February 25, 2014

William H. Thompson

Accounting Branch Chief

Securities and Exchange Commission

| Re: | Bio-Solution Corp. Form 10-K for the Fiscal Year Ended December 31, 2012 Filed March 22, 2013 Response Dated January 14, 2013 File No. 333-147917 |

Dear Mr. Thompson:

Thank-you for granting us addition time. We have reviewed your response letter dated January 14, 2014. Below are our responses. Bio-Solutions Corp recognizes that our Company is responsible for the adequacy and accuracy of the disclosures in the filing. Also, the staff comments or changes to disclosures in response to staff comments do not foreclose the Commission from taking any action with respect to the filing. In addition, our Company may not assert staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States.

Item 8. Financial Statements, page F-1

Report of Independent Registered Public Accounting Firm, page F-2

1. Please show us the updated auditor’s report to be included in the amendment you intend to file upon the completion of our review.

Company Response: Here is the corrected letter.

Report of Independent Registered Public Accounting Firm

To the Directors of

Bio-Solutions Corp.

We have audited the accompanying balance sheets of Bio-Solutions Corp. (the "Company") as of December 31, 2012 and 2011, and the related statements of operations and comprehensive loss, changes in stockholders' equity (deficit) and cash flows for the years ended December 31, 2012 and 2011 and for the statements of operations and comprehensive loss, changes in stockholders’ equity (deficit) and cash flows for the period October 1, 2011 through December 31, 2012 (Development Stage). These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement. We were not engaged to perform an audit of the Company’s internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of Bio-Solutions Corp. as of December 31, 2012 and 2011, and the results of its statements of operations and comprehensive loss, changes in stockholders’ equity (deficit), and cash flows for the year ended December 31, 2012 and 2011 and for the statements of operations and comprehensive loss, changes in stockholders’ equity (deficit) and cash flows for the period October 1, 2011 through December 31, 2012 (Development Stage) in conformity with U.S. generally accepted accounting principles.

The accompanying financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note 1 to the financial statements, the Company is in process of executing its business plan and expansion. The Company has not generated significant revenue to this point, however, has been successful in raising funds in their private placement. The lack of profitable operations and the need to continue to raise funds raise substantial doubt about the Company’s ability to continue as a going concern. Management’s plans in this regard are described in Note 1. The financial statements do not include any adjustments that might result from the outcome of this uncertainty.

/s/ KBL, LLP

New York, NY

March 22, 2013

2

Note 6 – Convertible Notes Payable, page F-15

2. We reviewed your response to comment 2 in our letter dated December 17, 2013. You state that the intrinsic values of the beneficial conversion features recognized as debt discounts were limited to the amount of proceeds allocated to the convertible debt instruments in accordance with ASC 470-20-30-8. However, we note that the discount amortization amounts reflected in the table on page 4 of your response equals the intrinsic value of the beneficial conversion features, which exceed the proceeds received upon issuance of the convertible notes as set forth in the table on page 3 of your response. Please address the following:

| · | Please tell us how you recorded the intrinsic value of the beneficial conversion features and why the discount amortization reflected in the amortization schedule on page 4 of your response exceeds the loan proceeds or revise the amortization table and the table on page 5 of your response accordingly. |

Company Response: The Company has revised the schedules to reflect the proper discounts as follows:

Short Term Loans - Convertible

BCF Adjustment

| Loan | Converted | Converion | Price on Date of | |||||||||||||||||||||

| Details | Curr | Proceeds | Shares | Price | Of Issuance | Discount | ||||||||||||||||||

| Q212 | ||||||||||||||||||||||||

| La Rocque - 11/30/2011 | On Demand | USD | 9,822 | 3,928,800 | 0.0025 | 0.0065 | 9,822 | |||||||||||||||||

| Envisionte - 12/16/2011 | 1 Year - 12.31.12 | USD | 4,100 | 1,640,000 | 0.0025 | 0.0100 | 4,100 | |||||||||||||||||

| Capital Consulting - 12/16/2011 | 1 Year - 12.31.12 | USD | 4,100 | 1,640,000 | 0.0025 | 0.0100 | 4,100 | |||||||||||||||||

| Capital Consulting - 3/31/2012 | 6 Month - 9.30.12 | USD | 15,000 | 1,666,667 | 0.0090 | 0.0265 | 15,000 | |||||||||||||||||

