SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

(Mark One)

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2011

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

for the transition period from to

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

Commission file number 333-154474

GRIFOLS, S.A.

(Exact name of Registrant as specified in its charter)

Kingdom of Spain

(Jurisdiction of incorporation)

Avinguda de la Generalitat, 152-158

Parc de Negocis Can Sant Joan

Sant Cugat del Vallès 08174

Barcelona, Spain

(address of principal executive offices)

David Ian Bell

General Counsel

Grifols Inc.

2410 Lillyvale Ave

Los Angeles, CA 90032-3514

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered, pursuant to Section 12(b) of the Act.

| | |

Title of each class | | Name of each exchange

on which registered |

American Depositary Shares evidenced by American Depositary Receipts, each American Depositary Share representing one-half of one Class B non-voting share of Grifols, S.A. | | The NASDAQ Stock Market LLC |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

(Title of Class)

None.

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

(Title of Class)

None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

| | | | |

| Large accelerated filer ¨ | | Accelerated filer ¨ | | Non-accelerated filer x |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| | | | |

| US GAAP ¨ | | International Financial Reporting Standards as issued by the International Accounting Standards Board x | | Other ¨ |

If “Other” has been checked in response to the previous question indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ¨ Item 18 x

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

Indicate the number of outstanding shares of each of the issuer’s classes of capital stock or common stock as of the close of business covered by the annual report.

213,064,899 Class A Shares

113,499,346 Class B Shares

GRIFOLS, S.A.

TABLE OF CONTENTS

ii

iii

GENERAL INFORMATION

As used in this annual report on Form 20-F, unless the context otherwise requires or as is otherwise indicated:

| | • | | all references in this document to “Grifols,” the “Company,” “we,” “us” and “our” refer to Grifols, S.A., a company (sociedad anónima) organized under the laws of Spain, and our consolidated subsidiaries, and for all periods following the closing of the acquisition of Talecris Biotherapeutics Holdings Corp., on June 1, 2011, these terms include Talecris Biotherapeutics Holdings Corp.; |

| | • | | all references to the “Group” or the “Grifols Group” are to Grifols, S.A. and the group of companies owned or controlled by Grifols, S.A.; |

| | • | | all references to “Talecris” refer to Talecris Biotherapeutics Holdings Corp., a Delaware corporation, and its consolidated subsidiaries, as existing prior to the closing of the acquisition; and |

| | • | | all references to the “acquisition” refer to our acquisition of Talecris, consummated on June 1, 2011. |

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

The basis of presentation of financial information of Grifols in this document is in conformity with the International Financial Reporting Standards, or IFRS, as issued by the International Accounting Standards Board, or IASB, and other legislative provisions containing the applicable legislation governing our financial information, unless indicated otherwise.

Talecris has been included in our consolidated financial statements from June 2, 2011, the day following the consummation of the offering.

All references in this annual report on Form 20-F to (i) “euro,” “€” or “EUR” are to the common currency of the European Union and (ii) “U.S. dollar,” “$” or “USD” are to the currency of the United States, or U.S.

All tabular disclosures are presented in thousands of euro except share and per share amounts, percentages and as otherwise indicated. Certain monetary amounts and other figures included in this annual report on Form 20-F have been subject to rounding adjustments. Accordingly, any discrepancies in any tables between the totals and the sums of amounts listed are due to rounding.

PRESENTATION OF MARKET INFORMATION

Market information (including market share, market position and industry data for our operating activities and those of our subsidiaries or of companies acquired by us) or other statements presented in this annual report on Form 20-F regarding our position (or that of companies acquired by us) relative to our competitors largely reflect the best estimates of our management. These estimates are based upon information obtained from customers, trade or business organizations and associations, other contacts within the industries in which we operate and, in some cases, upon published statistical data or information from independent third parties. Except as otherwise stated, our market share data, as well as our management’s assessment of our comparative competitive position, has been derived by comparing our sales figures for the relevant period to our management’s estimates of our competitors’ sales figures for such period, as well as upon published statistical data and information from independent third parties, and, in particular, the reports published and the information made available by, among others, the Marketing Research Bureau, or MRB. You should not rely on the market share and other market information presented herein as precise measures of market share or of other actual conditions.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This annual report contains statements that constitute “forward-looking statements” within the meaning of the U.S. Private Securities Litigation Reform Act of 1995. Forward-looking statements are typically identified by words such as “may,” “anticipate,” “believe,” “estimate,” “predict,” “expect,” “intend,” “forecast,” “will,” “would,” “should” or the negative of such terms or other variations on such terms or comparable or similar words or expressions.

These forward-looking statements reflect, as applicable, our management’s current beliefs, assumptions and expectations and are subject to a number of factors that may cause actual results to differ materially. These factors include, but are not limited to:

| | • | | our significant indebtedness; |

| | • | | our ability to service our indebtedness, which in turn depends on our ability to generate cash; |

| | • | | the restrictive covenants governing our debt; |

| | • | | risks related to compliance with reporting obligations under U.S. securities laws and our internal control over financial reporting; |

| | • | | limitations on the enforcement of civil liabilities under U.S. securities laws; |

| | • | | the risks associated with the potential damage or contamination of plasma, our main raw material; |

| | • | | side effects associated with our products; |

| | • | | our adherence to current good manufacturing practice, or cGMP; |

| | • | | our ability to procure adequate quantities of plasma and other materials that are acceptable for use in our manufacturing processes; |

| | • | | fluctuations in the balance between supply and demand with respect to the market for plasma-derived products; |

| | • | | product concentration risk; |

| | • | | increased competition in our industry; |

| | • | | the impact of competitive products and the pricing and actions of competitors; |

| | • | | potential product liability claims or product recalls involving our products; |

| | • | | the impact of our substantial capital expenditures; |

| | • | | market risks, such as interest rate risk and foreign exchange rate risk; |

| | • | | the unprecedented volatility in the global economy and fluctuations in the financial markets; |

| | • | | unexpected shut-downs of our manufacturing and storage facilities or delays in opening new facilities; |

| | • | | disruptions in our distribution channels; |

| | • | | our ability to protect our intellectual property rights and defend against allegations of infringement by others; |

| | • | | our ability to resume or replace sales to countries affected by the ongoing Foreign Corrupt Practices Act, or FCPA, investigation; |

| | • | | potential sanctions, if any, that the Department of Justice, or DOJ, or other federal agencies, may impose on us as a result of the ongoing FCPA investigation; |

| | • | | our ability to commercialize products in development; |

| | • | | implementation of healthcare reform law in the U.S.; |

| | • | | potential decreases or limitations on reimbursement for purchasers of our products; |

| | • | | regulatory actions or lawsuits brought under federal or state laws; |

| | • | | extensive environmental, health and safety laws and regulations; |

| | • | | our ability to maintain compliance with government regulations and licenses, including those related to plasma collection, production, and marketing; and |

| | • | | other factors that are set forth below under Item 3 of this Part I, “Key Information — D. Risk Factors.” |

We include forward-looking statements in Item 4, Item 5 and Item 11 of this Part I, “Information on the Company,” “Operating and Financial Review and Prospects” and “Quantitative and Qualitative Disclosures About Market Risk,” respectively. Forward-looking statements are not guarantees of future performance and involve risks and uncertainties, including those listed above, and actual results may differ materially from those in the forward-looking statements.

The forward-looking statements contained in this annual report speak only as of the date of this annual report. Except as required by law, we do not undertake to update any forward-looking statement to reflect events or circumstances after that date or to reflect the occurrence of unanticipated events.

2

PART I

| Item 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

| | A. | Directors and Senior Management |

Not applicable.

Not applicable.

Not applicable.

| Item 2. | OFFER STATISTICS AND EXPECTED TIMETABLE |

Not applicable.

| | B. | Method and Expected Timetable |

Not applicable.

| | A. | Selected Financial Data |

Selected Consolidated Financial Information

The following is a summary of our historical consolidated financial data for the periods ended and at the dates indicated below. You are encouraged to read this information together with Item 5 of this Part I, “Operating and Financial Review and Prospects,” and our audited consolidated financial statements starting on page F-1 of this annual report on Form 20-F.

