As filed with the Securities and Exchange Commission on July 31, 2009

Registration No. [_________]

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

GENSPERA, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 2834 | 20-0438951 | ||

(State or jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

9901 IH 10 West, Suite 800

San Antonio, TX, 78230

(210) 477-8537

FAX (210) 477-8547

(Address, including zip code, and telephone number,

including area code, of registrant’s principal executive offices)

Agent for Service:

National Corporate Research

800 Brazos St., Suite 400

Austin, TX 78701

800-345-4647

(Name, address, including zip code, and telephone number,

including area code, of agent for service)

Copy to:

Raul Silvestre

Silvestre Law Group, P.C.

31200 Via Colinas, Suite 200

Westlake Village, CA 91362

(818) 597-7552

Fax (818) 597-7551

Approximate date of commencement of proposed sale to the public: From time to time after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | ¨ (Do not check if smaller reporting company) | Smaller reporting company | x |

CALCULATION OF REGISTRATION FEE

Title of Each Class of Securities to be Registered | Amount to be Registered | Proposed Maximum Offering Price | Proposed Maximum Aggregate Offering Price | Amount of Registration Fee | ||||||||||

| Common Stock, par value $0.0001 per share | 2,558,686 | $ | 1.50 | (1) | $ | 3,838,029 | $ | 214.16 | ||||||

| Common Stock, par value $0.0001 per share (3) | 394,187 | $ | 1.50 | (2) | $ | 591,281 | $ | 32.99 | ||||||

| Common Stock, par value $0.0001 per share (4) | 50,000 | $ | 2.00 | (2) | $ | 100,000 | $ | 5.58 | ||||||

| Common Stock, par value $0.0001 per share (5) | 1,513,247 | $ | 3.00 | (2) | $ | 4,539,741 | $ | 253.32 | ||||||

| 4,516,120 | $ | 9,069,051 | $ | 506.05 | ||||||||||

| (1) | Estimated solely for the purpose of calculating the registration fee in accordance with Rule 457 of the Securities Act based upon a per share amount of $1.50, based on the price at which the securities were previously sold. There is currently no trading market for the Registrant's common stock. The price of $1.50 is a fixed price at which the selling stockholders identified herein may sell their shares until the Registrant's common stock is quoted, if ever, at which time the shares may be sold at prevailing market prices or privately negotiated prices. |

| (2) | Fee based on exercise price applicable to shares issuable upon exercise of warrants in accordance with Rule 457(g). |

| (3) | Represents shares of Common Stock issuable upon the exercise (at a price of $1.50 per share) of outstanding warrants. |

| (4) | Represents shares of Common Stock issuable upon the exercise (at a price of $2.00 per share) of outstanding warrants. |

| (5) | Represents shares of Common Stock issuable upon the exercise (at a price of $3.00 per share) of outstanding warrants. |

THE REGISTRANT HEREBY AMENDS THIS REGISTRATION STATEMENT ON SUCH DATE OR DATES AS MAY BE NECESSARY TO DELAY ITS EFFECTIVE DATE UNTIL THE REGISTRANT SHALL FILE A FURTHER AMENDMENT WHICH SPECIFICALLY STATES THAT THIS REGISTRATION STATEMENT SHALL THEREAFTER BECOME EFFECTIVE IN ACCORDANCE WITH SECTION 8(a) OF THE SECURITIES ACT OF 1933, AS AMENDED, OR UNTIL THE REGISTRATION STATEMENT SHALL BECOME EFFECTIVE ON SUCH DATE AS THE COMMISSION, ACTING PURSUANT TO SUCH SECTION 8(a), MAY DETERMINE.

SUBJECT TO COMPLETION, DATED JULY 31, 2009

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

PROSPECTUS

4,516,120 Shares

Common Stock

This prospectus relates to the resale of 4,516,120 shares of our common stock, by the selling stockholders identified on pages 32 of this prospectus (“Selling Stockholders”). We will not receive any proceeds from the sale of these shares by the selling stockholders.

Our common stock is not presently traded on any market or exchange, and we have not applied for listing or quotation on any public market. We anticipate seeking sponsorship for the trading of our common stock on the National Association of Securities Dealers OTC Bulletin Board upon the effectiveness of the registration statement of which this prospectus forms a part. However, we can provide no assurance that our shares will be traded on the OTC Bulletin Board or, if traded, that a public market will materialize. The Selling Stockholders will sell at a price of $1.50 per share until our shares are quoted, if ever, on an exchange in which a market develops or trading facility on which the shares are traded, and thereafter, at prevailing market prices or privately negotiated prices.

Our principal executive offices are located at 9901 IH 10 West, Suite 800, San Antonio, Texas, 78230, telephone number 210-477-8537.

Investing in our common stock is highly speculative and involves a high degree of risk. You should consider carefully the risks and uncertainties in the section entitled “ Risk Factors ” on page 4 of this prospectus.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THESE SECURITIES OR PASSED UPON THE ADEQUACY OR ACCURACY OF THIS PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

The date of this Prospectus is [_________]

2

TABLE OF CONTENTS

| Page | |

| FORWARD LOOKING STATEMENTS | 4 |

| RISK FACTORS | 4 |

| USE OF PROCEEDS | 10 |

| DIVIDEND POLICY | 10 |

| DETERMINATION OF OFFERING PRICE | 10 |

| OUR BUSINESS | 10 |

| PROPERTIES | 19 |

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 19 |

| LEGAL PROCEEDINGS | 26 |

| MANAGEMENT | 26 |

| EQUITY COMPENSATION PLAN INFORMATION | 29 |

| CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS | 30 |

| PRINCIPAL STOCKHOLDERS | 31 |

| SELLING STOCKHOLDERS | 32 |

| DESCRIPTION OF SECURITIES | 38 |

| MARKET FOR COMMON EQUITY & RELATED STOCKHOLDER MATTERS | 40 |

| SHARES ELIGIBLE FOR FUTURE SALE | 40 |

| PLAN OF DISTRIBUTION | 41 |

| INDEMNIFICATION OF DIRECTORS AND OFFICERS | 43 |

| LEGAL MATTERS | 43 |

| EXPERTS | 43 |

| INTERESTS OF NAMED EXPERTS AND COUNSEL | 43 |

| WHERE YOU CAN FIND MORE INFORMATION | 43 |

| FINANCIAL STATEMENTS | 44 |

You may rely only on the information contained in this prospectus. We have not authorized anyone to provide information or to make representations not contained in this prospectus. This prospectus is neither an offer to sell nor a solicitation of an offer to buy any securities other than those registered by this prospectus, nor is it an offer to sell or a solicitation of an offer to buy securities where an offer or solicitation would be unlawful. Neither the delivery of this prospectus, nor any sale made under this prospectus, means that the information contained in this prospectus is correct as of any time after the date of this prospectus.

3

We urge you to read this entire prospectus carefully, including the” Risk Factors” section and the financial statements and related notes included in our Annual Report on Form 10-K for the fiscal year ended December 31, 2008, filed with the Securities and Exchange Commission (“SEC”) on March 30, 2009 as well as all subsequent Quarterly Reports on Form 10-Q. As used in this prospectus, unless context otherwise requires, the words “we,” “us,”“our,” “the Company” and “GenSpera” refer to GenSpera, Inc. Also, any reference to “common shares,” “Common Stock,” “common shares” or “Common Shares” refers to our $.0001 par value common stock.

