Table of Contents

As filed with the Securities and Exchange Commission on December 21, 2007

Registration No. 333-

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

NiSource Energy Partners, L.P.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 4922 | 51-0658510 | ||

| (State or Other Jurisdiction of Incorporation or Organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

801 East 86th Avenue

Merrillville, Indiana 46410

877-647-5990

(Address, Including Zip Code, and Telephone Number,

Including Area Code, of Registrant’s Principal Executive Offices)

Carrie J. Hightman

Chief Legal Officer

801 East 86th Avenue

Merrillville, Indiana 46410

877-647-5990

(Name, Address, Including Zip Code, and Telephone Number,

Including Area Code, of Agent for Service)

Copies to:

| David P. Oelman Vinson & Elkins L.L.P. 1001 Fannin Street, Suite 2500 Houston, Texas 77002 (713) 758-2222 | Joshua Davidson Christopher Arntzen Baker Botts L.L.P. 910 Louisiana Street Houston, Texas 77002 (713) 229-1234 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. o

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If delivery of the prospectus is expected to be made pursuant to Rule 434, please check the following box. o

CALCULATION OF REGISTRATION FEE

| Proposed Maximum | Amount of | |||||

| Title of Each Class of | Aggregate Offering | Registration | ||||

| Securities to be Registered | Price(1)(2) | Fee | ||||

| Common units representing limited partner interests | $301,875,000 | $9,268 | ||||

| (1) | Includes common units issuable upon exercise of the underwriters’ option to purchase additional common units. | |

| (2) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o). |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

| The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted. |

Subject to Completion, dated December 21, 2007

PROSPECTUS

12,500,000 Common Units

Representing Limited Partner Interests

We are a limited partnership recently formed by NiSource Inc. This is the initial public offering of our common units. We currently estimate that the initial public offering price will be between $ and $ per common unit. Prior to this offering, there has been no public market for our common units. We intend to apply to list our common units on the New York Stock Exchange under the symbol “NIA.”

Investing in our common units involves risks. Please read “Risk Factors” beginning on page 17.

These risks include the following:

| • | We may not have sufficient cash from operations following the establishment of cash reserves and payment of fees and expenses, including cost reimbursements to our general partner, to enable us to make cash distributions to holders of our common units and subordinated units at the initial distribution rate under our cash distribution policy. |

| • | Our natural gas transportation operations are subject to regulation by federal agencies, including the Federal Energy Regulatory Commission, which could have an adverse impact on our ability to establish transportation rates that would allow us to recover the full cost of operating our pipelines, including a reasonable return, and our ability to make distributions to you. |

| • | NiSource Inc. controls our general partner, which has sole responsibility for conducting our business and managing our operations. Our general partner and its affiliates, including NiSource Inc., have conflicts of interest with us and limited fiduciary duties, and they may favor their own interests to your detriment. |

| • | Affiliates of NiSource Inc. are not limited in their ability to compete with us and are not obligated to offer us the opportunity to pursue additional assets or businesses, which could limit our commercial activities or our ability to acquire additional assets or businesses. |

| • | You will not be entitled to receive distributions or allocations of income or loss on your common units and your common units will be subject to redemption at a price that may be below the current market price, unless you are (1) an individual or entity subject to U.S. federal income taxation on the income generated by us or (2) an entity not subject to U.S. federal taxation on the income generated by us, but all of whose owners are subject to such taxation. |

| • | Holders of our common units have limited voting rights and are not entitled to elect our general partner or its directors. |

| • | You will experience immediate and substantial dilution of $16.41 in tangible net book value per common unit. |

| • | You may be required to pay taxes on your share of our income even if you do not receive any cash distributions from us. |

| Per Common Unit | Total | |||

| Initial public offering price | $ | $ | ||

| Underwriting discount(1) | $ | $ | ||

| Proceeds to NiSource Energy Partners, L.P. (before expenses) |

| (1) | Excludes an aggregate structuring fee equal to 0.375% of the gross proceeds of this offering, or approximately $ , payable to Lehman Brothers Inc. |

We have granted the underwriters a30-day option to purchase up to an additional 1,875,000 common units from us on the same terms and conditions as set forth above if the underwriters sell more than 12,500,000 common units in this offering.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

Lehman Brothers, on behalf of the underwriters, expects to deliver the common units on or about , 2008.

| Lehman Brothers | Citi |

, 2008

Table of Contents

Table of Contents

TABLE OF CONTENTS

| 1 | ||||

| 1 | ||||

| 1 | ||||

| 2 | ||||

| 3 | ||||

| 3 | ||||

| 15 | ||||

| 17 | ||||

| 17 | ||||

| 31 | ||||

| 38 | ||||

| 42 | ||||

| 43 | ||||

| 44 | ||||

| 46 | ||||

| 46 | ||||

| 47 | ||||

| 49 | ||||

| 53 | ||||

| 57 | ||||

| 60 | ||||

| 60 | ||||

| 61 | ||||

| 62 | ||||

| 63 | ||||

| 64 | ||||

| 64 | ||||

| 65 | ||||

| 65 | ||||

| 67 | ||||

| 68 | ||||

| 68 | ||||

| 71 | ||||

| 73 | ||||

| 75 | ||||

| 75 | ||||

| 75 | ||||

| 76 | ||||

| 78 | ||||

| 80 | ||||

| 81 |

i

Table of Contents

| 84 | ||||

| 85 | ||||

| 85 | ||||

| 87 | ||||

| 88 | ||||

| 90 | ||||

| 93 | ||||

| 93 | ||||

| 93 | ||||

| 94 | ||||

| 95 | ||||

| 96 | ||||

| 100 | ||||

| 100 | ||||

| 102 | ||||

| 106 | ||||

| 106 | ||||

| 108 | ||||

| 108 | ||||

| 108 | ||||

| 109 | ||||

| 109 | ||||

| 110 | ||||

| 110 | ||||

| 111 | ||||

| 112 | ||||

| 112 | ||||

| 112 | ||||

| 116 | ||||

| 116 | ||||

| 119 | ||||

| 120 | ||||

| 120 | ||||

| 121 | ||||

| 121 | ||||

| 122 | ||||

| 123 | ||||

| 123 | ||||

| 128 | ||||

| 131 | ||||

| 131 | ||||

| 131 | ||||

| 131 | ||||

| 133 | ||||

| 133 |

ii

Table of Contents

| 133 | ||||

| 133 | ||||

| 133 | ||||

| 133 | ||||

| 134 | ||||

| 135 | ||||

| 136 | ||||

| 136 | ||||

| 138 | ||||

| 139 | ||||

| 139 | ||||

| 140 | ||||

| 141 | ||||

| 141 | ||||

| 141 | ||||

| 141 | ||||

| 142 | ||||

| 142 | ||||

| 143 | ||||

| 143 | ||||

| 144 | ||||

| 144 | ||||

| 144 | ||||

| 144 | ||||

| 145 | ||||

| 145 | ||||

| 146 | ||||

| 147 | ||||

| 147 | ||||

| 148 | ||||

| 149 | ||||

| 154 | ||||

| 155 | ||||

| 157 | ||||

| 157 | ||||

| 158 | ||||

| 160 | ||||

| 161 | ||||

| 162 | ||||

| 163 | ||||

| 163 | ||||

| 163 | ||||

| 164 | ||||

| 164 | ||||

| 165 |

iii

Table of Contents

| 165 | ||||||||

| 165 | ||||||||

| 166 | ||||||||

| 166 | ||||||||

| 166 | ||||||||

| 166 | ||||||||

| 166 | ||||||||

| 166 | ||||||||

| 167 | ||||||||

| 167 | ||||||||

| 167 | ||||||||

| 167 | ||||||||

| F-1 | ||||||||

| A-1 | ||||||||

| B-1 | ||||||||

| C-1 | ||||||||

| D-1 | ||||||||

| Certificate of Limited Partnership | ||||||||

| Certificate of Formation | ||||||||

| Consent of Deloitte & Touche LLP | ||||||||

You should rely only on the information contained in this prospectus or any free writing prospectus prepared by or on behalf of us in connection with this offering. We have not, and the underwriters have not, authorized anyone to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. We are not, and the underwriters are not, making an offer to sell these securities in any jurisdiction where an offer or sale is not permitted. You should assume that the information appearing in this prospectus is accurate as of the date on the front cover of this prospectus. Our business, financial condition, results of operations and prospects may have changed since that date.

