Use these links to rapidly review the document

TABLE OF CONTENTS

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the Securities

Exchange Act of 1934 (Amendment No. )

| Filed by the Registrant | Filed by a Party other than the Registrant |

| | Check the appropriate box: | | ||||||

| Preliminary Proxy Statement | ||||||||

| CONFIDENTIAL, FOR USE OF THE COMMISSION ONLY (AS PERMITTED BY RULE 14a-6(e)(2)) | ||||||||

| Definitive Proxy Statement | ||||||||

| Definitive Additional Materials | ||||||||

| Soliciting Material under §.240.14a-12 | ||||||||

RMR Real Estate Income Fund

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

| | Payment of Filing Fee (Check the appropriate box): | | ||||||

| No fee required. | ||||||||

| Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | ||||||||

| | | | | | | | | |

| (1) Title of each class of securities to which transaction applies: | ||||||||

| | | | | | | | | |

| (2) Aggregate number of securities to which transaction applies: | ||||||||

| | | | | | | | | |

| (3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined) : | ||||||||

| | | | | | | | | |

| (4) Proposed maximum aggregate value of transaction: | ||||||||

| | | | | | | | | |

| (5) Total fee paid: | ||||||||

| Fee paid previously with preliminary materials. | ||||||||

| Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | ||||||||

| | | | | | | | | |

| (1) Amount Previously Paid: | ||||||||

| | | | | | | | | |

| (2) Form, Schedule or Registration Statement No.: | ||||||||

| | | | | | | | | |

| (3) Filing Party: | ||||||||

| | | | | | | | | |

| (4) Date Filed: | ||||||||

Notice of Special Meeting

of Shareholders and Proxy Statement

[Day of the Week], [Calendar date], 2020 at [ ] [a.][p.]m., Eastern Time

Two Newton Place, 255 Washington Street, Suite 100, Newton, Massachusetts 02458

LETTER TO OUR SHAREHOLDERS FROM OUR BOARD OF TRUSTEES

Dear Shareholder:

We invite you to a special meeting ("Special Meeting") of our shareholders in Newton, Massachusetts to consider a proposal to change our business from a registered investment company that makes equity investments in real estate companies to a real estate investment trust that will focus primarily on originating and investing in first mortgage whole loans secured by middle market and transitional commercial real estate. The enclosed Notice of Special Meeting and Proxy Statement provide you with important information about this proposal and our new business plan.

We believe that this proposal is the best path for our Company to increase shareholder value because it has the potential to increase the distributions we can pay to our shareholders in the future as well as the price at which our common shares trade relative to their net asset value.

Your support is very important. We encourage you to use telephone or internet methods, or sign and return a proxy card/voting instruction form, to authorize your proxy prior to the meeting so that your shares will be represented and voted at the meeting.

Thank you for being a shareholder and for your continued investment in our Company.

[ ], 20[19]

| Jennifer B. Clark John L. Harrington Joseph L. Morea Adam D. Portnoy Jeffrey P. Somers |

PRELIMINARY PROXY MATERIAL – SUBJECT TO COMPLETION

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

[Day of the Week], [Calendar date], 2020

[time], [a.m./p.m.], Eastern time

Two Newton Place, 255 Washington Street, Suite 100

Newton, Massachusetts 02458

ITEMS OF BUSINESS

- 1.

- To consider and vote upon a change in the Company's business from a registered investment company that makes equity investments in real estate companies to a real estate investment trust engaged in the business of originating and investing in first mortgage whole loans secured by middle market and transitional commercial real estate and to amend the Company's fundamental investment objectives and restrictions, and status as a "diversified" fund, to permit the Company to engage in its new business (the "Business Change Proposal"); and

- 2.

- To consider and vote upon the ratification of the Company's selection of RSM US LLP ("RSM") as the Company's independent registered public accounting firm ("Auditor Proposal").

RECORD DATE

You can vote if you were a shareholder of record as of the close of business on November 26, 2019.

PROXY VOTING

Shareholders as of the record date are invited to attend the Special Meeting. If you cannot attend in person, please vote in advance of the Special Meeting by using one of the methods described in the accompanying Proxy Statement.

[Calendar date], 20[19]

Newton, Massachusetts

By Order of the Board of Trustees,![]()

Jennifer B. Clark

Secretary

Please sign and return the proxy card or voting instruction form or use telephone or internet methods to authorize a proxy in advance of the Special Meeting. See the "Voting Information" section on page 28 for information about how to authorize a proxy by telephone or internet or how to attend the Special Meeting and vote your shares in person.

TABLE OF CONTENTS

| | Page | |||

|---|---|---|---|---|

PLEASE VOTE | 1 | |||

PROXY STATEMENT | 2 | |||

QUESTIONS & ANSWERS ABOUT THE PROXY MATERIALS AND VOTING | 3 | |||

BUSINESS CHANGE PROPOSAL | 6 | |||

Introduction | 6 | |||

Reasons for the Proposed Change | 6 | |||

Implementation of the Business Change Proposal and Related Risks | 12 | |||

Operation as a Mortgage REIT | 17 | |||

U.S. Federal Income Tax Considerations of the Company's Conversion to a REIT | 25 | |||

Taxation of the Company as a REIT | 25 | |||

AUDITOR PROPOSAL | 27 | |||

VOTING INFORMATION | 30 | |||

Required Vote | 30 | |||

Record Date | 30 | |||

Voting Methods | 30 | |||

Quorum, Abstentions and Broker Non-Votes | 31 | |||

Adjournments | 31 | |||

Revocation of Proxy | 31 | |||

SOLICITATION OF PROXIES | 32 | |||

COMMUNICATIONS WITH TRUSTEES | 32 | |||

SHAREHOLDER NOMINATIONS AND PROPOSALS | 32 | |||

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS | 34 | |||

DIRECTORS AND OFFICERS OF THE ADVISOR | 35 | |||

HOUSEHOLDING OF MEETING MATERIALS | 35 | |||

OTHER MATTERS | 36 | |||

APPENDIX A: Current CRE Market and Market Opportunity | A-1 | |||

APPENDIX B: Risk Factors | B-1 | |||

APPENDIX C: Summary of Material United States Federal Income Tax Considerations | C-1 | |||

PLEASE VOTE

It is very important that you vote on the future direction of our Company. The NYSE American LLC ("NYSE American") rules do not allow a broker, bank or other nominee who holds shares on your behalf to vote on the Business Change Proposal described below without your instructions.

PROPOSALS THAT REQUIRE YOUR VOTE

| PROPOSAL | MORE INFORMATION | BOARD RECOMMENDATION | CLASS OF SHARES VOTING | |||||

|---|---|---|---|---|---|---|---|---|

| | | | | | | | | |

| 1 | Business Change Proposal | Page 6 | FOR | Common shares and preferred shares of the Company, voting together as a single class, and preferred shares of the Company, voting as a separate class | ||||

2 | Auditor Proposal | Page 25 | FOR | Common shares and preferred shares of the Company, voting together as a single class | ||||

| | | | | | | | | |

You can vote in advance in one of three ways:

via the internet  | Visitwww.proxyvote.com and enter your 16 digit control number provided in your Notice Regarding the Availability of Proxy Materials, proxy card or voting instruction form before 11:59 p.m., Eastern time, on [Calendar Date], 2020 to authorize a proxyVIA THE INTERNET. | |

by phone | Call [ ] if you are a shareholder of record and [ ] if you are a beneficial owner before 11:59 p.m., Eastern time, on [Calendar Date], 2020 to authorize a proxyBY TELEPHONE. You will need the 16 digit control number provided on your Notice Regarding the Availability of Proxy Materials, proxy card or voting instruction form. | |

by mail  | Sign, date and return your proxy card if you are a shareholder of record or voting instruction form if you are a beneficial owner to authorize a proxyBY MAIL. |

If the meeting is postponed or adjourned, these times will be extended to 11:59 p.m., Eastern time, on the day before the reconvened meeting.

