Table of Contents

As filed with the Securities and Exchange Commission on December 24, 2008

Registration No. 333-154800

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1

to

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

HARRAH’S ENTERTAINMENT, INC.

(Exact name of registrant as specified in its charter)

| DELAWARE | 7993 | 62-1411755 | ||

(State or other jurisdiction of Incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

One Caesars Palace Drive

Las Vegas, NV 89109

(702) 407-6000

(Address, including zip code, and telephone number, including

area code, of Registrant’s Principal Executive Offices)

HARRAH’S OPERATING COMPANY, INC.

(Exact name of registrant as specified in its charter)

(See Schedule A for additional registrants)

| DELAWARE | 7993 | 75-1941623 | ||

(State or other jurisdiction of Incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

One Caesars Palace Drive

Las Vegas, NV 89109

(702) 407-6000

(Address, including zip code, and telephone number, including

area code, of Registrant’s principal executive offices)

Michael D. Cohen, Esq.

Vice President and Corporate Secretary

Harrah’s Entertainment, Inc.

One Caesars Palace Drive

Las Vegas, NV 89109

(702) 407-6000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With a copy to:

Monica K. Thurmond, Esq.

O’Melveny & Myers LLP

7 Times Square

New York, New York 10036

(212) 326-2000

Approximate date of commencement of proposed sale to public: As soon as practicable after this Registration Statement becomes effective.

If any securities being registered on this Form are to be offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

CALCULATION OF REGISTRATION FEE

Title of each Class of Securities to be Registered | Amount to be Registered | Proposed Maximum Per Note | Proposed Maximum Aggregate Offering Price(1) | Amount of Registration Fee(2) | |||||

10.75% Senior Notes due 2016 | $4,200,153,000 | 100% | $4,200,153,000 | $ | 165,066 | ||||

Guarantee of 10.75% Senior Notes due 2016(3) | — | — | — | (4) | |||||

10.75%/11.5% Senior Toggle Notes due 2018 | $1,052,583,000 | 100% | $1,052,583,000 | $ | 41,367 | ||||

Guarantee of 10.75% Senior Toggle Notes due 2018(3) | — | — | — | (4) | |||||

| (1) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(a) under the Securities Act of 1933, as amended (the “Securities Act”). The proposed maximum offering price is estimated solely for purpose of calculating the registration fee. |

| (2) | Calculated pursuant to Rule 457(f) of the rules and regulations of the Security Act. Paid by wire transfer on October 10, 2008. |

| (3) | Each of Harrah’s Operating Company, Inc.’s wholly-owned domestic subsidiaries jointly, severally and unconditionally guarantees, the 10.75% Senior Notes due 2016 and the 10.75% /11.5% Senior Toggle Notes due 2018 on a senior unsecured basis. |

| (4) | See Schedule A on the inside facing page for table of additional registrant guarantors. Pursuant to Rule 457(n) of the rules and regulations under the Securities Act, no separate fee for the guarantee is payable. |

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

SCHEDULE A

| Guarantor | State or Other Jurisdiction of Incorporation or Organization | Address of Registrants’ Principal Executive Offices | I.R.S. Identification | |||

Harrah’s Operating Company, Inc.(Issuer) | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 75-1941623 | |||

Harrah’s Entertainment, Inc.(Parent Guarantor) | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 62-1411755 | |||

California Clearing Corporation | California | One Caesars Palace Drive Las Vegas, NV 89109 | 92-2421291 | |||

Bally’s Midwest Casino, Inc. | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0404625 | |||

Bally’s Operator, Inc. | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 52-1919594 | |||

Caesars Palace Corporation | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0172791 | |||

Harrah’s International Holding Company, Inc. | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 26-1779042 | |||

Sheraton Tunica Corporation | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 04-3196700 | |||

AJP Holdings, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 75-3197770 | |||

AJP Parent, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 75-3197768 | |||

Biloxi Hammond, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 26-1241172 | |||

Biloxi Village Walk Development, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 38-3764302 | |||

Chester Facility Holding Company, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 51-0616907 | |||

Harrah’s Chester Downs Investment Company, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 76-0760472 | |||

Harrah’s Maryland Heights LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 43-1725857 | |||

Harrah’s MH Project, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 35-2276359 | |||

Harrah’s Operating Company Memphis, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 62-1802711 | |||

Harrah’s Shreveport/Bossier City Holding Company, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 71-0902683 | |||

Harrah’s Shreveport/Bossier City Investment Company, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 71-0902682 | |||

Harrah’s Sumner Investment Company, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 26-1527053 | |||

Harrah’s Sumner Management Company, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 26-1527133 | |||

Harrah’s West Warwick Gaming Company, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 47-0942639 | |||

Table of Contents

| Guarantor | State or Other Jurisdiction of Incorporation or Organization | Address of Registrants’ Principal Executive Offices | I.R.S. Identification | |||

Horseshoe Gaming Holding, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0425131 | |||

JCC Holding Company II, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 62-1650470 | |||

Koval Holdings Company, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 56-2599109 | |||

Reno Crossroads, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 22-3741494 | |||

Village Walk Construction, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 37-1549893 | |||

Winnick Parent, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 32-0136798 | |||

Winnick Holdings, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 42-1652004 | |||

Bally’s Olympia Limited Partnership | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 36-3938276 | |||

Caesars World, Inc. | Florida | One Caesars Palace Drive Las Vegas, NV 89109 | 59-0773674 | |||

Southern Illinois Riverboat/Casino Cruises, Inc. | Illinois | One Caesars Palace Drive Las Vegas, NV 89109 | 37-1272361 | |||

Casino Computer Programming, Inc. | Indiana | One Caesars Palace Drive Las Vegas, NV 89109 | 31-1721454 | |||

Roman Entertainment Corporation of Indiana | Indiana | One Caesars Palace Drive Las Vegas, NV 89109 | 95-4510681 | |||

Roman Holding Corporation of Indiana | Indiana | One Caesars Palace Drive Las Vegas, NV 89109 | 95-4510678 | |||

Caesars Riverboat Casino, LLC | Indiana | One Caesars Palace Drive Las Vegas, NV 89109 | 95-4510682 | |||

Horseshoe Hammond, LLC | Indiana | One Caesars Palace Drive Las Vegas, NV 89109 | 36-3865868 | |||

Players Bluegrass Downs, Inc. | Kentucky | One Caesars Palace Drive Las Vegas, NV 89109 | 61-1250331 | |||

Harrah’s Bossier City Investment Company, LLC | Louisiana | One Caesars Palace Drive Las Vegas, NV 89109 | 71-0902684 | |||

Horseshoe Shreveport, L.L.C. | Louisiana | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0442445 | |||

Jazz Casino Company, LLC | Louisiana | One Caesars Palace Drive Las Vegas, NV 89109 | 72-1429291 | |||

JCC Fulton Development, LLC | Louisiana | One Caesars Palace Drive Las Vegas, NV 89109 | 37-1527448 | |||

Players Riverboat II, LLC | Louisiana | One Caesars Palace Drive Las Vegas, NV 89109 | 72-1297055 | |||

Horseshoe Entertainment | Louisiana | One Caesars Palace Drive Las Vegas, NV 89109 | 72-1249477 | |||

Table of Contents

| Guarantor | State or Other Jurisdiction of Incorporation or Organization | Address of Registrants’ Principal Executive Offices | I.R.S. Identification | |||

BL Development Corp. | Minnesota | One Caesars Palace Drive Las Vegas, NV 89109 | 41-1754530 | |||

GCA Acquisition Subsidiary, Inc. | Minnesota | One Caesars Palace Drive Las Vegas, NV 89109 | 41-1815669 | |||

Grand Casinos, Inc. | Minnesota | One Caesars Palace Drive Las Vegas, NV 89109 | 41-1689535 | |||

Grand Media Buying, Inc. | Minnesota | One Caesars Palace Drive Las Vegas, NV 89109 | 41-1726209 | |||

