QuickLinks -- Click here to rapidly navigate through this document

As filed with the Securities and Exchange Commission on September 15, 2008

Registration No. 333-153004

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1 to

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

First Data Corporation

(Exact name of registrant issuer as specified in its charter)

SEE TABLE OF ADDITIONAL REGISTRANTS

| Delaware (State or other jurisdiction of incorporation) | 6199 (Primary Standard Industrial Classification Code Number) | 47-0731996 (I.R.S. Employer Identification Number) |

6200 South Quebec Street

Greenwood Village, Colorado 80111

(303) 967-8000

(Address, including zip code, and telephone number, including area code, of registrants' principal executive offices)

David R. Money

First Data Corporation

Executive Vice President, General Counsel and Secretary

6200 South Quebec Street

Greenwood Village, Colorado 80111

(303) 967-8000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With a copy to:

Richard A. Fenyes, Esq.

Simpson Thacher & Bartlett LLP

425 Lexington Avenue

New York, New York 10017-3954

Telephone: (212) 455-2000

Approximate date of commencement of proposed exchange offer:

As soon as practicable after this Registration Statement is declared effective.

If the securities being registered on this form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, please check the following box. o

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of "large accelerated filer," "accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) | Smaller reporting company o |

The Registrants hereby amend this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrants shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Additional Registrant Guarantors

| Exact Name of Registrant Guarantor as Specified in its Charter (or Other Organizational Document) | State or Other Jurisdiction of Incorporation or Organization | I.R.S. Employer Identification Number | Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant Guarantor's Principal Executive Offices | |||

|---|---|---|---|---|---|---|

Achex, Inc. | Delaware | 94-3338768 | 6200 South Quebec Street Greenwood Village, Colorado 80111 (303) 967-8000 | |||

Atlantic Bankcard Properties Corporation | North Carolina | 56-0927587 | 6200 South Quebec Street | |||

Atlantic States Bankcard Association, Inc. | Delaware | 47-0765184 | 6200 South Quebec Street | |||

B1 PTI Services, Inc. | Delaware | 58-2517182 | 6200 South Quebec Street | |||

Bankcard Investigative Group Inc. | Delaware | 58-2368158 | 6200 South Quebec Street | |||

Business Office Services, Inc. | Delaware | 62-1571233 | 6200 South Quebec Street | |||

BUYPASS Inco Corporation | Delaware | 51-0362700 | 6200 South Quebec Street | |||

Call Interactive Holdings LLC | Delaware | 45-0492144 | 6200 South Quebec Street | |||

CallTeleservices, Inc. | Nebraska | 58-2462499 | 6200 South Quebec Street | |||

Cardservice Delaware, Inc. | Delaware | 73-1631637 | 6200 South Quebec Street |

| Exact Name of Registrant Guarantor as Specified in its Charter (or Other Organizational Document) | State or Other Jurisdiction of Incorporation or Organization | I.R.S. Employer Identification Number | Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant Guarantor's Principal Executive Offices | |||

|---|---|---|---|---|---|---|

Cardservice International, Inc. | California | 95-4207932 | 6200 South Quebec Street Greenwood Village, Colorado 80111 (303) 967-8000 | |||

CESI Holdings, Inc. | Delaware | 11-3145051 | 6200 South Quebec Street | |||

CIFS Corporation | Delaware | 01-0593914 | 6200 South Quebec Street | |||

CIFS LLC | Delaware | 75-2984066 | 6200 South Quebec Street | |||

Concord Computing Corporation | Delaware | 36-3833854 | 6200 South Quebec Street | |||

Concord Corporate Services, Inc. | Delaware | 23-2709591 | 6200 South Quebec Street | |||

Concord EFS Financial Services, Inc. | Delaware | 01-0757630 | 6200 South Quebec Street | |||

Concord EFS, Inc. | Delaware | 04-2462252 | 6200 South Quebec Street | |||

Concord Emerging Technologies, Inc. | Arizona | 86-0837769 | 6200 South Quebec Street | |||

Concord Equipment Sales, Inc. | Tennessee | 62-1479971 | 6200 South Quebec Street | |||

Concord Financial Technologies, Inc. | Delaware | 13-4064184 | 6200 South Quebec Street |

| Exact Name of Registrant Guarantor as Specified in its Charter (or Other Organizational Document) | State or Other Jurisdiction of Incorporation or Organization | I.R.S. Employer Identification Number | Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant Guarantor's Principal Executive Offices | |||

|---|---|---|---|---|---|---|

Concord NN, LLC | Delaware | 01-0757616 | 6200 South Quebec Street Greenwood Village, Colorado 80111 (303) 967-8000 | |||

Concord One, LLC | Delaware | 01-0757619 | 6200 South Quebec Street | |||

Concord Payment Services, Inc. | Georgia | 58-1495598 | 6200 South Quebec Street | |||

Concord Processing, Inc. | Delaware | 57-1143159 | 6200 South Quebec Street | |||

Concord Transaction Services, LLC | Colorado | 20-0187517 | 6200 South Quebec Street | |||

Credit Performance Inc. | Delaware | 47-0789664 | 6200 South Quebec Street | |||

CTS Holdings, LLC | Colorado | 20-0675870 | 6200 South Quebec Street | |||

CTS, Inc. | Tennessee | 52-2251178 | 6200 South Quebec Street | |||

DDA Payment Services, LLC | Delaware | 20-0941440 | 6200 South Quebec Street | |||

DW Holdings, Inc. | Delaware | 20-8394043 | 6200 South Quebec Street | |||

EFS Transportation Services, Inc. | Tennessee | 62-1830443 | 6200 South Quebec Street |

| Exact Name of Registrant Guarantor as Specified in its Charter (or Other Organizational Document) | State or Other Jurisdiction of Incorporation or Organization | I.R.S. Employer Identification Number | Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant Guarantor's Principal Executive Offices | |||

|---|---|---|---|---|---|---|

EFTLogix, Inc. | Nevada | 86-0885804 | 6200 South Quebec Street Greenwood Village, Colorado 80111 (303) 967-8000 | |||

EPSF Corporation | Delaware | 51-0380978 | 6200 South Quebec Street | |||

FDC International Inc. | Delaware | 58-2293393 | 6200 South Quebec Street | |||

FDFS Holdings, LLC | Delaware | 84-1564482 | 6200 South Quebec Street | |||

FDGS Holdings General Partner II, LLC | Delaware | 83-0346356 | 6200 South Quebec Street | |||

FDGS Holdings, LLC | Delaware | 58-2574166 | 6200 South Quebec Street | |||

FDGS Holdings, LP | Delaware | 58-2582293 | 6200 South Quebec Street | |||

FDMS Partner, Inc. | Delaware | 73-1638409 | 6200 South Quebec Street | |||

FDR Interactive Technologies Corporation | New York | 22-2915649 | 6200 South Quebec Street | |||

FDR Ireland Limited | Delaware | 98-0122368 | 6200 South Quebec Street | |||

FDR Limited | Delaware | 98-0122367 | 6200 South Quebec Street |

| Exact Name of Registrant Guarantor as Specified in its Charter (or Other Organizational Document) | State or Other Jurisdiction of Incorporation or Organization | I.R.S. Employer Identification Number | Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant Guarantor's Principal Executive Offices | |||

|---|---|---|---|---|---|---|

FDR Missouri Inc. | Delaware | 47-0772712 | 6200 South Quebec Street Greenwood Village, Colorado 80111 (303) 967-8000 | |||

FDR Signet Inc. | Delaware | 58-2266420 | 6200 South Quebec Street | |||

FDR Subsidiary Corp. | Delaware | 47-0839789 | 6200 South Quebec Street | |||

First Data Aviation LLC | Delaware | 75-2977653 | 6200 South Quebec Street | |||

First Data Capital, Inc. | Delaware | 58-2436936 | 6200 South Quebec Street | |||

First Data Card Solutions, Inc. | Maryland | 75-1300913 | 6200 South Quebec Street | |||

