Gramercy Site Visit Exhibit 99.1 Noranda Aluminum Holding Corp August 4, 2010 |

2 Forward Looking Statements The following information contains, or may be deemed to contain, "forward- looking statements" (as defined in the U.S. Private Securities Litigation Reform Act of 1995). By their nature, forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. The future results of the issuer may vary from the results expressed in, or implied by, the following forward looking statements, possibly to a material degree. For a discussion of some of the important factors that could cause the issuer's results to differ from those expressed in, or implied by, the following forward-looking statements, please refer to our filings with the SEC, including our annual report on Form 10-K. |

3 Management Presenters Layle K. “Kip” Smith, President and Chief Executive Officer Robert Mahoney, Chief Financial Officer Ramon Gil, President, Noranda Alumina LLC |

4 Noranda Strategy Noranda Operating Model “Off to a Good Start…” Industry Dynamics Brief Noranda Alumina History Second quarter results: Successful performance while completing foundational projects that strengthened Noranda |

5 Second Quarter Highlights Noranda produced strong current quarter results… – Net income was $6.9 million ($0.14 per share), and includes the net negative impact of $11 million, or $0.21 per share, from special items – Operating cash flow was $118 million – Adjusted EBITDA was $79 million total, and $62 million excluding hedges – External volumes grew over 2Q-09 and 1Q-10 – Integrated cash cost for primary aluminum production improved to $0.66/lb – CORE contributed over $15 million in cost reduction, capital avoidance, and cash generation – Total indebtedness was $554 million, representing a 24% decrease from 1Q-10 – Cash and cash equivalents balances totaled $32 million. Senior revolving credit facility had no outstanding borrowings and $215 million available capacity … while setting a foundation for long-term value – Completed IPO as part of broad program to increase strategic flexibility, position company for growth and improve financial profile – Obtained favorable result in New Madrid power rate case – Signed final agreements for Jamaican fiscal regime |

6 Expect steady demand for billet/rod, subject to normal seasonal trends Primary Aluminum Products pricing to follow one month lag on LME Peak power rates apply throughout 3Q-10 Most cost inputs contracted through end of year at fixed prices; upward pressure on others Integrated cash cost is $0.66 for Q2-10; normalizing Q1-10 for smelter volume and alumina ramp up, YTD cost is $0.67 Strong Q2-10 demand in key primary aluminum product groups. Billet and rod up 40% and 7% against Q2-09. Billet and rod shipments up 21% and 22% against Q1-10 CORE initiatives and favorable input prices offset bauxite shipping delays, alumina ramp-up, and legal costs related to power case 2009 Normalized 3MOE 6/30/10 6MOE 6/30/10 LME 1.00 0.97 0.98 Midwest Premium 0.06 0.06 0.06 Midwest Transaction Price 1.06 1.04 1.04 Net integrated cash cost of primary aluminum 0.67 0.66 0.67 Integrated upstream margin per pound 0.39 0.38 0.37 Dollars per Pound Integrated Upstream Business Review Trends Trends Near-term Outlook Comments Comments Upstream Margin Upstream Margin 0 50 100 150 200 250 300 350 400 450 500 550 $- $0.10 $0.20 $0.30 $0.40 $0.50 $0.60 $0.70 $0.80 $0.90 $1.00 $1.10 2Q09 3Q09 4Q09 1Q10 2Q10 LME ($ per lb) Bauxite (kMt) Alumina (kMt) Primary aluminum (000 pounds) Left Axis Right Axis Right Axis Right Axis |

7 2009 Normalized(1) 3MOE 6/30/10 6MOE 6/30/10 Total primary aluminum shipments 580 147 267 Integrated upstream margin on cash cost 0.39 $ 0.38 $ 0.37 $ Integrated upstream EBITDA 224 $ 55 $ 99 $ Rolled products fabrication margin 35 15 26 Run-rate corporate expenses (29) (7) (14) Total Unhedged EBITDA 230 $ 62 $ 111 $ Corporate Summary Strong Q2-10 performance reflects impact of productivity programs and management execution, with help from improved aluminum prices Q2-10 improvements in cash cost validate $0.67 annual normalized 2009 benchmark Q2-10 rolled product results well ahead of 2009 Corporate expenses tracking to 2009 or better Expected GAAP annual effective tax rate is 33.6% Still have hedge accounting gains to reclassify through GAAP earnings, despite termination of aluminum hedges ($22 million per quarter in 3Q-10 and Q4-10) (1) Normalized based on $1.00 LME, $0.06 Mid-west Premium Comments Comments Business Summary Business Summary Corporate Cost Trends Corporate Cost Trends Near-term Outlook 2Q09 3Q09 4Q09 1Q10 2Q10 Corporate SG&A (GAAP) 7.9 9.2 7.2 9.7 28.8 Consulting Fees (0.7) (1.7) (1.1) (4.1) Stock Compensation (0.4) (1.0) (0.4) (0.4) (3.6) Apollo Fees (0.5) (0.5) (0.5) (0.5) (13.0) Restructuring - - - - (0.2) Other (1.4) 3.6 2.3 (1.2) (0.7) Run-rate corporate costs 5.0 11.4 6.9 6.5 7.3 |

