Table of Contents

Index to Financial Statements

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Form 10-K

(Mark One)

| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2008

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number 333-150853-4

Forbes Energy Services Ltd.

(Exact name of registrant as specified in its charter)

| Bermuda | 98-0581100 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

3000 South Business Highway 281 Alice, Texas | 78332 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (361) 664-0549

Securities registered pursuant to Section 12(b) or Section 12(g) of the Act: None

Indicate by check mark whether the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ¨ Yes þ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. þ Yes ¨ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. þ Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

¨ Large Accelerated Filer | ¨ Accelerated Filer | |

þ Non-Accelerated Filer | ¨ Smaller Reporting Company |

Indicate by check mark whether the registrant is a shell company (as defined in Exchange Act Rule 12b-2). ¨ Yes þ No

The aggregate market value of the voting stock held by non-affiliates of the registrant as of the last business day of the most recently completed second fiscal quarter, June 30, 2008, was approximately CDN$196,911,153 based on the closing sales price of the registrant’s common stock as reported by the Toronto Stock Exchange on June 30, 2008 of $7.99 per share.

Indicate the number of common shares outstanding of each of the registrant’s classes of common shares, as of the latest

practicable date.

At March 20, 2009, there were 32,611,200 common shares outstanding and 29,500,000 Class B non-voting shares outstanding.

Table of Contents

Index to Financial Statements

FORBES ENERGY SERVICES LTD. AND SUBSIDIARIES (a/k/a the “Forbes Group”)

i

Table of Contents

Index to Financial Statements

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K and any oral statements made in connection with it include certain forward-looking statements within the meaning of the federal securities laws. You can generally identify forward-looking statements by the appearance in such a statement of words like “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “potential,” “predict,” “project,” “should” or “will” or other comparable words or the negative of these words. When you consider our forward-looking statements, you should keep in mind the risk factors we describe and other cautionary statements we make in this Annual Report on Form 10-K. Our forward-looking statements are only predictions based on expectations that we believe are reasonable. Our actual results could differ materially from those anticipated in, or implied by, these forward-looking statements as a result of known risks and uncertainties set forth below and elsewhere in this Annual Report on Form 10-K. These factors include or relate to the following:

| • | supply and demand for oilfield services and industry activity levels in the current depressed market; |

| • | uncertainty in the global financial markets and worldwide economic downturn; |

| • | spending on the oil and natural gas industry given the recent worldwide economic downturn; |

| • | our level of indebtedness in the current depressed market; |

| • | impairment of our long-term assets; |

| • | our ability to maintain stable pricing; |

| • | potential for excess capacity in the current depressed market; |

| • | competition; |

| • | substantial capital requirements; |

| • | significant operating and financial restrictions under our indenture and credit facility; |

| • | technological obsolescence of operating equipment; |

| • | dependence on certain key employees; |

| • | concentration of customers; |

| • | substantial costs of compliance with reporting obligations, including the Sarbanes-Oxley Act; |

| • | material weaknesses in internal controls over financial reporting; |

| • | environmental and other governmental regulation; |

| • | risks inherent in our operations; |

| • | market response to global demands to curtail use of oil and natural gas; |

| • | change of control over us; |

| • | conflicts of interest between the principal equity investors and noteholders; |

| • | results of legal proceedings; |

| • | ability to fully integrate future acquisitions; |

| • | variation from projected operating and financial data; |

| • | variation from budgeted and projected capital expenditures; and |

| • | the other factors discussed under “Risk Factors.” |

ii

Table of Contents

Index to Financial Statements

We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. To the extent these risks, uncertainties and assumptions give rise to events that vary from our expectations, the forward-looking events discussed in this Annual Report on Form 10-K may not occur. All forward-looking statements attributable to us are qualified in their entirety by this cautionary statement.

Available Information

Information regarding the Company can be found on our internet website athttp://www.forbsenergyservices.com. In addition, our annual reports on Form 10-K, quarterly reports on Form 10-Q and amendments to those reports filed or furnished pursuant to Sections 13 or 15(d) of the Securities Exchange Act of 1934 are made available free of charge on our internet website as soon as reasonably practicable after these reports have been electronically filed with, or furnished to, the Securities and Exchange Commission (“SEC”). Information filed with the SEC may be read or copied at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. Information on operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. The SEC also maintains an internet website (http://www.sec.gov) that contains reports, proxy and information statements, and other information regarding issuers that file electronically.

iii

Table of Contents

Index to Financial Statements

Overview

We are an independent oilfield services contractor that provides a broad range of onshore drilling-related and production-related services to oil and natural gas companies, primarily onshore in Texas. The services we provide are used to help oil and natural gas companies develop and enhance the production of oil and natural gas, and include fluid hauling, fluid disposal, well maintenance, completion services, workovers and recompletions, plugging and abandonment, and tubing testing. We believe we operate one of the youngest fleets of well servicing rigs, including those commonly referred to as workover rigs, in Texas.

We believe that our broad range of services, which extends from initial drilling, through production, to eventual abandonment, is fundamental to establishing and maintaining the flow of oil and natural gas throughout the life cycle of our customers’ wells. We derive a majority of our revenues from services that support production from existing oil and natural gas operations.

Since our inception in September 2003, we have grown organically from a small South Texas operational base with two well servicing rigs and eight vacuum trucks to a major regional provider of an integrated offering of production and well services. We have successfully executed an aggressive organic growth strategy focused on fleet expansion with the construction of new equipment in a segment of the oilfield services industry characterized by competitors with aging fleets. We believe that our new well servicing rigs and equipment, with an average age of less than 2 years, significantly differentiate us from our competitors.

As of December 31, 2008, we operated from 27 locations across Texas and also operated out of one location in Mississippi and one in Mexico. We currently provide a wide range of services to a diverse group of over 730 companies. Our blue-chip customer base includes ConocoPhillips Company, Apache Corporation, Chesapeake Energy Corporation, Devon Energy Corporation, Dominion Resources, Inc., EOG Resources, Inc., and Penn Virginia Corporation, among others. John E. Crisp and Charles C. Forbes, our senior management team, have cultivated deep and ongoing relationships with these customers during their average of over 30 years of experience in the oilfield services industry. For the year ended December 31, 2008, we generated revenues of approximately $360.9 million.

We currently conduct our operations through the following two business segments:

| • | Well Servicing. The well servicing segment accounted for 52.6% of our revenues for the year ended December 31, 2008. As of December 31, 2008, the well servicing segment utilized our fleet of 170 well servicing rigs, which included 162 workover rigs and 8 swabbing rigs and related assets and equipment. These assets are used to provide well maintenance, including remedial repairs and removal and replacement of downhole production equipment, well workovers, including significant downhole repairs, re-completions and re-perforations, completion and swabbing activities, and plugging and abandoning services. In addition, as of December 31, 2008, we had a fleet of six tubing testing units that are used to conduct pressure testing of oil and natural gas production tubing. |

| • | Fluid Logistics. The fluid logistics segment accounted for 47.4% of our revenues for the year ended December 31, 2008. The fluid logistics segment utilizes our modern fleet of fluid transport trucks and related assets, including specialized vacuum, high-pressure pump and tank trucks, frac tanks, water wells, proprietary salt water disposal wells and facilities, and related equipment. These assets are used to provide, transport, store, and dispose of a variety of drilling and produced fluids used in, and generated by, oil and natural gas production. These services are required in most workover and completion projects and are routinely used in daily producing well operations. |

We believe that our two business segments are complementary and create synergies in terms of selling opportunities. Our multiple lines of service allow us to capitalize on our existing customer base to grow within existing markets, generate more business from existing customers, and increase operating profits. By offering customers the ability to reduce the number of vendors they use, we believe it helps improve the efficiency of our customers. This is demonstrated by the fact that 81.9% of our revenues for the year ended December 31, 2008, were from customers that utilized services of both of our business segments. Further, by having multiple service offerings that span the life cycle of the well, we believe that we have a competitive advantage over smaller competitors offering more limited services.

