As filed with the Securities and Exchange Commission on September 28, 2009

(Registration No. 333-156975)

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 3

TO

FORM F-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

NORTH AMERICAN MINERALS GROUP INC.

(Exact Name of Registrant as specified in its charter)

| Alberta | 1401 | N/A |

| (State or other Jurisdiction of | (Primary Standard Industrial | (I.R.S Employer |

| Incorporation or Organization) | Classification Code Number) | Identification No) |

North American Minerals Group Inc.

208 Woodpark Place, S.W. Calgary, Alberta, T2W 2S5 Canada

Tel: (888) 422-1122 Fax: (800) 424-3465

(Address, including zip code, and telephone number, including area code, of Registrant's principal executive offices)

Copy to:

Elliot H. Lutzker, Esq.

Phillips Nizer LLP

666 Fifth Avenue

New York, NY 10103-0084

(212) 977-9700 (telephone)

(212) 262-5152 (facsimile)

(Name, address, including zip code, and telephone number, including area code, of agent for service in the United States)

Approximate date of commencement of proposed sale to the public: as soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

CALCULATION OF REGISTRATION FEE

Title of Each Class of Securities To Be Registered | Amount To Be Registered | Proposed Maximum Offering Price Per Share (1) | Proposed Maximum Aggregate Offering Price (1) | Amount of Registration Fee (1) | ||||||||||||

| Units(2) | 4,000,000 Uts | $ | 0.25 | $ | 1,000,000 | $ | 55.80 | |||||||||

| Common Shares, no par value | 4,000,000 Shs. | (3 | ) | (3 | ) | (3 | ) | |||||||||

| Common Share Warrants | 4,000,000 Wts. | (3 | ) | (3 | ) | (3 | ) | |||||||||

| Common Shares, Underlying Warrants | 4,000,000 Shs. | (4)(5) | $ | 0.30 | $ | 1,200,000 | $ | 66.96 | ||||||||

| Common Shares, no par value | 2,500,000 | (5)(6) | $ | 0.25 | $ | 625,000 | $ | 34.88 | ||||||||

| Common Shares, no par value | 2,848,867 | (5)(7) | $ | 0.25 | $ | 712,217 | $ | 39.74 | ||||||||

| TOTAL | 13,348,867 | $ | 3,537,217 | $ | 197.38 | |||||||||||

| (1) | Estimated solely for the purpose of computing the registration fee pursuant to Rule 457(o) and 457(g) under the Securities Act of 1933, as amended. This fee was paid on January 27, 2009. |

| (2) | Consists of 4,000,000 Units, each Unit consisting of one Class A Common Share, no par value (“Common Shares”) and one Common Share Purchase Warrant (“Warrant”) to purchase one Common Share. |

| (3) | Pursuant to Rule 457(g), no additional registration fee is required for these shares and warrants included in the Units offered hereby. |

| (4) | Reflects Common Shares issuable upon the exercise of the Warrants underlying the Units in the Offering. |

| (5) | Pursuant to Rule 416 under the Securities Act, these shares include an indeterminate number of Common Shares issuable as a result of stock splits, stock dividends, recapitalizations or similar events and the anti-dilution provisions of the Warrants. |

| (6) | Common Shares issuable under the Registrant’s Stock Option Plan. |

| (7) | Common Shares issued and outstanding to be sold from time to time by existing shareholders of the Registrant. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the U.S. Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information contained in this prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission (the “SEC”) is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion – Dated September 28, 2009

Prospectus

NORTH AMERICAN MINERALS GROUP INC.

Up to 4,000,000 Units at $.25 per Unit

each Unit consisting of one Class A Common

Share and one Common Share Purchase Warrant to

purchase one Common Share; 2,848,867 issued and

outstanding Common Shares to be sold by Selling Shareholders

and 2,500,000 shares issuable under the Company’s stock option plan

This prospectus relates to the primary offering (the “Offering”) by the Company of up to: (i) 4,000,000 units (“Units”), each Unit consisting of one Class A Common Share (“Common Share”) and one Common Share Purchase Warrant (“Warrants”), being offered at $.25 per Unit; (ii) 4,000,000 Common Shares included in the Units; (iii) 4,000,000 Warrants included in the Units; and (iv) 4,000,000 Common Shares issuable upon exercise of Warrants at $.30 per share (the "Warrant Shares") included in the Units. In addition, 2,848,867 Common Shares held by existing shareholders (“Selling Shareholders”) and 2,500,000 Common Shares issuable under the Company's stock option plan may be offered for resale by option holders (“Optionees”).

The Offering will be conducted on a “best efforts” basis for up to ninety (90) days following the date of this prospectus at a fixed price of $0.25 per Unit, including the price at which the Common Shares and Warrants included in the Units are being offered. The Offering may be extended by the Company for up to an additional 30 days or terminated at an earlier date, at the Company’s sole discretion.

Before purchasing any of the Common Shares covered by this prospectus, carefully read and consider the risk factors included in the section entitled "Risk Factors" beginning on page 9. These securities involve a high degree of risk, and prospective purchasers should be prepared to sustain the loss of their entire investment. There is currently no public trading market for the securities.

Neither the United States Securities and Exchange Commission ("SEC"), the Alberta Securities Commission, the British Columbia Securities Commission, or any state or provincial securities commission, has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is ____________, 2009

We intend to seek a listing of Common Shares on the Over-The-Counter Bulletin Board (“OTCBB”), which is maintained by the Financial Industry Regulatory Authority, Inc. (“FINRA”). Until such time, if ever, that our Common Shares are listed on the OTCBB, or otherwise traded, the shares offered hereby by the Selling Shareholders and/or by Optionees under the Common Stock Option Plan may only be sold at an initial fixed price of $0.25 per share. If our shares are listed on the OTCBB we will file a supplement to this registration statement to reflect the shares offered hereby may be sold at prices relating to the prevailing market prices, at privately negotiated prices or through a combination of such methods, which may change from time to time and from offer to offer.

No shares have been issued under the Common Stock Option Plan. There are no limits on how many shares Optionees can sell pursuant to this registration statement. There are no end dates to when Selling Shareholders and/or Optionees may sell shares. However, we will file post-effective amendments to this registration statement to update the prospectus so that it remains current and/or to reflect any changes to Optionees’ information once the 2,500,000 Common Shares have been issued under the plan.

Because the Offering is being made on a “best-efforts” basis and there is no minimum number of Common Shares that must be sold by us during the 90-day selling period, we may receive little or no proceeds if we are not successful in selling the Common Shares. Our officers and directors, none of whom are registered broker-dealers will be offering the Common Shares on behalf of the Company pursuant to the exemption from broker-dealer registration provided by Rule 3a4-1 under the Securities Exchange Act of 1934 (the “Exchange Act”), in particular under Subsection (a)(4)(ii) or (iii) of Rule 3a4-1. Our officers and directors will not receive a commission or other compensation for shares sold by them.

You should rely only on the information contained or incorporated herein by reference, in this prospectus. We have not authorized anyone, including any salesperson or broker, to give oral or written information about this Offering, the Company, or the Common Shares offered hereby that is different from the information included in this prospectus. We are not making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should assume that the information contained in this prospectus is accurate only as of the date on the front cover of this prospectus. We will update this prospectus, from time to time, to include new information about us, and we will file supplements to the prospectus with the SEC. You should carefully read this prospectus, any prospectus supplement, and the information we, from time to time, file with the SEC as described under the caption "Where You Can Find Additional Information."