Until , 2008 (25 days after the date of this prospectus), all dealers that buy, sell or trade our common units, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers’ obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

iv

Table of Contents

This summary provides a brief overview of information contained elsewhere in this prospectus. You should read the entire prospectus carefully, including “Risk Factors” beginning on page 17 and the historical and pro forma financial statements. Unless indicated otherwise, the information presented in this prospectus assumes (1) an initial public offering price of $20.00 per common unit and (2) that the underwriters do not exercise their option to purchase additional units. We include a glossary of some of the terms used in this prospectus as Appendix D. References in this prospectus to “NiSource Energy Partners, L.P.,” “we,” “our,” “us” or like terms when used in a historical context refer to the business that NiSource Inc. is contributing to NiSource Energy Partners, L.P. in connection with this offering. When used in the present tense or prospectively, those terms refer to NiSource Energy Partners, L.P. and its subsidiaries. References to our “general partner” refer to NiSource GP, LLC. References to “NiSource” and “Columbia Gulf” refer to NiSource Inc. and its subsidiaries and Columbia Gulf Transmission Company, LLC, or its predecessor Columbia Gulf Transmission Company, respectively.

NiSource Energy Partners, L.P.

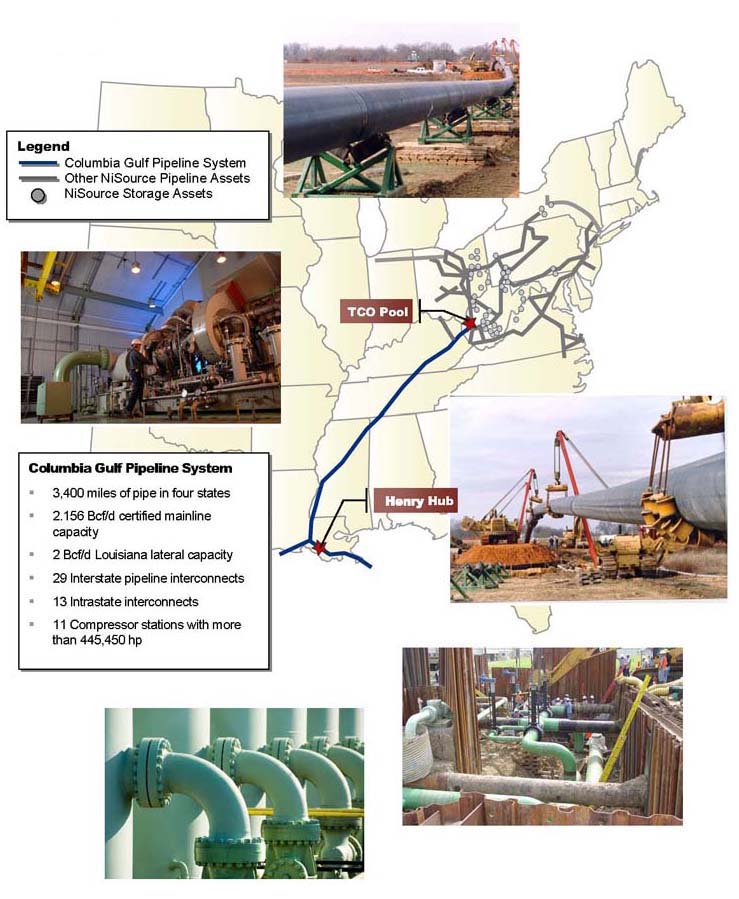

We are a growth-oriented Delaware limited partnership recently formed by NiSource to own and operate natural gas transportation pipelines and related energy infrastructure assets. Our initial asset is the Columbia Gulf pipeline system, an approximately 3,400 mile interstate natural gas transportation pipeline system that extends from southern Louisiana into Kentucky and is regulated by the Federal Energy Regulatory Commission (FERC).

NiSource is an energy holding company whose subsidiaries provide natural gas, electricity and other products and services to approximately 3.8 million customers located within a corridor that runs from the Gulf Coast through the Midwest to New England. At December 31, 2006, NiSource had approximately 16,000 miles of interstate pipelines (including the Columbia Gulf pipeline system) and operated one of the nation’s largest underground natural gas storage systems with 36 storage facilities capable of storing approximately 252 Bcf of working gas. We intend to utilize the significant experience of NiSource’s management team to execute our growth strategy, which includes the construction and acquisition of additional energy infrastructure assets.

The Columbia Gulf pipeline system consists of approximately 3,400 miles of pipelines and 11 compressor stations with approximately 445,450 horsepower located in Louisiana, Mississippi, Tennessee and Kentucky. The Columbia Gulf pipeline system primarily consists of:

| • | The Mainline System. Columbia Gulf’s Mainline System extends from southern Louisiana to a pipeline interconnection with Columbia Gas Transmission Corporation (Columbia Gas Transmission), a subsidiary of NiSource, in northeastern Kentucky. The Mainline System consists of approximately 2,550 miles of pipelines with peak-design throughput capacity of 2.2 Bcf/d; and | |

| • | The Louisiana Laterals. The Louisiana Laterals consist of the West Lateral and the East Lateral. The West Lateral extends from an interconnection with the Mainline System along the southern tier of Louisiana westward to Hackberry, Louisiana, while the East Lateral extends eastward to New Orleans and Venice, Louisiana. The Louisiana Laterals consist of approximately 850 miles of pipelines with maximum peak-design capacity in excess of 1.0 Bcf/d on each lateral. |

The Columbia Gulf pipeline system was originally constructed for the sole purpose of moving natural gas produced on the Gulf Coast to Midwestern and Mid-Atlantic end-use markets. Since 2006, approximately 1.5 Bcf/d of access to new supply and approximately 0.7 Bcf/d of access to new markets have been added to the system through new interconnects and other system modifications. As a result of this development of laterals and pipeline interconnects, the functionality of this system has fundamentally changed. In addition to traditional supplies on the Gulf Coast, we now have access to multiple strategic natural gas supply sources,

1

Table of Contents

including basins in North Texas (Barnett Shale), East Texas, North Louisiana and the Appalachian Basin. Similarly, we now provide a pathway for delivery to growing markets in the Southeast in addition to our traditional Midwestern and Mid-Atlantic markets. With interconnections to 29 interstate and 13 intrastate pipelines as of September 30, 2007, we no longer operate solely as a supplier of point-to-point gas transportation services, but as a flexible network that connects multiple producing areas to multiple end-use markets. By continuing to develop the Columbia Gulf pipeline system as a flexible transportation link, we believe we can increase the amount of cash we are able to distribute to you.

For the year ended December 31, 2006 and the nine months ended September 30, 2007, we generated net income of $18.3 million and $20.1 million, respectively, and EBITDA of $54.0 million and $49.0 million, respectively. After adjusting for certain transactions to be effected at the closing of this offering, we would have generated pro forma net income of $21.9 million and $25.1 million, respectively, and pro forma EBITDA of $54.1 million and $49.9 million, respectively. We define our EBITDA as net income plus interest expense (net of a non-cash allowance for funds used during construction, or AFUDC), income taxes and depreciation and amortization, less interest income and other, net. Please read “— Non-GAAP Financial Measures” for an explanation of how we calculate EBITDA, which is a financial measure we use to evaluate our performance, and for a reconciliation of EBITDA to its most directly comparable financial measures calculated and presented in accordance with generally accepted accounting principles in the United States (GAAP).

We transport natural gas for a broad mix of customers, including local gas distribution companies (LDCs), municipal utilities, direct industrial users, electric power generators, marketers, producers and liquified natural gas (LNG) importers. In addition to serving markets directly connected to our system, we serve markets and customers in a variety of other regions through numerous interconnections with major interstate and intrastate pipelines. The rates we charge are regulated by the FERC.

