UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10

GENERAL FORM FOR REGISTRATION OF SECURITIES

Pursuant to Section 12(b) or (g) of the Securities Exchange Act of 1934

Keating Capital, Inc.

(Exact Name of Registrant as Specified in its Charter)

| Maryland | 26-2582882 | |

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) |

5251 DTC Parkway, Suite 1000

Greenwood Village, CO 80111

(Address of Principal Executive Offices and Zip Code)

(720) 889-0139

(Registrant’s Telephone Number, including Area Code)

with a copy to:

Cynthia M. Krus, Esq.

John J. Mahon, Esq.

Sutherland Asbill & Brennan LLP

1275 Pennsylvania Ave, NW

Washington, DC 20004-2415

(202) 637-3593 fax

Securities to be registered under Section 12(b) of the Act: None.

| Title of Each Class to be so Registered | Name of Each Exchange on Which Each Class is to be Registered | |

Securities to be registered pursuant to Section 12(g) of the Act:

Common Stock, par value $0.001 per share

(Title of class)

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer," "accelerated filer” and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer □ | Accelerated file □ |

Non-accelerated filer □ (Do not check if a smaller reporting company) | Smaller reporting company þ |

TABLE OF CONTENTS

| Page | ||

| Business. | ||

| Risk Factors. | ||

| Financial Information. | ||

| Properties. | ||

| Security Ownership of Certain Beneficial Owners and Management. | ||

| Directors and Executive Officers. | ||

| Executive Compensation. | ||

| Certain Relationships and Related Transactions, and Director Independence. | ||

| Legal Proceedings. | ||

| Market Price of and Dividends on the Registrant’s Common Equity and Related Stockholder Matters. | ||

| Recent Sales of Unregistered Securities. | ||

| Description of Registrant’s Securities to be Registered. | ||

| Indemnification of Directors and Officers. | ||

| Financial Statements and Supplementary Data. | ||

| Changes in and Disagreements with Accountants on Accounting and Financial Disclosure. | ||

| Financial Statements and Exhibits. |

i

EXPLANATORY NOTE

Keating Capital, Inc. is filing this registration statement on Form 10 (the “Registration Statement”) under the Securities Exchange Act of 1934, as amended (the “Exchange Act”) on a voluntary basis to provide current public information to the investment community, to comply with applicable requirements for the quotation or listing of its securities on a national securities exchange or other public trading market and to permit it to file an election to be regulated as a business development company under the Investment Company Act of 1940, as amended (the “1940 Act”). In this Registration Statement, the “Company,” “we,” “us,” and “our” refer to Keating Capital, Inc.

Once this Registration Statement is deemed effective, we will be subject to the requirements of Section 13(a) of the Exchange Act, including the rules and regulations promulgated thereunder, which will require us to file annual reports on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K, and we will be required to comply with all other obligations of the Exchange Act applicable to issuers filing registration statements pursuant to Section 12(g) of the Exchange Act.

Concurrently with the filing of this Registration Statement, we have filed an election to be regulated as a business development company under the 1940 Act. Upon filing of such election, we became subject to the 1940 Act requirements applicable to business development companies.

FORWARD LOOKING STATEMENTS

This Registration Statement contains forward-looking statements that involve substantial risks and uncertainties. These forward-looking statements are not historical facts, but rather are based on current expectations, estimates and projections about us, our prospective portfolio investments, our industry, our beliefs, and our assumptions. Words such as “anticipates,” “expects,” “intends,” “plans,” “believes,” “seeks,” “estimates,” “would,” “should,” “targets,” “projects,” and variations of these words and similar expressions are intended to identify forward-looking statements. These statements are not guarantees of future performance and are subject to risks, uncertainties, and other factors, some of which are beyond our control and difficult to predict and could cause actual results to differ materially from those expressed or forecasted in the forward-looking statements including, without limitation:

| • | an economic downturn could impair our portfolio companies’ abilities to continue to operate, which could lead to the loss of some or all of our investments in such portfolio companies; | |

| • | an economic downturn could disproportionately impact the public ready growth companies which we intend to target for investment, causing us to suffer losses in our portfolio and experience diminished demand for capital from these companies; | |

| • | an inability to access the equity markets could impair our investment activities; and | |

| • | the risks, uncertainties and other factors we identify in “Risk Factors” and elsewhere in this Registration Statement and in our filings with the SEC. |

Although we believe that the assumptions on which these forward-looking statements are based are reasonable, any of those assumptions could prove to be inaccurate, and as a result, the forward-looking statements based on those assumptions also could be inaccurate. In light of these and other uncertainties, the inclusion of a projection or forward-looking statement in this prospectus should not be regarded as a representation by us that our plans and objectives will be achieved. These risks and uncertainties include those described or identified in “Risk Factors” and elsewhere in this Registration Statement. You should not place undue reliance on these forward-looking statements, which apply only as of the date of this Registration Statement. We do not undertake any obligation to update or revise any forward-looking statements.

ii

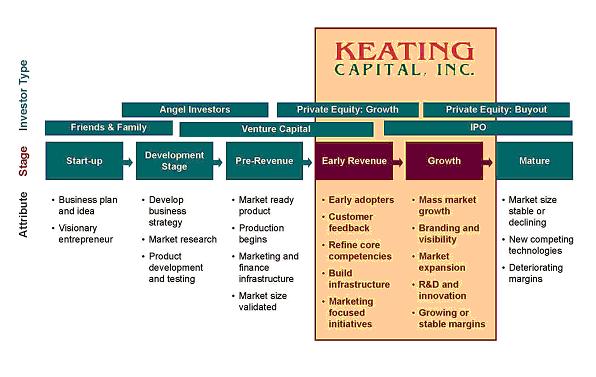

Background and Summary

We were incorporated on May 9, 2008 under the laws of the State of Maryland. Concurrently with the filing of this Registration Statement, we have filed an election to be regulated as a business development company under the 1940 Act. Keating Investments, LLC (“Keating Investments”) serves as our investment adviser and will also provide us with the administrative services necessary for us to operate. Keating Investments may also retain additional investment professionals in the future, based upon its needs.

Congress created business development companies in 1980 in an effort to help public capital reach smaller and growing private and public companies. We are designed to do precisely that. We intend to make minority, non-controlling equity investments in private businesses that are seeking growth capital and that we believe are committed to, and capable of, becoming public, which we refer to as “public ready” or “primed to become public.”

We intend to invest principally in equity securities and, to a lesser extent, debt securities of primarily non-public U.S.-based companies. Our investment objective is to maximize total return. In accordance with our investment objective, we intend to provide capital principally to U.S.-based, private companies with an equity value of less than $250 million, which we refer to as “micro-cap companies.” Our primary emphasis will be to generate capital gains through our equity investments in micro-cap companies. We may also make investments on an opportunistic basis in U.S.-based publicly-traded companies with market capitalizations of less than $250 million, as well as foreign companies that otherwise meet our investment criteria, subject to certain limitations imposed under the 1940 Act.

We intend to utilize a two-step investment process focused on an initial investment consisting of convertible debt and a subsequent follow-on investment consisting of common or convertible preferred stock or other equity, that will be contingent upon a portfolio company satisfying pre-established milestones towards the filing of a registration statement under the Securities Act of 1933, as amended (“Securities Act”) or the Exchange Act. Where appropriate, we may also negotiate to receive warrants, either as part of our initial or follow-on investments in our portfolio companies.

