Management Energy

A coal development company

Preliminary Project Plan

September 30, 2009

Prepared for

Management Energy, Inc.

30950 Rancho Viejo Road, Suite 120

San Juan Capistrano, CA 92675

Prepared by

| Daniel Jaouiche, President 314.608.6319 djaouiche@NRGDimensions.com |

| Energy Dimensions, LLC | Confidential | |

Energy Dimensions, LLC has been retained by Management Energy (MMEX) to develop an initial project plan focusing on the Bridger-Fromberg reserve in Montana. The project plan includes an assessment of MMEX’s strategic options in the current market environment to monetize the asset, and an initial action plan to begin implementation of the project plan. Unless otherwise indicated, Energy Dimensions, LLC is the source of all industry, market and project-specific data, assumptions and other information contained in this project plan.

| 2. | Company Value Proposition |

MGMT Energy, Inc. acquires and develops coal mining projects in the U.S. to provide coal to both domestic and foreign markets.

| Bridger-Fromberg Project Overview |

MMEX currently has a lease to develop the 6,250 acre Bolzer property located within the Bridger-Fromberg reserve in Montana. The Bridger-Fromberg reserve is located in southern Montana, southwest of Billings.

MMEX is seeking to obtain control of additional leases with total acreage in excess of 50,000 acres to mine a significant part of the Bridger-Fromberg Project. The project requires additional lease, distribution, and transport arrangements.

| Energy Dimensions, LLC | Confidential | 2 of 11 |

The railroad loading for this project is planned be located near Bridger, Montana on Burlington Northern’s Thermopolis/ Casper railroad line. The project requires the building of a rail line of approximately 5 miles to connect the mines to the Burlington Northern railroad line.

The project is still in the early development stage and requires additional drilling and study to establish reliable reserve estimates. Based on similar reserves in proximity and related coal seams, Energy Dimensions is assuming for purposes of this preliminary project plan a reserve size of at least 200 million tons, a heat rate of more than 11,000 Btu, and less than 1% sulfur.

| 4. | United States Coal Market |

U.S. Coal Consumption:

Electric-power-sector coal consumption fell by 11 percent in the first half of 2009. The decline resulted from lower total electricity generation combined with increases in generation from natural gas, nuclear, hydropower, and wind. Coal consumption in the electric power sector is projected to increase by almost 2 percent in 2010 but remains below the 1-billion short-ton level for the second consecutive year. Coal consumed for steam (retail and general industry) and coke production declined by 15 percent in the first quarter of 2009 compared with the first quarter of last year. The U.S. Energy Information Administration (“EIA”) forecasts lower consumption of coal in both sectors for the remainder of the year, followed by a combined increase in coal consumed by these sectors of more than 5 percent in 2010.

U.S. Coal Supply:

Coal production for the first 6 months of 2009 fell by more than 5 percent in response to lower U.S. coal consumption, fewer exports, and higher coal inventories; these conditions persist in the forecast for the remainder of 2009. EIA projects production declines by 1.4 percent in 2010, despite increases in domestic consumption and exports. Reductions in coal inventories and increased imports offset the increase in U.S. coal consumption.

U.S. Coal Prices:

The monthly average delivered electric-power-sector coal price reached a record high of $2.29 per million Btu in March 2009. The delivered cost of coal to the electric power sector had continued to rise, despite decreases in spot coal prices, lower prices for other fossil fuels, and declines in demand for coal for electricity generation, because a significant portion of power-sector coal contracts was entered into during a period of high prices for all fuels. EIA projects average power-sector coal price of $2.18 per million Btu for September 2009 which represents the first decline in price from the same month of the prior year since 2002. Projected power-sector coal prices fall over the EIA forecast to about $1.95 per million Btu in December 2010.

| Energy Dimensions, LLC | Confidential | 3 of 11 |

Five surface and one underground mine produced 43.4 million short tons of mostly sub-bituminous coal in 2007, ranking Montana 5th in State production behind WY, WV, KY and PA. Montana’s reserve base of 119 billion tons represents approximately a quarter of the total U.S. coal reserve base and ranks it first in ahead of IL, WY and WV.

