Pacific Oak Strategic Opportunity REIT (PCOK)

Filed: 27 Oct 10, 12:00am

Filed Pursuant to Rule 424(b)(3)

Registration No. 333-156633

| KBS STRATEGIC OPPORTUNITY REIT, INC. | |||

| Maximum Offering of 140,000,000 Shares of Common Stock | ||||

| Minimum Offering of 250,000 Shares of Common Stock |

KBS Strategic Opportunity REIT, Inc. is a newly organized Maryland corporation that intends to qualify as a real estate investment trust beginning with the taxable year that will end December 31, 2010. We expect to use substantially all of the net proceeds from this offering to invest in and manage a diverse portfolio of real estate-related loans, real estate-related debt securities and other real estate-related investments. We intend to originate and acquire mortgage, mezzanine, bridge and other real estate-related loans, to invest in real estate-related debt securities such as residential and commercial mortgage-backed securities and collateralized debt obligations and to invest in various types of opportunistic real estate. In addition, we may acquire equity securities of companies that make similar investments. We may make our investments through loan origination and the acquisition of individual assets or by acquiring portfolios of assets, other mortgage REITs or companies with investment objectives similar to ours. Because we have not yet identified any specific assets to acquire, we are considered a blind pool.

We are offering up to 100,000,000 shares of common stock in our primary offering for $10 per share, with volume discounts available to investors who purchase more than $1,000,000 of shares through the same participating broker-dealer. Discounts are also available for other categories of investors. We are also offering up to 40,000,000 shares pursuant to our dividend reinvestment plan at a purchase price initially equal to $9.50 per share. We expect to offer shares of common stock in our primary offering until one year from breaking escrow in this offering.

Investing in our common stock involves a high degree of risk. See “Risk Factors” beginning on page23 to read about risks you should consider before buying shares of our common stock. These risks include the following:

| • | Our charter does not require our directors to seek stockholder approval to liquidate our assets by a specified date, nor does our charter require our directors to list our shares for trading by a specified date. No public market currently exists for our shares, and we have no plans to list our shares on an exchange. Until our shares are listed, if ever, you may not sell your shares unless the buyer meets the applicable suitability and minimum purchase standards. If you are able to sell your shares, you would likely have to sell them at a substantial loss. |

| • | No one may own more than 9.8% of our stock unless exempted by our board. |

| • | We set the offering price of our shares arbitrarily. This price is unrelated to the book or net value of our assets or to our expected operating income. |

| • | We depend on our advisor to conduct our operations. Our advisor has a limited operating history. |

| • | We have no operating history, and as of December 31, 2009, our total assets consist of $192,656 cash. We have not identified any investments to acquire. |

| • | All of our executive officers, some of our directors and other key real estate and debt finance professionals are also officers, directors, managers, key professionals and/or holders of a controlling interest in our advisor, our dealer manager and other affiliated KBS entities. As a result, they will face conflicts of interest, including significant conflicts created by our advisor’s compensation arrangements with us and other KBS-advised programs and investors. Fees paid to our advisor in connection with transactions involving the origination, acquisition and management of our investments will be based on the cost of the investment, not on the quality of the investment or services rendered to us. This arrangement could influence our advisor to recommend riskier transactions to us. |

| • | If we raise substantially less than the maximum offering, we may not be able to invest in a diverse portfolio of real estate-related loans, real estate-related debt securities and other real estate-related investments and the value of your investment may vary more widely with the performance of specific assets. |

| • | We will pay substantial fees and expenses to our advisor, its affiliates and participating broker-dealers. These fees increase your risk of loss. |

| • | Our organizational documents do not restrict us from paying distributions from any source and do not restrict the amount of distributions we may pay from any source, including offering proceeds. Distributions paid from sources other than current or accumulated earnings and profits may constitute a return of capital. |

| • | We may incur debt exceeding 75% of the cost of our tangible assets with the approval of the conflicts committee. Higher debt levels increase the risk of your investment. |

| • | Continued disruptions in the financial markets and uncertain economic conditions could adversely affect our ability to implement our business strategy and generate returns to you. |

| • | We may invest in residential and commercial mortgage-backed securities, collateralized debt obligations and other structured debt securities as well as real estate-related loans. Many of these types of investments have become illiquid and considerably less valuable over the past two years. This reduced liquidity and decrease in value caused financial hardship for many investors in these assets. Many investors did not fully appreciate the risks of such investments. We can give you no assurances that our investments in these assets will be successful. |

Neither the SEC, the Attorney General of the State of New York nor any other state securities regulator has approved or disapproved of our common stock, determined if this prospectus is truthful or complete or passed on or endorsed the merits of this offering. Any representation to the contrary is a criminal offense.

This investment involves a high degree of risk. You should purchase these securities only if you can afford a complete loss of your investment. The use of projections or forecasts in this offering is prohibited. No one is permitted to make any oral or written predictions about the cash benefits or tax consequences you will receive from your investment.

Price to Public | Selling Commissions | Dealer Manager Fee | Net Proceeds (Before Expenses) | |||||||||||||

Primary Offering | ||||||||||||||||

Per Share | $ | 10.00 | * | $ | 0.65 | * | $ | 0.30 | * | $ | 9.05 | |||||

Total Minimum | $ | 2,500,000.00 | * | $ | 162,500.00 | * | $ | 75,000.00 | * | $ | 2,262,500.00 | |||||

Total Maximum | $ | 1,000,000,000.00 | * | $ | 65,000,000.00 | * | $ | 30,000,000.00 | * | $ | 905,000,000.00 | |||||

Dividend Reinvestment Plan | ||||||||||||||||

Per Share | $ | 9.50 | $ | 0.00 | $ | 0.00 | $ | 9.50 | ||||||||

Total Maximum | $ | 380,000,000.00 | $ | 0.00 | $ | 0.00 | $ | 380,000,000.00 | ||||||||

| * | Discounts are available for some categories of investors. Reductions in commissions and fees will result in corresponding reductions in the purchase price. |

The dealer manager, KBS Capital Markets Group LLC, our affiliate, is not required to sell any specific number or dollar amount of shares but will use its best efforts to sell the shares offered. The minimum permitted purchase is $4,000, except that Tennessee investors must invest at least $5,000. We will not sell any shares unless we raise gross offering proceeds of $2,500,000 from persons who are not affiliated with us or our advisor by November 20, 2010. Pending satisfaction of this condition, all subscription payments will be placed in an account held by the escrow agent, UMB Bank, N.A., in trust for our subscribers’ benefit, pending release to us. You are entitled to receive the interest earned on your subscription payment while it is held in the escrow account. Once we have raised the minimum offering amount and instructed the escrow agent to disburse the funds in the account, funds representing the gross purchase price for the shares will be distributed to us and the escrow agent will disburse directly to you any interest earned on your subscription payment while it was held in the escrow account, without reduction for fees. If we do not raise gross offering proceeds of $2,500,000 by November 20, 2010 we will promptly return all funds in the escrow account (including interest), and we will stop offering shares. We will not deduct any fees if we return funds from the escrow account because we are unable to raise the minimum offering amount.

We expect to sell the 100,000,000 shares registered in our primary offering within one year of breaking escrow. If we have not sold all of the shares within one year from breaking escrow, we may continue this offering until November 20, 2012. If we decide to extend the primary offering period, we will provide that information in a prospectus supplement. We may continue to offer shares under our dividend reinvestment plan after the primary offering terminates until we have sold 40,000,000 shares through the reinvestment of distributions. In many states, we will need to renew the registration statement or file a new registration statement to continue the offering beyond November 20, 2010. We may terminate this offering at any time.