Grand Casinos of Biloxi, LLC | Minnesota | One Caesars Palace Drive Las Vegas, NV 89109 | 41-1726211 | |||

Bally’s Tunica, Inc. | Mississippi | One Caesars Palace Drive Las Vegas, NV 89109 | 36-3887302 | |||

East Beach Development Corporation | Mississippi | One Caesars Palace Drive Las Vegas, NV 89109 | 30-0360590 | |||

Robinson Property Group Corp. | Mississippi | One Caesars Palace Drive Las Vegas, NV 89109 | 64-0840031 | |||

Grand Casinos of Mississippi, LLC - Gulfport | Mississippi | One Caesars Palace Drive Las Vegas, NV 89109 | 36-4262232 | |||

Harrah’s North Kansas City LLC | Missouri | One Caesars Palace Drive Las Vegas, NV 89109 | 62-1802713 | |||

B I Gaming Corporation | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0401326 | |||

Benco, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0409341 | |||

Caesars Entertainment Golf, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 52-2271238 | |||

Caesars Entertainment Akwesasne Consulting Corp. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 52-2307758 | |||

Caesars Entertainment Canada Holding, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0445777 | |||

Caesars Entertainment Finance Corp. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0410850 | |||

Caesars Entertainment Retail, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 90-0059931 | |||

Caesars Palace Realty Corp. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0109258 | |||

Caesars Palace Sports Promotions, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 93-0720413 | |||

Caesars United Kingdom, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 83-0421943 | |||

Caesars World Merchandising, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 94-2768968 | |||

CEI-Sullivan County Development Company | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 52-2338538 | |||

Table of Contents

| Guarantor | State or Other Jurisdiction of Incorporation or Organization | Address of Registrants’ Principal Executive Offices | I.R.S. Identification | |||

Consolidated Supplies, Services and Systems | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0424458 | |||

Desert Palace, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0097966 | |||

Dusty Corporation | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0398744 | |||

FHR Corporation | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0402426 | |||

Flamingo-Laughlin, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0240867 | |||

Harrah’s Alabama Corporation | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0308027 | |||

Harrah’s Arizona Corporation | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 62-1523519 | |||

Harrah’s Illinois Corporation | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0284653 | |||

Harrah’s Imperial Palace Corp. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 37-1518194 | |||

Harrah’s Interactive Investment Company | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0326036 | |||

Harrah’s Investments, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0317848 | |||

Harrah’s Kansas Casino Corporation | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0313173 | |||

Harrah’s Management Company | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0187173 | |||

Harrah’s Marketing Services Corporation | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 86-0889202 | |||

Harrah’s Maryland Heights Operating Company | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0343024 | |||

Harrah’s New Orleans Management Company | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 62-1534758 | |||

Harrah’s Pittsburgh Management Company | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0320269 | |||

Harrah’s Reno Holding Company, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 62-1440237 | |||

Harrah’s Southwest Michigan Casino Corporation | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0337476 | |||

Harrah’s Travel, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0400542 | |||

Harrah’s Tunica Corporation | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0292680 | |||

Harrah’s Vicksburg Corporation | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0292320 | |||

Table of Contents

| Guarantor | State or Other Jurisdiction of Incorporation or Organization | Address of Registrants’ Principal Executive Offices | I.R.S. Identification | |||

Harveys BR Management Company, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 91-2000710 | |||

Harveys C.C. Management Company, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0307948 | |||

Harveys Iowa Management Company, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0321071 | |||

HBR Realty Company, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 91-2000709 | |||

HCR Services Company, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0370327 | |||

HEI Holding Company One, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 37-1524630 | |||

HEI Holding Company Two, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 38-3737280 | |||

Las Vegas Resort Development, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 90-0123916 | |||

LVH Corporation | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0402427 | |||

Parball Corporation | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0410530 | |||

Players Development, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 22-3452913 | |||

Players Resources, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 22-3409555 | |||

Reno Projects, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0300954 | |||

Rio Development Company, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0220505 | |||

Tele/Info, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0188729 | |||

Trigger Real Estate Corporation | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0398745 | |||

190 Flamingo, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 38-3736606 | |||

Caesars India Sponsor Company, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 26-3478539 | |||

Corner Investment Company, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 37-1531785 | |||

DCH Exchange, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 61-1527745 | |||

Harrah’s Bossier City Management Company, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 71-0902685 | |||

Harrah’s Chester Downs Management Company, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 68-0590545 | |||

Table of Contents

| Guarantor | State or Other Jurisdiction of Incorporation or Organization | Address of Registrants’ Principal Executive Offices | I.R.S. Identification | |||

Harrah’s License Company, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 42-1643727 | |||

Harrah’s Shreveport Investment Company, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0292677 | |||

Harrah’s Shreveport Management Company, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 62-1839697 | |||

H-BAY, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 42-1640291 | |||

HCAL, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0313169 | |||

HHLV Management Company, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 87-0719578 | |||

Hole in the Wall, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 04-3813150 | |||

Horseshoe GP, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 94-3230241 | |||

Koval Investment Company, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 56-2599115 | |||

Las Vegas Golf Management, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 41-2171222 | |||

Nevada Marketing, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 30-0341987 | |||

Players Holding, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0346670 | |||

Players International, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 95-4175832 | |||

Players LC, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 22-3414663 | |||

Players Maryland Heights Nevada, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0345262 | |||

Players Riverboat Management, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0332373 | |||

Players Riverboat, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0332372 | |||

Roman Empire Development, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 35-2286976 | |||

TRB Flamingo, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 59-3797439 | |||

New Gaming Capital Partnership | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-6060088 | |||

Bally’s Park Place, Inc. | New Jersey | One Caesars Palace Drive Las Vegas, NV 89109 | 36-2931526 | |||

Boardwalk Regency Corporation | New Jersey | One Caesars Palace Drive Las Vegas, NV 89109 | 95-3147313 | |||

Table of Contents

| Guarantor | State or Other Jurisdiction of Incorporation or Organization | Address of Registrants’ Principal Executive Offices | I.R.S. Identification | |||

Caesars New Jersey, Inc. | New Jersey | One Caesars Palace Drive Las Vegas, NV 89109 | 22-2230292 | |||

Caesars World Marketing Corporation | New Jersey | One Caesars Palace Drive Las Vegas, NV 89109 | 22-2746389 | |||

GNOC, Corp. | New Jersey | One Caesars Palace Drive Las Vegas, NV 89109 | 22-2494608 | |||

Martial Development Corp. | New Jersey | One Caesars Palace Drive Las Vegas, NV 89109 | 22-3461012 | |||

Players Services, Inc. | New Jersey | One Caesars Palace Drive Las Vegas, NV 89109 | 22-3400988 | |||

Atlantic City Country Club 1, LLC | New Jersey | One Caesars Palace Drive Las Vegas, NV 89109 | 21-0600260 | |||

Harrah’s NC Casino Company, LLC | North Carolina | One Caesars Palace Drive Las Vegas, NV 89109 | 56-1936298 | |||

Harrah South Shore Corporation | California | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0074793 | |||

Showboat Atlantic City Mezz 1, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 26-1305647 | |||

Showboat Atlantic City Mezz 2, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 26-1305702 | |||

Showboat Atlantic City Mezz 3, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 26-1305739 | |||

Showboat Atlantic City Mezz 4, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 26-1305784 | |||

Showboat Atlantic City Mezz 5, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 26-1305816 | |||

Showboat Atlantic City Mezz 6, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 26-1305847 | |||

Showboat Atlantic City Mezz 7, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 26-1305886 | |||

Showboat Atlantic City Mezz 8, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 26-1305920 | |||

Showboat Atlantic City Mezz 9, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 26-1305951 | |||

Showboat Atlantic City Propco, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 26-1305988 | |||

Tahoe Garage Propco, LLC | Delaware | One Caesars Palace Drive Las Vegas, NV 89109 | 26-1777697 | |||

Harveys Tahoe Management Company, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 88-0370589 | |||

HTM Holding, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 26-2258855 | |||

Showboat Holding, Inc. | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 26-2397971 | |||

Table of Contents

| Guarantor | State or Other Jurisdiction of Incorporation or Organization | Address of Registrants’ Principal Executive Offices | I.R.S. Identification | |||

DCH Lender, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 26-2468212 | |||

Durante Holdings, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 42-168403 | |||

Caesars Entertainment Development, LLC | Nevada | One Caesars Palace Drive Las Vegas, NV 89109 | 83-0379289 | |||

Ocean Showboat, Inc. | New Jersey | One Caesars Palace Drive Las Vegas, NV 89109 | 22-2500790 | |||

Showboat Atlantic City Operating Company, LLC | New Jersey | One Caesars Palace Drive Las Vegas, NV 89109 | 26-1305623 | |||

Table of Contents

The information in this prospectus is not complete and may be changed. We may not complete the exchange offer and issue these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell securities and it is not soliciting an offer to buy these securities in any state where the offer is not permitted.