FORWARD-LOOKING STATEMENTS

Certain information contained in this prospectus and the documents incorporated by reference into this prospectus include forward-looking statements. All statements other than statements of historical facts, included in this prospectus regarding our strategy, future operations, future financial position, future revenues, projected costs, prospects and plans and objectives of management are forward-looking statements.

These forward-looking statements are not based on historical facts but rather on our expectations regarding future growth, results of operations, performance, future capital and other expenditures (including the amount, nature and sources of funding thereof), competitive advantages, business prospects and opportunities. Statements in this prospectus about our future-plans and intentions, results, levels of activity, performance, goals or achievements or other future events constitute forward-looking statements.

Words such as "might," "may," "will," "should," "could," "expect," "anticipate," "intend," "plan," "potential," "estimate," "likely," "believe," or "continue" and similar expressions have been used to identify these forward-looking statements. These words and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words.

-2-

These forward-looking statements reflect our current beliefs and are based on information currently available to us. Forward-looking statements involve significant risks and uncertainties. A number of factors could cause actual results to differ materially from the results discussed in the forward-looking statements including, but not limited to, changes in general economic and market conditions and other risk factors. Although the forward-looking statements contained herein are based upon what we believe to be reasonable assumptions, we cannot assure that actual results will be consistent with these forward-looking statements. Investors should not place undue reliance on forward-looking statements. These forward-looking statements are made as of the date of this prospectus and we assume no obligation to update or revise them to reflect new events or circumstances. Forward-looking statements and other information contained in this prospectus concerning the gem stone industry and our general expectations concerning the gem stone industry are based on estimates and prepared by us using data from publicly available industry sources as well as from market research and industry analysis and on assumptions based on data and knowledge of this industry which we believe to be reasonable. However, this data is inherently imprecise, although generally indicative of relative market positions, market shares and performance characteristics. We believe all industry data provided in the Prospectus is accurate, however, the gem stone industry involves risks and uncertainties and industry data is subject to change based on various factors. See "RISK FACTORS" beginning on page 9.

TABLE OF CONTENTS

| PROSPECTUS SUMMARY | 4 | |

| RISK FACTORS | 9 | |

| INFORMATION WITH RESPECT TO THE REGISTRANT AND THE OFFERING-IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS | 20 | |

| OFFER STATISTICS AND EXPECTED TIMETABLE | 22 | |

| KEY INFORMATION | 22 | |

| CAPITALIZATION AND INDEBTEDNESS | 29 | |

| REASONS FOR THE OFFER AND USE OF PROCEEDS | 29 | |

| INFORMATION ON THE COMPANY | 31 | |

| OPERATING AND FINANCIAL REVIEW AND PROSPECTS | 53 | |

| DIRECTORS, SENIOR MANAGEMENT AND ADVISERS | 63 | |

| MAJOR STOCKHOLDERS AND RELATED PARTY TRANSACTIONS | 70 | |

| FINANCIAL INFORMATION | 73 | |

| THE OFFER AND LISTING | 73 | |

| PRIOR SALES | 75 | |

| SELLING SHAREHOLDERS | 77 | |

| DILUTION | 84 | |

| ADDITIONAL INFORMATION | 85 | |

| QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 97 | |

| DESCRIPTION OF SECURITIES OTHER THAN EQUITY SECURITIES. | 97 | |

| MATERIAL CHANGES | 97 | |

| INCORPORATION OF CERTAIN INFORMATION BY REFERENCE | 97 | |

| DISCLOSURE OF COMMISSION POSITION ON INDEMNIFICATION FOR SECURITIES ACT LIABILITIES | 98 | |

| EXPERTS | 98 | |

| WHERE YOU CAN FIND MORE INFORMATION | 98 | |

| F-1 |

-3-

PROSPECTUS SUMMARY

The following summary is qualified in its entirety by the more detailed information and the financial statements and notes thereto appearing elsewhere in this prospectus. Prospective investors should consider carefully the information discussed under "Risk Factors." An investment in our securities presents substantial risks, and you could lose all or substantially all of your investment. In this prospectus, references to "U.S. dollars", "US$" or “USD” are to the currency of the United States and references to “CAD” or “Canadian dollars” are to the currency of Canada.

Use of Names

In this prospectus, unless the context otherwise requires, "NAMG," "we," "us" and "our" refer to North American Minerals Group Inc.

Overview

The Company was incorporated in the Province of Alberta, Canada, on February 17, 2006 and commenced operations in March 2006. The Company continued into British Columbia on April 24, 2006 and, subsequently, continued back to Alberta on September 13, 2007. We are engaged in the business of gem stone exploration. Our business focus is in Canada and the Western United States, with initial emphasis in the State of Colorado, as well as Wyoming.

As the Company is in the early exploration stage, its operations have been structured in a manner that management believes, brings the requisite skills and services to the Company in order to operate efficiently and at the same time manage overhead costs. It is anticipated that until proposed exploration programs are complete, independent consultants will be engaged to undertake the exploration programs and the Company will not have any employees. In addition, certain officers and directors of the Company are experienced in the identification and acquisition of mineral properties.

Business

The Company is an early stage gem stone exploration company focusing on kimberlite-hosted diamond resources in Canada and the Western United States, with initial emphasis in the State of Colorado, as well as Wyoming. The Company's strategy is to maximize shareholder value through successful exploration of the Properties (as defined below).

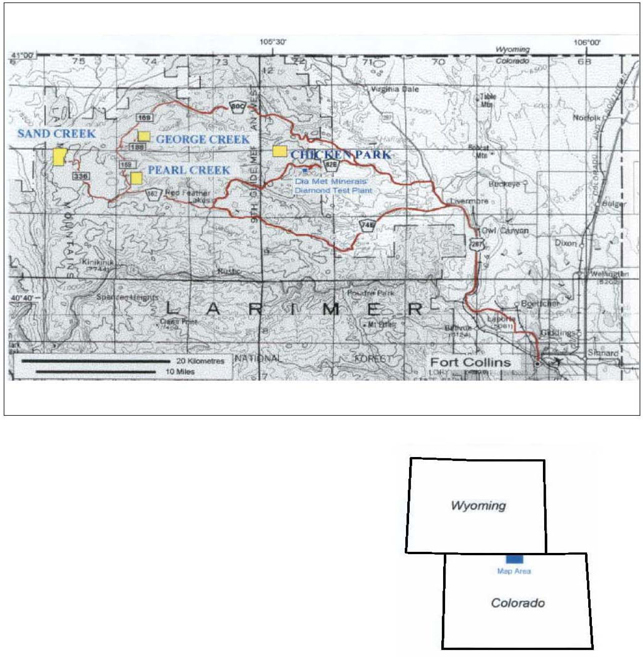

The Company has commissioned a National Instrument 43-101 (NI 43-101) compliant technical report on the Northern Colorado Diamond Project, Larimer County, Colorado, USA, as revised by report dated January 29, 2009 (the "Technical Report"), in respect of the Colorado Mineral Project. NI 43-101 are the specific requirements of the Canadian Securities Administrators setting forth the Standards of Disclosure for Mineral Projects. The NI 43-101 is a strict guideline for how public Canadian companies can disclose scientific and technical information about mineral projects. The instrument requires that a “qualified person” be attributed to the information. A qualified person is defined as: an engineer or geoscientist with at least 5 years experience in the mineral resources field and a subject matter expert in the mineral resources field and has a professional association. The Company intends to use the proceeds of the Offering to further explore the Properties through delineation drilling, bulk sampling, geological mapping and soil sampling as warranted. Additional property acquisitions in the general area of the Properties, are anticipated and the acquisition of additional properties in the immediate vicinity of the existing land package, is anticipated for the near future. These potential acquisitions are intended to cover targets identified by exploration work performed by other companies in the past and that possibly represent undiscovered kimberlite (a rock type in which diamonds are found) occurrences. Also considered in the near term, is the acquisition of properties also containing previously identified targets in the State Line Kimberlite District, but not necessarily contiguous to the Company's existing claims.

