1 1 September 3, 2013 Barclays Back-to-School Consumer Conference Exhibit 99.1 |

2 2 Chairman, President and Chief Executive Officer Murray S. Kessler |

3 Safe Harbor Disclaimer Safe Harbor Disclaimer You are cautioned that certain statements made in this presentation are “forward-looking” statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements include, without limitation, any statement that may project, indicate or imply future results, events, performance or achievements, and may contain the words “expect”, “intend”, “plan”, “anticipate”, “estimate”, “believe”, “will be”, “will continue”, “will likely result”, and similar expressions. In addition, any statement that may be provided by management concerning future financial performance (including future revenues, earnings or growth rates), ongoing business strategies or prospects, and possible actions by Lorillard, Inc. are also forward-looking statements as defined by the Act. Forward-looking statements are based on current expectations and projections about future events and are inherently subject to a variety of risks and uncertainties, many of which are beyond the control of Lorillard, Inc., and could cause actual results to differ materially from those anticipated or projected. Information describing factors that could cause actual results to differ materially from those in forward-looking statements is available in Lorillard, Inc.’s various filings with the Securities and Exchange Commission (“SEC”). These filings are available from the SEC over the Internet or on hard copy, and are, in some cases, available from Lorillard, Inc. as well. Forward-looking statements speak only as of the time they are made, and Lorillard, Inc. expressly disclaims any obligation or undertaking to update these statements to reflect any change in expectations or beliefs or any change in events, conditions or circumstances on which any forward-looking statement is based. This forward-looking statements disclaimer is only a brief summary of Lorillard, Inc.’s statutory forward-looking-statements disclaimer. You are urged to read that disclaimer, which is included in Lorillard Inc.’s Form 10-K and Form 10-Q filings with the SEC. |

4 Regulation G Compliance Regulation G Compliance You are also reminded that during this presentation, certain non-GAAP financial measures, such as Adjusted Earnings Per Share may be discussed. These measures should not be considered an alternative to net income, or any other measure of financial performance or liquidity presented in accordance with generally accepted accounting principles (GAAP). These measures are not necessarily comparable to a similarly titled measure of another company. Please refer to Appendix A for information that reconciles these measures with the most comparable GAAP measures. |

5 Lorillard is the #3 Tobacco Company in the USA Lorillard is the #3 Tobacco Company in the USA With Very Strong Brands With Very Strong Brands Source: Lorillard proprietary retail database (“EXCEL”). As of full year ended 12/31/2012. • The #2 U.S. Cigarette Brand - Newport ® • The #1 U.S. Menthol Brand - Newport • The #1 U.S. electronic cigarette – blu eCigs ® |

