|

As filed with the Securities and Exchange Commission on January 10, 2009 |

|

Registration No. 333-153726 |

|

SECURITIES AND EXCHANGE COMMISSION |

Washington, D.C. 20549 |

|

FORM S-1/A |

|

(Amendment No. 4) |

|

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 |

|

MAP FINANCIAL GROUP, INC. |

(Exact name of Registrant as specified in its charter) |

|

|

|

|

|

Nevada |

| 6199 |

| 26-2936813 |

|

| |||

(State or other jurisdiction of |

| (Primary Standard Industrial |

| (I.R.S. Employer Identification |

incorporation or organization) |

| Classification Code Number) |

| Number) |

|

460 West 34th Street, 10th Floor |

New York, New York 10001 |

Telephone: (212) 629-1955 |

(Address, including zip code, and telephone number, including area code, |

of Registrant’s principal executive offices) |

|

The Incorporator |

20 Robert Pitt Drive, Suite 214 |

Monsey, New York 10952 |

(Name, address, including zip code, and telephone number, including area code, |

of agent for service) |

|

Copies of all Correspondence to: |

|

David Lubin & Associates, PLLC |

26 East Hawthorne Avenue |

Valley Stream, New York 11580 |

Telephone: (516) 887-8200 |

Facsimile: (516) 887-8250 |

|

Approximate date of commencement of proposed sale to the public: From time to time after the effective date of this registration statement.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, please check the following box: x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non accelerated filer, or a small reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one)

|

|

|

|

|

Large accelerated filer | o |

| Accelerated filer | o |

|

|

|

|

|

Non-accelerated filer | o |

| Smaller reporting company | x |

Calculation of Registration Fee

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Title of Class of |

| Amount to be |

| Proposed |

| Proposed |

| Amount of |

| |||||||||

Common Stock, $0.001 per share |

| 500,000 |

|

| $ | 1.00 |

|

|

| $ | 500,000 |

|

|

| $ | 19.65 |

|

|

Total |

| 500,000 |

|

| $ | 500,000 |

|

|

| $ | 500,000 |

|

|

| $ | 19.65 | * |

|

(1) Estimated solely for the purpose of computing the amount of the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended.

(2) Represents up to a maximum of 500,000 shares of common stock, par value $0.0001 per share, to be offered and sold by the registrant.

* Previously paid.

In the event of a stock split, stock dividend or similar transaction involving our common stock, the number of shares registered shall automatically be increased to cover the additional shares of common stock issuable pursuant to Rule 416 under the Securities Act of 1933, as amended.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

THE INFORMATION IN THIS PROSPECTUS IS NOT COMPLETE AND MAY BE CHANGED. WE MAY NOT SELL THESE SECURITIES UNTIL THE REGISTRATION STATEMENT FILED WITH THE SECURITIES AND EXCHANGE COMMISSION IS EFFECTIVE. THIS PROSPECTUS IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT SOLICITING AN OFFER TO BUY THESE SECURITIES IN ANY STATE WHERE THE OFFER OR SALE IS NOT PERMITTED.

ii

PRELIMINARY PROSPECTUS SUBJECT TO COMPLETION DATED ______ __, 2009

Map Financial Group, Inc.

500,000 Shares of Common Stock

This prospectus relates to the initial public offering of Map Financial Group, Inc. We are offering up to 500,000 newly-issued shares of common stock, par value $0.001 per share. The shares will be offered and sold at a price of $1.00 per share on a “best efforts no minimum basis” by the directors and officers of Map Financial Group, Inc. on its behalf, and no underwriters or broker-dealers will be involved in the offering. Funds received as payment for shares will be deposited into a bank account maintained by us and under our control, and will immediately be available for our use.

There is no minimum number of shares that each subscriber is required to purchase and no minimum number of shares that must be sold in this offering. As a result, we might not be successful in raising a significant amount of capital in this offering.

The offering will commence as soon as practicable after the effective date of the registration statement relating to this prospectus and terminate 180 days after such effective date, but such termination date may be extended for up to an additional 90 days in our discretion. Map Financial Group reserves the right to terminate the offering at an earlier date, in its sole discretion, even if no shares are sold.

There has been no market for our securities and a public market may not develop, or, if any market does develop, it may not be sustained. Our common stock is not traded on any exchange or quoted on the over-the-counter market. After the effective date of the registration statement relating to this prospectus, we intend to have a market maker file an application with the Financial Industry Regulatory Authority, Inc. for our common stock to be eligible for trading on the Over-The-Counter Bulletin Board or a similar electronic inter-dealer quotation system. We do not yet have a market maker who has agreed to file such application.

INVESTING IN OUR SECURITIES INVOLVES SIGNIFICANT RISKS. SEE “RISK FACTORS” BEGINNING ON PAGE 4.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THESE SECURITIES OR DETERMINED IF THIS PROSPECTUS IS TRUTHFUL OR COMPLETE. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

The information in this prospectus is not complete and may be changed. This prospectus is included in the registration statement that was filed by us with the Securities and Exchange Commission. The selling security holders may not sell these securities until the registration statement becomes effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

The date of this prospectus is ____, 2009

iii

Table of Contents

|

|

|

|

|

| Page | |

|

| ||

| 1 |

| |

| 4 |

| |

| 13 |

| |

| 14 |

| |

| 14 |

| |

| 16 |

| |

| 19 |

| |

| 20 |

| |

| 20 |

| |

| 30 |

| |

| 30 |

| |

| 31 |

| |

| 31 |

| |

| 31 |

| |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

| 32 |

|

| 37 |

| |

Directors, Executive Officers, Promoters, and Control Persons |

| 38 |

|

| 40 |

| |

Security Ownership of Certain Beneficial Owners and Management |

| 42 |

|

| 43 |

| |

| 45 |

| |

| 45 |

| |

| 46 |

| |

| 46 |

| |

| 51 |

| |

Information Not Required in Prospectus |

|

|

|

iv

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements which relate to future events or our future financial performance. In some cases, you can identify forward-looking statements by terminology such as “may”, “should”, “expects”, “plans”, “anticipates”, “believes”, “estimates”, “predicts”, “potential” or “continue” or the negative of these terms or other comparable terminology. These statements are only predictions and involve known and unknown risks, uncertainties and other factors, including the risks in the section entitled “Risk Factors,” that may cause our or our industry’s actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements.

While these forward-looking statements, and any assumptions upon which they are based, are made in good faith and reflect our current judgment regarding the direction of our business, actual results will almost always vary, sometimes materially, from any estimates, predictions, projections, assumptions or other future performance suggested herein. Except as required by applicable law, including the securities laws of the United States, we do not intend to update any of the forward-looking statements to conform these statements to actual results.

