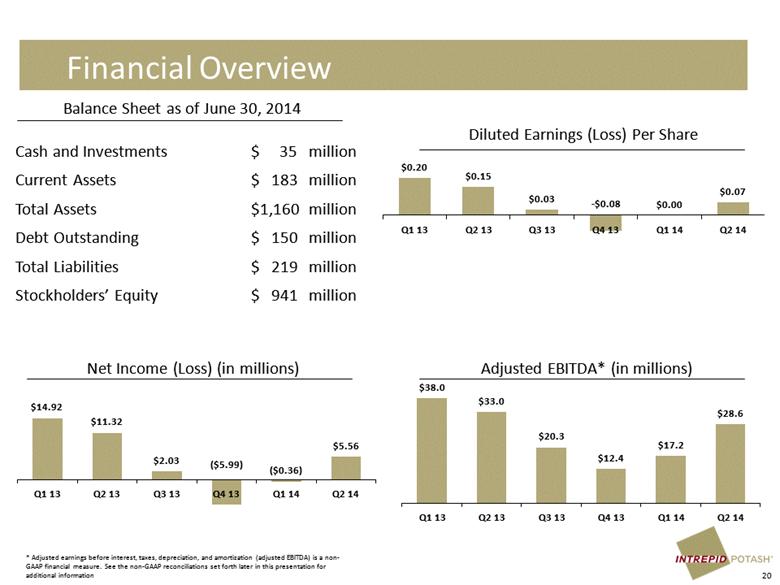

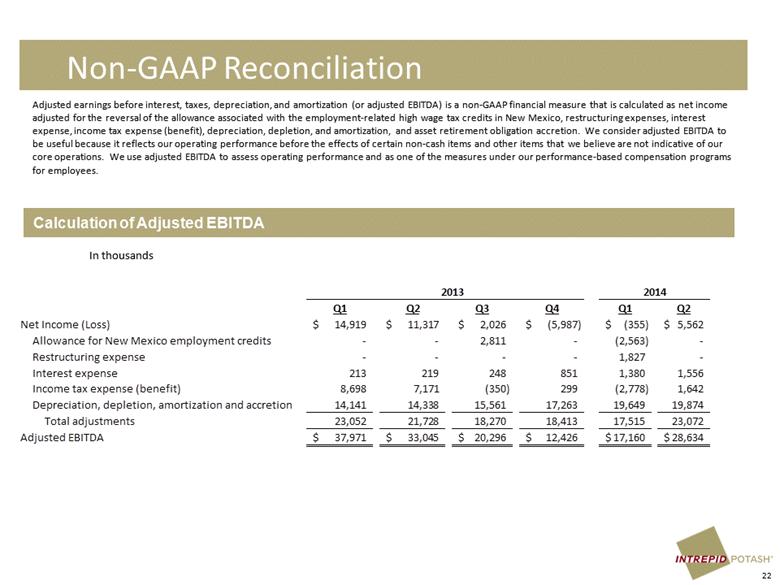

| Non-GAAP Reconciliation Calculation of Adjusted EBITDA Adjusted earnings before interest, taxes, depreciation, and amortization (or adjusted EBITDA) is a non-GAAP financial measure that is calculated as net income adjusted for the reversal of the allowance associated with the employment-related high wage tax credits in New Mexico, restructuring expenses, interest expense, income tax expense (benefit), depreciation, depletion, and amortization, and asset retirement obligation accretion. We consider adjusted EBITDA to be useful because it reflects our operating performance before the effects of certain non-cash items and other items that we believe are not indicative of our core operations. We use adjusted EBITDA to assess operating performance and as one of the measures under our performance-based compensation programs for employees. 22 In thousands 2013 2014 Q1 Q2 Q3 Q4 Q1 Q2 Net Income (Loss) 14,919 $ 11,317 $ 2,026 $ (5,987) $ (355) $ 5,562 $ Allowance for New Mexico employment credits - - 2,811 - (2,563) - Restructuring expense - - - - 1,827 - Interest expense 213 219 248 851 1,380 1,556 Income tax expense (benefit) 8,698 7,171 (350) 299 (2,778) 1,642 Depreciation, depletion, amortization and accretion 14,141 14,338 15,561 17,263 19,649 19,874 Total adjustments 23,052 21,728 18,270 18,413 17,515 23,072 Adjusted EBITDA 37,971 $ 33,045 $ 20,296 $ 12,426 $ 17,160 $ 28,634 $ |