Exhibit 99.1

FOR IMMEDIATE RELEASE

MATTRESS FIRM ANNOUNCES THIRD FISCAL QUARTER FINANCIAL RESULTS

— Net Sales Increased 50.7% Over Prior Year with 3.8% Comparable-store Sales Growth —

— Ninth Consecutive Quarter of Positive Comparable-Store Sales Growth —

— Adjusted EBITDA Increased Approximately 41% Over Prior Year —

— GAAP EPS Increased Approximately 49% to $0.67 and Adjusted EPS Increased 17% to $0.82 —

HOUSTON, December 7, 2015 /BUSINESSWIRE/ — Mattress Firm Holding Corp. (the “Company”) (NASDAQ: MFRM), the nation’s largest specialty mattress retailer, today announced its financial results for the third fiscal quarter (13 weeks) ended November 3, 2015. Net sales for the third fiscal quarter increased 50.7% over the prior year to $699.5 million, reflecting incremental sales from acquired and new stores, and comparable-store sales growth of 3.8%. The Company reported third fiscal quarter earnings per diluted share (“EPS”) on a generally accepted accounting principles (“GAAP”) basis of $0.67, and EPS on a non-GAAP adjusted basis, excluding acquisition-related costs, secondary offering costs and severance charges (“Adjusted”), of $0.82.

Expected diluted EPS on a GAAP basis and Adjusted basis are reconciled in the table below:

Third Fiscal Quarter Reconciliation of GAAP to Adjusted EPS and Adjusted Cash EPS**

See “Reconciliation of Reported (GAAP) to Adjusted Statements of Operations Data” for Notes

| | Thirteen Weeks Ended | | Thirty-Nine Weeks Ended | |

| | October 28, 2014 | | November 3, 2015 | | October 28, 2014 | | November 3, 2015 | |

GAAP EPS | | $ | 0.45 | | $ | 0.67 | | $ | 1.10 | | $ | 1.44 | |

Adjustments | | | | | | | | | |

Acquisition-related costs (1) | | 0.18 | | 0.14 | | 0.37 | | 0.34 | |

Secondary offering costs (2) | | — | | — | | — | | 0.01 | |

ERP system implementation costs (3) | | 0.03 | | — | | 0.09 | | 0.01 | |

Impairment charges and other expenses (4)(5) | | 0.04 | | 0.01 | | 0.08 | | 0.02 | |

Adjusted EPS* | | $ | 0.70 | | $ | 0.82 | | $ | 1.62 | | $ | 1.82 | |

Non-Cash Adjustments | | | | | | | | | |

Depreciation and amortization expense | | 0.20 | | 0.32 | | 0.56 | | 0.88 | |

Stock-based compensation expense | | 0.04 | | 0.05 | | 0.09 | | 0.11 | |

Adjusted Cash EPS* | | $ | 0.94 | | $ | 1.18 | | $ | 2.27 | | $ | 2.82 | |

* Due to rounding to the nearest cent, totals may not equal the sum of the lines in the table above.

** Reported sales results and expected GAAP and Adjusted EPS are preliminary and remain subject to adjustment until the filing of the Company’s Quarterly Report on Form 10-Q with the U.S. Securities and Exchange Commission.

“We are pleased with our third quarter results, with over 50% net sales growth and a 3.8% comparable-store sales increase, representing our ninth consecutive quarter of positive same store sales,” stated Steve Stagner, chief executive officer. “Our third quarter Adjusted EPS grew 17% from the prior year, as we continue to execute on our plan and integrate the nine acquisitions, totaling over 600 stores, that we completed in fiscal 2014. Our Sleep Train business continues to perform extremely well with strong sales growth as we convert the Mattress Discounters stores to the Sleep Train banner. With our recently streamlined organizational structure and initiatives in place, we believe we are well-positioned to execute on our growth strategies and capitalize on our relative market share strategy.”

5815 Gulf Freeway · Houston, TX · 77023 · Phone: 713-923-1090 · Fax: 713-923-1096

Preliminary Third Quarter Financial Summary

· Net sales for the third fiscal quarter increased 50.7% to $699.5 million, from $464.3 million in the comparable year period, reflecting incremental sales from acquired and new stores, and comparable-store sales growth of 3.8%. Comparable-store sales growth in the prior year period was 8.5%.

· Opened 87 new stores and closed 15 stores, bringing the total number of Company-operated stores to 2,295 as of the end of the third fiscal quarter.

· Income from operations was $47.8 million. Excluding $8.4 million of acquisition-related costs, secondary offering costs and severance charges, Adjusted income from operations was $56.2 million, as compared with $43.7 million for the comparable prior year period. Adjusted operating income margin was 8.0% of net sales as compared with 9.4% in fiscal 2014, and included a 70 basis-point increase from general and administrative expense leverage, offset by a 160 basis-point decline in gross margin, 40 basis-points of expense deleverage from sales and marketing expense, and 10 basis-points of combined operating margin declines in franchise fees and from losses on store closings. Please refer to “Reconciliation of Reported (GAAP) to Adjusted Statements of Operations Data” for a reconciliation of income from operations to Adjusted income from operations and other information.

· Net income was $23.9 million and GAAP EPS was $0.67. Excluding $5.2 million, net of income taxes, of acquisition-related costs, secondary offering costs and severance charges, Adjusted net income was $29.1 million and Adjusted EPS was $0.82. Please refer to “Reconciliation of Reported (GAAP) to Adjusted Statements of Operations Data” for a reconciliation of net income and GAAP EPS to Adjusted net income and Adjusted EPS, respectively, and other information.