1

Table of Contents

Index to Financial Statements

The following table summarizes the major components of our equipment fleet at the dates indicated.

| December 31, | ||||||||||

| 2008 | 2007 | 2006 | 2005 | 2004 | ||||||

Locations | 27 | 18 | 12 | 7 | 4 | |||||

Well Servicing Segment | ||||||||||

Workover rigs(1) | 162 | 95 | 41 | 17 | 11 | |||||

Swabbing rigs | 8 | 6 | 2 | — | — | |||||

Tubing testing units | 6 | 6 | 4 | 4 | 4 | |||||

Fluid Logistics Segment | ||||||||||

Vacuum trucks(1) | 294 | 205 | 147 | 99 | 26 | |||||

High-pressure pump trucks | 19 | 14 | 7 | 4 | 2 | |||||

Other heavy trucks | 57 | 43 | 25 | 16 | 6 | |||||

Frac tanks(1) | 1,370 | 951 | 568 | 241 | 105 | |||||

Salt water disposal wells | 15 | 14 | 9 | 6 | 4 | |||||

| (1) | At December 31, 2008, 26 of the vacuum trucks, 10 of the workover rigs and 143 of the frac tanks were leased. |

Corporate Structure

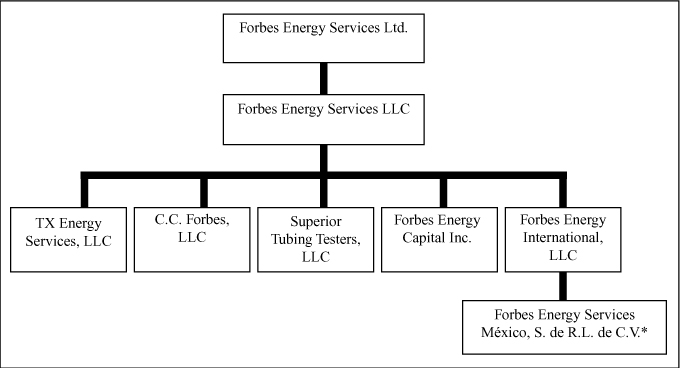

Forbes Energy Services Ltd. is a Bermuda company created to be the holding company for Forbes Energy Services LLC and its subsidiaries. Forbes Energy Services LLC is a Delaware limited liability company and the U.S. holding company for our operating entities. We operate primarily through the following four subsidiaries which are all Delaware limited liability companies directly owned by Forbes Energy Services LLC: C.C. Forbes, LLC; TX Energy Services, LLC; Superior Tubing Testers, LLC; and Forbes Energy International, LLC. Forbes Energy International, LLC was formed to hold Forbes Energy Services México, S. de R.L. de C.V., a Mexican company that conducts our Mexican operations. Forbes Energy Services LLC also holds Forbes Energy Capital Inc., a Delaware corporation created solely to be a co-issuer of our senior secured notes. The following chart graphically illustrates our current structure:

| * | Forbes Energy Services México, S. de R.L. de C.V. is 99.99% owned by Forbes Energy International, LLC and 0.01% owned by Forbes Energy Services LLC. |

2

Table of Contents

Index to Financial Statements

Reorganizations

Effective January 1, 2008, the members of each of C.C. Forbes, LLC, TX Energy Services, LLC and Superior Tubing Testers, LLC (which included Messrs. John Crisp and Charles Forbes and Ms. Janet Forbes) transferred all of the membership interests they held in such companies to Forbes Energy Services LLC in exchange for all of the outstanding membership interests in Forbes Energy Services LLC (the “Delaware Reorganization”).

In connection with a reorganization completed on May 29, 2008, (the “Bermuda Reorganization”) each of these members transferred 63% of their respective membership interests in Forbes Energy Services LLC to Forbes Energy Services Ltd. in exchange for Class B Shares. Of the proceeds from the Canadian initial public offering and simultaneous U.S. private placement of 24,644,500 common shares by Forbes Energy Services Ltd. in May 2008 (the “Initial Equity Offering”), $120 million was contributed by Forbes Energy Services Ltd. as additional capital to Forbes Energy Services LLC and used to pay the cash consideration for the repurchase by Forbes Energy Services LLC of the remaining membership interests held by the individuals who were members of such company. The purchase price for such transaction was determined on the basis of the price per common share under the initial public offering. Mr. John E. Crisp, the Chairman of the Board, President and Chief Executive Officer of Forbes Energy Services Ltd., Mr. Charles C. Forbes, the Executive Vice President and Chief Operating Officer of Forbes Energy Services Ltd., and Ms. Janet L. Forbes, a director of Forbes Energy Services Ltd., each received approximately $36 million from Forbes Energy Services LLC upon the repurchase of their remaining membership interests, or approximately 20.9% each of the gross proceeds of the Initial Equity Offering.

In connection with the Bermuda Reorganization, John E. Crisp, our President and Chief Executive Officer, Charles C. Forbes, our Executive Vice President and Chief Operating Officer, and Janet L. Forbes, one of our directors, who were the founders of the Forbes Group and were also the three largest owners of each of the entities comprising the original Forbes Group, along with all of the other members of Forbes Energy Services LLC, received Class B shares of Forbes Energy Services Ltd. The Class B shares are convertible at any time at the discretion of each holder into common shares. The Class B shares generally have no voting rights, but are permitted to approve certain actions.

Upon completion of the Bermuda Reorganization, Forbes Energy Services LLC became the wholly owned subsidiary of Forbes Energy Services Ltd. Our headquarters and executive offices are located at 3000 South Business Hwy 281, Alice, Texas 78332. We can be reached by phone at (361) 664-0549.