PLEASE VISIT:www.proxyvote.com

- •

- To review and download easy to read versions of our Proxy Statement.

- •

- To sign up for future electronic delivery to reduce the impact on the environment.

RMR Real Estate Income Fund ![]() 2019 Proxy Statement 1

2019 Proxy Statement 1

PRELIMINARY PROXY MATERIAL—SUBJECT TO COMPLETION

[Calendar Date], 20[19]

The Board of Trustees (the "Board") of the RMR Real Estate Income Fund, a Maryland statutory trust (the "Company," "we," "us," or "our"), is furnishing this proxy statement and accompanying proxy card (or voting instruction form) to you in connection with the solicitation of proxies by the Board for a special meeting of our shareholders. The meeting will be held at Two Newton Place, 255 Washington Street, Suite 100, Newton, Massachusetts 02458, on [ ], [ ], 2020, at [ ] [a.][p.]m., Eastern time, and any adjournment or postponements thereof (the "Meeting"). We are first making these proxy materials available to shareholders on or about [Calendar date], 20[19].

Only owners of record of common shares, par value $0.001 per share, and preferred shares, par value $0.001 per share, as of the close of business on November 26, 2019 (the "Record Date") are entitled to notice of, and to vote at, the meeting and at any postponements or adjournments thereof. Holders of common shares are entitled to one vote for each common share. Holders of preferred shares are entitled to one vote for each preferred share. On November 26, 2019, there were 10,202,009 common shares and 667 preferred shares issued and outstanding.

We will furnish, without charge, a copy of our annual report and most recent semi-annual report succeeding the annual report, if any, to any shareholder upon request. Requests should be directed to the Secretary of the Company at Two Newton Place, 255 Washington Street, Suite 300, Newton, Massachusetts 02458 (toll free telephone number (866) 790-8165). Copies can also be obtained by visiting our website at www.rmrfunds.com.1 Copies of our annual and semi-annual reports are also available on the EDGAR Database on the Securities and Exchange Commission's (the "SEC") website at www.sec.gov.

The mailing address of our principal executive offices is Two Newton Place, 255 Washington Street, Suite 300, Newton, Massachusetts 02548.

IMPORTANT NOTICE REGARDING THE AVAILABILITY OF PROXY MATERIALS

FOR THE SPECIAL MEETING TO BE HELD ON [DAY OF THE WEEK], [CALENDAR DATE], 2020.

THE NOTICE OF SPECIAL MEETING AND PROXY STATEMENT ARE AVAILABLE AT: WWW.PROXYVOTE.COM.

- 1

- Our Internet address is included in this proxy statement as a textual reference only. The information on the website is not incorporated by reference into this proxy statement.

2 RMR Real Estate Income Fund ![]() 2019 Proxy Statement

2019 Proxy Statement

QUESTIONS & ANSWERS ABOUT THE PROXY MATERIALS AND VOTING

1. ON WHAT PROPOSALS AM I BEING ASKED TO VOTE? |

You are being asked to consider and vote upon two proposals:

- •

- To approve changing our business from a registered investment company to a real estate investment trust, which we sometimes refer to as a "REIT." We refer to this proposal as the "Business Change Proposal" in the proxy materials.

If the Business Change Proposal is approved, we will change our business from a registered investment company that invests in equity securities issued by real estate companies to a REIT that will focus primarily on originating and investing in first mortgage whole loans, generally of $50.0 million or less, secured by middle market and transitional commercial real estate ("CRE"). In connection with this change to our business, we would amend our fundamental investment objectives and restrictions regarding purchasing and selling real estate and originating loans, as well as our status as a "diversified" fund, to allow us to engage in our new business as a mortgage REIT.

- •

- To ratify the appointment of RSM US LLP ("RSM") as our independent registered public accounting firm. We refer to this proposal as the "Auditor Proposal" in the proxy materials.

2. HOW DOES THE BOARD RECOMMEND THAT I VOTE? |

The Board unanimously recommends that you vote:

- •

- "FOR" the Business Change Proposal and

- •

- "FOR" the Auditor Proposal

3. WHY IS THE BOARD RECOMMENDING THE BUSINESS CHANGE PROPOSAL? |

The Board, including the members of the Board who are not interested persons (as defined in the Investment Company Act of 1940 (the "1940 Act")) of the Company (the "Independent Trustees"), believes that the Business Change Proposal is in the best interest of shareholders because it is the best path for our Company to increase shareholder value because it has the potential to increase the distributions we can pay to our shareholders in the future as well as the price at which our common shares trade relative to their net asset value ("NAV"). Over the course of many years, the Board has considered and implemented various strategies for increasing value for our shareholders. For a discussion of the principal considerations taken into account by the Board and a special committee (the "Special Committee") of the Board comprised of all the Independent Trustees, and a discussion of the potential risks in implementing the Business Change Proposal, see "Business Change Proposal—Reasons for the Proposed Change" and Appendix B.

4. IF THE BUSINESS CHANGE PROPOSAL IS APPROVED, WHAT WILL THE COMPANY DO TO IMPLEMENT THE PROPOSAL? |

If the Business Change Proposal is approved by shareholders, we will apply to the SEC for an order under the 1940 Act declaring that we have ceased to be a registered investment company (the "Deregistration Order"). Pending the SEC's issuance of the Deregistration Order, we intend to begin

RMR Real Estate Income Fund ![]() 2019 Proxy Statement 3

2019 Proxy Statement 3

realigning our portfolio consistent with our new business as a mortgage REIT. We anticipate that the implementation period may last approximately two years, with full implementation not projected until approximately the beginning of 2022. This time period is an estimate and may vary depending upon the length of the deregistration process with the SEC, tax considerations and the pace at which we will be able to originate or invest in first mortgage whole loans.

5. DOES OUR ADVISOR HAVE EXPERIENCE IN MANAGING A MORTGAGE REIT? WILL THERE BE ANY CHANGES TO THE COMPANY'S INVESTMENT ADVISORY AGREEMENT IN CONNECTION WITH THE BUSINESS CHANGE PROPOSAL? |

Our investment adviser, RMR Advisors LLC (the "Advisor"), and its affiliates have significant experience and expertise in managing REITs and in investing in middle market CRE. An affiliate of our Advisor currently manages a mortgage REIT, and we expect that the same personnel that conduct the business of that mortgage REIT would conduct our business if the Business Change Proposal is approved.

After we receive the Deregistration Order, our investment advisory agreement with our Advisor would be terminated. Our existing management fee is lower than the typical management fee for mortgage REITs. As a result, we expect to receive the benefit of establishing a portfolio of mortgage loans at a cost lower than would otherwise be expected to apply to a newly established mortgage REIT.

After deregistration, the Board anticipates we would enter into a new management agreement with our Advisor or an affiliate of our Advisor, who would continue to provide the day-to-day management of our operations, subject to the oversight and direction of the Board. While management fee expenses, as well as other operating expenses, are projected to increase as the Business Change Proposal becomes fully implemented following receipt of the Deregistration Order, these expenses are projected to be offset by higher projected income, resulting in higher projected net income per common share (thus supporting a potentially higher distribution rate in the long term) than without the implementation of the Business Change Proposal.

6. WHAT WILL HAPPEN TO THE COMPANY'S DIVIDEND IF THE BUSINESS CHANGE PROPOSAL IS APPROVED? |

During the transition period before our portfolio has been fully converted to its new investment strategy, we intend to try to maintain a quarterly managed distribution rate as high as is reasonably practicable. However, at some point during the implementation of the Business Change Proposal, the Board likely will need to temporarily reduce the managed distribution rate because we expect our cash flow from earnings and the status and availability of capital gains we realize from our portfolio to decline during the transition.

The full implementation of the Business Change Proposal, however, is anticipated to have a positive impact on the sustainability and potential growth of our earnings and distribution rate over the long term. We believe that, over the long term, our new investment strategies could result in our increasing cash flow from earnings, which could result in higher distributions to shareholders compared to historical levels, enhanced coverage for our distribution rate, the potential for share price appreciation, and/or the potential for narrowing or eliminating the discount at which our common shares historically have traded relative to their NAV.

