UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

☒ Quarterly report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the quarterly period ended June 30, 2024, or

☐ Transition report pursuant to section 13 or 15(d) of the Securities Exchange Act of 1934

Commission File Number 001-39529

BROADSTONE NET LEASE, INC.

(Exact name of registrant as specified in its charter)

| |

Maryland | 26-1516177 |

(State or other jurisdiction of

incorporation or organization) | (I.R.S. Employer

Identification No.) |

| |

207 High Point Drive Suite 300 Victor, New York | 14564 |

(Address of principal executive offices) | (Zip Code) |

(585) 287-6500

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | | | |

Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

Common Stock, $0.00025 par value | | BNL | | The New York Stock Exchange |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | |

Large accelerated filer |

| ☒ |

| Accelerated filer |

| ☐ |

Non-accelerated filer |

| ☐ |

| Smaller reporting company |

| ☐ |

Emerging growth company | | ☐ | | | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

There were 188,517,485 shares of the Registrants’ Common Stock, $0.00025 par value per share, outstanding as of July 29, 2024.

BROADSTONE NET LEASE, INC.

TABLE OF CONTENTS

Part I. FINANCIAL INFORMATION

Item 1. Financial Statements

Broadstone Net Lease, Inc. and Subsidiaries

Condensed Consolidated Balance Sheets

(Unaudited)

(in thousands, except per share amounts)

| | | | | | | | |

| | June 30,

2024 | | | December 31,

2023 | |

Assets | | | | | | |

Accounted for using the operating method: | | | | | | |

Land | | $ | 773,224 | | | $ | 748,529 | |

Land improvements | | | 324,138 | | | | 328,746 | |

Buildings and improvements | | | 3,708,366 | | | | 3,803,156 | |

Equipment | | | 8,248 | | | | 8,265 | |

Total accounted for using the operating method | | | 4,813,976 | | | | 4,888,696 | |

Less accumulated depreciation | | | (627,871 | ) | | | (626,597 | ) |

Accounted for using the operating method, net | | | 4,186,105 | | | | 4,262,099 | |

Accounted for using the direct financing method | | | 26,413 | | | | 26,643 | |

Accounted for using the sales-type method | | | 572 | | | | 572 | |

Property under development | | | 165,014 | | | | 94,964 | |

Investment in rental property, net | | | 4,378,104 | | | | 4,384,278 | |

Cash and cash equivalents | | | 18,282 | | | | 19,494 | |

Accrued rental income | | | 153,551 | | | | 152,724 | |

Tenant and other receivables, net | | | 2,604 | | | | 1,487 | |

Prepaid expenses and other assets | | | 33,255 | | | | 36,661 | |

Interest rate swap, assets | | | 56,444 | | | | 46,096 | |

Goodwill | | | 339,769 | | | | 339,769 | |

Intangible lease assets, net | | | 282,548 | | | | 288,226 | |

Total assets | | $ | 5,264,557 | | | $ | 5,268,735 | |

| | | | | | |

Liabilities and equity | | | | | | |

Unsecured revolving credit facility | | $ | 79,096 | | | $ | 90,434 | |

Mortgages, net | | | 77,970 | | | | 79,068 | |

Unsecured term loans, net | | | 896,574 | | | | 895,947 | |

Senior unsecured notes, net | | | 845,687 | | | | 845,309 | |

Accounts payable and other liabilities | | | 42,635 | | | | 47,534 | |

Dividends payable | | | 58,028 | | | | 56,869 | |

Accrued interest payable | | | 14,033 | | | | 5,702 | |

Intangible lease liabilities, net | | | 53,124 | | | | 53,531 | |

Total liabilities | | | 2,067,147 | | | | 2,074,394 | |

| | | | | | |

Commitments and contingencies (Note 16) | | | | | | |

| | | | | | |

Equity | | | | | | |

Broadstone Net Lease, Inc. equity: | | | | | | |

Preferred stock, $0.001 par value; 20,000 shares authorized, no shares issued or outstanding | | | — | | | | — | |

Common stock, $0.00025 par value; 500,000 shares authorized, 188,517 and 187,614 shares issued

and outstanding at June 30, 2024 and December 31, 2023, respectively | | | 47 | | | | 47 | |

Additional paid-in capital | | | 3,444,265 | | | | 3,440,639 | |

Cumulative distributions in excess of retained earnings | | | (449,893 | ) | | | (440,731 | ) |

Accumulated other comprehensive income | | | 60,383 | | | | 49,286 | |

Total Broadstone Net Lease, Inc. equity | | | 3,054,802 | | | | 3,049,241 | |

Non-controlling interests | | | 142,608 | | | | 145,100 | |

Total equity | | | 3,197,410 | | | | 3,194,341 | |

Total liabilities and equity | | $ | 5,264,557 | | | $ | 5,268,735 | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

Broadstone Net Lease, Inc. and Subsidiaries

Condensed Consolidated Statements of Income and Comprehensive Income

(Unaudited)

(in thousands, except per share amounts)

| | | | | | | | | | | | | | | | |

| | For the Three Months Ended

June 30, | | | For the Six Months Ended

June 30, | |

| | 2024 | | | 2023 | | | 2024 | | | 2023 | |

Revenues | | | | | | | | | | | | |

Lease revenues, net | | $ | 105,907 | | | $ | 109,353 | | | $ | 211,274 | | | $ | 228,345 | |

| | | | | | | | | | | | |

Operating expenses | | | | | | | | | | | | |

Depreciation and amortization | | | 37,404 | | | | 39,031 | | | | 75,176 | | | | 80,815 | |

Property and operating expense | | | 5,303 | | | | 4,988 | | | | 10,963 | | | | 10,874 | |

General and administrative | | | 9,904 | | | | 9,483 | | | | 19,336 | | | | 19,899 | |

Provision for impairment of investment in rental properties | | | 3,852 | | | | — | | | | 30,252 | | | | 1,473 | |

Total operating expenses | | | 56,463 | | | | 53,502 | | | | 135,727 | | | | 113,061 | |

| | | | | | | | | | | | |

Other income (expenses) | | | | | | | | | | | | |

Interest income | | | 649 | | | | 82 | | | | 882 | | | | 244 | |

Interest expense | | | (17,757 | ) | | | (20,277 | ) | | | (36,334 | ) | | | (41,416 | ) |

Gain on sale of real estate | | | 3,384 | | | | 29,462 | | | | 62,515 | | | | 32,877 | |

Income taxes | | | (531 | ) | | | (448 | ) | | | (939 | ) | | | (927 | ) |

Other income (expenses) | | | 748 | | | | (1,674 | ) | | | 2,443 | | | | (1,692 | ) |

Net income | | | 35,937 | | | | 62,996 | | | | 104,114 | | | | 104,370 | |

Net income attributable to non-controlling interests | | | (608 | ) | | | (2,982 | ) | | | (3,671 | ) | | | (5,052 | ) |

Net income attributable to Broadstone Net Lease, Inc. | | $ | 35,329 | | | $ | 60,014 | | | $ | 100,443 | | | $ | 99,318 | |

| | | | | | | | | | | | |

Weighted average number of common shares outstanding | | | | | | | | | | | | |

Basic | | | 187,436 | | | | 186,733 | | | | 187,363 | | | | 186,433 | |

Diluted | | | 196,470 | | | | 196,228 | | | | 196,379 | | | | 196,148 | |

Net earnings per share attributable to common stockholders | | | | | | | | | | | | |

Basic and diluted | | $ | 0.19 | | | $ | 0.32 | | | $ | 0.53 | | | $ | 0.53 | |

| | | | | | | | | | | | |

Comprehensive income | | | | | | | | | | | | |

Net income | | $ | 35,937 | | | $ | 62,996 | | | $ | 104,114 | | | $ | 104,370 | |

Other comprehensive income | | | | | | | | | | | | |

Change in fair value of interest rate swaps | | | (1,456 | ) | | | 19,652 | | | | 10,348 | | | | 1,753 | |

Realized loss on interest rate swaps | | | 62 | | | | 522 | | | | 221 | | | | 1,044 | |

Comprehensive income | | | 34,543 | | | | 83,170 | | | | 114,683 | | | | 107,167 | |

Comprehensive income attributable to non-controlling interests | | | (546 | ) | | | (3,937 | ) | | | (4,146 | ) | | | (5,138 | ) |

Comprehensive income attributable to Broadstone Net Lease, Inc. | | $ | 33,997 | | | $ | 79,233 | | | $ | 110,537 | | | $ | 102,029 | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

Broadstone Net Lease, Inc. and Subsidiaries

Condensed Consolidated Statements of Equity

(Unaudited)

(in thousands, except per share amounts)

| | | | | | | | | | | | | | | | | | | | | | | | |

| | Common

Stock | | | Additional

Paid-in

Capital | | | Cumulative

Distributions

in Excess of

Retained Earnings | | | Accumulated

Other

Comprehensive

Income | | | Non-

controlling

Interests | | | Total

Equity | |

Balance, January 1, 2024 | | $ | 47 | | | $ | 3,440,639 | | | $ | (440,731 | ) | | $ | 49,286 | | | $ | 145,100 | | | $ | 3,194,341 | |

Net income | | | — | | | | — | | | | 65,114 | | | | — | | | | 3,063 | | | | 68,177 | |

Issuance of 822 shares of common stock under equity incentive plan | | | — | | | | 116 | | | | — | | | | — | | | | — | | | | 116 | |

Offering costs, discounts, and commissions | | | — | | | | (36 | ) | | | — | | | | — | | | | — | | | | (36 | ) |

Stock-based compensation, net of 25 shares of restricted stock forfeited | | | — | | | | 1,475 | | | | — | | | | — | | | | — | | | | 1,475 | |

Retirement of 71 shares of common stock under equity incentive plan | | | — | | | | (1,040 | ) | | | — | | | | — | | | | — | | | | (1,040 | ) |

Conversion of 95 OP units to 95 shares of common stock | | | — | | | | 1,536 | | | | — | | | | — | | | | (1,536 | ) | | | — | |

Distributions declared ($0.285 per share and OP Unit) | | | — | | | | — | | | | (54,552 | ) | | | — | | | | (2,740 | ) | | | (57,292 | ) |

Change in fair value of interest rate swap agreements | | | — | | | | — | | | | — | | | | 11,274 | | | | 530 | | | | 11,804 | |

Realized loss on interest rate swap agreements | | | — | | | | — | | | | — | | | | 152 | | | | 7 | | | | 159 | |

Adjustment to non-controlling interests | | | — | | | | 4,220 | | | | — | | | | (3,878 | ) | | | (342 | ) | | | — | |

Balance, March 31, 2024 | | $ | 47 | | | $ | 3,446,910 | | | $ | (430,169 | ) | | $ | 56,834 | | | $ | 144,082 | | | $ | 3,217,704 | |

Net income | | | — | | | | — | | | | 35,329 | | | | — | | | | 608 | | | | 35,937 | |

Issuance of 55 shares of common stock under equity incentive plan | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | |

Offering costs, discounts, and commissions | | | — | | | | (200 | ) | | | — | | | | — | | | | — | | | | (200 | ) |

Contributions from non-controlling interests | | | — | | | | — | | | | — | | | | — | | | | 1,000 | | | | 1,000 | |