3

Table of Contents

Index to Financial Statements

Our Competitive Strengths

We believe that the following competitive strengths position us well within the oilfield services industry:

| • | Young and Modern Fleet. We believe we operate one of the youngest and most modern fleets of well servicing rigs among the large well-servicing companies, based on an average age of well servicing rigs. We believe over 80% of the active U.S. well servicing rig fleet was built prior to 1982, resulting in an average age in excess of 20 years. By contrast, approximately 89.4% of our 170 well servicing rigs at December 31, 2008 were built in the last three years. Many of our customers tell us that a younger and more modern fleet is more attractive to them because newer well servicing rigs require less down time for maintenance and generally are more reliable than older equipment. In addition, we believe that the level of our business is not subject to the same fluctuations as may be experienced by our competitors who operate primarily older equipment because new equipment is typically the first to be deployed and the last to be idled. As part of our strategy, we have undertaken to enhance our design specifications to improve the operational and safety characteristics of our equipment compared with older equipment. |

| • | Exposure to Revenue Streams Throughout the Life Cycle of the Well. Our maintenance and workover services expose us to demand from our customers throughout the life cycle of a well, from drilling through production and eventual abandonment. Each new well that is drilled provides us a potential multi-year stream of well services revenue, as our customers attempt to maximize and maintain a well’s productivity. Accordingly, demand for our services is generally driven by the total number of producing wells in a region and is generally less volatile than demand for new well drilling services. |

| • | High Level of Customer Retention with a Blue Chip Customer Base. Our top customers include many of the largest integrated and independent oil and natural gas companies operating onshore in the United States. We believe we have been successful in growing in our existing markets as well as expanding to new markets with existing customers due to the quality of our well servicing rigs, our personnel and our safety record. For example, members of our senior management have maintained excellent working relationships for over 20 years with our top customer. We believe the complementary nature of our two business segments also helps retain customers because of the efficiency we offer a customer that has multiple needs at the wellsite. Notably, 81.9% of our revenues from the year ended December 31, 2008 were from customers that utilize services of both of our business segments. |

| • | Industry-Leading Safety Record. For 2008, we had approximately 81.5 % fewer incidents than the industry average. Our customers tell us that our safety record and reputation are critical factors to purchasing and operations managers in their decision-making process. Over several years, we have developed a strong safety culture based on our training programs and safety seminars for our employees and customers. For example, for several years, members of our senior management have played an integral part in monthly joint safety training meetings with customer personnel. In addition, our purchase and deployment of new well servicing rigs with enhanced safety features has contributed to our strong safety record and reputation. |

| • | Experienced Senior Management Team and Operations Staff. Our senior management team of John E. Crisp and Charles C. Forbes has over 64 years of combined experience within the oilfield services industry. In addition, our next level of management, which includes our location managers, has an average of approximately 22 years of experience in the industry. |

Our Business Strategy

Our strategy is to continue to do the following:

| • | Focus on Proven and Established Oil and Natural Gas Basins. We focus our operations on customers that operate in well-established basins which have proven production histories and that have maintained a higher level of activity throughout various oil and natural gas pricing environments. Given the current depressed markets, we believe that this creates a more stable revenue stream for us as the production related services we provide our customers are tied more to ongoing production from proven wells and less to exploratory activity that has been negatively influenced by the recent precipitous decreases in oil and natural gas prices. Our experience shows that production-related services have generally withstood the current depressed economic conditions better than exploratory services. This allows us to improve or maintain utilization and margins for our fleet of assets. |

4

Table of Contents

Index to Financial Statements

| • | Establish and Maintain Leadership Position in Core Operating Areas. Based on our estimates, we believe that we have a majority market share in well servicing and fluid logistics in South Texas. We strive to establish and maintain market leadership positions within all of our core operating areas. To achieve this goal, we maintain close customer relationships and offer high-quality services and the newest equipment for our customers. In addition, our significant presence in our core operating areas facilitates employee retention and hiring and brand recognition. |

| • | Maintain a Disciplined Growth Strategy. Through the third quarter of 2008, we grew our business by following our customers to new locations which have been in reasonably close proximity to our existing locations. In 2007, we expanded from our initial presence in the Cotton Valley with a location in Marshall to Kilgore and Carthage, Texas. We have followed the same strategy in the Permian Basin, where we established an initial presence in Ozona and subsequently expanded to San Angelo, Monahans, Odessa and Big Spring, Texas. We believe that this growth strategy allows us to create synergies in geographic areas and then permits us to expand profitably from those geographic areas in which we have created a critical mass. During 2008, we expanded our field locations with operations to Mississippi and Mexico. During the fourth quarter of 2008, we severely curtailed our expansion due to the economic downturn that negatively impacted the energy industry. We have minimal capital expenditures planned for 2009 which primarily relate to our Mexico operation. These could be curtailed if the market deteriorates further. Timing of future expansion will be dictated by the recovery of exploration activity. |

Business Segments

Well Servicing Segment

Through a modern fleet of 170 well servicing rigs, as of December 31, 2008, situated in 16 locations across Texas, one in Mississippi and one in Mexico, we provide a comprehensive offering of well servicing activities to oil and natural gas companies in Texas and our other locations, including completions of newly drilled oil and natural gas wells, wellbore maintenance, workovers and re-completions, tubing testing, and plugging and abandonment services. Our well servicing rig fleet has an average age of approximately 2 years. As part of our operational strategy, we enhanced our design specifications to improve the operational and safety characteristics of our equipment compared with older equipment operated by others in the industry. These include increased derrick height and weight ratings, and increased mud pump horsepower. We believe these enhanced features translate into increased demand for our equipment and services along with better pricing for our equipment and personnel. In addition, we augment our well servicing rig fleet with auxiliary equipment, such as mud pumps, power swivels, mud plants, mud tanks, blow-out preventers, lighting plants, generators, pipe racks, and tongs, which results in incremental rental revenue and increases the profitability of a typical well service job.

We provide the following services in our well servicing segment:

| • | Completions. Utilizing our well servicing rig fleet, we perform completion services, which involve perforating and/or stimulating a wellbore to allow it to flow oil or natural gas, along with swabbing operations that are utilized to clean a wellbore prior to production. Completion operations are generally shorter term in nature and involve our equipment operating on a site for a period of two to three days. |

| • | Maintenance. Through our fleet of well servicing rigs, we provide for the removal and repair of sucker rods, downhole pumps and other production equipment, the repair of failed production tubing, and the removal of sand, paraffin and other downhole production-related byproducts that impair well productivity. These operations typically involve our well servicing rigs operating on a wellsite for five to seven days. |

| • | Workovers and Re-completions. We provide workover and re-completion services for existing wellbores. These services are designed to significantly enhance productivity by re-perforating to initiate or re-establish productivity from an oil and natural gas wellbore. In addition, we provide major downhole repairs such as casing repair, production tubing replacement, and deepening and sidetracking operations used to extend a wellbore laterally or vertically. These operations are typically longer term in nature and involve our well servicing rigs operating on a wellsite for one to two weeks at a time. |

| • | Tubing Testing. Through a fleet of six downhole testing units, we provide downhole tubing testing services that allow operators to verify tubing integrity. Tubing testing services are performed as production tubing is run into a new wellbore or on older wellbores as production tubing is replaced during a workover operation. Tubing testing services are complementary to our other service offerings and provide a significant opportunity for cross-selling. |

5

Table of Contents

Index to Financial Statements

| • | Plugging and Abandonment. Our well servicing rigs are also used in the process of permanently closing oil and natural gas wells that are no longer capable of producing in economic quantities. Plugging and abandonment work can be performed with a well servicing rig along with wireline and cementing equipment; however, this service is typically provided by companies that specialize in plugging and abandonment work. Many well operators bid this work on a “turnkey” basis, requiring the service company to perform the entire job, including the sale or disposal of equipment salvaged from the well as part of the compensation received, and complying with state regulatory requirements. We perform plugging and abandonment work in conjunction with equipment provided by other service companies. |

Fluid Logistics Segment

Our fluid logistics segment provides an integrated array of oilfield fluid sales, transportation, storage, and disposal services that are required on most workover, drilling, and completion projects and are routinely used in daily operation of producing wells by oil and natural gas producers. We have a substantial operational footprint with 19 fluid logistics locations across Texas as of December 31, 2008, and an extensive fleet of transportation trucks, high-pressure pump trucks, frac tanks, and proprietary disposal wells. This combination of services enables us to provide a one-stop source for oil and natural gas companies. We believe that the vast majority of our smaller competitors in this segment can provide some, but not all, of the equipment and services required by customers, thereby requiring them to use several companies to meet their requirements and increasing their administrative burden. In addition, by pursuing an integrated approach to service, we experience increased asset utilization rates, as multiple assets are usually required to provide a given service.