The Company's primary business objective for the foreseeable future is to explore the Colorado Mineral Project. Its strategy to achieve this objective is:

-4-

| · | to apply a focused "value added" exploration program using an integrated, science and technology-driven approach; |

| · | to identify and rank, on a timely and efficient basis, kimberlite targets identified from the results of its exploration; and |

| · | to drill kimberlite targets identified through its exploration initiatives. |

Exploration activities planned for George Creek, Pearl Creek and Chicken Park will focus on furthering the knowledge of the economic potential of the kimberlites proper, additional exploration will be carried out elsewhere on the existing land-package. Further, if the Company acquires additional mineral properties in the near future and in the immediate vicinity of the Properties), it will conduct such work and activities on these properties as is practicable, in order to locate additional kimberlite targets for future testing.

The Company's secondary objective is to locate economic gem stone properties of merit. The Company plans to aggressively acquire, exploit and explore natural resource prospects and will focus on acquisitions of mineral claims where management believes further exploration and exploitation opportunities exist. While largely opportunity driven, the Company plans to pursue a balanced portfolio of mineral reserve and resource prospects. In selecting exploration and exploitation prospects, management of the Company will choose those that it believes will offer an appropriate combination of risk and economic reward, recognizing that all exploration involves substantial risk and that a high degree of competition exists for prospects. To achieve sustainable and profitable growth, the Company believes in controlling the timing and costs of its projects whenever possible.

Mineral resource exploration involves substantial risk and no assurance can be given that exploration will prove successful in establishing commercially recoverable reserves. While management of the Company believes that it has the skills and resources necessary to achieve the Company's objectives, participation in the exploration of mineral resources and reserves has a number of inherent risks. See "Risk Factors."

The Company is currently engaged in the acquisition and exploration of mineral properties and as at the date hereof, holds limited interests in certain diamond mineral properties represented by the CMP Claims and the Ruby Claims, which are both defined below (the "Properties"). The Company intends to acquire additional properties and interests by negotiating with holders of leases, claims and/or permits. The Company will commit its own resources to the initial evaluation of mineral properties and in select situations, if and when warranted, will enter into joint-venture or farm-out agreements with other corporations or other industry players to complete or continue the further exploration of such properties.

Colorado Claims Purchase Agreement

On September 5, 2006, the Company entered into the Colorado Claims Purchase Agreement (the “CMP Claims”), pursuant to which the Company’s founders, Yosi Lapid, Amihay Lapid and Yonatan Lapid (the “Founders”) assigned, transferred and sold to the Company 100% of their interest in the CMP Claims in exchange for 14,200,000 Common Shares. The mining property was recorded at $2,130,000, the fair value determined by Howard G. Coopersmith, the Professional Geologist who prepared the above-described Technical Report and who became our President and Chief Executive Officer on September 17, 2009. The properties as a whole are subject to a minimum exploration expenditure of $155,000 which has been exceeded; $248,437 has been spent in 2006 and 2007. The Royalty of three percent (3%) of the net sales attributable to diamonds recovered from the CPM claims, is held by Ernest Black who is a Director of the Company. Upon further consideration for the CMP Claims, the Company assumed the obligation to pay the Black Royalty. Upon achieving commercial production of the CMP Claims, the Company has the right to unilaterally acquire, for a period of five (5) years, some or all of the Black Royalty upon payment to Black of $1,000,000 per Black Royalty percentage point (to a maximum of $3,000,000, at which time the Company will have satisfied all obligations under the Black Royalty). If, after six (6) years from the effective date of the Colorado Claims Purchase Agreement, commercial production of the Properties has not commenced, Black is entitled to be paid an annual advance on the Black Royalty of $50,000, to be set-off against any future Black Royalty payments made.

-5-

Asset Transfer Agreement

On September 5, 2006, the Company entered into the Asset Transfer Agreement, pursuant to which it transferred its undivided 100% interest in the CMP Claims to American Mining, a wholly-owned Delaware subsidiary of the Company. In return, American Mining assumed all rights and obligations associated with the CMP Claims, including the rights and obligations associated with the Black Royalty.

Ice Option Agreement and Re-Stated Ice Option Agreement

On May 22, 2007, the Company entered into an agreement with Ice Resources Inc.("Ice"), giving Ice the option to purchase a fifty percent (50%) interest in its Chicken Park, George Creek, Sand Creek and Pearl Creek properties (the "Ice Option Agreement"). Pursuant to the terms of the Ice Option Agreement, Ice was required to incur a total of $1,500,000 in exploration and development expenditures over a three-year period, at which time, the Company and Ice were obligated to negotiate in good faith toward the entering into of a 50/50 Joint Venture Agreement. On March 13, 2008, the Company and Ice renegotiated the Ice Option Agreement by mutually agreeing to cancel it in its entirety and enter into a new agreement (the "Re-Stated Ice Option Agreement"). Pursuant to the Re-Stated Ice Option Agreement, Ice obtained a fifteen percent (15%) carried interest in the Properties until feasibility has been reached, at which time Ice is responsible for carrying its pro-rata share of all expenses incurred in connection with the Properties. In consideration for the restructuring of the terms of its interest in the Properties, Ice relinquished the right to acquire an option to purchase a fifty percent (50%) interest in the Chicken Park, George Creek, Sand Creek and Pearl Creek properties. As further consideration, Ice provided the Company with four (4) additional mineral claims which provide the potential for expansion to the George Creek Property. Ice who was a related party to the Company; the former President and CEO of the Company is also a director and founder of Ice.

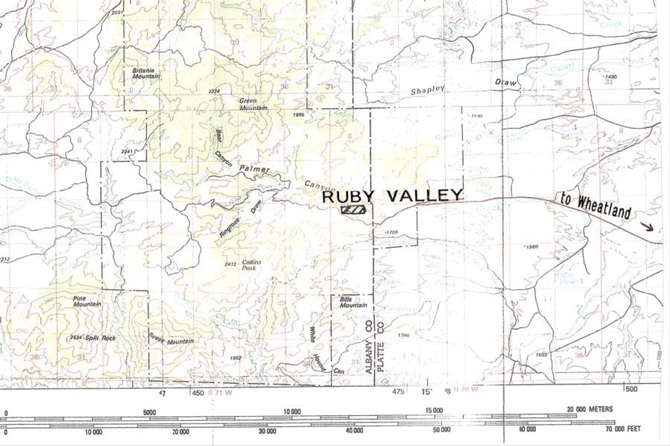

Ruby Valley Exploration and Option Agreement

On August 21, 2007, the Company entered into the Ruby Valley Exploration and Option Agreement, pursuant to which it obtained, for no additional consideration from Ice, the option to purchase 75% of 2 federal lode mining claims (the "Ruby Claims"), located in Albany County, Wyoming. No royalties are payable to Ice (as optionor) in respect of the Ruby Claims. To maintain its option on the Ruby Claims, the Company was required to incur, on or before each of first, second and third anniversaries of August 21, 2007, expenditures of $100,000. No independent valuation of the fair value of these payments was made. On November 19, 2008, the Ruby Valley Exploration and Option Agreement with Ice, was amended to waive the first year expenditure of $100,000 and increasing the second year expenditure to $200,000. In consideration for the amendment the Company agreed to issue to Ice, 100,000 options to purchase Common Shares in the Company at the price the Company issues its securities to the public market if and when it is publicly traded.

