Exhibit 99.1

|

Sidoti Institutional Investor Forum

March 2013

|

Forward-Looking Statements

This presentation contains statements that constitute forward-looking statements. All statements other than statements of historical facts are forward-looking statements. These statements include but are not limited to descriptions regarding the intent, belief or current expectations of the Company or its officers with respect to the results of operations and financial condition.

Such forward-looking statements are not guarantees of future performance and involve known and unknown risks, uncertainties, and other factors, including those discussed under “Risk Factors” or elsewhere in the Company’s periodic filings with the Securities and Exchange Commission, that may cause actual results, performance or achievements to be materially different from those expressed or implied in the forward-looking statements as a result of various factors and assumptions.

The Company has no obligation and does not undertake to revise forward-looking statements to reflect future events or circumstances.

|

|

Our Mission

To cultivate a healthier, happier world by spreading oodness through nourishing foo honest words and conduct that is considerate and forever kind to the planet.

|

Leading Natural and Organic Brand

Products in 25,000+ Stores

Net Sales Operating Income

$ Millions

17% CAGR

FY08

$162 (1)

LTM 12/31/12

$ Millions

+$20MM

$1

FY08

$21 (2)

LTM 12/31/12

Mac & Cheese

Snack Crackers

Graham Crackers

Fruit Snacks

(1) Adjusted for reduction in Net Sales of $1.6MM due to voluntary pizza recall in Q3 FY13

(2) Adjusted for advisory agreement termination fee of $1.3MM in FY12, $0.7MM in costs incurred in connection with secondary public offering that closed on August 6, 2012 and $2.3MM impact on gross profit ($1.3MM impact on net income after giving effect to income taxes) due to the recall in Q3 FY13

|

Continued Significant Momentum in Our Business

Leveraging Market Trends

Consumers Focused On Eating Healthy

Gr for

Or cts

Driving Our Growth Strategy

Expand Improve Distribution Placement

Drive Increase Household Innovation Penetration

|

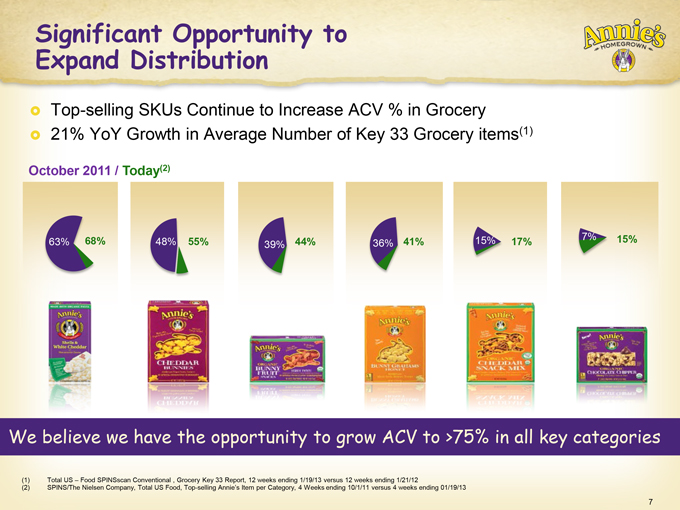

Significant Opportunity to Expand Distribution

Top-selling SKUs Continue to Increase ACV % in Grocery 21% YoY Growth in Average Number of Key 33 Grocery items(1)

October 2011 / Today(2)

63% 68%

48% 55%

36% 41%

15% 17%

7% 15%

We believe we have the opportunity to grow ACV to >75% in all key categories

(1) Total US – Food SPINSscan Conventional , Grocery Key 33 Report, 12 weeks ending 1/19/13 versus 12 weeks ending 1/21/12

(2) SPINS/The Nielsen Company, Total US Food, Top-selling Annie’s Item per Category, 4 Weeks ending 10/1/11 versus 4 weeks ending 01/19/13