Our pipeline system currently accesses natural gas supply from producing regions in Texas, Louisiana, the Gulf of Mexico and Appalachia, and is positioned to access new supplies from Gulf Coast LNG imports and non-traditional basins such as the Fayette Shale in Arkansas. Through interconnections with major interstate and intrastate pipelines, we also provide transportation of natural gas to growing markets in the Northeast, Midwest, Mid-Atlantic and Southeast United States, and serve industrial, commercial, electric generation and residential customers in Tennessee, Mississippi and Louisiana. We offer customers direct physical access to two of the most actively traded natural gas markets in North America at the Henry Hub in South Louisiana and the Columbia Gas Transmission Supply Pool (TCO Pool) at Leach, Kentucky.

We provide a significant portion of our transportation services under firm contracts that obligate our customers to pay monthly capacity reservation fees over the term of the contract. These monthly capacity reservation fees are payable to us regardless of the actual pipeline capacity utilized. An incremental usage fee based on the actual volume of natural gas transported is also applied when a customer utilizes the capacity it has reserved under these firm contracts. Though they are typically a small percentage of the total revenue we receive under our firm contracts, usage fees enable us to recover our variable costs incurred for the transportation of natural gas on our system. We also derive a portion of our revenues through interruptible contracts under which customers pay fees based on their utilization of our assets for transportation and other related services. Customers who have executed interruptible contracts are not assured capacity in our pipeline facilities. For the twelve months ended September 30, 2007, approximately 80.1% of our transportation revenues were derived from capacity reservation fees paid under firm contracts, approximately 8.7% of our transportation revenues were derived from usage fees under firm contracts and approximately 11.2% of our transportation revenues were derived from interruptible contracts.

The high percentage of our earnings derived from capacity reservation fees mitigates the risk to us of earnings fluctuations caused by changing supply and demand conditions. In addition, we do not own the gas we transport, and we retain a portion of the gas transported in our system to use as fuel for our compressors. As such, we have no direct commodity price exposure. For additional information about our contracts, please read “Management’s Discussion and Analysis of Financial Condition and Results of Operations — How We Evaluate Our Operations” and “Business — FERC Regulation.”

2

Table of Contents

Our primary business objectives are to generate predictable and stable cash flow and, over time, to increase our quarterly cash distribution per unit. We intend to achieve these objectives by executing the following strategies:

| • | Pursue economically attractive organic expansion opportunities and greenfield development projects; | |

| • | Optimize our asset base and increase profitability by expanding our points of supply and market access; and | |

| • | Grow through joint ventures, partnerships and accretive acquisitions of energy infrastructure assets from both NiSource and third parties. |

We believe we are well positioned to successfully execute our business strategies because of the following competitive strengths:

| • | Our strategic location allows us to transport natural gas from diverse supply sources to high-demand markets at competitive transportation rates; | |

| • | Our firm contracts and capacity reservation fees provide cash flow stability; | |

| • | Our pipeline assets have been prudently operated and well maintained; | |

| • | Our affiliation with NiSource; and | |

| • | Our experienced management team has a proven track record of operating large and complex interstate natural gas transportation, storage and marketing assets. |

Our Relationship with NiSource

One of our principal strengths is our relationship with NiSource, which following this offering will indirectly own our 2% general partner, all of our incentive distribution rights, and a 58.9% limited partner interest in us. NiSource is an energy holding company whose subsidiaries provide natural gas, electricity and other products and services to approximately 3.8 million customers located within a corridor that runs from the Gulf Coast through the Midwest to New England. NiSource is the largest natural gas distribution company operating east of the Rocky Mountains, as measured by number of customers. We intend to utilize the significant experience of NiSource’s management team to execute our growth strategy, including the construction and acquisition of additional energy infrastructure assets. NiSource’s common stock is traded on the New York Stock Exchange under the symbol “NI.”

NiSource’s Gas Transmission and Storage Operations subsidiaries own and operate approximately 16,000 miles of interstate pipelines (including the Columbia Gulf pipeline system) and operate one of the nation’s largest underground natural gas storage systems with 36 storage fields capable of storing approximately 252 Bcf of working gas as of December 31, 2006. Through its subsidiaries, NiSource owns and operates an interstate pipeline network extending from offshore in the Gulf of Mexico to Lake Erie, New York and the eastern seaboard. Together, these companies serve customers in 19 northeastern, Mid-Atlantic, Midwestern and southern states and the District of Columbia. The Gas Transmission and Storage Operations subsidiaries are engaged in several projects that will expand their facilities and throughput. The Millennium Pipeline is currently under construction and will connect the Empire Pipeline to the Algonquin Pipeline in order to transport natural gas to the greater New York City metropolitan area. In addition, Hardy Storage, a partnership that owns a natural gas storage field in West Virginia and serves the eastern United States, commenced operations in April 2007 and will be fully operational in 2009. In addition to its Gas Transmission and Storage Operations, NiSource’s Natural Gas Distribution Operations serves customers in nine states, and its Electric Operations generates, transmits and distributes electricity to customers in the northern part of Indiana and engages in wholesale and transmission transactions.

3

Table of Contents

We will enter into an omnibus agreement with NiSource, our general partner, and certain of their affiliates that will govern our relationship with them regarding certain reimbursement and indemnification matters. Please read “Certain Relationships and Related Party Transactions — Omnibus Agreement.” While our relationship with NiSource and its subsidiaries is a significant attribute, it may also be a source of conflicts. For example, neither NiSource nor any of its affiliates are prohibited from competing with us. NiSource and its affiliates may acquire, construct or dispose of assets in the future without any obligation to offer us the opportunity to purchase or construct those assets. Please read “Conflicts of Interest and Fiduciary Duties.”

Summary of Risk Factors

An investment in our common units involves risks. The following list of risk factors is not exhaustive. Please read carefully these and other risks described under “Risk Factors.”

Risks Related to Our Business

| • | We may not have sufficient cash from operations following the establishment of cash reserves and payment of fees and expenses, including cost reimbursements to our general partner, to enable us to make cash distributions to holders of our common units and subordinated units at the initial distribution rate under our cash distribution policy. | |

| • | On a pro forma basis we would not have had sufficient cash available for distribution to pay the full minimum quarterly distribution on all units for the year ended December 31, 2006 and the twelve months ended September 30, 2007, respectively. Please read “Our Cash Distribution Policy and Restrictions on Distributions.” | |

| • | The assumptions underlying our minimum estimated cash available for distribution we include in “Our Cash Distribution Policy and Restrictions on Distributions” are inherently uncertain and are subject to significant business, economic, financial, regulatory and competitive risks and uncertainties that could cause actual results to differ materially from those estimated. | |

| • | Our natural gas transportation operations are subject to regulation by the FERC, which could have an adverse impact on our ability to establish transportation rates that would allow us to recover the full cost of operating our pipelines, including a reasonable return, and our ability to make distributions to you. | |

| • | We may not be able to maintain or replace expiring gas transportation contracts at favorable rates. | |

| • | Any significant decrease in supplies of natural gas in our areas of operation could adversely affect our business and operating results and reduce our cash available for distribution to unitholders. |

Risks Inherent in an Investment in Us

| • | NiSource controls our general partner, which has sole responsibility for conducting our business and managing our operations. Our general partner and its affiliates, including NiSource, have conflicts of interest with us and limited fiduciary duties, and may favor their own interests to your detriment. | |

| • | Affiliates of NiSource are not limited in their ability to compete with us and are not obligated to offer us the opportunity to pursue additional assets or businesses, which could limit our commercial activities or our ability to acquire additional assets or businesses. | |

| • | You will not be entitled to receive distributions or allocations of income or loss on your common units, and your common units will be subject to redemption at a price that may be below the current market price, unless you are (1) an individual or entity subject to U.S. federal income taxation on the income generated by us or (2) an entity not subject to U.S. federal taxation on the income generated by us, but all of whose owners are subject to such taxation. |

4

Table of Contents

| • | Cost reimbursements to our general partner and its affiliates for services provided, which will be determined by our general partner, will be substantial and will reduce our cash available for distribution to you. | |

| • | Our partnership agreement limits our general partner’s fiduciary duties to holders of our common units and subordinated units and restricts the remedies available to holders of our common units and subordinated units for actions taken by our general partner that might otherwise constitute breaches of fiduciary duty. |

