MRC Global Inc. // 2012 KeyBanc Capital Markets Conference May 31, 2012 Exhibit 99.1 |

Page 2 MRC // Global Supplier of Choice ® ® Forward Looking Statements and GAAP Disclaimer This presentation contains forward-looking statements, including, for example, statements about the Company’s business strategy, its industry, its future profitability, growth in the Company’s various markets, the strength of future activity levels, and the Company’s expectations, beliefs, plans, strategies, objectives, prospects and assumptions. These forward-looking statements are not guarantees of future performance. These statements involve known and unknown risks, uncertainties and other factors that may cause the Company’s actual results and performance to be materially different from any future results or performance expressed or implied by these forward-looking statements. For a discussion of key risk factors, please see the risk factors disclosed in the Company’s registration statement on Form S-1 effective April 11, 2012, related to our common stock, and our Quarterly Statement on Form 10-Q for the quarter ended March 31, 2012, both of which are available on the SEC’s website at www.sec.gov. Undue reliance should not be placed on the Company’s forward-looking statements. Although forward-looking statements reflect the Company’s good faith beliefs, reliance should not be placed on forward-looking statements because they involve known and unknown risks, uncertainties and other factors, which may cause our actual results, performance or achievements to differ materially from anticipated future results, performance or achievements expressed or implied by such forward-looking statements. The Company undertakes no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events, changed circumstances or otherwise, except to the extent required by law. Statement Regarding use of Non-GAAP Measures: The Non-GAAP financial measures contained in this presentation (including, without limitation, EBITDA, Adjusted EBITDA, Adjusted EBITDA Margin, Adjusted Gross Profit, Return on Net Assets (RONA) and variations thereof) are not measures of financial performance calculated in accordance with GAAP and should not be considered as alternatives to net income (loss) or any other performance measure derived in accordance with GAAP or as alternatives to cash flows from operating activities as a measure of our liquidity. They should be viewed in addition to, and not as a substitute for, analysis of our results reported in accordance with GAAP, or as alternative measures of liquidity. Management believes that certain non- GAAP financial measures provide a view to measures similar to those used in evaluating our compliance with certain financial covenants under our credit facilities and provide financial statement users meaningful comparisons between current and prior year period results. They are also used as a metric to determine certain components of performance- based compensation. The adjustments and Adjusted EBITDA are based on currently available information and certain adjustments that we believe are reasonable and are presented as an aid in understanding our operating results. They are not necessarily indicative of future results of operations that may be obtained by the Company. |

Page 3 ® MRC // Global Supplier of Choice ® Executive Management Andrew Lane Chairman, President & Chief Executive Officer • Former Executive VP and COO of Halliburton • Former CEO of Kellogg Brown & Root • Former CEO of Landmark Graphics Jim Braun Executive Vice President & Chief Financial Officer • Former CFO of Newpark Resources • Former CFO of Baker Oil Tools • CPA and Former Partner with Deloitte & Touche |

Page 4 MRC // Global Supplier of Choice ® ® Investment Considerations • World-Class Management Team With Significant Distribution and Energy Experience • Clear Market Leader With Global Reach • Comprehensive Suite of Products and Services • Strong Long-Term Customer and Supplier Relationships • Scale and Reach Create Competitive Advantage • Robust Organic Growth Supported by Positive Secular Trends and Acquisition Opportunities • Operating leverage drives strong financial performance |

Page 5 MRC // Global Supplier of Choice ® ® Company Snapshot MRC by the numbers: 2011 Sales $4.8 B Locations 410+ Countries 18 Customers 12,000+ Suppliers 12,000+ SKU’s 150,000+ Employees 4,425 MRC is the largest global distributor of pipe, valves and fittings (PVF) to the energy industry. MRC is the largest global distributor of pipe, valves and fittings (PVF) to the energy industry. Upstream Midstream Downstream / Industrial Fittings Line Pipe / OCTG Flanges Valves Business Model Product Categories Industry Sector Projects 34% MRO 66% U.S. 80% Canada 13% lntl 7% |

Page 6 MRC // Global Supplier of Choice ® ® MRC History Founded 1921 1989 Acquires Appalachian Pipe & Supply 2007 Goldman Sachs Capital Partners Strategic Investment 1977 Founded 2005 Acquires Midfield Supply 2008 MRC acquires LaBarge 2007 Merger of McJunkin and Red Man to form MRC 2009 MRC opens Houston HQ 2009 MRC acquires Transmark 2010 MRC acquires South Texas Supply 2010 MRC acquires Dresser Oil Tools 2011 MRC acquires SPF 2011 MRC acquires VSC 2012 MRC acquires OneSteel Piping Systems 2012 MRC Global IPO; begins trading on NYSE VSC |