7. WHAT ARE THE TAX CONSEQUENCES OF IMPLEMENTING THE BUSINESS CHANGE PROPOSAL? |

We have elected to be treated and currently operate in a manner intended to qualify for taxation as a "regulated investment company" ("RIC") under the Internal Revenue Code of 1986, as amended (the "IRC"). Assuming we deregister as an investment company under the 1940 Act as a result of the

4 RMR Real Estate Income Fund ![]() 2019 Proxy Statement

2019 Proxy Statement

Business Change Proposal, our qualification for taxation as a RIC would terminate for the taxable year in which the Deregistration Order becomes effective (the "Deregistration Year") and we intend to elect to be taxed as a REIT under the IRC commencing with the Deregistration Year and in subsequent taxable years. See Appendix C for a detailed discussion of the tax consequences of implementing the Business Change Proposal.

Once the Business Change Proposal is fully implemented, we intend to make quarterly distributions to our shareholders in amounts that will, at a minimum, enable us to comply with the REIT provisions of the IRC that require annual distributions of at least 90% of our REIT taxable income (other than net capital gains). The actual amount of such distributions will be determined on a quarterly basis by the Board, taking into account the REIT tax requirements, our cash needs, our earnings, the market price of our common shares and other factors the Board considers relevant.

8. WHAT IS THE ESTIMATED COST ASSOCIATED WITH THE BUSINESS CHANGE PROPOSAL? WHO WILL BEAR THE COSTS AND EXPENSES ASSOCIATED WITH THE BUSINESS CHANGE PROPOSAL? |

We estimate that the third party costs and expenses associated with consideration and approval of the Business Change Proposal will be approximately $[ ]. All third party costs and expenses associated with the Business Change Proposal will be paid by our Advisor and not the Company.

9. WILL MY VOTE MAKE A DIFFERENCE? |

YES! Your vote is important to ensure that the proposals are adopted. We encourage all shareholders to participate in the governance of the Company.

10. WHAT WILL HAPPEN IF SHAREHOLDERS DO NOT APPROVE THE BUSINESS CHANGE PROPOSAL? |

If the Business Change Proposal is not approved, the Board may consider other options to enhance or preserve shareholder value, including continuing our current operation as a registered investment company.

11. HOW CAN I AUTHORIZE A PROXY TO VOTE MY SHARES? |

Please follow the instructions included on the enclosed proxy card.

12. WHOM DO I CALL IF I HAVE QUESTIONS REGARDING THE PROXY? |

You may contact our proxy solicitor:

Morrow Sodali LLC

470 West Avenue

Stamford, Connecticut 06902

Shareholders Call Toll Free: (800) 662-5200

Banks and Brokers Call Collect: (203) 658-9400

RMR Real Estate Income Fund ![]() 2019 Proxy Statement 5

2019 Proxy Statement 5

The Board, including the Independent Trustees, recommends that we change our business from a registered investment company that invests in securities issued by real estate companies to a company that will focus primarily on originating and investing in first mortgage whole loans, generally of $50.0 million or less, secured by middle market and transitional CRE. We define middle market CRE as commercial properties that have values of up to $75.0 million and transitional CRE as commercial properties subject to redevelopment or repositioning activities that are expected to increase the value of the properties. The changed business will seek to qualify for taxation as a REIT for U.S. federal income tax purposes. To permit us to engage in our new business, our fundamental investment restrictions regarding purchasing and selling real estate and originating loans, as well as our fundamental investment objectives and status as a "diversified" fund, would be amended to allow us to engage in our business as a mortgage REIT.

The Board believes that, over the long term, the Business Change Proposal would result in our increasing cash flow from earnings, which could result in higher distributions to shareholders compared to historical levels, enhanced coverage for our distribution rate, the potential for share price appreciation, and/or the potential for narrowing or eliminating the discount at which our common shares historically have traded relative to their NAV. Over the course of many years, the Board has considered and implemented various other strategies to increase shareholder value with disappointing results. For a variety of reasons discussed below, the Board believes that the Business Change Proposal is a better long term business strategy and is more likely to increase shareholder value than continuing to operate as a registered investment company.The Board has unanimously recommended that shareholders vote "FOR" the Business Change Proposal.

Set forth below is a summary of the Special Committee's and the Board's considerations in approving the Business Change Proposal.

Following preliminary discussion of the Business Change Proposal with some of the Independent Trustees, our Advisor formally presented the Business Change Proposal to the Board at a meeting on August 5, 2019. At that meeting, the Board formed the Special Committee to consider and make findings with respect to the Business Change Proposal and to report to the full Board on its deliberations, findings and recommendations. The Special Committee appointed Mr. Jeffrey Somers, Esq., to serve as its chair, given his prior experience as a 1940 Act attorney and service as special counsel to the Independent Trustees prior to becoming a member of the Board. The Special Committee and the Board reached their decision to unanimously recommend the Business Change Proposal after approximately four months of consideration, discussions and deliberations, during which the Special Committee met on eight occasions.

The Special Committee reviewed materials prepared by our Advisor relating to the Business Change Proposal, our investment objectives, strategies, and restrictions, the types of investments we intend to make if the Business Change Proposal is approved, the risk and return characteristics of those investments, projected income and expenses anticipated to be associated with implementing the Business Change Proposal and associated with operating as a mortgage REIT and related matters. These materials generally compared our business and prospects both with and without implementing the Business Change Proposal, and the Special Committee discussed these matters extensively with our Advisor. The Special Committee also engaged an independent financial consultant (the "Consultant") with experience in the investment management and REIT industries to assist the Special Committee in evaluating the Business Change Proposal. The Consultant prepared a report evaluating the commercial mortgage REIT industry and the anticipated broader impact of the implementation of the Business Change Proposal on the Company, including on our operations and performance. The Consultant's report also addressed perceived market and economic trends and their anticipated impact on the Company both with

6 RMR Real Estate Income Fund ![]() 2019 Proxy Statement

2019 Proxy Statement

and without the implementation of the Business Change Proposal. In the course of reviewing the report, together with information provided by our Advisor, and meeting in person with the Consultant and our Advisor, the Special Committee posed additional questions, requested additional information and financial projections from our Advisor and met separately in executive sessions to discuss the Business Change Proposal. During the course of its evaluation, the Special Committee also consulted with our Advisor and our legal counsel. At a Board meeting held on October 29, 2019, the Special Committee and the Board further discussed the Business Change Proposal and the Special Committee, after meeting in executive session, reported its findings to the full Board and unanimously recommended that the Board approve the Business Change Proposal and submit it to a vote of the Company's shareholders.

In reaching its decision to recommend the approval of the Business Change Proposal, the Special Committee, in consultation with the Consultant and our Advisor, considered various factors it deemed relevant, including, but not limited to, the following factors:

- •

- Our current and forecasted cash flow from earnings are not sufficient to support our current distribution rate over the long term without meaningful capital gains in the portfolio. While we currently have significant unrealized gains in our portfolio, these gains may be reduced or not be available as a result of changes in market or economic conditions and the Special Committee believes that reliance on the realization of such gains to support our distribution rate over the long term would not be prudent or in the best interests of us and our shareholders. We currently have a managed distribution policy that contemplates a distribution of $0.33 per common share on a quarterly basis. Our Advisor discussed with the Special Committee its view that, absent the Business Change Proposal, our distribution rate would need to be reduced in order to make our regular quarterly distributions sustainable over the long term. Our Advisor also discussed with the Special Committee its view that, at some point during the implementation of the Business Change Proposal if it is approved, the Board likely will need to temporarily reduce the managed distribution rate because we expect our cash flow from earnings and the status and availability of capital gains we realize from our portfolio to decline during the transition.

