Table of Contents

Filed Pursuant to Rule 424(b)(3)

Registration No. 333-270749, 333-270749-01, 333-270749-02, 333-270749-03

PROSPECTUS

WARNERMEDIA HOLDINGS, INC.

Offer to Exchange

$1,750,000,000 Outstanding 3.428% Senior Notes due 2024

for

$1,750,000,000 Registered 3.428% Senior Notes due 2024

$500,000,000 Outstanding 3.528% Senior Notes due 2024

for

$500,000,000 Registered 3.528% Senior Notes due 2024

$1,750,000,000 Outstanding 3.638% Senior Notes due 2025

for

$1,750,000,000 Registered 3.638% Senior Notes due 2025

$500,000,000 Outstanding 3.788% Senior Notes due 2025

for

$500,000,000 Registered 3.788% Senior Notes due 2025

$4,000,000,000 Outstanding 3.755% Senior Notes due 2027

for

$4,000,000,000 Registered 3.755% Senior Notes due 2027

$1,500,000,000 Outstanding 4.054% Senior Notes due 2029

for

$1,500,000,000 Registered 4.054% Senior Notes due 2029

$5,000,000,000 Outstanding 4.279% Senior Notes due 2032

for

$5,000,000,000 Registered 4.279% Senior Notes due 2032

$4,500,000,000 Outstanding 5.050% Senior Notes due 2042

for

$4,500,000,000 Registered 5.050% Senior Notes due 2042

$7,000,000,000 Outstanding 5.141% Senior Notes due 2052

for

$7,000,000,000 Registered 5.141% Senior Notes due 2052

$3,000,000,000 Outstanding 5.391% Senior Notes due 2062

for

$3,000,000,000 Registered 5.391% Senior Notes due 2062

$500,000,000 Outstanding Floating Rate Senior Notes due 2024

for

$500,000,000 Registered Floating Rate Senior Notes due 2024

WarnerMedia Holdings, Inc. (formerly known as Magallanes, Inc.) is offering to exchange (the “exchange offer”) (i) $1,750,000,000 aggregate principal amount of its outstanding 3.428% Senior Notes due 2024 (the “Old 2024 Senior Notes”) for a like principal amount of registered 3.428% Senior Notes due 2024 (the “New 2024 Senior Notes”), (ii) $500,000,000 aggregate principal amount of its outstanding 3.528% Senior Notes due 2024 (the “Old 2024 NC1 Senior Notes”) for a like principal amount of registered 3.528% Senior Notes due 2024 (the “New 2024 NC1 Senior Notes”), (iii) $1,750,000,000 aggregate principal amount of its outstanding 3.638% Senior Notes due 2025 (the “Old 2025 Senior Notes”) for a like principal amount of registered 3.638% Senior Notes due 2025 (the “New 2025 Senior Notes”), (iv) $500,000,000 aggregate principal amount of its outstanding 3.788% Senior Notes due 2025 (the “Old 2025 NC1 Senior Notes”) for a like principal amount of registered 3.788% Senior Notes due 2025 (the “New 2025 NC1 Senior Notes”), (v) $4,000,000,000 aggregate principal amount of its outstanding 3.755% Senior Notes due 2027 (the “Old 2027 Senior Notes”) for a like principal amount of registered 3.755% Senior Notes due 2027 (the “New 2027 Senior Notes”), (vi) $1,500,000,000 aggregate principal amount of its outstanding 4.054% Senior Notes due 2029 (the “Old 2029 Senior Notes”) for a like principal amount of registered 4.054% Senior Notes due 2029 (the “New 2029 Senior Notes”), (vii) $5,000,000,000 aggregate principal amount of its outstanding 4.279% Senior Notes due 2032 (the “Old 2032 Senior Notes”) for a like principal amount of registered 4.279% Senior Notes due 2032 (the “New 2032 Senior Notes”), (viii) $4,500,000,000 aggregate principal amount of its outstanding 5.050% Senior Notes due 2042 (the “Old 2042 Senior Notes”) for a like principal amount of registered 5.050% Senior Notes due 2042 (the “New 2042 Senior Notes”), (ix) $7,000,000,000 aggregate principal amount of its outstanding 5.141% Senior Notes due 2052 (the “Old 2052 Senior Notes”) for a like principal amount of registered 5.141% Senior Notes due 2052 (the “New 2052 Senior Notes”), (x) $3,000,000,000 aggregate principal amount of its outstanding 5.391% Senior Notes due 2062 (the “Old 2062 Senior Notes”) for a like principal amount of registered 5.391% Senior Notes due 2062 (the “New 2062 Senior Notes”), and (xi) $500,000,000 aggregate principal amount of its outstanding Floating Rate Senior Notes due 2024 (the “Old Floating Rate Senior Notes”, and, together with the Old 2024 Senior Notes, the Old 2024 NC1 Senior Notes, the Old 2025 Senior Notes, the Old 2025 NC1 Senior Notes, the Old 2027 Senior Notes, the Old 2029 Senior Notes, the Old 2032 Senior Notes, the Old 2042 Senior Notes, the Old 2052 Senior Notes and the Old 2062 Senior Notes, the “Old Notes”) for a like principal amount of registered Floating Rate Senior Notes due 2024 (the “New Floating Rate Senior Notes” and, together with the New 2024 Senior Notes, the New 2024 NC1 Senior Notes, the New 2025 Senior Notes, the New 2025 NC1 Senior Notes, the New 2027 Senior Notes, the New 2029 Senior Notes, the New 2032 Senior Notes, the New 2042 Senior Notes, the New 2052 Senior Notes and the New 2062 Senior Notes, the “New Notes”). As used herein, the term “Notes” shall mean the New Notes together with the Old Notes.

The terms of the New Notes are identical in all material respects to the terms of the Old Notes of the corresponding series, except that the New Notes are registered under the Securities Act of 1933, as amended (the “Securities Act”), and will not contain restrictions on transfer or provisions relating to additional interest, will bear different CUSIP numbers from the Old Notes of the corresponding series and will not entitle their holders to registration rights. The New Notes will be fully, unconditionally, jointly and severally guaranteed on an unsecured unsubordinated basis by the same entities that guarantee the Old Notes. Each guarantee constitutes a separate security that is being offered by the relevant guarantor.

The Notes will not be listed on any securities exchange or any automated dealer quotation system and there is currently no public market for the Old Notes or for the New Notes.

All untendered Old Notes will continue to be subject to the restrictions on transfer set forth in the Old Notes and in the indenture governing the Notes. In general, the Old Notes may not be offered or sold unless registered under the Securities Act, except pursuant to an exemption from, or in a transaction not subject to, registration under the Securities Act. Other than in connection with the exchange offer, the Issuer does not currently anticipate that it will register any series of the Old Notes under the Securities Act.

The exchange offer will expire at 5:00 p.m., New York City time, on April 28, 2023 (the “Expiration Date”) unless we extend the Expiration Date. You should read the section called “The Exchange Offer” for further information on how to exchange your Old Notes for New Notes.

See “Risk Factors” beginning on page 17 for a discussion of risk factors that you should consider prior to tendering your Old Notes in the exchange offer and risk factors related to ownership of the Notes.

Each broker-dealer that receives New Notes for its own account pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of such New Notes. The letter of transmittal states that by so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an “underwriter” within the meaning of the Securities Act. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of New Notes received in exchange for Old Notes where such Old Notes were acquired by such broker-dealer as a result of market-making activities or other trading activities. We have agreed that, for a period ending on the earlier of (i) 120 days from the date on which this registration statement is declared effective and (ii) the date on which no broker-dealer is required to deliver a prospectus in connection with market-making or other trading activities, we will make this prospectus available to any broker-dealer for use in connection with any such resale. See “Plan of Distribution.”

Neither the U.S. Securities and Exchange Commission (“SEC”) nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is March 31, 2023

Table of Contents

| 1 | ||||

| 17 | ||||

| 26 | ||||

| 28 | ||||

| 30 | ||||

| 39 | ||||

| 40 | ||||

| 63 | ||||

| 65 | ||||

| 67 | ||||

| 68 | ||||

| 69 | ||||

| 70 | ||||

| 71 | ||||

| 72 |

You should rely only on the information contained in, or incorporated by reference into, this prospectus or to which we have referred you. We have not authorized anyone to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. This prospectus does not constitute an offer to sell, or a solicitation of an offer to purchase, the securities offered by this prospectus in any jurisdiction to or from any person to whom or from whom it is unlawful to make such offer or solicitation of an offer in such jurisdiction. You should not assume that the information contained in this prospectus is accurate as of any date other than the date of this prospectus. Also, you should not assume that there has been no change in the affairs of Warner Bros. Discovery, Inc. and its subsidiaries since the date of this prospectus. Any information incorporated by reference herein is accurate only as of the date of the document incorporated by reference.