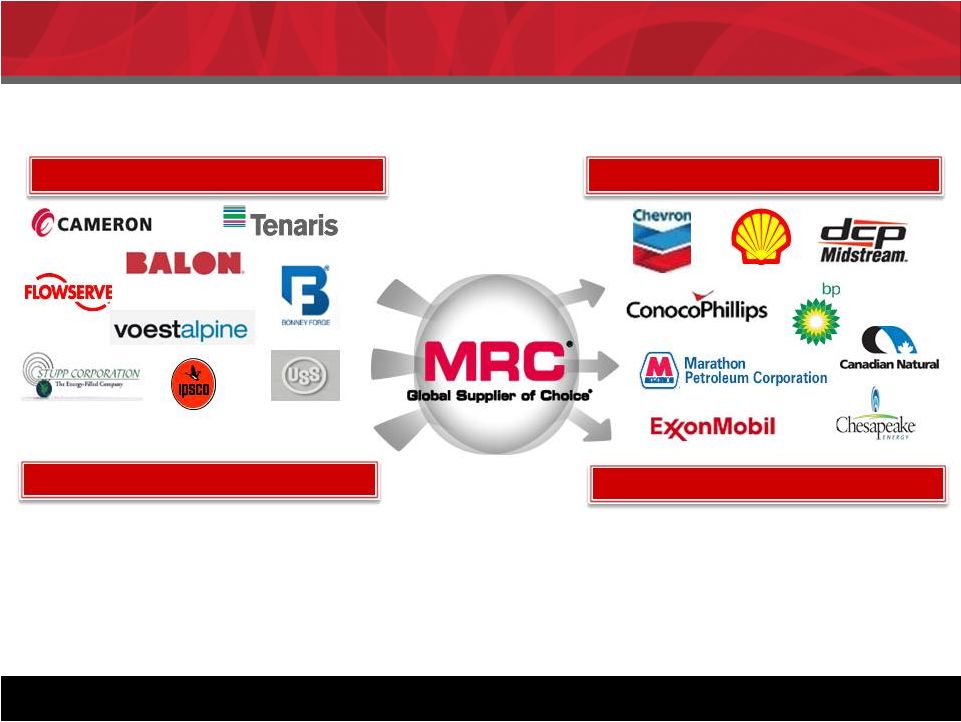

Page 7 MRC // Global Supplier of Choice ® ® Business Model • Access to over 12,000+ customers worldwide • Manufacturing and scale efficiencies • Reduced administrative and selling costs • Demand visibility • Customer feedback • Access to over 12,000+ suppliers worldwide • Scale / supplier consolidation benefits • Efficiencies and inventory management • Trusted long-term partnerships • Seamless integration, “customer connectivity” MRC plays a critical role in the complex, technical, global energy supply chain Suppliers Customers Supplier Benefits Customer Benefits |

Page 8 ® MRC // Global Supplier of Choice ® MRC Value Proposition MRC’s size and scale enable it to provide value-added services that create competitive advantages Customer Need MRC Value Add 1. Product Availability • Broad product offering • Over $1 billion in inventory 2. Achieve Lowest Installed Cost • Volume purchasing • Global sourcing from 35 countries 3. Outsource Non-core Functions • Inventory management • Integrated supply service 4. Ease of Doing Business • One-Stop Solution • Customized IT system interface 5. Product Support • Technical support • Product specialists 6. Financial Stability • Fortune 500 company • Over $4.8B sales 7. Quality Assurance • Manufacturer assessment & approved supplier list • Supplier Registration Process (SRP) |