For the full fiscal year-to-date:

· Net sales increased $715.4 million, or 59.2%, to $1,923.1 million, for the three fiscal quarters (thirty-nine weeks) ended November 3, 2015, from $1,207.7 million in the comparable year period, reflecting comparable store sales growth of 2.8% and incremental sales from new and acquired stores. Comparable-store sales growth in the prior year comparable period was 7.6%.

· The Company opened 236 new stores and closed 35 stores during the first three fiscal quarters of fiscal 2015, adding 201 net store units.

· Income from operations was $112.2 million, for the three fiscal quarters ended November 3, 2015. Excluding $21.6 million of acquisition-related costs, ERP system implementation costs, secondary offering costs, and impairment and severance charges, Adjusted income from operations was $133.8 million for the three fiscal quarters ended November 3, 2015, as compared with $101.7 million for the comparable prior year period. Adjusted operating income margin was 7.0% of net sales as compared with 8.4% in fiscal 2014, and included a 50 basis-point increase from general and administrative expense leverage, offset by a 110 basis-point decline in gross margin, 70 basis-points of expense deleverage from sales and marketing expense, and 10 basis-points of combined operating margin declines in franchise fees and from losses on store closings. Please refer to “Reconciliation of Reported (GAAP) to Adjusted Statements of Operations Data” for a reconciliation of income from operations to Adjusted income from operations and other information.

· Net income was $51.2 million for the three fiscal quarters ended November 3, 2015 and GAAP EPS was $1.44. Excluding $13.5 million, net of income taxes, of acquisition-related costs, ERP system implementation costs, secondary offering costs, and impairment and severance charges, Adjusted net income was $64.7 million for the three fiscal quarters and Adjusted EPS was $1.82. Please refer to “Reconciliation of Reported (GAAP) to

2

Adjusted Statements of Operations Data” for a reconciliation of net income and GAAP EPS to Adjusted net income and Adjusted EPS, respectively, and other information.

Acquisitions

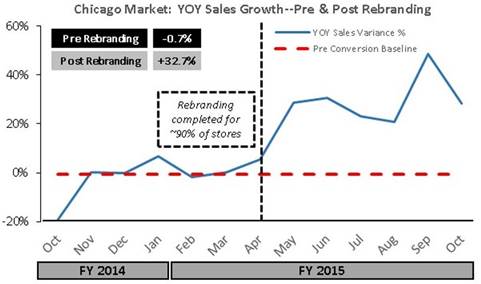

In September 2014, the Company completed the acquisition of the mattress specialty retail assets and operations of Back to Bed Inc., M World Mattress LLC, MCStores LLC and TBE Orlando LLC, which collectively operate Back to Bed and Bedding Experts retail stores in Illinois, Indiana and Wisconsin and Bedding Experts and Mattress Barn retail stores in Florida. The acquisition included approximately 131 mattress specialty retail stores primarily in the Chicago and Orlando metropolitan areas, for an aggregate purchase price of approximately $64.5 million. The rebranding of the acquired retail stores in the Chicago market was substantially complete by the end of May 2015. The Chicago market sales growth year-over-year (“YOY”) from those stores both prior to and subsequent to their rebranding is demonstrated by the chart below:

Balance Sheet

The Company had cash and cash equivalents of approximately $10.3 million at the end of the third fiscal quarter. Net cash provided by operating activities was $45.5 million for the third fiscal quarter. During the third quarter, the Company repaid approximately $17.5 million of debt, and as of November 3, 2015, there was $5 million outstanding under the revolving portion of the 2014 Senior Credit Facility (as defined in the Company’s filings with the Securities and Exchange Commission) and approximately $4.8 million in outstanding letters of credit, with additional borrowing capacity of $92.3 million.

3

Financial Guidance

The Company also reaffirmed the midpoint of its financial outlook for sales, Adjusted EBITDA and Adjusted EPS for the full fiscal year (52 weeks) ending February 2, 2016 (“fiscal year 2015”). This outlook is based on year-to-date results and efficiency initiatives that have been recently implemented by Management. These projections are forecasts and are intended solely to give investors an understanding of management’s expectations for the full fiscal year based on recent business trends. The projections do not take into account, or give effect for, acquisitions that may be completed by the Company during the fiscal year or any other events that are beyond the Company’s reasonable control. As used in the guidance table below, “Adjusted Cash EPS” is defined as adjusted net income as presented in the “Reconciliation of Reported (GAAP) to Adjusted Statements of Operations Data”, plus tax effected stock compensation expense and depreciation and amortization, divided by the number of diluted shares. Please refer to “Reconciliation of Reported (GAAP) to Adjusted Statements of Operations Data” for a reconciliation of GAAP EPS to Adjusted Cash EPS and other information which is not calculated on a GAAP basis. Comparable-store sales growth for fiscal year 2014 excludes incremental sales related to the 53rd week of operations. Adjusted data for future periods reflects management’s reasonable estimates of appropriate adjustments based on historical experience. Percentage growth calculations in the table below represent the midpoints of the guidance range provided.