Trends

Other than as disclosed in this prospectus, management of the Company is not aware of any trends , commitments, events or uncertainties other than general economic conditions, that are reasonably expected to have a material effect on the Corporation's business, financial condition or operations. See "Risk Factors".

Diamond Market Overview

Approximately 160 million carats of rough diamonds have been produced annually, with an approximate value of US$12.5 billion. Based upon the knowledge of Howard G. Coopersmith, the author of the Technical Report, world diamond production continues to slightly decline, while demand grows and outpaces production. In the last two months of 2008, the world financial crisis substantially impacted diamond sales. Retail sales dropped, and the inventory of polished goods grew to unacceptable levels. Mine production rough prices correspondingly dropped to levels seen in January 2008, negating large rough price increases seen in mid-year. Subsequently many of the world’s diamond mines were placed on care and maintenance, amounting to 30 to 40% of world production, to help correct this imbalance between rough production and polish consumption. At the end of 2008 and in early 2009, rough prices had dropped by about 40-50% and polished prices had dropped about 15%. The correction of this imbalance and resumption of normal pricing depends on the resolution of the world’s financial crisis. Based on their knowledge of the industry, including readily available information on the Internet, Management and Mr. Coopersmith believe diamond prices can be expected to be flat to slightly dropping for the remainder of 2009, with improvement seen in late 2009 or 2010.

-6-

OFFERING

Prospective investors should read the following together with the more detailed information concerning the Company, and the securities being sold in the Offering found elsewhere in this prospectus, before investing. Special attention should be paid to the risks described under the heading "Risk Factors."

Offering: By Company: | The Offering consists of up to 4,000,000 Units with aggregate gross proceeds of $1,000,000. Each Unit has a purchase price of $0.25 and consists of Common Shares and a Warrant to purchase an equal number of Common Shares at an exercise price of $0.30 per share (subject to adjustment) that expires two years from the Initial Closing Date, subject to earlier redemption. There is no minimum subscription. The Offering will be conducted by officers and directors of the Company on a “best efforts” basis at a fixed price of $0.25 per Unit, including the price at which the Common Shares and Warrants included in the Units are being offered. The Company’s officers and directors will rely on the exemption from broker-dealer registration under Subsection (a)(4)(ii) or (iii) of Rule 3a4-1 under the Exchange Act. This Offering will remain open until the earlier of: ninety (90) days following the date of this prospectus, unless extended by the Company for up to an additional 30 days; or the sale of the maximum Offering of Units, or the Company’s determination to terminate the Offering at an earlier date at its sole discretion. The early termination of the Offering shall be made public through the Company’s filing of a Form 8-K with the SEC. |

By Selling Shareholders: | 2,848,867 shares equal to 10% of the Company’s issued and outstanding Common Shares to be offered by Selling Stockholders; and 2,500,000 shares issuable under the Company’s stock option plan to be offered by Optionees. Until such time, if ever, that our Common Shares are listed on the OTCBB, or otherwise traded, the shares offered hereby by the Selling Shareholders and/or Optionees may only be sold at an initial fixed price of $0.25 per share. |

| Ownership of the Company: | Immediately following the Offering, it is anticipated that the outstanding capitalization of the Company will consist of: (i) 4,000,000 Common Shares if the maximum Offering is sold and (ii) 28,488,663 Common Shares that are held by the Company's existing stockholders, 10% of which have been registered herein for resale. Assuming the sale of the maximum Offering, the purchasers in the Offering will own approximately 12.3% of the 32,488,663 then outstanding Common Shares, and 21.9% upon exercise of Warrants to purchase 4,000,000 shares issuable to the purchasers in the Offering, without giving effect to the exercise of any outstanding warrants. |

| Use of Proceeds: | The Company intends to apply the net proceeds of the Offering (estimated to be approximately $850,000 if the maximum Offering is completed) for exploration and working capital. See “Use of Proceeds.” |

| The Company shall receive no consideration in connection with the sale of any shares registered under this prospectus for Selling Shareholders. In order for the Company to receive proceeds from the exercise of Warrants and/or options, a current prospectus will have to be in effect. |

-7-

| Warrant Redemption: | The Company may redeem all, but not less than all, of the unexercised Warrants included within the Units sold in the Offering, for $0.001 per Common Share underlying the Warrants, upon 30 days’ prior written notice to the holders (the period between such notice and the redemption date is referred to as the "Redemption Period"); provided that (i) the closing sale price of the Company's Common Shares on the principal trading market where the Common Shares is approved for quotation or principal national securities exchange where the Common Shares is listed exceeds $0.75 for 10 consecutive trading days and (ii) there is an effective registration statement covering the resale of the Common Shares underlying the Warrants for the entire Redemption Period. The holders may exercise the Warrants during the Redemption Period. Upon redemption of the Warrants, the holders will have no further rights with respect to the unexercised Warrants, except the right to receive the redemption price. |

| Stock Option Plan: | The Company has adopted a stock option plan, pursuant to which options to purchase up to 2,500,000 Common Shares are reserved for issuance to employees, officers, directors, and consultants. No shares have been issued under the Common Stock Option Plan. There are no limits on how many shares Optionees can sell pursuant to this registration statement. There are no end dates to when Selling Shareholders and/or Optionees may sell shares. However, we will file post-effective amendments to this registration statement to update the prospectus so that it remains current and/or to reflect any changes to Optionees’ information once the 2,500,000 Common Shares have been issued under the plan. |

| Directors and Senior Management: | Following the Registration, the Company's Board of Directors will be comprised of the following: |

1. Howard G. Coopersmith - President, CEO and Director, c/o North American Minerals Group Inc. 110 Wall Street 11th Floor, New York, NY 10005 USA | |

2. Zacharia Waxler - CFO and Director, c/o North American Minerals Group Inc. 110 Wall Street 11th Floor, New York, NY 10005 USA | |

| 3. Ernest Black – Director, c/o North American Minerals Group Inc. 208 Woodpark Place, S.W., Calgary, Alberta T2W 2S5, Canada. | |

| 4. Yair Lapid – Director, c/o North American Minerals Group Inc. 208 Woodpark Place, S.W., Calgary, Alberta T2W 2S5, Canada. | |

| 5. Alexander Levitski – Director, c/o North American Minerals Group Inc. 208 Woodpark Place, S.W., Calgary, Alberta T2W 2S5, Canada. | |

6. Richard Attoh-Okine – Director, c/o North American Minerals Group Inc. 110 Wall Street 11th Floor, New York, NY 10005 USA | |

| As a requirement to listing the Company's Common Stock on Nasdaq or on another securities exchange, the Company may need to add additional independent directors and increase the size of the Board of Directors at or following the Registration. The Board's composition (and that of its committees) will be subject to the corporate governance provisions of its primary trading market, including the requirement for appointment of independent directors in accordance with the Sarbanes-Oxley Act of 2002, and regulations adopted by the SEC and FINRA pursuant thereto. The Company is expected to adopt corporate governance provisions that would be required of a Nasdaq company at the time of the registration. Neither independent directors nor corporate governance provisions are required (except pursuant to applicable contracts) prior to listing on any securities exchange. |