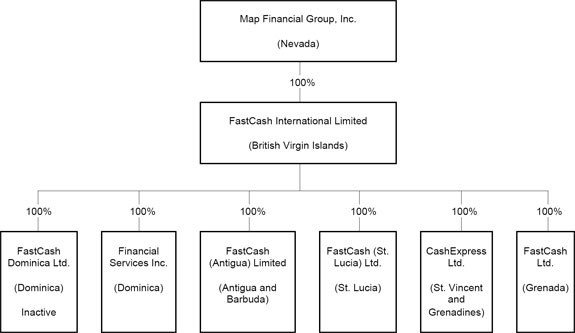

As used in this prospectus, references to the “Company,” “we,” “our” or “us” refer to Map Financial Group, Inc., unless the context otherwise indicates. The “Operating Subsidiaries” or “Affiliates” refers collectively to Financial Services Inc., FastCash (Antigua) Limited, FastCash (St. Lucia) Ltd., CashExpress Ltd. and FastCash Ltd.

The following summary highlights material information contained in this prospectus. Before making an investment decision, you should read the entire prospectus carefully, including the “Risk Factors” section, the financial statements and the notes to the financial statements.

Corporate Background

Map Financial Group, Inc. was incorporated under the laws of the State of Nevada on June 27, 2008, and it operates as a financial services holding company for five indirect, wholly-owned operating subsidiaries that provide micro-lending services in the Caribbean. On August 29, 2008 we completed the acquisition of FastCash International Limited, a British Virgin Islands financial services company, in exchange for 10 million shares of our common stock. On July 14, 2008 FastCash International and Robert Tonge, our Chief Operating Officer, executed a stock purchase agreement, pursuant to which FastCash International acquired all of the issued and outstanding share capital of Financial Services Inc., a Commonwealth of Dominica corporation, FastCash (Antigua) Limited, an Antigua and Barbuda corporation, FastCash (St. Lucia) Ltd., a St. Lucia corporation, CashExpress Ltd., a St. Vincent and Grenadines corporation, FastCash Ltd., a Grenada corporation, and FastCash Dominica Ltd., an inactive Commonwealth of

1

Dominica corporation. Through the Operating Subsidiaries, we offer short term micro-loans to the employees of various governmental agencies and private companies in the Commonwealth of Dominica, Antigua and Barbuda, St. Lucia, St. Vincent and the Grenadines and Grenada, as well as check cashing services. Revenues (unaudited) from January 1, 2008 to July 31, 2008 generated by the Operating Subsidiaries were $758,960, with a net profit of $166,500.

Our principal executive offices are currently located at 460 West 34th Street, 10th Floor, New York, New York 10001, and the telephone number at our principal executive offices is (212) 629-1955. We do not have an internet website at this time.

The Offering

|

|

|

Securities offered: |

| Up to 500,000 shares of common stock, to be issued and sold by the Company. |

|

|

|

Offering price: |

| $1.00 per share. The $1.00 offering price represents a significant premium over the $0.001 per share offering price for our shares of common stock in the private placement that we completed on July 31, 2008. We believe that the higher offering price is appropriate because the shares of our common stock offered hereby will be registered for public trading. |

|

|

|

Shares outstanding |

| 20,000,000 shares of common stock. |

|

|

|

Shares outstanding |

| 20,500,000 shares of common stock, if we are successful at selling all the shares offered hereby. |

|

|

|

|

| Jonathan Chesky Malamud, our CEO, President and a director, holds proxies entitling him to vote 100% of the outstanding stock. As a result, Mr. Malamud has complete control over all matters submitted to our stockholders for approval. None of our executive officers and directors has any intention to purchase shares in the offering. |

|

|

|

Market for the |

| There is currently no market for our securities. Our common stock is not traded on any exchange or on the over-the-counter market. After the effective date of the registration statement relating to this prospectus, we hope to have a market maker file an application with the FINRA for our common stock to be eligible for trading on the Over The Counter Bulletin Board. We do not yet have a market maker who has agreed to file such application. |

|

|

|

|

| There is no assurance that a trading market will develop, or, if developed, that it will be sustained. Consequently, a purchaser of our common stock may find it difficult to resell the securities |

2

|

|

|

|

| offered herein should the purchaser desire to do so when eligible for public resale. |

|

|

|

Use of proceeds: |

| If we are successful at selling the maximum of 500,000 shares we are offering, our gross proceeds from this offering will be $500,000. We intend to use these proceeds towards marketing, general and administrative expenses and working capital. See the section below entitled “Use of Proceeds.” |

|

|

|

Offering period |

| The offering will commence as soon as practicable after the effective date of the registration statement relating to this prospectus and terminate 180 days after such effective date, but such termination date may be extended for up to an additional 90 days in our discretion. |

|

|

|

|

| We reserve the right to terminate the offering at an earlier date, in our sole discretion, even if no shares are sold. In the event that the offering is terminated at an earlier date, funds received with respect to subscriptions made prior to any such termination will be non-refundable to subscribers. |

Summary Consolidated Financial Information

The following tables set forth: (i) certain summary, consolidated, unaudited, financial information regarding the results of operations of Map Financial Group, Inc. for the nine month periods ended September 30, 2008 and 2007, and its financial condition as at September 30, 2008 and September 30, 2007; and (ii) certain summary, combined, audited financial information regarding the results of operations of Financial Services, Inc. and Affiliates for the years ended December 31, 2008 and 2007, and their financial condition as at December 31, 2007 and 2006. This information is derived from, it should be read in conjunction with, and it is qualified in its entirety by reference to the audited financial statements of Map Financial Group for the period from June 27, 2008 (inception) to July 31, 2008, including the notes thereto, which are attached hereto as an exhibit, and the Management’s Discussion and Analysis of Financial Condition and Results of Operation below.

The financial statements of Map Financial Group, FastCash International and Financial Services, Inc. and Affiliates have been prepared in accordance with accounting principles generally accepted in the United States and general practices within the financial services industry. The financial condition and results of operations of FastCash International, Financial Services, Inc. and Affiliates are measured using the local currency, Eastern Caribbean Dollars, as the functional currency. FastCash International, Financial Services, Inc. and Affiliates generate and expend cash primarily in their local currency. Revenues and expenses have been translated into U.S. dollars at average exchange rates prevailing during the period. Assets and liabilities have been translated at the rates of exchange on the balance sheet date. There were no major exchange rate fluctuation during the period presented below, and therefore no foreign exchange gain or loss arising from translation was recorded for these periods.