FORWARD LOOKING STATEMENTS

This prospectus contains forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934 (the "Exchange Act"), which are intended to convey our expectations or predictions regarding the occurrence of possible future events or the existence of trends and factors that may impact our future plans and operating results. These forward-looking statements are derived, in part, from various assumptions and analyses we have made in the context of our current business plan and information currently available to us and in light of our experience and perceptions of historical trends, current conditions and expected future developments and other factors we believe are appropriate in the circumstances. You can generally identify forward looking statements through words and phrases such as “believe”, “expect”, “seek”, “estimate”, “anticipate”, “intend”, “plan”, “budget”, “project”, “may likely result”, “may be”, “may continue” and other similar expressions.

When reading any forward-looking statement you should remain mindful that actual results or developments may vary substantially from those expected as expressed in or implied by such statement for a number of reasons or factors, including but not limited to:

| · | our research and development activities, the development of a viable commercial product, and the speed with which regulatory authorizations and product launches may be achieved; |

| · | whether or not a market for our product develops and, if a market develops, the rate at which it develops; |

| · | our ability to sell our products; |

| · | our ability to attract and retain qualified personnel to implement our business plan and growth strategies; |

| · | our ability to develop sales, marketing, and distribution capabilities; |

| · | the accuracy of our estimates and projections; |

| · | our ability to fund our short-term and long-term financing needs; |

| · | changes in our business plan and corporate growth strategies; and |

| · | other risks and uncertainties discussed in greater detail in the section captioned “Risk Factors” |

RISK FACTORS

Investing in our common stock involves a high degree of risk. You should carefully consider the following risk factors and all other information contained in this prospectus before purchasing our common stock. If any of the following events were to occur, our business, financial condition or results of operations could be materially and adversely affected. In these circumstances, the market price of our common stock could decline, and you could lose some or all of your investment.

Risks Relating to Our Stage of Development

As a result of our limited operating history, you cannot rely upon our historical performance to make an investment decision.

Since inception in 2003 and through March 31, 2009 we have raised approximately $4,131,000 in capital. During this same period, we have recorded accumulated losses totaling $6,616,252. As of March 31, 2009, we had working capital of $461,623 and a deficiency in stockholders’ equity of $1,355,587. Our net losses for the two most recent fiscal years ended December 31, 2007 and 2008 have been $691,199 and $3,326,261, respectively. Since inception, we have generated no revenue.

Our limited operating history means that there is a high degree of uncertainty in our ability to: (i) develop and commercialize our technologies and proposed products; (ii) obtain approval from the United States Food and Drug Administration (“FDA”); (iii) achieve market acceptance of our proposed product, if developed; (iv) respond to competition; or (v) operate the business, as management has not previously undertaken such actions as a company. No assurances can be given as to exactly when, if at all, we will be able to fully develop, commercialize, market, sell or derive revenues from our business.

4

We will need to raise additional capital to continue operations.

We currently generate no cash. We have relied entirely on external financing to fund operations. Such financing has historically come primarily from the sale of common stock to third parties, loans from our Chief Executive Officer and the exercise of warrants/options. We have expended and will continue to expend substantial cash in the development and pre-clinical and clinical testing of our proposed products. We will require additional cash to conduct drug development, establish and conduct pre-clinical and clinical trials, support commercial-scale manufacturing arrangements and provide for the marketing and distribution of our products if developed. We anticipate that we will require an additional $7 million to take our lead drug through Phase II clinical evaluation, currently anticipated to occur in the fourth quarter of 2011.

In June and July of 2009, we raised an aggregate of $3,088,000 from the private placement of our securities. We anticipate, based on current proposed plans and assumptions relating to our operations and financing, that our current working capital as of March 31, 2009 and the proceeds of the offering will be sufficient to satisfy contemplated cash requirements through October of 2010, assuming we do not engage in an extraordinary transaction or otherwise face unexpected events or contingencies, any of which could affect cash requirements. As of July 31, 2009, we had cash on hand of approximately $2,740,000. Presently, the Company has an average monthly cash burn rate of approximately $176,000. We expect this average monthly cash burn rate to remain constant over the next fifteen months, assuming we do not engage in an extraordinary transaction or otherwise face unexpected events or contingencies. Accordingly, we will need to raise additional capital to fund anticipated operating expenses after October of 2010. We cannot assure you that financing whether from external sources or related parties will be available if needed or on favorable terms. If additional financing is not available when required or is not available on acceptable terms, we may be unable to fund operations and planned growth, develop or enhance our technologies, take advantage of business opportunities or respond to competitive market pressures. Any negative impact on our operations may make the raising of capital more difficult.

Additional funds may not be available on acceptable terms, if at all. If adequate funds are unavailable, we may have to delay, reduce the scope of or eliminate one or more of our research, development or commercialization programs or product launches or marketing efforts. Any such change may materially harm our business, financial condition and operations.

Our long term capital requirements are expected to depend on many factors, including:

| · | our development programs; |

| · | the progress and costs of pre-clinical studies and clinical trials; |

| · | the time and costs involved in obtaining regulatory clearance; |

| · | the costs involved in preparing, filing, prosecuting, maintaining and enforcing patent claims; |

| · | the costs of developing sales, marketing and distribution channels and our ability to sell our products; |

| · | competing technological and market developments; |

| · | market acceptance of our proposed products, if developed; |

| · | the costs for recruiting and retaining employees, consultants and professionals; and |

| · | the costs for educating and training physicians about our products. |

We may consume available resources more rapidly than currently anticipated, resulting in the need for additional funding. If adequate funds are not available, we may be required to significantly reduce or refocus our development and commercialization efforts.

Raising needed capital in the future may be difficult as a result of our limited operating history.

When making investment decisions, investors typically look at a company’s historical performance in evaluating the risks and operations of the business and the business’s future prospects. Our limited operating history makes such evaluation and an estimation of our future performance substantially more difficult. As a result, investors may be unwilling to invest in us or such investment may be on terms or conditions which are not acceptable. If we are unable to secure such additional finance, we may need to cease operations.

5

Our independent auditors have issued a qualified report as of and for the year ended December 31, 2008 with respect to our ability to continue as a going concern.

For the year ended December 31, 2008, our accountants issued a report relating to our audited financial statements which contains a qualification with respect to our ability to continue as a going concern because, among other things, our ability to continue as a going concern is dependent upon our ability to develop a product and generate profits from operations in the future or to obtain the necessary financing to meet our obligations and repay our liabilities when they come due. However, during 2009 we have raised approximately $3,788,000 through our private placements and we expect that our cash on hand of approximately $2,740,000 at July 31, 2009 will be sufficient to fund operations through October of 2010.

We may not be able to commercially develop our technologies.

We have concentrated our research and development on our drug technologies. Our ability to generate revenue and operate profitably will depend on our being able to develop these technologies for human applications. Our technologies are primarily directed toward the development of cancer therapeutic agents. We cannot guarantee that the results obtained in pre-clinical and clinical evaluation of our therapeutic agents will be sufficient to warrant approval by the FDA. Even if our therapeutic agents are approved for use by the FDA, there is no guarantee that they will exhibit an enhanced efficacy relative to competing therapeutic modalities such that they will be adopted by the medical community. Without significant adoption by the medical community our agents will have limited commercial potential which will likely result in the loss of your entire investment.

Inability to complete pre-clinical and clinical testing and trials will impair our viability.

We have recently submitted our first Investigational New Drug application (“IND”) to the FDA in order to commence clinical trials. On July 24, 2009, we were notified by the FDA that our IND was on clinical hold pending our response to certain questions provided by them concerning the clinical trial design. Even if we receive clearance from the FDA to commence trials, the outcome of the trials is uncertain and, if we are unable to satisfactorily complete such trials, or if such trials yield unsatisfactory results, we will be unable to commercialize our proposed products. No assurances can be given that the clinical trials, if commenced, will be successful. The failure of such trials could delay or prevent regulatory approval and could harm our ability to generate revenues, operate profitably or remain a viable business.