Tax Risks to Common Unitholders

| • | Our tax treatment depends on our status as a partnership for federal income tax purposes, as well as our not being subject to a material amount of entity-level taxation by individual states. If the Internal Revenue Service (IRS) were to treat us as a corporation for federal income tax purposes or we were to become subject to additional amounts of entity-level taxation for state tax purposes, then our cash available for distribution to you could be substantially reduced. | |

| • | We prorate our items of income, gain, loss and deduction between transferors and transferees of our units each month based upon the ownership of our units on the first day of each month, instead of on the basis of the date a particular unit is transferred. The IRS may challenge this treatment, which could change the allocation of items of income, gain, loss and deduction among our unitholders. | |

| • | If the IRS contests the federal income tax positions we take, the market for our common units may be adversely impacted, and the costs of any IRS contest will reduce our cash available for distribution to you. | |

| • | You may be required to pay taxes on your share of our income even if you do not receive any cash distributions from us. | |

| • | Tax gain or loss on disposition of our common units could be more or less than expected. | |

| • | Tax-exempt entities and non-U.S. persons face unique tax issues from owning our common units that may result in adverse tax consequences to them. |

5

Table of Contents

Formation Transactions and Partnership Structure

NiSource recently formed us as a Delaware limited partnership to own and operate certain natural gas transportation assets to be contributed to us by NiSource. As is common with publicly traded limited partnerships and in order to maximize operational flexibility, we will conduct our operations through subsidiaries. We will have one direct operating subsidiary initially, NiSource Operating LLC, a Delaware limited liability company that will conduct business through itself and its subsidiaries.

At the closing of this offering the following transactions will occur:

| • | NiSource will contribute Columbia Gulf to us; | |

| • | we will issue to a subsidiary of NiSource 8,584,349 common units and 10,222,715 subordinated units, representing an aggregate 58.9% limited partner interest in us; | |

| • | we will issue to NiSource GP, LLC, a subsidiary of NiSource, a 2% general partner interest in us and all of our incentive distribution rights, which will entitle our general partner to increasing percentages of the cash we distribute in excess of $0.345 per unit per quarter (115% of the minimum quarterly distribution); | |

| • | we will issue 12,500,000 common units to the public in this offering, representing a 39.1% limited partner interest in us, and will use the proceeds as described in “Use of Proceeds”; | |

| • | we will borrow approximately $37.0 million of term debt and $163.0 million of revolving debt under our $250.0 million credit facility and distribute the aggregate amount of such borrowings to subsidiaries of NiSource; and | |

| • | we will enter into an omnibus agreement with NiSource, our general partner and certain of their affiliates pursuant to which: |

| - | we will reimburse NiSource for the payment of certain operating expenses and for providing various general and administrative services; and | |

| - | NiSource will indemnify us for certain environmental and tax liabilities, title and right-of-way defects and certain government-mandated pipeline capital expenditures. |

Management of NiSource Energy Partners, L.P.

NiSource GP, LLC, our general partner, has sole responsibility for conducting our business and for managing our operations. An affiliate of NiSource, as the sole member of our general partner, will elect all seven members to the board of directors of NiSource GP, LLC, with at least three directors meeting the independence standards established by the New York Stock Exchange. We will have one independent director at the closing of this offering, with the balance to be elected within the time period prescribed by the New York Stock Exchange. All of the executive officers and certain of the directors of our general partner are employed by affiliates of NiSource and will allocate their time between managing our business and affairs and the business and affairs of NiSource and its affiliates. For more information about these individuals, please read “Management — Directors and Executive Officers.”

6

Table of Contents

Organizational Structure and Ownership

The following diagram depicts our organizational structure after giving effect to this offering and the related transactions assuming no exercise of the underwriters’ option to purchase additional common units.

| Public Common Units | 12,500,000 | 39.1% | ||||||

| NiSource Common Units | 8,584,349 | 26.9% | ||||||

| NiSource Subordinated Units | 10,222,715 | 32.0% | ||||||

| General Partner Units | 638,920 | 2.0% | ||||||

| Total | 31,945,984 | 100.0% | ||||||

7

Table of Contents

Principal Executive Offices and Internet Address

Our principal executive offices are located at 801 East 86th Avenue, Merrillville, Indiana 46410 and our telephone number is877-647-5990. Our website is located at http://www.nisourceenergypartners.com and will be activated in connection with the closing of this offering. We expect to make our periodic reports and other information filed with or furnished to the Securities and Exchange Commission (SEC) available free of charge through our website as soon as reasonably practicable after those reports and other information are electronically filed with or furnished to the SEC. Information on our website or any other website is not incorporated by reference into this prospectus and does not constitute a part of this prospectus.

Summary of Conflicts of Interest and Fiduciary Duties

General. Our general partner has a legal duty to manage us in a manner beneficial to holders of our common units and subordinated units. This legal duty originates in statutes and judicial decisions and is commonly referred to as a “fiduciary duty.” However, because our general partner is owned by NiSource, the officers and directors of our general partner also have fiduciary duties to manage our general partner in a manner beneficial to NiSource. As a result of this relationship, conflicts of interest may arise in the future between us and holders of our common units and subordinated units, on the one hand, and our general partner and its affiliates on the other hand.

Partnership Agreement Modifications to Fiduciary Duties. Our partnership agreement limits the liability and reduces the fiduciary duties of our general partner to holders of our common units and subordinated units. Our partnership agreement also restricts the remedies available to holders of our common units and subordinated units for actions that might otherwise constitute a breach of our general partner’s fiduciary duties owed to holders of our common units and subordinated units. Our partnership agreement also provides that affiliates of our general partner, including NiSource and its affiliates, are not restricted from competing with us. By purchasing a common unit, the purchaser agrees to be bound by the terms of our partnership agreement and, pursuant to the terms of our partnership agreement, each holder of common units consents to various actions contemplated in the partnership agreement and conflicts of interest that might otherwise be considered a breach of fiduciary or other duties under applicable state law.

For a more detailed description of the conflicts of interest and fiduciary duties of our general partner, please read “Conflicts of Interest and Fiduciary Duties.”

8

Table of Contents

The Offering

| Common units offered to the public | 12,500,000 common units; 14,375,000 common units if the underwriters’ option to purchase additional common units is exercised in full. | |

| Units outstanding after this offering | 21,084,349 common units and 10,222,715 subordinated units, representing 66.0% and 32.0%, respectively, limited partner interests in us. The general partner will own 638,920 general partner units. | |

| Use of proceeds | We intend to use the net proceeds of approximately $235.0 million from this offering, after deducting $15.0 million of underwriting discounts, but before paying offering expenses, to: | |

| • pay approximately $3.9 million of fees and expenses associated with the offering and related formation transactions, including a structuring fee payable to Lehman Brothers Inc. for evaluation, analysis and structuring of our partnership; | ||

| • distribute $71.7 million in cash to subsidiaries of NiSource as reimbursement for capital expenditures related to the Columbia Gulf assets incurred by subsidiaries of NiSource prior to the closing of this offering; | ||

| • retire approximately $31.1 million of indebtedness owed to a subsidiary of NiSource; | ||

| • purchase approximately $37.0 million of qualifying investment grade securities, which will be assigned as collateral to secure the term loan portion of our credit facility; | ||

| • use approximately $64.0 million to fund working capital; and | ||

• use the remaining amount of $27.3 million to offset identified maintenance capital expenditures, including an amount to offset costs we expect to incur in connection withgovernment-mandated pipeline improvements through 2010. | ||

| We also anticipate that we will borrow approximately $37.0 million in term debt and $163.0 million in revolving debt upon the closing of this offering, and we will distribute the net proceeds of such borrowings (or approximately $198.0 million, net of debt issuance costs) to subsidiaries of NiSource, which distribution will be made in partial consideration of the assets contributed to us upon the closing of this offering. | ||

| If the underwriters’ option to purchase an additional 1,875,000 common units is exercised in full, we will (1) use the net proceeds of approximately $35.1 million to purchase an equivalent amount of qualifying investment grade securities and (2) borrow an additional amount under the term loan portion of our credit facility equal to the net proceeds to be received from the exercise of the underwriters’ option. The qualifying securities purchased will be assigned as collateral to secure such additional term loan borrowings. The proceeds of the additional term loan borrowings will be used to redeem from a subsidiary of NiSource a number of common units equal to the number of common units issued upon |