| Nelson - 4/20/2012 | 6 Month - 10.20.12 | USD | 2,500 | 277,778 | 0.0090 | 0.0165 | 2,083 | |||||||||||||||||

| Adrian - 4/20/2012 | 6 Month - 10.20.12 | USD | 5,000 | 555,556 | 0.0090 | 0.0165 | 4,167 | |||||||||||||||||

| La Rocque - 4/30/2012 | On Demand | USD | 9,822 | 3,928,800 | 0.0025 | 0.0180 | 9,822 | |||||||||||||||||

| Bill Gallagher - 5/10/2012 | 6 Month - 11.15.12 | USD | 2,600 | 288,889 | 0.0090 | 0.0150 | 1,733 | |||||||||||||||||

| Capital Consulting - 5/15/2012 | 6 Month - 11.15.12 | USD | 3,500 | 388,889 | 0.0090 | 0.0180 | 3,500 | |||||||||||||||||

Q212 Total | 56,444 | 14,315,379 | 54,327 | |||||||||||||||||||||

| Q312 | ||||||||||||||||||||||||

| Capital Consulting - 7/18/2012 | 5 Months 12.17.12 | USD | 30,000 | 4,285,714 | 0.0070 | 0.0155 | 30,000 | |||||||||||||||||

| Capital Consulting - 8.22.2012 | 5 Months 1.22.13 | USD | 3,000 | 428,571 | 0.0070 | 0.0150 | 3,000 | |||||||||||||||||

Q312 Total | 33,000 | 4,714,285 | 33,000 | |||||||||||||||||||||

| Q412 | ||||||||||||||||||||||||

| Capital Consulting - 10.19.2012 | 6 Months 4.19.13 | USD | 10,000 | 1,428,571 | 0.0070 | 0.0180 | 10,000 | |||||||||||||||||

| Capital Consulting - 11.23.2012 | 6 Months 5.23.13 | USD | 7,000 | 1,000,000 | 0.0070 | 0.0125 | 5,500 | |||||||||||||||||

Q412 Total | 17,000 | 2,428,571 | 15,500 | |||||||||||||||||||||

| Q113 | ||||||||||||||||||||||||

| Finch- 1.28.2013 | Due on Demand 80% Last 10 Days - $0.01 floor | USD | 12,500 | 1,050,420 | 0.0119 | 0.0200 | 8,508 | |||||||||||||||||

| Capital Consulting - 1.30.2013 | 6 Months 7.30.13 | USD | 7,500 | 1,500,000 | 0.0050 | 0.0172 | 7,500 | |||||||||||||||||

| Capital Consulting - 2.20.2013 | 6 Months 8.20.13 | USD | 7,500 | 1,500,000 | 0.0050 | 0.0174 | 7,500 | |||||||||||||||||

| Finch- 2.26.2013 | Due on Demand 80% Last 10 Days - $0.01 floor | USD | 12,500 | 946,970 | 0.0132 | 0.0150 | 1,705 | |||||||||||||||||

Q113 Total | 40,000 | 4,997,390 | 25,213 | |||||||||||||||||||||

| Q213 | ||||||||||||||||||||||||

| Capital Consulting - 4.30.2013 | 6 Months 10.30.13 | USD | 10,000 | 2,000,000 | 0.0050 | 0.0148 | 10,000 | |||||||||||||||||

| Capital Consulting - 4.30.2013 | 6 Months 10.30.13 | USD | 10,000 | 1,000,000 | 0.0100 | 0.0148 | 4,800 | |||||||||||||||||

| Capital Consulting - 5.27.2013 | 6 Months 11.27.13 | USD | 12,500 | 2,500,000 | 0.0050 | 0.0159 | 12,500 | |||||||||||||||||

| Finch- 6.11.2013 | 2 Months 8.11.13 | USD | 6,500 | 1,000,000 | 0.0065 | 0.0090 | 2,500 | |||||||||||||||||

| Hanbury LTD - 6.11.2013 | 2 Months 8.11.13 | USD | 6,222 | 957,231 | 0.0065 | 0.0090 | 2,393 | |||||||||||||||||

| Select Management - 6.11.2013 | 2 Months 8.11.13 | USD | 6,500 | 1,000,000 | 0.0065 | 0.0090 | 2,500 | |||||||||||||||||

| Capital Consulting - 6.18.2013 | 6 Months 12.18.13 | USD | 12,500 | 2,500,000 | 0.0050 | 0.0150 | 12,500 | |||||||||||||||||

