1Q 2009 Earnings Call

May 8, 2009

Exhibit 99.2

The following information contains forward-looking statements, including forward-looking statements

within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward-looking

statements include, but are not limited to, statements concerning Colfax's plans, objectives,

expectations and intentions and other statements that are not historical or current facts. Forward-

looking statements are based on Colfax's current expectations and involve risks and uncertainties that

could cause actual results to differ materially from those expressed or implied in such forward-looking

statements. Factors that could cause Colfax's results to differ materially from current expectations

include, but are not limited to factors detailed in Colfax's reports filed with the U.S. Securities and

Exchange Commission as well as its Annual Report on Form 10-K under the caption “Risk Factors”. In

addition, these statements are based on a number of assumptions that are subject to change. This

presentation speaks only as of this date. Colfax disclaims any duty to update the information herein.

Forward-Looking Statements

1

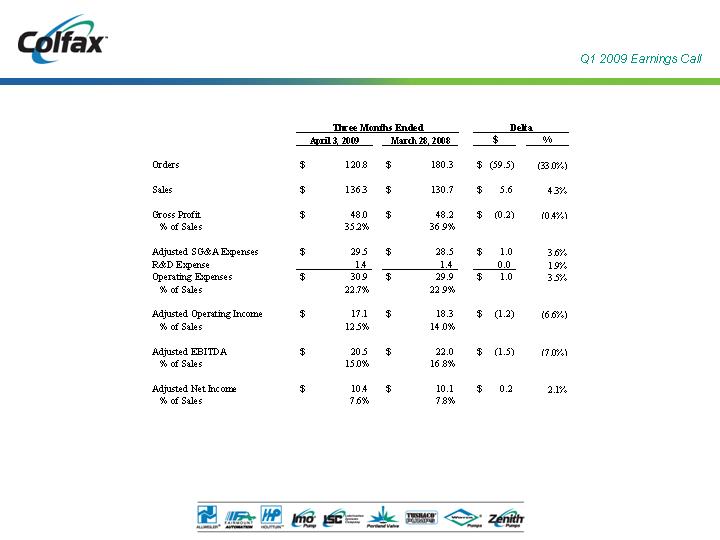

Adjusted net income of $10.4 million (24 cents per share), an increase of 2.1% including

negative currency effects of 5 cents per share

Net sales of $136.3 million, an increase of 4.3% (organic growth of 17.9%)

Adjusted operating income of $17.1 million, a decrease of 6.6% including negative

currency effects of $3.4 million

Adjusted EBITDA of $20.5 million, a decrease of 7.0% including negative currency

effects of $3.7 million

First quarter orders of $120.8 million, a decrease of 33.0% (organic decrease of 25.5%)

Backlog of $305.6 million

Solid performance in Q1 2009

Q1 2009 Highlights

2

Solid Results for Q1 2009

Organic sales up 18% year over year, down 13% sequentially (Q4 and Q1 seasonally

strongest and weakest, respectively)

Supported by strong backlog entering 2009

Organic sales in four strategic end markets increased 24% to 45%

Commercial marine – up 45%

Oil & gas – up 25%

Power generation – up 24%

Navy – up 32%

General industrial – down 2%

Strong growth in four strategic end markets

Q1 2009 Highlights Continued

3

Global Business Conditions Continued to Weaken in Q1

Organic orders declined 25% year over year, down 3% sequentially

Decline driven by commercial marine (down 57%) and general industrial (down 28%)

Decline in commercial marine orders includes cancellations of $6 million

Weakness in most general industrial submarkets including distribution, chemical

and building products

Power generation – down 12% (due to project timing)

Strong organic order growth in oil & gas (up 22%) and global navy (up 75%)

Weakening economy impacting orders

Q1 2009 Highlights Continued

4

Rightsizing to support declining orders

Organic sales growth over last 3 years (12%, 14% and 14%) supported by CBS initiatives

Able to be flexible in a declining market environment

Initial steps include reduction in temporary and contract workers

Initiated cost reductions worldwide (expect savings of $11 million in 2009)