We provide the following services in our fluid logistics segment:

| • | Fluid Hauling. At December 31, 2008, we owned or leased 370 fluid service vacuum trucks and trailers equipped with a fluid hauling capacity of up to 150 barrels per unit. Each fluid service truck unit is equipped to pump fluids from or into wells, pits, tanks, and other on-site storage facilities. The majority of our fluid service truck units are also used to transport water to fill frac tanks on well locations, including frac tanks provided by us and others, to transport produced salt water to disposal wells, including injection wells owned and operated by us, and to transport drilling and completion fluids to and from well locations. In conjunction with the rental of frac tanks, we use fluid service trucks to transport water for use in fracturing operations. Following completion of fracturing operations, our fluid service trucks are used to transport the flowback produced as a result of the fracturing operations from the wellsite to disposal wells. |

| • | Disposal Services. Most oil and natural gas wells produce varying amounts of salt water throughout their productive lives. Under Texas law, oil and natural gas wastes and salt water produced from oil and natural gas wells are required to be disposed of in authorized facilities, including permitted salt water disposal wells. Injection wells are licensed by state authorities and are completed in permeable formations below the fresh water table. At December 31, 2008, we operated 15 disposal wells in 12 locations across Texas, with injection capacity of over 120,000 barrels per day, that are permitted to dispose of salt water and incidental non-hazardous oil and natural gas wastes throughout our operational bases in Texas. Our transport trucks frequently transport fluids that are disposed of in these salt water disposal wells. The disposal wells have injection capacities ranging up to 15,000 barrels per day. The salt water disposal wells are strategically located in close proximity to the producing wells of our customers. We maintain separators at all 15 disposal wells, which permits us to salvage residual crude oil that is used in operations or later sold. |

| • | Equipment Rental. At December 31, 2008, we owned or leased a fleet of 1370 fluid storage tanks that can store up to 500 barrels of fluid each. This equipment is used by oilfield operators to store various fluids at the wellsite, including fresh water, brine and acid for frac jobs, flowback, temporary production, and mud storage. We transport the tanks on our trucks to well locations that are usually within a 75-mile radius of our nearest location. Frac tanks are used during all phases of the life of a producing well. A typical fracturing operation can be completed within four days using five to 25 or more frac tanks. We believe we maintain one of the youngest storage tank fleets in the industry with an average equipment age of approximately 3 years. |

| • | Fluid Sales. We sell and transport a variety of fluids used in drilling, completion and workover operations for oil and natural gas wells. Although a relatively small percentage of our overall business, the provision of these fluids drives asset utilization rates and revenue from associated equipment. Through these services, we provide fresh water used in fracturing fluid, completion fluids, cement, and drilling mud. In addition, we provide potassium chloride for completion fluids, brine water, and water-based drilling mud. |

6

Table of Contents

Index to Financial Statements

Seasonality

Our operations are impacted by seasonal factors. Please see “Item 1A Risk Factors – Activity in the oilfield services industry is seasonal and may affect our revenues during certain periods” in this Form 10-K for additional information.

Sales and Marketing

Sales and marketing functions are performed at two levels: at the field level and through our sales representatives and executives. At the field level, our operations and rig supervisors are in constant contact with their counterparts at our customers. This contact includes working closely in the field, problem resolution efforts, and 24-hour availability. Employees of our customers become accustomed to working closely with and depending on our personnel for assistance, guidance, advice, and in other areas where teams typically interact. Our objective is for our customers to see our employees as an extension of the customers’ employees and resources. These relationships not only secure business long-term, but also generate additional business as new opportunities arise.

Our sales representatives and executives perform more traditional sales activities such as calling on customers, sending proposals, and following up on jobs to ensure customer satisfaction. This includes heavy participation in customer safety programs where our executives and sales staff either participate in or teach safety classes at various customer locations. From a sales standpoint, this close involvement and support is key to establishing and maintaining long-term relationships with the major oil and natural gas companies.

We operate a decentralized sales and marketing organization, where local management teams are largely responsible for developing stronger relationships with customers at the field level. Our customers typically are relationship driven, make decisions at the local level, and are willing to pay higher rates for responsiveness and quality services.

We cross-market our well servicing rigs along with our fluid logistics services, thereby offering our customers the ability to minimize vendors, which we believe improves the efficiency of our customers. This is demonstrated by the fact that 81.9% of our revenues for the year ended December 31, 2008 were from customers that utilized services of both of our business segments.

Employees

At December 31, 2008, we had 1,876 employees. We have made significant investments to recruit employees, provide comprehensive employee training, and implement recognized standards for health and safety. None of our employees are represented by a union or employed pursuant to a collective bargaining agreement or similar arrangement. We have not experienced any strikes or work stoppages, and we believe we have good relations with our employees. Since December 31, 2008, as a result of the current depressed market conditions, we have reduced our workforce by approximately 34%, and reduced pay rates by approximately 17%.

Continued retention of existing qualified management and field employees and availability of additional qualified management and field employees will be a critical factor in our continued success as we work to gain operating efficiencies in the current depressed market.

Competition

Our competition includes small regional service providers as well as larger companies with operations throughout the continental United States and internationally. Our four largest competitors are Basic Energy Services, Inc., Complete Production Services, Inc., Key Energy Services, Inc., and Nabors Industries Ltd. We believe that these larger competitors primarily have centralized management teams that direct their operations and decision-making primarily from corporate and regional headquarters. In addition, because of their size, these companies market a large portion of their work to the major oil and natural gas companies. We compete primarily on the basis of the young age and quality of our equipment, our safety record, the quality and expertise of our employees, and our responsiveness to customer needs.

Customers

We served in excess of 730 customers during the year ended December 31, 2008. For this same time period, our largest customer comprised approximately 8.5% of our combined revenues, our five largest customers comprised approximately 30.3% of our combined revenues, and our ten largest customers comprised approximately 42.9% of our combined revenues. Through the third

7

Table of Contents

Index to Financial Statements

quarter of 2008, we had been expanding our market base and adding new customers, however, our expansion was scaled back in the fourth quarter due to the general decrease in activity in the oil and natural gas industry. The loss of our top customer or of several of the customers in the top ten would materially adversely affect our revenues and results of operations. We believe that customers lost could be replaced with other customers, but there can be no assurance that lost revenues could be replaced in a timely manner or at all, especially given the current market conditions.