Our additional financing requirements will result in dilution to existing stockholders.

We will require additional financing in the future. We are authorized to issue 80 million shares of common stock and 10 million shares of preferred stock. Such securities may be issued without the approval or consent of our stockholders. The issuance of our equity securities in connection with a future financing will result in a decrease of our current stockholders’ percentage ownership.

Risks Relating to Intellectual Property and Government Regulation

We may not be able to withstand challenges to our intellectual property rights.

We rely on our intellectual property, including our issued and applied for patents, as the foundation of our business. Our intellectual property rights may come under challenge. No assurances can be given that, even though issued, our current and potential future patents will survive claims alleging invalidity or infringement on other patents. The viability of our business will suffer if such patent protection becomes limited or is eliminated.

We may not be able to adequately protect our intellectual property.

Considerable research with regard to our technologies has been performed in countries outside of the United States. The laws protecting intellectual property in some of those countries may not provide protection for our trade secrets and intellectual property. If our trade secrets or intellectual property are misappropriated in those countries, we may be without adequate remedies to address the issue. At present, we are not aware of any infringement of our intellectual property. In addition to our patents, we rely on confidentiality and assignment of invention agreements to protect our intellectual property. These agreements provide for contractual remedies in the event of misappropriation. We do not know to what extent, if any, these agreements and any remedies for their breach will be enforced by a foreign court. In the event our intellectual property is misappropriated or infringed upon and an adequate remedy is not available, our future prospects will greatly diminish.

6

Our proposed products may not receive FDA approval.

The FDA and comparable government agencies in foreign countries impose substantial regulations on the manufacture and marketing of pharmaceutical products through lengthy and detailed laboratory, pre-clinical and clinical testing procedures, sampling activities and other costly and time-consuming procedures. Satisfaction of these regulations typically takes several years or more and varies substantially based upon the type, complexity and novelty of the proposed product. We have recently submitted our first IND application to the FDA. On July 24, 2009, we were notified by the FDA that our IND was on clinical hold pending our response to certain questions provided by them. There is no assurance that we will be able to adequately respond to the questions provided by the FDA or that even if such questions are answered, that the IND application will be granted on a timely basis, if at all. We cannot assure you that we will successfully complete any clinical trials in connection with any such IND application. Further, we cannot yet accurately predict when we might first submit any product license application for FDA approval or whether any such product license application would be granted on a timely basis, if at all. As a result, we cannot assure you that FDA approval for any products developed by us will be granted on a timely basis, if at all. Any delay in obtaining, or failure to obtain, such approvals could have a materially adverse effect on the commercialization of our products and the viability of the company.

Risks Relating to Competition

Our competitors have significantly greater experience and financial resources.

We compete against numerous companies, many of which have substantially greater financial and other resources than us. Several such enterprises have research programs and/or efforts to treat the same diseases we target. Companies such as Merck, Ipsen and Diatos, as well as others, have substantially greater resources and experience than we do and are situated to compete with us effectively. As a result, our competitors may bring competing products to market that would result in a decrease in demand for our product, if developed, which could have a materially adverse effect on the viability of the company.

Risks Relating to Reliance on Third Parties

We intend to rely exclusively upon the third-party FDA-approved manufacturers and suppliers for our products.

We currently have no internal manufacturing capability, and will rely exclusively on FDA-approved licensees, strategic partners or third party contract manufacturers or suppliers. Should we be forced to manufacture our products, we cannot give you any assurance that we will be able to develop internal manufacturing capabilities or procure third party suppliers. In the event we seek third party suppliers, they may require us to purchase a minimum amount of materials or could require other unfavorable terms. Any such event would materially impact our prospects and could delay the development and sale of our products. Moreover, we cannot give you any assurance that any contract manufacturers or suppliers that we select will be able to supply our products in a timely or cost effective manner or in accordance with applicable regulatory requirements or our specifications.

General Risks Relating to Our Business

We depend on Craig A. Dionne, PhD, our Chief Executive Officer, and Russell Richerson PhD, our Chief Operating Officer, for our continued operations.

The loss of Craig A. Dionne, PhD, our Chief Executive Officer, or Russell Richerson, PhD, our Chief Operating Officer, would be detrimental to us. We currently maintain a one million dollar “key person” life insurance policy on the life of Dr. Dionne but do not maintain a policy on Dr. Richerson. Our prospects and operations will be significantly hindered upon the death or incapacity of either of these key individuals. We currently do not have written employment agreements with Messrs Dionne or Richerson.

We will require additional personnel to execute our business plan.

Our anticipated growth and expansion into areas and activities requiring additional expertise, such as clinical testing, regulatory compliance, manufacturing and marketing, will require the addition of new management personnel and the development of additional expertise by existing management. There is intense competition for qualified personnel in such areas. There can be no assurance that we will be able to continue to attract and retain the qualified personnel necessary for the development of our business.

Our business is dependent upon securing sufficient quantities of a natural product that currently grows in very specific locations outside of the United States.

The therapeutic component of our products, including our lead compound G-202, is referred to as 12ADT. 12ADT functions by dramatically raising the levels of calcium inside cells, which leads to cell death. 12ADT is derived from a material called thapsigargin. Thapsigargin is derived from the seeds of a plant referred to as Thapsia garganica which grows along the coastal regions of Spain. We currently secure the seeds from Thapsibiza, SL, a third party supplier. There can be no assurances that the countries from which we can secure Thapsia garganica will continue to allow Thapsibiza, SL to collect such seeds and/or to do so and export the seeds derived from Thapsia garganica to the United States. In the event we are no longer able to import these seeds, we will not be able to produce our proposed drug and our business will be adversely impacted.

7

The current manufacturing process of G-202 requires acetonitrile.

The current manufacturing process for G-202 requires the common solvent acetonitrile. Beginning in late 2008, there has been a worldwide shortage of acetonitrile for a variety of reasons, and this shortage is predicted to last at least until the end of 2009 and possibly into future years. We have also observed that the available supply of acetonitrile is of variable quality, some of which is not suitable for our purposes. If we are unable to successfully change our manufacturing methods to avoid the reliance upon acetonitrile, we may incur prolonged production timelines and increased production costs. In an extreme case this situation could adversely affect our ability to manufacture G-202 altogether, thus significantly impacting our future operations.

In order to secure market share and generate revenues, our proposed products must be accepted by the health care community.

Our proposed products, if approved for marketing, may not achieve market acceptance since hospitals, physicians, patients or the medical community in general may decide not to accept and utilize them. We are attempting to develop products that will likely be first approved for marketing in late stage cancer where there is no truly effective standard of care. If approved for use in late stage, the drugs will then be evaluated in earlier stage where they would represent substantial departures from established treatment methods and will compete with a number of more conventional drugs and therapies manufactured and marketed by major pharmaceutical companies. It is too early in the development cycle of the drugs for us to accurately predict our major competitors. Nonetheless, the degree of market acceptance of any of our developed products will depend on a number of factors, including:

| · | our demonstration to the medical community of the clinical efficacy and safety of our proposed products; |

| · | our ability to create products that are superior to alternatives currently on the market; |

| · | our ability to establish in the medical community the potential advantage of our treatments over alternative treatment methods; and |

| · | the reimbursement policies of government and third-party payors. |

If the health care community does not accept our products for any of the foregoing reasons, or for any other reason, our business will be materially harmed.