We will not sell any shares to Pennsylvania investors unless we raise $33.4 million in gross offering proceeds (including sales made to residents of other jurisdictions) from persons not affiliated with us or our advisor. If we do not raise this amount within one year of breaking escrow in this offering, we will promptly return all funds held in escrow for the benefit of Pennsylvania investors. In addition, we will not sell any shares to Tennessee investors unless we raise $20 million in gross offering proceeds (including sales made to residents of other jurisdictions) from persons not affiliated with us or our advisor. If we do not raise this amount within one year of breaking escrow in this offering, we will promptly return all funds held in escrow for the benefit of Tennessee investors.

The date of this prospectus is March 31, 2010.

The shares we are offering through this prospectus are suitable only as a long-term investment for persons of adequate financial means and who have no need for liquidity in this investment. Because there is no public market for our shares, you will have difficulty selling your shares.

In consideration of these factors, we have established suitability standards for investors in this offering and subsequent purchasers of our shares. These suitability standards require that a purchaser of shares have either:

| • | a net worth of at least $250,000; or |

| • | gross annual income of at least $70,000 and a net worth of at least $70,000. |

In addition, the states listed below have established suitability requirements that are more stringent than ours and investors in these states are directed to the following special suitability standards:

| • | Kansas and Massachusetts – It is recommended by the office of the Kansas Securities Commissioner that Kansas investors not invest, and by the Massachusetts Securities Division that Massachusetts investors not invest, in the aggregate, more than 10% of their liquid net worth in this and similar direct participation investments. Liquid net worth is defined as that portion of net worth that consists of cash, cash equivalents and readily marketable securities. Massachusetts investors must also have either (a) a net worth of at least $300,000 or (b) a gross annual income of at least $90,000 and a net worth of at least $90,000. |

| • | California – Investors must have either (a) a net worth of at least $350,000 or (b) a gross annual income of at least $85,000 and a net worth of at least $250,000. In addition, shares will only be sold to California residents that have a liquid net worth of at least 10 times their investment in us. |

| • | Iowa – Investors must have either (a) a net worth of at least $350,000 or (b) a gross annual income of at least $70,000 and a net worth of at least $100,000. In addition, shares will only be sold to Iowa residents that have a liquid net worth of at least 10 times their investment in us. |

| • | Kentucky, Pennsylvania and Tennessee – Investors must have a liquid net worth of at least 10 times their investment in us. |

| • | Alabama, Michigan and Oregon – Investors must have a liquid net worth of at least 10 times their investment in us and our affiliates. |

In addition, because the minimum offering amount is less than $66,666,666, Pennsylvania investors are cautioned to carefully evaluate our ability to fully accomplish our stated objectives and to inquire as to the current dollar volume of subscriptions.

For purposes of determining the suitability of an investor, net worth in all cases should be calculated excluding the value of an investor’s home, home furnishings and automobiles. In the case of sales to fiduciary accounts, these suitability standards must be met by the fiduciary account, by the person who directly or indirectly supplied the funds for the purchase of the shares if such person is the fiduciary or by the beneficiary of the account.

Our sponsor, those selling shares on our behalf and participating broker-dealers and registered investment advisors recommending the purchase of shares in this offering must make every reasonable effort to determine that the purchase of shares in this offering is a suitable and appropriate investment for each stockholder based on information provided by the stockholder regarding the stockholder’s financial situation and investment objectives. See “Plan of Distribution — Suitability Standards” for a detailed discussion of the determinations regarding suitability that we require.

i

| i | ||||

| 1 | ||||

| 23 | ||||

| 23 | ||||

| 28 | ||||

| 30 | ||||

| 37 | ||||

| 49 | ||||

| 51 | ||||

| 53 | ||||

| 59 | ||||

| 61 | ||||

| 62 | ||||

| 65 | ||||

| 65 | ||||

| 66 | ||||

| 66 | ||||

| 69 | ||||

| 70 | ||||

Limited Liability and Indemnification of Directors, Officers, Employees and Other Agents | 70 | |||

| 71 | ||||

| 74 | ||||

| 75 | ||||

| 75 | ||||

| 78 | ||||

| 79 | ||||

| 85 | ||||

| 85 | ||||

| 85 | ||||

Receipt of Fees and Other Compensation by KBS Capital Advisors and its Affiliates | 87 | |||

Fiduciary Duties Owed by Some of Our Affiliates to Our Advisor and Our Advisor’s Affiliates | 87 | |||

| 87 | ||||

| 88 | ||||

| 93 | ||||

| 93 | ||||

| 94 | ||||

| 101 | ||||

| 102 | ||||

| 102 | ||||

| 104 | ||||

| 104 | ||||

| 105 | ||||

Investment Limitations to Avoid Registration as an Investment Company | 106 | |||

| 110 | ||||

| 111 | ||||

| 115 | ||||

| 116 | ||||

| 117 | ||||

| 117 | ||||

| 121 | ||||

| 122 | ||||

| 136 | ||||

| 140 | ||||

| 141 |

ii

| 141 | ||||

| 142 | ||||

| 142 | ||||

| 144 | ||||

| 144 | ||||

| 146 | ||||

| 146 | ||||

| 146 | ||||

| 147 | ||||

Advance Notice for Stockholder Nominations for Directors and Proposals of New Business | 147 | |||

| 147 | ||||

| 149 | ||||

| 150 | ||||

| 150 | ||||

| 151 | ||||

| 152 | ||||

| 152 | ||||

| 152 | ||||

| 155 | ||||

| 157 | ||||

| 157 | ||||

| 159 | ||||

| 159 | ||||

| 159 | ||||

| 159 | ||||

| 160 | ||||

| 160 | ||||

| 161 | ||||

| 161 | ||||

| 161 | ||||

| 161 | ||||

| 162 | ||||

| 162 | ||||

Compensation of Dealer Manager and Participating Broker-Dealers | 162 | |||

| 167 | ||||

| 168 | ||||

| 169 | ||||

| 169 | ||||

| 169 | ||||

| 170 | ||||

| 171 | ||||

| 171 | ||||

| 171 | ||||

| 172 | ||||

| 172 | ||||

Appendix A – Form of Subscription Agreement with Instructions | A-1 | |||

Appendix B – Amended and Restated Dividend Reinvestment Plan | B-1 |

iii

This prospectus summary highlights material information contained elsewhere in this prospectus. Because it is a summary, it may not contain all of the information that is important to you. To understand this offering fully, you should read the entire prospectus carefully, including the “Risk Factors” section and the financial statements, before making a decision to invest in our common stock.

What is KBS Strategic Opportunity REIT, Inc.?

KBS Strategic Opportunity REIT, Inc. is a newly organized Maryland corporation that intends to qualify as a real estate investment trust, or REIT, beginning with the taxable year that will end December 31, 2010. We expect to use substantially all of the net proceeds from this offering to invest in and manage a diverse portfolio of real estate-related loans, real estate-related debt securities and other real estate-related investments. We intend to originate and acquire mortgage, mezzanine, bridge and other real estate-related loan, to invest in real estate-related debt securities such as residential and commercial mortgage-backed securities and collateralized debt obligations and to invest in various types of opportunistic real estate. In addition, we may acquire equity securities of companies that make similar investments. We may make our investments through loan origination and the acquisition of individual assets or by acquiring portfolios of assets, other mortgage REITs or companies with investment objectives similar to ours. We plan to diversify our portfolio by investment type, investment size and investment risk with the goal of attaining a portfolio of income-producing assets that provide attractive and stable returns to our investors. We intend to structure, underwrite and originate many of the debt products in which we invest.