| Big Horn and Rosebud were Montana’s leading producing counties with 30.4 and 12.6 million tons respectively. The two major productive seams are Anderson-Dietz with a production of 20.5 million tons and Rosebud with 16.9 million tons production and average thickness of 22 feet. Over 60% of Montana’s production by volume is under union status. Employment from coal production in Montana is around 1,000. | |

| 6. | Key Regional Competitors |

The major Montana coal players are Rio Tinto Americas (Spring Creek Mine, Decker Mine 50%), and Westmoreland Coal Company (Rosebud, Absaloka and Savage Mines).

| Company | Mine | Production | Reserve | Coal | Seam | Operations |

| Rio Tinto Americas | Spring Creek | 15.7 million | 290 million | 9,350 Btu 0.34 % sulfur | 80 feet 0.7 - 2.8 | 4 surface pits on 6,700 acres |

| Westmoreland Coal Company | Rosebud, Colstrip | 13.1 million | 205 million | 8,500 Btu 0.74 % sulfur | | 3 surface pits, 25,000 acres |

| Rio Tinto (50%) Level 3 (50%) | Decker, Decker | 7.0 million | 200 million | 9,500 Btu 0.40 % sulfur | 15 - 52 feet | 7,000 acres |

| Westmoreland Coal Company | Absaloka, Hardin | 6.4 million | 81 million | 8,700 Btu 0.68 % sulfur | | 1 surface pit on 15,00 acres |

| Westmoreland Coal Company | Savage, Sidney | 0.36 million | 7 million | 6,550 Btu 0.55 % sulfur | | 1 surface pit on 900 acres |

| First Energy & Boich | Bull Mountain | 0.05 million | 800 million | 10,400 Btu 0.55 % sulfur | 9 – 17 feet | Underground, 1 cont. miner |

Source: Platts, EIA, Rio Tinto Americas, Westmoreland Energy, Bull Mountain

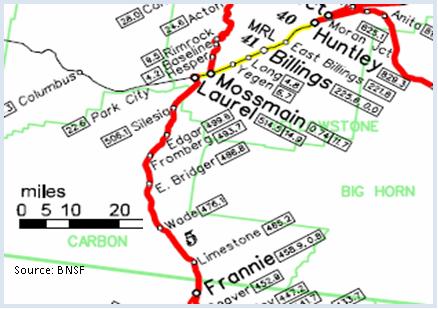

The chart depicts the major Montana and Wyoming coal mines and their location with respect to BNSF rail routes. Montana coal realized an average price of $11.80 per ton in 2007. We estimate that operating cost are in the $8 - $10 per ton range, as with similar Powder River Basin operations which are based on large scale surface operations.

| Energy Dimensions, LLC | Confidential | 4 of 11 |

| 7. | Competitive Price Analysis of Bridger-Fromberg Coal |

Bridger-Fromberg coal competes domestically on heat and sulfur specs (11,000 to 12,000 Btu and <1% respectively) most closely with other underground operations in Montana (Carpenter Creek, Bull Mountain), Colorado (Elk Creek, West Elk, Twentymile, Colowyo, Trapper, Bowie, King Coal, NM) and Utah (Aberdeen, Bear Canyon, Crandall Canyon, Deer Creek, Dugout Canyon, Sufco, West Ridge).

International competition with similar specs is seaborne steam coal from Colombia (Bolivar), South Africa (Richards Bay) and Australia (Newcastle).

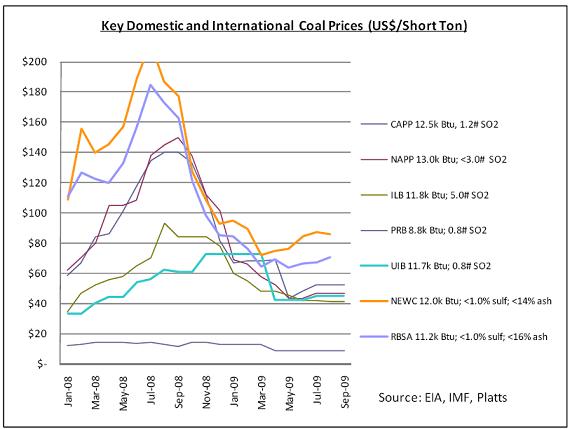

The chart depicts coal prices over the past 18 months in major producing basins with a focus on the Uinta Basin (Colorado), Newcastle FOB and Richards Bay FOB. It highlights the highs of summer 2008 and the lows of spring 2009, with a gradual recovery in the past 5 months. At $45/short ton Colorado coal runs about $40 below Newcastle, which in turn commands approximately a $10 premium over Richards Bay.