Stock-based compensation, net of 5 shares of restricted stock forfeited | | | — | | | | 2,073 | | | | — | | | | — | | | | — | | | | 2,073 | |

Conversion of 32 OP units to 32 shares of common stock | | | — | | | | 532 | | | | — | | | | — | | | | (532 | ) | | | — | |

Distributions declared ($0.290 per share and OP Unit) | | | — | | | | — | | | | (55,053 | ) | | | — | | | | (2,657 | ) | | | (57,710 | ) |

Change in fair value of interest rate swap agreements | | | — | | | | — | | | | — | | | | (1,391 | ) | | | (65 | ) | | | (1,456 | ) |

Realized loss on interest rate swap agreements | | | — | | | | — | | | | — | | | | 59 | | | | 3 | | | | 62 | |

Adjustment to non-controlling interests | | | — | | | | (5,050 | ) | | | — | | | | 4,881 | | | | 169 | | | | — | |

Balance, June 30, 2024 | | $ | 47 | | | $ | 3,444,265 | | | $ | (449,893 | ) | | $ | 60,383 | | | $ | 142,608 | | | $ | 3,197,410 | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

Broadstone Net Lease, Inc. and Subsidiaries

Condensed Consolidated Statements of Equity - Continued

(Unaudited)

(in thousands, except per share amounts)

| | | | | | | | | | | | | | | | | | | | | | | | |

| | Common

Stock | | | Additional

Paid-in

Capital | | | Cumulative

Distributions

in Excess of

Retained Earnings | | | Accumulated

Other

Comprehensive

Income | | | Non-

controlling

Interests | | | Total

Equity | |

Balance, January 1, 2023 | | $ | 47 | | | $ | 3,419,395 | | | $ | (386,049 | ) | | $ | 59,525 | | | $ | 169,587 | | | $ | 3,262,505 | |

Net income | | | — | | | | — | | | | 39,304 | | | | — | | | | 2,070 | | | | 41,374 | |

Issuance of 259 shares of common stock under equity incentive plan | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | |

Offering costs, discounts, and commissions | | | — | | | | (2 | ) | | | — | | | | — | | | | — | | | | (2 | ) |

Stock-based compensation, net of zero shares of restricted stock forfeited | | | — | | | | 1,879 | | | | — | | | | — | | | | — | | | | 1,879 | |

Retirement of 66 shares of common stock under equity incentive plan | | | — | | | | (1,175 | ) | | | — | | | | — | | | | — | | | | (1,175 | ) |

Conversion of 896 OP units to 896 shares of common stock | | | — | | | | 14,897 | | | | — | | | | — | | | | (14,897 | ) | | | — | |

Distributions declared ($0.275 per share and OP Unit) | | | — | | | | — | | | | (52,145 | ) | | | — | | | | (2,742 | ) | | | (54,887 | ) |

Change in fair value of interest rate swap agreements | | | — | | | | — | | | | — | | | | (17,003 | ) | | | (896 | ) | | | (17,899 | ) |

Realized loss on interest rate swap agreements | | | — | | | | — | | | | — | | | | 496 | | | | 26 | | | | 522 | |

Adjustment to non-controlling interests | | | — | | | | (460 | ) | | | — | | | | 498 | | | | (38 | ) | | | — | |

Balance, March 31, 2023 | | $ | 47 | | | $ | 3,434,534 | | | $ | (398,890 | ) | | $ | 43,516 | | | $ | 153,110 | | | $ | 3,232,317 | |

Net income | | | — | | | | — | | | | 60,014 | | | | — | | | | 2,982 | | | | 62,996 | |

Issuance of 51 shares of common stock under equity incentive plan | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | |

Offering costs, discounts, and commissions | | | — | | | | (10 | ) | | | — | | | | — | | | | — | | | | (10 | ) |

Stock-based compensation, net of six shares of restricted stock forfeited | | | — | | | | 1,539 | | | | — | | | | — | | | | — | | | | 1,539 | |

Conversion of 25 OP units to 25 shares of common stock | | | — | | | | 398 | | | | — | | | | — | | | | (398 | ) | | | — | |

Distributions declared ($0.280 per share and OP Unit) | | | — | | | | — | | | | (52,755 | ) | | | — | | | | (2,664 | ) | | | (55,419 | ) |

Change in fair value of interest rate swap agreements | | | — | | | | — | | | | — | | | | 18,722 | | | | 930 | | | | 19,652 | |

Realized loss on interest rate swap agreements | | | — | | | | — | | | | — | | | | 496 | | | | 26 | | | | 522 | |

Adjustment to non-controlling interests | | | — | | | | (5,769 | ) | | | — | | | | 5,694 | | | | 75 | | | | — | |

Balance, June 30, 2023 | | $ | 47 | | | $ | 3,430,692 | | | $ | (391,631 | ) | | $ | 68,428 | | | $ | 154,061 | | | $ | 3,261,597 | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

Broadstone Net Lease, Inc. and Subsidiaries

Condensed Consolidated Statements of Cash Flows

(Unaudited)

(in thousands)

| | | | | | | | |

| | For the Six Months Ended

June 30, | |

| | 2024 | | | 2023 | |

Operating activities | | | | | | |

Net income | | $ | 104,114 | | | $ | 104,370 | |

Adjustments to reconcile net income including non-controlling interests to net cash provided by

operating activities: | | | | | | |

Depreciation and amortization including intangibles associated with investment in rental property | | | 73,063 | | | | 77,039 | |

Provision for impairment of investment in rental properties | | | 30,252 | | | | 1,473 | |

Amortization of debt issuance costs and original issuance discount charged to interest expense | | | 1,966 | | | | 1,894 | |

Stock-based compensation expense | | | 3,548 | | | | 3,418 | |

Straight-line rent, direct financing and sales-type lease adjustments | | | (7,475 | ) | | | (14,250 | ) |

Gain on sale of real estate | | | (62,515 | ) | | | (32,877 | ) |

Other non-cash items | | | (2,239 | ) | | | 923 | |

Changes in assets and liabilities: | | | | | | |

Tenant and other receivables | | | (66 | ) | | | 371 | |

Prepaid expenses and other assets | | | 1,520 | | | | (192 | ) |

Accounts payable and other liabilities | | | (5,460 | ) | | | (4,383 | ) |

Accrued interest payable | | | 8,331 | | | | (1,182 | ) |

Net cash provided by operating activities | | | 145,039 | | | | 136,604 | |

| | | | | | |

Investing activities | | | | | | |

Acquisition of rental property | | | (218,891 | ) | | | (25,990 | ) |

Investment in property under development including capitalized interest of $2,601 and $267 in 2024 and 2023, respectively | | | (70,051 | ) | | | (37,449 | ) |

Capital expenditures and improvements | | | (3,304 | ) | | | (23,593 | ) |

Proceeds from disposition of rental property, net | | | 270,823 | | | | 118,253 | |

Change in deposits on investments in rental property | | | — | | | | 125 | |

Net cash (used in) provided by investing activities | | | (21,423 | ) | | | 31,346 | |

| | | | | | |

Financing activities | | | | | | |

Offering costs, discounts, and commissions | | | (461 | ) | | | (180 | ) |

Principal payments on mortgages and unsecured term loans | | | (1,117 | ) | | | (6,411 | ) |

Borrowings on unsecured revolving credit facility | | | 90,000 | | | | 125,000 | |

Repayments on unsecured revolving credit facility | | | (99,000 | ) | | | (201,000 | ) |

Cash distributions paid to stockholders | | | (108,385 | ) | | | (103,521 | ) |

Cash distributions paid to non-controlling interests | | | (5,389 | ) | | | (5,613 | ) |

Net cash used in financing activities | | | (124,352 | ) | | | (191,725 | ) |

Net decrease in cash and cash equivalents and restricted cash | | | (736 | ) | | | (23,775 | ) |

Cash and cash equivalents and restricted cash at beginning of period | | | 20,632 | | | | 60,040 | |

Cash and cash equivalents and restricted cash at end of period | | $ | 19,896 | | | $ | 36,265 | |

| | | | | | |

Reconciliation of cash and cash equivalents and restricted cash | | | | | | |

Cash and cash equivalents at beginning of period | | $ | 19,494 | | | $ | 21,789 | |

Restricted cash at beginning of period | | | 1,138 | | | | 38,251 | |

Cash and cash equivalents and restricted cash at beginning of period | | $ | 20,632 | | | $ | 60,040 | |

| | | | | | |

Cash and cash equivalents at end of period | | $ | 18,282 | | | $ | 20,763 | |

Restricted cash at end of period | | | 1,614 | | | | 15,502 | |

Cash and cash equivalents and restricted cash at end of period | | $ | 19,896 | | | $ | 36,265 | |

The accompanying notes are an integral part of these condensed consolidated financial statements.

Broadstone Net Lease, Inc. and Subsidiaries

Notes to the Condensed Consolidated Financial Statements (Unaudited)

1. Business Description

Broadstone Net Lease, Inc. (the “Corporation”) is a Maryland corporation formed on October 18, 2007, that elected to be taxed as a real estate investment trust (“REIT”) commencing with the taxable year ended December 31, 2008. Broadstone Net Lease, LLC (the Corporation’s operating company, or the “OP”), is the entity through which the Corporation conducts its business and owns (either directly or through subsidiaries) all of the Corporation’s properties. The Corporation is the sole managing member of the OP. The membership units not owned by the Corporation are referred to as OP Units and are recorded as non-controlling interests in the Condensed Consolidated Financial Statements. As the Corporation conducts substantially all of its operations through the OP, it is structured as an umbrella partnership real estate investment trust (“UPREIT”). The Corporation’s common stock is listed on the New York Stock Exchange under the symbol “BNL.” The Corporation, the OP, and its consolidated subsidiaries are collectively referred to as the “Company.”