As an integral part of our initial investment, we intend to partner with and help prepare our portfolio companies to become public and meet the governance and eligibility requirements of a NASDAQ Capital Market listing. Because we believe that the initial public offering (“IPO”) market is virtually non-existent for micro-cap companies, we intend that our portfolio companies will go public through the filing of a registration statement under the Securities Act or the Exchange Act. We intend to invest in micro-cap companies that we believe will be able to file a registration statement with the U.S. Securities and Exchange Commission (“SEC”) within approximately three to twelve months after our initial investment. These registration statements will typically take the form of a resale registration statement filed by a portfolio company under the Securities Act coupled with a concurrent registration of the portfolio company’s common stock under the Exchange Act, or alternatively a stand-alone registration statement registering the common stock of a portfolio company under the Exchange Act without a concurrent registered offering under the Securities Act. While we expect the common stock of our portfolio companies to be quoted on the Over-the-Counter Bulletin Board (the “OTC Bulletin Board”) following the completion of the registration process, we intend to target investments in portfolio companies that we expect will be able to qualify for a NASDAQ Capital Market listing within approximately twelve to eighteen months after completion of our follow-on investment.

We intend to maximize our potential for capital appreciation by capturing the significant valuation differentials between private and publicly traded securities. We believe that a NASDAQ Capital Market listing generally will provide our portfolio companies with visibility, marketability, and liquidity. Since we intend to be more patient investors, we believe that our portfolio companies may have an even greater potential for capital appreciation if they are able to demonstrate sustained earnings growth and are correspondingly rewarded by the public markets with a price-to-earnings (P/E) multiple appropriately linked to earnings performance.

1

The convertible debt instruments we expect to receive in connection with our initial investments will likely be unsecured or subordinated debt securities. The equity investments we expect to receive in connection with our follow-on investments will typically be non-controlling investments, meaning we will not be in a position to control the management, operation and strategic decision-making of the companies in which we invest. In the near term, we expect that our total initial and follow-on investments in each portfolio company will typically range from $250,000 to $500,000, although we may invest more than this threshold in certain opportunistic situations. We expect the size of our individual investments to increase if and to the extent our capital base increases in the future.

We expect that our capital will primarily be used by our portfolio companies to finance organic growth. To a lesser extent, our capital may be used to finance acquisitions and recapitalizations. Our investment adviser’s investment decisions will be based on an analysis of potential portfolio companies’ management teams and business operations supported by industry and competitive research, an understanding of the quality of their revenues and cash flow, variability of costs and the inherent value of their assets, including proprietary intangible assets and intellectual property. Our investment adviser will also assess each potential portfolio company as to its appeal in the public markets and its suitability for achieving and maintaining public company status.

During the quarter ended September 30, 2008, the state of the economy in the U.S. and abroad continued to deteriorate to what many believe is a recession, which could be long-term. The generally deteriorating economic situation, together with the limited availability of debt and equity capital, including through bank financing, will likely have a disproportionate impact on the micro-cap companies we intend to target for investment. As a result, we may experience a reduction in attractive investment opportunities in prospective portfolio companies that fit our investment criteria.

We expect that a significant portion of any dividends we may pay to our stockholders will likely result from realized capital gains, if any, generated from the sale of our equity investments, the timing of which we will likely be unable to predict. We do not expect to generate capital gains from the sale of our portfolio investments on a level or uniform basis from quarter to quarter. This will likely result in substantial fluctuations in our quarterly dividend payments to stockholders. In addition, since we expect to have an average holding period for our portfolio company investments of two to three years, it is unlikely we will generate any capital gains during our initial years of operations and thus we are likely to pay little or no dividends in our initial years of operation. Finally, since we expect to generate only nominal current interest or preferred dividend income from our portfolio investments, we expect that we will pay only limited dividends, if any, from current investment income.

We have a limited operating history. At this time, we do not have any arrangements, agreements or commitments to make an investment in a portfolio company. We are subject to all of the business risks and uncertainties associated with any new business, including the risk that we will not achieve our investment objective and that the value of your investment could decline substantially.

Since we have only recently commenced operations, we have limited financial information. Our audited financial statements for the period from inception (May 9, 2008) through September 30, 2008 are included in this Registration Statement.

Our principal executive offices are located at 5251 DTC Parkway, Suite 1000, Greenwood Village, CO 80111, and our telephone number is (720) 889-0139. We maintain a Web site on the Internet at www.keatingcapital.com. Information contained on our Web site is not incorporated by reference into this Registration Statement, and you should not consider information contained on our Web site to be part of this Registration Statement.

2

Private Issuances of Securities

On May 14, 2008, our investment adviser, Keating Investments, purchased 100 shares of our common stock at a price of $10.00 per share as our initial capital. On November 12, 2008, we completed the final closing of our initial private placement offering (the “Offering”). We sold a total of 569,800 shares of our common stock in the Offering at a price of $10.00 per share raising aggregate gross proceeds of $5,698,000. After the payment of commissions and other offering costs of approximately $449,195, we received aggregate net proceeds of approximately $5,248,805 in connection with the Offering.

As of September 30, 2008, we had cash resources of approximately $4,458,150 and no indebtedness other than accounts payable and accrued liabilities incurred in connection with our organization and in the ordinary course of business of approximately $99,091. For the period from October 1, 2008 through November 12, 2008, we received additional net proceeds from the sale of common stock in the Offering of approximately $502,702.

As of November 12, 2008, our shares of common stock were owned by a total of 37 persons, including our chief executive officer and chairman of the board of directors, our chief operating officer, and one of our independent directors, who own, in the aggregate, a total of 120,000 shares of our common stock, representing approximately 21.1% of our issued and outstanding shares of common stock following the Offering. See “Security Ownership of Certain Beneficial Owners and Management” below.

All shares of our common stock issued in the Offering are restricted shares and cannot be sold by the holders thereof without registration under the Securities Act or an available exemption from registration under the Securities Act.

We plan to invest the net proceeds of the Offering in portfolio companies in accordance with our investment objective and strategy described in this Registration Statement. We anticipate that it will take us up to twelve to twenty-four months to invest substantially all of the net proceeds of the Offering in accordance with our investment strategy, depending on the availability of appropriate investment opportunities consistent with our investment objective and market conditions. We cannot assure you we will achieve our targeted investment pace.

Pending such investments, we will invest the net proceeds of the Offering primarily in cash, cash equivalents, U.S. government securities and other high-quality investments that mature in one year or less from the date of investment. We expect that these types of investments will earn only modest yields. As a result, we do not intend to pay any dividends during this period. Further, because of our focus on equity investing, we expect that our dividend distributions, if any, will be subject to significant fluctuations. The management fee payable to Keating Investments by us will not be reduced while our assets are invested in such securities.

Business Development Company

We are a newly organized, externally managed, closed-end management investment company that has elected to be regulated as a business development company under the 1940 Act. We currently have no subsidiaries. As a business development company, we are required to comply with certain regulatory requirements. For example, to the extent provided by the 1940 Act, we are required to invest at least 70% of our total assets in eligible portfolio companies (“Eligible Portfolio Companies”). Also, while we are permitted to finance investments using debt, our ability to use debt will be limited in certain significant respects, most notably that we maintain a 200% asset coverage position. We do not anticipate financing the acquisition of investments using debt in the foreseeable future. See “Risk Factors – Risks Relating to Our Business and Structure.”

