Sprint / Clearwire Investor Call December 17, 2012 Exhibit 99.1 |

© 2012 Sprint Cautionary Statement 2 Cautionary Statement Regarding Forward-Looking Statements This presentation includes “forward-looking statements” within the meaning of the securities laws. The words “may,” “could,” “should,” “estimate,” “project,” “forecast,” “intend,” “expect,” “anticipate,” “believe,” “target,” “plan,” “providing guidance” and similar expressions are intended to identify information that is not historical in nature. This presentation contains forward-looking statements relating to the proposed merger and related transactions (the “transaction”) between Sprint and Clearwire. All statements, other than historical facts, including statements regarding the expected timing of the closing of the transaction; the ability of the parties to complete the transaction considering the various closing conditions; the expected benefits and efficiencies of the transaction; the competitive ability and position of Sprint and Clearwire; and any assumptions underlying any of the foregoing, are forward-looking statements. Such statements are based upon current plans, estimates and expectations that are subject to risks, uncertainties and assumptions. The inclusion of such statements should not be regarded as a representation that such plans, estimates or expectations will be achieved. You should not place undue reliance on such statements. Important factors that could cause actual results to differ materially from such plans, estimates or expectations include, among others, any conditions imposed in connection with the transaction, approval of the transaction by Clearwire stockholders, the satisfaction of various other conditions to the closing of the transaction contemplated by the merger agreement, and other factors discussed in Clearwire’s and Sprint’s Annual Reports on Form 10-K for their respective fiscal years ended December 31, 2011, their other respective filings with the U.S. Securities and Exchange Commission (the “SEC”) and the proxy statement and other materials that will be filed with the SEC by Clearwire in connection with the transaction. There can be no assurance that the transaction will be completed, or if it is completed, that it will close within the anticipated time period or that the expected benefits of the transaction will be realized. Sprint does not undertake any obligation to update any forward-looking statement to reflect events or circumstances after the date on which the statement is made or to reflect the occurrence of unanticipated events. Readers are cautioned not to place undue reliance on any of these forward-looking statements. |

© 2012 Sprint Soliciting Material Pursuant to 14a-12 3 Additional Information and Where to Find It In connection with the transaction, Clearwire will file a proxy statement and other materials with the SEC. INVESTORS AND SECURITY HOLDERS ARE ADVISED TO READ THE PROXY STATEMENT AND OTHER RELEVANT MATERIALS WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT CLEARWIRE AND THE TRANSACTION. Investors and security holders may obtain free copies of these documents (when they are available) and other documents filed with the SEC at the SEC's web site at www.sec.gov. In addition, the documents filed by CLEARWIRE with the SEC may be obtained free of charge by contacting CLEARWIRE at Clearwire, Attn: Investor Relations, (425) 636-5828. Clearwire’s filings with the SEC are also available on its website at http://corporate.clearwire.com. Participants in the Solicitation Clearwire and its officers and directors and Sprint and its officers and directors may be deemed to be participants in the solicitation of proxies from Clearwire’s stockholders with respect to the transaction. Information about Clearwire’s officers and directors and their ownership of Clearwire’s common shares is set forth in the proxy statement for Clearwire’s 2012 Annual Meeting of Stockholders, which was filed with the SEC on April 30, 2012. Information about Sprint’s officers and directors is set forth in Sprint’s Annual Report on Form 10-K for the year ended December 31, 2011, which was filed with the SEC on February 27, 2012. Investors and security holders may obtain more detailed information regarding the direct and indirect interests of the participants in the solicitation of proxies in connection with the transaction by reading the preliminary and definitive proxy statements regarding the transaction, which will be filed by Clearwire with the SEC. |

Sprint CEO Dan Hesse 4 |

© 2012 Sprint Expected Transaction Strategic Benefits • Optimize value creation of spectrum assets - Keeps spectrum intact - Gain full control of valuable spectrum resource and LTE deployment - Fair price to both shareholder bases • Timing of the transaction enables the efficient deployment of LTE on 2.5 with the greatest expected efficiencies 5 |