| | Fifty-Three | | Fifty-Two | | | |

| | Weeks Ended | | Weeks Ended | | | |

| | February 3, 2015 | | February 2, 2016 | | % Growth | |

New Store Growth (net of closures) | | 201 | | 250 - 270 | | — | |

Acquired Store Growth | | 668 | | 9 | | — | |

Net Sales (in millions) | | $ | 1,806 | | $2,530 - $2,550 | | 41 | % |

Comparable-Store Sales Growth | | 6.1 | % | Low Single Digit | | — | |

Adjusted EBITDA (in millions) | | $ | 190 | | $255 - $260 | | 35 | % |

GAAP EPS | | $ | 1.27 | | $1.88 - $1.94 | | 50 | % |

Adjustments (per share) | | $ | 0.76 | | $0.45 - $0.48 | | — | |

Adjusted EPS | | $ | 2.03 | | $2.33 - $2.42 | | 17 | % |

Adjusted Cash EPS | | $ | 2.99 | | $3.71 - $3.80 | | 26 | % |

| | | | | | | |

Diluted Share Count (in millions) | | 34.8 | | 35.6 | | — | |

Adjusted Tax Rate | | 39.5 | % | 37.7% | | — | |

Depreciation and Amortization (in millions) | | $ | 47 | | $68 | | 45 | % |

Interest Expense (in millions) | | $ | 22 | | $40 | | 82 | % |

Stock-based Compensation Expense (in millions) | | $ | 8 | | $11 | | 35 | % |

Net Capital Expenditures (in millions) | | $ | 72 | | $110 | | 52 | % |

Ending Net Debt (in millions) | | $ | 757 | | $680 | | -10 | % |

Call Information

A conference call to discuss third fiscal quarter results is scheduled for today, December 7, 2015, at 8:30 a.m. Eastern Time. The call will be hosted by Steve Stagner, chief executive officer, Ken Murphy, president, Alex Weiss, chief financial officer and Scott McKinney, vice president of investor relations.

The conference call will be accessible by telephone and the internet. To access the call, participants from within the U.S. may dial (877) 705-6003, and participants from outside the U.S. may dial (201) 493-6725. Participants may also access the call via live webcast by visiting the Company’s investor relations web site at ir.mattressfirm.com.

The replay of the call will be available from approximately 11:30 a.m. Eastern Time on December 7, 2015 through midnight Eastern Time on December 21, 2015. To access the replay, the domestic dial-in number is (877) 870-5176, the international dial-in number is (858) 384-5517, and the passcode is 13625562. The archive of the webcast will be available on the Company’s web site for a limited time.

4

Net Sales and Store Unit Information

The components of the net sales increase for the thirteen and thirty-nine weeks ended November 3, 2015 as compared to the corresponding prior year period were as follows (in millions):

| | Progression in Net Sales | |

| | Thirteen Weeks | | Thirty-Nine Weeks | |

| | Ended | | Ended | |

| | November 3, 2015 | | November 3, 2015 | |

Net sales for prior year period | | $ | 464.3 | | $ | 1,207.7 | |

Increase (Decrease) in Net Sales | | | | | |

Comparable-store sales | | 17.2 | | 32.4 | |

New stores | | 62.1 | | 165.3 | |

Acquired stores | | 159.5 | | 526.6 | |

Closed stores | | (3.6 | ) | (8.9 | ) |

Increase in net sales, net | | 235.2 | | 715.4 | |

Net sales for current year period | | $ | 699.5 | | $ | 1,923.1 | |

% increase | | 50.7 | % | 59.2 | % |

The composition of net sales by major category of product and services were as follows (in millions):

| | Thirteen Weeks Ended | | Thirty-Nine Weeks Ended | | | |

| | October 28, | | % of | | November 3, | | % of | | October 28, | | % of | | November 3, | | % of | |

| | 2014 | | Total | | 2015 | | Total | | 2014 | | Total | | 2015 | | Total | |

Conventional mattresses | | $ | 208.4 | | 44.9 | % | $ | 350.1 | | 50.2 | % | $ | 567.6 | | 47.0 | % | $ | 973.9 | | 50.6 | % |

Specialty mattresses | | 211.9 | | 45.6 | % | 286.6 | | 41.0 | % | 525.7 | | 43.5 | % | 777.7 | | 40.4 | % |

Furniture and accessories | | 35.7 | | 7.7 | % | 53.8 | | 7.7 | % | 91.4 | | 7.6 | % | 147.3 | | 7.7 | % |

Total product sales | | 456.0 | | 98.2 | % | 690.5 | | 98.7 | % | 1,184.7 | | 98.1 | % | 1,898.9 | | 98.7 | % |

Delivery service revenues | | 8.3 | | 1.8 | % | 9.0 | | 1.3 | % | 23.0 | | 1.9 | % | 24.2 | | 1.3 | % |

Total net sales | | $ | 464.3 | | 100.0 | % | $ | 699.5 | | 100.0 | % | $ | 1,207.7 | | 100.0 | % | $ | 1,923.1 | | 100.0 | % |

The activity with respect to the number of Company-operated store units was as follows:

| | Thirteen Weeks | | Thirty-Nine Weeks | |

| | Ended | | Ended | |

| | November 3, 2015 | | November 3, 2015 | |

Store units, beginning of period | | 2,223 | | 2,094 | |

New stores | | 87 | | 236 | |

Closed stores | | (15 | ) | (35 | ) |

Store units, end of period | | 2,295 | | 2,295 | |

5

Forward-Looking Statements

Certain statements contained in this press release are not based on historical fact and are “forward-looking statements” within the meaning of applicable federal securities laws and regulations. In many cases, you can identify forward-looking statements by terminology such as “may,” “would,” “should,” “could,” “forecast,” “feel,” “project,” “expect,” “plan,” “anticipate,” “believe,” “estimate,” “predict,” “intend,” “potential,” “continue” or the negative of these terms or other comparable terminology; however, not all forward-looking statements contain these identifying words. The forward-looking statements contained in this press release, such as those relating to our net sales, GAAP and Adjusted EPS and net store unit change for fiscal year 2015 and any anticipated effects of any recent acquisitions, are subject to various risks and uncertainties, including but not limited to downturns in the economy; reduction in discretionary spending by consumers; our ability to execute our key business strategies and advance our market-level profitability; our ability to profitably open and operate new stores and capture additional market share; our relationship with our primary mattress suppliers; our dependence on a few key employees; the possible impairment of our goodwill or other acquired intangible assets; the effect of our planned growth and the integration of our acquisitions on our business infrastructure; the impact of seasonality on our financial results and comparable-store sales; our ability to raise adequate capital to support our expansion strategy; our success in pursuing and completing strategic acquisitions; the effectiveness and efficiency of our advertising expenditures; our success in keeping warranty claims and comfort exchange return rates within acceptable levels; our ability to deliver our products in a timely manner; our status as a holding company with no business operations; our ability to anticipate consumer trends; risks related to our primary stockholder, J.W. Childs Associates, L.P.; heightened competition; changes in applicable regulations; risks related to our franchises, including our lack of control over their operation and our liabilities if they default on note or lease obligations; risks related to our stock and other factors set forth under “Risk Factors” in our Annual Report on Form 10-K for the fiscal year ended February 3, 2015 filed with the Securities and Exchange Commission (“SEC”) on April 3, 2015 and our other SEC filings. Forward-looking statements relate to future events or our future financial performance and reflect management’s expectations or beliefs concerning future events as of the date of this press release. Actual results of operations may differ materially from those set forth in any forward-looking statements, and the inclusion of a projection or forward-looking statement in this press release should not be regarded as a representation by us that our plans or objectives will be achieved. We do not undertake to publicly update or revise any of these forward-looking statements, whether as a result of new information, future events or otherwise

Non-GAAP Financial Measures

Adjusted EBITDA is defined as net income before income tax expense, interest income, interest expense, depreciation and amortization (“EBITDA”), without giving effect to non-cash goodwill and intangible asset impairment charges, gains or losses on store closings and impairment of store assets, gains or losses related to the early extinguishment of debt, financial sponsor fees and expenses, non-cash charges related to stock-based awards and other items that are excluded by management in reviewing the results of operations. We have presented Adjusted EBITDA because we believe that the exclusion of these items is appropriate to provide additional information to investors about our ongoing operating performance excluding certain non-cash and other items and to provide additional information with respect to our ability to comply with various covenants in documents governing our indebtedness and as a means to evaluate our period-to-period results. In evaluating Adjusted EBITDA, you should be aware that in the future we may incur expenses that are the same as or similar to some of the adjustments in this presentation. Our presentation of Adjusted EBITDA should not be construed to imply that our future results will be unaffected by any such adjustments. We have provided this information to analysts, investors and other third parties to enable them to perform more meaningful comparisons of past, present and future operating results and as a means to evaluate the results of our ongoing operations. Management also uses Adjusted EBITDA to determine executive incentive compensation payment levels. In addition, our compliance with certain covenants under the 2014 Senior Credit Facility, are calculated based on similar measures and differ from Adjusted EBITDA primarily by the inclusion of pro forma results for acquired businesses and new stores in those similar measures. Other companies in our industry may calculate Adjusted EBITDA differently than we do. Adjusted EBITDA is not a measure of performance under U.S. GAAP and should not be considered as a substitute for net income prepared in accordance with U.S. GAAP. Adjusted EBITDA has significant limitations as an analytical tool, and you should not consider it in isolation or as a substitute for analysis of our results as reported under U.S. GAAP.

6

The following table contains a reconciliation of our net income determined in accordance with U.S. GAAP to EBITDA and Adjusted EBITDA for the periods indicated (in thousands):

| | Thirteen Weeks Ended | | Thirty-Nine Weeks Ended | |

| | October 28, | | November 3, | | October 28, | | November 3, | |

| | 2014 | | 2015 | | 2014 | | 2015 | |

Net income | | $ | 15,613 | | $ | 23,873 | | $ | 37,631 | | $ | 51,232 | |

Income tax expense | | 9,677 | | 13,778 | | 23,762 | | 30,556 | |

Interest expense, net | | 4,067 | | 10,161 | | 10,352 | | 30,460 | |

Depreciation and amortization | | 10,101 | | 16,370 | | 28,302 | | 45,116 | |

Intangible assets and other amortization | | 917 | | 1,387 | | 2,528 | | 4,090 | |

EBITDA | | 40,375 | | 65,569 | | 102,575 | | 161,454 | |

Loss on store closings and impairment of store assets | | 133 | | 586 | | 1,039 | | 2,054 | |

Loss from debt extinguishment | | 2,288 | | — | | 2,288 | | — | |

Stock-based compensation | | 2,416 | | 2,653 | | 4,973 | | 6,533 | |

Secondary offering costs | | — | | 7 | | — | | 487 | |

Vendor new store funds (a) | | (391 | ) | 857 | | (834 | ) | 1,468 | |

Acquisition-related costs (b) | | 10,058 | | 8,156 | | 20,759 | | 19,351 | |

Other (c) | | 856 | | 547 | | 4,882 | | 1,317 | |

Adjusted EBITDA | | $ | 55,735 | | $ | 78,375 | | $ | 135,682 | | $ | 192,664 | |

(a) We receive cash payments from certain vendors for each new incremental store that we open (“new store funds”). New store funds are initially recorded in other noncurrent liabilities when received and are then amortized as a reduction of cost of sales over 36 months in our financial statements. Historically, we have considered new store funds as a component of Adjusted EBITDA when received since new store funds are included in cash provided from operations. The adjustment includes the amount of new store funds received during the period presented and eliminates the non-cash reduction in cost of sales included in our results of operations.

(b) Reflects both non-cash effects included in net income related to acquisition accounting adjustments made to inventories and other acquisition-related cash costs included in net income, such as direct acquisition costs and costs related to integration of acquired businesses.

(c) Consists of various items that management excludes in reviewing the results of operations, including $1.9 million of ERP system implementation costs incurred during the thirteen weeks ended October 28, 2014, and $0.7 million and $4.8 million of ERP system implementation costs incurred during the thirty-nine weeks ended November 3, 2015 and October 28, 2014, respectively.