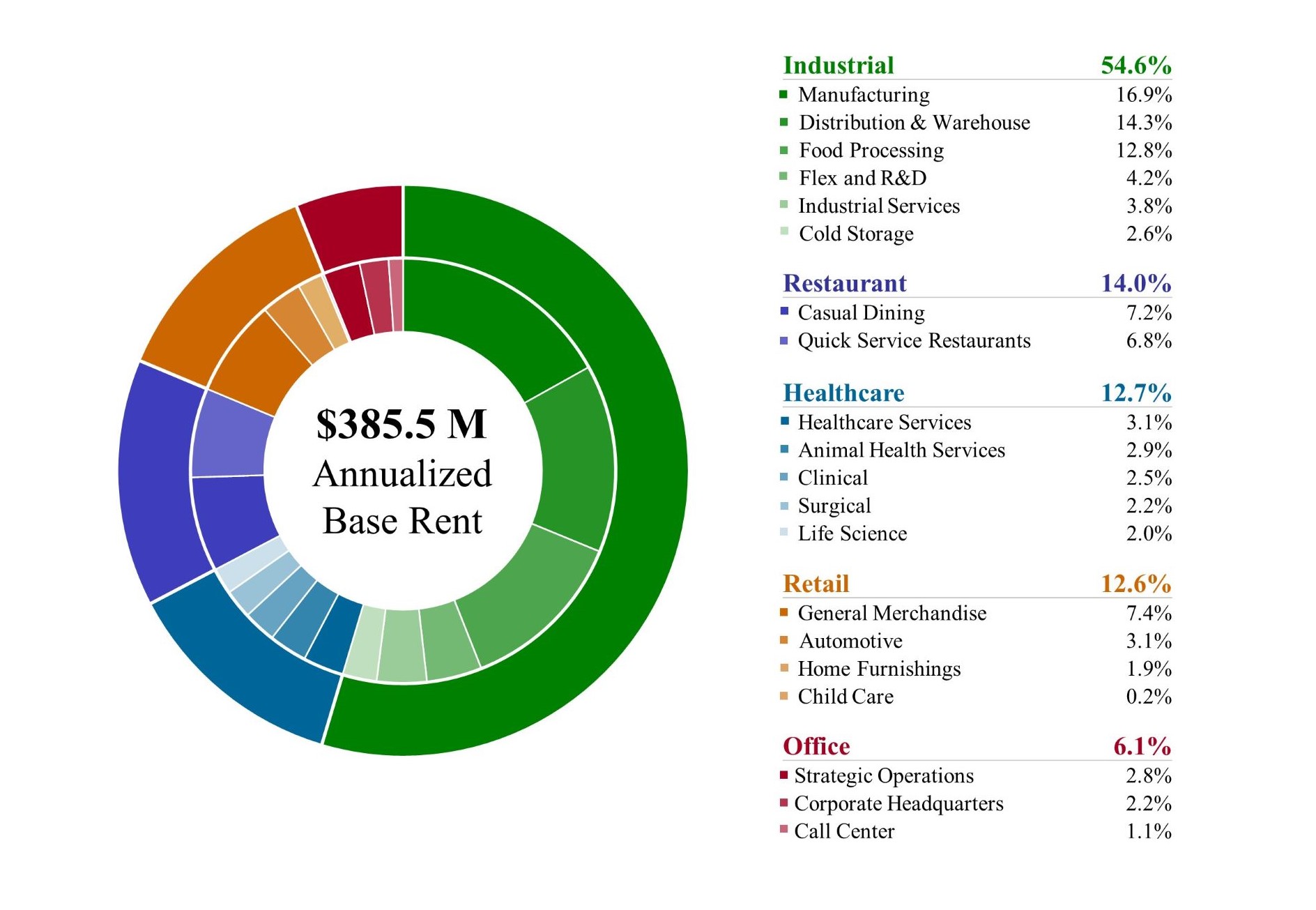

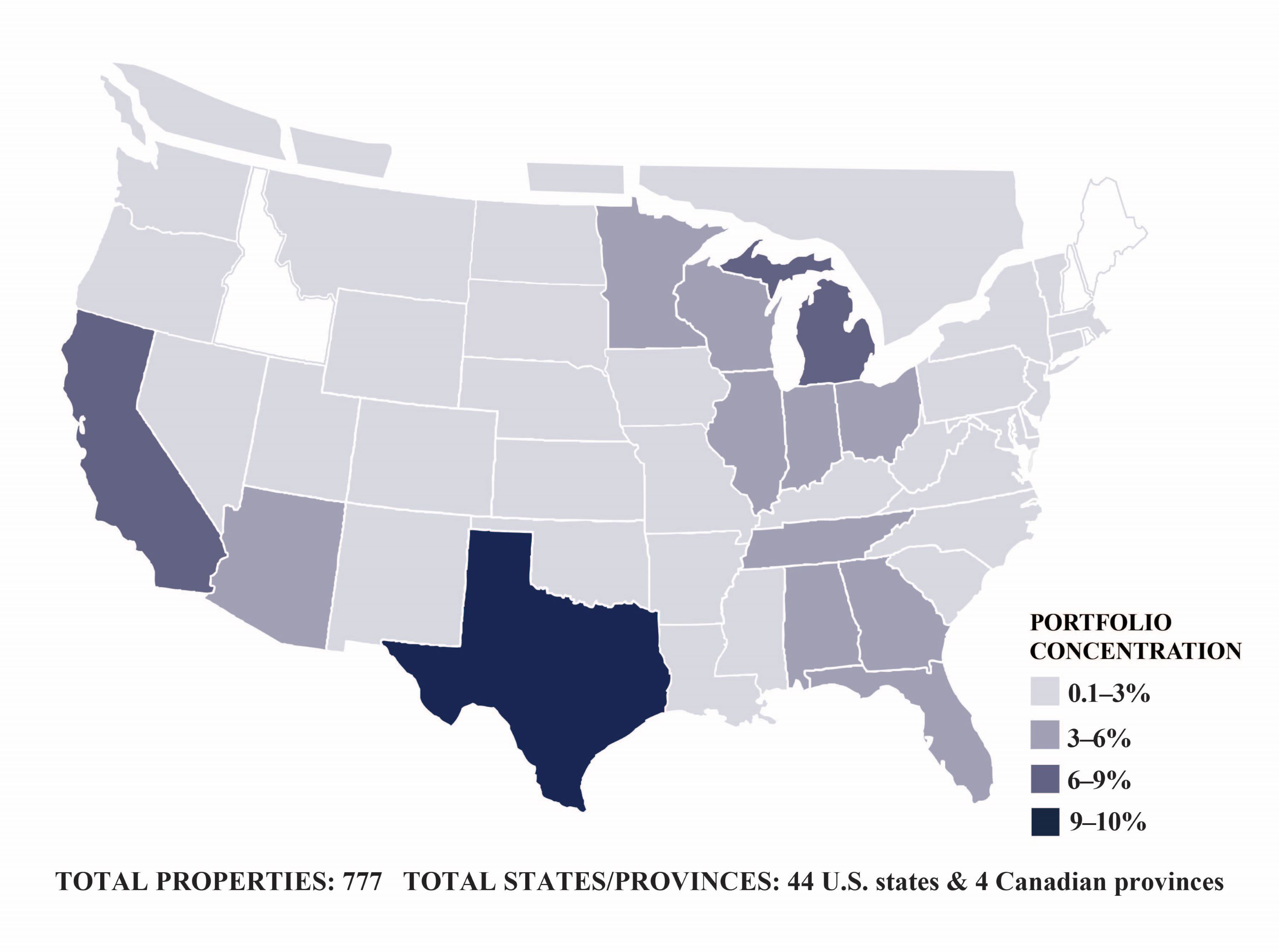

The Company is an industrial-focused, diversified net lease REIT that focuses on investing in income-producing, single-tenant net leased commercial properties, primarily in the United States. The Company leases industrial, restaurant, healthcare, retail, and office commercial properties under long-term lease agreements. At June 30, 2024, the Company owned a diversified portfolio of 777 individual commercial properties with 770 properties located in 44 U.S. states and seven properties located in four Canadian provinces.

The following table summarizes the outstanding equity and economic ownership interest of the Company:

| | | | | | | | | | | | | | | | | | | | | | | | |

| | June 30, 2024 | | | December 31, 2023 | |

(in thousands) | | Shares of

Common Stock | | | OP Units | | | Total Diluted

Shares | | | Shares of

Common Stock | | | OP Units | | | Total Diluted

Shares | |

Ownership interest | | | 188,517 | | | | 8,801 | | | | 197,318 | | | | 187,614 | | | | 8,928 | | | | 196,542 | |

Percent ownership of OP | | | 95.5 | % | | | 4.5 | % | | | 100.0 | % | | | 95.5 | % | | | 4.5 | % | | | 100.0 | % |

Refer to Note 14 for further discussion regarding the calculation of weighted average shares outstanding.

2. Summary of Significant Accounting Policies

The accompanying Condensed Consolidated Financial Statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”) for interim financial information (Accounting Standards Codification (“ASC”) 270, Interim Reporting) and Article 10 of the Securities and Exchange Commission’s (“SEC”) Regulation S-X. Accordingly, the Company has omitted certain footnote disclosures which would substantially duplicate those contained within the audited consolidated financial statements for the year ended December 31, 2023, included in the Company’s 2023 Annual Report on Form 10-K, filed with the SEC on February 22, 2024. Therefore, the readers of this quarterly report should refer to those audited consolidated financial statements, specifically Note 2, Summary of Significant Accounting Policies, for further discussion of significant accounting policies and estimates. The Company believes all adjustments necessary for a fair presentation have been included in these interim Condensed Consolidated Financial Statements (which include only normal recurring adjustments).

Principles of Consolidation

The Condensed Consolidated Financial Statements include the accounts and operations of the Company. All intercompany balances and transactions have been eliminated in consolidation.

When the Company obtains an economic interest in an entity, the Company evaluates the entity to determine if it should be deemed a variable interest entity (“VIE”) and, if so, whether the Company is the primary beneficiary and is therefore required to consolidate the entity. The accounting guidance for consolidation of VIEs is applied to certain entities in which the equity investors do not have the characteristics of a controlling financial interest or do not have sufficient equity at risk for the entity to finance its activities without additional subordinated financial support from other parties. Certain decision-making rights within a loan or joint-venture agreement may cause us to consider an entity a VIE. The contractual arrangements in a partnership agreement or other related contracts are reviewed to determine whether the entity is a VIE, and if the Company has variable interests in the VIE. The Company’s variable interests are then compared to those of the other variable interest holders to determine which party is the primary beneficiary of the VIE. A primary beneficiary: (i) has the power to direct the activities that most significantly impact the economic performance of the VIE and (ii) has the obligation to absorb losses or the right to receive benefits of the VIE that could potentially be significant to the VIE. The Company reassesses the initial evaluation of whether an entity is a VIE when certain events occur, and reassesses the primary beneficiary determination of a VIE on an ongoing basis based on current facts and circumstances. To the extent the Company has a variable interest in entities that are not evaluated under the VIE model, the Company evaluates its interests using the voting interest entity model.

The Corporation has complete responsibility for the day-to-day management of, authority to make decisions for, and control of the OP. Based on consolidation guidance, the Corporation has concluded that the OP is a VIE as the members in the OP do not possess kick-out rights or substantive participating rights. Accordingly, the Corporation consolidates its interest in the OP. However, because the Corporation holds the majority voting interest in the OP and certain other conditions are met, it qualifies for the exemption from providing certain disclosure requirements associated with investments in VIEs.

In June 2024, the Company invested $52.2 million in exchange for 98.1% ownership interest in a VIE. The Company is the primary beneficiary as it: (i) has the power to direct the activities that significantly impact the economic performance of the VIE, and (ii) has the obligation to absorb losses and the right to receive benefits of the VIE, and therefore consolidates the VIE. The following table presents a summary of selected financial data of the consolidated VIE included in the Condensed Consolidated Balance Sheets:

| | | | |

(in thousands) | | June 30,

2024 | |

Assets | | | |

Accounted for using the operating method: | | | |

Land | | $ | 7,644 | |

Land improvements | | | 2,508 | |

Buildings and improvements | | | 38,648 | |

Total accounted for using the operating method | | | 48,800 | |

Less accumulated depreciation | | | (240 | ) |

Accounted for using the operating method, net | | | 48,560 | |

Intangible lease assets, net | | | 3,926 | |

Other assets | | | 1,831 | |

Total assets | | $ | 54,317 | |

| | | |

Liabilities | | | |

Intangible lease liabilities, net | | $ | 555 | |

Other liabilities | | | 1,485 | |

Total liabilities | | $ | 2,040 | |

From time to time, the Company acquires properties using a reverse like-kind exchange structure pursuant to Section 1031 of the Internal Revenue Code (a “reverse 1031 exchange”) and, as such, the properties are in the possession of an Exchange Accommodation Titleholder (“EAT”) until the reverse 1031 exchange is completed. The EAT is classified as a VIE as it is a “thinly capitalized” entity. The Company consolidates the EAT because it is the primary beneficiary as it has the ability to control the activities that most significantly impact the EAT's economic performance and can collapse the 1031 exchange structure at its discretion. The assets of the EAT primarily consist of leased property (net real estate investment in rental property and lease intangibles).