First Data Commercial Services Holdings, Inc. | Delaware | 20-5626772 | 6200 South Quebec Street | |||

First Data Communications Corporation | Delaware | 22-2991933 | 6200 South Quebec Street | |||

First Data Digital Certificates Inc. | Delaware | 58-2508132 | 6200 South Quebec Street | |||

First Data Financial Services, L.L.C. | Delaware | 76-0561084 | 6200 South Quebec Street | |||

First Data Government Solutions, Inc. | Delaware | 59-2957887 | 6200 South Quebec Street |

| Exact Name of Registrant Guarantor as Specified in its Charter (or Other Organizational Document) | State or Other Jurisdiction of Incorporation or Organization | I.R.S. Employer Identification Number | Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant Guarantor's Principal Executive Offices | |||

|---|---|---|---|---|---|---|

First Data Government Solutions, LLC | Delaware | 58-2583070 | 6200 South Quebec Street Greenwood Village, Colorado 80111 (303) 967-8000 | |||

First Data Government Solutions, LP | Delaware | 58-2582959 | 6200 South Quebec Street | |||

First Data Integrated Services Inc. | Delaware | 47-0772477 | 6200 South Quebec Street | |||

First Data Latin America Inc. | Delaware | 47-0789663 | 6200 South Quebec Street | |||

First Data Merchant Services Corporation | Florida | 59-2126793 | 6200 South Quebec Street | |||

First Data Merchant Services Northeast, LLC | Delaware | 11-3383565 | 6200 South Quebec Street | |||

First Data Merchant Services Southeast, L.L.C. | Delaware | 11-3301903 | 6200 South Quebec Street | |||

First Data Mobile Holdings, Inc. | Delaware | 20-5449819 | 6200 South Quebec Street | |||

First Data Payment Services, LLC | Delaware | 26-0359308 | 6200 South Quebec Street | |||

First Data Pittsburgh Alliance Partner Inc. | Delaware | 11-3343001 | 6200 South Quebec Street | |||

First Data PS Acquisition Inc. | Delaware | 20-5449746 | 6200 South Quebec Street |

| Exact Name of Registrant Guarantor as Specified in its Charter (or Other Organizational Document) | State or Other Jurisdiction of Incorporation or Organization | I.R.S. Employer Identification Number | Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant Guarantor's Principal Executive Offices | |||

|---|---|---|---|---|---|---|

First Data Real Estate Holdings L.L.C. | Delaware | 84-1593311 | 6200 South Quebec Street Greenwood Village, Colorado 80111 (303) 967-8000 | |||

First Data Resources, LLC | Delaware | 47-0535472 | 6200 South Quebec Street | |||

First Data Retail ATM Services L.P. | Texas | 01-0757624 | 6200 South Quebec Street | |||

First Data Secure LLC | Delaware | 47-0902841 | 6200 South Quebec Street | |||

First Data Solutions L.L.C. | Delaware | 41-2032686 | 6200 South Quebec Street | |||

First Data Technologies, Inc. | Delaware | 04-3125703 | 6200 South Quebec Street | |||

First Data Voice Services | Delaware | 22-2915646 | 6200 South Quebec Street | |||

First Data, L.L.C. | Delaware | Not applicable | 6200 South Quebec Street | |||

FSM Services Inc. | Delaware | 58-2517180 | 6200 South Quebec Street | |||

FundsXpress Financial Network, Inc. | Texas | 74-2830594 | 6200 South Quebec Street | |||

FundsXpress, Inc. | Delaware | 74-2935781 | 6200 South Quebec Street |

| Exact Name of Registrant Guarantor as Specified in its Charter (or Other Organizational Document) | State or Other Jurisdiction of Incorporation or Organization | I.R.S. Employer Identification Number | Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant Guarantor's Principal Executive Offices | |||

|---|---|---|---|---|---|---|

FX Securities, Inc. | Delaware | 74-2943569 | 6200 South Quebec Street Greenwood Village, Colorado 80111 (303) 967-8000 | |||

Gibbs Management Group, Inc. | Georgia | 58-1791876 | 6200 South Quebec Street | |||

Gift Card Services, Inc. | Oklahoma | 73-1483616 | 6200 South Quebec Street | |||

Gratitude Holdings LLC | Delaware | 41-2077284 | 6200 South Quebec Street | |||

H & F Services, Inc. | Tennessee | 62-1646207 | 6200 South Quebec Street | |||

ICVerify Inc. | Delaware | Not applicable | 6200 South Quebec Street | |||

IDLogix, Inc. | Delaware | 71-0914684 | 6200 South Quebec Street | |||

Initial Merchant Services, LLC | Delaware | Not applicable | 6200 South Quebec Street | |||

Instant Cash Services, LLC | Delaware | 30-0412561 | 6200 South Quebec Street | |||

Intelligent Results, Inc. | Washington | 91-2113799 | 6200 South Quebec Street | |||

IPS Holdings Inc. | Delaware | 58-2496617 | 6200 South Quebec Street |

| Exact Name of Registrant Guarantor as Specified in its Charter (or Other Organizational Document) | State or Other Jurisdiction of Incorporation or Organization | I.R.S. Employer Identification Number | Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant Guarantor's Principal Executive Offices | |||

|---|---|---|---|---|---|---|

IPS Inc. | Colorado | 58-2615237 | 6200 South Quebec Street Greenwood Village, Colorado 80111 (303) 967-8000 | |||

JOT, Inc. | Nevada | 86-0882455 | 6200 South Quebec Street | |||

Linkpoint International, Inc. | Nevada | 95-4704661 | 6200 South Quebec Street | |||

LoyaltyCo LLC | Delaware | Not applicable | 6200 South Quebec Street | |||

MAS Inco Corporation | Delaware | 51-0362703 | 6200 South Quebec Street | |||

MAS Ohio Corporation | Delaware | 52-2139525 | 6200 South Quebec Street | |||

Money Network Financial, LLC | Delaware | 36-4483540 | 6200 South Quebec Street | |||

National Payment Systems Inc. | New York | 13-3789541 | 6200 South Quebec Street | |||

New Payment Services, Inc. | Georgia | 20-3848972 | 6200 South Quebec Street | |||

NPSF Corporation | Delaware | 52-2251181 | 6200 South Quebec Street | |||

PayPoint Electronic Payment Systems, LLC | Delaware | 82-0569438 | 6200 South Quebec Street |

| Exact Name of Registrant Guarantor as Specified in its Charter (or Other Organizational Document) | State or Other Jurisdiction of Incorporation or Organization | I.R.S. Employer Identification Number | Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant Guarantor's Principal Executive Offices | |||

|---|---|---|---|---|---|---|

PaySys International, Inc. | Florida | 59-2061461 | 6200 South Quebec Street Greenwood Village, Colorado 80111 (303) 967-8000 | |||

POS Holdings, Inc. | California | 94-3312834 | 6200 South Quebec Street | |||

QSAT Financial, LLC | Delaware | 91-1766549 | 6200 South Quebec Street | |||

REMITCO LLC | Delaware | 82-0580864 | 6200 South Quebec Street | |||

Sagebrush Holdings Inc. | Delaware | 75-3097583 | 6200 South Quebec Street | |||

Sagetown Holdings Inc. | Delaware | 75-3097496 | 6200 South Quebec Street | |||

Sageville Holdings LLC | Delaware | 68-0546814 | 6200 South Quebec Street | |||

Shared Global Systems, Inc. | Texas | 76-0352456 | 6200 South Quebec Street | |||

Size Technologies, Inc. | California | 94-3329671 | 6200 South Quebec Street | |||

Southern Telecheck, Inc. | Louisiana | 72-0780470 | 6200 South Quebec Street | |||

Star Networks, Inc. | Delaware | 59-3558624 | 6200 South Quebec Street |

| Exact Name of Registrant Guarantor as Specified in its Charter (or Other Organizational Document) | State or Other Jurisdiction of Incorporation or Organization | I.R.S. Employer Identification Number | Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant Guarantor's Principal Executive Offices | |||

|---|---|---|---|---|---|---|

Star Processing, Inc. | Delaware | 23-2696693 | 6200 South Quebec Street Greenwood Village, Colorado 80111 (303) 967-8000 | |||