Reduced headcount by about 5% (approximately 120 associates as of May 1)

European furlough programs begun (approximately 628 associates as of May 1)

Consolidated Aberdeen, NC facility

Severance and asset impairment costs minimal ($0.7 million)

Structuring business to match current conditions

Profit Protection Plans

5

Expect to maintain margins

Discretionary spending curtailed

Evaluating additional cost savings measures; have contingency plans in place

Based on visibility of 4 to 6 months, able to take preemptive actions as needed

CBS activity continues in all areas

Structuring business to match current conditions

Profit Protection Plans Continued

6

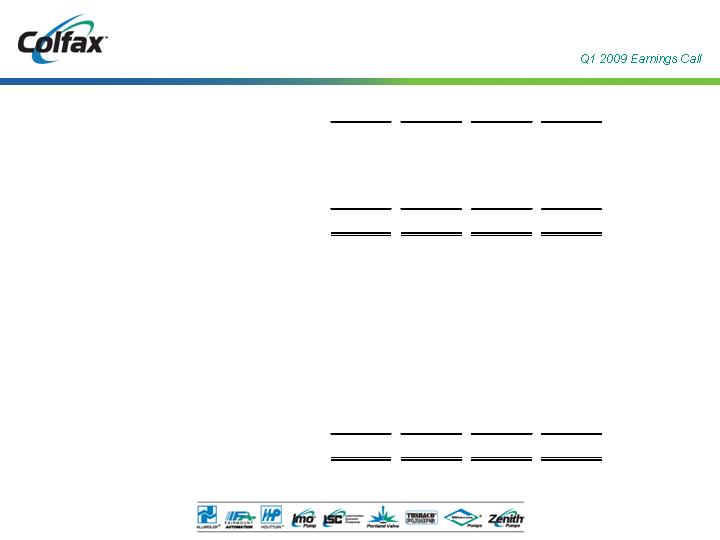

2009

Q1

2008

Q1

-

2008

2007

2006

2005

$720.0

$600.0

$480.0

$360.0

$240.0

$120.0

$0.0

$136.3

$130.7

$604.9

$506.3

$393.6

$345.5

15.0%

16.8%

17.5%

17.4%

16.3%

15.9%

% Margin

--

--

--

--

19.5%

4.5%

1.1%

13.9%

4.3%

--

28.6%

13.9%

Total Growth

(13.6)%

--

7.1%

0.8%

--

FX Translation

--

--

8.0%

1.4%

--

Acquisitions

17.9%

--

13.5%

11.8%

--

Existing

Businesses

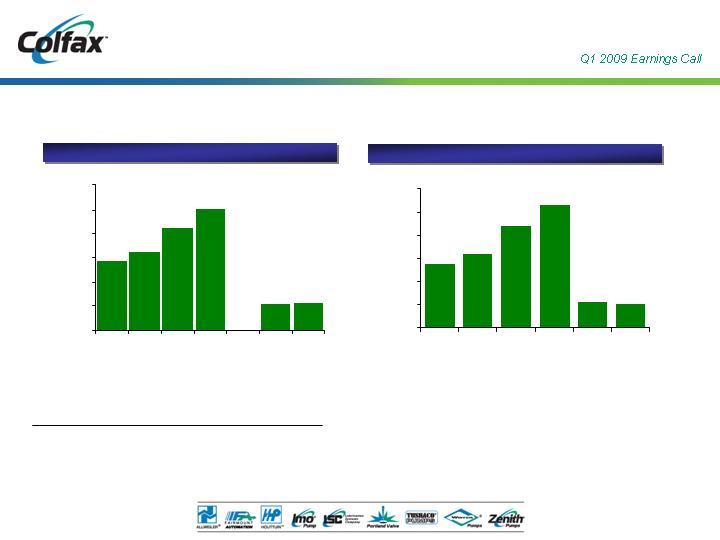

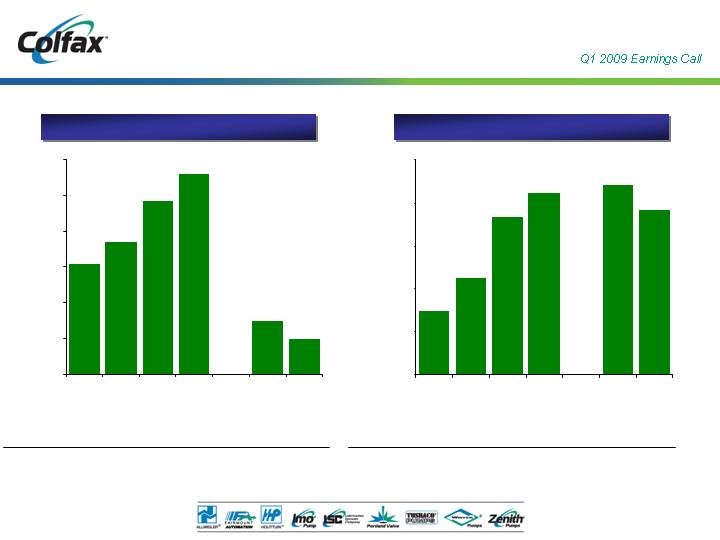

Revenue and Adjusted EBITDA

(1) Refer to Appendix for Non-GAAP reconciliation.

__________________

Note: Dollars in millions.

Revenue

Adjusted EBITDA (1)

$54.8

$64.1

$88.2

$105.6

$22.0

$20.5

$0.0

$20.0

$40.0

$60.0

$80.0

$100.0

$120.0

2005

2006

2007

2008

Q1

2008

Q1

2009

7

____________________

Note: Dollars in millions.