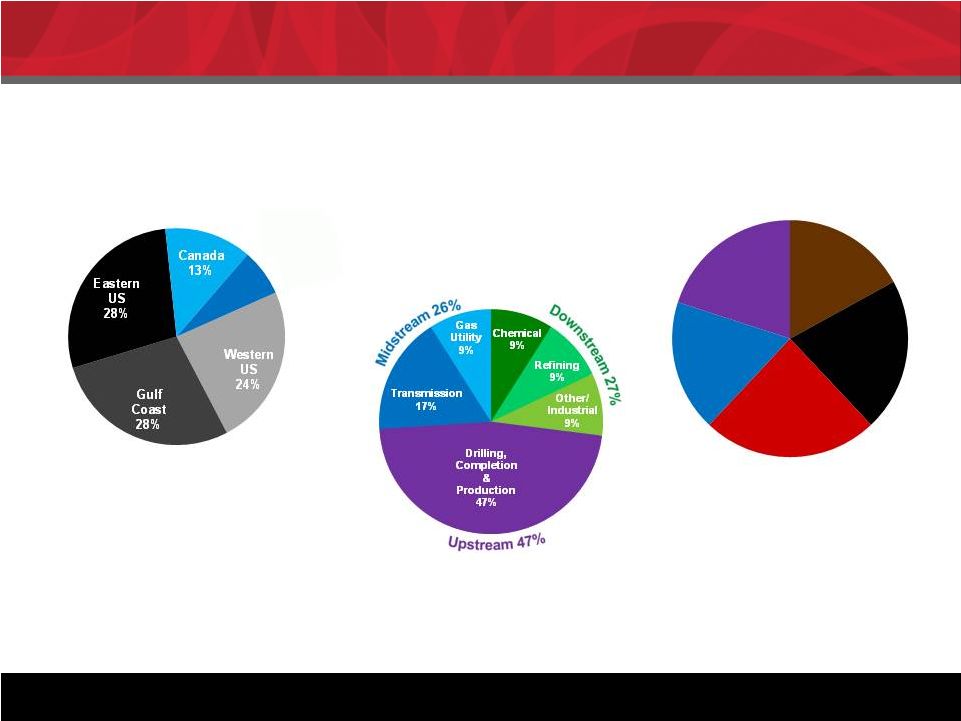

Page 9 MRC // Global Supplier of Choice ® ® MRC Presence By Geography Note: Business mix based on 2011 sales By Product Line Diversified by geography, sector, and product line By Industry Sector Rest of World 7% OCTG 17% Line Pipe 21% Valves 24% Fittings & Flanges 18% Other 20% |

Page 10 MRC // Global Supplier of Choice ® ® North America Well positioned to capitalize on shale, heavy oil and oil sands activity. Infrastructure Strong North American • 175+ Branches • 150+ pipe yards • 7 DCs • 12 Valve Automation Centers |

Page 11 MRC // Global Supplier of Choice ® ® International International E&P spending forecast to grow 12% in 2012* Expanding International Presence * Barclays Equity Research MRC Branches / Locations Regional Distribution Centers • 40+ branches • DCs in UK, Singapore and Australia • 11 valve automation centers |

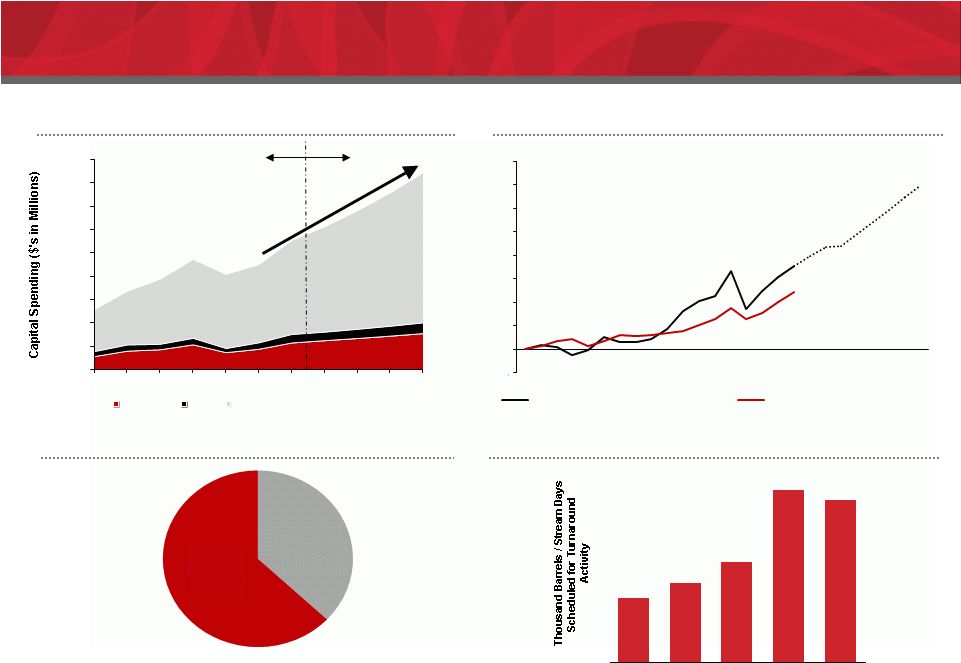

Page 12 MRC // Global Supplier of Choice ® ® Positive Trends 12 Strong Growth in Global E&P Spending 1 Source: Barclays 2012 E&P Spending Outlook Mid Year Update. 2 Source: Barclays 2012 E&P Spending Outlook Mid Year Update. 3 Source: Pipeline Safety and Hazardous Materials Administration, Wall Street Journal, for Top 10 states by pipeline mileage 4 Source: Industrial Info Resource, Inc. Based on quarterly average planned unit outages. Aging Infrastructure and New Legislation To Drive Pipeline Replacement 444 548 688 1,193 1,126 2009A 2010A 2011E 2012E 2013E WTI Prices and Global E&P Spending Continue Upward Trend Actual Estimates U.S. Refining Turnaround Activity Poised for Growth 4 Built After 1970 37% Built Before 1970 63% 0 100,000 200,000 300,000 400,000 600,000 700,000 800,000 900,000 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 500,000 - 100% 0% 100% 200% 300% 400% 500% 600% 700% 800% 1995 2000 2005 2010 2015E 2020E Inflation Adjusted WTI Prices (indexed) Global E&P Spending (indexed) 1 2 3 United States Canada Outside North America |

Page 13 MRC // Global Supplier of Choice ® ® Changing PVF Distribution Landscape Decentralized Procurement • PVF purchasing handled locally • Facility-by-facility basis • Separate contracts by product class: • Pipe • Valves • Fittings • Flanges • Supplies Centralized Procurement • Purchasing more consolidated • Contracts by “stream”: • National purchasing • Contracts cover all PVF • Customers seek vendors with size/scale Global • Far more consolidated • Global up / mid / downstream PVF contracts • National Oil Companies adopting distribution model Today 10 – 15 Years Ago Next 5 to 10 Years Consolidating energy industry benefits global players • Up • Mid • Down |