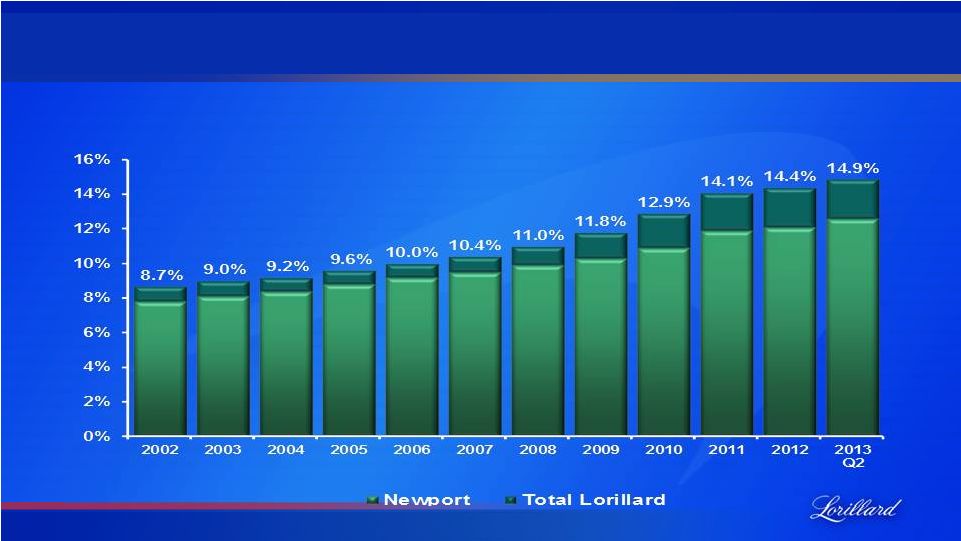

6 In Cigarettes, Lorillard has Gained Market Share In Cigarettes, Lorillard has Gained Market Share For Eleven Consecutive Years For Eleven Consecutive Years Lorillard Retail Market Share of U.S. Cigarettes Lorillard Retail Market Share of U.S. Cigarettes Source: MSA, Inc. Excel retail database. Source: MSA, Inc. Excel retail database. |

Driving a Consistent Track Record of Superior Financial Results Driving a Consistent Track Record of Superior Financial Results * Adjusted results. See Appendix A for further discussion of adjustments. Source: Company filings. 7 |

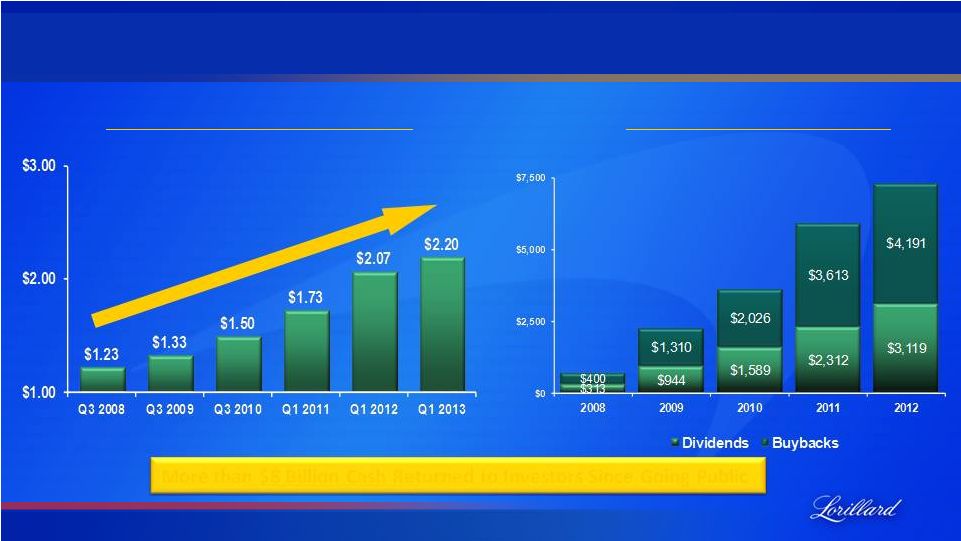

8 Allowing The Company to Return Significant Cash to Shareholders Allowing The Company to Return Significant Cash to Shareholders +79% Annualized Dividend Per Share $713 $2,254 $3,615 $5,925 $7,310 Cumulative Cash Returned In millions More than $8 Billion Cash Returned to Investors Since Going Public Source: Lorillard filings. Since Lorillard spin-off completed in June 2008. Dividend data adjusted to reflect 3-for-1 stock split effected January 15, 2013. |