-8-

| Advisers: | Our principal bankers are TD Canada Trust, Chinook Centre, 6455 Macleod Trail S.W., Calgary, Alberta, T2H 0K3. |

| Our U.S. legal adviser is Phillips Nizer LLP, 666 Fifth Avenue, 28th Floor, New York, New York 10103. | |

Our Canadian legal adviser is McCarthy Tetrault LLP, Suite 3300, 421-7th Avenue S.W., Calgary, Alberta, T2P 4K9 | |

| Auditors: | Deloitte & Touche LLP, audited our financial statements for the period from February 17, 2006 (inception) to the Fiscal year ended December 31, 2008. Deloitte & Touche LLP is registered with the Public Company Accounting Oversight Board ("PCAOB') in the United States and are Independent Registered Chartered Accountants in Canada with an address at 5140 Yonge Street, Suite 1700, Toronto, Ontario, M2N 6L7 Canada. |

| Risk Factors: | The securities offered hereby involve a high degree of risk and shall not be purchased by investors who cannot afford the loss of their entire investment. See “Risk Factors.” |

RISK FACTORS

An investment in our securities should be considered highly speculative due to various factors, including the nature of our business and the present stage of our development. An investment in our securities should only be undertaken by persons who have sufficient financial resources to afford the total loss of their investment. In addition to the usual risks associated with investment in a business, the following is a general description of significant risk factors which should be considered. You should carefully consider the following material risk factors and all other information contained in this prospectus before deciding to invest in our Common Shares. If any of the following risks occur, our business, financial condition, results of operations, and cash flows could be materially and adversely affected.

Risks Relating To Our Business

We have a limited operating history and our future success depends upon our ability to generate cash flow from Properties.

The Company's business operations are at an early stage of development and our success is largely dependent on the outcome of the exploration programs that we propose to undertake. None of the Properties are producing revenues and our ultimate success will depend on our ability to generate cash flow from the Properties in the future. We have not earned profits to date and there is no assurance that we will do so in the future. The Properties are in the exploration stage and there are no known commercial quantities of mineral reserves on the Properties. Significant capital investment will be required to achieve commercial production from the Properties and the Company will have to raise the necessary funds to continue these activities. The purpose of this Offering is to raise enough financing to carry out exploration activities on the Properties, with the objective of establishing economic quantities of mineral reserves.

-9-

Mineral exploration is highly speculative in nature and there can be no certainty of our successful exploration of profitable commercial diamond mining operations.

The exploration of mineral properties involves significant risks which even a combination of careful evaluation, experience and knowledge may not eliminate. Few properties which are explored are ultimately developed into producing mines. Substantial expenses may be incurred to locate and establish mineral reserves, to develop metallurgical processes and to construct mining and processing facilities at a particular site. Whether a mineral deposit will be commercially viable depends on a number of factors, including, but not limited to, the particular attributes of the deposit, such as size, grade, and proximity to infrastructure; drilling and other related costs which appear to be rising; and government regulations, including regulations relating to prices, taxes, royalties, land tenure, land use, importing and exporting of minerals and environmental protection. The exact effect of these factors cannot be accurately predicted, but the combination of these factors may result in us not receiving an adequate return on invested capital. There is no certainty that the expenditures made by us towards the exploration and evaluation of mineral deposits will result in discoveries of commercial quantities.

Current and new sites could lead to substantial costs, delays or other operational or financial difficulties.

The business of exploration for minerals involves a high degree of risk. Few properties that are explored are ultimately developed into mines. At present, three of the Properties contain known diamond deposits and the proposed exploration programs consist of both an exploratory search for such a deposit on all Properties and an expansion of the knowledge of the existing deposits to lead to an economic viability decision. Our operations are subject to all the hazards and risks normally associated with the exploration of diamonds, any of which could result in damage to life, property or the environment. Our operations may be subject to disruptions caused by unusual or unexpected formations, formation pressures, fires, power failures and labor disputes, flooding, explosions, cave ins, landslides, the inability to obtain suitable or adequate equipment, machinery, labor or adverse weather conditions. The availability of insurance for such hazards and risks is extremely limited or uneconomical at this time. The Company's operations are also subject to the additional risks associated with the short exploration season in northern Colorado. Ice and snow cover the State Line Kimberlite District typically restricting access from December to April. The economics of commercial production depend on many factors, including the cost of operations, the size and quality of the diamonds, proximity to infrastructure, financing costs and government regulations, including regulations relating to prices, taxes, royalties, land tenure, land use, importing and exporting diamonds and environmental protection. The effects of these factors cannot be accurately predicted, but any combination of these factors could adversely affect the economics of commencement or continuation of commercial diamond production. The profitability of the Company’s operations will depend on, among other things, the market price of diamonds. Diamond prices are affected by numerous factors beyond the control of the Company, including international economic and political conditions, levels of supply and demand, the policies of the Diamond Trading Corporation and international currency exchange rates.

Mining operations generally involve a high degree of risk

Mining operations are subject to all the hazards and risks normally encountered in the exploration of precious stones, including unusual and unexpected geological formations, seismic activity, rock bursts, cave-ins, flooding and other conditions involved in the drilling and removal of material, any of which could result in damage to, or destruction of, mines and other producing facilities, damage to life or property, environmental damage and possible legal liability. Mining operations could also experience periodic interruptions due to bad or hazardous weather conditions and other acts of God. Milling operations are subject to hazards such as equipment failure or failure of retaining dams around tailing disposal areas which may result in environmental pollution and consequent liabilities.

If any of these risks and hazards adversely affect our mining operations or our exploration activities, they may: (i) increase the cost of exploration to a point where it is no longer economically feasible to continue operations; (ii) require us to write down the carrying value of one or more mines or a property; (iii) cause delays or a stoppage in the exploration of minerals; (iv) result in damage to or destruction of mineral properties or processing facilities; and (v) result in personal injury or death or legal liability. Any or all of these adverse consequences may have a material adverse effect on our financial condition, results of operations, and future cash flows.

-10-

Our financial statements have been prepared assuming that the Company will continue as a going concern.

The accompanying financial statements to this prospectus have been prepared assuming the Company will continue as a going concern. As discussed in Note 2 to the audited financial statements, the Company’s ability to attain profitable operations and generate funds therefrom and to continue to obtain financing from investors sufficient to meet current and future obligations, raise doubt about the Company’s ability to continue as a going concern. The Company’s financial statements do not reflect the adjustments or reclassification of assets and liabilities which would be necessary if the going concern assumption were not appropriate. Our independent registered public accounting firm has included an explanatory paragraph expressing doubt about our ability to continue as a going concern in their report dated July 8, 2009.

We are an exploration-stage company and our estimates are only preliminary and based primarily on past geological mapping, silt, soil and rock sampling which may not reflect the actual deposits or the economic viability of extraction, thus, it is difficult to assess Commercial Deposits in our current sites.