We were incorporated in the State of Maryland on October 8, 2008 and we have not yet made any investments. Because we have not yet identified any specific assets to originate or acquire, we are considered to be a blind pool. We plan to own substantially all of our assets and conduct our operations through KBS Strategic Opportunity Limited Partnership, which we refer to as our Operating Partnership in this prospectus. We are the sole general partner of the Operating Partnership and, as of the date of this prospectus, our wholly owned subsidiary, KBS Strategic Opportunity Holdings LLC, is the sole limited partner of the Operating Partnership. Except where the context suggests otherwise, the terms “we,” “us,” “our” and “our company” refer to KBS Strategic Opportunity REIT, Inc., together with its subsidiaries, including the Operating Partnership and its subsidiaries, and all assets held through such subsidiaries.

Our external advisor, KBS Capital Advisors, will conduct our operations and manage our portfolio of investments. We have no paid employees.

Our office is located at 620 Newport Center Drive, Suite 1300, Newport Beach, California 92660. Our telephone number is (949) 417-6500. Our fax number is (949) 417-6520, and our web site address is www.kbsstrategicopportunityreit.com.

What is a mortgage REIT?

In general, a mortgage REIT is an entity that:

| • | combines the capital of many investors to invest in notes or other evidences of indebtedness or obligations secured or collateralized by real estate owned by the borrowers in connection with financing provided by us; |

| • | allows individual investors to invest in a professionally managed, large-scale, diversified portfolio of real estate-related investments; |

| • | pays distributions to investors of at least 90% of its annual REIT taxable income (computed without regard to the dividends paid deduction and excluding net capital gain); and |

| • | avoids the “double taxation” treatment of income that normally results from investments in a corporation because a REIT is not generally subject to federal corporate income taxes on that portion of its income distributed to its stockholders, provided certain income tax requirements are satisfied. |

1

However, under the Internal Revenue Code of 1986, as amended (the “Internal Revenue Code”), REITs are subject to numerous organizational and operational requirements. If we fail to qualify for taxation as a REIT in any year after electing REIT status, our income will be taxed at regular corporate rates, and we may be precluded from qualifying for treatment as a REIT for the four-year period following our failure to qualify. Even if we qualify as a REIT for federal income tax purposes, we may still be subject to state and local taxes on our income and property and to federal income and excise taxes on our undistributed income.

What are your investment objectives?

Our primary investment objectives are:

| • | to provide you with attractive and stable returns; and |

| • | to preserve and return your capital contribution. |

We will also seek to realize growth in the value of our investments by timing asset sales to maximize asset value.

We may return all or a portion of your capital contribution in connection with the sale of the company or the assets we will acquire or upon maturity or payoff of our debt investments. Alternatively, you may be able to obtain a return of all or a portion of your capital contribution in connection with the sale of your shares.

Though we intend to authorize and declare distributions when our board of directors determines we have sufficient cash flow, we may be unable or limited in our ability to make distributions to our stockholders. Further, no public trading market for our shares currently exists and, until our shares are listed, if ever, it may be difficult for you to sell your shares. Until our shares are listed, you may not sell your shares unless the buyer meets the applicable suitability and minimum purchase standards.

Are there any risks involved in an investment in your shares?

Investing in our common stock involves a high degree of risk. You should carefully review the “Risk Factors” section of this prospectus beginning on page 23, which contains a detailed discussion of the material risks that you should consider before you invest in our common stock. Some of the more significant risks relating to an investment in our shares include:

| • | Our charter does not require our directors to seek stockholder approval to liquidate our assets by a specified date, nor does our charter require our directors to list our shares for trading by a specified date. No public market currently exists for our shares of common stock, and we currently have no plans to list our shares on a national securities exchange. Until our shares are listed, if ever, you may not sell your shares unless the buyer meets the applicable suitability and minimum purchase standards. In addition, our charter prohibits the ownership of more than 9.8% of our stock, unless exempted by our board of directors, which may inhibit large investors from purchasing your shares. Our shares cannot be readily sold and, if you are able to sell your shares, you would likely have to sell them at a substantial discount from their public offering price. |

| • | We established the offering price of our shares on an arbitrary basis. This price may not be indicative of the price at which our shares would trade if they were listed on an exchange or actively traded, and this price bears no relationship to the book or net value of our assets or to our expected operating income. |

| • | We are dependent on our advisor to select investments and conduct our operations. Our advisor has a limited operating history. This inexperience makes our future performance difficult to predict. |

| • | We have no operating history and, as of December 31, 2009, our total assets consist of $192,656 cash. Because we have not identified any assets to originate or acquire with proceeds from this offering, you will not have an opportunity to evaluate our investments before we make them, making an investment in us more speculative. |

| • | We may change our targeted investments and investment guidelines at any time without the consent of our stockholders, which could result in our making investments that are different from, and possibly riskier than, the investments described in this prospectus. |

2

| • | All of our executive officers, some of our directors and other key real estate and debt finance professionals are also officers, directors, managers, key professionals and/or holders of a direct or indirect controlling interest in our advisor, our dealer manager and other affiliated KBS entities. As a result, all of our executive officers, some of our directors and other key real estate and debt finance professionals and our advisor and its affiliates will face conflicts of interest, including significant conflicts created by our advisor’s compensation arrangements with us and other programs and investors advised by KBS affiliates and conflicts in allocating time among us and these other programs and investors. Furthermore, these individuals may become employees of another KBS-sponsored program in an internalization transaction or, if we internalize our advisor, may not become our employees as a result of their relationship with other KBS-sponsored programs. These conflicts could result in action or inaction that is not in the best interests of our stockholders. |

| • | Our advisor and its affiliates will receive fees in connection with transactions involving the origination, acquisition and management of our investments. These fees will be based on the cost of the investment, and not based on the quality of the investment or the quality of the services rendered to us. This may influence our advisor to recommend riskier transactions to us. |

| • | We may also pay significant fees during our listing/liquidation stage. Although most of the fees payable during our listing/liquidation stage are contingent on our investors first enjoying agreed-upon investment returns, affiliates of KBS Capital Advisors could also receive significant payments even without our reaching the investment-return thresholds should we seek to become self-managed. Due to the apparent preference of the public markets for self-managed companies, a decision to list our shares on a national securities exchange might well be preceded by a decision to become self-managed. And given our advisor’s familiarity with our assets and operations, we might prefer to become self-managed by acquiring entities affiliated with our advisor. Such an internalization transaction could result in significant payments to affiliates of our advisor irrespective of whether you enjoyed the returns on which we have conditioned other incentive compensation. |

| • | If we raise substantially less than the maximum offering, we may not be able to invest in a diverse portfolio of real estate-related loans, real estate-related debt securities and other real estate-related investments and the value of your investment may vary more widely with the performance of specific assets. |

| • | We will pay substantial fees to and expenses of our advisor, its affiliates and participating broker-dealers, which payments increase the risk that you will not earn a profit on your investment. |