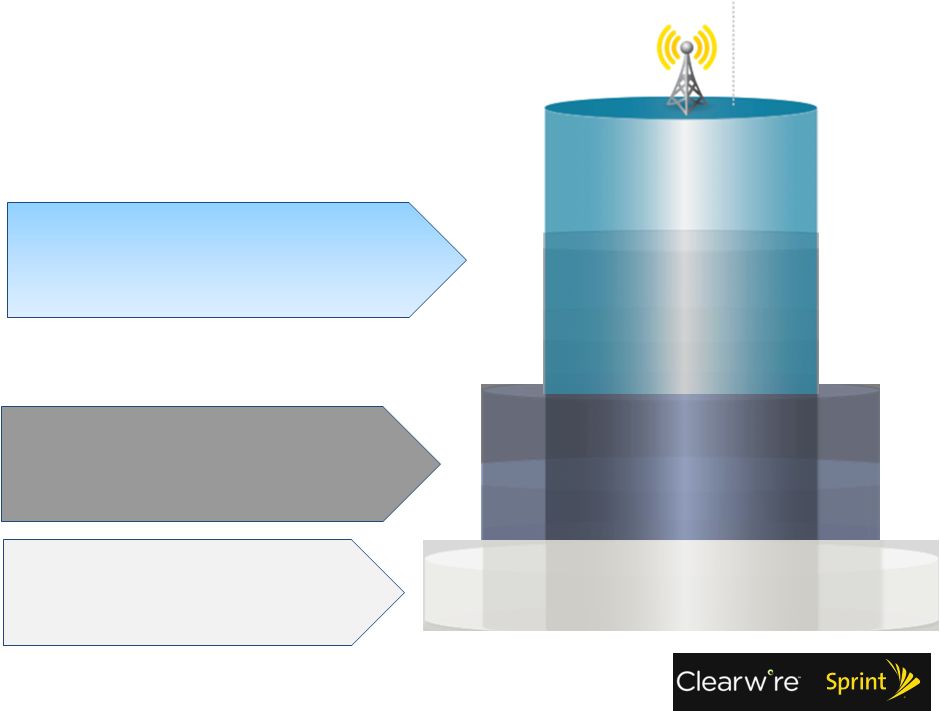

© 2012 Sprint Creates Robust Spectrum Portfolio LTE-TD – Depth enables capacity & speed Core LTE-FD deployment on G Block Enhanced propagation for LTE-FD deployment 6 800 MHz 1.9 GHz 2.5 GHz |

© 2012 Sprint Significant value for Sprint and Clearwire Shareholders • Fair Premium to Clearwire’s trading price pre Sprint-SoftBank announcement • Fair price per MHz PoP • Eliminates complexities and challenges of current inter-company governance • Best timing at initial planning stages of Clearwire LTE build-out 7 |

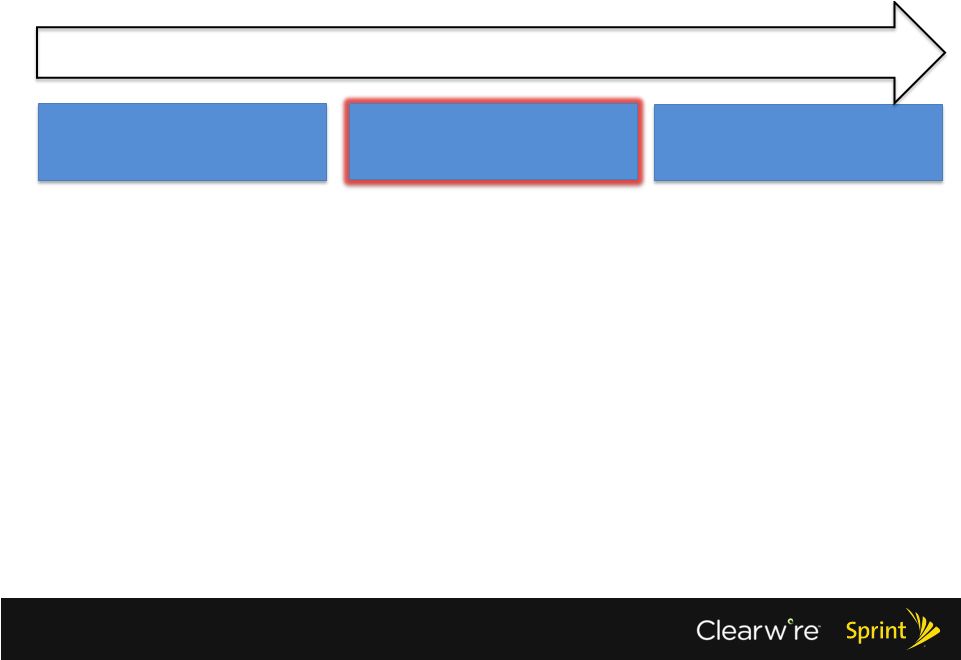

© 2012 Sprint Sprint Turnaround 8 2008 - 2011 2012 - 2013 2014+ • Transaction provides spectrum capacity to enable future growth • Facilitates more competitive service offerings to fuel margin expansion phase Recovery Investment Margin Expansion |

