Quanex Building Products Acquires HL Plastics June 16, 2015 Exhibit 99.1 |

Safe Harbor 1 Statements made during this presentation that use the words “estimated,” “expect,” “could,” “should,” “believe,” “will,” “might,” or similar words reflecting future expectations or beliefs are forward-looking statements. The forward-looking statements include, but are not limited to, references to synergies derived from acquisitions, future operating results of Quanex, the financial condition of Quanex, future uses of cash, expectations relating to capital and other expenditures, expenses and tax rates, expectations relating to the company’s industry, and the company’s future growth. The statements made during this presentation are based on current expectations. Actual results or events may differ materially from those described during this presentation. Factors that could impact future results may include, without limitation, the effect of both domestic and global economic conditions, the impact of competitive products and pricing, the availability and cost of raw materials, and customer demand, among others. For a more complete discussion of factors that may affect the company’s future performance, please refer to the company’s 10-K filing on December 12, 2014, under the Securities Exchange Act of 1934 (“Exchange Act”), in particular the section titled, “Private Securities Litigation Reform Act” contained therein. |

2 Transaction Overview Quanex has acquired HL Plastics for £95M ($149M) An excellent strategic fit, adding: • A great business – Fastest growing vinyl extruder in the UK • In an attractive market – Higher end and lower complexity than US • At a good time – Early in the UK housing/window recovery Expected to be accretive to EPS, EBITDA margins and ROIC • 2016 EPS accretion estimated between $0.20-$0.25 per share • EBITDA margin (18%) delivers on Quanex objective of improving total company margin towards 15% target • Expected to deliver IRR well in excess of WACC Adds $25M-$30M to mid-cycle EBITDA guidance Funded with cash and Quanex’s existing $150M credit facility Pro forma 4/30/15 leverage of 1.5x total debt/EBITDA at close Note: HL Plastics figures converted to USD at 1.57 USD / GBP Note on Non-GAAP Financial Measures: EBITDA (defined as net income or loss before interest, taxes, depreciation and amortization and other, net, as described in Quanex’s filings with the Securities and Exchange Commission) is a non-GAAP financial measure that Quanex's management uses to measure its operational performance and assist with financial decision-making. EBITDA is a key metric used by management in determining the value of annual incentive awards for its employees. Quanex believes this non-GAAP measure provides a consistent basis for comparison between periods, and will assist investors in understanding our financial performance when comparing our results to other investment opportunities. EBITDA may not be the same as that used by other companies. While the Company considers EBITDA to be an important measure of operating performance, the company does not intend for this information to be considered in isolation or as a substitute for net income or other measures prepared in accordance with US GAAP. Due to the high variability and difficulty in predicting certain items that affect GAAP net income (including in respect of the impact of HL Plastics), information reconciling forward-looking EBITDA as presented to GAAP financial measures is unavailable to Quanex without unreasonable effort. ROIC (or Return on Invested Capital), a financial measure used to quantify the returns Quanex earns on its invested capital, and IRR (or Internal Rate of Return), a metric that measures the net present value of all cash flows from a capital project or investment (both capital deployed and after tax cash flows received), are also non-GAAP financial measures. Quanex believes ROIC and IRR are meaningful indicators of performance and useful metrics for investors and financial analysts. Quanex’s calculations of ROIC and IRR may not be comparable to similarly titled definitions used by other companies and are not substitutes for financial information prepared in accordance with GAAP. |

3 Attractive Opportunity Consistent with Strategy Clear fit with Quanex’s core businesses Complementary technology and capabilities Best-in-class manufacturing operations Outstanding management team and employee base Strong, stand-alone platform requiring minimal operational integration Fastest growing vinyl window profile extruder in attractive U.K. market Strong margins and free cash flow Platform for future growth in Europe HL Plastics acquisition is consistent with Quanex’s strategic objectives of pursuing M&A opportunities that provide market leadership, superior technology and attractive financial returns |

