Exhibit (c) (9)

- CONFIDENTIAL -

Project Canine

Confidential Discussion Materials for the

Special Committee of the Board of Directors of Collie

December 16, 2012

- CONFIDENTIAL -

Disclaimer

This presentation has been prepared by Centerview Partners LLC ( “Centerview”) for use solely by the Special Committee of the Board of Directors (the “Special Committee”) of Collie (the “Company”) and the Audit Committee of the Board of Directors of the Company (the “Audit Committee”) in connection with its evaluation of the proposed transaction and the Company’s strategic alternatives and for no other purpose. The information contained herein is based upon information supplied by the Company and publicly-available information, and portions of the information contained herein may be based upon statements, estimates and forecasts provided by the Company. We have relied upon the accuracy and completeness of the foregoing information, and have not assumed any responsibility for any independent verification of such information or for any independent evaluation or appraisal of any of the assets or liabilities (contingent or otherwise) of the Company or any other entity,or concerning solvency or fair value of the Company, its assets or any other entity. With respect to financial forecasts, we have assumed that such forecasts have been reasonably prepared on bases reflecting the best currently available estimates and judgments of the management of the Company as to the future financial performance of the Company, and at your direction we have relied upon such forecasts, as provided by the Company’s management, with respect to the Company and Shepherd. We assume no responsibility for and express no view as to such forecasts or the assumptions on which they are based. The information set forth herein is based upon economic, monetary, market and other conditions as in effect on, and the information made available to us as of, the date hereof, unless indicated otherwise.

The financial analysis in this presentation is complex and is not necessarily susceptible to a partial analysis or summary description. In performing this financial analysis, Centerview has considered the results of its analysis as a whole and did not necessarily attribute a particular weight to any particular portion of the analysis considered. Furthermore, selecting any portion of Centerview’s analysis, without considering the analysis as a whole, would create an incomplete view of the process underlying its financial analysis. Centerview may have deemed various assumptions more or less probable than other assumptions, so the reference ranges resulting from any particular portion of the analysis described above should not be taken to be Centerview’s view of the actual value of the Company.

These materials and the information contained herein are confidential, were not prepared with a view toward public disclosure, and may not be disclosed publicly or made available to third parties without the prior written consent of Centerview. These materials and any other advice, written or oral, rendered by Centerview is intended solely for the benefit and use of the Special Committee and the Audit Committee (in their capacity as such) in their consideration of the proposed transaction, and are not for the benefit of, and do not convey any rights or remedies for any holder of securities of the Company or any other person. Centerview will not be responsible for and has not provided any tax, accounting, actuarial, legal or other specialist advice. This presentation is not a fairness opinion, recommendation, valuation or opinion of any kind, and is necessarily incomplete and should be viewed solely in conjunction with the oral presentation provided by Centerview.

1

- CONFIDENTIAL -

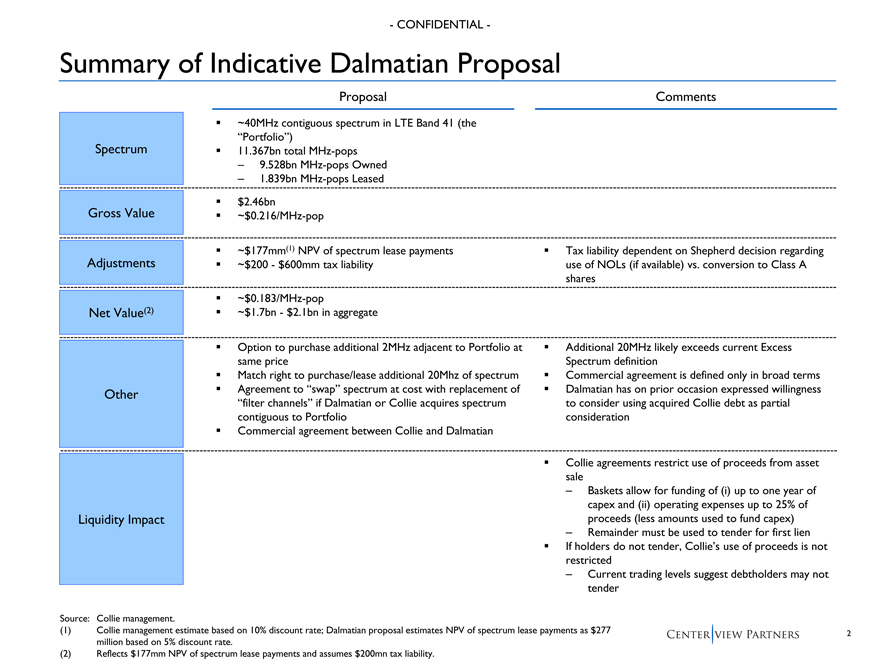

Summary of Indicative Dalmatian Proposal

Proposal Comments

~40MHz contiguous spectrum in LTE Band 41 (the Spectrum “Portfolio”)