3

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||

|

| Map Financial Group, Inc. |

| Financial Services, Inc. and Affiliates |

| ||||||||

|

| Consolidated Income Statements |

| Combined Income Statements |

| ||||||||

|

| Nine Months |

| Nine Months |

| Year Ended |

| Year Ended |

| ||||

|

| (Unaudited) |

| (Audited) |

| ||||||||

|

|

|

| ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Income |

| $ | 897,446 |

| $ | 365,487 |

| $ | 476,922 |

| $ | 188,539 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating Expenses |

|

| 706,168 |

|

| 277,188 |

|

| 519,414 |

|

| 170,278 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Income Tax Provision |

|

| 73,318 |

|

| 31,099 |

|

| 19,435 |

|

| 10,290 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Profit (Loss) |

|

| 117,960 |

|

| 57,200 |

|

| (61,927 | ) |

| (7,971 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic and Diluted Net Profit (Loss) Per Share: |

| $ | (1.23854 | ) | $ | 0.39855 |

| $ | (0.86788 | ) | $ | (0.51725 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Weighted Average Number of Common Shares Outstanding |

|

| 20,000,000 |

|

| 20,000,000 |

|

| 50,000 |

|

| 20,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Consolidated Balance Sheets |

| Combined Balance Sheets |

| ||||||||

|

| September 30, 2008 |

| September 30, 2007 |

| Year Ended |

| Year Ended |

| ||||

|

| (Unaudited) |

| (Audited) |

| ||||||||

|

|

|

| ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Current Assets |

| $ | 1,783,185 |

| $ | 955,108 |

| $ | 1,218,176 |

| $ | 327,662 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Assets |

|

| 1,846,074 |

|

| 982,967 |

|

| 1,257,572 |

|

| 359,909 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Current Liabilities |

|

| 1,731,349 |

|

| 868,245 |

|

| 1,257,618 |

|

| 298,467 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Liabilities and Stockholders’ Equity |

| $ | 1,846,074 |

| $ | 982,967 |

| $ | 1,275,572 |

| $ | 359,909 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

An investment in our common stock involves a high degree of risk. You should carefully consider the following factors and other information in this prospectus before deciding to invest in our company. If any of the following risks actually occur, our business, financial condition, results of operations and prospects for growth would likely suffer. As a result, you could lose all or part of your investment.

4

Risk Factors Relating to Our Company

We may never be able to effectuate our business plan or achieve any revenues or profitability; at this stage of our business, even with our good faith efforts, potential investors have a high probability of losing their entire investment.

Map Financial Group was established on June 27, 2008, to act as a holding company for the Operating Subsidiaries that provide micro-lending services in the Caribbean. Our operations to date have been focused on organizational, start-up and fund-raising activities and our acquisition of FastCash International Limited. Although the Operating Subsidiaries have been profitable in the past, they have limited operating histories. Furthermore, our revenue and income potential following the combination of the Operating Subsidiaries, which occurred in July 2008, is unproven, as the lack of operating history on a consolidated basis makes it difficult to evaluate the future prospects of our business. Failure to profitably integrate these businesses or to successfully combine and implement our operations and strategies could have a material adverse effect on our operating results.

Since repayment in full of our working capital loan facility is due on June 30, 2010, we might find ourselves in a position that we cannot lend any additional micro-loans. This situation would significantly impact our operations.

The Master Loan Agreement among MapCash Management, Ltd., FastCash International Limited and all its subsidiaries, pursuant to which FastCash International and the subsidiaries can borrow up to $10,000,000, is due and payable on demand. If we are unable to generate sufficient cash flows from operations, we will continue to be dependent on this credit facility. In the event of a default under the Master Loan Agreement, after repayment is demanded or if we are unable to borrow funds pursuant to the Master Loan Agreement for any other reason, we will not be able to make any additional loans until we enter into another credit facility or locate another source of financing. If we cannot secure a new credit facility or locate another source of funding and, as a result, cannot continue making loans after our existing credit facility matures, there would be a material adverse effect on our financial condition and results of operations and our stockholders may lose their entire investment in us.

If Ice Assets, LLC refuses to advance funds to MapCash Management, Ltd., MapCash Management might not be able to advance funds to us under the Master Loan Agreement and we will not be able to continue making micro-loans. This situation would significantly impact our operations.

MapCash Management, Ltd. obtains the funds required to make loans to FastCash International and the Operating Subsidiaries under the Master Loan Agreement pursuant to a $10,000,000 Line of Credit agreement between MapCash Management and Ice Assets, LLC, a New York limited liability company which is 50% owned by Joel Zev Drizin, a director of ours. The terms of the $10,000,000 Line of Credit agreement provide, among other things, that Ice Assets has sole and absolute discretion with respect to any advances to MapCash Management. If Ice Assets refuses to advance funds to

5

MapCash Management under the $10,000,000 Line of Credit agreement and if MapCash Management is unable to secure an alternative source of funding, MapCash Management might not be able to advance funds to us under the Master Loan Agreement. In any such event, if we cannot secure an alternative source of funding we will not be able to continue making micro-loans and that would have a material adverse effect on our financial condition and results of operations.

If we are unable to obtain additional financing, our business operations will be harmed. Even if we do obtain additional financing then our existing shareholders may suffer substantial dilution.

We require additional funds to operate our business and anticipate that we will require a minimum of $1,314,000 to fund our continued operations for the next twelve months. In addition, we have outstanding obligations to be paid in the next twelve months equaling $148,876. Although the Operating Subsidiaries are parties to the $10,000,000 Master Loan Agreement with MapCash Management, we currently have no definitive plan as to how we intend to raise the funds required to operate our business for the next twelve months and satisfy our outstanding obligations. The inability to raise the required capital will restrict our ability to grow and may reduce our ability to continue to conduct business operations. If we are unable to obtain necessary financing, we will likely be required to curtail our plans which could result in us not becoming profitable. If we have to issue stock, such additional equity financing may involve substantial dilution to our then existing shareholders.

We are subject to any new or additional laws enacted by foreign governments.

Based on legal opinions that we have received, we believe that we are not presently subject to the banking and financial institution laws and regulations of the Caribbean countries in which we operate. However, foreign governments may impose new or additional rules on offering short term micro-loans, including regulations which (i) regulate the interest rate which we can charge on the loans we make; (ii) prohibit transactions in, to or from certain countries, governments, nationals and individuals or entities; (iii) impose additional identification, reporting or recordkeeping requirements; (iv) limit or restrict the revenue which may be generated from such loans; (v) require additional disclosures to the borrowers; or (vi) require a license to lend money. In addition, we are subject to all other laws and regulations of the foreign countries in which we operate. Such legislation may curtail our operations, reduce the amount of profits we make on loans and otherwise have an adverse impact on our operations. We may not have the resources to obtain any new license requirements imposed by any regulatory agencies which have jurisdiction over our business.

If we lose the services of key members of our management team, we may not be able to execute our business strategy effectively.

The success of our business is dependent on the services of our officers and directors, particularly Mr. Jonathan Chesky Malamud, our CEO and President, Mr. Robert Tonge, our COO, and Mr. Samuel Rosenberg, our CFO. The services of these individuals are

6

critical to our overall management and operations as well as our strategic direction. None of these individuals are required to work exclusively for us, and we do not have any agreements, written or otherwise, with any of these individuals. We do not have any key-man life insurance policies. The loss of any of our management or key personnel could materially harm our business.

If we lose the services of NBL Technologies Inc., we may not be able to execute our business strategy effectively.

Each of the Operating Subsidiaries is a party to a three year services agreement with NBL Technologies Inc., a Belizean corporation that is controlled by our Chief Operating Officer, Robert Tonge. Pursuant to these agreements, NBL Technologies provides personnel management, facilities and equipment management and other services to the Operating Subsidiaries. If we are unable to obtain these services from NBL Technologies for any reason and are unable to secure an alternative provider of these services, we will not be able to execute our business strategy effectively and our stockholders may lose their entire investment in us.

