No

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-Q

(Mark one)

☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended June 30, 2020

or

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ______________ to _____________

Commission file number: 001-38589

COASTAL FINANCIAL CORPORATION

(Exact name of registrant as specified in its charter)

Washington | 56-2392007 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

5415 Evergreen Way, Everett, Washington | 98203 |

(Address of principal executive offices) | (Zip Code) |

(425) 257-9000 |

(Registrant’s telephone number, including area code) |

Not Applicable |

(Former name, former address and former fiscal year, if changed since last report) |

Securities registered pursuant to Section 12(b) of the Act:

| | |

Title of each class | Trading symbol(s) | Name of each exchange on which registered |

Common Stock, no par value per share | CCB | The Nasdaq Stock Market LLC |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an “emerging growth company.” See the definition of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large Accelerated Filer | | ☐ | | Accelerated Filer | | ☒ |

Non-Accelerated Filer | | ☐ | | Smaller Reporting Company | | ☒ |

| | | | Emerging Growth Company | | ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of August 4, 2020 there were 11,927,243 shares of the issuer’s common stock outstanding.

COASTAL FINANCIAL CORPORATION

Table of Contents

2

Forward-Looking Statements

This report may contain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements reflect our current views with respect to, among other things, future events and our financial performance. Any statements about our management’s expectations, beliefs, plans, predictions, forecasts, objectives, assumptions or future events or performance are not historical facts and may be forward-looking. These statements are often, but not always, made through the use of words or phrases such as “anticipate,” “believes,” “can,” “could,” “may,” “predicts,” “potential,” “should,” “will,” “estimate,” “plans,” “projects,” “continuing,” “ongoing,” “expects,” “intends” and similar words or phrases. All forward-looking statements, expressed or implied, included herewith are expressly qualified in their entirety by the cautionary statements contained or referred to herein. The inclusion of forward-looking information in this report should not be regarded as a representation by us or any other person that the future plans, estimates or expectations contemplated by us will be achieved. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs.

Factors that may affect our results are disclosed in “Item 1A. Risk Factors” in Part II of this report and in the section titled “Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2019 (“Form 10-K”). Some of the risks and uncertainties that may cause our actual results, performance or achievements to differ materially from those expressed include, but are not limited to, the following: the difficult market conditions and unfavorable economic conditions and uncertainties associated with the COVID-19 pandemic, particularly in the markets in which we operate and in which our loans are concentrated, including declines in housing markets, an increase in unemployment levels and slowdowns in economic growth; our expected future financial results; the overall health of the local and national real estate market; the credit risk associated with our loan portfolio, such as possible additional loan losses and impairment of collectability of loans as a result of the COVID-19 pandemic and policies and programs implemented by the Coronavirus Aid, Relief, and Economic Security Act ("CARES Act"), including its automatic loan forbearance provisions and the effects on our loan portfolio from our Paycheck Protection Program ("PPP") lending activities, specifically with our commercial real estate loans; our level of nonperforming assets and the costs associated with resolving problem loans; business and economic conditions generally and in the financial services industry, nationally and within our market area; our ability to maintain an adequate level of allowance for loan losses; our ability to successfully manage liquidity risk; our ability to implement our growth strategy and manage costs effectively; the composition of our senior leadership team and our ability to attract and retain key personnel; our ability to raise additional capital to implement our business plan; changes in market interest rates and impacts of such changes on our profits and business; the occurrence of fraudulent activity, breaches or failures of our information security controls or cybersecurity-related incidents; interruptions involving our information technology and telecommunications systems or third-party servicers; our ability to maintain our reputation; increased competition in the financial services industry; regulatory guidance on commercial lending concentrations; our partnership with broker-dealers and digital financial service providers; the effectiveness of our risk management framework; the costs and obligations associated with being a publicly traded company; the commencement and outcome of litigation and other legal proceedings and regulatory actions against us or to which we may become subject; the extensive regulatory framework that applies to us; the impact of recent and future legislative and regulatory changes and economic stimulus programs; and other changes in banking, securities and tax laws and regulations, and their application by our regulators; the impact on our operations due to epidemic illnesses, the effects of regional or national civil unrest, and political developments that may disrupt or increase volatility in securities or otherwise affect economic conditions; the impact of benchmark interest rate reform in the U.S. and implementation of alternative reference rates, such as the Secured Overnight Funding Rate, to the London Interbank Offered Rate ("LIBOR"); fluctuations in the value of the securities held in our securities portfolio; governmental monetary and fiscal policies; material weaknesses in our internal control over financial reporting; and our success at managing the risks involved in the foregoing items.

The foregoing factors should not be construed as exhaustive and should be read together with the other cautionary statements included in this report. If one or more events related to these or other risks or uncertainties materialize, or if our underlying assumptions prove to be incorrect, actual results may differ materially from what we anticipate. Furthermore, many of these risks and uncertainties are currently amplified by and may continue to be amplified by or may, in the future, be amplified by, the outbreak of the COVID-19 pandemic, including a possible second wave, the economic slowdown and the impact of varying governmental responses that affect our customers and the economies where they operate. You are cautioned not to place undue reliance on forward-looking statements. Further, any forward-looking statement speaks only as of the date on which it is made and we undertake no obligation to update or revise any forward-looking statement to reflect events or circumstances after the date on which the statement is made or to reflect the occurrence of unanticipated events, except as required by law.

3

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements

COASTAL FINANCIAL CORPORATION AND SUBSIDIARY

CONDENSED CONSOLIDATED BALANCE SHEETS (UNAUDITED)

(dollars in thousands)

ASSETS | |

| | June 30, | | | December 31, | |

| | 2020 | | | 2019 | |

Cash and due from banks | | $ | 26,510 | | | $ | 16,555 | |

Interest earning deposits with other banks (restricted cash of $0 and $27,355 at June 30, 2020 and December 31, 2019, respectively) | | | 147,666 | | | | 111,259 | |

Investment securities, available for sale, at fair value | | | 20,448 | | | | 28,360 | |

Investment securities, held to maturity, at amortized cost | | | 3,870 | | | | 4,350 | |

Other investments | | | 5,951 | | | | 4,505 | |

Loans receivable | | | 1,447,144 | | | | 939,103 | |

Allowance for loan losses | | | (14,847 | ) | | | (11,470 | ) |

Total loans receivable, net | | | 1,432,297 | | | | 927,633 | |

Premises and equipment, net | | | 16,668 | | | | 13,108 | |

Operating lease right-of-use assets | | | 7,635 | | | | 8,493 | |

Accrued interest receivable | | | 5,944 | | | | 2,980 | |

Bank-owned life insurance, net | | | 6,981 | | | | 6,882 | |

Deferred tax asset, net | | | 2,721 | | | | 2,743 | |

Other assets | | | 2,265 | | | | 1,658 | |

Total assets | | $ | 1,678,956 | | | $ | 1,128,526 | |

| | | | | | | | |

LIABILITIES AND SHAREHOLDERS’ EQUITY | |

LIABILITIES | | | | | | | | |

Deposits | | $ | 1,306,427 | | | $ | 967,959 | |

Federal Home Loan Bank (FHLB) advances | | | 24,999 | | | | 10,000 | |

Paycheck Protection Program Liquidity Facility | | | 190,156 | | | | - | |

Subordinated debt | | | | | | | | |

Principal amount $10,000 (less unamortized debt issuance costs of $14 and $21 at June 30, 2020 and December 31, 2019, respectively) | | | 9,986 | | | | 9,979 | |

Junior subordinated debentures | | | | | | | | |

Principal amount $3,609 (less unamortized debt issuance costs of $25 and $26 at June 30, 2020 and December 31, 2019, respectively) | | | 3,584 | | | | 3,583 | |

Deferred compensation | | | 919 | | | | 974 | |

Accrued interest payable | | | 312 | | | | 308 | |

Operating lease liabilities | | | 7,831 | | | | 8,679 | |

Other liabilities | | | 3,765 | | | | 2,871 | |

Total liabilities | | | 1,547,979 | | | | 1,004,353 | |

SHAREHOLDERS’ EQUITY | | | | | | | | |

Preferred stock, no par value: | | | | | | | | |

Authorized: 25,000,000 shares at June 30, 2020 and December 31, 2019; issued and outstanding: 0 shares at June 30, 2020 and December 31, 2019 | | | - | | | | - | |

Common stock, no par value: | | | | | | | | |

Authorized: 300,000,000 shares at June 30, 2020 and December 31, 2019; 11,926,263 voting shares at June 30, 2020 issued and outstanding and 11,913,885 voting shares at December 31, 2019 issued and outstanding | | | 87,309 | | | | 86,983 | |

Retained earnings | | | 43,617 | | | | 37,222 | |

Accumulated other comprehensive income (loss), net of tax | | | 51 | | | | (32 | ) |

Total shareholders’ equity | | | 130,977 | | | | 124,173 | |

Total liabilities and shareholders’ equity | | $ | 1,678,956 | | | $ | 1,128,526 | |

See accompanying Notes to Condensed Consolidated Financial Statements.