9

Table of Contents

| exercise of the underwriters’ option, at a price per common unit equal to the proceeds per common unit before expenses but after underwriting discounts and a structuring fee. | ||

| Cash distributions | We will make an initial quarterly distribution of $0.30 per common unit ($1.20 per common unit on an annualized basis) to the extent we have sufficient cash from operations after establishment of cash reserves and payment of fees and expenses, including payments to our general partner and its affiliates. Our ability to pay cash distributions at this initial distribution rate is subject to various restrictions and other factors described in more detail under the caption “Our Cash Distribution Policy and Restrictions on Distributions.” | |

| We will pay investors in this offering a prorated distribution for the first quarter during which we are a publicly traded partnership. Such distribution will cover the period from the closing date of this offering to and including March 31, 2008. We expect to pay this cash distribution on or about May 15, 2008. | ||

| Our partnership agreement requires us to distribute all of our cash on hand at the end of each quarter, less reserves established by our general partner. We refer to this cash as “available cash,” and we define its meaning in our partnership agreement and in the glossary of terms attached as Appendix D. Our partnership agreement also requires that we distribute all of our available cash from operating surplus each quarter in the following manner: | ||

• first, 98% to the holders of common units and 2% to our general partner, until each common unit has received a minimum quarterly distribution of $0.30 plus any arrearages from prior quarters; | ||

• second, 98% to the holders of subordinated units and 2% to our general partner, until each subordinated unit has received a minimum quarterly distribution of $0.30; and | ||

• third, 98% to all unitholders, pro rata, and 2% to our general partner, until each unit has received a distribution of $0.345. | ||

| If cash distributions to our unitholders exceed $0.345 per common unit in any quarter, our general partner will receive, in addition to distributions on its 2% general partner interest, increasing percentages, up to 50%, of the cash we distribute in excess of that amount. We refer to these distributions as “incentive distributions.” Please read “Provisions of Our Partnership Agreement Relating to Cash Distributions.” | ||

| The amount of pro forma available cash generated during the year ended December 31, 2006 would have been sufficient to allow us to pay approximately 55% of the minimum quarterly distribution on our common units, but no quarterly distributions on our subordinated units during that period. The amount of pro forma available cash generated during the twelve months ended September 30, 2007 would have been sufficient to allow us to pay approximately 81% of the minimum quarterly distribution on our our common units, but no quarterly distributions on our |

10

Table of Contents

| subordinated units during that period. For a calculation of our ability to make distributions to unitholders based on our pro forma results for 2006 and the twelve months ended September 30, 2007, please read “Our Cash Distribution Policy and Restrictions on Distributions — Unaudited Pro Forma Cash Available for Distribution for the Year Ended December 31, 2006 and the Twelve Months Ended September 30, 2007.” | ||

| We believe that, based on the estimates contained and the assumptions listed under the caption “Our Cash Distribution Policy and Restrictions on Distributions — Minimum Estimated Cash Available for Distribution for the Twelve-Month Period Ending March 31, 2009,” we will have sufficient cash available for distribution to make cash distributions for the four quarters ending March 31, 2009 at the initial distribution rate of $0.30 per common unit per quarter ($1.20 per common unit on an annualized basis) on all common units and subordinated units. | ||

| Subordinated units | Subsidiaries of NiSource will initially own all of our subordinated units. The principal difference between our common units and subordinated units is that in any quarter during the subordination period, holders of the subordinated units are entitled to receive the minimum quarterly distribution of $0.30 per unit only after the common units have received the minimum quarterly distribution plus any arrearages in the payment of the minimum quarterly distribution from prior quarters. Subordinated units will not accrue arrearages. The subordination period will end on the first business day after we have earned and paid at least $0.30 on each outstanding limited partner unit and general partner unit for any three consecutive, non-overlapping four quarter periods ending on or after March 31, 2011. The subordination period also will end upon the removal of our general partner other than for cause if the units held by our general partner and its affiliates are not voted in favor of such removal. | |

| When the subordination period ends, all remaining subordinated units will convert into common units on a one-for-one basis, and the common units will no longer be entitled to arrearages. Please read “Provisions of Our Partnership Agreement Related to Cash Distributions — Subordination Period.” | ||

| Early conversion of subordinated units | Alternatively, the subordination period will end on the first business day after we have earned and paid at least $1.80 (150% of the annualized minimum quarterly distribution) on each outstanding limited partner unit and general partner unit for any four quarter period ending on or after March 31, 2009. Please read “Provisions of Our Partnership Agreement Related to Cash Distributions — Subordination Period.” | |

| General Partner’s right to reset the target distribution levels | Our general partner has the right, at a time when there are no subordinated units outstanding and it has received incentive distributions at the highest level to which it is entitled (48%) for each of the prior four consecutive fiscal quarters, to reset the initial cash target distribution levels at higher levels based on the |

11

Table of Contents

| distribution at the time of the exercise of the reset election. Following a reset election by our general partner, the minimum quarterly distribution amount will be reset to an amount equal to the average cash distribution amount per common unit for the two fiscal quarters immediately preceding the reset election (such amount is referred to as the “reset minimum quarterly distribution”) and the target distribution levels will be reset to correspondingly higher levels based on the same percentage increases above the reset minimum quarterly distribution amount as in our current target distribution levels. | ||

| In connection with resetting these target distribution levels, our general partner will be entitled to receive Class B units. The Class B units will be entitled to the same cash distributions per unit as our common units and will be convertible into an equal number of common units. The number of Class B units to be issued will be equal to that number of common units whose aggregate quarterly cash distributions equaled the average of the distributions to our general partner on the incentive distribution rights in the prior two quarters. For a more detailed description of our general partner’s right to reset the target distribution levels upon which the incentive distribution payments are based and the concurrent right of our general partner to receive Class B units in connection with this reset, please read “Provisions of Our Partnership Agreement Related to Cash Distributions — General Partner’s Right to Reset Incentive Distribution Levels.” | ||

| Issuance of additional units | We can issue an unlimited number of units without the consent of our unitholders. Please read “Units Eligible for Future Sale” and “The Partnership Agreement — Issuance of Additional Securities.” | |

| Limited voting rights | Our general partner will manage and operate us. Unlike the holders of common stock in a corporation, you will have only limited voting rights on matters affecting our business. You will have no right to elect our general partner or its directors on an annual or other continuing basis. Our general partner may not be removed except by a vote of the holders of at least 662/3% of the outstanding units, including any units owned by our general partner and its affiliates, voting together as a single class. Upon consummation of this offering, our general partner and its affiliates will own an aggregate of approximately 60.0% of our common and subordinated units. This will give NiSource the ability to prevent our general partner’s involuntary removal. Please read “The Partnership Agreement — Voting Rights.” | |

| Limited call right | If at any time our general partner and its affiliates own more than 80% of the outstanding common units, our general partner has the right, but not the obligation, to purchase all of the remaining common units at a price not less than the then-current market price of the common units. | |

| Eligible Holders and redemptions | Only Eligible Holders will be entitled to receive distributions or be allocated income or loss from us. Eligible Holders are: | |

| • individuals or entities subject to United States federal income taxation on the income generated by us; or |

12

Table of Contents

| • entities not subject to United States federal taxation on the income generated by us, so long as all of the entity’s owners are subject to such taxation. | ||

| We have the right, which we may assign to any of our affiliates, but not the obligation, to redeem all of the common and subordinated units of any holder that is not an Eligible Holder or that has failed to certify or has falsely certified that such holder is an Eligible Holder. The purchase price for such redemption would be equal to the lower of the holder’s purchase price and the then-current market price of the units. The redemption price will be paid in cash or by delivery of a promissory note, as determined by our general partner. | ||

| Please read “Description of the Common Units — Transfer of Common Units” and “The Partnership Agreement — Non-Citizen Assignees; Redemption.” | ||

| Estimated ratio of taxable income to distributions | We estimate that if you own the common units you purchase in this offering through the record date for distributions for the period ending December 31, 2010, you will be allocated, on a cumulative basis, an amount of federal taxable income for that period that will be % or less of the cash distributed to you with respect to that period. For example, if you receive an annual distribution of $1.20 per unit, we estimate that your average allocable federal taxable income per year will be no more than $ per unit. Please read “Material Tax Consequences — Tax Consequences of Unit Ownership — Ratio of Taxable Income to Distributions.” | |

| Material tax consequences | For a discussion of other material federal income tax consequences that may be relevant to prospective unitholders who are individual citizens or residents of the United States, please read “Material Tax Consequences.” | |

| Exchange listing | We intend to apply to list our common units on the New York Stock Exchange under the symbol “NIA.” |