Page 14 MRC // Global Supplier of Choice ® ® Increasing Shareholder Value Growth Efficiency / Profitability Increase Capital Investment Increase Returns on New Capital Increase Profits on Existing Capital Optimize Cost of Capital Organic Growth • North American shale • Unconventional shale drilling • Midstream growth • Downstream – turnaround activity • Improve purchasing • Optimize inventory mix • Global sourcing • Focus on higher margin products • Leverage fixed costs • Improve working capital efficiency • Maintain leverage at 2.0x – 3.0x • Reduce overall cost of debt Acquisitions • International product line extensions • Valve & actuation • North American tuck-ins Revenue Growth: Target 10% to 12% per year Organic: 8% to 9% Acquisitions: 2% to 3% Projected Adjusted EBITDA margins 8.0 to 8.5% near term 9.0 to 9.5% mid term 10% 5 years |

Page 15 MRC // Global Supplier of Choice ® ® Unconventional Drilling Opportunity Legacy Basins Shale Plays Representative area Permian Bakersfield (Monterey) Marcellus Bakken Eagle Ford Utica Barnett Haynesville Utica Niobrara Age 50 to 100 years 1 to 10 years Primary resources Oil and Gas Oil, wet gas and dry gas Drilling method Vertical Horizontal Horizontal drilling with hydraulic fracturing “fracking” Typical environment Shallow well; typically low pressure Up to 3-5x the pipe requirements of a vertical well • Deeper wells • Higher pressure • Higher volumes Existing infrastructure Mature Requires upgrading Non existent, new or under construction PVF spend vs. traditional non-shale 3 – 5x Wellhead only Total spend 3 – 5x 5 – 10x Unconventional shale drilling is driving higher PVF spend |

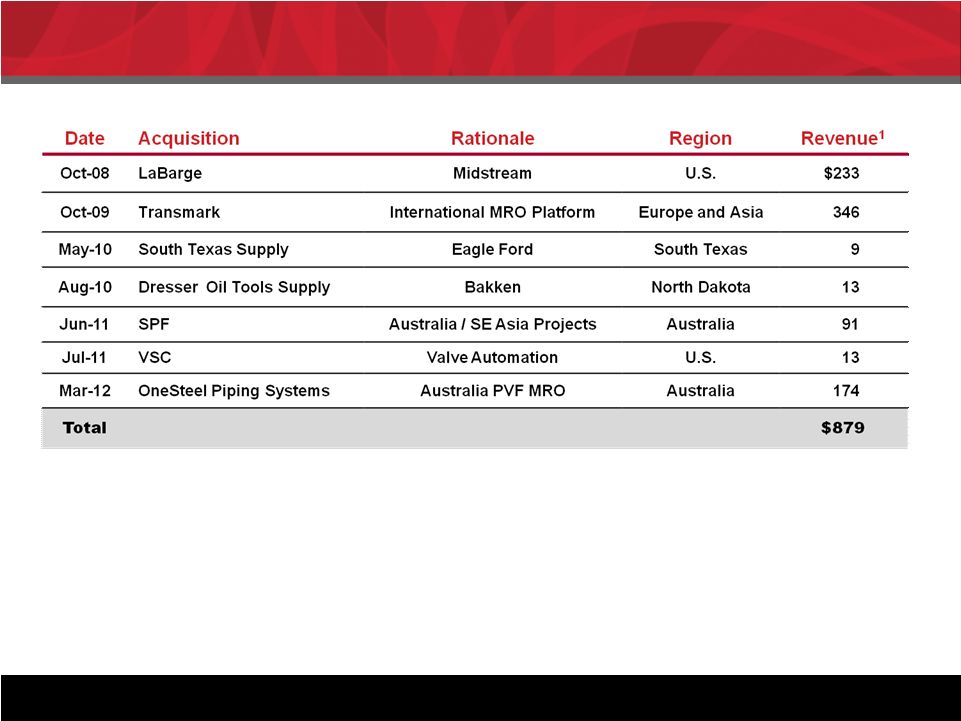

Page 16 MRC // Global Supplier of Choice ® ® Track Record of Successful M&A 1 Reflects reported revenues for the year of acquisition (US$ in millions) MRC has completed and successfully acquired $879 million of revenues since mid 2008 Current M&A Focus • International expansion • North America expansion • Valve and automation • Bolt-ons |