Adjusted EPS and the other “Adjusted” data provided in this press release, including Adjusted Cash EPS, are also considered non-GAAP financial measures. We report our financial results in accordance with GAAP; however, management believes evaluating our ongoing operating results may be enhanced if investors have additional non-GAAP basis financial measures to facilitate year-over-year comparisons. Management reviews non-GAAP financial measures to assess ongoing operations and considers them to be effective indicators, for both management and investors, of our financial performance over time. Our management does not advocate that investors consider such non-GAAP financial measures in isolation from, or as a substitute for, financial information prepared in accordance with GAAP. For more information, please refer to “Reconciliation of Reported (GAAP) to Adjusted Statements of Operations Data” below.

7

MATTRESS FIRM HOLDING CORP.

Consolidated Balance Sheets

(In thousands, except share amounts)

(unaudited)

| | February 3, | | November 3, | |

| | 2015 | | 2015 | |

Assets | | | | | |

Current assets: | | | | | |

Cash and cash equivalents | | $ | 13,475 | | $ | 10,282 | |

Accounts receivable, net | | 51,193 | | 51,346 | |

Inventories | | 163,518 | | 163,688 | |

Deferred income tax asset | | 8,882 | | 10,273 | |

Prepaid expenses and other current assets | | 43,019 | | 51,345 | |

Total current assets | | 280,087 | | 286,934 | |

Property and equipment, net | | 267,602 | | 310,079 | |

Intangible assets, net | | 215,953 | | 214,114 | |

Goodwill | | 821,349 | | 824,192 | |

Debt issue costs and other, net | | 24,033 | | 23,400 | |

Total assets | | $ | 1,609,024 | | $ | 1,658,719 | |

| | | | | |

Liabilities and Stockholders’ Equity | | | | | |

Current liabilities: | | | | | |

Notes payable and current maturities of long-term debt | | $ | 9,947 | | $ | 9,358 | |

Accounts payable | | 149,612 | | 171,695 | |

Accrued liabilities | | 98,250 | | 99,239 | |

Customer deposits | | 19,398 | | 18,083 | |

Total current liabilities | | 277,207 | | 298,375 | |

Long-term debt, net of current maturities | | 760,091 | | 688,145 | |

Deferred income tax liability | | 41,455 | | 45,441 | |

Other noncurrent liabilities | | 94,788 | | 130,617 | |

Total liabilities | | 1,173,541 | | 1,162,578 | |

| | | | | |

Commitments and contingencies | | | | | |

| | | | | |

Stockholders’ equity: | | | | | |

Common stock, $0.01 par value; 120,000,000 shares authorized; 35,134,187 and 35,101,632 shares issued and outstanding at February 3, 2015; and 35,323,271 and 35,267,237 shares issued and outstanding at November 3, 2015, respectively | | 351 | | 353 | |

Additional paid-in capital | | 435,882 | | 445,306 | |

Accumulated (deficit) retained earnings | | (750 | ) | 50,482 | |

Total stockholders’ equity | | 435,483 | | 496,141 | |

Total liabilities and stockholders’ equity | | $ | 1,609,024 | | $ | 1,658,719 | |

8

MATTRESS FIRM HOLDING CORP.

Consolidated Statements of Operations

(In thousands, except share and per share amounts)

(unaudited)

| | Thirteen Weeks Ended | | Thirty-Nine Weeks Ended | |

| | October 28, | | % of | | November 3, | | % of | | October 28, | | % of | | November 3, | | % of | |

| | 2014 | | Sales | | 2015 | | Sales | | 2014 | | Sales | | 2015 | | Sales | |

Net sales | | $ | 464,278 | | 100.0 | % | $ | 699,507 | | 100.0 | % | $ | 1,207,731 | | 100.0 | % | $ | 1,923,125 | | 100.0 | % |

Cost of sales | | 281,323 | | 60.6 | % | 434,767 | | 62.2 | % | 740,522 | | 61.3 | % | 1,199,607 | | 62.4 | % |

Gross profit from retail operations | | 182,955 | | 39.4 | % | 264,740 | | 37.8 | % | 467,209 | | 38.7 | % | 723,518 | | 37.6 | % |

Franchise fees and royalty income | | 1,238 | | 0.3 | % | 1,578 | | 0.3 | % | 3,516 | | 0.3 | % | 3,978 | | 0.2 | % |

Total gross profit | | 184,193 | | 39.7 | % | 266,318 | | 38.1 | % | 470,725 | | 39.0 | % | 727,496 | | 37.8 | % |

Operating expenses: | | | | | | | | | | | | | | | | | |

Sales and marketing expenses | | 109,632 | | 23.7 | % | 168,312 | | 24.1 | % | 285,295 | | 23.7 | % | 469,329 | | 24.4 | % |

General and administrative expenses | | 42,783 | | 9.2 | % | 49,608 | | 7.1 | % | 110,358 | | 9.1 | % | 143,865 | | 7.5 | % |

Loss on store closings and impairment of store assets | | 133 | | 0.0 | % | 586 | | 0.1 | % | 1,039 | | 0.1 | % | 2,054 | | 0.1 | % |

Total operating expenses | | 152,548 | | 32.9 | % | 218,506 | | 31.3 | % | 396,692 | | 32.9 | % | 615,248 | | 32.0 | % |

Income from operations | | 31,645 | | 6.8 | % | 47,812 | | 6.8 | % | 74,033 | | 6.1 | % | 112,248 | | 5.8 | % |

Other expense: | | | | | | | | | | | | | | | | | |

Interest expense, net | | 4,067 | | 0.9 | % | 10,161 | | 1.4 | % | 10,352 | | 0.8 | % | 30,460 | | 1.5 | % |