- •

- The Special Committee considered that, given the current phase of the real estate cycle, the current and projected interest rate environment and signs of a potentially declining economic environment, a debt-focused investment strategy (such as commercial mortgages) could provide us with a greater ability to generate returns for shareholders and could represent a more favorable risk-return tradeoff, as compared to investing in equity securities of companies engaged in real estate businesses. The Special Committee discussed the following advantages of a debt-focused investment strategy:

- o

- Debt is senior to equity and may offer lower risk of income volatility, particularly in a declining economic environment where common share distributions are likely the first income streams to come under pressure.

In considering the Business Change Proposal, the Special Committee noted its discussions with our Advisor and the Consultant regarding the anticipated positive impact that the implementation of the Business Change Proposal would have on the sustainability and potential growth of our earnings and distribution rate over the long term. The Special Committee in particular considered its evaluation that, over the long term, our new investment strategies could result in our increasing cash flow from earnings, which could result in higher distributions to shareholders compared to historical levels, enhanced coverage for our distribution rate, the potential for share price appreciation, and/or the potential for narrowing or eliminating the discount at which our common shares historically have traded relative to their NAV. The Special Committee also noted its view that, in light of the likely necessity of a reduction in the managed distribution rate at some point in 2020 with or without the approval of the Business Change Proposal, the Business Change Proposal would allow us to return to, or possibly exceed, the current distribution level once we have fully implemented our business plan as a mortgage REIT.

The Special Committee further considered that our Advisor has committed to pay all third party costs and expenses related to consideration and approval of the Business Change Proposal.

RMR Real Estate Income Fund ![]() 2019 Proxy Statement 7

2019 Proxy Statement 7

- o

- Debt service is a higher priority payment for a borrower compared to other expenses. Borrowers' principal and interest payments are paid first out of cash flows prior to any payments to equity security holders. Equity holders receive available cash flows, if any, after payment of debt service and property-related expenses and bear the risk of any cash shortfalls.

- o

- Decreases in property values first affect equity holders. In general, investing in mortgages and other real estate related debt better protects investors against declines in property values than real estate related equity investments. For example, CRE loan losses have historically only spiked during major financial crises, and CRE loans have generally performed well through both up and down economic cycles.

- •

- The Special Committee discussed trends in asset management noted by our Advisor and the Consultant, recognizing that passively managed funds have steadily gained market share while active managers have had increasing difficulty outperforming their indices. The Special Committee also discussed the total assets under management for passive funds, which was reported to have surpassed actively managed funds (such as the Company) in the United States in 2019. The Special Committee considered this indicator in light of the low level of trading volume in our shares and the discount at which the shares historically have traded from their NAV per share. The Special Committee also noted the net outflows for registered investment companies in the real estate sector generally in 2019 through August 2019, along with the greater net inflows for the commercial mortgage REIT sector during the first half of 2019. The Special Committee believes that these trends support the broader strategic rationale for the Business Change Proposal.

- •

- The Board assesses the Company's performance at each quarterly meeting. Over the last several years, the Board has reviewed reports from our Advisor noting that we have from time-to-time underperformed other closed-end funds investing in real estate companies, the MSCI U.S. REIT Total Return Index, our benchmark index, and the broader equity market generally. The Special Committee believes that the proposed change in strategy could lead to better competitive dynamics for us given the scalability of our Advisor's and its affiliates' broader real estate management and mortgage origination platform.

- •

- Shares of closed-end funds often trade in the marketplace at a discount to their NAV per share. This has been the case for our common shares, given that they have traded at a persistent discount to our NAV for the past several years, thus limiting our ability to raise capital to fund growth. The Board has been proactive in monitoring our discounts and has taken steps to attempt to narrow our discount, including, but not limited to, the following:

- o

- In 2008, the Board approved a plan to merge five closed-end funds managed by our Advisor into one new fund (i.e., the Company) in order to create a combined portfolio with greater assets, expense efficiencies, and increased average trading volume than those of any of the five funds individually.

- o

- In 2010, the Company, with the approval of the Board, adopted a Rule 10b5-1 Plan under the Securities Exchange Act of 1934 ("Exchange Act"), with a goal of, among other things, increasing liquidity for the Company's common shares.

- o

- In 2011, the Board approved a plan to merge the Company with Old RMR Real Estate Income Fund (formerly, RMR Asia Pacific Real Estate Fund) for reasons similar to the 2008 mergers.

The Special Committee noted that, notwithstanding these anticipated advantages, the particular nature of any economic downturns, recessions or financial crises, and issuer specific or asset class/property type specific credit risk could adversely impact the anticipated risk-return tradeoff for real estate related debt versus equity investing and lead to losses notwithstanding any perceived protection provided by investing in debt as opposed to equity.

8 RMR Real Estate Income Fund ![]() 2019 Proxy Statement

2019 Proxy Statement

- o

- In August 2017, the Board approved a rights offering in an attempt to provide increased liquidity for the Company's common shares and a larger asset base over which to spread the Company's fixed expenses and reduce the Company's discount.

- o

- Until May 2018, the Company engaged Destra Capital Investments LLC to provide the Company with secondary market support services in connection with the ongoing operation of the Company, including communicating with financial advisors that are representatives of broker-dealers and other financial intermediaries, with the NYSE American specialist for the Company's common shares, and with the closed end fund analyst community regarding the Company on a regular basis.

- o

- In February 2019, the Board approved a managed distribution plan (the "Managed Distribution Plan") that allows the Company to include long term capital gains, where applicable, as part of its regular fixed quarterly distribution to shareholders, with the belief that the receipt of a sizable and predictable distribution from the Company may result in a smaller discount to NAV over time.

- •

- As of November 30, 2019, we had approximately $367.3 million in total assets, approximately $262.0 million of which was attributable to our common shares. The Special Committee and our Advisor believe that our relatively small size may make it difficult for us to attract interest from institutional investors or market analysts and therefore may be an obstacle to enhancing our profile in the market and thus the market liquidity and trading prices of our common shares. Our relatively small size and large NAV discount also makes us vulnerable to the increasingly aggressive tactics of activist managers who employ abusive arbitrage strategies seeking short term profits that could adversely affect us and our long term shareholders. The Special Committee believes that the Business Change Proposal's potential for long term enhancement of our distribution rate and the price at which our common shares trade relative to their NAV could protect our long term shareholders from these vulnerabilities and preserve value for them, while at the same time improving market sentiment and recognition for us, which in turn could enhance the market liquidity of our common shares. Moreover, the Special Committee noted that, as a mortgage REIT and following receipt of the Deregistration Order, we would be able to use leverage in amounts in excess of that permitted by the 1940 Act, which may aid in supporting the long term enhancement of our earnings and distribution rate.

- •

- The Special Committee considered our Advisor's and its affiliates' ability to source mortgage origination opportunities and the likely timeline for transitioning our portfolio to mortgages. Our Advisor and the Special Committee discussed the continued market demand for alternative sources of CRE debt capital, including that the decrease in the number of, and availability of capital from, traditional CRE debt providers, such as banks and insurance companies, is a primary reason borrowers are seeking alternative sources of debt, particularly in transitional and middle market situations. The Special Committee noted that alternative CRE lenders generally are able to operate with fewer regulatory constraints than traditional CRE debt providers, such as banks and insurance companies, which allows alternative CRE lenders to create customized solutions to fit borrowers' specific business plans for the collateral properties. The Special Committee believes that this flexibility can afford us a competitive advantage over regulated

The Special Committee noted that despite these efforts, our common shares have continued to trade at a discount to NAV.

In evaluating mortgage REITs comparable to the strategy proposed for us, the Special Committee noted that these REITs often, though not always, traded at a premium to net asset value and considered the potential for the Business Change Proposal, in the long term, to act as a catalyst for providing shareholders with an improved likelihood of being able to trade their common shares at a price closer to, or perhaps even in excess of, NAV. In addition, the Special Committee noted the precedent of another registered investment company that deregistered and became a REIT and the impact of such conversion on the trading price of that fund, though the Special Committee also noted the different facts and circumstances applicable to that situation and that there could be no assurance that converting to a mortgage REIT would have a similar impact on the market price of our common shares.

