Exhibit 99.1

PRO FORMA VALUATION REPORT

OCEAN SHORE HOLDING CO.

Ocean City, New Jersey

HOLDING COMPANY FOR:

OCEAN CITY HOME BANK

Ocean City, New Jersey

Dated As Of:

August 22, 2008

Prepared By:

RP® Financial, LC.

1700 North Moore Street

Suite 2210

Arlington, Virginia 22209

RP® FINANCIAL, LC.

Financial Services Industry Consultants

August 22, 2008

Boards of Directors

OC Financial MHC

Ocean Shore Holding Co.

Ocean City Home Bank

1001 Asbury Avenue

Ocean City, New Jersey 08226-3329

Members of the Boards of Directors:

At your request, we have completed and hereby provide an independent appraisal (“Appraisal”) of the estimated pro forma market value of the common stock to be issued by Ocean Shore Holding Co., Ocean City, New Jersey (“OSHC” or the “Company”) in connection with the mutual-to-stock conversion of OC Financial MHC (the “MHC”). The MHC currently has a majority ownership interest in, and its principal asset consists of, approximately 57.20% of the common stock of OSHC (the “MHC Shares”), the mid-tier holding company for Ocean City Home Bank, Ocean City, New Jersey (the “Bank”). The remaining 42.80% of OSHC’s common stock is owned by public stockholders. OSHC, which completed its initial public stock offering in December 2004, owns 100% of the common stock of the Bank. It is our understanding that OSHC will offer its stock, representing the majority ownership interest held by the MHC, in a subscription offering to Eligible Account Holders, Supplemental Eligible Account Holders and Other Members. To the extent that shares remain available for purchase after satisfaction of all subscriptions received in the subscription offering, the shares may be offered for sale in a community offering to members of the local community and the public at large.

This Appraisal is furnished pursuant to the requirements of the Code of Federal Regulations 563b.7 and has been prepared in accordance with the “Guidelines for Appraisal Reports for the Valuation of Savings and Loan Associations Converting from Mutual to Stock Form of Organization” of the Office of Thrift Supervision (“OTS”), which have been adopted in practice by the Federal Deposit Insurance Corporation (“FDIC”).

Plan of Conversion and Stock Issuance

On August 20, 2008, the respective Boards of Directors of the MHC, the Company and the Bank adopted a Plan of Conversion and Reorganization (the “Plan of Conversion”), pursuant to which the mutual holding company will convert to the stock form of organization. Pursuant to the Plan of Conversion, (i) the MHC will convert to stock form, (ii) the MHC and the Company will merge into the Bank and the Bank will become a wholly owned subsidiary of a newly chartered stock company (the “Company”), (iii) the shares of common stock of the Company held by persons other than the MHC will be converted into shares of common stock of the Company pursuant to an exchange ratio designed to preserve the percentage ownership

| Washington Headquarters | ||

| Rosslyn Center | Telephone: (703) 528-1700 | |

| 1700 North Moore Street, Suite 2210 | Fax No.: (703) 528-1788 | |

| Arlington, VA 22209 | Toll-Free No.: (866) 723-0594 | |

| www.rpfinancial.com | E-Mail: mail@rpfinancial.com |

Boards of Directors

August 22, 2008

Page 2

interests of such persons, and (iv) the Company will offer and sell shares of its common stock to certain depositors of the Bank, residents of Bank’s local community and shareholders of the Company and others in the manner and subject to the priorities set forth in the Plan of Conversion. As of August 22, 2008, the MHC’s ownership interest in OSHC approximated 57.20%. The Company will also issue shares of its common stock to the public stockholders of OSHC pursuant to an exchange ratio that will result in the public shareholders owning the same aggregate percentage of the newly issued OSHC common stock as owned immediately prior to the conversion. As of August 22, 2008, the public stockholders’ ownership interest in OSHC approximated 42.80%.

RP® Financial, LC.

RP® Financial, LC. (“RP Financial”) is a financial consulting firm serving the financial services industry nationwide that, among other things, specializes in financial valuations and analyses of business enterprises and securities, including the pro forma valuation for savings institutions converting from mutual-to-stock form. The background and experience of RP Financial is detailed in Exhibit V-1. We believe that, except for the fee we will receive for our appraisal, we are independent of the Company, the Bank, the MHC and the other parties engaged by the Bank or the Company to assist in the stock conversion process.

Valuation Methodology

In preparing our Appraisal, we have reviewed the regulatory applications of OSHC, the Bank and the MHC, including the prospectus as filed with the OTS and the Securities and Exchange Commission (“SEC”). We have conducted a financial analysis of OSHC, the Bank and the MHC that has included a review of audited financial information for fiscal years ended December 31, 2003 through 2007, a review of various unaudited information and internal financial reports through June 30, 2008, and due diligence related discussions with OSHC’s management; Deloitte & Touche, LLP, the Company’s independent auditor; Kilpatrick Stockton, LLP, the Company’s conversion counsel; and Sandler O’Neill & Partners, L.P., the Company’s financial and marketing advisor in connection with the stock offering. All assumptions and conclusions set forth in the Appraisal were reached independently from such discussions. In addition, where appropriate, we have considered information based on other available published sources that we believe are reliable. While we believe the information and data gathered from all these sources are reliable, we cannot guarantee the accuracy and completeness of such information.

We have investigated the competitive environment within which OSHC operates and have assessed OSHC’s relative strengths and weaknesses. We have kept abreast of the changing regulatory and legislative environment for financial institutions and analyzed the potential impact on OSHC and the industry as a whole. We have analyzed the potential effects of the stock conversion on OSHC’s operating characteristics and financial performance as they relate to the pro forma market value of OSHC. We have analyzed the assets held by the MHC, which will be consolidated with OSHC’s assets and equity pursuant to the completion of conversion. We have reviewed the economic and demographic characteristics of the Company’s primary market area. We have compared OSHC’s financial performance and condition with selected publicly-traded thrifts in accordance with the Valuation Guidelines, as

Boards of Directors

August 22, 2008

Page 3

well as all publicly-traded thrifts and thrift holding companies. We have reviewed the current conditions in the securities markets in general and the market for thrift stocks in particular, including the market for existing thrift issues, initial public offerings by thrifts and thrift holding companies, and second-step conversion offerings. We have excluded from such analyses thrifts subject to announced or rumored acquisition, and/or institutions that exhibit other unusual characteristics.

The Appraisal is based on OSHC’s representation that the information contained in the regulatory applications and additional information furnished to us by OSHC and its independent auditor, legal counsel and other authorized agents are truthful, accurate and complete. We did not independently verify the financial statements and other information provided by OSHC, or its independent auditor, legal counsel and other authorized agents nor did we independently value the assets or liabilities of OSHC. The valuation considers OSHC only as a going concern and should not be considered as an indication of OSHC’s liquidation value.

Our appraised value is predicated on a continuation of the current operating environment for OSHC and for all thrifts and their holding companies. Changes in the local, state and national economy, the legislative and regulatory environment for financial institutions and mutual holding companies, the stock market, interest rates, and other external forces (such as natural disasters or significant world events) may occur from time to time, often with great unpredictability and may materially impact the value of thrift stocks as a whole or the value of OSHC’s stock alone. It is our understanding that there are no current plans for selling control of OSHC following completion of the second-step stock offering. To the extent that such factors can be foreseen, they have been factored into our analysis.

The estimated pro forma market value is defined as the price at which OSHC’s common stock, immediately upon completion of the second-step stock offering, would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or sell and both having reasonable knowledge of relevant facts.

Valuation Conclusion

It is our opinion that, as of August 22, 2008, the estimated aggregate pro forma valuation of the shares to be issued in the conversion of the MHC, including: (1) newly-issued shares representing the MHC’s ownership interest in OSHC, and (2) exchange shares issued to existing public shareholders of OSHC, was $78,670,386 at the midpoint, equal to 8,741,204 shares at a per share value of $9.00. The resulting range of value pursuant to regulatory guidelines and the corresponding number of shares based on the Board approved $9.00 per share offering price is set forth below.

