As filed with the Securities and Exchange Commission on May 14, 2008

Registration No. 333-_________

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Pansoft Company Limited

(Exact Name of Registrant as Specified in its Charter)

British Virgin Islands | 7371 | Not applicable |

(State or Other Jurisdiction of Incorporation or Organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

3/f, Qilu Software Park Building Jinan Hi-tech Zone Jinan, Shandong, People’s Republic of China 250101 | CT Corporation System 4701 Cox Road Suite 301 Glen Allen, Virginia 23060 |

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices) | (Name, address, including zip code, and telephone number, including area code, of agent for service) |

Copies to:

Bradley A. Haneberg, Esq.

Anthony W. Basch, Esq.

Kaufman & Canoles

Three James Center, 1051 East Cary Street, 12th Floor

Richmond, Virginia 23219

(804) 771-5700 - telephone

(804) 771-5777 - facsimile

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If delivery of the prospectus is expected to be made pursuant to Rule 434, check the following box. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer o | Accelerated filer o |

Non-accelerated filer o | Smaller reporting company x |

(Do not check if a smaller reporting company)

CALCULATION OF REGISTRATION FEE

Title of Each Class of Securities to be Registered | Amount to be Registered(1) | Proposed Maximum Offering Price per Share | Proposed Maximum Aggregate Offering Price | Amount of Registration Fee | |||||||||

| Ordinary Shares | 1,200,000 | (2) | $ | 6.00 | (2) | $ | 7,200,000 | (2) | |||||

Placement Agent Warrants(3) | 120,000 | (4) | $ | 0.001 | $ | 120 | (4) | ||||||

Ordinary Shares Issuable Upon Exercise of Placement Agent Warrants(3) | 120,000 | (5) | $ | 7.20 | (5) | $ | 900,000 | (5) | |||||

Total | $ | 8,100,120 | $ | 319 | |||||||||

(1) | In accordance with Rule 416(a), the Registrant is also registering an indeterminate number of additional ordinary shares that shall be issuable pursuant to Rule 416 to prevent dilution resulting from stock splits, stock dividends or similar transactions. |

(2) | The registration fee for securities to be offered by the Registrant is based on an estimate of the Proposed Maximum Aggregate Offering Price of the securities, and such estimate is solely for the purpose of calculating the registration fee pursuant to Rule 457(o). |

(3) | In connection with the Registrant’s sale of the ordinary shares registered hereby, the Registrant will sell to Anderson & Strudwick, Incorporated (the “placement agent”) warrants to purchase 120,000 ordinary shares of common stock (the “placement agent warrants”), such amount representing 10% of the aggregate number of ordinary shares sold by the Registrant pursuant to this registration statement. The price to be paid by the placement agent for the placement agent warrants is $0.001 per warrant. The exercise price of the placement agent warrants is $7.20 per ordinary share, representing 120% of the price of the ordinary shares offered hereby. The resale of the ordinary shares underlying the placement agent warrants is registered hereunder. The ordinary shares underlying the placement agent warrants are being registered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, as amended. |

(4) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457. |

(5) | The registration fee for securities to be offered by the placement agent is based on an estimate of the Proposed Maximum Aggregate Offering Price of the securities, and such estimate is solely for the purpose of calculating the registration fee pursuant to Rule 457(o). |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED ___________

Pansoft Company Limited

1,200,000 Ordinary Shares

This is the initial public offering of Pansoft Company Limited, a British Virgin Islands company. We are offering 1,200,000 ordinary shares through our placement agent, Anderson & Strudwick, Incorporated, on a “best efforts, all-or-none” basis.

We expect that the offering price will be $6.00 per ordinary share. No public market currently exists for our ordinary shares. We have applied for approval for quotation on the NASDAQ Capital Market under the symbol “PSOF” for the ordinary shares we are offering. We believe that upon the completion of the offering contemplated by this prospectus, we will meet the standards for listing on the NASDAQ Capital Market.

Investing in these ordinary shares involves significant risks. See “Risk Factors” beginning on page of this prospectus.

Per Ordinary Share | Total | ||||||

| Public Offering Price | $ | 6.00 | $ | 7,200,000 | |||

| Placement Commission | $ | 0.42 | $ | 504,000 | |||

| Proceeds to us, before expenses | $ | 5.58 | $ | 6,696,000 | |||

We expect total cash expenses for this offering to be approximately $_____. Our placement agent must sell 1,200,000 ordinary shares if any are to be sold. Our placement agent is required to use only its best efforts to sell the securities offered. The offering will terminate upon the earlier of: (i) a date mutually acceptable to us and our placement agent after which the 1,200,000 ordinary shares are sold or (ii) September 30, 2008. Until we sell at least 1,200,000 ordinary shares, all investor funds will be held in an escrow account at SunTrust Bank, Richmond, Virginia. If we do not sell at least 1,200,000 ordinary shares by September 30, 2008, all funds will be promptly returned to investors (within one business day) without interest or deduction.

These securities have not been approved or disapproved by the Securities and Exchange Commission or any state securities commission nor has the Securities and Exchange Commission or any state securities commission passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

Anderson & Strudwick,

Incorporated

Prospectus dated ________, 2008

Except where the context otherwise requires and for purposes of this prospectus only:

| · | the terms “we,” “us,” “our company,” “our” and “Pansoft” refer to Pansoft Company Limited, and its operating subsidiary, Pansoft (Jinan) Co., Ltd. (“PJCL”); |

| · | “shares” and “ordinary shares” refer to our ordinary shares; |

| · | “China” and “PRC” refer to the People’s Republic of China, and for the purpose of this prospectus only, excluding Taiwan, Hong Kong and Macau; and |

| · | all references to “RMB,” “Renminbi” and “¥” are to the legal currency of China and all references to “USD,” “U.S. dollars,” “dollars,” “U.S. $” and “$” are to the legal currency of the United States. |

This prospectus contains translations of certain RMB amounts into U.S. dollar amounts at a specified rate solely for the convenience of the reader. Unless otherwise stated, the translations of RMB into U.S. dollars have been made at the single rate of exchange of U.S. $1.00 to RMB7.2946, the exchange rate at December 31, 2007. We make no representation that the RMB or U.S. dollar amounts referred to in this prospectus could have been or could be converted into U.S. dollars or RMB, as the case may be, at any particular rate or at all. On May 9, 2008, the noon buying rate was $1.00 to RMB6.9876. See “Risk Factors - Fluctuation of the Renminbi could materially affect our financial condition and results of operations” for discussions of the effects of fluctuating exchange rates on the value of our ordinary shares. Any discrepancies in any table between the amounts identified as total amounts and the sum of the amounts listed therein are due to rounding.

For the sake of clarity, this prospectus follows English naming convention of first name followed by last name, regardless of whether an individual’s name is Chinese or English. For example, the name of the chief executive officer of Pansoft would be presented as “Hugh Wang” (English) or “Hu Wang” (Chinese), even though, in China, his name is presented as “Wang Hu” (王禲).