RMR Real Estate Income Fund ![]() 2019 Proxy Statement 9

2019 Proxy Statement 9

- •

- The Special Committee considered the experience and qualifications of our Advisor's and its affiliates' personnel in managing REITs and whether our total assets were sufficient to allow us to successfully implement the Business Change Proposal. The Special Committee noted the substantial experience of our Advisor's personnel and its affiliates in the real estate management, REIT and mortgage origination businesses and the experience of our Advisor's personnel that would manage us if the Business Change Proposal is approved. The Special Committee concluded that our Advisor has the wherewithal to successfully implement the Business Change Proposal. The Special Committee also considered the performance and trading history of another mortgage REIT managed by an affiliate of our Advisor and that the same personnel that conduct the business of the other mortgage REIT are expected to conduct our business if the Business Change Proposal is approved. In considering the performance of the other mortgage REIT, the Special Committee believed that the other mortgage REIT's unfavorable performance and trading history were due to a slow initial pace of loan origination and some operational and personnel issues associated with its commencement of operations. The Special Committee considered the steps taken by our Advisor's affiliate to remedy such issues and considered the rate at which mortgage loans subsequently were originated, the quality of those loans and the changes to personnel that manage the other mortgage REIT. The Special Committee concluded, in light of the remedies implemented by our Advisor's affiliate, that the problems that affected the other mortgage REIT are not likely to be repeated in connection with our transition to a mortgage REIT, and that the potential long term benefits to us of implementing the Business Change Proposal outweigh the risk of poor performance by us.

- •

- The Special Committee considered that, if shareholders approve the Business Change Proposal and we receive the Deregistration Order, the Board at the time would take the necessary steps under Maryland law to reorganize the Company as a Maryland REIT. In this regard, the Special Committee noted that the Board would likely make changes to the Company's governing documents in advance of or in connection with such reorganization. The Special Committee recognized that any such changes and any such reorganization could be accomplished under Maryland law without shareholder approval and that it was likely that our Board would effectuate the Company's reorganization to a Maryland REIT following receipt of the Deregistration Order. The Special Committee considered that, when compared with the Maryland statutory trust form, the Maryland REIT form is more conducive to the operations of a REIT and provides the trustees and management of a REIT with greater certainty and predictability in managing our affairs. The Special Committee noted that the Maryland REIT Law was enacted for companies that elect to be taxed as a REIT under the IRC and has specific provisions for REITs, including (a) provisions that validate restrictions on the ownership and transfer of shares, which facilitate satisfaction of certain of the U.S. federal income tax requirements for qualification as a REIT, and (b) provisions that permit the issuance of shares to holders for the specific purpose of satisfying the U.S. federal income tax requirements for qualification as a REIT regarding share ownership. Moreover, the Special Committee considered that being governed by the Maryland REIT Law will bring our governance more in line with that of other REITs as a majority of publicly traded REITs are formed as Maryland REITs under the Maryland REIT Law or Maryland corporations. In addition, the Special Committee noted the Maryland REIT Law (a) offers additional protections in the event of an unsolicited takeover attempt, which may better protect shareholder interests, and (b) provides shareholders greater voting rights than are currently provided under the Maryland Statutory Trust Act and our governing documents.

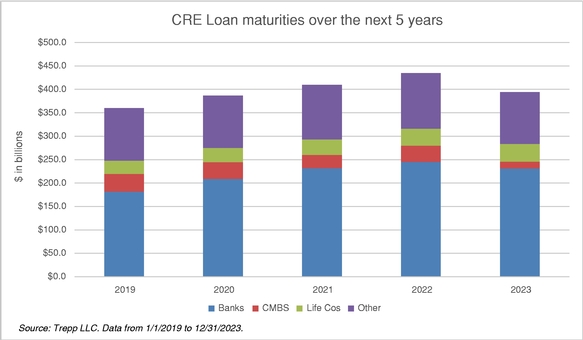

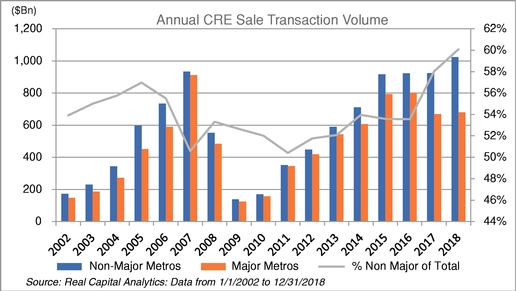

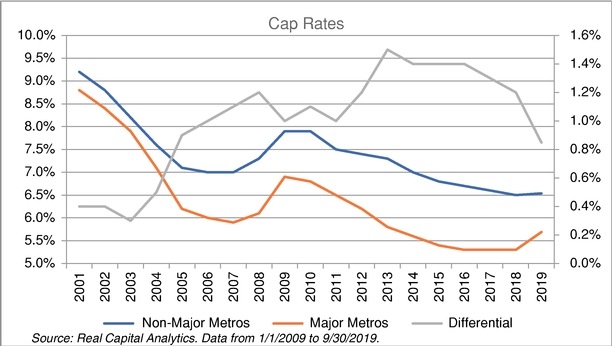

traditional CRE debt providers, especially with regard to transitional and middle market CRE debt financing. The Special Committee noted that our focus on providing debt financing for transitional and middle market CRE transactions will enable us to pursue investment opportunities that may offer superior risk adjusted investment returns as compared to more heavily regulated financial institutions and many other traditional CRE debt providers, who tend to focus on larger, more competitive markets. Our Advisor and the Special Committee also discussed the large volume of maturing CRE loans over the next five years and that the resulting need for borrowers to refinance assets is expected to provide an opportunity for originating CRE debt. A summary of the current CRE market is attached to this Proxy Statement as Appendix A.

10 RMR Real Estate Income Fund ![]() 2019 Proxy Statement

2019 Proxy Statement

- •

- The Special Committee considered that we would continue to be managed by our Advisor and noted the different management fee and expense structure that would apply to us as a mortgage REIT. The Special Committee noted that our existing management fee would remain in place until we obtain the Deregistration Order and that, during this transition period, our Advisor would be building our portfolio of mortgage loans. The Special Committee recognized that our existing management fee was lower than the typical management fee paid by mortgage REITs, and thus acknowledged that we were expected to receive the benefit of establishing a portfolio of mortgage loans at a cost lower than would otherwise be expected to apply to a newly established mortgage REIT. The Special Committee then considered that, while management fee expenses, as well as other operating expenses, were projected to increase as the Business Change Proposal became fully implemented following receipt of the Deregistration Order, these expenses were projected to be offset by higher projected income, resulting in higher projected net income per common share (thus supporting a potentially higher distribution rate in the long term) than without the implementation of the Business Change Proposal.

- •

- The Special Committee considered the impact to us of no longer being subject to regulation as a registered investment company under the 1940 Act. The Special Committee noted that the 1940 Act provides certain protections to shareholders that would no longer apply once we deregister under the 1940 Act. The Special Committee concluded that this result was appropriate given the differing nature of our business following the implementation of the Business Change Proposal as a type of business that Congress chose not to regulate under the 1940 Act. The Special Committee noted that the lack of 1940 Act regulation would permit us, post implementation of the Business Change Proposal, to compete with other similar mortgage REITs through the use of an appropriate amount of financial leverage for the business and through transacting with related parties without being subject to the restrictions of the 1940 Act. The Special Committee also noted that we would continue to be subject to Exchange Act reporting requirements and shareholders would continue to have the benefit of the significant regulatory protections provided by the corporate governance requirements of the NYSE American or another national securities exchange. See "—Implementation of the Business Change Proposal and Related Risks" and "—Operation as a Mortgage REIT."