Although our initial investments will typically consist of convertible debt instruments, we intend to invest our portfolio primarily in common and convertible preferred stock, through our follow-on investments in our portfolio companies. These follow-on investments will generally be conditioned on the achievement of pre-established milestones, which we believe will allow us to mitigate our financial exposure and assure that each portfolio company is committed to, and capable of, becoming a public company. As such, our initial investment in each portfolio company will generally be structured as an unsecured or subordinated, convertible debt instrument with a maturity of less than one year. Since our portfolio will be heavily weighted in favor of equity as opposed to debt investments, and as we expect to convert our initial debt investments into equity in most cases, we expect to earn only a minimal amount of investment income from debt investments in our portfolio.

3

We intend to provide capital primarily to micro-cap companies with an equity value of less than $250 million. With micro-cap companies historically having difficulty accessing the traditional capital markets and having less analyst coverage, less institutional ownership and lower trading volume, we believe an opportunity exists to become a preferred source of capital to such micro-cap companies, particularly given our public markets strategy and the expertise of our investment adviser.

Our investment activities will generally be focused on micro-cap companies that have demonstrated attractive revenue and earnings growth relative to their peers, and whose management teams are committed to becoming public reporting companies. We expect these public ready companies will also have some or all of the following characteristics:

| • | Operates in an attractive growth industry. We intend to focus on micro-cap companies across a broad range of attractive growth industries that we believe are being transformed or created anew by technological, economic and social forces and are capable of attracting interest from both retail and institutional investors. However, we will not generally seek investments in start-up companies, or companies operating in the real estate, mining, oil and gas exploration and production, biotechnology and construction industries. | |

| • | Immediate need for external capital. We intend to target micro-cap companies whose organic growth is currently constrained by limited capital, and which have reached a point in their development where we believe external capital is required. As part of our investment, we intend to offer a more stable form of equity capital for our portfolio companies, while requiring that their ownership structure align the economic interests of their management team with the success of the enterprise. | |

| • | Demonstrated revenue stream. We intend to invest in micro-cap companies that have a demonstrated revenue stream that we believe will make them attractive as publicly traded companies. As such, we do not intend to invest in developmental stage, pre-revenue stage and, with some exceptions, early revenue stage companies. | |

| • | Demonstrated profitability. We intend to focus on micro-cap companies that are at or near profitability on an earnings before interest, taxes, depreciation and amortization (“EBITDA”) basis. With the capital we provide, together with the projected EBITDA of our portfolio companies, we expect each of our portfolio companies to be able to finance their development over the next twelve to eighteen months without requiring additional outside capital subsequent to completion of our follow-on investment. Once our portfolio companies become listed on the NASDAQ Capital Market, which we generally expect to occur within twelve to eighteen months after completion of our follow-on investment, we would expect our portfolio companies to be positioned to conduct, if appropriate, a public follow-on offering. |

In addition to the foregoing, we currently intend to concentrate our investments in micro-cap companies having annual revenues between $10 million and $100 million that we believe have a strong prospect of revenue and earnings growth. We also expect our portfolio companies to generally have an equity valuation, before our investment, of between $25 and $200 million. These criteria provide general guidelines for our investment decisions; however, we may not require each prospective portfolio company in which we choose to invest to meet all of these criteria.

4

The success of our strategy depends largely on our ability to identify micro-cap companies that are committed to becoming, and that we believe we can assist in becoming, public companies. With over ten years experience sponsoring going public transactions, we believe that our investment adviser has the experience and expertise to assess which micro-cap companies are public ready and to assist such companies in achieving public status in a timely and cost-effective manner. Our two-step investment structure is designed to ensure that there is a shared commitment to going public between us and the management teams of each of our portfolio companies. As part of our initial debt investment, we will require that our portfolio companies agree to undertake the necessary steps to become a public reporting company through the filing of a registration statement under the Securities Act or the Exchange Act. In the event a portfolio company fails to complete the going public process in a satisfactory manner, our debt instruments will impose certain penalties, which we expect will generally include a right to put the debt investment back to the portfolio company at a premium to our initial investment.

While we believe that the use of economic disincentives will provide us with some downside protection on our initial investments, we believe the real incentive for our portfolio companies to become public is our more substantial follow-on investment that is tied to achieving certain pre-established milestones associated with the going public process, as well as what we believe are the advantages of becoming a public company. An important part of our investment adviser’s due diligence process will focus on assessing the appeal that a prospective portfolio company may have in the public markets, as well as its suitability for achieving and maintaining public company status. In addition, while we expect to make passive, non-controlling investments where we have little power to control the management, operation and strategic decision-making of our portfolio companies, we expect to provide managerial assistance to our portfolio companies throughout the investment process, especially as it pertains to the engagement of third party consultants with which our investment adviser has relationships, the completion of the going public process through the filing of a registration statement, and the design of an overall public markets strategy.

In the near term, we expect that our total initial and follow-on investment in each portfolio company will typically range from $250,000 to $500,000, although we may invest more than this threshold in certain opportunistic situations. We expect the size of our individual investments to increase if and to the extent our capital base increases in the future.

We intend to limit our investments in any one portfolio company to not more than 5% of our net assets; however, we may invest more than this threshold in certain opportunistic situations. With an initial capital base of approximately $5 million, we intend to limit our investments in any one portfolio company to $500,000, or 10% of our net assets. While this amount exceeds our target limit of 5% of net assets, we intend to be more selective during our initial investment period and take advantage of opportunistic situations at this higher level.

We will also generally limit our investments in any one portfolio company so that our total outstanding equity interest in the portfolio company is not more than 9.9% of a portfolio company’s outstanding equity, although we may exceed this threshold in certain opportunistic situations. We also intend to include certain “blocker” language in our warrant instruments which would prevent us from exercising warrants we are issued by our portfolio companies, if by doing so we would exceed the 9.9% level. We intend to be the lead investor in our portfolio investments and, to the extent our portfolio companies require more financing than we desire to invest, we anticipate seeking non-affiliated co-investors to participate in the financing of our portfolio companies. In addition, we expect our portfolio companies may engage one or more placement agents with whom our investment adviser has relationships to assist in capital raising from non-affiliated co-investors.

While our primary focus will be to generate capital gains on our equity investments in micro-cap companies, we may invest a portion of our portfolio in securities of other Eligible Portfolio Companies or other investments permitted under the 1940 Act, as well as up to 30% of our portfolio in other types of investments, including, investments in non-U.S.-based companies, for the purpose of diversifying our overall portfolio, improving our liquidity or enhancing returns to stockholders. We may also use this portion of our portfolio to invest in other types of securities, consistent with the regulatory requirements applicable to business development companies.

5

We are also permitted to borrow funds to make investments, subject to limitations on the amount of such borrowings under the 1940 Act. We do not currently anticipate borrowing funds to make investments in the foreseeable future.

