Exhibit 99.2

ANNUAL REPORT SANDSTORM GOLD ROYALTIES

SECTION 1 Company Profile 2021 Q4 A BRIGHTER WAY TO INVEST IN GOLDTM Corporate & Shareholder Information Stock Exchange Listings Toronto Stock Exchange TSX: SSL New York Stock Exchange NYSE: SAND Transfer Agent Computershare Investor Services 2nd Floor, 510 Burrard Street Vancouver, British Columbia V6C 3B9 T 604 661 9400 Corporate Secretary Christine Gregory Auditors PricewaterhouseCoopers LLP PricewaterhouseCoopers Place Suite 1400, 250 Howe Street Vancouver, British Columbia V6C 3S7 T 604 806 7000 F 604 806 7806 Board of Directors Andrew T. Swarthout David Awram David E. De Witt John P. A. Budreski Mary L. Little Nolan Watson Vera Kobalia Corporate Offices Vancouver Head Office Suite 1400, 400 Burrard Street Vancouver, British Columbia V6C 3A6 T 604 689 0234 F 604 689 7317 info@sandstormgold.com www.sandstormgold.com Toronto Office Suite 503, 36 Lombard Street Toronto, Ontario M5C 2X3 02

Q4 2021 Company Profile SECTION 1 SECTION 1 Corporate Profile Message to Our Shareholders 05 Global Asset Map 06 Management & Technical Team 12 Board of Directors 13 SECTION 2 Management’s Discussion & Analysis Company Highlights 18 Overview and Outlook 21 Key Producing Assets 22 Other Producing Assets 30 Development Assets 32 Summary of Annual Results 37 Summary of Quarterly Results 40 Quarterly Commentary 43 SECTION 3 Consolidated Financial Statements Financial Position 74 Income (Loss) 75 Comprehensive Income (Loss) 76 Cash Flow 77 Changes in Equity 78 Notes to the Consolidated Financial Statements 79 03

SECTION 1 Company Profile 2021 Q4 3 2 1 “ I BELIEVE GOLD IS WELL - POSITIONED TO FULFILL ITS ROLE AS A RELIABLE STORE OF VALUE OVER THE COMING DECADE .” 04

Q4 2021 Company Profile SECTION 1 A MESSAGE FROM PRESIDENT & CEO NOLAN WATSON At the outset of 2021, I spoke about what I considered to be three major catalysts for Sandstorm’s growth: 1) new cash-flowing deals, 2) share buybacks and potential dividends, and 3) the

de-risking

of Hod Maden. I am pleased to say that we achieved all three goals during the year. Despite these accomplishments, the gold market has struggled to realize meaningful gains over the past 18 months following an impressiverun-up

in early 2020. I continue to be a firm believer that the fundamentals for gold are favourable— perhaps the most favourable I’ve seen over the course of my 20+ year career. Hyperinflation, stratospheric levels of global debt, and continued uncertainty amongst world governments have investors actively pursuing new venues to store their wealth. With ballooning cryptocurrency markets, real estate valuations, and other real assets, I believe gold is well-positioned to fulfill its role as a reliable store of value over the coming decade. The question is—how can we best take advantage of a rising gold market? 05

SECTION 1 Company Profile 2021 Q4 Gold investors buy royalty and streaming companies for better risk-adjusted returns compared to other gold investments. At Sandstorm, we accomplish this through our primary mandate of strategic capital deployment in an effort to curate a diversified portfolio of precious metal assets. In 2021, Sandstorm allocated more capital than ever before in the history of the company. This year the team allotted $213 million in accretive royalty and streaming deals, further diversifying our portfolio with stable, long-term cash-flowing assets with excellent exploration upside (a staple characteristic of Sandstorm’s portfolio). With Sandstorm cash-flowing over $80 million a year, we have made significant strides in diversifying our royalty portfolio and the way in which we return capital to shareholders. We were able to take advantage of an under-appreciated gold market this year and bought back $34 million worth of Sandstorm shares (5.5 million shares) through our active buyback program. While we are not always able to purchase shares due to blackout and regulatory reasons, we have consistently demonstrated our ability to time the purchase of shares at idyllic prices. Since announcing our buyback program in late 2018, we’ve acquired shares on average at a 20% discount to the average share price (calculated November 15, 2018–December 31, 2021). 2021 also marked the declaration of Sandstorm’s inaugural dividend—something I personally have been anticipating for several years now. This is one more indication that Sandstorm is a stable and maturing company and one that $213M A record year of royalty and streaming deals $83.5M 2021 Cash Flows from Operations (excluding

non-cash

working capital) $34M Total Consideration of shares bought back in 2021 (5.5 million shares) Development & Exploration Producing Assets Diavik Relief Canyon Emigrant Gold Bar Sao Francisco Mercedes Santa Elena Fruta del Norte Gualcamayo Ming Thunder Creek & 144 Gap Black Fox HM Claim Triangle Zone BracemacMcLeod Aurizona Sossego The Northern System Chapada Don Nicolas Cerro Moro Karma Houndé Altintepe MWS Forrestania Vatukoula 06

Q4 2021 Company Profile SECTION 1 Environment Social Governance +55% Increase to $350 million credit facility linked to sustainability goals The world’s first royalty company with a sustainability-linked credit facility. will reward shareholders for their loyalty and commitment. Recently, I was reflecting on the early years of Sandstorm and what it looked like as a small

start-up

over a decade ago. I am very proud that Sandstorm today is able to makerecord-sized

deals, buy back shares, and initiate a sustainable dividend policy all at the same time—we have certainly come a long way as a company. In addition to the free-cash-flow generating machine that Sandstorm has become, we were also able to increase our credit facility by 55% through a new sustainability-linked revolving loan—the world’s first for a royalty company. With this new credit agreement, Sandstorm has access to lower interest terms by meeting various ESG goals. “ESG” is the buzzword of the day for many investors and funds, but it has been fundamental to the core of Sandstorm’s business since the beginning. As financiers of mining projects, we have always been thoughtful and strategic in how and where we deploy capital with the goal of influencing sustainable community development at a local level. The increase in available capital provides Sandstorm with the firepower needed to bid on larger, game-changing deals benefiting shareholders while also promoting corporate responsibility and fortifying our position as an industry leader in sustainability. Whenever we announce a new deal at Sandstorm, I get a lot of questions from investors about the terms, potential upside, and generally what I see as the benefit of the particular asset. While I’m happy to talk deal-specifics, I view asset acquisitions through the role they play in the larger context of Sandstorm’s portfolio. Our job as capital allocators is to use the money shareholders have entrusted to us and build a robust portfolio with strong 07

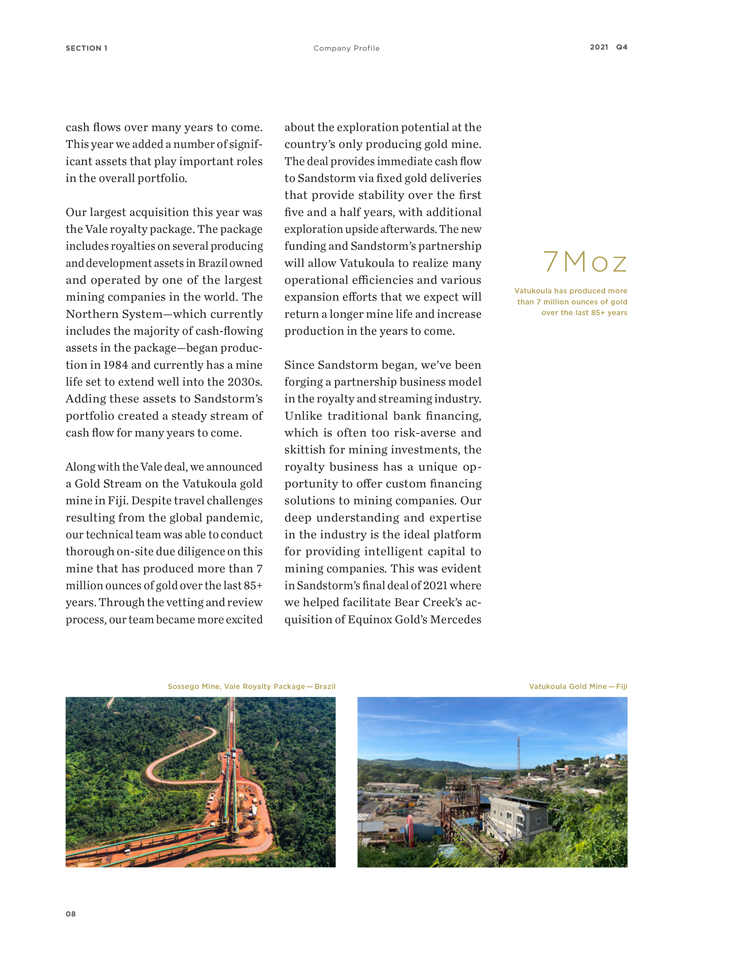

SECTION 1 Company Profile 2021 Q4 cash flows over many years to come. This year we added a number of significant assets that play important roles in the overall portfolio. Our largest acquisition this year was the Vale royalty package. The package includes royalties on several producing and development assets in Brazil owned and operated by one of the largest mining companies in the world. The Northern System—which currently includes the majority of cash-flowing assets in the package—began production in 1984 and currently has a mine life set to extend well into the 2030s. Adding these assets to Sandstorm’s portfolio created a steady stream of cash flow for many years to come. Along with the Vale deal, we announced a Gold Stream on the Vatukoula gold mine in Fiji. Despite travel challenges resulting from the global pandemic, our technical team was able to conduct thorough