- •

- The Special Committee considered the tax consequences of the Business Change Proposal, including that as a REIT, we expect to pay distributions to shareholders of at least 90% of our REIT taxable income (other than net capital gains). See "—U.S. Federal Income Tax Considerations of the Company's Conversion to a REIT" and Appendix C.

The Special Committee recognized that if the Company is unsuccessful in implementing the Business Change Proposal, the anticipated benefits of the Business Change Proposal may not be realized. The Special Committee also recognized that, based on projections, there would be an extended implementation period for the Business Change Proposal because of the anticipated length of time to obtain the Deregistration Order and the timing of becoming a REIT which may be impacted by tax considerations. This implementation period may last approximately two years, with full implementation not projected until approximately the beginning of 2022. The Special Committee noted that this time period was an estimate and may vary depending upon the length of the deregistration process with the SEC, tax considerations and the pipeline of mortgage origination opportunities. The Special Committee considered that, during this implementation period, the anticipated benefits of the Business Change Proposal, financial and otherwise, would not be realized or would only be realized to a lesser extent, and that during this period the Board likely will need to temporarily reduce the managed distribution rate, we may not maintain a comparable level of income, expenses may increase as a percentage of net assets, our common share price may exhibit increased volatility and a greater discount to NAV and we may be more vulnerable to activist closed-end fund investor activity. The Special Committee believes that the risk of these temporary disruptions is outweighed by the potential benefits of the Business Change Proposal upon its full implementation. The Special Committee in particular noted that our Advisor has committed to pay all third party costs and expenses related to consideration and approval of the Business Change Proposal.

RMR Real Estate Income Fund ![]() 2019 Proxy Statement 11

2019 Proxy Statement 11

- •

- The Special Committee took into account potential risks associated with implementing the Business Change Proposal, including those discussed in Appendix B.

In determining to approve the Business Change Proposal, the Board took into account the findings and recommendations of the Special Committee. The Board did not identify any particular factor as determinative, and each Trustee attributed different weights to the various factors. These factors were also considered by the Independent Trustees meeting separately from the full Board both with and without Company counsel. Following review and discussions with our Advisor and Company counsel, the Board, including the Independent Trustees, unanimously determined that the Business Change Proposal is advisable and in the best interests of us and our shareholders. On October 29, 2019, the Board, including the Independent Trustees, accepted the recommendations, findings and considerations of the Special Committee and unanimously approved the Business Change Proposal and directed that the Business Change Proposal be submitted for consideration by our shareholders. If shareholders do not approve the Business Change Proposal, the Board may consider other options to enhance or preserve shareholder value, including continuing our current operation as a registered investment company.

THE BOARD, INCLUDING THE INDEPENDENT TRUSTEES, UNANIMOUSLY RECOMMENDS THAT SHAREHOLDERS VOTE "FOR" THE BUSINESS CHANGE PROPOSAL.

Realignment of Portfolio and Deregistration. If the Business Change Proposal is approved by shareholders, we will begin to realign our portfolio so that we can rely on an exclusion from regulation under the 1940 Act available to companies primarily engaged in a real estate business and will apply to the SEC for a Deregistration Order. We intend to accomplish this by selling our existing investments as and when necessary to fund mortgage origination opportunities and/or by selling our existing investments and potentially temporarily holding liquid real estate assets, such as agency whole pool certificates, pending mortgage origination opportunities. We may elect to pursue one or both of these options at any given point in time depending upon a variety of factors, including the timing of receipt of the Deregistration Order, economic conditions, desired common share distribution level, and the availability of leverage facilities on acceptable terms, among others. The issuance of the Deregistration Order by the SEC is not within our control, and we anticipate that it may take a year or longer from the date of filing of the application to obtain the Deregistration Order. Until the SEC issues a Deregistration Order, we will continue to be registered as an investment company and will continue to be regulated under the 1940 Act.

Changes to Our Fundamental Investment Objectives and Restrictions. If the Business Change Proposal is approved, our fundamental investment objectives of earning and paying a high level of current income to common shareholders, with capital appreciation as a secondary objective, will be replaced with a non-fundamental primary objective to balance capital preservation with generating attractive risk adjusted returns. Additionally, if the Business Change Proposal is approved, our fundamental investment restrictions regarding purchasing and selling real estate and originating loans would be amended to permit us to engage in our new business strategy, as set forth below.

12 RMR Real Estate Income Fund ![]() 2019 Proxy Statement

2019 Proxy Statement

| Current Fundamental Restrictions | Fundamental Restrictions After Approval of Business Change Proposal But Before Deregistration | |

|---|---|---|

| | | |

| The Company may not purchase or sell real estate, except that the Company may invest in securities of companies that deal in real estate or are engaged in the real estate business, including REITs, and securities secured by real estate or such interests and the Company may hold and sell real estate or mortgages on real estate acquired through default, liquidation or other distributions of an interest in real estate as a result of the Company's ownership of such securities. | The Company may purchase or sell real estate, except to the extent that it would violate the 1940 Act. | |

The Company may not originate loans to other persons except by the lending of its securities, through the use of repurchase agreements and by the purchase of debt securities. | The Company may originate loans to other persons, except to the extent that it would violate the 1940 Act. | |

| | | |

Each of the amended policies would remain fundamental, as required by the 1940 Act, until we receive the Deregistration Order, at which time these policies (and other Company policies) could be changed by the Board without shareholder approval.

We currently have, and will retain until we receive the Deregistration Order, a fundamental investment policy to make investments that will result in concentration (25% or more of the value of our investments) in the securities of companies primarily engaged in the real estate industry and not in other industries; provided, however, this does not limit our investments in (i) U.S. Government obligations, or (ii) other obligations issued by governments or political subdivisions of governments. We note that for purposes of our investment policies and restrictions, we define a "real estate company" as an entity that derives at least 50% of its revenues from the ownership, leasing, management, construction, sale or financing of commercial, industrial or residential real estate, or has at least 50% of its assets in real estate, and we will consider agency whole pool certificates and other trusts that own mortgages or other interests in real estate to be real estate companies.

Changes to Our Non-Fundamental Investment Policies and Strategies. Our current non-fundamental investment policies and strategies provide that under normal market conditions, we invest:

- •

- at least 90% of our managed assets (consisting of the NAV of our common shares plus the liquidation preference of our preferred shares and the principal amount of our outstanding borrowings) ("Company Managed Assets") in income producing securities issued by real estate companies, including common shares, preferred shares and debt;

- •

- at least 75% of Company Managed Assets in securities issued by REITs;

- •

- no more than 10% of Company Managed Assets in securities denominated in currencies other than the U.S. dollar or traded on a non-U.S. stock exchange; and

- •

- at least 80% of Company Managed Assets in securities issued by real estate companies.

If the Business Change Proposal is approved, the foregoing policies and strategies will be replaced with the investment strategy described under "—Operation as a Mortgage REIT—Investment Strategy."

Change from "diversified" to "non-diversified" status. We currently operate as a "diversified" fund, which means that, with respect to 75% of our total assets, securities issued by a single company may not have a value greater than 5% of our total assets and we may not own more than 10% of the outstanding voting securities of the company. If the Business Change Proposal is approved, we will begin operating as a "non-diversified" investment company, which means we will no longer need to comply with the 1940 Act's diversification requirements. A non-diversified fund may invest a significant part or all of its investments in a small number of issuers. Having a larger percentage of assets in a smaller number of issuers makes a

RMR Real Estate Income Fund ![]() 2019 Proxy Statement 13

2019 Proxy Statement 13

non-diversified fund more susceptible to the risk that one single event or occurrence can have a significant adverse impact on the fund.