Q213 Total | 64,222 | 10,957,231 | 47,193 | |||||||||||||||||||||

| Q313 | ||||||||||||||||||||||||

| Capital Consulting - 8.2.2013 | 6 Months 2.2.14 | USD | 10,000 | 2,000,000 | 0.0050 | 0.0100 | 10,000 | |||||||||||||||||

Q313 Total | 10,000 | 2,000,000 | 10,000 | |||||||||||||||||||||

| Grand Total | 220,666 | 39,412,856 | 185,233 | |||||||||||||||||||||

| · | We note that the grand totals for the fourth quarter of fiscal 2012 and first and second quarters of fiscal 2013 on page 4 of your response do not equal the sum of the subtotals. As such, it appears that the grand totals carried forward to page 5 of your response are incorrect. Please advise or revise both tables. If you revise the table on page 5 of your response, please include fourth quarter data in the quarter to-date summary. |

3

Company Response: The Company has revised the schedules to reflect proper values and subtotals as follows:

Short Term Loans - Convertible

BCF Adjustment

| Discount Amortization | ||||||||||||||||||||||||||||||||

| Q212 | Q312 | Q412 | Q113 | Q213 | Q313 | Q413 | Q114 | |||||||||||||||||||||||||

| Q212 | ||||||||||||||||||||||||||||||||

| La Rocque - 11/30/2011 | 9,822 | |||||||||||||||||||||||||||||||

| Envisionte - 12/16/2011 | 2,050 | 1,025 | 1,025 | |||||||||||||||||||||||||||||

| Capital Consulting - 12/16/2011 | 2,050 | 1,025 | 1,025 | |||||||||||||||||||||||||||||

| Capital Consulting - 3/31/2012 | 7,500 | 7,500 | ||||||||||||||||||||||||||||||

| Nelson - 4/20/2012 | 868 | 1,042 | 174 | |||||||||||||||||||||||||||||

| Adrian - 4/20/2012 | 1,736 | 2,084 | 347 | |||||||||||||||||||||||||||||

| La Rocque - 4/30/2012 | 9,822 | |||||||||||||||||||||||||||||||

| Bill Gallagher - 5/10/2012 | 433 | 867 | 433 | |||||||||||||||||||||||||||||

| Capital Consulting - 5/15/2012 | 875 | 1,750 | 875 | |||||||||||||||||||||||||||||

Q212 Total | 35,156 | 15,292 | 3,879 | - | - | - | ||||||||||||||||||||||||||

| Q312 | ||||||||||||||||||||||||||||||||

| Capital Consulting - 7/18/2012 | 15,000 | 15,000 | ||||||||||||||||||||||||||||||

| Capital Consulting - 8.22.2012 | 900 | 1,800 | 300 | |||||||||||||||||||||||||||||

Q312 Total | - | 15,900 | 16,800 | 300 | - | - | - | - | ||||||||||||||||||||||||

| Q412 | ||||||||||||||||||||||||||||||||

| Capital Consulting - 10.19.2012 | 4,167 | 5,000 | 833 | |||||||||||||||||||||||||||||

| Capital Consulting - 11.23.2012 | 1,375 | 2,750 | 1,375 | |||||||||||||||||||||||||||||

Q412 Total | - | - | 5,542 | 7,750 | 2,208 | - | - | - | ||||||||||||||||||||||||

| Q113 | ||||||||||||||||||||||||||||||||

| Finch- 1.28.2013 | 8,508 | |||||||||||||||||||||||||||||||

| Capital Consulting - 1.30.2013 | 2,500 | 3,750 | 1,250 | |||||||||||||||||||||||||||||

| Capital Consulting - 2.20.2013 | 1,875 | 3,750 | 1,875 | |||||||||||||||||||||||||||||

| Finch- 2.26.2013 | 1,705 | |||||||||||||||||||||||||||||||

Q113 Total | - | - | - | 14,588 | 7,500 | 3,125 | - | - | ||||||||||||||||||||||||

| Q213 | ||||||||||||||||||||||||||||||||

| Capital Consulting - 4.30.2013 | 3,333 | 5,000 | 1,667 | |||||||||||||||||||||||||||||

