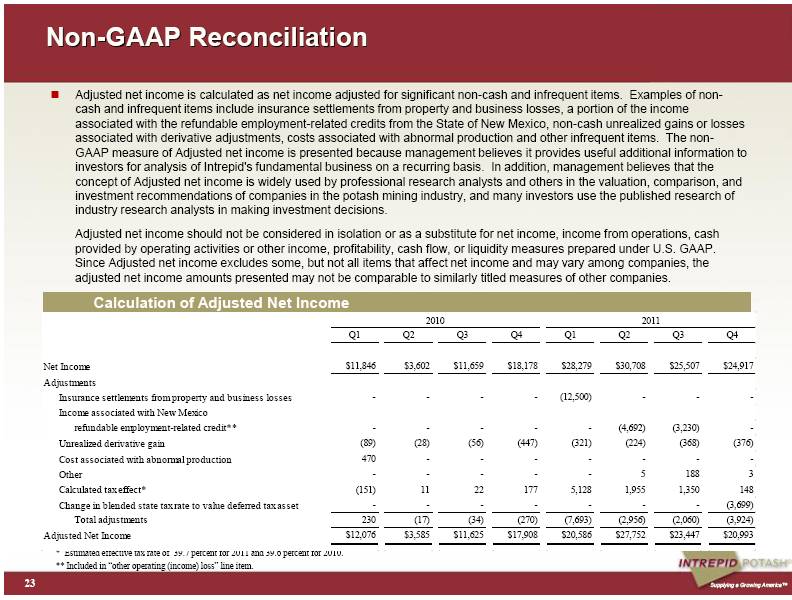

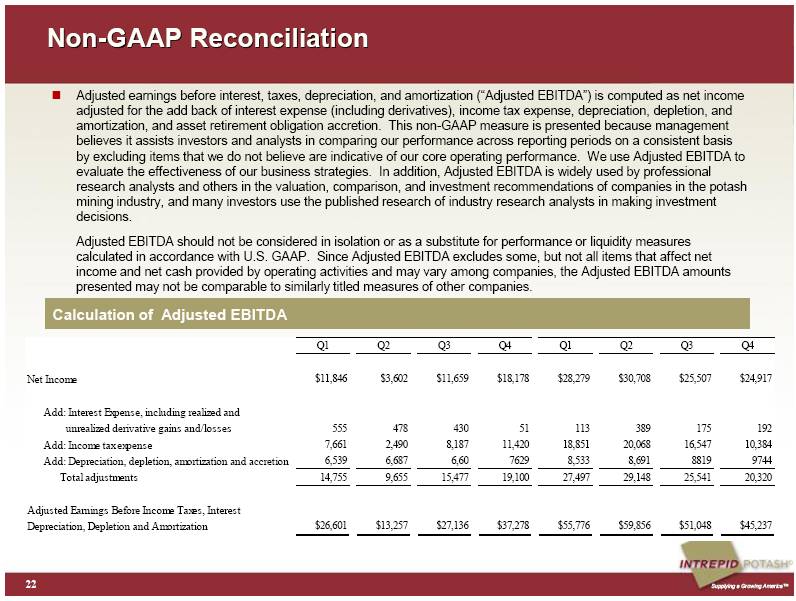

| Calculation of Adjusted EBITDA 22 Non-GAAP Reconciliation Adjusted earnings before interest, taxes, depreciation, and amortization (“Adjusted EBITDA”) is computed as net income adjusted for the add back of interest expense (including derivatives), income tax expense, depreciation, depletion, and amortization, and asset retirement obligation accretion. This non-GAAP measure is presented because management believes it assists investors and analysts in comparing our performance across reporting periods on a consistent basis by excluding items that we do not believe are indicative of our core operating performance. We use Adjusted EBITDA to evaluate the effectiveness of our business strategies. In addition, Adjusted EBITDA is widely used by professional research analysts and others in the valuation, comparison, and investment recommendations of companies in the potash mining industry, and many investors use the published research of industry research analysts in making investment decisions. Adjusted EBITDA should not be considered in isolation or as a substitute for performance or liquidity measures calculated in accordance with U.S. GAAP. Since Adjusted EBITDA excludes some, but not all items that affect net income and net cash provided by operating activities and may vary among companies, the Adjusted EBITDA amounts presented may not be comparable to similarly titled measures of other companies. Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 $11,846 $3,602 $11,659 $18,178 $28,279 $30,708 $25,507 $24,917 7,661 2,490 8,187 11,420 18,851 20,068 16,547 10,384 6,539 6,687 6,60 7629 8,533 8,691 8819 9744 Total adjustments 14,755 9,655 15,477 19,100 27,497 29,148 25,541 20,320 $26,601 $13,257 $27,136 $37,278 $55,776 $59,856 $51,048 $45,237 Depreciation, Depletion and Amortization 113 555 478 430 Add: Depreciation, depletion, amortization and accretion Adjusted Earnings Before Income Taxes, Interest 175 Net Income Add: Income tax expense Add: Interest Expense, including realized and unrealized derivative gains and/losses 192 51 389 |