This prospectus incorporates important business and financial information about us that is not included in or delivered with this prospectus. See “Where You Can Find More Information” and “Incorporation of Certain Information by Reference.” You may request a copy of any document incorporated by reference in this prospectus at no cost by calling us at (212) 548-5555 or writing us at the following address:

Warner Bros. Discovery, Inc.

230 Park Avenue South

New York, New York 10003

Attention: Investor Relations

If you would like to request copies of these documents, please do so by April 21, 2023 (which is five business days before the scheduled expiration of the exchange offer) in order to receive them before the expiration of the exchange offer.

Table of Contents

This summary highlights selected information contained elsewhere in this prospectus or the documents incorporated by reference in this prospectus. Because this is only a summary, it does not contain all of the information that you should consider in making your investment decision. You should read the following summary together with the entire prospectus, including the more detailed information regarding our company and the New Notes being exchanged in this offering appearing elsewhere in this prospectus or the documents incorporated by reference in this prospectus. You should also carefully consider, among other things, the matters discussed in the sections entitled “Risk Factors” in this prospectus or the documents incorporated by reference in this prospectus, and the consolidated financial statements and the related notes incorporated by reference in this prospectus, before deciding to invest in the Notes.

Except as the context otherwise requires, or as otherwise specified or used in this prospectus, (1) the terms “we,” “our,” “us,” “the Issuer” and “WMH” refer to WarnerMedia Holdings, Inc. (formerly known as Magallanes, Inc.) together with its subsidiaries; (2) the terms “WBD” or “the Parent Guarantor” refer to Warner Bros. Discovery, Inc. (formerly known as Discovery, Inc.), together with its subsidiaries; (3) the term “DCL” refers to Discovery Communications, LLC and (4) the term “Scripps” refers to Scripps Networks Interactive, Inc.

Warner Bros. Discovery, Inc.

On April 8, 2022 (the “Merger Closing Date”), Discovery, Inc. (“Discovery”) completed the Merger (as defined below) in which it acquired the business, operations and activities that constituted the WarnerMedia segment of AT&T Inc. (“AT&T”), subject to certain exceptions (the “WarnerMedia Business”) and changed its name from “Discovery, Inc.” to “Warner Bros. Discovery, Inc.”

On the Merger Closing Date, WBD and AT&T completed the transactions contemplated by (1) the Separation and Distribution Agreement, dated as of May 17, 2021 (as amended, the “Separation Agreement”), by and among AT&T, Magallanes, Inc. (“Spinco”) and Discovery, (2) that certain Agreement and Plan of Merger, dated as of May 17, 2021 (as amended, the “Merger Agreement”), by and among Discovery, Drake Subsidiary, Inc. (“Merger Sub”), AT&T and Spinco and (3) certain other agreements in connection with the transactions contemplated by the Merger Agreement and the Separation Agreement. Specifically, (1) AT&T transferred the WarnerMedia Business to Spinco, subject to certain exceptions as set forth in the Separation Agreement (the “Separation”), (2) thereafter, on the Merger Closing Date, AT&T distributed to its stockholders all of the shares of common stock, par value $0.01 per share, of Spinco (“Spinco common stock”) held by AT&T by way of a pro rata dividend such that each holder of shares of common stock, par value $1.00 per share, of AT&T (“AT&T common stock”) was entitled to receive one share of Spinco common stock for each share of AT&T common stock held as of the record date, April 5, 2022 (the “Distribution”), and (3) following the Distribution, Merger Sub merged with and into Spinco, with Spinco surviving as a wholly owned subsidiary of WBD (the “Merger” and together with the Separation and the Distribution, the “WarnerMedia Transactions”). Spinco was subsequently renamed “WarnerMedia Holdings, Inc.” Pursuant to the Merger Agreement, at the effective time of the Merger, each issued and outstanding share of Spinco common stock on the Merger Closing Date was automatically converted into the right to receive 0.241917 shares of WBD Series A common stock (“WBD common stock”).

WBD is a premier global media and entertainment company that combines the WarnerMedia Business’s premium entertainment, sports and news assets with Discovery’s leading non-fiction and international entertainment and sports businesses, thus offering audiences a differentiated portfolio of content, brands and franchises across television, film, streaming and gaming. Some of its iconic brands and franchises include Warner Bros. Pictures Group, Warner Bros. Television Group, DC, HBO, HBO Max, Discovery Channel,

1

Table of Contents

discovery+, CNN, HGTV, Food Network, TNT, TBS, TLC, OWN, Warner Bros. Games, Batman, Superman, Wonder Woman, Harry Potter, Looney Tunes, Hanna-Barbera, Game of Thrones, and The Lord of the Rings.

WBD is home to a powerful creative engine and one of the largest collections of owned content in the world and has one of the strongest hands in the industry in terms of the completeness and quality of assets and intellectual property across sports, news, lifestyle, and entertainment in virtually every region of the globe and in most languages. Additionally, WBD serves audiences and consumers around the world with content that informs, entertains, and, when at its best, inspires.

WBD’s asset mix positions it to drive a balanced approach to creating long-term value for shareholders. It represents the full entertainment eco-system, and the ability to serve consumers across the entire spectrum of offerings from domestic and international networks, premium pay-TV, streaming, production and release of feature films and original series, related consumer products and themed experience licensing, and interactive gaming.

WBD generates revenue from the sale of advertising on its networks and digital platforms (advertising revenue); fees charged to distributors that carry its network brands and programming, including cable, direct-to-home satellite, telecommunication and digital service providers, as well as through direct-to-consumer subscription services (distribution revenue); the release of feature films for initial exhibition in theaters, the licensing of feature films and television programs to various television, subscription video on demand and other digital markets, distribution of feature films and television programs in the physical and digital home entertainment market, sales of console games and mobile in-game content, sublicensing of sports rights, and licensing of intellectual property such as characters and brands (content revenue); and other sources such as studio tours and production services (other revenue).

The WBD common stock trades on the Nasdaq Global Select Market under the symbol “WBD”. Its principal executive offices are located at 230 Park Avenue South, New York, NY, 10003, and the telephone number is (212) 548-5555.

Discovery Communications, LLC

DCL is an indirect, wholly-owned subsidiary of WBD. DCL includes WBD’s Discovery Channel and TLC networks in the U.S. DCL is a Delaware limited liability company. Its principal executive offices are located at 230 Park Avenue South, New York, NY, 10003, and the telephone number is (212) 548-5555.

Scripps Networks Interactive, Inc.

Scripps is a direct, wholly-owned subsidiary of WBD. Certain of WBD’s operations, including Food Network and HGTV, are conducted through Scripps. Scripps is an Ohio corporation. Its principal executive offices are located at 230 Park Avenue South, New York, NY, 10003, and the telephone number is (212) 548-5555.

WarnerMedia Holdings, Inc.

WMH is a direct, wholly-owned subsidiary of WBD. WMH, which was originally named Magallanes, Inc., was organized specifically for the purpose of effecting the WarnerMedia Transactions. The WarnerMedia Business is conducted through WMH and its subsidiaries. Its principal executive offices are located at 230 Park Avenue South, New York, NY, 10003, and the telephone number is (212) 548-5555.

Recent Developments

On March 10, 2023, WMH completed its registered offering (the “3NC1 Senior Notes Offering”) of $1,500,000,000 aggregate principal amount of its 6.412% Senior Notes due 2026 (the “3NC1 Senior Notes”).

2

Table of Contents

The 3NC1 Senior Notes were issued pursuant to an indenture, dated as of March 10, 2023 (the “WMH Indenture”), among WMH, WBD and U.S. Bank Trust Company, National Association, as trustee (the “Trustee”), as supplemented by a supplemental indenture, dated as of March 10, 2023 (the “Supplemental Indenture” and, together with the WMH Indenture, the “3NC1 Indenture”), among WMH, WBD, DCL, Scripps and the Trustee. The 3NC1 Indenture contains certain covenants, events of default and other customary provisions. The 3NC1 Senior Notes are fully and unconditionally guaranteed on a senior unsecured basis by WBD, DCL and Scripps. WMH used the net proceeds from the 3NC1 Senior Notes Offering, together with available cash, to repay $1,500,000,000 of the borrowings outstanding under its Term Loan Facility (as defined herein) (the “Term Loan Repayment”).

