

Building Improvements | estimated useful life | |

Leasehold improvements or remaining lease term | shorter of useful life | |

| |

The estimated useful lives of the Company’s satellites are the remaining period of expected use for each satellite. Satellites are depreciated on a straight-line basis through the date they will be replaced by Iridium NEXT satellites. Based on the current launch schedule, the Company expects Iridium NEXT satellites to begin deployment in early 2015, with the final launch expected to occur by mid-2017.

Repairs and maintenance costs are expensed as incurred.”

As contemplated in that response, the Company has been including this disclosure in its financial statements since the second quarter of 2013.

The estimated useful lives of the Company’s satellites reflect the remaining period of expected use for each satellite. The satellites within the current constellation are depreciated on a straight-line basis through the date they will be replaced by Iridium NEXT satellites. Based on the current launch schedule, the Company expects Iridium NEXT satellites to begin deployment in mid-2015, with the final launch expected to occur by mid-2017. Based upon the current Iridium NEXT launch schedule, the individual satellites in the current constellation will have a total estimated useful life of 15 to 18 years from their respective launch dates.

With respect to building improvements, the building improvements have estimated useful lives of 5 to 39 years.

In future filings, the Company will include the following disclosure.

Satellites | 15-18 years | |

Ground system | 5-7 years | |

Equipment | 3-5 years | |

Internally developed software and purchased software | 3-7 years | |

Building | 39 years | |

Building Improvements | 5-39 years | |

Leasehold improvements | shorter of useful life | |

or remaining lease term |

| |

The estimated useful lives of the Company’s current constellation of satellites reflect the remaining period of expected use for each satellite. Satellites are depreciated on a straight-line basis through the date they will be replaced by Iridium NEXT satellites. Based on the current launch schedule, the Company expects Iridium NEXT satellites to begin deployment in mid-2015, with the final launch expected to occur by mid-2017.

Form 10-Q for Fiscal Quarter Ended September 30, 2014

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Revenues, Subscriber Equipment Revenues, pages 20 and 24

| 4. | We note your net increase in net subscriber equipment sales was due to the introduction of the Iridum Go!® product line for the three and nine month periods ended September 30, 2014. However, we also note a trend in declining satellite handset sales in 2013 that has continued in 2014. Please disclose in future filings, in greater detail, the impact of the trends in terms of equipment sales volume and product mix of your different product lines on your business and results of operations. We note your disclosure on page 20 that you “anticipate subscriber equipment revenue for the full year 2014 to exceed full year 2013.” |

Response to Comment 4:

In response to the Staff’s comment, the Company will revise the disclosure, in future filings, to read similar to the following for the applicable periods:

Subscriber equipment revenue increased $3.6 million, or 6%, for the nine months ended September 30, 2014 compared to the prior year period. This increase was primarily due to the launch of Iridium GO!, which contributed $3.2 million in revenue for the third quarter of 2014. Also, to a lesser extent, contributing to this increase were higher unit sales of L-Band transceivers and M2M devices, somewhat offset by targeted lower pricing on these products designed to promote the higher volumes we ultimately achieved. These increases in revenue were partially offset by a $0.9 million decrease in handset equipment revenue.

| |

Subscriber equipment revenue has decreased from 26% of total revenue in 2010 to 20% in 2013 and the Company expects this trend will continue as the rate of growth in service revenue is expected to exceed the rate of growth in equipment revenue. Consistent with this trend, the Company’s 2014 subscriber equipment revenue (based on preliminary unaudited results) reflects a further slight decrease as a percentage of total revenue. The Company plans to disclose the $3.2 million increase in subscriber equipment revenue related to Iridium GO! due to the qualitative nature of a new product launch; however, the Company does not deem the dollar amount of the increase significant. The Company believes that service revenue growth is a more important financial metric, and the Company provides more detailed information regarding its service revenue including forward looking guidance on expected service revenue growth. Accordingly, the Company believes that detailing insignificant changes in pricing or volume mix by product type would not be meaningful to users of the financial statements in understanding the Company’s business and financial results. However, in future filings, the Company will disclose changes in sales volume and product mix if those changes are deemed significant.

Other Income (expense), pages 22 and 24

| 5. | Please tell us and disclose the impact of the issuance of the contingent shares to Baron on August 6, 2014 had on your other income (expense). We note the increase in additional paid-in capital of approximately $3 million for the three months ended September 30, 2014. |

Response to Comment 5:

On May 2, 2014, the Company issued 7,692,308 shares of its common stock in a registered direct offering to certain investment funds affiliated with Baron Capital Group Inc. (“Baron”) at a price of $6.50 per share for aggregate gross proceeds of $50.0 million. Under the stock purchase agreement entered into with Baron, Baron was entitled to receive additional shares if, during the 90-day period following the date of the stock purchase agreement, the Company issued or sold securities below the price paid by Baron (the “price protection right”).

On May 14, 2014, in an unrelated transaction, the Company issued 8,483,608 shares of its common stock at $6.10 per share in an underwritten offering. As a

| |

result of this issuance at a price below Baron’s purchase price of $6.50 per share, the Company became obligated to deliver 504,413 additional shares of common stock to Baron. The additional shares were issued to Baron on August 6, 2014.

Given the proximity of the transactions (within 12 days), the Company estimated the initial value of the price protection right based upon the fair value of the additional shares at $3,076,919, (504,413 shares x $6.10). The Company also made the determination that the fair value of the price protection right for the remaining term of the 90-day period was zero, as the Company was not anticipating any additional equity financings through the date of expiration of the price protection right that would potentially trigger the obligation to issue additional shares to Baron. As of the filing date of the second quarter Form 10-Q on July 31, 2014, there were no additional equity financings and the right expired on July 31, 2014 with no additional shares issued to Baron beyond those related to the May 14th transaction.

The price protection right was considered to be indexed to the Company’s own stock and was subject to the guidance in ASC 815-40,Contracts in Entity’s Own Equity.As the obligation as of June 30, 2014, was required to be settled in shares, in accordance with ASC 815-40-25-1, the value of the additional 504,413 issuable shares were classified as additional paid-in capital in stockholders’ equity. As a result, there were no mark-to-market adjustments to be recorded to other income (expense) for the three-months ended June 30, 2014 or the three months ended September 30, 2014. Thus, the transaction had no impact to other income (expense).

The $3.0 million increase to additional paid-in capital as of September 30, 2014 was primarily due to stock-based compensation during the three months then ended and was unrelated to the Baron transaction.

In addition, upon the issuance of the additional shares in the three months ended September 30, 2014, the par value for the additional 504,413 shares issued to Baron was reclassified from additional paid-in-capital to common stock in the Company’s balance sheet as of September 30, 2014.

* * * * *

| |

Pursuant to the Staff’s letter, the Company further acknowledges that:

| • | the Company is responsible for the adequacy and accuracy of the disclosure in the filing; |

| • | Staff comments or changes to disclosure in response to Staff comments do not foreclose the Commission from taking any action with respect to the filing; and |

| • | the Company may not assert Staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States. |

Please fax any additional comment letters concerning the above-referenced filing to (703) 287-7425 and direct any questions or comments concerning the above-referenced filings or this response letter to Thomas Hickey at (703) 287-7411 or Kathy Morgan at (703) 287-7408.

| Very truly yours, |

| /s/ Thomas J. Fitzpatrick |

| Thomas J. Fitzpatrick |

| Chief Financial Officer |

| cc: | Thomas Hickey, Iridium Communications Inc. | |

| Kathy Morgan, Iridium Communications Inc. | ||

| Brent B. Siler, Cooley LLP | ||

| Brian F. Leaf, Cooley LLP |

| |