Table of Contents

As filed with the Securities and Exchange Commission on May 6, 2008

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

BIOMET, INC.

(Exact name of registrant as specified in its charter)

(see table of additional registrants)

| Indiana | 3842 | 35-1418342 | ||

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

56 East Bell Drive

Warsaw, Indiana 46582

(574) 267-6639

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Bradley J. Tandy

Senior Vice President, General Counsel and Secretary

Biomet, Inc.

56 East Bell Drive

Warsaw, Indiana 46582

(574) 267-6639

(Name, address, including zip code Telephone Number, Including Area Code, of Agent For Service)

Copy to:

| Craig B. Brod, Esq. | Robert M. Hayward, Esq. | |

| Sang Jin Han, Esq. | Theodore A. Peto, Esq. | |

| Cleary Gottlieb Steen & Hamilton LLP | Kirkland & Ellis LLP | |

| One Liberty Plaza | 200 E. Randolph Drive | |

| New York, New York 10006 | Chicago, Illinois 60601 | |

| (212) 225-2000 | (312) 861-2000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the Registration Statement becomes effective.

If any of the securities being registered on this Form are being offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ¨ Accelerated filer ¨ Non-accelerated filer x

CALCULATION OF REGISTRATION FEE

Title of each class of securities to be registered | Amount to be registered | Proposed maximum offering price per unit | Proposed maximum offering price (1) | Amount of registration fee | ||||

10% Senior Notes due 2017 | (1) | (1) | (1) | (1) | ||||

Guarantees of 10% Senior Notes due 2017(2) | (1)(3) | (1)(3) | (1)(3) | (1)(3) | ||||

10 3/8%/11 1/8% Senior Toggle Notes due 2017 | (1) | (1) | (1) | (1) | ||||

Guarantees of 10 3/8%/11 1/8% Senior Toggle Notes due 2017(2) | (1)(3) | (1)(3) | (1)(3) | (1)(3) | ||||

11 5/8% Senior Subordinated Notes due 2017 | (1) | (1) | (1) | (1) | ||||

Guarantees of 11 5/8% Senior Subordinated Notes due 2017(2) | (1)(3) | (1)(3) | (1)(3) | (1)(3) | ||||

| (1) | An indeterminate amount of securities are being registered hereby to be offered solely for market-making purposes by specified affiliates of the registrants. Pursuant to Rule 457(q) under the Securities Act of 1933, no filing fee is required. |

(2) | Each of Biomet, Inc.’s wholly-owned domestic subsidiaries jointly, severally and unconditionally guarantees the 10% Senior Notes due 2017 and the 10 3/8%/11 1/8% Senior Toggle Notes due 2017 on a senior unsecured basis, and the 11 5/8% Senior Subordinated Notes due 2017 on a senior unsecured basis. See inside facing page for table of additional registrant guarantors. |

| (3) | Pursuant to Rule 457(n) under the Securities Act, no separate fee is payable for the registration of the Guarantees. |

The registrants hereby amend this registration statement on such date or dates as may be necessary to delay its effective date until the registrants shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

TABLE OF ADDITIONAL REGISTRANT GUARANTORS

Exact Name of Registrant as Specified in its Charter | State or Other Jurisdiction of Incorporation or Organization | Primary Standard Industrial Classification Code Number | I.R.S. Employer Identification Number | Address, including Zip Code and Telephone Number, including Area Code, of Agent for Service, of Registrant’s Principal Executive Offices | ||||

Biolectron, Inc. | Delaware | 3842 | 13-2914413 | 3200 Las Vegas Blvd. Las Vegas, NV 89109 (574) 267-6639 | ||||

Biomet 3i, LLC | Florida | 3842 | 59-2816882 | 4555 Riverside Drive Palm Beach Gardens, FL 33410 (574) 267-6639 | ||||

Biomet Biologics, LLC | Indiana | 3842 | 03-04079652 | 56 E. Bell Drive Warsaw, IN 46582 (574) 267-6639 | ||||

Biomet Europe Ltd. | Delaware | 3842 | 35-1603620 | Toermalijnring 600 3316 LC Dordrecht The Netherlands (574) 267-6639 | ||||

Biomet Fair Lawn LLC | Indiana | 3842 | 31-1651311 | 20-01 Pollitt Drive Fairlawn, NJ 07410 (574) 267-6639 | ||||

Biomet Holdings Ltd. | Delaware | 3842 | 35-2022857 | 56 E. Bell Drive Warsaw, IN 46582 (574) 267-6639 | ||||

Biomet International Ltd. | Delaware | 3842 | 35-2046422 | 56 E. Bell Drive Warsaw, IN 46582 (574) 267-6639 | ||||

Biomet Leasing, Inc. | Indiana | 3842 | 35-2076217 | 56 E. Bell Drive Warsaw, IN 46582 (574) 267-6639 | ||||

Biomet Manufacturing Corporation |

Indiana |

3842 |

35-2074039 |

56 E. Bell Drive | ||||

Biomet Microfixation, LLC | Florida | 3842 | 59-1692523 | 1520 Tradeport Drive Jacksonville, FL 32218-2482 (574) 267-6639 | ||||

Biomet Orthopedics, LLC | Indiana | 3842 | 35-2074037 | 56 E. Bell Drive Warsaw, IN 46582 (574) 267-6639 | ||||

Biomet Sports Medicine, LLC | Indiana | 3842 | 35-1803072 | 56 E. Bell Drive Warsaw, IN 46852 (574) 267-6639 | ||||

Biomet Travel, Inc. | Indiana | 3842 | 56-2284-205 | 56 E. Bell Drive Warsaw, IN 46852 (574) 267-6639 | ||||

Table of Contents

Exact Name of Registrant as Specified in its Charter | State or Other Jurisdiction of Incorporation or Organization | Primary Standard Industrial Classification Code Number | I.R.S. Employer Identification Number | Address, including Zip Code and Telephone Number, including Area Code, of Agent for Service, of Registrant’s Principal Executive Offices | ||||

Blue Moon Diagnostics, Inc. | Indiana | 3842 | 35-2070282 | 56 E. Bell Drive Warsaw, IN 46852 (574) 267-6639 | ||||

Cross Medical Products, LLC | Delaware | 3842 | 31-0992628 | 181 Technology Drive Irvine, CA 92618 (574) 267-6639 | ||||

EBI Holdings, LLC | Delaware | 3842 | 22-2407246 | 100 Interpace Parkway Parsippany, NJ 07054 (574) 267-6639 | ||||

EBI, LLC | Indiana | 3842 | 31-1651314 | 100 Interpace Parkway Parsippany, NJ 07054 (574) 267-6639 | ||||

EBI Medical Systems, LLC | Delaware | 3842 | 22-2406619 | 100 Interpace Parkway Parsippany, NJ 07054 (574) 267-6639 | ||||

Electro-Biology, LLC | Delaware | 3842 | 22-2278360 | 6 Upper Pond Road Parsippany, NJ 07054-01079 (574) 267-6639 | ||||

Biomet Florida Services, LLC | Florida | 3842 | 20-0388276 | 4555 Riverside Drive Palm Beach Gardens, FL 33410 (574) 267-6639 | ||||

Implant Innovations Holdings, LLC |

Indiana |

3842 |

35-2088040 |

56 E. Bell Drive | ||||

Interpore Cross International, LLC | California | 3842 | 33-0818017 | 181 Technology Drive, Irvine, CA 92618 (574) 267-6639 | ||||

Interpore Spine Ltd. | Delaware | 3842 | 95-3043318 | 181 Technology Drive, Irvine, CA 92618 (574) 267-6639 | ||||

Kirschner Medical Corporation | Delaware | 3842 | 52-1319702 | 100 Interpace Parkway Parsippany, NJ 07054 (574) 267-6639 | ||||

Meridew Medical, Inc. | Indiana | 3842 | 35-2151951 | 56 E. Bell Drive Warsaw, IN 46580 (574) 267-6639 | ||||

Thoramet, Inc. | Indiana | 3842 | 35-2070281 | 56 E. Bell Drive Warsaw, IN 46580 (574) 267-6639 | ||||