Loss from debt extinguishment | | 2,288 | | 0.5 | % | — | | 0.0 | % | 2,288 | | 0.2 | % | — | | 0.0 | % |

Total other expenses | | 6,355 | | 1.4 | % | 10,161 | | 1.4 | % | 12,640 | | 1.0 | % | 30,460 | | 1.5 | % |

Income before income taxes | | 25,290 | | 5.4 | % | 37,651 | | 5.4 | % | 61,393 | | 5.1 | % | 81,788 | | 4.3 | % |

Income tax expense | | 9,677 | | 2.0 | % | 13,778 | | 2.0 | % | 23,762 | | 2.0 | % | 30,556 | | 1.6 | % |

Net income | | $ | 15,613 | | 3.4 | % | $ | 23,873 | | 3.4 | % | $ | 37,631 | | 3.1 | % | $ | 51,232 | | 2.7 | % |

| | | | | | | | | | | | | | | | | |

Basic net income per common share | | $ | 0.46 | | | | $ | 0.68 | | | | $ | 1.10 | | | | $ | 1.46 | | | |

Diluted net income per common share | | $ | 0.45 | | | | $ | 0.67 | | | | $ | 1.09 | | | | $ | 1.44 | | | |

| | | | | | | | | | | | | | | | | |

Reconciliation of weighted-average shares outstanding: | | | | | | | | | | | | | | | | | |

Basic weighted average shares outstanding | | 34,285,572 | | | | 35,228,906 | | | | 34,149,531 | | | | 35,188,012 | | | |

Effect of dilutive securities: | | | | | | | | | | | | | | | | | |

Stock options | | 374,518 | | | | 240,183 | | | | 344,025 | | | | 268,472 | | | |

Restricted shares | | 64,109 | | | | 70,750 | | | | 68,818 | | | | 79,934 | | | |

Diluted weighted average shares outstanding | | 34,724,199 | | | | 35,539,839 | | | | 34,562,374 | | | | 35,536,418 | | | |

9

MATTRESS FIRM HOLDING CORP.

Consolidated Statements of Cash Flows

(In thousands)

(unaudited)

| | Thirty-Nine Weeks Ended | |

| | October 28, 2014 | | November 3, 2015 | |

Cash flows from operating activities: | | 2014 | | 2015 | |

Net income | | $ | 37,631 | | $ | 51,232 | |

Adjustments to reconcile net income to cash flows provided by operating activities: | | | | | |

Depreciation and amortization | | 28,302 | | 45,116 | |

Loan fee and other amortization | | 3,507 | | 5,827 | |

Loss from debt extinguishment | | 2,288 | | — | |

Deferred income tax expense | | 2,325 | | 6,709 | |

Stock-based compensation | | 4,973 | | 7,256 | |

Loss on store closings and impairment of store assets | | 1,039 | | 2,054 | |

Construction allowances from landlords | | 4,813 | | 8,486 | |

Excess tax benefits associated with stock-based awards | | (1,585 | ) | (1,236 | ) |

Effects of changes in operating assets and liabilities, excluding business acquisitions: | | | | | |

Accounts receivable | | (22,124 | ) | 352 | |

Inventories | | (22,029 | ) | (214 | ) |

Prepaid expenses and other current assets | | (5,426 | ) | (8,325 | ) |

Other assets | | (8,501 | ) | (2,683 | ) |

Accounts payable | | 27,432 | | 21,252 | |

Accrued liabilities | | 26,822 | | 2,177 | |

Customer deposits | | 905 | | (1,315 | ) |

Other noncurrent liabilities | | (816 | ) | 27,923 | |

Net cash provided by operating activities | | 79,556 | | 164,611 | |

Cash flows from investing activities: | | | | | |

Purchases of property and equipment | | (54,998 | ) | (96,038 | ) |

Business acquisitions, net of cash acquired | | (561,013 | ) | 119 | |

Net cash used in investing activities | | (616,011 | ) | (95,919 | ) |

Cash flows from financing activities: | | | | | |

Proceeds from issuance of debt | | 990,800 | | 63,000 | |

Principal payments of debt | | (465,551 | ) | (137,056 | ) |

Debt issuance costs | | (10,188 | ) | — | |

Proceeds from exercise of common stock options | | 2,988 | | 1,877 | |

Excess tax benefits associated with stock-based awards | | 1,585 | | 1,236 | |

Purchase of vested stock-based awards | | (1,131 | ) | (942 | ) |

Net cash provided by (used in) financing activities | | 518,503 | | (71,885 | ) |

Net decrease in cash and cash equivalents | | (17,952 | ) | (3,193 | ) |

Cash and cash equivalents, beginning of period | | 22,878 | | 13,475 | |

Cash and cash equivalents, end of period | | $ | 4,926 | | $ | 10,282 | |

Cash paid for: | | | | | |

Interest | | $ | 10,869 | | $ | 29,209 | |

Income taxes | | $ | 11,505 | | $ | 18,515 | |

Supplemental disclosure of noncash investing activity: | | | | | |

Capital expenditures included in accounts payable and accruals at end of period | | $ | 4,098 | | $ | 11,493 | |

10

MATTRESS FIRM HOLDING CORP.