Unless otherwise indicated, the information in this prospectus assumes a 169.5253-for-one stock split effected in the form of a stock dividend to holders our ordinary shares prior to the completion of this offering.

This summary highlights information that we present more fully in the rest of this prospectus. This summary does not contain all of the information you should consider before buying ordinary shares in this offering. This summary contains forward-looking statements that involve risks and uncertainties, such as statements about our plans, objectives, expectations, assumptions or future events. In some cases, you can identify forward-looking statements by terminology such as “anticipate,” “estimate,” “plan,” “project,” “continuing,” “ongoing,” “expect,” “we believe,” “we intend,” “may,” “will,” “should,” “could,” and similar expressions. These statements involve estimates, assumptions, known and unknown risks, uncertainties and other factors that could cause actual results to differ materially from any future results, performances or achievements expressed or implied by the forward-looking statements. You should read the entire prospectus carefully, including the “Risk Factors” section and the financial statements and the notes to those statements.

Our Company

We are a holding company that owns all of the outstanding capital stock of PJCL, our wholly-owned operating subsidiary based in Jinan, China. Our business is divided into two distinct areas.

First, we are a leading developer of enterprise resource planning (“ERP”) software and professional services for participants in China’s oil and gas industry. ERP software addresses various facets of business operation including accounting, order processing, delivering, invoicing, inventory control, and customer relationship management. We have developed customized ERP software systems for PetroChina Company Limited and China National Petroleum Corporation, its state-owned parent company (together, “PetroChina”) and China Petrochemical Corporation/China Petroleum and Chemical Corporation and Sinopec Group, its state-owned parent company (together, “Sinopec”), large oil companies formed when the Chinese government decentralized the oil industry in China, and their respective predecessors.

Second, based on technology and business experience accumulated from our solutions and services provided for our larger clients, we have also developed an ERP software development platform for small-to-medium sized businesses (“SMEs”) in China. We combine solutions developed for our most sophisticated clients with network applications available on the Internet to provide increased opportunities for SMEs to enter the ERP market. We offer these SME solutions, named “PanSchema”, through an Internet-based, software-as-a-service model designed to customize cost-effective software solutions for Chinese SMEs. While Chinese SMEs represent a wide variety of industries, each with complex and unique software needs, we believe that SMEs may not be able to afford the costs associated with ERP software development offered through a traditional, consulting model. Rather, we developed PanSchema to permit third-party business consulting companies and small information technology service providers to develop customized ERP solutions to meet the particular needs of their SME clients. We cooperate with and train the consulting companies and information technology service providers to efficiently utilize PanSchema.

We expect, over time, to provide customized ERP software solutions to a wider variety of industries, including, but not limited to the pharmaceutical, energy and telecommunications industries. In addition, we will continue to actively develop and market PanSchema to a growing SME market throughout China. Our software solutions business is enhanced and supported by our consulting services and ongoing maintenance on existing software installations. Our principal executive offices are located at 3/f, Qilu Software Park Building, Jinan Hi-tech Zone, Jinan 250101, Shandong, People’s Republic of China. Our telephone number is (86531) 88871166. Our website address is www.pansoft.com. Information contained on the website is not a part of this prospectus.

Background of the Chinese Software Industry

The Chinese government began to focus upon technology and science shortly after the formation of the PRC. From 1948 to 1977, the Chinese government directly controlled all research, development and engineering activities through its State Development Planning Commission and State Science and Technology Commission. In the 1980s, China began to implement market-oriented economic reforms designed to improve Chinese science and technology industry. During this period, China further reduced the central government’s control over the operation of research oriented businesses. In the late 1980s, the central government authorized the operation of the first Chinese software companies. In the 1990s, Chinese policymakers again attempted to enhance the development of high technology businesses by experimenting with additional reduction of governmental control while also providing new forms of ownership for these businesses. In addition, in 1992, the Chinese government liberalized market access by adopting policies that favored foreign investment in high technology businesses. By the end of the 1990s, the Chinese government had abandoned most of its control over many high technology businesses and adopted a progressive tax structure designed to further encourage the financial development of these businesses. These policies positively impacted the development of Chinese software businesses. From 1992 to 2000, the Chinese software industry grew at an annual rate of more than 30%, albeit from a very small base. Today, the Chinese software industry continues to grow at a rapid pace. The Chinese software industry reached RMB580 billion in sales in 2007, an increase of 20% over 2006. China’s ERP sales were RMB3.4 billion in 2007, accounting for approximately 1.47% of total global ERP sales (Zikoo, 2007-2008 Chinese Software Industry Report). Notwithstanding the rapid growth, however, China still lags behind other developed countries as its software industry accounts for less than 6% of the global software market.

Our Industry

The overall scale of China’s ERP market reached RMB3.4 billion in 2007. Fierce competition is ongoing on the mid and low-end market between local ERP suppliers and their international counterparts, and among local suppliers themselves. On the mid and high-end market, the products and services of local ERP suppliers have not caught up with the increasingly demanding needs of sophisticated corporate users. We believe that China’s ERP market is currently entering into a new phase, in which the several products are emerging as the industry’s “top brands”.

The statistics last year from China’s General Administration of Quality Supervision, Inspection and Quarantine (AQSIQ) showed that ERP brand concentration has been intensified. The top 10 brands in 2006 accounted for 5% more market share than they did in 2005. However, we do not believe that any one brand is unassailably dominant in the market. No single brand claims more than a 15% share of the ERP market. We believe a significant number of Chinese manufacturers still lack sufficient IT applications and services for their needs. We believe that the manufacturing and distribution sector, which catalyzed the birth of ERP products, remains the key to ERP market scale.

In the context of economic transformation, local manufacturers face industrial restructuring and increased pressure from greatly shortened product lives while they strive to expand and strengthen their business operations. We believe that the use of advanced information technologies in management and operations is becoming more important to success in the market and that those local ERP suppliers who can leverage their understanding of these demands to deliver customized solutions to customers are the ones who will succeed in China’s maturing ERP industry.

Our Competitive Strengths

We believe the following strengths differentiate us from our competitors, enabling us to attain a leadership position in the ERP market in China.

| · | customized solution provider, rather than a standard software package seller; |

| · | service provider rather than product seller; |

| · | integration technology provider; |

| · | focus on large, sophisticated business clients, especially in China’s oil and gas industry; |

| · | ability to leverage solutions developed for larger clients for the benefit of smaller clients; |

| · | market leader with extensive ERP expertise; |

| · | strong solution and service development capability; |

| · | comprehensive solution and service offerings; |

| · | scalable, nationwide delivery and service platform; and |

| · | proven management with successful track record. |

Our Strategy

We are a leading ERP software and professional services for participants in China’s oil and gas industry. Our goal is to become the leading ERP provider in the entire ERP market in China. We intend to achieve this goal by implementing the following strategies:

| · | strengthen relationships with key clients; |

| · | diversify our client base and service offerings to capture new growth opportunities; |

| · | continue to enhance our development and delivery capabilities; |

| · | attract and retain quality employees; and |

| · | pursue strategic acquisitions and alliances that fit with our core competencies and growth strategy. |