on-site

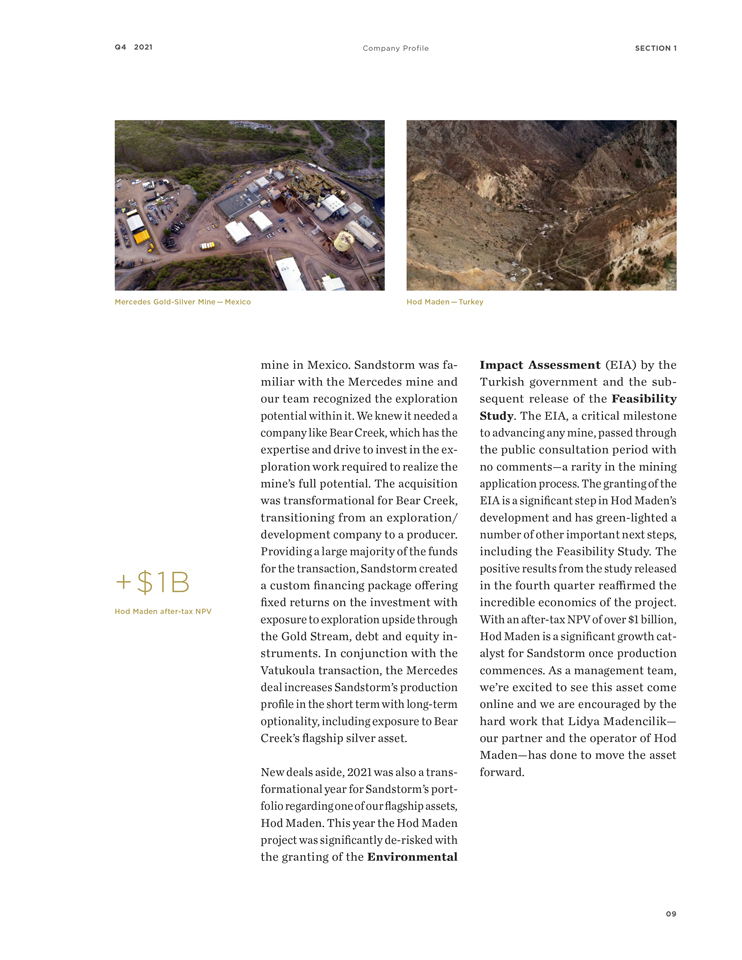

due diligence on this mine that has produced more than 7 million ounces of gold over the last 85+ years. Through the vetting and review process, our team became more excited about the exploration potential at the country’s only producing gold mine. The deal provides immediate cash flow to Sandstorm via fixed gold deliveries that provide stability over the first five and a half years, with additional exploration upside afterwards. The new funding and Sandstorm’s partnership will allow Vatukoula to realize many operational efficiencies and various expansion efforts that we expect will return a longer mine life and increase production in the years to come. Since Sandstorm began, we’ve been forging a partnership business model in the royalty and streaming industry. Unlike traditional bank financing, which is often too risk-averse and skittish for mining investments, the royalty business has a unique opportunity to offer custom financing solutions to mining companies. Our deep understanding and expertise in the industry is the ideal platform for providing intelligent capital to mining companies. This was evident in Sandstorm’s final deal of 2021 where we helped facilitate Bear Creek’s acquisition of Equinox Gold’s Mercedes 7Moz Vatukoula has produced more than 7 million ounces of gold over the last 85+ years Sossego Mine, Vale Royalty Package — Brazil Vatukoula Gold Mine — Fiji 08

Q4 2021 Company Profile SECTION 1 Mercedes Gold-Silver Mine — Mexico Hod Maden — Turkey +$1B Hod Maden

after-tax

NPV mine in Mexico. Sandstorm was familiar with the Mercedes mine and our team recognized the exploration potential within it. We knew it needed a company like Bear Creek, which has the expertise and drive to invest in the exploration work required to realize the mine’s full potential. The acquisition was transformational for Bear Creek, transitioning from an exploration/ development company to a producer. Providing a large majority of the funds for the transaction, Sandstorm created a custom financing package offering fixed returns on the investment with exposure to exploration upside through the Gold Stream, debt and equity instruments. In conjunction with the Vatukoula transaction, the Mercedes deal increases Sandstorm’s production profile in the short term with long-term optionality, including exposure to Bear Creek’s flagship silver asset. New deals aside, 2021 was also a transformational year for Sandstorm’s portfolio regarding one of our flagship assets, Hod Maden. This year the Hod Maden project was significantlyde-risked

with the granting of the Environmental Impact Assessment (EIA) by the Turkish government and the subsequent release of the Feasibility Study. The EIA, a critical milestone to advancing any mine, passed through the public consultation period with no comments—a rarity in the mining application process. The granting of the EIA is a significant step in Hod Maden’s development and has green-lighted a number of other important next steps, including the Feasibility Study. The positive results from the study released in the fourth quarter reaffirmed the incredible economics of the project. With anafter-tax

NPV of over $1 billion, Hod Maden is a significant growth catalyst for Sandstorm once production commences. As a management team, we’re excited to see this asset come online and we are encouraged by the hard work that Lidya Madencilik— our partner and the operator of Hod Maden—has done to move the asset forward. 09

SECTION 1 Company Profile 2021 Q4 “ A YEAR OF SIGNIFICANT CHANGE AT SANDSTORM THAT WILL INVOLVE A NUMBER OF MOVING PARTS . ” 10

Q4 2021 Company Profile SECTION 1 If Sandstorm is to continue to grow, we need to think bigger. For a royalty company, we recognize the unique nature of Hod Maden’s ownership structure. Since we acquired the asset in 2017, we’ve explored various options to transform our interest in Hod Maden into a more traditional Gold Stream. Along with this annual report, our team is excited to announce that we have taken the first steps in converting Hod Maden into a Gold Stream with the launch of a strategic base metals partner. We believe this will help realize the full value of this extraordinary asset for shareholders and streamline Sandstorm as a pure-play streaming and royalty company. The transformation of Sandstorm’s net profits interest in Hod Maden into a stream is part of a larger strategy for the Company—unlocking unrealized value. Over the years we’ve built the company to include assets of tremen- dous value, but we understand that not everything is given appropriate value by the market. Going forward, our management team is working on ways to realize this value for share- holders, including thinking of new and innovative ways to grow the company. Over the last 18 months, it has become increasingly clear that if Sandstorm is to continue to grow, we need to think bigger. In 2022, we’re working harder than ever to close larger accretive deals, streamline our portfolio to reflect a robust pure-play royalty company, and ensure that Sandstorm is a company shareholders are proud to own. Earlier I considered the question of how we take advantage of a rising gold market. Everything we’ve done to date—new accretive deals, initiating a dividend, buying back shares—is to ensure Sandstorm is “spring-loaded” and ready to pop when the gold industry comes back in favour. However, we’re not waiting for the gold market—the time to grow is now. This will be a year of significant change at Sandstorm that will involve a number of moving parts and big moves. I can assure you that your management team is focused on growing Sandstorm in responsible, creative and exciting ways. We’re thrilled that you are a part of this company, and we can’t wait to show you what’s in store for 2022 and beyond. 11

Section 1 Company Profile 2021 Q4 MANAGEMENT & TECHNICAL TEAM 1 NOLAN WATSON FCPA, FCA, CFA PRESIDENT & CEO 2 DAVID AWRAM B.Sc, Geologist SENIOR EXECUTIVE VP 3 ERFAN KAZEMI CPA, CA, CFA CFO 4 TOM BRUINGTON P.E., M.Sc. EXECUTIVE VP, PROJECT EVALUATION 5 RON HO CPA, CA, CFA SENIOR VP, FINANCE 6 IMOLA GÖTZ M.Sc., P.Eng. VP, MINING & ENGINEERING 7 KEITH LASKOWSKI Mining Geologist, MSc, QP VP, GEOLOGY 8 LIVIA DANILA CPA, CA VP, CORPORATE CONTROLLER 9 SARAH FORD CPA, CA, CFA VP, FINANCIAL PLANNING & ANALYSIS 10 KIM BERGEN CFA VP, CAPITAL MARKETS 11 IAN GRUNDY CPA, CA, CFA VP, CORPORATE DEVELOPMENT 12

Q4 2021 Company Profile SECTION 1 BOARD OF DIRECTORS 1 DAVID E. DE WITT CHAIRMAN 2 MARY L. LITTLE DIRECTOR 3 JOHN P. A. BUDRESKI DIRECTOR 4 VERA KOBALIA DIRECTOR 5 ANDREW T. SWARTHOUT DIRECTOR 6 NOLAN WATSON DIRECTOR 7 DAVID AWRAM DIRECTOR 13

2021 Q4 THIS PAGE INTENTIONALLY LEFT BLANK 14

FINANCIAL REPORTS Q4 Annual Report 2021 SANDSTORM GOLD LTD. DECEMBER 31ST, 2021

THIS PAGE INTENTIONALLY LEFT BLANK 16

Q4 | 2021 | |

Management’s Discussion and Analysis

FOR THE YEAR ENDED DECEMBER 31, 2021

This management’s discussion and analysis (“MD&A”) for Sandstorm Gold Ltd. and its subsidiary entities (collectively “Sandstorm”, “Sandstorm Gold” or the “Company”) should be read in conjunction with the audited consolidated financial statements of Sandstorm for the year ended December 31, 2021 and related notes thereto which have been prepared in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board (“IFRS”). The information contained within this MD&A is current to February 17, 2022 and all figures are stated in U.S. dollars unless otherwise noted.

17

Company Highlights

Record Operating Results

Another record year in terms of net income, revenue, cash flow and Attributable Gold Equivalent

1

ounces.

| · | Net income for the three months and year ended December 31, 2021 was $7.4 million and $27.6 million, respectively, compared with net income of $10.5 million and $13.8 million for the comparable periods in 2020. Net income for the most recently completed year represented a record for the Company. |

| · | Attributable Gold Equivalent ounces 1 |

| · | Revenue for the three months and year ended December 31, 2021 was $29.8 million and $114.9 million, respectively, compared with $29.7 million and $93.0 million for the comparable periods in 2020. Revenue for the most recently completed year represented a record for the Company. |

| · | Total Sales, Royalties and Income from other interests 1 (as defined hereinafter) for the three months and year ended December 31, 2021 was $29.8 million and $120.7 million, respectively, compared with $29.7 million and $93.0 million for the comparable periods in 2020. Total Sales, Royalties and Income from other interests1 for the most recently completed year represented a record for the Company. |

| · | Cash flows from operating activities, excluding changes in non-cash working capital1 , for the three months and year ended December 31, 2021 were $22.1 million and $83.5 million, respectively, compared with $22.5 million and $68.3 million for the comparable periods in 2020. Cash flows from operating activities, excluding changes innon-cash working capital1 for the most recently completed year represented a record for the Company. |

| · | Cost of sales, excluding depletion, for the three months and year ended December 31, 2021 were $3.7 million and $16.8 million, respectively, compared with $3.9 million and $14.0 million for the comparable periods in 2020. |

| · | Average cash costs 1 |

18

| · | Cash operating margins 1 |

| 1 | Refer to section on non-IFRS and other measures of this MD&A. |

Significant Acquisitions

Over $150 million in transactions on cash flowing assets:

| · | In May 2021, the Company acquired a package of royalties for consideration of $7 million. The package includes 21 royalties on development, advanced exploration and exploration stage projects located in Nevada and Montana. |

| · | In June 2021, the Company acquired a diverse package of Vale Royalties which provide holders with life of mine net sales royalties on certain of Vale’s producing and exploration assets. The royalties provide exposure to several of Vale’s long-life, low-cost assets and are expected to contribute to Sandstorm’s portfolio for several decades. |

| · | In June 2021, the Company agreed to acquire a Gold Stream on the operating Vatukoula gold mine in Fiji in exchange for a $30 million upfront deposit. The stream entitles Sandstorm to purchase 25,920 ounces of gold over a 5.5-year period and thereafter2.55%-2.9% of the gold produced from the mine for ongoing per ounce cash payments equal to 20% of the spot price of the gold. In addition to the Gold Stream, Sandstorm will also receive an effective 0.45% NSR on certain prospecting licenses. |

| · | In December 2021, the Company announced a $60 million financing package with Bear Creek Mining to facilitate its acquisition of the producing Mercedes gold-silver mine in Mexico from Equinox Gold Corp. The financing package includes a $37.5 million Gold Stream and a $22.5 million convertible debenture. The transaction is expected to close by March 31, 2022 and gold deliveries to Sandstorm will commence immediately thereafter. |