Boards of Directors

August 22, 2008

Page 4

| Total Shares | Offering Shares | Exchange Shares Issued to the Public Shareholders | Exchange Ratio | ||||||||||

Shares | (x | ) | |||||||||||

Maximum | 10,052,384 | 5,750,000 | 4,302,384 | 1.20773 | |||||||||

Midpoint | 8,741,204 | 5,000,000 | 3,741,204 | 1.05020 | |||||||||

Minimum | 7,430,023 | 4,250,000 | 3,180,023 | 0.89267 | |||||||||

Distribution of Shares | |||||||||||||

Maximum | 100.00 | % | 57.20 | % | 42.80 | % | |||||||

Midpoint | 100.00 | % | 57.20 | % | 42.80 | % | |||||||

Minimum | 100.00 | % | 57.20 | % | 42.80 | % | |||||||

Aggregate Market Value(1) | |||||||||||||

Maximum | 90,471,456 | $ | 51,750,000 | 38,721,456 | |||||||||

Midpoint | 78,670,836 | $ | 45,000,000 | 33,670,836 | |||||||||

Minimum | 66,870,207 | $ | 38,250,000 | 28,620,207 | |||||||||

| (1) | Based on offering price of $9.00 per share. |

Establishment of the Exchange Ratio

OTS regulations provide that in a conversion of a mutual holding company, the minority stockholders are entitled to exchange the public shares for newly issued shares of OSHC stock as a fully converted company. The Board of Directors of the MHC has independently determined the exchange ratio. The determined exchange ratio has been designed to preserve the current aggregate percentage ownership in OSHC equal to 57.20% as of June 30, 2008. The exchange ratio to be received by the existing minority shareholders of OSHC will be determined at the end of the offering, based on the total number of shares sold in the subscription and community offerings. Based upon this calculation, and the valuation conclusion and offering range concluded above, the exchange ratio would be 0.89267 shares, 1.05020 shares, and 1.20773 shares of newly issued shares of OSHC stock for each share of stock held by the public shareholders at the minimum, midpoint, and maximum of the offering range, respectively. RP Financial expresses no opinion on the proposed exchange of newly issued Company shares for the shares held by the public stockholders or on the proposed exchange ratio.

Limiting Factors and Considerations

Our valuation is not intended, and must not be construed, as a recommendation of any kind as to the advisability of purchasing shares of the common stock. Moreover, because such valuation is necessarily based upon estimates and projections of a number of matters, all of

Boards of Directors

August 22, 2008

Page 5

which are subject to change from time to time, no assurance can be given that persons who purchase shares of common stock in the conversion will thereafter be able to buy or sell such shares at prices related to the foregoing valuation of the estimated pro forma market value thereof. The appraisal reflects only a valuation range as of this date for the pro forma market value of OSHC immediately upon issuance of the stock and does not take into account any trading activity with respect to the purchase and sale of common stock in the secondary market following the completion of the second-step offering.

RP Financial’s valuation was based on the financial condition, operations and shares outstanding of OSHC as of June 30, 2008, the date of the financial data included in the prospectus. The proposed exchange ratio to be received by the current public stockholders of OSHC and the exchange of the public shares for newly issued shares of OSHC common stock as a full public company was determined independently by the Boards of Directors of the MHC, OSHC and the Bank. RP Financial expresses no opinion on the proposed exchange ratio to public stockholders or the exchange of public shares for newly issued shares.

RP Financial is not a seller of securities within the meaning of any federal and state securities laws and any report prepared by RP Financial shall not be used as an offer or solicitation with respect to the purchase or sale of any securities. RP Financial maintains a policy which prohibits RP Financial, its principals or employees from purchasing stock of its client institutions.

This valuation will be updated as provided for in the conversion regulations and guidelines. These updates will consider, among other things, any developments or changes in the financial performance and condition of OSHC, management policies, and current conditions in the equity markets for thrift shares, both existing issues and new issues. These updates may also consider changes in other external factors which impact value including, but not limited to: various changes in the legislative and regulatory environment for financial institutions, the stock market and the market for thrift stocks, and interest rates. Should any such new developments or changes be material, in our opinion, to the valuation of the shares, appropriate adjustments to the estimated pro forma market value will be made. The reasons for any such adjustments will be explained in the update at the date of the release of the update. The valuation will also be updated at the completion of OSHC’s stock offering.

| Respectfully submitted, |

RP® FINANCIAL, LC.

/s/ James P. Hennessey |

| James P. Hennessey |

| Director |

| RP® Financial, L.C | TABLE OF CONTENTS | |

| i |

TABLE OF CONTENTS

OCEAN SHORE HOLDING CO.

OCEAN CITY HOME BANK

Ocean City, New Jersey

DESCRIPTION | PAGE NUMBER | |||

CHAPTER ONE | OVERVIEW AND FINANCIAL ANALYSIS | |||

Introduction | I.1 | |||

Plan of Conversion and Reorganization | I.2 | |||

Purpose of the Reorganization | I.2 | |||

Strategic Overview | I.3 | |||

Balance Sheet Trends | I.6 | |||

Income and Expense Trends | I.11 | |||

Interest Rate Risk Management | I.16 | |||

Lending Activities and Strategy | I.17 | |||

Asset Quality | I.20 | |||

Funding Composition and Strategy | I.21 | |||

Subsidiaries | I.22 | |||

Legal Proceedings | I.22 | |||

CHAPTER TWO | MARKET AREA | |||

Introduction | II.1 | |||

Market Area Demographics | II.2 | |||

Summary of Local Economy and Workforce | II.4 | |||

Unemployment Trends | II.8 | |||

Market Area Deposit Characteristics | II.8 | |||

CHAPTER THREE | PEER GROUP ANALYSIS | |||

Peer Group Selection | III.1 | |||

Financial Condition | III.6 | |||

Income and Expense Components | III.9 | |||

Loan Composition | III.12 | |||

Credit Risk | III.12 | |||

Interest Rate Risk | III.15 | |||

Summary | III.17 | |||

| RP® Financial, L.C | TABLE OF CONTENTS | |

| ii |

TABLE OF CONTENTS

OCEAN SHORE HOLDING CO.

OCEAN CITY HOME BANK

Ocean City, New Jersey

(continued)

DESCRIPTION | PAGE NUMBER | |||||

| CHAPTER FOUR | VALUATION ANALYSIS | |||||

Introduction | IV.1 | |||||

Appraisal Guidelines | IV.1 | |||||

RP Financial Approach to the Valuation | IV.1 | |||||

Valuation Analysis | IV.2 | |||||

1. Financial Condition | IV.3 | |||||

2. Profitability, Growth and Viability of Earnings | IV.4 | |||||

3. Asset Growth | IV.5 | |||||

4. Primary Market Area | IV.5 | |||||

5. Dividends | IV.7 | |||||

6. Liquidity of the Shares | IV.7 | |||||

7. Marketing of the Issue | IV.8 | |||||

| A. | The Public Market | IV.8 | ||||

| B. | The New Issue Market | IV.15 | ||||

| C. | The Acquisition Market | IV.17 | ||||

| D. | Trading in OSHC’s Stock | IV.17 | ||||

8. Management | IV.18 | |||||

9. Effect of Government Regulation and Regulatory Reform | IV.18 | |||||

Summary of Adjustments | IV.19 | |||||

Valuation Approaches | IV.19 | |||||

1. Earnings Approach (“P/E” and “Core P/E”) | IV.21 | |||||

2. Book Value Approach (“P/B” and “P/TB”) | IV.21 | |||||

3. Assets Approach (“P/A”) | IV.22 | |||||

Valuation Conclusion | IV.22 | |||||

Establishment of the Exchange Ratio | IV.23 | |||||

| RP® Financial, LC. | LIST OF TABLES | |

| iii |

LIST OF TABLES

OCEAN SHORE HOLDING CO.

OCEAN CITY HOME BANK

Ocean City, New Jersey

TABLE | DESCRIPTION | PAGE | ||

| 1.1 | Historical Balance Sheets | I.7 | ||

| 1.2 | Historical Income Statements | I.12 | ||

| 2.1 | Map of Branch Locations | II.1 | ||

| 2.2 | Summary Demographic Data | II.3 | ||

| 2.3 | Estimated and Projected Employment | II.5 | ||

| 2.4 | Major Employers in Cape May and Atlantic Counties | II.7 | ||

| 2.5 | Unemployment Trends | II.8 | ||

| 2.6 | Cape May County and Atlantic County Deposit Detail | II.9 | ||

| 3.1 | Peer Group of Publicly-Traded Thrifts | III.3 | ||

| 3.2 | Balance Sheet Composition and Growth Rates | III.7 | ||

| 3.3 | Income as a % of Average Assets and Yields, Costs, Spreads | III.10 | ||

| 3.4 | Loan Portfolio Composition and Related Information | III.13 | ||

| 3.5 | Credit Risk Measures and Related Information | III.14 | ||

| 3.6 | Interest Rate Risk Measures and Net Interest Income Volatility | III.16 | ||

| 4.1 | Peer Group Market Area Comparative Analysis | IV.6 | ||

| 4.2 | Pricing Characteristics and After-Market Trends | IV.16 | ||

| 4.3 | Public Market Pricing | IV.24 | ||

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I. 1 |

I. OVERVIEW AND FINANCIAL ANALYSIS

Introduction

Ocean City Home Bank (the “Bank”), organized in 1887, is a federally chartered stock savings bank which conducts operations through its main office in Ocean City, New Jersey. The Bank serves the southern New Jersey shore communities through a main office and branch office which are situated in Cape May County and six branch offices which are situated in Atlantic County. The Bank’s markets are in the southeastern corner of New Jersey, approximately 65 miles east of Philadelphia and 130 miles south of New York.