| Energy Dimensions, LLC | Confidential | 5 of 11 |

7a. Domestic Pricing and Netbacks

The domestic markets for which Bridger-Fromberg coal has a transportation advantage over Colorado or Utah sourced coal are near the Lake Superior regions of Wisconsin, Minnesota and upstate Michigan that are not served by higher sulfur Illinois Basin coal. The map shows major coal flows from the Western U.S. coal basins heading mostly east on BNSF. For domestic consumption B-F coal would have to be priced an estimated $5 to $10/st below Colorado UIB coal to be competitive. Current Colorado prices are $45/st, with a high of $73/st at the beginning of the year, and a low of $42 this spring. B-F coal could be competitive domestically if $40/st for Colorado coal proves to be a bottom. Current Colorado price outlooks are $40/st trending towards $50 in 2013. Current netback prices for B-F coal could be $35 to $40/st, trending upward. At this netback price B-F production cost would have to come in at or below $30/st, which can be achieved in a modern longwall operation.

7b. International Pricing and Netbacks

The map also points to the geographic advantage Billings would have for any West Coast export play. Pacific Northwest FOB pricing should be less than Newcastle but above Richards Bay due to the distances to coastal China, which falls between the two. At current prices Pacific Northwest FOB should be around $75/short ton – converted from the internationally quoted metric ton to allow comparability with domestic netbacks. Shipping Bridger-Fromberg coal on BNSF to either Portland, OR; Seattle, WA; or Vancouver, BC at an estimated 2.0 cents/ton-mile should add approximately $20/t freight.

| From | To | Distance |

| Newcastle, Australia | Shanghai | 4,850 miles |

| Seattle, WA, U.S.A. | Shanghai | 5,700 miles |

| Richards Bay, South Africa | Shanghai | 7,180 miles |

| Energy Dimensions, LLC | Confidential | 6 of 11 |

7c. Value Chain Costs and Netbacks

A first-order value chain assessment is needed to evaluate the attractiveness of a domestic versus international sales strategy. Cost estimates are based on similar longwall operations at a production scale above 4 million tons per year. Coal removal, preparation and loading costs are cash cost (including taxes and royalties) plus an added DD&A charge. Rail transport is based on 2.0 cents/ton-mile to Pacific Northwest ports plus a port handling charge.

The value chain assessment indicates that Bridger-Fromberg coal could marginally compete in the domestic market with a $35 – 40/short ton netback, and very little room for error.

B-F coal could however reach Pacific Northwest ports for $52 – 64/st FOB, which would allow at current benchmark prices for a margin of $10 – 20/st. Shipping to Chinese coastal demand centers would add another $20 – 30/st in freight cost. While an important driver of overall cost of seaborne coal and impacting demand, shipping freight can be neglected here in this FOB netback evaluation.

| Strategy | Cost | Netback Benchmark | Netback Adjm. | Netb. Margin |

| Structure Long Term Domestic Contract | $31-39/st | $45/st UIB Col | -$5-10/st | +/- $5/st |

| Partner with Asian Player and Export to Asia via Pacific Northwest | $52-64/st | $87/st NEWC FOB $67/st RBSA FOB | -$10/st +$10/st | +$13-25/st |

This initial assessment confirms the ingoing hypothesis that the Asian export strategy could yield a superior margin over the domestic sales strategy, indicating a rank order of preference to be considered later in developing the strategies.

| 8. | Bridger-Fromberg Project Strengths, Weaknessess, Opportunities and Threats (SWOT) Assessment |

While the opportunities are there, the weaknesses and threats to the project are as well. The basic strategy for MMEX should be to leverage the project’s strengths and opportunities to the highest degree possible while overcoming the weaknesses and mitigating the threats. Any sale or other form of successful financial exit needs to prove a tangible value-add by the MMEX team through an end-to-end (mine to customer) business plan.

| Energy Dimensions, LLC | Confidential | 7 of 11 |

The following two-by-two matrix attempts to summarize all key strengths and weaknesses as well as key opportunities and threats that characterize this project and will need to be considered in developing strategies and action plans:

Strengths · Large and contiguous reserve · Relatively high Btu · Relatively low sulfur, ash and moisture · 5 miles to BNSF rail line | Weaknesses · Insufficient geologic data · Weak lease control · Likely underground operation · Significant capital investment for underground · Relatively high royalty rate for underground · Management team not assembled |