|

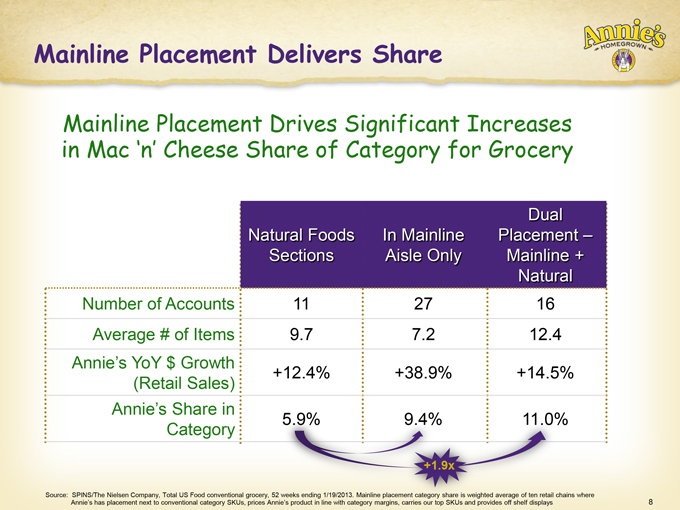

Mainline Placement Delivers Share

Mainline Placement Drives Significant Increases in Mac ‘n’ Cheese Share of Category for Grocery

Natural Foods Sections

In Mainline Aisle Only

Dual Placement – Mainline + Natural

Number of Accounts 11 27 16

Average # of Items 9.7 7.2 12.4

Annie’s YoY $ Growth

+12.4% +38.9% +14.5% (Retail Sales)

Annie’s Share in

5.9% 9.4% 11.0% Category

Source: SPINS/The Nielsen Company, Total US Food conventional grocery, 52 weeks ending 1/19/2013. Mainline placement category share is weighted average of ten retail chains where Annie’s has placement next to conventional category SKUs, prices Annie’s product in line with category margins, carries our top SKUs and provides off shelf displays

|

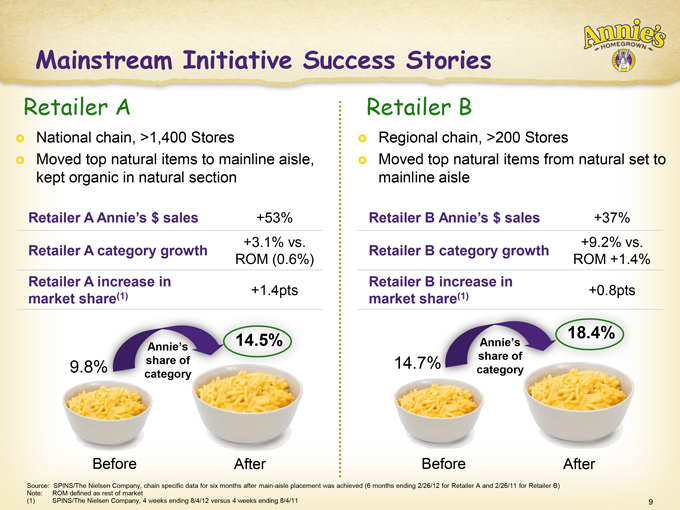

Mainstream Initiative Success Stories

Retailer A

£ National chain, >1,400 Stores

£ Moved top natural items to mainline aisle, kept organic in natural section

Retailer A Annie’s $ sales +53%

+3.1% vs.

Retailer A category growth

ROM (0.6%)

Retailer A increase in

(1) +1.4pts market share

9.8%

Annie’s share of category

Before After

Retailer B

Regional chain, >200 Stores

Moved top natural items from natural set to mainline aisle

Retailer B Annie’s $ sales +37%

Retailer B category growth +9.2% vs.

ROM +1.

Retailer B increase in

market share(1) +0.8pts

14.7%

Annie’s share of category

Before After

Source: SPINS/The Nielsen Company, chain specific data for six months after main-aisle placement was achieved (6 months ending 2/26/12 for Retailer A and 2/26/11 for Retailer B)

Note: ROM defined as rest of market

(1) SPINS/The Nielsen Company, 4 weeks ending 8/4/12 versus 4 weeks ending 8/4/11