We may be required to secure land for cultivation and harvesting of the seeds derived from Thapsia garganica.

We believe that we can satisfy our needs for clinical development of G-202 through completion of Phase III clinical studies from Thapsia garganica that grows naturally in the wild. In the event G-202 is approved for commercial marketing by the FDA, our current supply of Thapsia garganica may not be sufficient for the anticipated demand. We estimate that in order to secure sufficient quantities of Thapsia garganica for the commercialization of a product comprising G-202, we will need to secure approximately 100 acres of land to cultivate and grow Thapsia garganica. We anticipate the cost to lease such land would be $40,000 per year but have not yet fully assessed what other costs would be associated with a full-scale farming operation. There can be no assurances that we can secure such acreage, or that even if we are able to do so, that we could adequately grow sufficient quantities of Thapsia garganica to satisfy any commercial objectives that involve G-202. Our inability to secure adequate seeds will result in us not being able to develop and manufacture our proposed drug and will adversely impact our business.

Thapsia garganica and Thapsigargin can cause severe skin irritation.

It has been known for centuries that the plant Thapsia garganica can cause severe skin irritation when contact is made between the plant and the skin1. Skin plasters made from the plant have been part of the Medical Pharmacopeia2 in Western Europe as recently as the 1930s. The therapeutic action of the plaster is that of a severe counter-irritant. In 1978, thapsigargin was determined to be the skin-irritating component of the plant Thapsia garganica. The therapeutic component of our products, including our lead product G-202, is derived from thapsigargin. We obtain thapsigargin from the above-ground seeds of Thapsia garganica. These seeds are harvested by hand and those conducting the harvesting must wear protective clothing and gloves to avoid skin contact. Although we obtain the seeds from a third-party contractor located in Spain, and although the contractor has contractually waived any and all liability associated with collecting the seeds, it is possible that the contractor or those employed by the contractor may suffer medical issues related to the harvesting and subsequently seek compensation from us via, for example, litigation. No assurances can be given, despite our contractual relationship with the third party contractor, that we will not be the subject of litigation related to the harvesting

1 Christensen, S.B., Norup, E., and Rasmussen, U. (1984) in: Natural Products and Drug Development (Krogsgaard-Larsen, P., Christensen, S.B. and Kofod, H., eds.) pp 405-417, Munksgaard, Copenhagen.

2 Medical Pharmacopeia is a book containing an official list of medicinal drugs together with articles on their preparation and use.

8

The synthesis of 12ADT must be conducted in special facilities.

There are a limited number of facilities qualified to handle toxic agents for the manufacture of therapeutic compounds. This limits the potential number of possible manufacturing sites for our therapeutic compounds derived from Thapsia garganica. No assurances can be provided that these facilities will be available for the manufacture of our therapeutic compounds under our time schedules or within the parameters of our manufacturing budget. In the event facilities are not available for manufacturing our therapeutic compounds, the Company’s business and future prospects will be adversely affected.

Our lead therapeutic compound, G-202, has not been subjected to large scale manufacturing procedures

To date, G-202 has only been manufactured at a scale adequate to supply early stage clinical trials. There can be no assurances that the current procedure for manufacturing G-202 will work at a larger scale adequate for commercial needs. In the event G-202 cannot be manufactured in sufficient quantities, our future prospects could be significantly impacted.

We have no product liability insurance.

The testing, manufacturing, marketing and sale of human therapeutic products entail an inherent risk of product liability claims. We cannot assure you that substantial product liability claims will not be asserted against us. We have no product liability insurance. In the event we are forced to expend significant funds on defending product liability actions, and in the event those funds come from operating capital, we will be required to reduce our business activities, which could lead to significant losses.

We cannot assure you that adequate insurance coverage will be available in the future on acceptable terms.

Any significant claim would have a material adverse effect on our business, financial condition and results of operations. Insurance availability, coverage terms and pricing continue to vary with market conditions. We will endeavor to obtain appropriate insurance coverage for insurable risks that we identify. We may not be able to obtain appropriate insurance coverage. The occurrence of an uninsured claim may have an adverse material effect on our business.

Risks Relating Our Common Stock

There is no public market for our securities.

There is no public market for our securities. An investment in our common stock should be considered totally illiquid. No assurances can be given that a public market for our securities will ever materialize. Additionally, even if a public market for our securities develops and our securities become traded, the trading volume may be limited, making it difficult for an investor to sell shares.

We face risks related to compliance with corporate governance laws and financial reporting standards.

The Sarbanes-Oxley Act of 2002, as well as related new rules and regulations implemented by the Securities and Exchange Commission and the Public Company Accounting Oversight Board, require changes in the corporate governance practices and financial reporting standards for public companies. These new laws, rules and regulations, including compliance with Section 404 of the Sarbanes-Oxley Act of 2002 relating to internal control over financial reporting (“Section 404”), will materially increase the Company's legal and financial compliance costs and make some activities more time-consuming and more burdensome. As a result, management will be required to devote more time to compliance which could result in a reduced focus on the development thereby adversely affecting the Company’s development activities. Also, the increased costs will require the Company to seek financing sooner that it may otherwise have had to.

Starting in 2007, Section 404 of the Sarbanes-Oxley Act of 2002 requires that the Company's management assess the Company's internal control over financial reporting annually and include a report on its assessment in its annual report filed with the SEC. Effective December 15, 2009 for a smaller reporting company, the Company's independent registered public accounting firm is required to audit both the design and operating effectiveness of its internal controls and management's assessment of the design and the operating effectiveness of its internal controls.

Because of our limited resources, management has concluded that our internal control over financial reporting may not be effective in providing reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with U.S. generally accepted accounting principles.

To mitigate the current limited resources and limited employees, we rely heavily on direct management oversight of transactions, along with the use of legal and accounting professionals. As we grow, we expect to increase our number of employees, which will enable us to implement adequate segregation of duties within the Committee of Sponsoring Organizations of the Treadway Commission internal control framework.

9

We do not intend to pay cash dividends.

We do not anticipate paying cash dividends in the foreseeable future. Since we do not anticipate paying dividends, any gains on your investment will need to come through an increase in the price of our common stock. The lack of a market for our common stock makes such gains highly unlikely.

Our board of directors has broad discretion to issue additional securities which may greatly impact the value of our common stock.

We are entitled under our certificate of incorporation to issue up to 80,000,000 common and 10,000,000 “blank check” preferred shares. Blank check preferred shares provide the board of directors broad authority to determine voting, dividend, conversion, and other rights. As of July 31, 2009, we have issued and outstanding 15,107,279 common shares and we have 5,801,939 common shares reserved for issuance upon the exercise of current outstanding options, warrants and convertible securities. Accordingly, we will be entitled to issue up to 59,090,782 additional common shares and 10,000,000 additional preferred shares. Our board may generally issue those common and preferred shares, or options or warrants to purchase those shares, without further approval by our shareholders based upon such factors as our board of directors may deem relevant at that time. Any preferred shares we may issue shall have such rights, preferences, privileges and restrictions as may be designated from time-to-time by our board, including preferential dividend rights, voting rights, conversion rights, redemption rights and liquidation provisions. It is likely that we will be required to issue a large amount of additional securities to raise capital to further our development and marketing plans. It is also likely that we will be required to issue a large amount of additional securities to directors, officers, employees and consultants as compensatory grants in connection with their services, both in the form of stand-alone grants or under our various stock plans. We cannot give any assurance that we will not issue additional common or preferred shares, or options or warrants to purchase those shares, under circumstances we may deem appropriate at the time.