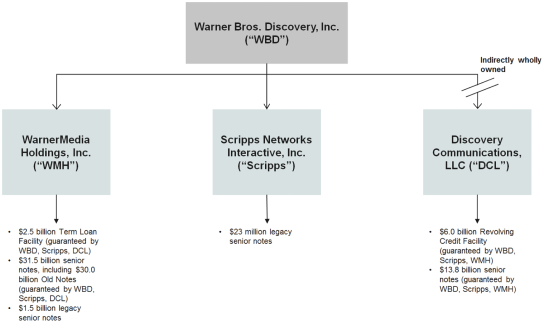

Debt Securities and Guarantee Structure

Set forth below is a diagram that graphically illustrates, in simplified form, the corporate debt and guarantee structure of WBD as of December 31, 2022, adjusted to give effect to the 3NC1 Senior Notes Offering and the Term Loan Repayment.

3

Table of Contents

Summary of the Terms of the Exchange Offer

Background | On March 15, 2022, WMH issued and privately placed, in each case pursuant to exemptions from the registration requirements of the Securities Act: |

| (i) $1,750,000,000 aggregate principal amount of its Old 2024 Senior Notes, |

| (ii) $500,000,000 aggregate principal amount of its Old 2024 NC1 Senior Notes, |

| (iii) $1,750,000,000 aggregate principal amount of its Old 2025 Senior Notes, |

| (iv) $500,000,000 aggregate principal amount of its Old 2025 NC1 Senior Notes, |

| (v) $4,000,000,000 aggregate principal amount of its Old 2027 Senior Notes, |

| (vi) $1,500,000,000 aggregate principal amount of its Old 2029 Senior Notes, |

| (vii) $5,000,000,000 aggregate principal amount of its Old 2032 Senior Notes, |

| (viii) $4,500,000,000 aggregate principal amount of its Old 2042 Senior Notes, |

| (ix) $7,000,000,000 aggregate principal amount of its Old 2052 Senior Notes, |

| (x) $3,000,000,000 aggregate principal amount of its Old 2062 Senior Notes, and |

| (xi) $500,000,000 aggregate principal amount of its Old Floating Rate Senior Notes. |

| In connection with the issuance of the Old Notes, WMH entered into a registration rights agreement, dated as of March 15, 2022 (as supplemented by the Counterpart to Registration Rights Agreement, dated as of April 8, 2022, the “Registration Rights Agreement”), with J.P. Morgan Securities LLC and Goldman Sachs & Co. LLC, as representatives of the initial purchasers of the Old Notes. Pursuant to the Registration Rights Agreement, WMH, WBD, DCL and Scripps have agreed, among other things, to consummate the exchange offer. |

The Notes | The terms of the New Notes will be identical in all material respects to the terms of the Old Notes, except that the New Notes will be |

4

Table of Contents

registered under the Securities Act and will not be subject to restrictions on transfer or contain provisions relating to additional interest, will bear different CUSIP and ISIN numbers than the Old Notes, will not entitle their holders to registration rights and will be subject to terms relating to book-entry procedures and administrative terms relating to transfers that differ from those of the Old Notes. |

| When we use the term “2024 Senior Notes” in this prospectus, the related discussion applies to both the Old 2024 Senior Notes and the New 2024 Senior Notes. |

| When we use the term “2024 NC1 Senior Notes” in this prospectus, the related discussion applies to both the Old 2024 NC1 Senior Notes and the New 2024 NC1 Senior Notes. |

| When we use the term “2025 Senior Notes” in this prospectus, the related discussion applies to both the Old 2025 Senior Notes and the New 2025 Senior Notes. |

| When we use the term “2025 NC1 Senior Notes” in this prospectus, the related discussion applies to both the Old 2025 NC1 Senior Notes and the New 2025 NC1 Senior Notes. |

| When we use the term “2027 Senior Notes” in this prospectus, the related discussion applies to both the Old 2027 Senior Notes and the New 2027 Senior Notes. |

| When we use the term “2029 Senior Notes” in this prospectus, the related discussion applies to both the Old 2029 Senior Notes and the New 2029 Senior Notes. |

| When we use the term “2032 Senior Notes” in this prospectus, the related discussion applies to both the Old 2032 Senior Notes and the New 2032 Senior Notes. |

| When we use the term “2042 Senior Notes” in this prospectus, the related discussion applies to both the Old 2042 Senior Notes and the New 2042 Senior Notes. |

| When we use the term “2052 Senior Notes” in this prospectus, the related discussion applies to both the Old 2052 Senior Notes and the New 2052 Senior Notes. |

| When we use the term “2062 Senior Notes” in this prospectus, the related discussion applies to both the Old 2062 Senior Notes and the New 2062 Senior Notes. |

| When we use the term “Floating Rate Senior Notes” in this prospectus, the related discussion applies to both the Old Floating Rate Senior Notes and the New Floating Rate Senior Notes. |

5

Table of Contents

| When we use the term “Notes” in this prospectus, the related discussion applies to both the Old Notes and the New Notes. |

| CUSIPs and ISINs for the Old Notes and the New Notes are set forth below: |

Series | Old Note | Old Note | Old Note ISIN | Old Note ISIN | New Note | New Note | ||||||

2024 Senior Notes | 55903V AC7 | U55632 AB6 | US55903VAC72 | USU55632AB67 | 55903V AW3 | US55903VAW37 | ||||||

2024 NC1 Senior Notes | 55903V AB9 | U55632 AK6 | US55903VAB99 | USU55632AK66 | 55903V AV5 | US55903VAV53 | ||||||

2025 Senior Notes | 55903V AE3 | U55632 AC4 | US55903VAE39 | USU55632AC41 | 55903V AZ6 | US55903VAZ67 | ||||||

2025 NC1 Senior Notes | 55903V AU7 | U55632 AL4 | US55903VAU70 | USU55632AL40 | 55903V AY9 | US55903VAY92 | ||||||

2027 Senior Notes | 55903V AG8 | U55632 AD2 | US55903VAG86 | USU55632AD24 | 55903V BA0 | US55903VBA08 | ||||||

2029 Senior Notes | 55903V AJ2 | U55632 AE0 | US55903VAJ26 | USU55632AE07 | 55903V BB8 | US55903VBB80 | ||||||

2032 Senior Notes | 55903V AL7 | U55632 AF7 | US55903VAL71 | USU55632AF71 | 55903V BC6 | US55903VBC63 | ||||||

2042 Senior Notes | 55903V AN3 | U55632 AG5 | US55903VAN38 | USU55632AG54 | 55903V BD4 | US55903VBD47 | ||||||

2052 Senior Notes | 55903V AQ6 | U55632 AH3 | US55903VAQ68 | USU55632AH38 | 55903V BE2 | US55903VBE20 | ||||||

2062 Senior Notes | 55903V AS2 | U55632 AJ9 | US55903VAS25 | USU55632AJ93 | 55903V BF9 | US55903VBF94 | ||||||

Floating Rate Senior Notes | 55903V AA1 | U55632 AA8 | US55903VAA17 | USU55632AA84 | 55903V AX1 | US55903VAX10 |

The Exchange Offer | We are offering to exchange Old Notes of each series for a like principal amount of New Notes of the corresponding series. The consummation of the exchange offer is not conditioned upon any minimum or maximum aggregate principal amount of Old Notes being tendered for exchange. |

Resale of New Notes | We believe the New Notes that will be issued in the exchange offer may be resold by most investors without compliance with the registration and prospectus delivery provisions of the Securities Act, subject to certain conditions. Each broker-dealer that receives New Notes for its own account in exchange for Old Notes, where such Old Notes were acquired by such broker-dealer as a result of market-making activities or other trading activities, must acknowledge that it will deliver a prospectus in connection with any resale of such New Notes. You should read the discussions under “The Exchange Offer” and “Plan of Distribution” for further information regarding the exchange offer and resale of the New Notes. |

Registration Rights Agreement | We are undertaking the exchange offer pursuant to the terms of the Registration Rights Agreement. Under the Registration Rights Agreement, WMH, WBD, DCL and Scripps agreed, among other things, to consummate an exchange offer for the Old Notes pursuant to an effective registration statement or to cause resales of the Old Notes to be registered. We have filed this registration statement to meet our obligations under the Registration Rights Agreement. If we fail to satisfy certain obligations under the Registration Rights Agreement, we would be required to pay additional interest to holders of the Old Notes under specified circumstances. See “Exchange Offer; Registration Rights.” |

6

Table of Contents

Consequences of Failure to Exchange the Old Notes | If we complete the exchange offer and you do not participate in it, then: |

| • | your Old Notes will continue to be subject to the existing restrictions upon their transfer; |

| • | certain interest rate provisions will no longer apply to your Old Notes; |

| • | we will have no further obligation to provide for the registration under the Securities Act of those Old Notes except under certain limited circumstances; and |

| • | the liquidity of the market for your Old Notes could be adversely affected. |

| See “The Exchange Offer—Terms of the Exchange Offer; Period for Tendering Old Notes.” |