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED MAY 6, 2008

PRELIMINARY PROSPECTUS

$775,000,000 10% Senior Notes due 2017

$775,000,000 10 3/8%/11 1/8% Senior Toggle Notes due 2017

$1,015,000,000 11 5/8% Senior Subordinated Notes due 2017

NOTES OFFERED

| • | $775 million of our 10% Senior Notes due 2017, which we refer to as the senior cash pay notes. |

• | $775 million of our 10 3/8%/11 1/8% Senior Toggle Notes due 2017, which we refer to as the senior toggle notes. |

• | $1,015 million of our 11 5/8% Senior Subordinated Notes due 2017, which we refer to as the senior subordinated notes. We refer to the senior cash pay notes and the senior toggle notes collectively as the senior notes. We refer to the senior notes and the senior subordinated notes collectively as the notes. |

MATURITY

| • | The notes will mature on October 15, 2017. |

INTEREST

| • | Senior cash pay notes: Interest is payable in cash and accrues at the rate of 10% per annum. |

• | Senior toggle notes: Interest accrues at the rate of 10 3/8% per annum and PIK interest (as defined below) accrues at the rate of 11 1/8% per annum. For any interest period (other than the first initial interest period) through October 15, 2012, we may elect to pay interest on the senior toggle notes (1) entirely in cash, (2) entirely by increasing the principal amount of the toggle notes or issuing new toggle notes, or PIK interest, or (3) 50% in cash and 50% in PIK interest. After October 15, 2012, all interest on the senior toggle notes will be payable in cash. |

• | Senior subordinated notes: Interest is payable in cash and accrues at the rate of 11 5/8% per annum. |

INTEREST PAYMENT DATES

| • | April 15 and October 15, commencing April 15, 2008. |

REDEMPTION

| • | We may redeem some or all of the notes on or after October 15, 2012 at redemption prices described in this prospectus. |

| • | We may also redeem up to 35% of the notes using the proceeds of certain equity offerings completed before October 15, 2010. |

CHANGE OF CONTROL

| • | If we experience a change of control, we must offer to purchase the notes. |

GUARANTEES

| • | Each of our existing and future wholly-owned domestic restricted subsidiaries, which guarantees our senior secured cash flow facilities, will jointly, severally and unconditionally guarantee the senior notes on a senior basis and the senior subordinated notes on a senior subordinated unsecured basis. |

RANKING

| • | The senior notes and the related guarantees are our and the guarantor’s general unsecured indebtedness, rank equally in right of payment to all of our and the guarantors’ existing and future senior unsecured indebtedness and other obligations and rank senior in right of payment to all of our and the guarantors’ existing and future subordinated indebtedness and other obligations. |

| • | The senior subordinated and the related guarantees are our and the guarantor’s general unsecured senior subordinated indebtedness, ranking junior in right of payment to any of our and the guarantors’ existing and future senior indebtedness and other obligations, rank equally in right of payment to all of our and our guarantors’ existing and future senior subordinated indebtedness and other obligations and rank senior in right of payment to any of our and the guarantors’ existing and future subordinated indebtedness and other obligations. |

See “Risk Factors” beginning on page 15 for a discussion of certain risks that you should consider before investing in the notes.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

This prospectus has been prepared for and may be used by Goldman, Sachs & Co. and any affiliates of Goldman, Sachs & Co. in connection with offers and sales of the notes related to market-making transactions in the notes effected from time to time. Goldman, Sachs & Co. or its affiliates may act as principal or agent in such transactions, including as agent for the counterparty when acting as principal or as agent for both counterparties, and may receive compensation in the form of discounts and commissions, including from both counterparties, when it acts as agents for both. Such sales will be made at prevailing market prices at the time of sale, at prices related thereto or at negotiated prices. We will not receive any proceeds from such sales.

The date of this prospectus is , 2008.

Table of Contents

You should rely only on the information contained or incorporated by reference in this prospectus. We have not authorized any person to provide you with any information or represent anything about us or this offering that is not contained in this prospectus. If given or made, any such other information or representation should not be relied upon as having been authorized by us. This prospectus does not offer to sell nor ask for offers to buy any of the securities in any jurisdiction where it is unlawful, where the person making the offer is not qualified to do so, or to any person who cannot legally be offered the securities. You should not assume that the information contained or incorporated by reference in this prospectus is accurate as of any date other than the date on the front cover of this prospectus or the date of any document incorporated by reference herein.

| Page | ||

| ii | ||

| ii | ||

| iv | ||

| iv | ||

| iv | ||

| v | ||

| 1 | ||

| 15 | ||

| 35 | ||

| 36 | ||

| 37 | ||

| 38 | ||

| 44 | ||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 47 | |

| 68 | ||

| 69 | ||

| 92 | ||

| 95 | ||

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT | 132 | |

| 135 | ||

| 137 | ||

| 142 | ||

| 204 | ||

| 268 | ||

CERTAIN MATERIAL UNITED STATES FEDERAL INCOME TAX CONSIDERATIONS | 270 | |

| 274 | ||

| 275 | ||

| 275 | ||

CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE | 275 | |

| F-1 |

i

Table of Contents

WHERE YOU CAN FIND MORE INFORMATION

We and the guarantors have filed with the Securities and Exchange Commission, or the SEC, a registration statement on Form S-1 under the Securities Act of 1933, as amended, or the Securities Act, with respect to the notes. This prospectus, which forms a part of the registration statement, does not contain all of the information set forth in the registration statement. For further information with respect to us, the guarantors or the notes, we refer you to the registration statement. Statements contained in this prospectus as to the contents of any contract or other document are not necessarily complete. We are not currently subject to the informational requirements of the Securities Exchange Act of 1934, as amended, or the Exchange Act. As a result of the offering of the notes, we will become subject to the informational requirements of the Exchange Act, and, in accordance therewith, will file reports and other information with the SEC. The registration statement, such reports and other information can be inspected and copied at the Public Reference Room of the SEC located at Room 1580, 100 F Street, N.E., Washington D.C. 20549. Copies of such materials, including copies of all or any portion of the registration statement, can be obtained from the Public Reference Room of the SEC at prescribed rates. You can call the SEC at 1-800-SEC-0330 to obtain information on the operation of the Public Reference Room. Such materials may also be accessed electronically by means of the SEC’s home page on the Internet (http://www.sec.gov).

Under the terms of the indentures relating to the notes, we have agreed that, whether or nor we are required to do so by the rules and regulations of the SEC, for so long as any of the notes remain outstanding, we will furnish to the trustee and holders of the notes the information specified therein. See “Description of Senior Notes” and “Description of Senior Subordinated Notes.”

This prospectus contains forward-looking statements within the meaning of the U.S. federal securities laws. Statements that are not historical facts, including statements about our beliefs and expectations, are forward-looking statements. Forward-looking statements include statements generally preceded by, followed by or that include the words “believe,” “could,” “expect,” “intend,” “may,” “anticipate,” “plan,” “predict,” “potential,” “estimate” or similar expressions. These statements include, but are not limited to, statements related to:

| • | the timing and number of planned new product introductions; |

| • | the effect of anticipated changes in the size, health and activities of the population or on the demand for our products; |

| • | assumptions and estimates regarding the size and growth of certain market categories; |

| • | our ability and intent to expand in key international markets; |

| • | the timing and anticipated outcome of clinical studies; |

| • | assumptions concerning anticipated product developments and emerging technologies; |

| • | the future availability of raw materials; |

| • | the anticipated adequacy of our capital resources to meet the needs of our business; |

| • | our continued investment in new products and technologies; |

| • | the ultimate marketability of products currently being developed; |

| • | the ability to successfully implement new technologies and transition certain manufacturing operations to China; |

| • | our ability to manage working capital and generate adequate cash flows to service outstanding debt; |

ii

Table of Contents

| • | our ability to sustain sales and earnings growth; |

| • | our goals for sales and earnings growth; |

| • | our success in achieving timely approval or clearance of our products with domestic and foreign regulatory entities; |

