As filed with the Securities and Exchange Commission on April 23, 2009

Registration No. 333-156467

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 1 TO

FORM S-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

CROWNBUTTE WIND POWER, INC.

(Exact name of registrant as specified in its charter)

| Nevada | 4911 | 20-0844584 |

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

111 5th Avenue NE

Mandan, ND 58554

(701) 667-2073

(Address, including zip code, and telephone number, including area code,

of registrant’s principal executive offices)

Timothy H. Simons

Chief Executive Officer

Crownbutte Wind Power, Inc.

111 5th Avenue NE

Mandan, ND 58554

(701) 667-2073

(Name, address, including zip code, and

telephone number, including area code, of agent for service)

Copy to:

Adam S. Gottbetter, Esq.

Gottbetter & Partners, LLP

488 Madison Avenue, 12th Floor

New York, NY 10022

(212) 400-6900

Approximate date of commencement of proposed sale to the public: From time to time after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. T

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer o Accelerated filer o

Non-accelerated filer o Smaller reporting company S

(Do not check if a smaller reporting company)

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be Registered | Amount to be Registered(1) | Proposed Maximum Offering Price Per Unit(2) | Proposed Maximum Aggregate Offering Price | Amount of Registration Fee |

| Common stock, par value $0.001 per share | 7,718,000 shares | $0.50 | $3,859,000 | $215.33 |

| (1) | Consists of 7,718,000 issued and outstanding shares of common stock. This registration statement shall also cover any additional shares of common stock that shall become issuable by reason of any stock dividend, stock split, recapitalization or other similar transaction effected without the receipt of consideration that results in an increase in the number of the outstanding shares of common stock. |

| (2) | The shares offered hereunder may be sold by the selling stockholders from time to time in the open market, through privately negotiated transactions or a combination of these methods, at a fixed price of $0.50 per share until our common stock is quoted on the OTC Bulletin Board, and thereafter at market prices prevailing at the time of sale or at negotiated prices. We intend to apply to list our common stock on the OTC Bulletin Board if and when we meet the listing requirements. We are currently in discussions with various market makers in order to arrange for an application to be made with respect to our common stock, in order to be approved for quotation on the OTC Bulletin Board upon the effectiveness of this registration statement. There can be no assurances, however, that a market maker will agree to do so or that we will meet the other listing requirements, that an established trading market in our common stock will develop, or if such a market does develop, that it will continue. We will file a post-effective amendment to this registration statement at that time to indicate that fact and that the shares will thereafter be sold by the selling stockholders at market prices prevailing at the time of sale or at negotiated prices. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. The selling stockholders may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and the selling stockholders are not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to completion, dated April 23, 2009

CROWNBUTTE WIND POWER, INC.

Prospectus

7,718,000 Shares

Common Stock

This prospectus relates to the sale of up to 7,718,000 issued and outstanding shares of our common stock, par value $0.001 per share, by the selling stockholders of Crownbutte Wind Power, Inc., a Nevada corporation, listed in this prospectus. The shares offered by this prospectus may be sold by the selling stockholders from time to time in the open market, through privately negotiated transactions or a combination of these methods, at a fixed price of $0.50 per share until our common stock is quoted on the OTC Bulletin Board, and thereafter at market prices prevailing at the time of sale or at negotiated prices.

We are registering the offer and sale of the common stock to satisfy registration rights we have granted to the selling stockholders. The distribution of the shares by the selling stockholders is not subject to any underwriting agreement. We will not receive any proceeds from the sale of the shares by the selling stockholders. We will bear all expenses of registration incurred in connection with this offering, but all selling and other expenses incurred by the selling stockholders will be borne by them.

There is no established public trading market for our stock. Our common stock is quoted on the Pink Sheets under the symbol CBWP.PK. On April 22, 2009, the last sale price for our common stock was $0.55 per share. These quotations reflect inter-dealer prices, without retail mark-up, mark-down or commissions, and may not represent actual transactions. We intend to apply to list our common stock on the OTC Bulletin Board if and when we meet the listing requirements. We are currently in discussions with various market makers in order to arrange for an application to be made with respect to our common stock, in order to be approved for quotation on the OTC Bulletin Board upon the effectiveness of the registration statement of which this prospectus is part. There can be no assurances, however, that a market maker will agree to do so or that we will meet the other listing requirements. We cannot give you any assurance that an established trading market in our common stock will develop, or if such a market does develop, that it will continue. We will file a post-effective amendment to the registration statement at that time to indicate that fact and that the shares will thereafter be sold by the selling stockholders at market prices prevailing at the time of sale or at negotiated prices.

The selling stockholders may be deemed, and any broker-dealer executing sell orders on behalf of the selling stockholders will be considered, “underwriters” within the meaning of the Securities Act of 1933. Commissions received by any broker-dealer will be considered underwriting commissions under the Securities Act of 1933.

Investing in our common stock involves a high degree of risk.

Before making any investment in our securities, you should read and carefully consider risks described in the “Risk Factors” section beginning on page 4 of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This prospectus is dated _______, 2008.

In considering the investment of our common stock described in this prospectus, you should rely only on the information contained in this prospectus or any prospectus supplement or amendment thereto. We have not authorized anyone to provide you with different information. This prospectus is not an offer to sell, or a solicitation to buy, shares of common stock in any jurisdiction where offers and sales would be unlawful. The information contained in this prospectus is complete and accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of the shares of common stock.

Until _________, all dealers that effect transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers’ obligation to deliver a prospectus when acting underwriters and with respect to their unsold allotments or subscriptions.

TABLE OF CONTENTS

Page

| SUMMARY | 2 |

| THE OFFERING | 6 |

| NOTE REGARDING FORWARD-LOOKING STATEMENTS | 6 |

| RISK FACTORS | 7 |

| SELLING STOCKHOLDERS | 23 |

| USE OF PROCEEDS | 27 |

| DETERMINATION OF OFFERING PRICE | 27 |

| MARKET FOR COMMON EQUITY AND RELATED STOCKHOLDER MATTERS | 28 |

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 29 |

| DESCRIPTION OF BUSINESS | 47 |

| PROPERTIES | 71 |

| LEGAL PROCEEDINGS | 72 |

| DIRECTORS, EXECUTIVE OFFICERS, PROMOTERS AND CONTROL PERSONS | 74 |

| SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT | 75 |

| EXECUTIVE COMPENSATION | 76 |

| CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS | 78 |

| PLAN OF DISTRIBUTION | 78 |

| DESCRIPTION OF SECURITIES | 81 |

| LEGAL MATTERS | 84 |

| EXPERTS | 84 |

| WHERE YOU CAN FIND MORE INFORMATION | 84 |

| DISCLOSURE OF COMMISSION POSITION ON INDEMNIFICATION FOR SECURITIES ACT LIABILITIES | 84 |

| INDEX TO CONSOLIDATED FINANCIAL STATEMENTS | F-1 |

The following summary highlights information contained elsewhere in this prospectus. Potential investors should read the entire prospectus carefully, including the more detailed information regarding our business provided below in the “Description of Business” section, the risks of purchasing our common stock discussed under the “Risk Factors” section, and our financial statements and the accompanying notes.

