As Filed with the Securities and Exchange Commission on January 26, 2016 |

| Registration No. |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

________________

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

________________

XG Sciences, INC.

(Exact name of registrant as specified in its charter)

Michigan |

| 2821 |

| 20-4998896 |

(State or other jurisdiction of |

| (Primary Standard Industrial |

| (I.R.S. Employer Identification |

3101 Grand Oak Drive

Lansing, MI 48911

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Philip L. Rose

Chief Executive Officer

XG Sciences, Inc.

3101 Grand Oak Drive

Lansing, MI 48911

Telephone: (517) 703-1110

(Name, address, including zip code, and telephone number, including area code, of agent for service)

________________

Copies to:

Clayton E. Parker, Esq.

Matthew Ogurick, Esq.

Camielle N. Green, Esq.

K&L Gates LLP

200 South Biscayne Boulevard, Suite 3900

Miami, Florida 33131-2399

Telephone: (305) 539-3306

Facsimile: (305) 358-7095

________________

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box.x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act of 1933, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act of 1933, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act of 1933, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer¨ |

| Accelerated filer¨ |

| Non-accelerated filer¨ |

| Smaller reporting companyx |

|

|

|

| (Do not check if a smaller reporting company) | ||

CALCULATION OF REGISTRATION FEE

Title of Each Class of Securities to be Registered |

| Amount to beRegistered |

| Proposed MaximumOffering PricePer Share(1) |

| Proposed Maximum AggregateOffering Price(1) |

| Amount ofRegistration Fee | |||

Primary Offering By XG Sciences, Inc. |

|

|

|

|

|

|

|

|

|

|

|

Common stock, no par value per share |

| 2,000,000 |

| $ | 8 |

| $ | 16,000,000 |

| $ | 1,611.20 |

Secondary Offering by selling securityholders(2) |

|

|

|

|

|

|

|

|

|

|

|

Common stock, no par value per share |

| 836,544 |

| $ | 8 |

|

|

|

|

|

|

Common stock, no par value per share, underlying warrants |

| 31,625 |

|

|

|

|

|

|

|

|

|

Common stock, no par value per share, underlying shares of Series A Preferred Stock |

| 3,376,299 |

|

|

|

|

|

|

|

|

|

Common stock, no par value per share, underlying shares of Series B Preferred Stock |

| 539,974 |

|

|

|

|

|

|

|

|

|

Total for Secondary Offering: |

| 4,784,442 |

| $ | 8 |

| $ | 38,275,536 |

| $ | 3,854.35 |

Total for Primary and Secondary Offering: |

| 6,784,442 |

|

|

|

|

|

|

| $ | 5,465.55 |

____________

(1) Calculated in accordance with Rule 457(o) under the Securities Act of 1933.

(2) This Registration Statement includes and covers the sale by selling securityholders named herein of up to 4,784,442 shares of the registrant’s common stock, including: (i) up to 836,544 shares previously issued to selling securityholders in private placements, (ii) up to 31,625 shares issuable upon exercise of warrants previously issued to selling securityholders, (iii) up to 3,376,299 shares issuable upon conversion by selling securityholders of Series A Preferred Stock previously issued to selling securityholders, and (iv) up to 539,974 shares issuable upon exchange by selling securityholders of Series B Preferred Stock previously issued to selling securityholders Pursuant to Rule 416 under the Securities Act of 1933, the shares being registered hereunder include such indeterminate number of shares of common stock as may be issuable with respect to the shares being registered hereunder as a result of stock splits, stock dividends or similar transactions. The proposed offering price per share for the Selling Stockholders was estimated solely for the purpose of calculating the registration fee pursuant to Rule 457 of Regulation C. The price of $8.00 is a fixed price at which the selling securityholders may sell their shares until our common stock is quoted on the OTC Bulletin Board or OTC Markets at which time the shares may be sold at prevailing market prices or at privately negotiated prices.

The Registrant amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall hereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, or until the registration statement shall become effective on such date as the Commission, acting pursuant to Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission becomes effective. This prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any state where the offer or sale is not permitted.

PRELIMINARY PROSPECTUS

Subject to completion, dated , 2016

6,784,442 shares of Common Stock of

XG SCIENCES, INC.

Primary Offering

This is the initial offering of common stock of XG Sciences, Inc., and no public market currently exists for the securities being offered. We are registering for sale a total of 2,000,000 shares of common stock at a fixed price of $8.00 per share to the general public in a best efforts offering. We estimate our total offering registration costs to be approximately $740,000, provided that a sales agent is engaged, as described further herein. There is no minimum number of shares that must be sold by us for the offering to proceed, and we will retain the proceeds from the sale of any of the offered shares. The offering is being conducted on a best efforts basis and the Company intends to engage the services of a sales agent to assist it with selling the shares. If the Company engages such a sales agent, we intend to pay a commission fee of up to 8%. For additional information please see the “Plan of Distribution for Primary Offering” .

The shares will be offered at a fixed price of $8.00 per share for a period of one hundred and eighty (180) days from the effective date of this prospectus. The offering shall terminate on the earlier of (i) when the offering period ends (180 days from the effective date of this prospectus), (ii) the date when the sale of all 2,000,000 shares is completed, and (iii) when our Board of Directors decides that it is in the best interest of the Company to terminate the offering prior to the completion of the sale of all 2,000,000 shares registered under the Registration Statement of which this prospectus is part.

Secondary Offering

In addition, the selling securityholders identified in this prospectus or any of their pledges, donees, transferees or other successors-in-interests may offer to sell, from time to time, in amounts at prices and on terms determined at the time of the offering, up to 4,784,442 additional shares of our common stock under this prospectus. We will not receive any proceeds from the sale of shares by the selling securityholders, but we will incur expenses in connection with the sale of those shares, including legal and accounting fees and we will receive proceeds from the cash exercise of the warrants held by selling securityholders.

Sales by the selling securityholders may occur through ordinary brokerage transactions, directly to market makers in our shares or through any other means described in the section of this prospectus entitled “Plan of Distribution for Secondary Offering”.

The selling securityholders have not engaged any underwriter in connection with the sale of their shares of common stock.

The offering price of $8.00 is a fixed price at which the selling securityholders may sell their shares until our common stock is quoted on the Over-the-Counter Bulletin Board (the “OTC Bulletin Board”) or OTC Markets at which time the common stock may be sold at prevailing market prices or at privately negotiated prices.

There has been no market for our securities and a public market may never develop, or, if any market does develop, it may not be sustained. Our common stock is not currently quoted on or traded on any exchange or on the over-the-counter market. After the effective date of this prospectus, we hope to have a market maker file an application with the Financial Industry Regulatory Authority (“FINRA”) for our common stock to be eligible for trading on the OTC Bulletin Board. To be eligible for quotation, issuers must remain current in their quarterly and annual filings with the Securities and Exchange Commission. If we are not able to pay the expenses associated with our reporting obligations we will not be able to apply for quotation on the OTC Bulletin Board. We do not yet have a market maker who has agreed to file such application. There can be no assurance that our common stock will ever be quoted on a stock exchange or a quotation service or that any market for our stock will develop. We further intend to apply for the listing of our common stock on the NASDAQ Capital Market.