Our Challenges

We believe our primary challenges are:

| · | single industry focus; |

| · | past and likely future dependence on a few clients for a significant portion of our revenue and this dependence is likely to continue. In 2006 and 2007, our four largest clients collectively accounted for 74% and 82% of our revenue, respectively; |

| · | uncertainties in our development, introduction and marketing of new solutions and services; |

| · | recruitment, training and retention of skilled software engineers and mid-level personnel; |

| · | competition from existing competitors and new market entrants; |

| · | execution of our growth strategy; |

| · | protection of our trade secrets and other valuable intellectual property. We have transferred intellectual property rights to a number of our clients and consequently may not own all the intellectual property rights to our current and future software solutions; and |

| · | reliance principally on dividends paid by our PRC operating subsidiaries to fund cash and financing requirements, while there are PRC laws restricting the ability of these subsidiaries from paying dividends or making other distributions to us. |

In addition, we face risks and uncertainties that may materially affect our business, financial condition, results of operations and prospects. Thus, you should consider the risks discussed in “Risk Factors” and elsewhere in this prospectus before investing in our ordinary shares.

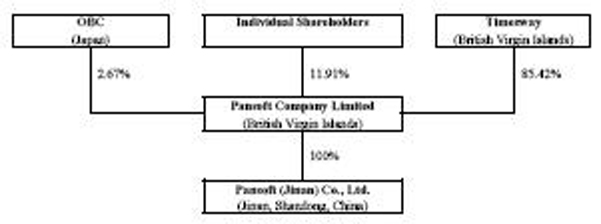

Our Corporate Information

We were incorporated as an international business company under the International Business Companies Act, 1984, in the British Virgin Islands on September 28, 2001. We were automatically re-registered as a British Virgin Islands business company under the BVI Business Companies Act, 2004 (as amended) (the “Companies Law”), on January 1, 2007. In June 2006, we acquired PJCL and created a holding company structure by which we were the parent company and PJCL was our operating subsidiary in China. PJCL was formed in September 2001 and has been focused on software development since its foundation. See “Our Corporate Structure.”

The Offering

| Shares offered: | 1,200,000 ordinary shares |

| Shares to be outstanding after offering: | 5,438,232 ordinary shares |

| Proposed NASDAQ Capital Market symbol: | “PSOF” |

| Risk Factors: | Investing in these securities involves a high degree of risk. As an investor, you should be able to bear a complete loss of your investment. You should carefully consider the information set forth in the “Risk Factors” section of this prospectus before deciding to invest in our ordinary shares. |

| Gross proceeds: | $7,200,000 |

| Closing of offering: | The offering contemplated by this prospectus will terminate upon the earlier of: (i) a date mutually acceptable to us and our placement agent after the offering is sold or (ii) September 30, 2008. |

Placement

We have engaged Anderson & Strudwick, Incorporated to conduct this offering on a “best efforts, all-or-none” basis. The offering is being made without a firm commitment by the placement agent, which has no obligation or commitment to purchase any of our ordinary shares. Our placement agent is required to use only its best efforts to sell the securities offered. The offering will terminate upon the earlier of: (i) a date mutually acceptable to us and our placement agent after which at least 1,200,000 ordinary shares are sold or (ii) September 30, 2008. Until we sell at least 1,200,000 ordinary shares, all investor funds will be held in an escrow account at SunTrust Bank, Richmond, Virginia. If we do not sell at least 1,200,000 ordinary shares by September 30, 2008, all funds will be promptly returned to investors (within one business day) without interest or deduction. Although they have not formally committed to do so, our affiliates may opt to purchase ordinary shares in connection with this offering. To the extent such individuals invest, they will purchase our ordinary shares with investment intent and without the intent to resell.

Summary Financial Information

In the table below, we provide you with summary financial data of our company. This information is derived from our consolidated financial statements included elsewhere in this prospectus. Historical results are not necessarily indicative of the results that may be expected for any future period. When you read this historical selected financial data, it is important that you read it along with the historical statements and notes and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included elsewhere in this prospectus.

For the Fiscal Year Ended December 31, | |||||||

2007 | 2006 | ||||||

($) | ($) | ||||||

| Total Sales | 5,219,622 | 3,161,553 | |||||

| Income from Operations | 2,341,518 | 1,190,200 | |||||

| Other Income (expense) | 27,214 | (8,850 | ) | ||||

| Net Income | 2,368,732 | 1,145,428 | |||||

| Other Comprehensive Income | 239,411 | 65,336 | |||||

| Comprehensive Income | 2,608,143 | 1,210,764 | |||||

| Basic and Diluted Earnings Per Share (based on 25,000 shares outstanding) | 94.75 | 45.82 | |||||

| Pro Forma Basic and Diluted Earnings per Share (giving effect to 169.5253-for-one stock split, after which 4,238,232 ordinary shares would be outstanding) | 0.56 | 0.27 | |||||

December 31, | |||||||

2007 | 2006 | ||||||

($) | ($) | ||||||

| Total Assets | 5,085,135 | 2,573,073 | |||||

| Total Current Liabilities | 467,025 | 563,106 | |||||

| Shareholders’ Equity | 4,618,110 | 2,009,967 | |||||

| Total liabilities and shareholders’ equity | 5,085,135 | 2,573,073 | |||||

Investment in our securities involves a high degree of risk. You should carefully consider the risks described below together with all of the other information included in this prospectus before making an investment decision. The risks and uncertainties described below are not the only ones we face, but represent the material risks to our business. If any of the following risks actually occurs, our business, financial condition or results of operations could suffer. In that case, you may lose all or part of your investment. You should not invest in this offering unless you can afford to lose your entire investment.

Risks Related to Our Business

We operate in a very competitive industry and may not be able to maintain our revenues and profitability.

More than 13,000 companies produce software in China. China’s MII estimates that, by 2010, Chinese companies will export approximately $12.5 billion worth of software. The ERP services market in China is intensely competitive and is characterized by frequent technological changes, evolving industry standards and changing client demands. We believe the principal competitive factors in our markets are:

| · | product quality; |

| · | adoption and implementation of standards; |

| · | emerging technology trends; |

| · | development of Internet software products; |

| · | reliability; |

| · | performance; |

| · | price; |

| · | vendor and product reputation; |

| · | financial stability; |

| · | features and functions; |

| · | ease of use; and |

| · | quality of support. |

A number of companies offer competitive products and services addressing certain of our target markets. Our most significant competition comes from well-funded international platform providers, such as SAP Ag (NYSE: SAP) and IBM (NYSE: IBM), domestic providers, such as Kingdee International Software Group Company Limited (HKEX: 0268) (“Kingdee”), Shandong Inspur Software Co., Ltd. (SHA: 600756), UFIDA Software Co., Ltd. (SSE: 600588) (“UFIDA”), and other targeted solutions providers in certain market segments in which we operate.