Our business segments charge customers by the hour, day or project for services, equipment and personnel.

We have master service agreements in place with most of our customers, under which projects are awarded on the basis of price, type of service, location of equipment, and the experience level of work crews.

Suppliers

We purchase or lease our well servicing rigs from several third-party suppliers. The following table provides information regarding our largest rig providers during the year ended December 31, 2008:

Rig Suppliers | Percentage of Purchases For the Year Ended December 31, 2008 | ||

Dragon Rig Sales and Service | 63.2 | % | |

Lanco Well Services Corp.* | 35.3 | % | |

Other | 1.5 | % |

| * | During 2008, Dragon Rig Sales and Service’s parent company acquired Lanco Well Services Corp. |

We have a strong and flexible working relationship with our principal well servicing rig suppliers who have verbally provided us with a right of first refusal on well servicing rigs under construction. We believe these verbal assurances permit us to delay any commitment to purchase a rig until such time as we are in need of the rig while effectively preventing our competitors from having access to such well servicing rigs unless we decline to accept them upon completion of construction.

We purchase well servicing chemicals, drilling fluids, and related supplies from various third-party suppliers. We purchase potassium chloride from two suppliers. For all other well servicing products, such as barite, surfactants, and drilling fluids, we purchase from various suppliers of well servicing products when needed.

Although we do not have written agreements with any of our suppliers (other than leases with respect to certain of our rigs and equipment), we have not historically suffered from an inability to purchase or lease equipment or purchase raw materials.

Insurance

Our operations are subject to risks inherent in the oilfield services industry, such as equipment defects, malfunctions, failures and natural disasters. In addition, hazards such as unusual or unexpected geological formations, pressures, blow-outs, fires or other conditions may be encountered in drilling and servicing wells, as well as the transportation of fluids and our assets between locations. We have obtained insurance coverage against certain of these risks which we believe is customary in the industry, including $1 million in general liability per occurrence, $25 million in umbrella coverage, and $25 million of excess liability coverage. Such insurance is subject to coverage limits and exclusions and may not be available for all of the risks and hazards to which we are exposed. In addition, no assurance can be given that such insurance will be adequate to cover our liabilities or will be generally available in the future or, if available, that premiums will be commercially justifiable. If we incur substantial liability and such damages are not covered by insurance or are in excess of policy limits, or if we incur such liability at a time when we are not able to obtain liability insurance, our business, results of operations and financial condition could be materially and adversely affected.

Environmental Regulations

Our operations are subject to various federal, state, and local laws and regulations pertaining to health, safety and the environment. Laws and regulations protecting the environment have become more stringent over the years, and in certain circumstances may impose strict liability, rendering us liable for environmental damage without regard to negligence or fault on our part. Moreover, cleanup costs, penalties, and other damages arising as a result of new, or changes to existing, environmental laws and regulations could be substantial and could have a material adverse effect on our financial condition, results of operations and cash flows. We believe that we conduct our operations in substantial compliance with current federal, state and local requirements related to health, safety and the environment.

8

Table of Contents

Index to Financial Statements

The following is a summary of the more significant existing environmental, health and safety laws and regulations to which our operations are subject and for which compliance may have a material adverse effect on our results of operation or financial position. See “Item 1A Risk Factors - Due to the nature of our business, we may be subject to environmental liability” in this Form 10-K for further details.

Hazardous Substances and Waste

TheComprehensive Environmental Response, Compensation, and Liability Act, as amended, or CERCLA, and comparable state laws impose liability without regard to fault or the legality of the original conduct on certain defined persons, including current and prior owners or operators of the site where a release of hazardous substances occurred and entities that disposed or arranged for the disposal of the hazardous substances found at the site. Under CERCLA, these responsible persons may be liable for the costs of cleaning up the hazardous substances, for damages to natural resources, and for the costs of certain health studies. In the course of our operations, we generate materials that are regulated as hazardous substances and, as a result, may incur CERCLA liability for cleanup costs. Also, claims may be filed for personal injury and property damage allegedly caused by the release of hazardous substances or other pollutants.

We also generate solid wastes that are subject to the requirements of theResource Conservation and Recovery Act, as amended, or RCRA, and comparable state statutes. Certain materials generated in the exploration, development, or production of crude oil and natural gas are excluded from RCRA’s hazardous waste regulation, but these wastes, which include wastes currently generated during our operations, could be designated as “hazardous wastes” in the future and become subject to more rigorous and costly disposal requirements. Any such changes in the laws and regulations could have a material adverse effect on our operating expenses.

Although we have used operating and disposal practices that were standard in the industry at the time, hydrocarbons or other wastes may have been released at properties owned or leased by us now or in the past, or at other locations where these hydrocarbons and wastes were taken for treatment or disposal. Under CERCLA, RCRA and analogous state laws, we could be required to clean up contaminated property (including contaminated groundwater), perform remedial activities to prevent future contamination, or pay for associated natural resource damages.

Water Discharges

We operate facilities that are subject to requirements of theClean Water Act, as amended, or CWA, and analogous state laws that impose restrictions and controls on the discharge of pollutants into navigable waters. Pursuant to these laws, permits must be obtained to discharge pollutants into state waters or waters of the United States, including to discharge storm water runoff from certain types of facilities. Spill prevention, control, and countermeasure requirements under the CWA require implementation of measures to help prevent the contamination of navigable waters in the event of a hydrocarbon spill. The CWA can impose substantial civil and criminal penalties for non-compliance.

Employee Health and Safety

We are subject to the requirements of the federalOccupational Safety and Health Act, as amended, or OSHA, and comparable state laws that regulate the protection of employee health and safety. OSHA’s hazard communication standard requires that information about hazardous materials used or produced in our operations be maintained and provided to employees, state and local government authorities, and citizens. We believe that our operations are in substantial compliance with OSHA requirements.

Other Laws and Regulations

We operate salt water disposal wells that are subject to the CWA,Safe Drinking Water Act, and state and local laws and regulations, including those established by the Environmental Protection Agency’s Underground Injection Control Program which establishes the minimum program requirements. Our salt water disposal wells are located in Texas, which requires us to obtain a permit to operate each of these wells. We have such permits for each of our salt water disposal wells. The Texas regulatory agency may suspend or modify any of these permits if such well operation is likely to result in pollution of fresh water, substantial violation of permit conditions or applicable rules, or leaks to the environment. We maintain insurance against some risks associated with our well service activities, but there can be no assurance that this insurance will continue to be commercially available or available at premium levels that justify its purchase by us. The occurrence of a significant event that is not fully insured or indemnified could have a materially adverse effect on our financial condition and operations.

9

Table of Contents

Index to Financial Statements

The following information describes certain significant risks and uncertainties inherent in our business. You should take these risks into account in evaluating us. This section does not describe all risks applicable to us, our industry or our business, and it is intended only as a summary of certain material risks. You should carefully consider such risks and uncertainties together with the other information contained in this Form 10-K. If any of such risks or uncertainties actually occurs, our business, financial condition or operating results could be harmed substantially and could differ materially from the plans and other forward-looking statements included in the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and elsewhere in this Form 10-K.