Reconciliation of Reported (GAAP) to Adjusted Statements of Operations Data

(In thousands, except share and per share amounts)

| | Thirteen Weeks Ended | |

| | October 28, 2014 | | November 3, 2015 | |

| | Income | | Income | | | | Diluted | | | | Income | | Income | | | | Diluted | | | |

| | From | | Before In- | | Net | | Weighted | | Diluted | | From | | Before In- | | Net | | Weighted | | Diluted | |

| | Operations | | come Taxes | | Income | | Shares | | EPS* | | Operations | | come Taxes | | Income | | Shares | | EPS* | |

As Reported | | $ | 31,645 | | $ | 25,290 | | $ | 15,613 | | 34,724,199 | | $ | 0.45 | | $ | 47,812 | | $ | 37,651 | | $ | 23,873 | | 35,539,839 | | $ | 0.67 | |

% of sales | | 6.8 | % | 5.4 | % | 3.4 | % | | | | | 6.8 | % | 5.4 | % | 3.4 | % | | | | |

Adjustments | | | | | | | | | | | | | | | | | | | | | |

Acquisition-related costs (1) | | 10,058 | | 10,058 | | 6,140 | | — | | 0.18 | | 8,156 | | 8,156 | | 5,028 | | — | | 0.14 | |

Secondary offering costs (2) | | — | | — | | — | | — | | — | | 7 | | 7 | | 7 | | — | | 0.00 | |

ERP system implementation costs (3) | | 1,982 | | 1,982 | | 1,209 | | — | | 0.03 | | — | | — | | — | | — | | — | |

Impairment charges(4) | | — | | — | | — | | — | | — | | — | | — | | — | | — | | — | |

Other expenses (5) | | 18 | | 2,306 | | 1,408 | | — | | 0.04 | | 242 | | 242 | | 149 | | — | | 0.01 | |

Total adjustments | | 12,058 | | 14,346 | | 8,757 | | — | | 0.25 | | 8,405 | | 8,405 | | 5,184 | | — | | 0.15 | |

As Adjusted | | $ | 43,703 | | $ | 39,636 | | $ | 24,370 | | 34,724,199 | | $ | 0.70 | | $ | 56,217 | | $ | 46,056 | | $ | 29,057 | | 35,539,839 | | $ | 0.82 | |

% of sales | | 9.4 | % | 8.5 | % | 5.2 | % | | | | | 8.0 | % | 6.6 | % | 4.2 | % | | | | |

Non-Cash Adjustments | | | | | | | | | | | | | | | | | | | | | |

Depreciation and amortization | | 11,369 | | 11,369 | | 6,942 | | — | | 0.20 | | 18,400 | | 18,400 | | 11,380 | | — | | 0.32 | |

Stock-based compensation expense | | 2,416 | | 2,416 | | 1,477 | | — | | 0.04 | | 2,653 | | 2,653 | | 1,640 | | — | | 0.05 | |

Total adjustments | | 13,785 | | 13,785 | | 8,418 | | — | | 0.24 | | 21,053 | | 21,053 | | 13,019 | | — | | 0.37 | |

Adjusted Cash EPS | | $ | 57,488 | | $ | 53,421 | | $ | 32,788 | | 34,724,199 | | $ | 0.94 | | $ | 77,270 | | $ | 67,109 | | $ | 42,076 | | 35,539,839 | | $ | 1.18 | |

| | Thirty-Nine Weeks Ended | |

| | October 28, 2014 | | November 3, 2015 | |

| | Income | | Income | | | | Diluted | | | | Income | | Income | | | | Diluted | | | |

| | From | | Before In- | | Net | | Weighted | | Diluted | | From | | Before In- | | Net | | Weighted | | Diluted | |

| | Operations | | come Taxes | | Income | | Shares | | EPS* | | Operations | | come Taxes | | Income | | Shares | | EPS* | |

As Reported | | $ | 74,033 | | $ | 61,393 | | $ | 37,631 | | 34,562,374 | | $ | 1.10 | | $ | 112,248 | | $ | 81,788 | | $ | 51,232 | | 35,536,418 | | $ | 1.44 | |

% of sales | | 6.1 | % | 5.1 | % | 3.1 | % | | | | | 5.8 | % | 4.3 | % | 2.7 | % | | | | |

Adjustments | | | | | | | | | | | | | | | | | | | | | |

Acquisition-related costs (1) | | 20,759 | | 20,759 | | 12,680 | | — | | 0.37 | | 19,351 | | 19,351 | | 11,913 | | — | | 0.34 | |

Secondary offering costs (2) | | — | | — | | — | | — | | — | | 487 | | 487 | | 487 | | — | | 0.01 | |

ERP system implementation costs (3) | | 5,071 | | 5,071 | | 3,097 | | — | | 0.09 | | 666 | | 666 | | 409 | | — | | 0.01 | |

Impairment charges(4) | | 482 | | 482 | | 294 | | — | | 0.01 | | 735 | | 735 | | 452 | | — | | 0.01 | |

Other (5) | | 1,369 | | 3,657 | | 2,234 | | — | | 0.06 | | 358 | | 358 | | 220 | | — | | 0.01 | |

Total adjustments | | 27,681 | | 29,969 | | 18,305 | | — | | 0.53 | | 21,597 | | 21,597 | | 13,481 | | — | | 0.38 | |

As Adjusted | | $ | 101,714 | | $ | 91,362 | | $ | 55,936 | | 34,562,374 | | $ | 1.62 | | $ | 133,845 | | $ | 103,385 | | $ | 64,713 | | 35,536,418 | | $ | 1.82 | |

% of sales | | 8.4 | % | 7.6 | % | 4.6 | % | | | | | 7.0 | % | 5.4 | % | 3.4 | % | | | | |

Non-Cash Adjustments | | | | | | | | | | | | | | | | | | | | | |

Depreciation and amortization | | 31,809 | | 31,809 | | 19,429 | | — | | 0.56 | | 50,943 | | 50,943 | | 31,361 | | — | | 0.88 | |

Stock-based compensation expense | | 4,973 | | 4,973 | | 3,038 | | — | | 0.09 | | 6,533 | | 6,533 | | 4,022 | | — | | 0.11 | |

Total adjustments | | 36,782 | | 36,782 | | 22,466 | | — | | 0.65 | | 57,476 | | 57,476 | | 35,382 | | — | | 1.00 | |

Adjusted Cash EPS | | $ | 138,496 | | $ | 128,144 | | $ | 78,402 | | 34,562,374 | | $ | 2.27 | | $ | 191,321 | | $ | 160,861 | | $ | 100,095 | | 35,536,418 | | $ | 2.82 | |

*Due to rounding to the nearest cent, totals may not equal the sum of the lines in the table above.