| Capital Consulting - 4.30.2013 | 1,600 | 2,400 | 800 | |||||||||||||||||||||||||||||

| Capital Consulting - 5.27.2013 | 2,083 | 6,250 | 4,167 | |||||||||||||||||||||||||||||

| Finch- 6.11.2013 | 625 | 1,875 | ||||||||||||||||||||||||||||||

| Hanbury LTD - 6.11.2013 | 598 | 1,795 | ||||||||||||||||||||||||||||||

| Select Management - 6.11.2013 | 625 | 1,875 | ||||||||||||||||||||||||||||||

| Capital Consulting - 6.18.2013 | 1,042 | 6,250 | 5,208 | |||||||||||||||||||||||||||||

Q213 Total | - | - | - | - | 9,907 | 25,445 | 11,842 | - | ||||||||||||||||||||||||

| Q313 | ||||||||||||||||||||||||||||||||

| Capital Consulting - 8.2.2013 | 3,333 | 5,000 | 1,667 | |||||||||||||||||||||||||||||

Q313 Total | - | - | - | - | - | 3,333 | 5,000 | 1,667 | ||||||||||||||||||||||||

| Grand Total | 35,156 | 31,192 | 26,221 | 22,638 | 19,615 | 31,903 | 16,842 | 1,667 | ||||||||||||||||||||||||

4

Here is the revised adjustment schedule with the Q412 data included:

Short Term Loans - Convertible

BCF Adjustment

| Discount Amortization | ||||||||||||||||||||||||||||

| Q212 | Q312 | Q412 | Q113 | Q213 | Q313 | Q413 | ||||||||||||||||||||||

| Quarter-To-Date Summary: | ||||||||||||||||||||||||||||

| BCF Interest Expense (Income) as Reported | 162,356 | 73,182 | (201,242 | ) | 42,074 | 57,754 | (108,666 | ) | ||||||||||||||||||||

| QTD Net Loss as Reported | (184,597 | ) | (282,940 | ) | 88,673 | (235,696 | ) | (344,634 | ) | (146,567 | ) | |||||||||||||||||

| QTD WASO | 67,190,397 | 73,773,114 | 95,859,866 | 108,771,254 | 132,694,907 | 167,946,447 | ||||||||||||||||||||||

| QTD EPS as Reported | (0.003 | ) | (0.004 | ) | 0.001 | (0.002 | ) | (0.003 | ) | (0.001 | ) | |||||||||||||||||

| BCF Interest Expense (Income) ##Adjusted## | 35,156 | 31,192 | 26,221 | 22,638 | 19,615 | 31,903 | 16,842 | |||||||||||||||||||||

| QTD Net Loss ##Adjusted## | (57,397 | ) | (240,950 | ) | (138,790 | ) | (216,260 | ) | (306,495 | ) | (287,136 | ) | ||||||||||||||||

| QTD WASO | 67,190,397 | 73,773,114 | 95,859,866 | 108,771,254 | 132,694,907 | 167,946,447 | ||||||||||||||||||||||

| QTD EPS ##Adjusted## | (0.001 | ) | (0.003 | ) | (0.001 | ) | (0.002 | ) | (0.002 | ) | (0.002 | ) | ||||||||||||||||

| QTD EPS Change (Dec.) Inc. | (0.002 | ) | (0.001 | ) | 0.002 | 0.000 | (0.001 | ) | 0.001 | |||||||||||||||||||

| Year-To-Date Summary: | ||||||||||||||||||||||||||||

| BCF Interest Expense (Income) as Reported | 162,356 | 235,537 | 34,296 | 42,074 | 99,828 | (8,838 | ) | |||||||||||||||||||||

| YTD Net Loss as Reported | (192,311 | ) | (475,251 | ) | (399,078 | ) | (235,696 | ) | (580,330 | ) | (726,897 | ) | ||||||||||||||||

| YTD WASO | 67,190,397 | 69,400,652 | 76,051,602 | 108,771,254 | 120,799,168 | 136,687,627 | ||||||||||||||||||||||

| YTD EPS as Reported | (0.003 | ) | (0.007 | ) | (0.005 | ) | (0.002 | ) | (0.005 | ) | (0.005 | ) | ||||||||||||||||

| BCF Interest Expense (Income) ##Adjusted## | 35,156 | 66,348 | 92,569 | 22,638 | 42,253 | 74,156 | 90,998 | |||||||||||||||||||||