Hod Maden Milestones and Conversion to Gold Stream

With Hod Maden’s recent approval of the Environmental Impact Assessment and the release of the feasibility study, the Company has entered into an agreement to sell its interest and receive a flagship Gold Stream.

| · | In October 2021, the Hod Maden project received the final approval of the Environmental Impact Assessment for the project from the Ministry of Environment and Urbanization of Turkey. The approval marks the next development phase and triggers several key catalysts including the application for the final permits and initiating long-lead construction items. |

| · | In November 2021, the Company announced the results of the Hod Maden Feasibility Study, for which Sandstorm holds a 30% interest. The study projects a pre-tax net present value (5% discount rate) of $1.3 billion and an internal rate of return of 41%. The study also outlines total production of more than 2.5 million gold equivalent ounces over a 13 year mine life and it is expected that gold will be produced at anall-in sustaining cost on aby-product basis of $334 per ounce1 |

19

| · | Subsequent to year end, the Company announced that it had reached an agreement with Royalty North Partners Ltd. to sell its 30% interest in Hod Maden and its equity interest in Entrée. In consideration, Sandstorm will receive a flagship Gold Stream on Hod Maden and a portion of debt and equity in the resulting New-Co. The transaction is subject to various closing conditions and is expected to close in the second half of 2022. With this transaction, Sandstorm intends to unlock additional value in Hod Maden through there-rating of the asset as a Gold Stream in its portfolio and further repositions Sandstorm as a pure-play precious metals royalty and streaming company. |

| 1 | Refer to section on non-IFRS and other measures of this MD&A. |

Inaugural Dividend and Other

Increased lending capacity and an inaugural dividend.

| · | On October 6, 2021, Sandstorm amended its revolving credit agreement allowing the Company to borrow up to $350 million, and incorporated sustainability-linked performance targets to become the first royalty company to establish an Environment, Social, and Governance linked credit facility. The ESG Revolving Facility incorporates sustainability-linked incentive pricing terms that allow Sandstorm to reduce borrowing costs as the Company’s sustainability performance targets are met. The tenure of the facility is four years and is extendable by mutual consent of Sandstorm and the banking syndicate. |

| · | On December 15, 2021 Sandstorm declared its inaugural dividend of CAD$0.02 per share, paid on January 28, 2022 and each quarter thereafter, subject to annual increases. |

| · | During the year ended December 31, 2021 and under the Company’s normal course issuer bid, the Company purchased and cancelled approximately 5.5 million common shares for total consideration of $34.2 million. |

20

Overview

Sandstorm is a growth-focused company that seeks to acquire royalties and gold and other metals purchase agreements (“Gold Streams” or “Streams”) from companies that have advanced stage development projects or operating mines. In return for making upfront payments to acquire a Stream, Sandstorm receives the right to purchase, at a fixed price per ounce or at a fixed percentage of the spot price, a percentage of a mine’s gold, silver, or other commodity (“Gold Equivalent” as further defined herein)

1

production for the life of the mine. Sandstorm helps other companies in the resource industry grow their businesses, while acquiring attractive assets in the process. The Company is focused on acquiring Streams and royalties from mines with low production costs, significant exploration potential and strong management teams. The Company currently has 230 Streams and royalties, of which 29 of the underlying mines are producing.| 1 | Refer to section on non-IFRS and other measures of this MD&A. |

Outlook

Based on the Company’s existing Streams and royalties, attributable Gold Equivalent ounces (individually and collectively referred to as “Attributable Gold Equivalent”) are forecasted to be between 65,000–70,000 ounces in 2022. Subject to the conversion of the Hod Maden interest into a Gold Stream, the Company is forecasting Attributable Gold Equivalent production to be over 100,000 ounces in 2025.

21

Key Producing Assets

Yamana Silver Stream

Yamana Gold Inc.

The Company has a silver stream on Yamana Gold Inc.’s (“Yamana”) gold-silver Cerro Moro mine, located in Santa Cruz, Argentina (the “Cerro Moro Mine” or “Cerro Moro”). Under the terms of the Yamana silver stream, Sandstorm has agreed to purchase for ongoing per ounce cash payments equal to 30% of the spot price of silver, an amount of silver from Cerro Moro equal to 20% of the silver produced (up to an annual maximum of 1.2 million ounces of silver), until Yamana has delivered to Sandstorm 7.0 million ounces of silver; then 9% of the silver produced thereafter.

Based on the cumulative ounces of silver purchased

to-date,

the Company’s current silver entitlement is 20%.The Cerro Moro Mine, which commenced commercial production in 2018, is located approximately 70 kilometres southwest of the coastal port city of Puerto Deseado in the Santa Cruz province of Argentina. Cerro Moro contains several high-grade epithermal gold and silver deposits, some of which will be mined via open pit and some via underground mining methods.

Chapada Copper Stream

Lundin Mining Corporation

The Company has a copper stream on Lundin Mining Corporation’s (“Lundin Mining”) open pit copper-gold Chapada mine located 270 kilometres northwest of Brasília in Goiás State, Brazil (“Chapada” or the “Chapada Mine”). Under the terms of the Lundin Mining copper stream, Sandstorm has agreed to purchase, for ongoing per pound cash payments equal to 30% of the spot price of copper, an amount of copper from the Chapada Mine equal to:

| i. | 4.2% of the copper produced (up to an annual maximum of 3.9 million pounds of copper) until the mine has delivered 39 million pounds of copper to Sandstorm; then |

| ii. | 3.0% of the copper produced until, on a cumulative basis, the mine has delivered 50 million pounds of copper to Sandstorm; then |

| iii. | 1.5% of the copper produced thereafter, for the life of the mine. |

Based on the cumulative pounds of copper purchased

to-date,

the Company’s current copper entitlement is 4.2%.22

Chapada has been in production since 2007 and is a relatively

low-cost

South American copper-gold operation. The ore is treated through a flotation plant with processing capacity of 24 million tonnes (“Mt”) of ore per annum. In October 2019, an updated technical report was filed which outlines production through 2050. For more information, visit the Lundin Mining website at www.lundinmining.com.Vale Royalties

Vale S.A.

Sandstorm holds a diverse package of royalties on several of Vale S.A.’s (“Vale”) assets located in Brazil. These royalties provide holders with life of mine net sales royalties on seven producing mines and several exploration properties covering a total area of interest of 15,564 square kilometres (the “Vale Royalties” or the “Vale Royalty Package”). Sandstorm’s attributable portion of the Vale Royalty Package is as follows:

Copper and Gold

| · | 0.03% net sales royalty on the Sossego copper-gold mine; and |

| · | 0.06% net sales royalty on copper and gold and a 0.03% net sales royalty on all other minerals from certain assets. |

Iron Ore

| · | 0.05% net sales royalty on iron ore sales from the Northern System; and |

| · | 0.05% net sales royalty on iron ore sales from a portion of the Southeastern System (subject to certain thresholds described below). |

Other

| · | 0.03% of net sales proceeds in the event of an underlying asset sale on certain assets. |

Vale is one of the world’s largest

low-cost

iron mining companies, contributing approximately 15% of global iron ore supply. Vale’s iron ore production is in the first quartile of the cost curve and the Northern and Southeastern Systems have reserve weighted mine lives of 30 years.NORTHERN SYSTEM

The Northern System is comprised of three mining complexes: Serra Sul, Serra Norte, and Serra Leste located in the Carajas District. In 2020, the Northern System produced 192 Mt of iron ore. Production capacity was 206 Mt at the end of 2020.

23

Vale expects that production capacity will reach a long-term target of 240 to 260 Mt, which would be achieved via the approved expansion at Serra Sul and other growth projects.

Mining commenced in 1984 at Serra Norte and, based on current Mineral Reserves, is currently expected to run through the late-2030s. Serra Sul began production in 2016 and is expected to produce through the late-2050s.

SOUTHEASTERN SYSTEM

The Southeastern System is comprised of three mining complexes: Itabira, Minas Centrais, and Mariana located in Minas Gerais. These complexes will start contributing to the Vale Royalties once a cumulative sales threshold of 1.7 billion tonnes of iron ore has been reached, which Vale most recently estimated would occur in 2024 or 2025. Sandstorm estimates that approximately 70% of iron sales from the Southeastern System are covered by the Vale Royalties. Vale expects production capacity to increase to 93 Mt by the end of 2022 from current levels of 70 Mt in 2021.

Houndé Royalty

Endeavour Mining Corporation

The Company has a 2% net smelter returns royalty (“NSR”) based on the production from the Houndé gold mine located in Burkina Faso, West Africa (“Houndé” or the “Houndé Mine”) which is owned and operated by Endeavour Mining Corporation (“Endeavour”).