Noranda Strategy Brief Noranda Alumina History “Off to a Good Start…” Industry Dynamics Noranda Operating Model Though we can’t control the LME, we exercise significant control and influence over the basic drivers of our success 8 |

Mission Every day we build a sustainable, integrated aluminum company founded on growth and successful long-term relationships with our customers, co-workers, suppliers, communities and investors 9 |

10 Noranda’s Integrated Operating Footprint Downstream Business Downstream Business Annual Capacity: 495mm lbs (2) St. Ann Bauxite Mine New Madrid Aluminum Smelter Newport Rolling Mills Salisbury Rolling Mills East Mill West Mill Huntingdon Rolling Mills Bauxite Discovery Bay, Jamaica 4.5mm Mt Alumina Gramercy, LA 1.2mm Mt Aluminum Primary Metal New Madrid, MO 263k Mt (580mm lbs) Fin stock (HVAC) and Auto, Semi-Rigid Container Stock, Flexible Packaging, Transformer Windings Huntingdon, TN Huntingdon West 235mm lbs (2) Huntingdon East 130mm lbs Newport, AR 35mm lbs Salisbury, NC 95mm lbs Products: Location: Annual Capacity: Upstream Business Upstream Business Annual Capacity: 580mm lbs 2009 Cash Cost at Full Production: $0.72 / lb (1) Gramercy Refinery Revenue Drivers: Volume & LME Residential construction / remodeling, packaging, U.S. consumer (1) We estimate that due to lost production volume in 2009 from the smelter outage, which caused lost efficiency and fixed cost absorption, our upstream cash cost of primary aluminum for FYE 2009 of $0.77 per pound was negatively impacted by $0.05 per pound. (2) Maximum capacity, with actual capacity depending upon production mix. |

11 Primary Aluminum Alumina Noranda Bauxite Mine Noranda Alumina Refinery New Madrid Primary Aluminum Smelter Bauxite The integration of our Upstream Business is the lynchpin to our strategy and sustainability – Significant Operating Leverage to LME • Integration provides for a more “fixed” cost base relative to non-integrated producers whose margins may be eroded by rising input costs that are correlated to LME • Third party sales of excess raw materials (e.g., bauxite and alumina) enhance our leverage to LME – Secure Supply • For our smelter and refinery, we have the ability to provide over 100% of our needs of alumina and bauxite – Low Cost & Operating Flexibility • Expanded portfolio of opportunities to drive cost out and increase productivity and sales Our strategy is founded on integrated production, cost independence from the LME, growth & productivity Vertically Integrated Upstream Business |

12 Geographic Mix Low Cost, Leading – Rolling Mill Operations Low cost Production – Huntingdon West is the foil mill with the lowest conversion cost in North America according to CRU – CORE Productivity – Footprint efficiency Flexibility – 10-30% of prime metal comes from New Madrid, but inter-company volume can be varied based on market conditions Focused Growth – Grow with key customers to “Win with Winners” – Increase share of demand – Top 10 customers 56% of sales Huntingdon, TN 2 plants, East and West Started 1967 & 2000 Max. East capacity: 130mm lbs Max. West capacity: 235mm lbs (1) Newport, AR Started 1951 Max. Capacity: 35mm lbs (1) Salisbury, NC Started 1965 Max. Capacity: 95mm lbs Four Rolling Mills in Three States 40% 17% 4% 4% Southeast USA West USA Northeast USA Midwest USA 34% Southwest USA Mexico 1% HVAC fin stock Container Transformer sheet Foil products Light gauge sheet Products Downstream Segment is a stable free cash flow generator (1) Capacity includes intracompany reroll of approximately 45mm lbs. |

13 Noranda Strategy Brief Noranda Alumina History “Off to a Good Start…” Industry Dynamics Noranda Operating Model Gramercy provides a critcial supply of alumina as part of our intergrated strategy |