3

The following table presents our consolidated financial data for the periods and as of the dates indicated. Our consolidated balance sheet data as of December 31, 2011 and 2010 and our consolidated statement of operations data for the years ended December 31, 2011, 2010 and 2009 is derived from our audited consolidated financial statements for those years, which are included in this annual report on Form 20-F. Our consolidated balance sheet data as of December 31, 2009, 2008 and 2007 and our consolidated statement of operations data for the year ended December 31, 2008 and 2007 is derived from our consolidated financial statements for those years, which are not included in this Form 20-F.

| | | | | | | | | | | | | | | | | | | | |

| | | As of December 31, | |

Consolidated Balance Sheet Data | | 2011 | | | 2010 | | | 2009 | | | 2008 | | | 2007 | |

ASSETS | | | | | | | | | | | | | | | | | | | | |

Non-current assets | | | | | | | | | | | | | | | | | | | | |

Intangible assets | | | | | | | | | | | | | | | | | | | | |

Goodwill | | | 1,895,101 | | | | 189,448 | | | | 174,000 | | | | 158,567 | | | | 150,243 | |

Other intangible assets | | | 1,008,307 | | | | 78,299 | | | | 69,385 | | | | 57,756 | | | | 57,223 | |

| | | | | | | | | | | | | | | | | | | | |

Total intangible assets | | | 2,903,408 | | | | 267,747 | | | | 243,385 | | | | 216,323 | | | | 207,466 | |

Property, plant and equipment | | | 775,869 | | | | 434,131 | | | | 371,705 | | | | 301,009 | | | | 201,332 | |

Investments in equity accounted investees | | | 1,001 | | | | 598 | | | | 383 | | | | 374 | | | | 243 | |

Non-current financial assets | | | 12,401 | | | | 7,535 | | | | 3,731 | | | | 1,636 | | | | 891 | |

Deferred tax assets | | | 185,824 | | | | 34,889 | | | | 33,395 | | | | 34,297 | | | | 34,110 | |

| | | | | | | | | | | | | | | | | | | | |

Total non-current assets | | | 3,878,503 | | | | 744,900 | | | | 652,599 | | | | 553,639 | | | | 444,042 | |

| | | | | | | | | | | | | | | | | | | | |

Current assets | | | | | | | | | | | | | | | | | | | | |

Inventories | | | 1,030,341 | | | | 527,865 | | | | 484,462 | | | | 373,098 | | | | 270,659 | |

Trade and other receivables | | | | | | | | | | | | | | | | | | | | |

Trade receivables | | | 408,263 | | | | 224,355 | | | | 207,840 | | | | 186,324 | | | | 174,351 | |

Other receivables | | | 108,616 | | | | 44,032 | | | | 39,540 | | | | 43,443 | | | | 28,624 | |

Current income tax assets | | | 15,110 | | | | 14,607 | | | | 7,802 | | | | 5,428 | | | | 2,402 | |

| | | | | | | | | | | | | | | | | | | | |

Trade and other receivables | | | 531,989 | | | | 282,994 | | | | 255,182 | | | | 235,195 | | | | 205,377 | |

Other current financial assets | | | 16,904 | | | | 12,946 | | | | 8,217 | | | | 6,680 | | | | 7,600 | |

Other current assets | | | 9,395 | | | | 80,628 | | | | 7,345 | | | | 5,259 | | | | 6,201 | |

Cash and cash equivalents | | | 340,586 | | | | 239,649 | | | | 249,372 | | | | 6,368 | | | | 5,690 | |

| | | | | | | | | | | | | | | | | | | | |

Total current assets | | | 1,929,215 | | | | 1,144,082 | | | | 1,004,578 | | | | 626,600 | | | | 495,527 | |

| | | | | | | | | | | | | | | | | | | | |

Total Assets | | | 5,807,718 | | | | 1,888,982 | | | | 1,657,177 | | | | 1,180,239 | | | | 939,569 | |

| | | | | | | | | | | | | | | | | | | | |

EQUITY AND LIABILITIES | | | | | | | | | | | | | | | | | | | | |

Equity | | | | | | | | | | | | | | | | | | | | |

Share capital | | | 117,882 | | | | 106,532 | | | | 106,532 | | | | 106,532 | | | | 106,532 | |

Share Premium | | | 890,355 | | | | 121,802 | | | | 121,802 | | | | 121,802 | | | | 131,832 | |

Reserves | | | 568,274 | | | | 403,604 | | | | 314,903 | | | | 247,669 | | | | 184,608 | |

Own shares | | | (1,927 | ) | | | (1,927 | ) | | | (677 | ) | | | (33,087 | ) | | | (28,893 | ) |

Interim dividend | | | — | | | | — | | | | (31,960 | ) | | | — | | | | — | |

Profit for the year attributable to the Parent | | | 50,307 | | | | 115,513 | | | | 147,972 | | | | 121,728 | | | | 87,774 | |

| | | | | | | | | | | | | | | | | | | | |

Total equity | | | 1,624,891 | | | | 745,524 | | | | 658,572 | | | | 564,644 | | | | 481,853 | |

Available-for-sale financial assets | | | — | | | | — | | | | — | | | | (158 | ) | | | (152 | ) |

Cash flow hedges | | | (21,184 | ) | | | (1,751 | ) | | | (1,948 | ) | | | — | | | | — | |

Translation differences | | | 58,800 | | | | (50,733 | ) | | | (90,253 | ) | | | (84,457 | ) | | | (98,516 | ) |

| | | | | | | | | | | | | | | | | | | | |

Other comprehensive income | | | 37,616 | | | | (52,484 | ) | | | (92,201 | ) | | | (84,615 | ) | | | (98,668 | ) |

| | | | | | | | | | | | | | | | | | | | |

Equity attributable to the Parent | | | 1,662,507 | | | | 693,040 | | | | 566,371 | | | | 480,029 | | | | 383,185 | |

| | | | | | | | | | | | | | | | | | | | |

Minority interest | | | 2,487 | | | | 14,350 | | | | 12,157 | | | | 1,250 | | | | 981 | |

| | | | | | | | | | | | | | | | | | | | |

Total Equity (Net Assets) | | | 1,664,994 | | | | 707,390 | | | | 578,528 | | | | 481,279 | | | | 384,166 | |

| | | | | | | | | | | | | | | | | | | | |

Non-current liabilities | | | | | | | | | | | | | | | | | | | | |

Grants | | | 1,366 | | | | 2,088 | | | | 2,311 | | | | 2,353 | | | | 4,545 | |

Provisions | | | 11,502 | | | | 1,378 | | | | 1,232 | | | | 3,045 | | | | 999 | |

Non-current financial liabilities | | | | | | | | | | | | | | | | | | | | |

Loans and borrowings, bonds and other marketable securities | | | 2,809,225 | | | | 665,385 | | | | 703,186 | | | | 311,513 | | | | 178,425 | |

Other financial liabilities | | | 136,563 | | | | 10,474 | | | | 12,552 | | | | 12,542 | | | | 11,064 | |

| | | | | | | | | | | | | | | | | | | | |

Total non-current financial liabilities | | | 2,945,788 | | | | 675,859 | | | | 715,738 | | | | 324,055 | | | | 189,489 | |

Deferred tax liabilities | | | 538,441 | | | | 79,141 | | | | 60,325 | | | | 51,969 | | | | 43,794 | |

| | | | | | | | | | | | | | | | | | | | |

Total non-current liabilities | | | 3,496,647 | | | | 758,466 | | | | 779,606 | | | | 381,422 | | | | 238,827 | |

| | | | | | | | | | | | | | | | | | | | |

4

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Current liabilities | | | | | | | | | | | | | | | | | | | | |

Provisions | | | 81,112 | | | | 4,365 | | | | 4,702 | | | | 3,830 | | | | 3,957 | |

Current financial liabilities | | | | | | | | | | | | | | | | | | | | |

Loans and borrowings, bonds and other marketable securities | | | 147,789 | | | | 191,635 | | | | 113,991 | | | | 147,547 | | | | 177,540 | |