|

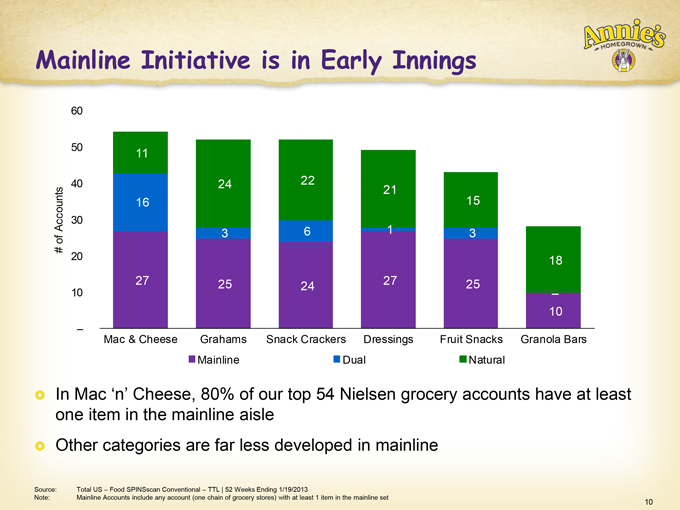

Mainline Initiative is in Early Innings

60

50

40 Accounts 30 of # 20

10

11 16

27

24

3 25

22

6 24

21

1 27

15

3 25

18

• 10

Mac & Cheese Grahams Snack Crackers Dressings Fruit Snacks Granola Bars Mainline Dual Natural

In Mac ‘n’ Cheese, 80% of our top 54 Nielsen grocery accounts have at least one item in the mainline aisle Other categories are far less developed in mainline

Source: Total US – Food SPINSscan Conventional – TTL | 52 Weeks Ending 1/19/2013

Note: Mainline Accounts include any account (one chain of grocery stores) with at least 1 item in the mainline set

|

Innovation Strategy

Optimization

Continually improve core lines to stay ahead of competition

~19% of Net Sales in FY2012 were from Products Introduced Since the Beginning of FY2010

|

Recent Introductions

Cheddar Squares

Organic Graham Crackers

Bernie’s

Farm M&C

Category Size $388 million(1)

Category Size $168 million(2)

Category Size $64 million(3)

(1) Category size based on square shaped cheddar crackers Nielsen US Food sales for 52 weeks ending 8/4/12 (2) Category size based on brick-style graham crackers Nielsen US Food sales for 52 weeks ended 1/19/13 (3) Category size based on Mac ‘n’ Cheese made with shaped pasta Nielsen US Food sale for 52 weeks ending 9/1/12

|

New Introduction: Deluxe Skillet Meals

8g Whole Grains

Made with Organic Pasta

100% Real rBST Free Cheese Deluxe Wet Cheese Pouch Format

No Artificial Flavors, Synthetic Colors or Preservatives

(1) Category size based on Nielsen US Food for 52 weeks ending 9/9/2012

|

Annie’s Frozen Strategy (“Frannie”)

Market Gap: All-family, natural/organic frozen that delivers on real

· Identified 7 initial “high-potential” frozen categories totaling

>$12B(1)

· Launched into >$4B frozen pizza category first(1)

· One additional category expected to launch in Q3 / Q4 FY2014

|

Frozen pizza Update

Pre-recall Trends

£ Achieved 14 ACV % in US Grocery and 47 ACV % in Natural channel(1) £ Strong and growing velocities

Pizza coming back on shelves now

£ Began shipping again on February 11th £ No lost distribution anticipated £ Broad March promotions designed to drive strong shelf execution at retail £ Additional spend to support re-launch in Q4 of FY13 and Q1 of FY14

(1) SPINS/The Nielsen Company, Total US Food, top-selling Annie’s item per category, 4 weeks ending 1/19/2013

|

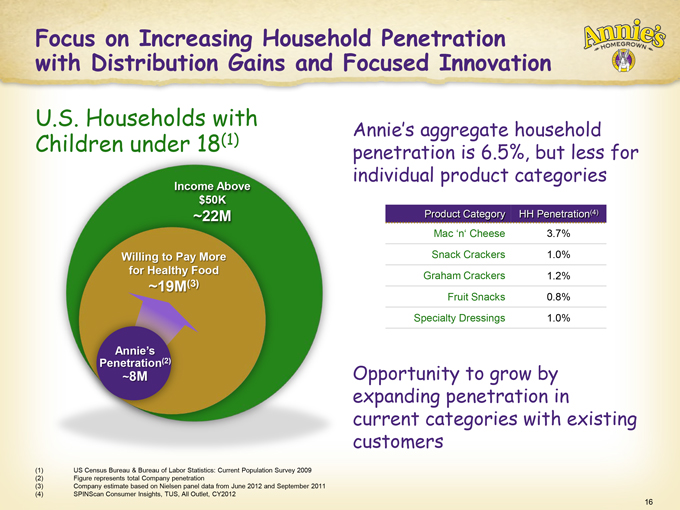

Focus on Increasing Household Penetration with Distribution Gains and Focused Innovation

U.S. Households with Children under 18(1)

Annie’s aggregate household penetration is 6.5%, but less for individual product categories