| • | our success in implementing our value creation and operational improvement programs; |

| • | the stability of certain foreign economic markets; |

| • | the impact of anticipated changes in the musculoskeletal industry and our ability to react to and capitalize on those changes; |

| • | our ability to successfully implement desired organizational changes; |

| • | the impact of our managerial changes; and |

| • | our ability to take advantage of technological advancements. |

Forward-looking statements reflect our current expectations and are not guarantees of performance. These statements are based on our management’s beliefs and assumptions, which in turn are based on currently available information. Important assumptions relating to these forward-looking statements include, among others, assumptions regarding demand for our products, expected pricing levels, raw material costs, the timing and cost of planned capital expenditures, expected outcomes of pending litigation, the solvency of our insurers and the ultimate resolution of allocation and coverage issues with those insurers, competitive conditions and general economic conditions. Readers of this prospectus are cautioned that reliance on any forward-looking statement involves risks and uncertainties. Although we believe that the assumptions on which the forward-looking statements contained herein are based are reasonable, any of those assumptions could prove to be inaccurate given the inherent uncertainties as to the occurrence or nonoccurrence of future events. There can be no assurance that the forward-looking statements contained in this prospectus will prove to be accurate. The inclusion of a forward-looking statement in this prospectus should not be regarded as a representation by us that our objectives will be achieved. Forward-looking statements also involve risks and uncertainties, which could cause actual results to differ materially from those contained in any forward-looking statement. Many of these factors are beyond our ability to control or predict and could, among other things, cause actual results to differ from those contained in forward-looking statements made in this prospectus and presented elsewhere by management from time to time. Such factors, among others, may have a material adverse effect upon our business, financial condition and results of operations and may include, but are not limited to, factors discussed under the heading “Risk Factors” and the following:

| • | changes in general economic conditions and interest rates; |

| • | changes in the availability of capital and financing sources; |

| • | changes in competitive conditions and prices in our markets; |

| • | changes in the relationship between supply of and demand for our products; |

| • | fluctuations in costs of raw materials and labor; |

| • | changes in other significant operating expenses; |

| • | decreases in sales of our principal product lines; |

| • | slow downs or inefficiencies in our product research and development efforts; |

| • | increases in expenditures related to increased government regulation of our business; |

| • | developments adversely affecting our sales activities outside the United States; |

| • | decreases in reimbursement levels by our customers; |

iii

Table of Contents

| • | difficulties in transitioning certain manufacturing operations to China; |

| • | challenges in effectively implementing restructuring and cost saving initiatives; |

| • | increases in cost-containment efforts by group purchasing organizations; |

| • | loss of our key management and other personnel or inability to attract such management and other personnel; |

| • | increases in costs of retaining existing independent sales agents of our products; |

| • | unanticipated expenditures related to litigation, including litigation related to the Merger, the past stock option grant practices and investigations by the U.S. Department of Justice and the SEC; and |

| • | failure to comply with the terms of the Deferred Prosecution Agreement and Corporate Integrity Agreement. |

We caution you not to place undue reliance on these forward-looking statements that speak only as of the date they were made. We do not undertake any obligation to publicly release any revisions to these forward-looking statements to reflect events or circumstances after the date of this prospectus or to reflect the occurrence of unanticipated events.

In this prospectus, we rely on and refer to information and statistics regarding our industry products and our market share based on revenues in the sectors in which we compete. Where possible, we obtained this information and statistics from third-party sources, such as independent industry publications, government publications or reports by market research firms, including, without limitation, Eurostat, Knowledge Enterprises, Inc., the U.S. Census Bureau, Wall Street research and from company research and trade interviews. In addition, we have supplemented third-party information where necessary with management estimates based on our review of internal surveys, information from our customers and vendors, trade and business organizations and other contacts in markets in which we operate, and our management’s knowledge and experience. However, these estimates are subject to change and are uncertain due to limits on the availability and reliability of primary sources of information and the voluntary nature of the data gathering process. Although we believe that these independent sources and our management’s estimates are reliable as of the date of this prospectus, the information contained in them has not been independently verified, and neither we nor Goldman, Sachs & Co. can assure you as to the accuracy or completeness of such information. As a result, you should be aware that market share and industry data included in this prospectus, and estimates and beliefs based on that data, may not be reliable. Neither we nor Goldman, Sachs & Co. make any representation as to the accuracy or completeness of such information.

Numerical figures included in this prospectus have been subject to rounding adjustments.

For purposes of presenting in U.S. dollars the amounts outstanding and the amounts available for borrowing under our senior secured credit facilities, euro-denominated European line of credit and yen-denominated Japanese lines of credit as well as the fair value of the interest rate swap agreements relating to our euro-denominated senior secured term loan facility, in each case as of February 29, 2008, we have used the noon buying rate in New York City for cable transfers in foreign currencies as certified for customs purposes by the

iv

Table of Contents

Federal Reserve Bank of New York for the euro of €1.00 to $1.5187 and yen of ¥1.00 to $0.009448. These rates are presented for informational purposes and are not the same as the rates that are used for purposes of translating euros or yen into U.S. dollars in our financial statements.

Unless otherwise noted or indicated by the context, in this prospectus:

| • | For periods prior to the Merger, the terms “Biomet,” “Company,” “we,” “us” and “our” refer to Biomet, Inc. as the target corporation and its consolidated subsidiaries, and for periods after the Merger, those terms refer to Biomet, Inc. as the surviving corporation and its consolidated subsidiaries, unless we expressly state otherwise or the context otherwise requires. |

| • | The term “Merger” refers to the merger of LVB Acquisition Merger Sub, Inc., an Indiana corporation and wholly-owned subsidiary of LVB Acquisition, Inc., and the initial issuer of the notes, with and into Biomet, with Biomet continuing as the surviving corporation after the merger. |

| • | The term “Transactions” refers to the transactions described in the section titled “The Transactions” included elsewhere in this prospectus. |

| • | The term “Sponsors” refers to the investment funds affiliated with The Blackstone Group, Goldman Sachs Capital Partners, Kohlberg Kravis Roberts & Co., or KKR, and TPG Capital, or TPG, that have committed to provide the equity investment to pay a portion of the cash consideration to be paid as part of the Merger. |

| • | The term “closing date” refers to September 25, 2007, the date of closing of the Merger. |

| • | The term “pro forma” refers to our financial information, as adjusted to give effect to the Transactions on the basis described, and subject to the qualifications expressed, under the heading “Unaudited Pro Forma Condensed Consolidated Financial Data.” |

| • | The term “domestic” refers to the United States and the term “international” refers to all countries other than the United States. |

| • | References to our fiscal years through and including fiscal 2007 are to the twelve months ended on May 31 of such year. |

v

Table of Contents

This summary contains basic information about us and this offering. Because it is a summary, it does not contain all of the information that is important to you. You should read this entire prospectus carefully, including the section entitled “Risk Factors” and our consolidated financial statements and the notes thereto included elsewhere in this prospectus, before participating in this offering.

Our Company

General

We are one of the largest orthopedic medical device companies in the United States and worldwide with operations in over 50 locations throughout the world and distribution in more than 70 countries. We design, manufacture and market a comprehensive range of both surgical and non-surgical products used primarily by orthopedic surgeons and other musculoskeletal medical specialists. For over 30 years, we have applied the most advanced engineering and manufacturing technology to the development of highly durable joint replacement systems and minimally invasive surgical procedures. For fiscal 2007 and the nine months ended February 29, 2008, we generated net sales of $2,107 million and pro forma net sales of $1,748 million, respectively.

Products

We operate in one business segment, musculoskeletal products, which includes the design, manufacture and marketing of products in four major market categories: Reconstructive Products, Fixation Devices, Spinal Products and Other Products. We have three reportable geographic markets: United States, Europe and International.