Subject to Completion, dated December 24, 2008

PRELIMINARY PROSPECTUS

Harrah’s Operating Company, Inc.

OFFERS TO EXCHANGE

$4,200,153,000 aggregate principal amount of its 10.75% Senior Notes due 2016 and

$1,052,583,000 aggregate principal amount of its 10.75%/11.5% Senior Toggle Notes due 2018, the issuance of each of which has been registered under the Securities Act of 1993, as amended (collectively, the “exchange notes”),

for

any and all of its outstanding 10.75% Senior Notes due 2016 and 10.75%/11.5% Senior Toggle Notes due 2018, respectively (collectively, the “original notes,” and together with the exchange notes, the “notes”).

Harrah’s Operating Company, Inc. hereby offers, upon the terms and subject to the conditions set forth in this prospectus and the accompanying letter of transmittal (which together constitute the “exchange offers”), to exchange up to $4,200,153,000 in aggregate principal amount of our registered 10.75% Senior Notes due 2016 and the guarantees thereof and $1,052,583,000 in the aggregate principal amount of our registered 10.75%/11.5% Senior Toggle Notes due 2018 and any guarantees thereof (the “exchange notes”), for a like principal amount of our unregistered 10.75% Senior Notes due 2016 and 10.75%/11.5% Senior Toggle Notes due 2018 (the “original notes”). We refer to the original notes and exchange notes collectively as the “notes.” The terms of the exchange notes and the guarantees thereof are identical to the terms of the original notes and the guarantees thereof in all material respects, except for the elimination of some transfer restrictions, registration rights and additional interest provisions relating to the original notes. The notes are irrevocably and unconditionally guaranteed by Harrah’s Entertainment, Inc. and the wholly-owned domestic subsidiaries of Harrah’s Operating Company, Inc. that guarantee obligations under the senior secured credit facilities (the “guarantors”). The notes will be exchanged in denominations of $2,000 and in integral multiples of $1,000.

We will exchange any and all original notes that are validly tendered and not validly withdrawn prior to 5:00 p.m., New York City time, on , 2009, unless extended.

We have not applied, and do not intend to apply, for listing of the notes on any national securities exchange or automated quotation system.

See “Risk Factors” beginning on page 23 of this prospectus for a discussion of certain risks that you should consider before participating in this exchange offers.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2009.

Table of Contents

Page | ||

| 1 | ||

| 23 | ||

| 36 | ||

| 37 | ||

| 38 | ||

| 49 | ||

| 50 | ||

Unaudited Pro Forma Condensed Consolidated Financial Information of Harrah’s Entertainment, Inc. | 52 | |

Unaudited Pro Forma Condensed Consolidated Financial Information of Harrah’s Operating Company, Inc. | 57 | |

| 63 | ||

Management’s Discussion and Analysis of Financial Condition And Results of Operations | 65 | |

| 115 | ||

| 120 | ||

| 129 | ||

| 138 | ||

Security Ownership of Certain Beneficial Owners and Management | 177 | |

| 178 | ||

| 181 | ||

| 186 | ||

| 252 | ||

| 253 | ||

| 254 | ||

| 254 | ||

| 254 | ||

| F-1 |

We have not authorized anyone to give you any information or to make any representations about us or the transactions we discuss in this prospectus other than those contained in this prospectus. If you are given any information or representations about these matters that is not discussed in this prospectus, you must not rely on that information. This prospectus is not an offer to sell or a solicitation of an offer to buy securities anywhere or to anyone where or to whom we are not permitted to offer or sell securities under applicable law. The delivery of this prospectus does not, under any circumstances, mean that there has not been a change in our affairs since the date of this prospectus. Subject to our obligation to amend or supplement this prospectus as required by law and the rules of the Securities and Exchange Commission, or the SEC, the information contained in this prospectus is correct only as of the date of this prospectus, regardless of the time of delivery of this prospectus or any sale of these securities.

The notes may not be offered or sold in or into the United Kingdom by means of any document except in circumstances that do not constitute an offer to the public within the meaning of the Public Offers of Securities Regulations 1995. All applicable provisions of the Financial Services and Markets Act 2000 must be complied with in respect of anything done in relation to the notes in, from or otherwise involving or having an effect in the United Kingdom.

The notes have not been and will not be qualified under the securities laws of any province or territory of Canada. The notes are not being offered or sold, directly or indirectly, in Canada or to or for the account of any resident of Canada in contravention of the securities laws of any province or territory thereof.

Until , 2009 (90 days after the date of this prospectus), all dealers effecting transactions in the exchange notes, whether or not participating in the exchange offers, may be required to deliver a prospectus.

i

Table of Contents

This summary highlights information appearing elsewhere in this prospectus. This summary is not complete and does not contain all of the information that you should consider before investing in the notes. You should carefully read the entire prospectus, including the information presented under the heading “Risk Factors” and the more detailed information in the unaudited pro forma condensed consolidated financial information and the historical financial statements and related notes presented elsewhere in this prospectus.

The exchange notes will be issued by Harrah’s Operating Company, Inc. (the “Issuer”), a Delaware corporation and a wholly-owned subsidiary of Harrah’s Entertainment, Inc., a Delaware corporation (“Harrah’s Entertainment”). Unless otherwise indicated or the context otherwise requires, references in this prospectus to “we,” “our,” “us,” and “the company” refer to Harrah’s Entertainment and its consolidated subsidiaries, and references in this prospectus to “Harrah’s Operating” or “HOC” refer to the Issuer and its consolidated subsidiaries, in each case after giving effect to the consummation of the Transactions described below under “—The Transactions.”

As of September 30, 2008, Harrah’s Entertainment owned or managed 52 casinos through its subsidiaries. In connection with the financing of the Acquisition described below under “—The Transactions,” six casinos were spun or transferred out of Harrah’s Operating to entities that are side-by-side with Harrah’s Operating. See “—The Transactions—CMBS Transactions.” In addition, in connection with the Transactions, London Clubs and its subsidiaries became subsidiaries of Harrah’s Operating. See “The Transactions—London Clubs Transfer.” Harrah’s Operating has remained a direct, wholly-owned subsidiary of Harrah’s Entertainment and as of September 30, 2008 owned or managed 46 of the 52 Harrah’s Entertainment casinos. Notwithstanding these spin-offs and transfers, management of Harrah’s Entertainment continues to manage all of the properties of Harrah’s Operating and those held by its sister subsidiaries as one company, but Harrah’s Operating is not entitled to receive any direct contribution or proceeds from its sister subsidiaries’ operations. Harrah’s Entertainment guarantees the notes; the CMBS subsidiaries do not. As a result, we have provided the historical financial and pro forma financial information of Harrah’s Entertainment as well as pro forma financial information of Harrah’s Operating to give a meaningful and complete presentation of the CMBS Transactions and the London Clubs Transfer, among others.