Our executive officers beneficially own a majority of the outstanding shares of our common stock, and other stockholders may not be able to influence control of the company or decision making by management of the company.

Our officers and directors presently own 91% of our outstanding common stock. In addition, Mr. Jonathan Chesky Malamud, our CEO, President and a director, holds proxies entitling him to vote 100% of the outstanding stock. As a result, our executive officers have complete control over all matters submitted to our stockholders for approval including the following matters: election of our board of directors; removal of any of our directors; amendment of our Articles of Incorporation or bylaws; and adoption of measures that could delay or prevent a change in control or impede a merger, takeover or other business combination involving us. Other stockholders may find the corporate decisions influenced by our executive officers are inconsistent with the interests of other stockholders. In addition, other stockholders may not be able to change the directors and officers, and are accordingly subject to the risk that management cannot manage the affairs of the Company in accordance with such stockholders’ wishes.

Our officers have no experience in managing a public company, which increases the risk that we will be unable to establish and maintain all required disclosure controls and procedures and internal controls over financial reporting and meet the public reporting and the financial requirements for our business.

Our management has a legal and fiduciary duty to establish and maintain disclosure controls and control procedures in compliance with the securities laws, including the requirements mandated by the Sarbanes-Oxley Act of 2002. Although our officers have substantial business experience, they have no experience in managing a public company. The standards that must be met for management to assess the internal control over financial reporting as effective are complex, and require significant documentation, testing and possible remediation to meet the detailed standards. Because our officers have

7

no prior experience with the management of a public company, we may encounter problems or delays in completing activities necessary to make an assessment of our internal control over financial reporting, and disclosure controls and procedures. In addition, the attestation process by our independent registered public accounting firm is new and we may encounter problems or delays in completing the implementation of any requested improvements and receiving an attestation of our assessment by our independent registered public accounting firm. If we cannot assess our internal control over financial reporting as effective or provide adequate disclosure controls or implement sufficient control procedures, or our independent registered public accounting firm is unable to provide an unqualified attestation report on such assessment, investor confidence and share value may be negatively impacted.

Risk Factors Relating to Our Common Stock

We may, in the future, issue additional common shares, which would reduce investors’ percent of ownership and may dilute our share value.

Our Articles of Incorporation authorizes the issuance of 500 million shares of common stock, par value $.001 per share, of which 20 million shares are currently issued and outstanding, and 5 million shares of preferred stock, par value $.001 per share, none of which are currently issued and outstanding. The future issuance of common stock or convertible preferred stock may result in substantial dilution in the percentage of our common stock held by our then existing shareholders. We may value any common stock issued in the future on an arbitrary basis. The issuance of common stock for future services or acquisitions or other corporate actions may have the effect of diluting the value of the shares held by our investors, and might have an adverse effect on any trading market for our common stock. We do not currently have any plans, arrangements or understandings to issue additional shares of common or preferred stock in the next twelve months.

Our common stock is subject to the “penny stock” rules of the Securities and Exchange Commission (“SEC”) and the trading market in our securities will in all likelihood be limited, which makes transactions in our stock cumbersome and may reduce the value of an investment in our stock.

The Securities and Exchange Commission has adopted Rule 15g-9 which establishes the definition of a “penny stock,” for the purposes relevant to us, as any equity security that has a market price of less than $5.00 per share or with an exercise price of less than $5.00 per share, subject to certain exceptions. For any transaction involving a penny stock, unless exempt, the rules require: (i) that a broker or dealer approve a person’s account for transactions in penny stocks; and (ii) the broker or dealer receive from the investor a written agreement to the transaction, setting forth the identity and quantity of the penny stock to be purchased. In order to approve a person’s account for transactions in penny stocks, the broker or dealer must: (i) obtain financial information and investment experience objectives of the person; and (ii) make a reasonable determination that the transactions in penny stocks are suitable for that person and the person has sufficient

8

knowledge and experience in financial matters to be capable of evaluating the risks of transactions in penny stocks.

The broker or dealer must also deliver, prior to any transaction in a penny stock, a disclosure schedule prescribed by the Security and Exchange Commission relating to the penny stock market, which, in highlight form: (i) sets forth the basis on which the broker or dealer made the suitability determination; and (ii) that the broker or dealer received a signed, written agreement from the investor prior to the transaction.

Generally, brokers may be less willing to execute transactions in securities subject to the “penny stock” rules. This may make it more difficult for investors to dispose of our common stock and cause a decline in the market value of our stock.

Disclosure also has to be made about the risks of investing in penny stocks in both public offerings and in secondary trading and about the commissions payable to both the broker-dealer and the registered representative, current quotations for the securities and the rights and remedies available to an investor in cases of fraud in penny stock transactions. Finally, monthly statements have to be sent disclosing recent price information for the penny stock held in the account and information on the limited market in penny stocks.

We intend to retain any future earnings to finance the development and expansion of our business. We do not anticipate paying any cash dividends on our common stock in the foreseeable future. Unless we pay dividends, our stockholders will not be able to receive a return on their shares unless they sell them at a price higher than that which they initially paid for such shares.

The market for penny stocks has experienced numerous frauds and abuses which could adversely impact investors in our stock.

We believe that the market for penny stocks has suffered from patterns of fraud and abuse. Such patterns include:

|

|

|

| • | Control of the market for the security by one or a few broker-dealers that are often related to the promoter or issuer; |

|

|

|

| • | Manipulation of prices through prearranged matching of purchases and sales and false and misleading press releases; |

|

|

|

| • | “Boiler room” practices involving high pressure sales tactics and unrealistic price projections by inexperienced sales persons; |

|

|

|

| • | Excessive and undisclosed bid-ask differentials and markups by selling broker-dealers; and |

The wholesale dumping of the same securities by promoters and broker-dealers after prices have been manipulated to a desired level, along with the inevitable collapse of those prices with consequent investor losses.

9

The offering price of our common stock could be higher than the market value, causing investors to sustain a loss of their investment.

The price of our common stock in this offering has not been determined by any independent financial evaluation, market mechanism or by our auditors, and is therefore, to a large extent, arbitrary. Our independent auditor has not reviewed management’s valuation, and therefore expresses no opinion as to the fairness of the offering price as determined by our management. As a result, the price of the common stock in this offering may not reflect the value perceived by the market. If the shares offered hereby cannot subsequently be sold at or above the price for which they are offered, investors may lose a portion or all of their investment.

The price at which we sold shares of our common stock in our private placement was significantly lower than the price of our common stock in this offering; if investors in our private placement offer to sell their shares at a lower price than the price per share in this offering, the market price of our shares would be adversely effected.

On July 31, 2008 we completed a private placement of 10 million shares of our common stock for aggregate gross proceeds of $10,000, or $0.001 per share. If this offering is completed and a public market for our shares is established, after the expiration of the applicable waiting period investors in our private placement may offer and sell a substantial number of shares at a price which is significantly lower than the $1 per share price in this offering. Any such offers and sales could have a material adverse effect on the value of our shares, as perceived by the market, making it difficult for investors in this offering to realize any gain on their investments in our common stock. The successful completion of this offering and the establishment of a public market for our shares would facilitate any such sales by the investors in our private placement.