Reconstructive Products. We are a worldwide leader in our principal market category, Reconstructive Products. Primary product offerings include implants and instrumentation for replacing knees and hips as well as extremity joints that have deteriorated due to disease (principally osteoarthritis) or injury. We have been among the fastest growing knee companies in the industry as a result of continued strong demand for our total and partial knee systems. We also believe that our innovative hip product offerings, including our broad platform of bearing options, represent competitive advantages and have led to excellent surgeon acceptance. This market category also includes our dental reconstructive device business, which includes implants and abutments, augmented by a growing line of our other reconstructive products such as regenerative products, accessories and biologics products. The Reconstructive Products category accounted for 71% of our net sales for fiscal 2007 and 73% of our pro forma net sales for the nine months ended February 29, 2008.

Fixation Devices. Fixation devices are used for setting and stabilizing damaged bones to support and/or augment the body’s natural healing process. We are a market leader for electrical stimulation devices for trauma indications, offering implantable and non-invasive products to stimulate bone growth. Other products include internal fixation devices (such as nails, plates, screws, pins and wires used to stabilize traumatic bone injuries), external fixation devices (used to stabilize fractures when alternative methods of fixation are not suitable), craniomaxillofacial fixation systems and bone substitute materials. The Fixation Devices category accounted for 11% of our net sales for fiscal 2007 and 10% of our pro forma net sales for the nine months ended February 29, 2008.

Spinal Products. Spinal products include devices and instrumentation for repairing defects or wear and tear in the vertebral column. Key products in this category include implantable and non-invasive electrical stimulation devices for spinal indications (used to enhance bone fusion success), spinal fixation systems used to

1

Table of Contents

stabilize the spine, bone substitute materials and allograft services used in spinal fusion procedures, as well as motion preservation systems. The Spinal Products category accounted for 10% of our net sales for fiscal 2007 and 9% of our pro forma net sales for the nine months ended February 29, 2008.

Other Products. We manufacture and distribute a number of other products, including sports medicine products (used in minimally-invasive orthopedic surgical procedures), orthopedic support products (also referred to as softgoods and bracing products), operating room supplies, casting materials, general surgical instruments, wound care products and other surgical products. The Other Products category accounted for 8% of our net sales for both fiscal 2007 and our pro forma net sales for the nine months ended February 29, 2008.

The following charts set forth our net sales by market category and geographic markets for fiscal 2007.

Industry

We participate in the worldwide orthopedic and dental implant markets, which management estimates to be $30 billion in market size. These markets enjoy favorable industry dynamics and Wall Street analysts estimate that these markets will grow at a compounded annual growth rate above 10% over the next five years. The orthopedic industry benefits from several favorable factors, including, but not limited to:

Favorable Demographics. An aging population is driving growth in the orthopedic products market. Many conditions that require orthopedic surgery affect people in middle age or later in life. As the baby boomer population ages and life expectancy increases, the elderly will represent a higher percentage of the overall population. According to a 2007 U.S. Census Bureau projection, the U.S. population aged 55 to 74 is expected to grow at approximately three times the average rate of population growth from 51 million and 18% of the population in 2007 to 76 million and 22% of the population by 2027. According to a 2006 Eurostat projection, the European population aged 65 and over will grow at approximately 16 times the average rate of population growth from 77 million and 17% of the population in 2005 to 135 million and 30% of the population in 2025.

Stable Industry Structure. Following a period of consolidation during the late 1990s, over the past nine years, we, together with Zimmer Holdings, Inc., DePuy, Inc. (a Johnson & Johnson company), Stryker Corporation and Smith & Nephew plc, have constituted over 85% of the orthopedic reconstructive industry’s worldwide revenues. These players have achieved critical components to success, including product innovations and advancements, accumulation of clinical data, regulatory expertise, economies of scale, and sales force and surgeon customer relationships, which have led to minimal market share movement among top players from year to year.

Close Working Relationships with Surgeon Customers. Due to the nature of orthopedic implants, the orthopedic medical device industry is unique with respect to the working relationships between orthopedic device manufacturers and their surgeon customers. As a component of innovation in the industry, some surgeons serve

2

Table of Contents

as consultants and are instrumental in the development of new products and the ongoing evaluation and improvement of existing products.

Technological Advancement of Orthopedic Products. Incremental and continuous technological advancement of orthopedic products is expanding the addressable market. Product innovation is improving the durability and performance of orthopedic devices and promoting less invasive surgery. Examples include bearing surfaces in hips with potential for greater longevity, premium knee systems that allow greater range of motion, and press fit hip stems that facilitate minimally invasive hip procedures. As a result of this ongoing innovation, we believe that surgeons are increasingly recommending and utilizing implant products for younger patients as well as elderly patients who are remaining healthier and more active than those of past generations.

Favorable Product Mix Shift. Continued product innovation is driving a favorable shift in mix towards premium products that offer enhanced outcomes for patients. Product evolution is also expanding the addressable market to include younger patients who are more likely to require and demand premium and high-performance products. In addition, the payor mix resulting from the broadening of the patient population to younger patients with private insurance creates a favorable environment due to the fact that joint procedures for non-Medicare payors are generally more profitable for hospitals.

Competitive Strengths

We believe we have a number of competitive strengths that will enable us to further enhance our position in the orthopedic medical device market.

Broad Market Leadership. We are the fourth largest player in the U.S. orthopedic reconstructive market and have maintained this position for over a decade. We have high representation at U.S. hospitals, supplying products to over 60% of hospitals performing joint replacement surgery. In addition, we are the third largest manufacturer and marketer of dental reconstructive products worldwide and maintain leadership positions in the electrical stimulation and craniomaxillofacial fields.

Leading Research and Development Platform.We have a long history of innovation, engineering, quality and successful new product launches. Demonstrating our research and development leadership, we have launched approximately 800 new products in the past nine fiscal years and plan to introduce approximately 100 new products during fiscal 2009.

Strong Relationships with Surgeon Customers. Based on their understanding of and satisfaction with our products, we enjoy long-standing relationships with our surgeon customers, many of which commence during the surgeon’s residency training program. Our support of medical education programs provides important training opportunities for orthopedic surgeons early in their career. In fact, supporting “hands-on” training provides opportunities for residents, fellows and attending surgeons to experience the clinical benefits of our products. Surgeons have historically exhibited limited willingness to switch manufacturers, as successful patient outcomes are related to the practitioners’ familiarity with the procedural characteristics and instrumentation of certain implants. As such, 19 of our top 25 surgeons have been our customers for at least 10 years.

Consistently Strong Operating Cash Flow Generation.Our business is characterized by consistently strong operating cash flows due to our robust operating history and moderate capital intensity. We have continually increased both revenues and profitability, with fiscal 2007 representing our 29th consecutive year of year-over-year net sales growth. Over the last 15 years, from fiscal 1992 to fiscal 2007, we increased net sales at compounded annual growth rate of approximately 15%. We have sustained growth through multiple macro- economic cycles, demonstrating a stable business profile. In addition, we have historically had modest capital expenditure and working capital requirements providing for strong operating cash flow conversion.

3

Table of Contents

Experienced and Dedicated Management Team.We have a highly experienced management team at both the corporate and operational level. Our team is led by Jeffrey R. Binder, a 15-year veteran of the orthopedic medical device industry, who was appointed President and Chief Executive Officer in February 2007. Daniel P. Florin was appointed Senior Vice President and Chief Financial Officer in June 2007 and brings 16 years of financial officer/controller experience in the medical device industry and five years of public accounting and auditing experience to Biomet. Glen A. Kashuba was appointed Senior Vice President and President of Biomet Trauma and Biomet Spine, or BTBS, in April 2007, having previously served as Worldwide President of Cordis Endovascular, a division of Johnson & Johnson. Gregory W. Sasso, who has been with us for 23 years, was appointed Senior Vice President and President of Biomet SBU Operations in June 2007. In February 2008, Jon C. Serbousek was appointed President of Biomet Orthopedics, having spent 21 years in the medical device industry including 8 years with Medtronic and 13 years with DePuy. Even though each of Messrs. Binder, Florin, Kashuba and Serbousek has been with us for less than two years, the members of our senior management team have an average tenure of 13 years with us. Overall, the members of our senior management team have an average tenure of 18 years in the medical device industry. Certain members of our management team made a contribution of new equity through cash equity contributions and/or rollover of existing equity interests in the Transactions.