Other financial liabilities | | | 14,507 | | | | 18,236 | | | | 12,230 | | | | 9,685 | | | | 9,555 | |

| | | | | | | | | | | | | | | | | | | | |

Total current financial liabilities | | | 162,296 | | | | 209,871 | | | | 126,221 | | | | 157,232 | | | | 187,095 | |

Debts with associates | | | 2,435 | | | | 1,162 | | | | — | | | | — | | | | — | |

Trade and other payables | | | | | | | | | | | | | | | | | | | | |

Suppliers | | | 280,722 | | | | 160,678 | | | | 120,909 | | | | 107,613 | | | | 90,790 | |

Other payables | | | 27,335 | | | | 11,928 | | | | 17,832 | | | | 9,068 | | | | 11,396 | |

Current income tax liabilities | | | 4,691 | | | | 4,172 | | | | 3,258 | | | | 16,362 | | | | 3,770 | |

| | | | | | | | | | | | | | | | | | | | |

Total trade and other payables | | | 312,748 | | | | 176,778 | | | | 141,999 | | | | 133,043 | | | | 105,956 | |

Other current liabilities | | | 87,486 | | | | 30,950 | | | | 26,121 | | | | 23,433 | | | | 19,568 | |

| | | | | | | | | | | | | | | | | | | | |

Total current liabilities | | | 646,077 | | | | 423,126 | | | | 299,043 | | | | 317,538 | | | | 316,576 | |

| | | | | | | | | | | | | | | | | | | | |

Total Liabilities | | | 4,142,724 | | | | 1,181,592 | | | | 1,078,649 | | | | 698,960 | | | | 555,403 | |

| | | | | | | | | | | | | | | | | | | | |

Total Equity and Liabilities | | | 5,807,718 | | | | 1,888,982 | | | | 1,657,177 | | | | 1,180,239 | | | | 939,569 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| | | For the Year Ended December 31, | |

Consolidated Statement of Operations Data | | 2011 | | | 2010 | | | 2009 | | | 2008 | | | 2007 | |

Revenues | | | 1,795,613 | | | | 990,730 | | | | 913,186 | | | | 814,311 | | | | 703,291 | |

Changes in inventories of finished goods and work in progress | | | (35,150 | ) | | | 45,749 | | | | 73,093 | | | | 31,058 | | | | 16,882 | |

Self-constructed non-current assets | | | 34,548 | | | | 33,513 | | | | 41,142 | | | | 25,794 | | | | 19,860 | |

Supplies | | | (431,552 | ) | | | (304,818 | ) | | | (286,274 | ) | | | (206,738 | ) | | | (196,308 | ) |

Other operating income | | | 2,193 | | | | 1,196 | | | | 1,443 | | | | 1,289 | | | | 2,322 | |

Personnel expenses | | | (488,641 | ) | | | (289,008 | ) | | | (273,168 | ) | | | (238,159 | ) | | | (209,049 | ) |

Other operating expenses | | | (428,510 | ) | | | (205,260 | ) | | | (203,381 | ) | | | (192,288 | ) | | | (158,273 | ) |

Amortization and depreciation | | | (90,639 | ) | | | (45,776 | ) | | | (39,554 | ) | | | (33,256 | ) | | | (31,528 | ) |

Transaction costs of Talecris business combination | | | (44,352 | ) | | | (16,999 | ) | | | — | | | | — | | | | — | |

Non-financial and other capital grants | | | 1,304 | | | | 728 | | | | 1,188 | | | | 2,941 | | | | 282 | |

Impairment and gains/(losses) on disposal of fixed assets | | | (35,953 | ) | | | (372 | ) | | | (1,147 | ) | | | (1,991 | ) | | | (1,125 | ) |

| | | | | | | | | | | | | | | | | | | | |

Results from operating activities | | | 278,861 | | | | 209,683 | | | | 226,528 | | | | 202,961 | | | | 146,354 | |

| | | | | | | | | | | | | | | | | | | | |

Finance income | | | 5,761 | | | | 4,526 | | | | 7,067 | | | | 2,682 | | | | 4,526 | |

Finance expenses | | | (200,562 | ) | | | (49,660 | ) | | | (27,087 | ) | | | (29,305 | ) | | | (23,523 | ) |

Change in fair value of financial instruments | | | 1,279 | | | | (7,593 | ) | | | (587 | ) | | | (1,268 | ) | | | 829 | |

Impairment of gains/(losses) on disposal of financial instruments | | | (805 | ) | | | 91 | | | | (245 | ) | | | — | | | | — | |

Exchange losses | | | (3,477 | ) | | | 1,616 | | | | (1,733 | ) | | | (2,825 | ) | | | (4,618 | ) |

| | | | | | | | | | | | | | | | | | | | |

Finance income and expense | | | (197,774 | ) | | | (51,020 | ) | | | (22,585 | ) | | | (30,716 | ) | | | (22,786 | ) |

| | | | | | | | | | | | | | | | | | | | |

Share of profit of equity accounted investees | | | (1,064 | ) | | | (879 | ) | | | 51 | | | | 24 | | | | 19 | |

| | | | | | | | | | | | | | | | | | | | |

Profit before income tax from continuing operations | | | 80,023 | | | | 157,784 | | | | 203,994 | | | | 172,269 | | | | 123,587 | |

| | | | | | | | | | | | | | | | | | | | |

Income tax expense | | | (29,795 | ) | | | (42,517 | ) | | | (56,424 | ) | | | (50,153 | | | | (35,239 | ) |

| | | | | | | | | | | | | | | | | | | | |

Profit after income tax from continuing operations | | | 50,228 | | | | 115,267 | | | | 147,570 | | | | 122,116 | | | | 88,348 | |

| | | | | | | | | | | | | | | | | | | | |

Profit attributable to equity holders of the Parent | | | 50,037 | | | | 115,513 | | | | 147,972 | | | | 121,728 | | | | 87,774 | |

Profit attributable to minority interest | | | (79 | ) | | | (246 | ) | | | (402 | ) | | | 388 | | | | 574 | |

| | | | | | | | | | | | | | | | | | | | |

Consolidated profit for the year | | | 50,228 | | | | 115,267 | | | | 147,570 | | | | 122,116 | | | | 88,348 | |

| | | | | | | | | | | | | | | | | | | | |

Basic earnings per ordinary share | | | 0.19 | | | | 0.54 | | | | 0.71 | | | | 0.58 | | | | 0.41 | |

Average number of shares | | | | | | | | | | | | | | | | | | | | |

Basic earnings per ordinary share from continuing operations | | | | | | | | | | | | | | | | | | | | |

Diluted earnings per ordinary share | | | 0.19 | | | | 0.54 | | | | 0.71 | | | | 0.58 | | | | 0.41 | |

Diluted earnings per ordinary share from continuing operations | | | | | | | | | | | | | | | | | | | | |

Cash dividend per ordinary share | | | — | | | | 0.13 | | | | 0.38 | | | | 0.17 | | | | 0.06 | |

5

Exchange Rates

The following tables show, for the periods indicated, the exchange rate between the U.S. dollar and the euro. This information is provided solely for your information and we do not represent that euro could be converted into U.S. dollars at these rates or at any other rate, during the periods indicated or at any other time. These rates are not the rates used by us in the preparation of our audited consolidated financial statements included in this annual report on Form 20-F.