Our investment activities are managed by Keating Investments. Keating Investments was founded in 1997 and is an investment adviser registered under the Investment Advisers Act of 1940, as amended (the “Advisers Act”). The managing member and majority owner of Keating Investments is Timothy J. Keating. Our investment adviser’s senior investment professionals are Timothy J. Keating, our Chairman of the Board and Chief Executive Officer, Ranjit P. Mankekar, our Chief Financial Officer, Treasurer and a member of our Board of Directors, and Kyle L. Rogers, our Chief Operating Officer and Secretary. In addition, Keating Investments’ other investment professionals consist of four portfolio company originators, two analysts and a chief compliance officer. Under our investment advisory and administrative services agreement with Keating Investments (the “Investment Advisory and Administrative Services Agreement”), we have agreed to pay Keating Investments, for its investment advisory services, an annual base management fee based on our gross assets as well as an incentive fee based on our performance. See “Investment Advisory and Administrative Services Agreement.”

As a business development company, we are required to meet certain regulatory tests, including the requirement to invest at least 70% of our total assets in Eligible Portfolio Companies. See “Regulation as a Business Development Company.”

Effective January 1, 2009, we also intend to elect to be treated for U.S. federal income tax purposes, and intend to qualify annually thereafter, as a regulated investment company (“RIC”) under Subchapter M of the Internal Revenue Code of 1986, as amended (the "Code"). See “Certain U.S. Federal Income Tax Considerations.” As a RIC, we generally will not have to pay corporate-level federal income taxes on any ordinary income or capital gains that we distribute to our stockholders in the form of dividends.

We believe that our investors, though an investment in our publicly traded business development company, will have access to the type of investments typically associated with late stage venture capital and lower middle market private equity funds. However, unlike those funds, which typically require lock-ups of five to seven years, it is intended that our investors will have access to liquidity in the form of a publicly traded stock once our common stock becomes quoted on the OTC Bulletin Board. There is no assurance that our common stock will become quoted on the OTC Bulletin Board and, even if it becomes quoted on the OTC Bulletin Board, we can make no assurance that an active trading market will develop.

Market Opportunity

Continued need for growth capital by public ready micro-cap companies looking for an equity partner. We believe a significant opportunity exists to provide growth, expansion and other types of capital to public ready micro-cap companies that have reached a point in their development where additional equity capital is needed. We believe our investment model offering non-controlling equity investments will provide an attractive vehicle for our portfolio companies to meet their capital needs. While we will require our portfolio companies to become public reporting companies, we believe that we will be viewed by prospective portfolio companies as a provider of “patient” capital, given our focus on longer-term growth versus short-term gains, which we believe will serve as a key differentiator for us. We believe there are a significant number of companies that are looking for the type of “patient” capital we will be able to provide. We also expect to bring enhanced value to our portfolio companies through our investment adviser’s going public and public markets expertise, rather than through financial engineering or as a strategic business adviser to our portfolio companies.

6

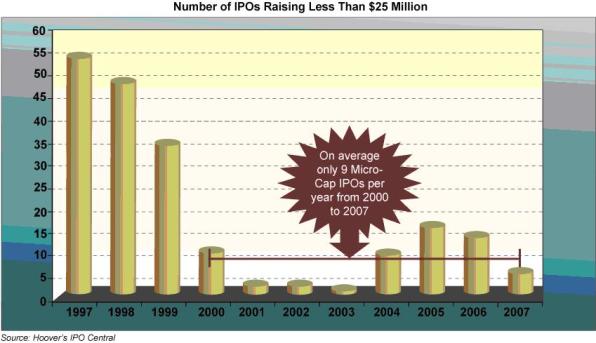

Absence of traditional IPO financing for micro-cap companies. We will focus on micro-cap companies that have demonstrated revenues, not pre-revenue or start-up companies, that are at a point in their development where we believe equity capital is required, but which are unable to raise capital through a traditional IPO or are unwilling, or unable due to market conditions, to raise capital from private equity and venture capital sources.

Since 2000, we believe the traditional IPO market has been virtually non-existent for micro-cap companies seeking to raise less than $25 million. In fact, from 2001 through 2007, there has been an average of only nine IPOs raising less than $25 million each year.

7

In response to this void, alternatives to the traditional IPO for micro-cap companies began to flourish in 2005. One of these alternatives was a “private investment in public equity,” or “PIPE,” offering which typically involved a reverse merger into a public shell company with a simultaneous PIPE investment – an industry in which our investment adviser was an active participant. While the PIPE offering temporarily filled this void, we believe that recent regulatory actions by the SEC which unfavorably impacted reverse mergers, coupled with the recent deterioration of the PIPE market as part of the broader difficulties within the U.S. credit markets generally, have largely limited recent PIPE offerings to more established, highly liquid, large-cap public companies. As a result, we believe there are many public ready micro-cap companies that meet our investment criteria, but simply do not have access to the U.S. public capital markets.

Difficult market for private equity and venture capital funds. We believe that the public ready micro-cap companies in which we intend to invest are also feeling the adverse impacts from the difficulties in current private equity and venture capital markets. Recently, private equity funds that typically relied on commercial banks or a syndicate of lenders to provide the debt capital necessary to produce their “leveraged” returns have seen these traditional sources of capital become largely closed. We believe that the impact of these tightened credit markets will be even more pronounced on the micro-cap companies we intend to target, as they tend to be unable to support large debt burdens. As a result, we believe private equity firms will be less interested in providing growth capital to public ready micro cap companies where leverage is limited.

We believe that venture capital funds are typically the least desired financing for our targeted growth companies due to pricing and control issues. While many venture capital firms have cash to invest, they typically insist on a controlling interest in their portfolio companies. Recent market trends, including the weak traditional IPO market in general, have put significant liquidity pressures on venture capital funds that are now faced with fewer attractive exit alternatives, extended holding periods and possible “mark to market” valuation write-downs.

Accordingly, we believe that many viable public ready micro-cap companies that fit our investment criteria will have limited, if any, access to the private equity market or venture capital financing, and we believe this trend is likely to continue for the foreseeable future.

Further, since our typical equity investment will be a non-controlling interest, we believe there is a significant opportunity for us to become a capital provider of choice for entrepreneurial businesses that are unwilling to give up a controlling interest typically mandated by both private equity and venture capital funds. While we will generally have no direct control over the management and strategic direction of our portfolio companies, we intend to ensure that our portfolio companies’ management teams have a meaningful equity stake and that their interests are aligned with our interests as an investor – mainly, to create stockholder value through a widely held and actively traded public stock. As part of the going public process, we also intend to provide our portfolio companies with recommendations on the composition of their board of directors, which we will require to be comprised of a majority of independent directors so as to satisfy the NASDAQ Capital Market initial listing requirements.

IPO financing alternative. We believe that there exist significant and continuing opportunities to originate and lead investments in public ready micro-cap companies. We believe that the market for the companies that we are targeting has historically been characterized by continual change, which creates an ongoing need for capital within that marketplace. We believe that there exists a significant market opportunity to meet the capital requirements of a growing number of these businesses as they find the U.S. public and private capital markets largely closed. We believe that the reasons for that closure relate more, in our view, to the state of the financial markets generally rather than the quality of these micro-cap companies. In addition, we believe that the capital markets have tended in recent years to be focused on larger funds and larger deals – deals which are magnitudes larger than what is required by the public ready micro-cap companies we intend to target.