State securities laws may limit secondary trading, which may restrict the states in which and conditions under which you can sell the shares offered by this prospectus.

Secondary trading in common stock sold in this offering will not be possible in any state until the common stock is qualified for sale under the applicable securities laws of the state or there is confirmation that an exemption, such as listing in certain recognized securities manuals, is available for secondary trading in the state. If we fail to register or qualify, or to obtain or verify an exemption for the secondary trading of the common stock in any particular state, the common stock could not be offered or sold to, or purchased by, a resident of that state. In the event that a significant number of states refuse to permit secondary trading in our common stock, the liquidity for the common stock could be significantly impacted thus causing you to realize a loss on your investment.

10

There is currently no public market for our securities, a public market for our securities might never develop and our common stock might never be quoted for trading and, even if quoted, it is likely to be subject to significant price fluctuations.

There has not been any established trading market for our common stock, and there is currently no public market whatsoever for our securities. Additionally, no public trading can occur until we file and have declared effective a Registration Statement with the SEC. Even after registration with the SEC, a lack of investor interest in us could prevent the development of an active, liquid trading market for our common stock. Active trading markets generally result in lower price volatility and more efficient execution of buy and sell orders for investors.

In addition, our common stock is unlikely to be followed by any market analysts, and there may be few institutions acting as market makers for our common stock. Either of these factors could adversely affect the liquidity and trading price of our common stock. Until our common stock is fully distributed and an orderly market develops in our common stock, if ever, the price at which it trades is likely to fluctuate significantly. Prices for our common stock will be determined in the marketplace and may be influenced by many factors, including the depth and liquidity of the market for shares of our common stock, developments affecting our business, including the impact of the factors referred to elsewhere in these Risk Factors, investor perception of the Company and general economic and market conditions.

If a market develops for our shares, sales of our shares relying upon Rule 144 may depress prices in that market by a material amount.

All of the outstanding shares of our common stock held by present stockholders are “restricted securities” within the meaning of Rule 144 under the Securities Act of 1933, as amended.

As restricted shares, they may be resold only pursuant to an effective registration statement or pursuant to the requirements of Rule 144 or other applicable exemptions from registration under the Securities Act and as required under applicable state securities laws. On November 15, 2007, the Securities and Exchange Commission adopted changes to Rule 144, which shorten the holding period for sales by non-affiliates to six months (subject to extension under certain circumstances) and remove the volume limitations for such persons. The changes became effective in February 2008. Rule 144 provides, in essence, that a shareholder that is not affiliated with the issuer (and has not been an affiliate of the issuer for at least 90 consecutive days prior to the sale) who has held restricted securities for a prescribed period may, under certain conditions, sell an unlimited number of the issuer’s restricted securities so long as the issuer has filed all reports and other material required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934, as applicable, during the preceding 12 months. With respect to affiliates, Rule 144 provides that an affiliate who has held restricted securities for a prescribed period may, under certain conditions, sell every three months, in brokerage transactions, a number of shares that does not exceed 1.0% of a company’s outstanding common stock. The alternative average weekly trading volume during the four calendar

11

weeks prior to the sale is not available to our shareholders being that the Over the Counter Bulletin Board (“OTCBB”) (if and when our shares are listed thereon) is not an “automated quotation system” and, accordingly, market based volume limitations are not available for securities quoted only over the OTCBB. As a result of the revisions to Rule 144, there is no limit on the amount of restricted securities that may be sold by a non-affiliate (i.e., a stockholder who has not been an officer, director or control person for at least 90 consecutive days) after the restricted securities have been held by the owner for a period of six months, if the Company has filed its required reports with the SEC. A sale under Rule 144 or under any other exemption from the Securities Act, if available, or pursuant to registration of shares of common stock of present stockholders, may have a depressive effect upon the price of the common stock in any market that may develop.

We may issue shares of preferred stock in the future that may adversely impact your rights as holders of our common stock.

Our Articles of Incorporation authorize us to issue up to 5,000,000 shares of “blank check” preferred stock. Accordingly, our board of directors will have the authority to fix and determine the relative rights and preferences of preferred shares, as well as the authority to issue such shares, without further stockholder approval. As a result, our board of directors could authorize the issuance of a series of preferred stock that would grant to holders preferred rights to our assets upon liquidation, the right to receive dividends before dividends are declared to holders of our common stock, and the right to the redemption of such preferred shares, together with a premium, prior to the redemption of the common stock. To the extent that we do issue any such shares of preferred stock, your rights as holders of common stock could be impaired thereby, including, without limitation, dilution of your ownership interests in us. In addition, shares of preferred stock could be issued with terms calculated to delay or prevent a change in control or make removal of management more difficult, which may not be in your interest as holders of common stock.

We may be exposed to potential risks resulting from new requirements under Section 404 of the Sarbanes-Oxley Act of 2002.

If we become registered with the SEC, we will be required, pursuant to Section 404 of the Sarbanes-Oxley Act of 2002, to include in our annual report our assessment of the effectiveness of our internal control over financial reporting. We do not have a sufficient number of employees to segregate responsibilities and may be unable to afford increasing our staff or engaging outside consultants or professionals to overcome our lack of employees.

The costs to meet our reporting and other requirements as a public company subject to the Securities Exchange Act of 1934 will be substantial and may result in us having insufficient funds to expand our business or even to meet routine business obligations.

If this offering is successful, we will become a public entity, subject to the reporting requirements of the Securities Exchange Act of 1934. As a result, we will incur ongoing

12

expenses associated with professional fees for accounting, legal and a host of other expenses for annual reports and proxy statements. We estimate that these costs will range up to $200,000 per year for the next few years and will be higher if our business volume and activity increases but lower during the first year of being public because our overall business volume will be lower, and we will not yet be subject to the requirements of Section 404 of the Sarbanes-Oxley Act of 2002. As a result, we may not have sufficient funds to grow our operations.

Because we are not subject to compliance with rules requiring the adoption of certain corporate governance measures, our stockholders have limited protections against interested director transactions, conflicts of interest and similar matters.

The Sarbanes-Oxley Act of 2002, as well as rule changes proposed and enacted by the SEC, the New York and American Stock Exchanges and the Nasdaq Stock Market as a result of Sarbanes-Oxley, require the implementation of various measures relating to corporate governance. These measures are designed to enhance the integrity of corporate management and the securities markets and apply to securities which are listed on those exchanges or the Nasdaq Stock Market. Because we are not presently required to comply with many of the corporate governance provisions and because we chose to avoid incurring the substantial additional costs associated with such compliance any sooner than necessary, we have not yet adopted these measures.

Because all our directors are non-independent, we do not currently have independent audit or compensation committees. As a result, our directors have the ability, among other things, to determine their own level of compensation. Until we comply with such corporate governance measures, regardless of whether such compliance is required, the absence of such standards of corporate governance may leave our stockholders without protections against interested director transactions, conflicts of interest and similar matters and investors may be reluctant to provide us with funds necessary to expand our operations.