As used in this annual report on Form 20-F, the term “Noon Buying Rate” refers to the rate of exchange for euro, expressed in U.S. dollars per euro, in the City of New York for cable transfers payable in foreign currencies as certified by the Federal Reserve Bank of New York for customs purposes. The Noon Buying Rate for the euro on March 23, 2012 was $1.3263 = €1.00. The following tables describe, for the periods and dates indicated, information concerning the Noon Buying Rate for the euro. Amounts are expressed in U.S. dollars per €1.00.

| | | | | | | | | | | | | | | | |

Annual Data (Year Ended December 31,) | | Period

End ($) | | | Average

Rate ($) (1) | | | High ($) | | | Low ($) | |

2007 | | | 1.4603 | | | | 1.3797 | | | | 1.4862 | | | | 1.2904 | |

2008 | | | 1.3919 | | | | 1.4695 | | | | 1.6010 | | | | 1.2446 | |

2009 | | | 1.4332 | | | | 1.3955 | | | | 1.5100 | | | | 1.2547 | |

2010 | | | 1.3269 | | | | 1.3216 | | | | 1.4536 | | | | 1.1959 | |

2011 | | | 1.2926 | | | | 1.4002 | | | | 1.4875 | | | | 1.2926 | |

Source: Federal Reserve Bank of New York

| | (1) | The average of the Noon Buying Rates for the euro on the last day reported of each month during the relevant period. |

| | | | | | | | |

Recent Monthly Data | | High ($) | | | Low ($) | |

September 2011 | | | 1.4283 | | | | 1.3446 | |

October 2011 | | | 1.4172 | | | | 1.3281 | |

November 2011 | | | 1.3803 | | | | 1.3244 | |

December 2011 | | | 1.3487 | | | | 1.2926 | |

January 2012 | | | 1.3192 | | | | 1.2682 | |

February 2012 | | | 1.3463 | | | | 1.3087 | |

March 2012 (through March 23) | | | 1.3320 | | | | 1.3025 | |

| | B. | Capitalization and Indebtedness |

Not Applicable.

| | C. | Reasons for the Offer and Use of Proceeds |

Not Applicable.

Risk Relating to Our Structure, Shares and American Depositary Shares

Our substantial level of indebtedness could adversely affect our financial condition, restrict our ability to react to changes to our business, and prevent us from fulfilling our obligations under our debt.

We incurred substantial indebtedness in connection with the acquisition of Talecris. In order to finance the acquisition, (i) we entered into a credit and guaranty agreement dated as of November 23, 2010 (as amended by the first and second amendments thereto, the “Original Senior Credit Agreement”) to provide for (a) senior term loans aggregating $2.5 billion and €440 million (the “Original Senior Term Loans”) and (b) revolving commitments in the amounts of $50 million, €36.7 million ($50 million equivalent) and the $200 million equivalent in multicurrencies (the “Original Revolving Credit Facilities”) and (ii) we issued $1.1 billion aggregate principal amount of 8.25% senior notes due 2018 (“Notes”). As of December 31, 2011, our outstanding debt consisted primarily of $2.5 billion and €438.9 million outstanding under the Original Senior Term Loans and $1.1 billion aggregate principal amount of our Notes. In addition, as of December 31, 2011, we had €94.9 million of indebtedness under other bank loans and €31.7 in capital lease obligations.

On February 29, 2012, we entered into an amendment and restatement of the Original Credit Agreement (the “Amended and Restated Senior Credit Agreement”), which provided for the repricing of all of the Original Senior Term Loans and the Original

6

Revolving Facilities. The Amended and Restated Senior Credit Agreement provides for (i) senior term loans aggregating $2.3 billion and €420 million (the “Amended Senior Term Loans”), and (ii) revolving commitments in the amounts of $140 million, €22 million and the $35 million equivalent in multicurrencies (the “Amended Revolving Credit Facilities”). As of the date of this annual report of Form 20-F, the Amended Senior Term Loans were fully funded and no amounts have been drawn on the Amended Revolving Credit Facilities.

Our substantial level of indebtedness increases the risk that we may be unable to generate sufficient cash to pay amounts due in respect to our indebtedness. See Item 5 of this Part I, “Operating and Financial Review and Prospects — B. Liquidity and Capital Resources — Sources of Credit,” for the terms of the Amended and Restated Senior Credit Agreement and Notes and for more detailed information regarding our indebtedness.

Our high level of indebtedness could have significant adverse effects on our business, including the following:

| | • | | our high level of indebtedness makes it more difficult for us to satisfy our obligations with respect to our outstanding debt; |

| | • | | our high level of indebtedness makes us more vulnerable to economic downturns and adverse developments in our business; |

| | • | | our ability to obtain additional financing for working capital, capital expenditures, acquisitions or general corporate purposes may be impaired; |

| | • | | we must use a substantial portion of our cash flow from operations to pay interest on our indebtedness, which will reduce the funds available to us for operations and other purposes; |

| | • | | all of the indebtedness outstanding under our purchase money indebtedness, equipment financing and real estate mortgages will have a prior ranking claim on the underlying assets; |

| | • | | our ability to fund a change of control offer may be limited; |

| | • | | our high level of indebtedness could place us at a competitive disadvantage compared to our competitors that may have proportionately less debt; |

| | • | | our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate may be limited; and |

| | • | | we may be restricted from making strategic acquisitions or exploiting other business opportunities. |

We expect to use cash flow from operations to pay our expenses and amounts due under our outstanding indebtedness. Our ability to make these payments depends on our future performance, which will be affected by financial, business, economic and other factors, many of which we cannot control. Our business may not generate sufficient cash flow from operations in the future and our anticipated growth in revenue and cash flow may not be realized, either or both of which could result in our being unable to repay indebtedness or to fund other liquidity needs. If we do not have enough money, we may be required to refinance all or part of our then-existing debt, sell assets or borrow more money. We may not be able to accomplish any of these alternatives on terms acceptable to us or at all. In addition, the terms of existing or future debt agreements may restrict us from adopting any of these alternatives. The failure to generate sufficient cash flow to service our indebtedness or to achieve any of these alternatives could materially and adversely affect our business, results of operations and financial condition.

Despite our substantial indebtedness, we may still incur significantly more debt. This could exacerbate the risks associated with our substantial leverage.

We may be able to incur significant additional indebtedness in the future. Although the Amended and Restated Senior Credit Agreement and the indenture that governs our Notes contain restrictions on the incurrence of additional indebtedness, these restrictions are subject to a number of qualifications and exceptions and the additional indebtedness incurred in compliance with these exceptions could be substantial. As of the date of this annual report on Form 20-F, there is $140 million, €22 million and the $35 million equivalent in multicurrencies of undrawn availability under the Amended Revolving Credit Facilities. In addition, the Amended and Restated Senior Credit Agreement also provides for incremental facilities that include an increase to the existing Revolving Credit Facilities and the establishment of one or more new term loan commitments, by an amount not to exceed $600 million in the aggregate. If we incur additional indebtedness, the risks related to our business associated with our high level of debt could intensify. For more information regarding our indebtedness, see Item 5 of this Part I, “Operating and Financial Review and Prospects — B. Liquidity and Capital Resources — Sources of Credit.”

7

To service our indebtedness and other obligations, we will require a significant amount of cash. Our ability to generate cash depends on many factors beyond our control.

Our ability to make payments on or to refinance our indebtedness and to fund working capital needs and planned capital expenditures will depend on our ability to generate cash in the future. A significant reduction in our operating cash flows resulting from changes in economic conditions, increased competition or other events beyond our control could increase the need for additional or alternative sources of liquidity and could have a material adverse effect on our business, financial condition, results of operations and prospects and our ability to service our debt and other obligations. If we are unable to service our indebtedness, we will be forced to adopt an alternative strategy that may include actions such as reducing capital expenditures, selling assets, restructuring or refinancing our indebtedness or seeking additional equity capital. We cannot assure you that any of these alternative strategies could be effected on satisfactory terms, if at all, or that they would yield sufficient funds to make required payments on our indebtedness.

We cannot assure you that our business will generate sufficient cash flows from operations or that future borrowings will be available to us under the Senior Credit Facilities or otherwise in an amount sufficient to enable us to pay our indebtedness or to fund our other liquidity needs. We may need to refinance all or a portion of our indebtedness on or before the maturity of the debt. We cannot assure you that we will be able to refinance any of our indebtedness, including our Amended and Restated Senior Credit Agreement or our Notes, on commercially reasonable terms or at all.

Covenants in our debt agreements will restrict our business in many ways.