(1) Acquisition-related costs, which are included in the “As Reported” results of operations, consist of acquisition-related costs as defined under U.S. GAAP, including advisory, legal, accounting, valuation, and other professional or consulting fees and, in addition, costs of integrating store and warehouse operations and corporate functions that are not expected to recur as acquisitions are absorbed. On March 3, 2014, we acquired the assets and operations of Yotes, Inc., including 34 mattress specialty retail stores. On March 3, 2014, we acquired the Virginia assets and operations of Southern Max LLC, including 3 mattress specialty retail stores. On April 3, 2014, we acquired the outstanding partnership interests in Sleep Experts Partners, L.P., including 55 mattress specialty retail stores. On June 4, 2014, we acquired substantially all of the mattress specialty retail assets and operations of Mattress Liquidators, Inc., including 67 mattress specialty retail stores, which operated Mattress King retail stores in Colorado and BedMart retail stores in Arizona. On September 8, 2014, we acquired substantially all of the mattress specialty retail assets and operations of Best Mattress Co., Inc., related to the operation of 15 mattress specialty retail stores under the brand Mattress Discounters in Pennsylvania. On September 30, 2014, we acquired substantially all of the mattress specialty retail assets and operations of Back to Bed Inc., M World Mattress LLC, MCStores LLC and TBE Orlando LLC, related to the operation of 131 mattress specialty retail stores under the brands Back to Bed and Bedding Experts in the Chicago metropolitan area and Mattress Barn in the Orlando metropolitan area. On October 20, 2014, we acquired 100% of the outstanding equity interests in The Sleep Train, Inc., related to the operation of 314 mattress specialty retail stores in California, Oregon, Washington, Nevada, Idaho and Hawaii. On January 6, 2015, we acquired substantially all of the mattress specialty retail assets and operations of Sleep America LLC, which operated approximately 45 Sleep America retail stores in Arizona. On January 13, 2015 we acquired substantially all of the mattress specialty retail assets and operations of Mattress World, Inc., related to the operation of 4 mattress specialty retail stores under the brand Mattress World in Pennsylvania. Acquisition-related costs, consisting of direct transaction costs and integration costs, are included in the results of operations as incurred. We incurred approximately $8.2 million and $10.1 million of acquisition-related costs during the thirteen weeks ended November 3, 2015 and October 28, 2014, respectively. We incurred approximately $19.4 million and $20.8 million of acquisition-related costs during the thirty-nine weeks ended November 3, 2015 and October 28, 2014, respectively.

11

(2) Reflects approximately $0.5 million for the thirty-nine weeks ended November 3, 2015, of costs borne by us in connection with a secondary offering of common stock by certain of our selling shareholders which was completed in April 2015. No offering proceeds were received by the Company.

(3) Reflects implementation costs included in the results of operations as incurred, consisting primarily of training-related costs, related to the roll-out of the Microsoft Dynamics AX for Retail ERP system. During the thirteen weeks ended October 28, 2014, we incurred approximately $2.0 million of ERP system implementation costs which includes $0.1 million of accelerated depreciation expense on our legacy ERP system. During the thirty-nine weeks ended November 3, 2015 and October 28, 2014, we incurred approximately $0.7 million and $5.1 million, respectively, of ERP system implementation costs which includes approximately none and $0.3 million , respectively, of accelerated depreciation expense on our legacy ERP system.

(4) Reflects approximately $0.7 million and $0.5 million of impairment of store assets recorded in the thirty-nine weeks ended November 3, 2015 and October 28, 2014, respectively.

(5) Reflects expensed legal fees related to our February 2014 debt amendment and extension recorded in the thirteen weeks ended April 29, 2014, and severance expense resulting from the Company’s realignment of its management structure at the beginning of the third fiscal quarter recorded in the thirteen weeks ended October 28, 2014. Reflects a loss on debt extinguishment incurred in connection with the October 2014 refinancing of our Senior Credit Facility related to the Sleep Train acquisition recorded in the thirteen and thirty-nine weeks ended October 28, 2014. Reflects severance expense related to changes in organizational structure recorded in the thirteen and thirty-nine weeks ended November 3, 2015

Our “As Adjusted” data is considered a non-U.S. GAAP financial measure and is not in accordance with, or preferable to, “As Reported,” or GAAP financial data. However, we are providing this information as we believe it facilitates year-over-year comparisons for investors and financial analysts.

About Mattress Firm

With more than 2,400 company-operated and franchised stores across 41 states, Mattress Firm Holding Corp. (MFRM) has the largest geographic footprint in the United States among multi-brand mattress retailers. Founded in 1986, Houston-based MFRM is the nation’s leading specialty bedding retailer with over $2.5 billion in sales over the past 12 months. MFRM, through its family of brands, including Mattress Firm and Sleep Train, offers a broad selection of both traditional and specialty mattresses, bedding accessories and other related products from leading manufacturers, including Sealy, Tempur-Pedic, Serta, Simmons, Stearns & Foster, and Hampton & Rhodes. More information is available at www.mattressfirm.com. MFRM’s website is not part of this press release.

Investor Relations Contact:

Scott McKinney, Vice President of Investor Relations, ir@mfrm.com or 713-328-3417

Media Contact:

Kimberly Wise, kwise@jacksonspalding.com or 214-646-1659

###

12