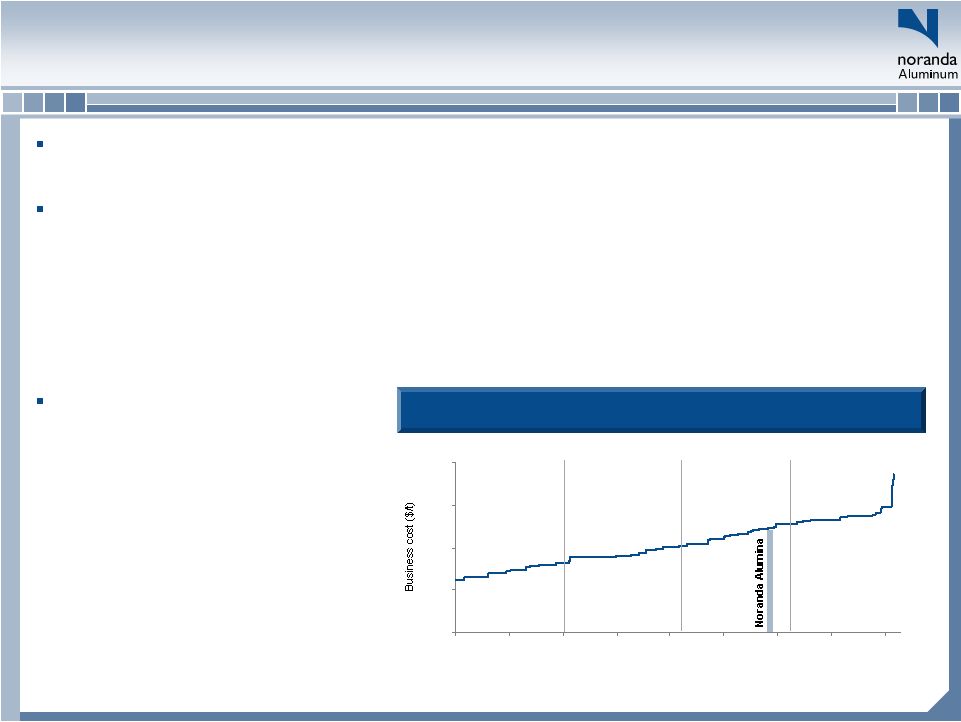

Noranda Bauxite and Alumina Overview On August 31, 2009, Noranda became the sole owner of the Gramercy refinery and St. Ann Bauxite operation – Noranda Bauxite – St. Ann – Economic joint venture with Government of Jamaica • Government receives royalties and levies, with Noranda controlling the business and output • Noranda maintains strong government relations with a new 6-year fiscal regime negotiated in 2009 – 4.5 million tonnes of annual production capacity with ~60% sold to Gramercy • Remaining production sold to Sherwin Alumina pursuant to a contract that was recently extended in principal through 2012 – CRU estimates that St. Ann was in the 2nd Quartile for site operating costs globally in 2009 $0 $100 $200 $300 $400 0 10000 20000 30000 40000 50000 60000 70000 80000 1 Quartile 2 Quartile 3 Quartile 4 Quartile Production (kt) Noranda Alumina - Gramercy – 1.2M mt per year production capacity for Smelter Grade Alumina (SGA) and Chemical Grade Alumina (CGA) – ~0.5mm Mt provided to New Madrid with remainder sold to third parties – One of three producers in the U.S., providing ~0.2mm Mt of CGA – Stable end market with attractive characteristics that complement the commodity SGA product group – 3-years of SGA sales contracted with credit- worthy customers CRU’s 2009 Alumina Cost Curve (1) _______________________ (1) Noranda cost curve position excludes benefits of 3 party bauxite and alumina sales. 14 st nd rd th rd Strategic drivers: integrated supply, productivity, sales growth – increased leverage to LME |

A Brief History of Noranda Alumina, LLC Construction on the alumina refinery began in 1957 with the first shipment of alumina occurring two years later. The Gramercy facility was originally owned by Kaiser. The refinery utilizes the Bayer process to chemically extract alumina from bauxite. Construction on the first red mud pond began in 1974. The refinery has undergone several expansions and modernizations since 1957 to increase annual capacity from .4 million metric tonnes to 1.2 million metric tonnes. In July 1999 the refinery shut down due to an explosion of the digestion unit. The refinery reopened in December 2000. In 2004, Noranda formed a joint partnership with Century Aluminum and purchased the Gramercy refinery and the St. Ann bauxite mining operations from Kaiser. In 2009, Noranda became sole owner of the refinery, which now operates as Noranda Alumina, LLC. 15 |