Investment Advisory Agreement. If the Business Change Proposal is approved, our current investment advisory agreement will remain in effect, including the existing investment advisory fee, until we receive the Deregistration Order. Under the terms of our investment advisory agreement, our Advisor provides us with an investment program, makes our day-to-day investment decisions and manages our business affairs in accordance with our investment objectives and policies, subject to the general supervision of the Board. As compensation for its services rendered and the related expenses borne by our Advisor, we pay our Advisor a monthly fee equal to an annual rate of 0.85% of our average daily managed assets. Our managed assets are equal to the NAV of our common shares plus the liquidation preference of our preferred shares and the principal amount of our outstanding borrowings. We may terminate the investment advisory agreement at any time without penalty by giving our Advisor sixty days' notice and paying any compensation earned prior to such termination, provided that such termination shall be directed or approved by the vote of a majority of our Trustees or by the vote of the holders of a "majority" (as defined in the 1940 Act) of our outstanding voting securities.

Following approval of the Business Change Proposal and receipt of the Deregistration Order, the Board anticipates that the existing agreement would be terminated and we would enter into a new management agreement with our Advisor or an affiliate of our Advisor, who would continue to provide for our day-to-day management, subject to the oversight and direction of our Board. See "—Operation as a Mortgage REIT—Terms of Management Agreement."

Distribution Policy. During the transition period before our portfolio has been fully converted to its new investment strategy, we intend to try to maintain a quarterly managed distribution rate as high as is reasonably practicable. However, there can be no assurance that we will not reduce our quarterly distributions during the investment strategy transition period, and the Board likely will need to temporarily reduce the managed distribution rate because we expect our cash flow from earnings and the status and availability of capital gains we realize from our portfolio to decline during the transition. This decline could result from the rotation out of existing investments, the need to establish income streams from mortgage originations, the potential for holding assets in temporary investments with lower yields such as agency whole pool certificates and the availability or unavailability of realized capital gains to distribute, among other potential variables. We anticipate distributing capital gains recognized on the sale of assets during this transition period, either as part of our quarterly distributions made pursuant to our Managed Distribution Plan, or at the end of the year in accordance with the requirements of subchapter M of the IRC.

The full implementation of the Business Change Proposal, however, is anticipated to have a positive impact on the sustainability and potential growth of our earnings and distribution rate over the long term. We believe that, over the long term, our new investment strategies could result in our increasing cash flow from earnings, which could result in higher distributions to shareholders compared to historical levels, enhanced coverage for our distribution rate, the potential for share price appreciation, and/or the potential for narrowing or eliminating the discount at which our common shares historically have traded relative to their NAV.

In the absence of the Business Change Proposal, our distribution rate would likely need to be reduced beginning in 2020 in order to make our regular quarterly distributions sustainable over the long term.

Auction Rate Preferred Shares and Credit Facility. If shareholders approve the Business Change Proposal, we intend to redeem our outstanding auction rate preferred shares and terminate our credit facility with BNP Paribas Prime Brokerage International, Ltd. We would seek to fund such redemptions and termination with a replacement credit facility designed for our new business as a mortgage REIT. See "—Operation as a Mortgage REIT—Policies and Investment Guidelines—Leverage Policies and Financing Strategy."

Change in Name. We expect to change our name to "RMR Mortgage Trust."

14 RMR Real Estate Income Fund ![]() 2019 Proxy Statement

2019 Proxy Statement

Effects of Deregistration. As a registered investment company, we are subject to extensive regulation under the 1940 Act. The 1940 Act, among other things,

- •

- regulates the composition of the Board, requiring that the Company be managed by a board of directors, at least 40% of whom are not "interested persons" of the Company, as defined in the 1940 Act;

- •

- requires that the Company's management agreement be approved by a majority of the directors who are not interested persons of the Company both initially and on an annual basis; the 1940 Act also generally requires that the Company's management agreement be approved initially by the Company's shareholders and that any material amendments to such agreement also be approved by the Company's shareholders;

- •

- provides shareholders with the right to terminate the management agreement;

- •

- restricts the extent to which the Company may utilize financial leverage; for every dollar of indebtedness outstanding, the Company is required to have at least three dollars of total assets and for every dollar of preferred shares outstanding, the Company is required to have at least two dollars of total assets);

- •

- limits the Company to issuing one class of indebtedness and one class of preferred shares; restricts the issuance of stock options, rights and warrants; prohibits the issuance of securities for services or for property other than cash or securities, except as a dividend or a distribution to security holders or in connection with a reorganization; restricts the sale of common shares at a price below NAV;

- •

- imposes restrictions on the Company's ability to engage in transactions with affiliated persons, including trustees and officers of the Company, our Advisor and its affiliates and other companies managed by our Advisor, unless such transactions are exempted by the SEC or a rule under the 1940 Act. These prohibitions generally apply to buying and selling securities and other property to or from affiliated persons; lending money to affiliated persons; or participating in joint transactions or profit sharing arrangements with affiliated persons;

- •

- regulates the form, content and frequency of financial reports to shareholders;

- •

- requires the Company to report its assets at their fair value rather than at cost in financial reports;

- •

- requires the Company to file periodic reports with the SEC designed for investment companies to disclose compliance with the 1940 Act and to present other financial information;

- •

- prohibits the Company from changing the nature of its business or fundamental investment objectives, policies and restrictions without the prior approval of its shareholders;

- •

- prohibits pyramiding of investment companies and the cross ownership of securities;

- •

- requires the Company to maintain its securities and other investments with certain types of custodians under conditions designed to assure the safety of the Company's assets;

- •

- provides for the bonding of certain employees;

- •

- requires the Company to have a written code of ethics and compliance policies and procedures designed to prevent violations of federal securities laws and a chief compliance officer charged with administering these policies;

- •

- regulates the manner in which repurchases of shares may be effected;

- •

- regulates plans of reorganization, including mergers with affiliates;

- •

- prohibits the Company from limiting the liability of any trustee and officer for willful misfeasance, bad faith, gross negligence or reckless regard of the duties involved in the conduct of his or her office; and

- •

- creates a right in private persons to bring actions in Federal courts to enforce compliance with certain, limited provisions of the 1940 Act.

RMR Real Estate Income Fund ![]() 2019 Proxy Statement 15

2019 Proxy Statement 15

After we receive a Deregistration Order, we will no longer be subject to regulations under the 1940 Act. Instead, as a mortgage REIT, we would be able to, among other things:

- •

- enter into a new management agreement with our Advisor without shareholder approval or change the management agreement;

- •

- shareholders will not have the right to require us to terminate the management agreement;

- •

- employ both direct and structural leverage on our mortgage loan investments in amounts in excess of what the 1940 Act permits;

- •

- issue multiple classes of indebtedness and capital stock, including multiple classes of common and preferred stock with different rights, preferences and privileges, and multiple classes of debt with varying terms, seniority and security interests;

- •

- issue stock options, rights and warrants for services or for property in addition to cash or securities, and may sell shares at a price below net asset value;

- •

- engage in transactions involving affiliated persons;

- •

- change our investment restrictions and policies without shareholder approval and without being subject to any regulatory restrictions under the 1940 Act; and

- •

- maintain our securities and other investments as we believe would be appropriate without being subject to any custody restrictions under the 1940 Act.

However, we would be regulated by, among other laws, the Exchange Act, which regulates, among other things:

- •

- soliciting proxies from shareholders;

- •

- filing interim and annual reports with the SEC, including annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K;

- •

- filing securities ownership reports by directors, officers and principal shareholders; and

- •

- restrictions on engaging in insider trading in securities, using manipulative devices in connection with certain security transactions, and making misleading statements in reports or documents filed with the SEC.

After we receive the Deregistration Order, we will continue to be managed by our Board and our officers. The Board will maintain substantially similar power, authority and discretion as the Board has before deregistration and be subject to the same duties under state law. Shareholders would also continue to have the benefit of the significant regulatory protections provided by the corporate governance requirements of the NYSE American or another national securities exchange, including those that require that a majority of the trustees be "independent directors" (as defined under NYSE American or other applicable exchange rules), trustee nominations and the compensation of all of our executive officers be subject to independent director approval, and that we hold an annual meeting of shareholders no later than one year after our first fiscal year following listing. In addition, consistent with the requirements of the NYSE American or another national securities exchange, we intend to adopt a code of conduct and ethics applicable to all trustees, officers and employees and retain the position of Director of Internal Audit, which is currently occupied by the individual who is also the Company's chief compliance officer.