Our Business

Our wholly-owned subsidiary, Crownbutte Wind Power, Inc., a North Dakota corporation (“Crownbutte ND”), was founded in 1999 by our Chief Executive Officer, Tim Simons, with the goal of addressing the requirements of regional utility companies to satisfy increasing renewable energy demands. We develop wind parks from green field to operation, which we have sold to regional utilities. One wind park developed by us from “green-field” or blank state to operation was purchased directly in 2001 by Basin Electric Power Cooperative (2.6 megawatts (MW) near Chamberlain, South Dakota). In addition to these two parks, we have completed various consulting activities with regional utilities and international energy companies. At the present time, we do not own or operate any wind parks. Currently, we have 11 projects totaling approximately 618 MW of prospective capacity in various phases of development primarily in North Dakota, South Dakota and Montana, with a total of over 40,000 acres under lease option. Our project management team is exploring other opportunities in this region. Our ultimate goal is to develop, own and operate merchant wind parks in the 20 to 60 MW capacity range.

We have developed what we believe is a unique process for bringing viable wind parks to market. While most developers have focused on large projects of 100 MW or more, we have found a niche in the 20 to 60 MW range. Our focus will be to bring these smaller parks from concept to operation. The project sites currently in development by us are located directly on some of the most ideal wind regimes in the country, with net capacity factors of up to forty-six percent (46%). These above-average net capacity factors have a significant impact on the amount of electricity that can be generated and therefore on future revenues. Our focus on smaller projects allows us to install parks where developers of larger projects would be at a disadvantage, because smaller projects more easily fit into the current transmission grid, which decreases the costs of upgrading downstream components. While small projects are the focus of our strategy, we have not ruled out the possibility of larger projects.

Our business model focuses on the development of merchant parks. We do not plan to enter into power purchase agreements unless they are offered on favorable terms. Currently in the upper Midwest, with the exception of Minnesota, power purchase agreements tend to be difficult to obtain. When power purchase agreements are available, they tend to be at a price per kilowatt hour (kWh) that is less than the market price of electricity. Merchant parks sell electricity on the open market. Based on spot prices for electricity over the past two years, our merchant parks would have received on average $0.05 per kWh. Selling power on the open market increases the risk of the projects. However, we believe, based on U.S. Department of Energy forecasts and our own analysis, that over the next decade the market price of electricity will continue to increase and that this merchant model will allows us to capture that upside potential.

In the past, we have been developing and then selling wind parks, in some cases remaining as a consultant for the party that purchased the park. We plan to continue to sell developments as a part of our ongoing business, but we intend to shift the focus of our business towards ownership and operation of merchant wind parks that we develop. We believe that this will allow us to grow our balance sheet and increase cash flow.

We intend to develop sites from “green field” (or blank slate) at a rate of approximately two to three additions to our pipeline per year, with each site likely to reach operation in approximately three years. Of the project sites we develop, we expect to sell to utilities and other developers about 60 MW worth of partially-developed (also known as “brown field”) sites from our portfolio per year beginning in 2009.

We expect to start construction on our first wind park that we will own and operate, a 20 MW project called Gascoyne I located south of Dickinson, North Dakota, in mid-2009. Our goal is to have approximately 110 MW of owned operating capacity by the end of 2010, and we target the construction and commissioning of approximately 200 MW of owned operating capacity annually thereafter, to achieve approximately 750 MW of owned operating capacity by the end of 2013. We do not currently and do not plan to act as an operator of wind parks we do not own.

2

In addition to green field developments, we are analyzing late stage developments of other wind developers. If a project appears to be feasible, we intend to pursue the purchase of the park.

To successfully develop, build and own wind parks, and to acquire other developments or make business acquisitions, we will need to raise capital. We plan to raise approximately $3 million through private placements of equity by March 2009, the proceeds of which, together with cash on hand, will be used for general corporate expenses associated with the hiring of new staff required to accelerate our development activities, as well as move into our new owner-operator business model, which requires oversight of construction of projects, as well as the operations and maintenance of projects after construction is complete. We do not anticipate a need to raise additional equity financing beyond this $3 million for these purposes, provided that we are able to sell to utilities or other developers one to two brown-field sites per year beginning in 2009.

We anticipate that we will need to arrange turbine supply loans to finance approximately 60 to 90% of the cost of a project’s turbines. After we have developed a wind energy project that we intend to own to the point where we are prepared to commence construction, we will need to raise construction financing to retire turbine indebtedness and to pay construction costs. Construction loans are generally secured by the project’s assets and our equity interests in the project companies. In certain instances we may enter into a construction loan for a single project, while in other instances we may be able to finance multiple projects through a single credit facility. We will also use equity capital contributions (our own and potentially from other investors as described above) to fund a portion of each project’s construction costs.

About This Offering

This prospectus relates to the public offering, which is not being underwritten, of up to 7,718,000 outstanding shares of our common stock by the selling stockholders listed in this prospectus. The shares offered by this prospectus may be sold by the selling stockholders from time to time in the open market, through negotiated transactions or otherwise at a fixed price of $0.50 per share until our common stock is quoted on the OTC Bulletin Board, and thereafter at market prices prevailing at the time of sale or at negotiated prices. We will receive none of the proceeds from the sale of the shares by the selling stockholders. We will bear all expenses of registration incurred in connection with this offering, but all selling and other expenses incurred by the selling stockholders will be borne by them.

The shares of common stock being offered by this prospectus relate to (i) 1,100,000 shares sold by Crownbutte ND in a private placement completed in April 2008, (ii) 3,118,000 shares sold by us in a private placement completed in September 2008 and (iii) 3,500,000 shares that were issued upon exercise of warrants issued to the placement agent in our private placement completed in September 2008.

The number of shares being offered by this prospectus represents approximately 29.4% of our outstanding shares of common stock as of April 21, 2009.

Corporate Information and History

We were incorporated in the State of Nevada on March 9, 2004, under the name ProMana Solutions, Inc. As ProMana Solutions, our business was to provide web-based, fully integrated solutions for managing payroll, benefits, human resource management and business processing outsourcing to small and medium sized businesses. Following the merger described below, we are no longer in that web services business.

On July 2, 2008, we amended our Articles of Incorporation to change our name to Crownbutte Wind Power, Inc.

Crownbutte ND was formed as a North Dakota limited liability company on May 11, 1999. On May 19, 2008, Crownbutte ND was converted to a North Dakota corporation.

3

On July 2, 2008, a special purpose acquisition subsidiary formed by us merged with and into Crownbutte ND, with Crownbutte ND surviving the merger, thereby becoming our wholly-owned subsidiary. Following the merger, we continued Crownbutte ND’s business operations. In connection with the merger, we changed our name to Crownbutte Wind Power, Inc. Upon the closing of the merger, the holders of all of the issued and outstanding shares of Crownbutte ND surrendered all of their shares and received shares of our common stock on a one-to-one basis. Also on the closing date, holders of issued and outstanding warrants to purchase shares of Crownbutte common stock received new warrants to purchase shares of our common stock, also on a one-to-one basis.