Ocean Shore Holding Co. (“OSHC” or the “Company”) was organized on April 22, 1998, concurrent with the Bank’s reorganization from a federally-chartered mutual savings bank into a two-tiered mutual holding company structure. In conjunction with the reorganization, OC Financial, MHC (the “MHC”), was formed and concurrently owns all the capital stock of the Company. No stock was issued publicly pursuant to the reorganization. The Bank transferred $100,000 of retained earnings to the Company and $50,000 of retained earnings to the MHC. At the same time, the Bank converted to a federally-chartered stock savings bank with the Company owning all of its outstanding stock. The Company is a unitary savings and loan holding company and conducts its operations primarily through the Bank.

On December 21, 2004, the Company completed a minority stock issuance, selling a minority ownership position (i.e., 45.7% of the total outstanding shares) to the public while the MHC retained a majority ownership interest (54.3% ownership). Gross proceeds raised in pursuant to the minority stock issuance totaled $38.4 million while additional shares with a value of $1.7 million based on the IPO price of $10.00 per share were contributed to the Ocean City Home Charitable Foundation, Inc. (the “Foundation”) resulting in no cash proceeds for the Company.

The most significant asset of the Company is its equity investment in the Bank; in addition, the Company has extended a loan to the Bank’s employee stock ownership plan (“ESOP”). As of June 30, 2008, the Company had $657.8 million in assets, $413.7 million in deposits and total equity of $63.6 million, or 9.66% of total assets. The Company’s audited financial statements are included by reference as Exhibit I-1. The Bank is a member of the Federal Home Loan Bank (“FHLB”) system, and its deposits are insured up to the regulatory maximums by the Federal Deposit Insurance Corporation (“FDIC”).

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I. 2 |

Plan of Conversion and Reorganization

On August 19, 2008, OSHC announced that the Boards of Directors of the MHC, OSHC and the Bank unanimously adopted a Plan of Conversion and Reorganization (the “Plan of Conversion”), pursuant to which OSHC will convert from the two-tier MHC structure to the full stock holding company structure and concurrently conduct a second-step conversion offering (“Second Step Conversion” or “Offering”) that will represent the MHC’s ownership interest in OSHC. As of June 30, 2008, the MHC’s ownership interest in OSHC approximated 57.1%. Pursuant to the plan of conversion, OSHC, which owns 100% of the Bank, will be succeeded by a new federally chartered stock corporation named OSHC Group, Inc. (“OSHC” or the “Company”). The Company will also issue exchange shares of its common stock to the public shareholders pursuant to an exchange ratio that will result in the same 42.9% aggregate ownership percentage as immediately before the Offering.

Purpose of the Reorganization

The Second Step Conversion will increase the capital level to support further expansion, improve the overall competitive position of OSHC in the local market area, enhance profitability and reduce interest rate risk. Importantly, the additional equity will provide a larger capital base for continued growth and diversification, as well as increase the lending capability including the funds available for lending. Future growth opportunities are expected through the current branch network as well as through de novo branching in the regional markets served. Additionally, the Company anticipates that growth opportunities will result from regional bank consolidation in the local market, particularly in the current economic and operating environment, and the resulting fallout of customers who are attracted to OSHC’s customer service and products and services. The MHC structure has limited the opportunity to acquire other institutions – so the Second Step Conversion should facilitate the Company’s ability to pursue such acquisitions through increased capital as well as the ability to use common stock as merger consideration. Further, the Second Step Conversion will increase the public ownership, which is expected to improve the liquidity of the common stock.

The projected use of stock proceeds is highlighted below.

| • | The Company. The Company is expected to retain up to 50% of the net conversion proceeds. At present, Company funds, net of the loan to the ESOP, are expected to be invested initially into high quality investment securities with short- to intermediate-term maturities, generally consistent |

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I. 3 |

with the current investment mix. Over time, Company funds are anticipated to be utilized for various corporate purposes, possibly including acquisitions, infusing additional equity into the Bank, repurchases of common stock, and the payment of regular and/or special cash dividends. |

| • | The Bank. The balance of the net offering proceeds will be infused into the Bank. Cash proceeds (i.e., net proceeds less deposits withdrawn to fund stock purchases) infused into the Bank are anticipated to become part of general operating funds, and are expected to initially be invested in short-term investments pending longer term deployment, i.e., funding lending activities, general corporate purposes and/or expansion and diversification. |

The Company expects to continue to pursue a controlled growth strategy, leveraging its strong pro forma capital, growing primarily through the current delivery channels. If appropriate, OSHC may also consider various capital management strategies to assist in the long-run objective of increasing return on equity.

Strategic Overview

Throughout much of its corporate history, the Company’s strategic focus has been that of a community-oriented financial institution with a primary focus on meeting the borrowing, savings and other financial needs of its local customers in Atlantic and Cape May Counties. In this regard, the Company has historically pursued a residential lending strategy for portfolio, with a moderate level of diversification into construction lending and commercial real estate lending. The Company has emphasized high quality and flexible customer service, capitalizing on its local orientation and relatively broad array of products and services.

In the early 1990s, the Company was a relatively small institution with approximately $100 million in total assets and conducted operations through two offices. Subsequently, under the direction of current management, OSHC embarked on a growth and expansion strategy which included: (1) adding six branch offices in the regional area; (2) increasing total assets to more than $650 million as of June 30, 2008. The Company’s growth has been facilitated by the development of targeted niches which have included focusing on residential mortgage lending including jumbo loans and/or loans secured by second homes and investment properties (estimated to approximate 50% of the residential mortgage portfolio), adoption of a sales culture to facilitate growth of lower costing savings and transaction accounts including accounts to commercial customers. The Company has also been successful in implementing a deposit program for local municipalities.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I. 4 |

The Company’s branching strategy commenced in 1994 with the opening of the Ventnor and Linwood offices. While the addition of these two offices substantially bolstered the market presence, they also entailed significant startup costs, thereby impairing the near term earnings position. The reduced earnings coupled with its modest capital surplus, led management to pursue the MHC reorganization for the purpose of issuing debt at the mid-tier level to bolster the Bank’s capital position (the timing of the debt issuance was prior to the completion of the minority stock issuance within the MHC structure in 2004). The additional capital, both through debt issued prior to the minority stock issuance and from the common equity raised through the minority stock issuance in 2004 facilitated the ability to pursue additional branching opportunities – the Egg Harbor Township office opened in 1998, the Absecon office opened in 2002, and the Northfield and Margate branches opened in 2005 and 2006, respectively.

Residential loan growth has been facilitated by the employment of two commissioned loan originators while growth of the commercial loan portfolio has been fostered by the employment of four experienced commercial lenders (including two in executive management) as well as support staff. The majority of the Company’s residential mortgage loans are originated internally by the Company’s commissioned loan officers. As noted above, OSHC has developed a niche in the area of residential mortgage lending including lending on second homes and investment properties in the local market. Moreover, jumbo mortgage lending (i.e., loans above the conforming loan limits) has always been an important element of the Company’s mortgage lending.

The majority of the Company’s permanent residential mortgage volume has been in 15 and 30 year mortgage loans. As a portfolio lender (secondary market sales have been limited), the Company has willingly accepted the interest rate risk related to such loans while managing its interest rate risk exposure through other techniques.

In addition to residential mortgage lending, the Company has sought to diversify the portfolio to including commercial mortgage and non-mortgage loans as well as construction loans. With the increased emphasis on the development of commercial account relationships, OSHC has developed extensive policies and procedures pertaining to credit standards and the administration of commercial accounts. Additionally, the Company has employed a total of four loan officers who have local commercial lending experience to conduct the commercial lending

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I. 5 |

operations while also developing the appropriate support functions in the loan underwriting, credit administration and loan servicing functions. Despite the commercial loan growth, residential mortgage loans continue to comprise the largest portion of the loan portfolio at $444.9 million, or 78.4% of total loans, as of June 30, 2008. In addition, the home equity loan portfolio has grown, and such loans totaled $57.1 million, or 10.1% of total loans, at June 30, 2008.