Q1 2009

Q1 2008

-

2008

2007

2006

2005

$720.0

$600.0

$480.0

$360.0

$240.0

$120.0

$0.0

$120.8

$180.3

$669.2

$581.5

$442.3

$370.4

Orders

Backlog

Orders and Backlog

--

--

--

--

15.1%

6.1%

2.0%

7.0%

(33.0)%

--

31.5%

19.4%

Total Growth

(7.5)%

--

7.8%

0.5%

--

FX Translation

--

--

6.1%

1.2%

--

Acquisitions

(25.5)%

--

17.6%

17.7%

--

Existing

Businesses

15.2%

(5.0)%

5.2%

15.0%

(13.6)%

--

63.3%

51.6%

Total Growth

(10.8)%

--

13.1%

12.1%

--

FX Translation

--

--

3.0%

--

--

Acquisitions

(2.8)%

--

47.2%

39.5%

--

Existing

Businesses

$118.3

$179.3

$292.8

$337.3

$353.6

$305.6

$0.0

$80.0

$160.0

$240.0

$320.0

$400.0

2005

2006

2007

2008

-

Q1 2008

Q1 2009

8

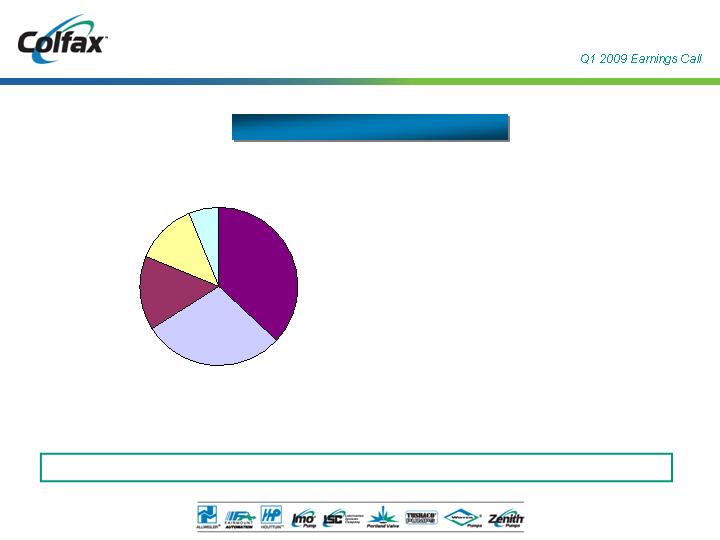

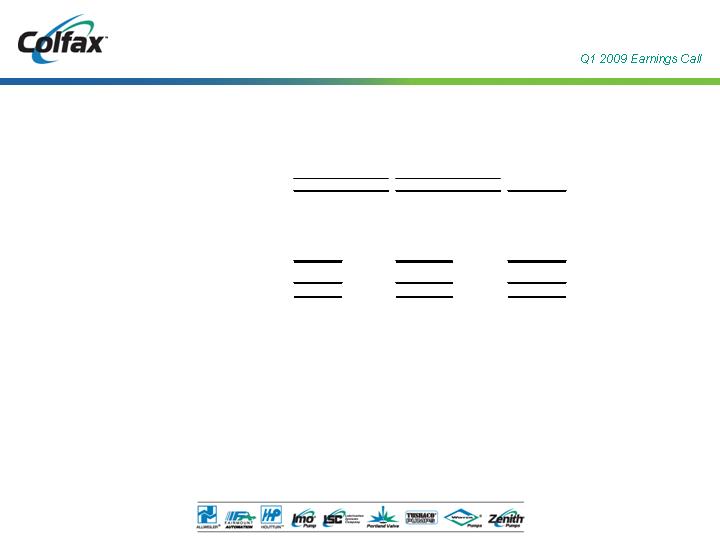

Q1 2009 Sales by End Market

Well positioned in five attractive and diverse end markets

Q1 2009 Sales: $136.3 million