Star Systems Assets, Inc. | Delaware | 33-0886220 | 6200 South Quebec Street | |||

Star Systems, Inc. | Delaware | 59-3558623 | 6200 South Quebec Street | |||

Star Systems, LLC | Delaware | 33-0886218 | 6200 South Quebec Street | |||

Strategic Investment Alternatives LLC | Delaware | 01-0716816 | 6200 South Quebec Street | |||

SurePay Real Estate Holdings, Inc. | Delaware | 58-2615240 | 6200 South Quebec Street | |||

SY Holdings, Inc. | Delaware | 83-0337977 | 6200 South Quebec Street | |||

TASQ Corporation | Delaware | 84-1581144 | 6200 South Quebec Street | |||

TASQ Technology, Inc. | California | 68-0345149 | 6200 South Quebec Street | |||

Taxware, LLC | Delaware | 68-0537213 | 6200 South Quebec Street | |||

Technology Solutions International, Inc. | Georgia | 58-1953753 | 6200 South Quebec Street |

| Exact Name of Registrant Guarantor as Specified in its Charter (or Other Organizational Document) | State or Other Jurisdiction of Incorporation or Organization | I.R.S. Employer Identification Number | Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant Guarantor's Principal Executive Offices | |||

|---|---|---|---|---|---|---|

TeleCheck Acquisition LLC | Delaware | 46-0478631 | 6200 South Quebec Street Greenwood Village, Colorado 80111 (303) 967-8000 | |||

TeleCheck Acquisition-Michigan, LLC | Delaware | Not applicable | 6200 South Quebec Street | |||

TeleCheck Holdings, Inc. | Georgia | 58-1922310 | 6200 South Quebec Street | |||

TeleCheck International, Inc. | Georgia | 58-2014182 | 6200 South Quebec Street | |||

TeleCheck Pittsburgh/West Virginia, Inc. | Pennsylvania | 25-1405316 | 6200 South Quebec Street | |||

TeleCheck Services, Inc. | Delaware | 58-2035074 | 6200 South Quebec Street | |||

Transaction Solutions Holdings, Inc. | Delaware | 73-1650437 | 6200 South Quebec Street | |||

Transaction Solutions, LLC | Delaware | 82-0547328 | 6200 South Quebec Street | |||

Unibex, LLC | Delaware | 20-0686414 | 6200 South Quebec Street | |||

Unified Merchant Services | Georgia | 58-2169129 | 6200 South Quebec Street | |||

Unified Partner, Inc. | Delaware | 73-1638403 | 6200 South Quebec Street |

| Exact Name of Registrant Guarantor as Specified in its Charter (or Other Organizational Document) | State or Other Jurisdiction of Incorporation or Organization | I.R.S. Employer Identification Number | Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant Guarantor's Principal Executive Offices | |||

|---|---|---|---|---|---|---|

ValueLink, LLC | Delaware | 20-0055795 | 6200 South Quebec Street Greenwood Village, Colorado 80111 (303) 967-8000 | |||

Virtual Financial Services, LLC | Delaware | 84-1596983 | 6200 South Quebec Street | |||

Yclip, LLC | Delaware | 47-0900299 | 6200 South Quebec Street |

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities, and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED SEPTEMBER 15, 2008

PRELIMINARY PROSPECTUS

FIRST DATA CORPORATION

Offer to Exchange (the "Exchange Offer")

$2,200,000,000 aggregate principal amount of its 97/8% Senior Notes due 2015 (the "exchange notes"), which have been registered under the Securities Act of 1933, as amended (the "Securities Act") for any and all of its outstanding 97/8% Senior Notes dues 2015 (the "outstanding notes").

We are conducting the exchange offer in order to provide you with an opportunity to exchange your unregistered outstanding notes for freely tradable notes that have been registered under the Securities Act.

The Exchange Offer

- •

- We will exchange all outstanding notes that are validly tendered and not validly withdrawn for an equal principal amount of exchange notes that are freely tradable.

- •

- You may withdraw tenders of outstanding notes at any time prior to the expiration date of the exchange offer.

- •

- The exchange offer expires at 11:59 p.m., New York City time, on , 2008, unless extended. We do not currently intend to extend the expiration date.

- •

- The exchange of outstanding notes for exchange notes in the exchange offer will not be a taxable event for U.S. federal income tax purposes.

- •

- The terms of the exchange notes to be issued in the exchange offer are substantially identical to the outstanding notes, except that the exchange notes will be freely tradable.

Results of the Exchange Offer

- •

- The exchange notes may be sold in the over-the-counter market, in negotiated transactions or through a combination of such methods. We do not plan to list the notes on a national market.

All untendered outstanding notes will continue to be subject to the restrictions on transfer set forth in the outstanding notes and in the indenture. In general, the outstanding notes may not be offered or sold, unless registered under the Securities Act, except pursuant to an exemption from, or in a transaction not subject to, the Securities Act and applicable state securities laws. Other than in connection with the exchange offer, we do not currently anticipate that we will register the outstanding notes under the Securities Act.

See "Risk Factors" beginning on page 12 for a discussion of certain risks that you should consider before participating in the exchange offer.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the exchange notes to be distributed in the exchange offer or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2008.

You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with different information. The prospectus may be used only for the purposes for which it has been published, and no person has been authorized to give any information not contained herein. If you receive any other information, you should not rely on it. We are not making an offer of these securities in any state where the offer is not permitted.

| | Page | |

|---|---|---|

Prospectus Summary | 1 | |

Risk Factors | 12 | |

Forward-Looking Statements | 29 | |

The Transactions | 30 | |

Use of Proceeds | 35 | |

Capitalization | 35 | |

Unaudited Pro Forma Condensed Consolidated Statement of Operations | 37 | |

Selected Historical Consolidated Financial Data | 43 | |

Management's Discussion and Analysis of Financial Condition and Results of Operations | 46 | |

Business | 121 | |

Management | 146 | |

Executive Compensation | 150 | |

Security Ownership of Certain Beneficial Owners | 177 | |

Certain Relationships and Related Party Transactions | 179 | |

Description of Other Indebtedness | 183 | |

The Exchange Offer | 191 | |

Description of Notes | 201 | |

Certain United States Federal Income Tax Consequences | 261 | |

Certain Erisa Considerations | 267 | |

Plan Of Distribution | 269 | |

Legal Matters | 270 | |

Experts | 270 | |

Available Information | 270 | |

Index to Financial Statements | F-1 |

i

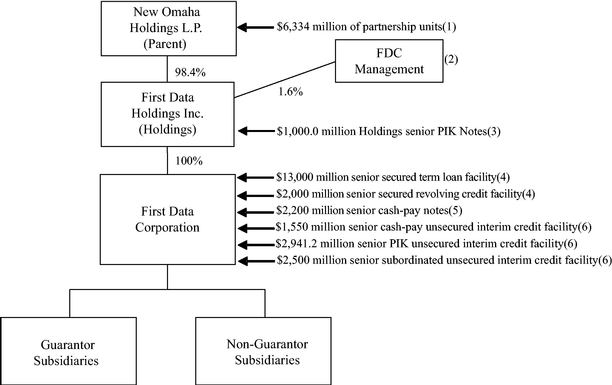

On April 1, 2007, Omaha Acquisition Corp. ("Acquisition Corp."), a Delaware corporation formed by investment funds associated with Kohlberg Kravis Roberts & Co. ("KKR"), entered into an Agreement and Plan of Merger (the "Merger Agreement") with First Data Corporation ("First Data") and New Omaha Holdings L.P. ("Parent") pursuant to which, effective September 24, 2007, Acquisition Corp. merged with and into First Data, with First Data continuing as the surviving corporation and a subsidiary of First Data Holdings, Inc. ("Holdings") (formerly known as New Omaha Holdings Corporation), a Delaware corporation, a newly formed subsidiary of Parent and our parent company (the "Merger"). As a result of the Merger, investment funds associated with or designated by KKR and certain other co-investors indirectly own First Data.