| • | Our distribution policy is not to use the proceeds of this offering to make distributions. However, our organizational documents do not restrict us from paying distributions from any source and do not restrict the amount of distributions we may pay from any source, including offering proceeds. Distributions paid from sources other than current or accumulated earnings and profits may constitute a return of capital. |

| • | If we are unable to find suitable investments, we may not be able to achieve our investment objectives or pay distributions. |

| • | Our policies do not limit us from incurring debt until our borrowings would exceed 75% of the cost of our tangible assets, and we may exceed this limit with the approval of the conflicts committee of our board of directors. High debt levels could limit the amount of cash we have available to distribute and could result in a decline in the value of your investment. |

| • | Continued disruptions in the financial markets and deteriorating economic conditions could adversely affect our ability to implement our business strategy and generate returns to you. |

| • | We may invest in residential and commercial mortgage-backed securities, collateralized debt obligations and other structured debt securities as well as real estate-related loans. Many of these types of investments have become illiquid and considerably less valuable over the past two years. This reduced liquidity and decrease in value caused financial hardship for many investors in these assets. Many investors did not fully appreciate the risks of such investments. We can give you no assurances that our investments in these assets will be successful. |

3

What is the role of the board of directors?

We operate under the direction of our board of directors, the members of which are accountable to us and our stockholders as fiduciaries. There are five members of our board of directors, three of which are independent of KBS Capital Advisors and its affiliates. Our charter requires that a majority of our directors be independent of KBS Capital Advisors and creates a committee of our board consisting solely of all of our independent directors. This committee, which we call the conflicts committee, is responsible for reviewing the performance of KBS Capital Advisors and must approve other matters set forth in our charter. Our directors are elected annually by the stockholders.

Who is your advisor and what will the advisor do?

KBS Capital Advisors LLC is our advisor. As our advisor, KBS Capital Advisors will manage our day-to-day operations and our portfolio of real estate-related investments on our behalf, all subject to the supervision of our board of directors. Our sponsors, Peter M. Bren, Keith D. Hall, Peter McMillan III and Charles J. Schreiber, Jr., and their team of real estate and debt finance professionals acting through KBS Capital Advisors will make most of the decisions regarding the selection, negotiation, financing and disposition of investments. KBS Capital Advisors also has the authority to make all of the decisions regarding our investments, subject to the limitations in our charter and the direction and oversight of our board of directors. KBS Capital Advisors will also provide asset-management, marketing, investor-relations and other administrative services on our behalf with the goal of maximizing our operating cash flow.

Our advisor has a limited operating history. As of the date of this prospectus, its operations have consisted solely of serving as the external advisor to KBS Real Estate Investment Trust, Inc., which launched its initial public offering and commenced real estate operations in 2006, and KBS Real Estate Investment Trust II, Inc., which launched its initial public offering and commenced real estate operations in 2008. KBS Capital Advisors will also serve as the advisor to KBS Real Estate Investment Trust III, Inc. and KBS Legacy Partners Apartment REIT, Inc. As of the date of this prospectus, the initial public offering of KBS Real Estate Investment Trust III, Inc. is in registration with the SEC. KBS Legacy Partners Apartment REIT, Inc. launched its initial public offering in March 2010 but as of the date of this prospectus, it has not broken escrow in its offering.

What is the experience of your sponsors and the real estate and debt finance professionals of your advisor?

Peter M. Bren, Keith D. Hall, Peter McMillan III and Charles J. Schreiber, Jr. control and indirectly own our advisor and the dealer manager of this offering. We refer to these individuals as our “sponsors.” Messrs. Bren and Schreiber are the managers of our advisor, although all four of our sponsors actively participate in the management and operations of our advisor. Our sponsors each have over 17 years of experience investing in real estate-related debt investments.

Our sponsors work together at KBS Capital Advisors with their team of real estate and debt finance professionals. These senior real estate and debt finance professionals have been through multiple financial cycles in their careers and have the expertise gained through hands-on experience in acquisitions, originations, loan workouts, asset management, dispositions, development, leasing and property and portfolio management. In particular, Geoffrey Hawkins has over 21 years of experience investing in real estate-related investments, with 19 years of experience specifically related to real estate-related debt investments, and Brian Ragsdale has over 19 years of experience investing in real estate-related investments, with 10 years of experience specifically related to real estate-related debt investments. Together with our four sponsors, Messrs. Hawkins and Ragsdale comprise the investment committee of KBS Capital Advisors that is responsible for our investment decisions. Subject to the limitations in our charter and the oversight of our board of directors, the investment committee of KBS Capital Advisors evaluates and approves our investments and financings.

4

On January 27, 2006, our four sponsors launched the initial public offering of KBS Real Estate Investment Trust, Inc., which we refer to as KBS REIT I in this prospectus. As of December 31, 2009, KBS REIT I had accepted aggregate gross offering proceeds of approximately $1.8 billion, including $129.5 million from shares issued pursuant to its dividend reinvestment plan. Of the amount raised pursuant to its dividend reinvestment plan, as of December 31, 2009, $51.3 million has been used to fund share redemptions pursuant to its share redemption program. KBS REIT I ceased offering shares in its primary initial public offering on May 30, 2008. On April 22, 2008, our four sponsors launched the initial public offering of KBS Real Estate Investment Trust II, Inc., which we refer to as KBS REIT II in this prospectus. As of December 31, 2009, KBS REIT II had accepted aggregate gross offering proceeds of approximately $929.9 million, including $23.2 million from shares issued pursuant to its dividend reinvestment plan. Of the amount raised pursuant to its dividend reinvestment plan, as of December 31, 2009, $1.9 million has been used to fund share redemptions pursuant to its share redemption program. KBS REIT II’s offering is expected to last until August 31, 2010, but KBS REIT II may extend its offering beyond that date. Our sponsors are also sponsoring KBS Real Estate Investment Trust III, Inc. and, together with Legacy Partners Residential Realty LLC and certain of its affiliates, our sponsors are also sponsoring KBS Legacy Partners Apartment REIT, Inc. KBS Real Estate Investment Trust III, Inc. and KBS Legacy Partners Apartment REIT, Inc. are each public real estate investment trusts. As of the date of this prospectus, the initial public offering of KBS Real Estate Investment Trust III, Inc. is in registration with the SEC. KBS Legacy Partners Apartment REIT, Inc. launched its initial public offering in March 2010 but as of the date of this prospectus, it has not broken escrow in its offering. In this prospectus, we refer to KBS Real Estate Investment Trust III, Inc. as KBS REIT III and we refer to KBS Legacy Partners Apartment REIT, Inc. as KBS Legacy Partners Apartment REIT.

Our advisor, KBS Capital Advisors, is the external advisor of KBS REIT I, KBS REIT II, KBS REIT III and KBS Legacy Partners Apartment REIT, and some or all of our sponsors are directors and/or executive officers of KBS REIT I, KBS REIT II, KBS REIT III and KBS Legacy Partners Apartment REIT. Through their affiliations with KBS REIT I, KBS REIT II and KBS Capital Advisors, as of December 31, 2009, our sponsors have overseen the investment in and management of approximately $3.8 billion of real estate and real estate-related investments on behalf of the investors in KBS REIT I and KBS REIT II, including $1.2 billion of real estate-related debt investments.