The royalty covers the Kari North and Kari South tenements (the “Houndé Tenements”), representing approximately 500 square kilometres of the Houndé property package. The Houndé Tenements host a Proven and Probable Mineral Reserve containing 2.1 million ounces of gold within 39.2 million tonnes of ore with an average grade of 1.7 grams per tonne gold. This Reserve is based on an economic

cut-off

grade of 0.5 grams per tonne gold. The Reserve Estimate is effective as of December 31, 2019 and includes the Vindaloo deposit, Kari West, stockpiles and the Bouéré deposit.Houndé is an open pit gold mine with a 4.0 million tonne per year processing plant using a gravity circuit and aplant. Endeavour announced an updated Inclusive Resource on November 12, 2020, which includes 3.3 million ounces of Measured and Indicated Resources contained in 61.6 million tonnes of ore with an average grade of 1.75 grams per tonne gold and 0.45 million ounces of Inferred Resources contained in 7.6 million tonnes of ore with an average grade of 1.9 grams per tonne gold at the Vindaloo, Kari Center, Kari Gap, Kari South, Kari West, Bouéré and stockpile areas combined, all of which are included within the Houndé

carbon-in-leach

24

Tenements (based on a 0.5 grams per tonneand Vindaloo South of 262,000 ounces of Measured and Indicated Resources contained in 18.9 million tonnes of ore with an average grade of 1.28 grams per tonne gold and 11,000 ounces of Inferred Resources contained in 0.2 million tonnes of ore with an average grade of 1.41 grams per tonne gold (based on a 0.5 grams per tonne gold

cut-off

grade). On January 17, 2022, Endeavour announced Mineral Resource additions at KariCentre-Gap-South

cut-off

grade). See www.endeavourmining.com for more information.Santa Elena Gold Stream

First Majestic Silver Corp.

The Company has a Gold Stream to purchase 20% of the life of mine gold produced from First Majestic Silver Corp.’s (“First Majestic”) open pit and underground Santa Elena mine, located in Mexico (the “Santa Elena Mine”), for a per ounce cash payment equal to the lesser of $468 and the then prevailing market price of gold.

The Santa Elena Mine was successfully transitioned from an open pit heap leach operation to an underground mining and milling operation and commercial production for the 3,000 tonne per day processing plant was declared in 2014. On November 24, 2021, First Majestic released an updated Technical Report for the Santa Elena Mine. The updated mine plan incorporates production from both the Santa Elena Mine and the nearby Ermitaño project, the latter of which is not subject to the Company’s Gold Stream.

Aurizona Gold Royalty

Equinox Gold Corp.

The Company has a 3%–5% sliding scale NSR on the production from Equinox Gold Corp.’s (“Equinox”) open pit Aurizona mine, located in Brazil (“Aurizona” or the “Aurizona Mine”) which achieved commercial production in 2019. At gold prices less than or equal to $1,500 per ounce, the royalty is a 3% NSR. At gold prices between $1,500 and $2,000 per ounce, the royalty is a 4% NSR. At gold prices above $2,000 per ounce, the royalty is a 5% NSR. The royalty is calculated based on sales for the month and the average monthly gold price. In addition, Sandstorm holds a 2% NSR on Equinox’s greenfields exploration ground. At any time prior to the commencement of commercial production at the greenfields exploration ground, Equinox can purchase

one-half

of the greenfields NSR for a cash payment of $10 million.On September 20, 2021, Equinox announced a positive

Pre-Feasibility

Study for an expansion to the Aurizona mine through the development of an underground mine which could be operated concurrently with the existingopen-pit

mine and is subject to the Company’s 3%–5% sliding scale NSR. The assessment outlines25

total production of 1.5 million ounces of gold over an eleven-year mine life and includes estimated Proven and Probable Mineral Reserves of 1.66 million ounces of gold (contained in 32.3 million tonnes at 1.6 grams per tonne gold with a

cut-off

grade of0.35-0.47

grams per tonne foropen-pit

and 1.8 grams per tonne gold for underground) with an expected average annual production of 137,000 ounces. ThePre-Feasibility

Study also includes an updated Mineral Resource estimate whereby the total Measured & Indicated Resources (exclusive of reserves) increased to an estimated 868,000 ounces contained in 18.1 million tonnes at 1.5 grams per tonne gold(cut-off

grade of 0.3 grams per tonne for open pit and 1.0 grams per tonne for underground resources). For more information refer to www.equinoxgold.com.Fruta del Norte Royalty

Lundin Gold Inc.

The Company has a 0.9% NSR on the precious metals produced from Lundin Gold Inc.’s (“Lundin Gold”) Fruta del Norte gold mine located in Ecuador (“Fruta del Norte” or “Fruta del Norte Mine”), which commenced commercial production in February 2020.

The royalty covers approximately 646 square kilometres, including all 29 mining concessions held by Lundin Gold. The Fruta del Norte Mineral Reserve contains an estimated 5.24 million ounces of gold in 20.3 million tonnes of ore with an average grade of 8.03 grams per tonne, as of December 31, 2020, ranking it amongst the highest-grade gold projects in the world (based on

cut-off

grade of 3.8 grams per tonne and 4.4 grams per tonne depending on mining method).In 2021, Lundin Gold commenced an

11,000-metre

drill program at Barbasco and Puente Princesa. Both targets are located south of Fruta del Norte within the same geological structure known as the Suarez Pull-Apart Basin and are located within the area of interest of the Company’s royalty. Recently, Lundin Gold announced that it had completed a plant expansion which increased the mill’s throughput from 3,500 tonnes per day to 4,200 tonnes per dayVatukoula Gold Stream

Vatukoula Gold Mines PTE Limited

In December 2021, the Company closed its previously announced gold purchase agreement which entitles it to purchase 25,920 ounces of gold over a

5.5-year

period (the “Fixed Delivery Period”) and thereafter 2.55%–2.9% of the gold produced from Vatukoula Gold Mines PTE Limited’s (“VGML”) underground gold mine located in Fiji (“Vatukoula” or the “Vatukoula Mine”) for ongoing per ounce cash26

payment equal to 20% of the spot price of the gold. In addition to the Gold Stream, Sandstorm will also receive an effective 0.45% NSR on certain prospecting licenses plus a five-kilometre area of interest.

Under the terms of the agreement, during the first 1.5 years of the Fixed Delivery Period, Sandstorm will receive 3,040 ounces of gold per year, increasing to 5,340 ounces of gold per year during the final four years of the Fixed Delivery Period. After which, Sandstorm will receive a variable proportion of gold produced from the Vatukoula Mine for the life of the mine.

As of the date of this MD&A, the Company had remitted $27 million of the $30 million purchase price, with the remaining amount subject to various milestones.

The Vatukoula Mine has produced more than 7 million ounces of gold over the last 85 years. Since 2013, annual mine production has averaged 30,000–40,000 ounces per year. With a portion of the stream proceeds, VGML plans to expand underground operations with a production target of 50,000–70,000 ounces per year in the next three to five years.

Mercedes Gold Stream

Bear Creek Mining Corporation

In December 2021, the Company entered into a $60 million financing package with Bear Creek Mining Corporation (“Bear Creek”) to facilitate Bear Creek’s acquisition of the producing Mercedes gold-silver mine in Sonora, Mexico (“Mercedes” or the “Mercedes Mine”) from Equinox. The financing package includes a $37.5 million Gold Stream on the Mercedes Mine and a $22.5 million convertible debenture, both of which are payable on closing.

Under the terms of the Gold Stream, Sandstorm has agreed to purchase 25,200 ounces of gold over a 3.5 year period (the “Fixed Delivery Term”) and thereafter 4.4% of the gold produced from Mercedes Mine. During the Fixed Delivery Term, Sandstorm will make ongoing per ounce cash payment equal to 7.5% of the spot price of the gold. After the receipt of the fixed deliveries, the ongoing per ounce cash payment will increase to 25% of the spot price of the gold.

The $22.5 million convertible debenture bears an interest rate of 6% per annum and has a term of 3 years. Sandstorm has the right to convert the principal amount of the debenture into common shares of Bear Creek, at any time prior to the maturity date, at a 35% premium, or as approved by the

TSX-V,

to Bear Creek’s share price on closing of the transaction.27

The transaction, which is expected to close by March 31, 2022, is subject to various closing conditions and the Fixed Delivery Term will begin on the earlier of the closing date or April 2022.

The Mercedes district has been the focus of mining activities dating back to the 1880s. Commercial production commenced at the Mercedes Mine in 2011 and the mine has produced over 800,000 ounces of gold. The Mercedes’ mill has a current capacity of 2,000 tonnes per day, with gold recoveries averaging approximately 95% over the past five years. Proven and Probable Reserves as at December 2020 totaled 2.6 million tonnes grading 3.9 grams per tonne gold and 29.2 grams per tonne silver, containing 325,000 ounces of gold and 2.45 million ounces of silver (based on a 2.1 grams per tonne gold

cut-off

grade, except Diluvio which is based on a 2.0 grams per tonne goldcut-off

grade). Mercedes has a strong track record of reserve replacement and Bear Creek intends on expanding its exploration program.Relief Canyon Gold Stream

Americas Gold and Silver Corporation

The Company has a precious metal stream on the Relief Canyon gold project in Nevada, U.S.A. (“Relief Canyon” or the “Relief Canyon Mine”), which is owned and operated by Americas Gold and Silver Corporation (“Americas Gold”). Under the terms of the Stream, Sandstorm is entitled to receive 32,022 ounces of gold over a 5.5 year period which began in the second quarter of 2020 (the “Fixed Deliveries”). After receipt of the Fixed Deliveries, the Company has agreed to purchase 4% of the gold and silver produced from the Relief Canyon Mine for ongoing per ounce cash payments equal to 30%–65% of the spot price of gold or silver, with the range dependent on the concession’s existing royalty obligations. In addition, Sandstorm will also receive a 1.4%–2.8% NSR on the area surrounding the Relief Canyon mine.

Americas Gold may elect to reduce the 4% Stream and NSR on the Relief Canyon mine by delivering 4,000 ounces of gold to Sandstorm (the “Purchase Option”). The Purchase Option may be exercised by Americas Gold at any time and is subject to a 10% annual premium. Upon exercising the Purchase Option, the 4% Stream will decrease to 2% and the NSR will decrease to 1%.

In January 2021, Americas Gold announced that it had achieved commercial production at the Relief Canyon Mine. Since then, the ramp up of operations has been challenging and the operation has proceeded withheap leaching with continued efforts to resolve metallurgical challenges. The mine is located in Nevada, U.S.A. at the southern end of the Pershing Gold and Silver Trend, which hosts other projects such as Coeur Mining Inc.’s Rochester mine.

run-of-mine

28

Black Fox Gold Stream

McEwen Mining Inc.

The Company has a Gold Stream to purchase 8% of the life of mine gold produced from McEwen Mining Inc.’s (“McEwen”) open pit and underground Black Fox mine, located in Ontario, Canada (the “Black Fox Mine”), and 6.3% of the life of mine gold produced from McEwen’s Black Fox Extension, which includes a portion of McEwen’s Pike River concessions, for a per ounce cash payment equal to the lesser of $577 and the spot price of gold.