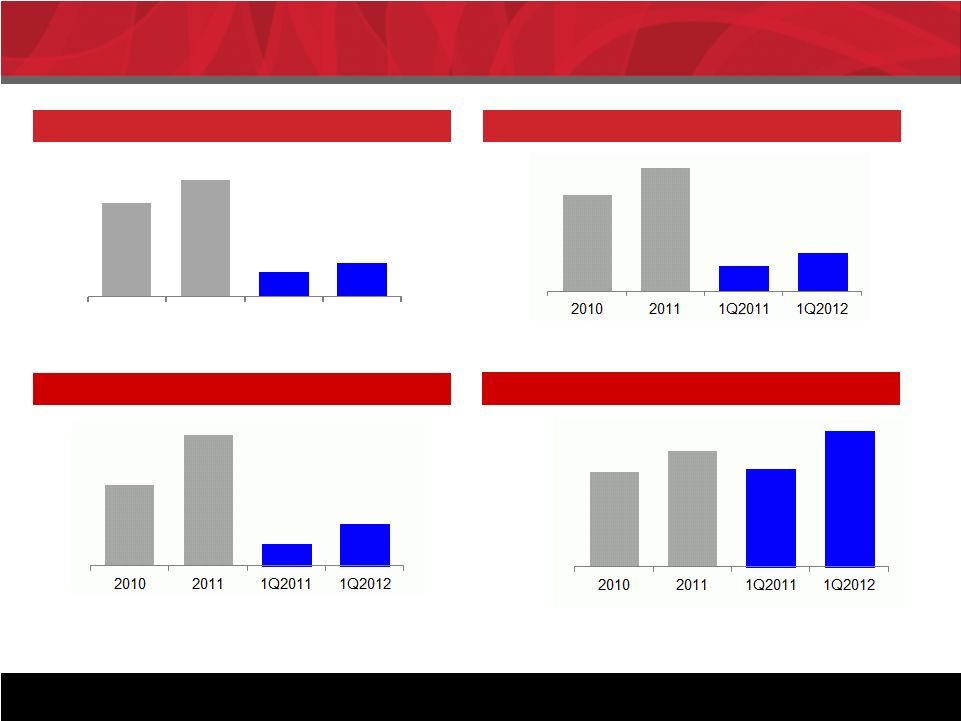

Page 17 MRC // Global Supplier of Choice ® ® Financial Trends Sales Adjusted Gross Profit and % Margin Source: Company management RONA calculation = Adjusted EBITDA divided by the sum of accounts receivable, inventory (plus the LIFO reserve), and PP&E less accounts payable. Adjusted EBITDA and % Margin Return on Net Assets (RONA) Strong growth and increasing profitability Y-o-Y Growth 26% 39% Y-o-Y Growth 26% 39% Y-o-Y Growth 61% 92% 5.8% 7.5% 6.1% 8.3% (US$ in millions) $3,846 $4,832 $992 $1,383 2010 2011 1Q2011 1Q2012 19.6% 24.1% 20.4% 28.2% $224 $361 $60 $115 $663 $850 $174 $260 17.2% 17.6% 17.5% 18.8% |

Page 18 First Quarter Update 18 In millions, except per share data ¹ As of May 31, 2012 First Quarter Full Year 2012 Outlook 1 2012 2011 Sales 1,383 $ 992 $ Sales $5.4 to $5.6 billion Cost of sales 1,146 845 Adjusted EBITDA % 8.0% to 8.5% of sales Gross profit 237 147 SG&A 146 117 Operating income 90 30 Net income 38 $ (1) $ EPS 0.44 $ (0.01) $ Adjusted EBITDA 115 $ 60 $ Adjusted EBITDA % 8.3% 6.0% First Quarter 2012 versus First Quarter 2011 • Revenues: Up 39% • Double digit growth rates in each of upstream, midstream and downstream and industrial sectors • Adjusted EBITDA: Up 92% MRC // Global Supplier of Choice ® ® |

Page 19 MRC // Global Supplier of Choice ® ® Capital Structure 19 • Pro forma for IPO with net proceeds of $334 million used to repay debt • New multi-currency Global ABL facility • ABL / HY bond ensures capital structure flexibility given absence of maintenance covenants ($ in millions) Pro Forma 3/31/2012 Cash and equivalents 59 $ $1.25 billion MRC Global ABL credit facility (2017) 237 $ 9.5% senior secured notes, net of discount (2016) 1,033 Other 8 Total debt 1,278 $ Stockholders' equity 1,099 $ Total capitalization 2,377 $ March 2012 TTM Adjusted EBITDA 415 $ Total debt/Adjusted EBITDA 3.1x Net debt/Adjusted EBITDA 2.9x |

Page 20 MRC // Global Supplier of Choice ® ® THANK YOU! |

Page 21 MRC // Global Supplier of Choice ® ® Appendix • First Quarter 2012 financial statements • Management Biographies |