8

We believe that we can offer public ready micro-cap companies that have solid financial qualifications and strong growth prospects with an attractive, well-structured capital markets alternative which is supported by our investment adviser’s public markets approach and expertise. Our focus will be to identify these companies and provide a two-step investment program that provides them a level of immediate capital followed by a more substantial equity financing component once they have proven they are ready to become a public company. We believe our two-step investment process and going public through the filing of a registration statement under the Securities Act or the Exchange Act may prove more time-effective and less costly than a traditional IPO for the micro-cap companies we intend to target. In addition, our investment in each portfolio company, unlike an IPO, will not generally depend on general market conditions or prevailing investor sentiment. We also believe that our investment adviser’s going public expertise and access to third-party consultants, that we expect will be retained by our portfolio companies, will allow our portfolio companies’ management teams to concentrate on maximizing their business potential and marketplace influence as we proceed through our disciplined and systematic going public process.

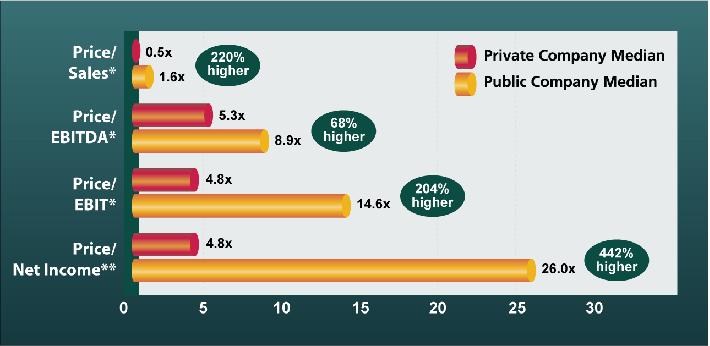

Benefits of being a public company. Typically, investors place a premium on liquidity, or having the ability to sell stock quickly. As a result, we believe that public companies typically trade at higher valuations than private companies with similar financial attributes. By going public, we believe that the value of our portfolio companies can be transformed – resulting in the creation of new value for existing shareholders upon going public.

Source: Pratt’s Stats® at BVMarketData.com, Public Stats™ at BVMarketData.com as of June 5, 2008 for transactions between January 1, 2003 and December 31, 2007. Used with permission from Business Valuation Resources, LLC.

*Valuation data based on a combined total of 4,900+ U.S. based private and public company transactions under $100 million.

**Keating Investments, LLC calculation based on those companies having positive net income, valuation data based on a combined total of 3,600+ U.S. based private and public company transactions under $100 million.

9

In addition to higher valuations, we believe that public companies also enjoy other benefits, including:

| • | lower cost of capital, superior access to the capital markets, and less stock dilution to founders when raising additional capital; | |

| • | creation of a stock currency to fund acquisitions; | |

| • | equity-based compensation to retain and attract management and employees; | |

| • | more liquidity for founders, minority shareholders, and investors; and | |

| • | added corporate prestige and visibility with customers, suppliers, employees and the financial community. |

Of course, public companies also incur significant obligations, such as the cost of periodic financial reporting, compliance with the Sarbanes-Oxley Act of 2002, as amended (the “Sarbanes-Oxley Act”), required disclosure of sensitive company information and restrictions on stock sales by major or controlling shareholders. But for the type of micro-cap companies we intend to target, we believe that the capital-raising opportunities and other benefits of being public may substantially outweigh these disadvantages.

Investment Strategy

We intend to implement the following strategies to take advantage of the market opportunity for providing capital to public ready micro-cap companies that we believe have strong prospects for growth and which are at a point in their development where we believe a significant equity investment is required:

Visionary, industry leading management. We plan to invest in businesses with a strong management team with industry experience, a visionary business strategy, a passionate commitment to achieve results, the proven ability to execute and lead, and a track record of being able to attract experienced industry talent. Our portfolio companies must have in place, or ready for hire, a qualified chief financial officer with a strong background in SEC reporting and compliance with proven experience in managing a micro-cap public company’s financial reporting, internal controls, accounting and finance functions, and investor relations.

Innovative and quality products. We intend to focus our investments on companies where there is a proven demand for the products or services they offer rather than focusing on ideas that have not been proven or situations in which a completely new market must be created. We look for businesses that are innovators, have technologies or products that extend, accelerate, or disrupt identified markets, have premium niche products capable of higher and more sustainable margins, and are able to attract top sales and engineering talent. We intend to target companies whose business will benefit from exposure as a public company and have appeal to retail and institutional investors alike.

Large potential markets. We intend to provide capital to established, but potentially undiscovered, micro-cap companies with demonstrated growth that we believe is sustainable in industries where we believe there are substantial, leading edge market opportunities. We intend to focus on micro-cap companies across a broad range of industries and markets that we believe will be capable of attracting interest from retail and institutional investors. We intend to focus on industries that we believe are being transformed or created anew by technological, economic and social forces – such as globalization, demographics, environment, energy, the knowledge economy and the Internet. We will look for businesses whose products or services are capable of moving into the mass market and disrupt existing, more mature markets. We will tend to limit our exposure to companies where long-term growth is dependent on favorable economic factors – such as a strong economy, rising consumer and business sentiment, lowering interest rates, falling inflation and stable financial markets.

10

Consistent and predictable results. We intend to focus on micro-cap companies that have realistic operating targets set by management that are consistently achieved, have a demonstrated ability to grow market share profitably, have growing and sustainable profits, generate or have the potential to generate recurring revenue streams, have recognized technological barriers to market entry and have a commitment to R&D spending to stay ahead of innovation. We intend to invest in micro-cap companies that we believe will be rewarded in the public markets for consistent and predictable financial results.

Aligned interests. We intend to target micro-cap companies that we believe offer substantial growth opportunities and proactively approach them regarding investment possibilities. We believe that the experience of our investment adviser’s senior investment professionals and their understanding of public ready micro-cap companies, our two-step financing structure, our public markets strategy and our investment adviser’s going public expertise, and the opportunity to capture a potential public company valuation premium will be attractive to prospective portfolio companies. We believe it is important that each of our portfolio companies’ management teams have a meaningful equity stake in their business and that their interests are aligned with our interests as investors in the portfolio company to create substantial stockholder value through a widely held and actively traded public stock.

Competitive Advantages

We believe that we will have the following competitive advantages over other providers of capital to public ready micro-cap companies including private equity firms, venture capital firms and reverse merger sponsors:

Public markets focus. We intend to invest in micro-cap companies that are committed to, and capable of, becoming public companies and have defensible valuations to support our initial investment pricing. We believe we have expertise in evaluating whether a portfolio company is capable of becoming a successful public company – both management commitment and skills and public market appeal. By providing capital to micro-cap companies that are at a point in their development where we believe an equity investment is required, we hope to accelerate their growth with a properly timed going public strategy. The going public process is a critical step in our overall investment process for each portfolio company that we expect will take between three and twelve months following our initial investment and be substantially completed before we make our more substantial follow-on investment.