Denominations of New Notes | Tendering holders of Old Notes must tender Old Notes in minimum denominations of $2,000 and integral multiples of $1,000 in excess thereof. New Notes will be issued in minimum denominations of $2,000 and integral multiples of $1,000 in excess thereof. |

Expiration Date | The exchange offer will expire at 5:00 p.m., New York City time, on April 28, 2023 (the “Expiration Date”), unless we extend it, in which case Expiration Date means the latest date and time to which the exchange offer is extended. |

Interest on the New Notes | The New Notes of each series will accrue interest from the most recent date to which interest has been paid or provided for on the Old Notes of the corresponding series. Any Old Notes not exchanged will remain outstanding and continue to accrue interest according to their terms. |

Conditions to the Exchange Offer | The exchange offer is subject to customary conditions. We will not be required to accept for exchange, or to issue any New Notes in exchange for, any Old Notes, and we may terminate or amend the exchange offer with respect to one or more series of Notes, if we determine in our reasonable judgment at any time before the Expiration Date that the exchange offer would violate applicable law or any applicable interpretation of the staff of the SEC. The foregoing condition is for our sole benefit and may be waived by us at any time. In addition, we will not accept for exchange any Old Notes tendered, and no New Notes will be issued in exchange for any such Old Notes, if at any time any stop order is threatened or in effect with respect to: |

| • | the registration statement of which this prospectus constitutes a part; or |

| • | the qualification of the indenture under the Trust Indenture Act of 1939, as amended (the “Trust Indenture Act”). |

7

Table of Contents

| See “The Exchange Offer—Conditions to the Exchange Offer.” We reserve the right to terminate or amend the exchange offer at any time prior to the Expiration Date upon the occurrence of any of the foregoing events. If we make a material change to the terms of the exchange offer, we will, to the extent required by law, disseminate additional offer materials and extend the exchange offer. |

Procedures for Tendering Old Notes | If you hold Old Notes through The Depository Trust Company (“DTC”) and wish to participate in the exchange offer, you must follow the automatic tender offer program (“ATOP”) procedures established by DTC for tendering the Old Notes that are held in book-entry form. The ATOP procedures require (i) that the Exchange Agent (as defined below) receive, prior to the expiration date of the exchange offer, a computer-generated message known as an “agent’s message” that is transmitted through ATOP and (ii) that DTC confirm that: |

| • | DTC has received the instructions to exchange your Old Notes; and |

| • | you agree to be bound by the terms of the letter of transmittal. |

| See “The Exchange Offer—Procedures for Tendering Old Notes.” |

Guaranteed Delivery Procedures | If you wish to tender your Old Notes, but cannot properly do so prior to the Expiration Date, you may tender your Old Notes according to the guaranteed delivery procedures set forth under “The Exchange Offer—Guaranteed Delivery Procedures.” |

Withdrawal Rights | Tenders of Old Notes may be withdrawn at any time prior to 5:00 p.m., New York City time, on the Expiration Date. To withdraw a tender of Old Notes, a notice of withdrawal must be actually received by the Exchange Agent at its address set forth in “The Exchange Offer—Exchange Agent” prior to 5:00 p.m., New York City time, on the Expiration Date. See “The Exchange Offer—Withdrawal Rights.” |

Acceptance of Old Notes and Delivery of New Notes | Except in some circumstances, any and all Old Notes that are validly tendered in the exchange offer prior to 5:00 p.m., New York City time, on the Expiration Date will be accepted for exchange. The New Notes issued pursuant to the exchange offer will be delivered promptly after such acceptance. See “The Exchange Offer—Acceptance of Old Notes for Exchange; Delivery of New Notes.” |

Certain U.S. Federal Income Tax Considerations | We believe that the exchange of the Old Notes for the New Notes will not constitute a taxable exchange for U.S. federal income tax purposes. See “Material United States Federal Income Tax Considerations.” |

Use of Proceeds | We will not receive any cash proceeds from the issuance of the New Notes in this exchange offer. |

Exchange Agent | U.S. Bank Trust Company, National Association is serving as the Exchange Agent (the “Exchange Agent”). |

8

Table of Contents

Summary of the Terms of the Notes

The terms of the New Notes offered in the exchange offer are identical in all material respects to the Old Notes, except that the New Notes:

| • | are registered under the Securities Act and therefore will not be subject to restrictions on transfer; |

| • | will not be subject to provisions relating to additional interest; |

| • | will bear different CUSIP numbers and ISINs; |

| • | will not entitle their holders to registration rights; and |

| • | will be subject to terms relating to book-entry procedures and administrative terms relating to transfers that differ from those of the Old Notes. |

The following summary contains basic information about the Notes and is not intended to be complete. For a more detailed description of the Notes, please refer to the section entitled “Description of Notes” in this prospectus.

Issuer | WarnerMedia Holdings, Inc. |

Parent Guarantor | Warner Bros. Discovery, Inc. |

Subsidiary Guarantors | Each domestic subsidiary of the Parent Guarantor that is a borrower or that guarantees the payment of any debt under the Senior Credit Facilities or any Material Debt (both as defined herein). See “Description of Notes.” As of the date of issuance of the New Notes, the only Subsidiary Guarantors will be DCL and Scripps. |

Notes Offered | $1,750,000,000 aggregate principal amount of New 2024 Senior Notes. |

$500,000,000 aggregate principal amount of New 2024 NC1 Senior Notes.

$1,750,000,000 aggregate principal amount of New 2025 Senior Notes.

$500,000,000 aggregate principal amount of New 2025 NC1 Senior Notes.

$4,000,000,000 aggregate principal amount of New 2027 Senior Notes.

$1,500,000,000 aggregate principal amount of New 2029 Senior Notes.

$5,000,000,000 aggregate principal amount of New 2032 Senior Notes.

$4,500,000,000 aggregate principal amount of New 2042 Senior Notes.

9

Table of Contents

$7,000,000,000 aggregate principal amount of New 2052 Senior Notes.

$3,000,000,000 aggregate principal amount of New 2062 Senior Notes.

$500,000,000 aggregate principal amount of New Floating Rate Senior Notes.

Interest Rates; Interest Payment Dates; Maturity Date | Each series of New Notes will have the same interest rates, maturity dates and interest payment dates as the corresponding series of Old Notes for which they are being offered in exchange, as set forth below: |

Series | Stated | Interest Rates | Interest Payment | |||

2024 Senior Notes | March 15, 2024 | 3.428% per annum | March 15 and September 15 | |||

2024 NC1 Senior Notes | March 15, 2024 | 3.528% per annum | March 15 and September 15 | |||

2025 Senior Notes | March 15, 2025 | 3.638% per annum | March 15 and September 15 | |||

2025 NC1 Senior Notes | March 15, 2025 | 3.788% per annum | March 15 and September 15 | |||

2027 Senior Notes | March 15, 2027 | 3.755% per annum | March 15 and September 15 | |||

2029 Senior Notes | March 15, 2029 | 4.054% per annum | March 15 and September 15 | |||

2032 Senior Notes | March 15, 2032 | 4.279% per annum | March 15 and September 15 | |||

2042 Senior Notes | March 15, 2042 | 5.050% per annum | March 15 and September 15 | |||

2052 Senior Notes | March 15, 2052 | 5.141% per annum | March 15 and September 15 | |||

2062 Senior Notes | March 15, 2062 | 5.391% per annum | March 15 and September 15 | |||

Floating Rate Senior Notes | March 15, 2024 | Compounded SOFR plus 1.78% per annum | March 15, June 15, September 15 and December 15 |

| Each New Note will bear interest from the most recent interest payment date on which interest has been paid on the corresponding Old Note. Any Old Notes not exchanged will remain outstanding and continue to accrue interest according to their terms. Holders of Old Notes that are accepted for exchange will be deemed to have waived the right to receive any payment in respect of interest accrued from the date of the last interest payment date in respect of their Old Notes until the date of the issuance of the New Notes. |

| Consequently, holders of New Notes will receive the same interest payments that they would have received had they not exchanged their Old Notes in the exchange offer. No accrued but unpaid interest will be paid with respect to any Old Notes tendered and not validly withdrawn prior to the withdrawal deadline. |