Unless otherwise specified, all pro forma financial information for periods ended after December 31, 2006 provided in this prospectus gives pro forma effect to the closing of the Transactions. Harrah’s Operating has not historically reported financial information on a stand-alone basis and has not prepared audited historical financial statements for this offering. Accordingly, the financial information presented herein for Harrah’s Operating has been prepared on an unaudited pro forma basis. The pro forma financial information has been derived from the Harrah’s Entertainment financial statements for the relevant periods, as adjusted to remove the historical financial information of all subsidiaries of and account balances at Harrah’s Entertainment that were not components of Harrah’s Operating.

1

Table of Contents

Our Company

Harrah’s Entertainment is the world’s largest and most geographically diversified gaming company with the #1 or #2 market share, based on revenue, in almost every major gaming market in the U.S., including Las Vegas and Atlantic City, the largest gaming markets in the U.S. As of September 30, 2008, we owned or managed 52 casinos across 12 U.S. states and six countries under the Harrah’s®, Caesars®, and Horseshoe® brand names, among others. Harrah’s Operating owned or managed 46 of these casinos. Harrah’s Entertainment operates the industry’s largest and most widely recognized customer recognition and loyalty program, called Total Rewards®, which has over 40 million members worldwide. In addition, we own and operate the World Series of Poker®.

Our History

Harrah’s Entertainment commenced its casino operations in 1937 and became a publicly listed company in 1971. Two years later, it became the first gaming company to be listed on the New York Stock Exchange (“NYSE”). In 1980, Harrah’s Entertainment was acquired by Holiday Inns, Inc. and was delisted from the NYSE. In 1995, Harrah’s Entertainment became a stand-alone company and resumed trading on the NYSE.

Harrah’s Entertainment has grown through a series of strategic acquisitions that have strengthened its scale, geographic diversity and leading market positions. In 1998, it completed its acquisition of Showboat, Inc. and in 1999, it purchased Rio Hotel & Casino, Inc. In 2000, it completed the purchase of Players International. During the next five years, Harrah’s Entertainment acquired Harveys Casino Resorts (2001), Horseshoe Gaming Holding Corp. (2004), the rights to the World Series of Poker (2004) and the Imperial Palace Hotel & Casino in Las Vegas (2005). Harrah’s Entertainment also acquired Caesars Entertainment, Inc. in 2005, which, at $9.3 billion, was the largest merger in the history of the gaming industry and secured Harrah’s Entertainment’s position as the world’s largest casino company. Additionally, Harrah’s Entertainment has expanded internationally, completing the acquisitions of London Clubs International plc (“London Clubs”) in 2006 and Macau Orient Golf in 2007.

In order to generate same store gaming revenue growth (defined as annual gaming revenue growth for properties held by Harrah’s Entertainment throughout the year) and cross-market play (defined as play by a guest in a property outside the home market of their primary gaming property) among its casinos, in 1997, Harrah’s Entertainment launched the Total Rewards program, which allows customers to earn benefits by playing at most Harrah’s Entertainment casinos, as well as WINet® (Winner’s Information Network), the industry’s first sophisticated nationwide customer database. Total Rewards was the first technology-based customer relationship management strategy implemented in the gaming industry and has been an effective tool used by management to enhance overall operating results.

Our Competitive Strengths

Industry’s largest and most geographically diversified gaming operator with leading market positions. Harrah’s Entertainment is the world’s largest and most geographically diversified gaming company, owning or managing 52 Harrah’s Entertainment properties in 12 U.S. states and six countries as of September 30, 2008. In addition, Harrah’s Entertainment’s properties operate as market leaders, having the #1 or #2 market share, based on revenue, in almost every major U.S. gaming market, including Las Vegas and Atlantic City, the largest gaming markets in the U.S. We use our scale and market leading position, in combination with our proprietary marketing technology and customer loyalty programs, to foster revenue growth and encourage repeat business. In addition, our scale and geographic diversity reduces our exposure to any single region, thereby providing income diversification and improving our risk profile.

2

Table of Contents

Superior business model based on nationwide customer database and loyalty program. Our strategy is to generate same store gaming revenue growth and growth in cross-market play through our superior marketing and technological capabilities in combination with our nationwide casino network. These capabilities have allowed us to generate financial results that have consistently outperformed our competitors in the markets in which we operate. The systems that we use to generate our same store gaming revenue growth and cross-market play are Total Rewards, which allows our customers to earn benefits by playing at most Harrah’s Entertainment casinos, and WINet, the industry’s first sophisticated nationwide customer database. We believe these marketing tools, coupled with the industry’s deepest geographic reach, provide us with a significant competitive advantage that enables us to efficiently market our products to a large and recurring customer base, and generate profitable revenue growth.

Our asset value has benefited from substantial historical investments. From January 1, 2005 through September 30, 2008, we have invested $6.3 billion in our asset base, $4.6 billion of which was invested in Harrah’s Operating assets. In addition, we are currently in the midst of several investments that have recently opened or are scheduled to open over the coming years, including the Horseshoe Hammond expansion in Indiana (opened in August 2008) and the renovation and expansion of Caesars Palace Las Vegas (scheduled to open in 2009). We believe these investments, in conjunction with our substantial historical investments, will enhance our credit profile and bolster future growth in EBITDA that we will recognize over time. Further underpinning our asset value, the majority of our properties operate on owned real estate, and many have excess land available for expansion.

Portfolio of the most highly recognized brand names in the gaming industry. Subsidiaries of Harrah’s Entertainment own or manage many of the most highly recognized brand names in the gaming industry, including Harrah’s®, Caesars®, Horseshoe®, Total Rewards®, the World Series of Poker®, Rio®, Paris®, Bally’s®, Flamingo®, Harveys®, Showboat® and Grand CasinoSM. Each of these brands has a strong identity and enjoys widespread customer recognition. This diverse collection of brands allows us to appeal to a wide range of customer preferences and capture multiple visits through our ability to offer differentiated gaming experiences. In casino brand awareness studies, several of our brands consistently achieve higher rates of recognition overall, as compared to our competitors.

Experienced management team with proven track record. Our management team, led by CEO Gary Loveman, has built Harrah’s Entertainment into an industry leader by geographically diversifying our operations and introducing technology-based decision science tools to loyalty programs. A former associate professor at the Harvard University Graduate School of Business Administration, Mr. Loveman joined us as Chief Operating Officer in 1998 and drew on his extensive background in retail marketing and service-management to develop Total Rewards. Mr. Loveman was promoted to CEO in January 2003 and was named “Best CEO” in the gaming & lodging industry by Institutional Investor magazine for 2003, 2004, 2005 and 2006. In addition, the other members of our senior management team possess significant gaming industry experience.

Our Business Strategy

Leverage our unique scale and proprietary loyalty programs to generate same store gaming revenue growth and cross-market play growth. We plan to continue to aggressively leverage our nationwide distribution platform and superior marketing and technological capabilities to generate same store gaming revenue growth and growth in cross-market play. Through the Total Rewards and WINet systems, we are able to effectively monitor the play of over 40 million program participants and target our efforts and marketing expenditures on their highest return uses as well as promote cross-market play. We believe that given the scale and geographic reach of Harrah’s Entertainment, we are uniquely positioned amongst our competitors to execute this strategy.

3

Table of Contents

Capitalize on strong growth trends in our industry. We have been successful in making investments that have generated incremental growth in our business and enabled us to post results that are superior to those of our competitors in the markets where we operate. These investments have historically been designed to improve the customer experience at existing properties, expand our capacity, or build new properties. We are currently pursuing select capital projects in proven markets that we believe will be accretive to our growth strategy and will generate attractive cash flow and returns on investment. For example, we are currently developing a new hotel tower at our iconic Caesars Palace in Las Vegas and recently unveiled a new vessel in Hammond, Indiana, which is expected to significantly increase our revenue-generating capacity in each of those markets. Additionally, we believe that we have opportunities to expand revenues and cash flow while further geographically diversifying our assets by pursuing selected international growth opportunities.