Opportunities · Positive netback as seaborne export play · Partner with Asian player and export · Long term domestic contract · Large scale coal conversion project? · Low cost underground - longwall potential? · Underground coal gasification? | Threats · Marginal domestic netback vs. competing coals · Weakening U.S. coal demand: 2009 < 1 billion tons · Low cost surface competitors at $8 – 10 per ton · Formidable competitors: Rio Tinto, Westmoreland · Bull Mountain / First Energy in start-up phase · Carpenter Creek – further advanced project stage · Coal upgrading projects in the PRB taking 8,500 Btu coal to 11,000 and above – at a cost |

| 9. | Strategic Options and Action Plans |

9a. Partner with Asian Player(s) and Export to Asia

Given surging demand in China and India resulting in an attractive export netback with upside potential and concurrent stagnation in domestic markets, a Western export play seems currently attractive and opportunistic.

This strategy would leverage some of the project’s strengths and opportunities and translate them into selling features for an Asian buyer:

| | · | Higher Btu coal travels further, putting the Bridger-Fromberg reserve as a top candidate for Western U.S. coals with export potential |

| | · | Large and contiguous reserves invite long-term contracts and facilitate capital investment |

| | · | Lower sulfur, ash and moisture will play to the need for cleaner coal, particularly in China |

| | · | Relative proximity to BNSF rail line will satisfy initial logistics scrutiny |

| Energy Dimensions, LLC | Confidential | 8 of 11 |

The strategy would also benefit from specific capabilities MMEX could bring to bear in form of:

| | · | Board members with extensive Chinese coal and energy contacts and |

| | · | Management team members with expertise in global coal market dynamics and energy players as partners |

The threat from existing low-cost operations and potential upgraded PRB coal would need to be countered by the higher Btu value and the prospect of a low-cost underground operation. This requirement is synonimous with large-scale longwall mining technology. China is leading the world in installed longwall mine operations, the production of longwall mining equipment, and the corresponding expertise. A Chinese partner with the technology and expertise or good access to it would help diminish one of the key threats (cost) for this project. As much of the capital investment for operation start-up would be tied in the longwall equipment itself, this strategy would also diminish the need to raise additional capital.

The following table summarizes the weakness and threats which are adressed through the export stategy (green) and the ones that would still need to be addressed (red):

Weaknesses · Insufficient geologic data · Weak lease control · Likely underground operation · Significant capital investment for underground · Relatively high royalty rate for underground · Management team not assembled | Need to be, or are Addressed Through: Additional geologic surveying prior to partnering Strengthen lease control by adding to 50,000 acres Low-cost answer to underground operation Partner bring capital equipment and expertise Renegotiate prior or after partnering Assemble basic management team |

Threats · Marginal domestic netback vs. competing coals · Weakening U.S. coal demand: 2009 < 1 billion tons · Low cost surface competitors at $8 – 10 per ton · Formidable competitors: Rio Tinto, Westmoreland · Bull Mountain / First Energy in start-up phase · Carpenter Creek – further advanced project stage · Coal upgrading projects in the PRB taking 8,500 Btu coal to 11,000 and above – at a cost | Need to be, or are Addressed Through: Avoids domestic netback competition Exporting into strengthening Asian demand Low cost underground ops and high Btu Need to study their export potential Bull Mountain is locked up with First Energy Need to closely monitor their strategy If cost and capital are managed, project should be competitive with upgrading technology |

The single most critical item will be to find one or more Asian partners to back the project with. Initial identification of these potential partners will kick-off phase I. Contacting and negotiations will likely be the most uncertain item in phase I with respect to timing. This action item however will need additional ground- and prep-work completed in order to have a credible and solid negotiating foundation. This ground work includes additional geologic data, competitor monitoring, logistics chain assessment, first cut mine plan and first cut capital and operations plans.