Since 1992, Messrs. Bren and Schreiber have teamed to invest in, manage and sell real estate and real estate-related investments on behalf of institutional investors. Together, Messrs. Bren and Schreiber founded KBS Realty Advisors, a registered investment advisor with the Securities and Exchange Commission (the “SEC”) and a nationally recognized real estate investment advisor. When we refer to a “KBS-sponsored” fund or program, we are referring to the private entities sponsored by an investment advisor affiliated with Messrs. Bren and Schreiber and KBS REIT I, KBS REIT II, KBS REIT III and KBS Legacy Partners Apartment REIT, the public, non-traded REITs that are currently being sponsored by Messrs. Bren, Hall, McMillan and Schreiber. When we refer to a “KBS-advised” investor, we are referring to institutional investors that have engaged an investment advisor affiliated with Messrs. Bren and Schreiber to provide real estate-related investment advice.

Messrs. Bren and Schreiber each have been involved in real estate development, management, acquisition, disposition and financing for more than 36 years, and with the acquisition, origination, management, disposition and financing of real estate-related debt investments for more than 17 years. Since 1992, the experience of the investment advisors affiliated with Messrs. Bren and Schreiber includes (as of December 31, 2009) sponsoring 14 private real estate funds that have invested approximately $3.3 billion (including equity, debt and investment of income and sales proceeds) in 288 real estate assets and, through five of these private funds, acquiring and originating mortgage loans, investing in commercial mortgage-backed securities, and managing and disposing of such investments.

In addition to their experience with these 14 funds referenced above, investment advisors affiliated with Messrs. Bren and Schreiber have also been engaged by four institutional investors to recommend real estate acquisitions and manage some of their investments. The amounts paid for the assets acquired and/or managed pursuant to these arrangements and for subsequent capital expenditures totaled over $3.9 billion, including the acquisition of $285 million in mortgage loans.

5

With respect to the experience of Messrs. Hall and McMillan, each has over 26 years of experience in real estate-related debt investments. Prior to founding KBS Capital Advisors with Messrs. Bren and Schreiber in 2004, Messrs. Hall and McMillan founded Willowbrook Capital Group, LLC, an asset-management company. Prior to forming Willowbrook in 2000, Mr. McMillan served as the Executive Vice President and Chief Investment Officer of SunAmerica Investments, Inc., which was later acquired by AIG. As Chief Investment Officer, he was responsible for over $75 billion in assets, including residential and commercial mortgage-backed securities, public and private investment grade and non-investment grade corporate bonds and commercial mortgage loans and real estate investments.

Prior to forming Willowbrook, Mr. Hall was a Managing Director at CS First Boston, where he managed CSFB’s distribution strategy and business development for the Principal Transaction Group’s $18 billion real estate securities portfolio. Before joining CSFB in 1996, he served as a Director in the Real Estate Products Group at Nomura Securities, with responsibility for the company’s $6 billion annual pipeline of fixed-income securities. Mr. Hall spent the 1980s as a Senior Vice President in the High Yield Department of Drexel Burnham Lambert’s Beverly Hills office, where he was responsible for distribution of the group’s high-yield real estate securities.

Will you use leverage?

Yes. We expect that once we have fully invested the proceeds of this offering, our debt financing will be 30% or less of the cost of our investments, although it may exceed this level during our offering stage. Our charter limits our borrowings to 75% of the cost of our tangible assets; however, we may exceed that limit if a majority of the conflicts committee approves each borrowing in excess of our charter limitation and we disclose such borrowing to our stockholders in our next quarterly report with an explanation from the conflicts committee of the justification for the excess borrowing. There is no limitation on the amount we may borrow for the purchase of any single asset.

We do not intend to exceed the leverage limit in our charter. Careful use of debt will help us to achieve our diversification goals because we will have more funds available for investment. However, high levels of debt could cause us to incur higher interest charges and higher debt service payments, which would decrease the amount of cash available for distribution to our investors.

6

What conflicts of interest will your advisor face?

KBS Capital Advisors and its affiliates will experience conflicts of interest in connection with the management of our business. Messrs. Bren, Hall, McMillan and Schreiber, who indirectly own and control KBS Capital Advisors, are our sponsors, and Messrs. Hall and McMillan are two of our executive officers and directors. KBS Capital Advisors is also the external advisor to KBS REIT I, KBS REIT II, KBS REIT III and KBS Legacy Partners Apartment REIT. Messrs. Bren, Hall, McMillan and Schreiber are executive officers of KBS REIT I, KBS REIT II and KBS REIT III, and Messrs. McMillan and Schreiber are also directors of KBS REIT I, KBS REIT II and KBS REIT III. In addition, Messrs. Bren and McMillan are executive officers of KBS Legacy Partners Apartment REIT, and Mr. Bren is a director of KBS Legacy Partners Apartment REIT. Messrs. Bren and Schreiber are also key real estate and debt finance professionals at KBS Realty Advisors and its affiliates, the advisors to the private KBS-sponsored programs and the investment advisors to institutional investors in real estate and real estate-related assets. In addition, Geoffrey Hawkins and Brian Ragsdale play a key role at KBS Capital Advisors in identifying, structuring and managing the debt-related investments for KBS REIT I, KBS REIT II and us and they will play a key role in identifying, structuring and managing the debt-related investments for KBS REIT III. Some of the material conflicts that KBS Capital Advisors and its affiliates will face include the following:

| • | Our sponsors and their team of real estate and debt finance professionals must determine which investment opportunities to recommend to us and the other KBS-sponsored programs that are raising funds for investment as of the date of this prospectus for whom KBS serves as an advisor as well as any programs KBS affiliates may sponsor in the future; |

| • | Our sponsors and their team of professionals at KBS Capital Advisors and its affiliates (including our dealer manager, KBS Capital Markets Group) will have to allocate their time between us and other programs and activities in which they are involved; |

| • | KBS Capital Advisors and its affiliates will receive fees in connection with transactions involving the purchase, origination, management and sale of our assets regardless of the quality of the asset acquired or the services provided to us; |

| • | KBS Capital Advisors and its affiliates, including our dealer manager, KBS Capital Markets Group, will receive fees in connection with our public offerings of equity securities; |

| • | The negotiation of the advisory agreement and the dealer manager agreement (including the substantial fees KBS Capital Advisors and its affiliates will receive thereunder) will not be at arm’s length; |

| • | KBS Capital Advisors may terminate the advisory agreement without penalty upon 60 days’ written notice and, upon termination of the advisory agreement, KBS Capital Advisors may be entitled to a termination fee if (based upon an independent appraised value of the portfolio) it would have been entitled to a subordinated participation in net cash flows had the portfolio been liquidated on the termination date. The termination fee would be payable in the form of a promissory note that becomes due only upon the sale of one or more assets or upon maturity or payoff of our debt investments, and the fee is payable solely from the proceeds from the sale, maturity or payoff of an asset and future asset sales, maturities or payoffs; |

| • | We may seek stockholder approval to internalize our management by acquiring assets and negotiating compensation for key real estate and debt finance professionals at our advisor and its affiliates. The payment of such consideration could result in dilution to your interest in us and could reduce the net income per share and funds from operations per share attributable to your investment. Additionally, in an internalization transaction, the real estate and debt finance professionals at our advisor that become our employees may receive more compensation than they receive from our advisor or its affiliates. These possibilities may provide incentives to our advisor or these individuals to pursue an internalization transaction rather than an alternative strategy, even if such alternative strategy might otherwise be in our stockholders’ best interests; and |

| • | Key real estate and debt finance professionals at our advisor may become employees of another KBS-sponsored program in an internalization transaction or, if we internalize our advisor, may not become our employees as a result of their relationship with other KBS-sponsored programs. |