Pursuant to the merger, we ceased operating as a provider of web-based, fully integrated solutions for managing payroll, benefits, human resource management and business processing outsourcing, and acquired the business of Crownbutte ND to develop wind parks from green field to operation and has continued Crownbutte ND’s business operations as a publicly-traded company.

At the closing of the merger, each share of Crownbutte ND’s common stock outstanding was converted into one share of our Common Stock. As a result, an aggregate of 18,100,000 shares of our Common Stock were issued to the holders of Crownbutte ND’s common stock. In addition, warrants to purchase an aggregate of 10,600,000 shares of Crownbutte ND’s outstanding at the time of the merger became warrants to purchase an equivalent number of shares of our Common Stock.

The merger agreement contains a provision for a post-closing adjustment to the number of shares of our Common Stock issued to the former Crownbutte ND stockholders, in an amount up to 2,000,000 shares of our Common Stock, to be issued on a pro rata basis for any breach of the Merger Agreement by us, discovered during the one-year period following the closing. In order to secure the indemnification obligations of Crownbutte ND under the merger agreement, 5% of the shares of our Common Stock to which the former Crownbutte ND stockholders are entitled in exchange for their shares of Crownbutte ND in connection with the Merger will be held in escrow for a period of one year.

The merger agreement contained customary representations and warranties and pre- and post-closing covenants of each party and customary closing conditions. Breaches of the representations and warranties will be subject to customary indemnification provisions.

The merger was treated as a recapitalization of the Company for financial accounting purposes. Crownbutte ND is considered the acquirer for accounting purposes, and our historical financial statements before the Merger have been replaced with the historical financial statements of Crownbutte ND before the Merger in all subsequent filings with the Securities and Exchange Commission (the “SEC”).

The parties have taken all actions necessary to ensure that the Merger is treated as a tax-free exchange under Section 368(a) of the Internal Revenue Code of 1986, as amended.

Contemporaneously with the merger, the then-existing assets and liabilities of the Company were transferred to Pro Mana Technologies, Inc., a New Jersey corporation, which at that time was a wholly-owned subsidiary of the Company. Contemporaneously with the merger, we transferred all of the outstanding capital stock of Pro Mana Technologies to certain pre-merger shareholders of the Company in exchange for the surrender and cancellation of an aggregate of 144,702 shares of our common stock and warrants to purchase 19,062 shares of our common stock held by those stockholders and certain covenants and indemnities. We no longer own Pro Mana Technologies.

On July 31, 2008, we effected a reverse stock split, as a result of which each 65.723 shares of our common stock (including those issued in connection with the merger) then issued and outstanding were converted into one share of our common stock. Unless otherwise stated herein or the context clearly indicates otherwise, all share and per share numbers in this prospectus relating to our common stock have been adjusted to give effect to the reverse stock split.

Our principal executive offices are located at 111 5th Avenue NE, Mandan, ND 58554, and our telephone number is (701) 667-2073. Our website address is www.crownbutte.com. The contents of our website are not part of this prospectus and should not be relied upon with respect to this prospectus.

4

Summary Financial Information

The following tables summarizes historical financial data regarding our business and should be read together with the information in the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the related notes included in this prospectus.

| Year Ended December 31, | ||||||||

| 2008 | 2007 | |||||||

| Statement of Operations Data | ||||||||

| Revenues | $ | 273,020 | $ | 720,100 | ||||

| Total costs and expenses | 4,228,801 | 345,064 | ||||||

| Net operating income (loss) | $ | (3,955,781 | ) | $ | 375,036 | |||

| Statement of Cash Flows Data | ||||||||

| Net cash (used in) provided by operating activities | $ | (1,047,827 | ) | $ | 404,488 | |||

| Cash and cash equivalents (end of period) | 304,703 | 125,744 | ||||||

| At December 31, | ||||||||

| 2008 | 2007 | |||||||

| Balance Sheet Data | ||||||||

| Current assets | $ | 479,842 | $ | 275,713 | ||||

| Total assets | $ | 826,545 | $ | 411,882 | ||||

| Current liabilities | $ | 179,641 | $ | 183,286 | ||||

| Total liabilities | $ | 179,641 | $ | 183,286 | ||||

| Total stockholders’ equity | $ | 646,904 | $ | 228,596 | ||||

5

THE OFFERING

| Common stock currently outstanding | 26,200,331 shares(1) | |

| Common stock offered by the Company | None | |

| Common stock offered by the selling stockholders | 7,718,000 shares(2) | |

| Use of proceeds | We will not receive any of the proceeds from the sales of our common stock by the selling stockholders. | |

| Pink Sheets symbol | CBWP.PK | |

| Risk Factors | You should carefully consider the information set forth in this prospectus and, in particular, the specific factors set forth in the “Risk Factors” section beginning on page 4 of this prospectus before deciding whether or not to invest in shares of our common stock. |

(1) As of April 21, 2009.

(2) Consists of 7,718,000 issued and outstanding shares of common stock.

NOTE REGARDING FORWARD-LOOKING STATEMENTS

Various statements in this prospectus, including those that express a belief, expectation or intention, as well as those that are not statements of historical fact, are forward-looking statements. The forward-looking statements may include projections and estimates concerning the timing and success of specific projects, revenues, income and capital spending. We generally identify forward-looking statements with the words “believe,” “intend,” “expect,” “seek,” “may,” “should,” “anticipate,” “could,” “estimate,” “plan,” “predict,” “project” or their negatives, and other similar expressions. All statements we make relating to our estimated and projected earnings, margins, costs, expenditures, cash flows, growth rates, financial results and projects developments and acquisitions or to our expectations regarding future industry or economic trends are forward-looking statements.

These forward-looking statements are subject to risks and uncertainties that may change at any time, and, therefore, our actual results may differ materially from those that we expected. The forward-looking statements contained in this prospectus are largely based on our expectations, which reflect many estimates and assumptions made by our management. These estimates and assumptions reflect our best judgment based on currently known market conditions and other factors. Although we believe such estimates and assumptions are reasonable, we caution that it is very difficult to predict the impact of known factors and it is impossible for us to anticipate all factors that could affect our actual results. In addition, management’s assumptions about future events may prove to be inaccurate. Management cautions all readers that the forward-looking statements contained in this prospectus are not guarantees of future performance, and we cannot assure any reader that such statements will be realized or the forward looking events and circumstances will occur. Actual results may differ materially from those anticipated or implied in the forward-looking statements due to the factors listed in the “Risk Factors” section and elsewhere in this prospectus. All forward-looking statements are based upon information available to us on the date of this prospectus. We undertake no obligation to update or revise any forward-looking statements as a result of new information, future events or otherwise, except as otherwise required by law. These cautionary statements qualify all forward-looking statements attributable to us, or persons acting on our behalf.