| YTD Net Loss ##Adjusted## | (65,111 | ) | (306,062 | ) | (457,351 | ) | (216,260 | ) | (522,755 | ) | (809,891 | ) | ||||||||||||||||

| YTD WASO | 67,190,397 | 69,400,652 | 76,051,602 | 108,771,254 | 120,799,168 | 136,687,627 | ||||||||||||||||||||||

| YTD EPS ##Adjusted## | (0.001 | ) | (0.004 | ) | (0.006 | ) | (0.002 | ) | (0.004 | ) | (0.006 | ) | ||||||||||||||||

| YTD EPS Change (Dec.) Inc. | (0.002 | ) | (0.003 | ) | 0.001 | 0.000 | (0.001 | ) | 0.001 | |||||||||||||||||||

| Debt Discount at Reporting Date | 19,171 | 20,979 | 10,258 | 12,833 | 40,411 | 18,508 | 1,667 | |||||||||||||||||||||

| Proposed Adjustment | ||||||||||||||||||||||||||||

| Debt Discount | 19,171 | 1,809 | (10,721 | ) | 2,575 | 27,578 | (21,903 | ) | (16,842 | |||||||||||||||||||

| Interest Expense | (127,200 | ) | (41,991 | ) | 227,462 | (19,436 | ) | (38,139 | ) | 140,569 | 16,842 | |||||||||||||||||

| Additional Paid in Capital | 108,029 | 40,182 | (216,741 | ) | 16,861 | 10,561 | (118,666 | ) | - | |||||||||||||||||||

5

| · | Please show us how to reconcile the data in the table on page 5 of your response to the carrying value of convertible debt and amounts charged to additional paid-in capital for each period presented in the table. |

Company Response: Here is the requested reconciliation:

Interest Expense | PIC | ||||||||

| as Reported | as Reported | ||||||||

| Q212 | 162,356 | (162,356 | ) | ||||||

| Q312 | 73,182 | (73,182 | ) | ||||||

| Q412 | (201,242 | ) | 201,242 | ||||||

| Q113 | 42,074 | (42,074 | ) | ||||||

| Q213 | 57,754 | (57,754 | ) | ||||||

| Q313 | (108,666 | ) | 108,666 | ||||||

| 25,458 | (25,458 | ) | |||||||

| as Corrected | as Corrected | ||||||||

| Q212 | 35,156 | (35,156 | ) | ||||||

| Q312 | 31,192 | (31,192 | ) | ||||||

| Q412 | 26,221 | (26,221 | ) | ||||||

| Q113 | 22,638 | (22,638 | ) | ||||||

| Q213 | 19,615 | (19,615 | ) | ||||||

| Q313 | 31,903 | (31,903 | ) | ||||||

| 166,725 | (166,725 | ) | |||||||

| Q413 Adjustment | |||||||||

| Interst Expense | 141,267 | ||||||||

| PIC | (141,267 | ) | |||||||

| Amount | |||||||||

| Orginal Disount | 185,233 | ||||||||

| Amortization | 166,725 | ||||||||

| Bal at 9.30.13 | 18,508 | ||||||||

| Q413 Amort | 16,842 | ||||||||

| Q114 Amort | 1,667 | ||||||||

| 18,508 | |||||||||

| · | Please update your assessment of materiality and tell us the authoritative literature you are relying on to conclude that a quantitatively material misstatement can be overcome by qualitative factors and the facts and circumstances that support your interpretation of the literature. |

Company Response: The Company believes it has supported the position that the qualitative factors far out weight the quantitative factors in our letter dated January 2, 2014. We have no further information to add.

6

Here is our reasoning from our letter dated January 2, 2014:

The qualitative factors we considered are as follows:

| · | The Company is a development stage Company with almost no revenues (5 boxes sold through 12.31.13) and minimal other operating activity. |

| · | The Company produced our first product (Type2Defense) in June 2013 and created an infomercial in September 2013, unfortunately the financing to launch the product fell through and we are currently working on new financing. The Company does not have the resources for a restatement. We are hoping to launch in Q114 and create jobs. |

| · | The restatement is for a non-cash item – amortization of discount (interest expense). We do not believe the quality of the financial statements will deteriorate by a $.001 or $.002 change in earnings per share. |

| · | The financials were issued with a going concern. The company is not misleading the users to the financial statements. Until the Company generates significant revenue – this is not a safe investment. |

| · | The Company will fully record and disclose the adjustment in the 12.31.13 Form 10-K. |