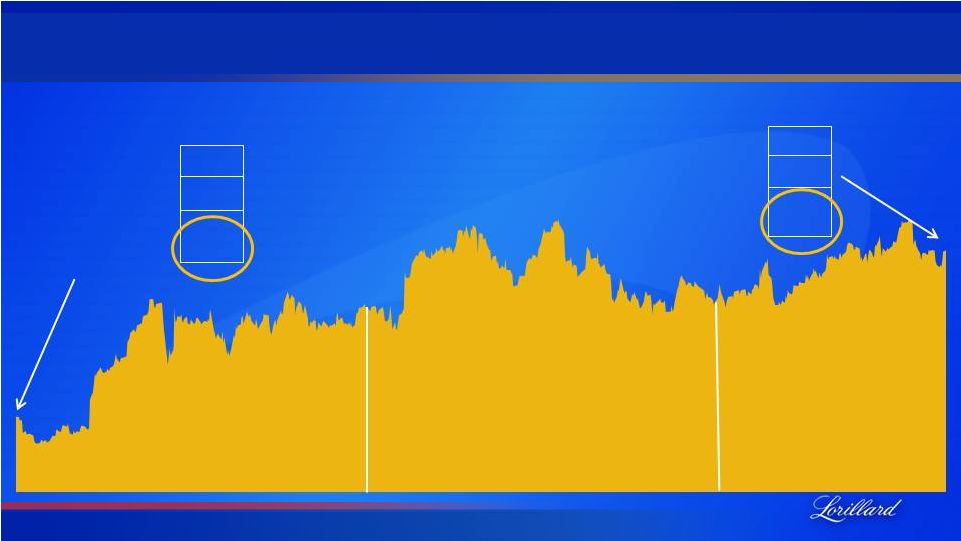

9 And Ultimately Contributing To Significant Increases In And Ultimately Contributing To Significant Increases In Shareholder Value Shareholder Value 2011 2012 Source: Bloomberg. As of August 27, 2013 Source: Bloomberg. As of August 27, 2013 Stock Price P/E Ratio Enterprise Value (B) 12.1 $11.8 $27 P/E Ratio Enterprise Value (B) 14.5 $18.1 Stock Price $43 2013 More than $6 billion of value creation since 12/31/2010 |

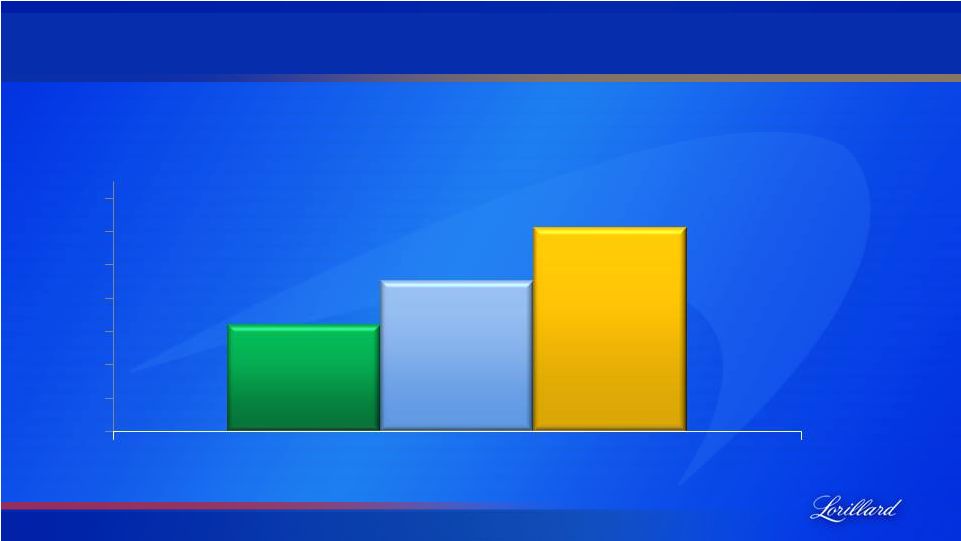

10 The First Half of 2013 Has Been a Continuation of The First Half of 2013 Has Been a Continuation of Lorillard’s Industry-Leading Fundamentals Lorillard’s Industry-Leading Fundamentals Lorillard YTD 2013 performance through June 30 versus year ago * Adjusted results. See Appendix A for further discussion of adjustments. Source: Company filings. Operating Income* E.P.S.* 6.4% 9.0% 12.2% 0% 2% 4% 6% 8% 10% 12% 14% YTD 2013 Change Net Sales (ex-FET) |

Pursuit of Lorillard’s Strategic Vision Should Allow The Company to Continue Delivering Superior Results Protect & Grow The Core “To Responsibly Bring Newport Pleasure To All Adult Smokers” * Double-digit shareholder return as measured by EPS growth and the dividend yield. With a Goal of Consistently Delivering a Double-Digit Shareholder Return* Over the Long-Term 11 Build Out Processes and Capabilities Carefully Pursue Close-in Adjacencies |