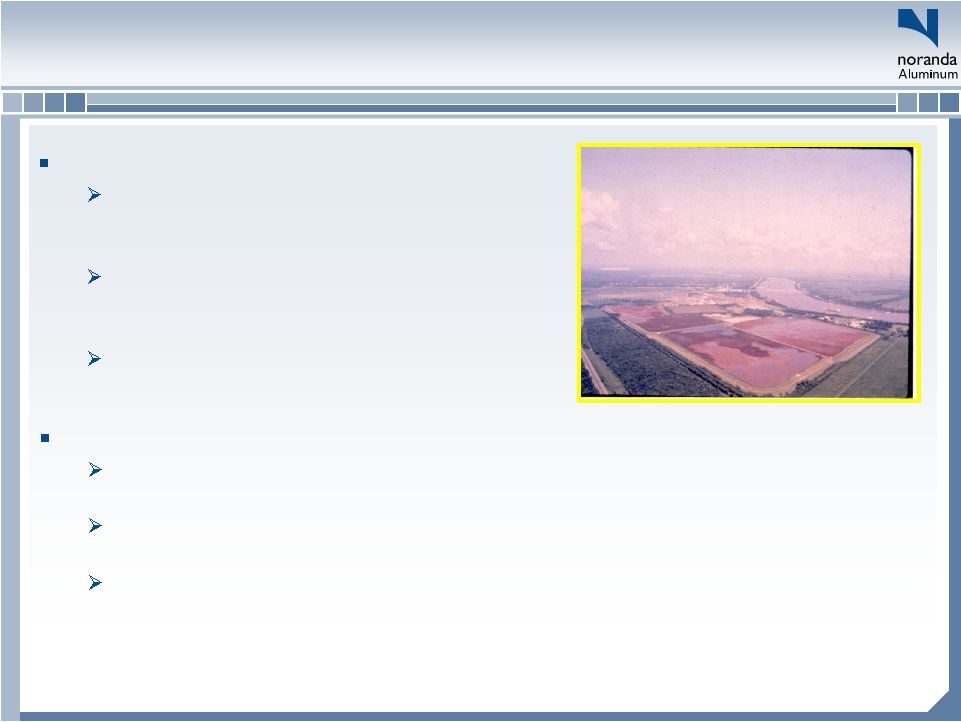

Red Mud Lakes Once alumina has been extracted, spent bauxite (‘red mud”) is managed in one of 4 Mud Lakes. Mud Lakes are permitted solid waste units designed to dewater the material and act as a final repository. Noranda Alumina has obligation to seal the Mud Lakes once they are no longer used. Environmental Bona Fide Prospective Purchase (BFPP) Protection Noranda and Century commissioned a pre-purchase due diligence investigation of the environmental conditions present at the refinery in 2004. State environmental officials ruled Gramercy met conditions for BFPP protections against liability for preexisting environmental conditions. Gramercy recorded a liability for the estimated cost for the BFPP remediation work and continues to monitor and update such estimates as necessary; Kaiser provided cash funding as part of transaction. 16 |

Safety is a Core Value MSHA Regulated Facility Maintains Process Safety Management program in addition to Occupational Safety Employee Involvement (ERT, Safe Start, JSC, Safety Recognition) Maintenance activities planned and scheduled Supported by SAP (CMMS) Health & Safety 17 |

Noranda Strategy Brief Noranda Alumina History “Off to a Good Start…” Industry Dynamics Noranda Operating Model We have two #1 Priorities: Get the Results, and Do the Right Things the Right Way 18 |

Our Two #1 Priorities Noranda has two number one priorities Do the right things the right way Get the results •Individual Behaviors •Team Disciplines •Sustainable Relationships •Legal •Ethical •Credible 19 |

Get the Results Get the Results Do the Right Things Do the Right Things the Right Way the Right Way Action oriented Ethics and Values Drive for results Process Management Safety Focus Problem solving Peer relationships Priority setting Managing through systems Existing for Customers Caring for Customers Respecting Suppliers Enriching Communities Rewarding Investors Two #1 Two #1 Priorities Priorities Sustainable Sustainable Goals Goals Core Core Values Values Noranda Mission |

Financial success in adverse conditions Reduced Production Cost Reduced Production Cost Improved Demand Share Improved Demand Share Reduced Debt Reduced Debt Generated More Cash (Free Cash Flow) Generated More Cash (Free Cash Flow) (Millions of dollars) 21 |