4 HL Plastics Company Overview Note: HL Plastics figures converted to USD at 1.57 USD / GBP Market leader and fastest growing vinyl window / door profile extruder in the UK Goes to market under Liniar brand name Headquartered in Denby, UK Employees: 420 Trailing twelve months revenue of £64M ($101M) and EBITDA of £12M ($18M) 2012 – 2014 revenue growth of 50% State-of-the-art manufacturing capabilities with ample capacity Superior technology with most energy efficient profile system in the UK Diverse customer base across UK and Ireland Strong and experienced management team Outstanding, stand-alone platform Revenue by Geography (2014) Revenue by Product (2014) Verandahs and Decking Bi-fold and Patio Doors Conservatory Roof Systems Windows Windows Verandahs and Decking Bi-fold and Patio Conservatory Roof Systems Wegoma Vintage 78% 8% 6% 3% 3% 2% U.K. Rest of Europe Other 95% 4% <1% |

5 HL Plastics Product Review Leading Liniar brand with co-branding opportunity for components Verandahs and Decking Bi-fold and Patio Doors Conservatory Roof Systems Wegoma Vintage Windows PVCu based products in this category provide an alternative to more traditional wood based products whilst also providing products with a recycled content base One of the first bespoke bi-fold doors into the market providing a number of product variations Liniar’s own proprietary conservatory roof system and other product sales Provides specialist machines into the window fabrication market Provides niche window manufacturing and product development Liniar PVCu windows are the most technically advanced in the market and designed in-house to meet the highest energy efficiency and safety standards |

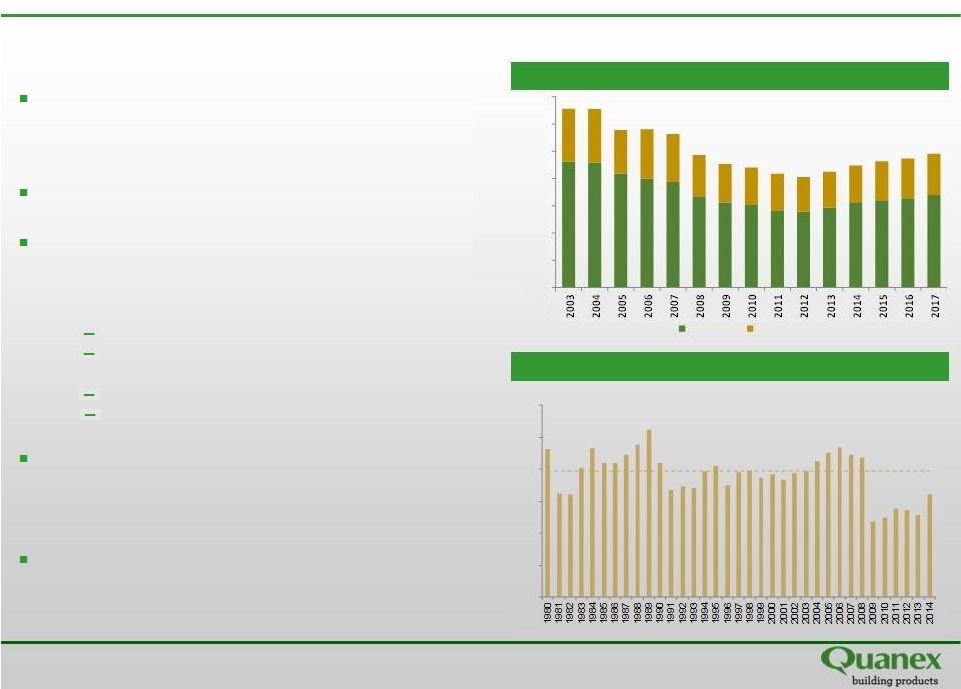

6 U.K. Vinyl Profiles Market Overview Favorable UK market dynamics Source: D&G Consulting – Autumn /Winter 2014 Historical UK Housing Starts (MM’s) Median: 197 UK Vinyl Profiles Production Source: UK Department for Communities and Local Government (In Tonnes) 0 50,000 100,000 150,000 200,000 250,000 300,000 350,000 Windows Other 0 50 100 150 200 250 300 Fragmented UK window and door market • ~1/3 size of N. American mkt • 2,000+ fabricators is same as N. American mkt Disciplined competitive landscape House system driven market • Windows marketed utilizing the brand of the extrusions (i.e. Liniar brand) • Efficient manufacturing model HL ~200 shapes Compared to ~2,000 for Quanex in US • Streamlined product offering ~60 systems available in total by all UK extruders Quanex alone in US has 2X number of systems Similar to the US, demand is driven by new construction and R&R, but much more heavily weighted to replacement UK construction market is at attractive point of cycle recovery • Housing starts grew 25% in 2014 |

7 Thank you |