The Corporation has no known commercial deposits or production, as its current activities are directed towards the exploration of existing diamond deposits on the George Creek, Pearl Creek and Chicken Park properties (the three properties within the Colorado Mineral Project on which kimberlite bodies have been identified) and the search for additional diamond deposits on the Properties. The exploration for diamond deposits is highly speculative. There is no guarantee that exploration on the Properties will lead to a discovery of commercial quantities of diamonds and commercial production. There is a degree of uncertainty to the estimation of diamond reserves and corresponding grades being mined or dedicated to future production. The estimating of diamonds is a subjective process and the accuracy of estimates is a function of the quantity and quality of data, the accuracy of statistical computations, and the assumptions used and judgments made in interpreting engineering and geological information. There is significant uncertainty in any geological estimate, and the actual deposits encountered and the economic viability of mining a deposit may differ significantly from our estimates. Until diamond reserves are actually mined and processed, the quantity of diamonds and reserve grades must be considered as estimates only. Any material change in quantity or diamond reserves, grade of stripping ration may affect the economic viability of the properties. In addition, there can be no assurance that recoveries in small scale laboratory tests will be duplicated in larger scale tests under on-site conditions or during production. This could materially and adversely affect estimates of the volume or grade of diamonds, estimated recover rates or resources, or of our ability to extract these precious stones reserves, could have a material effect on our financial condition, results of operations and future cash flows.

We may not be able to compete with current and potential exploration companies, most of which have greater resources and experience than we do in developing diamond mines.

The natural resource market is intensely competitive, highly fragmented and subject to rapid change. We may be unable to compete successfully with our existing competitors or with any new competitors. We will be competing with many exploration companies which have significantly greater personnel, financial, managerial and technical resources than we do. This competition from other companies with greater resources and reputations may result in our failure to maintain or expand our business.

We are dependent upon key consultants whose loss may adversely impact our business.

We rely heavily on the expertise, experience of our senior management, including Howard G. Coopersmith, who will continue as our President and Chief Executive Officer. We will seek to compensate and motivate our executives, as well as other consultants, through competitive consulting fees and bonus plans, to allow us to retain them or hire new key employees. As a result, if Mr. Coopersmith was to leave following the Offering, we could face substantial difficulty in hiring a qualified successor and could experience a loss in productivity while any such successor obtains the necessary training and experience. The retention of key management members and services cannot be guaranteed. We compete with numerous other companies and individuals in the search for and acquisition of mineral claims, leases and other mineral interests as well as for the recruitment and retention of qualified employees and contractors.

-11-

Because our business involves numerous operating hazards, we may be subject to claims of a significant size which would cost a significant amount of funds and resources to rectify. This could force us to cease our operations.

Our operations are subject to the usual hazards inherent in exploring for diamonds, such as general accidents, explosions, and craterings. The occurrence of these or similar events could result in the suspension of operations, damage to or destruction of the equipment involved and injury or death to personnel. Operations also may be suspended because of machinery breakdowns, abnormal climatic conditions, seasonal access to roads, access to rail or roads for shipment purposes, failure of subcontractors to perform or supply goods or services or personnel shortages. The occurrence of any such contingency would require us to incur additional costs, which would adversely affect our business.

Damage to the environment could also result from our operations. If our business is involved in one or more of these hazards, we may be subject to claims of a significant size which could force us to cease our operations.

Mineral resource exploration, production and related operations are subject to extensive rules and regulations of federal, provincial, state and local agencies. Failure to comply with these rules and regulations can result in substantial penalties. Our cost of doing business may be affected by the regulatory burden on the mineral industry. Since these rules and regulations frequently are amended or interpreted, we cannot predict the future cost or impact of complying with these laws.

Environmental enforcement efforts with respect to mineral operations have increased over the years, and it is possible that regulations could expand and have a greater impact on future mineral exploration operations. Any noncompliance with applicable regulatory requirements could subject us to penalties, fines and regulatory actions, the costs of which could harm our results of operations. We cannot be sure that our proposed business operations will not violate environmental laws in the future.

Our operations and properties are subject to extensive federal, state, provincial and local laws and regulations relating to environmental protection, including the generation, storage, handling, emission, transportation and discharge of materials into the environment, and relating to safety and health. These laws and regulations may do any of the following: (i) require the acquisition of a permit or other authorization before exploration commences, (ii) restrict the types, quantities and concentration of various substances that can be released in the environment in connection with exploration activities, (iii) limit or prohibit mineral exploration on certain lands lying within wilderness, wetlands and other protected areas, (iv) require remedial measures to mitigate pollution from former operations and (v) impose substantial liabilities for pollution resulting from our proposed operations.

The exploration of mineral reserves is subject to all of the usual hazards and risks associated with mineral exploration, which could result in damage to life or property, environmental damage, and possible legal liability for any or all damages. Such liabilities could exceed insurance policy limits or be excluded from coverage.

We may not be able to effectively control and manage our growth.

Our strategy envisions continuous growth. Our expected growth may impose a significant burden on our administrative and operational resources. The growth of our business may require significant additional investments of capital and increased demands on our management, workforce and facilities. We will be required to substantially expand our administrative and operational resources and attract, train, manage and retain qualified management and other personnel. Failure to do so or satisfy such increased demands would interrupt or would have a material adverse effect on our business and results of operations.

The mining industry is intensely competitive in all phases and our competitors may be better positioned than we are to adapt to rapid industry changes as we compete with other companies that have greater financial resources and technical facilities.

Competition in the gem stone mining industry involves competition primarily for mineral-rich properties which can be developed and produced economically, the technical expertise to find, develop and produce such properties, the labor to operate such properties and the capital for the purpose of financing development of such properties. Many of the our competitors not only explore for and mine gem stones, but conduct refining and marketing operations on a global basis. Many of our competitors have much greater financial and technical resources than we do. Such competition may result in our being unable to acquire desired properties, recruit or retain qualified employees or acquire the capital necessary to fund its operations and develop the Properties. Our inability to compete with other mining companies for mineral deposits could have a materially adverse effect on our results of operation, business, and cash flows.

-12-

Current economic recession could materially adversely affect the Company.

The Company’s future operations and performance depend significantly on worldwide economic conditions. Uncertainty about current global economic conditions poses a risk as consumers and businesses have postponed spending in response to tighter credit, negative financial news and/or declines in income or asset values, which could have a material negative effect on the demand for any gem stones the Company may discover. Demand for domestic gem stones could also differ materially from the Company’s expectations. Other factors that could influence demand include continuing increases in fuel and other energy costs, conditions in the residential real estate and mortgage markets, labor and healthcare costs, access to credit, consumer confidence, and other macroeconomic factors affecting consumer spending behavior. These and other economic factors could have a material adverse effect on demand for the Company’s products and services and on the Company’s financial condition, operating results, and cash flows.

The current financial turmoil affecting the banking system and financial markets and the possibility that financial institutions may consolidate, be nationalized or go out of business have resulted in a tightening in the credit markets, a low level of liquidity in many financial markets, and extreme volatility in fixed income, credit, currency and equity markets. There could be a number of follow-on effects from the credit crisis on the Company’s prospective operations, including insolvency of industry partners and contractors. The ultimate outcome of these economic conditions cannot be predicted, and they could have a negative impact on our liquidity and financial condition if our ability to borrow money to finance operations were to be impaired.

The Company continuously faces unexpected title risks.

Despite the exercise of proper due diligence with respect to determining the title to properties in which we have an interest, there is no guarantee that title to such properties will not be challenged or impugned. The Company's mineral property interests may be subject to prior unregistered agreements or transfers or native land claims and title may be affected by undetected defects. Surveys have not been carried out on any of our mineral properties in accordance with the laws of the jurisdiction in which such properties are situated; therefore, their existence and area could be in doubt. Until competing interests in the mineral lands have been determined, we can give no assurance as to the validity of title of the Company to those lands or the size of such mineral lands.

By not being able to make payment we may incur a loss of interest in the Properties.