6

An investment in shares of our common stock is highly speculative and involves a high degree of risk. We face a variety of risks that may affect our operations or financial results and many of those risks are driven by factors that we cannot control or predict. Before investing in our common stock you should carefully consider the following risks, together with the financial and other information contained in this prospectus. If any of the following risks actually occurs, our business, prospects, financial condition and results of operations could be materially adversely affected. In that case, the trading price of our common stock would likely decline and you may lose all or a part of your investment. Only those investors who can bear the risk of loss of their entire investment should participate in this offering.

Risks Related to Our Business and the Wind Energy Industry

We have limited experience in completing development of wind parks and no operating history as an owner-operator of wind parks.

To date we have developed and sold only two wind parks. We plan to continue to sell developments as a part of our ongoing business, but we intend to shift the focus of our business towards ownership and operation of merchant wind parks that we develop. We have no history as an owner-operator of wind parks from which you can evaluate our business plan, and our past performance cannot be taken as indicative of future results, especially as we change our business strategy.

The growth of our business depends upon our ability to convert our pipeline of projects under development into operating projects.

We currently do not own or operate any wind parks. We may not be successful in completing our pipeline of development projects as anticipated or at all. Our portfolio of wind energy projects includes approximately 618 MW of capacity in various stages of development. (See “Description of Business.”) We expect to start construction on one 20 MW project in 2009. Our goal is to have approximately 120 MW of owned operating capacity by the end of 2010, and we target the construction and commissioning of approximately 200 MW annually thereafter to achieve approximately 700 MW of owned operating capacity by the end of 2013. However, there can be no assurance we will achieve these goals.

The development and construction of wind energy projects involves numerous risks and uncertainties, including:

| · | access to liquid independent systems operator (“ISO”) markets or negotiation of power purchase agreements (“PPAs”), |

| · | availability of transmission lines with adequate capacity, |

| · | obtaining necessary land rights, |

| · | turbine procurement, |

| · | availability of turbine, construction and permanent financing, |

| · | extension of the renewable energy federal production tax credits (“PTCs”) beyond December 31, 2009, |

| · | obtaining necessary governmental and regulatory approvals and permits, and |

| · | negative public or community response, |

7

many of which are subject to intense competition and all of which may be beyond our control. We discuss each of these risks in additional detail below. These risks and uncertainties may prevent projects from progressing to construction and may cause us to fail to meet the targets of our development plan.

We may be unable to secure the project financing required to construct the projects currently in our portfolio.

If we fail to secure the project financing required for construction of these wind parks ($1.8-$2 million per MW of generating capacity), then Crownbutte will be relegated to being a green-field developer of prospective wind farm sites, whose income options will be limited to selling the development rights for those sites to entities that are capable of assembling the project financing required to construct, own, and operate wind farms. In such a case, Crownbutte’s financial position and prospects for income would be significantly impaired. The possibility of our failure to secure project finance therefore makes investment into Crownbutte risky.

We may elect not to proceed with projects currently in our portfolio.

We may elect not to proceed with projects currently in our portfolio. Our current portfolio of approximately 618 MW does not include projects representing 30 MW of prospective capacity that we have, since 2000, actively developed and then elected not to pursue. To date costs incurred with respect to projects we have elected not to pursue have been minimal, but this may not always be the case.

Our revenues may be inconsistent, creating a liquidity risk.

Until we make the transition to owner/operator, our revenues depend on making a small number (one to two transactions per year) of sales of the development rights to park in our pipeline. The negotiation and lead-time to completing such transactions are not easily predictable, and may not occur at the prices or on the timing we desire. Revenues therefore can be zero for extended periods, which can result in significant liquidity risk for the company.

Development of our projects depends on access to liquid ISO markets

We do not plan to enter into PPAs unless they are offered on favorable terms. Our business model focuses on the development of merchant parks, which sell electricity into a power spot market. There are several systems that provide real time and day-ahead spot markets for electricity such as Midwest ISO, PJM, ERCOT and Cal ISO. Our portfolio of projects is located predominately in the Midwest, and therefore our merchant projects would sell into the Midwest ISO’s (MISO) spot market.

It is possible that the MISO spot market becomes illiquid due to withdrawal of its member system owners, problems in the physical transmission infrastructure, or fundamental changes in the supply or demand of electricity. In the event that the spot market no longer functions efficiently, any income streams from the sale of electricity would have a material adverse effect on Crownbutte’s financial condition and operations.

We will depend on the availability of transmission lines with adequate capacity.

We expect to generally depend on electric transmission lines owned and operated by third parties to deliver the electricity we will sell. Some of our wind energy projects in development may have limited access to interconnection and transmission capacity. MISO will inform Crownbutte in such cases during the feasibility studies and systems impact studies that are part of the Interconnection Agreement process. We may not be able to secure access to the limited available interconnection or transmission capacity at reasonable systems upgrade cost, or at all. Since this Interconnection Agreement must be in place before any construction or turbine costs are incurred, this is a moderate financial risk for Crownbutte.

However, in the event of a failure in the transmission facilities after a project is completed, we may experience lost revenues. In addition, transmission limitations may cause us to curtail our production of electricity, impairing our ability to fully capitalize on the particular wind energy project’s potential. Any such failure could have a material adverse effect on our business, financial condition or results of operations.

8

The growth of our business depends on locating and obtaining control of suitable operating sites.

Wind energy projects require wind conditions that are found in limited geographic areas and particular sites. Further, wind energy projects must be interconnected to electricity transmission or distribution networks in order to deliver electricity. Once we have identified a suitable operating site, our ability to obtain requisite land control or other land rights (including access rights, setback and/or other easements) with respect to the site is subject to growing competition from other wind energy producers that have sufficient financial capacity to research, locate and obtain control of such sites and to obtain required electrical interconnection rights. Our competitors may impede our development efforts by acquiring control of all or a portion of a project site we desire to develop or obtaining a right to use land necessary to connect a project site to a transmission or distribution network. If a competitor obtains land rights critical to our project development efforts, we could incur losses as a result of stranded development costs. If we succeed in securing the property rights necessary to construct and interconnect our projects, such property rights must be insurable and otherwise satisfactory to our financing counterparties. Obtaining adequate property rights may delay development of a project, or may not be feasible. Any failure to obtain insurable property rights that are satisfactory to our financing counterparties would preclude our ability to obtain third-party financing and could prevent ongoing development and construction of the relevant projects.

Our wind energy projects’ use and enjoyment of real property rights obtained from third parties may be adversely affected by the rights of lien holders and lease holders whose rights are superior to those of the grantors of these real property rights.

Each of our wind energy projects is or will be located on land occupied pursuant to various easements and leases. Our rights pursuant to these easements and leases allow us to install wind turbines, related equipment and transmission lines for the projects and to operate the projects. The ownership interests in the land subject to these easements and leases may be subject to mortgages securing loans or other liens (such as tax liens) and other easement and lease rights of third parties (such as leases of oil, gas, coal or other mineral rights) that were created prior to our easements and leases. As a result, our rights under these easements or leases may be subject and subordinate to the rights of such third parties.