7

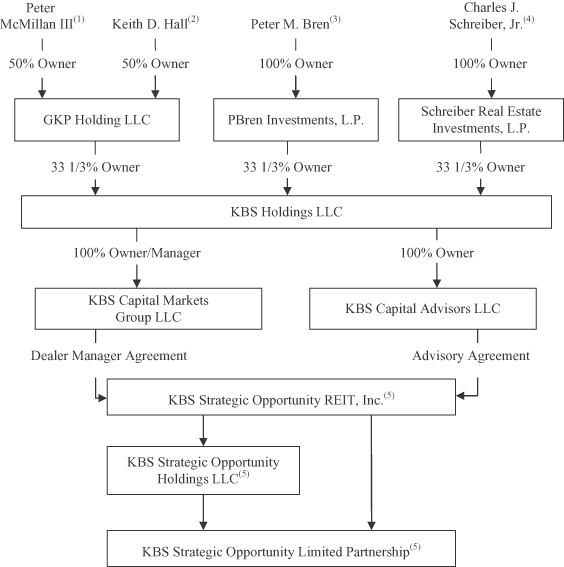

Who owns and controls the advisor?

The following chart shows the ownership structure of KBS Capital Advisors and entities affiliated with KBS Capital Advisors that will perform services for us:

(1) Peter McMillan III is our President and the chairman of our board of directors.

(2) Keith D. Hall is our Chief Executive Officer and a director.

(3) Other than de minimis amounts owned by family members or family trusts, Mr. Bren indirectly owns and controls PBren Investments, L.P.

(4) Other than de minimis amounts owned by family members or trusts, Mr. Schreiber indirectly owns and controls Schreiber Real Estate Investments, L.P.

(5) We are the sole member and manager of KBS Strategic Opportunity Holdings LLC. KBS Strategic Opportunity REIT, Inc. is the sole general partner of, and owns a 0.1% partnership interest in, KBS Strategic Opportunity Limited Partnership. KBS Strategic Opportunity Holdings LLC is the sole limited partner of, and owns the remaining 99.9% partnership interest in, KBS Strategic Opportunity Limited Partnership.

8

As of the date of this prospectus, Messrs. Bren, Hall, McMillan and Schreiber have not received any compensation from us for services provided in their capacity as principals of KBS Capital Advisors or its affiliates. In connection with this offering, we will pay or reimburse our advisor and its affiliates for the services described below.

What are the fees that you will pay to the advisor, its affiliates and your directors?

KBS Capital Advisors and its affiliates will receive compensation and reimbursement for services relating to this offering and the investment and management of our assets. We will also compensate our independent directors for their service to us. The most significant items of compensation are included in the table below. Selling commissions and dealer manager fees may vary for different categories of purchasers. This table assumes that we sell all shares at the highest possible selling commissions and dealer manager fees (with no discounts to any categories of purchasers) and assumes a $9.50 price for each share sold through our dividend reinvestment plan. No selling commissions or dealer manager fees are payable on shares sold through our dividend reinvestment plan.

Type of Compensation | Determination of Amount | Estimated Amount for (250,000 shares)/ Maximum Offering | ||

Organization and Offering Stage | ||||

Selling Commissions | Up to 6.5% of gross offering proceeds in the primary offering; no selling commissions are payable on shares sold under the dividend reinvestment plan; all selling commissions will be reallowed to participating broker-dealers. | $162,500/$65,000,000 | ||

Dealer Manager Fee | Up to 3.0% of gross offering proceeds in the primary offering; the dealer manager may reallow to any participating broker-dealer up to 1.0% of the gross offering proceeds attributable to that participating broker-dealer as a marketing fee and in special cases the dealer manager may increase the reallowance; no dealer manager fee is payable on shares sold under the dividend reinvestment plan. | $75,000/$30,000,000 | ||

| Other Organization and Offering Expenses | To date, our advisor has paid organization and offering expenses on our behalf. We will reimburse our advisor for these costs and future organization and offering costs it may incur on our behalf but only to the extent that the reimbursement would not cause the selling commissions, the dealer manager fee and the other organization and offering expenses borne by us to exceed 15.0% of gross offering proceeds as of the date of the reimbursement. If we raise the maximum offering amount in the primary offering and under the dividend reinvestment plan, we expect organization and offering expenses (other than selling commissions and the dealer manager fee) to be $14,826,833 or 1.07% of gross offering proceeds. These organization and offering expenses include all expenses (other than selling commissions and the dealer manager fee) to be paid by us in connection with the offering, including our legal, accounting, printing, mailing and filing fees, charges of our escrow holder and transfer agent, a $35 fee per subscription agreement payable to our advisor for reviewing and processing subscription agreements (which aggregate fees are expected to be approximately $1,000,000 if we raise the maximum offering amount in the primary offering), reimbursement of bona fide | $137,500/$14,826,833 | ||

9

Type of Compensation | Determination of Amount | Estimated Amount for (250,000 shares)/ Maximum Offering | ||

Organization and Offering Stage | ||||

due diligence expenses of broker-dealers, reimbursement of our advisor for costs in connection with preparing supplemental sales materials, the cost of bona fide training and education meetings held by us (primarily the travel, meal and lodging costs of registered representatives of broker-dealers), attendance and sponsorship fees and travel, meal and lodging costs for registered persons associated with our dealer manager and officers and employees of our affiliates to attend retail seminars conducted by broker-dealers and, in special cases, reimbursement to participating broker-dealers for technology costs associated with the offering, costs and expenses related to such technology costs, and costs and expenses associated with the facilitation of the marketing of our shares and the ownership of our shares by such broker-dealers’ customers.

| ||||

Acquisition and Development Stage | ||||

| Acquisition and Origination Fees | 1.0% of the cost of investments acquired by us, or the amount funded by us to acquire or originate loans, including acquisition and origination expenses and any debt attributable to such investments. Under our charter, a majority of the independent directors would have to approve any increase in the acquisition and origination fee payable to our advisor.

Our charter limits our ability to make an investment if the total of all acquisition and origination fees and expenses relating to the investment exceeds 6% of the contract purchase price or 6% of the total funds advanced. This limit may only be exceeded if a majority of the board of directors (including a majority of the members of the conflicts committee) not otherwise interested in the transaction approves the fees and expenses and finds the transaction to be commercially competitive, fair and reasonable to us. | $20,792 (minimum offering and no debt)/ $8,721,120 (maximum offering and no debt)/ $12,458,744 (maximum offering, assuming leverage of 30% of the cost of our investments (which is our expected leverage once we have fully invested the proceeds of this offering))/ $34,884,482 (maximum offering, assuming leverage of 75% of the cost of our investments (which is the maximum leverage permitted under our charter, unless a majority of our conflicts committee approves additional borrowings)) | ||

| Acquisition and Origination Expenses | Reimbursement of customary acquisition and origination expenses (including expenses relating to potential investments that we do not close), such as legal fees and expenses (including fees of independent contractor in-house counsel that are not employees of the advisor), costs of due diligence (including, as necessary, updated appraisals, surveys and environmental site assessments), travel and communication expenses, accounting fees and expenses and other closing costs and miscellaneous expenses relating to the acquisition or origination of real estate-related loans, real estate-related debt securities and other real estate-related investments. We estimate that these expenses will average approximately 0.6% of the purchase prices of our investments. | Actual amounts are dependent upon the total equity and debt capital we raise, the cost of our investments and the results of our operations; we cannot determine these amounts at the present time. | ||