We are an “emerging growth company” as that term is used in the Jumpstart Our Business Startups Act of 2012 and, as such, may elect to comply with certain reduced public company reporting requirements for future filings. Please refer to discussions under “Prospectus Summary” on page 1 and “Risk Factors” on page 8 of how and when we may lose emerging growth company status and the various exemptions that are available to us.

Investing in our securities involves a high degree of risk. See the section entitled “Risk Factors” on page 8 of this prospectus and in the documents we filed with the Securities and Exchange Commission that are incorporated in this prospectus by reference for certain risks and uncertainties you should consider.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2016.

TABLE OF CONTENTS

| 1 | |

| 5 | |

| 8 | |

| 19 | |

| 19 | |

| 20 | |

| 21 | |

| 22 | |

| 24 | |

| 25 | |

| 26 | |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND |

| 27 |

| 45 | |

| 66 | |

| 75 | |

| 78 | |

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND |

| 80 |

| 83 | |

| 89 | |

| 99 | |

| 101 | |

| 103 | |

| 103 | |

| 103 | |

| F-1 | |

| F-46 | |

| II-1 | |

| II-8 | |

| II-8 |

You should rely only on the information contained in this prospectus. We have not, and the selling securityholders have not, authorized any person to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. This prospectus is not an offer to sell, nor are the selling securityholders seeking an offer to buy, securities in any state where the offer or solicitation is not permitted. The information contained in this prospectus is complete and accurate as of the date on the front cover of this prospectus, but information may have changed since that date. We are responsible for updating this prospectus to ensure that all material information is included and will update this prospectus to the extent required by law.

i

This prospectus of XG Sciences, Inc., a Michigan corporation (together with its sole subsidiary, the “Company”, “XG Sciences”, “XGS” or “we”, “us”, or “our”) is a part of a registration statement on Form S-1 that we filed with the Securities and Exchange Commission. This summary highlights selected information contained elsewhere in this prospectus. This summary does not contain all the information that you should consider before investing in our common stock. You should carefully read the entire prospectus, including “Risk Factors”, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the financial statements and related notes beginning on page F-1 before making an investment decision.

XG Sciences was formed in May 2006 for the purpose of commercializing certain technology to produce graphene nanoplatelets. First discovered in 2004, graphene is a single layer of carbon atoms configured in an atomic-scale honeycomb lattice. Among many noted properties, graphene is harder than diamonds, lighter than steel but significantly stronger, and conducts electricity better than copper. Graphene nanoplatelets are particles consisting of multiple layers of graphene. Graphene nanoplatelets have unique capabilities for energy storage, thermal conductivity, electrical conductivity, barrier properties, lubricity and the ability to impart strength when incorporated into plastics or other matrices.

We believe the unique properties of graphene and graphene nanoplatelets will enable numerous new product applications and the market for such products will quickly grow to be a significant market opportunity. Our business model is to design, manufacture and sell advanced materials we call xGnP® graphene nanoplatelets and value-added products based on these nanoplatelets. We currently have hundreds of customers trialing our products for numerous applications, including, but not limited to lithium ion batteries, supercapacitors, thermal shielding and heat transfer, inks and coatings, printed electronics, construction materials, composites, and military uses.

Our proprietary manufacturing processes were developed at the Composite Materials and Structures Center in the College of Engineering of Michigan State University (“MSU”) and licensed to us in 2006. We licensed four U.S. patents and patent applications from MSU. However, over time, our scientists and engineers have made many further discoveries and inventions that are embodied in the form of ten additional patent applications, and numerous trade secrets. Our general IP strategy is to keep as trade secrets those manufacturing processes that are difficult to enforce should they be disclosed and to seek patent coverage for other manufacturing processes, materials derived from those processes, unique combinations of materials and end uses of materials containing graphene nanoplatelets. We believe that the combination of our rights under the MSU license, patents and patent applications, and our trade secrets create a strong intellectual property position.

We target our xGnP® nanoplatelets for use in a range of large and growing end-use markets. Our proprietary manufacturing processes allow us to produce nanoplatelets with varying performance characteristics that can be tuned to specific end-use applications based on customer requirements. We currently offer three commercial “grades” of bulk materials, each of which is available in various particle sizes. Other grades may be made available, depending on the needs for specific applications. In addition, we sell our material in the form of pre-dispersed mixtures with water, alcohol, or other organic solvents and resins. We also formulate xGnP® nanoplatelets into value-added products and formulations that further enhance the value we deliver to our customers. We have also licensed some of our base manufacturing technology to other companies and we consider technology licensing a component of our business model.

We sell products to customers around the world and have sold materials to over 850 customers (entities that have purchased our materials) in 47 countries since 2008. Some of these customers are research organizations and some are commercial organizations. Because graphene is a new material, our customers are developing new uses for our products and purchase them in quantities consistent with development purposes. A few of our customers have indicated to us that they have introduced commercial products that use our materials, but our customers are under no obligation to report to us on the usage of our materials. Our customers have included well-known automotive and OEM suppliers around the world (Ford, Johnson Controls, Magna, Honda Engineering) world-scale lithium ion battery manufacturers in the US, South Korea and China (Samsung SDI, LG Chem, Lishen, A123) and diverse specialty material companies (3M, BASF, Henkel, Dow Chemical, Dupont) as well as many others. We also work closely with our licensees, POSCO and Cabot Corporation (“Cabot”), who further extend our technology through their customer network. Ultimately, we expect to benefit in terms of royalties on sales of xGnP® produced and sold by our licensees.

1

|

|

|

The above graphs show total orders and customers based on actual purchases of our materials and do not include free samples or materials used in joint development programs. Nevertheless, the total dollar volume of these orders is not yet sufficient to cover our fixed operating expenses. The average order size in 2014, for example, was $2,175, which indicates to us that most of these orders are for materials that are not yet incorporated into large-volume commercial products.

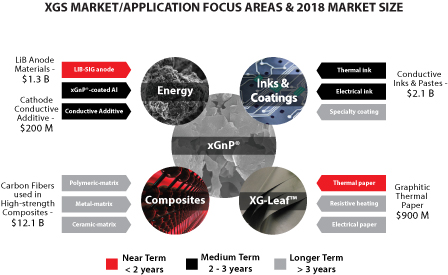

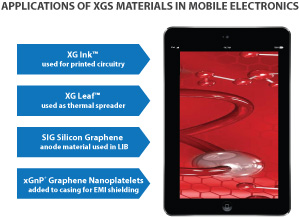

We also offer a sheet product, called XG Leaf®, to customers for a variety of thermal spreading and other applications. XG Leaf® is ideally suited for use in thermal management in cell phones, tablets and PC’s. As these devices continue to adopt faster electronics, higher data management capabilities, brighter displays with ever increasing definition, they generate more and more heat. Managing that heat is a key requirement for the portable electronics market and our XG Leaf® product line is well suited to address the need. In a press release dated March 3, 2015, Gartner, Inc., a leading research organization, estimated the 2014 global cell phone market at 1.88 billion units. Every cell phone has some form of thermal management system, and we believe many of the new smart phones being developed can benefit from the performance advantages we are able to achieve with XG Leaf®. In August 2015, International Data Corporation (IDC) in their Worldwide Quarterly Tablet Tracker, estimated the global shipment of tablets in 2015 at 212 million units. Thus, we believe our XG Leaf® product line is well positioned to address a very large and rapidly growing market.

According to Prismark Partners, LLC, a leading electronics industry consulting firm specializing in advanced materials, the 2014 market for finished graphitic heat spreaders as sold to the OEM and EMS companies with adhesive, PET, and/or copper backing for selected portable applications was $600 million, and is expected to reach $900 million in 2018. The market is currently in a significant expansion period driven by the demand for portable devices.

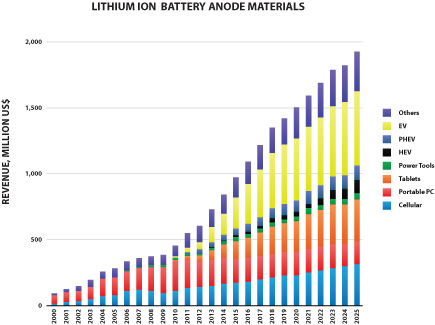

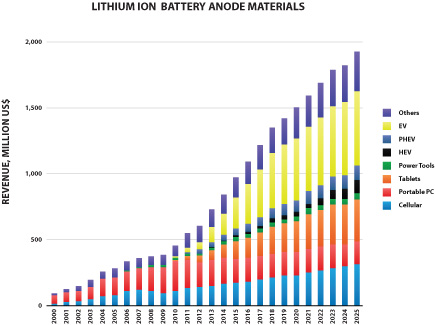

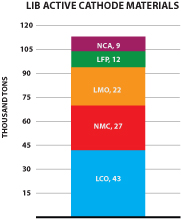

We also offer a specially formulated silicon-graphene composite material (also referred to as “SiG” in this prospectus) for use in lithium-ion battery anodes. SiG targets the never-ending need for higher battery capacity and longer life. In several customer trials, our SiG material has demonstrated the potential to increase battery energy storage capacity by 3-5x what is currently available with conventional lithium ion batteries today. The market for materials used in lithium ion battery anodes is large and growing as shown in the figure below (Avicenne Energy, “The Rechargeable Battery Market, 2014–2025”, July 2015). We believe our ability to address next generation anode materials represents a significant opportunity for us.

2

We also offer specially-formulated inks and coatings for electrical and thermal applications that are showing promise in diverse customer applications such as advanced packaging, electrostatic dissipation and thermal management.

These three product areas — custom XG Leaf® sheets, our SiG anode materials, and custom inks/coatings — comprise the set of core value-added product groups on which we are focusing our internal development resources.

We have developed and scaled-up capacity for two manufacturing processes — one based on chemical intercalation of graphite and subsequent exfoliation and classification; and the second based on a high-shear mechanical process. In March 2012, we took possession of a production facility under terms of a long-term lease and moved our headquarters to this new location. Initial production commenced in this facility in September 2012. Currently, this facility is capable of producing approximately 30 – 50 tons per year of intercalated materials (depending on product mix) if operated on a continuous basis. We also operate a separate production facility in leased manufacturing space which is used for the production of certain specialty materials. This facility is capable of producing approximately 30 – 60 tons per year of materials (depending on product mix) if operated on a continuous basis. We believe these manufacturing facilities will be sufficient to meet demands for the majority of our bulk materials for a number of years, with suitable additions of capital equipment as warranted. However, additional manufacturing capabilities for certain value-added products and certain bulk materials remain to be developed and will likely require the acquisition of additional facilities. In particular, the production processes for XG Leaf® and our silicon-graphene electrode materials and our conductive inks will require additional capital and additional facilities to meet expected future customer demand.

As of the date of this prospectus, we have not yet demonstrated sales of products at a level capable of covering our fixed expenses. Since inception, we have not demonstrated the capability to produce sufficient materials to generate the ongoing revenues necessary to sustain our operations in the long-term. Nor have we demonstrated the ability to generate sufficient sales to sustain the business. There can be no assurance that the Company will ever produce a profit.

Many of the Company’s products represent new products that have not yet been fully developed and for which manufacturing operations have not yet been fully scaled. This means that investors are subject to all the risks incident to the creation and development of multiple new products and their associated manufacturing processes, and each investor should be prepared to withstand a complete loss of their investment.

3

Because we are subject to these uncertainties, there may be risks that management has failed to anticipate and you may have a difficult time evaluating our business and your investment in our Company. Our ability to become profitable depends primarily on our ability to successfully commercialize our products in the future. Even if we successfully develop and market our products, we may not generate sufficient or sustainable revenue to achieve or sustain profitability, which could cause us to cease operations and you will lose all of your investment.

We have no sustainable base of products approved for commercial use by our customers, have never generated significant product revenues and may never achieve sufficient revenues for profitable operations, which could cause us to cease operations.

XG Sciences primarily sells bulk materials or products made with these materials to other companies for incorporation into their products. A few customers have incorporated our materials and offered them for sale in commercial markets. However, to date, there has been no incorporation of our materials or products into customer products that are released for commercial sale in sufficient volume to cover the fixed costs. Because there is limited history of commercial success for our products, it is possible that large scale adoption of our materials may never happen and that we will never achieve the level of revenues necessary to sustain our business.

Developing, manufacturing and selling nanomaterials in commercially-viable quantities requires substantial funding. As of December 31, 2014, September 30, 2015 and December 31, 2015, we had cash on hand of approximately $2.1 million, $1.6 million and $1.1 million, respectively. In addition to our cash on hand, we currently have an ongoing offering of Series B Preferred Stock, but we have no assurance that we will raise any additional funds under this offering. On December 31, 2015, we issued non-convertible promissory notes (the “December Notes”) and warrants to purchase 20,625 shares of common stock (the “December Warrants”) to several existing stockholders. The December Notes mature on June 30, 2016 and the December Warrants have a five year term and a strike price of $8.00. We cannot determine how much additional funds we might raise under the private placement. Under the terms of the private placement, the conversion price of the Series A Preferred Stock was adjusted to $6.40 per share and holders of Series B Preferred Stock received the right to exchange units each consisting of one share of Series B Preferred Stock and related warrants to purchase shares of common stock (each, a “Series B Unit”) previously purchased, for common stock at a rate of 2 shares of common stock for each Series B Unit. The Company’s financial projections show that the Company may need to raise an additional $15 million or more before it is capable of achieving sustainable cash flow from operations. There is no assurance that the Company will be able to raise these funds or that the terms and conditions of future financing will be workable or acceptable for the Company and its stockholders. In the event that the Company is not able to raise substantial additional funds in the future, the Company would be forced to cease operations and you would lose all of your investment.

Since our inception we have incurred annual losses every year and have accumulated a deficit from operations of $33,471,774 through September 30, 2015. As of September 30, 2015 our total stockholder’s deficit was $11,909,972. As of the date of this prospectus, we have cash on hand that is only sufficient to fund our operations through March 2016.

As of the date of this prospectus, we had 23 full-time employees. Employees include the following five senior managers that report to the CEO: a Vice President of Operations, a Vice President of Energy Markets, a Vice President of Research & Development, a Controller and a Senior Vice President. The Company employs a total of 6 full-time scientists and technicians in its R&D group, including the Vice President of Research & Development.

4

Common stock to be offered by the Company |

|

|

|

|

|

Common stock to be offered by the selling securityholders |

|

|

|

|

|

Secondary offering price |

| The selling securityholders may sell their shares at $8.00 per share until our shares are quoted on the OTCBB, and thereafter at prevailing market prices or privately negotiated prices. We determined this offering price arbitrarily, and the selling securityholders will be able to sell their shares once the offering is effective and would theoretically have a marketplace to sell their shares. |

|

|

|

Common stock issued and outstanding before the offerings |

|

|

|

|

|

Primary offering price |

| $8.00 per share |

|

|

|

Duration of primary offering |

| 2,000,000 shares will be offered by the Company for a period of one hundred and eighty (180) days from the effective date of this prospectus. The offering shall terminate on the earlier of (i) when the offering period ends (180 days from the effective date of this prospectus), (ii) the date when the sale of all 2,000,000 shares is completed, and (iii) when the Board of Directors decides that it is in the best interest of the Company to terminate the offering prior the completion of the sale of all 2,000,000 shares registered under the Registration Statement of which this prospectus is part. |

|

|

|

Common stock issued and outstanding after the offerings after giving effect to the sale of 2,000,000 shares by the Company and 4,784,442 shares by the selling securityholders |

|

|

|

|

|

Ticker Symbol and Market for our common stock |

|

|

5

Primary offering use of |

|

|

|

|

|

Subscriptions |

| All subscriptions, once accepted by us, are irrevocable. |

|

|

|

Risk Factors |

| The common stock offered hereby involves a high degree of risk and should not be purchased by investors who cannot afford the loss of their entire investment. See “Risk Factors” beginning on page 8. |

|

|

|

Dividend policy |

| We do not intend to pay dividends on our common stock. We plan to retain any earnings for use in the operation of our business and to fund future growth. |

There is no assurance that we will raise the full $16,000,000 anticipated from the sale by the Company of 2,000,000 shares, and there is no guarantee that we will receive any proceeds from the offering. We may sell only a small portion or none of the offered primary shares.

Unless we specifically state otherwise, the share information in this prospectus is as of December 31, 2015, and reflects or assumes:

• the exchange of each Series B Unit for 2 shares of common stock;

• the exclusion of 419,750 shares of common stock issuable upon exercise of outstanding options, at a weighted average purchase price of $12.05 per share;

• the exclusion of the additional 180,250 shares of common stock reserved for issuance pursuant to our 2007 Stock OptionPlan; and

• the exclusion of the 1,072,720 shares of common stock underlying Series A Preferred Stock underlying warrants.

Emerging Growth Company

In April 2012, the Jumpstart Our Business Startups Act of 2012, or the JOBS Act, was enacted. Section 107 of the JOBS Act provides that an “emerging growth company,” or EGC, can take advantage of the extended transition period for complying with new or revised accounting standards. Thus, an EGC can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. We have irrevocably elected not to avail ourselves of this extended transition period and, as a result, we will adopt new or revised accounting standards on the relevant dates on which adoption of such standards is required for other public companies.

We are in the process of evaluating the benefits of relying on other exemptions and reduced reporting requirements under the JOBS Act. Subject to certain conditions, as an EGC, we intend to rely on certain of these exemptions, including exemptions from the requirement to provide an auditor’s attestation report on our system of internal controls over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act and from any requirement that may be adopted by the Public Company Accounting Oversight Board regarding mandatory audit firm rotation or a supplement to the auditor’s report providing additional information about the audit and the financial statements, known as the auditor discussion and analysis. We will remain an EGC until the earlier of: the last day of the fiscal year in which we have total annual gross revenues of $1.0 billion or more; the last day of the fiscal year following the fifth anniversary of the date of the completion of this offering; the date on which we have issued more than $1.0 billion in nonconvertible debt during the previous three years; or the date on which we are deemed to be a large accelerated filer under the rules of the SEC.

6

Corporate Information

The Company was incorporated in Michigan on May 23, 2006 and is organized as a “C” corporation under the applicable laws of the United States and State of Michigan. Our headquarters and principal executive offices are located at 3101 Grand Oak Drive, Lansing, Michigan, 48911 and our telephone number is (517) 703-1110. Our website address ishttp://www.xgsciences.com, although the information contained in, or that can be accessed through, our website is not part of this prospectus.

7

THE SECURITIES BEING OFFERED INVOLVE A HIGH DEGREE OF RISK AND, THEREFORE, SHOULD BE CONSIDERED EXTREMELY SPECULATIVE. THEY SHOULD NOT BE PURCHASED BY PERSONS WHO CANNOT AFFORD THE POSSIBILITY OF THE LOSS OF THEIR ENTIRE INVESTMENT. PROSPECTIVE INVESTORS SHOULD READ THE ENTIRE PROSPECTUS, INCLUDING ALL EXHIBITS, AND CAREFULLY CONSIDER, AMONG OTHER FACTORS, THE FOLLOWING RISK FACTORS.

Risks Relating to Our Business and Industry

We are a young company with a limited operating history, making it difficult for you to evaluate our business and your investment.

XG Sciences, Inc. was incorporated on May 23, 2006. We have not yet demonstrated sales of products at a level capable of covering our fixed expenses. Since inception, we have not demonstrated the capability to produce sufficient materials to generate the ongoing revenues necessary to sustain our operations in the long-term. Nor have we demonstrated the ability to generate sufficient sales to sustain the business. There can be no assurance that the Company will ever produce a profit.

Many of the Company’s products represent new products that have not yet been fully developed and for which manufacturing operations have not yet been fully scaled. This means that investors are subject to all the risks incident to the creation and development of multiple new products and their associated manufacturing processes, and each investor should be prepared to withstand a complete loss of their investment.

Because we are subject to these uncertainties, there may be risks that management has failed to anticipate and you may have a difficult time evaluating our business and your investment in our Company. Our ability to become profitable depends primarily on our ability to successfully commercialize our products in the future. Even if we successfully develop and market our products, we may not generate sufficient or sustainable revenue to achieve or sustain profitability, which could cause us to cease operations and you will lose all of your investment.

We have no sustainable base of products approved for commercial use by our customers, have never generated significant product revenues and may never achieve sufficient revenues for profitable operations, which could cause us to cease operations.

XG Sciences primarily sells bulk materials or products made with these materials to other companies for incorporation into their products. To date, there has been no significant incorporation of our materials or products into customer products that are released for commercial sale. Because there is no demonstrated history of commercial success for our products, it is possible that such commercial success may never happen and that we will never achieve the level of revenues necessary to sustain our business.

We will need to raise substantial additional capital in the future to fund our operations and we may be unable to raise such funds when needed and on acceptable terms, which could have a materially adverse effect on our business.

Developing, manufacturing and selling nanomaterials in commercially-viable quantities requires substantial funding. As of December 31, 2014, June 30, 2015 and December 31, 2015, we had cash on hand of approximately $2.1 million, $1.6 million and $1.1 million, respectively. In addition to our cash on hand, we currently have an ongoing offering of Series B Preferred Stock, but we have no assurance that we will raise any additional funds under this offering. The Company’s financial projections show that the Company may need to raise an additional $15 million or more before it is capable of achieving sustainable cash flow from operations. There is no assurance that the Company will be able to raise these funds or that the terms and conditions of future financing will be workable or acceptable for the Company and its stockholders. In the event that the Company is not able to raise substantial additional funds in the future, the Company would be forced to cease operations and you would lose all of your investment.

If we are unable to continue as a going concern, our securities will have little or no value.

The report of our independent registered public accounting firm that accompanies our consolidated financial statements for the year ended December 31, 2014 contains a going concern qualification in which such firm expressed substantial doubt about our ability to continue as a going concern. We currently anticipate that our cash and cash equivalents will be sufficient to fund

8

our operations through April 2016, without raising additional capital. Our continuation as a going concern is dependent upon continued financial support from our shareholders, the ability of us to obtain necessary equity and/or debt financing to continue operations, and the attainment of profitable operations. These factors raise substantial doubt regarding our ability to continue as a going concern. We cannot make any assurances that additional financings will be available to us and, if available, completed on a timely basis, on acceptable terms or at all. If we are unable to complete an equity or debt offering, or otherwise obtain sufficient financing when and if needed, it would negatively impact our business and operations, which would likely cause the price of our common stock to decline. It could also lead to the reduction or suspension of our operations and ultimately force us to cease our operations.

We have limited experience in the higher volume manufacturing that will be required to support profitable operations, and the risks associated with scaling to larger production quantities may be substantial.

We have limited experience manufacturing our products. We have established small-scale commercial or pilot-scale production facilities for our bulk powders, XG Leaf® and SiG materials, but these facilities do not have the existing production capacity to produce sufficient quantities of materials for us to reach sustainable sales levels. In order to develop the capacity to produce much higher volumes, it will be necessary to produce multiples of existing processes or engineer new production processes in some cases. There is no guarantee that we will be able to economically scale-up our production processes to the levels required. If we are unable to scale-up our production processes and facilities to support sustainable sales levels, we may be forced to cease operations and you will lose all of your investment.

Projection of fixed monthly expenses and operating losses for the near future means that investors may not earn a return on their investment or may lose all of their investment.

Because of the nature of the Company’s business, the Company projects considerable fixed expenses that lead to projected monthly deficits for the near future. Fixed manufacturing expenses to maintain production facilities, compensation expenses for scientists and other critical personnel, and ongoing rent and utilities amount to several hundred thousand dollars per month, and the Company believes that such expenses are required as a precursor to significant customer sales. However, there can be no assurance that monthly sales will ever reach a sufficient level to cover the cost of ongoing monthly expenses. If sufficient regular monthly sales are not generated to cover these fixed expenses, we will continue to experience monthly profit deficits which, if not eliminated, will require continuing new investment in the Company. If monthly deficits continue beyond levels that investors find tolerable, we may not be able to raise additional funds and may be forced to cease operations and you will lose all of your investment.

We have a long and complex sales cycle and have not demonstrated the ability to operate successfully in this environment.

It has been our experience since our inception that the average sales cycle for our products can range from one to seven years from the time a customer begins testing our products until the time that they could be successfully used in a commercial product. The product introduction timing will vary based on the target market, with automotive uses typically being toward the long end and consumer electronics toward the shorter end. We have not demonstrated a track record of success in completing customer development projects, which makes it difficult for you to evaluate the likelihood of our future success. The sales and development cycle for our products is subject to customer budgetary constraints, internal acceptance procedures, competitive product assessments, scientific and development resource allocations, and other factors beyond our control. If we are not able to successfully accommodate these factors to enable customer development success, we will be unable to achieve sufficient sales to reach profitability. In this case, the Company may not be able to raise additional funds and may be forced to cease operations and you will lose all of your investment.

We could be adversely affected by our exposure to customer concentration risk.

We are subject to customer concentration risk as a result of our reliance on a relatively small number of customers for a significant portion of our revenues. For 2014 and 2013 we had one customer whose revenue was 37% and 77%, respectively, of total revenues. In 2014 we also had another customer that represented 28% of total revenues. Due to the nature of our businessand the relatively large size of many of the applications our customers are developing, we anticipate that we will be dependent on a relatively small number of customers for the majority of our revenues for the next several years. It is possible that only one or two customers could place orders sufficient to utilize most or all of our existing manufacturing capacity. In this case, there would be a risk of significant loss of future revenues if one or more of these customers were to stop ordering our materials, which could in turn have a material adverse effect on our business and on your investment.

9

Our revenues often fluctuate significantly based on one-off orders from customers or from the recognition of grant revenues which vary from period-to-period, which may materially impact our financial results from period to period.

Because of the potential for large revenue swings from one-time large orders or grants it may be difficult to accurately forecast the needs for inventory, working capital, and other financial resources from period-to-period. Such orders would require a significant short-term increase in our production capacity and would require the financial resources to add staff and support the associated working capital. If such large one-time orders were not handled smoothly, customer confidence in us as a viable supplier could be reduced and we might not succeed in capturing the additional larger orders that may be reflected in our business plan.

We operate in an advanced technology arena where hypothesized properties and benefits of our products may not be achieved in practice, or in which technological change may alter the attractiveness of our products.

Because there is no sustained history of successful use of our products in commercial applications, there is no assurance that broad successful commercial applications may be technically feasible. Most, if not all, of the scientific and engineering data related to our products has been generated in our own laboratories or in laboratory environments at our customers or third-parties, like universities and national laboratories. It is well known that laboratory data is not always representative of commercial applications.

Likewise, we operate in a market that is subject to rapid technological change. Part of our business strategy is to monitor such change and take steps to remain technologically current, but there is no assurance that such strategy will be successful. If the Company is not able to adapt to new advances in materials sciences, or if unforeseen technologies or materials emerge that are not compatible with our products and services or that could replace our products and services, our revenues and business prospects would likely be adversely affected. Such an occurrence may have severe consequences, including the potential for our investors to lose all of their investment.

Competitors that are larger and better funded may cause the Company to be unsuccessful in selling its products.

The Company operates in a market that is expected to have significant competition in the future. Global research is being conducted by substantially larger companies who have greater financial, personnel, technical, and marketing resources. There can be no assurance that the Company’s strategy of offering better materials based on the Company’s proprietary exfoliated graphite nanoplatelets will be able to compete with other companies, many of whom will have significantly greater resources, on a continuing basis. In the event that we cannot compete successfully, the Company may be forced to cease operations and investors may lose some or all of their investment.

Because of our small size and limited operating history, we are dependent on key employees.

The Company’s operations and development are dependent upon the experience and knowledge of Philip L. Rose, our Chief Executive Officer, Michael R. Knox, our Senior Vice President, Dr. Liya Wang, Vice President of Research & Development, Robert Privette, Vice President of Energy Markets, Scott Murray, Vice President of Operations, Dr. Inhwan Do, Technical Director, and Dr. Hiroyuki Fukushima, Technical Director. If the services of any of these individuals should become unavailable, the Company’s business operations might be adversely affected. If several of these individuals became unavailable at the same time, the ability of the Company to continue normal business operations might be adversely affected to the extent that revenue or profits could be diminished and investors could lose some or all of their investment.

Our success depends in part on our ability to protect our intellectual property rights, and our inability to enforce these rights could have a material adverse effect on our competitive position.

We rely on the patent, trademark, copyright and trade-secret laws of the United States and the countries where we do business to protect our intellectual property rights. We may be unable to prevent third parties from using our intellectual property without our authorization. The unauthorized use of our intellectual property could reduce any competitive advantage we have developed, reduce our market share or otherwise harm our business. In the event of unauthorized use of our intellectual property, litigation to protect or enforce our rights could be costly, and we may not prevail.

Many of our technologies are not covered by any patent or patent application, and our issued and pending U.S. and non-U.S. patents may not provide us with any competitive advantage and could be challenged by third parties. Our inability to secure issuance of our pending patent applications may limit our ability to protect the intellectual property rights these pending patent applications were intended to cover. Our competitors may attempt to design around our patents to avoid liability for

10

infringement and, if successful, our competitors could adversely affect our market share. Furthermore, the expiration of our patents may lead to increased competition.

Our pending trademark applications may not be approved by the responsible governmental authorities and, even if these trademark applications are granted, third parties may seek to oppose or otherwise challenge these trademark applications. A failure to obtain trademark registrations in the United States and in other countries could limit our ability to protect our products and their associated trademarks and impede our marketing efforts in those jurisdictions.

In addition, effective patent, trademark, copyright and trade secret protection may be unavailable or limited in some foreign countries. In some countries, we do not apply for patent, trademark or copyright protection. We also rely on unpatented proprietary manufacturing expertise, continuing technological innovation and other trade secrets to develop and maintain our competitive position. Although we generally enter into confidentiality agreements with our employees and third parties to protect our intellectual property, these confidentiality agreements are limited in duration and could be breached, and may not provide meaningful protection of our trade secrets or proprietary manufacturing expertise. Adequate remedies may not be available if there is an unauthorized use or disclosure of our trade secrets and manufacturing expertise. In addition, others may obtain knowledge about our trade secrets through independent development or by legal means. The failure to protect our processes, apparatuses, technology, trade secrets and proprietary manufacturing expertise, methods and compounds could have a material adverse effect on our business by jeopardizing critical intellectual property.

Where a product formulation or process is kept as a trade secret, third parties may independently develop or invent and patent products or processes identical to our trade-secret products or processes. This could have an adverse impact on our ability to make and sell products or use such processes and could potentially result in costly litigation in which we might not prevail.

We could face intellectual property infringement claims that could result in significant legal costs and damages and impede our ability to produce key products, which could have a material adverse effect on our business, financial condition and results of operations.

If we fail to maintain effective internal controls over financial reporting, the price of our common stock may be adversely affected.

We are required to establish and maintain appropriate internal controls over financial reporting. Failure to establish those controls, or any failure of those controls once established, could adversely impact our public disclosures regarding our business, financial condition or results of operations. Any failure of these controls could also prevent us from maintaining accurate accounting records and discovering accounting errors and financial frauds. Rules adopted by the U.S. Securities and Exchange Commission (“SEC”) pursuant to Section 404 of the Sarbanes-Oxley Act of 2002 require annual assessment of our internal control over financial reporting, and the standards that must be met for management to assess the internal control over financial reporting as effective are new and complex, and require significant documentation, testing and possible remediation to meet the detailed standards. We may encounter problems or delays in completing activities necessary to make an assessment of our internal control over financial reporting. If we cannot assess our internal control over financial reporting as effective, investor confidence and share value may be negatively impacted.

In addition, management’s assessment of internal controls over financial reporting may identify weaknesses and conditions that need to be addressed in our internal controls over financial reporting or other matters that may raise concerns for investors. Any actual or perceived weaknesses and conditions that need to be addressed in our internal control over financial reporting, disclosure of management’s assessment of our internal controls over financial reporting, or disclosure of our independent registered public accounting firm’s report on management’s assessment of our internal controls over financial reporting may have an adverse impact on the price of our common stock.

Future adverse regulations could affect the viability of the business.

The Company’s bulk products have been approved for sale in the United States by the U.S. Environmental Protection Agency after a detailed review of our products and production processes for our H, M and C grade materials. In most cases, as far as we are aware, there are no current regulations elsewhere in the world that prevent or prohibit the sale of the Company’s products. Nevertheless, the sale of nano-materials is a subject of regulatory discussion and review in many countries around the world. In some cases, there is a discussion of potential testing requirements for toxicity or other health effects of nano-materials before they can be sold in certain jurisdictions. If such regulations are enacted in the future, the Company’s business could be adversely affected because of the requirement for expensive and time-consuming tests or other regulatory compliance. There can be no assurance that future regulations might not severely limit or even prevent the sale of the Company’s products in major markets, in which case the Company’s financial prospects might be severely limited, causing investors to lose some or all of their investment.

11

Compliance with changing regulation of corporate governance and public disclosure will result in additional expenses and will divert time and attention away from revenue generating activities.

Changing laws, regulations and standards relating to corporate governance and public disclosure, including the Sarbanes-Oxley Act of 2002 and related SEC regulations, have created uncertainty for public companies and significantly increased the costs and risks associated with accessing the public markets and public reporting. Our management team will need to invest significant management time and financial resources to comply with both existing and evolving standards for public companies, which will lead to increased general and administrative expenses and a diversion of management time and attention from revenue generating activities to compliance activities, which could have an adverse effect on our business.

Risks Relating To Our Common Stock

There is a risk of dilution of your percentage ownership of common stock in the Company.

In addition to the shares which we may sell pursuant to this offering, the Company has the right to raise additional capital or incur borrowings from third parties to finance its business. The Company may also implement public or private mergers, business combinations, business acquisitions and similar transactions pursuant to which it would issue substantial additional capital stock to outside parties, causing substantial dilution in the ownership of the Company by its existing stockholders. Our Board of Directors has the authority, without the consent of any of the stockholders, to cause the Company to issue more shares of common stock and/or preferred stock at such price and on such terms and conditions as are determined by the Board in its sole discretion.

The sale of the shares being offered by us hereunder, as well as the shares of common stock and Series A Preferred Stock issuable upon the exercise of warrants, the shares issuable upon conversion of Series A Preferred Stock, the shares issuable upon the exercise of options and warrants, shares of Series A Preferred Stock which were issued upon the conversion of secured convertible notes on December 31, 2015, shares issuable upon conversion of Series B Preferred Stock, shares issuable upon exchange of the Series B Units, and the issuance of additional shares of capital stock by the Company will dilute your ownership percentage in the Company and could impair our ability to raise capital in the future through the sale of equity securities.

Certain stockholders who are also officers and directors of the Company may have significant control over our management, which may not be in your best interests.

The directors, or the entities they represent, and executive officers of the Company owned more than 44% of the voting stock of the Company on December 31, 2015. Furthermore, these same executives and directors, or the companies they represent, converted secured convertible notes into an additional 1,456,128 shares of the Series A Preferred Stock in the Company on December 31, 2015. As of December 31, 2015, assuming the sale of no additional new equity before then, the percentage of common stock controlled by directors, or the companies they represent, and officers of the Company represented approximately 72% of total voting stock outstanding. As a result, such entities have a significant influence on the affairs and management of the Company, as well as on all matters requiring stockholder approval, including electing and removing members of the Company’s Board of Directors, causing the Company to engage in transactions with affiliated entities, causing or restricting the sale or merger of the Company, and certain other matters. Such concentration of ownership and control could have the effect of delaying, deferring or preventing a change in control of the Company even when such a change of control would be in the best interests of the Company’s stockholders.

We may, in the future, issue additional shares of common stock, which would reduce investors’ percent of ownership and may dilute our share value.

Our Articles of Incorporation, as amended, authorize the issuance of up to 25,000,000 shares of common stock and up to 8,000,000 shares of preferred stock. As of December 31, 2015, the Company had 836,544 shares of common stock, 1,800,696 shares of Series A Preferred Stock and 269,987 shares of Series B Preferred Stock issued and outstanding. We intend to convert our Series A Preferred Stock at a per share ratio of 1.875 to 1, which would result in a post-conversion common stock underlying Series A Preferred Stock of 3,376,299 shares. In addition to the 269,987 shares of Series B Preferred Stock issued, holders of Series B Preferred Stock have the right, at their discretion, to exchange each Series B Unit for two shares of common stock which result in the issuance of 539,974 shares of common stock. As of the date of this prospectus, no Series B Unit holder has exchanged their Series B Units into shares of common stock.

In addition, all outstanding secured convertible notes converted into 1,456,126 shares of Series A Preferred Stock on December 31, 2015. As of December 31, 2015, the Company had also granted options to purchase up to 419,750 shares of

12

common stock and had issued warrants to purchase up to 256,522 shares of common stock and 1,072,720 shares of Series A Preferred Stock. Each holder of a Series B Unit will exchange his, her or its Series B Unit for two shares of the Company’s common stock in accordance with the terms of the Certificate of Designations of Series B Convertible Preferred Stock (“Series B Designations”), which will result in an additional issuance of common stock of 539,974 shares. In total, therefore, we have already issued or committed to issue up to 6,276,912 shares of common stock (assuming the exchange of Series B Preferred Stock and the conversion of Series A Preferred Stock) and we are authorized to issue up to 18,723,088 additional shares of common stock. The future issuance of common stock may result in substantial dilution in the percentage of our common stock held by our then existing stockholders. We may value any common stock issued in the future on an arbitrary basis. The issuance of common stock for future services or acquisitions or other corporate actions may have the effect of diluting the value of the shares held by our investors, might have an adverse effect on any trading market for our common stock and could impair our ability to raise capital in the future through the sale of equity securities.

We have a large number of restricted shares outstanding, a portion of which may be sold under Rule 144, which may reduce the market price of our shares.

Of the 836,544 shares of common stock issued and outstanding as of December 31, 2015, the 1,800,696 outstanding shares of Series A Preferred Stock and the 269,987 shares of Series B Preferred Stock that we intend to convert into shares of common stock upon the listing of our common stock on a Qualified National Exchange (as defined in the Certificate of Designations of Series A Convertible Preferred Stock “Series A Designations”, see also “Description of Securities — Preferred Stock”), and assuming no notes, warrants or stock options are converted or exercised, 762,770 shares are held by non-affiliates and 2,144,547 are held by affiliates of the Company. The 2,144,547 shares held by affiliates are deemed “restricted securities” within the meaning of Rule 144 as promulgated under the Securities Act. Our Series A Preferred Stock will be converted at a per share ratio of 1.875 to 1, which would result in a post-conversion common stock underlying Series A Preferred Stock of 3,376,299 shares. In addition to the 269,987 shares of Series B Preferred Stock issued, holders of Series B Preferred Stock have the right, at their discretion, to exchange each Series B Unit for two shares of common stock which result in the issuance of 539,974 shares of common stock.

It is anticipated that all of the “restricted securities” will be eligible for resale under Rule 144. In general, under Rule 144, subject to the satisfaction of certain other conditions, a person, who is not an affiliate (and who has not been an affiliate for a period of at least three months immediately preceding the sale) and who has beneficially owned restricted shares of our common stock for at least six months is permitted to sell such shares without restriction, provided that there is sufficient public information about us as contemplated by Rule 144. An affiliate who has beneficially owned restricted shares of our common stock for a period of at least one year may sell a number of shares equal to one percent of our issued and outstanding common stock approximately every three months.

The possibility that substantial amounts of our common stock may be sold under Rule 144 into the public market may adversely affect prevailing market prices for the common stock and could impair our ability to raise capital in the future through the sale of equity securities.

The Company is considered a smaller reporting company and is exempt from certain disclosure requirements, which could make our stock less attractive to potential investors.

Rule 12b-2 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) defines a “smaller reporting company” as an issuer that is not an investment company, an asset-backed issuer, or a majority-owned subsidiary of a parent that is not a smaller reporting company and that:

• Had a public float of less than $75 million as of the last business day of its most recently completed second fiscal quarter, computed by multiplying the aggregate worldwide number of shares of its voting and non-voting common equity held by non-affiliates by the price at which the common equity was last sold, or the average of the bid and asked prices of common equity, in the principal market for the common equity; or

• In the case of an initial registration statement under the Securities Act or Exchange Act for shares of its common equity, had a public float of less than $75 million as of a date within 30 days of the date of the filing of the registration statement, computed by multiplying the aggregate worldwide number of such shares held by non-affiliates before the registration plus, in the case of a Securities Act registration statement, the number of such shares included in the registration statement by the estimated public offering price of the shares; or

13

• In the case of an issuer whose public float as calculated under paragraph (1) or (2) of this definition was zero, had annual revenues of less than $50 million during the most recently completed fiscal year for which audited financial statements are available.

As a “smaller reporting company” (in addition to and without regard to our status as an “emerging growth company”) we are not required and may not include a “Compensation Discussion and Analysis” section in our proxy statements; we provide only 3 years of business development information; provide fewer years of selected financial data; and have other “scaled” disclosure requirements that are less comprehensive than issuers that are not “smaller reporting companies” which could make our stock less attractive to potential investors, which could make it more difficult for you to sell your shares.

The Company is considered an “emerging growth company” and we cannot be certain if the reduced disclosure requirements applicable to emerging growth companies will make our common stock less attractive to investors.

We are an “emerging growth company,” as defined in the Jumpstart our Business Startups Act of 2012, and we may take advantage of certain exemptions from various reporting requirements that are applicable to other public companies, including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act, reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements, and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved.

We will remain an emerging growth company until the earlier of (i) the last day of the fiscal year (A) following the fifth anniversary of our first sale of common equity securities pursuant to an effective registration statement, (B) in which we have total annual gross revenue of at least $1.0 billion, or (C) the date that we become a “large accelerated filer” as defined in Rule 12b-2 under the Exchange Act, which would occur if the market value of our common stock that is held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter, and (ii) the date on which we have issued more than $1.0 billion in non-convertible debt during the prior three-year period.