Enhance operational efficiency. We have identified significant opportunities to streamline our operations, improve our cost structure and optimize working capital. Our management team implemented a comprehensive profitability improvement program in September 2006 that identified three primary initiatives: organizational restructuring, a transformation of our teleservices (i.e., call centers) strategy, and procurement savings. In accordance with the shared services agreement, which is described under “Certain Relationships and Related Party Transactions—Shared Services Agreement,” 70% of these savings have been allocated to Harrah’s Operating.

Maximize free cash flow. Our combination of stable and predictable revenues, high operating margins, and well managed maintenance capital expenditures allow us to generate significant cash flow. We intend to maintain rigorous control over capital investment projects, and future growth capital will be spent only upon the expectation of attractive returns. We believe that our predictable maintenance capital expenditures, improved working capital management and cost savings initiatives should enhance our ability to generate free cash flow.

4

Table of Contents

The Transactions

The Acquisition

On December 19, 2006, Harrah’s Entertainment entered into a definitive merger agreement with Hamlet Holdings LLC, a Delaware limited liability company (“Hamlet Holdings”), and Hamlet Merger Inc., a Delaware corporation and a wholly-owned subsidiary of Hamlet Holdings (“Merger Sub”). Hamlet Holdings and Merger Sub were formed and are controlled by affiliates of Apollo Global Management, LLC (“Apollo”) and TPG Capital, LP (“TPG” and, together with Apollo, the “Sponsors”). Pursuant to the merger agreement, on January 28, 2008, Merger Sub merged with and into Harrah’s Entertainment, and each share of Harrah’s Entertainment common stock issued and outstanding immediately prior to the effective time of the merger, was converted into the right to receive $90.00 in cash, which, when taken together with the net settlement of outstanding options, stock appreciation rights, restricted stock and restricted stock units, represents merger consideration of $17,241 million in the aggregate. We refer to the merger and payment of merger consideration as the “Acquisition.”

Upon completion of the Acquisition, Hamlet Holdings, funds affiliated with and controlled by the Sponsors, certain co-investors and certain members of management became the owners of all of the outstanding equity interests of Harrah’s Entertainment. Hamlet Holdings, the members of which are comprised of an equal number of individuals affiliated with each of the Sponsors, holds all of the voting common stock of Harrah’s Entertainment. The voting common stock does not have any economic rights. Funds affiliated with and controlled by the Sponsors, their co-investors and members of management each hold non-voting common stock and non-voting preferred stock. For more information regarding the equity ownership of Harrah’s Entertainment upon the closing of the Acquisition, see “—Corporate Structure” and “Security Ownership of Certain Beneficial Owners and Management.”

CMBS Transactions

In connection with the CMBS portion of the financing for the Acquisition described in more detail below under “—The Financing,” Harrah’s Operating spun off to Harrah’s Entertainment the following casino properties and related operating assets of those casinos (collectively, the “CMBS Closing Assets”) at or prior to the closing of the Acquisition: Harrah’s Las Vegas, Rio and Flamingo Las Vegas in Las Vegas, Nevada; Harrah’s Atlantic City and Showboat Atlantic City in Atlantic City, New Jersey; and Harrah’s Lake Tahoe, Harveys Lake Tahoe and Bill’s Lake Tahoe in Lake Tahoe, Nevada. All of the CMBS Closing Assets were spun out of Harrah’s Operating and its subsidiaries through a series of distributions, liquidations, transfers and contributions. We refer to the spin-off of the CMBS Closing Assets by Harrah’s Operating, resulting in the ownership of those assets by Harrah’s Entertainment through subsidiaries of Harrah’s Entertainment that are not also subsidiaries of Harrah’s Operating, as the “CMBS Spin-Off.”

Subsequent to the closing of the Acquisition and the CMBS Spin-Off, Paris Las Vegas and Harrah’s Laughlin and their related operating assets were spun out of Harrah’s Operating and its subsidiaries, and Harrah’s Lake Tahoe, Harveys Lake Tahoe, Bill’s Lake Tahoe and Showboat Atlantic City and their related operating assets were transferred to subsidiaries of Harrah’s Operating from Harrah’s Entertainment. We refer to the spin-off of Paris Las Vegas and Harrah’s Laughlin by Harrah’s Operating and the transfer to subsidiaries of Harrah’s Operating of Harrah’s Lake Tahoe, Harveys Lake Tahoe, Bill’s Lake Tahoe and Showboat Atlantic City as the “Post-Closing CMBS Transaction,” and we refer to the following casino properties and related operating assets of those casinos as the “CMBS Assets”: Harrah’s Las Vegas, Rio, Paris Las Vegas and Flamingo Las Vegas in Las Vegas, Nevada; Harrah’s Atlantic City in Atlantic City, New Jersey and Harrah’s Laughlin in Laughlin, Nevada. The Post-Closing CMBS Transaction occurred in May 2008.

5

Table of Contents

As illustrated below under “—Corporate Structure,” the holders of the CMBS Assets (the “CMBS Borrowers”), are side-by-side with Harrah’s Operating under Harrah’s Entertainment. Pursuant to a shared services agreement, Harrah’s Operating provides the CMBS Borrowers with certain corporate management and administrative operations and costs are allocated by Harrah’s Operating for providing such services. These operations include, but are not limited to, payroll, marketing, accounting and legal. The agreement also memorializes certain short-term cash management arrangements and other operating efficiencies that reflect the way in which Harrah’s Entertainment has historically operated its business. See “Certain Relationships and Related Party Transactions—Shared Services Agreement.” We refer to the CMBS Spin-Off together with the subsequent Post-Closing CMBS Transaction as the “CMBS Transactions.”

London Clubs Transfer

In December 2006, we acquired London Clubs, which owns and/or manages casinos in the United Kingdom, Egypt and South Africa. When acquired, London Clubs and its subsidiaries became wholly-owned subsidiaries of Harrah’s Entertainment and not subsidiaries of Harrah’s Operating. In connection with the CMBS Transactions and the financing described below under “—The Financing,” London Clubs and its subsidiaries, with the exception of those related to the London Clubs’ South African operations, became subsidiaries of Harrah’s Operating on or before the closing of the Acquisition. During the second quarter of 2008, Harrah’s Entertainment transferred to Harrah’s Operating the London Clubs’ South African operations, as well. We refer to the transfer of the London Clubs operations to Harrah’s Operating as the “London Clubs Transfer.”

The Financing

On January 28, 2008, the Acquisition was financed with the following:

| • | a cash equity investment by the Sponsors, their co-investors and certain members of management in Harrah’s Entertainment of approximately $6,079 million; |

| • | the proceeds from the incurrence by Harrah’s Operating of $5,275 million of senior unsecured cash pay interim loans; |

| • | the proceeds from the incurrence by Harrah’s Operating of $1,500 million of senior unsecured PIK toggle interim loans; |

| • | borrowings of $7,250 million by Harrah’s Operating under the term loan portion of our new $9,250 million senior secured credit facilities, which also includes a $2,000 million revolving credit facility none of which was drawn at closing, but was subject to $188 million in outstanding letters of credit; and |

| • | $6,500 million of mortgage loans and related mezzanine financing under a real estate facility (the “CMBS Financing”) entered into by the CMBS Borrowers (with a payment guarantee by Harrah’s Entertainment of the operating leases thereunder) and secured initially by the CMBS Closing Assets and, after the Post-Closing CMBS Transaction, the CMBS Assets. |

Harrah’s Operating used the proceeds of the notes which were issued on February 1, 2008 to reduce its interim loan borrowings described above on a dollar-for-dollar basis. Harrah’s Operating currently has $343 million of unsecured cash pay loans outstanding and $97 million of senior unsecured PIK toggle loans outstanding.

Harrah’s Operating used a portion of the proceeds of the senior secured credit facilities described above to repay all outstanding borrowings under its existing credit facilities, which, as of January 28, 2008, amounted to approximately $5,796 million.