A default by a landowner at one or more of our wind energy projects under a mortgage could result in foreclosure of the landowner’s property and thereby terminate our easements and leases required to operate the projects. Similarly, it is possible that another lien holder, such as a government authority with a tax lien, could foreclose upon a parcel and take ownership and possession of the portion of the project located on that parcel. In addition, the rights of a third party pursuant to a superior lease could result in damage to or disturbance of the equipment at a project, or require relocation of project assets.

If any of our wind energy projects were to suffer the loss of all or a portion of its wind turbines or related equipment as a result of a foreclosure by a mortgagee or other lien holder of a land parcel, or damage arising from the conduct of superior lease holders, our operations and revenues could be adversely affected.

Development of wind projects is dependent on the availability of turbines and turbine financings.

Wind energy projects require delivery and assembly of turbines. The prices of turbines and electrical and other equipment have increased in recent years and may continue to increase as the demand for such equipment increases more rapidly than supply, or if the prices of key components and raw materials used to build the equipment increase. We may encounter supply and/or logistical issues in securing turbines due to the limited number of turbine suppliers and current high demand for turbines. While we have received quotes from turbine suppliers and have seen some evidence of softening turbine prices and shorter delivery lead times as the financial market turmoil during the autumn of 2008 has slowed the installation of new wind capacity, we currently have no turbines under contract. We may not be able to purchase a sufficient quantity of turbines from suppliers, and suppliers may give priority to other customers. Turbine suppliers may delay the performance of or be unable to meet contractual commitments, or components and equipment may be unavailable, which would have a material adverse effect on our business, financial condition and results of operations.

In addition, we expect to require third-party turbine supply loans or other financing for our turbine purchases, which account for the majority of the total cost of a wind energy project. An inability to obtain such financing on attractive terms in the future may preclude us from obtaining additional turbines, severely limiting our growth. Moreover, a significant increase in the cost of obtaining such financing could have a material adverse effect on the investment returns we achieve from our projects.

9

In addition, spare parts for wind turbines and key pieces of electrical equipment may be unavailable to us. If we were to experience a serial failure of any spare part we would incur delays in waiting for shipment of these items to the site. In addition, we do not carry spare substation main transformers. These transformers are designed specifically for each wind energy project, and the current lead time to order this equipment is up to one year. If we have to replace any of our transformers, we would be unable to sell electricity from the affected wind energy project.

When we purchase our turbines, we also enter into warranty agreements with the manufacturer. Damages payable by the manufacturer under these agreements are typically subject to an aggregate maximum cap that is a portion of the total purchase price of the turbines. Losses in excess of these caps will be our responsibility. Since our turbine warranties generally expire within a certain period of time after the turbine delivery date or the date such turbine is commissioned, we may lose all or a portion of the benefit of the warranties if we are unable to deploy turbines we have purchased upon delivery.

We will need to raise additional capital to meet our business requirements, and such capital raising may be costly or difficult to obtain and could dilute current stockholders’ ownership interests.

To date, our capital expenditures and working capital requirements have been funded by income from operations and equity capital. Our income from operations will not be sufficient to fund our business plan. We plan to raise approximately $1 million through private placements of equity by August 2009, the proceeds of which, together with cash on hand, will be used for general corporate expenses associated with the hiring of new staff required to accelerate our development activities, as well as move into our new owner-operator business model, which requires oversight of construction of projects, as well as the operations and maintenance of projects after construction is complete. However, we may be unable to secure this additional financing on terms acceptable to us, or at all, at times when we need such financing. We do not anticipate a need to raise additional equity financing beyond this $3 million to fund development, operating and maintenance costs provided that we are able to sell to utilities or other developers one to two brown-field sites per year beginning in 2009. These fundings do not include financing of project construction and operation. See “Our projects will entail significant capital expenditures and construction costs, and we will require additional financing to construct and operate them” below.

If we are unable to obtain such additional equity financing on a timely basis, we may have to curtail our development activities or be forced to sell assets, perhaps on unfavorable terms, which would have a material adverse effect on our business, financial condition and results of operations. We may incur substantial costs in pursuing future capital financing, including investment banking fees, legal fees, accounting fees, securities law compliance fees, printing and distribution expenses and other costs. We may also be required to recognize non-cash expenses in connection with certain securities we may issue, such as convertible notes, restricted stock, stock options and warrants, which may adversely impact our financial condition. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations” below.

Any future issuance of our equity or equity-backed securities may dilute then-current stockholders’ ownership percentages. See “You may experience dilution of your ownership interests due to the future issuance of additional shares of our common stock” below.

Our projects will entail significant capital expenditures and construction costs, and we will require additional financing to construct and operate them.

We are in a capital intensive business, and our projects in development and construction have entailed and will entail significant capital expenditures and construction costs, and recovery of the capital investment in a wind energy project generally occurs over a lengthy period of time. The capital investment required to construct a wind energy project is primarily based on the costs of fixed assets required for the project. We will require additional financing, including tax equity financing transactions (described below), to complete the construction of and to operate our existing projects. Additional financing may not be available on acceptable terms or at all.

10

After we have developed a wind energy project that we intend to own to the point where we are prepared to commence construction, we would expect typically to enter into a limited recourse construction loan. Proceeds from construction loans would typically be used to retire turbine indebtedness and to pay construction costs, including costs to construct roads, substations, transmission lines and the balance of plant. Construction loans are generally secured by the project’s assets and our equity interests in the project companies. In certain instances we may enter into a construction loan for a single project, while in other instances we may be able to finance multiple projects through a single credit facility. We will also likely use equity capital contributions (our own and potentially from other investors as described above) to fund a portion of each project’s construction costs.

We would forego the need for construction loans (as well as turbine supply loans) if we are able to secure 100% debt or 100% equity-based investment for any given project. A 100% debt financing would be done on a limited recourse basis and be secured by the project assets and our equity. In a 100% equity financing, the outside equity investors would contribute all of the project costs as equity in return for an 80% to 90% share of the returns. However, while we are exploring these possibilities, these structures have not in the past been the norm in the wind generation industry and may not be available.

Once construction of a wind energy project is completed and commercial operations commence, we will seek to finance the project on a long-term basis through a combination of term loans and tax equity financing. (See “We expect to be materially dependent on tax equity financing arrangements” below.)

The unprecedented upheaval in the debt and equity markets in the U.S. and around the world in recent months has made all categories of financing more difficult to secure. In addition, the lower profits achieved by many financial institutions has made tax equity investing less available in general. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Project Finance.”

Our strategy of relying on a merchant park model may make project and tax equity financing more difficult and may adversely affect results of operations.

Our business model focuses on the development of merchant parks. We do not plan to enter into power purchase agreements unless they are offered on favorable terms. Merchant parks sell electricity on the open market. The reliance on the merchant market (i.e., the lack of PPAs) can be a significant barrier to achieving construction financing and project financing with tax equity investors (as described below), many of whom seek the security of long-term PPAs with power off-takers.

Our efforts to secure project finance have confirmed that investment banks and other financial institutions that have brokered or directly financed wind projects in the past have a continued desire to see PPA’s as the off-take arrangement in place for projects they seek to represent or finance. Such a desire for a PPA on the part of financiers is natural, but may not be possible to achieve by Crownbutte. There are no federal or state mandates in place that require utilities to offer PPA’s in North Dakota, where the bulk of Crownbutte’s projects are located.