Premier Equity Sponsorship.The Blackstone Group, Goldman Sachs Capital Partners, KKR and TPG are among the most well-known and respected financial sponsors in the world. The Sponsors have made investments in over 950 companies and collectively have more than $125 billion of assets under management. The Sponsors and the Co-Investors (as defined below) contributed approximately $5,387 million of equity in connection with the Transactions, representing 46% of the total funding for the Transactions, as part of one of the largest private equity investments in history. The Sponsors have considerable experience in the healthcare sector with investments in companies such as Accellent Inc., HCA Inc., IASIS Healthcare Corporation, Quintiles Transnational Corp., ReAble Therapeutics, Inc. and Vanguard Health Systems, Inc., among others.

Business Strategy

We intend to enhance our position as a leading orthopedic medical device company by pursuing the following strategic initiatives:

Continue to Develop and Launch New Products and Technologies. We plan to continue to aggressively develop new products, technologies and materials by leveraging our established research and development platform. While we have a strong engineering heritage, we recently have taken steps to enhance our research and development efforts, with the appointment of two global heads charged with coordinating research and development efforts across the organization, which should improve time to market and leverage best technologies and innovations available throughout all business segments and regions. We anticipate that our future research and development investment will be consistent with historical results as a percentage of net sales.

Enhance Surgeon Customer Relationships through Product Performance and Innovation. We intend to continue to meet the demanding needs of our surgeon customers and hospital customers by providing clinically superior and innovative products that offer a cost-effective means of treating patients. Our success has been built on responsiveness to the needs of the health care community, the outstanding clinical performance of our products and our ongoing commitment to continued product innovation.

Expand Our Global Reach. We intend to continue to increase the geographic presence of each of our business categories. There are considerable opportunities for global expansion as healthcare spending increases in international markets—the United States and Canada together accounted for approximately 65% of the global orthopedic market in 2006, but only approximately 5% of the world’s population. We particularly plan to focus

4

Table of Contents

on deepening our position in under-penetrated regions with attractive opportunities for growth, including Asia and Latin America, by deploying more resources to capture market opportunities, as well as by leveraging our established worldwide manufacturing facilities and sales force. We believe we can successfully grow our presence in these regions by differentiating ourselves as a provider with a comprehensive portfolio of leading musculoskeletal products.

Focus on Operational Efficiency. We have identified significant opportunities to streamline operations. The historically decentralized nature of our management and decision-making structure creates opportunities to improve operational efficiency as we centralize operations and increase focus, coordination and accountability throughout the organization. Plans include manufacturing footprint optimization, implementation of Six Sigma and Lean Manufacturing, procurement and offshoring initiatives, as well as reduction in overhead expenses. These initiatives will enable us to maximize asset utilization, optimize working capital and increase cash flow, as well as accelerate product development and enhance customer service.

Maximize Operating Cash Flow. We are focused on maximizing our operating cash flow. Over the last 20 years, we have consistently generated significant operating cash flow due to our business growth, strong operating margins and modest capital expenditure and other cash requirements. These solid business fundamentals will be supplemented by recently implemented initiatives to improve working capital, which historically has not been a focus area of management. In addition, we will benefit from identified cost savings as we enhance operational efficiencies. We plan to use available cash after capital expenditures to reduce leverage and strengthen our balance sheet.

Corporate Information

Biomet is incorporated in the state of Indiana. Our principal executive offices are located at 56 East Bell Drive, Warsaw, Indiana 46582. Our website address is www.biomet.com. The information on our website is not deemed to be part of this prospectus. For additional information, contact our Corporate Communications department at (574) 372-1514.

The Transactions

On December 18, 2006, we entered into an Agreement and Plan of Merger with LVB Acquisition, Inc., or Parent, and LVB Acquisition Merger Sub, Inc., or Purchaser, which agreement was amended and restated as of June 7, 2007 (as may be amended and restated, supplemented or otherwise modified from time to time, the “Merger Agreement”). Pursuant to the Merger Agreement, on June 13, 2007, Purchaser commenced a cash tender offer, or the Offer, to purchase all of our outstanding common shares, without par value, or the Shares, at a price of $46.00 per Share, or the Offer Price, without interest and less any required withholding taxes. The Offer was made pursuant to Purchaser’s offer to purchase dated June 13, 2007 and the related letter of transmittal, each of which was filed with the SEC on June 13, 2007. The Offer expired at 12:00 midnight, New York City time, on July 11, 2007, with approximately 82% of the outstanding Shares having been tendered to Purchaser. At our special meeting of shareholders held on September 5, 2007, more than 91% of our shareholders voted to approve the Merger, and Parent acquired us on September 25, 2007 through a reverse subsidiary merger with Purchaser with Biomet, Inc. being the surviving company. Subsequent to the acquisition, we became a subsidiary of our Parent, which is controlled by LVB Acquisition Holding, LLC, or Holding, an entity controlled by the Sponsors and their Co-Investors.

5

Table of Contents

The Merger was completed on September 25, 2007 and was financed through:

| • | the proceeds from the initial offering of the original notes; |

| • | initial borrowings under our senior secured credit facilities and our senior unsecured bridge facilities; |

| • | equity investments funded by direct and indirect equity investments from certain investment funds associated with or designated by the Sponsors, or the Sponsor Funds, certain investors who have agreed to co-invest with the Sponsor Funds, including investment funds affiliated with certain of the initial purchasers of the original notes, or the Co-Investors, and certain of our executive officers and members of our senior management, or the Management Participants, who rolled over existing equity interests and/or made cash equity contributions; and |

| • | our cash on hand. |

On October 16, 2007, the borrowings under our senior unsecured cash pay bridge facility, our senior unsecured PIK-option bridge facility and our senior subordinated unsecured bridge facility were repaid with the proceeds from the follow-on offering of the equal amounts of the additional original senior cash pay notes, original senior toggle notes and original senior subordinated notes, respectively.

We refer to these transactions, including the Merger and our payment of any fees and expenses related to these transactions, collectively as the “Transactions.” See “Description of Other Indebtedness” for a description of our senior secured credit facilities.

In connection with the Transactions, we incurred significant indebtedness and became highly leveraged. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources.” In addition, we allocated the purchase price to the fair value of the assets and liabilities of Biomet based on estimated fair value. The preliminary purchase accounting adjustments increased the carrying value of our property and equipment, inventory and established intangible assets (such as corporate and product names, core and completed technology, customer relationships), among other things. Subsequent to the Transactions, interest expense and non-cash depreciation and amortization charges have significantly increased. As a result, our successor financial statements subsequent to the Transactions are not comparable to our predecessor financial statements.

6

Table of Contents

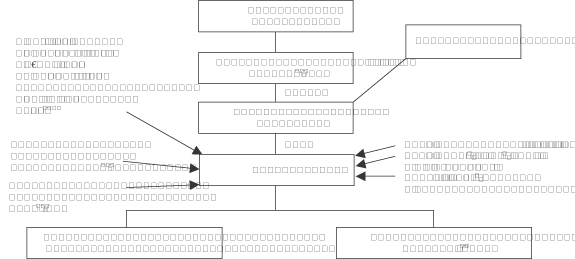

Ownership and Corporate Structure

The following chart illustrates our ownership and corporate structure after giving effect to the Transactions.