The Black Fox Mine began operating as an open pit mine in 2009 (depleted in 2015) and transitioned to underground operations in 2011. McEwen continues to invest in an exploration program which includes surface and underground drilling. For more information refer to www.mcewenmining.com.

Karma Gold Stream

Endeavour Mining Corporation

The Company has a Gold Stream which entitles it to purchase 25,000 ounces of gold over a five-year period and thereafter 1.625% of the gold produced from Endeavour’s open pit heap leach Karma gold mine located in Burkina Faso, West Africa (“Karma” or the “Karma Mine”) for ongoing per ounce cash payment equal to 20% of the spot price of gold. The Gold Stream, which on a gross basis requires Endeavour to deliver 100,000 ounces of gold over a five-year period starting March 31, 2016 and thereafter 6.5% of the equivalent gold production at the Karma Mine, is syndicated 75% and 25% between Franco-Nevada Corp. and Sandstorm, respectively. With the conclusion, in March 2021, of the five-year delivery period, Sandstorm’s Gold Stream entitlement is now at 1.625%.

Bracemac-McLeod Royalty

Glencore PLC

Sandstorm has a 3% NSR based on 100% of the production from the Bracemac-McLeod property located in Matagami, Quebec, Canada (“Bracemac-McLeod” or the “Bracemac-McLeod Mine”) which is owned and operated by a subsidiary of Glencore PLC (“Glencore”).

The Bracemac-McLeod Mine is a high-grade volcanogenic massive sulphide deposit located in the historic and prolific Matagami mining district of Quebec. Continuous mining and milling operations have been active in the Matagami district for over fifty years with ten previously operating mines and one other currently producing mine. The Bracemac-McLeod Mine began initial production in the second half of 2013 and mining is scheduled to conclude in 2022.

29

Diavik Diamond Royalty

Rio Tinto PLC

The Company has a 1% gross proceeds royalty based on the production from the Diavik mine located in Lac de Gras, Northwest Territories, Canada (“Diavik” or the “Diavik Mine”) which is owned and operated by Rio Tinto PLC (“Rio Tinto”).

The Diavik Mine is Canada’s largest diamond mine. The mine began producing diamonds in January 2003 and has since produced more than 100 million carats from three kimberlite pipes (A154 South, A154 North, and A418). In the fourth quarter of 2018, Rio Tinto announced that it had achieved commercial production at its fourth open pit diamond pipe (A21).

Other Producing Assets

Ming Gold Stream

Rambler Metals & Mining PLC

The Company has a Gold Stream to purchase approximately 25% of the first 175,000 ounces of gold produced and 12% of the life of mine gold produced thereafter, from Rambler Metals & Mining PLC’s (“Rambler”) Ming copper-gold mine, located in Newfoundland, Canada (“Ming” or the “Ming Mine”). There are no ongoing per ounce payments required by Sandstorm in respect of the Ming Mine Gold Stream. In the event that the metallurgical recoveries of gold at the Ming Mine are below 85%, the percentage of gold that Sandstorm shall be entitled to purchase shall be increased proportionally. Based on 2020 metallurgical recoveries, Sandstorm’s 2021 gold purchase entitlement was adjusted to 31%.

The Ming Mine has been in operation since 2012 and continued production is expected from both the high-grade Massive Sulphide Zone and the Lower Footwall Zone. For more information refer to www.ramblermines.com.

Gualcamayo Royalty

Mineros S.A.

The Company has a 1% NSR on the Gualcamayo gold mine (the “Gualcamayo Mine”) which is located in San Juan province, Argentina and is owned and operated by Mineros S.A. (“Mineros”). The Gualcamayo Mine is an open pit, heap leach operation. Mineros is a Latin American gold producer with operations in Argentina, Colombia, and Nicaragua.

30

Thunder Creek Royalty

Pan American Silver Corp.

The Company has a 1% NSR on the gold produced from the Thunder Creek and 144 properties (“Thunder Creek” or the “Thunder Creek Mine”) which are part of the Timmins West mine complex in Ontario, Canada which is owned and operated by Pan American Silver Corp. Thunder Creek is an underground mine that has been in production since 2010 and has produced more than 500,000 ounces of gold.

Mine Waste Solutions Royalty

Harmony Gold Mining Company Limited

The Company has a 1% NSR on the gold produced from Mine Waste Solutions tailings recovery operation (“MWS”) which is located near Stilfontein, South Africa, and is owned and operated by Harmony Gold Mining Company Limited. MWS is a gold and uranium tailings recovery operation. The operation

re-processes

multiple tailings dumps in the area through three production modules, the last of which was commissioned in 2011.HM Claim

Agnico Eagle Mines Limited

The Company has a 2% NSR on a part of the Macassa mine complex located in Kirkland Lake, Ontario, Canada (“HM Claim”), which is owned and operated by Agnico Eagle Mines Limited. The Kirkland Lake mining camp has been a prolific gold producer since mining began there in 1914. The HM Claim is an area that hosts the easterly extension of the south mine complex and is located southeast of the #2 shaft at the Macassa mine.

Triangle Zone

Eldorado Gold Corp.

The Company has a 2% NSR on a part of the Triangle zone located within the Lamaque gold project located in Quebec, Canada (“Triangle Zone”), which is owned and operated by Eldorado Gold Corp. (“Eldorado”). The Triangle Zone is an Archean greenstone-hosted orogenic lode gold deposit and the royalty covers a portion of the Triangle Zone’s reserves and resources. Eldorado achieved commercial production in March 2019.

31

Emigrant Springs Royalty

Newmont Corporation

The Company has a 1.5% NSR, payable by Newmont Corporation (“Newmont”), on a portion of the Emigrant Springs gold mine (the “Emigrant Springs Mine”) which is located in the Carlin Trend in Nevada, U.S.A. The Emigrant Springs Mine is owned by Nevada Gold Mines LLC which is a joint venture owned 61.5% by Barrick Gold Corporation (“Barrick”) and 38.5% by Newmont and operated by Barrick. The Emigrant Springs Mine is an open pit, heap leach operation that has been in production since the third quarter of 2012.

Development Assets

Hod Maden

Lidya Madencilik Sanayi ve Ticaret A.S.

The Company has a 30% net profits interest and a 2% NSR on the Hod Maden gold-copper project, which is located in Artvin Province, northeastern Turkey (the “Hod Maden Project” or “Hod Maden”). The project is operated and

co-owned

by a Turkish partner, Lidya Madencilik Sanayi ve Ticaret A.S. (“Lidya”), which owns the remaining interest in the project. Lidya is a strong local partner with experience exploring, developing, permitting, and operating projects in Turkey. Lidya is part of a large Turkish conglomerate called Çalik Holding and is currently involved in several projects in Turkey including a partnership with SSR Mining Inc. on the producing Çöpler mine.In October 2021, the Hod Maden project received the final approval of the Environmental Impact Assessment (“EIA”) for the project from the Ministry of Environment and Urbanization of Turkey.

In November 2021, a Feasibility Study was released. The results of which demonstrate a Proven and Probable Mineral Reserve of 2.5 million ounces of gold and 129,000 tonnes of copper being mined over a

13-year

mine life (8.7 million tonnes at 8.8 grams per tonne gold and 1.5% copper or 11.1 grams per tonne gold equivalent using a breakevencut-off

value of $82/tonne and incrementalcut-off

values of $63 per tonne for stopes and $40 per tonne for development). The study projects apre-tax

net present value (5% discount rate) of $1.3 billion and an internal rate of return of 41%. It is estimated that gold will be produced at anall-in

sustaining cost on aby-product

basis1

of $334 per ounce. For more information refer to www.sandstormgold.com.With the approval of the EIA and release of the Feasibility Study, Hod Maden moves into the next stage of development including the application for the final permits and initiating long-lead construction items.

32

Subsequent to year end, the Company announced that it had reached an agreement with Royalty North Partners Ltd. to sell its 30% interest in Hod Maden and its equity interest in Entrée. In consideration, Sandstorm will receive a flagship Gold Stream on Hod Maden and a portion of debt and equity in the resulting issuer

(“New-Co”).

The transaction is subject to various closing conditions and is expected to close in the second half of 2022. The accounting for the transaction will be finalized on closing based on the facts and circumstances at that time. With this transaction, Sandstorm intends to unlock additional value in Hod Maden through there-rating

of the asset as a Gold Stream in its portfolio and further repositions Sandstorm as a pure-play precious metals royalty and streaming company.New-Co

will become a strategic partner to Sandstorm that will allow both companies to collaborate on future acquisitions.New-Co’s

business intent is to actively grow its existing portfolio of assets, with a focus on base metal projects. The two companies may partner together whereby Sandstorm purchases streams on the precious metalby-products

from the base metal project acquisitions made byNew-Co.

| 1 | Refer to section on non-IFRS and other measures of this MD&A. |

Hugo North Extension & Heruga Gold Stream

Entrée Resources Ltd.

The Company has a Gold Stream with Entrée Resources Ltd. (“Entrée”) to purchase an amount equal to 5.62% and 4.26%, respectively, of the gold and silver produced from the Hugo North Extension and Heruga deposits located in Mongolia, (the “Hugo North Extension” and “Heruga”, respectively) for per ounce cash payments equal to the lesser of $220 per ounce of gold and $5 per ounce of silver and the then prevailing market price of gold and silver, respectively. Additionally, Sandstorm has a copper stream to purchase an amount equal to 0.42% of the copper produced from Hugo North Extension and Heruga for per pound cash payments equal to the lesser of $0.50 per pound of copper and the then prevailing market price of copper.

The Company is not required to contribute any further capital, exploration, or operating expenditures to Entrée.

The Hugo North Extension is a copper-gold porphyry deposit and Heruga is a copper-gold-molybdenum porphyry deposit. Both projects are located in the South Gobi Desert of Mongolia, approximately 570 kilometres south of the capital city of Ulaanbaatar and 80 kilometres north of the border with China. The Hugo North Extension and Heruga are part of the Oyu Tolgoi mining complex and are managed by Oyu Tolgoi LLC, a subsidiary of Turquoise Hill Resources Ltd. and the Government of Mongolia, and its project manager Rio Tinto PLC. Entrée retains a 20% interest in the Hugo North Extension and Heruga.

33

Entrée recently announced the completion of an updated Feasibility Study on its interest in the Entrée/Oyu Tolgoi joint venture property. The updated report aligns Entrée’s disclosure with that of other Oyu Tolgoi project stakeholders on development of the first lift of the underground mine. Entrée further announced that optimization studies on Panel 1 are currently underway which have the potential to further improve Lift 1 economics for the Entrée/Oyu Tolgoi joint venture.