13

Table of Contents

Summary Historical and Pro Forma Financial and Operating Data

The following table shows (i) summary historical financial and operating data of Columbia Gulf and (ii) summary pro forma financial data of NiSource Energy Partners, L.P. for the periods and as of the dates indicated. The summary historical financial data of Columbia Gulf as of December 31, 2005 and 2006 and for the years ended December 31, 2004, 2005 and 2006 are derived from the historical audited financial statements of Columbia Gulf appearing elsewhere in this prospectus. The summary historical financial data for Columbia Gulf as of September 30, 2007 and for the nine months ended September 30, 2006 and 2007 are derived from the historical unaudited financial statements of Columbia Gulf appearing elsewhere in this prospectus. The table should also be read together with “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

The summary pro forma financial data of NiSource Energy Partners, L.P. for the year ended December 31, 2006, and as of and for the nine months ended September 30, 2007 are derived from the unaudited pro forma financial statements of NiSource Energy Partners, L.P. included elsewhere in this prospectus. The pro forma adjustments have been prepared as if certain transactions to be effected at the closing of this offering had taken place on September 30, 2007, in the case of the pro forma balance sheet, and as of January 1, 2006, in the case of the pro forma statements of operations for the year ended December 31, 2006, and for the nine months ended September 30, 2007. These transactions include:

| • | Columbia Gulf’s distribution of accounts receivable of $62.4 million to NiSource; | |

| • | Our receipt of $250.0 million in gross proceeds from the issuance and sale of 12,500,000 common units to the public; | |

| • | Our borrowing approximately $37.0 million in term debt and $163.0 million in revolving debt under our new $250.0 million credit facility; | |

| • | Our use of proceeds from this offering and related borrowings to pay transaction fees and expenses and underwriting commissions, retire assumed indebtedness, reimburse subsidiaries of NiSource for certain capital expenditures, make distributions to subsidiaries of NiSource, fund working capital and anticipated capital expenditures, and purchase qualifying investment grade securities; and | |

| • | The disposition of certain offshore assets currently owned by Columbia Gulf. |

The following table includes the non-GAAP financial measure of EBITDA. We define our EBITDA as net income plus interest expense (net of a non-cash allowance for funds used during construction, or AFUDC), income taxes and depreciation and amortization, less interest income and other, net. For a reconciliation of EBITDA to its most directly comparable financial measures calculated and presented in accordance with GAAP, please read “— Non-GAAP Financial Measures.”

| NiSource Energy | ||||||||||||||||||||||||||||

| Partners, L.P. Pro Forma | ||||||||||||||||||||||||||||

| Columbia Gulf | Nine Months | |||||||||||||||||||||||||||

| Nine Months Ended | Year Ended | Ended | ||||||||||||||||||||||||||

| Year Ended December 31, | September 30, | December 31, | September 30, | |||||||||||||||||||||||||

| 2004 | 2005 | 2006 | 2006 | 2007 | 2006 | 2007 | ||||||||||||||||||||||

| (In millions, except per unit and operating data) | ||||||||||||||||||||||||||||

Statement of Operations Data: | ||||||||||||||||||||||||||||

| Total operating revenues | $ | 127.0 | $ | 116.1 | $ | 123.3 | $ | 90.8 | $ | 99.6 | $ | 117.3 | $ | 94.5 | ||||||||||||||

| Operating expenses: | ||||||||||||||||||||||||||||

| Operation and maintenance | 55.7 | 51.3 | 61.2 | 41.2 | 44.4 | 55.1 | 38.4 | |||||||||||||||||||||

| Depreciation and amortization | 23.2 | 22.2 | 22.0 | 16.5 | 16.4 | 19.1 | 14.8 | |||||||||||||||||||||

| Other taxes | 7.8 | 8.5 | 8.1 | 6.0 | 6.2 | 8.1 | 6.2 | |||||||||||||||||||||

| Total operating expenses | 86.7 | 82.0 | 91.3 | 63.7 | 67.0 | 82.3 | 59.4 | |||||||||||||||||||||

| Operating income | 40.3 | 34.1 | 32.0 | 27.1 | 32.6 | 35.0 | 35.1 | |||||||||||||||||||||

| Other income (deductions): | ||||||||||||||||||||||||||||

| Interest expense (net of AFUDC) | (5.4 | ) | (5.0 | ) | (2.7 | ) | (2.2 | ) | (1.8 | ) | (15.2 | ) | (10.7 | ) | ||||||||||||||

| Interest income | 0.4 | 0.6 | 0.5 | 0.5 | — | 1.5 | 0.8 | |||||||||||||||||||||

| Other, net | — | 0.5 | 0.7 | 0.7 | — | 0.7 | — | |||||||||||||||||||||

| Income taxes | (13.1 | ) | (11.7 | ) | (12.2 | ) | (9.2 | ) | (10.7 | ) | (0.1 | ) | (0.1 | ) | ||||||||||||||

| Net income | $ | 22.2 | $ | 18.5 | $ | 18.3 | $ | 16.9 | $ | 20.1 | $ | 21.9 | $ | 25.1 | ||||||||||||||

| Net income per limited partners’ unit | ||||||||||||||||||||||||||||

| Common unit | $ | 1.02 | $ | 0.90 | ||||||||||||||||||||||||

| Subordinated unit | — | 0.55 | ||||||||||||||||||||||||||

14

Table of Contents

| NiSource Energy | ||||||||||||||||||||||||||||

| Partners, L.P. Pro Forma | ||||||||||||||||||||||||||||

| Columbia Gulf | Nine Months | |||||||||||||||||||||||||||

| Nine Months Ended | Year Ended | Ended | ||||||||||||||||||||||||||

| Year Ended December 31, | September 30, | December 31, | September 30, | |||||||||||||||||||||||||

| 2004 | 2005 | 2006 | 2006 | 2007 | 2006 | 2007 | ||||||||||||||||||||||

| (In millions, except per unit and operating data) | ||||||||||||||||||||||||||||

Balance Sheet Data (at period end): | ||||||||||||||||||||||||||||

| Total Assets | $ | 716.0 | $ | 763.1 | $ | 783.3 | $ | 841.2 | ||||||||||||||||||||

| Net property plant and equipment | 305.5 | 310.6 | 321.5 | 321.5 | ||||||||||||||||||||||||

Long-term debt-affiliated, excluding amounts due within one year | 67.9 | 67.9 | 67.9 | 265.9 | ||||||||||||||||||||||||

| Total capitalization | 552.6 | 556.1 | 576.2 | 701.8 | ||||||||||||||||||||||||

Other Financial Data: | ||||||||||||||||||||||||||||

| Net cash provided by operating activities | $ | 45.3 | $ | 51.0 | $ | 40.1 | $ | 26.7 | $ | 20.0 | $ | 43.7 | $ | 25.0 | ||||||||||||||

| EBITDA | 63.5 | 56.3 | 54.0 | 43.6 | 49.0 | 54.1 | 49.9 | |||||||||||||||||||||

| Maintenance capital expenditures(1) | 7.0 | 31.4 | 22.2 | 13.2 | 11.6 | 22.2 | 11.6 | |||||||||||||||||||||

| Expansion capital expenditures(1) | — | 0.1 | 2.9 | 1.1 | 10.5 | 2.9 | 10.5 | |||||||||||||||||||||

Columbia Gulf Operating Data: | ||||||||||||||||||||||||||||

Mainline: | ||||||||||||||||||||||||||||

| Transportation capacity (Bcf/d)(2) | 2.156 | 2.156 | 2.156 | 2.156 | 2.156 | |||||||||||||||||||||||

| Contracted firm capacity (Bcf/d)(3) | 2.453 | 2.177 | 2.266 | 2.245 | 2.471 | |||||||||||||||||||||||

| Transported volumes (Bcf) | 523.6 | 506.7 | 519.7 | 392.3 | 477.4 | |||||||||||||||||||||||