| (1) | The guarantors provide unsecured guarantees of the notes as well as guarantees of and pledges of assets under our senior secured cash flow facilities. The guarantors are co-borrowers and provide pledges of assets under our senior secured asset-based revolving credit facility. Holding guarantees and pledges its assets under our senior secured cash flow facilities and our senior secured asset-based revolving credit facility, in each case as described in more detail under “Description of Other Indebtedness.” |

| (2) | On September 25, 2007, we entered into a $2,340 million U.S. dollar-denominated senior secured term loan facility and a €875 million (approximately $1,329 million) euro-denominated senior secured term loan facility, each with a seven and a half-year maturity. We borrowed the full amount available under our senior secured term loan facilities at the closing of the Transactions to pay a portion of the Transactions. In the third quarter of fiscal 2008, we repaid $6 million of outstanding loans under our U.S. dollar-denominated senior secured term loan facility and $3 million of outstanding loans under our euro-denominated senior secured term loan facility. |

| (3) | On September 25, 2007, we entered into a $400 million senior secured cash flow revolving credit facility with a six-year maturity. We borrowed approximately $131 million under our senior secured cash flow revolving credit facility on or about the closing date of the Transactions to pay a portion of the Transactions. As of February 29, 2008, we had $74 million outstanding borrowings under our senior secured cash flow revolving credit facility. |

| (4) | On September 25, 2007, we entered into a $350 million senior secured asset-based revolving credit facility with a six-year maturity. As of February 29, 2008, the borrowing base under our senior secured asset-based revolving credit facility was $350 million. As of February 29, 2008, we did not have any outstanding borrowings under our senior secured asset-based revolving credit facility. |

The Sponsors

The Blackstone Group

The Blackstone Group is a leading global alternative asset manager and provider of financial advisory services. Its alternative asset management businesses include the management of corporate private equity funds, real estate opportunity funds, funds of hedge funds, mezzanine funds, senior debt funds, proprietary hedge funds

7

Table of Contents

and closed-end mutual funds. The Blackstone Group also provides various financial advisory services, including mergers and acquisitions advisory, restructuring and reorganization advisory and fund placement services. Its website address is http://www.blackstone.com.

Goldman Sachs Capital Partners

Founded in 1869, Goldman, Sachs & Co. is one of the oldest and largest investment banking firms. Goldman Sachs is also a global leader in private corporate equity and mezzanine investing. Established in 1991, the Goldman Sachs Capital Partners family of funds is part of the firm’s Principal Investment Area in the Merchant Banking Division. Goldman Sachs’ Principal Investment Area has formed 14 investment vehicles aggregating $72 billion of capital to date. Significant investments include: ARAMARK, Burger King, CVR Energy, Inc., Education Management Corporation, Hawker Beechcraft, HealthMarkets, Kabel Deutschland, Knight Inc. (formerly known as Kinder Morgan), Polo Ralph Lauren, Prysmian Cables & Systems, VoiceStream Wireless, and YES Network. GS Capital Partners VI is the current primary investment vehicle for Goldman Sachs to make large, privately negotiated equity investments.

KKR

Established in 1976, KKR is a leading global alternative asset manager. The core of the Firm’s franchise is sponsoring and managing funds that make private equity investments in North America, Europe, and Asia. Throughout its history, KKR has brought a long-term investment approach to portfolio companies, focusing on working in partnership with management teams and investing for future competitiveness and growth. The Firm’s sponsored funds include KKR Private Equity Investors, L.P. (Euronext Amsterdam: KPE), a permanent capital fund that invests in KKR-identified investments; and two credit strategy funds, KKR Financial (NYSE: KFN) and the KKR Strategic Capital Funds, which make investments in debt transactions. KKR has offices in New York, Menlo Park, San Francisco, London, Paris, Hong Kong, Tokyo, Sydney and Beijing.

TPG Capital

TPG Capital is the global buyout group of TPG, a leading private investment firm founded in 1992, with more than $50 billion of assets under management and offices in San Francisco, London, Hong Kong, New York, Minneapolis, Fort Worth, Melbourne, Menlo Park, Moscow, Mumbai, Beijing, Shanghai, Singapore and Tokyo. TPG Capital has extensive experience with global public and private investments executed through leveraged buyouts, recapitalizations, spinouts, joint ventures and restructurings. TPG Capital’s investments span a variety of industries including healthcare, retail/consumer, travel, media and communications, industrials, technology and financial services. Please visit www.tpg.com.

8

Table of Contents

Summary of the Terms of the Notes

Issuer | Biomet, Inc. |

Notes Offered

Senior Cash Pay Notes | $775 million in aggregate principal amount of 10% Senior Notes due 2017. |

Senior Toggle Notes | $775 million in aggregate principal amount of 10 3/8%/11 1/8% Senior Toggle Notes due 2017. |

Senior Subordinated Notes | $1,015 million in aggregate principal amount of 11 5/8% Senior Subordinated Notes due 2017. |

Maturity Dates | The notes will mature on October 15, 2017. |

Interest Rate | Interest on the senior cash pay notes is payable in cash and accrues at a rate of 10% per annum. |

Cash interest on the senior toggle notes accrues at a rate of 10 3/8% per annum, and PIK interest will accrue at a rate of 11 1/8% per annum. The initial interest payment on the senior toggle notes will be payable in cash. For any interest period thereafter through October 15, 2012, we may elect to pay interest on the senior toggle notes (1) entirely in cash, (2) entirely by increasing the principal amount of the toggle notes or issuing new toggle notes, or PIK interest, or (3) 50% in cash interest and 50% in PIK interest. After October 15, 2012, all interest on the senior toggle notes will be payable in cash. If we elect to pay PIK interest, we will increase the principal amount of the senior toggle notes or issue senior toggle notes in an amount equal to the amount of PIK interest for the applicable interest payment period to holders of the senior toggle notes on the relevant record date.

Interest on the senior subordinated notes is payable in cash and accrues at a rate of 11 5/8% per annum.

Interest Payment Dates | April 15 and October 15, commencing April 15, 2008. |

Guarantees | Each of our existing and future wholly-owned domestic restricted subsidiaries will jointly, severally and unconditionally guarantee the senior notes on a senior unsecured basis and the senior subordinated notes on a senior subordinated unsecured basis, in each case to the extent such subsidiaries guarantee our senior secured cash flow facilities. |

Ranking | The senior notes and the related guarantees are our and the guarantors’ general unsecured senior indebtedness and: |

| • | rank equally in right of payment to all of our and the guarantors’ existing and future indebtedness and other obligations that are not, by their terms, expressly subordinated in right of payment to the notes and the related guarantees (including borrowings under our senior secured credit facilities); |

9

Table of Contents

| • | are senior in right of payment to any of our and the guarantors’ existing and future senior subordinated and subordinated indebtedness and other obligations (including the senior subordinated notes and the related guarantees) that are, by their terms, expressly subordinated in right of payment to the notes and the related guarantees; and |

| • | are effectively subordinated to all of our and the subsidiary guarantors’ existing and future senior secured indebtedness and other obligations (including borrowings under our senior secured credit facilities) to the extent of the value of the assets securing such indebtedness and other obligations. |

The senior subordinated notes and the related guarantees are our and the guarantors’ general unsecured senior subordinated indebtedness and:

| • | rank junior in right of payment to any of our and the guarantors’ existing and future senior indebtedness and other obligations (including the senior notes and the related guarantees and borrowings under our senior secured credit facilities); |

| • | rank equally in right of payment to all of our and the guarantors’ existing and future senior subordinated indebtedness and other obligations; and |

| • | are senior in right of payment to any of our and the guarantors’ existing and future subordinated indebtedness and other obligations that are, by their terms, expressly subordinated in right of payment to the senior subordinated notes and the related guarantees. |

As of February 29, 2008, on a pro forma basis after giving effect to the Transactions, we and the guarantors would have had $3,733 million of senior secured indebtedness outstanding, consisting of borrowings and the related guarantees under our senior secured credit facilities. As of February 29, 2008, we also had:

| • | an additional approximately $326 million of borrowing capacity under our senior secured cash flow revolving facility, which, if borrowed, would be senior secured indebtedness; |

| • | an additional $350 million available for borrowing under our senior secured asset-based revolving credit facility, subject to borrowing base limitations, which, if borrowed, would be senior secured indebtedness; |

| • | the option to raise incremental term loans or increase the cash flow revolving credit facility commitments under our senior secured cash flow facilities of up to an amount that would cause our Senior Secured Leverage Ratio (as defined in our senior secured cash flow facilities) to be equal to or less than 4.50 to 1.00, which, if borrowed, would be senior secured indebtedness; and |

10

Table of Contents

| • | the option to increase the asset-based revolving credit facility commitments under our senior secured asset-based revolving credit facility by up to $100 million, which, if borrowed, would be senior secured indebtedness. |

Optional Redemption | We may redeem the notes, in whole or in part, at any time prior to October 15, 2012 at a price equal to 100% of the aggregate principal amount of the notes plus the applicable “make whole” premium as described in “Description of Senior Notes—Optional Redemption” or in “Description of Senior Subordinated Notes—Optional Redemption,” plus accrued and unpaid interest, if any, to the applicable redemption date. |

We may redeem the notes, in whole or in part, at any time on or after October 15, 2012, at the applicable redemption price specified in “Description of Senior Notes—Optional Redemption” or in “Description of Senior Subordinated Notes—Optional Redemption,” in each case, plus accrued and unpaid interest, if any, to the applicable redemption date.