Page 22 MRC // Global Supplier of Choice ® ® Appendix *In April 2012, MRC Global issued 17.0 million shares of common stock as part of its initial public offering, resulting in a total of 101.5 million shares outstanding post transaction MRC Global Inc. Condensed Consolidated Statements of Operations (Unaudited) (Dollars in thousands, except per share amounts) Three Months Ended March 31, March 31, 2012 2011 Sales $ 1,382,632 $ 991,813 Cost of sales 1,146,071 844,847 Gross profit 236,561 146,966 Selling, general and administrative expenses 146,384 117,357 Operating income 90,177 29,609 Other income (expense): Interest expense (33,717) (33,500) Write off of debt issuance costs (1,685) - Change in fair value of derivative instruments 2,125 1,868 Other, net 1,747 205 (31,530) (31,427) Income (l oss) before income taxes 58,647 (1,818) Income tax expense (benefit) 21,113 (690) Net income (loss) $ 37,534 $ (1,128) Effective tax rate 36.0% 38.0% Basic earnings (loss) per common share $ 0.44 $ (0.01) Diluted earnings (loss) per common share $ 0.44 $ (0.01) Weighted -average common shares, basic * 84,437 84,413 Weighted -average common shares, diluted * 84,756 84,413 |

Page 23 MRC // Global Supplier of Choice ® ® Appendix MRC Global Inc. Condensed Consolidated Balance Sheets (Unaudited) (Dollars in thousands) March 31, December 31, March 31, 2012 2011 2011 Assets Current assets: Cash $ 58,833 $ 46,127 $ 42,080 Accounts receivables, net 871,227 791,280 594,892 Inventories, net 1,022,851 899,064 783,554 Other current assets 17,598 11,437 39,554 Total current assets 1,970,509 1,747,908 1,460,080 Other assets 44,767 39,212 45,534 Property, plant and equipment, net 114,173 107,430 103,950 Intangible assets: Goodwill 568,811 561,270 551,720 Other intangible assets, net 780,198 771,867 808,220 1,349,009 1,333,137 1,359,940 $ 3,478,458 $ 3,227,687 $ 2,969,504 Liabilities and stockholders’ equity Current liabilities: Trade accounts payable $ 555,556 $ 479,584 $ 420,085 Accrued expenses and other current liabilities 142,500 108,973 106,909 Income taxes payable 26,133 11,950 - Deferred revenue 2,440 4,450 14,026 Deferred income taxes 69,155 68,210 70,825 Total current liabilities 795,784 673,167 611,845 Long-term obligations: Long-term debt, net 1,611,960 1,526,740 1,333,008 Deferred income taxes 287,585 288,985 302,274 Other liabilities 18,108 17,933 21,797 1,917,653 1,833,658 1,657,079 Stockholders’ equity 765,021 720,862 700,580 $ 3,478,458 $ 3,227,687 $ 2,969,504 |

Page 24 MRC // Global Supplier of Choice ® ® Net proceeds (payments) on/from revolving credit facilities Appendix MRC Global Inc. Condensed Consolidated Balance Sheets (Unaudited) (Dollars in thousands) Three Months Ended March 31, March 31, 2012 2011 Operating activities Net income (loss) $ 37,534 $ (1,128) Depreciation and amortization 4,131 4,003 Amortization of intangibles 12,317 12,443 Equity-based compensation expense 1,841 1,483 Deferred income tax benefit (2,110) (1,127) Amortization of debt issuance costs 2,326 2,990 Write off of debt issuance costs 1,685 - Increase in LIFO reserve 6,900 10,065 Change in fair value of derivative instruments (2,125) (1,868) Provision for uncollectible accounts 727 (278) 700 2,264 Changes in operating assets and liabilities: Accounts receivable (44,150) 8,257 Inventories (68,807) (24,706) 14,044 2,983 Other current assets (5,834) 539 Accounts payable 43,816 (10,685) Deferred revenue (2,026) (4,137) Accrued expenses and other current liabilities 17,346 4,714 18,315 5,812 Investing activities Purchases of property, plant and equipment (4,458) (1,964) 1,195 140 Acquisition of the assets and operations of OneSteel Piping Systems (72,816) - Proceeds from the sale of assets held for sale - 10,933 (3,813) 2,830 Net cash (used in) provided by investing activities (79,892) 11,939 Financing activities 114,146 (30,830) (31,456) - Debt issuance costs paid (7,099) - 75,591 (30,830) Increase (decrease) in cash 14,014 (13,079) Effect of foreign exchange rate on cash (1,308) (1,043) Cash - beginning of period 46,127 56,202 Cash - end of period $ 58,833 $ 42,080 Proceeds from the disposition of property, plant and equipment Other investment and notes receivable transactions Non-operating losses and other items not using cash Adjustments to reconcile net income (loss) to net cash provided by operations: Income taxes payable Net cash provided by operations Payments on long-term obligations Net cash provided by (used in) financing activities |