We believe that new market entrants may attempt to develop fully integrated enterprise-level systems targeting Chinese SMEs and oil and gas companies. Many of our existing competitors, as well as a number of potential new competitors, have significantly greater financial, technical and marketing resources than we do. Although we have experienced rapid growth in an extremely competitive environment, we cannot guarantee that we will be able to compete successfully against current or future competitors. As a result of this product concentration and uncertain product life cycles, we may not be as protected from new competition or industry downturns as a more diversified competitor. See “Our Business - Competition.”

We expect competition to increase from domestic and international competitors as additional companies compete to provide ERP services in China. Increased competition may result in price reductions, reduced margins and inability to gain or hold market share.

In addition, our competitors may introduce new business models. If these new business models are more attractive to customers than the business models we currently use, our customers may switch to our competitors’ services, and we may lose market share. We cannot assure you that we will be able to compete successfully against any new or existing competitors, or against any new business models our competitors may implement. In addition, the increased competition we anticipate in the ERP industry may also reduce the number of companies for which we are able to provide ERP services, or cause us to reduce our fees in order to attract or retain customers. All of these competitive factors could have a material adverse effect on our revenues and profitability.

Currently, revenues are highly dependent on China’s oil industry in general and on a few customers involved in that industry in particular.

While we provide ERP services to companies in a variety of industries, we have a particular focus on providing ERP solutions for companies in the oil and gas industry in China. In particular, we derive a substantial portion of our revenues related from our key customers in this industry, Sinopec and PetroChina and their subsidiary and parent companies.

Sinopec, Sinopec Group and their subsidiaries accounted for approximately 36% and 47% of our revenues in 2007 and 2006, respectively, and any termination of the services we provide to Sinopec and its subsidiaries would materially harm our operations.

PetroChina, China National Petroleum Corporation (CNPC and their subsidiaries accounted for approximately 43% and 16% of our revenues in 2007 and 2006, respectively, and any termination of the services we provided to PetroChina and its subsidiaries would materially harm our operations.

We anticipate that our dependence on a limited number of customers will continue for the foreseeable future. Consequently, any one of the following events may cause material fluctuations or declines in our revenues:

| · | reduction, delay or cancellation of orders from one or more of our significant customers; |

| · | loss of one or more of our significant customers and our failure to identify additional or replacement customers; and |

| · | failure of any of our significant customers to make timely payment for our products. |

To anticipate our client’s future ERP needs, build their trust and develop suitable solutions, we must maintain a close relationship with our key clients. Any failure to maintain this close relationship, due to unsuccessful sales and marketing efforts, lack of suitable solutions, unsatisfactory performance or other reasons, could result in our losing a client and its business. This is especially true for PetroChina and Sinopec, as many of the subsidiary branches of these companies have independent purchasing power for their information technology needs. If we lose a key client or a portion of work we currently receive from it, a key client significantly reduces its purchasing levels or delays a major purchase or we fail to attract additional major clients, our revenues could decline, and our operating results could be materially and adversely affected.

We may be unable to maintain current ERP software fees in the future.

We believe one reason for our success in competing with international ERP providers in the past has been the typical difference in fees for our development services and products, in particular our fees for custom solution development. For our custom development services, our prices are tied to the wages we pay our developers. China’s average wages have been increasing rapidly for the last several years, causing our services to become correspondingly more expensive.

We believe that increased competition within China and international competitors’ growing familiarity with the Chinese ERP market may result in a decrease in prices of our domestic competitors and a “leveling of the field” with our international competitors. For example, we provide some ERP services that contemplate ongoing maintenance fees. Several local ERP competitors have begun to charge low annual maintenance fees, in some cases less than a 5% fee, and to waive fees for first-year maintenance. To the extent our customers demand similar concessions or additional services, we may need to reconsider our fee structures. We cannot assure that any new fee structures would be accepted in the market or that we will be able to maintain our profitability if we are required to reduce these fees.

We may be forced to reduce the prices of our software products due to shortened product life cycles, increased competition and reduced bargaining power with our clients, which could lead to reduced revenues and profitability.

The software industry in China is developing rapidly and related technology trends are constantly evolving. This results in frequent introduction of new products and services, shortening product life cycles and significant price competition from our competitors. As the life cycle of a software product matures, the average selling price of the same product generally declines. A shortening life cycle of our software products generally could result in price erosion for these products if we are unable to introduce new products, or if our new products are not favorably received by our clients. We may be unable to offset the effect of declining average sales prices through increased sales volumes and/or reductions in our costs. Furthermore, we may be forced to reduce the prices of our software products in response to offerings made by our competitors. Finally, we may not have the same level of bargaining power we have enjoyed in the past when it comes to negotiating for the prices of our software products.

Any significant failure in our information technology systems could subject us to contractual liabilities to our clients, harm our reputation and adversely affect our results of operations.

Our business and operations are highly dependent on the ability of our information technology systems to timely process various transactions across different markets and solutions. In particular, our Internet-based ERP solutions rely heavily on the stability of our systems. The proper functioning of these systems, is critical to our business and to our ability to compete effectively. Our ERP business activities in particular may be materially disrupted in the event of a partial or complete failure of any of our primary information technology or communication systems, which could be caused by, among other things, software malfunction, computer virus attacks, conversion errors due to system upgrading, damage from fire, earthquake, power loss, telecommunications failure, unauthorized entry or other events beyond our control. We could also experience system interruptions due to the failure of their systems to function as intended or the failure of the systems relied upon to deliver services such as the Internet, processors that integrate with other systems and networks and systems of third parties. Loss of all or part of the systems for a period of time could have a material adverse effect on our business and business reputation. We may be liable to our clients for breach of contract for interruptions in service. Due to the numerous variables surrounding system disruptions, the extent or amount of any potential liability cannot be predicted. While we believe that this risk disproportionately affects our Internet-based ERP operations, which currently constitute a small portion of our overall business, the growth of our Internet-based ERP operations may make this risk more material to our overall business in the future.

Our computer networks may be vulnerable to security risks that could disrupt our services and adversely affect our results of operations.

Our computer networks may be vulnerable to unauthorized access, computer hackers, computer viruses and other security problems caused by unauthorized access to, or improper use of, systems by third parties or employees. A hacker who circumvents security measures could misappropriate proprietary information or cause interruptions or malfunctions in operations. Although we intend to continue to implement security measures, computer attacks or disruptions may jeopardize the security of information stored in and transmitted through computer systems of our customers. Actual or perceived concerns that our systems may be vulnerable to such attacks or disruptions may deter existing and potential clients from using our solutions or services. As a result, we may be required to expend significant resources to protect against the threat of these security breaches or to alleviate problems caused by these breaches. Losses or liabilities that are incurred as a result of any of the foregoing could have a material adverse effect on our business. While we believe that this risk disproportionately affects our Internet-based ERP operations, which currently constitute a small portion of our overall business, the growth of our Internet-based ERP operations may make this risk more material to our overall business in the future.

Chinese businesses may not be as open to ERP services as businesses in other countries.