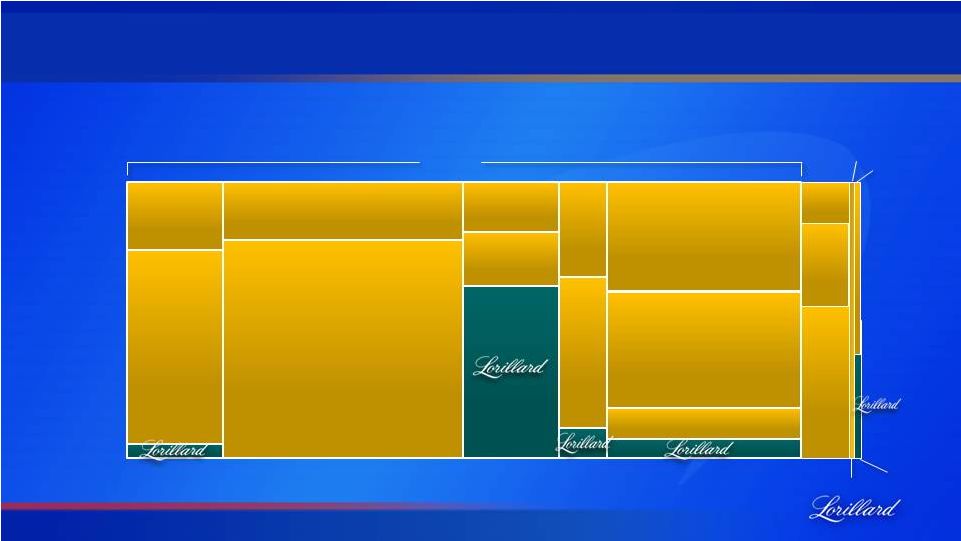

12 As The Company Uniquely has Numerous Close-In “White Space” Growth Opportunities it is Pursuing, While Protecting its Core Franchise 2012 U.S. Tobacco Market Segmentation 100% 80% 60% 40% 20% 0% NFF Menthol Discount MST 0.2 % 8.8 % 90.5 % 15.1 B Packs/Cans RJR Altria Altria RJR RJR Altria All Others RJR Altria RJR Altria Others RJR Altria 0.5 % Snus Source: MSA, Inc. Excel retail database. Non-Full Flavor Non-Menthol Full-Flavor Menthol e-Cigs Full-Flavor Non-Menthol |

13 1. Profitably maintain a stable Newport Full-Flavor franchise in the core through a disciplined and focused approach 2. Offset cigarette industry declines through close-in adjacency expansion – Geographic expansion of Newport promotions west of the Mississippi River – Product expansion into Non-Menthol (Red & Gold) 3. Establish Lorillard as “first and best” with blu eCigs in electronic cigarettes 4. Defend Lorillard’s freedom to operate – hold regulators to science-based decisions 5. Continue to reward shareholders with superior returns Accordingly, Lorillard’s Strategic Priorities Are as Follows: Accordingly, Lorillard’s Strategic Priorities Are as Follows: |