The Merger, the equity investment by the co-investors (described in more detail under "The Transactions"), the initial borrowings under our senior secured credit facilities (described in more detail under "The Transactions"), the offering of the senior PIK notes of Holdings and the contribution of the net proceeds to First Data as common equity (described in more detail under "The Transactions"), the borrowings under First Data's unsecured debt, the repayment of amounts outstanding under our previously existing credit facilities other than certain foreign lines of credit, the tender offers and consent solicitation of our previously existing notes and the payment of related premiums, fees and expenses are collectively referred to in this prospectus as the "Transactions."

In connection with the Transactions, we entered into (i) a senior unsecured interim loan agreement, dated as of September 24, 2007, with Citibank, N.A., as administrative agent, which consists of (a) a $3,750.0 million senior unsecured cash-pay term loan facility with a term of eight years (the "senior cash-pay unsecured interim credit facility") and (b) a $2,750.0 million senior unsecured PIK term loan facility with a term of eight years (the "senior PIK unsecured interim credit facility"), (ii) a senior subordinated unsecured credit loan agreement, dated as of September 24, 2007, with Citibank, N.A., as administrative agent, which consists of a $2,500.0 million senior subordinated unsecured term loan facility with a term of eight and a half years (the "senior subordinated unsecured interim credit facility") and (iii) a $13,000.0 million senior secured term loan facility with a seven-year maturity (the "senior secured credit facilities").

The financial information presented in this prospectus is presented for two periods: Predecessor and Successor, which primarily relate to the periods preceding the Transactions and the period succeeding the Transactions, respectively. The Predecessor period includes results of First Data through September 24, 2007. The Successor period includes the results of operations of Acquisition Corp. for the period prior to the Merger from March 29, 2007 (its formation) through September 24, 2007 (comprised entirely of the change in fair value of certain forward starting, deal contingent interest rate swaps) and includes Post-Merger results of First Data for the period beginning September 25, 2007, including all impacts of purchase accounting.

Financial information identified in this prospectus as "pro forma" gives effect to the Transactions described in this prospectus, as well as the offering of the notes (including the exchange notes).

A substantial portion of our business is conducted through "alliances" with banks and other institutions. Where we discuss the operations of our Merchant Services and International segments, such discussions include our alliances since they generally do not have their own operations (other than certain majority owned and equity method alliances) and are part of our core operations. Our alliance structures take on different forms, including consolidated subsidiaries, equity method investments and revenue sharing arrangements. Under the alliance program, we and a bank or other institution form a joint venture, either contractually or through a separate legal entity. Merchant contracts may be contributed to the venture by us and/or the bank or institution. The banks or other institutions generally provide card association sponsorship, clearing and settlement services. These institutions typically act as a merchant referral source when the institution has an existing banking or other

ii

relationship. We provide transaction processing and related functions. Both owners may provide management, sales, marketing and other administrative services. The alliance structure allows us to be the processor for multiple financial institutions, any one of which may be selected by the merchant as their bank partner.

At June 30, 2008, there were eight affiliates accounted for under the equity method of accounting, comprised of five merchant alliances and three strategic investments in companies in related markets. The majority of equity earnings relate to the Chase Paymentech alliance, our largest merchant alliance. Chase Paymentech is 51% owned by J.P. Morgan Chase Bank, N.A. ("JPMorgan") and 49% owned by us. On May 27, 2008, we announced we had reached an agreement with JPMorgan to end the joint venture, Chase Paymentech Solutions™, a global payments and merchant acquiring entity, by the end of 2008. In the interim, we and JPMorgan will continue to operate the joint venture. After the transition, we and JPMorgan will operate separate payment businesses. We will continue to provide transaction processing and data commerce solutions for allocated merchants through our current technology platforms. We will assume management of the full-service independent sales organization ("ISO") and Agent Bank unit of the joint venture and will integrate 49% of the joint venture's assets and a portion of the joint venture employees into our existing merchant acquiring business. We have historically accounted for our minority interest in the joint venture under the equity method of accounting. After the transition, the portion of the alliance's business retained by us will be reflected on a consolidated basis throughout the financial statements. The information included in this prospectus does not reflect the impact of the end of this joint venture though, on a pro forma basis, it would not be expected to have a material impact on our historical income (loss) from continuing operations.

KKR 2006 Fund L.P. and certain affiliates of the initial purchasers (collectively, the "Equity Investors") made equity contributions to Parent in connection with the closing of the Transactions. In addition, GS Mezzanine Partners VI Fund, L.P. and the Goldman Sachs Group, Inc. purchased $380 million and $620 million, respectively, of senior PIK notes of Holdings in connection with the closing of the Transactions.

Unless the context requires otherwise, in this prospectus, "First Data," "FDC," the "company," "we," "us" and "our" refers to First Data Corporation and its consolidated subsidiaries, both before and after the consummation of the Transactions described herein. References to the "notes" refers to the outstanding $2,200,000,000 aggregate principal amount of its 97/8% Senior Notes due 2015 and the exchange notes.

iii

This summary highlights key aspects of the information contained elsewhere in this prospectus and may not contain all of the information you should consider before investing in the notes. You should read this summary together with the entire prospectus, including the information presented under the heading "Risk Factors" and the information in the unaudited pro forma condensed consolidated financial information and the historical financial statements and related notes appearing elsewhere in this prospectus. For a more complete description of our business, see the "Business" section in this prospectus.

We are a leading provider of electronic commerce and payment solutions for merchants, financial institutions and card issuers globally. We have operations in 37 countries, serving more than 5.4 million merchant locations and more than 2,000 card issuers and their customers. With a wide geographic presence and a broad product offering, we are well-positioned to capitalize on the continued shift from cash and checks to electronic payment transactions.

We have built long-standing relationships with merchants, financial institutions and card issuers globally through superior industry knowledge and high-quality, reliable service. As a result, our revenue is highly diversified across customers, products, geography and distribution channels, with no single customer accounting for more than 3.5% of our 2007 successor or predecessor consolidated revenue (excluding reimbursables). We also enter into alliances with banks and other institutions, increasing our broad geographic coverage and presence in various industries. The contracted and stable nature of our revenue base makes our business highly predictable. Our revenue is recurring in nature, as we typically initially enter into multi-year contracts with our merchant, financial institution and card issuer customers.

Acquisition of InComm Holdings, Inc.

On April 28, 2008, we announced that we had reached an agreement to acquire InComm Holdings Inc. ("InComm") for approximately $980 million consisting of stock in Holdings and approximately $665 million in cash plus contingent future payments of up to $250 million over a three-year performance period based on the performance of our combined stored value business. InComm is a distributor of gift cards, prepaid wireless products, reloadable debit cards, digital music downloads, content, games, software and bill payment solutions. InComm also provides stored value product marketing and technology solutions to international markets in Europe and Canada. The transaction is subject to customary closing conditions and regulatory approvals. The parties have agreed to extend the completion date of the transaction in order to complete certain closing conditions and to negotiate and mutually agree upon changes to the merger terms. Subject to our reaching agreement with the sellers on such revised terms, we would expect to close the transaction in the second half of 2008.