Failure to meet applicable payment, work and expenditure commitments on the Properties may result in forfeiture of our interest in the Properties. A portion of the proceeds of the Offering have been allotted towards payment of processing of samples taken from the Properties which will be evaluated.

We are required to always have the proper permits and licenses.

Our operations require licenses, permits and in some cases renewals of existing licenses and permits from various governmental authorities. The Company's ability to obtain, sustain or renew such licenses and permits on acceptable terms is subject to changes in regulations and policies and to the discretion of the applicable local and federal governmental authorities.

The industry in which we operate is continually evolving, which makes it difficult to evaluate our future prospects and increases the risk of an investment in our securities. Thus, the volatility of diamond prices may negatively impact us.

The availability of a ready market for diamonds to be sold by the Company depends upon numerous factors beyond our control, the exact effects of which cannot be accurately predicted. The factors (the list of which is not exhaustive), include general economic activity, world diamond prices, action taken by other producing nations, the availability and pricing of other substitute minerals, and the effect of government regulation and taxation. Historically, diamond prices have fluctuated and are affected by numerous factors, including world production levels, international economic trends, currency exchange fluctuations or regional political events, over all of which the Company has no control. The aggregate effect of these factors is impossible to predict. Consequently, as a result of the above factors and others, price forecasting can be difficult to predict. If the price of certain diamonds should drop significantly, the economic prospect of operations in which the Company has an interest, could be significantly reduced or rendered economic. In addition, De Beers and the Diamond Trading Corporation (which is owned by De Beers), retain substantial influence in the diamond industry, controlling approximately 40% of the world production of diamonds, and consequently maintain the ability to influence the price of diamonds.

-13-

Taxation

Existing and future tax regimes, legislation and regulations, including royalty structures in Canada and the United States, could cause diamond deposits to be uneconomic. The Company has no control over government regulations and/or royalties on minerals which could change at any time making the Company’s projects uneconomic.

Uninsured risks

As a participant in exploration and mining programs, we may become subject to liability for hazards such as unusual geological or unexpected operating conditions that cannot be insured against or against which it may elect not to be so insured because of high premium costs or other reasons. As is customary for businesses at a similar stage of development as the Company, and operating in the industry in which we operate, the Company is currently uninsured against all such risks, as such insurance is either unavailable or uneconomic at this time. The Company is also not currently able to obtain key-man life insurance or property insurance as such insurance is uneconomical at this time. Therefore, we may incur liability to third parties (in excess of any insurance coverage) arising from pollution or other damage or injury causing the Company financial hardship.

We may face certain land claims

Native American rights may be claimed on Canadian Crown properties or other types of tenure with respect to which mining rights have been conferred. The Company is not aware of any Native American land claims having been asserted or any legal actions relating to aboriginal issues having been instituted with respect to any of the Properties.

The legal basis of a land claim is a matter of considerable legal complexity and the impact of a land claim settlement and self government agreements cannot be predicted with any certainty. In addition, Native American rights could by way of a negotiated settlement or judicial pronouncement have an adverse effect on the Company's activities. Such impact could be marked and in certain circumstances, could delay or even prevent the Company’s exploration or mining activities.

We are subject to local and Federal environmental laws and requirements, not abiding by such requirements may have detrimental consequences on our business.

Mining operations are subject to various environmental laws and regulations including, for example, those relating to waste treatment, emissions and disposal. Companies must generally comply with permits or standards governing, among other things, tailing dams and the disposal areas, water consumption, air emissions and water discharges. Existing and possible future environmental legislation, regulations and actions could cause significant expense, capital expenditures, restrictions and delays in the Company's activities, the extent of which cannot be predicted and which may be beyond the capacity of the Company to fund. The Company's right to exploit any minerals it discovers is subject to various reporting requirements and to acquiring certain government approvals, including environmental approvals which may not be granted without inordinate delays or at all.

A violation of health and safety laws or the failure to comply with the instructions of relevant health and safety authorities, could lead to, among other things, a temporary shutdown of all or a portion of the Company's operations.

Such a risk, leading the Company to a loss of the right to prospect for diamonds or the imposition of costly compliance procedures could have a material adverse effect on the Company's operations and/or financial condition and liquidity.

-14-

We have previously operated as a private company and have no experience in attempting to comply with U.S. public company obligations. In addition, we only recently began to reconcile our financial reports from Canadian GAAP to U.S. GAAP. Attempting to comply with these requirements will increase our costs and require additional management resources, and we still may fail to comply.

We only recently began to reconcile our financial statements from Canadian GAAP to U.S. GAAP. We expect to encounter substantial difficulty attracting qualified staff with requisite experience due to the high level of competition for experienced financial professionals. In the short term, we are providing training for our current full-time consultants with respect to U.S. GAAP. However, our training may not be effective. We will face increased legal, accounting, administrative and other costs and expenses as a public company that we did not incur as a private company. Compliance with the U.S. Sarbanes-Oxley Act of 2002, as well as other rules of the SEC, and the Public Company Accounting Oversight Board, will result in significant initial costs to us, as well as an ongoing increase in our legal, audit and financial compliance costs.

Because our directors, executive officers and other affiliates are among our largest stockholders, they can exert significant control over our business and affairs and have actual or potential interests that may depart from those of investors in the Offering.

Our Founders, directors, executive officers and their affiliates will own or control a significant percentage of the Common Shares following the completion of the Offering. They beneficially own an aggregate of 18,650,000 Common Shares (including 2,000,000 shares held by Peter Leger, our former President and CEO which the Board has authorized to be cancelled), representing 65% of the outstanding Common Shares. If the maximum Offering is completed our directors, executive officers and their affiliates will beneficially own approximately 57% of the outstanding Common Shares. These figures do not give effect to the exercise of Warrants offered hereby, any outstanding warrants, nor any increase in beneficial ownership that such persons may experience in the future upon vesting or other maturation of exercise rights under any of the options or warrants they may hold or in the future be granted or if they otherwise acquire additional Common Shares. The interests of such persons may differ from the interests of our other shareholders, including purchasers of Units in the Offering. As a result, in addition to their board seats and offices, such persons will have significant influence over and control all corporate actions requiring stockholder approval, irrespective of how the Company's other stockholders, including purchasers in the Offering, may vote, including the following actions:

· to elect or defeat the election of our directors;

· to amend or prevent amendment of our Articles of Incorporation or Bylaws;

· to effect or prevent a registration, sale of assets or other corporate transaction; and

· to control the outcome of any other matter submitted to our stockholders for vote.

Such persons' stock ownership may discourage a potential acquirer from making a tender offer or otherwise attempting to obtain control of the Company, which in turn could reduce our stock price or prevent our stockholders from realizing a premium over our stock price.

Because of the early stage of development and the nature of our business, our securities are considered highly speculative.

Our securities must be considered highly speculative, generally because of the nature of our business and the early stage of its development. We are engaged in the business of exploring natural resource properties. Accordingly, we have not generated any revenues nor have we realized a profit from our operations to date and there is little likelihood that we will generate any revenues or realize any profits in the near term. Any profitability in the future from our business will be dependent upon locating and exploring economic reserves of natural resources, which itself is subject to numerous risk factors as set forth herein. Since we have not generated any revenues, we will have to raise additional monies through the sale of our equity securities or debt in order to continue our business operations.

-15-

We are an exploration stage company, and there is no assurance that a commercially viable deposit or "reserve" of diamonds exists in the properties in which we have claim.