Income Above $50K

Willing to Pay More for Healthy Food

~19M(3)

Willing to Pay More for Healthy Food

~19M(3)

Opportunity to grow by expanding penetration in current categories with existing customers

(1) US Census Bureau & Bureau of Labor Statistics: Current Population Survey 2009 (2) Figure represents total Company penetration (3) Company estimate based on Nielsen panel data from June 2012 and September 2011 (4) SPINScan Consumer Insights, TUS, All Outlet, CY2012

|

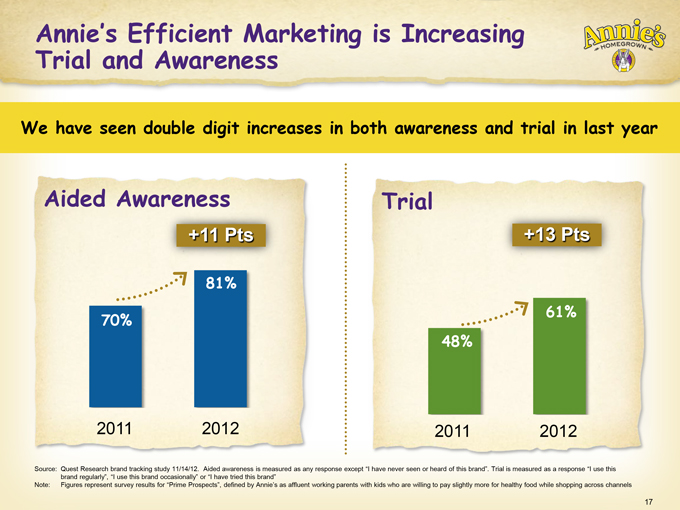

Annie’s Efficient Marketing is Increasing

Trial and Awareness

We have seen double digit increases in both awareness and trial in last year

Aided Awareness

+11 Pts

70%

2011

81%

2012

Trial

48%

61%

2011

2012

Source: Quest Research brand tracking study 11/14/12. Aided awareness is measured as any response except “I have never seen or heard of this brand”. Trial is measured as a response “I use this brand regularly”, “I use this brand occasionally” or “I have tried this brand” Note: Figures represent survey results for “Prime Prospects”, defined by Annie’s as affluent working parents with kids who are willing to pay slightly more for healthy food while shopping across channels

|

Financials

|

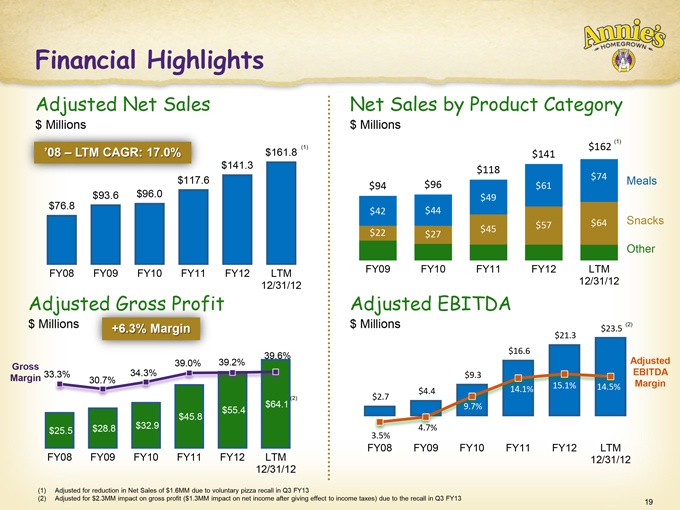

Financial Highlights

Adjusted Net Sales

$ Millions

‘08 – LTM CAGR: 17.0%

$76.8

$93.6

$96.0

$141.3

$161.8 (1)

FY08 FY09 FY10 FY11 FY12 LTM 12/31/12

Adjusted Gross Profit

$ Millions

+6.3% Margin

Gross Margin

33.3%

30.7%

39.0%

FY08 FY09 FY10 FY11 FY12 LTM 12/31/12

(1) Adjusted for reduction in Net Sales of $1.6MM due to voluntary pizza recall in Q3 FY13

(2) Adjusted for $2.3MM impact on gross profit ($1.3MM impact on net income after giving effect to income taxes) due to the recall in Q3 FY13

|

Quarterly Review

Adjusted Net Sales YoY Growth Sales

$ Millions % Growth

$46.7

$43.0 24.9% 24.7% (1)

$38.9 (1)

