Exhibit 99.1

PRO FORMA VALUATION REPORT

FIRST SAVINGS FINANCIAL GROUP, INC

Clarksville, Indiana

PROPOSED HOLDING COMPANY FOR:

FIRST SAVINGS BANK, F.S.B.

Clarksville, Indiana

Dated As Of:

May 16, 2008

Prepared By:

RP® Financial, LC.

1700 North Moore Street

Suite 2210

Arlington, Virginia 22209

RP® FINANCIAL, LC. | ||||

| Financial Services Industry Consultants |

May 16, 2008

Board of Directors

First Savings Bank, F.S.B.

501 East Lewis & Clark Parkway

Clarksville, IN 47129

Members of the Board of Directors:

At your request, we have completed and hereby provide an independent appraisal ("Appraisal") of the estimated pro forma market value of the common stock which is to be issued in connection with the mutual-to-stock conversion transaction described below.

This Appraisal is furnished pursuant to the conversion regulations promulgated by the Office of Thrift Supervision (“OTS”). Specifically, this Appraisal has been prepared in accordance with the “Guidelines for Appraisal Reports for the Valuation of Savings and Loan Associations Converting from Mutual to Stock Form of Organization” as set forth by the OTS, and applicable regulatory interpretations thereof.

Description of Plan of Conversion

The Board of Directors of First Savings Bank, F.S.B., Clarksville, Indiana (“First Savings” or the “Bank”) adopted the plan of conversion on April 30, 2008, incorporated herein by reference. Pursuant to the plan of conversion, the Bank will convert from a federally-chartered mutual savings bank to a federally-chartered stock savings bank and become a wholly-owned subsidiary of First Savings Financial Group, Inc. (“FSFG” or the “Company”), a newly formed Indiana corporation. FSFG will offer 100% of its common stock in a subscription offering to Eligible Account Holders, the Employee Stock Ownership Plan (the “ESOP”), Supplemental Eligible Account Holders and Other Members, as such terms are define for purposes of applicable federal regulatory guidelines governing mutual-to-stock conversions. To the extent that shares remain available for purchase after satisfaction of all subscriptions received in the subscription offering, the shares may be offered for sale to members of the general public in a community offering and/or a syndicated community offering. Going forward, FSFG will own 100% of the Bank's stock, and the Bank will initially be FSFG’s sole subsidiary. A portion of the net proceeds received from the sale of the common stock will be used to purchase all of the then to be issued and outstanding capital stock of the Bank and the balance of the net proceeds will be retained by the Company.

Washington Headquarters Rosslyn Center 1700 North Moore Street, Suite 2210 Arlington, VA 22209 www.rpfinancial.com |

Telephone: (703) 528-1700 Fax No.: (703) 528-1788 Toll-Free No.: (866) 723-0594 E-Mail: mail@rpfinancial.com |

Board of Directors

May 16, 2008

Page 2

At this time, no other activities are contemplated for the Company other than the ownership of the Bank, a loan to the newly-formed ESOP and reinvestment of the proceeds that are retained by the Company. In the future, FSFG may acquire or organize other operating subsidiaries, diversify into other banking-related activities, pay dividends or repurchase its stock, although there are no specific plans to undertake such activities at the present time.

Concurrent with the Conversion, the Bank will form a charitable foundation called the First Savings Charitable Foundation (the “Foundation”). The Bank will make a contribution to the Foundation of $1.2 million, consisting of $100,000 of cash plus 110,000 shares of conversion stock with a value of $1.1 million based on the $10.00 per share IPO price.

RP® Financial, LC.

RP® Financial, LC. (“RP Financial”) is a financial consulting firm serving the financial services industry nationwide that, among other things, specializes in financial valuations and analyses of business enterprises and securities, including the pro forma valuation for savings institutions converting from mutual-to-stock form. The background and experience of RP Financial is detailed in Exhibit V-1. We believe that, except for the fee we will receive for our appraisal, we are independent of the Bank and the other parties engaged by the Bank to assist in the corporate reorganization and stock issuance process.

Valuation Methodology

In preparing our appraisal, we have reviewed the Bank’s and the Company’s regulatory applications, including the prospectus as filed with the OTS and the Securities and Exchange Commission (“SEC”). We have conducted a financial analysis of the Bank that has included due diligence related discussions with First Savings’ management; Monroe Shine & Company, Inc., the Bank’s independent auditor; Kilpatrick Stockton, LLP, First Savings’ conversion counsel; and Keefe, Bruyette & Woods, Inc., which has been retained as the financial and marketing advisor in connection with the Bank’s stock offering. All conclusions set forth in the Appraisal were reached independently from such discussions. In addition, where appropriate, we have considered information based on other available published sources that we believe are reliable. While we believe the information and data gathered from all these sources are reliable, we cannot guarantee the accuracy and completeness of such information.

We have investigated the competitive environment within which First Savings operates and have assessed the Bank’s relative strengths and weaknesses. We have monitored all material regulatory and legislative actions affecting financial institutions

Board of Directors

May 16, 2008

Page 3

generally and analyzed the potential impact of such developments on First Savings and the industry as a whole to the extent we were aware of such matters. We have analyzed the potential effects of the stock conversion on the Bank’s operating characteristics and financial performance as they relate to the pro forma market value of FSFG. We have reviewed the economy and demographic characteristics of the primary market area in which the Bank currently operates. We have compared First Savings’ financial performance and condition with publicly-traded thrift institutions evaluated and selected in accordance with the Valuation Guidelines, as well as all publicly-traded thrifts and thrift holding companies. We have reviewed conditions in the securities markets in general and the market for thrifts and thrift holding companies, including the market for new issues.

The Appraisal is based on First Savings’ representation that the information contained in the regulatory applications and additional information furnished to us by the Bank and its independent auditors, legal counsel, investment bankers and other authorized agents are truthful, accurate and complete. We did not independently verify the financial statements and other information provided by the Bank, or its independent auditors, legal counsel, investment bankers and other authorized agents nor did we independently value the assets or liabilities of the Bank. The valuation considers First Savings only as a going concern and should not be considered as an indication of the Bank’s liquidation value.

Our appraised value is predicated on a continuation of the current operating environment for the Bank and the Company and for all thrifts and their holding companies. Changes in the local and national economy, the federal and state legislative and regulatory environments for financial institutions and mutual holding companies, the stock market, interest rates, and other external forces (such as natural disasters or significant world events) may occur from time to time, often with great unpredictability, and may materially impact the value of thrift stocks as a whole or the Bank’s value alone. It is our understanding that First Savings intends to remain an independent institution and there are no current plans for selling control of the Bank as a converted institution. To the extent that such factors can be foreseen, they have been factored into our analysis.

The estimated pro forma market value is defined as the price at which the Company’s stock, immediately upon completion of the offering, would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or sell and both having reasonable knowledge of relevant facts.

Valuation Conclusion

It is our opinion that, as of May 16, 2008, the aggregate pro forma market value of the Company’s common stock, including the stock portion of the contribution to the Foundation immediately following the offering, is $32,000,000 at the midpoint, equal to

Board of Directors

May 16, 2008

Page 4

3,200,000 shares issued at a per share value of $10.00. The resulting range of value pursuant to regulatory guidelines and the corresponding number of shares based on the Board approved $10.00 per share offering price is set forth below.

Valuation Range | Offering Amount | Foundation Shares | Total Issued | ||||||

Shares | |||||||||

Minimum | 2,626,500 | 110,000 | 2,736,500 | ||||||

Midpoint | 3,090,000 | 110,000 | 3,200,000 | ||||||

Maximum | 3,553,500 | 110,000 | 3,663,500 | ||||||

Supermaximum | 4,086,525 | 110,000 | 4,196,525 | ||||||

Value | |||||||||

Minimum | $ | 26,265,000 | $ | 1,100,000 | $ | 27,365,000 | |||

Midpoint | $ | 30,900,000 | $ | 1,100,000 | $ | 32,000,000 | |||

Maximum | $ | 35,535,000 | $ | 1,100,000 | $ | 36,635,000 | |||

Supermaximum | $ | 40,865,250 | $ | 1,100,000 | $ | 41,965,250 | |||

Limiting Factors and Considerations

The valuation is not intended, and must not be construed, as a recommendation of any kind as to the advisability of purchasing shares of the common stock. Moreover, because such valuation is determined in accordance with applicable OTS regulatory guidelines and is necessarily based upon estimates and projections of a number of matters, all of which are subject to change from time to time, no assurance can be given that persons who purchase shares of common stock in the conversion will thereafter be able to buy or sell such shares at prices related to the foregoing valuation of the estimated pro forma market value thereof. The appraisal reflects only a valuation range as of this date for the pro forma market value of FSFG immediately upon issuance of the stock and does not take into account any trading activity with respect to the purchase and sale of common stock in the secondary market on the date of issuance of such securities or at anytime thereafter following the completion of the public stock offering.

The valuation prepared by RP Financial in accordance with applicable OTS regulatory guidelines was based on the financial condition and operations of First Savings as of March 31, 2008, the date of the financial data included in the prospectus.

RP Financial is not a seller of securities within the meaning of any federal and state securities laws and any report prepared by RP Financial shall not be used as an

Board of Directors

May 16, 2008

Page 5

offer or solicitation with respect to the purchase or sale of any securities. RP Financial maintains a policy which prohibits RP Financial, its principals or employees from purchasing stock of its financial institution clients.

The valuation will be updated as provided for in the OTS conversion regulations and guidelines. These updates will consider, among other things, any developments or changes in the financial performance and condition of First Savings, management policies, and current conditions in the equity markets for thrift stocks, both existing issues and new issues. These updates may also consider changes in other external factors which impact value including, but not limited to: various changes in the federal and state legislative and regulatory environments for financial institutions, the stock market and the market for thrift stocks, and interest rates. Should any such new developments or changes be material, in our opinion, to the valuation of the shares, appropriate adjustments to the estimated pro forma market value will be made. The reasons for any such adjustments will be explained in the update at the date of the release of the update.

| Respectfully submitted, |

| RP® FINANCIAL, LC. |

| /s/ James P. Hennessey |

| James P. Hennessey |

| Director |

| RP® Financial, LC. | TABLE OF CONTENTS | |

| i |

TABLE OF CONTENTS

FIRST SAVINGS FINANCIAL GROUP, INC.

FIRST SAVINGS BANK, F.S.B.

Clarksville, Indiana

DESCRIPTION | PAGE NUMBER | |||

| CHAPTER ONE | OVERVIEW AND FINANCIAL ANALYSIS | |||

Introduction | I.1 | |||

Plan of Conversion | I.1 | |||

Establishment of a Charitable Foundation | I.2 | |||

Strategic Overview | I.2 | |||

Balance Sheet Trends | I.6 | |||

Income and Expense Trends | I.10 | |||

Impact of Freeze/Termination of Defined Benefit Pension Plan | I.15 | |||

Interest Rate Risk Management | I.16 | |||

Lending Activities and Strategy | I.17 | |||

Asset Quality | I.21 | |||

Funding Composition and Strategy | I.22 | |||

Subsidiaries | I.23 | |||

Legal Proceedings | I.23 | |||

| CHAPTER TWO | MARKET AREA | |||

Introduction | II.1 | |||

National Economic Factors | II.2 | |||

Market Area Demographics | II.4 | |||

Local Economy | II.6 | |||

Unemployment Trends | II.8 | |||

Market Area Deposit Characteristics and Competition | II.9 | |||

| CHAPTER THREE | PEER GROUP ANALYSIS | |||

Peer Group Selection | III.1 | |||

Financial Condition | III.7 | |||

Income and Expense Components | III.10 | |||

Loan Composition | III.13 | |||

Credit Risk | III.15 | |||

Interest Rate Risk | III.17 | |||

Summary | III.19 | |||

| RP® Financial, LC. | TABLE OF CONTENTS | |

| ii |

TABLE OF CONTENTS

FIRST SAVINGS FINANCIAL GROUP, INC.

FIRST SAVINGS BANK, F.S.B.

Clarksville, Indiana

(continued)

DESCRIPTION | PAGE NUMBER | |||

| CHAPTER FOUR | VALUATION ANALYSIS | |||

Introduction | IV.1 | |||

Appraisal Guidelines | IV.1 | |||

RP Financial Approach to the Valuation | IV.1 | |||

Valuation Analysis | IV.2 | |||

1. Financial Condition | IV.3 | |||

2. Profitability, Growth and Viability of Earnings | IV.4 | |||

3. Asset Growth | IV.6 | |||

4. Primary Market Area | IV.6 | |||

5. Dividends | IV.8 | |||

6. Liquidity of the Shares | IV.9 | |||

7. Marketing of the Issue | IV.9 | |||

A. The Public Market | IV.10 | |||

B. The New Issue Market | IV.17 | |||

C. The Acquisition Market | IV.18 | |||

8. Management | IV.21 | |||

9. Effect of Government Regulation and Regulatory Reform | IV.22 | |||

Summary of Adjustments | IV.22 | |||

Valuation Approaches | IV.22 | |||

1. Price-to-Earnings ("P/E") | IV.24 | |||

2. Price-to-Book ("P/B") | IV.25 | |||

3. Price-to-Assets ("P/A") | IV.26 | |||

Comparison to Recent Offerings | IV.26 | |||

Valuation Conclusion | IV.27 | |||

| RP® Financial, LC. | LIST OF TABLES | |

| iii |

LIST OF TABLES

FIRST SAVINGS FINANCIAL GROUP, INC.

FIRST SAVINGS BANK, F.S.B.

Clarksville, Indiana

TABLE | DESCRIPTION | PAGE | ||

| 1.1 | Historical Balance Sheet Data | I.7 | ||

| 1.2 | Historical Income Statements | I.11 | ||

| 2.1 | Summary Demographic Data | II.5 | ||

| 2.2 | Southern Indiana Major Employers | II.7 | ||

| 2.3 | Primary Market Area Employment Sectors | II.8 | ||

| 2.4 | Unemployment Trends | II.9 | ||

| 2.5 | Deposit Summary | II.10 | ||

| 2.6 | Market Area Deposit Competitors | II.11 | ||

| 3.1 | Peer Group of Publicly-Traded Thrifts | III.4 | ||

| 3.2 | Balance Sheet Composition and Growth Rates | III.8 | ||

| 3.3 | Income as a Pct. of Avg. Assets and Yields, Costs, Spreads | III.11 | ||

| 3.4 | Loan Portfolio Composition and Related Information | III.14 | ||

| 3.5 | Credit Risk Measures and Related Information | III.16 | ||

| 3.6 | Interest Rate Risk Measures and Net Interest Income Volatility | III.18 | ||

| 4.1 | Peer Group Market Area Comparative Analysis | IV.7 | ||

| 4.2 | Pricing Characteristics and After-Market Trends | IV.19 | ||

| 4.3 | Market Pricing Comparatives | IV.20 | ||

| 4.4 | Public Market Pricing | IV.29 | ||

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.1 |

I. OVERVIEW AND FINANCIAL ANALYSIS

Introduction

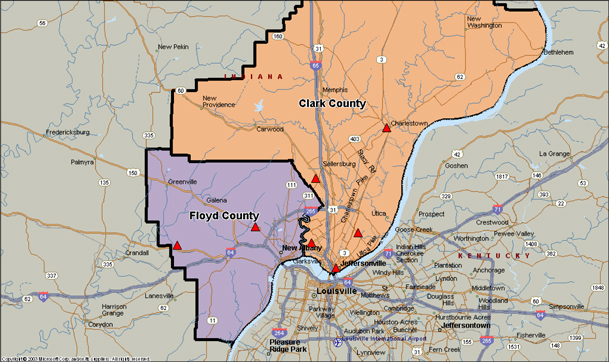

The background of First Savings Bank, F.S.B. (“First Savings” or the “Bank”) dates back to 1937 when First Savings was organized as a federal chartered savings and loan association with the name First Federal Savings and Loan Association of Jeffersonville. The Bank changed its name to First Savings Bank, F.S.B. in 1996, and changed its charter from a federal savings and loan association to a federal savings bank. With the mutual to stock conversion in 2008, the Bank will organize a holding company to be named First Savings Financial Group, Inc. (“FSFG” or the “Company”). In addition to the Bank’s main office, the Bank operates two branch offices in Jeffersonville, and single office locations in Charlestown, Sellersburg, Floyds Knobs and Georgetown, Indiana. The main office and 4 of the Bank’s branches are located in Clark County and 2 branches are located in Floyd County. Located along the northern shore of the Ohio River, Clark and Floyd Counties are situated across the Ohio River from Louisville, Kentucky, and are within the Louisville metropolitan area. A map of the Bank’s branch offices is provided in the analysis of the Bank’s market area. First Savings is a member of the Federal Home Loan Bank ("FHLB") system, and its deposits are insured up to the regulatory maximums by the Federal Deposit Insurance Corporation ("FDIC"). At March 31, 2008, First Savings had $212.6 million in assets, $174.1 million in deposits and total equity of $29.4 million equal to 13.8% of total assets. First Savings’ audited financial statements are included by reference as Exhibit I-1.

Plan of Conversion

The Board of Directors of the Bank adopted a plan to reorganize from the mutual form of organization to the stock form of organization within a holding company structure (the “Plan”) on April 30, 2008. As part of the reorganization, the Bank will become a wholly-owned subsidiary of FSFG, an Indiana Corporation which will be formed as part of the Conversion. FSFG will issue all of its common stock to the public. Concurrent with the Conversion, the Company will retain up to 50% of the net offering

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.2 |

proceeds and infuse the balance of the net proceeds into the Bank. It is not anticipated that the Company will initially engage in any business activity other than ownership of the Bank subsidiary.

Pursuant to the Plan, the Company will offer the public shares of common stock in a subscription offering to Eligible Account Holders, Tax-Qualified Employee Benefit Plans, Supplemental Eligible Account Holders, and other members of the Bank. Upon completion of the subscription offering, any shares of common stock not subscribed for in the subscription offering will be offered in a direct community offering and potentially a syndicated community offering.

Establishment of a Charitable Foundation

In order to enhance the historically strong community service and reinvestment activities of the Bank, the Company will establish the First Savings Charitable Foundation, Inc. (the “Foundation”), a private charitable foundation, in connection with the Offering. The Company will make a contribution to the Foundation equal to $1.2 million, consisting of $100,000 of cash plus 110,000 shares of conversion stock with a value of $1.1 million based on the $10.00 per share IPO price. The Foundation’s charitable giving is intended to complement the Bank’s existing community reinvestment activities, and will be dedicated to help fund local projects and to support certain civic, charitable and cultural organizations within the communities served by the Bank. The Bank believes the Foundation will enhance its already strong reputation for community service. The Foundation’s ownership of the Company’s stock will enable the local community served to share in the potential increase in market value and dividends over time.

Strategic Overview

Throughout much of its corporate history, the Bank’s strategic focus has been that of a community oriented financial institution with a primary focus on meeting the borrowing, savings and other financial needs of its local customers in Clark and Floyd counties, and other nearby areas in southern Indiana and northern Kentucky, generally

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.3 |

within the Louisville metropolitan area. In this regard, the Bank has historically pursued a portfolio residential lending strategy typical of a thrift institution, with the primary avenue of loan diversification being construction lending.

Commencing early in the current decade, the Bank sought to mitigate the balance sheet and earnings impact of loan runoff which resulted from high prepayment rates within the fixed rate 1-4 family mortgage loan portfolio by undertaking greater investment in commercial real estate lending. Additionally, in an effort to further stem the impact of loan portfolio shrinkage, First Savings also originated 1-4 mortgage loans to investors secured by properties in the local market. While the loans to investors typically carried relatively strong interest yields and short-to-intermediate term repricing structures, they have also had a relatively high rate of delinquency and chargeoff as the Bank’s market has been impacted by a weak residential housing market, particularly in the low-to-moderate income segment which characterized the collateral properties within the investor loan portfolio. Management estimates that approximately 28.0% of the residential mortgage loan portfolio is non-owner occupied as of March 31, 2008.

Commencing with the employment of the current managing officer in fiscal 2006, the Bank sought to gradually reorient the Bank’s business plan to one more reflective of a full service community banking organization. Such efforts were intensified with the employment of the current chief lending officer (“CLO”) in latter half of 2006 who also possessed substantial commercial lending experience within a commercial banking environment in the Bank’s Louisville area markets. Reflecting the reorientation of the Bank’s operations, the Bank’s lending operations consist of two principal segments as follows: (1) residential mortgage lending; and (2) commercial and construction lending in conjunction with the intensified efforts to become a full-service community bank. In this regard, the Bank has emphasized high quality and flexible service, capitalizing on its local orientation and expanded array of products and services.

With this transition in recent years, the Bank has sought to develop the infrastructure to undertake the broad-based community banking strategy it is seeking to implement. In this regard, management has revamped the policies and procedures pertaining to credit standards and the administration of commercial accounts.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.4 |

Additionally, the Bank employs a total of four loan officers including the CLO who have local mortgage lending experience (including several with commercial lending experience) to conduct the broad-based lending operations while also developing the appropriate support functions in the loan underwriting, credit administration and loan servicing functions. Concurrent with the revamping of the lending function, the Bank has also been seeking to develop a more effective sales culture with respect to all key customer contact points within First Savings while it has also been evaluating potential de novo branching opportunities for the future, to more fully exploit the potential of its market and to provide superior access and service to its targeted customers.

In summary, the post-offering business plan of the Bank is expected to continue to focus on products and services which have been the Bank’s traditional emphasis. Specifically, the Bank will continue to be an independent community-oriented financial institution with a commitment to local real estate mortgage financing with operations funded by retail deposits, borrowings, equity capital and internal cash flows. In addition, the Bank will seek to continue to develop the infrastructure management believes First Savings requires in order to be an effective competitor in the commercial and retail banking arena locally. Accordingly, First Savings will continue to employ additional staff as needed to support growth of its commercial and consumer banking products and services. Additionally, First Savings plans to continue to make additional capital investments in its retail branch network, both in terms of its existing 7 retail banking offices as well as de novo branch offices. In this regard, the Bank is planning to purchase or construct up to two branches over the next three to four years. While specific locations have yet to be identified, new branches will generally be located in First Savings’ existing market in Clark and Floyd Counties and will result in a significant capital outlay (in the general range of $2.0 million for the two planned offices) and increased expense related to staffing and operating the new offices.

First Savings will be seeking to leverage its infrastructure investments in office facilities and technology through balance sheet and fee income growth and on-going development of strong customer relationships, as it seeks to become a leading community bank in the markets served. In the near term, the Bank will continue to incur substantial costs which may negatively impact profitability.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.5 |

The Bank’s Board of Directors has elected to convert to the stock form of ownership to improve the competitive position of the Bank. The capital realized from the Conversion will increase the operating flexibility and overall financial strength of the Bank, as well as support the expansion of the Bank’s strategic focus of providing competitive community banking services in its local market area as described above. The additional capital realized from stock proceeds will increase liquidity to support funding of future loan growth and other interest-earning assets. The Bank’s higher capital position resulting from the infusion of stock proceeds will also serve to reduce interest rate risk, through enhancing the Bank’s interest-earning-assets-to-interest-bearing-liabilities (“IEA/IBL”) ratio. The additional funds realized from the Conversion will provide an alternative funding source to deposits and borrowings in meeting the Bank’s future funding needs. Additionally, the Bank’s higher equity-to-assets ratio will also better position the Bank to take advantage of expansion opportunities as they arise. Such expansion would most likely occur through growth at existing offices as well as through targeted branching. The Bank will also be better positioned to pursue growth through acquisition of other financial service providers following the Conversion, given its strengthened capital position and status as a stock company. At this time, the Bank has no specific plans for expansion other than through establishing additional branches. The projected use of proceeds has been highlighted below.

| • | Company. The Company is expected to retain up to 50% of the net offering proceeds. At present, Company funds, net of the loan to the ESOP, are expected to be placed into short-term investment securities. Over time, Company funds are anticipated to be utilized for various corporate purposes, possibly including acquisitions, infusing additional equity into the Bank, repurchases of common stock, and the payment of regular and/or special cash dividends. |

| • | Bank. The balance of the net offering proceeds will be infused into the Bank in exchange for all of the Bank’s newly-issued stock. The increase in the Bank’s capital will be less, as the amount to be borrowed by the ESOP to fund an 8% stock purchase will be accounted for as a contra-equity. Cash proceeds (i.e., net proceeds |

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.6 |

less deposits withdrawn to fund stock purchases) infused into the Bank are anticipated to become part of general operating funds, and are expected to initially be invested in short-term investments pending longer term deployment, i.e., funding lending activities and for general corporate purposes. |

Balance Sheet Trends

Growth Trends

Table 1.1 shows the Bank’s historical balance sheet data for the past five and one-half years. From September 30, 2003 through March 31, 2008, First Savings’ assets shrank modestly at a 1.15% compounded annual rate. Within the asset base, cash and equivalents declined, while investment securities and loans receivable reported modest annual increases. In this regard, the Bank had very high liquidity levels in 2003 and 2004 reflecting the impact of heavy loan prepayments in the residential mortgage portfolio. The cash has subsequently been redeployed into investment securities and whole loans as reflected in their modest positive long-term growth rates. Total assets have diminished, however, as the reduction of excess cash assets coupled with the increase in borrowings has been utilized to fund deposit outflows; deposits have diminished at a compounded annual rate of 2.60% since September 2003.

Annual equity growth equaled 2.5% since the end of fiscal 2003, with the modest growth rate reflecting the Bank’s moderate return on equity (“ROE”), particularly as the Bank incurred additional expenses associated with the build-up of its infrastructure as well as relatively high loan loss provisions in connection with its portfolio of investor loans secured by 1-4 family properties. The post-offering equity growth rate may likely continue to be modest given the increased equity, the initial anticipated low return on the net offering proceeds in the current interest rate environment, the cost of the stock benefit plans, public company reporting and the expense of targeted branching. Over the longer term, as the new equity is leveraged through growth, the return on equity may improve. A summary of First Savings’ key operating ratios for the past five and one-half years is presented in Exhibit I-2.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.7 |

Table 1.1

First Savings Bank, F.S.B.

Historical Balance Sheet Data

| As of September 30, | As of March 31 2008 | 9/30/03-3/31/08 Annual. Growth Rate | |||||||||||||||||||||||||||||||||||||

| 2003 | 2004 | 2005 | 2006 | 2007 | |||||||||||||||||||||||||||||||||||

| Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Pct | |||||||||||||||||||||||||||

| ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | (%) | |||||||||||||||||||||||||||

Total Amount of: | |||||||||||||||||||||||||||||||||||||||

Assets | $ | 223,940 | 100.00 | % | $ | 216,529 | 100.00 | % | $ | 205,796 | 100.00 | % | $ | 206,399 | 100.00 | % | $ | 203,321 | 100.00 | % | $ | 212,624 | 100.00 | % | -1.15 | % | |||||||||||||

Cash and cash equivalents | 56,084 | 25.04 | % | 21,904 | 10.12 | % | 14,651 | 7.12 | % | 15,223 | 7.38 | % | 10,395 | 5.11 | % | 9,233 | 4.34 | % | -33.03 | % | |||||||||||||||||||

Securities available for sale | 0 | 0.00 | % | 7,534 | 3.48 | % | 7,039 | 3.42 | % | 5,897 | 2.86 | % | 8,260 | 4.06 | % | 10,424 | 4.90 | % | N.M. | ||||||||||||||||||||

Securities held-to-maturity | 3,091 | 1.38 | % | 14,650 | 6.77 | % | 11,602 | 5.64 | % | 8,219 | 3.98 | % | 7,422 | 3.65 | % | 9,100 | 4.28 | % | 27.12 | % | |||||||||||||||||||

FHLB stock | 1,419 | 0.63 | % | 1,419 | 0.66 | % | 1,464 | 0.71 | % | 1,379 | 0.67 | % | 1,336 | 0.66 | % | 1,336 | 0.63 | % | -1.33 | % | |||||||||||||||||||

Loans receivable, net | 155,644 | 69.50 | % | 163,305 | 75.42 | % | 163,676 | 79.53 | % | 166,695 | 80.76 | % | 167,371 | 82.32 | % | 171,018 | 80.43 | % | 2.12 | % | |||||||||||||||||||

Deposits | 195,979 | 87.51 | % | 187,516 | 86.60 | % | 175,451 | 85.25 | % | 175,891 | 85.22 | % | 168,782 | 83.01 | % | 174,085 | 81.87 | % | -2.60 | % | |||||||||||||||||||

FHLB advances | 0 | 0.00 | % | 0 | 0.00 | % | 0 | 0.00 | % | 0 | 0.00 | % | 3,000 | 1.48 | % | 8,000 | 3.76 | % | N.M. | ||||||||||||||||||||

Equity | $ | 26,353 | 11.77 | % | $ | 27,245 | 12.58 | % | $ | 28,487 | 13.84 | % | $ | 28,850 | 13.98 | % | $ | 29,662 | 14.59 | % | $ | 29,399 | 13.83 | % | 2.46 | % | |||||||||||||

Loans/Deposits | 79.42 | % | 87.09 | % | 93.29 | % | 94.77 | % | 99.16 | % | 98.24 | % | |||||||||||||||||||||||||||

Offices Open | 7 | 7 | 7 | 7 | 7 | 7 | |||||||||||||||||||||||||||||||||

| (1) | Ratios are as a percent of ending assets. |

Sources: First Savings’ prospectus, audited and unaudited financial statements and RP Financial calculations.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.8 |

Loans Receivable

Loans receivable totaled $171.0 million, or 80.4% of total assets, as of March 31, 2008, and reflects modest growth since the end of fiscal 2003 approximating 2.1% on a compounded annual basis. Over this period, the proportion of loans to total assets has increased modestly as the rate of loan growth exceeded the asset growth rate. Additionally, the composition of the loan portfolio has gradually shifted to include a higher proportion of 1-4 family mortgage loans and commercial loans including both commercial mortgage and non-mortgage commercial and industrial (“C&I”) loans. The growth of commercial mortgage and C&I loans reflecting the Bank’s current strategic emphasis on commercial lending and management’s efforts to build the Bank’s capabilities in this regard. Growth in the commercial loan portfolio has been partially offset by First Savings’ diminished construction lending, which is reflective of the weak housing market which has resulted in lower demand and more restrictive lending terms on the part of First Savings.

As referenced above, the balance of the 1-4 family mortgage loan portfolio has increased over the last five years, notwithstanding management’s recent efforts to focus on commercial lending. Specifically, permanent 1-4 family residential mortgage loans have increased modestly in proportion to total loans (from 59.1% of total loans in fiscal 2003, to 63.0% of total loans as of March 31, 2008. Likewise, commercial mortgage and C&I loans have increased in recent years to equal 8.8% and 6.0% of total loans, respectively, but nonetheless remain a modest part of the loan portfolio overall. Commercial mortgage loans are generally secured by office buildings and retail structures and mixed-use buildings while C&I loans generally consist of lines of credit and business term loans, frequently with non-mortgage collateral. Over the corresponding timeframe, construction and land loans have diminished from 15.0% as of the end of fiscal 2003, to 9.6% as of March 31, 2008.

Cash, Investments and Mortgage-Backed Securities

The intent of the Bank’s investment policy is to provide adequate liquidity, to generate a favorable return on excess investable funds and to support the established

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.9 |

credit and interest rate risk objectives. The ratio of cash and investments including MBS has fluctuated based primarily on loan demand and cash inflows from deposits and borrowings and has declined modestly since the end of fiscal 2003, from 27.1% of assets to 14.2% as of March 31, 2008. The comparatively modest level of cash and investments currently is reflective of the Bank’s general preference to invest in whole loans.

The Bank’s investment securities and MBS equaled $20.9 million, or 9.8% of total assets, as of March 31, 2008, while cash and interest bearing deposits and term deposits totaled $9.2 million, or 4.3% of assets. As of March 31, 2008, the cash and investments portfolio consisted of cash, interest-earning deposits in other financial institutions, mortgage-backed securities issued by Ginnie Mae, Fannie Mae or Freddie Mac, U.S. government agency obligations and other high quality investments, including those issued by municipalities. Additionally, the Bank maintains permissible equity investments such as FHLB stock with a fair value of $1.3 million as of March 31, 2008. The Bank’s investment securities are classified both as held-to-maturity (“HTM”) and available for sale (“AFS”), with the HTM portfolio primarily comprised of MBS (see Exhibit I-3 for the investment portfolio composition).

No major changes to the composition and practices with respect to the management of the investment portfolio are anticipated over the near term, except that it is expected that the Bank will generally classify securities as AFS at the time of purchase (including MBS). The level of cash and investments is anticipated to increase initially following the Conversion, pending gradual redeployment into higher yielding loans.

Funding Structure

Retail deposits have consistently been the substantial portion of balance sheet funding. Since fiscal year-end 2003, deposits have diminished at a 2.6% compounded annual rate. Over this time frame, the composition of deposits has remained relatively stable with the largest portion in certificates of deposits, which have constituted in excess of two-thirds of total deposits over the last three fiscal years. As of

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.10 |

March 31, 2008, certificates of deposit totaled $124.3 million, equal to 71.4% of total deposits while savings and transaction accounts totaled $49.8 million, equal to 28.6% of total deposits.

The Bank has recently commenced utilizing borrowed funds, consisting of FHLB advances. As of March 31, 2008, borrowed funds in the form of FHLB advances totaled $8.0 million, representing 3.8% of total assets. The Bank typically utilizes borrowings: (1) when such funds are priced attractively relative to deposits; (2) to lengthen the duration of liabilities; (3) to enhance earnings when attractive revenue enhancement opportunities arise; and (4) to generate additional liquid funds, if required. Recent growth in borrowings was primarily due to the attractive rate on term funds relative to deposits with comparable maturities and the need for additional liquidity to fund loan growth.

Capital

Annual capital growth for the Bank has been moderate since the end of 2003, equal to 2.5% on a compounded annual basis, in part reflecting the Bank’s moderate earnings and strong pre-Conversion equity levels. As of March 31, 2008, the Bank’s equity totaled $29.4 million, or 13.8% of total assets. The Bank maintained capital surpluses relative to its regulatory capital requirements at March 31, 2008, and thus qualified as a “well capitalized” institution. The offering proceeds will serve to further strengthen the Bank’s regulatory capital position and support further growth. The equity growth rate is expected to slow for the Bank on a post-offering basis given the pro forma increase in equity, low reinvestment yields currently available, the potential dividend policy, and branching and other growth-related expenses.

Income and Expense Trends

Table 1.2 shows the Bank’s historical income statements for the past five years and for the 12 months ended March 31, 2008. The Bank reported positive earnings over the past five and one-half years, but with significant year-to-year fluctuations such that earnings trends over the period are difficult to discern. Earnings fluctuated between

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.11 |

Table 1.2

First Savings Bank, F.S.B.

Historical Income Statements

| For the Fiscal Year Ended September 30, | For the 12 Mths Ended, March 31, 2008 | |||||||||||||||||||||||||||||||||||||||||

| 2003 | 2004 | 2005 | 2006 | 2007 | ||||||||||||||||||||||||||||||||||||||

| Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | |||||||||||||||||||||||||||||||

| ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | |||||||||||||||||||||||||||||||

Interest income | $ | 11,931 | 5.31 | % | $ | 10,552 | 4.77 | % | $ | 10,874 | 5.15 | % | $ | 12,223 | 5.85 | % | $ | 13,078 | 6.43 | % | $ | 12,818 | 6.39 | % | ||||||||||||||||||

Interest expense | (6,166 | ) | -2.74 | % | (4,496 | ) | -2.03 | % | (4,255 | ) | -2.01 | % | (5,250 | ) | -2.51 | % | (6,183 | ) | -3.04 | % | (6,188 | ) | -3.08 | % | ||||||||||||||||||

Net interest income | $ | 5,765 | 2.56 | % | $ | 6,056 | 2.74 | % | $ | 6,619 | 3.13 | % | $ | 6,973 | 3.34 | % | $ | 6,895 | 3.39 | % | $ | 6,630 | 3.30 | % | ||||||||||||||||||

Provision for loan losses | (131 | ) | -0.06 | % | (226 | ) | -0.10 | % | (336 | ) | -0.16 | % | (813 | ) | -0.39 | % | (758 | ) | -0.37 | % | (1,541 | ) | -0.77 | % | ||||||||||||||||||

Net interest income after provisions | $ | 5,634 | 2.51 | % | $ | 5,830 | 2.64 | % | $ | 6,283 | 2.97 | % | $ | 6,160 | 2.95 | % | $ | 6,137 | 3.02 | % | $ | 5,089 | 2.54 | % | ||||||||||||||||||

Other operating income | $ | 837 | 0.37 | % | $ | 679 | 0.31 | % | $ | 961 | 0.45 | % | $ | 889 | 0.43 | % | $ | 841 | 0.41 | % | $ | 953 | 0.47 | % | ||||||||||||||||||

Operating expense | (4,644 | ) | -2.06 | % | (5,047 | ) | -2.28 | % | (5,601 | ) | -2.65 | % | (6,129 | ) | -2.94 | % | (5,737 | ) | -2.82 | % | (5,936 | ) | -2.96 | % | ||||||||||||||||||

Net operating income | $ | 1,827 | 0.81 | % | $ | 1,462 | 0.66 | % | $ | 1,643 | 0.78 | % | $ | 920 | 0.44 | % | $ | 1,241 | 0.61 | % | $ | 106 | 0.05 | % | ||||||||||||||||||

Employee severance expense | $ | 0 | 0.00 | % | $ | 0 | 0.00 | % | $ | 0 | 0.00 | % | $ | (324 | ) | -0.16 | % | $ | 0 | 0.00 | % | $ | 0 | 0.00 | % | |||||||||||||||||

Gain(loss) on sale of stock | 0 | 0.00 | % | 0 | 0.00 | % | 345 | 0.16 | % | 0 | 0.00 | % | 0 | 0.00 | % | 0 | 0.00 | % | ||||||||||||||||||||||||

Net income before tax | $ | 1,827 | 0.81 | % | $ | 1,462 | 0.66 | % | $ | 1,988 | 0.94 | % | $ | 596 | 0.29 | % | $ | 1,241 | 0.61 | % | $ | 106 | 0.05 | % | ||||||||||||||||||

Income tax provision | (725 | ) | -0.32 | % | (578 | ) | -0.26 | % | (784 | ) | -0.37 | % | (241 | ) | -0.12 | % | (427 | ) | -0.21 | % | 34 | 0.02 | % | |||||||||||||||||||

Net income (loss) | $ | 1,102 | 0.49 | % | $ | 884 | 0.40 | % | $ | 1,204 | 0.57 | % | $ | 355 | 0.17 | % | $ | 814 | 0.40 | % | $ | 140 | 0.07 | % | ||||||||||||||||||

Adjusted Earnings | ||||||||||||||||||||||||||||||||||||||||||

Net income | $ | 1,102 | 0.49 | % | $ | 884 | 0.40 | % | $ | 1,204 | 0.57 | % | $ | 355 | 0.17 | % | $ | 814 | 0.40 | % | $ | 140 | 0.07 | % | ||||||||||||||||||

Add(Deduct): Net gain/(loss) on sale | 0 | 0.00 | % | 0 | 0.00 | % | (345 | ) | -0.16 | % | 324 | 0.16 | % | 0 | 0.00 | % | 0 | 0.00 | % | |||||||||||||||||||||||

Tax effect (2) | 0 | 0.00 | % | 0 | 0.00 | % | 137 | 0.06 | % | (128 | ) | -0.06 | % | 0 | 0.00 | % | 0 | 0.00 | % | |||||||||||||||||||||||

Adjusted earnings | $ | 1,102 | 0.49 | % | $ | 884 | 0.40 | % | $ | 996 | 0.47 | % | $ | 551 | 0.26 | % | $ | 814 | 0.40 | % | $ | 140 | 0.07 | % | ||||||||||||||||||

Expense Coverage Ratio (3) | 124.1 | % | 120.0 | % | 118.2 | % | 113.8 | % | 120.2 | % | 111.7 | % | ||||||||||||||||||||||||||||||

Efficiency Ratio (4) | 70.3 | % | 74.9 | % | 73.9 | % | 78.0 | % | 74.2 | % | 78.3 | % | ||||||||||||||||||||||||||||||

Effective Tax Rate | 39.7 | % | 39.5 | % | 39.4 | % | 40.4 | % | 34.4 | % | -32.1 | % | ||||||||||||||||||||||||||||||

| (1) | Ratios are as a percent of average assets. |

| (2) | Assumes a 39.6% effective tax rate for federal & state income taxes. |

| (3) | Expense coverage ratio calculated as net interest income before provisions for loan losses divided by operating expenses. |

| (4) | Efficiency ratio calculated as operating expenses divided by the sum of net interest income before provisions for loan losses plus other income (excluding net gains). |

Sources: First Savings’ prospectus, audited & unaudited financial statements and RP Financial calculations.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.12 |

0.40% of average assets and 0.57% of average assets for the fiscal 2003 through fiscal 2005 period, and for fiscal 2007. Earnings were comparatively modest in fiscal 2006 (0.17% of average assets) and for the 12 months ended March 31, 2008 (0.07% of average assets), reflecting the impact of higher loan loss provisions and management severance-related costs (reflects a non-recurring expense for fiscal 2006 only). In general, the Bank’s profitability ratios have been comparatively modest, even after excluding several one-time non-recurring expenses, as a result of balance sheet shrinkage and a high operating expenses ratio which has been trending upward. These and other trends with respect to First Savings’ income and expenses will be discussed in the balance of this section.

Net Interest Income

Over the past five and one-half years, the Bank’s net interest income to average assets ratio generally reflects a positive trend, increasing from 2.56% of average assets in fiscal 2003, to a peak level of 3.39% of average assets in fiscal 2007, before declining modestly to 3.30% of average assets for the 12 months ended March 31, 2008. The increase in the net interest income ratio since 2005 reflects a modest widening of the Bank’s interest rate spread, attributable to a greater increase in the overall yield on interest-earnings assets, offset in part by a higher average cost of interest-bearing liabilities. During the six months ended March 31, 2008, the Bank’s interest spread decreased modestly to 2.94%, compared to 3.15% during the six months ended March 31, 2007, with the decline attributable to declining asset yields. At March 31, 2008, First Savings’ interest rate spread equaled 2.95%. The Bank’s net interest rate spreads and yields and costs for the past three and one-half years are set forth in Exhibits I-4.

Loan Loss Provisions

Provisions for loan losses have typically been limited reflecting the Bank’s relatively strong asset quality historically and the secured nature of the loan portfolio; the majority of the loan portfolio is secured by real estate collateral in the Bank’s local market area, which traditionally represents a relatively strong real estate market.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.13 |

However, loan loss provisions have recently been subject to increase as a result of deterioration of the portfolio of investor loans commencing in fiscal 2006, which caused loan loss provisions to increase to a level of $813,000 (0.39% of average assets) in fiscal 2006, $758,000 (0.37% of average assets) in fiscal 2007 and $1.5 million (0.77% of average assets) for the 12 months ended March 31, 2008.

As previously discussed, the increase in loan loss provisions for the most recent 12 month period is attributable to the Bank’s portfolio of investor loans secured by single family properties, typically in low to moderate income areas in southern Indiana. In particular, First Savings established additional allowances for loan and lease losses (“ALLLs”) against 35 loans to one borrower with a principal balance of $2.0 million where the Bank’s perceives the market value has deteriorated significantly since the loans were originated. The additional ALLLs established for this one group of loans totaled $969,000 for the 12 months ended March 31, 2008.

Going forward, the Bank will continue to evaluate the adequacy of the level of general valuation allowances (“GVAs”) on a regular basis, and establish additional loan loss provisions in accordance with the Bank’s asset classification and loss reserve policies. However, management expects that loan loss provisions may likely be lower than the 0.77% of average assets level reported for the 12 months ended March 31, 2008.

Non-Interest Income

Other non-interest income has generally been rising, and increased to a level of $953,000, equal to 0.47% of average assets for the 12 months ended March 31, 2008, which is the peak level reported by the Bank over the prior five and one-half fiscal years. The bulk of First Savings’ fee income is comprised of fees related to its depository activities, lending, mortgage servicing and debit and credit interchange activities. Additionally, non-interest income was further enhanced by the purchase of BOLI, wherein the income from the increase in the cash surrender value of the policies is reflected as non-interest income. The ratio of non-interest income to average assets is moderate in comparison to many community banks due in part to competitive

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.14 |

conditions prevailing locally and the owing to the fact the First Savings’ fee generating commercial deposit relationships and other fee generating activities are currently limited. Management will seek to increase the level of non-interest fee income by continuing to expand fee generating commercial loan and deposit relationships and other non-interest sources of income. However, growth in the level of non-interest operating income is expected to be gradual.

Operating Expenses

The Bank’s operating expenses have increased in modestly in recent years, notwithstanding modest asset shrinkage which would otherwise tend to limit the growth of operating costs, as a result of growth in compensation and benefits and other factors related to posturing First Savings’ commercial lending operations. Additionally, health and benefits costs have continued to spiral upward. Overall, operating expenses have increased from $4.6 million in fiscal 2003, equal to 2.06% of average assets, to $5.9 million, equal to 2.96% of average assets for the 12 months ended March 31, 2008.

Operating expenses are expected to increase following the Conversion as a result of the expense of the stock-related benefit plans, the cost related to operating as a public company and as a result of long-term plans to continue to expand the branch network. With regard to this latter factor, the Bank plans to establish two or more new branches over the next three to four years which will entail additional expenses related to staffing and operating costs as well as depreciation expense on the fixed asset investment. Furthermore, First Savings expects to continue to gradually build its commercial lending staffing levels take advantage of the expanded branch coverage. The Bank will be seeking to offset such costs over time through growth and increased efficiency.

Non-Operating Income/Expense

Non-operating income and expenses have had a limited impact on earnings over the last five fiscal years, and have primarily consisted of gains on the sale of loans and investments. Non-operating income totaled $345,000, equal to 0.16% of assets, in

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.15 |

fiscal 2004, which was attributable to a gain on the sale of the Bank’s equity investment in its electronic data processor. In the following year, the Bank incurred non-operating severance costs related to the termination of the Bank’s managing officer. The Bank did not have any non-operating income or expense for the 12 months ended March 31, 2008.

Taxes

The Bank’s average tax rate generally has ranged from 34% to 40% over the last five fiscal years. The Bank’s tax rate was skewed to a negative rate for the 12 months ended March 31, 2008, as a result of a the low level of net income overall and the tax benefit recorded for the most recent six month period. In the future, the Bank’s tax rate is expected to approximate the long-term average rate in the range of 34% to 40%.

Efficiency Ratio

The Bank’s efficiency ratio reflects an adverse trend since the end of fiscal 2003 largely due to (1) the increase in the operating expense ratio as the Bank’s asset base shrank modestly while operating costs to continued to grow and (2) the benefits related to an expanding level of non-interest income and net interest income were comparatively modest. As a result of the foregoing, the efficiency ratio increased from 70.3% in fiscal 2003 to 78.3% for the 12 months ended March 31, 2008, which represents the highest ratio reported by First Savings over the last five fiscal years. On a post-offering basis, the efficiency ratio is expected to show some improvement as the net interest ratio increases with the reinvestment of proceeds, although the increased operating expenses (reflecting the costs of building and staffing new branches as well as public company and stock plans expenses) may limit the improvement.

Impact of Freeze/Termination of Defined Benefit Pension Plan

First Savings has taken steps to freeze the defined benefit pension plan in place for employees which is expected to occur in the quarter ended June 30, 2008,

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.16 |

subsequent to the date of financial data herein. As a result, each active participant’s pension benefit will be determined based on the participant’s compensation and duration of Employment as of June 30, 2008, and compensation and employment after that date will not be taken into account in determining pension benefits under the pension plan. Based on information from First Savings’ actuaries, the Bank estimates it will record a one-time gain from the curtailment of the pension plan which will be reported in the June 30, 2008 quarter. The pre-tax gain on curtailment is estimated to total $615,000 which will result in an after-tax gain of $371,000. The Bank intends to replace this management benefit with the stock-based benefit plans established in connection with the Conversion.

Interest Rate Risk Management

The primary aspects of the Bank’s interest rate risk management include:

| • | Emphasizing the origination of adjustable rate 1-4 family residential mortgage loans and selling a portion of the longer-term fixed-rate loans (i.e., maturities in excess of 15 years dependent upon the rate environment) originated to the secondary market; |

| • | Diversifying portfolio loans into other types of shorter-term or adjustable rate lending, including commercial and construction lending; |

| • | Maintaining an investment portfolio, comprised of high quality, liquid securities and maintaining an ample balance of securities classified as available for sale; |

| • | Promoting transaction accounts and, when appropriate, longer term CDs; |

| • | Utilizing longer-term borrowing when such funds are attractively priced relative to deposits and prevailing reinvestment opportunities; |

| • | Maintaining a strong capital level; and |

| • | Increasing non-interest income within constraints imposed by the local market and product mix. |

The rate shock analysis as of March 31, 2008 (see Exhibit I-5) shows that the expected change in the net portfolio value (“NPV”) as a percent of the portfolio value of assets under a 200 basis point increase in interest rates was negative 42 basis points (with a 12.99% NPV ratio) while a 100 basis point decrease in interest rates resulted in

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.17 |

a change of negative 23 basis points (with a 13.18% post-shock NPV ratio, suggesting that the Company’s economic value would be adversely impacted under both rising and falling interest rate scenarios. At the same time, the change in either a rising or declining rate environment is limited and the post-shock NPV ratio is very strong suggesting limited interest rate risk exposure overall.

Importantly, there are numerous limitations inherent in such analyses, such as the credit risk of Company’s adjustable rate loans in a rising interest rate environment. Moreover, the Company’s interest rate risk exposure is projected to be further reduced following the completion of the Conversion and reinvestment of the net conversion proceeds into interest-earning assets.

Lending Activities and Strategy

First Savings’ lending activities have traditionally emphasized 1-4 family permanent mortgage loans (including second mortgage and home equity lines of credit) and such loans continue to comprise the largest component of the Bank’s loan portfolio. Beyond 1-4 family loans, lending diversification by the Bank has emphasized construction/land loans and commercial real estate loans. Non-mortgage lending, in the form of commercial business and consumer loans, have also been a moderate area of lending diversification for the Bank. Going forward, the Bank’s lending strategy is expected to remain fairly consistent with recent historical trends, with the origination of 1-4 family permanent mortgage loans remaining as the largest source of loan originations and construction/land and commercial real estate loans remaining as the primary area of lending diversification. Over time, the Bank is expecting to continue to build its ability to service commercial account relationships through the employment of additional experienced commercial loan officers as well as by promoting strong internally generated loan officer candidates from within the Bank. Details regarding the Company’s loan portfolio composition and characteristics are included in Exhibits I-6, I-7 and I-8.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.18 |

Residential Lending

As of March 31, 2008, residential mortgage loans equaled $109.9 million, or 63.0% of total loans. Adjustable rate residential mortgage loans comprise approximately one-half of the residential mortgage portfolio as it has been the Bank’s practice to sell a portion of the longer term fixed rate loans (i.e., with maturities greater than 15 years) into the secondary market on a servicing released basis with the timing and magnitude of sales dependent upon market and interest rate conditions. Thus, the balance of the permanent residential mortgage loan portfolio generally consists of fixed rate loans with maturities of 15 years or less.

ARM loans offered by the Bank include loans with one, three and five year repricing periods for the initial period and which adjust annually thereafter. Fixed rate 1-4 family mortgage loans offered by the Bank have terms of up to 30 years. A portion of the residential loans originated are not saleable in the conforming secondary market due to various underwriting characteristics (i.e. loan size, nature of collateral, etc.). Other loans are generally underwritten to secondary market standards specified. All loans in excess of an 80% loan-to-value (“LTV”) ratio must have private mortgage insurance. The Bank’s underwriting policies permit originations of LTVs of up to 97%, with an LTV limit of 75% on non-owner occupied property. As previously discussed, the Bank had previously developed a niche in financing non-owner occupied residential properties and estimates that 28.0% of its residential mortgage loans are to real estate investors based on financial data as of March 31, 2008. The current focus of permanent 1-4 family lending is to owner occupants.

As a complement to the 1-4 family permanent mortgage lending activities, the Bank also offers home equity loans. Such loans typically have shorter maturities and higher interest rates than traditional 1-4 family lending. Home equity loans and lines of credit totaled $10.5 million, equal to 6.0% of total loans as of March 31, 2008.

Construction Loans

Construction lending has diminished modestly over the last several years which is reflective of the current weak housing market, particularly for new homes.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.19 |

Accordingly, First Savings has retrenched from construction lending by limiting its lending to the strongest projects and borrowers. As a result, construction and land loans have diminished from 15.0% as of the end of fiscal 2003, to 9.6% as of March 31, 2008.

The Bank originates residential and, to a lesser extent, commercial construction loans. Such lending shortens the average duration of assets and support asset yields. The Bank generally limits such loans to known builders and developers with established lending relationships with the Bank. In the case where the Bank is making a construction loan to the owner of the structure, First Savings typically structures the loan as a construction loan which converts to a permanent loan upon completion of the construction phase. Substantially all of the Bank’s construction lending is in markets served by a First Savings branch or a contiguous area. Construction loans generally have terms of up to 12 months and LTV ratios up to 97% for a residential property (with PMI for the portion over 80%) and 80% for a commercial property.

Multi-Family and Commercial Mortgage Lending

Multi-family and commercial mortgage lending has been an area of portfolio diversification for the Bank, and totaled $15.3 million (8.8% of total loans) and $5.2 million (3.0% of total loans) as of March 31, 2008. Such loans are typically secured by properties in the Bank’s market area and are generally originated by the Bank but may include participation interests purchased from other local lenders. The substantial majority of such mortgage loans originated by the Bank are secured by properties in southern Indiana or nearby northern Kentucky.

Multi-family and commercial mortgage loans are typically adjustable over a five year period and or fixed rate loans with a five year balloon term such that the loan effectively reprices within a five year timeframe. Balloon loans are frequently renegotiated as the loan approaches its maturity with new terms and conditions which take into account the then prevailing conditions of the market, borrower and collateral property. Such loans typically possess amortization periods of 15 to 20 years, and loan-to-value ratios of up to 80%, and target a debt-coverage ratio of at least 1.2 times.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.20 |

The typical commercial or multi-family loans that the Bank will be seeking to make will have a principal balance in the range of $250,000 to $2.5 million, but may be larger, particularly if the loan is well-collateralized or extended to a very credit-worthy borrower. Multi-family and commercial real estate loans are secured by office buildings, retail and industrial use buildings, apartments and other structures such as strip shopping centers, retail shops and various other properties. Most income producing property loans originated by the Bank are for the purpose of financing existing structures rather than new construction. Such loans will generally be collateralized by local properties.

Non-Mortgage Lending

The Bank’s efforts to increase commercial lending have included mortgage lending as well as C&I non-mortgage lending. As of March 31, 2008, commercial business loans totaled $10.4 million, equal to 6.0% of total loans. The Bank offers commercial loans to sole proprietorships, professional partnerships and various other small businesses. The types of commercial loans offered include lines of credit and business term loans. Most lines of credit and business term loans are secured by real estate and other assets such as equipment, inventory and accounts receivable.

Consumer loans are generally offered to provide a full line of loan products to customers and typically include student loans, loans on deposits, auto loans, and unsecured personal loans. As of March 31, 2008, consumer loans totaled $16.7 million, equal to 9.6% of total loans. Excluding home equity loans which are secured by a mortgage, the consumer loan balance totaled $6.2 million, equal to 3.6% of loans.

Loan Originations, Purchases and Sales

Exhibit I-9, which shows the Bank’s loan originations/purchases, repayments and sales over the past three fiscal years, highlights the Bank’s emphasis on residential mortgage lending with a modest level of diversification in other loan types, including

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.21 |

commercial mortgage and construction loans, as well as non-mortgage loans. Total loan originations were relatively consistent over the last three fiscal years, reflecting the limited growth trends for the portfolio overall, and ranged from $83.5 million to $91.7 million, and totaled $91.4 million for the 12 months ended March 31, 2008. Recent trends with respect to loan portfolio balances, including growth in the permanent 1-4 family loan portfolio and shrinkage of the construction loan portfolio, are evidenced by the underlying origination volumes. The Bank is primarily a portfolio lender as loan sales have been limited since the end of fiscal 2005.

Asset Quality

The Bank has typically operated with a higher level of NPAs relative to many thrifts in the Midwest, which reflected asset quality problems in the portfolio of residential mortgage loans (primarily including investor loans), which also translated into a higher level of foreclosure activity with a relatively significant balance of real estate owned (“REO”) and other foreclosed assets. The level of NPAs increased over the six months ended March 31, 2008, reflecting the deterioration of a group of residential mortgage loans to one investor as more fully described below.

As shown in Exhibit I-10, the balance of NPAs has fluctuated at levels above 1% of total assets, from a low of 1.15% as of the end of fiscal 2003, to a high of 2.50% as of March 31, 2008. As of March 31, 2008, NPAs were comprised of $3.6 million of non-accruing loans, $418,000 of accruing loans 90 days or more past due, and $1.3 million of REO and other foreclosed assets. Importantly, approximately $2.0 million of the increase over the six months ended March 31, 2008, was attributable to a group of 35 residential mortgage loans to one borrower secured by investment properties in southern Indiana. In this regard, the Bank’s perceives the market value has deteriorated significantly since the loans were originated and as a result, First Savings established $867,000 of additional ALLLs for this one group of loans for the most recent six month period.

To track the Bank’s asset quality and the adequacy of valuation allowances, First Savings has established detailed asset classification policies and procedures which are

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.22 |

consistent with regulatory guidelines. Detailed asset classifications are reviewed quarterly by senior management and the Board. Pursuant to these procedures, when needed, the Bank establishes additional valuation allowances to cover anticipated losses in classified or non-classified assets. As of March 31, 2008, the Bank maintained valuation allowances of $2.5 million, equal to 1.43% of total loans, and 47.05% of non-performing assets (see Exhibit I-11 for details).

Funding Composition and Strategy

Deposits have consistently accounted for the major portion of the Bank’s interest-bearing funding composition and at March 31, 2008 deposits equaled 95.6% of First Savings’ interest-bearing funding composition. Exhibit I-12 sets forth the Bank’s deposit composition for the past three and one-half years and Exhibit I-13 provides the interest rate and maturity composition of the CD portfolio at March 31, 2008. Certificates of deposit constitute the largest portion of the Bank’s deposit base, and recent trends in the Bank’s deposit composition show that the composition of the deposit base has remained relatively stable. Transaction and savings account deposits equaled $49.8 million or 28.6% of total deposits at March 31, 2008, versus $62.5 million or 35.6% of total deposits as of March 31, 2008.

The balance of the Bank’s deposits consists of CDs, with First Savings’ current CD composition reflecting a higher concentration of short-term CDs (maturities of one year or less). As of March 31, 2008, the CD portfolio totaled $124.3 million, or 71.4% of total deposits as of March 31, 2008 and 67.5% of the CDs were scheduled to mature in one year or less. As of March 31, 2008, jumbo CDs (CD accounts with balances of $100,000 or more) amounted to $31.9 million or 25.7% of total CDs. First Savings does not maintain any brokered CDs.

As of March 31, 2008, borrowed funds totaled $8.0 million and consisted solely of FHLB advances. Recent growth in borrowings was primarily due to the attractive rate on term funds and the need for additional liquidity in the absence of deposit growth. It is management’s current intention to focus on deposit growth to fund future operations but it will continue to evaluate the use of borrowings when the perceived cost relative to deposits is favorable and potentially for wholesale leverage purposes on a post-Conversion basis.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.23 |

Subsidiaries

First Savings has two subsidiaries, Southern Indiana Financial Corporation and FFCC, Inc., both of which are organized as Indiana corporations. Southern Indiana Financial Corporation is an independent insurance agency, offering various types of annuities and life insurance policies. FFCC, Inc. was organized for the purposes of purchasing, holding and disposing of real estate owned.

In addition, the Bank has plans to form one or more additional wholly-owned subsidiaries to hold investment securities in order to take advantage of certain favorable income tax treatment afforded under Indiana law.

Legal Proceedings

The Bank is not involved in any pending legal proceedings other than routine legal proceedings occurring in the ordinary course of business which, in the aggregate, are believed by management to have a material adverse effect on the Bank’s financial condition. First Savings is involved in litigation seeking restitution from a former fee appraiser related to appraisals obtained on 1-4 family loans to investors. At this point, it is difficult for the Bank to quantify the amount and timing of any damage award which may be forthcoming, if any.

| RP® Financial, LC. | MARKET AREA | |

| II.1 |

II. MARKET AREA

Introduction

First Savings conducts operations out of the main office and six branch offices in southern Indiana. The Bank’s main office is located in Clarksville, two offices are located in Jeffersonville, and single office locations are maintained in Charlestown, Sellersburg, Floyds Knobs and Georgetown, Indiana. The main office and four of the Bank’s branches are located in Clark County and the remaining two branches are located in Floyd County. Located along the northern shore of the Ohio River, both Clark and Floyd Counties are situated along the banks of the Ohio River within the Louisville, Kentucky metropolitan area as reflected in the map below. Exhibit II-1 provides additional information on the Bank’s office properties.

First Savings Bank, F.S.B.

Branch Network

The Bank’s markets in southern Indiana are part of the Greater Louisville metropolitan area (“MSA”) which is a mid-sized metropolitan area with a total population

| RP® Financial, LC. | MARKET AREA | |

| II.2 |

approximating 1.2 million. The numerous bridges that connect Indiana and Kentucky’s interstate system provide easy and convenient access to either side of the river for all residents of the Louisville metropolitan area.

The Bank’s competitive environment includes a large number of thrifts, commercial banks and other financial service providers, including credit unions, some of which have a regional or national presence. The primary market area economy is fairly diversified, although manufacturing businesses remain the cornerstone of the regional economy. Major employment sectors in the regional economy include services, wholesale/retail trade and manufacturing.

Future growth opportunities for the Bank depend on the future growth and stability of the regional economy, demographic growth trends, and the nature and intensity of the competitive environment. These factors have been briefly examined to help determine the growth potential that exists for the Bank and the relative economic health of the Bank’s market area.

National Economic Factors

The future success of the Bank’s operations is partially dependent upon various national and local economic trends. Signs of the economy potentially slipping into a recession continued to emerge in 2008, with January employment data showing a drop in payrolls for the first time since 2003. The January unemployment rate dipped to 4.9%, as the civilian labor force shrank slightly. January economic data also showed retailers continuing to experience a decline in sales. New home sales fell in January for a third straight month, pushing activity down to the slowest pace in nearly 13 years. Due to the ongoing housing slump, the Federal Reserve cut its economic growth forecast for 2008. Consumer confidence dropped sharply in February amid growing concerns of a forthcoming recession. Other data that indicated the economy was heading towards a recession included a decline in February manufacturing activity to a five year low, and the number of homes entering foreclosure hit a record in the fourth quarter of 2007. February employment data showed a loss of jobs, although the unemployment rate dipped to 4.8%. Falling home prices spurred an increase in

| RP® Financial, LC. | MARKET AREA | |

| II.3 |

February existing home sales, although new home sales continued to decline in February. The weak housing market was further evidenced by a decrease in residential construction activity during February, which pushed the mark for decreased residential construction activity to a record 24 consecutive months. Manufacturing activity edged up slightly in March 2008, although the March reading still signaled that the manufacturing sector was still in contraction. March employment data showed a third straight month of job losses, with the unemployment rate increasing from 4.8% to 5.1%. The prolonged housing slump continued into March, with sales of new homes plunging to the slowest pace in over 16 years despite sharply lower prices. Sales and prices of existing homes were also down in March. Orders for durable goods dropped for the third consecutive month in March, providing further evidence that the economy was sliding into recession.

In terms of interest rates trends over the past few quarters, the downward trend in long-term Treasury yields continued to prevail in early 2008, as economic data generally pointed towards an economy growing weaker. Interest rates declined further on news of a surprise 0.75% rate cut by the Federal Reserve a week before its scheduled rate meeting at the end of January, with the yield on the 10-year Treasury note dipping below 3.50%. Treasury yields edged slightly higher in the week before the Federal Reserve meeting. The Federal Reserve meeting at the end of January concluded with a second rate cut over a nine day period, as the target rate was cut by 0.5% to 3.0%. Interest rates stabilized during the first half of February, with more economic data pointing towards a recession, and then edged higher going into late-February on inflation worries fueled by a 0.4% jump in January consumer prices. More signs of a softening U.S. economy and renewed worries of the deepening credit crisis highlighted by the collapse of investment banking firm Bear Stearns pushed bond yields lower at the end of February and the first half of March, with the yield on the 10-year Treasury dipping below 3.5% in mid-March. The Federal Reserve cut its target rate by 0.75% to 2.25% at its mid-March meeting, which along with renewed worries about the economy pushed Treasury yields lower heading into the second half of March. Treasury yields edged higher at the end of the first quarter, with the 10-year Treasury yield stabilizing around 3.5%.

| RP® Financial, LC. | MARKET AREA | |

| II.4 |

Interest rates were fairly stable during the first half of April 2008, as economic data pointed towards the U.S. economy going into recession. Most notably, March employment data showed job losses for a third consecutive month and April consumer confidence dropped to a new low for the fourth month in a row. Economic data showing higher wholesale and consumer prices in March, along with an unexpected drop in weekly unemployment claims in late –April, push long-term Treasury yields higher in the second half of April. At the end of April, the Federal Reserve lowered its target rate by a quarter point to 2%. The rate cut was the seventh in eight months, although the Federal Reserve signaled that it may be ready for a pause. Long-term Treasury yields stabilized during the first couple of weeks of May. As of May 16, 2008, the bond equivalent yields for U.S. Treasury bonds with terms of one and ten years equaled 2.09% and 3.85%, respectively, versus comparable year ago yields of 4.82% and 4.71%. Exhibit II-2 provides historical interest rate trends.

Market Area Demographics