This prospectus relates to the initial public offering and sale by us of up to an aggregate of 500,000 shares of the Company’s common stock, par value $0.001 per share. Such shares will be offered and sold at a price of $1.00 per share on a “best efforts no minimum basis” by our directors and officers on our behalf, and no underwriters or broker-dealers will be involved in the offering. Funds received as payment for shares will be deposited into a bank account maintained by us and under our control, and will immediately be available for our use. All funds received by us will be retained for our use and will not be refunded.

There is no minimum number of shares that each subscriber is required to purchase and no minimum number of shares that must be sold in this offering. As a result, we might not be successful in raising a significant amount of capital in this offering.

The offering will commence as soon as practicable after the effective date of the registration statement relating to this prospectus and terminate 180 days after such

13

effective date, but such termination date may be extended for up to an additional 90 days in our discretion. We reserve the right to terminate the offering at an earlier date, in our sole discretion, even if no shares are sold.

If the sale of the maximum amount of shares being offered herein is achieved, of which there is no assurance, we estimate that the net proceeds from this offering will be approximately $400,000, after deducting $100,000 for estimated offering expenses, which include legal and accounting fees.

The proceeds are expected to be disbursed, in the priority set forth below, during the first twelve (12) months after the successful completion of the offering as set forth in the table below. The table below sets forth the use of proceeds if only 250,000 shares and if all 500,000 shares are sold.

|

|

|

|

|

|

|

|

|

| Sale of |

| Sale of |

| ||

|

|

|

| ||||

|

|

|

|

|

| ||

Gross Proceeds: |

| $ | 250,000 |

| $ | 500,000 |

|

Offering Expenses: |

| $ | 100,000 |

| $ | 100,000 |

|

Net Proceeds: |

| $ | 150,000 |

| $ | 400,000 |

|

The net proceeds will be used as follows:

|

|

|

|

|

|

|

|

Marketing: |

| $ | 30,000 |

| $ | 80,000 |

|

|

|

|

|

|

|

|

|

Working Capital: |

| $ | 120,000 |

| $ | 320,000 |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

Totals: |

| $ | 150,000 |

| $ | 400,000 |

|

That portion of the net proceeds not required for immediate expenditure may be deposited into an interest-bearing account or invested in short-term government notes, treasury bills, or similar obligations of financial institutions, at the sole discretion of the Company.

DETERMINATION OF OFFERING PRICE

Our common stock is presently not traded on any market or securities exchange and we have not applied for listing or quotation on any public market. Our Company will be offering the shares of common stock being covered by this prospectus at a price of $1.00 per share. Such offering price does not have any relationship to any established criteria of value, such as book value or earnings per share. Because we have no significant operating history and have not generated any revenues to date, the price of our common stock is not based on past earnings, nor is the price of our common stock indicative of the

14

current market value of the assets owned by us. No valuation or appraisal has been prepared for our business and potential business expansion.

The $1.00 offering price represents a significant premium over the $0.001 per share offering price for our shares of common stock in the private placement that we completed on July 31, 2008. We believe that the higher offering price is appropriate because the shares of our common stock offered hereby will be registered for public trading.

The offering price was determined arbitrarily based on a determination of the Board of Directors of the price at which they believed investors would be willing to purchase the shares. Additional factors that were included in determining the offering price are the lack of liquidity resulting from the fact that there is no present market for our stock and the high level of risk considering our lack of profitable operating history.

DILUTION

10,000,000 shares of our presently issued and outstanding shares of common stock were issued in a private placement to our initial shareholders at par value in consideration for cash payments aggregating $10,000. In contrast, all of the shares offered hereby are being offered at $1.00 per share. Accordingly, the shares being offered hereby are being offered at a significantly higher price than the price paid by our founders, officers, directors and affiliates for shares of common stock purchased by them before this offering. The following table assumes that 500,000 shares will be issued and sold in this offering and compares, on a pro forma basis, the ownership percentage acquired and the consideration paid by our founders, officers, directors and affiliates to the ownership percentage and offering price per share being offered hereby.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Number |

| Percentage of |

| Consideration Paid |

| Percentage of Total |

| Average |

| |||

|

|

|

|

|

|

| ||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||

Initial Shareholders, Officers and Directors |

| 10,000,000 |

| 48.78 | % | $ | 10,000 |

|

| 1.96 | % | $ | 0.001 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

New Investors |

| 500,000 |

| 2.44 | % | $ | 500,000 |

|

| 98.04 | % | $ | 1.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

| 10,500,000 | (1) | 51.22 | % | $ | 510,000 |

|

| 100 | %(2) |

|

|

|

(1) Excludes 10,000,000 shares issued to Bayville Global, Ltd. on August 29, 2008 in exchange for all of the issued and outstanding share capital of FastCash International Limited, a British Virgin Islands company.

(2) Excludes the consideration paid by Bayville Global, Ltd. for 10,000,000 shares of our common stock that were issued to Bayville Global, Ltd. on August 29, 2008 in exchange for all of the issued and outstanding share capital of FastCash International Limited.

15

“Dilution” as the term is used herein, is a reduction in the value of a purchaser’s investment measured by the difference between the purchase price and the net tangible book value of the common shares after the purchase takes place. “Net book value” represents the amount of total assets less the amount of total liabilities divided by the number of shares of our common stock outstanding. This dilution arises mainly from the arbitrary decision as to the offering price per share and the lower book value of the shares of our currently outstanding. As we are a development stage company with limited assets, no operations or revenues at this time, there is no reasonable measure of the net tangible book value per share for our outstanding common stock.

The following table summarizes the dilution which investors participating in the offering would incur and the benefit to current shareholders as a result of this offering, if 250,000 shares or 500,000 shares are sold (after deducting any legal, accounting, printing, or other offering costs incurred in connection with this offering, which are estimated to be approximately $100,000 in the aggregate).

|

|

|

|

|

|

|

|

|

| Sale of 250,000 Shares |

| Sale of 500,000 Shares |

| ||

|

|

|

| ||||

|

|

|

|

|

| ||

Net Tangible Book Value Per Share Prior to the Offering |

| $ | 0.011 |

| $ | 0.011 |

|

|

|

|

|

|

|

|

|

Increase in Net Tangible Book Value Per Share Attributable to this Offering |

| $ | 0.007 |

| $ | 0.020 |

|

|

|

|

|

|

|

|

|

Net Tangible Book Value Per Share After this Offering |

| $ | 0.018 |

| $ | 0.031 |

|

|

|

|

|

|

|

|

|

Dilution to New Investors |

| $ | 0.982 |

| $ | 0.969 |

|

There has been no market for our securities. Our common stock is not traded on any exchange or on the over-the-counter market. After the effective date of the registration statement relating to this prospectus, we hope to have a market maker file an application with the Financial Industry Regulatory Authority for our common stock to eligible for trading on the OTCBB. We do not yet have a market maker who has agreed to file such application.

We are offering up to a maximum of 500,000 shares of our common stock by direct public offering on a “best efforts no minimum basis.” The offering price is $1.00 per share. The shares will be sold on our behalf by our officers and directors. None of our officers or directors will receive any commissions or proceeds from the offering for selling shares on our behalf. No brokers, dealers or finders or agent for commission are involved in this offering.