10

Table of Contents

Ranking | The New Notes will be WMH’s senior unsecured obligations and will rank equally in right of payment to all of its existing and future senior unsecured debt and senior in right of payment to all of its future subordinated debt. The New Notes will be effectively subordinated to any of WMH’s future secured debt to the extent of the value of the assets securing such debt, and the New Notes will be structurally subordinated to the liabilities of WMH’s subsidiaries. |

| As of December 31, 2022, adjusted to give effect to the 3NC1 Senior Notes Offering and the Term Loan Repayment: |

| • | WMH’s outstanding indebtedness consisted of $30.0 billion aggregate principal amount of the Old Notes, $1.5 billion aggregate principal amount of the 3NC1 Senior Notes, $2.5 billion of borrowings under its Term Loan Facility, its guarantees of $13.8 billion aggregate principal amount of DCL’s senior debt securities and its guarantee of $0 billion of borrowings under DCL’s Revolving Credit Facility; |

| • | WMH had no secured indebtedness outstanding; and |

| • | WMH’s subsidiaries had $1.5 billion in aggregate principal amount of indebtedness outstanding. |

| See “Description of Notes” for definitions of the Term Loan Facility and the Revolving Credit Facility. |

Parent Guarantee | All payments on the New Notes, including principal and interest (and premium, if any), will be fully and unconditionally guaranteed on an unsecured and unsubordinated basis by the Parent Guarantor. See “Description of Notes—Guarantees—Guarantee by the Parent Guarantor.” |

| The Parent Guarantee of the New Notes will rank equally in right of payment with all of the Parent Guarantor’s existing and future senior debt and senior in right of payment to all of the Parent Guarantor’s future subordinated debt. The Parent Guarantee will be effectively subordinated to any of the Parent Guarantor’s future secured debt to the extent of the value of the assets securing such debt, and the Parent Guarantee will be structurally subordinated to the liabilities of the Parent Guarantor’s subsidiaries (other than WMH and the Subsidiary Guarantors). |

| As of December 31, 2022, adjusted to give effect to the 3NC1 Senior Notes Offering and the Term Loan Repayment: |

| • | the Parent Guarantor’s outstanding indebtedness consisted of its guarantees of $13.8 billion aggregate principal amount of DCL’s senior debt securities, its guarantees of $30.0 billion aggregate principal amount of the Old Notes, its guarantees of $1.5 billion aggregate principal amount of the 3NC1 Senior Notes, its |

11

Table of Contents

guarantee of $0 billion of borrowings under DCL’s Revolving Credit Facility and its guarantee of $2.5 billion of borrowings under WMH’s Term Loan Facility; |

| • | WBD had no secured indebtedness outstanding; and |

| • | the Parent Guarantor’s subsidiaries, other than DCL and Scripps as described under “—Subsidiary Guarantors,” and WMH and certain of its subsidiaries as described under “—Ranking,” had no indebtedness outstanding. |

| See “Description of Notes” for definitions of the Term Loan Facility and the Revolving Credit Facility. |

Subsidiary Guarantors | All payments on the New Notes, including principal and interest (and premium, if any), will be fully and unconditionally guaranteed on an unsecured and unsubordinated basis by each wholly-owned domestic subsidiary of the Parent Guarantor that is a borrower or that guarantees the payment of any debt under the Senior Credit Facilities or any Material Debt. Each such guarantee of the New Notes will rank equally in right of payment with all other existing and future unsecured and unsubordinated indebtedness of each such subsidiary guarantor. Each such guarantee will be effectively subordinated to each such subsidiary guarantor’s future secured indebtedness to the extent of the value of the assets securing that debt. |

| As of December 31, 2022, adjusted to give effect to the 3NC1 Senior Notes Offering and the Term Loan Repayment: |

| • | DCL’s outstanding indebtedness consisted of $13.8 billion of senior debt securities, $0 billion of borrowings under its Revolving Credit Facility, its guarantees of $30.0 billion aggregate principal amount of the Old Notes, its guarantees of $1.5 billion aggregate principal amount of the 3NC1 Senior Notes and its guarantee of $2.5 billion of borrowings under WMH’s Term Loan Facility; |

| • | DCL had available borrowing capacity of $6.0 billion of its Revolving Credit Facility; |

| • | Scripps’ outstanding indebtedness consisted of $23.0 million of senior notes issued by Scripps prior to the acquisition of Scripps by WBD, its guarantees of $30.0 billion aggregate principal amount of the Old Notes, its guarantees of $1.5 billion aggregate principal amount of the 3NC1 Senior Notes, its guarantees of $13.8 billion aggregate principal amount of DCL’s senior debt securities, its guarantee of $0 billion of borrowings under DCL’s Revolving Credit Facility and its guarantee of $2.5 billion of borrowings under WMH’s Term Loan Facility; |

| • | None of DCL’s or Scripps’ subsidiaries had any secured debt outstanding; and |

| • | None of DCL’s or Scripps’ subsidiaries had any indebtedness outstanding. |

12

Table of Contents

| See “Description of Notes” for definitions of the Term Loan Facility and the Revolving Credit Facility. |

| See “Risk Factors—Risks Related to the Notes—DCL and Scripps conduct a substantial amount of their operations, and WBD and the Issuer conduct substantially all of their respective operations, through subsidiaries. WBD, the Issuer, DCL and Scripps may be limited in their ability to access funds from their subsidiaries to service their debt, including the Notes and the note guarantees. In addition, the Notes will not be guaranteed, except in certain circumstances, by any subsidiaries of WBD other than DCL and Scripps and each other wholly owned domestic subsidiary of WBD that in the future becomes a borrower or that guarantees the payment of any debt under the Senior Credit Facilities or any Material Debt.” |

Optional Redemption | Each series of New Notes will have the same redemption terms as the corresponding series of Old Notes for which they are being offered in exchange, as set forth below: |

| Floating Rate Senior Notes: WMH will not have the option to redeem the Floating Rate Senior Notes, in whole or in part, prior to their maturity date. |

| 2024 Senior Notes: WMH may redeem the 2024 Senior Notes, in whole or in part, at any time prior to their maturity at a redemption price equal to 100% of the principal amount of the 2024 Senior Notes, plus a “make-whole” premium equal to the Adjusted Treasury Rate (as defined herein) plus 30 basis points, plus accrued and unpaid interest, if any, to, but excluding, the date of redemption. |

| 2024 NC1 Senior Notes: WMH may redeem the 2024 NC1 Senior Notes, in whole or in part, at any time prior to their maturity at a redemption price equal to 100% of the principal amount of the 2024 NC1 Senior Notes, plus accrued and unpaid interest, if any, to, but excluding, the date of redemption. |

| 2025 Senior Notes: WMH may redeem the 2025 Senior Notes, in whole or in part, at any time prior to their maturity at a redemption price equal to 100% of the principal amount of the 2025 Senior Notes, plus a “make-whole” premium equal to the Adjusted Treasury Rate plus 30 basis points, plus accrued and unpaid interest, if any, to, but excluding, the date of redemption. |

| 2025 NC1 Senior Notes: WMH may redeem the 2025 NC1 Senior Notes, in whole or in part, at any time prior to their maturity at a redemption price equal to 100% of the principal amount of the 2025 NC1 Senior Notes, plus accrued and unpaid interest, if any, to, but excluding, the date of redemption. |

13

Table of Contents

| 2027 Senior Notes: Prior to February 15, 2027, WMH may redeem the 2027 Notes, in whole or in part, at any time at a redemption price equal to 100% of the principal amount of the 2027 Senior Notes, plus a “make-whole” premium equal to the Adjusted Treasury Rate plus 30 basis points, plus accrued and unpaid interest, if any, to, but excluding, the date of redemption. On and after February 15, 2027, WMH may redeem the 2027 Senior Notes, in whole or in part, at any time prior to their maturity at a redemption price equal to 100% of the principal amount of the 2027 Senior Notes, plus accrued and unpaid interest, if any, to, but excluding, the date of redemption. |

| 2029 Senior Notes: Prior to January 15, 2029, WMH may redeem the 2029 Senior Notes, in whole or in part, at any time at a redemption price equal to 100% of the principal amount of the 2029 Senior Notes, plus a “make-whole” premium equal to the Adjusted Treasury Rate plus 35 basis points, plus accrued and unpaid interest, if any, to, but excluding, the date of redemption. On and after January 15, 2029, WMH may redeem the 2029 Senior Notes, in whole or in part, at any time prior to their maturity at a redemption price equal to 100% of the principal amount of the 2029 Senior Notes, plus accrued and unpaid interest, if any, to, but excluding, the date of redemption. |

2032 Senior Notes: WMH will not have the option to redeem the 2032 Notes prior to March 15, 2027. On and after March 15, 2027 and prior to December 15, 2031, WMH may redeem the 2032 Notes, in whole or in part, at any time at a redemption price equal to 100% of the principal amount of the 2032 Senior Notes, plus a “make-whole” premium equal to the Adjusted Treasury Rate plus 40 basis points, plus accrued and unpaid interest, if any, to, but excluding, the date of redemption. On and after December 15, 2031, WMH may redeem the 2032 Notes, in whole or in part, at any time prior to their maturity at a redemption price equal to 100% of the principal amount of the 2032 Senior Notes, plus accrued and unpaid interest, if any, to, but excluding, the date of redemption.