The portions of a consolidated entity not owned by the Company are presented as non-controlling interests as of and during the periods presented.

Basis of Accounting

The Condensed Consolidated Financial Statements have been prepared in accordance with GAAP.

The preparation of Condensed Consolidated Financial Statements in conformity with GAAP requires management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent liabilities at the date of the Condensed Consolidated Financial Statements and the reported amounts of revenues and expenses during the reporting periods. Accordingly, actual results may differ from those estimates.

Investment in Property Under Development

Land acquired for development and construction and improvement costs incurred in connection with the development of new properties are capitalized and recorded as Property under development in the accompanying Condensed Consolidated Balance Sheets until construction has been completed. Such capitalized costs include all direct and indirect costs related to planning, development, and construction, including interest, real estate taxes, and other miscellaneous costs incurred during the construction period. Once completed, the property under development is placed in service and depreciation commences. The following tables summarize the Company’s investments in property under development:

| | | | | | | | |

(in thousands) | | June 30,

2024 | | | December 31,

2023 | |

Development, construction and improvement costs | | $ | 160,950 | | | $ | 93,501 | |

Capitalized interest | | | 4,064 | | | | 1,463 | |

Property under development | | $ | 165,014 | | | $ | 94,964 | |

| | | | | | | | | | | | | | | | |

| | For the Three Months Ended

June 30, | | | For the Six Months Ended

June 30, | |

(in thousands) | | 2024 | | | 2023 | | | 2024 | | | 2023 | |

Investment in properties under development,

excluding capitalized costs | | $ | 30,591 | | | $ | 37,182 | | | $ | 67,450 | | | $ | 37,182 | |

Long-lived Asset Impairment

The Company reviews long-lived assets to be held and used for possible impairment when events or changes in circumstances indicate that their carrying amounts may not be recoverable. If, and when, such events or changes in circumstances are present, an impairment exists to the extent the carrying value of the long-lived asset or asset group exceeds the sum of the undiscounted cash flows expected to result from the use of the long-lived asset or asset group and its eventual disposition. Such cash flows include expected future operating income, as adjusted for trends and prospects, as well as the effects of demand, competition, and other factors. An impairment loss is measured as the amount by which the carrying amount of the long-lived asset or asset group exceeds its fair value. Significant judgment is made to determine if and when impairment should be taken. The Company’s assessment of impairment as of June 30, 2024 and 2023 was based on the most current information available to the Company. Certain of the Company’s properties may have fair values less than their carrying amounts. However, based on the Company’s plans with respect to each of those properties, the Company believes that their carrying amounts are recoverable and therefore, no impairment charges were recognized other than those described below. If the operating conditions mentioned above deteriorate or if the Company’s expected holding period for assets changes, subsequent tests for impairments could result in additional impairment charges in the future.

Inputs used in establishing fair value for impaired real estate assets generally fall within Level 3 of the fair value hierarchy, which are characterized as requiring significant judgment as little or no current market activity may be available for validation. The main indicator used to establish the classification of the inputs is current market conditions, as derived through the use of published commercial real estate market information and information obtained from brokers and other third party sources. The Company determines the valuation of impaired assets using generally accepted valuation techniques including discounted cash flow analysis, income capitalization, analysis of recent comparable sales transactions, actual sales negotiations, and bona fide purchase offers received from third parties. Management may consider a single valuation technique or multiple valuation techniques, as appropriate, when estimating the fair value of its real estate.

The following table summarizes the Company’s impairment charges:

| | | | | | | | | | | | | | | | |

| | For the Three Months Ended

June 30, | | | For the Six Months Ended

June 30, | |

(in thousands, except number of properties) | | 2024 | | | 2023 | | | 2024 | | | 2023 | |

Number of properties | | | 2 | | | | — | | | | 14 | | | | 1 | |

Impairment charge | | $ | 3,852 | | | $ | — | | | $ | 30,252 | | | $ | 1,473 | |

During the three and six months ended June 30, 2024, the Company recognized impairment of of $3.9 million and $30.3 million, respectively, resulting from changes in the Company’s long-term hold strategy with respect to the individual properties. The impairments primarily include $18.1 million on two healthcare properties and $11.2 million on 11 healthcare properties sold as part of a portfolio with a gain of $59.1 million, excluding any impairment, and were based on actual and expected sales prices of the individual properties.

Restricted Cash

Restricted cash generally includes escrow funds the Company maintains pursuant to the terms of certain mortgages, lease agreements, and undistributed proceeds from the sale of properties under Section 1031 of the Internal Revenue Code of 1986, as amended (the “Code”), and is reported within Prepaid expenses and other assets in the Condensed Consolidated Balance Sheets. Restricted cash consisted of the following:

| | | | | | | | |

| | June 30, | | | December 31, | |

(in thousands) | | 2024 | | | 2023 | |

Escrow funds and other | | $ | 1,614 | | | $ | 1,138 | |

1031 exchange proceeds | | | — | | | | — | |

| | $ | 1,614 | | | $ | 1,138 | |

Rent Received in Advance

Rent received in advance represents tenant rent payments received prior to the contractual due date, and is included in Accounts payable and other liabilities in the Condensed Consolidated Balance Sheets. Rent received in advance consisted of the following:

| | | | | | | | |

(in thousands) | | June 30,

2024 | | | December 31,

2023 | |

Rent received in advance | | $ | 14,292 | | | $ | 14,776 | |

Fair Value Measurements

Recurring Fair Value Measurements

The balances of financial instruments measured at fair value on a recurring basis are as follows (see Note 9):

| | | | | | | | | | | | | | | | |

| | June 30, 2024 | |

(in thousands) | | Total | | | Level 1 | | | Level 2 | | | Level 3 | |

Interest rate swap, assets | | $ | 56,444 | | | $ | — | | | $ | 56,444 | | | $ | — | |

| | | | | | | | | | | | | | | | |

| | December 31, 2023 | |

(in thousands) | | Total | | | Level 1 | | | Level 2 | | | Level 3 | |

Interest rate swap, assets | | $ | 46,096 | | | $ | — | | | $ | 46,096 | | | $ | — | |

Long-term Debt – The fair value of the Company’s debt was estimated using Level 1, Level 2, and Level 3 inputs based on recent secondary market trades of the Company’s 2031 Senior Unsecured Public Notes (see Note 7), recent comparable financing transactions, recent market risk premiums for loans of comparable quality, applicable Secured Overnight Financing Rate (“SOFR”), Canadian Dollar Offered Rate (“CDOR”), Canadian Overnight Repo Rate Average (“CORRA”), U.S. Treasury obligation interest rates, and discounted estimated future cash payments to be made on such debt. The discount rates estimated reflect the Company’s judgment as to the approximate current lending rates for loans or groups of loans with similar maturities and assumes that the debt is outstanding through maturity. Market information, as available, or present value techniques were utilized to estimate the amounts required to be disclosed. Since such amounts are estimates that are based on limited available market information for similar transactions and do not acknowledge transfer or other repayment restrictions that may exist on specific loans, it is unlikely that the estimated fair value of any such debt could be realized by immediate settlement of the obligation.

The following table summarizes the carrying amount reported in the Condensed Consolidated Balance Sheets and the Company’s estimate of the fair value of the unsecured revolving credit facility, mortgages, unsecured term loans, and senior unsecured notes which reflects the fair value of interest rate swaps:

| | | | | | | | |

(in thousands) | | June 30,

2024 | | | December 31,

2023 | |

Carrying amount | | $ | 1,907,151 | | | $ | 1,919,607 | |

Fair value | | | 1,751,768 | | | | 1,761,177 | |

Non-recurring Fair Value Measurements

The Company’s non-recurring fair value measurements at June 30, 2024 and December 31, 2023 consisted of the fair value of impaired real estate assets that were determined using Level 3 inputs.

Right-of-Use Assets and Lease Liabilities

The Company is a lessee under non-cancelable operating leases associated with its corporate headquarters and other office spaces as well as with leases of land (“ground leases”). The Company records right-of-use assets and lease liabilities associated with these leases. The lease liability is equal to the net present value of the future payments to be made under the lease, discounted using estimates based on observable market factors. The right-of-use asset is generally equal to the lease liability plus initial direct costs associated with the leases. The Company includes in the recognition of the right-of-use asset and lease liability those renewal periods that are reasonably certain to be exercised, based on the facts and circumstances that exist at lease inception. Amounts associated with percentage rent provisions are considered variable lease costs and are not included in the initial measurement of the right-of-use asset or lease liability. The Company has made an accounting policy election, applicable to all asset types, not to separate lease from nonlease components when allocating contract consideration related to operating leases.

Right-of-use assets and lease liabilities associated with operating leases were included in the accompanying Condensed Consolidated Balance Sheets as follows:

| | | | | | | | | | |

| | | | June 30, | | | December 31, | |

(in thousands) | | Financial Statement Presentation | | 2024 | | | 2023 | |

Right-of-use assets | | Prepaid expenses and other assets | | $ | 7,387 | | | $ | 8,476 | |

Lease liabilities | | Accounts payable and other liabilities | | | 7,757 | | | | 8,256 | |

The Company’s right-of-use assets and lease liabilities primarily consist of a lease for the Company’s corporate office space, which expires in October 2033. The lease contains two five-year extension options, exercisable at the Company’s discretion, that are not reasonably certain to be exercised, and are therefore excluded from our calculation of the lease liability.

3. Acquisitions of Rental Property

The Company closed on the following acquisitions during the six months ended June 30, 2024:

| | | | | | | | | | | |

(in thousands, except number of properties) | | Number of | | | Real Estate | | |

Date | | Property Type | | Properties | | | Acquisition Price | | |

April 4, 2024 | | Retail & Restaurant | | | 8 | | | $ | 84,500 | | (a) |

April 18, 2024 | | Industrial & Retail | | | 5 | | | | 65,000 | | |

May 21, 2024 | | Retail | | | 1 | | | | 12,590 | | |

May 30, 2024 | | Industrial | | | 5 | | | | 31,493 | | |

June 6, 2024 | | Industrial | | | 1 | | | | 9,470 | | |

June 24, 2024 | | Retail | | | 2 | | | | 14,000 | | |

| | | | | 22 | | | $ | 217,053 | | (b) |

(a)In April 2024, the Company acquired $52.0 million of real estate assets. In June 2024, the Company contributed these assets in exchange for preferred equity in a consolidated VIE (see Note 2).

(b)Acquisition price excludes capitalized acquisition costs of $1.7 million.