16

The offering will commence as soon as practicable after the effective date of the registration statement relating to this prospectus. It will terminate 180 days after such effective date, but such termination date may be extended for up to an additional 90 days in our discretion. We reserve the right to terminate the offering at an earlier date, in our sole discretion, even if no shares are sold.

There are no other minimum purchase requirements, and there are no arrangements to place the funds in an escrow, trust, or similar account. Funds received by us as payment for shares subscribed for in the offering will be deposited into a bank account maintained by us and under our control and will immediately be available for our use. All funds received by us will be retained for our use and will not be refunded.

As noted above, we will sell the shares in this offering through our officers and directors. Such persons will receive no commission from the sale of any shares. They will not register as a broker-dealer under section 15 of the Securities Exchange Act of 1934, in reliance upon Rule 3a4-1. Rule 3a4-1 sets forth those conditions under which a person associated with an issuer may participate in the offering of the issuer’s securities and not be deemed to be a broker/dealer. The conditions are namely: (1) The person is not statutorily disqualified, as that term is defined in Section 3(a)(39) of the Exchange Act, at the time of his participation; (2) The person is not compensated in connection with his participation by the payment of commissions or other remuneration based either directly or indirectly on transactions in securities; (3) The person is not at the time of their participation, an associated person of a broker/dealer; and (4) The person meets the conditions of Paragraph (a)(4)(ii) of Rule 3a4-1 of the Exchange Act, in that he (A) primarily performs, or is intended primarily to perform at the end of the offering, substantial duties for or on behalf of the issuer otherwise than in connection with transactions in securities; and (B) is not a broker or dealer, or an associated person of a broker or dealer, within the preceding twelve (12) months; and (C) does not participate in selling and offering of securities for any issuer more than once every twelve (12) months other than in reliance on Paragraphs (a)(4)(i) or (a)(4)(iii).

Our officers and directors are not statutorily disqualified, are not being compensated, and are not associated with a broker/dealer. They are and will continue to be our officers and directors at the end of the offering and have not been during the last twelve months and are currently not a broker/dealer or associated with a broker/dealer. They will not participate in selling and offering securities for any issuer more than once every twelve months.

Only after our registration statement relating to this prospectus is declared effective by the SEC, do we intend to hold investment meetings in various states where the offering will be registered. We will not utilize the Internet or any form of paid media to advertise our offering, but rather through meetings arranged by our officers and directors and their business associates and their friends or relatives who may also distribute the prospectus to potential investors who are interested in us and in making a possible investment in the offering. No shares purchased in this offering will be subject to any kind of lock-up or trust agreement, implicit or explicit.

17

Procedures for Subscribing

We will not accept any money until this registration statement is declared effective by the SEC. Once the registration statement is declared effective by the SEC, if you decide to subscribe for any shares in this offering, you must

1. execute and deliver a subscription agreement, a copy of which is included with the prospectus.

2. deliver a check or certified funds to us for acceptance or rejection.

All checks for subscriptions must be made payable to “Map Financial Group Inc.”

Right to Reject Subscriptions

We have the right to accept or reject subscriptions in whole or in part, for any reason or for no reason. All monies from rejected subscriptions will be returned immediately by us to the subscriber, without interest or deductions. Subscriptions for securities will be accepted or rejected within 48 hours after we receive them.

All expenses of the registration statement including, but not limited to, legal, accounting, printing and mailing fees are and will be borne by us.

Underwriters

We have no underwriter and do not intend to have one. In the event that we sell or intend to sell by means of any arrangement with an underwriter, then we will file a post-effective amendment to this registration statement on Form S-1 to accurately reflect the changes to us and our financial affairs and any new risk factors, and in particular to disclose such material relevant to this Plan of Distribution.

Regulation M

We are subject to Regulation M of the Securities Exchange Act of 1934. Regulation M governs activities of underwriters, issuers, selling security holders, and others in connection with offerings of securities. Regulation M prohibits distribution participants and their affiliated purchasers from bidding for purchasing or attempting to induce any person to bid for or purchase the securities being distributed.

Penny Stock Regulations

You should note that our stock is a penny stock. The Securities and Exchange Commission has adopted Rule 15g-9 which generally defines “penny stock” to be any equity security that has a market price (as defined) less than $5.00 per share or an exercise price of less than $5.00 per share, subject to certain exceptions. Our securities are covered by the penny stock rules, which impose additional sales practice requirements on broker-dealers who sell to persons other than established customers and

18

“accredited investors”. The term “accredited investor” refers generally to institutions with assets in excess of $5,000,000 or individuals with a net worth in excess of $1,000,000 or annual income exceeding $200,000 or $300,000 jointly with their spouse. The penny stock rules require a broker-dealer, prior to a transaction in a penny stock not otherwise exempt from the rules, to deliver a standardized risk disclosure document in a form prepared by the SEC which provides information about penny stocks and the nature and level of risks in the penny stock market. The broker-dealer also must provide the customer with current bid and offer quotations for the penny stock, the compensation of the broker-dealer and its salesperson in the transaction and monthly account statements showing the market value of each penny stock held in the customer’s account. The bid and offer quotations, and the broker-dealer and salesperson compensation information, must be given to the customer orally or in writing prior to effecting the transaction and must be given to the customer in writing before or with the customer’s confirmation. In addition, the penny stock rules require that prior to a transaction in a penny stock not otherwise exempt from these rules, the broker-dealer must make a special written determination that the penny stock is a suitable investment for the purchaser and receive the purchaser’s written agreement to the transaction. These disclosure requirements may have the effect of reducing the level of trading activity in the secondary market for the stock that is subject to these penny stock rules. Consequently, these penny stock rules may affect the ability of broker-dealers to trade our securities. We believe that the penny stock rules discourage investor interest in and limit the marketability of our common stock.

The following description of our capital stock is a summary and is qualified in its entirety by the provisions of our Articles of Incorporation which have been filed as an exhibit to our registration statement of which this prospectus is a part.

Common Stock

We are authorized to issue 500,000,000 shares of common stock, par value $0.001, of which 20,000,000 shares are issued and outstanding as of October 27, 2008. Each holder of shares of our common stock is entitled to one vote for each share held of record on all matters submitted to the vote of stockholders, including the election of directors. The holders of shares of common stock have no preemptive, conversion, subscription or cumulative voting rights. There is no provision in our Articles of Incorporation or By-laws that would delay, defer or prevent a change in control of our Company.

Preferred Stock

We are authorized to issue 5,000,000 shares of preferred stock, par value $0.001, none of which is issued and outstanding. Our board of directors has the right, without shareholder approval, to issue preferred shares with rights superior to the rights of the holders of shares of common stock. As a result, preferred shares could be issued quickly and easily, negatively affecting the rights of holders of common stock and could be issued with terms calculated to delay or prevent a change in control or make removal of

19

management more difficult. Because we may issue up to 5,000,000 shares of preferred stock in order to raise capital for our operations, your ownership interest may be diluted which results in your percentage of ownership in our Company decreasing.