Hackett River Royalty

Glencore PLC

The Company has a 2% NSR on the Hackett River property located in Nunavut, Canada (the “Hackett River Project” or “Hackett River”) which is owned by a subsidiary of Glencore.

Hackett River is a silver-rich volcanogenic massive sulphide deposit and is one of the largest undeveloped projects of its kind. The property contains four massive sulphide bodies that occur over a 6.6 kilometre strike length. A Preliminary Economic Assessment updated in 2010 evaluated a possible large-scale open pit and underground operation, processing up to 12,000 tonnes per day. The most recent Glencore Reserves and Resources statement, effective December 31, 2020, reported 27.1 million tonnes of Indicated Resources containing 4.5% zinc and 130.0 grams per tonne silver plus 60.0 million tonnes of Inferred Resources with 4.0% zinc and 150.0 grams per tonne silver. For more information refer to www.glencore.com and the Technical Report dated July 26, 2010 under Sabina Gold & Silver Corp.’s profile on www.sedar.com.

Lobo-Marte Royalty

Kinross Gold Corporation

The Company has a 1.05% NSR on production from the Lobo-Marte project located in the Maricunga gold district of Chile (the “Lobo-Marte Project” or “Lobo-Marte”) which is owned by Kinross Gold Corporation (“Kinross”).

In the fourth quarter of 2021, Kinross announced the results of a Feasibility Study for the Lobo-Marte Project. The study estimates a new Probable Mineral Reserve of 6.7 million ounces contained in 160.7 million tonnes at an average grade of 1.3 grams per tonne gold with additional Indicated Resources of 2.4 million ounces contained in 99.4 million tonnes at an average grade of 0.7 grams per tonne gold and Inferred Resources of 0.4 million ounces contained in 18.5 million tonnes at an average grade of 0.75 grams per tonne gold. Kinross estimates a total life of mine production of approximately 4.7 million gold ounces during a

16-year

mine life, which includes34

14 years of mining followed by two years of residual processing. Reserves and Resources are estimated based on appropriate

cut-off

grades calculated using $1,200 per ounce gold prices. For more information refer to www.kinross.com.Agi Dagi & Kirazli Royalty

Alamos Gold Inc.

The Company has a $10 per ounce royalty based on the production from the Agi Dagi and the Kirazli gold development projects located in the Çanakkale Province of northwestern Turkey (“Agi Dagi” and “Kirazli”, respectively) which are both owned by Alamos Gold Inc. (“Alamos Gold”). The royalty is payable by Newmont and is subject to a maximum of 600,000 ounces from Agi Dagi and a maximum of 250,000 ounces from Kirazli.

A 2017 Feasibility Study on Agi Dagi and a 2017 Feasibility Study on Kirazli contemplated both projects as stand-alone open pit, heap leach operations. Under the respective studies, Agi Dagi is expected to produce an average of 177,600 ounces of gold per year over a

6-year

mine life while Kirazli is expected to produce an average of 104,000 ounces of gold per year over a5-year

mine life. For more information refer to www.alamosgold.com.Prairie Creek Royalty

NorZinc Ltd.

The Company has a 1.2% NSR on the Prairie Creek project (the “Prairie Creek Project”) located in the Northwest Territories, Canada and owned by NorZinc Ltd. (“NorZinc”). The Prairie Creek Project is a zinc, silver and lead project that is 100%-owned by NorZinc and based on a 2017 Feasibility Study has an estimated Proven and Probable Mineral Reserve of 8.1 million tonnes containing 8.6% zinc, 124.2 grams per tonne silver and 8.1% lead. For more information, refer to www.norzinc.com.

Mt. Hamilton Royalty

Waterton Precious Metals Fund II Cayman, LP

The Company has a 2.4% NSR on the Mt. Hamilton gold project (the “Mt. Hamilton Project”). The Mt. Hamilton Project is located in White Pine County, Nevada, U.S.A. and is owned by Waterton Precious Metals Fund II Cayman, LP.

35

Revolving Credit Facility

In October 2021, Sandstorm amended its revolving credit agreement, allowing the Company to borrow up to $350 million and incorporating sustainability-linked performance targets to establish an Environment, Social, and Governance (“ESG”) linked credit facility (“ESG Revolving Facility”). The ESG Revolving Facility is for general corporate purposes, from a syndicate of banks including The Bank of Nova Scotia, Bank of Montreal, National Bank of Canada, Canadian Imperial Bank of Commerce, and Royal Bank of Canada (the “Syndicate”). The term of the ESG Revolving Facility is for four years and is extendable by mutual consent of Sandstorm and the Syndicate. The amounts drawn on the ESG Revolving Facility are subject to interest at LIBOR plus 1.875%–3.0% per annum, and the undrawn portion of the ESG Revolving Facility is subject to a standby fee of 0.422%–0.675% per annum, both of which are dependent on the Company’s leverage ratio.

The ESG Revolving Facility incorporates sustainability-linked incentive pricing terms that allow Sandstorm to reduce the borrowing costs from the interest rates described above as the Company’s ESG performance targets are met. These targets focus on increasing the Company’s producing assets which report under sustainability and climate related standards as well as maintaining and improving the Company’s own external ESG rating and ensuring diverse representation at the senior management and board levels. As of the date of the MD&A, there are no amounts drawn under the ESG Revolving Facility and the full $350 million remains available.

36

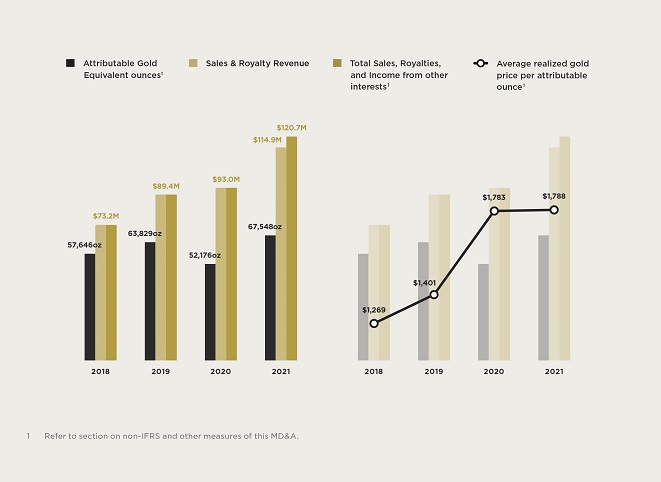

Summary of Annual Results

YEAR ENDED

In $000s (except for per share and per ounce amounts) | Dec. 31, 2021 | Dec. 31, 2020 | Dec. 31, 2019 | |||||||||

Total revenue | $ | 114,860 | $ | 93,025 | $ | 89,434 | ||||||

Attributable Gold Equivalent ounces 1 | 67,548 | 52,176 | 63,829 | |||||||||

Sales | $ | 71,722 | $ | 58,660 | $ | 63,602 | ||||||

Royalty revenue | 43,138 | 34,365 | 25,832 | |||||||||

Average realized gold price per attributable ounce 1 | 1,788 | 1,783 | 1,401 | |||||||||

Average cash cost per attributable ounce 1 | 249 | 269 | 286 | |||||||||

Cash flows from operating activities | 81,139 | 65,616 | 57,339 | |||||||||

Net income | 27,622 | 13,817 | 16,397 | |||||||||

Basic income per share | 0.14 | 0.07 | 0.09 | |||||||||

Diluted income per share | 0.14 | 0.07 | 0.09 | |||||||||

Total assets | 620,858 | 649,921 | 623,175 | |||||||||

Total long-term liabilities | 20,873 | 8,345 | 48,414 | |||||||||

| 1 | Refer to section on non-IFRS and other measures of this MD&A. |

37

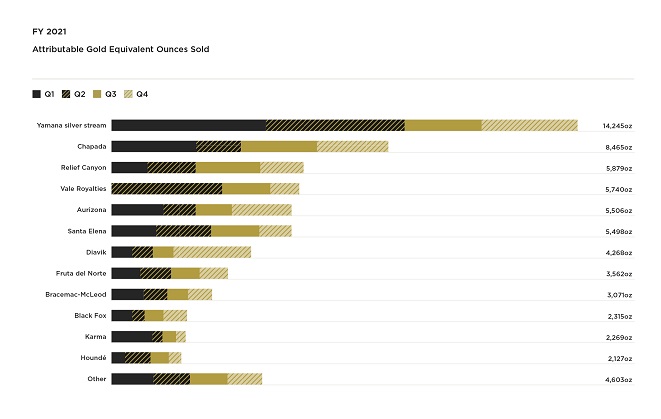

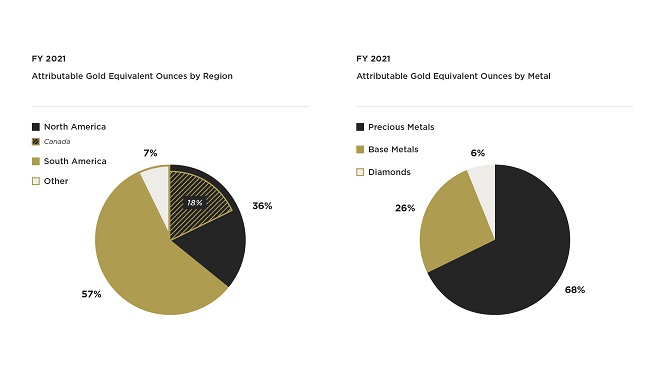

The Company’s operating segments for the year ended December 31, 2021 are summarized in the table below:

In $000s (except for ounces sold) | Product | Attributable Gold Equivalent ounces | Sales and royalty revenues | Cost of sales excluding depletion | Depletion expense | Stream, Royalty and Other Interests Impairments | Gain on Vale Royalties financial instrument | Income (loss) before taxes | Cash flows from operating activities | |||||||||||||||||||||||||||

Aurizona | Gold | 5,506 | $ | 9,844 | $ | - | $ | 815 | $ | - | $ | - | $ | 9,029 | $ | 9,444 | ||||||||||||||||||||

Black Fox | Gold | 2,315 | 4,154 | 1,309 | 1,888 | - | - | 957 | 2,845 | |||||||||||||||||||||||||||

Bracemac-McLeod 1 | Various | 3,071 | 5,487 | - | 1,545 | - | - | 3,942 | 4,995 | |||||||||||||||||||||||||||

Chapada | Copper | 8,465 | 15,118 | 4,541 | 2,963 | - | - | 7,614 | 10,577 | |||||||||||||||||||||||||||

Diavik | Diamonds | 4,268 | 7,647 | - | 3,372 | - | - | 4,275 | 7,097 | |||||||||||||||||||||||||||