Crownbutte has not, to date secured project financing for any of its parks in development. If PPA’s cannot be secured, and financiers decline to fund any of Crownbutte’s merchant park model projects, there will be a significant adverse effect on Crownbutte’s finances and operations.

We expect to be materially dependent on tax equity financing arrangements.

We intend to seek to secure tax equity financing to provide the majority of the permanent capital needs for each project we will own. The availability of tax equity financing depends on federal tax attributes that encourage renewable energy development. These attributes primarily include (i) renewable energy federal PTCs, which are federal income tax credits related to the quantity of renewable energy produced and sold during a taxable year and (ii) accelerated depreciation of renewable energy assets as calculated under the Modified Accelerated Cost Recovery System of the Internal Revenue Code (“MACRS”). We do not expect to generate sufficient taxable income from owned projects to use all of the PTCs or the accelerated depreciation expected to be available to us under these programs. We intend to seek to maximize project profitability, improve project returns and reduce equity capital requirements by monetizing the value of these incentives through tax equity financing transactions.

11

In a typical tax equity financing, we would receive an up-front cash payment in exchange for an equity interest in our subsidiary that owns the project. These equity interests entitle the investors to receive a substantial portion of the project’s cash distributions from electricity sales and related hedging agreements, PTCs and taxable income or loss until such investors reach an agreed rate of return on their up-front cash payment. As a result, a tax equity financing substantially reduces the cash distributions from the applicable projects available to us for other uses, and the period during which the tax equity investors receive cash distributions from electricity sales and related hedging agreements may last longer than expected if our wind energy projects perform below our expectations.

Moreover, there are a limited number of potential tax equity investors, they have limited funds and wind energy developers compete with other renewable energy developers and others for tax equity financing. To date, the wind industry’s tax equity investors have been large financial institutions with significant taxable income. The unprecedented upheaval in the debt and equity markets in the U.S. and around the world in recent months has resulted in lower profits for many financial institutions, making tax equity investing less available in general. Furthermore, as the renewable energy industry expands, the cost of tax equity financing may increase and there may not be sufficient tax equity financing available to meet the total demand in any year. If we are unable to enter into tax equity financing agreements with attractive pricing terms or at all, we may not be able to use the tax benefits provided by PTCs and accelerated tax depreciation, which could have a material adverse effect on our business, financial condition and results of operations.

In addition, our tax equity financing agreements are expected to provide our tax equity investors with a number of approval rights with respect to the applicable project or projects, including approvals of annual budgets, indebtedness, incurrence of liens, sales of assets outside the ordinary course of business and litigation settlements. As a result of these restrictions, the manner in which we conduct our business may be limited. See “Management‘s Discussion and Analysis of Financial Condition and Results of Operations—Project Finance.”

The growth of our business depends upon the extension of the expiration date of the PTC/ITC, which currently expires on December 31, 2012, and other federal and state governmental policies and standards that support renewable energy development.

We depend heavily on government policies supporting renewable energy that make the development and operation of wind energy projects economically feasible. In particular, we cannot economically develop and construct our pipeline of development projects without the federal PTC, which will expire on December 31, 2012, unless legislation is enacted to extend it. The PTC currently provides a $21 federal tax credit per megawatt hour (“MWh”) for a renewable energy facility that uses wind, geothermal or closed-loop biomass fuel sources in each of the first ten years of its operation and applies to facilities that are placed in service before the end of 2012. These facilities will continue to benefit from the current PTC incentive until the end of the ten-year period from the date on which the wind turbines are placed in service. Without an extension of the expiration date of the PTC, wind energy projects may not be economically feasible to develop and construct.

An option to the PTC is the 30% Investment Tax Credit (“ITC”) wherein a taxpayer may claim 30% of investment amount as a tax credit in lieu of the PTC.

As part of the February 2009 American Recovery and Reinvestment Act (“ARRA”), a project placed in service in 2009 or 2010 may claim a cash grant from the Treasury department instead of the ITC. The grant does not constitute taxable income.

In addition to the PTC/ITC, we rely on other incentives that support the sale of energy generated from renewable sources, including state adopted RPS programs. RPS programs often operate in tandem with a credit trading system through which generators can buy or sell RECs that are issued by the state to generators of renewable energy to meet mandated renewable requirements. At this time, North Dakota has no RPS, and it is not anticipated that they will have RPS in the near future. Other states including Montana and Minnesota provide a range of incentives through RPS programs.

While federal and state governments have promoted renewable energy in the past, policies may be adversely modified or support of renewable energy development, particularly wind energy, may not continue. If governmental authorities fail to continue supporting, or reduce their support for, the development of renewable energy projects, particularly wind energy projects, it could materially adversely affect our ability to develop and construct our pipeline of development projects and grow our business.

12

The design, construction and operation of wind energy projects are highly regulated activities.

The design, construction and operation of wind energy projects are highly regulated activities requiring various material governmental and regulatory approvals and permits. Procedures for the granting of operating and construction permits vary by jurisdiction and certain jurisdictions may deny requests for permits for a variety of reasons. Further, we may not be able to renew construction and operating permits when required. Failure to procure and maintain the necessary permits may prevent ongoing development, construction and continuing operation of our projects. In addition, in some circumstances we may have to commence construction prior to obtaining all required permits, which exposes us to the risk that we may subsequently be unable to secure all of the permits required to complete the project. If this were to occur, we could experience considerable losses as a result of our prior investment.

Our projects may be subject to regulation by the Federal Energy Regulatory Commission (“FERC”) under the Federal Power Act (“FPA”) or other regulations that regulate the sale of electricity, which may adversely affect our business.

Certain of our projects may be able to obtain qualifying facility (or “QF”) status under the Public Utility Regulatory Policies Act, or PURPA. QFs are exempt from certain provisions of the FPA, including the accounting and reporting requirements, and mergers and acquisitions oversight, facility disposition regulations and several other provisions of the FPA. Additionally, renewable energy facilities with a generating capacity of 30 MW or less are exempt from FERC's ratemaking authority under the FPA.

Exempt wholesale generators (“EWGs”) are generation owning public utilities (including producers of renewable energy, such as wind projects) that are engaged exclusively in the business of owning and/or operating generating facilities and selling electric energy at wholesale. The owner of a renewable energy facility that has been certified as an EWG in accordance with FERC's regulations is subject to the FPA and to FERC's ratemaking jurisdiction, but FERC typically grants EWGs the authority to charge market-based rates as long as the EWG can demonstrate that it does not have, or has adequately mitigated, market power and cannot otherwise erect barriers to market entry. FERC generally grants an EWG waivers from many of the requirements that are otherwise imposed on public utilities under the FPA.