10

Type of Compensation | Determination of Amount | Estimated Amount for (250,000 shares)/ Maximum Offering | ||

Operational Stage | ||||

| Asset Management Fees | With respect to investments in loans and any investments other than real property, the asset management fee will be a monthly fee calculated, each month, as one-twelfth of 0.75% of the lesser of (i) the amount actually paid or allocated to acquire or fund the loan or other investment, inclusive of fees and expenses related thereto and the amount of any debt associated with or used to acquire or fund such investment and (ii) the outstanding principal amount of such loan or other investment, plus the fees and expenses related to the acquisition or funding of such investment, as of the time of calculation. With respect to investments in real property, the asset management fee will be a monthly fee equal to one-twelfth of 0.75% of the sum of the amount paid or allocated to acquire the investment, inclusive of fees and expenses related thereto and the amount of any debt associated with or used to acquire such investment. In the case of investments made through joint ventures, the asset management fee will be determined based on our proportionate share of the underlying investment. | Actual amounts are dependent upon the total equity and debt capital we raise, the cost of our investments and the results of our operations; we cannot determine these amounts at the present time. | ||

| Other Operating Expenses | We will reimburse our advisor for costs of providing services to us, including our allocable share of the advisor’s overhead, such as rent, employee costs, utilities and IT costs. Though our advisor may seek reimbursement for employee costs under the advisory agreement, the advisor does not intend to do so at this time. If our advisor does decide to seek reimbursement for employee costs, such costs may include our proportionate share of the salaries of persons involved in the preparation of documents to meet SEC reporting requirements. We will not reimburse the advisor or its affiliates for employee costs in connection with services for which our advisor earns acquisition and origination fees or disposition fees (other than reimbursement of travel and communication expenses) or for the salaries and benefits our advisor or its affiliates may pay to our executive officers. | Actual amounts are dependent upon the total equity and debt capital we raise, the cost of our investments and the results of our operations; we cannot determine these amounts at the present time. | ||

11

Type of Compensation | Determination of Amount | Estimated Amount for (250,000 shares)/ Maximum Offering | ||

Operational Stage | ||||

| Independent Director Compensation | We will pay each of our independent directors an annual retainer of $40,000. We will also pay our independent directors for attending meetings as follows: (i) $2,500 for each board meeting attended, (ii) $2,500 for each committee meeting attended (except that the committee chairman will be paid $3,000 for each meeting attended), (iii) $2,000 for each teleconference board meeting attended, and (iv) $2,000 for each teleconference committee meeting attended (except that the committee chairman will be paid $3,000 for each teleconference committee meeting attended). All directors will receive reimbursement of reasonable out-of-pocket expenses incurred in connection with attendance at meetings of the board of directors. No independent director fees or director reimbursements are payable unless we raise the minimum offering amount of $2,500,000; until we raise the minimum offering amount, fees and other amounts payable to our board of directors will accrue without interest. | Actual amounts are dependent upon the total number of board and committee meetings that each independent director attends; we cannot determine these amounts at the present time. | ||

Operational and Liquidation/Listing Stage | ||||

| Subordinated Participation in Net Cash Flows (payable only if we are not listed on a national exchange) | After investors in our offering have received a return of their net capital contributions and a 7.0% per year cumulative, noncompounded return, KBS Capital Advisors is entitled to receive 15.0% of our net cash flows, whether from continuing operations, net sale proceeds or otherwise. Net sales proceeds means the net cash proceeds realized by us after deduction of all expenses incurred in connection with a sale, including disposition fees paid to KBS Capital Advisors. The 7.0% per year cumulative, noncompounded return is calculated based on the amount of capital invested in the offering. In making this calculation, an investor’s net capital contribution is reduced to the extent distributions in excess of a cumulative, noncompounded, annual return of 7.0% are paid (from whatever source), except to the extent such distributions would be required to supplement prior distributions paid in order to achieve a cumulative, noncompounded, annual return of 7.0%. This fee is payable only if we are not listed on an exchange.

| Actual amounts are dependent upon the results of our operations; we cannot determine these amounts at the present time. | ||

12

Type of Compensation | Determination of Amount | Estimated Amount for (250,000 shares)/ Maximum Offering |

Liquidation/Listing Stage | ||||

| Disposition Fees | For substantial assistance in connection with the sale of investments, we will pay our advisor or its affiliates 1.0% of the contract sales price of each loan, debt-related security, real property or other investment sold (including residential or commercial mortgage-backed securities or collateralized debt obligations issued by a subsidiary of ours as part of a securitization transaction); provided, however, that if in connection with such disposition commissions are paid to third parties unaffiliated with our advisor, the fee paid to our advisor and its affiliates may not exceed the commissions paid to such unaffiliated third parties, and provided further that the disposition fees paid to our advisor, its affiliates and unaffiliated third parties may not exceed 6.0% of the contract sales price. The conflicts committee will determine whether the advisor or its affiliate has provided substantial assistance to us in connection with the sale of an asset. We will not pay a disposition fee upon the maturity, prepayment or workout of a loan or other debt-related investment, provided that if we take ownership of a property as a result of a workout or foreclosure of a loan we will pay a disposition fee upon the sale of such property. We do not intend to sell assets to affiliates. However, if we do sell an asset to an affiliate, our organizational documents would not prohibit us from paying our advisor a disposition fee. Before we sold an asset to an affiliate, our charter would require that a majority of the board of directors (including a majority of the members of the conflicts committee) not otherwise interested in the transaction conclude that the transaction is fair and reasonable to us. Although we are most likely to pay disposition fees to our advisor or an affiliate during our liquidation stage, these fees may also be incurred during our operational stage. | Actual amounts are dependent upon the results of our operations; we cannot determine these amounts at the present time. | ||

| Subordinated Incentive Listing Fee (payable only if we are listed on a national exchange) | 15.0% of the amount by which (i) our adjusted market value plus distributions exceeds (ii) the aggregate capital contributed by investors plus an amount equal to a 7.0% cumulative, noncompounded return to investors. | Actual amounts are dependent upon the results of our operations; we cannot determine these amounts at the present time. | ||

13

How many investments do you currently own?

We currently do not own any investments, and as of December 31, 2009, our total assets consist of $192,656 cash. Because we have not yet identified any specific assets to acquire, we are considered to be a blind pool. As significant investments become probable, we will supplement this prospectus to provide information regarding the likely investment. We will also supplement this prospectus to provide information regarding material changes to our portfolio, including the closing of significant asset originations or acquisitions.

If I buy shares, will I receive distributions and how often?