Harrah’s Operating also used a portion of the proceeds described above (including the senior secured credit facilities) to repurchase $131 million of its 7.5% Senior Notes due 2009, $394 million of its 8.875% Senior

6

Table of Contents

Subordinated Notes due 2008, $424 million of its 7.5% Senior Notes due 2009, $299 million of its 7% Senior Notes due 2013, all $250 million of its Senior Floating Rate Notes due 2008 and $375 million of its Floating Rate Contingent Convertible Senior Notes due 2024 (collectively, the “Retired Notes”) pursuant to tender offers and consent solicitations (collectively, the “Tender Offer”) completed on the same day as the Acquisition, as well as a discharge of all Senior Floating Rate Notes that were not tendered in the Tender Offer. We refer to the Tender Offer, the discharge, the repayment of senior unsecured interim loans with the proceeds of the notes which were issued on February 1, 2008 and the other financing transactions described above as the “Financing.”

New Hedging Arrangements

Harrah’s Operating entered into three new hedging arrangements with respect to LIBOR borrowings under the senior secured credit facilities, all of which fix the floating rate of interest thereunder to a fixed rate.

Throughout this prospectus, we collectively refer to the Acquisition, the CMBS Transactions, the London Clubs Transfer, the Financing and the new hedging arrangements as the “Transactions.”

Recent Events

In August 2008, construction was completed on the renovation and expansion of Horseshoe Hammond, property in the Illinois/Indiana region, which includes a two-level entertainment vessel including a 108,000-square-foot casino.

Construction has been completed on an upgrade and expansion of Harrah’s Atlantic City, which includes a new hotel tower with approximately 960 rooms, a casino expansion and a retail and entertainment complex. Portions of the new hotel tower opened in the first six months of 2008, and the remaining phase opened in July 2008.

On July 2, 2008, Harrah’s Operating made the permitted election under the (i) Indenture governing its 10.75%/11.5% Senior Toggle Notes due 2018 and (ii) Senior Unsecured Interim Loan Agreement dated January 28, 2008, to pay all interest due on February 1, 2009 for the notes and February 2, 2009 for the loan in kind. Harrah’s Operating intends to use the cash savings generated by this election for general corporate purposes. Harrah’s Operating is evaluating opportunities to retire other of its debt instruments in order to take advantage of current debt market conditions and thereby extend the weighted average maturity of its capital structure.

On December 24, 2008, Harrah’s Operating completed private exchange offers (the “Private Exchange Offers”) to exchange for its outstanding (i) 5.50% Senior Notes due 2010, (ii) 7.875% Senior Subordinated Notes due 2010, (iii) 8.0% Senior Notes due 2011, (iv) 8.125% Senior Subordinated Notes due 2011, (v) 5.375% Senior Notes due 2013, (vi) 5.625% Senior Notes due 2015, (vii) 6.50% Senior Notes due 2016, (viii) 5.75% Senior Notes due 2017; (ix) 10.75%/11.5% Senior Toggle Notes due 2018 and (x) 10.75% Senior Notes due 2016 (collectively, the “Old Notes”) up to $2.1 billion aggregate principal amount of (i) new 10.00% Second-Priority Senior Secured Notes due 2015 (the “2015 Second Lien Notes”), for Old Notes maturing between 2010 and 2013, and (ii) new 10.00% Second-Priority Senior Secured Notes due 2018 (the “2018 Second Lien Notes”), for Old Notes maturing between 2015 and 2018. Under the terms of the Private Exchange Offers, holders of Old Notes maturing in 2010 and 2011 could elect to receive cash in lieu of the 2015 Second Lien Notes for the Old Notes they tendered. Harrah’s Operating paid approximately $289 million to the holders that elected to receive cash in lieu of the 2015 Second Lien Notes that they would have otherwise received in exchange for their Old Notes maturing in 2010 and 2011.

The 2015 Second Lien Notes and 2018 Second Lien Notes are guaranteed by Harrah’s Entertainment and are secured on a second-priority basis by substantially all of the assets of Harrah’s Operating and the assets of its

7

Table of Contents

subsidiary pledgors that have pledged their assets to secure Harrah’s Operating’s obligations under the senior secured credit facilities. The purpose of the Private Exchange Offers was to reduce the outstanding principal amount of indebtedness of Harrah’s Operating and to extend the weighted average maturity of Harrah’s Operating’s outstanding indebtedness.

On December 24, 2008 Harrah’s Operating exchanged approximately $203 million of 2015 Second Lien Notes, $848 million of 2018 Second Lien Notes and $289 million in cash for the following Old Notes: (i) $371 million in aggregate principal amount at maturity of the 5.50% Senior Notes due 2010; (ii) $64 million in aggregate principal amount at maturity of the 7.875% Senior Subordinated Notes due 2010; (iii) $20 million in aggregate principal amount at maturity of the 8.0% Senior Notes due 2011; (iv) $91 million in aggregate principal amount at maturity of the 8.125% Senior Subordinated Notes due 2011; (v) $221 million in aggregate principal amount at maturity of the 5.375% Senior Notes due 2013; (vi) $136 million in aggregate principal amount at maturity of the 5.625% Senior Notes due 2015; (vii) $99 million in aggregate principal amount at maturity of the 6.50% Senior Notes due 2016; (viii) $140 million in aggregate principal amount at maturity of the 5.75% Senior Notes due 2017; (ix) $350 million in aggregate principal amount at maturity of the 10.75%/11.5% Senior Toggle Notes due 2018; (x) $732 million in aggregate principal amount at maturity of the 10.75% Senior Notes due 2016. In addition, Harrah’s Operating issued an aggregate of $12 million principal amount of 2015 Second Lien Notes to the dealer managers and to its financial advisor as compensation for their services in connection with the Private Exchange Offers.

8

Table of Contents

The Sponsors

Apollo

Apollo was founded in 1990 and is among the most active and successful private investment firms in the United States in terms of both number of investment transactions completed and aggregate dollars invested. With current assets under management of $45 billion as of June 30, 2008, Apollo’s private equity business has invested approximately $23 billion of equity capital, from inception through June 30, 2008, in a wide variety of industries, both domestically and internationally. Companies owned or controlled by Apollo and affiliates or in which Apollo and affiliates have a significant equity investment include, among others, NCL Corporation, Oceania Cruises, AMC Entertainment, Inc., Hexion Specialty Chemicals, Inc., Rexnord Industries LLC and Berry Plastics Group, Inc.

TPG

TPG is a private investment partnership that was founded in 1992 and currently has more than $55 billion of assets under management. Headquartered in Fort Worth, with offices in San Francisco, London, Hong Kong, New York, Melbourne, Menlo Park, Moscow, Mumbai, Shanghai, Singapore and Tokyo, TPG has extensive experience with global public and private investments executed through leveraged buyouts, recapitalizations, spinouts, joint ventures and restructurings. TPG seeks to invest in world-class franchises across a range of industries. Prior investments include Alltel, Avaya, Burger King, Continental, Hotwire, J Crew, MGM, Neiman Marcus, Petco, Sabre, Seagate, Texas Genco, TXU and Univision.