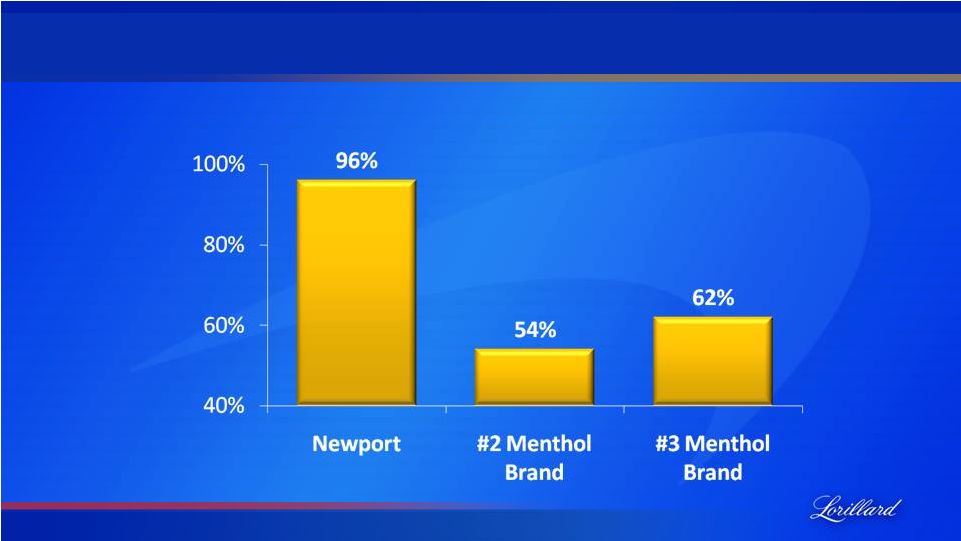

14 FF Menthol Rest of Industry Stability of Newport Full-Flavor Menthol in the Core is Job #1 Premium Full-Flavor Menthol, Core States Premium Full-Flavor Menthol, Core States Newport Newport All Other All Other Newport All Other Newport All Other 74% 74% 73% 74% Newport Share of Premium Full-Flavor Menthol Core States 5 Year CAGRs 2007 - 2012 -1.2% -5.0% Source: MSA, Inc. Excel retail database. Year-to-date 2013 as of August 17, 2013. 0% 20% 40% 60% 80% 100% 2010 2011 2012 2013 YTD |

15 Advertising Advertising Achieved Through Strong Brand-Building Achieved Through Strong Brand-Building Brand-Building Initiatives Brand-Building Initiatives Product Product Merchandising Merchandising • Consistent 40-year campaign • Distinctive & recognizable • Proven messaging • Iconic brand • Consumer preferred • Unique taste profile • 32,000 new retail plans • New product visibility • Best relationships in industry 61% Net Promoter Score |

16 Percentage of 2013 Menthol Volume Sold at Full Price* Percentage of 2013 Menthol Volume Sold at Full Price* * Source: MSA, Inc. Excel retail database, year-to-date through 8/17/2013. Full price is defined as within 50 cents per pack of the most common retail price of the mainline brand. And Achieved Without Heavy Use of Discounting And Achieved Without Heavy Use of Discounting |

17 1. Profitably maintain a stable Newport Full-Flavor franchise in the core through a disciplined and focused approach 2. Offset cigarette industry declines through close-in adjacency expansion – Geographic expansion of Newport promotions west of the Mississippi River – Product expansion into Non-Menthol (Red & Gold) 3. Establish Lorillard as “first and best” with blu eCigs in electronic cigarettes 4. Defend Lorillard’s freedom to operate – hold regulators to science-based decisions 5. Continue to reward shareholders with superior returns Lorillard’s Strategic Priorities Lorillard’s Strategic Priorities |

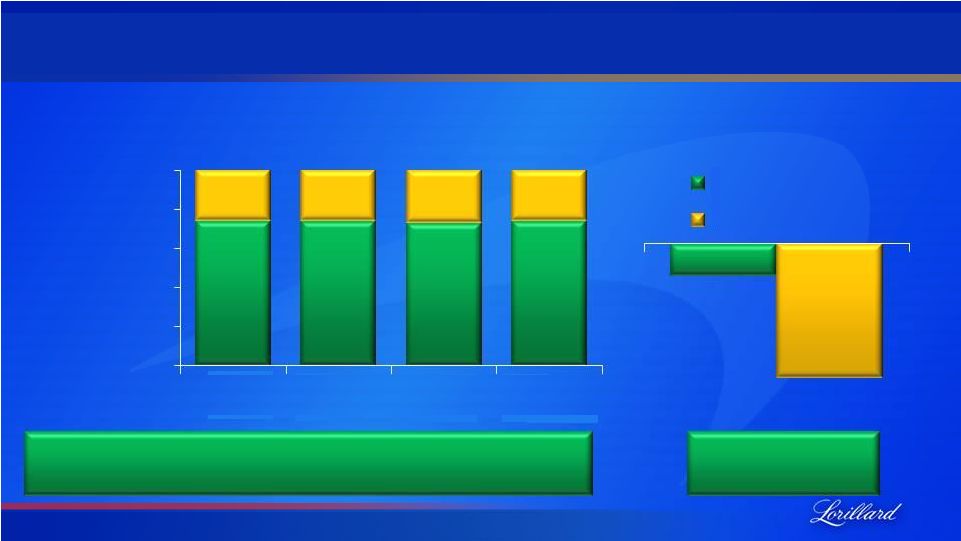

18 Results from geographic expansion strategy in the non-core Newport Total Lorillard Source: MSA, Inc. Excel retail database. Pre-period is 2009 change and Post-period is 2012 change. Geographic Expansion of Promotions and Product Line Geographic Expansion of Promotions and Product Line Have Been Successful Have Been Successful -4.9% 5.5% Volume Trends 4.3% 5.0% Market Share 5.5% 7.3% Pre Post -1.1% 18.6% Pre Post |