Our Officers and Scientific Advisors beneficially own approximately 43% of our outstanding common shares.

Our Officers and Scientific Advisors own approximately 43% of our issued and outstanding common shares. As a consequence of their level of stock ownership, the group will substantially retain the ability to elect or remove members of our board of directors, and thereby control our management. This group of shareholders has the ability to significantly control the outcome of corporate actions requiring shareholder approval, including mergers and other changes of corporate control, going private transactions, and other extraordinary transactions any of which may be in opposition to the best interest of the other shareholders and may negatively impact the value of your investment.

USE OF PROCEEDS

We will not receive any of the proceeds from the sale of the shares by any of the selling stockholders, but we will receive up to $5,231,022 upon the exercise of warrants in the event they are exercised for cash. We will use the proceeds received from the exercise of warrants, if any, for working capital.

DIVIDEND POLICY

We have never paid or declared cash dividends on our common stock, and we do not intend to pay or declare cash dividends on our common stock in the foreseeable future.

DETERMINATION OF OFFERING PRICE

The Selling Stockholders will initially offer their shares at $1.50 per share until such time as or common stock becomes traded on an exchange or over the counter, if ever. Once traded, the shares will be offered at prevailing market prices, privately negotiated prices, or in any other fashion as described in the section of this Prospectus entitled “Plan of Distribution.” The selling price has no relationship to any established criteria of value, such as book value or earnings per share. The price was chosen arbitrarily.

OUR BUSINESS

Our History

We are a biotechnology company focused on the discovery and development of pro-drug cancer therapeutics, an emerging medical science. A pro-drug is an inactive precursor of a drug that is converted into its active form only at the site of the tumor. We were incorporated as a Delaware corporation in 2003.

10

In early 2004, the intellectual property underlying the our technologies was assigned from Johns Hopkins University to the technologies’ co-inventors, Dr. John Isaacs, Dr. Soren Christensen, Dr. Hans Lilja and Dr. Samuel Denmeade. The Co-inventors granted us an option to license the intellectual property in return for our continued prosecution of the patent portfolio containing the intellectual property. This option was exercised in early 2008 by reimbursement of past patent prosecution costs previously incurred by Johns Hopkins University. Subsequently, the co-inventors assigned us the intellectual property in April of 2008. Our activities during the period of 2004-2007 were limited to the continued prosecution of the relevant patents.

Dr. John Isaacs and Dr. Sam Denmeade serve on our Scientific Advisory Board as Chief Scientific Advisor and Chief Medical Advisor, respectively. Dr Soren Christensen and Dr. Hans Lilja also serve on the Company’s Scientific Advisory Board. We currently have no oral or written agreements with Johns Hopkins University with regard to any other intellectual property or research activities.

The Potential of Our Pro-Drug Therapies

Cancer chemotherapy involves treating patients with cytotoxic drugs (compounds or agents that are toxic to cells). Chemotherapy is often combined with surgery or radiation in the treatment of early stage disease and it is the preferred, or only, treatment option for many forms of cancer in later stages of the disease. However, major drawbacks of chemotherapy include:

| Side effects | Non-cancer cells in the body are also affected, often leading to serious side effects. |

| Incomplete tumor kill | Many of the leading chemotherapeutic agents act during the process of cell division - they might be effective with tumors comprised of rapidly-dividing cells, but are much less effective for tumors that contain cells that are slowly dividing. |

| Resistance | Cancers will often develop resistance to current drugs after repeated exposure, limiting the number of times that a treatment can be effectively applied. |

Pro-drug chemotherapy is a relatively new approach to cancer treatment that is being investigated as a means to get higher concentrations of cytotoxic agents at the tumor location while avoiding the toxicity of these high doses in the rest of the body. An inactive form of a cytotoxin (referred to as the “pro-drug”) is administered to the patient. The pro-drug is converted into the active cytotoxin only at the tumor site.

We believe that, if successfully developed, pro-drug therapies have the potential to provide an effective therapeutic approach to a broad range of solid tumors. We have proprietary technologies that we believe appear, in animal models, to meet the requirements for an effective pro-drug. In addition, we believe that our cytotoxin addresses two other issues prevalent with current cancer drugs - it kills slowly- and non-dividing cancer cells as well as rapidly dividing cancer cells, and does not appear to trigger the development of resistance to its effects.

Our Technology

Our technology supports the creation of pro-drugs by attaching “masking/targeting agents” (agents that simultaneously mask the toxicity of the cytotoxin and help target the cytotoxin to the tumor) to the cytotoxin “12ADT”, and does so in a way that allows conversion of the pro-drug to its active form selectively at the site of tumors. We own patents that contain claims that cover 12ADT as a composition of matter.

Cytotoxin

12ADT is a chemically modified form of thapsigargin, a cytotoxin that kills fast-, slow- and non-dividing cells. Our two issued core patents, both entitled “Tissue Specific Prodrug,” contain claims which cover the composition of 12ADT.

11

Masking/Targeting Agent

We use peptides as our masking/targeting agents. Peptides are short strings of amino-acids, the building blocks of many components found in cells. When attached to 12ADT, they can make the cytotoxin inactive - once removed, the cytotoxin is active again. Our technology takes advantage of the fact that the masking peptides can be removed by chemical reactors in the body called enzymes, and that the recognition of particular peptides by particular enzymes can be very specific. The peptides also make 12ADT soluble in blood. When it is removed, 12ADT returns to its natural insoluble state and precipitates directly into nearby cells.

How we make our pro-drugs

How our pro-drugs work

Our Approach

Our approach is to identify specific enzymes that are found at high levels in tumors relative to other tissues in the body. Upon identifying these enzymes, we create peptides that are recognized predominantly by those enzymes in the tumor and not by enzymes in normal tissues. This double layer of recognition adds to the tumor-targeting found in our pro-drugs. Because the exact nature of our masking/targeting peptides is so refined and specific, they form the basis for another set of our patents and patent applications on the combination of the peptides and 12ADT.

12

Our Pro-Drug Development Candidates

We currently have four pro-drug candidates identified based on this technology, as summarized in the table below (at this time we are only developing G-202):

| Pro-Drug Candidate | Activating enzyme | Target location of activation enzyme | Status | ||||

| G-202 | Prostate Specific Membrane Antigen (PSMA) | The blood vessels of all solid tumors | · | Investigational New Drug Application planned is filed with the US Food and Drug Administration. Currently on Clinical Hold pending our response to questions. | |||

| G-114 | Prostate Specific Antigen (PSA) | Prostate cancers | · | Validated efficacy in pre-clinical animal models (Johns Hopkins University) | |||

| G-115 | Prostate Specific Antigen (PSA) | Prostate cancers | · | Validated efficacy in pre-clinical animal models (Johns Hopkins University) | |||

| Ac-GKAFRR-L12ADT | Human glandular kallikrein 2 (hK2) | Prostate cancers | · | Validated efficacy in pre-clinical animal models (Johns Hopkins University) | |||

Strategy

Business Strategy

We plan to develop a series of therapies based on our pro-drug technology platform and bring them through Phase I/II clinical trials.

Manufacturing and Development Strategy

Under the planning and direction of key personnel, we expect to outsource all of our Good Laboratory Practices (“GLP”) preclinical development activities (e.g., toxicology) and Good Manufacturing Practices (“GMP”) manufacturing and clinical development activities to contract research organizations (“CRO”) and contract manufacturing organizations (“CMO”). Manufacturing will also be outsourced to organizations with approved facilities and manufacturing practices.