The industry in which we operate is highly volatile, and there can be no assurance that demand for our services will improve from recent depressed levels.

The demand, pricing and terms for oilfield services in our existing or future service areas largely depend upon the level of exploration and development activity for both crude oil and natural gas in the United States. Oil and natural gas industry conditions are influenced by numerous factors over which we have no control, including oil and natural gas prices, expectations about future oil and natural gas prices, levels of consumer demand, the cost of exploring for, producing and delivering oil and natural gas, the expected rates of declining current production, the discovery rates of new oil and natural gas reserves, available pipeline and other oil and natural gas transportation capacity, weather conditions, political, regulatory and economic conditions, and the ability of oil and natural gas companies to raise equity capital or debt financing.

The level of activity in the oil and natural gas industry in the United States is volatile and has recently experienced a significant downturn. No assurance can be given that trends in oil and natural gas exploration and production activities will improve or, if so, when such improvement will occur. Continuation of the recent substantial reduction in oil and natural gas prices will likely continue to have a negative effect on oil and natural gas production levels and therefore affect the demand for drilling and well services by oil and natural gas companies. Any addition to, or elimination or curtailment of, government incentives for companies involved in the exploration for and production of oil and natural gas could have a significant effect on the oilfield services industry in the United States. Lower oil and natural gas prices could also cause our customers to seek to terminate, renegotiate or fail to honor our services contracts, affect the fair market value of our equipment fleet which in turn could trigger a write down of our assets for accounting purposes, affect our ability to retain skilled oilfield services personnel, and affect our ability to obtain access to capital to fund and grow our business. In connection with the preparation of our 2008 year-end financial statements, it was determined that our goodwill was fully impaired and it was fully written off effective in the fourth quarter of 2008. A further material decline in crude oil or natural gas prices or industry activity could have a material adverse effect on our business, financial condition, results of operations and cash flows.

We may be adversely affected by uncertainty in the global financial markets and worldwide economic downturn.

Our future results may be impacted by the worldwide economic downturn, continued volatility or further deterioration in the debt and equity capital markets, inflation, deflation, or other adverse economic conditions that may negatively affect us or parties with whom we do business resulting in their non-payment or inability to perform obligations owed to us such as the failure of customers to honor their commitments, the failure of major suppliers to complete orders or the failure by Citibank, N.A. to provide expected funding under our revolving credit agreement. Additionally, credit market conditions may slow our collection efforts as customers experience increased difficulty in obtaining requisite financing, potentially leading to lost revenue and higher than normal accounts receivable. This could result in greater expense associated with collection efforts and increased bad debt expense.

The cost of raising money in the debt and equity capital markets has increased substantially during the current financial crisis while the availability of funds from those markets has diminished significantly. The current global economic downturn may adversely impact our ability to issue additional debt and institutional investors have responded to their customers by increasing interest rates, enacting tighter lending standards and refusing to refinance existing debt upon maturity or on terms similar to expiring debt. Even though we completed a private placement of 7,966,500 shares of our common stock for aggregate net proceeds of $30.0 million in the fourth quarter of 2008, we may require additional capital in the future. However, due to the above listed factors, we cannot be certain that additional funding will be available if needed and, to the extent required, on acceptable terms.

10

Table of Contents

Index to Financial Statements

Our business depends on domestic spending by the oil and natural gas industry, and this spending and our business may be adversely affected by industry and financial market conditions that are beyond our control.

We depend on our customers’ willingness to make operating and capital expenditures to explore, develop and produce oil and natural gas in the United States. Customers’ expectations for lower market prices for oil and natural gas, as well as the availability of capital for operating and capital expenditures, may curtail spending thereby reducing demand for our services and equipment.

Industry conditions are influenced by numerous factors over which we have no control, such as the supply of and demand for oil and natural gas, domestic and worldwide economic conditions, political instability in oil and natural gas producing countries and merger and divestiture activity among oil and natural gas producers. The volatility of the oil and natural gas industry and the consequent impact on exploration and production activity could adversely impact the level of drilling and workover activity by some of our customers. This reduction may cause a decline in the demand for our services or adversely affect the price of our services. In addition, reduced discovery rates of new oil and natural gas reserves in our market areas also may have a negative long-term impact on our business, even in an environment of stronger oil and natural gas prices, to the extent existing production is not replaced and the number of producing wells for us to service declines.

Recent adverse changes in capital markets have also caused a number of oil and natural gas producers to announce reductions in capital budgets for future periods. Limitations on the availability of capital, or higher costs of capital, for financing expenditures may cause these and other oil and natural gas producers to make additional reductions to capital budgets in the future even if commodity prices remain at historically high levels.

These same economic factors impact our customers’ ability to pay amounts due to us on a timely basis. This may impact some customers more severely causing them to be unable to pay their vendors for extended periods, if at all. This could have a negative impact on our cash flow.

Our indebtedness could restrict our operations and make us more vulnerable to adverse economic conditions.

As of December 31, 2008, our long-term debt, including current maturities, was $212.2 million. In the event the downturn continues or worsens, our level of indebtedness may adversely affect operations and limit our growth. Our level of indebtedness may affect our operations in several ways, including the following:

| • | by increasing our vulnerability to general adverse economic and industry conditions; |

| • | due to the fact that the covenants that are contained in the agreements governing our indebtedness limit our ability to borrow funds, dispose of assets, pay dividends and make certain investments; |

| • | due to the fact that any failure to comply with the financial or other covenants of our debt could result in an event of default, which could result in some or all of our indebtedness becoming immediately due and payable; and |

| • | due to the fact that our level of debt may impair our ability to obtain additional financing in the future for working capital, capital expenditures, acquisitions or other general corporate purposes. |

Under our Credit Facility, an event of default will be deemed to have occurred if there is a change in control over us or if a material adverse change occurs with regards to our financial position, our consolidated business, assets, operations, properties or prospects, our ability to timely pay the obligations under the Credit Facility or the enforceability of the material terms of any material loan document against us. The lender under the Credit Facility could at some future date make a determination that such a material adverse change had occurred, which is outside our control. Due to cross-default provisions in our Credit Facility and the indenture governing our Senior Secured Notes, a default and acceleration of outstanding debt under one debt agreement would result in the default and possible acceleration of outstanding debt under our other agreement. Accordingly, a default under a material adverse change clause or otherwise could result in all or a portion of our outstanding debt becoming immediately due and payable. If this occurred, we might not be able to obtain waivers or secure alternative financing to satisfy all of our obligations simultaneously. These events could have a material adverse effect on our business, financial position, results of operations and cash flows and the ability to satisfy the obligations under our debt agreements.

11

Table of Contents

Index to Financial Statements

Impairment of our long-term assets may adversely impact our financial position and results of operations.

We evaluate our long-term assets including property, equipment, identifiable intangible assets and goodwill in accordance with generally accepted accounting principles in the U.S. We used estimated future cash flows in assessing recoverability of our long-lived assets and an impairment of goodwill. The cash flow projections are based on our current operating plan, estimates and judgmental assessments. We perform this assessment of potential impairment at least annually, but also whenever facts and circumstances indicate that the carrying value of the net assets may not be recoverable due to various external or internal factors, termed a “triggering event.” We have recorded goodwill impairment charges of $4.4 million for the year ended December 31, 2008. If we determine that our estimates of future cash flows were inaccurate or our actual results for 2009 are materially different than expected, we could record additional impairment charges at interim periods during 2009 or in future years, which could have a material adverse effect on our financial position and results of operations.