$36.6 $37.9 22.7%

$32.3 $34.3 20.4% 19.9% 20.1%

$29.3 $30.8 18.7% 17.5%

$28.6

$24.1 $24.7

$22.0 12.3%

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

FY10 FY11 FY12 FY13 FY11 FY12 FY13

Operating Profit Operating Margin

$ Millions % Margin

$7.1(3)

(2) 15.6% (3)

$6.1 $6.2 14.6% 14.3% (2) 15.1%

$5.3 (4)

$4.6 $4.8 $4.6(4) 11.5% 12.1% 10.5% 12.1%

$3.7 $3.6 8.7%

$3.3

$2.8

$2.1

$1.0

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

FY12 FY13 FY11 FY12 FY13

FY10 FY11

(1) Adjusted for reduction in Net Sales of $1.6MM due to voluntary pizza recall

(2) Adjusted for advisory agreement termination fee of $1.3MM

(3) Adjusted for secondary offering costs of $704k

(4) Adjusted for recall charges of $2.3MM 20

|

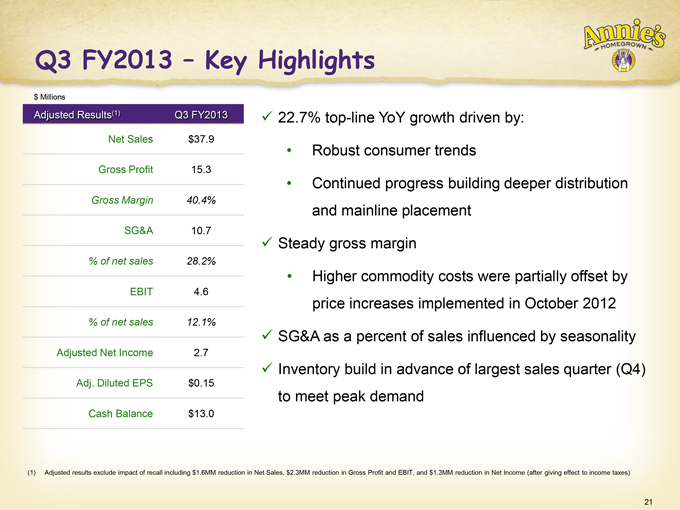

Q3 FY2013 – Key Highlights

$ Millions

Adjusted Results(1) Q3 FY2013 ü 22.7% top-line YoY growth driven by:

Net Sales $37.9

· Robust consumer trends

Gross Profit 15.3 Continued progress building deeper distribution

Gross Margin 40.4%

and mainline placement

SG&A 10.7

ü Steady gross margin

% of net sales 28.2%

· Higher commodity costs were partially offset by

EBIT 4.6

price increases implemented in October 2012

% of net sales 12.1% as a

ü SG&A percent of sales influenced by seasonality

Adjusted Net Income 2.7

ü Inventory build in advance of largest sales quarter (Q4)

Adj. Diluted EPS $0.15

to meet peak demand

Cash Balance $13.0

(1) Adjusted results exclude impact of recall including $1.6MM reduction in Net Sales, $2.3MM reduction in Gross Profit and EBIT, and $1.3MM reduction in Net Income (after giving effect to income taxes)

|

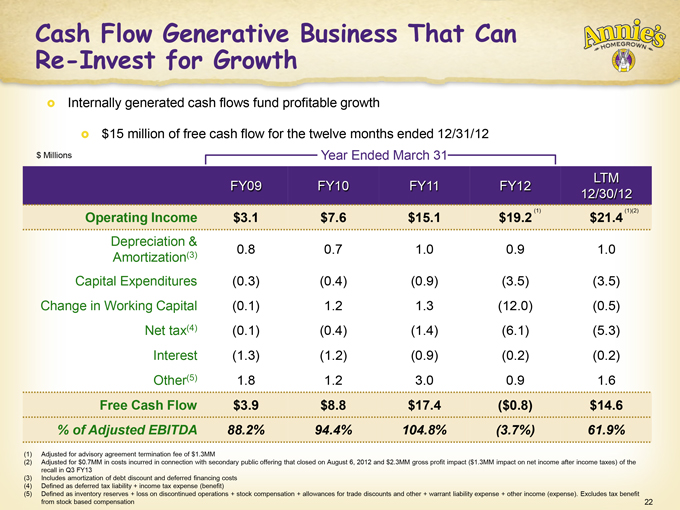

Cash Flow Generative Business That Can

Re-Invest for Growth

£ Internally generated cash flows fund profitable growth

£ $15 million of free cash flow for the twelve months ended 12/31/12

$ Millions Year Ended March 31

LTM

FY09 FY10 FY11 FY12

12/30/12

Operating Income $3.1 $7.6 $15.1 $19.2 (1) $21.4 (1)(2)