Recent studies about the effectiveness of implementing ERP systems in China suggest that the success rate for such implementations is lower than in other developed countries. Academics have theorized that some of the reasons that studies have found implementation success rates of up to 33% include the following:

| · | The Chinese economy has only recently opened to foreign investment and Western business practices including ERP systems. |

| · | Foreign companies are still learning to adapt their ways of doing business to Chinese cultural and business models. |

| · | Chinese businesses tend to expect ERP systems to adapt to the way business is already done, rather than to change business practices to match a given ERP system. |

| · | ERP implementation under such requirements can be expensive and time-consuming, as shown by one study that found that over 90% of ERP implementations were either late or over budget. |

While the majority of our ERP services have been provided to a small number of very large companies, we cannot assure that we will be successful in implementing ERP solutions for SMEs.

We may lose our clients and our financial results would suffer if our clients change the decision-making body for their ERP system, merge with or are acquired by other companies, develop their own in-house capabilities or fail to expand.

We believe that doing business in China is influenced by sound client relationships, or guanxi (关系). Our business may be harmed if our guanxi with our clients deteriorates for any reason, including the following:

| · | Our clients may change their decision-making body for making ERP investments and key decision makers may change. For each key client, we use a team dedicated to its projects and to maintaining stable and close relationships with the relevant ERP procurement decision-makers. We build these extensive relationships over the course of several years. If a client centralizes purchasing decisions or otherwise changes the decision making body or level within the company at which the purchase decision is made or a key decision-maker is replaced, transferred or leaves the company, our client relationships may be disrupted and we may be unable to effectively and timely restore these relationships. |

| · | Consolidation of our clients and growth of in-house capabilities. As our clients grow in size, they may exert pricing pressure on vendors, and/or find it more cost-effective to set up their own ERP solutions, instead of relying on third-party companies for solutions and services. |

| · | Our clients fail to expand. Our clients may not successfully compete with their domestic and foreign competitors in the future. If our clients suffer a reduced market share or their results of operations and financial condition are otherwise adversely affected, they may reduce spending on our products and change expansion plans for their ERP systems, which in turn may materially and adversely affect our growth and results of operations. |

Defects in our software, errors in our systems integration or maintenance services or our failure to perform our professional services could result in a loss of clients and decrease in revenues, unexpected expenses and a reduction in market share.

Our software solutions are complex and may contain defects, errors and bugs when first introduced to the market or to a particular client, or as new versions are released. Because we cannot test for all possible scenarios, our solutions may contain errors which are not discovered until after they have been installed and we may not be able to correct these problems on a timely basis. These defects, errors or bugs could interrupt or delay completion of projects or sales to our clients. In addition, our reputation may be damaged and we may fail to obtain new projects from existing clients or new clients. We may make mistakes when we provide systems integration and maintenance services.

We also provide a range of ERP services and must meet stringent quality requirements for performing these services. If we fail to meet these requirements, we may be subject to claims for breach of contracts with our clients. Any such claim or adverse resolution of such claim against us may hurt our reputation and have a material adverse effect on our business.

We may not be able to adequately protect our intellectual property, which could cause us to be less competitive.

Our success will depend in part on our ability to protect and maintain intellectual property rights and licensing arrangements for our products. We rely on a combination of copyright, trademark and trade secret laws and restrictions on disclosure to protect our intellectual property rights. Piracy of intellectual property is widespread in China and despite our efforts to protect our intellectual property rights, unauthorized parties may attempt to copy or otherwise obtain and use our technology. Monitoring unauthorized use of our technology is difficult and costly, and we cannot be certain that the steps we have taken will prevent misappropriations of our technology, particularly in countries where the laws may not protect our intellectual property rights as fully as in other countries such as the United States of America, or U.S. In addition, third parties may seek to challenge, invalidate, circumvent or render unenforceable any intellectual property rights owned by us. From time to time, we may have to resort to litigation to enforce our intellectual property rights, which could result in substantial costs, diversion of our management’s attention and diversion of our other resources.

We share intellectual property rights to a number of our software solutions with Sinopec and PetroChina. We may be subject to intellectual property infringement claims from these clients and others, which may force us to incur substantial legal expenses and, if determined adversely against us, may materially disrupt our business and materially affect our gross margin and net income.

We have developed certain ERP software solutions in the oil and gas industry as commissioned by our customers in which we have agreed to share intellectual property rights. These affected contracts provided that we have the rights to own and commercialize any substantial improvements we make to the software solutions developed for clients under these contracts. We have also sold, and may sell in the future, variations of these software solutions to other clients.

If we are found to have violated the intellectual property rights of others, we may be enjoined from using such intellectual property rights, or we may incur licensing fees or be forced to develop alternatives. For example, if one of the companies from which we obtain software does not own all relevant intellectual property rights for the software we obtained, we could be liable for damages from the owner of such rights.

In addition, we typically provide indemnification to clients who purchase our solutions against potential infringement of intellectual property rights underlying those solutions, and are therefore subject to the risk of indemnity claims. We may incur substantial expenses in defending against these third party infringement claims, regardless of their merit. Successful infringement or licensing claims against us may result in substantial monetary liabilities, reputational harm, lost sales and lower gross margins which may materially and adversely affect our business, gross margin and net income. While we believe that, because we develop much of our own software, we are at a lower risk of such claims of infringement than we would be if we licensed all of our software from other companies, we cannot guarantee that third-parties will not make claims of infringement against us.

We are heavily dependent upon the services of technical and managerial personnel that possess skills to develop and implement ERP software, and we may have to actively compete for their services.

We are heavily dependent upon our ability to attract, retain and motivate skilled technical, managerial and consulting personnel, especially highly skilled engineers involved in ongoing product development and consulting personnel. Our ability to install, maintain and enhance our ERP software is substantially dependent upon our ability to locate, hire and train qualified personnel. As ERP concepts have only recently been adopted in China, the number of qualified technical, managerial and consulting personnel is limited. Many of our technical, managerial and consulting personnel possess skills that would be valuable to all companies engaged in software development, and the Chinese software industry is characterized by a high level of employee mobility and aggressive recruiting of skilled personnel. Consequently, we expect that we will have to actively compete with other Chinese software developers for these employees. Our ability to profitably operate is substantially dependent upon our ability to locate, hire, train and retain our technical, managerial and consulting personnel. Although we have not experienced difficulty locating, hiring, training or retaining our employees to date, there can be no assurance that we will be able to retain our current personnel, or that we will be able to attract, assimilate other personnel in the future. If we are unable to effectively obtain and maintain skilled personnel, the quality of our software products and the effectiveness of installation and training could be materially impaired. See “Our Business - Employees.”

We are heavily dependent upon the services of Value Added Resellers (“VARs”) to customize our PanSchema ERP platform for use in a variety of industries, and we may have to actively compete for their services.