We may be unable to maintain pricing on our core services.

Through the first three quarters of 2008, we were able to maintain consistent pricing for our services given the high level of demand through such period. However, as a result of pressures stemming from deteriorating market conditions and falling commodity prices, it has become increasingly difficult to maintain our prices. We have and will likely continue to face pricing pressure from our customers and our competitors. We have made price concessions, and may be compelled to make further price concessions, in order to maintain market share. The inability to maintain our pricing or further reductions in our pricing may have a material negative impact on our financial position, operating results, and cash flows.

Industry capacity may adversely affect our business.

Through the first three quarters of 2008, we had excellent utilization rates. As a result of the current worldwide economic downturn and decline in U.S. onshore exploration and production activities, demand in the industry generally is much lower than in the past which also means that neither we nor our competitors are utilizing significant portions of our respective rig fleets and related equipment. Lower utilization of our fleet has led to reduced pricing for our services. Capacity that exceeds current demand in the industry has further exacerbated the pricing pressure for our services. Although oilfield service companies are not likely to add significant new capacity under current market conditions, in light of current market conditions and the deteriorating demand for our services, the excess capacity could cause us to experience continued pressure on the pricing of our services and our utilization. This could have a material negative impact on our financial position, operating results, and cash flows.

The industry in which we operate is highly competitive.

The oilfield services industry is highly competitive and we compete with a substantial number of companies, some of which have greater technical and financial resources than we have. Our four largest competitors are Basic Energy Services, Inc., Complete Production Services, Inc., Key Energy Services Inc. and Nabors Industries Ltd. Our ability to generate revenues and earnings depends primarily upon our ability to win bids in competitive bidding processes and to perform awarded projects within estimated times and costs. There can be no assurance that competitors will not substantially increase the resources devoted to the development and marketing of products and services that compete with ours, or that new or existing competitors will not enter the various markets in which we are active. In certain aspects of our business, we also compete with a number of small and medium-sized companies that, like us, have certain competitive advantages such as low overhead costs and specialized regional strengths. In addition, reduced levels of activity in the oil and natural gas industry could intensify competition and the pressure on competitive pricing and may result in lower revenues or margins to us.

We anticipate having substantial capital requirements that, if not met, may slow our operations.

Our business strategy is based in part upon the continued expansion of our fleet through the purchase of new well servicing rigs, vacuum trucks, and related equipment. In order to continue to implement our business strategy, we will be required to expend substantial sums for any such purchases. We expect to pay for these capital expenditures through cash flow from operations, borrowings under the Credit Facility, short-term equipment vendor financings, and other permitted financings. To continue to fund future growth, including making additional capital expenditures to purchase additional equipment and, over the longer term, to remain competitive, we may need to obtain additional financings, some of which may be secured, and/or to raise capital through the sale of additional debt or equity securities. Our ability to obtain financing or to access the capital markets for future offerings may be limited by the restrictive covenants in our current and future debt agreements, by our future financial condition, and by adverse market conditions resulting from, among other things, general economic conditions and contingencies and uncertainties beyond our control.

12

Table of Contents

Index to Financial Statements

In light of the current market conditions and the deteriorating demand for our services, capital requirements for new equipment purchases are not currently an issue. However, an upturn in the market would renew the risks discussed in this risk factor.

The indenture governing the Senior Secured Notes and the credit agreement governing the Credit Facility impose significant operating and financial restrictions on us that may prevent us from pursuing certain business opportunities and restrict our ability to operate our business.

The indenture governing the Senior Secured Notes and the credit agreement governing the Credit Facility contain covenants that restrict our ability to take various actions, such as

| • | incurring or guaranteeing additional indebtedness or issuing disqualified capital stock; |

| • | creating or incurring liens; |

| • | engaging in business other than our current business and reasonably related extensions thereof; |

| • | making loans and investments; |

| • | paying certain dividends, distributions, redeeming subordinated indebtedness or making other restricted payments; |

| • | incurring dividend or other payment restrictions affecting certain subsidiaries; |

| • | transferring or selling assets; |

| • | entering into transactions with affiliates; |

| • | making capital expenditures; |

| • | entering into sale/leaseback transactions; and |

| • | consummating a merger, consolidation or sale of all or substantially all of our assets. |

In addition, the credit agreement requires us to comply with specified financial ratios, including regarding minimum net worth, fixed charge coverage and similar such ratios.

Our ability to comply with these covenants will likely be affected by events beyond our control, and we cannot assure that we will satisfy those requirements.

The restrictions contained in the indenture and the credit agreement could also limit our ability to plan for or react to market conditions, meet capital needs or otherwise restrict our activities or business plans and adversely affect our ability to fund our operations, enter into acquisitions or to engage in other business activities that would be in our interest.

We are subject to the risk of technological obsolescence.

Our ability to maintain our current business and win new business will depend upon continuous improvements in operating equipment, among other things. There can be no assurance that we will be successful in our efforts in this regard or that we will have the resources available to continue to support this need to have our equipment remain technologically up to date and competitive. Our failure to do so could have a material adverse effect on us. No assurances can be given that competitors will not achieve technological advantages over us.

We are highly dependent on certain of our officers and key employees.

Our success is dependent upon our key management, technical and field personnel, especially John E. Crisp, our President and Chief Executive Officer, Charles C. Forbes, our Executive Vice President and Chief Operating Officer, and other key executive officers. Any loss of the services of any one of such officers or a sufficient number of other employees could have a material adverse effect on our business and operations. Our ability to expand our services is dependent upon our ability to attract and retain additional qualified employees. The ability to secure the services of additional personnel may be constrained in times of strong industry activity.

13

Table of Contents

Index to Financial Statements

Our customer base is concentrated within the oil and natural gas production industry and loss of a significant customer could cause our revenue to decline substantially.

We served in excess of 730 customers for the year ended December 31, 2008. For this same time period, our largest customer comprised approximately 8.5% of our combined revenues, our five largest customers comprised approximately 30.3% of our combined revenues, and our top ten customers comprised approximately 42.9% of our combined revenues. Although we have been continually expanding our market base and adding new customers since inception, these customers currently represent a large portion of our combined revenues. The loss of our top customer or of several of our top customers would adversely affect our revenues and results of operations. We may be able to replace customers lost with other customers, but there can be no assurance that lost revenues could be replaced in a timely manner, with the same margins or at all.

We will continue to incur significant costs as a result of being obligated to comply with Securities Exchange Act reporting requirements, the Sarbanes-Oxley Act and Canadian reporting requirements, and our management will be required to devote substantial time to compliance matters.