Reconciliation of EBITDA to Net Income 22 Comments Adjusted EBITDA for three months ended June 30, 2010 78.8 $ Interest (Expense)/Income, Net (8.5) prospectively, based on post-IPO debt balances at applicable interest rates (1) Depreciation & Amortization (25.1) 2Q is reasonable proxy going forward, at $25 million per quarter (2) LIFO/LCM (9.9) Will vary from period-to-period with LME and inventory levels Interest Rate Swap MTM (5.6) Will vary from period-to-period with change in notional and market LIBOR (3) MTM (Loss)/Gain on NatGas (5.8) Will vary from period-to-period with change in hedged volume and Henry Hub (3) AOCI Reclassification of Alim. Hedges 22.2 Set amount, with next 12 months disclosed (4) AOCI Reclassification of NatGas Hedges (1.5) Relatively predictable amount, with estimate for next 12 months disclosed (4) Stock Compensation Expense (3.8) 2Q-10 contained $3.2 million of acceleration Non-Cash Pension Expense (1.8) Approximately $1.8 million per quarter, based on 2Q amounts (5) Other on-going items (1.0) Represents gains and losses on asset disposals, other, say $1 million per quarter (6) Gain) loss on debt repurchase (2.5) Would continue after 2Q-10 only when there are are debt paydowns Charges related to termination of derivatives (4.9) Doesn't continue after 2Q-10 Restructuring and sponsor fees (20.3) Doesn't continue after 2Q-10 Pre-Tax Income 10.3 Income tax expense 3.4 At 2Q, forecasted annual GAAP rate was disclosed as 33.6% (7) 6.9 $ Weighted average shares 49.1 3Q will be based on amount outstanding at end of 2Q-10 (8) Diluted options 1.0 Will vary based on stock price, but Q2-10 is appropriate proxy (9) Diluted shares 50.1 Diluted EPS 0.14 $ (1) See page 12 of June 2010 Form 10-Q for balance and rate information. (2) See page 50 of June 2010 Form 10-Q for 2Q-10 actual amount. (3) See page 19 of June 2010 Form 10-Q for hedged quantities and rates. (4) See page 19 of June 2010 Form 10-Q for amounts to be reclassified in future. (5) See page 52 of June 2010 Form 10-Q for Q2-10 actual amount. (6) See page 52 of June 2010 Form 10-Q for LTM "Loss on disposal" (0.4 million) and "other" (0.6 million). (7) See page 17 of June 2010 Form 10-Q for 33.6% annual 2010 rate. (8) See cover of June 2010 Form 10-Q for most recent share number. (9) See page 23 of June 2010 Form 10-Q for Q2-10 impact of dilutive securities. Note: Amounts in millions, except per share data |

Noranda Strategy Brief Noranda Alumina History “Off to a Good Start…” Industry Dynamics Noranda Operating Model Noranda is well positioned to take advantage of a recovery in Aluminum prices 23 |

1300 1500 1700 1900 2100 2300 2500 2700 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 Market Fundamentals Global demand for aluminum is expected to continue to increase… Aluminum’s consensus estimated sustainable price is meaningfully above current prices… We hold a positive outlook for Aluminum’s fundamentals over the medium and long-term, based on two views: Consumption Growth Driven by China Total Consumption (1) 30.4 37.4 44.3 55.6 65.4 China Consumption (1) 6.1 12.6 18.4 25.0 30.1 -- 23% 18% 26% 18% % Growth -- 108% 46% 36% 20% % Growth Source: CRU (1) In millions of tonnes Prices Below Consensus Sustainable Level Source: Harbor intelligence ALUMINUM LONG TERM MINIMUM EQUILIBRIUM PRICE (annual average; consensus forecasts from up to 20 analysts) ESTIMATED LT MINIMUM EQUILIBRIUM $2,450 CASH PRICE $2,109 so far 2010 24 |

Source: Davenport Chinese Aluminum Consumption & Production China – Analysis Revaluation of the RMB – stronger RMB relative to the dollar Increases purchasing power of RMB – increased ability to import products (aluminum) Dollar denominated prices increase – LME price per tonne will increase in USD, supporting smelters located in the US China historically has produced at or near its aluminum consumption China has imposed severe export taxes on aluminum Exports are highly unlikely CRU forecasts China being net importers of Aluminum in the medium term Power – China is already short of power Unstable prices Job creation as a primary goal More efficient uses of power exist that create more jobs per kilowatt hour of electricity 25 |