Expiration of Our Alliance with Chase Paymentech

Our largest merchant alliance, Chase Paymentech Solutions™, a global payments and merchant acquiring entity, is 51% owned by JPMorgan and 49% owned by FDC. On May 27, 2008, we announced we had reached agreement with JPMorgan to end the Chase Paymentech joint venture by the end of 2008. In the interim, the two companies will continue to operate the joint venture. After the transition, JPMorgan and FDC will operate separate payment businesses. We will continue to provide transaction processing and data commerce solutions for allocated merchants through our current technology platforms. We will assume management of the full-service independent sales organization ("ISO") and Agent Bank unit of the joint venture and will integrate 49% of the joint venture's assets and a portion of the joint venture employees into our existing merchant acquiring business. We have

1

historically accounted for our minority interest in the joint venture under the equity method of accounting. Subsequent to the wind up of the joint venture, the portion of the alliance's business retained by us will be reflected on a consolidated basis throughout the financial statements. As a result and on a pro forma basis, the expiration would not be expected to have a material impact on historical net income (loss) and our historical reported revenues and expenses would increase. Expiration of the alliance will result in the loss of JPMorgan branch referrals and access to the JPMorgan brand. Additionally, expiration in 2008 will cause us to incur an obligation associated with taxes. Based on preliminary estimates and assumptions this obligation could be in excess of $200 million. A significant portion of this obligation may, however, be recovered through the future amortization of increased tax basis generated by this event. Expiration will also pose the following potential risks: loss of certain processing volume over time, disruption of the business due to the need to identify and transition to a new financial institution sponsorship and clearing services for the merchants allocated to FDC, and post-expiration competition by JPMorgan, any of which could have a material adverse effect on our operations and results.

Amendments to Our Interim Loan Agreements

On June 19, 2008, we entered into the First Amendment (the "First Senior Amendment") to the Senior Unsecured Interim Loan Agreement, dated as of September 24, 2007 (as amended and restated as of October 24, 2007, the "Amended Senior Unsecured Interim Loan Agreement"). The First Senior Amendment amends the Amended Senior Unsecured Interim Loan Agreement to increase the interest rates on borrowings (i) at any date on or after June 19, 2008 and prior to August 18, 2008, to 8.490% per annum with respect to senior cash-pay loans and 9.320% per annum with respect to senior PIK loans, and (ii) at any date on or after August 18, 2008, to 9.875% per annum with respect to senior cash-pay loans and 10.550% per annum with respect to senior PIK loans. The lenders in respect of the senior cash-pay loans and senior PIK loans will have the option on September 24, 2008 and on the 15th day of each calendar month thereafter to exchange such loans for notes having substantially identical terms, as applicable. See "Description of Other Indebtedness—Senior Unsecured Cash-pay Term Loan Facility and Senior Unsecured PIK Term Loan Facility."

Also on June 19, 2008, we entered into the First Amendment (the "First Senior Subordinated Amendment") to the Senior Subordinated Interim Loan Agreement, dated as of September 24, 2007 (as amended and restated as of October 24, 2007, the "Amended Senior Subordinated Interim Loan Agreement"). The First Senior Subordinated Amendment amends the Amended Senior Subordinated Interim Loan Agreement to increase the interest rates on borrowings (i) at any date on or after June 19, 2008 and prior to August 18, 2008 to 9.800% per annum, and (ii) at any date on or after August 18, 2008, to 11.250% per annum. The lenders in respect of the subordinated loans will have the option on September 24, 2008 and on the 15th day of each calendar month thereafter to exchange such loans for notes having substantially identical terms. See "Description of Other Indebtedness—Senior Subordinated Unsecured Interim Term Loan Facility."

Other Developments

In July 2008, our subsidiary Integrated Payment Systems Inc. ("IPS") agreed with The Western Union Company ("Western Union") that on October 1, 2009, IPS will assign and transfer to Western Union, among other things, certain assets and equipment used by IPS to issue retail money orders and an amount sufficient to satisfy all outstanding retail money orders. On the closing date, Western Union will assume IPS's role as issuer of the retail money orders. The transfer will result in a significant decrease to the IPS settlement asset portfolio.

General economic conditions in the United States continue to show signs of weakening. Many of our businesses rely in part on the number and size of consumer transactions which may be challenged by a declining U.S. economy and difficult capital markets. After experiencing a rebound in the early

2

part of 2008 from the slow 2007 holiday spending period, domestic merchant transaction growth has since slowed slightly. This reduction in spending is across a wide range of categories, with discounters showing less of an effect than smaller retailers. While we are partially insulated from specific industry trends through our diverse market presence, broad slowdowns in consumer spending could have a material adverse impact on future revenues and profits.

Kohlberg, Kravis Roberts & Co.

Established in 1976, KKR is a leading global alternative asset manager. The core of the Firm's franchise is sponsoring and managing funds that make private equity investments in North America, Europe, and Asia. Throughout its history, KKR has brought a long-term investment approach to portfolio companies, focusing on working in partnership with management teams and investing for future competitiveness and growth. The Firm's sponsored funds include KKR Private Equity Investors, L.P. (Euronext Amsterdam: KPE), a permanent capital fund that invests in KKR-identified investments; and two credit strategy funds, KKR Financial and the KKR Strategic Capital Funds, which make investments in debt transactions. KKR has offices in New York, Menlo Park, San Francisco, London, Paris, Hong Kong, and Tokyo.

Our principal executive offices are located at 6200 S. Quebec Street, Greenwood Village, CO 80111. The telephone number of our principal executive offices is (303) 967-8000. Our Internet address ishttp://www.firstdata.com. Information on our web site does not constitute part of this prospectus.

3

On October 24, 2007, First Data issued in a private offering $2,200,000,000 aggregate principal amount of 97/8% senior notes due 2015.

General | In connection with the private offering, First Data and the guarantors of the outstanding notes entered into a registration rights agreement with the initial purchasers pursuant to which they agreed, among other things, to deliver this prospectus to you and to complete the exchange offer within 360 days after the date of original issuance of the outstanding notes. You are entitled to exchange in the exchange offer your outstanding notes for exchange notes which are identical in all material respects to the outstanding notes except: | |||

• | the exchange notes have been registered under the Securities Act; | |||

• | the exchange notes are not entitled to any registration rights which are applicable to the outstanding notes under the registration rights agreement; and | |||

• | the additional interest provisions of the registration rights agreement are not applicable. | |||

The Exchange Offer | First Data is offering to exchange $2,200,000,000 aggregate principal amount of 97/8% senior notes due 2015. | |||

You may only exchange outstanding notes in minimum denominations of $2,000 and integral multiples of $1,000 in excess of $2,000. | ||||

Resale | Based on an interpretation by the staff of the Securities and Exchange Commission (the "SEC") set forth in no-action letters issued to third parties, we believe that the exchange notes issued pursuant to the exchange offer in exchange for the outstanding notes may be offered for resale, resold and otherwise transferred by you (unless you are our "affiliate" within the meaning of Rule 405 under the Securities Act) without compliance with the registration and prospectus delivery provisions of the Securities Act, provided that: | |||

• | you are acquiring the exchange notes in the ordinary course of your business; and | |||

• | you have not engaged in, do not intend to engage in, and have no arrangement or understanding with any person to participate in, a distribution of the exchange notes. | |||

If you are a broker-dealer and receive exchange notes for your own account in exchange for outstanding notes that you acquired as a result of market-making activities or other trading activities, you must acknowledge that you will deliver this prospectus in connection with any resale of the exchange notes. See "Plan of Distribution." | ||||

4

Any holder of outstanding notes who: | ||||

• | is our affiliate; | |||

• | does not acquire exchange notes in the ordinary course of its business; or | |||

• | tenders its outstanding notes in the exchange offer with the intention to participate, or for the purpose of participating, in a distribution of exchange notes | |||

cannot rely on the position of the staff of the SEC enunciated inMorgan Stanley & Co. Incorporated (available June 5, 1991) andExxon Capital Holdings Corporation (available May 13, 1988), as interpreted inShearman & Sterling (available July 2, 1993), or similar no-action letters and, in the absence of an exemption therefrom, must comply with the registration and prospectus delivery requirements of the Securities Act in connection with any resale of the exchange notes. | ||||

Expiration Date | The exchange offer will expire at 11:59 p.m., New York City time, on , 2008, unless extended by First Data. First Data currently does not intend to extend the expiration date. | |||

Withdrawal | You may withdraw the tender of your outstanding notes at any time prior to the expiration of the exchange offer. First Data will return to you any of your outstanding notes that are not accepted for any reason for exchange, without expense to you, promptly after the expiration or termination of the exchange offer. | |||