The Company’s consideration of ASC 250-10-S99-2 in recommending to correct the accounting errors in the three months ended 12.31.13 are as follows.

| · | FN74 - The Company has properly determined that the overstatement of the liability and understatement of expense resulted from an error rather than a change in accounting estimate and appropriately quantified the amount of this error for the purpose of evaluating materiality for the current year. Based on the quantitative factors the misstatement is material. However, based on the qualitative factors the Company’s position is the misstatement is not material. |

| · | FN75 - Topic 1N addresses certain of these quantitative issues. The Company is proposing the “iron curtain” approach that quantifies a misstatement based on the effects of correcting the misstatement existing in the balance sheet at the end of the current year, irrespective of the misstatements year of origination. |

| · | FN76 - FASB Concepts Statement No. 2, Qualitative Characteristics of Accounting Information. The Company’s position: there is a low probability that the judgment of a reasonable person relying upon the financial statements and notes would have been changed or influenced by the correction of the misstatement. |

| · | FN77 - Statement 154, paragraph 2h [Section 250-10-20]. The Company will quantify the current year misstatement using both the iron curtain approach and the rollover approach in the 12.31.13 Form 10-K. We will quantify the current year and prior year impact on the current year financial statements. |

Conclusion:

The Company’s position is to record the 2012 and 2013 misstatement in the three months ended 12.31.13 and properly disclose the adjustment in the 12.31.13 Form 10-K as described above.

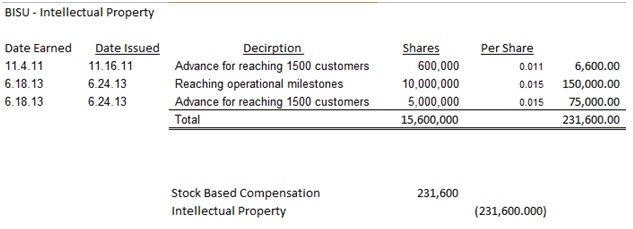

Note 10 – Intellectual Property, page F-17

3. We reviewed your response to comment 3 in our letter dated December 17, 2013. We note that ASC 805-30 includes guidance on the recognition of a contingent consideration arrangement in connection with a business combination. However, it does not appear that ASC 805-50 addresses the recognition of a contingent consideration arrangement in connection with an asset purchase. Please tell us your basis in GAAP for the recognizing the contingent payments based on achieving certain operational milestones as an additional cost of the intellectual property. In doing so, please address the following:

| · | Tell us the terms of Mr. Gallagher’s and Dr. Mallangi’s continuing employment and how the contingent consideration arrangement might be affected if their employment was terminated. Please refer to 805-10-55-25(a). |

Company Response – There would be no impact – the shares would be paid to Mr. Gallaher if his employment was terminated. Mr. Mallangi was never owed any shares. He was simply paid as a consultant with cash.

7

| · | It appears that the fair value of the intellectual property exceeded the initial purchase price given your agreement to provide additional consideration based on performance. Tell us how you determined the fair value of the intellectual property and your basis in GAAP for capitalizing additional consideration as paid. |

| · | With regards to the number of shares owned, ASC 805-10-55-25(e) suggests that if the selling shareholders who owned substantially all of the shares in the acquiree (Type2Defense) continue as key employees, that fact may indicate that the arrangement is, in substance, a profit-sharing arrangement intended to provide compensation for postcombination services. In-light- of the fact that your only employees are Mr. Gallagher and Dr. Mallangi, formerly of Type2Defense, who are now in key roles for Bio-Solutions, please explain your consideration of this guidance in determining the contingent payments represent additional consideration rather than compensation. |

Company Response – Agreed see bullet point two above.

| · | Please explain your basis in GAAP for your determination that additional consideration for achieving operational milestones is not representative of compensation to employees for services rendered in achieving those milestones. Please refer to 805-10-55-25(g). |

Company Response – Agreed see bullet point two above.

The Company recognizes the comments from the previous letter dated November 20, 2013 and December 17, 2013 in addition to the comments above and will implement all changes discussed in all three letters.

Best Regards,

/s/ William Gallagher

William Gallagher

CEO, CFO and Director of Bio-Solutions

8