Because the regulatory requirements specifically applicable to financial statements of registered investment companies would no longer be applicable to the Company, the financial information in our financial statements after we receive the Deregistration Order will change. For example, once we are no longer an investment company, we will no longer be required to present a schedule of portfolio of investments as part of our financial statements or report investments at fair value.

16 RMR Real Estate Income Fund ![]() 2019 Proxy Statement

2019 Proxy Statement

Reorganization to a Maryland REIT. As a holder of our common shares, your rights are governed by the Maryland Statutory Trust Act and our organizational documents. Because Maryland has a statutory scheme specifically designed for REITs, we expect that the Board will take the necessary steps under Maryland law to reorganize the Company as a Maryland REIT following our receipt of the Deregistration Order and make changes to the Company's governing documents in advance of or in connection with such reorganization. Any such changes and any such reorganization can be accomplished under Maryland law without shareholder approval. If we reorganize as a Maryland REIT, your rights as a holder of common shares of the Company will be governed by the Maryland REIT Law and by any amended organizational documents adopted by the Board at that time.

There are several differences between the Maryland Statutory Trust Act and the Maryland REIT Law that you should consider. The default provisions of the Maryland Statutory Trust Act may generally be altered in the declaration of trust or bylaws of a Maryland statutory trust, including provisions relating to shareholders' rights, preferences and privileges. The Maryland REIT Law is a more structured statutory framework that provides shareholders greater voting and other rights that may not be modified to the same extent as permitted under the Maryland Statutory Trust Act. For example:

- •

- Under the Maryland Statutory Trust Act, the declaration of trust or bylaws of a Maryland statutory trust may limit or eliminate shareholder voting rights with respect to the election and removal of trustees, mergers, conversions and amendments to the declaration of trust. Under the Maryland REIT Law, shareholders are entitled to vote on the election and removal of trustees and a Maryland REIT generally may not amend its declaration of trust, merge or convert without shareholder approval.

- •

- The Maryland Statutory Trust Act and the Maryland REIT Law both provide for duties of trustees that are analogous to those of directors of a Maryland corporation. However, under the Maryland Statutory Trust Act, the statutory duties of trustees may be modified or limited in the declaration of trust or bylaws, provided that the duty to act in good faith may not be eliminated. Under the Maryland REIT Law, the statutory duties of trustees may not be modified or limited by provisions in the declaration of trust or bylaws.

- •

- The Maryland Statutory Trust Act, unlike the Maryland REIT Law, does not expressly (i) limit the ability of a Maryland statutory trust to indemnify its trustees and officers for certain actions or (ii) permit a Maryland statutory trust to adopt statutory takeover defenses, including provisions related to business combinations and the ability of the board to self-classify.

See Appendix B for more information on the risks associated with the Business Change Proposal.

The following discussion assumes that, unless otherwise noted, the Business Change Proposal has been approved by shareholders and we have fully implemented the Business Change Proposal, reorganized as a mortgage REIT and received the Deregistration Order. See Appendix B for more information on the risks associated with the Business Change Proposal.

Investment Strategy

As a mortgage REIT, our primary investment objective will be to balance capital preservation with generating attractive risk adjusted returns. We will seek to achieve this objective by primarily investing in first mortgage whole loans secured by middle market and transitional CRE. The first mortgage loans in which we plan to invest will generally have the following characteristics:

- •

- principal balances of less than $50.0 million;

- •

- stabilized LTV ratios of 75% or less;

- •

- terms of five years or less;

- •

- floating interest rates based on LIBOR (or other applicable benchmark interest rate index) plus spreads of 275 to 400 basis points;

RMR Real Estate Income Fund ![]() 2019 Proxy Statement 17

2019 Proxy Statement 17

- •

- non-recourse to sponsors (subject to customary non-recourse carve-out guarantees) and secured by middle market and transitional CRE across the United States; and

- •

- equity owned by well capitalized sponsors with experience investing in the relevant real estate property type.

We will invest in first mortgage whole loans that provide bridge financing on transitional CRE properties. These investments will typically be secured by properties undergoing redevelopment or repositioning activities that are expected to increase the value of the properties. We will fund these loans over time as the borrowers' business plans for the properties are carried out. Our loans secured by transitional CRE will typically be bridge loans that are usually refinanced, with the proceeds from other CRE mortgage loans or property sales. We expect to receive origination fees, extension fees, modification or similar fees in connection with our bridge loans. Bridge loans may lead to future investment opportunities for us, including takeout mortgage loans with the same borrowers and properties.

Our Advisor and the Board believe that our mortgage investment strategy is appropriate for the current market environment. However, to capitalize on investment opportunities at different times in the economic and CRE investment cycle, we may change our investment strategy from time to time. Our Advisor and the Board believe that the flexibility of our investment strategy and the experience and resources of our Advisor and its affiliates, will allow us to take advantage of changing market conditions to preserve capital and generate attractive risk adjusted returns on its investments. The Board will be able to modify such strategies without the consent of the shareholders to the extent that the Board determines that such modification is in our best interest.

Policies and Investment Guidelines

If the Business Change Proposal is approved by shareholders, the Board will approve our operating and regulatory policies and investment guidelines. The Board currently anticipates adopting the policies and guidelines described below. The Board may, in its discretion, revise or waive such policies and guidelines from time to time in response to changes in market conditions or business opportunities without shareholder approval.

Leverage Policies and Financing Strategy. To increase the returns on our investments, after issuance of the Deregistration Order, we plan to employ both direct and structural leverage on our first mortgage loan investments, which we expect generally will not exceed, on a debt to equity basis, a ratio of 3-to-1, an increase from the ratio of 1-to-2 set by the 1940 Act.

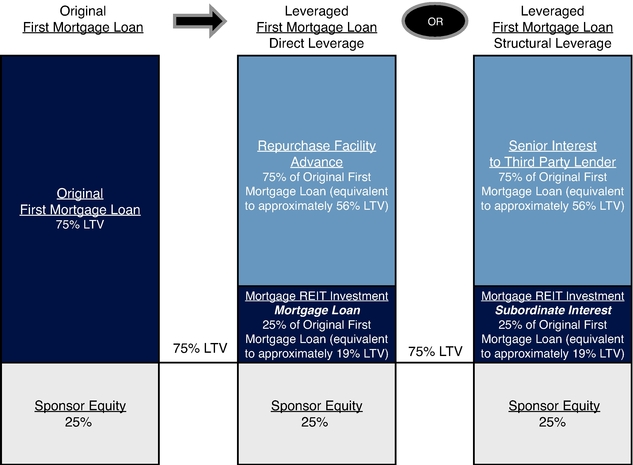

We expect our initial direct leverage will come from repurchase facilities for which we may pledge whole first mortgage loans as collateral. Structural leverage will involve the sale of senior interests in first mortgage loans, such as A-Notes, to third parties and our retention of B-Notes and other subordinated interests in the loans. Below is an illustration of the leverage strategies we plan to use with our first mortgage loan investments.

18 RMR Real Estate Income Fund ![]() 2019 Proxy Statement

2019 Proxy Statement

REPRESENTATIVE CAPITAL STACK ON A FUNDED FIRST MORTGAGE LOAN

We anticipate that repurchase agreements we may enter with banks will be related to our first mortgage loan investments, and we do not currently plan to enter repurchase agreements regarding our subordinated mortgage, mezzanine loan or preferred equity investments. We believe that the relationships our Advisor and its affiliates, as well as other companies managed by our Advisor's affiliates (the "RMR managed companies"), have with commercial and investment banks and other sources of financing may be of assistance to us to arrange our financings. For example, as of November 30, 2019, the RMR managed companies had 34 banking relationships for over $4.7 billion of revolving credit facilities and term loans, and these existing relationships may provide us with introductions to these lenders and expedite their diligence of our operations.