Conditions to the Exchange Offer | Each exchange offer is subject to customary conditions, which First Data may waive. See "The Exchange Offer—Conditions to the Exchange Offer." | |||

Procedures for Tendering Outstanding Notes | If you wish to participate in the exchange offer, you must complete, sign and date the applicable accompanying letter of transmittal, or a facsimile of such letter of transmittal, according to the instructions contained in this prospectus and the letter of transmittal. You must then mail or otherwise deliver the letter of transmittal, or a facsimile of such letter of transmittal, together with your outstanding notes and any other required documents, to the exchange agent at the address set forth on the cover page of the letter of transmittal. | |||

5

If you hold outstanding notes through The Depository Trust Company ("DTC") and wish to participate in the exchange offer, you must comply with the Automated Tender Offer Program procedures of DTC by which you will agree to be bound by the letter of transmittal. By signing, or agreeing to be bound by, the letter of transmittal, you will represent to us that, among other things: | ||||

• | you are not our "affiliate" within the meaning of Rule 405 under the Securities Act; | |||

• | you do not have an arrangement or understanding with any person or entity to participate in the distribution of the exchange notes; | |||

• | you are acquiring the exchange notes in the ordinary course of your business; and | |||

• | if you are a broker-dealer that will receive exchange notes for your own account in exchange for outstanding notes that were acquired as a result of market-making activities, you will deliver a prospectus, as required by law, in connection with any resale of such exchange notes. | |||

Special Procedures for Beneficial Owners | If you are a beneficial owner of outstanding notes that are registered in the name of a broker, dealer, commercial bank, trust company or other nominee, and you wish to tender those outstanding notes in the exchange offer, you should contact the registered holder promptly and instruct the registered holder to tender those outstanding notes on your behalf. If you wish to tender on your own behalf, you must, prior to completing and executing the letter of transmittal and delivering your outstanding notes, either make appropriate arrangements to register ownership of the outstanding notes in your name or obtain a properly completed bond power from the registered holder. The transfer of registered ownership may take considerable time and may not be able to be completed prior to the expiration date. | |||

Guaranteed Delivery Procedures | If you wish to tender your outstanding notes and your outstanding notes are not immediately available, or you cannot deliver your outstanding notes, the letter of transmittal or any other required documents, or you cannot comply with the procedures under DTC's Automated Tender Offer Program for transfer of book-entry interests prior to the expiration date, you must tender your outstanding notes according to the guaranteed delivery procedures set forth in this prospectus under "The Exchange Offer—Guaranteed Delivery Procedures." | |||

6

Effect on Holders of Outstanding Notes | As a result of the making of, and upon acceptance for exchange of all validly tendered outstanding notes pursuant to the terms of the exchange offer, First Data and the guarantors of the notes will have fulfilled a covenant under the registration rights agreement. Accordingly, there will be no increase in the applicable interest rate on the outstanding notes under the circumstances described in the registration rights agreement. If you do not tender your outstanding notes in the exchange offer, you will continue to be entitled to all the rights and limitations applicable to the outstanding notes as set forth in the indenture, except First Data and the guarantors of the notes will not have any further obligation to you to provide for the exchange and registration of untendered outstanding notes under the registration rights agreement. To the extent that outstanding notes are tendered and accepted in the exchange offer, the trading market for outstanding notes that are not so tendered and accepted could be adversely affected. | |||

Consequences of Failure to Exchange | All untendered outstanding notes will continue to be subject to the restrictions on transfer set forth in the outstanding notes and in the indenture. In general, the outstanding notes may not be offered or sold, unless registered under the Securities Act, except pursuant to an exemption from, or in a transaction not subject to, the Securities Act and applicable state securities laws. Other than in connection with the exchange offer, First Data and the guarantors of the notes do not currently anticipate that they will register the outstanding notes under the Securities Act. | |||

Certain United States Federal Income Tax Consequences | The exchange of outstanding notes for exchange notes in the exchange offer will not be a taxable event for United States federal income tax purposes. See "Certain United States Federal Income Tax Consequences." | |||

Use of Proceeds | We will not receive any cash proceeds from the issuance of the exchange notes in the exchange offer. See "Use of Proceeds." | |||

Exchange Agent | Wells Fargo Bank, National Association is the exchange agent for the exchange offer. The addresses and telephone numbers of the exchange agent are set forth in the section captioned "The Exchange Offer—Exchange Agent." | |||

7

The summary below describes the principal terms of the exchange notes. Certain of the terms and conditions described below are subject to important limitations and exceptions. The "Description of Notes" section of this prospectus contains more detailed descriptions of the terms and conditions of the outstanding notes and exchange notes. The exchange notes will have terms identical in all material respects to the outstanding notes, except that the exchange notes will not contain terms with respect to transfer restrictions, registration rights and additional interest for failure to observe certain obligations in the registration rights agreement.

Issuer | First Data Corporation | |||

Securities Offered | $2,200,000,000 aggregate principal amount of 97/8% senior notes due 2015. | |||

Maturity Date | The exchange notes will mature on September 24, 2015. | |||

Interest Rate | Interest on the exchange notes will be payable in cash and will accrue at a rate of 97/8% per annum. | |||

Interest Payment Dates | We will pay interest on the exchange notes on March 31 and September 30. Interest began to accrue from the issue date of the notes. | |||

Ranking | The exchange notes will be unsecured senior obligations and will: | |||

• | rank equal in right of payment with all of our existing and future senior indebtedness, including under our senior cash-pay unsecured interim credit facility and senior PIK unsecured interim credit facility and any senior cash-pay notes or senior PIK notes issued in exchange therefor (together, the "senior unsecured debt"), each of which is scheduled to mature in 2015; | |||

• | rank senior in right of payment to all existing and future subordinated indebtedness, including under our senior subordinated unsecured interim credit facility (the "senior subordinated unsecured debt" and collectively, with the senior unsecured debt, the "unsecured debt"), which is scheduled to mature in 2016; | |||

• | be effectively subordinated, to the extent of the value of the assets securing such indebtedness, to our and our guarantors' obligations under the senior secured credit facilities (including any future obligations thereto); and | |||

• | be effectively subordinated in right of payment to all existing and future indebtedness and other liabilities of our non-guarantor subsidiaries (other than indebtedness and liabilities owed to us or one of our guarantor subsidiaries). | |||

As of June 30, 2008, on a pro forma basis after giving effect to the exchange offer (1) the exchange notes and related guarantees would have ranked effectively junior to approximately $12,951.3 million of senior secured indebtedness under our senior secured credit facilities and $195.0 million of other secured debt, which represents capital leases, (2) the exchange notes and related guarantees would have ranked effectively junior to $7,500.0 million notional of floating rate | ||||

8

| to fixed rate swaps that hedge interest rate risk exposure on the senior secured term loan facility as well as €91.1 million and $115.0 million Australian dollars notional, respectively, of cross currency swaps that serve as net investment hedges; these derivative instruments are pari passu with the senior secured indebtedness and represented a negative mark to market (liability) of $217.9 million as of June 30, 2008 and (3) we would have had an additional $1,870.0 million of available capacity under our senior secured revolving credit facility (without giving effect to approximately $42.0 million of outstanding letters of credit as of June 30, 2008). In addition, we have lines of credit, available solely for settlement funding except as otherwise noted, associated with: | ||||

| • | First Data Deutschland, which totaled approximately €160 million (approximately US$251 million as of June 30, 2008), of which approximately US$131.7 million was available for borrowings as of June 30, 2008; | |||

| • | Cashcard Australia, Ltd., which totaled approximately 160 million Australian dollars (approximately US$154 million as of June 30, 2008), of which US$87.2 million was available for borrowings as of June 30, 2008; and | |||

| • | First Data Polska, the maximum amount available, which varies for peak needs during the year, which totaled approximately 245 million Polish zloty (approximately US$114 million as of June 30, 2008), all of which was available for borrowings as of June 30, 2008. | |||

| • | Our joint venture with Allied Irish Banks, p.l.c., of which we own 50.1%, which totaled committed lines of credit of €145 million (approximately US$227 million as of June 30, 2008), all but €10 million of which is available solely for settlement activity purposes and of which US$175.9 million was available for borrowings as of June 30, 2008. | |||

| Our Merchant Solutions joint venture partner funds settlement activity on behalf of the joint venture in accordance with the joint venture's operating agreement and on an uncommitted basis. The joint venture, which is consolidated by us, had $64.8 million outstanding under this agreement as of June 30, 2008. | ||||