In addition, we may redeem up to 35% aggregate principal amount of the notes at any time prior to October 15, 2010, with the net cash proceeds from certain equity offerings at the applicable redemption price specified in “Description of Senior Notes—Optional Redemption” or in “Description of Senior Subordinated Notes—Optional Redemption,” in each case, plus accrued and unpaid interest, if any, to the applicable redemption date.

Change of Control | If we experience specific kinds of changes of control, we must offer to repurchase all of the notes at 101% of their principal amount, plus accrued and unpaid interest, if any, to the repurchase date. |

Certain Covenants | The indentures governing the notes, among other things, limit our ability and the ability of our subsidiaries to: |

| • | incur or guarantee additional indebtedness; |

| • | incur liens; |

| • | pay dividends on or make distributions in respect of our capital stock or make other restricted payments; |

| • | make investments; |

| • | consolidate, merge, sell or otherwise dispose of certain assets; and |

| • | enter into transactions with our affiliates. |

These covenants are subject to important exceptions, limitations and qualifications as described in “Description of Senior Notes—Certain Covenants” and “Description of Senior Subordinated Notes—Certain Covenants.”

Risk Factors | See “Risk Factors” and the other information in this prospectus for a discussion of some of the factors you should carefully consider before investing in the notes. |

11

Table of Contents

Summary Historical Consolidated and

Unaudited Pro Forma Condensed Consolidated Financial and Other Data

The following table presents our summary historical andpro forma financial information as of and for the periods presented. The summary historical financial information as of May 31, 2006 and 2007 and for each of the years in the three-year period ended May 31, 2007 have been derived from, and should be read in conjunction with, our audited financial statements included elsewhere in this prospectus. The summary historical financial information as of May 31, 2005 has been derived from our audited financial statements not included in this prospectus. The unaudited summary historical financial information as of and for the nine months ended February 28, 2007 and as of February 29, 2008 and for the period from June 1, 2007 through July 11, 2007 and for the period from July 12, 2007 through February 29, 2008 are derived from, and should be read in conjunction with, our unaudited condensed consolidated financial statements included elsewhere in this prospectus, and, except as otherwise described herein, have been prepared on a basis consistent with our annual audited financial statements and, in the opinion of management, include all adjustments consisting of normal recurring accruals considered necessary for a fair presentation of such data. Certain amounts recorded in previous periods have been reclassified to conform to the current presentation.

The Offer for Biomet’s Shares was completed successfully on July 11, 2007. Although Biomet continues as the same legal entity after the Merger, Holding’s cost of acquiring Biomet has been pushed-down to establish a new accounting basis for Biomet. Accordingly, the financial information in the table below for the nine months ended February 29, 2008 is presented separately for the period prior to the completion of the Offer (from June 1, 2007 through July 11, 2007, the “Predecessor” or “Predecessor Period”) and the period after the completion of the Offer (from July 12, 2007 through February 29, 2008, the “Successor” or “Successor Period”), which relate to the accounting periods preceding and succeeding the completion of the Offer. The summary financial information as of February 29, 2008 and for the Successor Period are not comparative to the summary financial information as of and for the nine months ended February 28, 2007 because of the new basis of accounting resulting from the Merger. Our results of operations for the Predecessor Period and the Successor Period should not be considered representative of our future results of operations.

In addition, as noted in Note B of Notes to Consolidated Financial Statements included elsewhere in this prospectus, the summary historical financial information as of and for the year ended May 31, 2007 has been prepared on the basis of an April 30 fiscal year for our foreign subsidiaries for financial reporting purposes. Subsequent to the completion of the Offer, we eliminated this one-month lag at our foreign subsidiaries, and therefore, the summary historical financial information as of and for the year ended May 31, 2007 is not comparative to the summary financial information as of and for the Successor Period due to the elimination of this one-month lag for financial purposes at our foreign subsidiaries.

The summary unaudited pro forma condensed consolidated statements of operations for the year ended May 31, 2007 is based on our audited financial statements appearing elsewhere in this prospectus and gives effect to the Transactions as if they had occurred on June 1, 2006. The summary unaudited pro forma condensed consolidated statements of operations for the nine months ended February 29, 2008 is based on our unaudited condensed consolidated financial statements included elsewhere in this prospectus and gives effect to the Transactions as if they had occurred on June 1, 2006. See “The Transactions.” The unaudited pro forma condensed consolidated statements of operations should not be considered representative of our future results of operations.

Please refer to “Unaudited Pro Forma Condensed Consolidated Financial Data,” “Selected Historical Consolidated Financial and Other Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our financial statements and notes thereto included elsewhere in this prospectus. The

12

Table of Contents

audited consolidated financial statements for each of the years in the three-year period ended May 31, 2007 have been audited by Ernst & Young LLP, an independent registered public accounting firm.

As a result of the report from the special committee formed by our Board of Directors, or the Special Committee, to conduct an independent investigation of our past stock option grant practices, and based on the determinations of our Audit Committee, we have restated our consolidated balance sheets as of May 31, 2005 and 2006 and the consolidated statements of operations for the fiscal years ended May 31, 2005 and 2006 to reflect the impact of additional share-based compensation expense and other adjustments described in our Amended Annual Report on Form 10-K/A, which was filed with the SEC on May 29, 2007.

| Historical | Pro Forma | |||||||||||||||||||||||||||||||||

| Predecessor | Successor | Fiscal Year Ended May 31, 2007 | Nine Months Ended February 29, 2008 | |||||||||||||||||||||||||||||||

| Fiscal Year Ended May 31, | Nine Months Ended February 28, 2007 | June 1, 2007 through July 11, 2007 | July 12, 2007 through February 29, 2008 | |||||||||||||||||||||||||||||||

($ in millions) | 2005 | 2006 | 2007 | |||||||||||||||||||||||||||||||

| (unaudited) | (unaudited) | (unaudited) | (unaudited) | (unaudited) | ||||||||||||||||||||||||||||||

Statements of Operations Data: | ||||||||||||||||||||||||||||||||||

Net sales | $ | 1,880 | $ | 2,026 | $ | 2,107 | $ | 1,558 | $ | 249 | $ | 1,499 | $ | 2,107 | $ | 1,748 | ||||||||||||||||||

Cost of sales | 533 | 582 | 642 | 454 | 102 | 614 | 650 | 530 | ||||||||||||||||||||||||||

Gross margin | 1,347 | 1,444 | 1,465 | 1,104 | 147 | 885 | 1,457 | 1,218 | ||||||||||||||||||||||||||

Selling, general and administrative expense | 697 | 750 | 881 | 592 | 194 | 834 | 889 | 675 | ||||||||||||||||||||||||||

Research and development expense | 80 | 85 | 94 | 71 | 34 | 59 | 94 | 69 | ||||||||||||||||||||||||||

In-process research and development | 26 | — | — | — | — | 479 | — | — | ||||||||||||||||||||||||||

Amortization | — | — | — | 6 | 1 | 227 | 362 | 268 | ||||||||||||||||||||||||||

Operating income (loss) | 544 | 609 | 490 | 435 | (82 | ) | (713 | ) | 112 | 206 | ||||||||||||||||||||||||

Other income (loss), net | 11 | 14 | 21 | 17 | — | (1 | ) | 6 | (1 | ) | ||||||||||||||||||||||||