The Public Utility Holding Company Act of 2005 (“PUHCA”) in part provides that any entity that owns, controls or holds power to vote 10% or more of the outstanding voting securities of a "public utility company" (which is defined to include an "electric utility company") or a company that is a "holding company" of a public utility company or public utility holding company, is subject to certain regulations granting FERC, access to books and records and oversight over certain affiliate transactions. State regulatory commissions may in some instances also have access to books and records of holding companies. However, entities that are holding companies solely by virtue of their ownership of QFs and EWGs are exempt from are exempt from most of the PUHCA requirements.

We intend that each of our wind parks will file a self-certification with the FERC that it is an exempt wholesale generator. As a result, under current federal law, we would not be subject to regulation as a holding company under PUHCA and would not be subject to this regulation as long as each "public utility company" in which we have an interest is (i) a qualifying facility, (ii) an exempt wholesale generator or (iii) subject to another exemption or waiver.

Although the sale of electric energy has been to some extent deregulated, the industry is subject to increasing regulation and even the threat of re-regulation. Due to major regulatory restructuring initiatives at the federal and state levels, the U.S. electric industry has undergone substantial changes over the past several years. We cannot predict the future design of wholesale power markets or the ultimate effect ongoing regulatory changes will have on our business. Other proposals to re-regulate may be made and legislative or other attention to the electric power market restructuring process may delay or reverse the movement towards competitive markets. If the deregulation of the electric power markets is reversed, discontinued or delayed, our business prospects and financial results could be negatively affected. See “Business—Regulation” for more information.

13

Negative public or community response to wind energy projects may adversely affect our ability to construct our projects.

There has been negative public and/or community response to wind energy projects in some areas of the United States, and such factors may adversely affect our ability to construct our projects in certain areas. In addition, legal challenges may result in an injunction against construction or operation, impeding our ability to place projects in operation according to schedule, meet our development and construction targets or generate revenues. An increase in opposition to the granting of permits or unfavorable outcomes of such challenges could materially and adversely affect our development plans.

Projects that reach construction may not be completed or, if completed, may not meet our return expectations.

Those projects that do progress to construction may not be completed on a timely basis or at all or, if completed, may not meet our return expectations, due to factors such as:

| · | schedule delays, |

| · | cost overruns, |

| · | failure to receive turbines or other critical components and equipment from third parties on schedule and according to design specifications |

| · | unsatisfactory completion of construction, |

| · | shortfalls of anticipated capacity factor, |

| · | adverse weather, |

| · | lower natural gas prices, |

| · | lower than forecast spot electricity prices, and |

| · | force majeure or other events out of our control. |

Any of the above factors could give rise to construction delays and construction costs in excess of our budgets, which could prevent us from completing construction of a project, cause defaults under our financing transactions and impair our business, financial condition and results of operations.

In a situation where a PPA is in place, if we fail to construct a wind energy project in a timely manner or do not deliver electricity in accordance with the applicable PPA, the PPA may be terminated and/or we could be required to pay liquidated damages.

Wind energy project revenues are highly dependent on suitable wind and associated weather conditions.

The energy and revenues generated at a wind energy project are highly dependent on climatic conditions, particularly wind conditions, which are variable and difficult to predict. Turbines will only operate within certain wind speed ranges that vary by turbine model and manufacturer, and there is no assurance that the wind resource at any given project site will fall within such specifications.

When we develop a wind energy project, we evaluate the quality of the wind resources at the selected site through a number of means, and we retain third-party experts to assist us in this evaluation. We base our investment decisions with respect to each wind energy project on the findings of wind studies conducted on-site before starting construction. We use the wind data that we gather to develop projections of the wind energy project’s performance, revenue generation, operating profit, debt capacity, tax equity capacity and return on investment, which are fundamental elements of our business planning. Wind resource projections at the start of commercial operations can also have a significant impact on the amount of third-party capital that we can raise, including the expected contributions by tax equity investors. However, actual climatic conditions at a project site, particularly wind conditions, may not conform to the findings of these wind studies, and, therefore, our wind energy projects may not meet anticipated production levels, which could adversely affect our forecasted profitability. In addition, global climate change could change existing wind patterns; such effects are impossible to predict.

14

The amount of electricity generated by a wind energy project depends upon many factors, including the quality of the wind resource, turbine performance, aerodynamic losses resulting from wear, degradation of turbine components, icing, required shutdowns and conditions on the electrical transmission network.

We project the net annual capacity factor for each project in our development portfolio. Net capacity factor is one element used in measuring the productivity of a wind turbine, wind energy project or any other power production facility. It compares the turbine’s production over a given period of time with the amount of power the turbine could have produced if it had run at full capacity for the same amount of time.

| Net Capacity Factor | = | Amount of power produced over time (usually measured annually) | ||

| Power that would have been produced if turbine operated at full capacity 100% of the time over the same period of time |

Our net capacity factor projections are subject to change and are not intended to predict the wind at any specific time over the turbine’s 20-year useful life. Even if our predictions of a wind energy project’s net capacity factor become validated over time, the energy projects may experience hours, days, months, and even years that are below our wind resource projections.

Projections of net capacity factor depend on wind resource projections, which rely upon assumptions such as wind speeds, interference between turbines, effects of vegetation and land use and terrain effects. The amount of electricity generated by a wind energy project depends upon many factors in addition to the quality of the wind resource, including turbine performance, aerodynamic losses resulting from wear on the wind turbine, degradation of turbine components, icing and the number of times an individual turbine or entire wind energy project may need to be shut down for maintenance or to avoid damage. In addition, conditions on the electrical transmission network can affect the amount of energy we can deliver to the network. Wind energy projects in our portfolio may fail to meet our energy production expectations in any given time period. If our wind energy projections are not realized, we could face a number of material issues, including:

| • | our energy sales may be significantly lower than we forecast; |

| • | our energy hedging arrangements may be adversely affected; |

| • | we may not produce sufficient energy to meet our forward REC sales and, as a result, we may have to buy RECs on the open market to cover our position; |

| • | we may earn fewer PTCs than projected, which would increase the period during which we must make certain distributions and allocations to our tax equity investors; and |

| • | our wind energy projects may not generate sufficient cash flow to make payments on principal and interest as they become due on our project related debt. |

If, as a result of inaccurate wind resource projections, the performance of one or more of our wind energy projects falls below our projected net capacity factor levels, our business, financial condition and results of operations could be materially adversely affected.

15

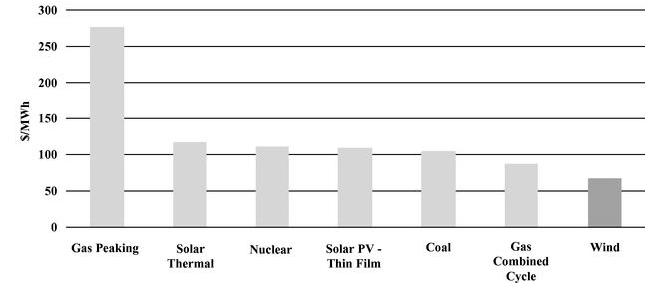

Volatile natural gas prices may adversely impact the market price for electricity.