An action plan to pursue the Asian export strategy could therefore be as follows:

| Energy Dimensions, LLC | Confidential | 9 of 11 |

9a Phase I: Prior to Partner Agreement –

| 1. | Board and management team to draw up a list of potential partners and customers in China and/or rest of Asia – MMEX team |

| 2. | Improve geologic survey data – Engineering consultants |

| 3. | Study strategies of current MT and PRB producers and new entrants – MMEX team |

| 4. | Evaluate rail and port options and their price per ton and capital investment needed (rail spur, coal handling facilities, etc) – MMEX team with BNSF |

| 5. | Develop first cut mine plan – Engineering consultants |

| 6. | Develop capital and operations plan (longwall) for project – MMEX team and consultants |

| 7. | Contact potential partners in Asia and begin negotiations – MMEX team |

| 8. | Begin negotiation for additional leaseholds and royalties – MMEX team |

| 9. | Identify capabilities needed to recruit appropriate management talent – MMEX team |

9b. Structure Long-Term Contract with Domestic Off-Taker

While the domestic outlook for coal demand is currently depressed and overshadowed by impending carbon regulation, some utilities have chosen to make long term coal off-take commitments in the past 12 to 18 months. First Energy’s acquisition of the Bull Mountain Mine and Duke Energy’s long term contract with Peabody Energy backing the opening of its new Bear Run surface mine in Indiana are two prominent examples.

For long term contracts utilities will weigh price considerations as high as security of supply and longevity of reserve, which would support Bridger-Fromberg. This strategic path would identify other coal-heavy utilities and power generators that have continued to bet on coal and have not yet made large off-take commitment. These players include AEP, Southern, NRG, and Ameren.

Some of the action items for phase I of this strategy would look similar to the Asian export strategy. The biggest difference is that longwall or other mining expertise and the associated capital would not be provided by the partner. The exit strategy would therefore be to mature the project to the highest degree possible with MMEX’s limited resources and then sell it to a utility, power generator, or coal company.

The following table summarizes the weakness and threats which are adressed through the domestic off-take stategy (green) and the ones that would still need to be addressed (red):

| Energy Dimensions, LLC | Confidential | 10 of 11 |

Weaknesses · Insufficient geologic data · Weak lease control · Likely underground operation · Significant capital investment for underground · Relatively high royalty rate for underground · Management team not assembled | Need to be, or are Addressed Through: Additional geologic surveying prior to partnering Strengthen lease control by adding to 50,000 acres Low-cost answer to underground operation May need to raise some capital for initial equipment Renegotiate prior or after partnering Assemble basic management team |

Threats · Marginal domestic netback vs. competing coals · Weakening U.S. coal demand: 2009 < 1 billion tons · Low cost surface competitors at $8 – 10 per ton · Formidable competitors: Rio Tinto, Westmoreland · Bull Mountain / First Energy in start-up phase · Carpenter Creek – further advanced project stage · Coal upgrading projects in the PRB taking 8,500 Btu coal to 11,000 and above – at a cost | Need to be, or are Addressed Through: Will play negatively into reserve/ project valuation Strong competition for new long term contracts Low cost underground ops and high Btu Are more dependent on domestic expansion Bull Mountain is locked up with First Energy Need to closely monitor their strategy If cost and capital are managed, project should be competitive with upgrading technology |

9 b Phase I: Set up for Domestic Contract

| 1. | Management team to draw up a list of potential long term offtakers – MMEX team |

| 2. | Improve geologic survey data – Engineering consultants |

| 3. | Study strategies of current MT and PRB producers and new entrants – MMEX team |

| 4. | Evaluate rail and port options and their price per ton and capital investment needed (rail spur, coal handling facilities, etc) – MMEX team with BNSF |

| 5. | Develop first cut mine plan – Engineering consultants |

| 6. | Develop capital and operations plan (longwall) for project – MMEX team and consultants |

| 7. | Contact domestic players and begin negotiations – MMEX team |

| 8. | Begin negotiation for additional leaseholds and royalties – MMEX team |

| 9. | Identify capabilities needed to recruit appropriate management talent – MMEX team |

9c. Joint Tier 1 and Tier 2 Action Plan

7 out of 9 action items for the domestic off-take strategy are similar to the Asian export strategy, although the payout is likely to be lower and the hurdles higher. Given this large overlap of action items it would be most efficient to pursue both strategies simultaneously. A large-scale mine-mouth coal conversion project or an underground coal gasification project would rank in the third tier in terms of chances for success and should be put on a back-burner for the time being.

| Tier | Strategy | Margin | Execution |

| 1 | Partner with Asian Player and Export to Asia | +$13-25/st | Pursue simultaneously for the first 3 – 6 months |

| 2 | Structure Long Term Domestic Contract | +/- $5/st |

| 3 | a)Large-scale Coal Conversion Project b)Underground Coal Gasification Project | | Put on hold but monitor for new information and opportunities |

| Energy Dimensions, LLC | Confidential | 10 of 11 |