9

Table of Contents

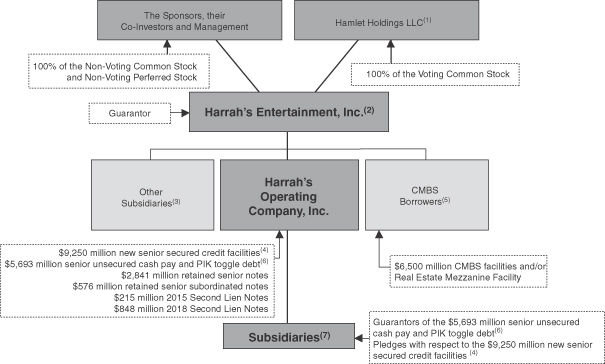

Corporate Structure

| (1) | The members of Hamlet Holdings are Leon Black, Joshua Harris and Marc Rowan, each of whom is affiliated with Apollo, and David Bonderman, James Coulter and Jonathan Coslet, each of whom is affiliated with TPG. Each member holds approximately 17% of the limited liability company interests of Hamlet Holdings. |

| (2) | Harrah’s Entertainment currently guarantees all of the Retained Notes of Harrah’s Operating and the senior secured credit facilities and the senior unsecured interim loans, each of which are described under “Description of Other Indebtedness.” It also guarantees the notes. In addition, it has provided a payment guarantee of any operating leases under the CMBS Facilities. The guarantee of Harrah’s Entertainment of the obligations under the notes is structurally subordinated to any guarantee of the operating leases under the CMBS Facilities. |

| (3) | Includes captive insurance subsidiaries. |

| (4) | Concurrently with the Acquisition, we entered into the senior secured credit facilities, which includes a $2,000 million revolving credit facility, of which $250 million was drawn at September 30, 2008. There were approximately $196 million in letters of credit outstanding under this facility at September 30, 2008. See “Description of Other Indebtedness—Senior Secured Credit Facilities.” |

| (5) | The CMBS Borrowers and their respective subsidiaries do not guarantee the notes, the senior unsecured cash pay interim loans, the senior unsecured PIK toggle interim loans, the senior secured credit facilities or any other indebtedness of Harrah’s Operating and are not directly liable for any obligations thereunder. |

| (6) | Includes the notes, as well as $343 million of senior unsecured cash pay interim loans and $97 million of senior unsecured PIK toggle interim loans that remain outstanding. |

| (7) | Each of the wholly owned domestic subsidiaries of Harrah’s Operating that pledged its assets to secure the senior secured credit facilities guarantees the notes, the senior unsecured cash pay interim loans and the senior unsecured PIK toggle interim loans. Non-U.S. subsidiaries of Harrah’s Operating do not guarantee the notes. In addition, subsidiaries that are not directly or indirectly wholly owned by Harrah’s Operating that do not, or that are not otherwise required to, secure the senior secured credit facilities do not guarantee the notes. See note 17 to our audited consolidated financial statements and note 15 to our unaudited consolidated financial statements for financial information regarding our non-guarantor subsidiaries. |

10

Table of Contents

Summary of the Terms of the Exchange Offers

In connection with the closing of the Acquisition, Harrah’s Operating entered into a registration rights agreement with the initial purchasers of the original notes. Under that agreement, Harrah’s Operating agreed to deliver to you this prospectus and to consummate the exchange offers.

Original Notes

Original Cash Pay Notes | $4,200,153,000 aggregate principal amount of 10.75% Senior Notes due 2016 and the guarantees thereof; and |

Original Toggle Notes | $1,052,583,000 aggregate principal amount of 10.75%/11.5% Senior Toggle Notes due 2018 and the guarantees thereof. |

Notes Offered

Exchange Cash Pay Notes | 10.75% Senior Notes due 2016. The terms of the “exchange cash pay notes” are substantially identical to those terms of the “original cash pay notes,” except that the transfer restrictions, registration rights and provisions for additional interest relating to the original notes do not apply to the exchange notes. We refer to the exchange cash pay notes and the original cash pay notes collectively as the “cash pay notes.” |

Exchange Toggle Notes | 10.75%/11.5% Senior Toggle Notes due 2018. The terms of the “exchange toggle notes” are substantially identical to those terms of the “original toggle notes,” except that the transfer restrictions, registration rights and provisions for additional interest relating to the original notes do not apply to the exchange notes. We refer to the exchange toggle notes and the original toggle notes collectively as the “senior toggle notes.” We refer to the exchange cash pay notes and the exchange toggle notes as the “exchange notes.” |

Exchange Offers | The Issuer is offering to exchange: |

| • | up to $4,200,153,000 aggregate principal amount of its exchange cash pay notes that have been registered under the Securities Act, for an equal amount of its original cash pay notes; and |

| • | up to $1,052,583,000 aggregate principal amount of its exchange toggle notes that have been registered under the Securities Act, for an equal amount of its original toggle notes. |

The Issuer is also offering to satisfy certain of its obligations under the registration rights agreement that the Issuer entered into when it issued the original notes in transactions exempt from registration under the Securities Act.

Expiration Date; Withdrawal of Tenders | The exchange offers will expire at 5:00 p.m., New York City time, on , 2009, or such later date and time to which the Issuer extends it. The Issuer does not currently intend to extend the expiration date. A tender of original notes pursuant to the exchange |

11

Table of Contents

offers may be withdrawn at any time prior to the expiration date. Any original notes not accepted for exchange for any reason will be returned without expense to the tendering holder promptly after the expiration or termination of the exchange offers. |

Conditions to the Exchange Offers | The exchange offers are subject to customary conditions, some of which the Issuer may waive. For more information, see “The Exchange Offers—Certain Conditions to the Exchange Offers.” |

Procedures for Tendering Old Notes | If you wish to accept the exchange offers, you must complete, sign and date the accompanying letter of transmittal, or a copy of the letter of transmittal, according to the instructions contained in this prospectus and the letter of transmittal. You must also mail or otherwise deliver the letter of transmittal, or the copy, together with the original notes and any other required documents, to the exchange agent at the address set forth on the cover of the letter of transmittal. If you hold original notes through The Depository Trust Company (“DTC”) and wish to participate in the exchange offers, you must comply with the Automated Tender Offer Program procedures of DTC, by which you will agree to be bound by the letter of transmittal. |

By signing or agreeing to be bound by the letter of transmittal, you will represent to us that, among other things:

| • | any exchange notes that you receive will be acquired in the ordinary course of your business; |

| • | you have no arrangement or understanding with any person or entity, including any of our affiliates, to participate in the distribution of the exchange notes; |

| • | if you are a broker-dealer that will receive exchange notes for your own account in exchange for original notes that were acquired as a result of market-making activities, that you will deliver a prospectus, as required by law, in connection with any resale of the exchange notes; and |

| • | you are not our “affiliate” as defined in Rule 405 under the Securities Act, or, if you are an affiliate, you will comply with any applicable registration and prospectus delivery requirements of the Securities Act. |

Guaranteed Delivery Procedures | If you wish to tender your original notes and your original notes are not immediately available or you cannot deliver your original notes, the letter of transmittal or any other documents required by the letter of transmittal or comply with the applicable procedures under DTC’s Automated Tender Offer Program prior to the expiration date, you must tender your original notes according to the guaranteed delivery procedures set forth in this prospectus under “The Exchange Offers—Guaranteed Delivery Procedures.” |

Effect on Holders of Original Notes | As a result of the making of, and upon acceptance for exchange of all validly tendered original notes pursuant to the terms of, the exchange |

12

Table of Contents

offers, the Issuer will have fulfilled a covenant contained in the registration rights agreement for the original notes and, accordingly, the Issuer will not be obligated to pay additional interest as described in the registration rights agreement. If you are a holder of original notes and do not tender your original notes in the exchange offers, you will continue to hold such original notes and you will be entitled to all the rights and limitations applicable to the original notes in the indenture, except for any rights under the registration rights agreement that, by their terms, terminate upon the consummation of the exchange offers. |

Consequences of Failure to Exchange | All untendered original notes will continue to be subject to the restrictions on transfer provided for in the original notes and in the indenture. In general, the original notes may not be offered or sold unless registered under the Securities Act, except pursuant to an exemption from, or in a transaction not subject to, the Securities Act and applicable state securities laws. Other than in connection with the exchange offers, the Issuer does not currently anticipate that it will register the original notes under the Securities Act. |

Resale of the Exchange Notes | Based on an interpretation by the staff of the SEC set forth in no-action letters issued to third parties, we believe that the exchange notes issued pursuant to the exchange offers in exchange for original notes may be offered for resale, resold and otherwise transferred by you (unless you are the our “affiliate” within the meaning of Rule 405 under the Securities Act) without compliance with the registration and prospectus delivery provisions of the Securities Act, provided that you: |

| • | are acquiring the exchange notes in the ordinary course of business; and |

| • | have not engaged in, do not intend to engage in, and have no arrangement or understanding with any person or entity, including any of the Issuer’s affiliates, to participate in, a distribution of the exchange notes. |

In addition, each participating broker-dealer that receives exchange notes for its own account pursuant to the exchange offers in exchange for original notes that were acquired as a result of market-making or other trading activity must also acknowledge that it will deliver a prospectus in connection with any resale of the exchange notes. For more information, see “Plan of Distribution.” Any holder of original notes, including any broker-dealer, who:

| • | is our affiliate, |

| • | does not acquire the exchange notes in the ordinary course of its business, or |

| • | tenders in the exchange offers with the intention to participate, or for the purpose of participating, in a distribution of exchange notes, |

13

Table of Contents

cannot rely on the position of the staff of the Commission expressed in Exxon Capital Holdings Corporation, Morgan Stanley & Co., Incorporated or similar no-action letters and, in the absence of an exemption, must comply with the registration and prospectus delivery requirements of the Securities Act in connection with the resale of the exchange notes.