The Company closed on the following acquisitions during the six months ended June 30, 2023:

| | | | | | | | | | | |

(in thousands, except number of properties) | | Number of | | | Real Estate | | |

Date | | Property Type | | Properties | | | Acquisition Price | | |

March 14, 2023 | | Retail | | | 1 | | | $ | 5,221 | | |

May 16, 2023 | | Industrial | | | 2 | | | | 10,432 | | |

May 22, 2023 | | Industrial | | | 1 | | | | 17,300 | | (c) |

May 25, 2023 | | Industrial | | | 1 | | | | 9,952 | | |

| | | | | 5 | | | $ | 42,905 | | (d) |

(c)Acquisition of land to be developed in connection with a $204.8 million build-to-suit transaction expected to fund in multiple draws through October 2024 (see Note 16).

(d)Acquisition price excludes capitalized acquisition costs of $2.8 million.

The Company allocated the purchase price of these properties to the fair value of the assets acquired and liabilities assumed. The following table summarizes the purchase price allocation for completed real estate acquisitions:

| | | | | | | | | |

| | For the Six Months Ended

June 30, | | |

(in thousands) | | 2024 | | | 2023 | | |

Land | | $ | 50,741 | | | $ | 2,461 | | |

Land improvements | | | 10,121 | | | | 2,694 | | |

Buildings and improvements | | | 142,866 | | | | 18,647 | | |

Property under development | | | — | | | | 19,648 | | |

Acquired in-place leases (e) | | | 17,956 | | | | 2,400 | | |

Acquired above-market leases (f) | | | 1,028 | | | | — | | |

Acquired below-market leases (g) | | | (3,996 | ) | | | (166 | ) | |

| | $ | 218,716 | | | $ | 45,684 | | |

(e)The weighted average amortization period for acquired in-place leases is 11 years and 15 years for acquisitions completed during the six months ended June 30, 2024 and 2023, respectively.

(f)The weighted average amortization period for acquired above-market leases is six years for acquisitions completed during the six months ended June 30, 2024. There were no above-market leases acquired during the six months ended June 30, 2023.

(g)The weighted average amortization period for acquired below-market leases is nine years and 20 years for acquisitions completed during the six months ended June 30, 2024 and 2023, respectively.

The above acquisitions were funded using a combination of available cash on hand and unsecured revolving credit facility borrowings. All real estate acquisitions closed during the six months ended June 30, 2024 and 2023, qualified as asset acquisitions and as such, acquisition costs were capitalized.

4. Sale of Real Estate

The Company closed on the following sales of real estate, none of which qualified as discontinued operations:

| | | | | | | | | | | | | | | | | |

| | For the Three Months Ended

June 30, | | | For the Six Months Ended

June 30, | | |

(in thousands, except number of properties) | | 2024 | | | 2023 | | | 2024 | | | 2023 | | |

Number of properties disposed | | | 3 | | | | 4 | | | | 40 | | | | 7 | | |

Aggregate sale price | | $ | 24,350 | | | $ | 69,390 | | | $ | 276,102 | | | $ | 121,264 | | |

Aggregate carrying value | | | (20,473 | ) | | | (38,381 | ) | | | (209,846 | ) | | | (85,376 | ) | |

Additional sales expenses | | | (493 | ) | | | (1,547 | ) | | | (3,741 | ) | | | (3,011 | ) | |

Gain on sale of real estate | | $ | 3,384 | | | $ | 29,462 | | | $ | 62,515 | | | $ | 32,877 | | |

5. Investment in Rental Property and Lease Arrangements

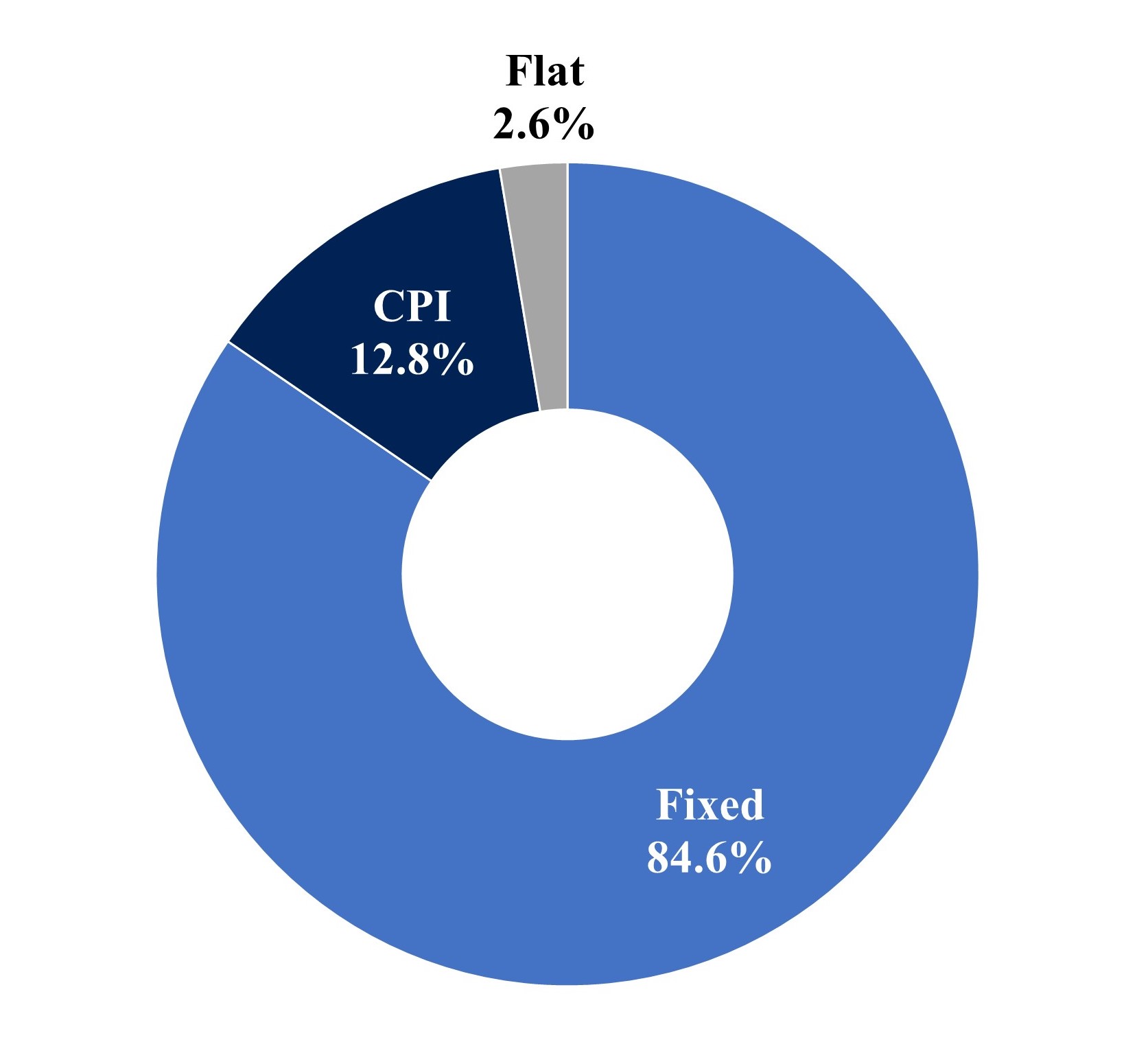

The Company generally leases its investment rental property to established tenants in the industrial, restaurant, healthcare, retail, and office property types. At June 30, 2024, the Company had 777 real estate properties, 764 of which were leased under leases that have been classified as operating leases, nine that have been classified as direct financing leases, one that has been classified as a sales-type lease, and three that were vacant. Of the nine leases classified as direct financing leases, three include land portions which are accounted for as operating leases. The sales-type lease includes a land portion which is accounted for as an operating lease. Most leases have initial terms of 10 to 20 years. The Company’s leases generally provide for limited increases in rent as a result of fixed increases, increases in the Consumer Price Index (“CPI”), or increases in the tenant’s sales volume. Generally, tenants are also required to pay all property taxes and assessments, substantially maintain the interior and exterior of the building, and maintain property and liability insurance coverage. The leases also typically provide for one or more multiple-year renewal options, at the election of the tenant, and are subject to generally the same terms and conditions as the initial lease.

Investment in Rental Property – Accounted for Using the Operating Method

Depreciation expense on investment in rental property was as follows:

| | | | | | | | | | | | | | | | |

| | For the Three Months Ended

June 30, | | | For the Six Months Ended

June 30, | |

(in thousands) | | 2024 | | | 2023 | | | 2024 | | | 2023 | |

Depreciation | | $ | 29,480 | | | $ | 30,989 | | | $ | 59,474 | | | $ | 62,146 | |

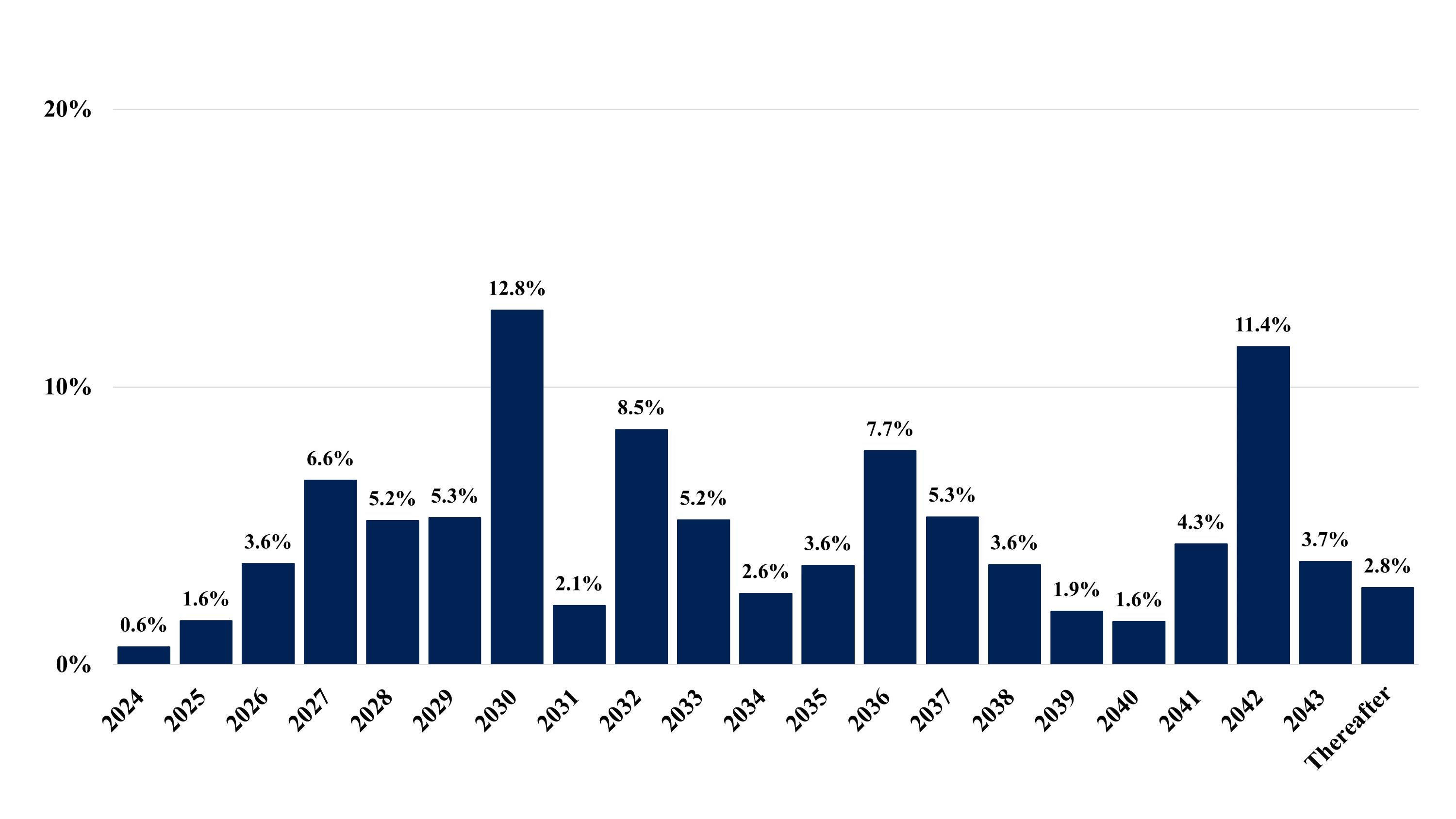

Estimated lease payments to be received under non-cancelable operating leases with tenants at June 30, 2024 are as follows:

| | | | |

(in thousands) | | | |

Remainder of 2024 | | $ | 194,506 | |

2025 | | | 400,269 | |

2026 | | | 398,481 | |

2027 | | | 384,581 | |

2028 | | | 368,069 | |

Thereafter | | | 3,075,488 | |

| | $ | 4,821,394 | |

Since lease renewal periods are exercisable at the option of the tenant, the above amounts only include future lease payments due during the initial lease terms. Such amounts exclude any potential variable rent increases that are based on changes in the CPI or future variable rents which may be received under the leases based on a percentage of the tenant’s gross sales. Additionally, certain of our leases provide tenants with the option to terminate their leases in exchange for termination penalties, or that are contingent upon the occurrence of a future event. Future lease payments within the table above have not been adjusted for these termination rights.

Investment in Rental Property – Direct Financing Leases

The Company’s net investment in direct financing leases was comprised of the following:

| | | | | | | | |

(in thousands) | | June 30,

2024 | | | December 31,

2023 | |

Undiscounted estimated lease payments to be received | | $ | 33,569 | | | $ | 35,155 | |

Estimated unguaranteed residual values | | | 14,547 | | | | 14,547 | |

Unearned revenue | | | (21,605 | ) | | | (22,944 | ) |

Reserve for credit losses | | | (98 | ) | | | (115 | ) |

Net investment in direct financing leases | | $ | 26,413 | | | $ | 26,643 | |

Undiscounted estimated lease payments to be received under non-cancelable direct financing leases with tenants at June 30, 2024 are as follows:

| | | | |

(in thousands) | | | |

Remainder of 2024 | | $ | 1,586 | |

2025 | | | 3,285 | |

2026 | | | 3,357 | |

2027 | | | 3,426 | |

2028 | | | 3,496 | |

Thereafter | | | 18,419 | |

| | $ | 33,569 | |

The above rental receipts do not include future lease payments for renewal periods, potential variable CPI rent increases, or variable percentage rent payments that may become due in future periods.

The following table summarizes amounts reported as Lease revenues, net in the Condensed Consolidated Statements of Income and Comprehensive Income:

| | | | | | | | | | | | | | | | | |

| | For the Three Months Ended

June 30, | | | For the Six Months Ended

June 30, | | |

(in thousands) | | 2024 | | | 2023 | | | 2024 | | | 2023 | | |

Contractual rental amounts billed for operating leases | | $ | 95,736 | | | $ | 96,456 | | | $ | 193,285 | | | $ | 194,558 | | |

Adjustment to recognize contractual operating lease billings

on a straight-line basis | | | 5,177 | | | | 7,380 | | | | 10,281 | | | | 14,750 | | |

Net write-offs of accrued rental income | | | — | | | | — | | | | (2,556 | ) | | | (105 | ) | |

Variable rental amounts earned | | | 659 | | | | 452 | | | | 1,257 | | | | 793 | | |

Earned income from direct financing leases | | | 689 | | | | 689 | | | | 1,371 | | | | 1,380 | | |

Interest income from sales-type leases | | | 15 | | | | 15 | | | | 29 | | | | 29 | | |

Operating expenses billed to tenants | | | 4,651 | | | | 4,594 | | | | 9,756 | | | | 9,669 | | |

Other income from real estate transactions | | | 12 | | | | 3 | | | | 79 | | | | 7,395 | | (a) |

Adjustment to revenue recognized for uncollectible rental

amounts billed, net | | | (1,032 | ) | | | (236 | ) | | | (2,228 | ) | | | (124 | ) | |

Total lease revenues, net | | $ | 105,907 | | | $ | 109,353 | | | $ | 211,274 | | | $ | 228,345 | | |

(a)The six months ended June 30, 2023, includes $7.5 million of lease termination fee income recognized in connection with the simultaneous lease termination and sale of an underlying office property for an additional $32.0 million in proceeds.

6. Intangible Assets and Liabilities, and Leasing Fees

The following is a summary of intangible assets and liabilities, and leasing fees, and related accumulated amortization:

| | | | | | | | |

(in thousands) | | June 30,

2024 | | | December 31,

2023 | |

Lease intangibles: | | | | | | |

Acquired above-market leases | | $ | 41,237 | | | $ | 44,711 | |

Less accumulated amortization | | | (18,377 | ) | | | (20,312 | ) |

Acquired above-market leases, net | | | 22,860 | | | | 24,399 | |

Acquired in-place leases | | | 415,062 | | | | 416,206 | |

Less accumulated amortization | | | (155,374 | ) | | | (152,379 | ) |

Acquired in-place leases, net | | | 259,688 | | | | 263,827 | |

Total intangible lease assets, net | | $ | 282,548 | | | $ | 288,226 | |

Acquired below-market leases | | $ | 99,650 | | | $ | 98,535 | |

Less accumulated amortization | | | (46,526 | ) | | | (45,004 | ) |

Intangible lease liabilities, net | | $ | 53,124 | | | $ | 53,531 | |

Leasing fees | | $ | 17,676 | | | $ | 18,117 | |

Less accumulated amortization | | | (6,399 | ) | | | (6,426 | ) |

Leasing fees, net | | $ | 11,277 | | | $ | 11,691 | |

Amortization of intangible lease assets and liabilities, and leasing fees was as follows:

| | | | | | | | | | | | | | | | | | |

(in thousands) | | | | For the Three Months Ended

June 30, | | | For the Six Months Ended

June 30, | |

Intangible | | Financial Statement Presentation | | 2024 | | | 2023 | | | 2024 | | | 2023 | |

Acquired in-place leases and leasing fees | | Depreciation and amortization | | $ | 7,840 | | | $ | 8,001 | | | $ | 15,536 | | | $ | 18,589 | |

Above-market and below-market leases | | Lease revenues, net | | | 1,096 | | | | 1,088 | | | | 2,117 | | | | 3,782 | |

There was no accelerated amortization for the three and six months ended June 30, 2024, respectively. There was no accelerated amortization for the three months ended June 30, 2023. For the six months ended June 30, 2023, amortization expense includes $0.9 million of accelerated amortization resulting from early lease terminations.

Estimated future amortization of intangible assets and liabilities, and leasing fees at June 30, 2024 is as follows:

| | | | |

(in thousands) | | | |

Remainder of 2024 | | $ | 13,401 | |

2025 | | | 26,102 | |

2026 | | | 25,050 | |

2027 | | | 23,161 | |

2028 | | | 20,888 | |

Thereafter | | | 132,099 | |

| | $ | 240,701 | |

7. Unsecured Credit Agreements

The following table summarizes the Company’s unsecured credit agreements:

| | | | | | | | | | | | |

| | Outstanding Balance | | | | | |

(in thousands, except interest rates) | | June 30,

2024 | | | December 31,

2023 | | | Interest Rate | | Maturity Date |

Unsecured revolving credit facility | | $ | 79,096 | | | $ | 90,434 | | | Applicable reference rate + 0.85% (a) | | Mar. 2026 (c) |

Unsecured term loans: | | | | | | | | | | |

2026 Unsecured Term Loan | | | 400,000 | | | | 400,000 | | | one-month adjusted SOFR + 1.00% (b) | | Feb. 2026 |

2027 Unsecured Term Loan | | | 200,000 | | | | 200,000 | | | one-month adjusted SOFR + 0.95% (b) | | Aug. 2027 |

2029 Unsecured Term Loan | | | 300,000 | | | | 300,000 | | | one-month adjusted SOFR + 1.25% (b) | | Aug. 2029 |

Total unsecured term loans | | | 900,000 | | | | 900,000 | | | | | |

Unamortized debt issuance costs, net | | | (3,426 | ) | | | (4,053 | ) | | | | |

Total unsecured term loans, net | | | 896,574 | | | | 895,947 | | | | | |

Senior unsecured notes: | | | | | | | | | | |

2027 Senior Unsecured Notes - Series A | | | 150,000 | | | | 150,000 | | | 4.84% | | Apr. 2027 |

2028 Senior Unsecured Notes - Series B | | | 225,000 | | | | 225,000 | | | 5.09% | | Jul. 2028 |

2030 Senior Unsecured Notes - Series C | | | 100,000 | | | | 100,000 | | | 5.19% | | Jul. 2030 |

2031 Senior Unsecured Public Notes | | | 375,000 | | | | 375,000 | | | 2.60% | | Sep. 2031 |

Total senior unsecured notes | | | 850,000 | | | | 850,000 | | | | | |

Unamortized debt issuance costs and

original issuance discount, net | | | (4,313 | ) | | | (4,691 | ) | | | | |

Total senior unsecured notes, net | | | 845,687 | | | | 845,309 | | | | | |

Total unsecured debt, net | | $ | 1,821,357 | | | $ | 1,831,690 | | | | | |

(a)At June 30, 2024 and December 31, 2023, a balance of $6.0 million and $15.0 million was subject to the one-month SOFR of 5.34% and 5.35%, respectively. The remaining balance of $100 million Canadian Dollar (“CAD”) borrowings remeasured to $73.1 million United States Dollar (”USD”) and $75.4 million USD, at June 30, 2024 and December 31, 2023, respectively, and was subject to the adjusted daily simple CORRA of 4.80% at June 30, 2024 and one-month CDOR, of 5.46% at December 31, 2023. Effective May 24, 2024, the $100 million CAD borrowings converted into an adjusted daily simple CORRA borrowing resulting from CDOR’s cessation in June 2024.

(b)At June 30, 2024 and December 31, 2023, one-month SOFR was 5.34% and 5.35%, respectively.

(c)The Company’s unsecured revolving credit facility contains two six-month extension options subject to certain conditions, including the payment of an extension fee equal to 0.0625% of the revolving commitments.

At June 30, 2024, the weighted average interest rate on all outstanding borrowings was 5.30% exclusive of interest rate swap agreements, and 3.73% inclusive of interest rate swap agreements.