Guarantees | The exchange notes will be jointly and severally and fully and unconditionally guaranteed on a senior basis by each of our direct and indirect wholly owned domestic subsidiaries that guarantees the senior secured credit facilities. Each of the guarantees of the senior notes will be a general senior obligation of each guarantor and will: | |||

| • | rank senior in right of payment to all existing and future subordinated indebtedness of the guarantor subsidiary, including their guarantees under our senior subordinated unsecured debt; | |||

9

| • | rank equally in right of payment with all existing and future senior indebtedness of the guarantor subsidiary, including their guarantees under our senior unsecured debt; | |||

| • | be effectively subordinated, to the extent of the value of the assets securing such indebtedness, to our and the guarantors' obligations under the senior secured credit facilities (including any future obligations thereto); and | |||

| • | be effectively subordinated in right of payment to all existing and future indebtedness and other liabilities of any subsidiary of a guarantor that is not also a guarantor of the notes. | |||

| Any guarantee of the exchange notes will be released in the event such guarantee is released under the senior secured credit facilities. | ||||

| Our non-guarantor subsidiaries accounted for approximately $1,163.1 million, or 26.9%, of our consolidated revenue for the six months ended June 30, 2008, and approximately $9,962.0 million, or 29.1%, of our total assets excluding settlement assets, and approximately $771.6 million, or 2.8%, of our total liabilities excluding settlement liabilities, in each case as of June 30, 2008. | ||||

Optional Redemption | We may redeem the exchange notes, in whole or in part, at any time prior to September 30, 2011, at a price equal to 100% of the principal amount of the exchange notes redeemed plus accrued and unpaid interest to the redemption date and a "make-whole premium," as described under "Description of Notes—Optional Redemption." | |||

| We may redeem the exchange notes, in whole or in part, on or after September 30, 2011, at the redemption prices set forth under "Description of Notes—Optional Redemption." | ||||

| Additionally, from time to time on or before September 30, 2010, we may choose to redeem up to 35% of the principal amount of each of the exchange notes with the proceeds from one or more public equity offerings at the redemption prices set forth under "Description of Notes—Optional Redemption." | ||||

Change of Control Offer | Upon the occurrence of a change of control, you will have the right, as holders of the exchange notes, to require us to repurchase some or all of your exchange notes at 101% of their face amount, plus accrued and unpaid interest to the repurchase date. See "Description of Notes—Repurchase at the Option of Holders—Change of Control." | |||

Asset Sale Proceeds Offer | Upon the occurrence of a non-ordinary course asset sale, you will have the right, as holders of the exchange notes, to require us to repurchase some or all of your exchange notes at 100% of their face amount, plus accrued and unpaid interest to the repurchase date. See "Description of Notes—Repurchase at the Option of Holders—Change of Control." | |||

10

Certain Covenants | The indenture governing the exchange notes contains covenants limiting our ability and the ability of our restricted subsidiaries to: | |||

| • | incur additional debt or issue certain preferred shares; | |||

| • | pay dividends on or make other distributions in respect of our capital stock or make other restricted payments; | |||

| • | make certain investments; | |||

| • | sell certain assets; | |||

| • | create liens on certain assets to secure debt; | |||

| • | consolidate, merge, sell or otherwise dispose of all or substantially all of our assets; | |||

| • | enter into certain transactions with our affiliates; and | |||

| • | designate our subsidiaries as unrestricted subsidiaries. | |||

| These covenants are subject to a number of important limitations and exceptions. See "Description of Notes." | ||||

Voting | The exchange notes will be treated along with certain other senior unsecured debt of First Data as a single class for voting purposes and consent by the holders of the exchange notes will not be sufficient by itself to take any action requiring majority consent or the action of holders of at least 30% of the debt entitled to vote unless, in the case of the latter, at least 91.2% of the holders of the exchange notes as of June 30, 2008, consent to such action. | |||

Original Issue Discount | Because the "stated redemption price at maturity" of the exchange notes exceeds their "issue price" by more than the statutory de minimis threshold, the exchange notes will be treated as having been issued with original issue discount for United States federal income tax purposes. A U.S. holder (as defined in "Certain United States Federal Income Tax Consequences") of an exchange note will be required to include such original issue discount in gross income as it accrues, in advance of the receipt of cash attributable to that income and regardless of the U.S. holder's regular method of accounting for United States federal income tax purposes. See "Certain United States Federal Income Tax Consequences" for more detail. | |||

No Prior Market | The exchange notes will be freely transferable but will be new securities for which there will not initially be a market. Accordingly, we cannot assure you whether a market for the exchange notes will develop or as to the liquidity of any such market that may develop. The initial purchasers in the private offering of the outstanding notes have informed us that they currently intend to make a market in the exchange notes; however, they are not obligated to do so, and they may discontinue any such market-making activities at any time without notice. | |||

You should consider carefully all of the information set forth in this prospectus prior to exchanging your outstanding notes. In particular, we urge you to consider carefully the factors set forth under the heading "Risk Factors."

11

You should carefully consider the risk factors set forth below as well as the other information contained in this prospectus before deciding to tender your outstanding notes in the exchange offer. Any of the following risks could materially and adversely affect our business, financial condition, operating results or cash flow; however, the following risks are not the only risks facing us. Additional risks and uncertainties not currently known to us or those we currently view to be immaterial also may materially and adversely affect our business, financial condition or results of operations. In such a case, the trading price of the exchange notes could decline or we may not be able to make payments of interest and principal on the exchange notes, and you may lose all or part of your original investment.

Risks Related to the Exchange Offer

There may be adverse consequences if you do not exchange your outstanding notes.

If you do not exchange your outstanding notes for exchange notes in the exchange offer, you will continue to be subject to restrictions on transfer of your outstanding notes as set forth in the offering memorandum distributed in connection with the private offering of the outstanding notes. In general, the outstanding notes may not be offered or sold unless they are registered or exempt from registration under the Securities Act and applicable state securities laws. Except as required by the registration rights agreement, we do not intend to register resales of the outstanding notes under the Securities Act. You should refer to "Prospectus Summary—The Exchange Offer" and "The Exchange Offer" for information about how to tender your outstanding notes.

The tender of outstanding notes under the exchange offer will reduce the outstanding amount of the outstanding notes, which may have an adverse effect upon, and increase the volatility of, the market prices of the outstanding notes due to a reduction in liquidity.

Your ability to transfer the exchange notes may be limited by the absence of an active trading market, and there is no assurance that any active trading market will develop for the exchange notes.

We are offering the exchange notes to the holders of the outstanding notes. The outstanding notes were offered and sold in October 2007 to institutional investors and are eligible for trading in the PORTAL market.

We do not intend to apply for a listing of the exchange notes on a securities exchange or on any automated dealer quotation system. There is currently no established market for the exchange notes, and we cannot assure you as to the liquidity of markets that may develop for the exchange notes, your ability to sell the exchange notes or the price at which you would be able to sell the exchange notes. If such markets were to exist, the exchange notes could trade at prices that may be lower than their principal amount or purchase price depending on many factors, including prevailing interest rates, the market for similar notes, our financial and operating performance and other factors. The initial purchasers in the private offering of the outstanding notes have advised us that they currently intend to make a market with respect to the exchange notes. However, these initial purchasers are not obligated to do so, and any market making with respect to the exchange notes may be discontinued at any time without notice. In addition, such market making activity may be limited during the pendency of the exchange offer or the effectiveness of a shelf registration statement in lieu thereof. Therefore, we cannot assure you that an active market for the exchange notes will develop or, if developed, that it will continue. Historically, the market for non-investment grade debt has been subject to disruptions that have caused substantial volatility in the prices of securities similar to the notes. The market, if any, for the exchange notes may experience similar disruptions and any such disruptions may adversely affect the prices at which you may sell your exchange notes.