The Company’s interest-earning assets (“IEA”) also consist of interest-earning deposits and short-to-intermediate term investment securities and MBS, the majority of which are currently classified as available for sale (“AFS”). The Company’s general balance sheet objective is to deploy funds primarily into loans and maintain moderate balances of cash and investments, given the higher yields on loans. At the same time, this broad objective has been tempered as the Company has sought to utilize the investment portfolio as a means of shortening the average duration of the asset portfolio given the fixed rate lending emphasis. The liquidity of the investment portfolio has also been a key objective given the high proportion of transaction accounts.

Retail deposits have consistently served as the primary interest-bearing funding source for the Company. The Company has sought to increase the deposit base through management’s efforts to develop a comprehensive sales culture throughout the principal customer contact points of the Company. In this regard, OSHC’s focus has been on developing broad customer relationships emphasizing the value that the Company brings to the customer relationship as a whole. These sales oriented strategies have also been implemented to attract both commercial and consumer account relationships with a focus on building transaction accounts.

The Company’s focus on service and convenience has been reflected in both the renovation of existing branches and ongoing development of new branches. The Company has introduced alternative delivery mechanisms including ATMs, a telephone call center and Internet banking to support the relatively high level of transaction accounts. Partially as a result of the recent checking account growth, transaction and savings accounts currently comprise a larger portion of the Company’s deposit composition than certificate of deposits (“CDs”).

OSHC has sought to establish a niche in marketing transaction accounts to local municipalities and school districts. As of June 30, 2008, the Company had deposit relationships with five municipal governments and thirteen school districts. As of June 30, 2008, municipal

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I. 6 |

deposits totaled $56.1 million, equal to 13.6% of total deposits and 42.4% of interest-bearing checking accounts. Management believes that the success of this public unit deposit program is attributable to the high level of service provided, competitive rate structure and lower fee structure.

The Company has typically utilized borrowings in two different respects: (1) as a supplemental funding source to favorably manage funding costs and to manage interest rate risk; and (2) longer-term borrowings to finance growth and diversification as a supplement to funding operations through deposits. Following the Second Step Conversion, the Company believes it will continue to utilize FHLB advances when the “all in” cost of funds compares favorably to deposits.

The Company’s earnings base is largely dependent upon net interest income and operating expense levels, reflecting a traditional operating strategy. In this regard, the Company’s earnings from fiscal 2005 through 2007 were impacted by spread compression, reflecting the impact of Federal Reserve rate hikes which caused a flattening yield curve and rising funding costs for the Company. However, recent rate reductions by the Fed have positively impacted OSHC’s spreads which, coupled with balance sheet growth, has resulted in a favorable spread and overall earnings trend for the last several quarters.

The post-offering business plan of the Company is expected to be similar to the recent strategy with similar products and services. Specifically, the Company will continue to be an independent community-oriented financial institution with a commitment to local real estate and non-mortgage financing with operations funded by retail deposits, borrowings, equity capital and internal cash flows. The Company expects to continue to emphasize permanent residential mortgage lending and, to a lesser extent, commercial real estate and construction lending. Balance sheet growth is expected to be enhanced through the establishment of additional branches in the regional market (two de novo branches are targeted to be established within the next 18 months).

Balance Sheet Trends

Growth Trends

The Company’s strategy of growth and expansion, both through internal growth at existing branches and de novo branching, is evidenced in Table 1.1. Since December 31, 2003,

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I. 7 |

Table 1.1

Ocean Shore Holding Co.

Historical Balance Sheets

| As of the Fiscal Year Ended December 31, | As of June 30, 2008 | Compounded Annual Growth Rate | |||||||||||||||||||||||||||||||||||||

| 2003 | 2004 | 2005 | 2006 | 2007 | |||||||||||||||||||||||||||||||||||

| Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Pct(1) | |||||||||||||||||||||||||||

| ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | (%) | |||||||||||||||||||||||||||

Total Amount of: | |||||||||||||||||||||||||||||||||||||||

Assets | $ | 479,844 | 100.00 | % | $ | 528,444 | 100.00 | % | $ | 543,846 | 100.00 | % | $ | 562,260 | 100.00 | % | $ | 629,523 | 100.00 | % | $ | 657,837 | 100.00 | % | 7.26 | % | |||||||||||||

Securities -HTM | 3,807 | 0.79 | % | 10,544 | 2.00 | % | 9,729 | 1.79 | % | 5,266 | 0.94 | % | 4,657 | 0.74 | % | 4,407 | 0.67 | % | 3.31 | % | |||||||||||||||||||

Securities -AFS | 123,865 | 25.81 | % | 106,259 | 20.11 | % | 84,462 | 15.53 | % | 62,865 | 11.18 | % | 54,259 | 8.62 | % | 39,012 | 5.93 | % | -22.64 | % | |||||||||||||||||||

Loans receivable (net) | 301,778 | 62.89 | % | 340,585 | 64.45 | % | 412,005 | 75.76 | % | 433,342 | 77.07 | % | 528,058 | 83.88 | % | 567,312 | 86.24 | % | 15.06 | % | |||||||||||||||||||

Cash and cash equivalents | 28,759 | 5.99 | % | 47,396 | 8.97 | % | 13,400 | 2.46 | % | 33,357 | 5.93 | % | 9,540 | 1.52 | % | 10,978 | 1.67 | % | -19.27 | % | |||||||||||||||||||

Deposits | 390,274 | 81.33 | % | 415,328 | 78.59 | % | 416,914 | 76.66 | % | 417,024 | 74.17 | % | 415,231 | 65.96 | % | 413,735 | 62.89 | % | 1.31 | % | |||||||||||||||||||

FHLB advances | 10,000 | 2.08 | % | 10,000 | 1.89 | % | 27,000 | 4.96 | % | 54,000 | 9.60 | % | 120,230 | 19.10 | % | 149,190 | 22.68 | % | 82.32 | % | |||||||||||||||||||

Subordinated debt | 15,464 | 3.22 | % | 15,464 | 2.93 | % | 15,464 | 2.84 | % | 15,464 | 2.75 | % | 15,464 | 2.46 | % | 15,464 | 2.35 | % | 0.00 | % | |||||||||||||||||||

Other borrowings | 35,504 | 7.40 | % | 22,840 | 4.32 | % | 18,460 | 3.39 | % | 7,090 | 1.26 | % | 8,000 | 1.27 | % | 7,250 | 1.10 | % | -29.74 | % | |||||||||||||||||||

Equity | 23,975 | 5.00 | % | 59,795 | 11.32 | % | 60,568 | 11.14 | % | 62,551 | 11.12 | % | 63,047 | 10.02 | % | 63,551 | 9.66 | % | 24.19 | % | |||||||||||||||||||

Loans/Deposits | 77.32 | % | 82.00 | % | 98.82 | % | 103.91 | % | 127.17 | % | 137.12 | % | |||||||||||||||||||||||||||

Offices Open | 6 | 6 | 6 | 7 | 8 | 8 | |||||||||||||||||||||||||||||||||

| (1) | Percent of assets except as noted. |

Source: Ocean Shore Holding Co.’s prospectus, SNL Financial, and RP® Financial, LC. calculations.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I. 8 |

total assets increased at a 7.3% compounded annual rate, from $479.8 million to $657.8 million currently. Loans have realized a faster growth rate than total assets and thus increased in proportion to total assets, from 62.9% at December 31, 2003, to 86.2% at June 30, 2008, which limited the net interest margin compression during the challenging yield curve environment (i.e., modestly sloped to flat or slightly inverted yield curve) which prevailed during fiscal 2006 and 2007. Specifically, loans have increased at a 15.1% rate over the period from the end of fiscal 2003 through June 30, 2008, while investment securities diminished over the corresponding timeframe, both in dollar terms and in proportion to total assets.

The Company’s assets are funded through a combination of deposits, borrowings and retained earnings. Deposits have always comprised the majority of funding liabilities but growth has been limited over the last several years as asset growth has largely been funded by borrowings. Specifically, since the end of fiscal 2003, the balance of deposits has increased by $23.5 million to equal $413.7 million, and thus reflects a compounded annual growth rate of only 1.3%. At the same time, borrowings in the form of FHLB advances have increased from $10.0 million as of the end of fiscal 2003, to $149.2 million as of June 30, 2008, which reflects an 82.3% compounded annual growth rate. The balance of subordinated debt has remained unchanged since 2003, while reverse repurchase agreements have diminished.