Clearwire CEO Erik Prusch 9 |

© 2012 Sprint Transaction Provides Certain and Attractive Value for Clearwire’s Shareholders • • • • • • 10 Initial indication of interest $2.60 final proposal $2.97 (+14%) ~40% premium to Clearwire’s price on November 20 (Date preceding Sprint’s initial indication of interest) ~130% premium to Clearwire’s price on October 10 (Date preceding confirmation of Sprint/Softbank discussions and rumors of Clearwire involvement) $10bn total Clearwire enterprise value $2.2bn equity purchase price $2.97/share in cash |

© 2012 Sprint Clearwire Board Has Reviewed Available Strategic Alternatives Over the Course of the Last Two Years • Clearwire Board and management performed a comprehensive review of strategic alternatives to maximize shareholder value over the past two years • Upon first indication of Sprint interest in current transaction, the Clearwire Board formed a Special Committee comprised solely of Directors independent from Sprint to review the strategic alternatives available to the Company. The Special Committee: Hired its own legal and financial advisors, and conducted a careful and rigorous process Received fairness opinion from its financial advisors Made unanimous recommendation to Board that offer is fair to and in the best interest of non-Sprint Class A shareholders • Along with receiving Special Committee recommendation, the Board conducted its own review with its financial and legal advisors and also received a fairness opinion, and unanimously determined that this transaction was fair to and in the best interests of our non-Sprint shareholders 11 |

© 2012 Sprint Clearwire Explored Wide Range of Strategic Alternatives to Maximize Shareholder Value Alternative Explored Considerations Add New Non-Sprint Wholesale Customers • Ability to attract additional major customers is single-biggest factor in long- term viability of our business • Likelihood of success remains uncertain given current industry dynamics Partnerships or Other Strategic Transactions • Held extensive discussions with potential strategic partners and investors • Unable to secure new partnerships given existing governance agreements • Would not be able to sell whole company – Sprint has made it clear they are not sellers • Capital needs of the business are significant - Invested >$3B capex on WiMAX network and LTE upgrade to date - Limited ability to finance LTE build and obtain additional wholesale customers with substantial data capacity needs - Have taken significant steps to improve positioning of retail business and reduce costs 12 |

© 2012 Sprint Alternative Explored Considerations Sell Excess Spectrum • Hired investment bank to conduct auction in 2010 o Resulted in handful of bids with spectrum values well below those recently speculated by some shareholders, analysts and reporters o Were not successful in reaching agreement before we elected to pursue other available financing options o Since then, engaged in series of conversations with a number of parties (no compelling offer resulted) • Over past several weeks received one credible, but preliminary, proposal o Worked to improve proposal, but value well below recent speculation o Special Committee and Board concluded that Sprint transaction was better alternative for non-Sprint Class A shareholders • Recently reached out again to all parties previously in discussions with – no new interest generated • Even with sale of a meaningful block of spectrum, this does not address Clearwire’s fundamental issue: inability to attract a second major wholesale customer Financing Alternatives (Debt / Equity) • In contact with lenders/participants in capital markets • Have very limited access to new debt capital • Only have ~ 360mm shares available under current share authorization • Substantial funding gap – not enough capital available to fund plan Financial Restructuring • Spent significant time with advisors to understand implications / risks of restructuring • Believe financial restructuring is quite possible should Sprint transaction not close Clearwire Explored Wide Range of Strategic Alternatives to Maximize Shareholder Value 13 |

Sprint CFO Joe Euteneuer 14 |

© 2012 Sprint Transaction Overview 15 • $2.97 per share in cash for approximately 50% of Clearwire’s shares not already owned by Sprint • $2.2 billion cash payment to Clearwire’s non-Sprint shareholders • Clearwire’s outstanding debt and spectrum lease obligations of approximately $6.3 billion will remain outstanding • Over $800 million of projected year-end 2012 cash on Clearwire’s balance sheet • Loan of up to $800 million • Exchangeable for equity at $1.50 per share • $80 million per month to be loaned to Clearwire starting 1/1/13 |

© 2012 Sprint Financial Benefits and Costs 16 • Estimated total efficiencies of approximately $1 billion NPV , including reduction in Clearwire cost of debt • Expect slight dilution to Adjusted OIBDA in 2H13 and neutral impact in 2014 |

© 2012 Sprint Roadmap to Completion 17 • Customary closing conditions, including regulatory approvals • Clearwire shareholder vote – affirmative vote of at least 75% of outstanding shares (including Sprint) and a majority of non-Sprint owned shares • Completion of Sprint’s previously announced transaction with SoftBank • SoftBank has provided its consent to the transaction • Expected to close mid-2013 |

© 2012 Sprint Expected Transaction Strategic Benefits 18 • Optimize value creation of spectrum assets - Keeps spectrum intact - Gain full control of valuable spectrum resource and LTE deployment - Fair price to both shareholder bases • Timing of the transaction enables the efficient deployment of LTE on 2.5 with the greatest expected efficiencies |

19 Q&A |