The agreements governing our indebtedness and other financial obligations applicable to us contain various covenants that limit our ability to, among other things:

| | • | | incur or assume liens or additional debt or provide guarantees in respect of obligations of other persons; |

| | • | | issue redeemable stock and preferred equity; |

| | • | | pay dividends or distributions or redeem or repurchase capital stock; |

| | • | | prepay, redeem or repurchase debt; |

| | • | | make loans, investments and capital expenditures; |

| | • | | enter into agreements that restrict distributions from our subsidiaries; |

| | • | | sell assets and capital stock of our subsidiaries; |

| | • | | enter into certain transactions with affiliates; and |

| | • | | consolidate or merge with or into, or sell substantially all of our assets to, another person. |

A breach of any of these covenants could result in a default. Upon the occurrence of an event of default under the Amended and Restated Senior Credit Agreement, the lenders could elect to declare all amounts outstanding under Amended and Restated Senior Credit Agreement to be immediately due and payable and terminate all commitments to extend further credit. If we were unable to repay those amounts, the lenders could proceed against the collateral granted to them to secure that indebtedness. We have pledged a significant portion of our assets as collateral under Amended and Restated Senior Credit Agreement. If the lenders under the Amended and Restated Senior Credit Agreement accelerate the repayment of borrowings, we may not have sufficient assets to repay the Amended and Restated Senior Credit Agreement and our other indebtedness, including our Notes. Our borrowings under the Amended and Restated Senior Credit Agreement are at variable rates of interest and expose us to interest rate risk. If interest rates increase, our debt service obligations on the variable rate indebtedness would increase even though the amount borrowed remained the same, and our net income would decrease. See Item 11 of this Part I, “Quantitative and Qualitative Disclosures About Market Risk — Interest Rate Risk.”

Our ability to meet our financial obligations depends on our ability to receive dividends and other distributions from our subsidiaries.

Our principal assets are the equity interests that we hold in our operating subsidiaries. As a result, we are dependent on dividends and other distributions from our subsidiaries to generate the funds necessary to meet our financial obligations, including the payment of principal and interest on our outstanding debt. Our subsidiaries may not generate sufficient cash from operations to enable us to make principal and interest payments on our indebtedness. In addition, any payment of dividends, distributions, loans or advances to us by our subsidiaries could be subject to restrictions on dividends or, in the case of foreign subsidiaries, restrictions on repatriation of earnings under applicable local law and monetary transfer restrictions in the jurisdictions in which our subsidiaries operate. In addition, payments to us by our subsidiaries will be contingent upon our subsidiaries’ earnings. Our subsidiaries are

8

permitted under the terms of our indebtedness to incur additional indebtedness that may restrict payments from those subsidiaries to us. We cannot assure you that agreements governing current and future indebtedness of our subsidiaries will permit those subsidiaries to provide us with sufficient cash to fund payments on our indebtedness when due.

Our subsidiaries are legally distinct from us and, except for existing and future subsidiaries that will be guarantors of certain indebtedness, have no obligation, contingent or otherwise, to pay amounts due on our debt or to make funds available to us for such payment.

We are a foreign private issuer under the rules and regulations of the Securities and Exchange Commission and, thus, are exempt from a number of rules under the Securities Exchange Act of 1934 and are permitted to file less information with the Securities and Exchange Commission than a company incorporated in the U.S.

As a foreign private issuer under the Securities Exchange Act of 1934, or Exchange Act, we are exempt from certain rules under the Exchange Act, including the proxy rules, which impose certain disclosure and procedural requirements for proxy solicitations. Moreover, we are not required to file periodic reports and financial statements with the Securities and Exchange Commission, or SEC, as frequently or as promptly as U.S. companies with securities registered under the Exchange Act; we are not required to file financial statements prepared in accordance with United States generally accepted accounting principles; and we are not required to comply with SEC Regulation FD, which imposes certain restrictions on the selective disclosure of material information. In addition, our officers, directors and principal shareholders are not subject to the reporting or short-swing profit recovery provisions of Section 16 of the Exchange Act or the rules under the Exchange Act with respect to their purchases and sales of our Class A shares or Class B shares. Accordingly, you may receive less information about us than you would receive about a company incorporated in the U.S. and may be afforded less protection under the U.S. federal securities laws than you would be afforded with respect to a company incorporated in the U.S. If we lose our status as a foreign private issuer at some future time, we will no longer be exempt from such rules and, among other things, will be required to file periodic reports and financial statements as if we were a company incorporated in the U.S. The costs incurred in fulfilling these additional regulatory requirements could be substantial.

Additionally, pursuant to The NASDAQ Stock Market LLC, or NASDAQ, Listing Rules, as a foreign private issuer, we may elect to follow our home country practice in lieu of the corporate governance requirements of the NASDAQ Listing Rule 5600 Series, with the exception of those rules which are required to be followed pursuant to the provisions of NASDAQ Listing Rule 5615(a)(3). We have elected to follow Spanish practices in lieu of the requirements of the NASDAQ Listing Rule 5600 Series to the extent permitted under NASDAQ Listing Rule 5615(a)(3). See Item 16.G. of Part II, “Corporate Governance.”

If we discover significant deficiencies in our internal control over financial reporting, it may adversely affect our ability to provide timely and reliable financial information and satisfy our reporting obligations under U.S. federal securities laws, which also could affect the market price of our American Depositary Shares or our ability to remain listed on NASDAQ.

Effective internal and disclosure controls are necessary for us to provide reliable financial reports and effectively prevent fraud and to operate successfully as a public company. If we cannot provide reliable financial reports or prevent fraud, our reputation and operating results would be harmed. A “significant deficiency” is a deficiency, or combination of deficiencies, in internal control over financial reporting that is less severe than a material weakness, yet important enough to merit attention of those responsible for oversight of our financial reporting.

To the extent that any material weakness or significant deficiency exists in our or our consolidated subsidiaries’ internal control over financial reporting, such material weakness or significant deficiency may adversely affect our ability to provide timely and reliable financial information necessary for the conduct of our business and satisfaction of our reporting obligations under U.S. federal securities laws, which could affect our ability to remain listed on NASDAQ. Ineffective internal and disclosure controls could cause investors to lose confidence in our reported financial information, which could have a negative effect on the trading price of our American Depositary Shares, or ADSs, or the rating of our debt.

The Grifols family may continue to exercise significant influence over the conduct of our business.

The Grifols family and Scranton Enterprises B.V. own, directly and indirectly, 35.3% of our Class A shares. The Class A shares exercise 100% of voting control of our company. As a result, the Grifols family and Scranton Enterprises B.V. may exercise significant influence over matters requiring shareholders’ approval including, among other things, the election of our board of directors, or Board, dividend policy and certain fundamental corporate action, such as the issuance of bonds, a merger or a dissolution. Conflicts may arise between the interests of the principal shareholders and those of the other shareholders, and the principal shareholders may choose to resolve the conflict in a way that does not coincide with the interests of the other shareholders.

9

The market price of our Class B ADSs on NASDAQ may be volatile.

The market price of our Class B ADSs may be volatile as a result of various factors, many of which are beyond our control. These factors include, but are not limited to, the following:

| | • | | market expectations for our financial performance; |

| | • | | actual or anticipated fluctuations in our results of operations and financial condition; |

| | • | | changes in the estimates of our results of operations by securities analysts; |

| | • | | potential or actual sales of blocks of our Class B ADSs in the market by any shareholder or short selling of our Class B ADSs. Any such transaction could occur at any time or from time to time, with our without notice; |

| | • | | the entrance of new competitors or new products in the markets in which we operate; |

| | • | | volatility in the market as a whole; and |

| | • | | the risk factors mentioned in this section. |

The market price of our Class B ADSs may be adversely affected by any of the preceding or other factors regardless of operations and financial condition.

Fluctuations in the exchange rate between the U.S. dollar and the euro may increase the risk of holding our ADSs or shares.

The Spanish securities market for equity securities consists of four stock exchanges located in Madrid, Barcelona, Bilbao and Valencia, or, collectively, the Spanish Stock Exchanges. The majority of the transactions conducted on the Spanish Stock Exchanges are done through the Automated Quotation System (Sistema Interbancario Bursátil Español, orS.I.B.E.).