Interest expense | (9 | ) | (12 | ) | (9 | ) | (9 | ) | — | (372 | ) | (594 | ) | (445 | ) | |||||||||||||||||||

Income (loss) before income taxes | 546 | 611 | 502 | 443 | (82 | ) | (1,086 | ) | (476 | ) | (240 | ) | ||||||||||||||||||||||

Provision (benefit) for income taxes | 197 | 205 | 166 | 149 | (27 | ) | (213 | ) | (190 | ) | (102 | ) | ||||||||||||||||||||||

Net income (loss) | $ | 349 | $ | 406 | $ | 336 | $ | 294 | $ | (55 | ) | $ | (873 | ) | $ | (286 | ) | $ | (1,380 | ) | ||||||||||||||

13

Table of Contents

| Historical | ||||||||||||||||||

| Predecessor | Successor | |||||||||||||||||

| Fiscal Year Ended May 31, | Nine Months Ended February 28, 2007 | Nine Months Ended February 29, 2008 | ||||||||||||||||

($ in millions) | 2005 | 2006 | 2007 | |||||||||||||||

| (unaudited) | (unaudited) | |||||||||||||||||

Balance Sheet Data (at period end): | ||||||||||||||||||

Cash and cash equivalents | $ | 91 | $ | 126 | $ | 105 | $ | 126 | $ | 97 | ||||||||

Total current assets | 1,192 | 1,299 | 1,452 | 1,373 | 1,421 | |||||||||||||

Total assets | 2,115 | 2,283 | 2,458 | 2,358 | 13,602 | |||||||||||||

Short-term borrowings | 282 | 277 | 82 | 100 | 42 | |||||||||||||

Total current liabilities | 515 | 518 | 346 | 346 | 608 | |||||||||||||

Total liabilities | 546 | 563 | 409 | 374 | 9,156 | |||||||||||||

Total shareholders’ equity | 1,569 | 1,720 | 2,049 | 1,984 | 4,446 | |||||||||||||

| Historical | ||||||||||||||||||||||||||

| Predecessor | Successor | |||||||||||||||||||||||||

| Fiscal Year Ended May 31, | Nine Months Ended February 28, 2007 | June 1, 2007 through July 11, 2007 | July 12, 2007 through February 29, 2008 | |||||||||||||||||||||||

($ in millions, except ratios) | 2005 | 2006 | 2007 | |||||||||||||||||||||||

| (unaudited) | (unaudited) | (unaudited) | ||||||||||||||||||||||||

Statements of Cash Flows Data: | ||||||||||||||||||||||||||

Net cash (used in) provided by: | ||||||||||||||||||||||||||

Operating activities | $ | 411 | $ | 413 | $ | 440 | $ | 295 | $ | 60 | $ | 84 | ||||||||||||||

Investing activities | (301 | ) | (121 | ) | (214 | ) | (56 | ) | 11 | (11,708 | ) | |||||||||||||||

Financing activities | (98 | ) | (258 | ) | (251 | ) | (239 | ) | 1 | 11,532 | ||||||||||||||||

Other Financial Data: | ||||||||||||||||||||||||||

Depreciation and amortization | $ | 70 | $ | 82 | $ | 97 | $ | 69 | $ | 9 | $ | 315 | ||||||||||||||

Capital expenditures | (97 | ) | (109 | ) | (143 | ) | (89 | ) | (22 | ) | (129 | ) | ||||||||||||||

Ratio of earnings to fixed charges(1) | 61.7 | x | 51.9 | x | 56.8 | x | 52.6 | x | — | — | ||||||||||||||||

| (1) | For purposes of computing the ratio of earnings to fixed charges, “earnings” consist of operating income plus other income plus cash dividends received from equity interests, less the equity income recorded. Fixed charges consist of interest expense, including amortization of debt issuance costs and interest capitalized. The interest portion of rental expense is not significant. On a pro forma basis, earnings were inadequate to cover fixed charges for fiscal 2007, and the period from July 12, 2007 through February 29, 2008 by $478 million, and $430 million, respectively. Earnings were also inadequate to cover fixed charges for the period from June 1, 2007 through July 11, 2007 by $82 million. |

14

Table of Contents

You should carefully consider the risks described below before investing in the notes. The risks described below are not the only ones facing our company. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial may also materially and adversely affect our business or results of operations in the future. Any of the following risks could materially adversely affect our business, financial condition or results of operations. In such case, you may lose all or part of your investment in the notes.

Risks Related to Our Indebtedness and the Notes

Our substantial level of indebtedness could materially adversely affect our ability to generate sufficient cash to fulfill our obligations under the notes, our ability to react to changes in our business and our ability to incur additional indebtedness to fund future needs.

We are highly leveraged. As of February 29, 2008, we had total indebtedness of approximately $6,309 million. The following chart shows our level of indebtedness as of February 29, 2008:

($ in millions) | |||

European line of credit | $ | 5 | |

Japanese lines of credit | — | ||

Senior secured term loan facilities | 3,659 | ||

Senior secured cash flow revolving credit facility | 74 | ||

Senior secured asset-based revolving credit facility | — | ||

Senior cash pay notes | 775 | ||

Senior toggle notes | 775 | ||

Senior subordinated notes | 1,015 | ||

Premium on debt | 6 | ||

Total | $ | 6,309 | |

On a pro forma basis after giving effect to the Transactions, our cash interest expense, net for fiscal 2007 would have been $584 million. As of February 29, 2008, we had outstanding approximately $3,733 million in aggregate principal amount of indebtedness under our senior secured credit facilities that would bear interest at a floating rate. Purchaser entered into a series of interest rate swap agreements to fix the interest rates on approximately 56% of the borrowings under our senior secured credit facilities. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Quantitative and Qualitative Disclosures about Market Risk—Interest Rate Risk.” An increase of 0.125% in these floating rates would increase our annual interest expense on the borrowings that are not subject to the interest rate swap agreements by approximately $2 million. See “Unaudited Pro Forma Condensed Consolidated Financial Data.”

Our substantial level of indebtedness increases the possibility that we may be unable to generate cash sufficient to pay, when due, the principal of, interest on or other amounts due in respect of our indebtedness. Our substantial indebtedness, combined with our other financial obligations and contractual commitments, could have important consequences for our noteholders. For example, it could:

| • | make it more difficult for us to satisfy our obligations with respect to our indebtedness, including the notes, and any failure to comply with the obligations under any of our debt instruments, including restrictive covenants, could result in an event of default under the indentures governing the notes and the agreements governing such other indebtedness; |

| • | require us to dedicate a substantial portion of our cash flow from operations to payments on our indebtedness, thereby reducing funds available for working capital, capital expenditures, acquisitions, research and development and other purposes; |

15

Table of Contents

| • | increase our vulnerability to adverse economic and industry conditions, which could place us at a competitive disadvantage compared to our competitors that have relatively less indebtedness; |

| • | limit our flexibility in planning for, or reacting to, changes in our business and the industries in which we operate; |

| • | limit our noteholders’ rights to receive payments under the notes if secured creditors have not been paid; |

| • | limit our ability to borrow additional funds, or to dispose of assets to raise funds, if needed, for working capital, capital expenditures, acquisitions, research and development and other corporate purposes; and |

| • | prevent us from raising the funds necessary to repurchase all notes tendered to us upon the occurrence of certain changes of control, which would constitute a default under the indentures governing the notes. |

Restrictions imposed by the indentures governing the notes, our senior secured credit facilities and our other outstanding indebtedness may limit our ability to operate our business and to finance our future operations or capital needs or to engage in other business activities.

The terms of our senior secured credit facilities and the indentures governing the notes restrict us and our subsidiaries from engaging in specified types of transactions. These covenants restrict our and our restricted subsidiaries’ ability, among other things, to:

| • | incur additional indebtedness; |

| • | pay dividends on our capital stock or redeem, repurchase or retire our capital stock or indebtedness; |

| • | make investments, loans, advances and acquisitions; |

| • | create restrictions on the payment of dividends or other amounts to us from our restricted subsidiaries; |

| • | engage in transactions with our affiliates; |