4

COASTAL FINANCIAL CORPORATION AND SUBSIDIARY

CONDENSED CONSOLIDATED STATEMENTS OF INCOME (UNAUDITED)

(dollars in thousands, except for per share data)

| | Three months ended June 30, | | | Six months ended June 30, | |

| | 2020 | | 2019 | | | 2020 | | 2019 | |

INTEREST AND DIVIDEND INCOME | | | | | | | | | | | | | | |

Interest and fees on loans | | $ | 15,154 | | $ | 10,917 | | | $ | 27,781 | | $ | 21,336 | |

Interest on interest earning deposits with other banks | | | 130 | | | 652 | | | | 488 | | | 1,460 | |

Interest on investment securities | | | 53 | | | 160 | | | | 172 | | | 313 | |

Dividends on other investments | | | 89 | | | 75 | | | | 105 | | | 89 | |

Total interest income | | | 15,426 | | | 11,804 | | | | 28,546 | | | 23,198 | |

INTEREST EXPENSE | | | | | | | | | | | | | | |

Interest on deposits | | | 1,096 | | | 1,420 | | | | 2,650 | | | 2,856 | |

Interest on borrowed funds | | | 337 | | | 198 | | | | 539 | | | 389 | |

Total interest expense | | | 1,433 | | | 1,618 | | | | 3,189 | | | 3,245 | |

Net interest income | | | 13,993 | | | 10,186 | | | | 25,357 | | | 19,953 | |

PROVISION FOR LOAN LOSSES | | | 1,930 | | | 547 | | | | 3,508 | | | 1,087 | |

Net interest income after provision for loan losses | | | 12,063 | | | 9,639 | | | | 21,849 | | | 18,866 | |

NONINTEREST INCOME | | | | | | | | | | | | | | |

Deposit service charges and fees | | | 677 | | | 781 | | | | 1,400 | | | 1,507 | |

BaaS fees | | | 475 | | | 502 | | | | 1,054 | | | 948 | |

Loan referral fees | | | 70 | | | 473 | | | | 1,123 | | | 1,106 | |

Mortgage broker fees | | | 152 | | | 111 | | | | 314 | | | 196 | |

Sublease and lease income | | | 31 | | | 10 | | | | 61 | | | 20 | |

Gain on sales of loans, net | | | - | | | 132 | | | | - | | | 121 | |

Other income | | | 115 | | | 123 | | | | 239 | | | 218 | |

Total noninterest income | | | 1,520 | | | 2,132 | | | | 4,191 | | | 4,116 | |

NONINTEREST EXPENSE | | | | | | | | | | | | | | |

Salaries and employee benefits | | | 5,215 | | | 4,529 | | | | 10,898 | | | 9,087 | |

Occupancy | | | 933 | | | 930 | | | | 1,860 | | | 1,924 | |

Data processing | | | 621 | | | 499 | | | | 1,172 | | | 1,028 | |

Director and staff expenses | | | 187 | | | 217 | | | | 457 | | | 457 | |

Excise taxes | | | 262 | | | 180 | | | | 465 | | | 345 | |

Marketing | | | 116 | | | 108 | | | | 228 | | | 202 | |

Legal and professional fees | | | 474 | | | 293 | | | | 797 | | | 702 | |

Federal Deposit Insurance Corporation (FDIC) assessments | | | 74 | | | 134 | | | | 144 | | | 209 | |

Business development | | | 48 | | | 96 | | | | 173 | | | 198 | |

Other expense | | | 1,015 | | | 657 | | | | 1,770 | | | 1,153 | |

Total noninterest expense | | | 8,945 | | | 7,643 | | | | 17,964 | | | 15,305 | |

Income before provision for income taxes | | | 4,638 | | | 4,128 | | | | 8,076 | | | 7,677 | |

PROVISION FOR INCOME TAXES | | | 967 | | | 854 | | | | 1,681 | | | 1,595 | |

NET INCOME | | $ | 3,671 | | $ | 3,274 | | | $ | 6,395 | | $ | 6,082 | |

Basic earnings per common share | | $ | 0.31 | | $ | 0.28 | | | $ | 0.54 | | $ | 0.51 | |

Diluted earnings per common share | | $ | 0.30 | | $ | 0.27 | | | $ | 0.52 | | $ | 0.50 | |

Weighted average number of common shares outstanding: | | | | | | | | | | | | | | |

Basic | | | 11,917,394 | | | 11,895,026 | | | | 11,913,321 | | | 11,889,597 | |

Diluted | | | 12,190,284 | | | 12,202,197 | | | | 12,185,154 | | | 12,192,647 | |

See accompanying Notes to Condensed Consolidated Financial Statements.

5

COASTAL FINANCIAL CORPORATION AND SUBSIDIARY

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (UNAUDITED)

(dollars in thousands)

| | Three months ended June 30, | | | Six months ended June 30, | |

| | 2020 | | | 2019 | | | 2020 | | | 2019 | |

NET INCOME | | $ | 3,671 | | | $ | 3,274 | | | $ | 6,395 | | | $ | 6,082 | |

OTHER COMPREHENSIVE INCOME, before tax | | | | | | | | | | | | | | | | |

Securities available-for-sale | | | | | | | | | | | | | | | | |

Unrealized holding (loss) gain during the period | | | (4 | ) | | | 1,014 | | | | 105 | | | | 1,334 | |

Income tax benefit (expense) related to unrealized holding (loss) gain | | | 1 | | | | (213 | ) | | | (22 | ) | | | (280 | ) |

OTHER COMPREHENSIVE (LOSS) INCOME, net of tax | | | (3 | ) | | | 801 | | | | 83 | | | | 1,054 | |

COMPREHENSIVE INCOME | | $ | 3,668 | | | $ | 4,075 | | | $ | 6,478 | | | $ | 7,136 | |

See accompanying Notes to Condensed Consolidated Financial Statements.

6

COASTAL FINANCIAL CORPORATION AND SUBSIDIARY

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN SHAREHOLDERS’ EQUITY (UNAUDITED)

(dollars in thousands)

| | Shares of Common Stock | | | Common Stock | | | Retained Earnings | | | Accumulated Other Comprehensive Income (Loss) | | | Total | |

BALANCE, March 31, 2019 | | | 11,902,715 | | | $ | 86,579 | | | $ | 26,829 | | | $ | (1,043 | ) | | $ | 112,365 | |

Net income | | | - | | | | - | | | | 3,274 | | | | - | | | | 3,274 | |

Issuance of restricted stock awards | | | - | | | | - | | | | - | | | | - | | | | - | |

Forfeiture of restricted stock awards | | | (1,200 | ) | | | - | | | | - | | | | - | | | | - | |

Exercise of stock options | | | 6,670 | | | | 42 | | | | - | | | | - | | | | 42 | |

Stock-based compensation | | | - | | | | 109 | | | | - | | | | - | | | | 109 | |

Other comprehensive income | | | - | | | | - | | | | - | | | | 801 | | | | 801 | |

BALANCE, June 30, 2019 | | | 11,908,185 | | | $ | 86,730 | | | $ | 30,103 | | | $ | (242 | ) | | $ | 116,591 | |

| | | | | | | | | | | | | | | | | | | | |

BALANCE, March 31, 2020 | | | 11,929,413 | | | $ | 87,166 | | | $ | 39,946 | | | $ | 54 | | | $ | 127,166 | |

Net income | | | - | | | | - | | | | 3,671 | | | | - | | | | 3,671 | |

Forfeiture of restricted stock awards | | | (3,500 | ) | | | - | | | | - | | | | - | | | | - | |

Exercise of stock options | | | 350 | | | | 2 | | | | - | | | | - | | | | 2 | |

Stock-based compensation | | | - | | | | 141 | | | | - | | | | - | | | | 141 | |

Other comprehensive loss | | | - | | | | - | | | | - | | | | (3 | ) | | | (3 | ) |

BALANCE, June 30, 2020 | | | 11,926,263 | | | $ | 87,309 | | | $ | 43,617 | | | $ | 51 | | | $ | 130,977 | |

| | | | | | | | | | | | | | | | | | | | |

BALANCE, December 31, 2018 | | | 11,893,203 | | | $ | 86,431 | | | $ | 24,021 | | | $ | (1,296 | ) | | $ | 109,156 | |

Net income | | | - | | | | - | | | | 6,082 | | | | - | | | | 6,082 | |

Issuance of restricted stock awards | | | 2,352 | | | | - | | | | - | | | | - | | | | - | |

Forfeiture of restricted stock awards | | | (1,200 | ) | | | - | | | | - | | | | - | | | | - | |

Exercise of stock options | | | 13,830 | | | | 84 | | | | - | | | | - | | | | 84 | |

Stock-based compensation | | | - | | | | 215 | | | | - | | | | - | | | | 215 | |

Other comprehensive income | | | - | | | | - | | | | - | | | | 1,054 | | | | 1,054 | |

BALANCE, June 30, 2019 | | | 11,908,185 | | | $ | 86,730 | | | $ | 30,103 | | | $ | (242 | ) | | $ | 116,591 | |

| | | | | | | | | | | | | | | | | | | | |

BALANCE, December 31, 2019 | | | 11,913,885 | | | $ | 86,983 | | | $ | 37,222 | | | $ | (32 | ) | | $ | 124,173 | |

Net income | | | - | | | | - | | | | 6,395 | | | | - | | | | 6,395 | |

Issuance of restricted stock awards | | | 6,248 | | | | - | | | | - | | | | - | | | | - | |

Forfeiture of restricted stock awards | | | (3,500 | ) | | | - | | | | - | | | | - | | | | - | |

Exercise of stock options | | | 9,630 | | | | 56 | | | | - | | | | - | | | | 56 | |

Stock-based compensation | | | - | | | | 270 | | | | - | | | | - | | | | 270 | |

Other comprehensive income | | | - | | | | - | | | | - | | | | 83 | | | | 83 | |

BALANCE, June 30, 2020 | | | 11,926,263 | | | $ | 87,309 | | | $ | 43,617 | | | $ | 51 | | | $ | 130,977 | |

See accompanying Notes to Condensed Consolidated Financial Statements.