Page 25 MRC // Global Supplier of Choice ® ® Appendix MRC Global Inc. Supplemental Infomation (Unaudited) Calculation of Adjusted EBITDA (Dollars in millions) Three Months Ended March 31, March 31, 2012 2011 Net income (loss) $ 37.5 $ (1.1) Income tax expense (benefit) 21.1 (0.7) Interest expense 33.7 33.5 Write off of debt issuance costs 1.7 - Depreciation and amortization 4.1 4.0 Amortization of intangibles 12.3 12.4 Increase in LIFO reserve 6.9 10.1 Change in fair value of derivative instruments (2.1) (1.9) Equity-based compensation expense 1.8 1.5 Legal and consulting expenses (1.2) 1.2 Other non-cash expenses (0.6) 1.0 Adjusted EBITDA $ 115.2 $ 60.0 Note to above: Adjusted EBITDA consists of net income plus interest, income taxes, depreciation and amortization, amortization of intangibles and other non-recurring, non-cash charges (such as gains/losses on the early extinguishment of debt, changes in the fair value of derivative instruments and goodwill impairment), and plus or minus the impact of our LIFO costing methodology. The Company has included Facility and provides investors a helpful measure for comparing its operating performance with the performance of other companies that have different financing and capital structures or tax rates. Adjusted EBITDA as a supplemental disclosure because we believe Adjusted EBITDA is an important measure under its Global ABL |

Page 26 MRC // Global Supplier of Choice ® ® Appendix Andy Lane Chairman, President & CEO Andrew Lane has served as our president and chief executive officer since September 2008. Andrew became the chairman of the board in December 2009. He has also served as a director of our company since September 2008. From December 2004 to December 2007, he served as executive vice president and chief operating officer of Halliburton Company, where he was responsible for Halliburton’s overall operational performance, managed over 50,000 employees worldwide and oversaw several mergers and acquisitions integrations. Prior to that, he held a variety of leadership roles within Halliburton, serving as president and chief executive officer of Kellogg Brown & Root, Inc. from July 2004 to November 2004, as senior vice president, global operations of Halliburton Energy Services Group from April 2004 to July 2004, as president of the Landmark Division of Halliburton Energy Services Group from May 2003 to March 2004, and as president and chief executive officer of Landmark Graphics Corporation from April 2002 to April 2003. He was also chief operating officer of Landmark Graphics from January 2002 to March 2002 and vice president, production enhancement PSL, completion products PSL and tools/testing/TCP of Halliburton Energy Services Group from January 2000 to December 2001. Mr. Lane also served as a director of KBR, Inc. from June 2006 to April 2007. He began his career in the oil and gas industry as a field engineer for Gulf Oil Corporation in 1982, and later worked as a production engineer in Gulf Oil’s Pipeline Design and Permits Group. Mr. Lane received a B.S. in mechanical engineering from Southern Methodist University. He is a member of the executive board of the Southern Methodist University School of Engineering. Jim Braun Executive VP & CFO Jim Braun has served as our executive vice president and chief financial officer since November 2011. Prior to joining the company, Mr. Braun served as chief financial officer of Newpark Resources, Inc. He joined Newpark in 2006 where he led financial management and furthered the execution of that company’s strategic business plan as a member of the executive team. Newpark provides drilling fluids and other products and services to the oil and gas exploration and production industry, both inside and outside of the U.S. Before joining Newpark, Mr. Braun was chief financial officer, of Baker Oil Tools, one of the largest divisions of Baker Hughes Incorporated, a Fortune 500 provider of drilling, formation evaluation, completion and production products and services to the worldwide oil and gas industry. In his role at Baker Oil Tools, he was responsible for the divisional financial management of the company including accounting, planning, internal controls, tax, IT, acquisitions and divestitures. From 1998 until 2002, he was vice president, finance and administration, of Baker Petrolite, the oilfield specialty chemical business division of Baker Hughes. Previously, he served as vice president and controller of Baker Hughes. Earlier in his career, he was a partner with Deloitte & Touche in Houston, Texas. Mr. Braun graduated from the University of Illinois at Urbana-Champaign with a B.A. and is a certified public accountant. |