Warrants and Options

There are no warrants, options or other convertible securities currently outstanding.

INTEREST OF NAMED EXPERTS AND COUNSEL

No expert or counsel named in this prospectus as having prepared or certified any part of this prospectus or having given an opinion upon the validity of the securities being registered or upon other legal matters in connection with the registration or offering of the common stock was employed on a contingency basis or had, or is to receive, in connection with the offering, a substantial interest, directly or indirectly, in the Company or any of its parents or subsidiaries. Nor was any such person connected with the Company or any of its subsidiaries as a promoter, managing or principal underwriter, voting trustee, director, officer or employee.

Map Financial Group, Inc. was incorporated under the laws of the State of Nevada on June 27, 2008, to act as a holding company for five indirect, wholly-owned operating subsidiaries that provide micro-lending services in the Caribbean, which subsidiaries are referred to herein as the Operating Subsidiaries. Through the Operating Subsidiaries, we offer short term micro-loans to the employees of various governmental agencies and private companies in the Commonwealth of Dominica, Antigua and Barbuda, St. Lucia, St. Vincent and the Grenadines and Grenada, as well as check cashing services.

The address of our principal executive office is 460 West 34th Street, 10th Floor, New York, New York 10001. Our telephone number is (212) 629-1955. We do not have an internet website at this time.

History

On July 14, 2008 FastCash International Limited acquired the Operating Subsidiaries and FastCash Dominica Ltd., which has been inactive since its formation, from Robert Tonge, our Chief Operating Officer. Each of the Operating Subsidiaries was owned and operated by Mr. Tonge from the date of its incorporation until it was acquired by FastCash International.

On July 31, 2008, we completed a private placement of 10 million shares of our common stock to 18 investors. The consideration paid for the shares was $0.001 per share, for aggregate gross proceeds of $10,000.

20

On August 29, 2008 we acquired all of the shares of FastCash International from Bayville Global, Ltd., a British Virgin Islands corporation, in a share exchange in which we issued 10 million shares of our common stock to Bayville Global.

The following chart illustrates our corporate structure:

Business

The management of FastCash International has established and, through the Operating Subsidiaries, it manages the operations of 5 branch offices and one agency (FastCash Ltd.) in five Eastern Caribbean countries. Each of the Operating Subsidiaries is a party to a three-year services agreement with NBL Technologies Inc., a Belizean corporation that is controlled by our Chief Operating Officer, Robert Tonge. Pursuant to these services agreements, NBL Technologies provides personnel management, facilities and equipment management and other services to our operating subsidiaries. FastCash International provides comprehensive management and personnel training and ongoing support for the employees of the Operating Subsidiaries. Training covers all aspects of the business, including loan approvals and processing, technology, marketing and banking and accounting. FastCash International also provides customer support via telephone and email. FastCash International obtains these services from its parent, Map Financial Group, pursuant to the terms of the Master Services Agreement between Map Financial

21

Group and FastCash International. In accordance with this agreement, which has a term of 3 years and is automatically renewable unless terminated by either party upon 180 days, payment for these services is based on the costs incurred by FastCash International.

The bulk of our revenues are generated by interest on the loans that we make and associated fees, which together accounted for over approximately 99% of our revenues in the seven months ended July 31, 2008 and approximately 98% of our revenues in the year ended December 31, 2007. The balance of our revenues are generated by check cashing services. Until May 2008 an immaterial portion of our revenues was generated by sales of pre-paid debit cards.

Loan funds are given to the employee/borrower on a pre-paid debit card. These cards are made available to us pursuant to the terms of the Master Loan Agreement, dated as of August 6, 2008, between MapCash Management Ltd., FastCash International Limited, FastCash Dominica Ltd. and the Operating Subsidiaries. Once a loan is approved and the required documentation is finalized, loan proceeds are made available to the borrower within a few hours of the loan approval. We have developed an integrated, proprietary, secure Internet-based system to administer the funding and processing of cash advance loans and payments.

Lending Practices. Our lending practices are tailored to the special circumstances in developing markets. In order to minimize our exposure, credit will only be offered to employees of institutions that have been approved in advance. All loans are repaid by the borrowers’ employers through salary deductions, and the prospective borrower must be an employee in good-standing for a minimum length of time. The loan amounts will be limited to a pre-determined percentage of the employee’s take-home pay. Prior to making any loan, the borrower’s employer acknowledges the terms of the borrower’s employment – generally how long the person has been employed and his or her current salary. Then the employer authorizes monthly salary deductions of interest, fees and principal from the employee’s paycheck, and the employee signs a promissory note for the aggregate principal amount of the loan, the interest and the fees. Although the employee is personally obligated to the particular Operating Subsidiary that is making the loan, the monthly installment payments are automatically deducted from the borrower’s paycheck and sent to the lending subsidiary directly by the employer.

The current negative economic conditions have not had any significant impact on our business to date. Although demand for our loans has not been affected, we recognize that borrowers may become unemployed as a result of layoffs and have taken steps to minimize the number of borrowers who are employed by especially vulnerable industries, such as the tourism industry.

Approved Employers; Approval Process

In order to qualify as an approved institution, an employer must (i) be in continuous operation for a period of at least two years, (ii) be registered with the national insurance or social security agencies and be current in all of its related payment obligations, and (iii) submit a registration form bearing a corporate seal and the signature of the owner, manager of chief accountant. Our local staff will be asked to confirm that they are personally familiar with the employer and its level of operations, and if they are not a representative will visit the prospective employer’s office in order to confirm the veracity of the information submitted in the registration form.

22

To date we have extended loans to the employees of an aggregate of approximately 1,302 approved institutions. In the Commonwealth of Dominica, where operations commenced in June 2004 - more than two years before our expansion into other countries - we have extended loans to the employees of approximately 382 approved institutions. In St. Lucia, where the population is significantly bigger than the population in the other countries in which we operate, we have extended loans to the employees of approximately 362 approved institutions. In St. Vincent and the Grenadines we have extended loans to the employees of approximately 215 approved institutions, in Grenada we have extended loans to the employees of approximately 183 approved institutions, and in Antigua and Barbuda we have extended loans to the employees of approximately 160 approved institutions.

In the seven months ended July 31, 2008, the Operating Subsidiaries extended loans to the employees of a total of 926 approved institutions, an increase of approximately 8.8% as compared to a total of 859 participating institutions in the year ended December 31, 2007, and almost 83% more than the 506 total number of participating institutions in the seven months ended July 31, 2007.

In the seven months ended July 31, 2008, 251 participating institutions, or 27.1% of the total, were located in St. Lucia and 243 participating institutions, or 26.2% of the total, were located in the Commonwealth of Dominica. In the same period, 19.1% of the participating institutions were located in St. Vincent and the Grenadines, 17.1% were located in Grenada and 10.5% were located in Antigua and Barbuda. In the year ended December 31, 2007, 33.9% of the participating institutions were located in St. Lucia, 32.1% were located in the Commonwealth of Dominica, 13.7% were located in Antigua and Barbuda, 12.1% were located in St. Vincent and the Grenadines, and 8.1% were located in Grenada.