Our Class A shares and Class B shares are listed on the Spanish Stock Exchanges and quoted on the Automated Quotation System in euro. In addition, our Class B shares are traded in the U.S. on the NASDAQ Global Select Market in the form of ADSs, evidenced by American Depositary Receipts, or ADRs, in U.S. dollars. Fluctuations in the exchange rate between the U.S. dollar and the euro may result in temporary differences between the value of our ADSs and the value of our shares, which may result in heavy trading by investors seeking to exploit such differences. This may increase the volatility of, and have an adverse effect on, the price of our shares or ADSs.

In addition, as a result of fluctuations in the exchange rate between the U.S. dollar and the euro, the U.S. dollar equivalent of the proceeds that a holder of our ADSs would receive upon the sale in Spain of any shares withdrawn from the ADR depositary and the U.S. dollar equivalent of any cash dividends paid in euro on our shares represented by the ADSs could also decline.

Subscription (or preemptive) rights may be unavailable to U.S. holders of our shares or ADSs.

In the case of a future increase of our registered share capital, existing shareholders will generally be entitled to subscription (or preemptive) rights pursuant to Spanish law, unless waived by a resolution of the shareholders or, if such power has been delegated to the Board pursuant to a shareholders’ resolution, by a resolution of the Board and except in certain situations, such as capital increases made for an in-kind contribution, in which subscription (or preemptive) rights are not applicable by law. Holders of the Class B shares will generally not have a right to vote on any resolution on a capital increase or on the waiver of subscription (or preemptive) rights, unless such resolution does not treat the Class B shares in the same way as the Class A shares, except in the limited circumstances set out in the Articles of Association of Grifols, S.A., or Articles of Association.

Even if preemptive rights are granted, holders of our ADSs or U.S. resident shareholders may not be able to exercise subscription (or preemptive) rights, in which case holders of our ADSs could be substantially diluted, unless a registration statement under the Securities Act of 1933, or Securities Act, is effective with respect to such rights and the shares for which they give such right or an exemption from the registration requirements of the Securities Act is available.

We intend to evaluate at the time of any rights offering the costs and potential liabilities associated with any such registration requirements, as well as the benefits of enabling the exercise of subscription (or preemptive) rights for the shares. In doing so, we will also evaluate any other factors that we may consider appropriate at the time. There can be no assurance that we will decide to comply with such registration requirements. If no such registration requirements are satisfied, the depositary will sell the subscription (or preemptive) rights relating to the ADSs on deposit and will distribute the proceeds of such sale, if any, to the holders of the ADSs. If the depositary is unable to sell rights that are not exercised or not distributed or if the sale is not lawful or reasonably practicable, it will allow the rights to lapse, in which case no value will be given for these rights.

10

ADS holders may be subject to limitations on the transfer of their ADSs.

ADSs are transferable on the books of the depositary. However, the depositary may refuse to deliver, transfer or register transfers of ADSs generally when the books of the depositary are closed or if such action is deemed necessary or advisable by the depositary or by us because of any requirement of law or of any government or governmental body or commission or under any provision of the deposit agreement. Moreover, the surrender of ADSs and withdrawal of our shares may be suspended subject to the payment of fees, taxes and similar charges or if we direct the depositary at any time to cease new issuances and withdrawals of our shares during periods specified by us in connection with shareholders’ meetings, the payment of dividends or as otherwise reasonably necessary for compliance with any applicable laws or government regulations.

Your ability to enforce civil liabilities under U.S. securities laws may be limited.

We are a company organized under the laws of Spain, and most of our subsidiaries are also incorporated outside of the U.S. A substantial portion of our assets and the assets of our subsidiaries are located outside of the U.S. In addition, nearly all of our directors and officers and certain of our subsidiaries’ officers are nationals or residents of countries other than the U.S., and all or a substantial portion of such persons’ assets are located outside the U.S. As a result, it may be difficult for investors to effect service of process within the U.S. upon us or certain subsidiaries or their directors or officers with respect to matters arising under the Securities Act or to enforce against them judgments of courts of the U.S. predicated upon civil liability under the Securities Act. It may also be difficult to recover fully in the U.S. on any judgment rendered against such persons or against us or certain of our subsidiaries.

In addition, there is doubt as to the enforceability in Spain of original actions, or of actions for enforcement of judgments of U.S. courts of liabilities, predicated solely upon the securities laws of the U.S. If a judgment was obtained outside Spain and efforts were made to enforce the judgment in Spain, there is some doubt that Spanish courts would agree to recognize and enforce a foreign judgment. Accordingly, even if you obtain a favorable judgment in a U.S. court, you may be required to re-litigate your claim in Spain.

Risks Relating to Our Business

Our manufacturing processes are complex and involve biological intermediates that are susceptible to contamination and variations in yield.

Plasma is a raw material that is susceptible to damage and contamination and may contain human pathogens, any of which would render the plasma unsuitable as raw material for further manufacturing. For instance, improper storage of plasma by us or third-party suppliers, if any, may require us to destroy some of our raw material. If unsuitable plasma is not identified and discarded prior to the release of the plasma to our manufacturing processes, it may be necessary to discard intermediate or finished product made from that plasma or to recall any finished product released to the market, resulting in a charge to cost of goods sold.

The manufacture of our plasma products is an extremely complex process of fractionation (separating the plasma into component proteins), purification, filling and finishing. Our products can become non-releasable or otherwise fail to meet our specifications through a failure of one or more of our product testing, manufacturing, process controls and quality assurance processes. We may detect instances in which an unreleased product was produced without adherence to our manufacturing procedures, or plasma used in our production process was not collected or stored in a compliant manner consistent with cGMP regulations or other regulations. Such an event of noncompliance would likely result in our determination that the impacted products should not be released and therefore should be destroyed. For example, a malfunction of the Gamunex® intravenous immunoglobulin, or IVIG, chromatography system just prior to Talecris’ formation transaction in 2005 resulted in the processing of IVIG products containing elevated levels of antibodies for over one month. Talecris’ total cost related to this incident, including the costs of product loss, investigation, testing, disposal, and other remedial actions, was approximately $41.6 million. Talecris subsequently recovered from Bayer HealthCare LLC, or Bayer, $10.7 million through its 2005 working capital adjustment and $9.0 million in the first quarter of 2007 through a settlement.

Once we have manufactured our plasma-derived products, they must be handled carefully and kept at appropriate temperatures. Our failure, or the failure of third parties that supply, ship or distribute our products, to properly care for our plasma-derived products may require that such products be destroyed.

While we expect to write off small amounts of work-in-process inventories in the ordinary course of business due to the complex nature of plasma, our processes and our products, unanticipated events may lead to write-offs and other costs materially in excess of our expectations. We have in the past had issues with product quality and purity that have caused us to write off the value of our product. Such write-offs and other costs could cause material fluctuations in our profitability. Furthermore, contamination of our products could cause investors, consumers or other third parties with whom we conduct business to lose confidence in the reliability

11

of our manufacturing procedures, which could adversely affect sales and profits. In addition, faulty or contaminated products that are unknowingly distributed could result in patient harm, threaten the reputation of our products and expose us to product liability damages and claims.

Additionally, due to the nature of plasma, there will be variations in the biologic properties of the plasma we collect or purchase for fractionation that may result in fluctuations in the obtainable yield of desired fractions, even if cGMP is followed. Lower yields may limit production of our plasma-derived products due to capacity constraints. If these batches of plasma with lower yields impact production for extended periods, it may reduce the total capacity of product that we could market and increase our cost of goods sold, thus reducing our profitability.

Once our products are approved and marketed, we must continually monitor them for signs that their use may elicit serious and unexpected side effects, which could jeopardize our ability to continue marketing our products. We may also be required to conduct post-approval clinical trials as a condition to licensing a product.