11.367bn total MHz-pops

– 9.528bn MHz-pops Owned

– 1.839bn MHz-pops Leased

$2.46bn

Gross Value ~$0.216/MHz-pop

~$177mm(1) NPV of spectrum lease payments Tax liability dependent on Shepherd decision regarding Adjustments ~$200—$600mm tax liability use of NOLs (if available) vs. conversion to Class A shares

~$0.183/MHz-pop

Net Value(2) ~$1.7bn—$2.1bn in aggregate

Option to purchase additional 2MHz adjacent to Portfolio at Additional 20MHz likely exceeds current Excess same price Spectrum definition

Match right to purchase/lease additional 20Mhz of spectrum Commercial agreement is defined only in broad terms Other ??Agreement to “swap” spectrum at cost with replacement of ??Dalmatian has on prior occasion expressed willingness “filter channels” if Dalmatian or Collie acquires spectrum to consider using acquired Collie debt as partial contiguous to Portfolio consideration

Commercial agreement between Collie and Dalmatian

Collie agreements restrict use of proceeds from asset sale

– Baskets allow for funding of (i) up to one year of capex and (ii) operating expenses up to 25% of Liquidity Impact proceeds (less amounts used to fund capex)

– Remainder must be used to tender for first lien

If holders do not tender, Collie’s use of proceeds is not restricted

– Current trading levels suggest debtholders may not tender

Source: Collie management.

(1) Collie management estimate based on 10% discount rate; Dalmatian proposal estimates NPV of spectrum lease payments as $277 million based on 5% discount rate.

(2) Reflects $177mm NPV of spectrum lease payments and assumes $200mn tax liability.

2

- CONFIDENTIAL -

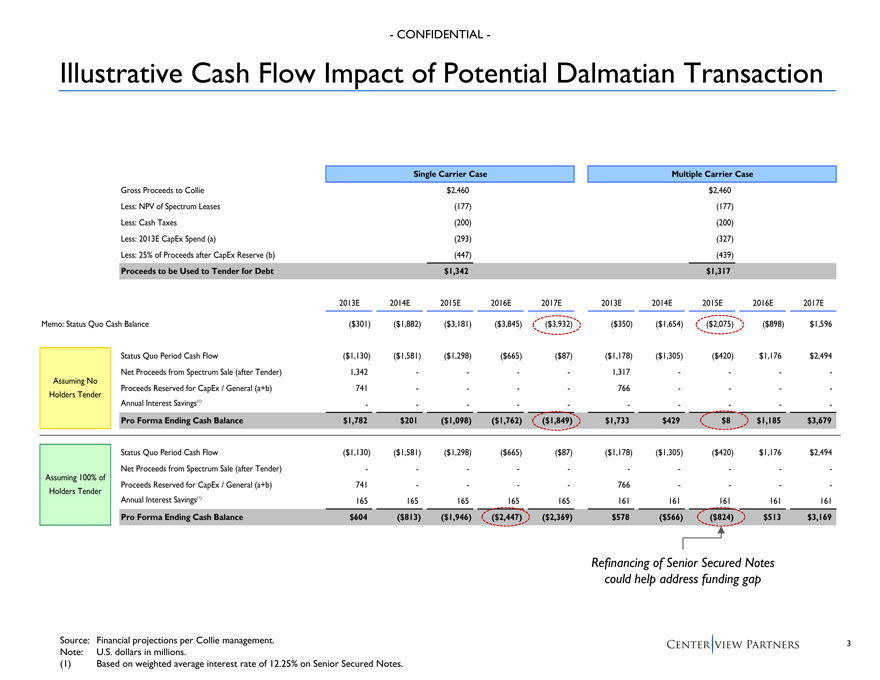

Illustrative Cash Flow Impact of Potential Dalmatian Transaction

Single Carrier Case Multiple Carrier Case

Gross Proceeds to Collie $2,460 $2,460 Less: NPV of Spectrum Leases (177) (177) Less: Cash Taxes (200) (200) Less: 2013E CapEx Spend (a) (293) (327) Less: 25% of Proceeds after CapEx Reserve (b) (447) (439)