(2)%

18%

(14)%

4%

General Industrial

Total

32%

29%

Global Navy

24%

11%

Power Generation

25%

20%

Oil & Gas

Commercial Marine

45%

21%

Organic Growth

Total Growth

Power

Generation

13%

Oil & Gas

15%

Commercial

Marine

29%

General

Industrial

37%

Global Navy

6%

9

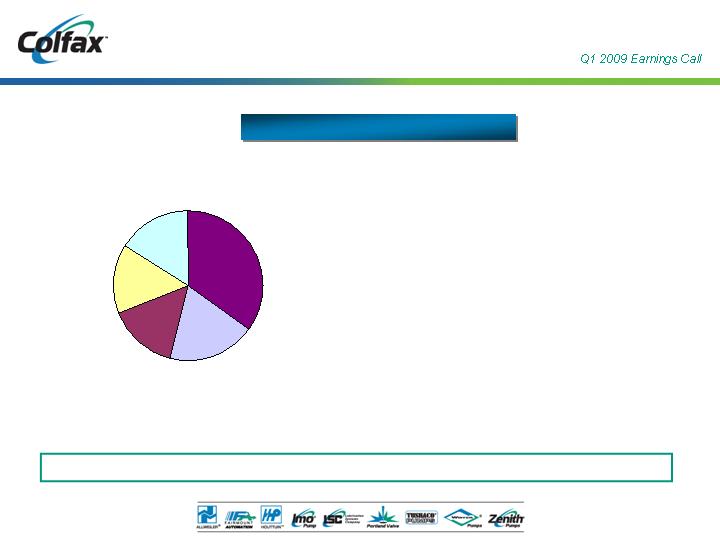

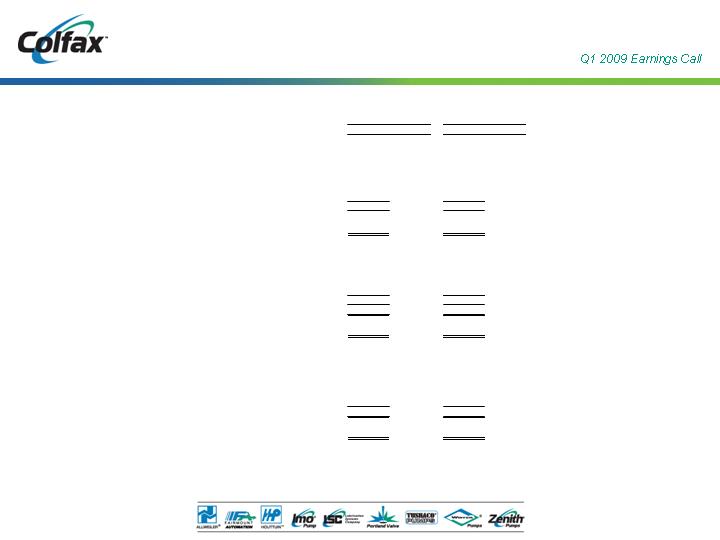

Q1 2009 Orders by End Market

Oil & Gas and Global Navy showing healthy organic growth

Q1 2009 Orders: $120.8 million

(28)%

(25)%

(36)%

(33)%

General Industrial

Total

75%

73%

Global Navy

(12)%

(21)%

Power Generation

22%

16%

Oil & Gas

Commercial Marine

(57)%

(64)%

Organic Growth

Total Growth

Oil & Gas

15%

Commercial

Marine

19%

General

Industrial

35%

Global Navy

16%

Power

Generation

15%

10

Strong balance sheet

Debt to adjusted EBITDA < 1

Debt of $95 million, principal payments of $5 million in 2009, matures in 2013

Cash = $34 million