In addition to our employees, value-added resellers, or VARs, are an integral element in the success of our PanSchema ERP platform. VARs are individuals or companies that do not develop their own software but instead use our platform to develop specialized solutions in a variety of industries. These VARs are able to tailor our PanSchema ERP platform so that it meets the needs of SMEs in various industries. These SMEs will download the version of PanSchema developed by a given VAR, and in so doing will generate revenues for both the VAR and our company. Presumably, a VAR will only use our software to develop specialized solutions if it believes our software, as modified, will be most attractive to the VAR’s target market. As ERP concepts have only recently been adopted in China, the number of qualified VARs is limited. Many VARs possess skills that would be valuable to all companies engaged in software development, and our competitors are likely to want to encourage the VARs to develop tailored ERP software for them as well, to the extent our competitors choose to follow a similar model to PanSchema. Consequently, we expect that we will have to actively compete with other Chinese software developers for the attention of VARs. Our ability to profitably operate is substantially dependent upon our ability to continue to work with talented VARs. There can be no assurance that we will be able to attract VARs or to maintain relationships with them in the future. A failure to maintain working relationships with VARs could materially impair our PanSchema platform.

Increases in wages for technical professionals will increase our net cash outflow and our gross margin and profit margin may decline.

Historically, wages for comparably skilled technical personnel in the Chinese ERP services industry have been lower than in developed countries, such as in the U.S. or Europe. In recent years, wages in China’s software services industry in general and the ERP industry in particular have increased and may continue to increase at faster rates. Wage increases will increase our cost of ERP software solutions of the same quality and increase our cost of operations. As a result, our gross margin and profit margin may decline. In the long term, unless offset by increases in efficiency and productivity of our work force, wage increases may also result in increased prices for our solutions and services, making us potentially less competitive. Increases in wages, including an increase in the cash component of our compensation expenses, will increase our net cash outflow and our gross margin and profit margin may decline.

Fluctuations in our clients’ spending cycles and other factors can cause our revenues and operating results to vary significantly from quarter to quarter and from year to year.

Our revenues and operating results will vary significantly from quarter to quarter and from year to year due to a number of factors, many of which are outside of our control. Most of our clients in the oil and gas industry pay a significant portion of our fees in the fourth quarter. For our customized solutions, we generally incur costs evenly during the project life while most of the related revenues are generated later in the project as we reach project milestones and complete projects. Also, the Chinese New Year holiday typically falls between late January and February of each year. As a result, relatively few contracts are signed in the first calendar quarter, with an increase in the second calendar quarter and with most of our contracts signed and completed in the third and fourth calendar quarters. Due to the annual budget cycles of most of our clients, we also may be unable to accurately estimate the demand for our solutions and services beyond the immediate calendar year, which could adversely affect our business planning. Moreover, our results will vary depending on our clients’ business needs from year to year. Due to these and other factors, our operating results have fluctuated significantly from quarter to quarter and from year to year. These fluctuations are likely to continue in the future, and operating results for any period may not be indicative of our future performance in any future period.

A significant portion of our revenues are fixed amounts according to our sales and service contracts. If we fail to accurately estimate costs and determine resource requirements in relation to our projects, our margins and profitability could be materially and adversely affected.

A significant portion of the ERP software development and ongoing service revenues we generate are fixed amounts according to our sales contracts or bids we submit. Our projects often involve complex technologies and must often be completed within compressed timeframes and meet increasingly sophisticated client requirements. We may be unable to accurately assess the time and resources required for completing projects and price our projects accordingly. If we underestimate the time or resources required we may experience cost overruns and mismatches in project staffing. Conversely, if we over estimate requirements, our bids may become uncompetitive and we may lose business as a result. Furthermore, any failure to complete a project within the stipulated timeframe could expose us to contractual and other liabilities and damage our reputation.

Our financial performance is directly related to our ability to adapt to technological change and evolving standards when developing and improving our ERP software products.

The ERP software industry is subject to rapid technological change, changing customer requirements, frequent new product introductions and evolving industry standards that may render existing software obsolete. In particular, improved access to high-speed Internet and wireless networks may affect the ERP software industry in the near future. In addition, as the Chinese economy has only recently begun to incorporate various Western economic factors, ERP systems have only recently been adopted by Chinese businesses. As a result, our position in the Chinese ERP industry could be eroded rapidly by the speed with which Chinese businesses continue to adopt Western business practices and technological advancements that we do not embrace. The life cycles of our software are difficult to estimate. Our software products must keep pace with technological developments, conform to evolving industry standards and address the increasingly sophisticated needs of our customers. In particular, we believe that we must continue to respond quickly to users’ needs for broad functionality. To the extent we are unable to develop and introduce products in a timely manner, we believe that our customers and potential customers will obtain products from our competitors promptly and our sales will correspondingly suffer. See “Our Business - Pansoft Solutions - Internet-based ERP for SMEs.”

We are substantially dependent upon our key personnel, particularly Hugh Wang, our Chairman, Guoqiang Lin, our Chief Executive Officer, and Allen Zhang, our Vice President of Finance.

Our performance is substantially dependent on the performance of our executive officers and key employees. In particular, the services of:

| · | Hugh Wang, our Chairman, |

| · | Guoqiang Lin, our Chief Executive Officer, and |

| · | Allen Zhang, our Vice President of Finance. |

would be difficult to replace. We do not have in place “key person” life insurance policies on any of our employees. The loss of the services of any of our executive officers or other key employees could substantially impair our ability to successfully implement our existing business strategy and develop new programs and enhancements.

As a software-oriented business, our ability to operate profitably is directly related to our ability to develop and protect our proprietary technology.

We rely on a combination of trademark, trade secret, nondisclosure and copyright law to protect our ERP software, which may afford only limited protection. Although the Chinese government has issued us 4 copyrights on our software, we cannot guarantee that competitors will be unable to develop technologies that are similar or superior to our technology. Despite our efforts to protect our proprietary rights, unauthorized parties, including customers and consultants, may attempt to reverse engineer or copy aspects of our software products or to obtain and use information that we regard proprietary. Although we are currently unaware of any unauthorized use of our technology, in the future, we cannot guarantee that others will not use our technology without proper authorization.

We develop our software products on third-party middleware software programs that are licensed by our customers from third parties, generally on a non-exclusive basis. Because we believe that there are a number of widely available middleware programs available (including, among others, IBM Websphare, Oracle DBMS, and Sybase DBMS), we do not currently anticipate that we will experience difficulties obtaining these programs. The termination of any such licenses, or the failure of the third-party licensors to adequately maintain or update their products, could result in delay in our ability to develop certain of our products while we seek to implement technology offered by alternative sources. Nonetheless, while it may be necessary or desirable in the future to obtain other licenses, there can be no assurance that they will be able to do so on commercially reasonable terms or at all.

Although some of our software is standalone software, much of our software is built as an add-on to software developed by other companies. In particular, the following software is an add-on to software developed by SAP:

| · | group accounting software (also may be used independently from SAP) |

| · | general reporting system |

| · | heterogeneous data exchange platform software |

| · | planning and statistics software |

The following software is an add-on to software developed by Oracle:

| · | business intelligence software |

| · | heterogeneous data exchange platform software |

In the future, we may develop software that relies on these and other third parties’ software. There can be no guarantee that our software will be completely compatible with these third-parties’ software or that these third parties will not develop functionally similar software that integrates more efficiently with their own software platforms.