Annual equity growth equaled 24.2% since the end of fiscal 2003, with the expanded equity base primarily reflecting the impact of retained earnings over the period and the minority stock issuance completed in fiscal 2004. Since the end of fiscal 2004, equity has increased from $59.8 million to $63.6 million which is attributable to retained earnings exceeding dividend payments and stock repurchases for the period. Modest growth of capital since completion of the minority stock issuance coupled with balance sheet growth achieved over the period resulted in a diminishing capital ratio since 2004. Specifically, the equity-to-assets ratio declined from 11.3% as of the end of fiscal 2004 (just after the 2004 minority stock issuance) to 9.7% as of June 30, 2008. Going forward, the post-offering equity growth rate is expected to be impacted by a number of factors including the higher level of capitalization, the reinvestment and leveraging of the offering proceeds, the expense of the stock benefit plans and the potential impact of dividends and stock repurchases.

Loans Receivable

Loans receivable totaled $567.3 million, or 86.2% of total assets, as of June 30, 2008, and reflects steady growth since year end 2003. Permanent 1-4 family mortgage loans

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I. 9 |

comprise the largest segment of the loan portfolio, equal to 78.4% of total loans. The residential mortgage loan portfolio consists primarily of fixed rate mortgage loans, which comprise the substantial majority of residential mortgage loans originated. The Company is a portfolio lender and typically retains the longer term fixed rate loans it originates; secondary market loan sales have been limited.

Notwithstanding the recent efforts to expand commercial lending, OSHC remains primarily a residential mortgage lender. Overall, mortgage loans (including loans secured by 1-4 family properties, multi-family and commercial mortgages and properties under construction) comprised 86.9% of total loans, while home equity loans comprised an additional 10.1% of total loans. Commercial and industrial loans (“C&I loans”) currently approximate 2.9% of total loans while consumer loans (excluding home equity loans) total less than 1% of total loans. Loan portfolio diversification to date has primarily been in commercial real estate lending.

Cash, Investments and Mortgage-Backed Securities

The intent of the Company’s investment policy is to provide adequate liquidity, to generate a favorable return on excess investable funds and to support the established credit and interest rate risk objectives. The ratio of cash and investments including MBS has fluctuated based primarily on loan demand and cash inflows from deposits and borrowings and has declined since the end of fiscal 2003, from 32.6% of assets to 8.3% as of June 30, 2008. The comparatively modest level of cash and investments currently is reflective of the Company’s general preference to invest in whole loans coupled with recent loan growth which has resulted in the redeployment of funds from investments into loans.

The Company’s investment securities and MBS equaled $43.4 million, or 6.6% of total assets, as of June 30, 2008, while cash and interest bearing deposits and term deposits totaled $11.0 million, or 1.7% of assets. As of June 30, 2008, the cash and investments portfolio consisted of cash, interest-earning deposits in other financial institutions, mortgage-backed securities issued by Ginnie Mae, Fannie Mae or Freddie Mac, U.S. government agency obligations and other high quality investments, including investment grade securities issued by corporations and municipalities. Additionally, the Company maintains permissible equity investments such as FHLB stock with a fair value of $8.0 million as of June 30, 2008. The Company’s investment securities are classified both as held-to-maturity (“HTM”) and available for sale (“AFS”), with the HTM portfolio primarily comprised of MBS (see Exhibit I-3 for the investment portfolio composition).

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I. 10 |

No major changes to the composition and practices with respect to the management of the investment portfolio are anticipated over the near term, except that it is expected that the Company will generally classify securities as AFS at the time of purchase (including MBS). The level of cash and investments is anticipated to increase initially following the Second Step Conversion, pending gradual redeployment into higher yielding loans.

Bank Owned Life Insurance

As of June 30, 2008, the balance of bank owned life insurance (“BOLI”) totaled $10.6 million,which reflects growth since the end of fiscal 2003 primarily owing to increases in the cash surrender value of the policies. The balance of the BOLI reflects the value of life insurance contracts on selected members of the Bank’s management and has been purchased with the intent to offset various benefit program expenses on a tax advantaged basis. The increase in the cash surrender value of the BOLI is recognized as an addition to other non-interest income on an annual basis.

Funding Structure

Since fiscal year-end 2003, deposits have increased at a 1.31% compounded annual rate. Deposit growth has been limited in recent periods owing to a conscious decision by the Company to limit deposits costs in a challenging earnings and spread environment which prevailed through fiscal 2007, preferring to rely primary on FHLB advances to fund asset growth achieved since fiscal 2003. The limited deposit growth which has been realized since fiscal 2005 has primarily been realized in the CD portfolio, which increased from $130.5 million or 31.3% of deposits as of the end of fiscal 2005, to 40.5% of deposits as of June 30, 2008.

Notwithstanding the recent growth in CDs in proportion to total deposits, checking and savings accounts continue to comprise the majority of the Company’s deposit base and reflect the success of marketing initiatives designed to attract savings and transaction accounts from local retail and business customers. Moreover, OSHC’s has enjoyed success in attracting business checking and sweep accounts and demand deposits for municipalities pursuant to a marketing initiative which commenced at the beginning of the decade. The municipal deposits totaled $56.1 million as of June 30, 2008, while municipal deposit balances outstanding are typically in the range of $50 million to $90 million and the Company has depository relationships with various municipal entities in southern New Jersey.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I. 11 |

The Company typically utilizes borrowings: (1) when such funds are priced attractively relative to deposits; (2) to lengthen the duration of liabilities; (3) to enhance earnings when attractive revenue enhancement opportunities arise; and (4) to generate additional liquid funds, if required. Borrowed funds, primarily consisting of FHLB advances have been the primary source of funds utilized to fund asset growth

A portion of the funds borrowed by the Company in the form of subordinated debt was infused into the Company to bolster regulatory capital to facilitate growth and branching initiatives. Subordinated debt totaled $15.5 million, equal to 2.4% of total assets as of June 30, 2008.

Equity

As a mutual institution, the Company’s equity was primarily impacted by the level of earnings. With the completion of the minority stock issuance in December 2004, OSHC’s equity was more than doubled to $59.8 million, or 11.3% of assets as of December 31, 2004. Since fiscal year end 2004 of the limited increase in retained earnings has reflected the Company’s capital strategies, including the payment of shareholder dividends and share repurchases. As a result, the Company’s equity has only grown to $63.6 million, as of June 30, 2008, reflecting a 1.8% compounded annual rate of growth since completion of the minority stock issuance. However, the equity ratio has declined since fiscal 2004 reflecting the impact of asset growth. The Bank maintained strong surpluses relative to its regulatory capital requirements at June 30, 2008, and thus qualified as a “well capitalized” institution. The offering proceeds will serve to further strengthen the Company’s regulatory capital position and support further growth. As discussed previously, the post-offering equity growth rate is expected to be impacted by a number of factors including the higher level of capitalization, the reinvestment of the offering proceeds, the expense of the stock benefit plans and the potential impact of dividends and stock repurchases.

Income and Expense Trends

Table 1.2 shows the Company’s historical income statements for the past five years and for the 12 months ended June 30, 2008. The Company’s core earnings were relatively stable from fiscal 2003 to fiscal 2004 when the Company was a mutual institution but subsequently increased in fiscal 2005 and 2006 as the benefit of reinvestment of the net conversion proceeds

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I. 12 |

Table 1.2

Ocean Shore Holding Co.