Material Tax Consequences | The exchange of original notes for exchange notes in the exchange offers will not be a taxable event for U.S. federal income tax purposes. For more information, see “Certain U.S. Federal Tax Considerations.” |

Use of Proceeds | We will not receive any cash proceeds from the issuance of the exchange notes in the exchange offers. |

Exchange Agent | U.S. Bank National Association is the exchange agent for the exchange offers. The address and telephone number of the exchange agent are set forth in the section captioned “The Exchange Offers—Exchange Agent.” |

14

Table of Contents

Summary of the Terms of the Exchange Notes

The following summary highlights the material information regarding the exchange notes contained elsewhere in this prospectus. We urge you to read this entire prospectus, including the “Risk Factors” section and the consolidated financial statements and related notes.

Issuer | Harrah’s Operating Company, Inc. |

Notes Offered

Exchange Cash Pay Notes | $4,200,153,000 aggregate principal amount of 10.75% Senior Notes due 2016. The exchange cash pay notes and the original cash pay notes will be considered to be a single class for all purposes under the indenture, including waivers, amendments, redemptions and offers to purchase. |

Exchange Toggle Notes | $1,052,583,000 aggregate principal amount of 10.75%/11.5% senior toggle notes due 2018. The exchange toggle notes and the original toggle notes will be considered to be a single class for all purposes under the indenture, including waivers, amendments, redemptions and offers to purchase. |

Maturity Date | The exchange cash pay notes will mature on February 1, 2016. The exchange toggle notes will mature on February 1, 2018. |

Interest Rate | Interest on the exchange cash pay notes will be payable in cash and will accrue at a rate of 10.75% per annum. |

Cash interest on the exchange toggle notes will accrue at a rate of 10.75% per annum, and PIK interest will accrue at a rate of 11.5% per annum. The initial interest payment on the exchange toggle notes will be payable in cash. For any interest period thereafter through February 1, 2013, the Issuer may elect to pay interest on the exchange toggle notes (i) in cash, (ii) by increasing the principal amount of the toggle notes or by issuing new toggle notes (“PIK interest”) or (iii) by paying interest on half of the principal amount of the exchange toggle notes in cash interest and half by increasing the principal amount of the exchange toggle notes or by issuing new toggle notes (“partial PIK interest”). After February 1, 2013, all interest on the exchange toggle notes will be payable in cash. If the Issuer elects to pay PIK interest or partial PIK interest, the Issuer will increase the principal amount of the exchange toggle notes or issue new exchange toggle notes or in an amount equal to the amount of PIK interest or partial PIK interest for the applicable interest period (rounded up to the nearest $1) to holders of the exchange toggle notes on the relevant record date.

On July 2, 2008, the Issuer made the permitted election under the Indenture governing its 10.75%/11.5% Senior Toggle Notes due 2018 to pay all interest due on February 1, 2009 for the notes and February 2, 2009 in kind.

15

Table of Contents

Interest Payment Dates | February 1 and August 1, commencing on August 1, 2008. |

Ranking | The exchange notes will be the Issuer’s senior unsecured obligations and will: |

| • | rank senior in right of payment to all existing and future debt and other obligations that are, by their terms, expressly subordinated in right of payment to the exchange notes; |

| • | rank equally in right of payment to all of the Issuer’s existing and future senior debt; and |

| • | be effectively subordinated to all of the Issuer’s existing and future secured debt (including obligations under the Issuer’s senior secured credit facilities), to the extent of the value of the assets securing such debt, and are structurally subordinated to all obligations of each of the Issuer’s subsidiaries that is not a guarantor of the notes. |

As of September 30, 2008, after giving pro forma effect to the Private Exchange Offers, the notes and the senior unsecured cash pay interim loans and senior unsecured PIK toggle interim loans ranked (1) effectively junior to $7,464 million of senior secured indebtedness under the senior secured credit facilities, the 2015 Second Lien Notes, the 2018 Second Lien Notes and other senior secured indebtedness, (2) effectively senior to approximately $2,809 million face value of senior unsecured indebtedness to the extent of the guarantees provided by the guarantor subsidiaries, (3) contractually senior to approximately $536 million face value of retained notes constituting senior subordinated indebtedness and (4) effectively junior to $6,500 million of indebtedness of its non-guarantor subsidiaries. Further, the Issuer had $1,554 million available for additional borrowing under its new revolving credit facility (after giving effect to approximately $196 million in outstanding letters of credit), all of which would be secured.

Guarantees | The exchange notes will be jointly and severally irrevocably and unconditionally guaranteed by Harrah’s Entertainment and each of the material wholly-owned domestic subsidiaries of Harrah’s Operating, in each case to the extent such entity pledged its assets to secure the senior secured credit facilities of Harrah’s Operating. Similarly, the guarantees will be the senior unsecured obligations of the guarantors and will: |

| • | rank senior in right of payment to all of the applicable guarantor’s future debt and other obligations that are, by their terms, expressly subordinated in right of payment to the exchange notes; |

| • | rank equally in right of payment to all other applicable guarantor’s existing and future senior debt and other obligations that are not, by their terms, expressly subordinated in right of payment to the exchange notes; and |

| • | are effectively subordinated to all of the applicable guarantor’s existing and future secured debt (including indebtedness secured |

16

Table of Contents

by such guarantor’s assets, such as the Issuer’s senior secured credit facilities), to the extent of the value of the assets securing such debt, and are structurally subordinated to all obligations of each of the Issuer’s or Harrah’s Entertainment’s subsidiaries that is not a guarantor of the exchange notes. |

Any guarantee of the exchange notes will be released in the event such assets pledged to secure the senior secured credit facilities are released under the senior secured credit facilities.

Optional Redemption | The Issuer may redeem the exchange notes, in whole or part, at any time prior to February 1, 2012 with respect to the exchange cash pay notes, and February 1, 2013, with respect to the exchange toggle notes at a price equal to 100% of the principal amount of the exchange notes redeemed plus accrued and unpaid interest to the redemption date and a “make-whole premium,” as described in “Description of Exchange Notes—Optional Redemption.” |

The Issuer may redeem the notes, in whole or in part, on or after February 1, 2012 with respect to the exchange cash pay notes, and February 1, 2013, with respect to the exchange toggle notes at the redemption prices set forth under “Description of Exchange Notes—Optional Redemption.”

Optional Redemption After Certain Equity Offerings | At any time (which may be more than once) before February 1, 2011, the Issuer may choose to redeem up to 35% of the principal amount of each of the exchange cash pay notes and the exchange toggle notes at a redemption price equal to 110.75% of the face amount thereof with respect to the exchange cash pay notes and 110.75% of the face amount thereof, with respect to the exchange toggle notes, in each case, with the net proceeds of one or more equity offerings to the extent such net cash proceeds are received by or contributed to us and so long as at least 50% of the aggregate principal amount of the exchange notes at maturity issued of the applicable series remains outstanding afterwards. See “Description of Exchange Notes—Optional Redemption.” |