Natural gas is one of the major sources of energy for the generation of electricity in the U.S. The prices for natural gas have been very volatile in recent months and years, with temporary highs in June-July of 2008 that were four times the prices in January 2002. Since June, the prices for natural gas used in electricity generation have fallen back to levels seen in December 2007 and January 2008. It is not possible to reliably predict what the price behavior for natural gas will be in the future. If prices continue to fall, they will adversely impact the economics for wind power, since natural gas-based generation is one of the chief competitors to wind energy. While there can be no assurance, in the long term we expect that the continuing need to control greenhouse gas emissions, and the fact that all fossil fuels are a finite resource, will allow wind power ot continue to compete favorably with natural gas.

A sustained decline in market prices for electricity may materially adversely affect our revenues and the growth of our business.

We may not be able to develop or operate our pipeline of development projects economically if there is a sustained material decline in market prices for electricity. Electricity prices are affected by various factors and may decline for many reasons that are not within our control, including changes in the cost or availability of fuel, regulation and acts of governments and regulators, changes in supply of generation capacity, changes in power transmission or fuel transportation capacity, seasonality, weather conditions and changes in demand for electricity. In addition, other power generators may develop alternative technologies to produce power, including fuel cells; clean coal and coal gasification; micro turbines; photovoltaic (solar) cells or tidal current based generators, or improve upon traditional technologies and equipment, such as more efficient gas turbines or nuclear or coal power plants with simplified and safer designs, among others. Advances in these or other technologies could cause a sustained decline in market prices for electricity. If there is a sustained decline in the market prices of electricity, we may not develop and construct our pipeline of development projects and grow our business, and/or we may not be able to operate completed projects economically, which would have a material adverse effect on our revenues.

While we will explore the viability of hedging against the possible drop of local electricity prices, in our anticipated spot market solid hedging instruments (with high correlations to the local power market price histories) may not be available, which would represent an overall risk to the success of the business model, and is a possible barrier to achieving project financing.

The continuing U.S. recession will adversely affect the price of electricity in the near term.

As the U.S. continues in recession, all prices in the economy, including the price of electricity, will experience downward pressure. To the extent that Crownbutte intends to use open market venues (i.e. the “merchant” markets) to sell power, variability of electricity prices are a risk to profitability in the short term. Over the long term, the demand for electricity is driven by the number of consumers, the numbers of electricity-powered devices employed and the efficiency of those devices.

A sustained decline in market prices for RECs may materially adversely affect our revenues and the growth of our business.

Similarly, if there is a sustained material decline in Renewable Energy Certificates (“RECs”) prices, we may not be able to achieve expected revenues, which would have an adverse effect on the investment returns on our projects. A REC is a stand-alone tradable instrument representing the attributes associated with one megawatt hour of energy produced from a renewable energy source. These attributes typically include reduced air and water pollution, reduced greenhouse gas emissions and increased use of domestic energy sources. Many states use RECs to track and verify compliance with their Renewable Portfolio Standards (“RPS”) programs, which vary among states, but generally require power suppliers to provide a minimum percentage or base amount of electricity from specified renewable energy sources for a given period of time. Retail energy suppliers can meet the requirements by purchasing RECs from renewable energy generators, in addition to producing or acquiring the electricity from renewable sources.

16

Our hedging strategy may not adequately manage our commodity price risk, may expose us to significant losses and may limit our ability to benefit from higher electricity prices.

Our ownership and operation of wind energy projects will expose us to volatility in market prices of electricity and RECs. In an effort to stabilize our returns from electricity sales, we intend to carefully review the electricity sale options for each of our development projects. As part of this review, we will assess the appropriateness of entering into a fixed price PPA and/or a financial hedge. If we sell our electricity into a liquid ISO market, we may enter into a financial hedge with institutional investors in order to stabilize our projected revenue stream.

Under the terms of our anticipated financial hedges, we would not be obligated to physically deliver or purchase electricity, but we would receive payments for certain quantities of electricity based on a fixed price and would be obligated to pay the market electricity price for the same quantities of electricity. Thus, if market prices of electricity increase, we are obligated to make payments under these financial hedges. Our financial hedges will cover quantities of electricity that we estimate we can produce with a high degree of certainty. As a result, gains or losses under the financial hedges should be offset by decreases or increases in our revenues from spot sales of electricity in liquid ISO markets. However, the actual amount of electricity we generate from operations may be materially different from our estimates for a variety of reasons, including variable wind conditions, catastrophic events such as fires, earthquakes, storms and changes in weather patterns due to climate change. To the extent actual amounts produced fall short of the quantities covered in our financial hedges, we will not be hedged and we will be exposed to commodity price risk. In the event a project does not generate the amount of electricity covered by the related hedge, we could incur significant losses under the financial hedge if electricity prices rise substantially above the fixed prices provided for in the hedge. If a project generates more electricity than is covered by the relevant hedge, the excess production will not be hedged and the revenues we derive will be subject to market price fluctuations.

We may seek to sell forward a portion of our RECs in an effort to hedge against future declines in REC prices. If our projects are unable to generate the amount of electricity required to earn the RECs sold forward or if we are unable for any reason to qualify our electricity for RECs in relevant states, we may incur significant losses.

We may be required to post cash collateral and issue letters of credit for obligations under hedging arrangements, which may not be available on acceptable terms and if available would reduce our capacity to borrow for other purposes. Our inability to effectively manage market risks and our hedging activities may have a material adverse effect on our business, financial condition or results of operations. In addition, our hedging activities may also limit our ability to realize the full benefit of increases in electricity prices and RECs. See “Management’s Discussion and Analysis of Financial Condition and Results of operations—Hedging.”

We will be dependent upon the continued and uninterrupted operation of a limited number of operating wind parks in a limited geographic area.

We intend to shift the focus of our business towards ownership and operation of merchant wind parks, but we currently have no owned wind energy projects in operation, and we anticipate having only a limited number of wind parks in operation over the next two years. As a result, in future our operations may be subject to material interruption if any of our wind parks is damaged or otherwise adversely affected by one or more accidents, severe weather or other natural disasters. Tornados, lightning strikes, floods, severe storms, wildfires or other exceptional weather conditions or natural disasters could damage our wind energy projects and related facilities and decrease production levels. These events could have a material adverse effect on our revenues, particularly to the extent that they affect multiple wind energy projects and project sites. In addition, a majority of our planned wind parks will be located in the three-state region of North Dakota, South Dakota and Montana. If any of our future operating wind parks experiences material interruptions or if the regulatory environment or energy market characteristics in these states were to change in a manner adverse to us, it could have an adverse effect on our business, results of operations and financial condition.

17

Factors beyond our control could cause us to experience increased costs with respect to our wind energy projects.

Factors such as:

| · | increases in the costs of labor or materials, |

| · | higher than anticipated financing costs for our wind energy projects, |

| · | non-performance by third-party suppliers or subcontractors, |

| · | turbine breakdowns, |

| · | electricity network and other utility service failures, and |

| · | major incidents and/or catastrophic events, such as fires, earthquakes or storms, |

may cause us to experience increased costs with respect to our wind energy projects and have a material adverse effect on our business, financial condition and results of operations.