We are an exploration stage company and cannot assure you that a commercially viable deposit, or "reserve," exists in our properties. Therefore, determination of the existence of a reserve will depend on appropriate and sufficient exploration work and the evaluation of legal, economic and environmental factors. If we fail to find a commercially viable deposit our financial condition and results of operations will be materially adversely affected.

RISKS RELATING TO OUR COMMON SHARES AND POTENTIAL TRADING MARKET

Our Common Shares will be subject to the "Penny Stock" rules of the SEC and any potential trading market in our securities is limited, which makes transactions in our stock cumbersome and may reduce the value of an investment in our stock

The SEC has adopted regulations that generally define a "penny stock" to be any equity security other than a security excluded from such definition by Rule 3a51-1 under the Exchange Act. For the purposes relevant to our Company, it is any equity security that has a market price of less than $5.00 per share, subject to certain exceptions.

It is anticipated that our Common Shares will be regarded as a "penny stock", since our shares are not listed on a national securities exchange or quoted on Nasdaq within the United States, and to the extent the market price for its shares is less than $5.00 per share. The penny stock rules require a broker-dealer to deliver a standardized risk disclosure document prepared by the SEC, to provide the customer with additional information including current bid and offer quotations for the penny stock, the compensation of the broker-dealer and its salesperson in the transaction, monthly account statements showing the market value of each penny stock held in the customer's account, and to make a special written determination that the penny stock is a suitable investment for the purchaser and receive the purchaser's written agreement to the transaction. To the extent these requirements may be applicable they will reduce the level of trading activity in the secondary market for the Common Shares of the Company and may severely and adversely affect the ability of broker-dealers to sell the our Common Shares.

There is no current trading market for our securities and if a trading market does not develop, purchasers of our securities may have difficulty selling their shares.

There is currently no established public trading market for our securities and an active trading market in our securities may not develop or, if developed, may not be sustained. We intend to apply for quotation of our securities on the OTC Bulletin Board maintained by FINRA. If for any reason our Common Shares are not listed on the OTC Bulletin Board or a public trading market does not otherwise develop, purchasers of the Common Shares may have difficulty selling their shares should they desire to do so.

United States securities laws may limit secondary trading, which may restrict the states in which and conditions under which you can sell the shares offered by this prospectus.

Secondary trading in Common Shares sold in this offering will not be possible in any state in the U.S. unless and until the Common Shares are qualified for sale under the applicable securities laws of the state or there is confirmation that an exemption, such as listing in certain recognized securities manuals, is available for secondary trading in such state. The Company may not be successful in registering or qualifying the Common Shares for secondary trading, or identifying an available exemption for secondary trading in our Common Shares in every state. If we fail to register or qualify, or to obtain or verify an exemption for the secondary trading of, the Common Shares in any particular state, the Common Shares could not be offered or sold to, or purchased by, a resident of that state. In the event that a significant number of states refuse to permit secondary trading in our Common Shares, the market for the Common Shares could be adversely affected.

-16-

Since we are a "Foreign Private Issuer" under United States securities laws, our stockholders may have less complete and timely data about us.

We are considered a "foreign private issuer" under the Securities Act of 1933, as amended. As an issuer incorporated in the Province of Alberta, Canada we are exempt from Section 14 proxy rules and Section 16 of the Securities Exchange Act of 1934, as amended. The submission of proxy and annual meeting of stockholders information (prepared to Canadian standards) on Form 6-K and the exemption from Section 16 rules regarding sales of Common Shares by insiders may result in stockholders having less complete and timely data as compared to information that may be available about U.S. issuers.

We have not and do not intend to pay any cash dividends on our Common Shares, and consequently our stockholders will not be able to receive a return on their shares unless they sell them.

We intend to retain any future earnings to finance the development and expansion of our business. We have not, and do not, anticipate paying any cash dividends on our Common Shares in the foreseeable future. Unless we pay dividends, our stockholders will not be able to receive a return on their shares unless they sell them.

We may, in the future, issue additional Common Shares or other securities, including our Preferred Shares, which would reduce investors' percentage ownership and may dilute the value of our shares.

Our Articles of Incorporation authorize the issuance of an unlimited number of Common Shares without par value and an unlimited number of Preferred Shares without par value. The future issuance of our unlimited authorized Common Shares may result in substantial dilution in the percentage of our Common Shares held by our then existing shareholders. We may value any Common Shares issued in the future on an arbitrary basis. The issuance of Common Shares for future services or acquisitions or other corporate actions may have the effect of diluting the value of the Common Shares held by our investors, and might have an adverse effect on any trading market for our Common Shares.

Our Board of Directors may issue, without stockholder approval, Preferred Shares that have rights and preferences superior to those of Common Shares and that may delay or prevent a change of control. After the offering, there will be no Preferred Shares outstanding. However, our Board of Directors may set the rights and preferences of any class of Preferred Shares in its sole discretion without the approval of the holders of Common Shares. The rights and preferences of these Preferred Shares may be superior to those of the Common Shares. Accordingly, the issuance of Preferred Shares may adversely affect the rights of holders of Common Shares.

Following the effective date of this prospectus, we will become subject to the reporting requirements of federal securities laws, which can be expensive and may divert resources from other projects, thus impairing our ability grow.

As a result of this registration statement, we expect to become a public reporting company and, accordingly, subject to the information and reporting requirements of the Exchange Act and other federal securities laws, including compliance with the Sarbanes-Oxley Act of 2002, as described below. The costs of preparing and filing annual and quarterly reports, proxy statements and other information with the SEC and furnishing audited reports to stockholders would cause our expenses to be higher than they would be if we remained privately held. In addition, we will incur substantial expenses in connection with the requirement to register the Common Shares underlying the Warrants included in the Units and keep such Registration Statement effective.

Following the effective date of this prospectus, we will have to periodically evaluate our Internal Controls and Procedures and Management will have to report on the Internal Control Over Financial Reporting. If we fail to maintain an effective system of internal controls and procedures, we may not be able to accurately report our financial results and detect any fraud. This in turn could adversely affect our Business and the trading price of our stock.

Effective internal and disclosure controls are necessary for us to provide reliable financial reports and effectively prevent fraud and to operate successfully as a public company. If we cannot provide reliable financial reports or prevent fraud, our reputation and operating results would be harmed. We have in the past discovered, and may in the future discover, areas of our disclosure and internal controls that need improvement. As a result after a review of our December 2007 and 2008 operating results, we identified certain deficiencies in some of our disclosure controls and procedures.

-17-

We have undertaken improvements to our internal controls in an effort to remediate these deficiencies and comply with requirements and procedures as defined in Rules 13a-14 and 15(d)-15(e) of the Exchange Act, as amended. We cannot be certain that our efforts to improve our internal and disclosure controls will be successful or that we will be able to maintain adequate controls over our financial processes and reporting in the future. Any failure to develop or maintain effective controls or difficulties encountered in their implementation or other effective improvement of our internal and disclosure controls could harm our operating results or cause us to fail to meet our reporting obligations. If we are unable to adequately establish or improve our internal controls over financial reporting, our external auditors may not be able to issue an unqualified opinion on the effectiveness of our controls. Ineffective internal and disclosure controls could also cause investors to lose confidence in our reported financial information, which would likely have a negative effect on the trading price of our securities.

We can provide no assurance that our internal control over our financial reporting will be effective under Section 404 of the Sarbanes-Oxley Act of 2002. Establishing internal controls over our financial reporting, following the transition period for newly public companies, is likely to increase our costs.