Under our indenture, we are required to file reports under the Securities Exchange Act of 1934, as amended, with the Securities and Exchange Commission, or the Commission. In addition, the Sarbanes-Oxley Act of 2002, as well as rules subsequently implemented by the Commission have imposed various requirements on public companies, including the establishment and maintenance of effective disclosure controls and procedures, internal controls and corporate governance practices. We are also required to comply with the rules and regulations applicable to public companies in Canada and to file reports with the Canadian securities administrators. Accordingly, we will continue to incur significant legal, accounting and other expenses. Our management and other personnel will continue to devote a substantial amount of time and resources to comply with these requirements. These rules and regulations will increase our legal and financial compliance costs.

The Sarbanes-Oxley Act of 2002 requires, among other things, that we maintain effective internal controls for financial reporting and disclosure. In particular, commencing in fiscal 2009, we will be required to perform system and process evaluation and testing of our internal controls over financial reporting to allow management and our independent registered public accounting firm to report on the effectiveness of our internal controls over financial reporting, as required by Section 404 of the Sarbanes-Oxley Act of 2002. Our testing, or the subsequent testing by our independent registered public accounting firm, may reveal deficiencies in our internal controls over financial reporting that are deemed to be material weaknesses or significant deficiencies in addition to the ones discussed below. We expect to continue to incur significant expense and devote substantial management effort toward ensuring compliance in particular with Section 404. Moreover, if we are not able to comply with the requirements of Section 404 in a timely manner, if we identify possible future deficiencies in our internal controls in addition to the ones discussed below that are deemed to be material weaknesses or if we fail to adequately address existing and future deficiencies, we could be subject to sanctions or investigations by the SEC or other regulatory authorities, which would entail expenditure of additional financial and management resources.

We face several risks relating to material weaknesses in our internal control over financial reporting.

In connection with the preparation of the Forbes Group’s combined financial statements for the years ended December 31, 2006 and 2007 and our consolidated financial statements for the year ended December 31, 2008, we identified control deficiencies that constitute material weaknesses in the design and operation of our internal control over financial reporting. A material weakness is a deficiency, or combination of deficiencies, in internal control over financial reporting, such that there is a reasonable possibility that a material misstatement of our annual or interim financial statements will not be prevented or detected on a timely basis. The following material weaknesses were present at December 31, 2008.

| • | We did not maintain an appropriate accounting and financial reporting organizational structure to support the activities of the Forbes Group. Specifically, we did not maintain a sufficient complement of personnel with an appropriate level of accounting knowledge, experience and training to ensure the proper selection, application and implementation of GAAP. |

| • | We did not maintain effective controls over the preparation and review of the consolidated/combined financial statements and disclosures. |

| • | We did not design or maintain effective controls over purchase accounting. Specifically, we did not design and maintain effective controls over the accuracy and completeness of the purchase price allocation associated with the January 1, 2008 Delaware Reorganization. This material weakness resulted in the requirement to restate the Company’s unaudited condensed consolidated financial statements issued and filed for the quarters ended June 30, 2008 and September 30, 2008 (as well as the issued but unfiled financial statements for the quarter ended March 31, 2008). |

14

Table of Contents

Index to Financial Statements

| • | We did not design and maintain effective controls over the review of the accuracy and completeness of the income tax provision. This material weakness resulted in the requirement to restate the Company’s unaudited condensed consolidated financial statements issued and filed for the quarters ended June 30, 2008 and September 30, 2008. |

These material weaknesses could result in a future material misstatement to substantially all the accounts and disclosures that would result in a material misstatement to the annual or interim consolidated financial statements that would not be prevented or detected. Accordingly we have determined that each of the above control deficiencies represents a material weakness.

Internal control deficiencies could cause investors to lose confidence in our reported financial information. In addition, even if we are successful in strengthening our controls and procedures, our controls and procedures may not be adequate to prevent or identify irregularities or errors or to facilitate the fair presentation of our financial statements. We can give no assurance that the measures we have taken to date, or any future measures we may take, will remediate the material weaknesses identified or that any additional material weaknesses and significant deficiencies or additional restatements of financial results will not arise in the future due to a failure to implement and maintain adequate internal control over financial reporting or circumvention of these controls.

Activity in the oilfield services industry is seasonal and may affect our revenues during certain periods.

Our operations are impacted by seasonal factors. Historically, our business has been negatively impacted during the winter months due to inclement weather, fewer daylight hours and holidays. Our well servicing rigs are mobile, and we operate a significant number of oilfield vehicles. During periods of heavy snow, ice or rain, we may not be able to move our equipment between locations, thereby reducing our ability to generate rig or truck hours. In addition, the majority of our well servicing rigs work only during daylight hours. In the winter months when daylight time becomes shorter, this reduces the amount of time that the well servicing rigs can work and therefore has a negative impact on total hours worked. Finally, we historically have experienced significant slowdown during the Thanksgiving and Christmas holiday seasons.

We rely heavily on our suppliers and do not maintain written agreements with any such suppliers.

Our ability to compete and grow will be dependent on our access to equipment, including well servicing rigs, parts and components, among other things, at a reasonable cost and in a timely manner. We do not maintain written agreements with any of our suppliers (other than operating leases for certain equipment), and we are therefore dependent on the relationships we maintain with them. Failure of suppliers to deliver such equipment, parts and components at a reasonable cost and in a timely manner would be detrimental to our ability to maintain existing customers and obtain new customers. No assurance can be given that we will be successful in maintaining our required supply of such items.

We rely heavily on two suppliers for potassium chloride, a principal raw material that is critical for our operations. While the materials are generally available, if we were to have a problem sourcing raw materials or transporting these materials from one of these two vendors, our ability to provide some of our services could be limited. Alternate suppliers exist for all other raw materials. The source and supply of materials has been consistent in the past, however, in periods of high industry activity, periodic shortages of certain materials have been experienced and costs have been affected. We do not have contracts with, but we do maintain relationships with, a number of suppliers in an attempt to mitigate this risk. However, if current or future suppliers are unable to provide the necessary raw materials, or otherwise fail to deliver products in the quantities required, any resulting delays in the provision of services to our customers could have a material adverse effect on our business, results of operations, financial condition and cash flows.

We do not maintain written agreements with respect to some of our salt water disposal wells.

Our ability to continue to provide well maintenance services depends on our continued access to salt water disposal wells. Four of our 14 salt water disposal wells are located on the premises of third parties who have not entered into a written lease with us. We do not maintain written surface leases or right of way agreements with these third parties and we are therefore dependent on the relationships we maintain with them. Failure to maintain relationships with these third parties could impair our ability to access and maintain the applicable salt water disposal wells and any well servicing equipment located on their property. If that occurred, we would increase the levels of fluid injection at our remaining salt water disposal wells. However, our permits to inject fluid into the salt water disposal wells is subject to maximum pressure limitations and if multiple salt water disposal wells became unavailable, this might adversely impact our operations.

15

Table of Contents

Index to Financial Statements

We extend credit to our customers which presents a risk of non-payment.

A substantial portion of our accounts receivable are with customers involved in the oil and natural gas industry, whose revenues may be affected by fluctuations in oil and natural gas prices. Collection of these receivables could be influenced by economic factors affecting this industry. We do not have significant exposure to any individual customer other than our top customer, which accounted for approximately 8.5% of the revenues for the year ended December 31, 2008.

Due to the nature of our business, we may be subject to environmental liability.