Going public expertise. Our investment adviser’s senior investment professionals and various third party consultants, with which our investment adviser has relationships, have extensive experience in taking companies public and designing capital markets and investor relations programs. Our investment adviser has been a reverse merger sponsor for more than a decade and has completed 19 going public transactions over the last five years. Our investment adviser’s senior investment professionals and various third party consultants will assist our portfolio companies in this going public process. We will generally require that one of our recommended third party consultants be retained by our portfolio companies to actively participate and lead the going public process. These third party consultants are highly experienced in the going public process, SEC compliance matters, public company reporting, and legal and financial matters associated with micro-cap companies. We believe the involvement of a third party consultant will result in a more coordinated, timely and cost-effective going public process – allowing each portfolio company’s management team to remain focused on growing their business.

Obtaining NASDAQ Capital Market exchange listing. We believe that a NASDAQ Capital Market listing generally will provide our portfolio companies with visibility, marketability, liquidity and third party established valuations, all of which will aid in their future capital raising efforts. More specifically, the advantages that a NASDAQ Capital Market listing is expected to have for our portfolio companies include:

| • | Visibility – greater access to investment analyst coverage to disseminate our portfolio companies’ stories, and added corporate prestige and visibility with exchange listing; |

11

| • | Valuation and liquidity – potential for more stock liquidity as retail brokers become more interested in making a market in the stock and soliciting their clients to purchase the stock and as institutional investors who typically do not invest in OTC Bulletin Board stocks consider investments; and | |

| • | Access to capital – greater interest from top- and mid-tier investment banking firms to conduct a public follow-on offering for our portfolio companies. |

We intend to utilize our investment adviser’s expertise in public markets strategies to assist our portfolio companies in the design of a comprehensive aftermarket support program aimed at achieving a NASDAQ Capital Market listing. We also intend to leverage our investment adviser’s expertise and access to their contacts and third party consultants to develop and execute a disciplined plan to upgrade our portfolio companies from the OTC Bulletin Board to the NASDAQ Capital Market, which we anticipate will take twelve to eighteen months after completion of our follow-on investment in each portfolio company. The following table summarizes the initial listing requirements for companies that want to list their securities on the NASDAQ Capital Market. A company must meet all of the requirements under at least one of the three standards below.

| Requirements | Standard 1 | Standard 21 | Standard 3 |

| Stockholders’ equity | $5 million | $4 million | $4 million |

| Market value of publicly held shares | $15 million | $15 million | $5 million |

| Operating history | 2 years | N/A | N/A |

Market value of listed securities2 | N/A | $50 million | N/A |

| Net income from continuing operations (in latest fiscal year or in two of last three fiscal years) | N/A | N/A | $750,000 |

Publicly held shares3 | 1 million | 1 million | 1 million |

| Bid price | $4 | $4 | $4 |

Shareholders (round lot holders)4 | 300 | 300 | 300 |

| Market makers | 3 | 3 | 3 |

| Corporate governance | Yes | Yes | Yes |

1Seasoned companies (those companies already listed or quoted on another marketplace) qualifying only under the market value of listed securities requirement must meet the market value of listed securities and the bid price requirements for 90 consecutive trading days prior to applying for listing.

2Listed securities are defined as “securities listed on NASDAQ or another national securities exchange.”

3Publicly held shares is defined as total shares outstanding, less any shares held by officers, directors or beneficial owners of 10% or more.

4Round lot holders are shareholders of 100 shares or more.

We believe our public markets strategy, coupled with a successful listing on NASDAQ Capital Market, will give us an expected portfolio company investment horizon of two to three years via an orderly public market exit, which we believe represents a substantially shorter investment horizon when compared to traditional private equity and venture capital investments which have investment periods of five to seven years.

12

Two-step equity investment structure. We will use a two-step investment structure with an initial investment that allows us to meet the immediate capital needs of a portfolio company in a timely manner. Our more substantial follow-on investments, typically within three to twelve months after our initial investment, will be tied to pre-established milestone achievements including continued business performance, new management hires and substantial completion of a going public process through the filing of a registration statement. Although our initial investments will typically be structured as convertible debt, our primary focus will be on equity investments. We believe our non-controlling, equity investment structure will provide an attractive vehicle for our portfolio companies to meet their immediate and short-term capital needs. We also believe that our flexible approach to structuring investments will facilitate positive, long-term relationships with our portfolio companies and better position them to conduct a subsequent registered public follow-on offering, if necessary, after they obtain a NASDAQ Capital Market listing.

Non-controlling, minority investments. We intend to make non-controlling, minority investments in our portfolio companies. We believe this makes us a more attractive source of capital in comparison to private equity and venture capital funds which typically require controlling investments. Although we will not generally have the power to control the management, operations and strategic decision-making of the companies in which we invest, we expect to provide managerial assistance to our portfolio companies throughout the investment process, especially as it pertains to the engagement of our investment adviser’s recommended third party consultants, the completion of the going public process, and the design of an overall public markets strategy. We believe that we will bring enhanced value to the process through our investment adviser’s public markets expertise, rather than through financial engineering or by serving as a strategic adviser to our portfolio companies.

Liquidity premium. Our investment strategy is principally focused on generating capital gains through equity investments in our portfolio companies. We intend to maximize our potential for capital appreciation by capturing the significant valuation differentials between private and publicly traded securities. We believe that a NASDAQ Capital Market listing generally will provide our portfolio companies with visibility, marketability, and liquidity. Since we intend to be more patient investors, we believe that our portfolio companies may have an even greater potential for capital appreciation if they are able to demonstrate sustained earnings growth and are correspondingly rewarded by the public markets with a price-to-earnings (P/E) multiple appropriately linked to earnings performance.

Investment Selection

Investment criteria. We have identified criteria that we believe are important in meeting our investment objective. These criteria provide general guidelines for our investment decisions; however, we may not require each prospective portfolio company in which we choose to invest to meet all of these criteria.

| • | Revenue growth — We will seek to invest primarily in micro-cap companies that are already generating revenue and which we believe have significant growth potential. We intend to invest in companies with annual revenues of $10 to $100 million. We intend to examine the market segment in which each prospective portfolio company is operating, including its size, geographic focus and competition, to determine whether that company is likely to continue its current growth rate prior to investing. | |

| • | Large addressable markets — We will seek to invest in businesses where we believe there is a proven demand for the company’s products or services that address large market opportunities. We believe that large markets not only provide for more attractive growth prospects, but also have the ability to support a healthy competitive environment with more than one successful competitor. |

13

| • | Strong industry position — We will seek to invest in companies that have developed defendable market positions within their respective markets and are well positioned to capitalize on growth opportunities. We will seek to invest in companies that demonstrate competitive advantages versus their competitors, which should help to protect their market position and profitability and permit them to adapt to changes in their respective business environments. | |

| • | Strong, experienced management team — We will generally require that our portfolio companies have an experienced management team. We will also require our portfolio companies to have in place proper incentives to induce management to succeed and to act in concert with our interests as investors, including having significant equity interests. | |

| • | Profitable on EBITDA basis — We will focus on companies that are at or near profitability on an EBITDA basis. We will seek to invest in companies that we believe will provide a predictable and growing EBITDA. We expect that projected EBITDA, together with the proceeds from our investments, will be a key means by which our portfolio companies will financially support their future growth plans until they are listed on NASDAQ Capital Market and ready for a registered public follow-on offering. | |

| • | Attractive public markets company — We intend to invest in public ready micro-cap companies whose management is committed to, and capable of, becoming a public company, whose business we believe will benefit from exposure as a public company and will have appeal to retail and institutional investors, and that we believe is capable of obtaining a NASDAQ Capital Market listing typically within twelve to eighteen months after we complete our follow-on investment. | |

| • | Regulatory compliance — We will generally require that our portfolio companies have in place, or ready for hire, a qualified chief financial officer with a strong background in SEC reporting, Sarbanes-Oxley Act compliance, Generally Accepted Accounting Principles (“GAAP”), accounting and internal controls management, and investors relations. Before we complete our more substantial follow-on equity investment, our portfolio companies will be required to have GAAP compliant financial statements for at least the past two years which have been audited by a Public Company Accounting Oversight Board (“PCAOB”) registered auditor acceptable to us. |