The Company is subject to various financial and operational covenants and financial reporting requirements pursuant to its unsecured credit agreements. These covenants require the Company to maintain certain financial ratios. As of June 30, 2024, and for all periods presented, the Company believes it was in compliance with all of its loan covenants. Failure to comply with the covenants would result in a default which, if the Company were unable to cure or obtain a waiver from the lenders, could accelerate the repayment of the obligations. Further, in the event of default, the Company may be restricted from paying dividends to its stockholders in excess of dividends required to maintain its REIT qualification. Accordingly, an event of default could have a material effect on the Company.

Debt issuance costs and original issuance discounts are amortized as a component of Interest expense in the accompanying Condensed Consolidated Statements of Income and Comprehensive Income. The following table summarizes debt issuance cost and original issuance discount amortization:

| | | | | | | | | | | | | | | | |

| | For the Three Months Ended

June 30, | | | For the Six Months Ended

June 30, | |

(in thousands) | | 2024 | | | 2023 | | | 2024 | | | 2023 | |

Debt issuance costs and original issuance discount amortization | | $ | 983 | | | $ | 986 | | | $ | 1,966 | | | $ | 1,972 | |

8. Mortgages

The Company’s mortgages consist of the following:

| | | | | | | | | | | | | | | | |

| | Origination | | Maturity | | | | | | | | | | |

(in thousands, except interest rates) | | Date | | Date | | Interest | | June 30, | | | December 31, | | | |

Lender | | (Month/Year) | | (Month/Year) | | Rate | | 2024 | | | 2023 | | | |

Wilmington Trust National Association | | Apr-19 | | Feb-28 | | 4.92% | | $ | 43,531 | | | $ | 44,207 | | | (a) (b) (c) (d) |

Wilmington Trust National Association | | Jun-18 | | Aug-25 | | 4.36% | | | 18,506 | | | | 18,725 | | | (a) (b) (c) (d) |

PNC Bank | | Oct-16 | | Nov-26 | | 3.62% | | | 16,018 | | | | 16,241 | | | (b) (c) |

Total mortgages | | | | | | | | | 78,055 | | | | 79,173 | | | |

Debt issuance costs, net | | | | | | | | | (85 | ) | | | (105 | ) | | |

Mortgages, net | | | | | | | | $ | 77,970 | | | $ | 79,068 | | | |

(a)Non-recourse debt includes the indemnification/guaranty of the Company pertaining to fraud, environmental claims, insolvency, and other matters.

(b)Debt secured by related rental property and lease rents.

(c)Debt secured by guaranty of the OP.

(d)Mortgage was assumed as part of the acquisition of the related property. The debt was recorded at fair value at the time of assumption.

At June 30, 2024, investment in rental property of $119.1 million was pledged as collateral against the Company’s mortgages.

Estimated future principal payments to be made under the above mortgages and the Company’s unsecured credit agreements (see Note 7) at June 30, 2024 are as follows:

| | | | |

(in thousands) | | | |

Remainder of 2024 | | $ | 1,143 | |

2025 | | | 20,195 | |

2026 | | | 495,939 | |

2027 | | | 351,596 | |

2028 | | | 263,278 | |

Thereafter | | | 775,000 | |

| | $ | 1,907,151 | |

Certain of the Company’s mortgages provide for prepayment fees and can be terminated under certain events of default as defined under the related agreements. These prepayment fees are not reflected as part of the table above.

9. Interest Rate Swaps

During the three months ended June 30, 2024, the Company entered into nine forward-starting interest rate swaps with various institutions for a total notional amount of $460.0 million in order to mitigate the impact of interest rate variability over the term of the Company’s current and expected debt obligations. These swap arrangements are effective during various periods between March and December 2025 and mature in 2030.

The following is a summary of the Company’s outstanding interest rate swap agreements:

| | | | | | | | | | | | | | | | | | | | | | | | | |

(in thousands, except interest rates) | | | | | | | June 30, 2024 | | | December 31, 2023 | | |

Counterparty | | Maturity Date | | Fixed

Rate | | | Variable Rate Index (a) | | Notional

Amount | | | Fair

Value | | | Notional

Amount | | | Fair

Value | | |

Effective Swaps: | | | | | | | | | | | | | | | | | | | | |

Wells Fargo Bank, N.A. | | October 2024 | | | 2.72 | % | | daily compounded SOFR | | $ | 15,000 | | | $ | 103 | | | $ | 15,000 | | | $ | 255 | | |

Capital One, National Association | | December 2024 | | | 1.58 | % | | daily compounded SOFR | | | 15,000 | | | | 239 | | | | 15,000 | | | | 445 | | |

Bank of Montreal | | January 2025 | | | 1.91 | % | | daily compounded SOFR | | | 25,000 | | | | 428 | | | | 25,000 | | | | 713 | | |

Truist Financial Corporation | | April 2025 | | | 2.20 | % | | daily compounded SOFR | | | 25,000 | | | | 553 | | | | 25,000 | | | | 734 | | |

Bank of Montreal | | July 2025 | | | 2.32 | % | | daily compounded SOFR | | | 25,000 | | | | 670 | | | | 25,000 | | | | 768 | | |

Truist Financial Corporation | | July 2025 | | | 1.99 | % | | daily compounded SOFR | | | 25,000 | | | | 751 | | | | 25,000 | | | | 888 | | |

Truist Financial Corporation | | December 2025 | | | 2.30 | % | | daily compounded SOFR | | | 25,000 | | | | 911 | | | | 25,000 | | | | 887 | | |

Bank of Montreal | | January 2026 | | | 1.92 | % | | daily compounded SOFR | | | 25,000 | | | | 1,054 | | | | 25,000 | | | | 1,071 | | |

Bank of Montreal | | January 2026 | | | 2.05 | % | | daily compounded SOFR | | | 40,000 | | | | 1,611 | | | | 40,000 | | | | 1,615 | | |

Capital One, National Association | | January 2026 | | | 2.08 | % | | daily compounded SOFR | | | 35,000 | | | | 1,395 | | | | 35,000 | | | | 1,389 | | |

Truist Financial Corporation | | January 2026 | | | 1.93 | % | | daily compounded SOFR | | | 25,000 | | | | 1,051 | | | | 25,000 | | | | 1,067 | | |

Capital One, National Association | | April 2026 | | | 2.68 | % | | daily compounded SOFR | | | 15,000 | | | | 517 | | | | 15,000 | | | | 439 | | |

Capital One, National Association | | July 2026 | | | 1.32 | % | | daily compounded SOFR | | | 35,000 | | | | 2,216 | | | | 35,000 | | | | 2,186 | | |

Bank of Montreal | | December 2026 | | | 2.33 | % | | daily compounded SOFR | | | 10,000 | | | | 509 | | | | 10,000 | | | | 423 | | |

Bank of Montreal | | December 2026 | | | 1.99 | % | | daily compounded SOFR | | | 25,000 | | | | 1,473 | | | | 25,000 | | | | 1,299 | | |

Toronto-Dominion Bank | | March 2027 | | | 2.46 | % | | one-month CDOR | | | 14,619 | | (b) | | 588 | | | | 15,087 | | (b) | | 572 | | |

Wells Fargo Bank, N.A. | | April 2027 | | | 2.72 | % | | daily compounded SOFR | | | 25,000 | | | | 1,102 | | | | 25,000 | | | | 806 | | |

Bank of Montreal | | December 2027 | | | 2.37 | % | | daily compounded SOFR | | | 25,000 | | | | 1,557 | | | | 25,000 | | | | 1,215 | | |

Capital One, National Association | | December 2027 | | | 2.37 | % | | daily compounded SOFR | | | 25,000 | | | | 1,550 | | | | 25,000 | | | | 1,197 | | |

Wells Fargo Bank, N.A. | | January 2028 | | | 2.37 | % | | daily compounded SOFR | | | 75,000 | | | | 4,665 | | | | 75,000 | | | | 3,632 | | |

Bank of Montreal | | May 2029 | | | 2.09 | % | | daily compounded SOFR | | | 25,000 | | | | 2,267 | | | | 25,000 | | | | 1,835 | | |

Regions Bank | | May 2029 | | | 2.11 | % | | daily compounded SOFR | | | 25,000 | | | | 2,237 | | | | 25,000 | | | | 1,801 | | |

Regions Bank | | June 2029 | | | 2.03 | % | | daily compounded SOFR | | | 25,000 | | | | 2,329 | | | | 25,000 | | | | 1,900 | | |

U.S. Bank National Association | | June 2029 | | | 2.03 | % | | daily compounded SOFR | | | 25,000 | | | | 2,334 | | | | 25,000 | | | | 1,908 | | |

Regions Bank | | August 2029 | | | 2.58 | % | | one-month SOFR | | | 100,000 | | | | 6,462 | | | | 100,000 | | | | 4,392 | | |

Toronto-Dominion Bank | | August 2029 | | | 2.58 | % | | one-month SOFR | | | 45,000 | | | | 2,946 | | | | 45,000 | | | | 2,021 | | |

U.S. Bank National Association | | August 2029 | | | 2.65 | % | | one-month SOFR | | | 15,000 | | | | 932 | | | | 15,000 | | | | 618 | | |

U.S. Bank National Association | | August 2029 | | | 2.58 | % | | one-month SOFR | | | 100,000 | | | | 6,490 | | | | 100,000 | | | | 4,427 | | |

U.S. Bank National Association | | August 2029 | | | 1.35 | % | | daily compounded SOFR | | | 25,000 | | | | 3,192 | | | | 25,000 | | | | 2,828 | | |

Regions Bank | | March 2032 | | | 2.69 | % | | one-month CDOR | | | 14,619 | | (b) | | 931 | | | | 15,087 | | (b) | | 677 | | |

U.S. Bank National Association | | March 2032 | | | 2.70 | % | | one-month CDOR | | | 14,619 | | (b) | | 930 | | | | 15,087 | | (b) | | 678 | | |

Bank of Montreal | | March 2034 | | | 2.81 | % | | one-month CDOR | | | 29,239 | | (c) | | 2,082 | | | | 30,174 | | (c) | | 1,410 | | |

| | | | | | | | | | 973,096 | | | | 56,075 | | | | 975,435 | | | | 46,096 | | |

Forward Starting Swaps: (d) | | | | | | | | | | | | | | | | | | | | |

Bank of Montreal | | March 2030 | | | 3.80 | % | | daily simple SOFR | | | 80,000 | | | | — | | | | — | | | | — | | |

JPMorgan Chase Bank, N.A. | | March 2030 | | | 3.79 | % | | daily simple SOFR | | | 50,000 | | | | 35 | | | | — | | | | — | | |

U.S. Bank National Association | | June 2030 | | | 3.73 | % | | daily simple SOFR | | | 70,000 | | | | 76 | | | | — | | | | — | | |

Truist Financial Corporation | | June 2030 | | | 3.73 | % | | daily simple SOFR | | | 55,000 | | | | 48 | | | | — | | | | — | | |

Manufacturers & Traders Trust Company | | September 2030 | | | 3.71 | % | | daily simple SOFR | | | 50,000 | | | | 29 | | | | — | | | | — | | |

Regions Bank | | September 2030 | | | 3.69 | % | | daily simple SOFR | | | 15,000 | | | | 13 | | | | — | | | | — | | |

Truist Financial Corporation | | September 2030 | | | 3.70 | % | | daily simple SOFR | | | 15,000 | | | | 14 | | | | — | | | | — | | |

Toronto-Dominion Bank | | December 2030 | | | 3.66 | % | | daily simple SOFR | | | 70,000 | | | | 101 | | | | — | | | | — | | |

Regions Bank | | December 2030 | | | 3.66 | % | | daily simple SOFR | | | 55,000 | | | | 53 | | | | — | | | | — | | |

| | | | | | | | | | 460,000 | | | | 369 | | | | — | | | | — | | |

Total Swaps | | | | | | | | | $ | 1,433,096 | | | $ | 56,444 | | | $ | 975,435 | | | $ | 46,096 | | |

(a)Effective July 1, 2024, the variable rate index for CDOR based swaps will convert to daily compounded CORRA concurrent with CDOR’s cessation.