Historical Income Statements

| As of the Fiscal Year Ended December 31, | ||||||||||||||||||||||||||||||||||||||||||

| 2003 | 2004 | 2005 | 2006 | 2007 | For the 12 Months Ended June 30, 2008 | |||||||||||||||||||||||||||||||||||||

| Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | |||||||||||||||||||||||||||||||

| ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | |||||||||||||||||||||||||||||||

Interest Income | $ | 22,516 | 4.81 | % | $ | 22,722 | 4.52 | % | $ | 26,272 | 4.87 | % | $ | 29,839 | 5.31 | % | $ | 32,619 | 5.49 | % | $ | 34,765 | 5.72 | % | ||||||||||||||||||

Interest Expense | (10,015 | ) | -2.14 | % | (9,398 | ) | -1.87 | % | (11,017 | ) | -2.04 | % | (14,620 | ) | -2.60 | % | (17,481 | ) | -2.94 | % | (17,984 | ) | -2.96 | % | ||||||||||||||||||

Net Interest Income | $ | 12,501 | 2.67 | % | $ | 13,324 | 2.65 | % | $ | 15,255 | 2.83 | % | $ | 15,219 | 2.71 | % | $ | 15,138 | 2.55 | % | $ | 16,781 | 2.76 | % | ||||||||||||||||||

Provision for Loan Losses | (360 | ) | -0.08 | % | (360 | ) | -0.07 | % | (300 | ) | -0.06 | % | (300 | ) | -0.05 | % | (261 | ) | -0.04 | % | (270 | ) | -0.04 | % | ||||||||||||||||||

Net Interest Income after Provisions | $ | 12,141 | 2.59 | % | $ | 12,964 | 2.58 | % | $ | 14,955 | 2.77 | % | $ | 14,919 | 2.65 | % | $ | 14,877 | 2.51 | % | $ | 16,511 | 2.72 | % | ||||||||||||||||||

Other Operating Income | 2,008 | 0.43 | % | 2,389 | 0.48 | % | 2,316 | 0.43 | % | 2,332 | 0.41 | % | 2,622 | 0.44 | % | 2,727 | 0.45 | % | ||||||||||||||||||||||||

Operating Expense | (10,002 | ) | -2.14 | % | (11,002 | ) | -2.19 | % | (12,201 | ) | -2.26 | % | (12,806 | ) | -2.28 | % | (13,069 | ) | -2.20 | % | (13,318 | ) | -2.19 | % | ||||||||||||||||||

Net Operating Income | $ | 4,147 | 0.89 | % | $ | 4,351 | 0.87 | % | $ | 5,070 | 0.94 | % | $ | 4,445 | 0.79 | % | $ | 4,430 | 0.75 | % | $ | 5,920 | 0.97 | % | ||||||||||||||||||

Net Gain(Loss) on Sale of Securities | — | 0.00 | % | — | 0.00 | % | — | 0.00 | % | — | 0.00 | % | — | 0.00 | % | (362 | ) | -0.06 | % | |||||||||||||||||||||||

Expense of Charitable Foundation | — | 0.00 | % | (2,000 | ) | -0.40 | % | — | 0.00 | % | — | 0.00 | % | — | 0.00 | % | — | 0.00 | % | |||||||||||||||||||||||

Net Gain(Loss) on Sale of Loans | 118 | 0.03 | % | — | 0.00 | % | — | 0.00 | % | — | 0.00 | % | — | 0.00 | % | — | 0.00 | % | ||||||||||||||||||||||||

Total Non-Operating Income/(Expense) | $ | 118 | 0.03 | % | $ | (2,000 | ) | -0.40 | % | $ | — | 0.00 | % | $ | — | 0.00 | % | $ | — | 0.00 | % | $ | (362 | ) | -0.06 | % | ||||||||||||||||

Net Income Before Tax | $ | 4,265 | 0.91 | % | $ | 2,351 | 0.47 | % | $ | 5,070 | 0.94 | % | $ | 4,445 | 0.79 | % | $ | 4,430 | 0.75 | % | $ | 5,557 | 0.91 | % | ||||||||||||||||||

Income Taxes | (1,551 | ) | -0.33 | % | (1,045 | ) | -0.21 | % | (1,994 | ) | -0.37 | % | (1,296 | ) | -0.23 | % | (1,639 | ) | -0.28 | % | (2,068 | ) | -0.34 | % | ||||||||||||||||||

Net Income (Loss) Before Extraord. Items | $ | 2,714 | 0.58 | % | $ | 1,306 | 0.26 | % | $ | 3,076 | 0.57 | % | $ | 3,149 | 0.56 | % | $ | 2,791 | 0.47 | % | $ | 3,489 | 0.57 | % | ||||||||||||||||||

Estimated Core Net Income | ||||||||||||||||||||||||||||||||||||||||||

Net Income | $ | 2,714 | 0.58 | % | $ | 1,306 | 0.26 | % | $ | 3,076 | 0.57 | % | $ | 3,149 | 0.56 | % | $ | 2,791 | 0.47 | % | $ | 3,489 | 0.57 | % | ||||||||||||||||||

Addback(Deduct): Non-Recurring (Inc)/Exp | (118 | ) | -0.03 | % | 2,000 | 0.40 | % | — | 0.00 | % | — | 0.00 | % | — | 0.00 | % | 362 | 0.06 | % | |||||||||||||||||||||||

Tax Effect (2) | 47 | 0.01 | % | (799 | ) | -0.16 | % | — | 0.00 | % | — | 0.00 | % | — | 0.00 | % | (145 | ) | -0.02 | % | ||||||||||||||||||||||

Estimated Core Net Income | $ | 2,643 | 0.56 | % | $ | 2,507 | 0.50 | % | $ | 3,076 | 0.57 | % | $ | 3,149 | 0.56 | % | $ | 2,791 | 0.47 | % | $ | 3,707 | 0.61 | % | ||||||||||||||||||

Memo: | ||||||||||||||||||||||||||||||||||||||||||

Expense Coverage Ratio (3) | 124.99 | % | 121.11 | % | 125.03 | % | 118.84 | % | 115.83 | % | 126.00 | % | ||||||||||||||||||||||||||||||

Efficiency Ratio (4) | 68.94 | % | 70.02 | % | 69.44 | % | 72.96 | % | 73.59 | % | 68.27 | % | ||||||||||||||||||||||||||||||

Effective Tax Rate | 36.37 | % | 44.45 | % | 39.33 | % | 29.16 | % | 37.00 | % | 37.21 | % | ||||||||||||||||||||||||||||||

| (1) | Reflects income and expense as a percent of average assets. |

| (2) | Assumes a 39.94% effective tax rate for federal & state income taxes. |

| (3) | Net interest income divided by operating expenses. |

| (4) | Operating expenses as a percent of the sum of net interest income and other operating income (excluding gains on sale). |

Source: Ocean Shore Holding Co.’s prospectus, SNL Financial, and RP® Financial, LC. calculations.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I. 13 |

and balance sheet growth were realized into earnings. Earnings diminished in fiscal 2007 relative to the prior two fiscal years as net interest income diminished modest due to spread compression and as operating costs continued to increase. Earnings have been increasing in the most recent fiscal year to equal $3.5 million, or 0.56% of average assets, for the twelve months ended June 30, 2008, as reversion to a positively sloped yield curve environment has improved the Company’s interest rate spreads. These and other trends with respect to OSHC’s income and expenses will be discussed in the balance of this section.

Net Interest Income

Net interest income has grown over the period reflected in Table 1.2 primarily due to balance sheet growth and an increase in the proportion of higher yielding loans reflecting the redeployment of funds out of the cash and investment portfolio (the investment portfolio has been diminishing in recent periods). Specifically, net interest income increased from $12.5 million in fiscal 2003 to $16.8 million for the 12 months ended June 30, 2008. However, the ratio of net interest income to average has remained fluctuated modestly over the corresponding time frame, increasing to a peak level of 2.83% of average assets before diminishing to 2.55% of average assets in fiscal 2007. Net interest income increased to $16.8 million, or 2.76% of average assets for the twelve months ended June 30, 2008.

Spread compression was a key factor contributing to the flat level of net interest income experienced over the fiscal 2005 to 2007 periods while balance sheet growth prevented the level of net interest income from declining significantly. In this regard, the Federal Reserve increased the targeted federal funds rate to 5.25% through June 2006 and maintained this level for over a year through September 2007 leading to a flat to mildly inverted yield curve which adversely impacted OSHC’s interest rate spreads. Subsequent reductions in the targeted federal funds rate by the Federal Reserve have favorably impacted the Company’s yield-cost spreads.

Specifically, the Company’s interest rate spread decreased from 2.75% in fiscal 2005, to 2.40% in fiscal 2007 while increasing to 2.59% over the first six months of fiscal 2008 (see Exhibit I-4). The initial reinvestment of the offering proceeds should increase net interest income as the funds are reinvested, with longer-term earnings benefits realized through leveraging of the proceeds.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I. 14 |

Loan Loss Provisions

Provisions for loan losses have typically been limited reflecting the Company’s relatively strong asset quality historically and the secured nature of the loan portfolio; the majority of the loan portfolio is secured by real estate collateral in the Company’s relatively strong local market area. Going forward, the Company will continue to evaluate the adequacy of the level of general valuation allowances (“GVAs”) on a regular basis, and establish additional loan loss provisions in accordance with the Company’s asset classification and loss reserve policies.

For the 12 months ended June 30, 2008, loan loss provisions totaled $270,000, or 0.04% of average assets, which reflects modest growth in the loan portfolio rather than specific loan problems. The level of loan loss provisions also limited chargeoffs; loan chargeoffs equaled $4,000 in fiscal 2007 while there were no chargeoffs for the six months ended June 30, 2008.