In the future, we may receive notices claiming that we are infringing the proprietary rights of third parties. While we believe that we do not infringe and have not infringed upon the rights of others, we cannot guarantee that we will not become the subject of infringement claims or legal proceedings by third parties with respect to our current programs or future software developments. In addition, we may initiate claims or litigation against third parties for infringement of our proprietary rights or to establish the validity of our proprietary rights. Any such claims could be time consuming, result in costly litigation, cause product shipment delays or force us to enter into royalty or license agreements rather than dispute the merits of such claims, thereby impairing our financial performance by requiring us to pay additional royalties and/or license fees to third parties. See “Our Business - Pansoft Solutions - Internet-based ERP for SMEs” “- Pansoft Solutions - Oil and Gas Industry” and “-Proprietary Rights.”

We may not pay dividends.

Although we previously paid a single cash dividend in 2006, we do not currently anticipate paying any dividends on our ordinary shares. Although we have historically been a profitable enterprise, we cannot assure you that our operations will continue to result in sufficient revenues to enable us to operate at profitable levels or to generate positive cash flows. Furthermore, there is no assurance that our Board of Directors will declare dividends even if we are profitable. Dividend policy is subject to the discretion of our Board of Directors and will depend on, among other things, our future earnings, financial condition, capital requirements and other factors. Under British Virgin Islands law, we may only pay dividends from surplus (the excess, if any, at the time of the determination of the total assets of our company over the sum of our liabilities, as shown in our books of account, plus our capital), and we must be solvent before and after the dividend payment in the sense that we will be able to satisfy our liabilities as they become due in the ordinary course of business; and the realizable value of assets of our company will not be less than the sum of our total liabilities, other than deferred taxes as shown on our books of account, and our capital. If we determine to pay dividends on any of our ordinary shares in the future, as a holding company, we will be dependent on receipt of funds from our operating subsidiary, PJCL. See “Dividend Policy.”

Foreign Operational Risks

We may become a passive foreign investment company, which could result in adverse U.S. tax consequences to U.S. investors.

Based upon the nature of our business activities, we may be classified as a passive foreign investment company, or PFIC, by the U.S. Internal Revenue Service, or IRS, for U.S. federal income tax purposes. Such characterization could result in adverse U.S. tax consequences to you if you are a U.S. investor. For example, if we are a PFIC, a U.S. investor will become subject to burdensome reporting requirements. The determination of whether or not we are a PFIC is made on an annual basis and will depend on the composition of our income and assets from time to time. Specifically, we will be classified as a PFIC for U.S. tax purposes if either:

| · | 75% or more of our gross income in a taxable year is passive income; or |

| · | the average percentage of our assets by value in a taxable year which produce or are held for the production of passive income (which includes cash) is at least 50%. |

The calculation of the value of our assets is based, in part, on the then market value of our ordinary shares, which is subject to change. In addition, the composition of our income and assets will be affected by how, and how quickly, we spend the cash we raise in this offering. We cannot assure you that we will not be a PFIC for any taxable year. See “Taxation - United States Federal Income Taxation - Passive Foreign Investment Company.”

You may face difficulties in protecting your interests, and your ability to protect your rights through the U.S. federal courts may be limited, because we are incorporated under British Virgin Islands law, conduct substantially all of our operations in China and all of our officers and directors reside outside the United States.

We are incorporated and registered in the British Virgin Islands, and conduct substantially all of our operations in China through our wholly owned subsidiary in China, PJCL. All of our officers and directors reside outside the United States and some or all of the assets of those persons are located outside of the United States. As a result, it may be difficult or impossible for you to bring an original action against us or against these individuals in a British Virgin Islands or China court in the event that you believe that your rights have been infringed under the U.S. federal securities laws or otherwise. Even if you are successful in bringing an action of this kind, the laws of the British Virgin Islands and of China may render you unable to enforce a judgment against our assets or the assets of our directors and officers. There is no statutory recognition in the British Virgin Islands of judgments obtained in the United States, although the courts of the British Virgin Islands will generally recognize and enforce a non-penal judgment of a foreign court of competent jurisdiction without retrial on the merits. For more information regarding the relevant laws of the British Virgin Islands and China, see “Enforceability of Civil Liabilities.”

Our corporate affairs are governed by our memorandum and articles of association and by the Companies Law and the common law of the British Virgin Islands. The rights of shareholders to take legal action against our directors and us, actions by minority shareholders and the fiduciary responsibilities of our directors to us under British Virgin Islands law are to a large extent governed by the common law of the British Virgin Islands. The common law of the British Virgin Islands is derived in part from comparatively limited judicial precedent in the British Virgin Islands as well as from English common law, which has persuasive, but not binding, authority on a court in the British Virgin Islands. The rights of our shareholders and the fiduciary responsibilities of our directors under British Virgin Islands law are not as clearly established as they would be under statutes or judicial precedents in the United States. In particular, the British Virgin Islands has no securities laws as compared to the United States, and provides a lower level of protection to investors. In addition, British Virgin Islands companies may not have standing to initiate a shareholder derivative action before the federal courts of the United States.

As a result of all of the above, our public shareholders may have more difficulty in protecting their interests through actions against our management, directors or major shareholders than would shareholders of a corporation incorporated in a jurisdiction in the United States.

A slowdown in the Chinese economy or an increase in its inflation rate may slow down our growth and profitability.

The Chinese economy has grown at an approximately 9 percent rate for more than 25 years, making it the fastest growing major economy in recorded history. In 2007, China’s economy grew by 11.4%, the fastest pace in 11 years. In particular, China’s software industry has grown dramatically in the last year, with software products increasing by 24.1%, system integration increasing by 18.5%, software technology services increasing by 23.9% and embedded system software increasing by 24.5% in the first eight months of 2007 over the first eight months of 2006, according to China’s MII.

While China’s economy has grown, inflation has also recently become a major issue of concern. On March 18, 2007, China’s central bank, the People’s Bank of China, announced that the bank reserve ratio would rise half a percentage point to 15.5 percent from March 25, in an effort to reduce inflation pressures hours after Premier Wen Jiabao highlighted inflation as a major concern for the government. China’s consumer price index growth rate reached 8.7% year over year in 2008.

We cannot assure you that growth of the Chinese economy will be steady, that inflation will be controllable or that any slowdown in the economy or uncontrolled inflation will not have a negative effect on our business. Several years ago, the Chinese economy experienced deflation, which may recur in the future. More recently, the Chinese government announced its intention to continuously use macroeconomic tools and regulations to slow the rate of growth of the Chinese economy, the results of which are difficult to predict. Adverse changes in the Chinese economy will likely impact the financial performance of a variety of industries in China that use or would be candidates to use our products. If such adverse changes were to occur, our customers and potential customers could reduce spending on our products and services. See “Our Business - Background of the Chinese Software Industry.”

We do not have business interruption, litigation or natural disaster insurance.