Fruta del Norte | Gold | 3,562 | 6,367 | - | 2,304 | - | - | 4,063 | 4,465 | |||||||||||||||||||||||||||

Houndé | Gold | 2,127 | 3,803 | - | 1,610 | - | - | 2,193 | 3,802 | |||||||||||||||||||||||||||

Karma | Gold | 2,269 | 4,065 | 824 | 1,935 | - | - | 1,306 | 3,241 | |||||||||||||||||||||||||||

Relief Canyon | Gold | 5,879 | 10,499 | - | 4,711 | - | - | 5,788 | 10,499 | |||||||||||||||||||||||||||

Santa Elena | Gold | 5,498 | 9,786 | 2,568 | 280 | - | - | 6,938 | 7,357 | |||||||||||||||||||||||||||

Vale Royalties | Iron Ore | 5,740 | 4,398 | - | 1,444 | - | (5,887 | ) | 8,841 | 198 | ||||||||||||||||||||||||||

Yamana silver stream | Silver | 14,245 | 25,460 | 7,603 | 10,415 | - | - | 7,442 | 17,857 | |||||||||||||||||||||||||||

Other 2 | Various | 4,603 | 8,232 | - | 2,422 | 408 | - | 5,402 | 8,658 | |||||||||||||||||||||||||||

Corporate | - | - | - | - | - | - | (22,937 | ) | (9,896 | ) | ||||||||||||||||||||||||||

Consolidated | 67,548 | $ | 114,860 | $ | 16,845 | $ | 35,704 | $ | 408 | $ | (5,887 | ) | $ | 44,853 | $ | 81,139 | ||||||||||||||||||||

| 1 | Royalty revenue from Bracemac-McLeod consists of $2.8 million from copper and $2.7 million from zinc. |

| 2 | Includes royalty revenue from gold of $7.6 million and other base metals of $0.6 million. |

The Company’s operating segments for the year ended December 31, 2020 are summarized in the table below:

In $000s (except for ounces sold) | Product | Attributable Gold Equivalent ounces | Sales and royalty revenues | Cost of sales excluding depletion | Depletion expense | Stream, Royalty and Other Interests Impairments | Other | Income (loss) before taxes | Cash flows from operating activities | |||||||||||||||||||||||||||

Aurizona | Gold | 4,958 | $ | 8,850 | $ | - | $ | 1,067 | $ | - | $ | - | $ | 7,783 | $ | 7,950 | ||||||||||||||||||||

Black Fox | Gold | 2,137 | 3,693 | 1,194 | 1,014 | - | - | 1,485 | 2,500 | |||||||||||||||||||||||||||

Bracemac-McLeod 1 | Various | 1,634 | 2,946 | - | 1,485 | - | - | 1,461 | 3,234 | |||||||||||||||||||||||||||

Chapada | Copper | 5,585 | 9,904 | 3,021 | 2,914 | - | - | 3,969 | 6,883 | |||||||||||||||||||||||||||

Diavik | Diamonds | 1,489 | 2,716 | - | 2,085 | 7,862 | 392 | (7,623 | ) | 3,075 | ||||||||||||||||||||||||||

Fruta del Norte | Gold | 1,815 | 3,302 | - | 1,256 | - | - | 2,046 | 1,408 | |||||||||||||||||||||||||||

Houndé | Gold | 4,874 | 8,740 | - | 3,816 | - | - | 4,924 | 6,633 | |||||||||||||||||||||||||||

Karma | Gold | 4,584 | 8,184 | 1,619 | 3,843 | - | - | 2,722 | 6,438 | |||||||||||||||||||||||||||

Relief Canyon | Gold | 3,819 | 7,096 | - | 2,820 | - | - | 4,276 | 7,096 | |||||||||||||||||||||||||||

Santa Elena | Gold | 5,526 | 9,749 | 2,552 | 312 | - | - | 6,885 | 7,100 | |||||||||||||||||||||||||||

Yamana silver stream | Silver | 10,912 | 19,199 | 5,660 | 10,119 | - | - | 3,420 | 13,540 | |||||||||||||||||||||||||||

Other 2 | Various | 4,843 | 8,646 | - | 2,393 | 1,015 | - | 5,238 | 7,553 | |||||||||||||||||||||||||||

Corporate | - | - | - | - | - | 135 | (12,310 | ) | (7,794 | ) | ||||||||||||||||||||||||||

Consolidated | 52,176 | $ | 93,025 | $ | 14,046 | $ | 33,124 | $ | 8,877 | $ | 527 | $ | 24,276 | $ | 65,616 | |||||||||||||||||||||

| 1 | Royalty revenue from Bracemac-McLeod consists of $1.4 million from copper and $1.5 million from zinc. |

| 2 | Includes royalty revenue from gold of $8.1 million and other base metals of $0.5 million. |

38

39

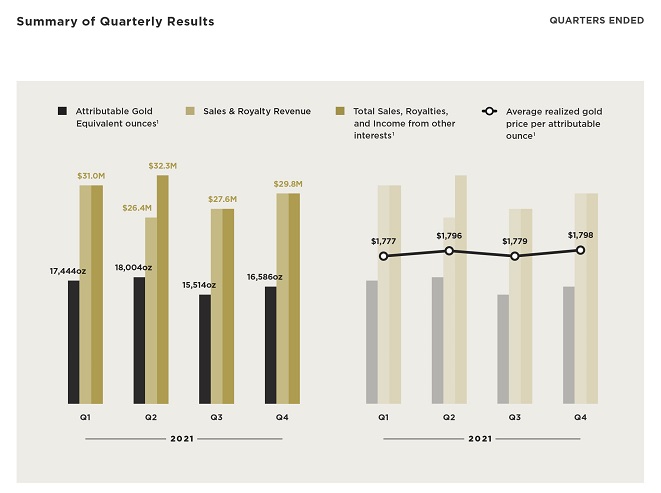

Summary of Quarterly Results

QUARTERS ENDED

In $000s (except for per share and per ounce amounts) | Dec. 31, 2021 | Sep. 30, 2021 | Jun. 30, 2021 | Mar. 31, 2021 | ||||||||||||

Total revenue | $ | 29,821 | $ | 27,596 | $ | 26,446 | $ | 30,997 | ||||||||

Attributable Gold Equivalent ounces 1 | 16,586 | 15,514 | 18,004 | 17,444 | ||||||||||||

Sales | $ | 15,772 | $ | 16,879 | $ | 17,487 | $ | 21,584 | ||||||||

Royalty revenue | 14,049 | 10,717 | 8,959 | 9,413 | ||||||||||||

Average realized gold price per attributable ounce 1 | 1,798 | 1,779 | 1,796 | 1,777 | ||||||||||||

Average cash cost per attributable ounce 1 | 224 | 238 | 227 | 307 | ||||||||||||

Cash flows from operating activities | 19,505 | 17,914 | 19,998 | 23,722 | ||||||||||||

Net income | 7,395 | 6,622 | 8,636 | 4,969 | ||||||||||||

Basic income per share | 0.04 | 0.03 | 0.04 | 0.03 | ||||||||||||

Diluted income per share | 0.04 | 0.03 | 0.04 | 0.03 | ||||||||||||

Total assets | 620,858 | 640,920 | 648,741 | 638,659 | ||||||||||||

Total long-term liabilities | 20,873 | 17,425 | 14,342 | 10,723 | ||||||||||||

In $000s (except for per share and per ounce amounts) | Dec. 31, 2020 | Sep. 30, 2020 | Jun. 30, 2020 | Mar. 31, 2020 | ||||||||||||

Total revenue | $ | 29,696 | $ | 23,267 | $ | 18,730 | $ | 21,332 | ||||||||

Attributable Gold Equivalent ounces 1 | 15,795 | 12,068 | 10,920 | 13,393 | ||||||||||||

Sales | $ | 17,560 | $ | 14,187 | $ | 12,580 | $ | 14,333 | ||||||||

Royalty revenue | 12,136 | 9,080 | 6,150 | 6,999 | ||||||||||||

Average realized gold price per attributable ounce 1 | 1,880 | 1,928 | 1,715 | 1,593 | ||||||||||||

Average cash cost per attributable ounce 1 | 248 | 258 | 257 | 314 | ||||||||||||

Cash flows from operating activities | 19,806 | 18,085 | 12,351 | 15,374 | ||||||||||||

Net income (loss) | 10,504 | 6,518 | 7,137 | (10,342 | ) | |||||||||||

Basic income (loss) per share | 0.05 | 0.03 | 0.04 | (0.06 | ) | |||||||||||

Diluted income (loss) per share | 0.05 | 0.03 | 0.04 | (0.06 | ) | |||||||||||

Total assets | 649,921 | 608,748 | 607,471 | 576,316 | ||||||||||||

Total long-term liabilities | 8,345 | 3,638 | 3,096 | 53,221 | ||||||||||||

| 1 | Refer to section on non-IFRS and other measures of this MD&A. |

40

| 1 | Refer to section on non-IFRS and other measures of this MD&A. |

Changes in sales, net income, and cash flows from operating activities from quarter to quarter are affected primarily by fluctuations in production at the mines, the timing of shipments, changes in the price of commodities, as well as acquisitions of Streams and royalty interests and the commencement of operations of mines under construction. For more information refer to the quarterly commentary below.