7

COASTAL FINANCIAL CORPORATION AND SUBSIDIARY

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED)

(dollars in thousands)

| | Six months ended June 30, | |

| | 2020 | | | 2019 | |

CASH FLOWS FROM OPERATING ACTIVITIES | | | | | | | | |

Net income | | $ | 6,395 | | | $ | 6,082 | |

Adjustments to reconcile net income to net cash provided by operating activities: | | | | | | | | |

Provision for loan losses | | | 3,508 | | | | 1,087 | |

Depreciation and amortization | | | 620 | | | | 606 | |

Loss on disposition of fixed assets | | | 12 | | | | 5 | |

Decrease in operating lease right-of-use assets | | | 842 | | | | 499 | |

Decrease in operating lease liabilities | | | (846 | ) | | | (450 | ) |

Gain on sales of loans | | | - | | | | (121 | ) |

Net premium amortization (discount accretion) on investment securities | | | 19 | | | | (13 | ) |

Stock-based compensation | | | 270 | | | | 215 | |

Increase in bank-owned life insurance value | | | (99 | ) | | | (95 | ) |

Deferred tax (benefit) expense | | | - | | | | (18 | ) |

Net change in other assets and liabilities | | | (2,720 | ) | | | (3,127 | ) |

Total adjustments | | | 1,606 | | | | (1,412 | ) |

Net cash provided by operating activities | | | 8,001 | | | | 4,670 | |

CASH FLOWS FROM INVESTING ACTIVITIES | | | | | | | | |

Net (increase) decrease in interest earning deposits with other banks | | | (63,762 | ) | | | 26,906 | |

Purchase of investment securities available for sale | | | (14,989 | ) | | | (3,182 | ) |

Change in other investments, net | | | (1,446 | ) | | | (634 | ) |

Principal paydowns of investment securities available-for-sale | | | 16 | | | | 32 | |

Principal paydowns of investment securities held-to-maturity | | | 451 | | | | 39 | |

Maturities and calls of investment securities available-for-sale | | | 23,000 | | | | - | |

Purchase of participation loans | | | - | | | | (7,000 | ) |

Proceeds from sale of loans | | | - | | | | 1,581 | |

Increase in loans receivable, net | | | (508,172 | ) | | | (72,055 | ) |

Purchases of premises and equipment, net | | | (4,192 | ) | | | (377 | ) |

Net cash used by investing activities | | | (569,094 | ) | | | (54,690 | ) |

CASH FLOWS FROM FINANCING ACTIVITIES | | | | | | | | |

Net increase in demand deposits, NOW and money market, and savings | | | 352,642 | | | | 62,364 | |

Net (decrease) increase in time deposits | | | (14,174 | ) | | | 2,166 | |

Net repayments from short term FHLB borrowing | | | (10,000 | ) | | | - | |

Net advances from long term FHLB borrowing | | | 24,999 | | | | - | |

Net advances from Paycheck Protection Program Liquidity Facility | | | 190,156 | | | | - | |

Proceeds from exercise of stock options | | | 56 | | | | 84 | |

Net cash provided by financing activities | | | 543,679 | | | | 64,614 | |

NET CHANGE IN CASH, DUE FROM BANKS AND RESTRICTED CASH | | | (17,414 | ) | | | 14,594 | |

CASH, DUE FROM BANKS AND RESTRICTED CASH, beginning of year | | | 43,910 | | | | 40,319 | |

CASH, DUE FROM BANKS AND RESTRICTED CASH, end of quarter | | $ | 26,496 | | | $ | 54,913 | |

SUPPLEMENTAL SCHEDULE OF OPERATING AND INVESTING ACTIVITIES | | | | | | | | |

Interest paid | | $ | 3,185 | | | $ | 3,226 | |

Income taxes paid | | | 1,815 | | | | 1,790 | |

SUPPLEMENTAL SCHEDULE OF NONCASH TRANSACTIONS | | | | | | | | |

Fair value adjustment of securities available-for-sale, gross | | $ | 105 | | | $ | 1,334 | |

In conjunction with ASU 2016-02 as detailed in Note 6 to the Unaudited Consolidated Financial Statements, the following assets and liabilities were recognized: | | | | | | | | |

Operating lease right-of-use assets | | $ | - | | | $ | 9,421 | |

Operating lease liabilities | | $ | - | | | $ | 9,591 | |

See accompanying Notes to Condensed Consolidated Financial Statements.

8

COASTAL FINANCIAL CORPORATION AND SUBSIDIARY

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED)

Note 1 - Description of Business and Summary of Significant Accounting Policies

Nature of operations - Coastal Financial Corporation (“Corporation” or “Company”) is a registered bank holding company whose wholly owned subsidiaries are Coastal Community Bank (“Bank”) and Arlington Olympic LLC (“LLC”). The Company is a Washington state corporation that was organized in 2003. The Bank was incorporated and commenced operations in 1997 and is a Washington state-chartered commercial bank and Federal Reserve System (“Federal Reserve”) state member bank. Arlington Olympic LLC was formed in 2019 and owns the Company’s Arlington branch, which the Bank leases from the LLC.

The Company provides a full range of banking services to small and medium-sized businesses, professionals, and individuals throughout the greater Puget Sound area through its 15 branches in Snohomish, Island, and King Counties, the Internet, and its mobile banking application. The Company opened its 15th branch in Arlington, Washington during the second quarter 2020. The Bank’s main branch and the headquarters of the Bank and Company are located in Everett, Washington. The Bank’s deposits are insured in whole or in part by the FDIC. The Bank’s loans and deposits are primarily within the greater Puget Sound area, and the Bank’s primary funding source is deposits from customers. The Bank also provides banking as a service (“BaaS”) that allow the Company’s broker dealers and digital financial service partners to offer their customers banking services. The Bank is subject to regulation by the Federal Reserve and the Washington State Department of Financial Institutions Division of Banks. The Federal Reserve also has supervisory authority over the Company.

Financial statement presentation - The accompanying unaudited interim condensed consolidated financial statements have been prepared in accordance with U.S. generally accepted accounting principles (“GAAP”) for interim reporting requirements and with instructions to Form 10-Q and Article 10 of Regulation S-X, and therefore do not include all the information and notes included in the annual consolidated financial statements in conformity with GAAP. These interim condensed consolidated financial statements and accompanying notes should be read in conjunction with the Company’s audited consolidated financial statements and accompanying notes included in the Company’s Annual report on Form 10-K as filed with the U.S. Securities and Exchange Commission (“SEC”) on March 12, 2020. Operating results for the three and six months ended June 30, 2020 are not necessarily indicative of the results that may be expected for future periods.

Amounts presented in the consolidated financial statements and footnote tables are rounded and presented in thousands of dollars except per-share amounts, which are presented in dollars. In the narrative footnote discussion, amounts are rounded to thousands and presented in dollars.

In management’s opinion, all accounting adjustments necessary to accurately reflect the financial position and results of operations on the accompanying consolidated financial statements have been made. These adjustments include normal and recurring accruals considered necessary for a fair and accurate presentation.

Principles of consolidation - The consolidated financial statements include the accounts of the Company and the Bank. All significant intercompany accounts have been eliminated in consolidation.

Business Segments - The Company is managed by legal entity and not by lines of business. The entity’s primary business is that of a traditional banking institution, gathering deposits and originating loans for portfolio in its market areas. The Bank offers a wide variety of deposit products to its customers. Lending activities include the origination of real estate, commercial and industrial, and consumer loans. Interest income on loans is the Company’s primary source of revenue, and is supplemented by interest income on deposits with other banks, interest income from investment securities, deposit service charges, and other service provided activities. The Company has determined that its current business and operations consist of a single reporting segment and, therefore, segment disclosures are not required.

Estimates - The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Management believes that its critical accounting policies include determining the allowance for loan losses, the fair value of the Company’s deferred tax assets, and financial instruments. Actual results could differ significantly from those estimates.

Subsequent Events - The Company has evaluated events and transactions subsequent to June 30, 2020 for potential recognition or disclosure. To the extent any events and conditions exist, disclosures are made regarding the nature of events and the estimated

9

financial effects for those events and conditions. The Company is not aware of any subsequent events which would require recognition or disclosure in the consolidated financial statements other than the ones presented below.

The Company recently became a registered lender in the Main Street Lending Program (“MSLP”), which was established by the Federal Reserve, to support lending to small- and medium-sized businesses and nonprofit organizations that were in sound financial condition before the onset of the COVID-19 pandemic. The Company has not yet made any MSLP loans. As a registered lender, the Company will be better positioned to provide financial assistance to customers as the COVID-19 pandemic evolves.