Commercialization Strategy

We intend to license our drug compounds to third parties after Phase I/II clinical trials. It is expected that such third parties would then continue to develop, market, sell, and distribute the resulting products.

Market and Competitive Considerations

G-202

Our primary focus is the opportunity offered by our lead pro-drug candidate, G-202. We believe that we have validated G-202 as a drug candidate to treat various forms of solid tumors; including breast, urinary bladder, kidney and prostate cancer based on the ability of G-202 to cause tumor regression in animal models of these diseases. We filed our first IND for G-202 on June 23, 2009. On July 24, 2009 we were notified by the FDA that our IND is on clinical hold pending our response to certain questions regarding our trial design. Pending clearance by the FDA we plan to begin the clinical evaluation of G-202 in late 2009. We hope to eventually demonstrate that G-202 is more efficacious than current commercial products that treat solid tumors by disrupting their blood supply.

13

Potential Markets for G-202

We believe that if successfully developed, G-202 has the potential to treat a range of solid tumors by disrupting their blood supply. It is too early in the development process to determine target indications. The table below summarizes a number of the potential United States patient populations which we believe may be amenable to this therapy and represent potential target markets.

| Estimated Number of | Probability of Developing (birth to death) | |||||||

| Cancer | New Cases (2006) | Male | Female | |||||

| Prostate | 234,460 | 1 in 6 | - | |||||

| Breast | 214,640 | n/a | 1 in 8 | |||||

| Urinary Bladder | 61,420 | 1 in 28 | 1 in 88 | |||||

| Kidney Cancer | 38,890 | n/a | n/a | |||||

Source: CA Cancer J. Clin 2006; 56;106-130

The clinical opportunity for G-202

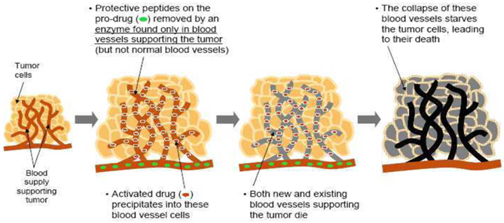

We believe that current anti-angiogenesis drugs (drugs that disrupt the blood supply to tumors) validate the clinical approach and market potential of G-202. Angiogenesis is the physiological process involving the growth of new blood vessels from pre-existing vessels and is a normal process in growth and development, as well as in wound healing. Angiogenesis is also a fundamental step in the development of tumors from a clinically insignificant size to a malignant state because no tumor can grow beyond a few millimeters in size without the nutrition and oxygenation that comes from an intimately associated blood supply. Interrupting this process has been targeted as a point of intervention for slowing or reversing tumor growth. A well known example of a successful anti-angiogenic approach is the recently approved drug, AvastinTM, a monoclonal antibody that inhibits the activity of Vascular Endothelial Growth Factor (“VEGF”), which is important for the growth and survival of endothelial cells.

These types of anti-angiogenic drugs have only a limited therapeutic effect with increased median patient survival times of only a few months. Our approach is designed to destroy both the existing and newly growing tumor vasculature, rather than just block new blood vessel formation. We anticipate that this approach will lead to a more immediate collapse of the tumors nutrient supply and consequently an enhanced rate of tumor destruction.

G-202 destroys new and existing blood vessels in tumors

Competition

The pharmaceutical, biopharmaceutical and biotechnology industries are very competitive, fast moving and intense, and expected to be increasingly so in the future. Although we are not aware of any competitor who is developing a drug that is designed to destroy both the existing and newly growing tumor vasculature in a manner similar to G-202, there are several marketed drugs and drugs in development that attack tumor-associated blood vessels to some degree. For example, Avastin TM is a marketed product that acts predominantly as an anti-angiogenic agent. Zybrestat TM is another drug in development that is described as a vascular-disrupting agent that inhibits blood flow to tumors. It is impossible to accurately ascertain how well our drug will compete against these or other products that may be in the marketplace until we have human patient data for comparison.

14

Other larger and well funded companies have developed and are developing drug candidates that, if not similar in type to our drug candidates, are designed to address the same patient or subject population. Therefore, our lead product, other products in development, or any other products we may acquire or in-license may not be the best, the safest, the first to market, or the most economical to make or use. If a competitor’s product or product in development is better than ours, for whatever reason, then our ability to license our technology could be diminished and our sales could be lower than that of competing products, if we are able to generate sales at all.

Patents and Proprietary Rights

Our success will likely depend upon our ability to preserve our proprietary technologies and operate without infringing on the proprietary rights of other parties. However, we may rely on certain proprietary technologies and know-how that are not patentable or that we determine to keep as trade secrets. We protect our proprietary information, in part, by the use of confidentiality and assignment of invention agreements with our employees, consultants, significant scientific collaborators and sponsored researchers that generally provide that all inventions conceived by the individual in the course of rendering services to us shall be our exclusive property.

The intellectual property underlying our technology is covered by certain patents and patent applications previously owned by the Johns Hopkins University ("JHU"). In early 2004, the intellectual property underlying the Company’s technologies was assigned from JHU to the co-inventors, Dr. John Isaacs, Dr. Soren Christensen, Dr. Hans Lilja and Dr. Samuel Denmeade, who in turn granted us an option to license the intellectual property in return for our continued prosecution of the patent portfolio. This option was exercised in early 2008 by payment to the co-inventors of past patent prosecution costs previously incurred by Johns Hopkins University (approximately $122,000) and additional fees (approximately $62,000) to cover the tax consequences of such payments to the co-inventors. Subsequently, the co-inventors assigned us the intellectual property in April of 2008 and we recorded these assignments in the United States Patent & Trademark Office. By virtue of the April 2008 assignments, we have no further financial obligations to the inventors or to JHU with regard to the assigned intellectual property. JHU retains a paid-up, royalty-free, non-exclusive license to use the intellectual property for non-profit purposes. Each of the co-inventors remains affiliated with the Company as a member of the Scientific Advisory Board.

| Number | Country | Filing Date | Issue Date | Expiration Date | Title | ||||||

| Patents Issued | |||||||||||

| 6,504,014 | US | 6/7/00 | 1/7/2003 | 6/6/2020 | Tissue specific pro-drug (TG) | ||||||

| 6,545,131 | US | 7/28/00 | 4/8/2003 | 7/27/2020 | Tissue specific pro-drug (TG) | ||||||

| 6,265,540 | US | 5/19/98 | 7/24/2001 | 5/18/2018 | Tissue specific pro-drug (PSA) | ||||||

| 6,410,514 | US | 6/7/00 | 6/25/2002 | 6/6/2020 | Tissue specific pro-drug (PSA) | ||||||

| 7,053,042 | US | 7/28/00 | 5/30/2006 | 7/27/2020 | Activation of peptide pro-drugs by HK2 | ||||||

| 7,468,354 | US | 11/30/01 | 12/23/08 | 11/29/2021 | Tissue specific pro-drug (G-202, PSMA) | ||||||

| Patents Pending | |||||||||||

| US 2004/0029778 | US | 11/30/01 | Pending | N/A | Tissue specific pro-drugs (PSMA) | ||||||

| PCT/US01/45100 | WO | 11/30/01 | Pending | N/A | Tissue specific pro-drugs (PSMA) | ||||||

| US 2006/0183689 | US | 8/24/05 | Pending | N/A | Activation of peptide pro-drugs by HK2 | ||||||

| US 2006/0217317 | US | 11/18/03 | Pending | N/A | Activation of peptide pro-drugs by HK2 | ||||||

| US 2008/0247950 | US | 3/15/07 | Pending | N/A | Activation of peptide pro-drugs by HK2 | ||||||

| US 2007/0160536 | US | 1/6/2006 | Pending | N/A | Tumor Activated Pro-drugs (PSA,G-115) | ||||||

| US 2009/0163426 | US | 11/25/08 | Pending | N/A | Tumor specific pro-drugs (PSMA) |

15

When appropriate, we will continue to seek patent protection for inventions in our core technologies and in ancillary technologies that support our core technologies or which we otherwise believe will provide us with a competitive advantage. We will accomplish this by filing and maintaining patent applications for discoveries we make, either alone or in collaboration with scientific collaborators and strategic partners. Typically, we plan to file patent applications in the United States. In addition, we plan to obtain licenses or options to acquire licenses to patent filings from other individuals and organizations that we anticipate could be useful in advancing our research, development and commercialization initiatives and our strategic business interest.