Laterals (East and West): | ||||||||||||||||||||||||||||

| Transportation capacity (Bcf/d)(4) | 2.157 | 2.157 | 2.157 | 2.157 | 2.157 | |||||||||||||||||||||||

| Contracted firm capacity (Bcf/d) | 0.616 | 0.589 | 0.680 | 0.634 | 0.870 | |||||||||||||||||||||||

| Transported volumes (Bcf) | 428.9 | 422.1 | 379.7 | 291.3 | 247.6 | |||||||||||||||||||||||

| (1) | Maintenance capital expenditures are capital expenditures made to replace partially or fully depreciated assets, to maintain the existing operating capacity of our assets and to extend their useful lives, or other capital expenditures that are incurred in maintaining existing system volumes and related cash flows. Expansion capital expenditures are made to acquire additional assets to grow our business, to expand and upgrade our systems and facilities, and to construct or acquire similar systems or facilities. This includes projects designed to reduce costs or enhance revenues. | |

| (2) | Represents one-way peak-design capacity from Rayne, Louisiana to Leach, Kentucky. | |

| (3) | Our contracted firm capacity exceeds our one-way peak-design capacity during the indicated periods as a result of our ability to transport natural gas in multiple directions on our pipeline system. | |

| (4) | Represents the maximum combined peak-design capacity of the two laterals — East (1.054 Bcf/d) and West(1.103 Bcf/d). |

We define our EBITDA as net income plus interest expense (net of AFUDC), income taxes and depreciation and amortization, less interest income and other, net. EBITDA is used as a supplemental financial measure by management and by external users of our financial statements, such as investors and commercial banks, to assess:

| • | the financial performance of our assets without regard to financing methods, capital structure or historical cost basis; | |

| • | the ability of our assets to generate cash sufficient to pay interest on our indebtedness and to make distributions to our partners; and | |

| • | our operating performance and return on invested capital as compared to those of other publicly traded limited partnerships that own energy infrastructure assets, without regard to their financing methods and capital structure. |

EBITDA should not be considered an alternative to net income, operating income, net cash provided by operating activities or any other measure of financial performance or liquidity presented in accordance with GAAP. EBITDA excludes some, but not all, items that affect net income and operating income and these

15

Table of Contents

measures may vary among other companies. Therefore, EBITDA as presented may not be comparable to similarly titled measures of other companies.

The following tables present reconciliations of the non-GAAP financial measure of EBITDA to the respective GAAP financial measures of net income and net cash provided (used) by operating activities on a historical basis and on a pro forma basis as adjusted for this offering.

| NiSource Energy Partners, L.P. | ||||||||||||||||||||||||||||

| Pro Forma | ||||||||||||||||||||||||||||

| Columbia Gulf | Nine Months | |||||||||||||||||||||||||||

| Nine Months Ended | Year Ended | Ended | ||||||||||||||||||||||||||

| Year Ended December 31, | September 30, | December 31, | September 30, | |||||||||||||||||||||||||

| 2004 | 2005 | 2006 | 2006 | 2007 | 2006 | 2007 | ||||||||||||||||||||||

| (In millions) | ||||||||||||||||||||||||||||

Reconciliation of Non-GAAP | ||||||||||||||||||||||||||||

“EBITDA” to GAAP “Net income” | ||||||||||||||||||||||||||||

| Net income | $ | 22.2 | $ | 18.5 | $ | 18.3 | $ | 16.9 | $ | 20.1 | $ | 21.9 | $ | 25.1 | ||||||||||||||

| Add: | ||||||||||||||||||||||||||||

| Interest expense (net of AFUDC) | 5.4 | 5.0 | 2.7 | 2.2 | 1.8 | 15.2 | 10.7 | |||||||||||||||||||||

| Income taxes | 13.1 | 11.7 | 12.2 | 9.2 | 10.7 | 0.1 | 0.1 | |||||||||||||||||||||

| Depreciation and amortization | 23.2 | 22.2 | 22.0 | 16.5 | 16.4 | 19.1 | 14.8 | |||||||||||||||||||||

| Less: | ||||||||||||||||||||||||||||

| Interest income | 0.4 | 0.6 | 0.5 | 0.5 | — | 1.5 | 0.8 | |||||||||||||||||||||

| Other, net | — | 0.5 | 0.7 | 0.7 | — | 0.7 | — | |||||||||||||||||||||

EBITDA | $ | 63.5 | $ | 56.3 | $ | 54.0 | $ | 43.6 | $ | 49.0 | $ | 54.1 | $ | 49.9 | ||||||||||||||

Reconciliation of Non-GAAP | ||||||||||||||||||||||||||||

“EBITDA” to GAAP “Net cash provided by operating activities” | ||||||||||||||||||||||||||||

| Net cash provided by operating activities | $ | 45.3 | $ | 51.0 | $ | 40.1 | $ | 26.7 | $ | 20.0 | $ | 43.7 | $ | 25.0 | ||||||||||||||

| Less: | ||||||||||||||||||||||||||||

| Interest income | 0.4 | 0.6 | 0.5 | 0.5 | — | 1.5 | 0.8 | |||||||||||||||||||||

| Add: | ||||||||||||||||||||||||||||

| Interest expense (net of AFUDC) | 5.4 | 5.0 | 2.7 | 2.2 | 1.8 | 15.2 | 10.7 | |||||||||||||||||||||

| Income taxes paid | 10.3 | 10.7 | 9.4 | 9.2 | 10.0 | 0.1 | 0.1 | |||||||||||||||||||||

| Other | 1.0 | 1.1 | (4.3 | ) | (5.1 | ) | (2.8 | ) | (10.0 | ) | (5.1 | ) | ||||||||||||||||

| Changes in operating working capital | 1.9 | (10.9 | ) | 6.6 | 11.1 | 20.0 | 6.6 | 20.0 | ||||||||||||||||||||

EBITDA | $ | 63.5 | $ | 56.3 | $ | 54.0 | $ | 43.6 | $ | 49.0 | $ | 54.1 | $ | 49.9 | ||||||||||||||

16

Table of Contents

Limited partner interests are inherently different from capital stock of a corporation, although many of the business risks to which we are subject are similar to those that would be faced by a corporation engaged in similar businesses. You should consider carefully the following risk factors together with all of the other information included in this prospectus in evaluating an investment in our common units.

If any of the following risks were actually to occur, our business, financial condition, results of operations and cash flows could be materially adversely affected. In that case, we might not be able to make distributions on our common units, the trading price of our common units could decline and you could lose all or part of your investment.

We may not have sufficient cash from operations following the establishment of cash reserves and payment of fees and expenses, including cost reimbursements to our general partner, to enable us to make cash distributions to holders of our common units and subordinated units at the initial distribution rate under our cash distribution policy.

In order to make cash distributions at our initial distribution rate of $0.30 per common unit per complete quarter, or $1.20 per unit per year, we will require available cash of approximately $9.6 million per quarter, or $38.3 million per year, based on the number of common units and subordinated units outstanding immediately after completion of this offering, whether or not the underwriters exercise their option to purchase additional common units. We may not have sufficient available cash from operating surplus each quarter to enable us to make cash distributions at the initial distribution rate under our cash distribution policy. The amount of cash we can distribute on our units principally depends upon the amount of cash we generate from our operations, which will fluctuate based on, among other things:

| • | the rates we charge for our transportation services, the volume of capacity under contract and the volumes of natural gas our customers transport; | |

| • | the demand for natural gas in the markets served by our system and the quantities of natural gas available for transport on our system; | |

| • | legislative or regulatory action affecting the demand for natural gas, the supply of natural gas, the rates we can charge, how we contract for services, our existing contracts, our operating costs and our operating flexibility; | |

| • | the imposition of requirements by state agencies that materially reduce the demand of our customers, such as local distribution companies and power generators, for our pipeline services; | |

| • | the commodity price of natural gas, which could reduce the quantities of natural gas available for transport if prolonged low natural gas prices cause diminished natural gas exploration and production activity in specific regions of the United States, particularly on the Gulf Coast and in the Gulf of Mexico; | |

| • | the creditworthiness of our customers — if a customer files for bankruptcy protection, there is no assurance we will be kept whole for the revenue that would have been realized had the contract been honored for its entire term; | |

| • | the level of our operating and maintenance and general and administrative costs; | |

| • | the level of capital expenditures we incur to maintain our assets; | |

| • | regulatory and economic limitations on the development of LNG import terminals in the Gulf Coast region; and | |

| • | successful development of LNG import terminals in the eastern or northeastern United States, which could reduce the need for natural gas to be transported on the Columbia Gulf pipeline system. |

17

Table of Contents

In addition, the actual amount of cash we will have available for distribution will depend on other factors, some of which are beyond our control, including:

| • | unanticipated required capital expenditures; | |

| • | our debt service requirements and other liabilities; | |

| • | fluctuations in our working capital needs; | |

| • | our ability to borrow funds and access capital markets; | |

| • | restrictions on distributions contained in our debt agreements; and | |

| • | the amount of cash reserves established by our general partner. |

For a description of additional restrictions and factors that may affect our ability to make cash distributions, please read “Our Cash Distribution Policy and Restrictions on Distributions.”