On July 4, the President signed legislation extending the PPP to August 8, 2020. The PPP was originally set to expire on June 30, 2020. The Company will continue to serve its customers and prospective new customers to originate loans in its markets through the latest extension date. The Company funded $10.0 million in PPP loans from July 1, 2020 through August 5, 2020, helping over 1,015 additional people in its communities.

On August 3, 2020 the Bank announced it is working with Google to introduce digital bank accounts, which will be available to its customers through Google Pay in 2021.

Accounting policies – The Company’s complete accounting policies are described in Note 1, summary of significant accounting policies of the Company’s audited consolidated financial statements as of and for the years ended December 31, 2019 and 2018 included in the Company’s Annual Report Form 10-K filed with the SEC on March 12, 2020.

Reclassifications - Certain amounts reported in prior quarters' consolidated financial statements have been reclassified to conform to the current presentation with no effect on stockholders’ equity or net income.

Note 2 - Recent accounting standards

Recent Accounting Guidance

In March 2020, various regulatory agencies, including the Board of Governors of the Federal Reserve System and the Federal Deposit Insurance Corporation, (the “agencies”) issued an interagency statement on loan modifications and reporting for financial institutions working with customers affected by the COVID-19. The interagency statement was effective immediately and impacted accounting for loan modifications. Under Accounting Standards Codification 310-40, Receivables – Troubled Debt Restructurings by Creditors, a restructuring of debt constitutes a troubled debt restructuring (“TDR”) if the creditor, for economic or legal reasons related to the debtor’s financial difficulties, grants a concession to the debtor that it would not otherwise consider. The agencies confirmed with the staff of the Financial Accounting Standards Board (“FASB”) that short-term modifications made on a good faith basis in response to COVID-19 to borrowers who were current prior to any relief are not to be considered TDRs. This includes short-term (e.g., six months) modifications such as payment deferrals, fee waivers, extensions of repayment terms, or other delays in payment that are insignificant. Borrowers considered current are those that are less than 30 days past due on their contractual payments at the time a modification program is implemented. To be eligible a loan modification must be (1) related to COVID-19; (2) executed on a loan that was not more than 30 days past due as of December 31, 2019; and (3) executed between March 1, 2020, and the earlier of (A) 60 days after the date of termination of the federal National Emergency or (B) December 31, 2020. See Note 4 of the Condensed Consolidated Financial Statements of this Report for disclosure of the impact to date.

Recent Accounting Guidance Not Yet Effective

In September 2016, the FASB issued ASU 2016-13, Financial Instruments-Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments. The amendments replace the incurred loss impairment methodology in current GAAP with a methodology that reflects expected credit losses and requires consideration of a broader range of reasonable and supportable information to inform credit loss estimates. The amendment is effective for annual periods beginning after December 15, 2019 and interim period within those annual periods. As a smaller reporting company, the Company’s implementation will be effective January 1, 2023. The Company is actively assessing the data and the model needs and are evaluating the impact of adopting the amendment. The Company expects to recognize a one-time cumulative effect adjustment to the allowance for loan losses as of the beginning of the first reporting period in which the new standard is effective, but cannot yet determine the magnitude of any such one-time adjustment or the overall impact of the new guidance on the consolidated financial statements.

10

Note 3 - Investment Securities

The amortized cost and fair values of investment securities at the date indicated are as follows:

| | Amortized Cost | | | Gross Unrealized Gains | | | Gross Unrealized Losses | | | Fair Value | |

| | (dollars in thousands) | |

June 30, 2020 | | | | | | | | | | | | | | | | |

Available-for-sale | | | | | | | | | | | | | | | | |

U.S. Treasury securities | | $ | 19,990 | | | $ | 53 | | | $ | (1 | ) | | $ | 20,042 | |

U.S. Agency collateralized mortgage obligations | | | 118 | | | | 5 | | | | - | | | | 123 | |

U.S. Agency residential mortgage-backed securities | | | 21 | | | | - | | | | - | | | | 21 | |

Municipal bonds | | | 255 | | | | 7 | | | | - | | | | 262 | |

Total available-for-sale securities | | | 20,384 | | | | 65 | | | | (1 | ) | | | 20,448 | |

Held-to-maturity | | | | | | | | | | | | | | | | |

U.S. Agency residential mortgage-backed securities | | | 3,870 | | | | 121 | | | | - | | | | 3,991 | |

Total investment securities | | $ | 24,254 | | | $ | 186 | | | $ | (1 | ) | | $ | 24,439 | |

| | Amortized Cost | | | Gross Unrealized Gains | | | Gross Unrealized Losses | | | Fair Value | |

| | (dollars in thousands) | |

December 31, 2019 | | | | | | | | | | | | | | | | |

Available-for-sale | | | | | | | | | | | | | | | | |

U.S. Treasury securities | | $ | 24,988 | | | $ | 1 | | | $ | (44 | ) | | $ | 24,945 | |

U.S. Government agencies | | | 3,000 | | | | - | | | | (1 | ) | | | 2,999 | |

U.S. Agency collateralized mortgage obligations | | | 129 | | | | - | | | | - | | | | 129 | |

U.S. Agency residential mortgage-backed securities | | | 27 | | | | - | | | | - | | | | 27 | |

Municipal bonds | | | 257 | | | | 3 | | | | - | | | | 260 | |

Total available-for-sale securities | | | 28,401 | | | | 4 | | | | (45 | ) | | | 28,360 | |

Held-to-maturity | | | | | | | | | | | | | | | | |

U.S. Agency residential mortgage-backed securities | | | 4,350 | | | | - | | | | (21 | ) | | | 4,329 | |

Total investment securities | | $ | 32,751 | | | $ | 4 | | | $ | (66 | ) | | $ | 32,689 | |

| | | | | | | | | | | | | | | | |

The amortized cost and fair value of debt securities at June 30, 2020, by contractual maturity, are shown below. Expected maturities will differ from contractual maturities because issuers or the underlying borrowers may have the right to call or prepay obligations with or without call or prepayment penalties. Mortgage-backed securities and collateralized mortgage obligations are shown separately, since they are not due at a single maturity date.

| | Available-for-Sale | | | Held-to-Maturity | |

| | Amortized Cost | | | Fair Value | | | Amortized Cost | | | Fair Value | |

| | (dollars in thousands) | |

June 30, 2020 | | | | | | | | | | | | | | | | |

Amounts maturing in | | | | | | | | | | | | | | | | |

One year or less | | $ | 14,991 | | | $ | 14,991 | | | $ | - | | | $ | - | |

After one year through five years | | | 5,254 | | | | 5,313 | | | | - | | | | - | |

| | | 20,245 | | | | 20,304 | | | | - | | | | - | |

U.S. Agency residential mortgage-backed securities and collateralized mortgage obligations | | | 139 | | | | 144 | | | | 3,870 | | | | 3,991 | |

| | $ | 20,384 | | | $ | 20,448 | | | $ | 3,870 | | | $ | 3,991 | |

Investment securities with carrying values of $19,480,000 and $16,843,000 at June 30, 2020 and December 31, 2019 respectively, were pledged to secure public deposits and for other purposes as required or permitted by law.

11

There were 0 sales of securities available for sale during the three or six months ended June 30, 2020 and 2019.

Information pertaining to securities with gross unrealized losses at the dates indicated, aggregated by investment category and length of time that individual securities have been in a continuous loss position, follows:

| | Less Than 12 Months | | | 12 Months or Greater | | | Total | |

| | Fair Value | | | Gross Unrealized Losses | | | Fair Value | | | Gross Unrealized Losses | | | Fair Value | | | Gross Unrealized Losses | |

| | (dollars in thousands) | |

June 30, 2020 | | | | | | | | | | | | | | | | | | | | | | | | |

Available-for-sale | | | | | | | | | | | | | | | | | | | | | | | | |

U.S. Treasury securities | | $ | 14,991 | | | $ | (1 | ) | | $ | - | | | $ | - | | | $ | - | | | $ | - | |

Total investment securities | | $ | 14,991 | | | $ | (1 | ) | | $ | - | | | $ | - | | | $ | - | | | $ | - | |

| | | | | | | | | | | | | | | | | | | | | | | | |

December 31, 2019 | | | | | | | | | | | | | | | | | | | | | | | | |

Available-for-sale | | | | | | | | | | | | | | | | | | | | | | | | |

U.S. Treasury securities | | $ | 9,994 | | | $ | (3 | ) | | $ | 4,956 | | | $ | (41 | ) | | $ | 14,950 | | | $ | (44 | ) |

U.S. Government agencies | | | - | | | | - | | | | 2,999 | | | | (1 | ) | | | 2,999 | | | | (1 | ) |

Total available-for-sale securities | | | 9,994 | | | | (3 | ) | | | 7,955 | | | | (42 | ) | | | 17,949 | | | | (45 | ) |

Held-to-maturity | | | | | | | | | | | | | | | | | | | | | | | | |

U.S. Agency residential mortgage-backed securities | | | 3,140 | | | | (14 | ) | | | 1,189 | | | | (7 | ) | | | 4,329 | | | | (21 | ) |

Total investment securities | | $ | 13,134 | | | $ | (17 | ) | | $ | 9,144 | | | $ | (49 | ) | | $ | 22,278 | | | $ | (66 | ) |

At June 30, 2020 and December 31, 2019, there were 2 and 6 securities in an unrealized loss position, respectively. Unrealized losses have not been recognized into income because management does not intend to sell and does not expect that it will be required to sell the investments. The decline is largely due to changes in market conditions and interest rates, rather than credit quality. The fair value is expected to recover as the underlying securities in the portfolio approach maturity date and market conditions improve. The Company does 0t consider these securities to be other than temporarily impaired at June 30, 2020 and December 31, 2019.

Note 4 - Loans and Allowance for Loan Losses

The composition of the loan portfolio is as follows as of the periods indicated:

| | June 30, | | | December 31, | |

| | 2020 | | | 2019 | |

| | | | | | | | |

Commercial and industrial loans | | $ | 551,550 | | | $ | 111,401 | |

Real estate loans: | | | | | | | | |

Construction, land, and land development | | | 102,422 | | | | 97,034 | |

Residential real estate | | | 122,949 | | | | 115,011 | |

Commercial real estate | | | 678,335 | | | | 613,398 | |

Consumer and other loans | | | 4,735 | | | | 4,214 | |

Gross loans receivable | | | 1,459,991 | | | | 941,058 | |

Net deferred origination fees and premiums | | | (12,847 | ) | | | (1,955 | ) |

Loans receivable | | $ | 1,447,144 | | | $ | 939,103 | |

Included in consumer and other loans are overdrafts of $13,000 and $26,000 at June 30, 2020 and December 31, 2019, respectively. The Company has pledged loans totaling $359,278,000 and $163,522,000 at June 30, 2020 and December 31, 2019, respectively, for borrowing lines at the FHLB and Federal Reserve Bank (“FRB”).

The balance of Small Business Administration (“SBA”) and United States Department of Agriculture (“USDA”) loans was $470,700,000 and $36,592,000 at June 30, 2020 and December 31, 2019, respectively. PPP loans of $438,077,000 at June 30, 2020 are included in the commercial and industrial loans balance. Included in these totals are SBA and USDA loans serviced for others totaling $21,101,000 and $21,498,000 at June 30, 2020 and December 31, 2019, respectively. Net deferred origination fees include $10,639,000 of net fees from PPP loans as of June 30, 2020.

12

The Company, at times, purchases individual loans at fair value as of the acquisition date. Purchased loans with remaining balances totaled $25,151,000 and $32,937,000 as of June 30, 2020 and December 31, 2019, respectively. Unamortized premiums totaled $398,000 and $527,000 as of June 30, 2020 and December 31, 2019, respectively, and are amortized into interest income over the life of the loans.

The Company has purchased participation loans with remaining balances totaling $35,456,000 and $31,352,000 as of June 30, 2020 and December 31, 2019, respectively.

The following is a summary of the Company’s loan portfolio segments:

Commercial and industrial loans - Commercial and industrial loans are secured by business assets including inventory, receivables and machinery and equipment of businesses located generally in the Company’s primary market area. Loan types include revolving lines of credit, term loans, and loans secured by liquid collateral such as cash deposits or marketable securities. The Company also issues letters of credit on behalf of its customers. Risk arises primarily due to the difference between expected and actual cash flows of the borrowers. In addition, the recoverability of the Company’s investment in these loans is also dependent on other factors primarily dictated by the type of collateral securing these loans. The fair value of the collateral securing these loans may fluctuate as market conditions change. In the case of loans secured by accounts receivable, the recovery of the Company’s investment is dependent upon the borrower’s ability to collect amounts due from its customers. Also included in this category are SBA 7(a) loans, which allow small business owners to apply for financial assistance via the PPP as prescribed in the CARES Act. These loans have a contractual rate of 1.0%, with maturity terms of two to five years, are unsecured, 100% guaranteed and loan proceeds may be forgiven by the U.S. Government / SBA if used for certain purposes.

Construction, land and land development loans – The Company originates loans for the construction of 1-4 family, multifamily, and Commercial Real Estate (“CRE”) properties in the Company’s market area. Construction loans are considered to have higher risks due to construction completion and timing risk, the ultimate repayment being sensitive to interest rate changes, government regulation of real property and the availability of long-term financing. Additionally, economic conditions may impact the Company’s ability to recover its investment in construction loans, as adverse economic conditions may negatively impact the real estate market, which could affect the borrower’s ability to complete and sell the project. Additionally, the fair value of the underlying collateral may fluctuate as market conditions change. The Company occasionally originates land loans for the purpose of facilitating the ultimate construction of a home or commercial building. The primary risks include the borrower’s ability to pay and the inability of the Company to recover its investment due to a material decline in the fair value of the underlying collateral.

Residential real estate loans - Residential real estate loans include various types of loans for which the Company holds real property as collateral. Included in this segment are first lien single family loans, which are occasionally purchased to diversify the Company’s loan portfolio, and rental portfolios secured by one-to-four family homes. The primary risks of residential real estate loans include the borrower’s inability to pay, material decreases in the value of the collateral, and significant increases in interest rates which may make the loan unprofitable.

Commercial real estate (includes owner occupied and nonowner occupied) loans - Commercial real estate loans include various types of loans for which the Company holds real property as collateral. The primary risks of commercial real estate loans include the borrower’s inability to pay, material decreases in the value of the collateralized real estate and significant increases in interest rates, which may make the real estate loan unprofitable. Commercial real estate loans may be more adversely affected by conditions in the real estate markets or in the general economy.

Consumer and other loans – The Company originates a limited number of consumer loans, generally for banking customers only, which consist primarily of home equity lines of credit, saving account secured loans, and auto loans. This loan category also includes overdrafts. Repayment of these loans is dependent on the borrower’s ability to pay and the fair value of the underlying collateral.

13

The following table illustrates an age analysis of past due loans as of the dates indicated:

| | 30-89 Days Past Due | | | 90 Days or More Past Due | | | Total Past Due | | | Current | | | Total Loans | | | Recorded Investment 90 Days or More Past Due and Still Accruing | |

| | (dollars in thousands) | |

June 30, 2020 | | | | | | | | | | | | | | | | | | | | | | | | |

Commercial and industrial loans | | $ | - | | | $ | 689 | | | $ | 689 | | | $ | 550,861 | | | $ | 551,550 | | | $ | - | |

Real estate loans: | | | | | | | | | | | | | | | | | | | | | | | | |

Construction, land and land development | | | 3,270 | | | | - | | | | 3,270 | | | | 99,152 | | | | 102,422 | | | | - | |

Residential real estate | | | 121 | | | | 63 | | | | 184 | | | | 122,765 | | | | 122,949 | | | | - | |

Commercial real estate | | | 413 | | | | - | | | | 413 | | | | 677,922 | | | | 678,335 | | | | - | |

Consumer and other loans | | | - | | | | - | | | | - | | | | 4,735 | | | | 4,735 | | | | - | |

| | $ | 3,804 | | | $ | 752 | | | $ | 4,556 | | | $ | 1,455,435 | | | $ | 1,459,991 | | | $ | - | |

Less net deferred origination fees and premiums | | | | | | | | | | | | | | | | | | | (12,847 | ) | | | | |

Loans receivable | | | | | | | | | | | | | | | | | | $ | 1,447,144 | | | | | |

| | 30-89 Days Past Due | | | 90 Days or More Past Due | | | Total Past Due | | | Current | | | Total Loans | | | Recorded Investment 90 Days or More Past Due and Still Accruing | |

| | (dollars in thousands) | |

December 31, 2019 | | | | | | | | | | | | | | | | | | | | | | | | |

Commercial and industrial loans | | $ | 143 | | | $ | 965 | | | $ | 1,108 | | | $ | 110,293 | | | $ | 111,401 | | | $ | - | |

Real estate loans: | | | | | | | | | | | | | | | | | | | | | | | | |

Construction, land and land development | | | - | | | | - | | | | - | | | | 97,034 | | | | 97,034 | | | | - | |

Residential real estate | | | - | | | | 65 | | | | 65 | | | | 114,946 | | | | 115,011 | | | | - | |

Commercial real estate | | | 417 | | | | - | | | | 417 | | | | 612,981 | | | | 613,398 | | | | - | |

Consumer and other loans | | | 4 | | | | - | | | | 4 | | | | 4,210 | | | | 4,214 | | | | - | |

| | $ | 564 | | | $ | 1,030 | | | $ | 1,594 | | | $ | 939,464 | | | | 941,058 | | | $ | - | |

Less net deferred origination fees and premiums | | | | | | | | | | | | | | | | | | | (1,955 | ) | | | | |

Loans receivable | | | | | | | | | | | | | | | | | | $ | 939,103 | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | |

14

A summary of information pertaining to impaired loans as of the period indicated:

| | Unpaid Contractual Principal Balance | | | Recorded Investment With No Allowance | | | Recorded Investment With Allowance | | | Total Recorded Investment | | | Related Allowance | |

| | (dollars in thousands) | |

June 30, 2020 | | | | | | | | | | | | | | | | | | | | |

Commercial and industrial loans | | $ | 986 | | | $ | 689 | | | $ | - | | | $ | 689 | | | $ | - | |

Real estate loans: | | | | | | | | | | | | | | | | | | | | |

Construction, land and land development | | | 3,270 | | | | 3,270 | | | | - | | | | 3,270 | | | | - | |

Residential real estate | | | 72 | | | | 63 | | | | - | | | | 63 | | | | - | |

Commercial real estate | | | 413 | | | | 413 | | | | - | | | | 413 | | | | - | |

Total | | $ | 4,741 | | | $ | 4,435 | | | $ | - | | | $ | 4,435 | | | $ | - | |

| | | | | | | | | | | | | | | | | | | | |

December 31, 2019 | | | | | | | | | | | | | | | | | | | | |

Commercial and industrial loans | | $ | 1,431 | | | $ | 965 | | | $ | - | | | $ | 965 | | | $ | - | |

Real estate loans: | | | | | | | | | | | | | | | | | | | | |

Residential real estate | | | 73 | | | | 65 | | | | - | | | | 65 | | | | - | |

Consumer | | | 2 | | | | - | | | | 2 | | | | 2 | | | | 2 | |

Total | | $ | 1,506 | | | $ | 1,030 | | | $ | 2 | | | $ | 1,032 | | | $ | 2 | |

| | | | | | | | | | | | | | | | | | | | |

The following tables summarize the Company’s average recorded investment and interest income recognized on impaired loans by loan class for the three and six months ended June 30, 2020 and 2019:

| | Three Months Ended | |

| | June 30, 2020 | | | June 30, 2019 | |

| | Average Recorded Investment | | | Interest Income Recognized | | | Average Recorded Investment | | | Interest Income Recognized | |

| | (dollars in thousands) | |

Commercial and industrial loans | | $ | 694 | | | $ | - | | | $ | 890 | | | $ | - | |

Real estate loans: | | | | | | | | | | | | | | | | |

Construction, land and land development | | | 252 | | | | - | | | | - | | | | - | |

Residential real estate | | | 63 | | | | - | | | | 71 | | | | - | |

Commercial real estate | | | 9 | | | | - | | | | - | | | | - | |

Total | | $ | 1,018 | | | $ | - | | | $ | 961 | | | $ | - | |

| | | | | | | | | | | | | | | | |

| | Six Months Ended | |

| | June 30, 2020 | | | June 30, 2019 | |

| | Average Recorded Investment | | | Interest Income Recognized | | | Average Recorded Investment | | | Interest Income Recognized | |

| | (dollars in thousands) | |

Commercial and industrial loans | | $ | 789 | | | $ | - | | | $ | 718 | | | $ | - | |

Real estate loans: | | | | | | | | | | | | | | | | |

Construction, land and land development | | | 63 | | | | - | | | | - | | | | - | |

Residential real estate | | | 64 | | | | - | | | | 72 | | | | - | |

Commercial real estate | | | 2 | | | | - | | | | - | | | | - | |

Consumer and other loans | | | 1 | | | | - | | | | - | | | | - | |

Total | | $ | 919 | | | $ | - | | | $ | 790 | | | $ | - | |

The Company grants restructurings in response to borrower financial difficulty, and generally provides for a temporary modification of loan repayment terms. The restructured loans on accrual status represent the only impaired loans accruing interest. In order for a restructured loan to be considered for accrual status, the loan’s collateral coverage generally will be greater than or equal to

15

100% of the loan balance, the loan is current on payments, and the borrower must either prefund an interest reserve or demonstrate the ability to make payments from a verified source of cash flow for an extended period of time, usually at least six months in duration.

NaN loans were restructured in the three or six months ended June 30, 2020 and June 30, 2019 that qualified as troubled debt restructurings (“TDRs”). The Company has 0 commitments to loan additional funds to borrowers whose loans were classified as TDRs at June 30, 2020, as there were 0 outstanding TDRs at June 30, 2020.

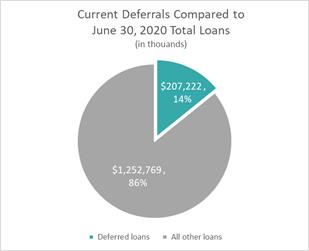

The Company is in contact with borrowers with existing loans that have been impacted by COVID-19. The Company has restructured payments for loan customers during this uncertain time to help alleviate financial hardships, deferring payments on 215 loans, representing $207.2 million in outstanding loans, and $5,611,000 in unused commitments, as of June 30, 2020. In accordance with GAAP and interagency guidance issued on March 22, 2020, these short-term modifications, six months or less, made on a good faith basis in response to COVID-19 to borrowers that were current prior to any relief, are not considered troubled debt restructurings.

When loans are placed on nonaccrual status, all accrued interest is reversed from current period earnings. Payments received on nonaccrual loans are generally applied as a reduction to the loan principal balance. If the likelihood of further loss is removed, the Company will recognize interest on a cash basis only. Loans may be returned to accruing status if the Company believes that all remaining principal and interest is fully collectible and there has been at least six months of sustained repayment performance since the loan was placed on nonaccrual.

An analysis of nonaccrual loans by category consisted of the following at the periods indicated:

| | June 30, | | | December 31, | |

| | 2020 | | | 2019 | |

| | (dollars in thousands) | |

Commercial and industrial loans | | $ | 689 | | | $ | 965 | |

Real estate loans: | | | | | | | | |

Construction, land and land development | | | 3,270 | | | | - | |

Residential real estate | | | 63 | | | | 65 | |

Commercial real estate | | | 413 | | | | - | |

Total nonaccrual loans | | $ | 4,435 | | | $ | 1,030 | |

Credit Quality and Credit Risk

Federal regulations require that the Company periodically evaluate the risks inherent in its loan portfolio. In addition, the Company’s regulatory agencies have authority to identify problem loans and, if appropriate, require them to be reclassified. There are three classifications for problem loans: Substandard, Doubtful, and Loss. Substandard loans have one or more defined weaknesses and are characterized by the distinct possibility that the Company will sustain some loss if the deficiencies are not corrected. Doubtful loans have the weaknesses of loans classified as Substandard, with additional characteristics that suggest the weaknesses make collection or recovery in full after liquidation of collateral questionable on the basis of currently existing facts, conditions, and values. There is a high possibility of loss in loans classified as Doubtful. A loan classified as Loss is considered uncollectible and of such little value that continued classification of the credit as a loan is not warranted. If a loan or a portion thereof is classified as Loss, it must be charged-off, meaning the amount of the loss is charged against the allowance for loan losses, thereby reducing that reserve. The Company also classifies some loans as Watch or Other Loans Especially Mentioned (“OLEM”). Loans classified as Watch are performing assets and classified as pass credits but have elements of risk that require more monitoring than other performing loans and are reported in the OLEM column in the following table. Loans classified as OLEM are assets that continue to perform but have shown deterioration in credit quality and require close monitoring.

16

Loans by credit quality risk rating are as follows as of the periods indicated:

| | Pass | | | Other Loans Especially Mentioned | | | Sub- Standard | | | Doubtful | | | Total | |

| | (dollars in thousands) | |

June 30, 2020 | | | | | | | | | | | | | | | | | | | | |

Commercial and industrial loans | | $ | 540,641 | | | $ | 9,433 | | | $ | 1,476 | | | $ | - | | | $ | 551,550 | |

Real estate loans: | | | | | | | | | | | | | | | | | | | | |

Construction, land, and land development | | | 99,152 | | | | - | | | | 3,270 | | | | - | | | | 102,422 | |

Residential real estate | | | 122,473 | | | | 413 | | | | 63 | | | | - | | | | 122,949 | |

Commercial real estate | | | 666,337 | | | | 11,585 | | | | 413 | | | | - | | | | 678,335 | |

Consumer and other loans | | | 4,735 | | | | - | | | | - | | | | - | | | | 4,735 | |

| | $ | 1,433,338 | | | $ | 21,431 | | | $ | 5,222 | | | $ | - | | | | 1,459,991 | |

Less net deferred origination fees | | | | | | | | | | | | | | | | | | | (12,847 | ) |

Loans receivable | | | | | | | | | | | | | | | | | | $ | 1,447,144 | |

| | | | | | | | | | | | | | | | | | | | |

December 31, 2019 | | | | | | | | | | | | | | | | | | | | |

Commercial and industrial loans | | $ | 104,911 | | | $ | 4,740 | | | $ | 1,750 | | | $ | - | | | $ | 111,401 | |

Real estate loans: | | | | | | | | | | | | | | | | | | | | |

Construction, land, and land development | | | 97,034 | | | | - | | | | - | | | | - | | | | 97,034 | |

Residential real estate | | | 114,823 | | | | 123 | | | | 65 | | | | - | | | | 115,011 | |

Commercial real estate | | | 608,773 | | | | 4,625 | | | | - | | | | - | | | | 613,398 | |

Consumer and other loans | | | 4,212 | | | | - | | | | 2 | | | | | | | | 4,214 | |

| | $ | 929,753 | | | $ | 9,488 | | | $ | 1,817 | | | $ | - | | | | 941,058 | |

Less net deferred origination fees | | | | | | | | | | | | | | | | | | | (1,955 | ) |

Loans receivable | | | | | | | | | | | | | | | | | | $ | 939,103 | |

| | | | | | | | | | | | | | | | | | | | |

Allowance for Loan Losses

The Company’s allowance for loan losses (“ALLL”) covers estimated credit losses on individually evaluated loans that are determined to be impaired as well as estimated probable losses inherent in the remainder of the loan portfolio. The ALLL is prepared using the information provided by the Company’s credit review process together with economic information gathered from published sources. Qualitative factors that are included in the analysis include industry data and data from peer institutions.

The loan portfolio is segmented into groups of loans with similar risk profiles. Each segment possesses varying degrees of risk based on the type of loan, the type of collateral, and the sensitivity of the borrower or industry to changes in external factors such as economic conditions. An estimated loss rate calculated from the Company’s actual historical loss rates adjusted for current portfolio trends, economic conditions, and other relevant internal and external factors, is applied to each group’s aggregate loan balances. The $438.1 million in PPP loans as of June 30, 2020 are 100% guaranteed and were not subject to the allowance analysis or assigned an allowance.

The Company’s provision for credit losses of $1.9 million and $3.5 million during the three and six months ended June 30, 2020, respectively, is related to the growth in the loan portfolio along with an increase in qualitative factors primarily related to the uncertainties in the economic outlook from the COVID-19 pandemic. The Company is not required to implement the provisions of the Current Expected Credit Loss (“CECL”) accounting standard until January 1, 2023 and is continuing to account for the allowance for loan losses under the incurred loss model.

17

The following tables summarize the allocation of the ALLL, as well as the activity in the ALLL attributed to various segments in the loan portfolio, as of and for the three and six months ended June 30, 2020:

| | Commercial and Industrial | | | Construction, Land, and Land Development | | | Residential Real Estate | | | Commercial Real Estate | | | Consumer and Other | | | Unallocated | | | Total | |

| | (dollars in thousands) | |

Three Months Ended June 30, 2020 | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

ALLL balance, March 31, 2020 | | $ | 2,837 | | | $ | 3,647 | | | $ | 2,232 | | | $ | 3,889 | | | $ | 96 | | | $ | 224 | | | $ | 12,925 | |

Provision for loan losses or (recapture) | | | 23 | | | | (269 | ) | | | 437 | | | | 1,346 | | | | 45 | | | | 348 | | | | 1,930 | |

| | | 2,860 | | | | 3,378 | | | | 2,669 | | | | 5,235 | | | | 141 | | | | 572 | | | | 14,855 | |

Loans charged-off | | | (11 | ) | | | - | | | | - | | | | - | | | | (2 | ) | | | - | | | | (13 | ) |

Recoveries of loans previously charged-off | | | 4 | | | | - | | | | - | | | | - | | | | 1 | | | | - | | | | 5 | |

Net (charge-offs) recoveries | | | (7 | ) | | | - | | | | - | | | | - | | | | (1 | ) | | | - | | | | (8 | ) |

ALLL balance, June 30, 2020 | | $ | 2,853 | | | $ | 3,378 | | | $ | 2,669 | | | $ | 5,235 | | | $ | 140 | | | $ | 572 | | | $ | 14,847 | |

Six Months Ended June 30, 2020 | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

ALLL balance, December 31, 2019 | | $ | 2,366 | | | $ | 2,745 | | | $ | 2,069 | | | $ | 3,126 | | | $ | 104 | | | $ | 1,060 | | | $ | 11,470 | |

Provision for loan losses or (recapture) | | | 612 | | | | 633 | | | | 600 | | | | 2,109 | | | | 42 | | | | (488 | ) | | | 3,508 | |

| | | 2,978 | | | | 3,378 | | | | 2,669 | | | | 5,235 | | | | 146 | | | | 572 | | | | 14,978 | |

Loans charged-off | | | (130 | ) | | | - | | | | - | | | | - | | | | (7 | ) | | | - | | | | (137 | ) |

Recoveries of loans previously charged-off | | | 5 | | | | - | | | | - | | | | - | | | | 1 | | | | - | | | | 6 | |

Net (charge-offs) recoveries | | | (125 | ) | | | - | | | | - | | | | - | | | | (6 | ) | | | - | | | | (131 | ) |

ALLL balance, June 30, 2020 | | $ | 2,853 | | | $ | 3,378 | | | $ | 2,669 | | | $ | 5,235 | | | $ | 140 | | | $ | 572 | | | $ | 14,847 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

As of June 30, 2020 | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

ALLL amounts allocated to | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Individually evaluated for impairment | | $ | - | | | $ | - | | | $ | - | | | $ | - | | | $ | - | | | $ | - | | | $ | - | |

Collectively evaluated for impairment | | | 2,853 | | | | 3,378 | | | | 2,669 | | | | 5,235 | | | | 140 | | | | 572 | | | | 14,847 | |

ALLL balance, June 30, 2020 | | $ | 2,853 | | | $ | 3,378 | | | $ | 2,669 | | | $ | 5,235 | | | $ | 140 | | | $ | 572 | | | $ | 14,847 | |

Loans individually evaluated for impairment | | $ | 689 | | | $ | 3,270 | | | $ | 63 | | | $ | 413 | | | $ | - | | | | | | | $ | 4,435 | |

Loans collectively evaluated for impairment | | | 550,861 | | | | 99,152 | | | | 122,886 | | | | 677,922 | | | | 4,735 | | | | | | | | 1,455,556 | |

Loan balance, June 30, 2020 | | $ | 551,550 | | | $ | 102,422 | | | $ | 122,949 | | | $ | 678,335 | | | $ | 4,735 | | | | | | | $ | 1,459,991 | |

18

The following tables summarize the allocation of the ALLL, as well as the activity in the ALLL attributed to various segments in the loan portfolio, as of and for the three and six months ended June 30, 2019:

| | Commercial and Industrial | | | Construction, Land, and Land Development | | | Residential Real Estate | | | Commercial Real Estate | | | Consumer and Other | | | Unallocated | | | Total | |

| | (dollars in thousands) | |

Three months ended June 30, 2019 | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Balance, March 31, 2019 | | $ | 2,069 | | | $ | 1,852 | | | $ | 1,623 | | | $ | 2,750 | | | $ | 79 | | | $ | 1,542 | | | $ | 9,915 | |

Provision for loan losses or (recapture) | | | 419 | | | | 534 | | | | 191 | | | | 95 | | | | 1 | | | | (693 | ) | | | 547 | |

| | | 2,488 | | | | 2,386 | | | | 1,814 | | | | 2,845 | | | | 80 | | | | 849 | | | | 10,462 | |

Loans charged-off | | | (7 | ) | | | - | | | | - | | | | - | | | | (15 | ) | | | - | | | | (22 | ) |

Recoveries of loans previously charged-off | | | 1 | | | | - | | | | - | | | | - | | | | 2 | | | | - | | | | 3 | |

Net (charge-offs) recoveries | | | (6 | ) | | | - | | | | - | | | | - | | | | (13 | ) | | | - | | | | (19 | ) |

Balance, June 30, 2019 | | $ | 2,482 | | | $ | 2,386 | | | $ | 1,814 | | | $ | 2,845 | | | $ | 67 | | | $ | 849 | | | $ | 10,443 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Six months ended June 30, 2019 | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Balance, December 31, 2018 | | $ | 2,039 | | | $ | 1,806 | | | $ | 1,647 | | | $ | 2,648 | | | $ | 77 | | | $ | 1,190 | | | $ | 9,407 | |

Provision for loan losses or (recapture) | | | 448 | | | | 580 | | | | 167 | | | | 226 | | | | 7 | | | | (341 | ) | | | 1,087 | |

| | | 2,487 | | | | 2,386 | | | | 1,814 | | | | 2,874 | | | | 84 | | | | 849 | | | | 10,494 | |

Loans charged-off | | | (7 | ) | | | - | | | | - | | | | (29 | ) | | | (20 | ) | | | - | | | | (56 | ) |

Recoveries of loans previously charged-off | | | 2 | | | | - | | | | - | | | | - | | | | 3 | | | | - | | | | 5 | |

Net (charge-offs) recoveries | | | (5 | ) | | | - | | | | - | | | | (29 | ) | | | (17 | ) | | | - | | | | (51 | ) |

Balance, June 30, 2019 | | $ | 2,482 | | | $ | 2,386 | | | $ | 1,814 | | | $ | 2,845 | | | $ | 67 | | | $ | 849 | | | $ | 10,443 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

As of June 30, 2019 | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

ALLL amounts allocated to | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Individually evaluated for impairment | | $ | 229 | | | $ | - | | | $ | - | | | $ | - | | | $ | - | | | $ | - | | | $ | 229 | |

Collectively evaluated for impairment | | | 2,253 | | | | 2,386 | | | | 1,814 | | | | 2,845 | | | | 67 | | | | 849 | | | | 10,214 | |

ALLL balance, June 30, 2019 | | $ | 2,482 | | | $ | 2,386 | | | $ | 1,814 | | | $ | 2,845 | | | $ | 67 | | | $ | 849 | | | $ | 10,443 | |

Loans individually evaluated for impairment | | $ | 1,579 | | | $ | - | | | $ | 69 | | | $ | - | | | $ | - | | | | | | | $ | 1,648 | |

Loans collectively evaluated for impairment | | | 99,531 | | | | 84,666 | | | | 100,377 | | | | 557,692 | | | | 2,893 | | | | | | | | 845,159 | |

Loan balance, June 30, 2019 | | $ | 101,110 | | | $ | 84,666 | | | $ | 100,446 | | | $ | 557,692 | | | $ | 2,893 | | | | | | | $ | 846,807 | |

The following table summarizes the allocation of the ALLL attributed to various segments in the loan portfolio as of December 31, 2019.

| | Commercial and Industrial | | | Construction, Land, and Land Development | | | Residential Real Estate | | | Commercial Real Estate | | | Consumer and Other | | | Unallocated | | | Total | |

| | (dollars in thousands) | |

As of December 31, 2019 | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

ALLL amounts allocated to | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Individually evaluated for impairment | | $ | - | | | $ | - | | | $ | - | | | $ | - | | | $ | 2 | | | $ | - | | | $ | 2 | |

Collectively evaluated for impairment | | | 2,366 | | | | 2,745 | | | | 2,069 | | | | 3,126 | | | | 102 | | | | 1,060 | | | | 11,468 | |

ALLL balance, December 31, 2019 | | $ | 2,366 | | | $ | 2,745 | | | $ | 2,069 | | | $ | 3,126 | | | $ | 104 | | | $ | 1,060 | | | $ | 11,470 | |

Loans individually evaluated for impairment | | $ | 965 | | | $ | - | | | $ | 65 | | | $ | - | | | $ | 2 | | | | | | | $ | 1,032 | |

Loans collectively evaluated for impairment | | | 110,436 | | | | 97,034 | | | | 114,946 | | | | 613,398 | | | | 4,212 | | | | | | | | 940,026 | |

Loan balance, December 31, 2019 | | $ | 111,401 | | | $ | 97,034 | | | $ | 115,011 | | | $ | 613,398 | | | $ | 4,214 | | | | | | | $ | 941,058 | |

19

Note 5 - Deposits

The composition of consolidated deposits consisted of the following at the periods indicated:

| | June 30, | | | December 31, | |

| | 2020 | | | 2019 | |

| | (dollars in thousands) | |

Demand, noninterest bearing | | $ | 563,794 | | | $ | 371,243 | |

NOW and money market | | | 576,376 | | | | 437,908 | |

Savings | | | 72,045 | | | | 53,365 | |

BaaS-brokered deposits | | | 26,529 | | | | 23,586 | |

Time deposits less than $250,000 | | | 43,900 | | | | 51,644 | |

Time deposits $250,000 and over | | | 23,783 | | | | 30,213 | |

Total deposits | | $ | 1,306,427 | | | $ | 967,959 | |

The following table presents the maturity distribution of time deposits as of June 30, 2020 (dollars in thousands):

Twelve months | | $ | 53,220 | |

One to two years | | | 10,084 | |

Two to three years | | | 2,394 | |

Three to four years | | | 657 | |

Four to five years | | | 1,328 | |

| | $ | 67,683 | |

Note 6 - Leases

The Company has committed to rent premises used in business operations under non-cancelable operating leases and determines if an arrangement meets the definition of a lease upon inception.

The Company adopted the provisions of ASU 2016-02 (Topic 842) on January 1, 2019. Operating lease right-of-use (“ROU”) assets represent a right to use an underlying asset for the contractual lease term. Operating lease liabilities represent an obligation to make lease payments arising from the lease. Operating lease ROU assets and operating lease liabilities were recognized in the Company’s Unaudited Consolidated Balance Sheets for leases that existed at the adoption date, based on the present value of lease payments over the remaining lease term. ROU assets were further adjusted for lease incentives. Operating leases entered into after the adoption date were recognized as an operating lease ROU asset and operating lease liability at the commencement date of the new lease.

The Company’s leases do not provide an implicit interest rate, therefore the Company used its incremental collateralized borrowing rates commensurate with the underlying lease terms to determine the present value of operating lease liabilities. There were no new leases during the period.

The Company’s operating lease agreements contain both lease and non-lease components, which are generally accounted for separately. The Company’s lease agreements do not contain any residual value guarantees.

Operating leases with terms of 12 months or less are not included in ROU assets and operating lease liabilities recorded in the Company’s consolidated balance sheets. Operating lease terms include options to extend when it is reasonably certain that the Company will exercise such options, determined on a lease-by-lease basis. As of June 30, 2020, the Company does 0t have any leases that have not yet commenced. At June 30, 2020, lease expiration dates ranged from two to 26 years, with additional renewal options on certain leases typically ranging from 5 to 10 years. At June 30, 2020, the weighted average remaining lease term for the Company’s operating leases was 10.6 years.

Rental expense for operating leases is recognized on a straight-line basis over the lease term and amounted to $334,000 and $348,000, respectively, for the three months ended June 30, 2020 and 2019 and $678,000 and $711,000, respectively for the six months ended June 30, 2020 and 2019. Variable lease components, such as inflation adjustments, are expensed as incurred and not included in ROU assets and operating lease liabilities.

20

The following table presents the minimum annual lease payments under the terms of these leases, inclusive of renewal options that the Company is reasonably certain to renew, at June 30, 2020:

| | June 30, | |

(dollars in thousands) | | 2020 | |

July 1, 2020 to December 31, 2020 | | $ | 634 | |

2021 | | | 1,254 | |

2022 | | | 1,258 | |

2023 | | | 1,269 | |

2024 | | | 864 | |

2025 and thereafter | | | 3,922 | |

Total lease payments | | | 9,201 | |

Less: amounts representing interest | | | 1,370 | |

Present value of lease liabilities | | $ | 7,831 | |

The following table presents the components of total lease expense and operating cash flows for the six months ended June 30, 2020:

| | June 30, | |

(dollars in thousands) | | 2020 | |

Lease expense: | | | | |

Operating lease expense | | $ | 662 | |

Variable lease expense | | | 72 | |

Total lease expense (1) | | $ | 734 | |

Cash paid: | | | | |

Cash paid reducing operating lease liabilities | | $ | 722 | |

| | | | |

(1) Included in net occupancy expense in the Condensed Consolidated Statements of Income (Unaudited). | | | | |

Note 7 - Stock-Based Compensation

Stock Options and Restricted Stock

On April 30, 2018, the Company’s shareholders approved the Coastal Financial Corporation 2018 Omnibus Incentive Plan (“2018 Plan”). The 2018 Plan authorizes the Company to grant awards, including but not limited to, stock options restricted stock units, and restricted stock awards, to eligible employees, directors or individuals that provide service to the Company, up to an aggregate of 500,000 shares of common stock. The 2018 Plan replaces both the Company’s 2006 Stock Option and Equity Compensation Plan (“2006 Plan”) and its Directors’ Stock Bonus Plan. Existing awards under the previous plans will vest under the terms granted and 0 further awards will be made under these plans. Shares available to be granted under the 2018 Plan totaled 281,225 at June 30, 2020.

Stock Option Awards

The fair value of each option award is estimated on the date of grant using the Black-Scholes option pricing model that uses the assumptions noted in the following table. Expected volatilities are based on historical volatility of the Company’s stock and other factors. The Company uses the vesting term and contractual life to determine the expected life. The risk-free interest rate for periods within the contractual life of the option is based on the U.S. Treasury yield curve in effect at the time of grant. Compensation expense related to unvested stock option awards is reversed at date of forfeiture.

21

The following assumptions were used to estimate the value of options granted under the 2018 Plan as applicable in the period indicated:

| | Six months ended June 30, 2019 | |

Expected term | | 10.0 years | |

Expected stock price volatility | | | 48.79 | % |

Risk-free interest rate | | | 2.74 | % |

Expected dividends | | NaN | |

Weighted average grant date fair value | | $ | 9.22 | |

A summary of stock option activity under the 2018 Plan and 2006 Plan during the three months ended June 30, 2020:

Options | | Shares | | | Weighted- Average Exercise Price | | | Weighted- Average Remaining Contractual Term (Years) | | | Aggregate Intrinsic Value | |

(dollars in thousands, except per share amounts) | | | | | | | | | | | | | | | | |

Outstanding at December 31, 2019 | | | 784,217 | | | $ | 7.73 | | | | 5.95 | | | $ | 6,587 | |

Granted | | | - | | | | - | | | | - | | | | | |

Exercised | | | (9,630 | ) | | | 5.82 | | | | - | | | | | |

Forfeited or expired | | | - | | | | - | | | | - | | | | | |

Outstanding at June 30, 2020 | | | 774,587 | | | $ | 7.75 | | | | 5.47 | | | $ | 5,305 | |

Vested or expected to vest at June 30, 2020 | | | 774,587 | | | $ | 7.75 | | | | 5.47 | | | $ | 5,305 | |

Exercisable at June 30, 2020 | | | 329,724 | | | $ | 6.41 | | | | 4.13 | | | $ | 2,681 | |

The total or aggregate intrinsic value (which is the amount by which the stock price exceeds the exercise price) of options exercised during the three and six months ended June 30, 2020 was $3,000 and $94,000, respectively, and was $66,000 and $135,000 for the three and six months ended June 30, 2019, respectively.

As of June 30, 2020, there was $2.1 million of total unrecognized compensation cost related to nonvested stock options granted under the 2018 Plan and 2006 Plan. Total unrecognized compensation costs are adjusted for unvested forfeitures. The Company expects to recognize that cost over a weighted-average period of approximately 7.0 years. Compensation expense recorded related to stock options was $92,000 and $187,000 for the three and six months ended June 30, 2020, respectively, and $101,000 and $198,000 for the three and six months ended June 30, 2019, respectively.

Restricted Stock Units

In February 2020, the Company granted 78,756 restricted stock units under the 2018 Plan to employees, which vest ratably over 10 years. In April 2020, the Company granted 1,490 restricted stock units under the 2018 Plan to an employee, which vest ratably over 10 years.