Page 27 MRC // Global Supplier of Choice ® ® Appendix Rory Isaac Executive VP Global Business Development Rory M. Isaac has served as executive vice president business development at our company since December 2008. Prior to that, he served as senior corporate vice president of sales (focusing on downstream, industrials and gas utilities operations) at our company since November 2007. He served as senior corporate vice president national accounts at McJunkin from 1995 to 2000 and as senior corporate vice president national accounts, utilities and marketing at McJunkin from 2000 to 2007. Mr. Isaac joined McJunkin in 1981. He has extensive experience in sales, customer relations and management and has served at McJunkin as a branch manager, regional manager and regional vice president. In 1995 he began working in the corporate office of McJunkin in Charleston, West Virginia as senior vice president for national accounts, where he was responsible for managing and growing McJunkin’s national accounts customer base and directing business development efforts into integrated supply markets. In 1999 he took on the additional responsibility of growing McJunkin’s market share in key initiative areas including gas products and marketing McJunkin’s capabilities. Prior to joining McJunkin, Mr. Isaac worked at Consolidated Services, Inc. and Charleston Supply Company. Mr. Isaac attended the Citadel. Jim Underhill Executive VP & Chief Operating Officer (COO) North America James F. Underhill has served as our executive vice president and chief operating officer of our company since November 2011. Jim served as executive vice president and chief financial officer from November 2007 through November 2011. At McJunkin, he served as chief financial officer from May 2006 through October 2007, as senior vice president of accounting and information services from 1994 to May 2006, and vice president and controller from 1987 to 1994. Prior to 1987, Mr. Underhill served as controller, assistant controller, and corporate accounting manager. Mr. Underhill joined McJunkin in 1980 and has since overseen McJunkin’s accounting, information systems, and mergers and acquisitions areas. He has been involved in numerous implementations of electronic customer solutions and has had primary responsibility for the acquisition and integration of more than 30 businesses. Mr. Underhill was also project manager for the design, development, and implementation of McJunkin’s FOCUS operating system. He received a B.A. in accounting and economics from Lehigh University in 1977 and is a certified public accountant. Prior to joining McJunkin, Mr. Underhill worked in the New York City office of the accounting firm of Main Hurdman. Dan Churay Executive VP Corporate Affairs, General Counsel & Corporate Secretary Daniel J. Churay has served as our executive vice president and general counsel since August 2011. Prior to joining the company, Mr. Churay served as the president and chief executive officer of Rex Energy Corporation, an independent oil and gas company, from December 2010 to June 2011. From September 2002 to December 2010, Mr. Churay served as executive vice president, general counsel and secretary of YRC Worldwide Inc., a Fortune 500 transportation and logistics company, with primary responsibility for YRC Worldwide Inc.’s legal, risk, compliance and external affairs matters, including its internal audit function. From 1995 to 2002, Mr. Churay served as the deputy general counsel and assistant secretary of Baker Hughes Incorporated, a Fortune 500 company that provides products and services to the petroleum and continuous process industries, where he was responsible for legal matters relating to acquisitions, divestitures, treasury matters and securities offerings. From 1989 to 1995, Mr. Churay was an attorney at the law firm of Fulbright & Jaworski LLP in Houston, Texas. Mr. Churay received a bachelor’s degree in economics from the University of Texas and a Juris Doctor degree from the University of Houston Law Center, where he was a member of the law review. |

Page 28 MRC // Global Supplier of Choice ® ® Appendix Scott Hutchinson Executive VP North America Operations Scott Hutchinson has served MRC as our executive vice president North America operations since November 2009. Mr. Hutchinson began his career with MRC as an outside sales representative for Grant Supply in Houston, TX when the company was acquired by McJunkin Corporation. In May 1990, he was promoted to regional manager of Northern and Southern California. He was promoted to senior vice president of the Midwest region in October 1998. During this time he was key in the acquisitions of Wilkins Supply, Joliet Valve, Cigma and Valvax, solidifying and expanding the market reach of the company in the Midwest. On January 1, 2009, his responsibility increased when he was promoted to senior vice president of the Eastern region, which combined the Midwest and Eastern regions, covering most operational units east of the Mississippi River including the Chicago market. On June 1, 2009, MRC rolled the Appalachian region into the Eastern region, and Mr. Hutchinson assumed responsibility for those upstream operations based in the Appalachian basin. His extensive background in branch sales and operations was instrumental as he led a very effective integration effort. Prior to MRC, Mr. Hutchinson received a Bachelor of Arts degree in Marketing from the University of Central Florida in 1977. Between 1979 and 1984 he worked for Fluor as a senior buyer, and then started work with Grant Supply in 1984. Neil P. Wagstaff Executive VP International Operations Neil P. Wagstaff has served as our executive vice president international operations and as chief executive officer of MRC Transmark since November 2009. From July 2006 until November 2009, he served as group chief executive of Transmark Fcx Group B.V. where he was responsible for the group’s overall performance in 13 operating companies in Europe, Asia and Australia and overseeing a number of acquisitions and integrations. Prior to that, he held a variety of positions within Transmark Fcx, serving as a group divisional director from 2003, responsible for operations in the UK and Asia, as well as managing director for the UK businesses. He was also sales and marketing director of Heaton Valves prior to the acquisition by Transmark group in 1996, as well as Sales and Marketing Director for Hattersley Heaton valves and Shipham Valves. He has extensive experience in international sales management and marketing having worked in the international arena since 1987. Mr. Wagstaff began his career in the valve manufacturing business in 1983 when he studied mechanical engineering at the Saunders Valve Company and developed professionally through a number of sales management positions. Educated at London Business School he is a chartered director and fellow of the UK Institute of Directors. Gary Ittner Executive VP Global Supply Chain Management Gary A. Ittner has served as our executive vice president and chief administrative officer since September 2010. Prior to that, he served as executive vice president supply chain management from October 2008 and prior to that, he served as our senior corporate vice president of supply chain management since November 2007. He has specific responsibility for the procurement of all industrial valves, automation, fittings and alloy tubular products. Prior to November 2007, he served as senior corporate vice president of supply management at McJunkin since March 2001. Before joining the Supply Management Group, Mr. Ittner worked in various field positions including branch manager, regional manager, and senior regional vice president. He is a past chairman of the executive committee of the American Supply Association’s Industrial Piping Division. Mr. Ittner began working at McJunkin in 1971 following his freshman year at the University of Cincinnati and joined the company full-time following his graduation in 1974. |