$130 million available on revolver

Strong cash flow

Adjusted EBITDA (TTM) of $104 million

Strong balance sheet and credit availability provide flexibility

Strong Financial Condition

11

Refer to Appendix for Non-GAAP reconciliation.

__________________

Note: Dollars in millions.

Income Statement Summary

12

____________________

Note: Dollars in millions.

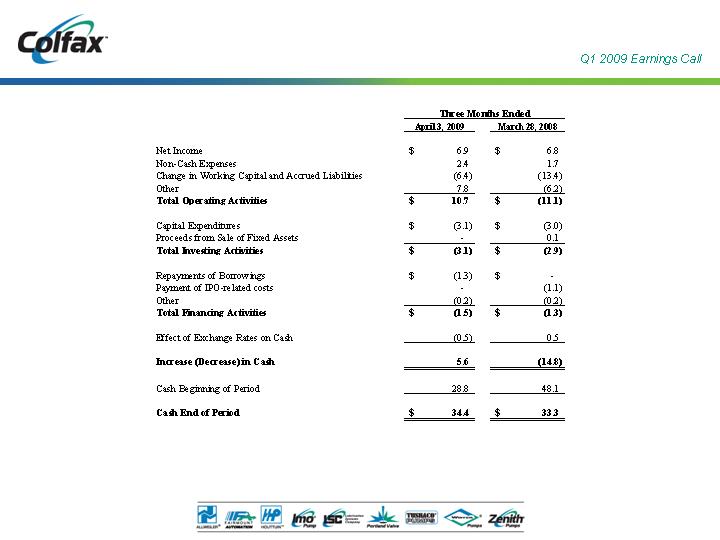

Statement of Cash Flows Summary

13

Adjusted EPS for 2009 of $1.00 to $1.07

2009 Outlook Summary

$540 million

to

$525 million

2009 Total

(4)%

to

(2)%

2009 Organic growth (1)

Revenue Range

$1.07

to

$1.00

2009 Adjusted net income per share (2)

$0.76

to

$0.69

2009 Net income per share

EPS Range

(1) Excludes impact of foreign exchange rate fluctuations and acquisitions

(2) Excludes impact of asbestos coverage litigation and asbestos liability and defense costs

(See Appendix for Non-GAAP reconciliation)