As for all pharmaceutical products, the use of our products sometimes produces undesirable side effects or adverse reactions or events, or, collectively, “adverse events.” For the most part, these adverse events are known, are expected to occur at some frequency and are described in the products’ labeling. Known adverse events of a number of our products include allergic or anaphylactic reactions including shock and the transmission of infective agents. Further, the use of certain products sometimes produces additional adverse events, which are detailed below.

| | • | | The use of albumin sometimes produces the following adverse events: hypervolaemia, circulatory overload, pulmonary edema, hyperhydration and allergic manifestations including urticaria, chills, fever and changes in respiration, pulse and blood pressure. |

| | • | | The use of blood clotting factor ix, or Factor IX, sometimes produces the following adverse events: the induction of neutralizing antibodies; thromboembolism, including myocardial infarction; disseminated intravascular coagulation; venous thrombosis and pulmonary embolism; and, in the case of treatment for immune tolerance induction, nephrotic syndrome. |

| | • | | The use of the anti-hemophilic blood clotting factor, or Factor VIII, sometimes produces the following adverse events: the induction of neutralizing antibodies, thromboembolic events and hemolytic anemia or hemolysis. |

| | • | | The use of IVIG sometimes produces the following adverse events: nausea, vomiting, asthenia, pyrexia, rigors, injection site reaction, allergic or anaphylactic reaction, aseptic meningitis, arthralgia, back pain, dizziness, headache, rash, pruritus, urticaria, hemolysis or hemolytic anemia, hyperproteinemia, increased serum viscosity and hyponatremia, thromboembolic reactions such as myocardial infarction, stroke, pulmonary embolism and deep vein thromboses, transfusion-related acute lung injury and renal dysfunction and acute renal failure. |

| | • | | The use of anti-hepatitis B IVIG sometimes produces the following adverse events: thromboembolic reactions such as myocardial infarction, stroke, pulmonary embolism and deep vein thromboses, aseptic meningitis, hemolytic anemia or hemolysis and acute renal failure. |

| | • | | The use of Plasbumin® 5%, 20% or 25% sometimes produces the following adverse events: allergic manifestations including urticaria, chills, fever and changes in respiration, pulse and blood pressure. |

| | • | | The use of Plasmanate® sometimes produces the following adverse events: hypotension, flushing, urticaria, back pain, nausea and headache. |

| | • | | The use of Koate®-DVI, which we license exclusively in the U.S. to Kedrion S.p.A, a corporation organized under the laws of Italy, or Kedrion, sometimes produces the following adverse events: allergic type reactions; tingling in the arm, ear and face; blurred vision; headache; nausea; stomach ache; and jittery feeling. |

| | • | | The use of Prolastin® or its successor in the U.S. and Canada, Prolastin®-C, alpha-1 proteinase inhibitor, or A1PI, sometimes produces the following adverse events: dyspnea, tachycardia, rash, chest pain, chills, influenza-like symptoms, hypersensitivity, hypotension and hypertension. |

In addition, the use of our products may be associated with serious and unexpected adverse events, or with less serious reactions at a greater than expected frequency. This may be especially true when our products are used in critically ill patient populations. When these unexpected events are reported to us, we must make a thorough investigation to determine causality and implications for product safety. These events must also be specifically reported to the applicable regulatory authorities. If our evaluation concludes, or regulatory authorities perceive, that there is an unreasonable risk associated with the product, we would be obligated to withdraw the impacted lot(s) of that product. Furthermore, an unexpected adverse event caused by a new product could be recognized only after extensive use of the product, which could expose us to product liability risks, enforcement action by regulatory authorities and damage to our reputation and public image.

12

Once we produce a product, we rely on physicians to prescribe and administer it as we have directed and for the indications described on the labeling. It is not, however, unusual for physicians to prescribe our products for unapproved, or off-label, uses or in a manner that is inconsistent with our directions. To the extent such off-label uses and departures from our administration directions become pervasive and produce results such as reduced efficacy or other adverse effects, the reputation of our products in the marketplace may suffer.

When a new product is approved, the Food and Drug Administration, or FDA, or other regulatory authorities may require post-approval clinical trials, sometimes called Phase IV clinical trials. If the results of such trials are unfavorable, this could result in the loss of the license to market the product, with a resulting loss of sales.

Our ability to continue manufacturing and distributing our products depends on our and our suppliers’ continued adherence to cGMP regulations.

The manufacturing processes for our products are governed by detailed written procedures and federal regulations that set forth cGMP requirements for blood and blood products. Our quality operations unit monitors compliance with these procedures and regulations, and the conformance of materials, manufacturing intermediates and final products to their specifications. Failure to adhere to established procedures or regulations, or to meet a specification, could require that a product or material be rejected and destroyed. There are relatively few opportunities for us to rework, reprocess or salvage nonconforming materials or products.

Our adherence to cGMP regulations and the effectiveness of our quality systems are periodically assessed through inspections of our facilities by the FDA and analogous regulatory authorities of other countries. We cannot assure you that we will not be cited for deficiencies in the future. If deficiencies are noted during an inspection, we must take action to correct those deficiencies and to demonstrate to the regulatory authorities that our corrections have been effective. If serious deficiencies are noted or if we are unable to prevent recurrences, we may have to recall product or suspend operations until appropriate measures can be implemented. We are required to report some deviations from procedures to the FDA. Even if we determine that the deviations were not material, the FDA could require us to take similar measures. Since cGMP reflects ever-evolving standards, we regularly need to update our manufacturing processes and procedures to comply with cGMP. These changes may cause us to incur costs without improving our profitability or the safety of our products. For example, more sensitive testing assays (if and when they become available) may be required or existing procedures or processes may require revalidation, all of which may be costly and time-consuming and could delay or prevent the manufacturing of a product or launch of a new product.

Changes in manufacturing processes, including a change in the location where the product is manufactured or a change of a third-party manufacturer, may require prior FDA review and approval or revalidation of the manufacturing processes and procedures in accordance with cGMP. There may be comparable foreign requirements.

For example, we have finished the construction of a new plant at our facility located in Los Angeles, California, or our Los Angeles facility, for the production of IVIG and we have begun the validation process with the appropriate regulatory authorities. To validate our manufacturing processes and procedures following completion of upgraded facilities, we must demonstrate that the processes and procedures at the upgraded facilities are comparable to those currently in place at our facilities. To provide such a comparative analysis, both the existing processes and the processes that we expect to be implemented at our upgraded facilities must comply with the regulatory standards prevailing at the time that our expected upgrade is completed. In addition, regulatory requirements, including cGMP regulations, continually evolve. Failure to adjust our operations to conform to new standards as established and interpreted by applicable regulatory authorities would create a compliance risk that could impair our ability to sustain normal operations.

In addition, we have completed the process of transferring the manufacture of our Thrombate III® product from Bayer’s Berkeley, California, biologics manufacturing facility to our Clayton, North Carolina plasma fractionation and manufacturing facility, or Clayton facility, that we are currently validating with regulatory approval expected in 2012. We cannot guarantee that we have a sufficient inventory of intermediates and finished product to meet demand until the new facility is approved and manufacturing can recommence. To validate our manufacturing processes and procedures following completion of the upgraded facilities, we must demonstrate that the processes and procedures at the upgraded facilities are comparable to those currently in place at Bayer’s facilities. In order to provide such a comparative analysis, both the existing processes and the processes that we expect to be implemented at our upgraded facilities must comply with the regulatory standards prevailing at the time that our expected upgrade is completed. If the FDA does not approve the transfer, our ability to market our Thrombate III® product will be seriously impaired or eliminated. In addition, regulatory requirements, including cGMP regulations, continually evolve. Failure to adjust our operations to conform to new standards as established and interpreted by applicable regulatory authorities would create a compliance risk that could impair our ability to sustain normal operations.

A number of inspections by the FDA and foreign control authorities, including the European Medicines Agency, or EMA, have been conducted or are expected at our plasma collection centers in 2012. Some of these inspections are of licensed centers to

13

assess ongoing compliance with cGMP. If the FDA (or other authorities) finds these centers not to be in compliance, our ongoing operations or plans to expand plasma collections would be adversely affected.

We would become supply-constrained and our financial performance would suffer if we could not obtain adequate quantities of FDA-approved source plasma.

In order for plasma to be used in the manufacturing of our products, the individual centers at which the plasma is collected must be licensed by the FDA and approved by the regulatory authorities, such as the EMA, of those countries in which we sell our products. When a new plasma collection center is opened and on an ongoing basis after its licensure, it must be inspected by the FDA and the EMA for compliance with cGMP and other regulatory requirements. An unsatisfactory inspection could prevent a new center from being licensed or risk the suspension or revocation of an existing license.