Non-Interest Income

Other income has shown an upward trend in dollar terms and as a percent of average assets since fiscal 2003, from $2.0 million (0.43% of average assets) to $2.7 million (0.45% of average assets) for the 12 months ended June 30, 2008, reflecting OSHC’s balance sheet growth, expansion of overall business volumes and continued growth of fee generating products such as commercial lending and transaction accounts. The bulk of OSHC’s fee income is comprised of fees related to its depository activities, lending, and mortgage servicing. However, the Company has also diversified into non-traditional product lines (primarily brokerage services), which provide a modest amount fee income. Additionally, non-interest income was further enhanced by the purchase of BOLI, wherein the income from the increase in the cash surrender value of the policies is reflected as non-interest income. Growth in the level of non-interest operating income is expected to be gradual in future periods.

Operating Expenses

The Company’s operating expenses have increased in recent years due to asset growth, increased lending activities in both the residential and commercial portfolios, de novo branching and revenue diversification strategies. Specifically, cost increases reflect increased business volumes facilitated by the employment of seasoned commercial lenders and support

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I. 15 |

staff and the opening of four full service branch offices since 1998. While operating expenses have experienced a pronounced increase, commensurate asset growth resulted in limited growth of the ratio of operating expenses in relation to average assets. Specifically, fiscal 2003 operating expenses approximated $10.0 million, or 2.14% of average assets, while operating expenses approximated $13.3 million, or 2.19% of average assets, for the most recent 12 months period ending June 30, 2008.

Operating expenses are expected to increase on a post-offering basis as a result of the expense of the additional stock-related benefit plans, as well as the planned branching and growth initiatives which are currently underway. At the same time, continued balance sheet growth and reinvestment of the offering proceeds should largely offset the anticipated expense increase.

Non-Operating Income/Expense

Non-operating income and expenses have typically had a limited impact on earnings over the last several years, and have primarily consisted of gains on the sale of loans and investments. The most significant non-operating item was the expense of a charitable foundation established by the Company in connection with the minority stock issuance in 2004, which totaled $2.0 million. For the twelve months ended June 30, 2008, OSHC reported losses on securities totaling $362,000 (0.06% of average assets) reflecting a valuation impairment charge ($312,000) and a loss on the sale of securities ($50,000).

Taxes

The Company’s average tax rate has ranged between 29.16% and 44.45% over the last five fiscal years and equaled 37.21% for the 12 months ended June 30, 2008. The Company is evaluating the merits of establishing a special purpose investment subsidiary for the purpose of minimizing its state tax liability, which approximates 9.0% of pre-tax income. If the Company pursues this strategy, the Company’s marginal tax rate on taxable income may be reduced from approximately 40%, to as low as 37%, which would reflect its marginal federal corporate tax rate.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I. 16 |

Efficiency Ratio

The Company’s efficiency ratio fluctuated in a narrow range from 68.9% to 70.0% over the fiscal 2003 to 2005 period, while subsequently increasing (i.e., becoming less favorable) through fiscal 2007 to a level of 73.59%. The increasing trend during the fiscal 2005 to 2007 periods was consistent with the trend for core earnings over the period which were diminishing. The efficiency ratio diminished to 68.27% for the twelve months ended June 30, 2008, primarily reflecting the impact of the increasing level of net interest income. On a post-offering basis, the efficiency ratio may show some improvement from the benefit of reinvesting the proceeds from the Offering. However, a portion of the benefit is expected to be offset by the increased expense of the stock benefit plans.

Interest Rate Risk Management

The primary aspects of the Company’s interest rate risk management include:

| • | Diversifying portfolio loans into other types of shorter-term or adjustable rate lending, including commercial and construction lending; |

| • | Maintaining an investment portfolio, comprised of high quality, liquid securities and maintaining an ample balance of securities classified as available for sale; |

| • | Promoting transaction accounts (including municipal deposits) and, when appropriate, longer term CDs; |

| • | Utilizing longer-term borrowing when such funds are attractively priced relative to deposits and prevailing reinvestment opportunities; |

| • | Maintaining a strong capital level; |

| • | Increasing non-interest income; |

| • | Limiting investment in fixed assets and other non-earnings assets; and |

| • | Potentially selling a portion of the fixed rate mortgage loans originated based on risk and profitability considerations. |

The rate shock analysis as of June 30, 2008 (see Exhibit I-5) as prepared by OTS for the Company, reflects a liability sensitive position with the net portfolio value (“NPV”) declining by a 344 basis points pursuant to a positive 200 basis point instantaneous and permanent rate shock, resulting in a post-shock NPV ratio equal to 7.32%. The post-shock NPV ratio for the Company on a consolidated basis is not modeled but may likely be lower given its more leveraged structure on a reported basis. However, in addition to modeling the NPV ratio, the Company also projects the potential changes to its net interest income (“NII”) for a 12 and 24

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I. 17 |

month period under rising and falling interest rate scenarios. Pursuant to a positive 200 basis point instantaneous and permanent rate shock, the Company’s net interest income is projected to decrease by less than 7.2% within a 12 month period and by 8.0% over a 24 month period relative to the base case levels, providing evidence of a liability sensitive position over the short term.

Overall, the data indicates mixed that rising rates would have an adverse impact over the short term (i.e., over the next 24 month period). At the same time, there are numerous limitations inherent in such analyses such as the credit risk of Company’s loans pursuant to changing interest rates. Additionally, such analyses do not measure the impact of changing spread relationships as interest rates among various asset and liability accounts rarely move in tandem.

One factor impacting the Company’s interest rate risk which is particularly difficult to quantify is the degree to which deposits will reprice in a response to a change in interest rates. Several factors potentially make the Company’s deposit costs somewhat more volatile than many similar institutions. Specifically, the Company prices its deposits in the upper end of the competitive range which may result in a more rate sensitive depositor base. Additionally, the approximately $56.1 million of municipal transaction accounts as of June 30, 2008, carry rates which are tied to the 91 Day T-bill rate, in effect making these accounts highly sensitive to changes in short term money market rates.

Lending Activities and Strategy

The Company’s lending activities have been focused primarily on 1-4 family permanent mortgage lending. Lending diversification has largely included home equity loans, and to a lesser extent, loans secured by commercial real estate and multi-family loans, construction loans, and consumer loans. Details regarding the Company’s loan portfolio composition and characteristics are included in Exhibits I-6 and I-7. As of June 30, 2008, permanent first mortgage loans secured by residential properties totaled $444.9 million, equal to 78.4% of total loans, while home equity loans totaled $57.1 million, or 10.1% of loans. Commercial real estate and multi-family loans together approximated 6.6% of total loans; the remaining balance was comprised of construction loans and non-mortgage commercial and industrial (“C&I”) loans and various types of consumer credit.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I. 18 |

Residential Lending

As of June 30, 2008, residential mortgage loans equaled $444.9 million, or 78.5% of total loans, the majority of which were fixed rate mortgages. Adjustable rate mortgage (“ARM”) loans approximated $55.8 million as of June 30, 2008 (including hybrid loans). Although the Company originates both fixed rate and adjustable rate 1-4 family loans, market demand is dominated by fixed rate loans. While the Company’s fixed rate loans are offered with a wide range of terms, including 10, 15, 20, 25 and 30 years, the bulk of the recent origination activity has consisted of 15 and 30 year loans.

The majority of the 1-4 family residential mortgage loans conform to standards set by either Freddie Mac or Fannie Mae. Most non-conforming residential loans are non-conforming as to the loan amount (i.e., jumbo loans) or due to the characteristics of the property, while otherwise meeting the agency credit criteria. The Company originates 1-4 family loans up to a loan-to-value (“LTV”) ratio of 95%, with private mortgage insurance (“PMI”) being required for loans in excess of a 80% LTV ratio. The majority of the Company’s construction loan portfolio is secured by residential properties. The substantial portion of 1-4 family mortgage loans have been originated by the Company and are secured by residences in the local market.

As a result of the Company’s market presence in the southern New Jersey shore area, the residential mortgage portfolio has a relatively high proportion of mortgage loans secured by second homes or by investment properties (i.e., seasonal beach rental properties). In this regard, management estimates that approximately 50% the residential mortgage portfolio is comprised of loans secured by the borrower’s primary residence, while the balance is secured by either second homes or rental properties, thus raising the risk profile of such loans.