$2.5 million

Incremental public company costs

43.3 million

Outstanding shares

$8 million

Interest expense

32%

Tax rate

$1.32

Euro

$7 million

Asbestos liability and defense costs

$12 million

Asbestos coverage litigation

Assumptions

14

Well Positioned for the Future

Leading Brand Names

Generating Aftermarket

Sales and Services

Experienced Management

Team in Place to Grow

Organically and Through

Strategic Acquisitions

Global Leader in Specialty

Fluid Handling Products

Proven Application

Expertise in Solving

Critical Customer Needs

Serving Fast

Growing Infrastructure

Driven End Markets

CBS-Driven Culture Focused

on Profitable Sales Growth

15

Appendix

16

Disclaimer

Adjusted net income, adjusted net income per share, adjusted operating income and adjusted EBITDA exclude

asbestos liability and defense cost (income) and asbestos coverage litigation expense, certain legacy legal

charges, certain due diligence costs, certain severance and asset impairment charges as well as one time initial

public offering-related costs to the extent they impact the periods presented. Adjusted selling, general and

administrative expenses exclude severance and asset impairment costs, certain legacy legal charges and

certain due diligence costs to the extent they impact the periods presented. Adjusted net income also reflects

interest expense as if the initial public offering (IPO) had occurred at the beginning of 2007 and presents income

taxes at an effective tax rate of 32% in 2009 and 34% in 2008. Adjusted net income per share in 2008 assumes

the 44,006,026 shares outstanding at the closing of the IPO to be outstanding since January 1, 2007. Projected

adjusted net income per share excludes asbestos coverage litigation, asbestos liability and defense costs and

severance and asset impairment costs. Organic sales growth and organic order growth (decline) exclude the

impact of foreign exchange rate fluctuations. These non-GAAP financial measures assist Colfax in comparing

its operating performance on a consistent basis because, among other things, they remove the impact of

changes in our capital structure and asset base, non-recurring items such as IPO-related costs, legacy asbestos

issues (except in the case of EBITDA) and items outside the control of its operating management team.

Sales and order information by end market are estimates. We periodically update our customer groupings in

order to refine these estimates. During 2008, reclassifications of previously reported amounts were made to

conform to current period presentation. No changes have been made to total sales or orders.

17

____________________

Note: Dollars in thousands.

Non-GAAP Reconciliation

April 3, 2009

March 28, 2008

EBITDA

Net income

6,861

$

6,798

$

Interest expense

1,846

4,497

Provision for income taxes

3,103

3,578

Depreciation and amortization

3,373

3,695

EBITDA

15,183

$

18,568

$

EBITDA margin

11.1%

14.2%

Adjusted EBITDA

Net income

6,861

$

6,798

$

Interest expense

1,846

4,497

Provision for income taxes

3,103

3,578

Depreciation and amortization

3,373

3,695

Severance and asset impairment costs

661

-

Asbestos liability and defense costs

1,645

278

Asbestos coverage litigation expense

2,966

3,139

Adjusted EBITDA

20,455

$

21,985

$

Adjusted EBITDA margin

15.0%

16.8%

Three Months Ended

18

Non-GAAP Reconciliation

____________________

Note: Dollars in thousands.

2008

2007

2006

2005

EBITDA

Net (loss) income

(571)

$

64,882

$

94

$

12,247

$

Interest expense

11,822

19,246

14,186

9,026

Provision for income taxes

5,438

39,147

3,866

6,907

Depreciation and amortization

14,788

15,239

11,481

11,430

EBITDA

31,477

$

138,514

$

29,627

$

39,610

$

EBITDA margin

5.2%

27.4%

7.5%

11.5%

Adjusted EBITDA

Net (loss) income

(571)

$

64,882

$

94

$

12,247

$

Interest expense

11,822

19,246

14,186

9,026

Provision for income taxes

5,438

39,147

3,866

6,907

Depreciation and amortization

14,788

15,239

11,481

11,430

Legacy asbestos expense (income)

12,391

(50,346)

33,816

18,112

IPO - related costs

57,017

-

-

-

Legacy legal expenses

4,131

-

8,330

3,100

Due diligence costs

582

-

-

-

Other post-employment benefit settlement

-

-

(9,102)

(251)

Cross currency swap

-

-

-

(2,075)

Environmental indemnification

-

-

-

(3,100)

Discontinued operations

-

-

1,397

(616)

Adjusted EBITDA

105,598

$

88,168

$

64,068

$

54,780

$

Adjusted EBITDA margin

17.5%

17.4%

16.3%

15.9%

19

____________________

Note: Dollars in thousands, except per share amounts.