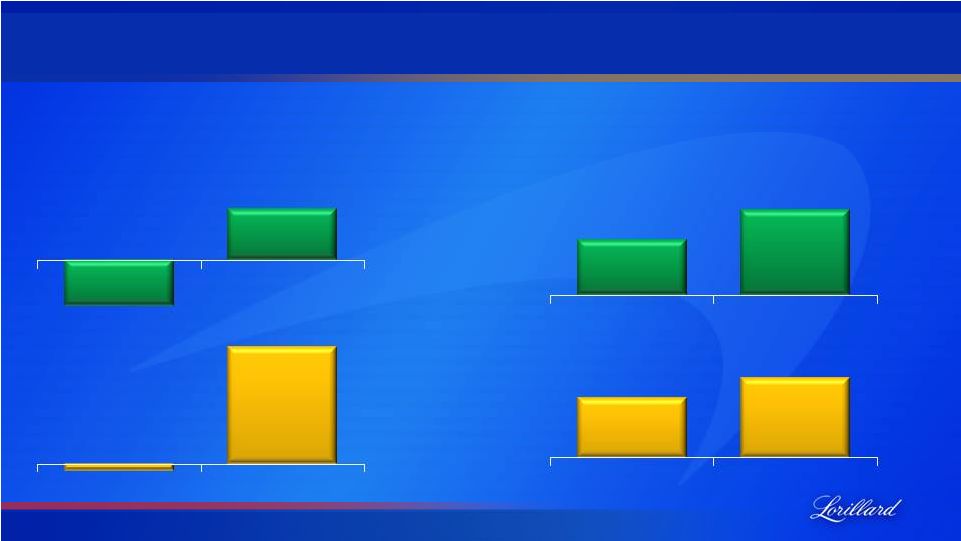

19 Source: MSA, Inc. Excel retail database. As Has Lorillard’s Entry into Non-Menthol, First with As Has Lorillard’s Entry into Non-Menthol, First with Newport Red Newport Red Premium Non-Menthol Full Flavor Premium Non-Menthol Full Flavor Units by Brand Units by Brand • 0.9% retail market share • 2.2 billion units in 2012 • Pricing up more than 35% since launch |

20 Non-Menthol Gold Represents an Even Bigger Opportunity Non-Menthol Gold Represents an Even Bigger Opportunity Sources: MSA, Inc. Excel Retail Database ; Newport 80mm Box Gold Non-Menthol Product Test, January 2011; Newport Non-Menthol Gold Online Packaging Test, August 2011; • Recently authorized by FDA • Consumer-preferred taste • Consumer-preferred packaging • Priced in-line with Newport Red Premium Non-Menthol Non-Full Flavor Premium Non-Menthol Non-Full Flavor Units by Brand Units by Brand |

Shipments Expected to Commence on October 4, 2013 21 |

1. Profitably maintain a stable Newport Full-Flavor franchise in the core through a disciplined and focused approach 2. Offset cigarette industry declines through close-in adjacency expansion – Geographic expansion of Newport promotions west of the Mississippi River – Product expansion into Non-Menthol (Red & Gold) 3. Establish Lorillard as “first and best” with blu eCigs in electronic cigarettes 4. Defend Lorillard’s freedom to operate – hold regulators to science-based decisions 5. Continue to reward shareholders with superior returns Lorillard’s Strategic Priorities 22 |

• Category estimated at $1 billion with 100% annual market growth • Awareness = ~100% • Trial = 43% • Repeat Usage = 26% • ~1% impact on cigarettes • Gives Lorillard a major seat in the harm reduction debate Lorillard’s Acquisition of blu eCigs Gives the Company A Head-Start in an Emerging New Category Sources: Wells Fargo/Nielsen estimates, research note dated 7/26/2013; Lorillard Adult Tobacco User Survey; May 2013 (n=523) 23 |