We cannot predict if investors will find our common stock less attractive because we may rely on these exemptions. If some investors find our common stock less attractive as a result, there may be a less active trading market for our common stock and our stock price may be more volatile when trading occurs.

We will become subject to the periodic reporting requirements of the Exchange Act, which will require us to incur audit fees and legal fees in connection with the preparation of such reports. These additional costs will negatively affect our ability to earn a profit.

Following the effective date of the registration statement in which this prospectus is included, we will be required to file periodic reports with the Securities and Exchange Commission pursuant to the Exchange Act and the rules and regulations thereunder. In order to comply with such requirements, our independent registered auditors will have to review our financial statements on a quarterly basis and audit our financial statements on an annual basis. Moreover, our legal counsel will have to review and assist in the preparation of such reports. Factors such as the number and type of transactions that we engage in and the complexity of our reports cannot accurately be determined at this time and may have a major negative effect on the cost and amount of time to be spent by our auditors and attorneys. However, the incurrence of such costs will be an expense to our operations and thus have a negative effect on our ability to meet our overhead requirements and earn a profit.

However, for as long as we remain an “emerging growth company” we intend to take advantage of certain exemptions from various reporting requirements until we are no longer an “emerging growth company.”

We also qualify as a smaller reporting company, and so long as we remain a smaller reporting company, we benefit from the same exemptions and exclusions as an emerging growth company. In the event that we cease to be an emerging growth company as a result of a lapse of the five year period, but continue to be a smaller reporting company, we would continue to be subject to the exemptions available to emerging growth companies until such time as we were no longer a smaller reporting company.

After, and if ever, we are no longer an “emerging growth company,” we expect to incur significant additional expenses and devote substantial management effort toward ensuring compliance with those requirements applicable to companies that are not “emerging growth companies,” including Section 404 of the Sarbanes-Oxley Act.

14

For so long as we are an emerging growth company, we may rely on certain exemptions provided in the JOBS Act, including reduced disclosure regarding executive compensation, not seeking an advisory vote with respect to executive compensation and not requiring our independent registered public accounting firm to attest to the effectiveness of our internal control over financial reporting, which could make our common stock less attractive to investors due to the nature of the reduced disclosure.

We are an “emerging growth company,” as defined in the JOBS Act, and may remain an emerging growth company for up to five years. For so long as we remain an emerging growth company, we are permitted and plan to rely on exemptions from certain disclosure requirements that are applicable to other public companies that are not emerging growth companies. These exemptions include not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002, or SOX Section 404, not being required to comply with any requirement that may be adopted by the Public Company Accounting Oversight Board regarding mandatory audit firm rotation or a supplement to the auditor’s report providing additional information about the audit and the financial statements, reduced disclosure obligations regarding executive compensation and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved. In this prospectus, we have provided only two years of audited financial statements and have not included all of the executive compensation related information that would be required if we were not an emerging growth company. We cannot predict whether investors will find our common stock less attractive if we rely on these exemptions. If some investors find our common stock less attractive as a result, there may be a less active trading market for our common stock and our stock price may be more volatile.

In addition, the JOBS Act provides that an emerging growth company can take advantage of an extended transition period for complying with new or revised accounting standards. This allows an emerging growth company to delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. We have irrevocably elected not to avail ourselves of this exemption from new or revised accounting standards and, therefore, we will be subject to the same new or revised accounting standards as other public companies that are not emerging growth companies.

If securities or industry analysts do not publish research or reports or publish unfavorable research about our business, the price and trading volume of our common stock could decline.

The trading market for our common stock will depend in part on the research and reports that securities or industry analysts publish about us or our business. We do not currently have and may never obtain research coverage by securities and industry analysts. If no securities or industry analysts commence coverage of us, the trading price for our common stock and other securities would be negatively affected. In the event we obtain securities or industry analyst coverage, if one or more of the analysts who covers us downgrades our securities, the price of our securities would likely decline. If one or more of these analysts ceases to cover us or fails to publish regular reports on us, interest in the purchase of our securities could decrease, which could cause the price of our common stock and other securities and their trading volume to decline.

Because our common stock is “penny stock,” you may have greater difficulty selling your shares.

Penny stocks are generally equity securities with a price of less than $5.00, other than securities registered on certain national securities exchanges or quoted on the Nasdaq system, provided that current price and volume information with respect to transactions in such securities is provided by the exchange or quotation system. Because our securities constitute “penny stocks” within the meaning of the rules, the rules apply to us and to our securities. The rules may further affect the ability of owners of shares to sell our securities in any market that might develop for them. As long as the trading price of our common stock is less than $5.00 per share, even if our common stock is quoted on the OTCBB or the OTC Markets, the common stock will be subject to Rule 15g-9 under the Exchange Act. The penny stock rules require a broker-dealer, prior to a transaction in a penny stock, to deliver a standardized risk disclosure document prepared by the SEC, that:

• contains a description of the nature and level of risk in the market for penny stocks in both public offerings and secondary trading;

• contains a description of the broker’s or dealer’s duties to the customer and of the rights and remedies available to the customer with respect to a violation to such duties or other requirements of securities laws;

• contains a brief, clear, narrative description of a dealer market, including bid and ask prices for penny stocks and the significance of the spread between the bid and ask price;

• contains a toll-free telephone number for inquiries on disciplinary actions;

15

• defines significant terms in the disclosure document or in the conduct of trading in penny stocks; and

• contains such other information and is in such form, including language, type, size and format, as the SEC shall require by rule or regulation.

The broker-dealer also must provide, prior to effecting any transaction in a penny stock, the customer with: (a) bid and offer quotations for the penny stock; (b) the compensation of the broker-dealer and its salesperson in the transaction; (c) the number of shares to which such bid and ask prices apply, or other comparable information relating to the depth and liquidity of the market for such stock; and (d) a monthly account statements showing the market value of each penny stock held in the customer’s account. In addition, the penny stock rules require that prior to a transaction in a penny stock not otherwise exempt from those rules; the broker-dealer must make a special written determination that the penny stock is a suitable investment for the purchaser and receive the purchaser’s written acknowledgment of the receipt of a risk disclosure statement, a written agreement to transactions involving penny stocks, and a signed and dated copy of a written suitably statement. These disclosure requirements may have the effect of reducing the trading activity in the secondary market for our stock.

Because we do not intend to pay any cash dividends on our common stock, our stockholders will not be able to receive a return on their shares unless they sell them.

We intend to retain any future earnings to finance the development and expansion of our business. We do not anticipate paying any cash dividends on our common stock in the foreseeable future. Unless we pay dividends, our stockholders will not be able to receive a return on their shares unless they sell them. There is no assurance that stockholders will be able to sell shares when desired.

Downturns in general economic conditions could adversely affect our profitability.

Downturns in general economic conditions can cause fluctuations in demand for our products, product prices, volumes and gross margins. Future economic conditions may not be favorable to our industry. A decline in the demand for our products or a shift to lower-margin products due to deteriorating economic conditions could adversely affect sales of our products and our profitability and could also result in impairments of certain of our assets.

Furthermore, any uncertainty in economic conditions may result in a slowdown to the global economy that could affect our business by reducing the prices that our customers may be able or willing to pay for our products or by reducing the demand for our products.