Depreciation &

(3) 0.8 0.7 1.0 0.9 1.0

Amortization

Capital Expenditures (0.3) (0.4) (0.9) (3.5) (3.5)

Change in Working Capital (0.1) 1.2 1.3 (12.0) (0.5)

Net tax(4) (0.1) (0.4) (1.4) (6.1) (5.3)

Interest (1.3) (1.2) (0.9) (0.2) (0.2)

Other(5) 1.8 1.2 3.0 0.9 1.6

Free Cash Flow $3.9 $8.8 $17.4 ($0.8) $14.6

% of Adjusted EBITDA 88.2% 94.4% 104.8% (3.7%) 61.9%

(1) Adjusted for advisory agreement termination fee of $1.3MM

(2) Adjusted for $0.7MM in costs incurred in connection with secondary public offering that closed on August 6, 2012 and $2.3MM gross profit impact ($1.3MM impact on net income after income taxes) of the

recall in Q3 FY13

(3) Includes amortization of debt discount and deferred financing costs

(4) Defined as deferred tax liability + income tax expense (benefit)

(5) Defined as inventory reserves + loss on discontinued operations + stock compensation + allowances for trade discounts and other + warrant liability expense + other income (expense). Excludes tax benefit

from stock based compensation 22

|

Investment Highlights

INDUSTRY PERFORMANCE

Natural and BRAND Excellent Growth FUTURE Organic – Trajectory Fast Growing Leading Brand Supported by Building on Food Category with Strong Efficient Model Growing Core Consumer Business and alty and Track Record ailer Appeal of Innovation

|

Appendix

|

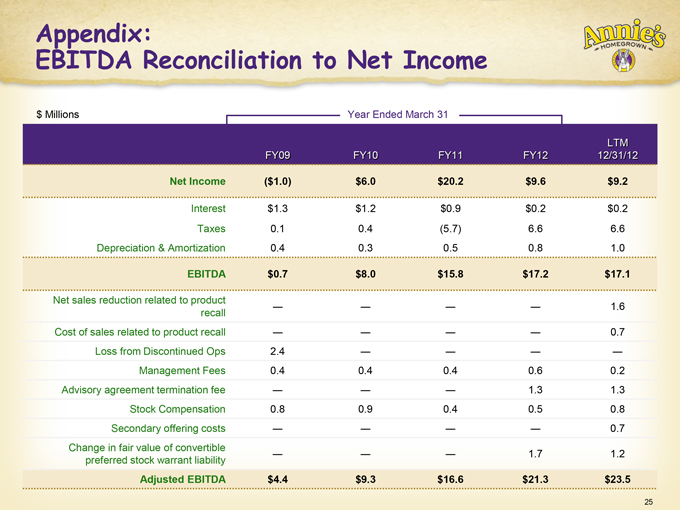

Appendix:

EBITDA Reconciliation to Net Income

$ Millions Year Ended March 31

LTM FY09 FY10 FY11 FY12 12/31/12

Net Income ($1.0) $6.0 $20.2 $9.6 $9.2

Interest $1.3 $1.2 $0.9 $0.2 $0.2 Taxes 0.1 0.4 (5.7) 6.6 6.6 Depreciation & Amortization 0.4 0.3 0.5 0.8 1.0

EBITDA $0.7 $8.0 $15.8 $17.2 $17.1

Net sales reduction related to product

¯ ¯ ¯ ¯ 1.6 recall Cost of sales related to product recall ¯ ¯ ¯ ¯ 0.7 Loss from Discontinued Ops 2.4 ¯ ¯ ¯ ¯ Management Fees 0.4 0.4 0.4 0.6 0.2 Advisory agreement termination fee ¯ ¯ ¯ 1.3 1.3 Stock Compensation 0.8 0.9 0.4 0.5 0.8 Secondary offering costs ¯ ¯ ¯ ¯ 0.7 Change in fair value of convertible

¯ ¯ ¯ 1.7 1.2 preferred stock warrant liability

Adjusted EBITDA $4.4 $9.3 $16.6 $21.3 $23.5

|

Thank You!