• National retail roll-out – 110,000+ outlets currently • National TV and print advertising campaign ($40 MM 2013 marketing spend) • Product enhancements & quality controls • Increased manufacturing capacity & inventory Lorillard Has Been Focused on Being First and Best 24 |

Brand-Building is the Top Priority Stephen Dorff Jenny McCarthy 25 |

26 Old Pack New Pack MSRP $59.99 $34.99 Size Cigarette pack Slim as a smart phone Battery Pack charge indicator Pack & cig charge indicator Retailer margin ~20% ~30% Lorillard Believes that Rechargeables are the Key to Long-Term Profitability and Achieving Margins Comparable to Cigarettes |

Source: MSA, Inc. Excel retail database for electronic cigarettes, as of July 31, 2013. * blu eCigs internal estimates. ~10% Market Share* ~12,000 Retail Outlets Quarterly blu eCigs Retail Market Share 40%+ Market Share ~110,000 Retail Outlets Through These Efforts, blu eCigs has Emerged as The #1 e-Cig Company 50% 40% 30% 20% 10% 0% Q2 2012 Q3 2012 Q4 2012 YTD 2013 44% 34% 15% * 10% * EPS Accretive in Year 1 27 |

28 1. Profitably maintain a stable Newport Full-Flavor franchise in the core through a disciplined and focused approach 2. Offset cigarette industry declines through close-in adjacency expansion – Geographic expansion of Newport promotions west of the Mississippi River – Product expansion into Non-Menthol (Red & Gold) 3. Establish Lorillard as “first and best” with blu eCigs in electronic cigarettes 4. Defend Lorillard’s freedom to operate – hold regulators to science-based decisions 5. Continue to reward shareholders with superior returns Lorillard’s Strategic Priorities |

• FDA’s PSE is Fundamentally Flawed – Lack of transparency in FDA’s selection and weighting of studies – FDA’s conclusions often based on strained interpretations of data not supported by suitable evidence – FDA inappropriately uses “association” instead of causation – FDA appears to ignore the most critical peer review comments – FDA relies upon unpublished and non-peer reviewed studies Scientific evidence does not support a finding that a product standard related to menthol would be “appropriate for public health” Lorillard’s Position on Menthol is Based on Science 29 |

Lorillard Agrees with Comments from the CTP Director “As a regulatory agency, we can only go as far as the regulatory science will take us.” “The bottom line is we need more information.” Mitch Zeller, Director, FDA Center for Tobacco Products - New York Times, July 23, 2013 30 |

• 60-Day comment period runs through September 23, 2013 • Lorillard will submit its review of the menthol science • There is no deadline or timeline for FDA to determine what regulatory actions, if any, are appropriate • FDA-NIH funded PATH Studies may provide additional information on menthol over the next several years • We continue to believe that FDA’s evaluation of menthol in cigarettes will be a very long process • Lorillard is fully prepared to respond to any FDA action on menthol FDA’s Menthol Evaluation Going Forward Lorillard Intends to Hold Regulators to a Science-Based Decision 31 |

32 1. Profitably maintain a stable Newport Full-Flavor franchise in the core through a disciplined and focused approach 2. Offset cigarette industry declines through close-in adjacency expansion – Geographic expansion of Newport promotions west of the Mississippi River – Product expansion into Non-Menthol (Red & Gold) 3. Establish Lorillard as “first and best” with blu eCigs in electronic cigarettes 4. Defend Lorillard’s freedom to operate – hold regulators to science-based decisions 5. Continue to reward shareholders with superior returns Lorillard’s Strategic Priorities |

Industry Leading Fundamentals Lean Cost Structure Focus on Returning Cash to Shareholders Consistent Delivery of a Double Digit Total Shareholder Return* Over the Long-Term Lorillard Formula for Success is Unchanged * Double-digit shareholder return as measured by EPS growth and the dividend yield. 33 |