12

Certain persons who participate in the exchange offer must deliver a prospectus in connection with resales of the exchange notes.

Based on interpretations of the staff of the SEC contained inExxon Capital Holdings Corp., SEC no-action letter (April 13, 1988),Morgan Stanley & Co. Inc., SEC no-action letter (June 5, 1991) andShearman & Sterling, SEC no-action letter (July 2, 1983), we believe that you may offer for resale, resell or otherwise transfer the exchange notes without compliance with the registration and prospectus delivery requirements of the Securities Act. However, in some instances described in this prospectus under "Plan of Distribution," certain holders of exchange notes will remain obligated to comply with the registration and prospectus delivery requirements of the Securities Act to transfer the exchange notes. If such a holder transfers any exchange notes without delivering a prospectus meeting the requirements of the Securities Act or without an applicable exemption from registration under the Securities Act, such a holder may incur liability under the Securities Act. We do not and will not assume, or indemnify such a holder against, this liability.

Risks Related to Our Indebtedness

Our substantial leverage could adversely affect our ability to raise additional capital to fund our operations, limit our ability to react to changes in the economy or our industry, expose us to interest rate risk to the extent of our variable rate debt and prevent us from meeting our obligations under the notes.

We are highly leveraged. The following chart shows our level of indebtedness and certain other information as of June 30, 2008.

| | (in millions) | ||||

|---|---|---|---|---|---|

Senior secured credit facilities(1) | |||||

Revolving credit facility | $ | 130.0 | |||

Term loan facility | 12,821.3 | ||||

Senior cash-pay notes due 2015 | 2,200.0 | ||||

Senior cash-pay unsecured interim credit facility(2) | 1,550.0 | ||||

Senior PIK unsecured interim credit facility(2) | 2,941.2 | ||||

Senior subordinated unsecured interim credit facility(2) | 2,500.0 | ||||

Capital lease obligations and other debt(3) | 678.1 | ||||

Total | $ | 22,820.6 | |||

- (1)

- Upon the closing of the Transactions, we entered into senior secured credit facilities, consisting of (a) a $2,000.0 million senior secured revolving credit facility with a six-year maturity, $200.0 million of which was drawn on the closing date of the Transactions to fund costs related to the Transactions and $130.0 million of which was outstanding as of June 30, 2008 (without giving effect to approximately $42.0 million of outstanding letters of credit as of June 30, 2008) and (b) a $13,000.0 million senior secured term loan facility with a seven year maturity, approximately $1,000.0 million of which was available in euros, $12,775.0 million of which was drawn on the date of the closing of the Transactions. A portion of the term loan facility in the amount of $225.0 million, which is approximately the amount of Previously Existing Notes not tendered and remaining outstanding after consummation of the tender offers for such notes, remained available from time to time prior to December 31, 2008. This delayed draw facility may be drawn as the Previously Existing Notes are repaid (of which approximately $25.6 million and $68.1 million was drawn on December 24, 2007 and August 1, 2008, respectively, when certain Previously Existing Notes were repaid). The principal balance of the term loan facility was $12,821.3 as of June 30, 2008 and is net of quarterly installment payments of 1% annual principal amortization of the original funded principal amount and also reflects the foreign exchange impact of the euro-demoninated portion as well as the aforementioned delayed term loan draw executed prior to June 30, 2008. See "Description of Other Indebtedness—Senior Secured Credit Facilities."

- (2)

- The $1,550.0 million senior cash-pay unsecured interim credit facility and the $2,941.2 million senior PIK unsecured interim credit facility are scheduled to mature on September 24, 2015. The senior PIK unsecured interim credit facility balance has increased from inception balance of $2,750.0 million due to the "payment" of accrued interest through June 30, 2008. The $2,500.0 million senior subordinated unsecured interim credit facility is scheduled to mature on March 31, 2016.

13

- (3)

- Consists primarily of $177.4 million of Previously Existing Notes not repaid as part of the tender offer or the subsequent repayment in December 2007 and remaining outstanding as of June 30, 2008 (net of unamortized portion of purchase price adjustments to reflect debt at fair market value effective with the Merger), $195.0 million of capital lease obligations, $237.2 million of borrowings outstanding against lines of credit associated with our non-guarantor subsidiaries and $64.8 million of settlement activity funding provided by our joint venture partner, in accordance with the joint venture's operating agreement and on an uncommitted basis, in connection with our Merchant Solutions joint venture which we consolidate. We have lines of credit associated with First Data Deutschland, which totaled approximately €160 million (approximately US$251 million as of June 30, 2008), US$119.3 million of which was outstanding as of June 30, 2008. We also have lines of credit associated with Cashcard Australia, Ltd., which totaled approximately 160 million Australian dollars (approximately US$154 million as of June 30, 2008), US$66.8 million of which was outstanding as of June 30, 2008. Finally, we have two credit facilities associated with First Data Polska, which are periodically used to fund settlement activity. The maximum amount available under the facilities, which varies for peak needs during the year, totaled approximately 245 million Polish zloty (approximately US$114 million as of June 30, 2008), with no amount outstanding as of June 30, 2008. In January 2008 and in connection with our newly established joint venture with Allied Irish Banks, p.l.c., of which we own 50.1%, we entered into committed lines of credit for a total of €145 million (approximately US$227 million as of June 30, 2008), all but €10 million of which is available solely for settlement activity purposes, US$51.1 million of which was outstanding as of June 30, 2008.

Our high degree of leverage could have important consequences for you, including:

- •

- increasing our vulnerability to adverse economic, industry or competitive developments;

- •

- requiring a substantial portion of cash flow from operations to be dedicated to the payment of principal and interest on our indebtedness, therefore reducing our ability to use our cash flow to fund our operations, capital expenditures and future business opportunities;

- •

- exposing us to the risk of increased interest rates because certain of our borrowings, including borrowings under our senior secured credit facilities, will be at variable rates of interest;

- •

- making it more difficult for us to satisfy our obligations with respect to our indebtedness, including the notes, and any failure to comply with the obligations of any of our debt instruments, including restrictive covenants and borrowing conditions, could result in an event of default under the indenture governing the notes and the agreements governing such other indebtedness;

- •

- restricting us from making strategic acquisitions or causing us to make unintended divestitures;

- •

- making it more difficult for us to obtain network sponsorship and clearing services from financial institutions as a result of our increased leverage;

- •

- limiting our ability to obtain additional financing for working capital, capital expenditures, product development, debt service requirements, acquisitions and general corporate or other purposes; and

- •

- limiting our flexibility in planning for, or reacting to, changes in our business or market conditions and placing us at a competitive disadvantage compared to our competitors who are less highly leveraged and who therefore, may be able to take advantage of opportunities that our leverage prevents us from exploiting.

Increase in interest rates may negatively impact our operating results and financial condition.

Certain of our borrowings, including borrowings under our senior secured credit facilities, to the extent the interest rate is not fixed by an interest rate swap, are at variable rates of interest. An increase in interest rates would have a negative impact on our results of operations by causing an increase in interest expense.

At June 30, 2008, we had $12,951.3 million aggregate principal amount of variable rate indebtedness under our senior secured credit facilities. A 100 basis point increase in such rates would increase our annual interest expense by approximately $129.5 million. At June 30, 2008 and currently,

14

we have interest rate swaps that fix the interest rate on $7.5 billion in notional amount of this variable rate indebtedness thus reducing the impact of a 100 basis point increase in rates to $54.5 million.

Our pro forma cash interest expense, net for the year ended December 31, 2007 was $1,669.5 million.

Despite our high indebtedness level, we and our subsidiaries still may be able to incur significant additional amounts of debt, which could further exacerbate the risks associated with our substantial indebtedness.