Proceeds to be Used to Tender for Debt $1,342 $1,317

2013E 2014E 2015E 2016E 2017E 2013E 2014E 2015E 2016E 2017E

Memo: Status Quo Cash Balance ($301) ($1,882) ($3,181) ($3,845) ($3,932) ($350) ($1,654) ($2,075) ($898) $1,596

Status Quo Period Cash Flow ($1,130) ($1,581) ($1,298) ($665) ($87) ($1,178) ($1,305) ($420) $1,176 $2,494 Net Proceeds from Spectrum Sale (after Tender) 1,342 — — 1,317 — —Assuming No Proceeds Reserved for CapEx / General (a+b) 741 — — 766 — —Holders Tender Annual Interest Savings(1) — — — — —

Pro Forma Ending Cash Balance $1,782 $201 ($1,098) ($1,762) ($1,849) $1,733 $429 $8 $1,185 $3,679

Status Quo Period Cash Flow ($1,130) ($1,581) ($1,298) ($665) ($87) ($1,178) ($1,305) ($420) $1,176 $2,494 Net Proceeds from Spectrum Sale (after Tender) — — — — —Assuming 100% of Proceeds Reserved for CapEx / General (a+b) 741 — — 766 — —Holders Tender Annual Interest Savings(1) 165 165 165 165 165 161 161 161 161 161

Pro Forma Ending Cash Balance $604 ($813) ($1,946) ($2,447) ($2,369) $578 ($566) ($824) $513 $3,169

Refinancing of Senior Secured Notes could help address funding gap

Source: Financial projections per Collie management. Note: U.S. dollars in millions.

(1) Based on weighted average interest rate of 12.25% on Senior Secured Notes.

3 |

|

- CONFIDENTIAL -

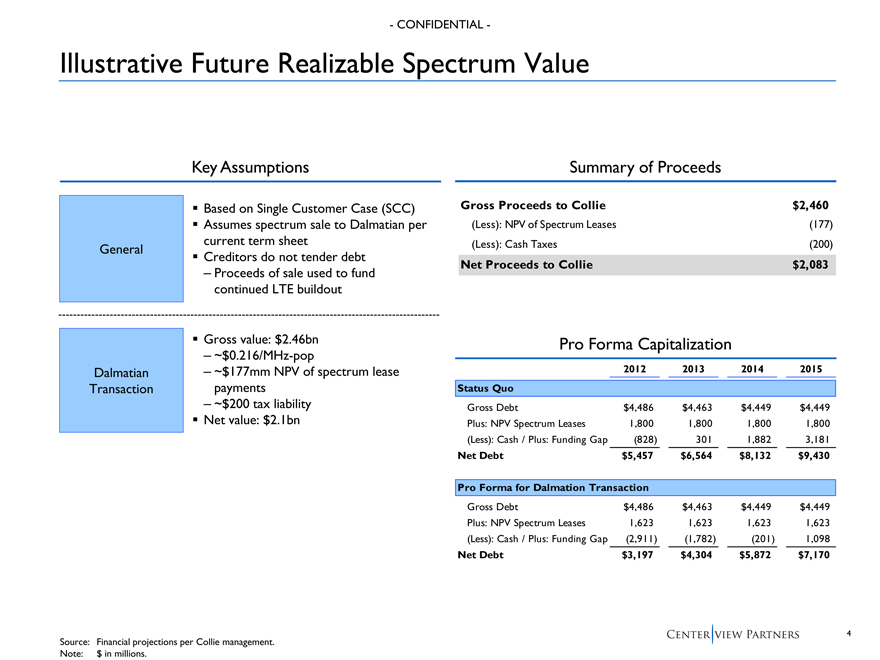

Illustrative Future Realizable Spectrum Value

Key Assumptions Summary of Proceeds

Based on Single Customer Case (SCC) Gross Proceeds to Collie $2,460

Assumes spectrum sale to Dalmatian per (Less): NPV of Spectrum Leases (177)

current term sheet (Less): Cash Taxes (200)

General

Creditors do not tender debt

Net Proceeds to Collie $2,083

– Proceeds of sale used to fund continued LTE buildout

??Gross value: $2.46bn Pro Forma Capitalization

– ~$0.216/MHz-pop

Dalmatian – ~$177mm NPV of spectrum lease 2012 2013 2014 2015 Transaction payments Status Quo

– ~$200 tax liability Gross Debt $4,486 $4,463 $4,449 $4,449

Net value: $2.1bn Plus: NPV Spectrum Leases 1,800 1,800 1,800 1,800 (Less): Cash / Plus: Funding Gap (828) 301 1,882 3,181

Net Debt $5,457 $6,564 $8,132 $9,430

Pro Forma for Dalmation Transaction

Gross Debt $4,486 $4,463 $4,449 $4,449 Plus: NPV Spectrum Leases 1,623 1,623 1,623 1,623 (Less): Cash / Plus: Funding Gap (2,911) (1,782) (201) 1,098

Net Debt $3,197 $4,304 $5,872 $7,170

Source: Financial projections per Collie management. Note: $ in millions.