Due diligence. If a potential portfolio company meets all, or most, of the characteristics described above, our investment adviser’s investment professionals will perform a preliminary due diligence review including company assessments, market and competitive analysis, evaluation of management team, financial models and business risks, and assessments of transaction size, pricing and structure. The process outlined below provides general parameters for our investment adviser’s investment decisions, although not all will be followed in evaluating each opportunity. Upon successful completion of this preliminary evaluation process, our investment adviser’s investment committee will decide whether to enter into a non-binding letter of intent, continue the due diligence process and move forward towards the completion of an investment transaction.

Our due diligence process will typically encompass the following steps:

| • | Assessment of management — Our investment adviser will typically perform an assessment including a review of experience, passion, proven leadership ability, vision, ability to attract key employees, dispute resolution skills, and reputation in the market. Our investment adviser will generally corroborate and verify management’s track record, industry accomplishments and leadership capabilities through extensive background checks, interviews with management, employees, references and other industry leaders, and on-site visits. Our investment adviser will also assess the qualifications and experience of the chief financial officer to manage micro-cap public companies. |

14

| • | Market and competitive analysis — Our investment adviser will utilize its investment analysts and engage, on an as-needed basis, outside experts to perform market and competitive analysis and due diligence. This analysis and due diligence typically will provide our investment adviser with a detailed understanding of the prospective portfolio company’s business, market opportunities and operations. This analysis may include: |

| • | industry and competitive analysis, including verification of market potential, the relative position of the prospective portfolio company within its market, the existence of significant barriers to entry for potential competitors, and pricing elasticity; | |

| • | customer and vendor interviews to assess reputation within its market; | |

| • | assessment of technology and intellectual capital; and | |

| • | examination of potential regulatory and legal issues. |

| • | Business model and financial assessment — Prior to making an investment decision, our investment adviser will typically review a prospective portfolio company’s business model and financial reporting. This will include a thorough review of historical and prospective financial information, accounting practices and financial models, and investment and loan documents. Our investment adviser intends to challenge management’s financial assumptions, make an independent assessment of revenue and earnings quality, and conduct interviews with attorneys and auditors. | |

| • | Strategic and public company analysis — Our investment adviser will also generally perform a strategic analysis of each prospective portfolio company, during which it will evaluate operating and market risks, public company attractiveness, comparable public company valuations, potential to become a public company in a cost-effective and timely manner, management commitment to being a public company, and potential appeal to retail and institutional investors in the aftermarket. |

Deal sourcing. We believe that the combined experience of our investment adviser’s investment professionals will provide us with access to a significant number of investment opportunities. Our investment adviser’s strong reputation in the reverse merger industry has exposed us to an established network of contacts and sources from which we intend to generate investment opportunities in public ready micro-cap companies that are seeking alternatives to traditional IPO financing. Our investment adviser’s network includes relationships with prior deal participants, prospective management teams, entrepreneurs, industry organizations, corporate development professionals, financial institutions, high net worth and institutional investors and service professionals.

We also expect to receive deal referrals from strategic advisers, industry consultants, industry analysts, portfolio company managers, finders, lawyers, accountants and investment bankers. In addition, we expect that our investment adviser’s investment professionals will also serve as the direct source of proprietary deal referrals from their own business networks.

In many transactions, we expect that our investment adviser’s investment professionals will have prior knowledge of a prospective portfolio company and will have developed a relationship with its management or investors over a period of time resulting in an investment opportunity. We believe that such relationship building will serve us in several ways with respect to our investments, including: (i) generating investments on a timely, non-auction basis; (ii) assuring an alignment of interests between us and our portfolio companies’ management teams; and (iii) providing comfort that our portfolio companies’ management teams are committed to, and capable of, becoming public and achieving a NASDAQ Capital Market listing. We intend to make investments in negotiated transactions as opposed to auction situations.

15

We also intend to implement a proactive marketing program to communicate with our investment adviser’s established referral network and with companies that meet our investment criteria.

Investment decisions. Keating Investments is registered as an investment adviser under the Advisers Act, and will serve as our investment adviser. Keating Investments will manage our day-to-day operations and will determine companies in which we will invest. Our investment adviser’s investment committee (“Investment Committee”) must unanimously approve each new investment that we make. The members of the Investment Committee currently consist of Timothy J. Keating, Ranjit P. Mankekar and Kyle L. Rogers, who are the senior investment professionals of Keating Investments and our executive officers. We believe the Investment Committee’s approach embraces a rigorous investment process with well-defined investment parameters, risk assessment techniques and valuation metrics that are applied consistently to all investments.

Investment Structure

Once our investment adviser has determined that a prospective portfolio company is suitable for investment, it will work with the management team of that company and, if necessary, its other capital providers, including senior and junior lenders, and equity capital providers, to structure an investment. We intend to utilize a two-step investment process focused on an initial investment, consisting of convertible debt, and a subsequent follow-on investment, consisting of common or convertible preferred stock or other equity, that will be contingent upon a portfolio company satisfying pre-established milestones towards the filing of a registration statement under the Securities Act or the Exchange Act. Where appropriate, we may also negotiate to receive warrants, either as part of our initial or follow-on investments in our portfolio companies.

We believe that our two-step investment structure is an attractive approach for prospective portfolio companies that complements the going public process and strategy we intend to implement with each of our portfolio companies. We also believe our non-controlling, equity investment structure provides an attractive vehicle for our portfolio companies to meet their immediate and short-term capital needs. While we believe there are numerous micro-cap businesses that are both interested in, and capable of, becoming public companies, many of these companies lack the personnel, organization, expertise and control systems to properly become a public company and manage the SEC compliance and filing requirements and general business aspects of being public. We believe that the founders of many existing micro-cap companies realize the potential benefits of being public, but also recognize the tremendous effort it takes to become a public company and maintain the public company status. Our two-step investment structure is designed to ensure our portfolio companies are public ready before we make our follow-on investments. We believe that our portfolio company management teams will benefit from this approach because our portfolio companies can focus on growing their business and increasing their earnings after having hired the right personnel to operate as a public company, including an experienced chief financial officer.

The investment structure discussed below is intended to provide general guidelines for the terms and conditions which we intend to negotiate for our investments; however, we may not require each investment to contain all of these terms and conditions.

Seed investments in form of convertible debt. In the near term, we expect that our initial investments in a portfolio company will typically range from $100,000 to $250,000 each. However, we expect this investment size to increase as the size of our capital base increases. We anticipate structuring our investments primarily as unsecured and subordinated loans that provide for a fixed interest rate that will provide us with a modest level of current interest income. We will set interest rates based on prevailing market rates at the time of our investment for comparable types of investments. Typically, these loans will have maturities not to exceed one year, which coincides with the maximum period we believe is required to complete the going public process.