The Company’s home equity loans including fixed rate amortizing term loans (“HELs”) as well as variable rate lines of credit (“HELOCs”). Such loans typically have shorter maturities and higher interest rates than traditional 1-4 family lending. Home equity loans approximated $57.1 million as of June 30, 2008. When combined with the first mortgage loan, the Company will make home equity loans up to a 90% LTV.

Multi-Family and Commercial Mortgage Lending

Multi-family and commercial mortgage lending has been an area of portfolio diversification for the Company. Such loans are typically secured by properties in southern New Jersey and are generally originated by the Company but may include participation interests

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I. 19 |

purchased from other local lenders (including loans which are for low-to-moderate income housing). As of June 30, 2008, multi-family and commercial mortgage loans equaled $37.3 million (6.6% of loans).

Multi-family and commercial mortgage loans are typically offered with fixed rates of interest for the first five years of the loan, which are then subject to call provision or rate adjustment. Such loans typically possess terms ranging from one to five years, with amortization periods of five to 20 years, and LTV ratios of up to 80%, and target a debt-coverage ratio of at least 1.2 times. Multi-family and commercial real estate loans are secured by office buildings, retail and industrial use buildings, apartments and other structures such as strip shopping centers, retail shops and various other properties. Most income producing property loans originated by the Company are for the purpose of financing existing structures rather than new construction.

Construction Loans

Construction lending has been relatively modest overall in recent years as reflected in the construction loan balance of $10.8 million, equal to 1.9% of total loans. The Company originates residential and, to a lesser extent, commercial construction loans. Such lending shortens the average duration of assets and support asset yields. The Company generally limits such loans to known builders and developers with established lending relationships with the Company. The majority of the Company’s construction lending is in Atlantic and Cape May Counties. Construction loans generally have variable rates of interest, terms of up to 2 years (but most typically 12 months) and LTV ratios up to 90% for a residential property and 80% for a commercial property.

Non-Mortgage Lending

The Company’s efforts to increase commercial lending have primarily centered on the development of real estate secured relationships, as the balance of non-mortgage C&I loans are less than one-half the balance of the mortgage secured commercial and multi-family mortgage loan portfolio. As of June 30, 2008, C&I loans totaled $16.2 million, or 2.9% of total loans. The Company offers commercial loans to sole proprietorships, professional partnerships and various other small businesses. The types of commercial loans offered include lines of credit and business term loans. Most line of credit and business term loans are secured by real estate and other assets such as inventory or accounts receivable. The Company also offers time notes, letters of credit and loans guaranteed by the Small Business Administration.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I. 20 |

Consumer loans are generally offered to provide a full line of loan products to customers and typically include student loans, loans on deposits, auto loans, and unsecured personal loans. As of June 30, 2008, consumer loans excluding home equity loans totaled $820,000 million, equal to 0.1% of total loans.

Loan Originations, Purchases and Sales

Exhibit I-8 provides a historical summary of the Company’s lending activities. Consistent with its strategy, 1-4 family permanent mortgage and home equity lending comprised the substantial majority of loan originations over this time frame. Specifically, during fiscal 2007, permanent 1-4 family mortgage loan originations totaled $112.0 million (69.3% of total originations); home equity loan originations, which comprised the substantial majority of consumer loan originations, totaled an additional $27.9 million (17.3% of total originations). Originations of 1-4 family loans increased notably in fiscal 2007 (from $56.2 million in fiscal 2006) reflecting a favorable rate environment, more limited competition, and favorable growth trends locally, and the trend to increasing origination volumes has continued into fiscal 2008.

As reflected in Exhibit I-8, loan purchases and sales have been limited, as the Company is primarily a portfolio lender. Purchases totaled $12.7 million in fiscal 2007, but equaled only $2.3 million for the first six months of fiscal 2008. The last loan sale occurred in fiscal 2003 and totaled $5.1 million.

Asset Quality

The Company’s asset quality has historically been strong and the level of non-performing assets (“NPAs”) is low in relation to industry averages but has been trending upward in recent periods reflecting weakness in the local real estate market. As reflected in Exhibit I-9, the NPA balance was $1.9 million, equal to 0.29% total assets. The ratio of allowances to total loans equaled 0.44% while reserve coverage in relation to NPAs was 129.1% (see Exhibit I-10).

The Company has established detailed asset classification policies and procedures which are consistent with regulatory guidelines. Detailed asset classifications are reviewed monthly by senior management and the Board. Additionally, the Company performs a review of major loans (i.e., balances in excess of $1 million) at least annually while also performing

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I. 21 |

reviews of randomly selected homogenous loans. Pursuant to these procedures, when needed, the Company establishes additional valuation allowances to cover anticipated losses in classified or non-classified assets. Such reserve adequacy reviews are conducted by management on at least a quarterly basis.

Funding Composition and Strategy

Deposits have consistently been the Company’s primary source of funds. As of June 30, 2008, deposits totaled $413.7 million, which reflects a modest 1.3% compounded annual growth since the end of fiscal 2003. As previously discussed, the Company has consciously limited its offered deposit rates in recent periods owing to a challenging earnings and spread environment. In view of targeted loan and asset growth, OSHC has preferred to fund asset growth primarily through FHLB advances, which have increased by $139.2 million since the end of fiscal 2003, which reflects an 82.3% compounded annual rate of growth.

Deposit solicitation efforts for the Company have been facilitated by the opening of four branch offices since 1998, the development of a sales oriented call program, and the implementation of a strategy to solicit transaction accounts to local municipalities and school districts. Management believes that the Company’s deposit pricing places the Company in the upper end of the range of the local competition.

Lower costing savings and transaction accounts totaling $246.1 million comprised approximately 59.5% of the Company’s deposits at June 30, 2008 (see Exhibit I-11). The proportion of savings and transaction accounts reflects a modest decrease since fiscal 2005 both as a result of the level of competition locally and owing to increasing short term interest rates since 2005, which increased the relative attractiveness of CDs for many deposit customers. The balance of the deposit base is comprised of CDs ($167.6 million equal to 40.5% of total deposits), the majority of which have remaining maturities of one year or less. As of June 30, 2008, CDs with balances equal to or in excess of $100,000 equaled $56.9 million.

As of June 30, 2008, borrowed funds consisted of subordinated debt ($15.5 million), FHLB advances ($149.2 million) and other borrowed funds ($7.3 million), primarily consisting of variable rate or short term repos. As previously discussed, the subordinated debt was issued by the Company to provide additional capital for the Bank, and to provide investment income at the holding company level through reinvestment into MBS. The Repos have generally been employed to provide short term liquid funds for reinvestment into securities at a positive spread.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I. 22 |

The FHLB advances in the Company’s portfolio generally consist of fixed rate fixed term advances (though many are callable) obtained with objective of extending the duration of liabilities so as to minimize the Company’s interest rate risk exposure.

Subsidiary

The Company has one subsidiary, Seashore Financial Services, LLC., which is primarily involved in the sale of non-deposit investment and insurance products.

Legal Proceedings

Other than the routine legal proceedings that occur in the Company’s ordinary course of business, the Company is not involved in litigation which is expected to have a material impact on the Company’s financial condition or operations.

| RP® Financial, LC. | MARKET AREA | |

| II.1 |

II. MARKET AREA

Introduction

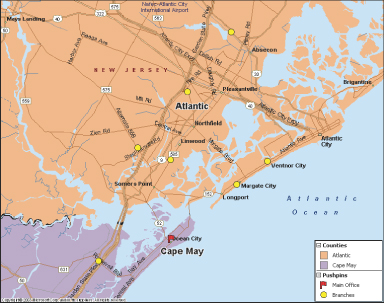

Established in 1887, the Bank has always been operated pursuant to a strategy of strong community service, which it continued after organizing into OSHC, and its dedication to being a community-oriented financial institution has supported customer loyalty and recent growth trends. OSHC is headquartered in Ocean City, New Jersey, and serves the southern New Jersey shore communities through a total of eight full service branches. A total of six branches are located in Atlantic County while two branches are situated in Cape May County. The Company’s markets are in the southeastern corner of New Jersey, approximately 65 miles east of Philadelphia and 130 miles south of New York.

The Company will continue to consider growth through the acquisition of branches or whole institutions if such opportunities should arise, while two de novo branches are planned for the next three years. A map showing the Company’s office coverage is set forth below and details regarding the Company’s offices and recent trends with respect to market interest rate levels are set forth in Exhibit II-1 and II-2, respectively.

Table 2.1

Ocean Shore Holding Co.

Map of Branch Locations

| RP® Financial, LC. | MARKET AREA |

II. 2