2042 Senior Notes: Prior to September 15, 2041, WMH may redeem the 2042 Senior Notes, in whole or in part, at any time at a redemption price equal to 100% of the principal amount of the 2042 Senior Notes, plus a “make-whole” premium equal to the Adjusted Treasury Rate plus 40 basis points, plus accrued and unpaid interest, if any, to, but excluding, the date of redemption. On and after September 15, 2041, WMH may redeem the 2042 Senior Notes, in whole or in part, at any time prior to their maturity at a redemption price equal to 100% of the principal amount of the 2042 Senior Notes, plus accrued and unpaid interest, if any, to, but excluding, the date of redemption.

2052 Senior Notes: WMH will not have the option to redeem the 2052 Senior Notes prior to March 15, 2027. On and after March 15, 2027 and prior to September 15, 2051, WMH may redeem the 2052

14

Table of Contents

Senior Notes, in whole or in part, at any time at a redemption price

equal to 100% of the principal amount of the 2052 Senior Notes, plus

a “make-whole” premium equal to the Adjusted Treasury Rate plus 45 basis points, plus accrued and unpaid interest, if any, to, but excluding, the date of redemption. On and after September 15, 2051, WMH may redeem the 2052 Senior Notes, in whole or in part, at any time prior to their maturity at a redemption price equal to 100% of the principal amount of the 2052 Senior Notes, plus accrued and unpaid interest, if any, to, but excluding, the date of redemption.

| 2062 Senior Notes: WMH will not have the option to redeem the 2062 Senior Notes prior to March 15, 2027. On and after March 15, 2027 and prior to September 15, 2061, WMH may redeem the 2062 Notes, in whole or in part, at any time at a redemption price equal to 100% of the principal amount of the 2062 Notes, plus a “make-whole” premium equal to the Adjusted Treasury Rate plus 50 basis points, plus accrued and unpaid interest, if any, to, but excluding, the date of redemption. On and after September 15, 2061, WMH may redeem the 2062 Senior Notes, in whole or in part, at any time prior to their maturity at a redemption price equal to 100% of the principal amount of the 2062 Senior Notes, plus accrued and unpaid interest, if any, to, but excluding, the date of redemption. |

| See “Description of Notes—Optional Redemption.” |

Change of Control Triggering Event | If a Change of Control Triggering Event occurs, WMH must offer to repurchase the Notes at a price equal to 101% of the principal amount of the Notes, plus accrued and unpaid interest, if any, to, but excluding, the date of repurchase. See “Description of Notes—Change of Control Offer to Repurchase.” |

Sinking Fund | None. |

Covenants | WMH will issue each series of the New Notes as a separate series of debt securities. Each series of New Notes will be issued under the senior indenture, dated as of March 15, 2022 (the “base indenture”), by and among WMH, AT&T and the trustee, as amended and supplemented by the first supplemental indenture, dated as of April 8, 2022 (the “first supplemental indenture”; the base indenture, as amended and supplemented by the first supplemental indenture is referred to herein as the “indenture”), by and among WMH, WBD, DCL, Scripps and the trustee. The indenture restricts, among other things WMH’s and its subsidiaries’ ability to: |

| • | incur liens; and |

| • | enter into sale and leaseback transactions. |

| If any Subsidiary Guarantor and its subsidiaries are subsidiaries of the Parent Guarantor but not subsidiaries of WMH, then such Subsidiary Guarantor and its subsidiaries are treated as if they were subsidiaries of WMH for all purposes under the indenture. |

15

Table of Contents

| In addition, the indenture limits WMH’s and WBD’s ability to consolidate or merge with or into another company, or sell all or substantially all of the assets of WMH or WBD, as applicable. |

Form and Denomination of Notes | The New Notes of each series will be issued in the form of one or more fully-registered global securities, without coupons, in denominations of $2,000 in principal amount and integral multiples of $1,000 in excess thereof. These global securities will be deposited with the trustee as custodian for, and registered in the name of, a nominee of DTC. Except in the limited circumstances described under “Book-Entry, Form and Delivery,” New Notes will not be issued in certificated form or exchanged for interests in global securities. |

Trustee, registrar and transfer agent | U.S. Bank Trust Company, National Association. |

Governing Law | The indenture and the Notes are governed by the laws of the State of New York. |

Further Issues | WMH may from time to time, without notice to or consent of the holders of the Notes, create and issue additional senior notes, which may include Notes of the same series as any series offered hereby, ranking equally and ratably with the Notes of such series offered hereby in all respects, provided that if such additional senior notes are not fungible with the original senior notes of such series for U.S. federal income tax purposes, such additional senior notes will have separate CUSIP numbers. |

Risk Factors | An investment in the New Notes offered in the exchange offer involves risk. Before making an investment decision, you should carefully consider the risks described in “Risk Factors,” as well as other information included or incorporated by reference into this prospectus, including the risk factors set forth in Warner Bros. Discovery’s Annual Report on Form 10-K for the year ended December 31, 2022 (the “2022 WBD Annual Report”). |

16

Table of Contents

Participating in the exchange offer and any investment in the Notes involves risks. You should carefully consider the following risks, as well as the other information contained or incorporated by reference in this prospectus, before making an investment decision. In particular, you should carefully consider the risks and uncertainties included in Item 1A, “Risk Factors,” of the 2022 WBD Annual Report which is incorporated by reference in this prospectus. For a discussion of additional uncertainties associated with forward-looking statements in this prospectus, see “Cautionary Note Regarding Forward-Looking Statements.” If any of those risks or the following risks actually occurs, WBD’s businesses, and your investment in the Notes, could be negatively affected. These risks and uncertainties are not the only ones we face. Additional risks and uncertainties not presently known to us, or that we currently deem immaterial, may also materially and adversely affect their business operations, results of operations, financial condition or prospects. If any of these risks materializes, our ability to pay interest on the Notes when due or to repay the Notes at maturity could be adversely affected, and the trading prices of the Notes could decline substantially.

Risks Related to the Exchange Offer

If you fail to exchange your Old Notes, they will continue to be restricted securities and may become less liquid.

Old Notes that you do not tender or WMH does not accept will, following the exchange offer, continue to be restricted securities, and may not be offered or sold except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act and applicable state securities laws.

If a large number of outstanding Old Notes are exchanged for New Notes issued in the exchange offer, we expect that the liquidity of the market for any Old Notes remaining after the completion of the exchange offer will be substantially limited. Any Old Notes tendered and exchanged in the exchange offer will reduce the aggregate principal amount of the Old Notes of the applicable series outstanding. Following the exchange offer, if you do not tender your Old Notes you generally will not have any further registration rights, and your Old Notes will continue to be subject to certain transfer restrictions. Accordingly, the liquidity of the market for the Old Notes could be adversely affected.

Late deliveries of Old Notes and other required documents could prevent a holder from exchanging its Old Notes.

Holders are responsible for complying with all exchange offer procedures. The issuance of New Notes in exchange for Old Notes will only occur upon completion of the procedures described in this prospectus under “The Exchange Offer.” Therefore, holders of Old Notes who wish to exchange them for New Notes should allow sufficient time for timely completion of the exchange offer procedures. Neither we nor the exchange agent are obligated to extend the offer or notify you of any failure to follow the proper procedures or waive any defect if you fail to follow the proper procedures.

If you are a broker-dealer, your ability to transfer the New Notes may be restricted.

A broker-dealer that purchased Old Notes for its own account as part of market-making or trading activities must comply with the prospectus delivery requirements of the Securities Act when it sells the New Notes. Our obligation to make this prospectus available to broker-dealers is limited. Consequently, we cannot guarantee that a proper prospectus will be available to broker-dealers wishing to resell their New Notes.

17

Table of Contents

Risks Related to the Notes

WBD has a significant amount of debt and may incur significant amounts of additional debt, which could adversely affect WBD’s financial health and its ability to react to changes in its business.