(b)The contractual notional amount is $20.0 million CAD.

(c)The contractual notional amount is $40.0 million CAD.

(d)Forward starting swaps have effective dates that are five years prior to each respective maturity date.

At June 30, 2024, the weighted average interest rate on all outstanding borrowings was 3.73%, inclusive of a weighted average fixed rate on effective interest rate swaps of 2.28%.

The total amounts recognized, and the location in the accompanying Condensed Consolidated Statements of Income and Comprehensive Income, from converting from variable rates to fixed rates under these agreements were as follows:

| | | | | | | | | | | | | | |

| | Amount of (Loss) Gain | | | Reclassification from | | | Total Interest Expense | |

| | Recognized in | | | Accumulated Other | | | Presented in the Condensed | |

| | Accumulated Other | | | Comprehensive Income | | | Consolidated Statements of | |

(in thousands) | | Comprehensive | | | | | Amount of | | | Income and Comprehensive | |

For the Three Months Ended June 30, | | Income | | | Location | | Gain | | | Income | |

2024 | | $ | (1,456 | ) | | Interest expense | | $ | 7,619 | | | $ | 17,757 | |

2023 | | | 19,652 | | | Interest expense | | | 6,182 | | | | 20,277 | |

| | | | | | | | | | | | | | |

| | Amount of Gain | | | Reclassification from | | | Total Interest Expense | |

| | Recognized in | | | Accumulated Other | | | Presented in the Condensed | |

| | Accumulated Other | | | Comprehensive Income | | | Consolidated Statements of | |

(in thousands) | | Comprehensive | | | | | Amount of | | | Income and Comprehensive | |

For the Six Months Ended June 30, | | Income | | | Location | | Gain | | | Income | |

2024 | | $ | 10,348 | | | Interest expense | | $ | 15,167 | | | $ | 36,334 | |

2023 | | | 1,753 | | | Interest expense | | | 11,179 | | | | 41,416 | |

Amounts related to the interest rate swaps expected to be reclassified out of Accumulated other comprehensive income to Interest expense during the next twelve months are estimated to be a gain of $25.3 million.

10. Non-Controlling Interests

The following table summarizes OP Units exchanged for shares of common stock:

| | | | | | | | | | | | | | | | |

| | For the Three Months Ended

June 30, | | | For the Six Months Ended

June 30, | |

(in thousands) | | 2024 | | | 2023 | | | 2024 | | | 2023 | |

OP Units exchanged for shares of common stock | | | 32 | | | | 25 | | | | 127 | | | | 921 | |

Value of units exchanged | | $ | 532 | | | $ | 398 | | | $ | 2,068 | | | $ | 15,295 | |

11. Credit Risk Concentrations

The Company maintained bank balances that, at times, exceeded the federally insured limit during the six months ended June 30, 2024. The Company has not experienced losses relating to these deposits and management does not believe that the Company is exposed to any significant credit risk with respect to these amounts based on the financial position and capitalization of the banks.

For the six months ended June 30, 2024 and 2023, the Company had no individual tenants or common franchises that accounted for more than 10% of Lease revenues, net, excluding lease termination fees.

12. Equity

At-the-Market Program (“ATM Program”)

In May 2024, the Company replaced its prior ATM Program with a new ATM Program, through which it may, from time to time, publicly offer and sell shares of common stock having an aggregate gross sales price of up to $400.0 million. The Company’s ATM Program provides for forward sale agreements, enabling the Company to set the price of shares upon pricing the offering, while delaying the issuance of shares and the receipt of the net proceeds. The Company was authorized to publicly offer and sell shares of common stock having an aggregate gross sales price of up to $400.0 million under the prior ATM Program, of which the Company sold shares of common stock having an aggregate gross sales price of $254.6 million. During the six months ended June 30, 2024, and June 30, 2023, no shares were issued under the applicable ATM Program and, as of June 30, 2024, the Company has $400.0 million of available capacity under the new ATM Program.

Share Repurchase Program

The Company has a stock repurchase program (the “Repurchase Program”), which authorizes the Company to repurchase up to $150.0 million of the Company’s common stock. On March 12, 2024, the Company’s Board of Directors re-authorized the Repurchase Program for a 12-month period beginning on March 14, 2024. Under the Repurchase Program, repurchases of the Company’s stock can be made in the open market or through private transactions from time to time over the 12-month period, depending on prevailing market conditions and compliance with applicable legal and regulatory requirements. The timing, manner, price, and amount of any repurchases of common stock under the Repurchase Program will be determined at the Company’s discretion, using available cash resources. During the six months ended June 30, 2024 and 2023, no shares of the Company’s common stock were repurchased under the Repurchase Program.

13. Stock-Based Compensation

Restricted Stock Awards

During the three and six months ended June 30, 2024, the Company awarded 55,064 and 833,007 shares of restricted stock awards (“RSAs”), respectively, to officers, employees and non-employee directors under the Company’s equity incentive plan. During the three and six months ended June 30, 2023, the Company awarded 50,531 and 309,630 shares of RSAs, respectively, to officers, employees and non-employee directors under the Company’s equity incentive plan. The holder of RSAs is generally entitled at all times on and after the date of issuance of the restricted common shares to exercise the rights of a stockholder of the Company, including the right to vote the shares and the right to receive dividends on the shares. The RSAs vest over a one-, three-, four-, or five-year period from the date of the grant and are subject to the holder’s continued service through the applicable vesting dates and in accordance with the terms of the individual award agreements. The weighted average value of awards granted per share during the three and six months ended June 30, 2024, were $15.23 and $14.77, respectively, which were based on the market price per share of the Company’s common stock on the grant dates. The weighted average value of awards granted per share during the three and six months ended June 30, 2023, were $16.33 and $17.52, respectively.

The following table presents information about the Company’s RSAs:

| | | | | | | | | | | | | | | | |

| | For the Three Months Ended

June 30, | | | For the Six Months Ended

June 30, | |

(in thousands) | | 2024 | | | 2023 | | | 2024 | | | 2023 | |

Compensation cost | | $ | 1,346 | | | $ | 932 | | | $ | 2,389 | | | $ | 2,660 | |

Dividends declared on unvested RSAs | | | 300 | | | | 142 | | | | 595 | | | | 278 | |

Fair value of shares vested during the period | | | 762 | | | | 520 | | | | 3,969 | | | | 3,384 | |

As of June 30, 2024, there was $14.4 million of unrecognized compensation costs related to the unvested restricted shares, which is expected to be recognized over a weighted average period of 3.6 years.

The following table presents information about the Company’s restricted stock activity:

| | | | | | | | | | | | | | | | |

| | For the Three Months Ended June 30, | |

| | 2024 | | | 2023 | |

(in thousands, except per share amounts) | | Number of Shares | | | Weighted Average

Grant Date Fair

Value per Share | | | Number of Shares | | | Weighted Average

Grant Date Fair

Value per Share | |

Unvested at beginning of period | | | 1,036 | | | $ | 15.57 | | | | 495 | | | $ | 19.00 | |

Granted | | | 55 | | | | 15.23 | | | | 51 | | | | 16.33 | |

Vested | | | (50 | ) | | | 16.33 | | | | (32 | ) | | | 20.22 | |

Forfeited | | | (5 | ) | | | 16.98 | | | | (6 | ) | | | 18.90 | |

Unvested at end of period | | | 1,036 | | | | 15.51 | | | | 508 | | | | 18.65 | |

| | | | | | | | | | | | | | | | |

| | For the Six Months Ended June 30, | |

| | 2024 | | | 2023 | |

(in thousands, except per share amounts) | | Number of Shares | | | Weighted Average

Grant Date Fair

Value per Share | | | Number of Shares | | | Weighted Average

Grant Date Fair

Value per Share | |

Unvested at beginning of period | | | 492 | | | $ | 18.63 | | | | 396 | | | $ | 20.36 | |

Granted | | | 833 | | | | 14.77 | | | | 310 | | | | 17.52 | |

Vested | | | (259 | ) | | | 18.70 | | | | (192 | ) | | | 20.33 | |

Forfeited | | | (30 | ) | | | 18.68 | | | | (6 | ) | | | 18.90 | |

Unvested at end of period | | | 1,036 | | | | 15.51 | | | | 508 | | | | 18.65 | |

Performance-based Restricted Stock Units

During the six months ended June 30, 2024, the Company issued target grants of 202,308 of performance-based restricted stock units (“PRSUs”), under the Company’s equity incentive plan to the officers of the Company. During the six months ended June 30, 2023, the Company issued target grants of 186,481 of PRSUs. During the three months ended June 30, 2024 and 2023, there were no PRSUs issued. The awards are non-vested restricted stock units where the vesting percentages and the ultimate number of units vesting will be measured 50% based on the relative total shareholder return (“rTSR”) of the Company’s common stock as compared to the rTSR of peer companies, as identified in the grant agreements, over a three-year period, and 50% based on the rTSR of the Company’s common stock as compared to the rTSR of the MSCI US REIT Index over a three year measurement period. Vesting percentages range from 0% to 200% with a target of 100%. rTSR means the percentage appreciation in the fair market value of one share over the three-year measurement period beginning on the date of grant, assuming the reinvestment of dividends on the ex-dividend date. The target number of units is based on achieving a rTSR equal to the 55th percentile of the peer companies and MSCI US REIT Index. For PRSUs issued during the six months ended June 30, 2024 that achieve a percentile rank of at least the 55th percentile, and the absolute rTSR of the Company is negative for the performance period, the awards will be reduced by 25%, not to result in a reduction less than target. Dividends accrue during the measurement period and will be paid on the PRSUs ultimately earned at the end of the measurement period in either cash or common stock, at the discretion of the Compensation Committee of the Board of Directors. The grant date fair value of the PRSUs was measured using a Monte Carlo simulation model based on assumptions including share price volatility.

The following table presents compensation cost recognized on the Company’s performance-based restricted stock units:

| | | | | | | | | | | | | | | | |

| | For the Three Months Ended

June 30, | | | For the Six Months Ended

June 30, | |

(in thousands) | | 2024 | | | 2023 | | | 2024 | | | 2023 | |

Compensation cost | | $ | 727 | | | $ | 607 | | | $ | 1,159 | | | $ | 758 | |

As of June 30, 2024, there was $5.4 million of unrecognized compensation costs related to the unvested PRSUs, which is expected to be recognized over a weighted average period of 2.1 years.

The following table presents information about the Company’s performance-based restricted stock unit activity:

| | | | | | | | | | | | | | | | |