4

- CONFIDENTIAL -

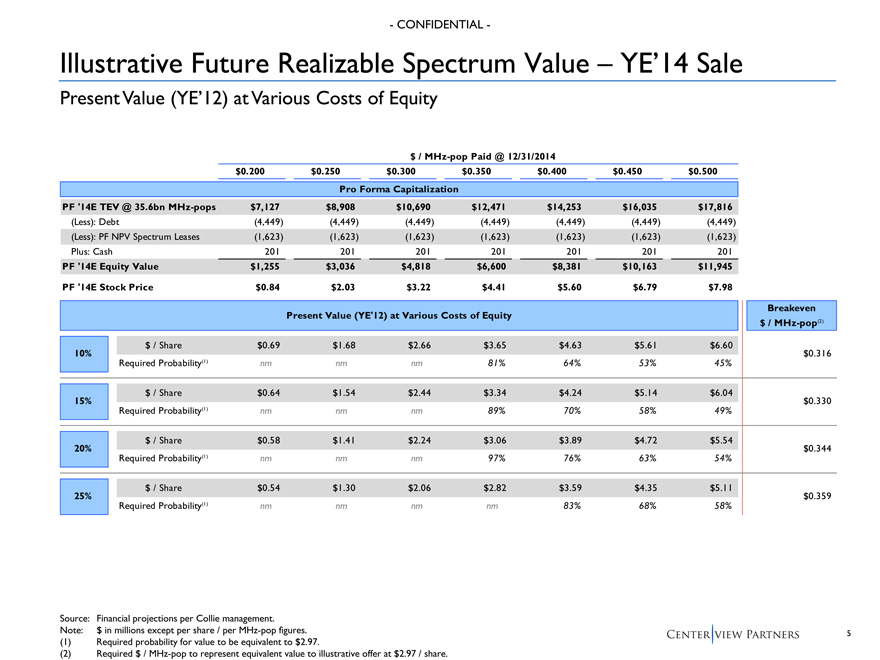

Illustrative Future Realizable Spectrum Value – YE’14 Sale

Present Value (YE’12) at Various Costs of Equity

$ / MHz-pop Paid @ 12/31/2014 $0.200 $0.250 $0.300 $0.350 $0.400 $0.450 $0.500 Pro Forma Capitalization PF ‘14E TEV @ 35.6bn MHz-pops $7,127 $8,908 $10,690 $12,471 $14,253 $16,035 $17,816

(Less): Debt (4,449) (4,449) (4,449) (4,449) (4,449) (4,449) (4,449) (Less): PF NPV Spectrum Leases (1,623) (1,623) (1,623) (1,623) (1,623) (1,623) (1,623) Plus: Cash 201 201 201 201 201 201 201

PF ‘14E Equity Value $1,255 $3,036 $4,818 $6,600 $8,381 $10,163 $11,945

PF ‘14E Stock Price $0.84 $2.03 $3.22 $4.41 $5.60 $6.79 $7.98

Breakeven Present Value (YE’12) at Various Costs of Equity

$ / MHz-pop(2)

$ / Share $0.69 $1.68 $2.66 $3.65 $4.63 $5.61 $6.60

10% $0.316 Required Probability(1) nm nm nm 81% 64% 53% 45%

$ / Share $0.64 $1.54 $2.44 $3.34 $4.24 $5.14 $6.04

15% $0.330 Required Probability(1) nm nm nm 89% 70% 58% 49%

$ / Share $0.58 $1.41 $2.24 $3.06 $3.89 $4.72 $5.54

20% $0.344 Required Probability(1) nm nm nm 97% 76% 63% 54%

$ / Share $0.54 $1.30 $2.06 $2.82 $3.59 $4.35 $5.11

25% $0.359 Required Probability(1) nm nm nm nm 83% 68% 58%

Source: Financial projections per Collie management. Note: $ in millions except per share / per MHz-pop figures. (1) Required probability for value to be equivalent to $2.97.

(2) Required $ / MHz-pop to represent equivalent value to illustrative offer at $2.97 / share.

5