As of December 31, 2022, WBD had approximately $49.3 billion of consolidated debt, of which approximately $365 million was then current. WBD’s substantial level of indebtedness increases the possibility that it may be unable to generate cash sufficient to pay when due the principal of, interest on, or other amounts associated with its indebtedness. In addition, DCL and certain other subsidiaries of WBD had the ability to draw down $6.0 billion of the $6.0 billion Revolving Credit Facility (after giving effect to $0 million represented by outstanding letters of credit) in the ordinary course, which would have the effect of increasing its indebtedness. WBD is also permitted, subject to certain restrictions under its existing indebtedness, to obtain additional long-term debt and working capital lines of credit to meet future financing needs. This would have the effect of increasing WBD’s total leverage.

WBD’s substantial leverage could have significant negative consequences on its financial condition and results of operations, including:

| • | impairing its ability to meet one or more of the financial ratio covenants contained in its debt agreements or to generate cash sufficient to pay interest or principal, which could result in an acceleration of some or all of its outstanding debt in the event that an uncured default occurs; |

| • | increasing WBD’s vulnerability to general adverse economic and market conditions; |

| • | limiting WBD’s ability to obtain additional debt or equity financing; |

| • | requiring the dedication of a substantial portion of WBD’s cash flow from operations to service its debt, thereby reducing the amount of cash flow available for other purposes; |

| • | requiring WBD to sell debt or equity securities or to sell some of its core assets, possibly on unfavorable terms, to meet payment obligations; |

| • | limiting WBD’s flexibility in planning for, or reacting to, changes in its business and the markets in which it competes; and |

| • | placing WBD at a possible competitive disadvantage with less leveraged competitors and competitors that may have better access to capital resources. |

DCL and Scripps conduct a substantial amount of their operations, and WBD and the Issuer conduct substantially all of their respective operations, through subsidiaries. WBD, the Issuer, DCL and Scripps may be limited in their ability to access funds from their subsidiaries to service their debt, including the Notes and the note guarantees. In addition, the Notes will not be guaranteed, except in certain circumstances, by any subsidiaries of WBD other than DCL and Scripps and each other wholly owned domestic subsidiary of WBD that in the future becomes a borrower or that guarantees the payment of any debt under the Senior Credit Facilities or any Material Debt.

DCL and Scripps conduct a substantial amount of their operations, and WBD and the Issuer conduct substantially all of their respective operations, through subsidiaries. Accordingly, they depend on their subsidiaries’ earnings and advances or loans made by the subsidiaries to them (and potentially dividends or distributions by the subsidiaries to them) to provide funds necessary to meet their obligations, including the payments of principal, premium, if any, and interest on the Notes. If WBD, the Issuer, DCL and Scripps are unable to access the cash flows of their respective subsidiaries, they would be unable to meet their debt obligations.

The subsidiaries of WBD are separate and distinct legal entities and, except to the extent that they guarantee the Notes, have no obligation, contingent or otherwise, to pay any amounts due on the Notes or to make funds

18

Table of Contents

available to the Issuer to do so. In addition, the ability of the subsidiaries of WBD to pay dividends or otherwise transfer assets to WBD is subject to various restrictions under applicable law and limitations under contractual obligations. In the event of a bankruptcy, liquidation or reorganization of any of WBD’s subsidiaries, holders of their indebtedness and their trade creditors will generally be entitled to payment of their claims from the assets of those subsidiaries before any assets are made available for distribution to WBD. In addition, the indenture governing the Notes allows WBD to create new subsidiaries and invest in their subsidiaries, none of whose assets you will have any claim against, except to the extent that they guarantee the Notes. The Notes will be guaranteed on a senior unsecured basis by WBD and each wholly owned domestic subsidiary of WBD that is a borrower or that guarantees the payment of any debt under the Senior Credit Facilities or any Material Debt. There can be no assurance that any other future domestic subsidiary of WBD will guarantee indebtedness of DCL or the Issuer under the Senior Credit Facilities and, as a result, be required to guarantee the Notes. In the event that a future domestic subsidiary does guarantee the Notes as a result of its guaranteeing indebtedness of DCL or the Issuer under the Senior Credit Facilities, there also can be no assurance that such guarantee of the Senior Credit Facilities and, as a result, such guarantee of the Notes, will remain in place. There can be no assurance that DCL and Scripps will continue to guarantee the Senior Credit Facilities, and thus continue to be required to guarantee the Notes.

The Notes will be effectively subordinated to the Issuer’s and the guarantors’ future secured indebtedness to the extent of the value of the property securing that indebtedness.

The Notes will not be secured by any of the Issuer’s or the guarantors’ assets. As a result, the Notes and the note guarantees will be effectively subordinated to the Issuer’s and the guarantors’ future secured indebtedness with respect to the assets that secure that indebtedness. The effect of this subordination is that upon a default in payment on, or the acceleration of, any of the Issuer’s secured indebtedness, or in the event of bankruptcy, insolvency, liquidation, dissolution or reorganization of the Issuer or the guarantors, the proceeds from the sale of assets securing any secured indebtedness will be available to pay obligations on the Notes only after all such secured debt has been paid in full. As a result, the holders of the Notes may receive less, ratably, than the holders of secured debt in the event of the Issuer’s or the guarantors’ bankruptcy, insolvency, liquidation, dissolution or reorganization.

The Notes will be structurally subordinated to all obligations of WBD’s existing and future subsidiaries (other than the Issuer) that are not and do not become guarantors of the Notes.

The Notes will be guaranteed on a senior unsecured basis by WBD and each wholly owned domestic subsidiary of WBD that is a borrower or that guarantees the payment of any debt under the Senior Credit Facilities or any Material Debt. As of the date of issuance of the Notes, DCL and Scripps will guarantee the Notes. Except for such subsidiary guarantors of the Notes, WBD’s subsidiaries, including all of its non-domestic subsidiaries, will have no obligation, contingent or otherwise, to pay amounts due under the Notes or to make any funds available to pay those amounts, whether by dividend, distribution, loan or other payment. The Notes and note guarantees will be structurally subordinated to all indebtedness and other obligations of any non-guarantor subsidiary such that in the event of insolvency, liquidation, reorganization, dissolution or other winding up of any subsidiary that is not a guarantor, all of that subsidiary’s creditors (including trade creditors) would be entitled to payment in full out of that subsidiary’s assets before WBD or the Issuer would be entitled to any payment.

DCL and Scripps conduct a substantial amount of their operations, and WBD and the Issuer conduct substantially all of their respective operations, through subsidiaries. For the year ended December 31, 2022, on a pro forma basis after giving effect to the Merger, WBD’s subsidiaries other than the Issuer, DCL and Scripps represented approximately 95% of WBD’s consolidated revenues. As of December 31, 2022, WBD’s subsidiaries other than the Issuer, DCL and Scripps represented approximately 94% of WBD’s consolidated total assets and had approximately $35.4 billion of total liabilities, including trade payables but excluding intercompany liabilities.

19

Table of Contents

In addition, WBD’s subsidiaries that provide, or will provide, note guarantees will be automatically released from those note guarantees upon the occurrence of certain events. See “Description of Notes—Guarantees—Guarantee by Subsidiaries of the Parent Guarantor.”

If any note guarantee is released, no holder of the Notes will have a claim as a creditor against that subsidiary, and the indebtedness and other liabilities, including trade payables and preferred stock, if any, whether secured or unsecured, of that subsidiary will be effectively senior to the claim of any holders of the Notes.

Variable rate indebtedness subjects the Issuer and WBD to interest rate risk, which could cause their respective debt service obligations to increase significantly.

Borrowings under the Senior Credit Facilities and certain other indebtedness of the Issuer and WBD are at variable rates of interest and expose the Issuer and WBD to interest rate risk. As interest rates increase, the Issuer’s and WBD’s debt service obligations on their respective variable rate indebtedness increase even though the amount borrowed remains the same, and their respective net income and cash flows, including cash available for servicing their respective indebtedness, will correspondingly decrease.

The indenture governing the Notes does not restrict the ability of the Issuer, WBD or any of their respective subsidiaries to incur additional unsecured debt, pay dividends or make other distributions to holders of its equity securities or repurchase their respective securities or to take other actions that could negatively impact their ability to pay their obligations under the Notes or the note guarantees, respectively.

None of the Issuer, WBD or any of their respective subsidiaries will be restricted under the terms of the indenture governing the Notes from incurring additional unsecured debt, paying dividends or making other distributions to holders of its equity securities or repurchasing its respective securities. In addition, WBD will not be restricted under the terms of the indenture governing the Notes from incurring secured indebtedness or entering into sale and leaseback transactions, and the limited covenants applicable to the Notes will not require the Issuer, WBD or any of their respective subsidiaries to achieve or maintain any minimum financial results relating to their respective financial position or results of operations. The ability to recapitalize, incur additional debt and take a number of other actions that are not limited by the terms of the indenture governing the Notes could have the effect of diminishing the Issuer’s and the guarantors’ ability to make payments on the Notes or the note guarantees, respectively, when due.