2010 2011 2012 2013- 1H Leverage 1.0 X 1.3X 1.6 X 1.8 X Long-Term Debt $1.77 B $2.60 B $3.11 B $3.57 B Shares Repurchased (millions) 27.0 46.7 14.8 7.7 Dividend Payout 63% 66% 73% nm Weighted Average Interest Rate on Debt 6.2% 5.7% 5.2% 5.0% * See Appendix A for further discussion of leverage. Continually Improving Capital Structure 34 |

Consistently Rewarding Shareholders with Superior Returns 35 Source: Bloomberg. From Carolina Group IPO on 1/31/2002 through 8/27/2013. |

36 1. Delivering superior results over the long-term 2. Core cigarette business still has running room 3. e-Cigarettes are a significant growth opportunity 4. Lorillard believes that science does not support disproportionate regulation of menthol cigarettes 5. As always, the Company is focused on rewarding shareholders Summary Summary |

Questions Questions Murray S. Kessler Murray S. Kessler Chairman, President and Chief Executive Officer Chairman, President and Chief Executive Officer David H. Taylor David H. Taylor Executive Vice President and Chief Financial Officer 37 |

38 Appendix A Appendix A Regulation G Reconciliations Regulation G Reconciliations Year ended December 31, 2011 Operating Income Diluted EPS E-Cigarette Segment Operating Income Reported (GAAP) results $1,892 $2.66 N/A GAAP results include the following: 1) Impact of RAI mark-to-market adjustments on Lorillard’s tobacco settlement expense included in cost of sales (25) (0.03) N/A Adjusted (Non-GAAP) results $1,867 $2.63 N/A Year ended December 31, 2012 Operating Income Diluted EPS E-Cigarette Segment Operating Income Reported (GAAP) results $1,878 $2.81 $1 GAAP results include the following: 1) Impact of RAI mark-to-market pension accounting adjustments on Lorillard’s tobacco settlement expense included in cost of sales (8) (0.01) - 2) Impact of RJRT adjustments to its 2001-2005 operating income and restructuring charges on Lorillard’s tobacco settlement expense included in cost of sales 7 0.01 3) Expenses incurred in conjunction with the acquisition of blu eCigs 6 0.01 1 Adjusted (Non-GAAP) results $1,883 $2.82 $2 Reconciliation of Reported (GAAP) to Adjusted (Non-GAAP) Results (Amounts in millions, except per share data) (Unaudited) |

39 Appendix A (cont.) Appendix A (cont.) Regulation G Reconciliations Regulation G Reconciliations Reconciliation of Reported (GAAP) to Adjusted (Non-GAAP) Results (Amounts in millions, except per share data) (Unaudited) Six Months Ended June 30, 2013 Operating Income Diluted EPS E-Cigarette Segment Operating Income Reported (GAAP) results $1.101 $1.69 $9 GAAP results include the following: 1) Favorable impact of the reduction in Lorillard's MSA payment s as a result of the settlement to resolve certain MSA payment disputes approved by the arbitration panel in March 2013 included as an offset to tobacco settlement expense in cost of sales (154) (0.25) - 1) Estimated costs to comply with or otherwise resolve the U.S. Government Case judgment included in selling, general and administrative expenses 20 0.03 - Adjusted (Non-GAAP) results $967 $1.47 $9 |

40 Appendix A (cont.) Appendix A (cont.) Regulation G Reconciliations Regulation G Reconciliations Leverage Ratios Leverage Ratios 2010 2011 2012 2013 - Q1 2013 - Q2 Adjusted operating income $1,725 $1,867 $1,883 $1,883 (1) $1,883 (1) Depreciation and amortization 35 37 39 39 39 Earnings before interest, taxes, depreciation and amortization (B) $1,760 $1,904 $1,922 $1,922 $1,922 Long-term debt $1,769 $2,595 $3,111 $3,101 $3,571 Fair value of interest rate swap (69) (95) (111) (101) (71) Long-term debt, net of fair value of interest rate swap (A) $1,700 $2,500 $3,000 $3,000 $3,500 Leverage (A/B) 1.0 1.3 1.6 1.6 1.8 (1) Estimated based on 2012 Adjusted operating income. |

41 |