In the case of our unsecured and subordinated debt investments, we intend to tailor the terms of our initial investments to the facts and circumstances of the transaction and prospective portfolio company, negotiating a structure that seeks to protect our rights and manage our risk while creating incentives for the portfolio company to achieve its business plan and complete the going public process in a timely manner. For example, when structuring a debt investment, we will seek to limit the downside potential of our investments by:

16

| • | requiring a total return on our investments (including both interest and potential equity appreciation) that compensates us for credit risk; | |

| • | incorporating “put” protection into the investment structure; and | |

| • | negotiating covenants and other contractual provisions in connection with our investments. Such provisions may include affirmative and negative covenants, default penalties, lien protection, change of control provisions and board rights, including either observation or participation rights. |

Our initial investments may include an equity component, such as warrants to buy common stock in our portfolio companies. Any warrants we receive with our initial debt securities will require us to pay an additional cost to exercise, and thus, if our portfolio companies appreciate in value, we may be able to realize additional investment return in the form of capital gains from the exercise of these warrants. Any warrants associated with our initial investments will typically be detachable, which will allow us to receive repayment of our principal while retaining our equity interests in the portfolio companies.

We also intend to structure our initial debt investments to give us the option to convert our debt into common stock at a pre-determined conversion price, subject to adjustment for certain events including performance events. Our conversion prices will generally be determined by reference to an agreed upon discount from the common stock price in our follow-on investment. If we complete the follow-on investment, the convertible debt instrument will be automatically converted into common stock upon the filing of the registration statement. Since our convertible debt investments will have elements of both debt and equity instruments, we believe that we will be able to realize fixed returns in the form of interest payments associated with debt until the follow-on investment is completed, while maintaining an opportunity to participate in the capital appreciation of the portfolio company, if any, through the conversion of debt to equity at the time of the follow-on investment. In the event we do not complete a follow-on investment with a portfolio company, or if a portfolio company abandons the going public process, we expect that our debt instrument will provide for a reset default conversion price. However, in such a case, we will likely take steps to exit the investment.

In many cases, we will also obtain registration rights in connection with the common stock underlying the warrants and convertible debt investments associated with our initial investment. We may structure our initial investments to provide provisions protecting our rights as a minority-interest holder, as well as puts, or rights to sell such securities back to the company, upon the occurrence of specified events. We may also include exercise and conversion price adjustments based on certain events. We will seek to achieve additional investment return in the form of capital gains from the appreciation and sale of the common stock underlying the warrants and convertible debt associated with our initial investment.

Our initial investments will also typically contain a “put” option which will allow us to require the company to redeem the loan, at any time prior to maturity, at a premium to the outstanding loan amount. We may exercise this “put” option in the event the portfolio company either: (i) completes a debt or equity financing with a third party, or (ii) fails to complete, or elects to abandon, the going public process.

As a condition of our initial investment, we will generally require the portfolio company to engage a third party consultant recommended by our investment adviser and experienced in the going public process to actively participate in and lead the process.

17

We intend to act as the lead investor in all of our follow-on investments. To the extent our portfolio companies require more financing than we desire to invest, we may seek non-affiliated co-investors to participate in the financing of our portfolio companies. In addition, we expect our portfolio companies may engage one or more non-affiliated placement agents with whom our investment adviser has had prior experience to assist in capital raising from such non-affiliated co-investors.

Going public process. The going public process for our portfolio companies – though the filing of a registration statement under the Securities Act or the Exchange Act – is a critical step in our overall investment process. We expect that this going public process will be implemented during the three to twelve month period following our initial investment, and we will require that it be completed, and the registration statement be ready for filing with the SEC, at the time we make our follow-on investment. Our investment adviser’s senior investment professionals and certain third party consultants, who we expect will be retained by our portfolio companies, will assist our portfolio companies in this going public process, which will generally commence immediately after our initial investment. We will require that one of our investment adviser’s recommended third party consultants be engaged by the portfolio company to actively participate and lead the going public process. These third party consultants are experienced in the going public process, SEC compliance matters, public company reporting, and legal and financial matters associated with micro-cap companies.

We do not intend to close on a follow-on investment in a portfolio company unless and until the portfolio company satisfactorily completes the going public process and the registration statement is in final form acceptable to us and ready for filing with the SEC. The registration statement may take the form of a primary offering or resale registration statement filed by the portfolio company under the Securities Act coupled with a concurrent registration of the portfolio company’s common stock under the Exchange Act, or alternatively a stand-alone registration statement registering the common stock of a portfolio company under the Exchange Act without a concurrent registered offering under the Securities Act. We believe that there may be situations where a portfolio company in which we made an initial investment will not be capable of completing the going public process to our satisfaction. In these cases, we will not provide any follow-on investment and will attempt to take steps to promptly obtain repayment of our investments in accordance with the terms of our convertible debt instruments.

For portfolio companies who receive follow-on investment financing from us, we believe the going public process we have required as condition thereto will help prepare the portfolio company to comply with the public company regulatory environment and, at the same time, better position it to best extract value from its growth initiatives.

Our going public process through the filing of a registration statement under the Securities Act or the Exchange Act will generally include the following steps which will be coordinated and led by the third party consultant:

| • | Verify business and financial disclosures — Assure accuracy of public disclosures regarding the portfolio company’s business, operations, management, products and services, markets, finances, major contracts, tangible and intangible properties, business strategies, related party transactions, compensation arrangements and stock ownership. Organize all supporting documentation, diligence materials and corporate information. | |

| • | Review and preparation of business plans and financial models — Thorough review of historical and prospective financial information, accounting practices and financial models, review investment and loan documents, challenge management’s financial assumptions, and review revenue and earnings quality. Assist in preparation of business history and plans, and management discussion and analysis. |

18

| • | Coordinate audit and legal processes — Work directly with the portfolio company’s internal staff and their audit and legal teams to prepare, present, review and complete audited financial statements, footnote disclosures and supporting analysis and documentation. Assist in internal control compliance matters. | |

| • | Assess and make recommendations on financial management team — Continue assessment of chief financial officer’s capabilities to lead and manage financial reporting and accounting functions for a public company. Make recommendations for additional hires, if necessary. Before our follow-on investment is made, a portfolio company must have in place, or ready for hire, a qualified chief financial officer with a strong background in SEC reporting, Sarbanes-Oxley Act compliance, GAAP accounting and internal controls management, and investor relations. | |

| • | Composition of board of directors – Work directly with the portfolio company’s management to identify the ideal composition of the board of directors and to assess the skills and experience they should be seeking from new board members including the financial expert. The majority of the board must consist of independent directors and the proper board committee charters must be adopted and the committees selected, all in compliance with the initial quotation requirements of NASDAQ Capital Market. | |

| • | Preparation and filing of registration statements – Work directly with the portfolio company’s internal staff and their audit and legal teams to prepare and complete appropriate documentation for filing with the SEC under the Exchange Act, as applicable. Before our follow-on investment is made, the registration statement must be in final form ready for filing with the SEC at the closing of the follow-on investment. | |