Non-GAAP Reconciliation

April 3, 2009

March 28, 2008

Adjusted Net Income and Adjusted Earnings per Share

Net income

6,861

$

6,798

$

Severance and asset impairment costs

661

-

Asbestos liability and defense costs

1,645

278

Asbestos coverage litigation expense

2,966

3,139

Interest adjustment to effect IPO at beginning of period

-

1,577

Tax adjustment to effective rate of 32% and 34%, respectively

(1,773)

(1,648)

Adjusted net income

10,360

$

10,144

$

Adjusted net income margin

7.6%

7.8%

Weighted average shares outstanding - diluted

43,312,306

-

Shares outstanding at closing of IPO

-

44,006,026

Adjusted net income per share

0.24

$

0.23

$

Net income per share-basic

and diluted in accordance with GAAP

0.16

$

0.31

$

Adjusted Operating Income

Operating income

11,810

$

14,873

$

Severance and asset impairment costs

661

-

Asbestos liability and defense costs

1,645

278

Asbestos coverage litigation expense

2,966

3,139

Adjusted operating income

17,082

$

18,290

$

Adjusted operating income margin

12.5%

14.0%

Three Months Ended

20

____________________

Note: Dollars in thousands.

Non-GAAP Reconciliation

April 3, 2009

March 28, 2008

Adjusted SG&A Expense

Selling, general and administrative expenses

30,187

$

28,507

$

Severance and asset impairment costs

661

-

Adjusted selling, general and administrative expenses

29,526

$

28,507

$

21.7%

21.8%

Three Months Ended

21

____________________

Note: Dollars in millions.

Sales & Order Growth

Backlog

at

$

%

$

%

Period

End

Three Months Ended March 28, 2008

130.7

$

180.3

$

353.6

$

Components of Growth:

Existing Businesses

23.4

17.9%

(45.9)

(25.5%)

(9.8)

(2.8%)

Foreign Currency Translation

(17.8)

(13.6%)

(13.6)

(7.5%)

(38.2)

(10.8%)

Total Growth

5.6

4.3%

(59.5)

(33.0%)

(48.0)

(13.6%)

Three Months Ended April 3, 2009

136.3

$

120.8

$

305.6

$

Sales

Orders

22

Sales & Order Growth

____________________

Note: Dollars in millions.

$

%

$

%

Year Ended December 31, 2005

345.5

$

370.4

$

Components of Growth:

Organic Growth from Existing Businesses

40.7

11.8%

65.6

17.7%

Acquisitions

4.8

1.4%

4.4

1.2%

Foreign Currency Translation

2.6

0.8%

1.9

0.5%

Total Growth

48.1

13.9%

71.9

19.4%

Year Ended December 31, 2006

393.6

$

442.3

$

Components of Growth:

Organic Growth from Existing Businesses

53.3

13.5%

77.7

17.6%

Acquisitions

31.3

8.0%

27.2

6.1%

Foreign Currency Translation

28.1

7.1%

34.3

7.8%

Total Growth

112.7

28.6%

139.2

31.5%

Year Ended December 31, 2007

506.3

$

581.5

$

Components of Growth:

Organic Growth from Existing Businesses

70.2

13.9%

40.9

7.0%

Acquisitions

5.5

1.1%

11.7

2.0%

Foreign Currency Translation

22.9

4.5%

35.1

6.1%

Total Growth

98.6

19.5%

87.7

15.1%

Year Ended December 31, 2008

604.9

$

669.2

$

Sales

Orders

23

Non-GAAP Reconciliation

Projected net income per share - fully diluted

0.69

$

0.76

$

Severance and asset impairment costs *

0.01

0.01

Asbestos coverage litigation

0.19

0.19

Asbestos liability and defense costs

0.11

0.11

Projected adjusted net income per share - fully diluted

$ 1.00

$ 1.07

* Actual costs for first quarter 2009

EPS Range

Colfax Corporation

Reconciliation of Projected 2009 Net Income Per Share to Adjusted Net Income Per Share

Amounts in Dollars

(unaudited)

24