Manufacturing & Development

12ADT is manufactured by chemically modifying the cytotoxin thapsigargin, which is isolated from the seeds of Thapsia garganica, a plant found in the Mediterranean. Our pro-drug, G-202, is then manufactured by attaching a specific peptide to 12ADT.

Outsource Manufacturing

To leverage our experience and available financial resources, we do not plan to develop company-owned or company-operated manufacturing facilities. We plan to outsource all drug manufacturing to contract manufacturers that operate in compliance with GMP. We may also seek to refine the current manufacturing process and final drug formulation to achieve improvements in storage temperatures and the like.

Supply of Raw Materials – Thapsibiza SL

To our knowledge, there is only one commercial supplier of Thapsia garganica seeds. In April 2007, we obtained the proper permits from the United States Department of Agriculture (“USDA”) for the importation of Thapsia garganica seeds. In January 2008, we entered into a sole source agreement with this supplier, Thapsibiza, SL. The material terms of the agreement are as follows:

| Term | The term of the agreement is for 5 years. | |

| Exclusivity | Thapsibiza shall exclusively provide Thapsia garganica seeds to the Company. The Company has the ability to seek addition suppliers to supplement the supply from Thapsibiza, SL. | |

| Pricing | The price shall be 300 Euro/kg. Thapsibiza may, from time to time, without notice, increase the price to compensate for any increased governmental taxes. | |

Minimum Order | Upon successfully securing $5,000,000 of equity financing, and for so long as the Company continues to develop drugs derived from thapsigargin, the minimum purchase shall be 50kg per harvest period year. | |

| Indemnification | Once the product is delivered to an acceptable carrier, the Company shall be responsible for an injury or damage result from the handling of the product. Prior to delivery, Thapsibiza shall be solely responsible. |

Government Regulation

The FDA, as well as drug regulators in state and local jurisdictions, imposes substantial requirements upon the clinical development, manufacturing and marketing of pharmaceutical products. The process we are required by the FDA to complete before our drug compound may be marketed in the U.S. generally involves the following:

| · | Preclinical laboratory and animal tests; |

| · | Submission of an IND, which must become effective before human clinical trials may begin; |

16

| · | Adequate and well-controlled human clinical trials to establish the safety and efficacy of the product candidate for its intended use; |

| · | Submission to the FDA of an New Drug Application (“NDA”); and |

| · | FDA review and approval of an NDA. |

The testing and approval process requires substantial time, effort, and financial resources, and we cannot be certain that any approval will be granted on an expeditious basis, if at all. Preclinical tests include laboratory evaluation of the drug candidate, its chemistry, formulation and stability, as well as animal studies to assess the potential safety and efficacy of the drug candidate. Certain preclinical tests must be conducted in compliance with good laboratory practice regulations. Violations of these regulations can, in some cases, lead to invalidation of the studies, requiring such studies to be replicated. In some cases, long-term preclinical studies are conducted while clinical studies are ongoing.

The results of the preclinical tests, together with manufacturing information and analytical data, are submitted to the FDA as part of an IND, which must become effective before we may begin human clinical trials. The IND automatically becomes effective 30 days after receipt by the FDA, unless the FDA, within the 30-day time period, raises concerns or questions about the conduct of the trials as outlined in the IND and imposes a clinical hold. In such a case, the IND sponsor and the FDA must resolve any outstanding concerns before clinical trials can begin. Our submission of an IND may not result in FDA authorization to commence clinical trials. All clinical trials must be conducted under the supervision of a qualified investigator in accordance with good clinical practice regulations. These regulations include the requirement that all prospective patients provide informed consent. Further, an independent Institutional Review Board (“IRB”) at each medical center proposing to conduct the clinical trials must review and approve any clinical study. The IRB also monitors the study and must be kept informed of the study’s progress, particularly as to adverse events and changes in the research. Progress reports detailing the results of the clinical trials must be submitted at least annually to the FDA and more frequently if adverse events occur.

Human cancer drug clinical trials are typically conducted in three sequential phases that may overlap:

| · | Phase I: The drug candidate is initially introduced into cancer patients and tested for safety and tolerability at escalating dosages, |

| · | Phase II: The drug candidate is studied in a limited cancer patient population to further identify possible adverse effects and safety risks, to evaluate the efficacy of the drug candidate for specific targeted diseases and to determine dosage tolerance and optimal dosage. |

| · | Phase III: When Phase II evaluations demonstrate that a dosage range of the drug candidate may be effective and has an acceptable safety profile, Phase III trials are undertaken to further evaluate dose response, clinical efficacy and safety profile in an expanded patient population, often at geographically dispersed clinical study sites. |

Our business strategy is to bring our drug candidates through Phase I/II clinical trials before licensing them to third parties who would then further develop the drugs and seek marketing approval. Once the drug is approved, the third party licensee will be expected to market, sell, and distribute the products in exchange for some combination of up-front payments, royalty payments, and milestone payments. Management cannot be certain that we, or our licensees, will successfully initiate or complete Phase I, Phase II, or Phase III testing of our product candidates within any specific time period, if at all. Furthermore, the FDA or the IRB or the IND sponsor may suspend clinical trials at any time on various grounds, including a finding that the patients are being exposed to an unacceptable health risk.

Concurrent with clinical trials and pre-clinical studies, we also must develop information about the chemistry and physical characteristics of the drug and finalize a process for manufacturing the product in accordance with GMP requirements. The manufacturing process must be capable of consistently producing quality batches of the experimental drug, and management must develop methods for testing the quality, purity, and potency of the final experimental drugs. Additionally, appropriate packaging must be selected and tested.

The results of the drug development efforts and pre-clinical and clinical studies are then submitted to the FDA as part of an NDA for approval of the marketing and commercial shipment of the product. The FDA reviews each NDA submitted and may request additional information, rather than accepting the NDA for filing. In this event, the application must be resubmitted with the additional information included. The resubmitted application is also subject to review before the FDA accepts it for filing. Once the FDA accepts the NDA for filing, the agency begins an in-depth review of the NDA. The FDA has substantial discretion in the approval process and may disagree with our, or our licensees’, interpretation of the data submitted.

17

The review process may be significantly extended by FDA requests for additional information or clarification regarding information already provided. Also, as part of this review, the FDA may refer the application to an appropriate advisory committee, typically a panel of clinicians, for review, evaluation and a recommendation. The FDA is not bound by the recommendation of the advisory committee. Manufacturing establishments are also subject to inspections prior to NDA approval to assure compliance with GMPs and with manufacturing commitments made in the relevant marketing application.