41

The Company’s operating segments for the three months ended December 31, 2021 are summarized in the table below:

In $000s (except for ounces sold) | Product | Attributable Gold Equivalent ounces | Sales and royalty revenues | Cost of sales excluding depletion | Depletion expense | Income (loss) before taxes | Cash flows from operating activities | |||||||||||||||||||

Aurizona | Gold | 1,833 | $ | 3,297 | $ | - | $ | 188 | $ | 3,109 | $ | 2,347 | ||||||||||||||

Black Fox | Gold | 730 | 1,321 | 414 | 595 | 312 | 907 | |||||||||||||||||||

Bracemac-McLeod 1 | Various | 727 | 1,307 | - | 454 | 853 | 1,261 | |||||||||||||||||||

Chapada | Copper | 2,183 | 3,924 | 1,179 | 747 | 1,998 | 2,745 | |||||||||||||||||||

Diavik | Diamonds | 2,366 | 4,254 | - | 639 | 3,615 | 4,184 | |||||||||||||||||||

Fruta del Norte | Gold | 872 | 1,567 | - | 569 | 998 | 1,152 | |||||||||||||||||||

Houndé | Gold | 376 | 675 | - | 264 | 411 | 94 | |||||||||||||||||||

Karma | Gold | 299 | 538 | 107 | 256 | 175 | 431 | |||||||||||||||||||

Relief Canyon | Gold | 1,334 | 2,388 | - | 1,130 | 1,258 | 2,388 | |||||||||||||||||||

Santa Elena | Gold | 986 | 1,774 | 461 | 50 | 1,263 | 1,810 | |||||||||||||||||||

Vale Royalties | Iron Ore | 890 | 1,600 | - | 666 | 934 | 198 | |||||||||||||||||||

Yamana silver stream | Silver | 2,930 | 5,268 | 1,546 | 2,323 | 1,399 | 3,722 | |||||||||||||||||||

Other | Gold | 1,060 | 1,908 | - | 472 | 1,436 | 1,907 | |||||||||||||||||||

Corporate | - | - | - | - | (6,164 | ) | (3,641 | ) | ||||||||||||||||||

Consolidated | 16,586 | $ | 29,821 | $ | 3,707 | $ | 8,353 | $ | 11,597 | $ | 19,505 | |||||||||||||||

| 1 | Royalty revenue from Bracemac-McLeod consists of $0.7 million from copper and $0.6 million from zinc. |

The Company’s operating segments for the three months ended December 31, 2020 are summarized in the table below:

In $000s (except for ounces sold) | Product | Attributable Gold Equivalent ounces | Sales and royalty revenues | Cost of sales excluding depletion | Depletion expense | Income (loss) before taxes | Cash flows from operating activities | |||||||||||||||||||

Aurizona | Gold | 1,445 | $ | 2,716 | $ | - | $ | 226 | $ | 2,490 | $ | 2,516 | ||||||||||||||

Black Fox | Gold | 555 | 1,037 | 312 | 263 | 462 | 727 | |||||||||||||||||||

Bracemac-McLeod 1 | Various | 454 | 853 | - | 394 | 459 | 1,123 | |||||||||||||||||||

Chapada | Copper | 1,550 | 2,914 | 875 | 778 | 1,261 | 2,039 | |||||||||||||||||||

Diavik | Diamonds | 612 | 1,149 | - | 12 | 1,137 | 1,000 | |||||||||||||||||||

Fruta del Norte | Gold | 1,040 | 1,955 | - | 648 | 1,307 | 680 | |||||||||||||||||||

Houndé | Gold | 1,580 | 2,970 | - | 1,058 | 1,912 | 2,231 | |||||||||||||||||||

Karma | Gold | 834 | 1,566 | 304 | 698 | 564 | 1,104 | |||||||||||||||||||

Relief Canyon | Gold | 1,667 | 3,152 | - | 1,238 | 1,914 | 3,152 | |||||||||||||||||||

Santa Elena | Gold | 1,080 | 2,025 | 500 | 61 | 1,464 | 1,445 | |||||||||||||||||||

Yamana silver stream | Silver | 3,405 | 6,401 | 1,931 | 2,715 | 1,755 | 4,471 | |||||||||||||||||||

Other 2 | Various | 1,573 | 2,958 | - | 438 | 2,520 | 2,085 | |||||||||||||||||||

Corporate | - | - | - | - | (1,331 | ) | (2,767 | ) | ||||||||||||||||||

Consolidated | 15,795 | $ | 29,696 | $ | 3,922 | $ | 8,529 | $ | 15,914 | $ | 19,806 | |||||||||||||||

| 1 | Royalty revenue from Bracemac-McLeod consists of $0.5 million from copper and $0.4 million from zinc. |

| 2 | Includes royalty revenue from gold of $2.9 million and other base metals of $0.1 million. |

42

Three Months Ended December 31, 2021 Compared to the

Three Months Ended December 31, 2020

For the three months ended December 31, 2021, net income and cash flows from operating activities were $7.4 million and $19.5 million, respectively, compared with $10.5 million and $19.8 million for the comparable period in 2020. The decrease in net income is primarily attributable to:

| · | A $3.1 million decrease in the gains recognized on the revaluation of the Company’s investments; whereby, a loss of $0.2 million was recognized by the Company during the three months ended December 31, 2021; while during the three months ended December 31, 2020 the Company recognized a gain of $2.9 million mostly driven by an increase in the fair value of the Americas Gold convertible debenture. |

For the three months ended December 31, 2021, revenue was $29.8 million compared with $29.7 million for the comparable period in 2020. The increase is attributable to a 5% increase in Attributable Gold Equivalent Ounces sold partially offset by an 4% decrease in the average realized selling price of gold. In particular, the increase in revenue was driven by:

| · | A $3.1 million increase in revenue attributable to the Diavik mine largely due to diamond price increases, the receipt of previously unrecognized royalty payments and the timing of sales; |

| · | A $1.6 million increase in revenue attributable to the Vale Royalties, which were purchased in June 2021; and |

| · | A $1.0 million increase in revenue attributable to the Chapada copper stream primarily due to an increase in the average realized selling price of copper which increased from an average of $2.96 per pound during the three months ended December 31, 2020 to an average of $4.16 per pound during the equivalent period in 2021; |

Partially offset by:

| · | A $2.3 million decrease in revenue attributable to the Houndé Mine largely driven by a 76% decrease in the number of Attributable Gold Equivalent ounces sold. The decrease is primarily due to mine sequencing whereby Endeavour is currently mining areas of the Houndé Mine not subject to the Company’s royalty; |

43

| · | A $1.1 million decrease in revenue attributable to the Yamana silver stream primarily due to a 15% decrease in the number of silver ounces sold, as well as a decrease in the average realized selling price of silver which decreased from an average of $23.83 per ounce during the three months ended December 31, 2020 to an average of $23.05 per ounce during the equivalent period in 2021; and |

| · | A $1.0 million decrease in revenue attributable to the Karma Mine largely driven by an 64% decrease in the number of Attributable Gold Equivalent Ounces sold. The decrease is primarily due to the conclusion of the five-year fixed delivery period in accordance with the terms of the Gold Stream in the first quarter of 2021, reducing Sandstorm’s Gold Stream entitlement to 1.625% of production. In contrast, in the fourth quarter of 2020, Sandstorm’s entitlement was 1,250 ounces per quarter. |

Year Ended December 31, 2021 Compared to the

Year Ended December 31, 2020

For the year ended December 31, 2021, net income and cash flows from operating activities were $27.6 million and $81.1 million, respectively, compared with net income and cash flows from operating activities of $13.8 million and $65.6 million for the comparable period in 2020. The increase in net income is attributable to an increase in revenue (described in greater detail below) as well as:

| · | An $8.5 million decrease in non-cash impairment charges; whereby, the Company recorded a $0.4 million impairment related to certain royalties within the Company’s Other segment during the year ended December 31, 2021; while for the comparable period in 2020 the Company recorded an impairment of $8.9 million related to the Company’s Diavik royalty and certain other royalties within the Company’s Other segment; and |

| · | A $5.9 million gain on the revaluation of the Company’s financial instrument related to the Vale Royalties which was both entered into and disposed of during the year ended December 31, 2021; |

Partially offset by:

| · | An increase in tax expense of $6.8 million primarily as a result of the increase in net income; |

44

| · | A $5.5 million decrease in the gains recognized on the revaluation of the Company’s investments; whereby, a loss of $1.7 million was recognized by the Company during the year ended December 31, 2021, primarily driven by the change in fair value of the Americas Gold convertible; while during the year ended December 31, 2020 the Company recognized a gain of $3.8 million primarily driven by the change in fair value of the Company’s Equinox warrants; |

| · | A $2.8 million increase in cost of sales, excluding depletion partly due to an increase in Attributable Gold Equivalent ounces sold; and |

| · | A $2.6 million increase in depletion expense also partly due to an increase in Attributable Gold Equivalent ounces sold. |

For the year ended December 31, 2021, revenue was $114.9 million compared with $93.0 million for the comparable period in 2020. The increase is largely attributable to a 29% increase in Attributable Gold Equivalent ounces sold. In particular, the increase in revenue was driven by:

| · | A $6.3 million increase in revenue attributable to the Yamana silver stream primarily due to an increase in the average realized selling price of silver which increased from an average of $19.18 per ounce during the year ended December 31, 2020 to an average of $24.84 per ounce during the equivalent period in 2021; |

| · | A $5.2 million increase in revenue attributable to the Chapada copper stream primarily due to an increase in the average realized selling price of copper which increased from an average of $2.73 per pound during the year ended December 31, 2020 to an average of $4.04 per pound during the equivalent period in 2021; |

| · | A $4.9 million increase in royalty revenue attributable to the Diavik mine largely due to diamond price increases and the timing of sales; |

| · | A $4.4 million increase in revenue attributable to the Vale Royalties, which was acquired in June 2021; |

| · | A $3.4 million increase in sales revenue attributable to the Relief Canyon Gold Stream which commenced making fixed deliveries to Sandstorm in May 2020; |

| · | A $3.1 million increase in revenue attributable to the Fruta del Norte Mine largely driven by a 96% increase in the Attributable Gold Equivalent ounces sold. The increase in ounces is attributable to the fact that during the year |

45

ended December 31, 2020, production at Fruta del Norte was impacted by a temporary suspension of operations due to concerns over the spread of COVID-19 as well as the initial ramp up to commercial production; whereas in the comparable period in 2021, the mine was operating with fewerCOVID-19 related disruptions and with the benefit of optimization efforts undertaken in 2021 by Lundin Gold; and |

| · | A $2.5 million increase in royalty revenue attributable to the Bracemac-McLeod mine largely due to commodity price increases; |

Partially offset by:

| · | A $4.9 million decrease in revenue attributable to the Houndé Mine largely driven by a 56% decrease in the number of Attributable Gold Equivalent ounces sold. The decrease is primarily due to mine sequencing whereby Endeavour is currently mining areas of the Houndé mine not subject to the Company’s royalty; and |

| · | A $4.1 million decrease in revenue attributable to the Karma Mine largely driven by a 51% decrease in the number of gold ounces sold. The decrease is primarily due to the conclusion of the five-year fixed delivery period in accordance with the terms of the Gold Stream in the first quarter of 2021, reducing Sandstorm’s Gold Stream entitlement to 1.625% of production. In contrast, during the year ended December 31, 2020, Sandstorm’s entitlement was 1,250 ounces per quarter. |

Three Months Ended December 31, 2021 Compared to the

Other Quarters Presented

When comparing net income of $7.4 million and cash flow from operating activities of $19.5 million for the three months ended December 31, 2021 with net income/loss and cash flow from operating activities for the other quarters presented, the following items impact comparability: