UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

_________________________________

FORM 10-Q

_________________________________

|

| |

þ

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended March 31, 2018

or

|

| |

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ___________ to ___________

Commission File Number: 001-36257

RETROPHIN, INC.

(Exact name of registrant as specified in its charter)

|

| | | | |

| | Delaware | | 27-4842691 | |

| | (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) | |

|

| | |

| | 3721 Valley Centre Drive, Suite 200, San Diego, CA 92130 | |

| | (Address of Principal Executive Offices) | |

|

| | |

| | (760) 260-8600 | |

| | (Registrant’s Telephone number including area code) | |

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

|

| | | |

| Large accelerated filer | þ

| Accelerated filer | ¨ |

| Non-accelerated filer | ¨ | Smaller reporting company | ¨ |

| | | Emerging growth company | ¨ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

The number of shares of outstanding common stock, par value $0.0001 per share, of the Registrant as of April 30, 2018 was 39,943,960.

RETROPHIN, INC.

Form 10-Q

For the Fiscal Quarter Ended March 31, 2018

TABLE OF CONTENTS

FORWARD LOOKING STATEMENTS

This report contains forward-looking statements regarding our business, financial condition, results of operations and prospects. Words such as “expects,” “anticipates,” “intends,” “plans,” “believes,” “seeks,” “estimates” and similar expressions or variations of such words are intended to identify forward-looking statements, but are not deemed to represent an all-inclusive means of identifying forward-looking statements as denoted in this report. Additionally, statements concerning future matters are forward-looking statements.

Although forward-looking statements in this report reflect the good faith judgment of our management, such statements can only be based on facts and factors currently known by us. Consequently, forward-looking statements are inherently subject to risks and uncertainties and actual results and outcomes may differ materially from the results and outcomes discussed in or anticipated by the forward-looking statements. Factors that could cause or contribute to such differences in results and outcomes include, without limitation, those specifically addressed under the headings “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in our annual report on Form 10-K for the fiscal year ended December 31, 2017 (the "2017 10-K"), and in this Form 10-Q and information contained in other reports that we file with the Securities and Exchange Commission (the “SEC”). You are urged not to place undue reliance on these forward-looking statements, which speak only as of the date of this report.

We file reports with the SEC. The SEC maintains a website (www.sec.gov) that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC, including us. You can also read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. You can obtain additional information about the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330.

We undertake no obligation to revise or update any forward-looking statements in order to reflect any event or circumstance that may arise after the date of this report, except as required by law. Readers are urged to carefully review and consider the various disclosures made throughout the entirety of this quarterly report, which are designed to advise interested parties of the risks and factors that may affect our business, financial condition, results of operations and prospects.

PART I - FINANCIAL INFORMATION

Item 1. Financial Statements

RETROPHIN, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

(in thousands, except share amounts)

|

| | | | | | | |

| | March 31, 2018 | | December 31, 2017 |

| Assets | (unaudited) | | |

|

| Current assets: | |

| | |

|

| Cash and cash equivalents | $ | 61,117 |

| | $ | 99,394 |

|

| Marketable securities | 202,939 |

| | 201,236 |

|

| Accounts receivable, net | 12,981 |

| | 13,872 |

|

| Inventory, net | 5,142 |

| | 5,351 |

|

| Prepaid expenses and other current assets | 2,011 |

| | 3,112 |

|

| Prepaid taxes | 2,613 |

| | 2,842 |

|

| Total current assets | 286,803 |

| | 325,807 |

|

| Property and equipment, net | 3,042 |

| | 3,230 |

|

| Other assets | 6,457 |

| | 5,556 |

|

| Investment-equity | 15,000 |

| | — |

|

| Intangible assets, net | 188,556 |

| | 184,817 |

|

| Goodwill | 936 |

| | 936 |

|

| Total assets | $ | 500,794 |

| | $ | 520,346 |

|

| Liabilities and Stockholders' Equity | |

| | |

|

| Current liabilities: | |

| | |

|

| Accounts payable | $ | 9,423 |

| | $ | 18,938 |

|

| Accrued expenses | 31,644 |

| | 36,018 |

|

| Guaranteed minimum royalty | 2,000 |

| | 2,000 |

|

| Other current liabilities | 3,958 |

| | 3,902 |

|

| Business combination-related contingent consideration | 9,500 |

| | 9,100 |

|

| Derivative financial instruments, warrants | — |

| | 15,710 |

|

| Total current liabilities | 56,525 |

| | 85,668 |

|

| Convertible debt | 45,238 |

| | 45,077 |

|

| Other non-current liabilities | 4,617 |

| | 2,472 |

|

| Guaranteed minimum royalty, less current portion | 12,939 |

| | 13,095 |

|

| Business combination-related contingent consideration, less current portion | 82,000 |

| | 80,900 |

|

| Total liabilities | 201,319 |

| | 227,212 |

|

| Stockholders' Equity: | |

| | |

|

| Preferred stock $0.001 par value; 20,000,000 shares authorized; 0 issued and outstanding as of March 31, 2018 and December 31, 2017 | — |

| | — |

|

| Common stock $0.0001 par value; 100,000,000 shares authorized; 39,873,285 and 39,373,745 issued and outstanding as of March 31, 2018 and December 31, 2017, respectively | 4 |

| | 4 |

|

| Additional paid-in capital | 486,717 |

| | 471,800 |

|

| Accumulated deficit | (185,717 | ) | | (177,655 | ) |

| Accumulated other comprehensive loss | (1,529 | ) | | (1,015 | ) |

| Total stockholders' equity | 299,475 |

| | 293,134 |

|

| Total liabilities and stockholders' equity | $ | 500,794 |

| | $ | 520,346 |

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

RETROPHIN, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE LOSS

(in thousands, except share and per share amounts)

(unaudited)

|

| | | | | | | |

| | Three Months Ended March 31, |

| | 2018 | | 2017 |

| Net product sales | $ | 38,432 |

| | $ | 33,620 |

|

| Operating expenses: | |

| | |

|

| Cost of goods sold | 1,613 |

| | 709 |

|

| Research and development | 24,636 |

| | 20,860 |

|

| Selling, general and administrative | 26,468 |

| | 23,115 |

|

| Change in fair value of contingent consideration | 3,627 |

| | 3,344 |

|

| Total operating expenses | 56,344 |

| | 48,028 |

|

| Operating loss | (17,912 | ) | | (14,408 | ) |

| Other income (expenses), net: | |

| | |

|

| Other income, net | 121 |

| | 126 |

|

| Interest expense, net | (358 | ) | | (132 | ) |

| Change in fair value of derivative instruments | — |

| | 1,260 |

|

| Total other income (expense), net | (237 | ) | | 1,254 |

|

| Loss before provision for income taxes | (18,149 | ) | | (13,154 | ) |

| Income tax benefit (expense) | (229 | ) | | 2,064 |

|

| Net loss | $ | (18,378 | ) | | $ | (11,090 | ) |

| | | | |

| Net loss per common share: |

|

|

|

|

|

| Basic | $ | (0.46 | ) |

| $ | (0.29 | ) |

| Diluted | $ | (0.46 | ) |

| $ | (0.32 | ) |

| Weighted average common shares outstanding: |

|

|

|

|

|

| Basic | 39,657,418 |

|

| 38,045,317 |

|

| Diluted | 39,657,418 |

|

| 39,158,922 |

|

| | | | |

| Comprehensive loss: | |

| | |

|

| Net loss | $ | (18,378 | ) | | $ | (11,090 | ) |

| Foreign currency translation | 22 |

| | (76 | ) |

| Unrealized gain (loss) on marketable securities | (536 | ) | | 146 |

|

| Comprehensive loss | $ | (18,892 | ) | | $ | (11,020 | ) |

The accompanying notes are an integral part of these condensed consolidated financial statements.

RETROPHIN, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(unaudited, in thousands) |

| | | | | | | |

| | For the Three Months Ended March 31, |

| | 2018 | | 2017 |

| Cash Flows From Operating Activities: | | | |

| Net loss | $ | (18,378 | ) | | $ | (11,090 | ) |

| Adjustments to reconcile net income to net cash provided by operating activities: | |

| | |

|

| Depreciation and amortization | 4,348 |

| | 4,284 |

|

| Deferred income tax benefit | — |

| | (2,064 | ) |

| Interest income from notes receivable | — |

| | (325 | ) |

| Non-cash interest expense | 413 |

| | 376 |

|

| Amortization of premiums on marketable securities | 356 |

| | 287 |

|

| Share based compensation | 4,659 |

| | 7,093 |

|

| Change in fair value of liability classified warrants | — |

| | (1,260 | ) |

| Change in fair value of contingent consideration | 3,627 |

| | 3,344 |

|

| Payments related to change in fair value of contingent consideration | (4,245 | ) | | (914 | ) |

| Inventory Reserve | 816 |

| | 25 |

|

| Other | 75 |

| | 53 |

|

| Changes in operating assets and liabilities, net of business acquisitions: | |

| | |

|

| Accounts receivable | 886 |

| | 3,076 |

|

| Inventory | (593 | ) | | (574 | ) |

| Other current and non-current operating assets | 421 |

| | (946 | ) |

| Accounts payable and accrued expenses | (9,330 | ) | | (4,626 | ) |

| Other current and non-current operating liabilities | 2,211 |

| | (146 | ) |

| Net cash used in operating activities | (14,734 | ) | | (3,407 | ) |

| Cash Flows From Investing Activities: | |

| | |

|

| Purchase of fixed assets | (39 | ) | | (838 | ) |

| Cash paid for intangible assets | (8,217 | ) | | (3,477 | ) |

| Proceeds from the sale/maturity of marketable securities | 26,924 |

| | 8,440 |

|

| Purchase of marketable securities | (29,519 | ) | | — |

|

| Cash paid for investments - equity | (10,000 | ) | | — |

|

| Net cash provided by (used in) investing activities | (20,851 | ) | | 4,125 |

|

| Cash Flows From Financing Activities: | |

| | |

|

| Payment of acquisition-related contingent consideration | (7,066 | ) | | (1,068 | ) |

| Payment of guaranteed minimum royalty | (500 | ) | | (500 | ) |

| Payment of other liability | — |

| | (250 | ) |

| Proceeds from exercise of warrants | 608 |

| | — |

|

| Proceeds from exercise of stock options | 4,256 |

| | 1,964 |

|

| Net cash provided by (used in) financing activities | (2,702 | ) | | 146 |

|

| Effect of exchange rate changes on cash | 10 |

| | 4 |

|

| Net change in cash | (38,277 | ) | | 868 |

|

| Cash, beginning of year | 99,394 |

| | 41,002 |

|

| Cash, end of period | $ | 61,117 |

| | $ | 41,870 |

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

RETROPHIN, INC. AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATMENTS

NOTE 1. DESCRIPTION OF BUSINESS

Organization and Description of Business

Retrophin, Inc. (“we”, “our”, “us”, “Retrophin” and the “Company”) refers to Retrophin, Inc., a Delaware corporation, as well as our direct and indirect subsidiaries. Retrophin is a fully integrated biopharmaceutical company headquartered in San Diego, California focused on the development, acquisition and commercialization of therapies for the treatment of rare diseases. We regularly evaluate and, where appropriate, act on opportunities to expand our product pipeline through licenses and acquisitions of products in areas that will serve patients with rare diseases and that we believe offer attractive growth characteristics.

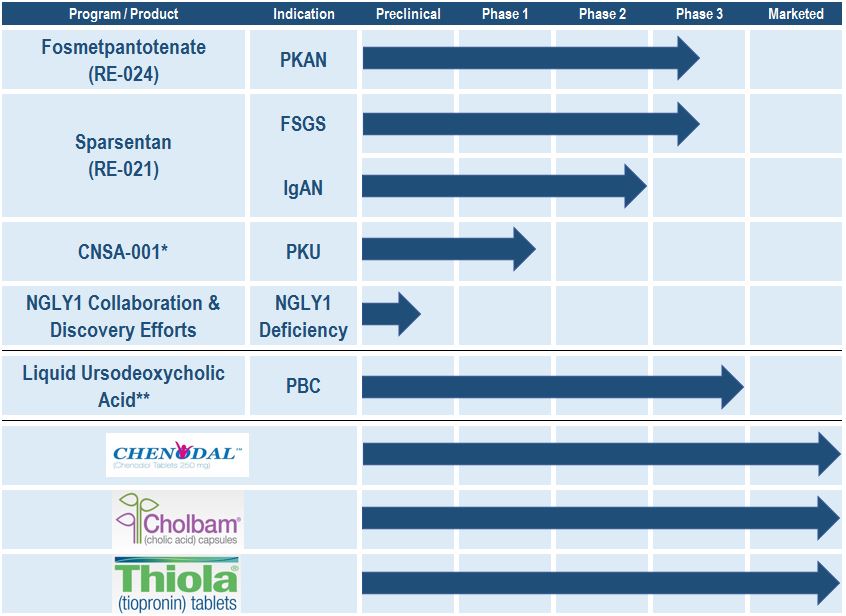

The Company is developing the following pipeline products:

The Company is developing fosmetpantotenate (RE-024), a novel small molecule, as a potential treatment for pantothenate kinase-associated neurodegeneration (“PKAN”). PKAN is a genetic neurodegenerative disorder that is typically diagnosed in the first decade of life. Consequences of PKAN include dystonia, dysarthria, rigidity, retinal degeneration, and severe digestive problems. There are currently no viable treatment options for patients with PKAN. Fosmetpantotenate is a phosphopantothenate replacement therapy that aims to restore levels of this key substrate in PKAN patients.

Sparsentan (RE-021) is an investigational product candidate which acts as both a potent angiotensin receptor blocker (“ARB”), as well as a selective endothelin receptor antagonist (“ERA”), with in vitro selectivity toward endothelin receptor type A. The Company secured a license to sparsentan from Ligand Pharmaceuticals, Inc. and Bristol-Myers Squibb Company (who referred to it as DARA). The Company is developing sparsentan as a treatment for:

| |

| ▪ | Focal segmental glomerulosclerosis ("FSGS"), which is a leading cause of end-stage renal disease and nephrotic syndrome (“NS”). There are no U.S. Food and Drug Administration ("FDA") approved pharmacologic treatments for FSGS and off-label resources are limited to ACE/ARBs, steroids, and immunosuppressant agents, which are effective in only a subset of patients. |

| |

| ▪ | Immunoglobulin A nephropathy ("IgAN"), which is characterized by hematuria, proteinuria, and variable rates of progressive renal failure. There is no FDA approved treatment for IgAN. |

The Company is a party to a joint development agreement with Censa Pharmaceuticals Inc. ("Censa"), a privately held biotechnology company focused on developing therapies for orphan metabolic diseases, to evaluate sepiapterin ("CNSA-001") for the treatment of phenylketonuria ("PKU"). CNSA-001 is an orally bioavailable form of a natural precursor of tetrahydrobiopterin ("BH4") with the potential to provide improved phenylalanine ("Phe") reduction in patients with PKU when compared to BH4.

PKU is a rare, genetic metabolic condition in which the body cannot breakdown Phe due to a missing or defective phenylalanine hydroxylase ("PAH") enzyme. High Phe levels can lead to developmental and physical growth delay, executive function impairment, seizures, and microcephaly caused by toxic Phe accumulation in the brain.

The Company is party to a three-way Cooperative Research and Development Agreement ("CRADA") with the National Institutes of Health’s National Center for Advancing Translational Sciences and patient advocacy foundation NGLY1.org to collaborate on research efforts aimed at the identification of potential small molecule therapeutics for N-glycanase deficiency ("NGLY1").

NGLY1 is an extremely rare genetic disorder believed to be caused by a deficiency in an enzyme called N-glycanase-1, which is encoded by the gene NGLY1. The condition has been characterized by symptoms such as developmental delays, seizures, complex hyperkinetic movement disorders, diminished reflexes and an inability to produce tears. There are no approved therapeutic options for NGLY1 deficiency, and current therapeutic strategies are limited to symptom management.

Liquid ursodeoxycholic acid ("L-UDCA") is a liquid formulation of ursodeoxycholic acid being developed for the treatment of a rare liver disease called primary biliary cholangitis ("PBC"). The Company obtained the rights to L-UDCA in 2016 with the intention of making L-UDCA commercially available to the subset of PBC patients who have difficulty swallowing.

The Company sells the following three products:

| |

| • | Chenodal® (chenodiol tablets) is approved in the United States for the treatment of patients suffering from gallstones in whom surgery poses an unacceptable health risk due to disease or advanced age. Chenodal has also been the standard of care for cerebrotendinous xanthomatosis ("CTX") patients for more than three decades and the Company is currently pursuing adding this indication to the label. |

| |

| • | Cholbam® (cholic acid capsules) is approved in the United States (approved and marketed in Europe for select indications as Kolbam) for the treatment of bile acid synthesis disorders due to single enzyme defects and is further indicated for adjunctive treatment of patients with peroxisomal disorders. |

| |

| • | Thiola® (tiopronin tablets) is approved in the United States for the prevention of cystine (kidney) stone formation in patients with severe homozygous cystinuria. |

NOTE 2. BASIS OF PRESENTATION AND SIGNIFICANT ACCOUNTING POLICIES

The accompanying unaudited condensed consolidated financial statements should be read in conjunction with the audited consolidated financial statements and notes thereto included in the 2017 10-K filed with the SEC on February 27, 2018. The accompanying condensed consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States (“GAAP”) for interim financial information, the instructions for Form 10-Q and the rules and regulations of the SEC. Accordingly, since they are interim statements, the accompanying condensed consolidated financial statements do not include all of the information and notes required by GAAP for annual financial statements, but reflect all adjustments consisting of normal, recurring adjustments, that are necessary for a fair presentation of the financial position, results of operations and cash flows for the interim periods presented. Interim results are not necessarily indicative of the results that may be expected for any future periods. The December 31, 2017 balance sheet information was derived from the audited financial statements as of that date. Certain reclassifications have been made to the prior period consolidated financial statements to conform to the current period presentation.

A summary of the significant accounting policies applied in the preparation of the accompanying condensed consolidated financial statements follows:

Principles of Consolidation

The unaudited condensed consolidated financial statements represent the consolidation of the accounts of the Company and its subsidiaries in conformity with GAAP. All intercompany accounts and transactions have been eliminated in consolidation.

Revenue Recognition

Effective January 1, 2018, the Company adopted Accounting Standards Codification (" ASC"), Topic 606, Revenue from Contracts with Customers, using the full retrospective transition method. This standard applies to all contracts with customers, except for contracts that are within the scope of other standards, such as leases, insurance, collaboration arrangements and financial instruments. Under Topic 606, an entity recognizes revenue when its customer obtains control of promised goods or services, in an amount that reflects the consideration which the entity expects to receive in exchange for those goods or services. To determine revenue recognition for arrangements that an entity determines are within the scope of Topic 606, the entity performs the following five steps: (i) identify the contract(s) with a customer; (ii) identify the performance obligations in the contract; (iii) determine the transaction price; (iv) allocate the transaction price to the performance obligations in the contract; and (v) recognize revenue when (or as) the entity satisfies a performance obligation. The Company only applies the five-step model to contracts when it is probable that the entity will collect the consideration it is entitled to in exchange for the goods or services it transfers to the customer. See Note 3 for further discussion.

Adoption of New Accounting Standards

In May 2014, the Financial Accounting Standard Board ("FASB") issued ASU No. 2014-09, Revenue from Contracts with Customers. Under the new standard, revenue is recognized at the time a good or service is transferred to a customer for the amount of consideration for which the entity expects to be entitled for that specific good or service. Entities may use a full retrospective approach or report the cumulative effect as of the date of adoption. The Company adopted the new standard on January 1, 2018 using the full retrospective approach and there was no impact on the timing or recognition of revenue because its only revenue source is product sales and because no variable consideration exists. The new standard also requires enhanced disclosures about the nature, amount, timing and uncertainty of revenue and cash flows arising from customer contracts. See Note 3 for further discussion.

In July 2017, the FASB issued ASU No. 2017-11, Earnings Per Share (Topic 260); Distinguishing Liabilities from Equity (Topic 480); Derivatives and Hedging (Topic 815): (Part I) Accounting for Certain Financial Instruments with Down Round Features. These amendments simplify the accounting for certain financial instruments with down round features. The amendments require companies to disregard the down round feature when assessing whether the instrument is indexed to its own stock, for purposes of determining liability or equity classification. See Note 6 for further discussion.

In January 2017, the FASB issued ASU 2017-01, Business Combinations (Topic 805): Clarifying the Definition of a Business. The new guidance dictates that, when substantially all of the fair value of the gross assets acquired (or disposed of) is concentrated in a single identifiable asset or a group of similar identifiable assets, it should be treated as an acquisition or disposal of an asset. The guidance was adopted as of January 1, 2018.

Recently Issued Accounting Pronouncements

From time to time, new accounting pronouncements are issued by the FASB or other standard setting bodies. Unless otherwise discussed, the Company believes that the impact of recently issued standards that are not yet effective will not have a material impact on its consolidated financial position or results of operations upon adoption.

In February 2016, the FASB issued ASU No. 2016-02, Leases. The new standard establishes a right-of-use ("ROU") model that requires a lessee to record a ROU asset and a lease liability on the balance sheet for all leases with terms longer than 12 months. Leases will be classified as either finance or operating, with classification affecting the pattern of expense recognition in the income statement. The new standard is effective for fiscal years beginning after December 15, 2018, including interim periods within those fiscal years. A modified retrospective transition approach is required for lessees for capital and operating leases existing at, or entered into after, the beginning of the earliest comparative period presented in the financial statements, with certain practical expedients available. The Company is in the process of evaluating the impact of this guidance on its consolidated financial statements and related disclosures; however, based on the Company's current operating leases, it is expected to have a material impact on the company's consolidated balance sheet by increasing assets and liabilities.

In June 2016, the FASB issued ASU No. 2016-13, Financial Instruments - Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments. Topic 326 amends guidance on reporting credit losses for assets held at amortized cost basis and available for sale debt securities. For assets held at amortized cost basis, Topic 326 eliminates the probable initial recognition threshold in current GAAP and, instead, requires an entity to reflect its current estimate of all expected credit losses. The allowance for credit losses is a valuation account that is deducted from the amortized cost basis of the financial assets to present the net amount expected to be collected. For available for sale debt securities, credit losses should be measured in a manner similar to current GAAP, however Topic 326 will require that credit losses be presented as an allowance rather than as a write-down. This ASU update affects entities holding financial assets and net investment in leases that are not accounted for at fair value through net income. The amendments affect loans, debt securities, trade receivables, net investments in leases, off balance sheet credit exposures, reinsurance receivables, and any other financial assets not excluded from the scope that have the contractual right to receive cash. This update is effective for fiscal years beginning after December 15, 2019, including interim periods within those fiscal years. As of March 31, 2018, the Company holds $202.9 million in available for sale debt securities that are affected by this ASU. If adopted as of March 31, 2018, this would not have a material impact on the company's financial statements.

In February 2018, the FASB issued ASU 2018-02, Reclassification of Certain Tax Effects from Accumulated Other Comprehensive Income. The new guidance addresses a specific consequence of the newly enacted federal income tax law (the "Tax Act"). This accounting update allows a reclassification from accumulated other comprehensive income to retained earnings for stranded tax effects resulting from the Tax Act. The amendments eliminate the stranded tax effects that were created as a result of the reduction of historical U.S. federal corporate income tax rates to the newly enacted U.S. federal corporate income tax rates. The accounting update is effective January 1, 2019, with early adoption permitted, and is to be applied either in the period of adoption or retrospectively to each period in which the effect of the change in the U.S. federal corporate income tax rate in the Tax Act is recognized. The Company is currently evaluating the potential effect of the guidance on its consolidated financial statements.

NOTE 3. REVENUE RECOGNITION

Product Revenue, Net

The Company sells Chenodal and Cholbam (Kolbam), which are aggregated as bile acid products, and Thiola through direct-to-patient distributors. The Company sells its products worldwide, with more than 95% of the revenue generated in North America.

Revenues from product sales are recognized when the customer obtains control of the Company’s product, which occurs upon delivery to the customer.

Deductions from Revenue

Revenues from product sales are recorded at the net sales price, which includes provisions resulting from discounts, rebates and co-pay assistance that is offered to its customers, health care providers, payors and other indirect customers relating to the Company’s sales of its products. These provisions are based on the amounts earned or to be claimed on the related sales and are classified as a reduction of accounts receivable (if the amount is payable to the customer) or as a current liability (if the amount is payable to a party other than a customer). Where appropriate, these reserves take into consideration the Company’s historical experience, current contractual and statutory requirements, specific known market events and trends, industry data and forecasted customer buying and payment patterns. Overall, these reserves reflect the Company’s best estimates of the amount of consideration to which it is entitled based on the terms of the contract. If actual results in the future vary from the Company’s provisions, the Company will adjust the provision, which would affect net product revenue and earnings in the period such variances become known. Our historical experience is that such adjustments have been immaterial.

Government Rebates: We calculate the rebates that we will be obligated to provide to government programs and deduct these estimated amounts from our gross product sales at the time the revenues are recognized. Allowances for government rebates and discounts are established based on actual payer information, which is reasonably estimated at the time of delivery, and the government-mandated discounts applicable to government-funded programs. Rebate discounts are included in other current liabilities in the accompanying consolidated balance sheets.

Commercial Rebates: We calculate the rebates that we incur due to contracts with certain commercial payors and deduct these amounts from our gross product sales at the time the revenues are recognized. Allowances for commercial rebates are established based on actual payer information, which is reasonably estimated at the time of delivery. Rebate discounts are included in other current liabilities in the accompanying consolidated balance sheets.

Prompt Pay Discounts: We offer discounts to certain customers for prompt payments. We accrue for the calculated prompt pay discount based on the gross amount of each invoice for those customers at the time of sale.

Product Returns: Consistent with industry practice, we offer our customers a limited right to return product purchased directly from the Company, which is principally based upon the product’s expiration date. Generally, shipments are only made upon a patient prescription thus returns are minimal.

Co-pay Assistance: We offer a co-pay assistance program, which is intended to provide financial assistance to qualified commercially insured patients with prescription drug co-payments required by payors. The calculation of the accrual for co-pay assistance is based on an identification of claims and the cost per claim associated with product that has been recognized as revenue.

The Company had the following net product revenues (in thousands):

|

| | | | | | | |

| | For the three months ended: |

| | March 31, 2018 | | March 31, 2017 |

| Bile acid products | $ | 18,508 |

| | $ | 15,736 |

|

| Thiola | 19,924 |

| | 17,884 |

|

| Total net product revenue | $ | 38,432 |

| | $ | 33,620 |

|

NOTE 4. MARKETABLE SECURITIES

The Company's marketable securities as of March 31, 2018 and December 31, 2017 were comprised of available-for-sale marketable securities which are carried at fair value, with the unrealized gains and losses reported in accumulated other comprehensive income. Realized gains and losses and declines in value judged to be other-than-temporary, if any, on available-for-sale securities are included in other income or expense. Interest and dividends on securities classified as available-for-sale are included in interest income. The amortized cost of debt securities is adjusted for amortization of premiums and accretion of discounts to maturity. Such amortization and accretion is included in interest income. During the three months ended March 31, 2018, investment activity for the Company included $26.9 million in maturities and $29.7 million in purchases, all relating to debt based marketable securities.

Marketable securities consisted of the following (in thousands): |

| | | | | | | |

| | March 31, 2018 | | December 31, 2017 |

| Marketable Securities: | | | |

| Commercial paper | $ | 10,339 |

| | $ | 6,897 |

|

| Corporate debt securities | 162,648 |

| | 164,297 |

|

| Securities of government sponsored entities | 29,952 |

| | 30,042 |

|

| Total marketable securities: | $ | 202,939 |

| | $ | 201,236 |

|

The following is a summary of short-term marketable securities classified as available-for-sale as of March 31, 2018 (in thousands): |

| | | | | | | | | | | | | | |

| | Remaining Contractual Maturity

(in years) | | Amortized Cost | | | Unrealized Losses | | Aggregate Estimated Fair Value |

| Marketable securities: | | | | | | | | |

| Commercial paper | Less than 1 | | $ | 10,384 |

| | | $ | (45 | ) | | $ | 10,339 |

|

| Corporate debt securities | Less than 1 | | 88,525 |

| | | (439 | ) | | 88,086 |

|

| Securities of government-sponsored entities | Less than 1 | | 30,019 |

| | | (67 | ) | | 29,952 |

|

| Total maturity less than 1 year | | | 128,928 |

| | | (551 | ) | | 128,377 |

|

| Corporate debt securities | 1 to 2 | | 75,276 |

| | | (714 | ) | | 74,562 |

|

| Total maturity 1 to 2 years | | | 75,276 |

| | | (714 | ) | | 74,562 |

|

| Total available-for-sale securities | | | $ | 204,204 |

| | | $ | (1,265 | ) | | $ | 202,939 |

|

The following is a summary of short-term marketable securities classified as available-for-sale as of December 31, 2017 (in thousands): |

| | | | | | | | | | | | | | |

| | Remaining Contractual Maturity (in years) | | Amortized Cost | | | Unrealized Losses | | Aggregate Estimated Fair Value |

| Marketable securities: | | | | | | | | |

| Commercial paper | Less than 1 | | $ | 6,911 |

| | | $ | (14 | ) | | $ | 6,897 |

|

| Corporate debt securities | Less than 1 | | 86,531 |

| | | (198 | ) | | 86,333 |

|

| Securities of government-sponsored entities | Less than 1 | | 30,132 |

| | | (90 | ) | | 30,042 |

|

| Total maturity less than 1 year | | | 123,574 |

| | | (302 | ) | | 123,272 |

|

| Corporate debt securities | 1 to 2 | | 78,388 |

| | | (424 | ) | | 77,964 |

|

| Total maturity 1 to 2 years | | | 78,388 |

| | | (424 | ) | | 77,964 |

|

| Total available-for-sale securities | | | $ | 201,962 |

| | | $ | (726 | ) | | $ | 201,236 |

|

The primary objective of the Company’s investment portfolio is to enhance overall returns while preserving capital and liquidity. The Company’s investment policy limits interest-bearing security investments to certain types of instruments issued by institutions with primarily investment grade credit ratings and places restrictions on maturities and concentration by asset class and issuer.

The Company reviews the available-for-sale investments for other-than-temporary declines in fair value below cost basis each quarter and whenever events or changes in circumstances indicate that the cost basis of an asset may not be recoverable. This evaluation is based on a number of factors, including the length of time and the extent to which the fair value has been below the cost basis and adverse conditions related specifically to the security, including any changes to the credit rating of the security, and the intent to sell, or whether the Company will more likely than not be required to sell the security before recovery of its amortized cost basis. The assessment of whether a security is other-than-temporarily impaired could change in the future due to new developments or changes in assumptions related to any particular security. As of March 31, 2018 and December 31, 2017, the Company believed the cost basis for available-for-sale investments was recoverable in all material respects.

NOTE 5. FUTURE ACQUISITION RIGHT AND JOINT DEVELOPMENT AGREEMENT

Censa Pharmaceuticals Inc.

In December 2017, the Company entered into a Future Acquisition Right and Joint Development Agreement (the “Option Agreement”) with Censa Pharmaceuticals Inc. (“Censa”), which became effective in January 2018. The Company has agreed to fund certain development activities of Censa’s CNSA-001 program, in an aggregate amount expected to be approximately $17 million through proof of concept, and has the right, but not the obligation, to acquire Censa (the “Option”) on the terms and subject to the conditions set forth in a separate Agreement and Plan of Merger. In exchange for the Option, the Company paid $10 million, and an additional $5 million upon Censa’s completion of a specified development milestone set forth in the Option Agreement.

If the Company exercises the Option, the Company will acquire Censa for $65 million in upfront consideration, subject to certain adjustments, paid as a combination of 20% in cash and 80% in shares of the Company’s common stock, valued at a fixed price of $21.40 per share; provided, however, that Censa may elect on behalf of its equity holders to receive the upfront consideration in 100% cash if the average price per share of the Company’s common stock for the ten trading days ending on the date the Company provides a notice of interest to exercise the Option is less than $19.26. In addition, if the Company exercises the Option and acquires Censa, the Company would be required to make further cash payments to Censa’s equity holders of up to an aggregate of $25 million if the CNSA-001 program achieves specified development and commercial milestones.

The Company determined that Censa is a variable interest entity ("VIE") and concluded that the Company is not the primary beneficiary of the VIE. As such, the Company did not consolidate Censa’s results into its consolidated financial statements. The Company will continue to monitor facts and circumstances for changes that could potentially result in the Company becoming the primary beneficiary.

As of March 31, 2018, the Company has paid $10.0 million as an upfront payment and $5.0 million in development funding to Censa. In addition, the Company accrued $5.0 million related to a development milestone payable to Censa within 45 days of achievement. The Company capitalized the upfront payment and accrued milestone, and expensed the development funding paid. The Company is treating the upfront payment and milestone, both of which are compensation for the purchase option, as a cost-method investment with a total carrying value of $15.0 million as March 31, 2018. The Company's maximum exposure to loss related to this VIE is limited to the carrying value of its investment.

NOTE 6. DERIVATIVE FINANCIAL INSTRUMENTS

Since 2013, the Company has issued five tranches of common stock purchase warrants to secure financing, remediate covenant violations and provide consideration for amendments with respect to a credit facility extinguished in 2015.

Historically, the Company accounted for these instruments, which do not have fixed settlement provisions, as derivative instruments in accordance with FASB ASC 815-40, Derivative and Hedging – Contracts in Entity’s Own Equity. This was due to an anti-dilution provision for the warrants that provides for a reduction to the exercise price if the Company issues equity or equity linked instruments in the future at an effective price per share less than the exercise price then in effect for the warrant ("down round provision"). As such, the warrants were re-measured at each balance sheet date based on estimated fair value. Changes in estimated fair value were recorded as non-cash adjustments within other income (expenses), net, in the Company’s accompanying Condensed Consolidated Statements of Operations and Comprehensive Loss. The Company recorded a gain on the change in the estimated fair value of warrants of $1.3 million for the three months ended March 31, 2017.

As of January 1, 2018 the Company early adopted ASU 2017-11, which revised the guidance for instruments with down round provisions. As such the Company treats outstanding warrants as free-standing equity linked instruments that will be recorded to equity in the Consolidated Balance Sheet.

In accordance with the guidance presented in the ASU, the fair value of the derivative liability balance as of December 31, 2017 of $15.7 million was reclassified by means of a cumulative-effect adjustment to equity as of January 1, 2018.

Impact of the adoption of ASU 2017-11 on equity (in thousands):

|

| | | | | | | | | | | | | | | |

| | Common stock | Additional paid in capital | Accumulated other comprehensive loss | Accumulated deficit | Total stockholders' equity (deficit) |

| Balance–December 31, 2017 | $ | 4 |

| $ | 471,800 |

| $ | (1,015 | ) | $ | (177,655 | ) | $ | 293,134 |

|

| Balance-March 31, 2018 before effect of ASU 17-11 | 4 |

| 481,323 |

| (1,529 | ) | (196,033 | ) | 283,765 |

|

| Effect of ASU 17-11 | — |

| 5,394 |

| | 10,316 |

| 15,710 |

|

| Balance–March 31, 2018 | $ | 4 |

| $ | 486,717 |

| $ | (1,529 | ) | $ | (185,717 | ) | $ | 299,475 |

|

The Company calculated the fair value of the warrants using the Black-Scholes Model as of December 31, 2017, using the following assumptions:

|

| | | |

| | December 31, 2017 |

| Fair value of common stock | $ | 21.07 |

|

| Remaining life of the warrants (in years) | 0.1 - 2.0 years |

|

| Risk-free interest rate* | 1.39 - 1.89% |

|

| Expected volatility** | 33 - 43% |

|

| Dividend yield | — | % |

*The risk-free interest rate is based on the U.S. Treasury security rates for the remaining term of the warrants at the measurement date.

**Expected volatility is based on an analysis of the Company’s historical volatility.

NOTE 7. FAIR VALUE MEASUREMENTS

Financial Instruments and Fair Value

The Company accounts for financial instruments in accordance with ASC 820, Fair Value Measurements and Disclosures (“ASC 820”). ASC 820 establishes a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value. The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements). The three levels of the fair value hierarchy under ASC 820 are described below:

Level 1 – Unadjusted quoted prices in active markets that are accessible at the measurement date for identical, unrestricted assets or liabilities;

Level 2 – Quoted prices in markets that are not active or financial instruments for which all significant inputs are observable, either directly or indirectly; and

Level 3 – Prices or valuations that require inputs that are both significant to the fair value measurement and unobservable.

The valuation techniques used to measure the fair value of the Company’s marketable securities and all other financial instruments, all of which have counter-parties with high credit ratings, were valued based on quoted market prices or model driven valuations using significant inputs derived from or corroborated by observable market data. Based on the fair value hierarchy, the Company classified marketable securities within Level 2.

In estimating the fair value of the Company’s derivative liabilities, the Company used the Black Scholes Model as of December 31, 2017. Based on the fair value hierarchy, the Company classified the derivative liability within Level 3. The Company adopted ASU 2017-11 as of January 1, 2018 and is no longer required to treat outstanding warrants as derivative liabilities measured at fair value. See Note 6 for further discussion.

In estimating the fair value of the Company’s contingent consideration, the Company used the probability-based expected method for royalty payments based on projected revenues. Based on the fair value hierarchy, the Company classified contingent consideration within Level 3 because valuation inputs are based on projected revenues discounted to a present value.

Financial instruments with carrying values approximating fair value include cash and cash equivalents, accounts receivable, and accounts payable, due to their short term nature. As of March 31, 2018, the estimated fair value of convertible debt was $63.4 million, considering factors such as market conditions, prepayment and make-whole provisions, variability in pricing from multiple lenders and the term of the debt.

The following table presents the Company’s assets and liabilities, measured and recognized at fair value on a recurring basis, classified under the appropriate level of the fair value hierarchy as of March 31, 2018 (in thousands): |

| | | | | | | | | | | | | | | |

| As of March 31, 2018 |

| Total carrying and estimated fair value | | Quoted prices in active markets

(Level 1) | | Significant other observable inputs (Level 2) | | Significant unobservable inputs (Level 3) |

| Assets: | | | | | | | |

| Cash and cash equivalents | $ | 61,117 |

| | $ | 61,117 |

| | $ | — |

| | $ | — |

|

| Marketable securities, available-for-sale | 202,939 |

| | — |

| | 202,939 |

| | — |

|

| Total | $ | 264,056 |

| | $ | 61,117 |

| | $ | 202,939 |

| | $ | — |

|

| Liabilities: | | | | | | | |

| Business combination-related contingent consideration | $ | 91,500 |

| | $ | — |

| | $ | — |

| | $ | 91,500 |

|

| Total | $ | 91,500 |

| | $ | — |

| | $ | — |

| | $ | 91,500 |

|

The following table presents the Company’s assets and liabilities, measured and recognized at fair value on a recurring basis, classified under the appropriate level of the fair value hierarchy as of December 31, 2017 (in thousands):

|

| | | | | | | | | | | | | | | |

| | As of December 31, 2017 |

| | Total carrying and estimated fair value | | Quoted prices in active markets (Level 1) | | Significant other observable inputs (Level 2) | | Significant unobservable inputs (Level 3) |

| Assets: | | | | | | | |

| Cash and cash equivalents | $ | 99,394 |

| | $ | 92,726 |

| | $ | 6,668 |

| | $ | — |

|

| Marketable securities, available-for-sale | 201,236 |

| | — |

| | 201,236 |

| | — |

|

| Total | $ | 300,630 |

| | $ | 92,726 |

| | $ | 207,904 |

| | $ | — |

|

| Liabilities: | | | | | | | |

| Derivative liability related to warrants | $ | 15,710 |

| | $ | — |

| | $ | — |

| | $ | 15,710 |

|

| Business combination-related contingent consideration | 90,000 |

| | — |

| | — |

| | 90,000 |

|

| Total | $ | 105,710 |

| | $ | — |

| | $ | — |

| | $ | 105,710 |

|

The following table sets forth a summary of changes in the estimated fair value of the Company's business combination-related contingent consideration for the three months ended March 31, 2018 (in thousands): |

| | | |

| | Fair Value Measurements of Acquisition-Related Contingent Consideration

(Level 3) |

| Balance at January 1, 2018 | $ | 90,000 |

|

| Increase from revaluation of contingent consideration | 3,627 |

|

| Contractual payments included in accrued liabilities at March 31, 2018 | (2,127 | ) |

| Contractual payments | — |

|

| Balance at March 31, 2018 | $ | 91,500 |

|

The fair value of contingent consideration liabilities was determined by applying a form of the income approach (a level 3 input), based upon the probability-weighted projected payment amounts discounted to present value at a rate appropriate for the risk of achieving the performance targets. The key assumptions included in the calculations were the earn-out period payment probabilities, projected revenues, discount rate and the timing of payments. The present value of the expected payments considers the time at which the obligations are expected to be settled and a discount rate that reflects the risk associated with the performance payments.

During the three months ended March 31, 2018, the Company incurred charges of $3.6 million in operating expenses on the Condensed Consolidated Statements of Operations and Comprehensive Loss for the revaluation of the contingent consideration liabilities. For the three months ended March 31, 2018, $0.8 million, $1.8 million, and $1.0 million of the charges were related to the increase in contingent consideration liabilities for the products Chenodal and Cholbam and product candidate L-UDCA, respectively. In each case, the value increased due to changes in the estimated timing of payments. During the three months ended March 31, 2017, the Company incurred charges of $3.3 million in operating expenses on the Condensed Consolidated Statement of Operations and Comprehensive Loss for the revaluation of the contingent consideration liabilities. For the three months ended March 31, 2017, $1.4 million, $1.1 million, and $0.8 million of the charges were related to the increase in contingent consideration liabilities for the products Chenodal and Cholbam and product candidate L-UDCA, respectively. In each case, the value increased due to changes in the estimated timing of payments.

NOTE 8. INTANGIBLE ASSETS

As of March 31, 2018, the net book value of amortizable intangible assets was approximately $188.6 million.

The following table sets forth amortizable intangible assets as of March 31, 2018 and December 31, 2017 (in thousands):

|

| | | | | | | |

| March 31, 2018 | | December 31, 2017 |

| Finite-lived intangible assets | $ | 243,865 |

| | $ | 235,863 |

|

| Less: accumulated amortization | (55,309 | ) | | (51,046 | ) |

| Net carrying value | $ | 188,556 |

| | $ | 184,817 |

|

The following table summarizes amortization expense for the three months ended March 31, 2018 and 2017 (in thousands):

|

| | | | | | | |

| Three Months Ended March 31, |

| 2018 | | 2017 |

| Research and development | $ | 103 |

| | $ | 81 |

|

| Selling, general and administrative | 4,096 |

| | 4,090 |

|

| Total amortization expense | $ | 4,199 |

| | $ | 4,171 |

|

During the three months ended March 31, 2018, the Company made a development payment to Ligand Pharmaceuticals for $4.6 million relating to sparsentan which was recorded as an increase to the Ligand license intangible asset.

NOTE 9. CONVERTIBLE NOTES PAYABLE

On May 29, 2014, the Company entered into a Note Purchase Agreement relating to a private placement by the Company of $46.0 million aggregate principal senior convertible notes due in 2019 (the “Notes”) which are convertible into shares of the Company’s common stock at an initial conversion price of $17.41 per share. The conversion price is subject to customary anti-dilution protection. The Notes bear interest at a rate of 4.5% per annum, payable semiannually in arrears on May 15 and November 15 of each year. The Notes mature on May 30, 2019 unless earlier converted or repurchased in accordance with their terms, and there are no contractual payments due prior to that date. At March 31, 2018 and December 31, 2017, the aggregate carrying value of the Notes was $45.2 million and $45.1 million, respectively.

NOTE 10. ACCRUED EXPENSES

Accrued expenses at March 31, 2018 and December 31, 2017 consisted of the following (in thousands):

|

| | | | | | | |

| | March 31, 2018 | | December 31, 2017 |

| Government rebates payable | $ | 6,372 |

| | $ | 5,883 |

|

| Compensation related costs | 5,693 |

| | 7,749 |

|

| Accrued royalties and contingent consideration | 5,870 |

| | 6,429 |

|

| Research and development | 9,553 |

| | 6,989 |

|

| Selling, general and administrative | 2,058 |

| | 3,896 |

|

| Restructuring expenses | 42 |

| | 3,549 |

|

| Miscellaneous accrued | 2,056 |

| | 1,523 |

|

| Total accrued expenses | $ | 31,644 |

| | $ | 36,018 |

|

NOTE 11. LOSS PER COMMON SHARE

Basic and diluted net loss per common share is calculated by dividing net loss applicable to common stockholders by the weighted-average number of common shares outstanding during the period, without consideration of common stock equivalents. The Company’s potentially dilutive shares, which include outstanding stock options, restricted stock units, warrants, and shares issuable upon conversion of the Notes, are considered to be common stock equivalents and are only included in the calculation of diluted net loss per share when their effect is dilutive.

Basic and diluted net loss per share is calculated as follows (net loss amounts are stated in thousands):

|

| | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended March 31, |

| | 2018 | | 2017 |

| | Shares | | Net Loss | | EPS | | Shares | | Net Loss | | EPS |

| Basic loss per share | 39,657,418 |

| | $ | (18,378 | ) | | $ | (0.46 | ) | | 38,045,317 |

| | $ | (11,090 | ) | | $ | (0.29 | ) |

| Dilutive shares related to warrants | — |

| | — |

| |

|

| | 1,113,605 |

| | — |

| |

|

|

| Change in fair value of derivative instruments | — |

| | — |

| |

|

| | — |

| | (1,260 | ) | |

|

|

| Dilutive loss per share | 39,657,418 |

| | $ | (18,378 | ) | | $ | (0.46 | ) | | 39,158,922 |

| | $ | (12,350 | ) | | $ | (0.32 | ) |

The following shares were excluded because they were anti-dilutive (in thousands):

|

| | | | | | |

| | Three Months Ended March 31, | |

| | 2018 | | 2017 | |

| Restricted stock units | 139 |

| | 332 |

| |

| Convertible debt | 2,642 |

| | 2,642 |

| |

| Options | 7,025 |

| | 6,405 |

| |

| Warrants | 633 |

| | — |

| |

| Total anti-dilutive shares | 10,439 |

| | 9,379 |

| |

NOTE 12. COMMITMENTS AND CONTINGENCIES

Leases and Sublease Agreements

|

| | | | | | |

| Facilities | | Annual Base Rent | | Lease Expiration | | Comments |

| Occupied Locations | | | | | | |

Corporate Headquarters San Diego, CA | | $2.1 million | | July 2024 | | |

| Vacated Locations | | | | | | |

| New York, NY | | $0.5 million | | November 2018 | | Sublet through expiration |

Research Collaboration and Licensing Agreements

As part of the Company's research and development efforts, the Company enters into research collaboration and licensing agreements with unrelated companies, scientific collaborators, universities, and consultants. These agreements contain varying terms and provisions which include fees and milestones to be paid by the Company, services to be provided, and ownership rights to certain proprietary technology developed under the agreements. Some of these agreements contain provisions which require the Company to pay royalties, in the event the Company sells or licenses any proprietary products developed under the respective agreements.

Legal Proceedings

In August 2017, Martin Shkreli, the Company’s former Chief Executive Officer, was convicted on securities fraud charges following investigations by the U.S. Attorney for the Eastern District of New York and the U.S Securities and Exchange Commission. The Company was not a target of these investigations and cooperated with them fully. In connection with these proceedings, Mr. Shkreli sought advancement of his legal fees from the Company. The Company disputed its obligation to pay these amounts in full, and in November 2016, the Company and Mr. Shkreli entered into a binding settlement arrangement under which the Company advanced $2.8 million in legal fees to Mr. Shkreli’s counsel. The Company also advanced an additional $2 million in legal fees once the matter proceeded to trial. In December 2017, the Company agreed to advance Mr. Shkreli $625,000 in full satisfaction of its obligation to advance fees to Mr. Shkreli in connection with his appeal of his conviction. The Company has been reimbursed by its directors’ and officers’ insurance carriers for $3.3 million of the legal fees the Company advanced in connection with the pre-trial and trial proceedings. Pending the outcome of Mr. Shkreli's appeal, the insurance carriers have reserved their rights to assert that certain of the advanced funds pertain to claims excluded from coverage under the relevant insurance policy and are therefore recoverable by the carriers. As a result, the

final amount of the reimbursement from the insurance carriers is not currently estimable. In addition, a portion of the legal fees the Company has advanced to Mr. Shkreli will be subject to reimbursement by Mr. Shkreli under Delaware law in the event it is ultimately determined that Mr. Shkreli is not entitled to be indemnified by the Company in these proceedings.

In August 2015, the Company filed a lawsuit in federal district court for the Southern District of New York against Mr. Shkreli, asserting that he breached his fiduciary duty of loyalty during his tenure as the Company’s Chief Executive Officer and a member of its Board of Directors. Mr. Shkreli served a demand for JAMS arbitration on Retrophin, claiming that Retrophin had breached his December 2013 employment agreement. In response to Mr. Shkreli’s arbitration demand, the Company asserted counterclaims in the arbitration that are substantially similar to the claims it previously asserted in the federal lawsuit against Mr. Shkreli. The federal Court granted a stay of the federal lawsuit pending a determination by the arbitration panel whether the Company’s counterclaims would be litigated in the arbitration, as the Company is seeking. In April 2016, the arbitration panel granted the parties’ request for a stay of the proceedings pending settlement discussions. In connection with these proceedings, Mr. Shkreli sought advancement of his legal fees from the Company relating to his defense of the Company’s claims against him. Pursuant to the November 2016 binding term sheet, the significant majority of the existing legal fees related to these proceedings that Mr. Shkreli claimed should be advanced were offset and satisfied by a $2.025 million judgment against Mr. Shkreli in a different case, and the Company paid $0.4 million in legal fees to Mr. Shkreli's counsel. The legal fees the Company has advanced will be subject to reimbursement by Mr. Shkreli under Delaware law in the event it is ultimately determined that Mr. Shkreli is not entitled to be indemnified by the Company in these proceedings. The Company will also be subject to additional obligations when the litigation resumes, as well as advancement obligations in the interim.

For the three months ended March 31, 2018 and 2017, the Company recorded no expenses under the settlement agreement. For the three months ended March 31, 2017, the Company paid $1.0 million under the settlement. No reimbursements from the Company's directors’ and officers’ insurance carriers were received during the three months ended March 31, 2018 and 2017. Of the $3.3 million reimbursed by the insurance carriers, $2.6 million is recorded as a liability on the Consolidated Balance Sheet pending the outcome of Mr. Shkreli's appeal.

From time to time the Company is involved in legal proceedings arising in the ordinary course of business. The Company believes there is no litigation pending that could have, individually or in the aggregate, a material adverse effect on its results of operations or financial condition.

NOTE 13. SHARE BASED COMPENSATION

Restricted Shares

Service and Performance Based Restricted Stock Units

The following table summarizes the Company’s restricted stock activity during the three months ended March 31, 2018:

|

| | | | | | |

| | Number of Restricted Stock Units | | Weighted Average Grant Date Fair Value |

| Unvested December 31, 2017 | 345,332 |

| | $ | 20.51 |

|

| Granted | 18,061 |

| | 22.18 |

|

| Vested | (11,377 | ) | | 18.33 |

|

| Forfeited/canceled | (12,666 | ) | | 22.84 |

|

| Unvested March 31, 2018 | 339,350 |

| | $ | 20.58 |

|

At March 31, 2018, unamortized stock compensation for restricted stock units was $2.1 million, with a weighted-average recognition period of 1.2 years.

Performance Based Restricted Stock Units

The Company did not grant any performance based restricted stock units during the three months ended March 31, 2018.

Stock Options

The following table summarizes stock option activity during the three months ended March 31, 2018:

|

| | | | | | | | | | | | |

| | Shares Underlying Options | | Weighted Average Exercise Price | | Weighted Average Remaining Contractual Life (years) | | Aggregate Intrinsic Value (in thousands) |

| Outstanding at December 31, 2017 | 7,153,668 |

| | $ | 17.16 |

| | 6.95 | | $ | 39,010 |

|

| Granted | 136,500 |

| | 24.08 |

| | | | |

| Exercised | (319,551 | ) | | 13.32 |

| | | | |

| Forfeited/canceled | (198,002 | ) | | 25.35 |

| | | | |

| Outstanding at March 31, 2018 | 6,772,615 |

| | $ | 17.25 |

| | 7.02 | | $ | 43,054 |

|

At March 31, 2018, unamortized stock compensation for stock options was $24.7 million, with a weighted-average recognition period of 2.6 years.

At March 31, 2018, outstanding options to purchase 4.5 million shares of common stock were exercisable with a weighted-average exercise price per share of $16.16.

Share Based Compensation

The following table sets forth total non-cash stock-based compensation for the three months ended March 31, 2018 and 2017 (in thousands):

|

| | | | | | | | |

| | Three Months Ended March 31, | |

| | 2018 | | 2017 | |

| Research and development | $ | 1,407 |

| | $ | 2,656 |

| |

| Selling, general & administrative | 3,202 |

| | 4,437 |

| |

| Total | $ | 4,609 |

| | $ | 7,093 |

| |

Exercise of Warrants

During the three months ended March 31, 2018, the Company issued 168,612 shares of common stock upon the exercise of outstanding warrants for cash received by the Company in the amount of $0.6 million. See Note 6 for changes in warrant accounting.

At March 31, 2018 and December 31, 2017, warrants to purchase 990,810 and 1,159,424 shares of common stock, respectively, were outstanding.

NOTE 14. INCOME TAXES

The following table summarizes our effective tax rate and income tax benefit (expense) for the three months ended March 31, 2018 and 2017 (dollars in millions):

|

| | | | | | | |

| | Three Months Ended March 31, |

| | 2018 | | 2017 |

| Effective tax rate | (1.3 | )% | | 15.7 | % |

| Income tax benefit (expense) | $ | (0.2 | ) | | $ | 2.1 |

|

For the three months ended March 31, 2018 and 2017, we recognized an income tax expense of $0.2 million and an income tax benefit of $2.1 million, respectively, representing an effective tax rate of (1.3)% and 15.7%, respectively. Under GAAP, quarterly effective tax rates may vary significantly depending on the actual operating results in the various tax jurisdictions, and significant transactions, as well as changes in the valuation allowance related to the expected recovery of deferred tax assets.

For the three months ended March 31, 2018, when compared to the same period in 2017, the change in the tax benefit and decrease in the effective income tax rate was primarily attributable to the increase of the U.S. federal valuation allowance in 2018.

At March 31, 2018, we had no unrecognized tax benefits. We did not recognize any interest or penalties related to unrecognized tax benefits during the three months ended March 31, 2018.

On December 22, 2017, the President of the United States signed into law the Tax Cuts and Jobs Act. The Tax Legislation reduces the US federal corporate tax rate from 35% to 21%, as well as making several other significant changes to the tax law, effective January 1, 2018. Pursuant to the Securities and Exchange Commission Staff Accounting Bulletin No. 118, Income Tax Accounting Implications of the Tax Cuts and Jobs Act (SAB 118), given the amount and complexity of the changes in tax law resulting from the Tax Legislation, the Company has not finalized the accounting for the income tax effects of the Tax Legislation. This includes the provisional amounts recorded related to the re-measurement of the deferred taxes and the change to our valuation allowance. The impact of the Tax Legislation may differ from this estimate during the one-year measurement period due to, among other things, further refinement of the Company's calculation, changes in interpretations and assumptions the Company has made, guidance that may be issued and actions the Company may take as a result of the Tax Legislation.

At March 31, 2018, the Company is still analyzing certain aspects of the Tax Legislation and refining its calculations, which could potentially affect the analysis of the Company’s deferred tax assets and liabilities and its valuation allowance. Any subsequent adjustment is not expected to be material to the Company’s financial position or results of operations.

NOTE 15. INVENTORY

Inventory, net of reserves, consisted of the following at March 31, 2018 and December 31, 2017 (in thousands):

|

| | | | | | | |

| | March 31, 2018 | | December 31, 2017 |

| Raw materials | $ | 3,743 |

| | $ | 3,435 |

|

| Finished goods | 1,399 |

| | 1,916 |

|

| Total inventory | $ | 5,142 |

| | $ | 5,351 |

|

The inventory reserve was $1.3 million and $0.7 million at March 31, 2018 and December 31, 2017, respectively.

NOTE 16. ACCOUNTS RECEIVABLES

Accounts receivable, net of reserves for prompt pay discounts and doubtful accounts, was $13.0 million and $13.9 million at March 31, 2018 and December 31, 2017, respectively. The total reserves for both periods were immaterial.

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion and analysis of our financial condition and results of operations should be read in conjunction with our unaudited condensed consolidated financial statements and related notes included in this Quarterly Report on Form 10-Q and the audited financial statements and notes thereto as of and for the year ended December 31, 2017 and the related Management’s Discussion and Analysis of Financial Condition and Results of Operations, both of which are contained in our Annual Report on Form 10-K for the year ended December 31, 2017, filed with the Securities and Exchange Commission (SEC) on February 27, 2018. Past operating results are not necessarily indicative of results that may occur in future periods.

Forward-Looking Statements

The information in this discussion contains forward-looking statements and information within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act, which are subject to the “safe harbor” created by those sections. These forward-looking statements include, but are not limited to, statements concerning our strategy, future operations, future financial position, future revenues, projected costs, prospects and plans and objectives of management. The words “anticipates,” “believes,” “estimates,” “expects,” “intends,” “may,” “plans,” “projects,” “will,” “would” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words. We may not actually achieve the plans, intentions or expectations disclosed in our forward-looking statements and you should not place undue reliance on our forward-looking statements. Actual results or events could differ materially from the plans, intentions and expectations disclosed in the forward-looking statements that we make. These forward-looking statements involve risks and uncertainties that could cause our actual results to differ materially from those in the forward-looking statements, including, without limitation, the risks set forth in Part II, Item IA, “Risk Factors” in this Quarterly Report on Form 10-Q and in our other filings with the SEC. The forward-looking statements are applicable only as of the date on which they are made, and we do not assume any obligation to update any forward-looking statements.

Overview

We are a biopharmaceutical company headquartered in San Diego, California, focused on identifying, developing and delivering life-changing therapies to people living with rare diseases.

Our Product Candidates and Products on the Market

**Acquired rights in 2016; activities underway with the intention of making the liquid formulation commercially available in the United States.

We are developing the following pipeline products:

Fosmetpantotenate

We are developing fosmetpantotenate, a novel small molecule, as a potential treatment for pantothenate kinase-associated neurodegeneration (“PKAN”). PKAN is a genetic neurodegenerative disorder that is typically diagnosed in the first decade of life. Consequences of PKAN include dystonia, dysarthria, rigidity, retinal degeneration, and severe digestive problems. PKAN is estimated to affect up to 5,000 patients worldwide. There are currently no viable treatment options for patients with PKAN. Fosmetpantotenate is a phosphopantothenate replacement therapy that aims to restore levels of this key substrate in PKAN patients. Certain international health regulators have approved the initiation of dosing fosmetpantotenate in PKAN patients under physician-initiated studies in accordance with local regulations in their respective countries.

In 2015 and 2016 we filed an IND, completed a Phase I clinical trial and obtained both orphan drug and fast track designations in the United States. Additionally, we received orphan drug designation in the European Union and reached an agreement with the U.S. Food and Drug administration ("FDA") under the Special Protocol Assessment (SPA) process for a Phase 3 clinical trial for PKAN. In July 2017, the first patient was dosed in our Phase 3 FORT (FOsmetpantotenate Replacement Therapy) study and enrollment continues.

Sparsentan

Sparsentan is an investigational product candidate which acts as both a potent angiotensin receptor blocker (“ARB”), as well as a selective endothelin receptor antagonist (“ERA”), with in vitro selectivity toward endothelin receptor type A. We have secured a license to sparsentan from Ligand Pharmaceuticals, Inc. and Bristol-Myers Squibb Company (who referred to it as DARA). We are developing sparsentan as a treatment for:

| |

| • | Focal segmental glomerulosclerosis ("FSGS"), a leading cause of end-stage renal disease and nephrotic syndrome (“NS”). There are currently no FDA approved pharmacologic treatments for FSGS and off-label resources are limited to ACE/ARBs, steroids, and immunosuppressant agents, which are effective in only a subset of patients. Every year approximately 5,400 patients are diagnosed with FSGS and we estimate that there are up to 40,000 FSGS patients in the United States with approximately half of them being candidates for sparsentan. In 2015 and 2016 we received orphan drug designation in the United States and European Union and received positive data from our Phase 2 DUET study of sparsentan for the treatment of FSGS. In April 2018, we announced the initiation of the Phase 3 DUPLEX Study of sparsentan in FSGS. This pivotal DUPLEX Study is designed to include an interim analysis of modified partial remission of proteinuria. We expect that successful achievement of this endpoint will serve as the basis for Subpart H accelerated approval of sparsentan in the United States and Conditional Marketing Authorization (CMA) consideration in Europe. The confirmatory endpoint of the study will compare changes in slope of estimated glomerular filtration rate, or eGFR. |

| |

| ▪ | Immunoglobulin A nephropathy ("IgAN"), which is characterized by hematuria, proteinuria, and variable rates of progressive renal failure. With an estimated prevalence of more than 100,000 in the United States and greater numbers in Europe and Asia, IgAN is the most common primary glomerular disease. Most patients are diagnosed between the ages of 16 and 35, with up to 40% progressing to end stage renal disease within 15 years. There are currently no FDA approved treatments for IgAN. The current standard of care is renin-angiotensin-aldosterone system (RAAS) blockade with immunosuppression also being commonly used for patients with significant proteinuria or rapidly progressive glomerulonephritis. Based on recent interactions we have had with the FDA and EMA, we are planning to initiate a single Phase 3 clinical trial designed to serve as the basis for an NDA filing for sparsentan for the treatment of IgAN. We are currently working to harmonize the protocol design for this Phase 3 study by incorporating the feedback to guide our clinical activity. We expect to initiate this study during the fourth quarter of 2018. |

CNSA-001

In December 2017, we entered into a Future Acquisition Right and Joint Development Agreement with Censa Pharmaceuticals, Inc. ("Censa"), which became effective on January 4, 2018 upon the satisfaction of certain conditions. Pursuant to the agreement, we agreed to fund certain development activities of Censa’s CNSA-001 program, in an aggregate amount expected to be approximately $17 million through proof of concept, and have the right, but not the obligation, to acquire Censa (the “Option”) on the terms and subject to the conditions set forth in a separate Agreement and Plan of Merger (the “Merger Agreement”). In exchange for the Option, on January 8, 2018, we paid Censa $10 million, and are required to pay Censa an additional $5 million upon Censa’s completion of a specified development milestone set forth in the Option Agreement, all of which will be distributed to Censa’s equityholders.

Censa, a privately held biotechnology company focused on developing therapies for the orphan metabolic diseases, is developing CNSA-001 for the treatment of phenylketonuria ("PKU"). CNSA-001 is an orally bioavailable form of a natural precursor of tetrahydrobiopterin ("BH4") with the potential to provide improved phenylalanine ("Phe") reduction in patients with PKU when compared to BH4. Preclinical research has suggested CNSA-001 may provide improved bioavailability, plasma stability and tissue exposure, leading to higher intracellular BH4 levels and subsequent greater Phe reduction when compared to the current standard of care in PKU. In pre-clinical models, CNSA-001 has also shown an ability to cross the blood-brain barrier which, if supported by clinical data, may lead to broader utility in additional indications such as primary BH4 deficiency (PBD) and Segawa syndrome. CNSA-001 is currently being evaluated in single and multiple ascending dose studies and a Phase 2 proof of concept study in PKU is expected to commence in mid-2018.

PKU is a rare, genetic metabolic condition in which the body cannot breakdown Phe due to a missing or defective phenylalanine hydroxylase ("PAH") enzyme. High Phe levels can lead to developmental and physical growth delay, executive function impairment, seizures, and microcephaly caused by toxic Phe accumulation in the brain. PKU is typically diagnosed at birth.