In order for a plasma collection center to maintain its license, its operations must continue to conform to cGMP and other regulatory requirements. In the event that we determine a plasma collection center did not comply with cGMP in collecting plasma, we may be unable to use and may ultimately destroy plasma collected from that center, which would be recorded as a charge to cost of goods. Additionally, if noncompliance in the plasma collection process is identified after the impacted plasma has been pooled with compliant plasma from other sources, entire plasma pools, in-process intermediate materials and final products could be impacted. Consequently, we could experience significant inventory impairment provisions and write-offs which could adversely affect our business and financial results. During 2008, Talecris experienced such an event at one of their plasma collection centers, which resulted in a charge to cost of goods sold of $23.3 million, for which they subsequently recovered $19.4 million through December 31, 2010. In this particular instance, a portion of the impacted plasma had been released to manufacturing prior to Talecris’ detection of the issue.

We plan to obtain our supplies of plasma for use in our manufacturing processes through collections at our plasma collection centers and through selective acquisitions or remodeling and relocations of existing centers. This strategy is dependent upon our ability to successfully integrate new centers, to obtain FDA and other necessary approvals for the remaining unlicensed centers, to maintain a cGMP compliant environment in all centers, and to expand production and attract donors to our centers.

Our ability to increase and improve the efficiency of production at our plasma collection centers may be affected by changes in the economic environment and population in selected regions where we operate plasma collection centers, by the entry of competitive centers into regions where we operate, by misjudging the demographic potential of individual regions where we expect to increase production and attract new donors, by unexpected facility related challenges, or by unexpected management challenges at selected plasma collection centers.

A significant disruption in our supply of plasma could have a material adverse effect on our business and our growth plans.

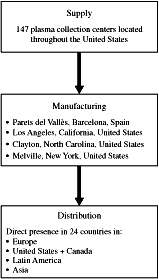

The majority of our revenue depends on our access to U.S. source plasma (plasma obtained through plasmapheresis), the principal raw material for our plasma derivative products. Our ability to increase revenues depends substantially on increased access to plasma. We expect that our plasma needs through 2015 will be met through the volumes of collection at our 147 plasma collection centers in the U.S. and supplemented by approximately 800,000 liters of plasma per year to be purchased from third-party suppliers pursuant to multiple plasma purchase agreements. If we are unable to obtain sufficient quantities of source plasma, we may be unable to find an alternative cost-effective source of plasma.

If we are unable to obtain sufficient quantities of source plasma, we would be limited in our ability to maintain current manufacturing levels of plasma derivative products. As a result, we could experience a substantial decrease in net sales or profit margins, a loss of customers, a negative effect on our reputation as a reliable supplier of plasma derivative products or a substantial delay in our production growth plans.

Our current business plan envisages an increase in the production of plasma derivative products, which depends on our ability to increase plasma collections or improve product yield. The ability to increase plasma collections may be limited, our supply of plasma could be disrupted or the cost of plasma could increase substantially, as a result of numerous factors, including:

| | • | | A reduction in the donor pool. Regulators in most of the largest markets for plasma derivative products, including the U.S., restrict the use of plasma collected from specific countries and regions in the manufacture of plasma derivative products. For example, the appearance of the variant Creutzfeldt-Jakob, or mad cow, disease, which resulted in the suspension of the use of plasma collected from U.K. residents and concern over the safety of blood products, which has led to increased domestic and foreign regulatory control over the collection and testing of plasma and the disqualification of certain segments of the population from the donor pool, have significantly reduced the potential donor pool. The appearance of new viral strains could further reduce the potential donor pool. Also, improvements in socioeconomic conditions in the areas |

14

| | where our and our suppliers’ collection centers are located could reduce the attractiveness of financial incentives for donors, resulting in increased donor fees or a reduction in the number of donors. |

| | • | | Regulatory requirements. The collection of plasma is heavily regulated, and our ability to collect plasma (or to increase plasma collection) through our collection centers, or to obtain plasma from other suppliers, may be limited or disrupted by the inability to obtain or maintain necessary regulatory licenses to operate plasma collection centers in a timely manner or at all, or by the temporary or permanent shutdown of our or our suppliers’ plasma collection centers as a result of regulatory violations. |

| | • | | Plasma supply sources. In recent years, there has been vertical integration in the industry as plasma derivatives manufacturers have been acquiring plasma collection centers. Any significant disruption in the supply of plasma or an increased demand for plasma may require plasma from alternative sources, which may not be available on a timely basis. |

A significant portion of our revenue has historically been derived from sales of our immunoglobulin products and we expect that they will continue to comprise a significant portion of our sales. Any adverse market event with respect to these products would have a material adverse effect on us.

We have historically derived a significant portion of our net sales from our immunoglobulin products, including our IVIG products. If either of our IVIG products, Flebogamma® or Gamunex®, or Gamunex®-C immunoglobulin, lost significant sales or was substantially or completely displaced in the market, we would lose a significant and material source of our net revenue. Similarly, if either Flebogamma® or Gamunex®-C/Gamunex® was to become the subject of litigation or an adverse governmental ruling requiring us to cease sales of it, our business could be adversely affected. Although we do not currently anticipate any significant decrease in the sales of any of these products, a significant decrease could result from plasma procurement and manufacturing issues resulting in lower product availability for sales and changing market conditions.

Our products face increased competition.

Our products have experienced increased competition. Each of Baxter and CSL Behring has launched 10% liquid IVIG products in the U.S. Octopharma and Bio Products Laboratory has launched 5% liquid IVIG products. Additionally, Biotest is seeking approval for a 10% liquid IVIG product in the U.S., which, if approved, will further increase competition among liquid IVIG products. As competition has increased, competitors have discounted the price of IVIG products. Furthermore, many customers are increasingly price sensitive with respect to IVIG products. If customers demand lower priced products from our competitors, we may lose sales or be forced to lower our prices.

The FDA recently approved Gamunex®-C for the subcutaneous route of administration for the A1PI indication. In 2010, CSL Behring received FDA approval for and launched Hizentra Immune Globulin Subcutaneous (Human) 20% liquid. Baxter also recently obtained approval for the subcutaneous use of its 10% liquid IVIG, and it has conducted a trial to obtain FDAorphan drug designation for the product in neurology, which was already granted in the European Union in 2011. We also believe that our competitors are developing several new products and technologies, which may include an improved route of administration for indications beyond A1PI.

Until December 2002, Talecris’ A1PI product, Prolastin® A1PI, was the only plasma product licensed and marketed for the therapy of congenital A1PI deficiency-related emphysema in the U.S. Baxter and CSL Behring received licenses for Aralast and Zemaira, respectively, which were launched in the U.S. in 2003. In addition, Kamada Ltd. received approval of its biological license application, or BLA, for its A1PI, Glassia, on July 1, 2010.

While LFB Biomedicaments has a license in France for Alfalastin, we have the only licensed A1PI products with EMA Community marketing authorization. Of our competitors that are currently pursuing licensing trials in Europe, one offers a more concentrated intravenous formulation than the ones we offer in Europe. Should our competitors receive approvals in Europe sooner than expected, it will impact our unit volumes and share of sales. Our current and future competitors may increase their sales, lower their prices or change their distribution model, causing harm to our product sales and financial condition. Also, if the attrition rate of our A1PI patient base accelerates faster than we have forecast, we would have fewer patients and lower sales volume.

Similarly, if a new AIP1 formulation with a significantly improved rate of administration (such as aerosol inhalation) is developed, the market share of our A1PI products could be negatively impacted. Similarly, several companies are attempting to develop products which could be substitutions for A1PI, including retinoic acid, oral synthetic elastase inhibitors and gene therapy. While these products are in the early stages of development, they may eventually be successfully developed and launched.

In addition, our plasma-derived products face competition from non-plasma products and other courses of treatments. For example, two Rho(D) intramuscular (hyperimmune) globulins for intravenous administration, Cangene’s WinRho SDF and CSL

15