The insurance industry in China is still at an early state of development. In particular PRC insurance companies offer limited business products. As a result, we do not have any business liability or disruption insurance coverage for our operations in China. Any business interruption, litigation or natural disaster may result in our business incurring substantial costs and the diversion of resources.

Any recurrence of severe acute respiratory syndrome, or SARS, pandemic avian influenza or another widespread public health problem, could adversely affect the Chinese economy as a whole, the software development industry in general and our ability to profitably provide services.

A renewed outbreak of SARS, pandemic avian influenza or another widespread public health problem in China, where we earn most of our revenues, could have a negative effect on our operations. Our operations may be affected by a number of health-related factors, including the following:

| · | quarantines or closures of some or our offices or the companies for which we provide services, which would severely disrupt our operations; |

| · | the sickness or death of our key officers and employees; and |

| · | a general slowdown in the Chinese economy. |

The possible quarantine of our offices or the sickness or death of our key officers and employees would restrict our ability to develop our software solutions. Any of the foregoing events or other unforeseen consequences of public health problems could adversely affect our markets or our ability to operate profitably.

Uncertainties with respect to the PRC legal system could adversely affect us.

There are substantial uncertainties regarding the interpretation and application of PRC laws and regulations, including, but not limited to, the laws and regulations governing our business, or the enforcement and performance of our contractual arrangements with our customers.

We conduct our business primarily through PJCL, which is generally subject to laws and regulations applicable to foreign investment in China and, in particular, laws applicable to wholly foreign-owned enterprises. We and PJCL are considered foreign persons or foreign invested enterprises controlled by PRC citizens under PRC law. As a result, we and PJCL are subject to PRC law limitations on foreign ownership of Chinese companies. These laws and regulations are relatively new and may be subject to change, and their official interpretation and enforcement may involve substantial uncertainty. The effectiveness of newly enacted laws, regulations or amendments may be delayed, resulting in detrimental reliance by foreign investors. New laws and regulations that affect existing and proposed future businesses may also be applied retroactively.

In addition, we depend on a variety of development, purchase and service agreements in the operation of our business. Almost all of these agreements are governed by PRC law. The PRC legal system is based on written statutes. Prior court decisions may be cited for reference but have limited precedential value. Since 1979, PRC legislation and regulations have significantly enhanced the protections afforded to various forms of foreign investments in China. However, since the PRC legal system continues to rapidly evolve, the interpretations of many laws, regulations and rules are not always uniform and enforcement of these laws, regulations and rules involve uncertainties, which may limit legal protections available to us. In addition, any litigation in China may be protracted and result in substantial costs and diversion of resources and management attention.

The PRC government has broad discretion in dealing with violations of laws and regulations, including levying fines, revoking business and other licenses and requiring actions necessary for compliance. In particular, licenses and permits issued or granted to us by relevant governmental bodies may be revoked at a later time by higher regulatory bodies. We cannot predict the effect of the interpretation of existing or new PRC laws or regulations on our businesses. We cannot assure you that our current ownership and operating structure would not be found in violation of any current or future PRC laws or regulations. As a result, we may be subject to sanctions, including fines, and could be required to restructure our operations or cease to provide certain services. Any of these or similar actions could significantly disrupt our business operations or restrict us from conducting a substantial portion of our business operations, which could materially and adversely affect our business, financial condition and results of operations. See “Our Business - Background of the Chinese Software Industry.”

PRC laws on overseas listings of PRC businesses are uncertain and may in the future require approval from and filing with PRC government agencies.

Within the last five years, the PRC government has, on several occasions, amended its regulations relating to overseas listings of PRC businesses. Most recently, on August 8, 2006, six PRC regulatory agencies, including the Ministry of Commerce, the State Administration for Industry and Commerce, CSRC and SAFE, jointly issued the Regulations on Mergers and Acquisitions of Domestic Enterprises by Foreign Investors. This regulation became effective on September 8, 2006 and includes provisions that purport to require offshore special purpose vehicles:

| (i) | controlled directly or indirectly by PRC companies or citizens; and |

| (ii) | formed for the purpose of effecting an overseas listing of a PRC company |

to obtain the approval of CSRC prior to the completion of the overseas listing. On September 8, 2006, CSRC published procedures regarding the approval process associated with overseas listings of special purpose vehicles. There is little precedent as to how CSRC will interpret the new regulation and apply the related procedures.

We completed the formation of our offshore holding company structure prior to the implementation of the new regulation. Further, given that these new regulations are not retroactive in nature, we are not currently required to seek and obtain governmental approval to complete the offering contemplated hereby. The PRC government, however, could alter its interpretations of the regulation at any time. To the extent the PRC government alters its current practice of remaining silent regarding overseas listings of PRC businesses like ours, we may be required to seek additional government approval to complete this offering, and we cannot guarantee that we would obtain such approval.

Governmental control of currency conversion may affect the value of your investment.

The PRC government imposes controls on the convertibility of the Renminbi into foreign currencies and, in certain cases, the remittance of currency out of China. We receive the majority of our revenues in Renminbi. Shortages in the availability of foreign currency may restrict the ability of our subsidiary, PJCL. to remit sufficient foreign currency to pay dividends or other payments to us, or otherwise satisfy its foreign currency denominated obligations. Under existing PRC foreign exchange regulations, payments of current account items, including profit distributions, interest payments and expenditures from trade-related transactions, can be made in foreign currencies without prior approval from the PRC State Administration of Foreign Exchange by complying with certain procedural requirements. However, approval from appropriate government authorities is required where Renminbi is to be converted into foreign currency and remitted out of China to pay capital expenses such as the repayment of bank loans denominated in foreign currencies. The PRC government may also at its discretion restrict access in the future to foreign currencies for current account transactions. If the foreign exchange control system prevents us from obtaining sufficient foreign currency to satisfy our currency demands, we may not be able to pay dividends, if any, in foreign currencies to our shareholders.

Fluctuation in the value of the Renminbi may have a material adverse effect on your investment.

The value of the Renminbi against the U.S. dollar and other currencies may fluctuate and is affected by, among other things, changes in political and economic conditions. On July 21, 2005, the PRC government changed its decade-old policy of pegging the value of the Renminbi to the U.S. dollar. Under the new policy, the Renminbi is permitted to fluctuate within a narrow and managed band against a basket of certain foreign currencies. This change in policy has resulted in an appreciation of the Renminbi against the U.S. dollar. While the international reaction to the Renminbi revaluation has generally been positive, there remains significant international pressure on the PRC government to adopt an even more flexible currency policy, which could result in a further and more significant appreciation of the Renminbi against the U.S. dollar. Any significant revaluation of Renminbi may materially and adversely affect our cash flows, revenues, earnings and financial position, and the value of, and any dividends payable on, our ordinary shares in U.S. dollars. For example, an appreciation of Renminbi against the U.S. dollar would make any new Renminbi denominated investments or expenditures more costly to us, to the extent that we need to convert U.S. dollars into Renminbi for such purposes. See “Exchange Rate Information.”

Our business benefits from certain government incentives. Expiration, reduction or discontinuation of, or changes to, these incentives will increase our tax burden and reduce our net income.