On a pro forma basis we would not have had sufficient cash available for distribution to pay the full minimum quarterly distribution on all units for the year ended December 31, 2006 and the twelve months ended September 30, 2007, respectively.

The amount of available cash we need to pay the minimum quarterly distribution for four quarters on all of our units to be outstanding immediately after this offering is approximately $38.3 million. The amount of pro forma available cash generated during the year ended December 31, 2006 would have been sufficient to allow us to pay approximately 55% of the minimum quarterly distributions on our common units, but it would not have been sufficient to allow us to pay any distributions on our subordinated units during that period. The amount of pro forma available cash generated during the twelve months ended September 30, 2007 would have been sufficient to allow us to pay approximately 81% of the minimum quarterly distribution on our common units, but no quarterly distributions on our subordinated units during that period. For a calculation of our ability to make distributions to unitholders based on our pro forma results for 2006 and the twelve months ended September 30, 2007, please read “Our Cash Distribution Policy and Restrictions on Distributions.”

The assumptions underlying our minimum estimated cash available for distribution we include in “Our Cash Distribution Policy and Restrictions on Distributions” are inherently uncertain and are subject to significant business, economic, financial, regulatory and competitive risks and uncertainties that could cause actual results to differ materially from those estimated.

Our estimate of cash available for distribution set forth in “Our Cash Distribution Policy and Restrictions on Distributions” has been prepared by management and we have not received an opinion or report on it from our or any other independent auditor. The assumptions underlying this estimate are inherently uncertain and are subject to significant business, economic, financial, regulatory and competitive risks and uncertainties that could cause actual results to differ materially from those assumed. For example, as discussed in “— Minimum Estimated Cash Available for Distribution for the Twelve-Month Period Ending March 31, 2009,” we expect to incur approximately $24.1 million of maintenance capital expenditures for the twelve months ending March 31, 2009, $8.5 million of which we expect to be recurring in nature. While we believe our assumption regarding the amount of recurring maintenance capital expenditures is reasonable, we have incurred total annual maintenance capital expenditures in amounts significantly in excess of $8.5 million per year in the past, including $22.2 million of total maintenance capital expenditures in 2006 and $31.4 million of total maintenance capital expenditures in 2005. If our future maintenance capital expenditures are higher than expected, our anticipated results could be adversely impacted. If we do not achieve our anticipated results, we may not be able to pay the full minimum quarterly distribution or any amount on our common units or subordinated units, in which event the market price of our common units may decline materially.

18

Table of Contents

The amount of cash we have available for distribution to holders of our common units and subordinated units depends primarily on our cash flow and not solely on profitability, which may prevent us from making cash distributions during periods when we record net income.

You should be aware that the amount of cash we have available for distribution depends primarily upon our cash flow, including cash flow from financial reserves and working capital or other borrowings, and not solely on profitability, which will be affected by non-cash items. As a result, we may make cash distributions during periods when we record net losses for financial accounting purposes and may not make cash distributions during periods when we record net earnings for financial accounting purposes.

Our natural gas transportation operations are subject to regulation by the FERC, which could have an adverse impact on our ability to establish transportation rates that would allow us to recover the full cost of operating our pipelines, including a reasonable return, and our ability to make distributions to you.

Our interstate natural gas transportation operations are subject to federal, state and local regulatory authorities. Specifically, our natural gas pipeline system is subject to regulation by the FERC under the Natural Gas Act of 1938 (NGA). The federal regulation extends to such matters as:

| • | transportation of natural gas; | |

| • | rates, operating terms and conditions of service; | |

| • | the types of services we may offer to our customers; | |

| • | construction of new facilities; | |

| • | acquisition, extension or abandonment of services or facilities; | |

| • | accounts and records; | |

| • | commercial relationships and communications with affiliated companies involved in certain aspects of the natural gas business; and | |

| • | the initiation and discontinuation of services. |

We may only charge rates that we have been authorized to charge by the FERC. In addition, the FERC prohibits natural gas companies from unduly preferring or unreasonably discriminating against any person with respect to pipeline rates or terms and conditions of service.

The maximum recourse rates that may be charged by our pipeline for its transportation services are established through the FERC’s ratemaking process, and those recourse rates, as well as the terms and conditions of service, are set forth in our FERC-approved tariff. Pursuant to the FERC’s jurisdiction over rates, existing rates may be challenged by complaint, proposed rate increases may be challenged by protest, and either may be challengedsua sponteby the FERC. Any successful challenge against our rates could have an adverse impact on our revenues associated with providing transportation services. Generally, the maximum filed recourse rates for interstate pipelines are based on the cost of service plus an approved return on equity, which may be determined through the use of a proxy group of similarly situated companies. On July 19, 2007, the FERC issued a proposed policy statement addressing the issue of the proxy groups it will use to decide the return on equity of natural gas pipelines. The FERC uses a discounted cash flow model that incorporates the use of proxy groups to develop a range of reasonable returns earned on equity interests in companies with corresponding risks. The FERC then assigns a rate of return on equity within that range to reflect specific risks of that pipeline when compared to the proxy group companies. The proposed policy statement describes the FERC’s intention to allow the use of master limited partnerships in proxy groups, with certain restrictions, which could lower the return that would otherwise be allowed. The FERC has requested comments on the proposed policy. Please read “Business — FERC Regulation — FERC Policy Statement on Proxy Groups for Rates of Return Determinations.” Other key determinants in the ratemaking process are costs of providing service, including an income tax allowance, allowed rate of return and volume throughput and contractual capacity commitment assumptions. The allowed rate of return must be approved by the FERC as part of the resolution of each rate case. The maximum applicable recourse rates and terms and conditions for service are

19

Table of Contents

found in each pipeline’s FERC-approved tariff. Rate design and the allocations of costs can also impact a pipeline’s profitability. Our interstate pipelines may also use “negotiated rates” which, in theory, could involve rates above or below the “recourse rate.” A prerequisite for having the right to agree to negotiated rates is that the negotiated rate customers must have had the option to take service under the pipeline’s maximum recourse rates.

Finally, we cannot give any assurance regarding the likely future regulations under which we will operate our natural gas transportation business or the effect such regulation could have on our business, financial condition, results of operations and ability to make distributions to you.

We could be subject to penalties and fines if we fail to comply with FERC regulations.

Should we fail to comply with all applicable FERC-administered statutes, rules, regulations and orders, we could be subject to substantial penalties and fines. Under the Energy Policy Act of 2005, the FERC has civil penalty authority under the NGA to impose penalties for current violations of up to $1,000,000 per day for each violation, to revoke existing certificate authority, and to order disgorgement of profits associated with any violation. Columbia Gulf and Columbia Gas Transmission are currently cooperating with the FERC on an informal non-public investigation in connection with an audit initiated in 2003 that covers a period beginning in 1999 that evaluates whether Columbia Gulf and Columbia Gas Transmission properly followed the FERC’s regulations. We cannot predict what the result of that audit will be, but the FERC has indicated that it may seek to impose penalties under the NGPA. Please read “Business — FERC Regulation.”

The outcome of certain rate cases involving the FERC policy statements is uncertain and could affect the amount of any allowance our system can include for income taxes in establishing its rates for service, which would in turn impact our revenues.