The Issuer may not be able to repurchase all of the Notes upon a change of control triggering event, which would result in a default under the Notes.

Upon the occurrence of a Change of Control Triggering Event (as defined herein), unless the Issuer has exercised its right to redeem the Notes, each holder of the Notes will have the right to require the Issuer to repurchase all or any part of such holder’s Notes at a price equal to 101% of their principal amount, plus accrued and unpaid interest, if any, to, but excluding, the date of repurchase. If a Change of Control Triggering Event occurs, there can be no assurance that the Issuer would have sufficient financial resources available to satisfy its obligations to repurchase the Notes. In addition, the ability of the Issuer to repurchase the Notes for cash may be limited by law, or by the terms of other agreements relating to its indebtedness outstanding at that time. Any failure by the Issuer to repurchase the Notes as required under the indenture governing the Notes would result in a default under the indenture, which could have material adverse consequences for the Issuer and for holders of the Notes.

Holders of the Notes may not be able to determine when a change of control giving rise to their right to have the Notes repurchased has occurred following a sale of “substantially all” of WBD’s assets.

One of the circumstances under which a change of control may occur is upon the sale or disposition of “all or substantially all” of WBD’s assets. There is no precise established definition of the phrase “substantially all”

20

Table of Contents

under applicable law and the interpretation of that phrase will likely depend upon particular facts and circumstances. Accordingly, the ability of a holder of Notes to require WMH to repurchase its Notes as a result of a sale of less than all of WBD’s, to another person may be uncertain.

Changes in the Issuer’s and WBD’s credit ratings or the debt markets could adversely affect the trading prices of the Notes.

The trading prices for the Notes will depend on many factors, including:

| • | the Issuer’s and WBD’s credit ratings with major credit rating agencies; |

| • | the prevailing interest rates being paid by other companies similar to the Issuer and WBD; |

| • | the financial condition, financial performance and future prospects of the Issuer or WBD; and |

| • | the overall condition of the financial markets. |

The condition of the financial markets and prevailing interest rates have fluctuated significantly in the past and are likely to fluctuate in the future. Such fluctuations could have an adverse effect on the trading prices of the Notes.

In addition, credit rating agencies continually review their ratings for the companies that they follow, including the Issuer and WBD. A negative change in the rating of the Issuer or WBD could have an adverse effect on the trading prices of the Notes.

There may be no active trading market for the New Notes, and, if one develops, it may not be liquid.

The New Notes will constitute new issues of securities for which there is no established trading market. We do not intend to apply for listing of the Notes on any national securities exchange or for inclusion of the Notes on any automated dealer quotation system. A trading market for the Notes may not develop, or if a market for the Notes were to develop, the Notes may trade at a discount from their original offering prices, depending upon many factors, including prevailing interest rates, the market for similar securities, general economic conditions and our financial condition. There can be no assurance as to the development or liquidity of any market for the Notes, the ability of the holders to sell their Notes or the prices at which the holders would be able to sell their Notes.

Risks related to the Floating Rate Notes

The Floating Rate Notes bear additional risks.

The Floating Rate Notes will bear interest at a floating rate, and accordingly carry significant risks not associated with conventional fixed rate debt securities. These risks include fluctuation of the interest rates and the possibility that you will receive an amount of interest that is lower than expected. WMH has no control over a number of matters, including economic, financial and political events, which are important in determining the existence, magnitude and longevity of these risks and their results.

The Secured Overnight Financing Rate (“SOFR”) is a relatively new reference rate and its composition and characteristics are not the same as the London Inter-Bank Offered Rate (“LIBOR”).

On June 22, 2017, the Alternative Reference Rates Committee (“ARRC”) convened by the Board of Governors of the Federal Reserve System and the Federal Reserve Bank of New York identified the SOFR as the rate that, in the consensus view of the ARRC, represented best practice for use in certain new U.S. dollar derivatives and other financial contracts. SOFR is a broad measure of the cost of borrowing cash overnight collateralized by U.S. Treasury securities, and has been published by the Federal Reserve Bank of New York

21

Table of Contents

since April 2018. The Federal Reserve Bank of New York has also begun publishing historical indicative SOFR from 2014. Investors should not rely on any historical changes or trends in SOFR as an indicator of future changes in SOFR.

The composition and characteristics of SOFR are not the same as those of LIBOR, and SOFR is fundamentally different from LIBOR for two key reasons. First, SOFR is a secured rate, while LIBOR is an unsecured rate. Second, SOFR is an overnight rate, while LIBOR is a forward-looking rate that represents interbank funding over different maturities (e.g., three months). As a result, there can be no assurance that SOFR (including Compounded SOFR) will perform in the same way as LIBOR would have at any time, including, without limitation, as a result of changes in interest and yield rates in the market, market volatility or global or regional economic, financial, political, regulatory, judicial or other events.

SOFR may be more volatile than other benchmark or market rates.

Since the initial publication of SOFR, daily changes in SOFR have, on occasion, been more volatile than daily changes in other benchmark or market rates, such as U.S. dollar LIBOR. Although changes in Compounded SOFR generally are not expected to be as volatile as changes in daily levels of SOFR, the return on and value of the Floating Rate Notes may fluctuate more than floating rate debt securities that are linked to less volatile rates. In addition, the volatility of SOFR has reflected the underlying volatility of the overnight U.S. Treasury repo market. The Federal Reserve Bank of New York has at times conducted operations in the overnight U.S. Treasury repo market in order to help maintain the federal funds rate within a target range. There can be no assurance that the Federal Reserve Bank of New York will continue to conduct such operations in the future, and the duration and extent of any such operations is inherently uncertain. The effect of any such operations, or of the cessation of such operations to the extent they are commenced, is uncertain and could be materially adverse to investors in the Floating Rate Notes.

Any failure of SOFR to gain market acceptance could adversely affect the Floating Rate Notes.

According to the ARRC, SOFR was developed for use in certain U.S. dollar derivatives and other financial contracts as an alternative to U.S. dollar LIBOR in part because it is considered a good representation of general funding conditions in the overnight U.S. Treasury repurchase agreement market. However, as a rate based on transactions secured by U.S. Treasury securities, it does not measure bank-specific credit risk and, as a result, is less likely to correlate with the unsecured short-term funding costs of banks. This may mean that market participants would not consider SOFR a suitable replacement or successor for all of the purposes for which U.S. dollar LIBOR historically has been used (including, without limitation, as a representation of the unsecured short-term funding costs of banks), which may, in turn, lessen market acceptance of SOFR. Any failure of SOFR to gain market acceptance could adversely affect the return on and value of the Floating Rate Notes and the price at which investors can sell the Floating Rate Notes in the secondary market. In addition, some investors may be unwilling or unable to trade the Floating Rate Notes without changes to their information technology systems, both of which could adversely impact the liquidity and trading price of the Floating Rate Notes.

In addition, if SOFR does not prove to be widely used as a benchmark in securities that are similar or comparable to the Floating Rate Notes, the trading price of the Floating Rate Notes may be lower than those of securities that are linked to rates that are more widely used. Similarly, market terms for floating rate debt securities linked to SOFR, such as the spread over the base rate reflected in interest rate provisions or the manner of compounding the base rate, may evolve over time, and trading prices of the Floating Rate Notes may be lower than those of later-issued SOFR-based debt securities as a result. Investors in the Floating Rate Notes may not be able to sell the Floating Rate Notes at all or may not be able to sell the Floating Rate Notes at prices that will provide them with a yield comparable to similar investments that have a developed secondary market, and may consequently suffer from increased pricing volatility and market risk.

22

Table of Contents

The interest rate on the Floating Rate Notes is based on a Compounded SOFR rate and the SOFR Index, both of which are relatively new in the marketplace.

For each interest period (as defined herein), the interest rate on the Floating Rate Notes is based on Compounded SOFR, which is calculated using the SOFR Index (as defined herein) published by the Federal Reserve Bank of New York according to the specific formula described under “Description of Notes—Interest on the Floating Rate Notes—Compounded SOFR,” not the SOFR rate published on or in respect of a particular date during such interest period or an arithmetic average of SOFR rates during such period. For this and other reasons, the interest rate on the Floating Rate Notes during any interest period will not necessarily be the same as the interest rate on other SOFR-linked investments that use an alternative basis to determine the applicable interest rate. Further, if the SOFR rate in respect of a particular date during an interest period is negative, its contribution to the SOFR Index will be less than one, resulting in a reduction to Compounded SOFR used to calculate the interest payable on the Floating Rate Notes on the Floating Rate Interest Payment Date (as defined herein) for such interest period.