Under the Prescription Drug User Fee Act (“PDUFA”), submission of an NDA with clinical data requires payment of a fee to the FDA, which is adjusted annually. For fiscal year 2009, that fee is $1,247,200. In return, the FDA assigns a goal (often months) for standard NDA reviews from acceptance of the application to the time the agency issues its “complete response,” in which the FDA may approve the NDA, deny the NDA if the applicable regulatory criteria are not satisfied, or require additional clinical data. Even if this data is submitted, the FDA may ultimately decide that the NDA does not satisfy the criteria for approval. If the FDA approves the NDA, the product becomes available for physicians to prescribe. Even if the FDA approves the NDA, the agency may decide later to withdraw product approval if compliance with regulatory standards is not maintained or if safety problems are recognized after the product reaches the market. The FDA may also require post-marketing studies, also known as Phase IV studies, as a condition of approval to develop additional information regarding the efficacy and safety of a product. In addition, the FDA requires surveillance programs to monitor approved products that have been commercialized, and the agency has the power to require changes in labeling or to prevent further marketing of a product based on the results of these post-marketing programs.

Satisfaction of the above FDA requirements or requirements of state, local and foreign regulatory agencies typically takes several years. Government regulation may delay or prevent marketing of potential products for a considerable period of time and impose costly procedures upon our activities. Management cannot be certain that the FDA or any other regulatory agency will grant approval for our lead product G-202 (or any other products we may develop, acquire, or in-license) under development on a timely basis, if at all. Success in preclinical or early-stage clinical trials does not assure success in later-stage clinical trials. Data obtained from preclinical and clinical activities are not always conclusive and may be susceptible to varying interpretations that could delay, limit or prevent regulatory approval. Even if a product receives regulatory approval, the approval may be significantly limited to specific indications or uses. Further, even after regulatory approval is obtained, later discovery of previously unknown problems with a product may result in restrictions on the product or even complete withdrawal of the product from the market. Delays in obtaining, or failures to obtain regulatory approvals would have a material adverse effect on our business.

Any products manufactured or distributed by us, or our licensees, pursuant to the FDA clearances or approvals are subject to pervasive and continuing regulation by the FDA, including record-keeping requirements, reporting of adverse experiences with the drug, submitting other periodic reports, drug sampling and distribution requirements, notifying the FDA and gaining its approval of certain manufacturing or labeling changes, complying with certain electronic records and signature requirements, and complying with the FDA promotion and advertising requirements. Failure to comply with these regulations could result, among other things, in suspension of regulatory approval, recalls, suspension of production or injunctions, seizures, or civil or criminal sanctions. Management cannot be certain that our present or future subcontractors or licensees will be able to comply with these regulations and other FDA regulatory requirements.

Our product candidates are also subject to a variety of state laws and regulations in those states or localities where our lead product G-202 (and any other products we may develop, acquire, or in-license) will be marketed. Any applicable state or local regulations may hinder our ability to market our lead product G-202 (and any other products we may develop, acquire, or in-license) in those states or localities. In addition, whether or not FDA approval has been obtained, approval of a pharmaceutical product by comparable governmental regulatory authorities in foreign countries must be obtained prior to the commencement of clinical trials and subsequent sales and marketing efforts in those countries. The approval procedure varies in complexity from country to country, and the time required may be longer or shorter than that required for FDA approval. We may incur significant costs to comply with these laws and regulations now or in the future.

The FDA’s policies may change, and additional government regulations may be enacted which could prevent or delay regulatory approval of our potential products. Moreover, increased attention to the containment of health care costs in the U.S. and in foreign markets could result in new government regulations that could have a material adverse effect on our business. Management cannot predict the likelihood, nature or extent of adverse governmental regulation that might arise from future legislative or administrative action, either in the U.S. or abroad.

Other Regulatory Requirements

The U.S. Federal Trade Commission and the Office of the Inspector General of the U.S. Department of Health and Human Services (“HHS”) also regulate certain pharmaceutical marketing practices. Also, reimbursement practices and HHS coverage of medicine or medical services are important to the success of procurement and utilization of our product candidates, if they are ever approved for commercial marketing.

We are also subject to numerous federal, state and local laws relating to such matters as safe working conditions, manufacturing practices, environmental protection, fire hazard control, and disposal of hazardous or potentially hazardous substances. We may incur significant costs to comply with these laws and regulations now or in the future. Management cannot assure you that any portion of the regulatory framework under which we currently operate will not change and that such change will not have a material adverse effect on our current and anticipated operations.

18

Employees

As of July 31, 2009 we employed 2 individuals who are also our 2 executive officers.

PROPERTIES

Our executive offices are located at 9901 IH 10 West, Suite 800, San Antonio, TX, 78230. We lease this facility consisting of approximately 200 square feet, for $1800 per month inclusive of receptionist, telecommunication, and internet services. Our lease expires on September 30, 2009.

We also rent a virtual office at 12100 Wilshire Blvd, 8th Floor, Los Angeles, CA 90025 to maintain a business presence in that state and for meetings with participants who are located within travel distance to Los Angeles so as not to require travel exclusively to our executive office in San Antonio. This contract carries forward on a month by month basis at a charge of $210 per month.

The aforesaid properties are in good condition and we believe they will be suitable for our purposes for the next 12 months. There is no affiliation between us or any of our principals or agents and our landlords or any of their principals or agents.

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL

CONDITION AND RESULTS OF OPERATIONS

This Management’s Discussion and Analysis of Financial Condition and Results of Operations section (“MD&A”) contains statements and information about management’s view of our future expectations, plans and prospects, that constitute forward-looking statements. These statements are subject to risks and uncertainties that could cause actual results and events to differ materially from those we anticipate. We undertake no obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise.

Our MD& is organized as follows:

| • | Overview — Discussion of our business and plan of operations, overall analysis of financial and other highlights affecting the company in order to provide context for the remainder of MD&A. |

| • | Significant Accounting Policies — Accounting policies that we believe are important to understanding the assumptions and judgments incorporated in our reported financial results and forecasts. |

| • | Results of Operations — Analysis of our financial results comparing: (i) the first quarter of 2009 to the comparable period in 2008; and (ii) our financial results for 2008 to 2007. |

| • | Liquidity and Capital Resources — A discussion of our financial condition and potential sources of liquidity. |

The various sections of this MD&A contain a number of forward-looking statements. Words such as “expects,” “goals,” “plans,” “believes,” “continues,” “may,” and variations of such words and similar expressions are intended to identify such forward-looking statements. In addition, any statements that refer to projections of our future financial performance, our anticipated growth and trends in our businesses, and other characterizations of future events or circumstances are forward-looking statements. Such statements are based on our current expectations and could be affected by the uncertainties and risk factors described throughout this filing and particularly in the Risk Factors section of this Prospectus. Our actual results may differ materially.

Overview

We are a development stage company focused on the development of targeted cancer therapeutics for the treatment of cancerous tumors, including breast, prostate, bladder and kidney cancer. Our operations are based in San Antonio, TX.

Management's Plan of Operation

We are pursuing a business plan related to the development of targeted cancer therapeutics for the treatment of cancerous tumors, including breast, prostate, bladder and kidney cancer. We are considered to be in the development stage as defined by SFAS No. 7, “Accounting and reporting by Development Stage Enterprises“.

19

Business Strategy

Our business strategy is to develop a series of therapeutics based on our target-activated pro-drug technology platform and bring them through Phase I/II clinical trials. At that point, we plan to license the rights to further development of the drug candidates to major pharmaceutical companies. We believe that major pharmaceutical companies see significant value in drug candidates that have passed one or more phases of clinical trials, and these organizations have the resources and expertise to finalize drug development and market the drugs.

Plan of Operation

We have made significant progress in key areas such as drug manufacture, toxicology, and pre-clinical activities for our lead compound G-202.