We will declare distributions when our board of directors determines we have sufficient cash flow. During our offering stage, we expect that we will fund any distributions from interest income on our debt investments, rental income on our real property investments and to the extent we acquire investments with short maturities or investments that are close to maturity, we may fund distributions with the proceeds received at the maturity, payoff or settlement of those investments. Upon completion of our offering stage, we expect to fund distributions from interest and rental income on investments, the maturity, payoff or settlement of investments and from strategic sales of loans, debt securities, properties and other assets. We do not expect to make significant asset sales (and concomitant distributions) during our offering stage because, as a REIT, we will generally have to hold our assets for two years in order to meet the safe harbor to avoid a 100% prohibited transactions tax, unless such assets are held through a TRS or other taxable corporation. At such time as we have assets that we have held for at least two years, we anticipate that we may authorize and declare distributions based on gains on asset sales monthly, to the extent we close on the sale of one or more assets and the board of directors does not determine to reinvest the proceeds of such sales. Because we intend to fund distributions from cash flow, we do not expect our board of directors to declare distributions on a set monthly or quarterly basis. Rather, our board of directors will declare distributions from time to time based on cash flow from our investments and our investment activities.

To maintain our qualification as a REIT, we must make aggregate annual distributions to our stockholders of at least 90% of our REIT taxable income (which is computed without regard to the dividends paid deduction or net capital gain and which does not necessarily equal net income as calculated in accordance with GAAP). If we meet the REIT qualification requirements, we generally will not be subject to federal income tax on the income that we distribute to our stockholders each year. See “Federal Income Tax Considerations — Taxation of KBS Strategic Opportunity REIT, Inc. — Annual Distribution Requirements.” In general, we anticipate making distributions to our stockholders of at least 100% of our REIT taxable income so that none of our income is subject to federal income tax. Our board of directors may authorize distributions in excess of those required for us to maintain REIT status depending on our financial condition and such other factors as our board of directors deems relevant.

Our distribution policy is not to use sources other than cash flow from operations and investment activities to pay distributions. However, our organizational documents do not restrict us from paying distributions from any source nor do our organizational documents restrict the amount of distributions we may pay from any source, including proceeds from this offering or the proceeds from the issuance of securities in the future, third party borrowings, advances from our advisor or sponsors or from our advisor’s deferral of its fees under the advisory agreement. Distributions paid from sources other than current or accumulated earnings and profits may constitute a return of capital. From time to time, we may generate taxable income greater than our taxable income for financial reporting purposes, or our taxable income may be greater than our cash flow available for distribution to stockholders. In these situations we may make distributions in excess of our cash flow from operations and investment activities to satisfy the REIT distribution requirement described above. In such an event, we would look first to third party borrowings to fund these distributions.

We have not established a minimum distribution level, and our charter does not require that we make distributions to our stockholders.

14

May I reinvest my distributions in shares of KBS Strategic Opportunity REIT, Inc.?

Yes. You may participate in our dividend reinvestment plan by checking the appropriate box on the subscription agreement or by filling out an enrollment form we will provide to you at your request. The purchase price for shares purchased under the dividend reinvestment plan will initially be $9.50. Once we establish an estimated value per share that is not based on the price to acquire a share in our primary offering or a follow-on public offering, shares issued pursuant to our dividend reinvestment plan will be priced at the estimated value per share of our common stock, as determined by our advisor or another firm chosen for that purpose. We expect to establish an estimated value per share not based on the price to acquire a share in the primary offering or a follow-on public offering after the completion of our offering stage. We will consider our offering stage complete when we are no longer publicly offering equity securities –whether through this offering or follow-on public offerings – and have not done so for 18 months. No selling commissions or dealer manager fees will be payable on shares sold under our dividend reinvestment plan. We may amend or terminate the dividend reinvestment plan for any reason at any time upon 10 days’ notice to the participants. We may provide notice by including such information (a) in a Current Report on Form 8-K or in our annual or quarterly reports, all publicly filed with the SEC or (b) in a separate mailing to the participants.

Will the distributions I receive be taxable as ordinary income?

Yes and No. Generally, distributions that you receive, including distributions that are reinvested pursuant to our dividend reinvestment plan, will be taxed as ordinary income to the extent they are from current or accumulated earnings and profits. Participants in our dividend reinvestment plan will also be treated for tax purposes as having received an additional distribution to the extent that they purchase shares under the dividend reinvestment plan at a discount to fair market value. As a result, participants in our dividend reinvestment plan may have tax liability with respect to their share of our taxable income, but they will not receive cash distributions to pay such liability.

To the extent any portion of your distribution is not from current or accumulated earnings and profits, it will not be subject to tax immediately; it will be considered a return of capital for tax purposes and will reduce the tax basis of your investment (and potentially result in taxable gain). Distributions that constitute a return of capital, in effect, defer a portion of your tax until your investment is sold or we are liquidated, at which time you will be taxed at capital gains rates. However, because each investor’s tax considerations are different, we suggest that you consult with your tax advisor.

Will you register as an investment company?

We intend to conduct our operations so that neither we nor any of our subsidiaries will be required to register as an investment company under the Investment Company Act of 1940, as amended (the “Investment Company Act”). Under the relevant provisions of Section 3(a)(1) of the Investment Company Act, we will not be deemed to be an “investment company” if:

| • | we are not engaged primarily, nor do we hold ourselves out as being engaged primarily, nor propose to engage primarily, in the business of investing, reinvesting or trading in securities (the “Primarily Engaged Test”); and |

| • | we are not engaged and do not propose to engage in the business of investing, reinvesting, owning, holding or trading in securities and do not own or propose to acquire “investment securities” having a value exceeding 40% of the value of our total assets on an unconsolidated basis (the “40% Test”). “Investment securities” excludes U.S. government securities and securities of majority-owned subsidiaries that are not themselves investment companies and are not relying on the exception from the definition of investment company under Section 3(c)(1) or Section 3(c)(7) (relating to private investment companies). |

Depending on the nature of our portfolio, we believe that we and our Operating Partnership may be able to satisfy both tests above. With respect to the 40% Test, we expect that most of the entities through which we and our Operating Partnership own our assets will be majority-owned subsidiaries that are not themselves investment companies and are not relying on the exceptions from the definition of investment company under Section 3(c)(1) or Section 3(c)(7).

15

With respect to the Primarily Engaged Test, we and our Operating Partnership are holding companies and do not intend to invest or trade in securities ourselves. Through the majority-owned subsidiaries of our Operating Partnership, we and our Operating Partnership will be primarily engaged in the non-investment company businesses of these subsidiaries.

We expect that most of the subsidiaries of our Operating Partnership will be able to rely on Section 3(c)(5)(C) of the Investment Company Act for an exception from the definition of an investment company. (Any other subsidiaries of our Operating Partnership will be able to rely on the exceptions for private investment companies pursuant to Section 3(c)(1) and Section 3(c)(7) of the Investment Company Act.) The SEC staff’s position on Section 3(c)(5)(C) generally requires that an issuer maintain at least 55% of its assets in “mortgages and other liens on and interests in real estate” (“Qualifying Assets”); at least 80% of its assets in Qualifying Assets plus real estate-related assets (“Real Estate-Related Assets”); and no more than 20% of the value of its assets in other than Qualifying Assets and Real Estate-Related Assets (“Miscellaneous Assets”). To constitute a Qualifying Asset under this 55% requirement, a real estate interest must meet various criteria; therefore, certain of our subsidiaries will be limited by the provisions of the Investment Company Act and SEC staff interpretations with respect to the value of the assets that they may own at any given time.

If, however, the value of the subsidiaries of our Operating Partnership that must rely on Section 3(c)(1) or Section 3(c)(7) is greater than 40% of the value of the assets of our Operating Partnership, then we and our Operating Partnership may seek to rely on the exception from registration under Section 3(c)(6) if we and our Operating Partnership are “primarily engaged,” through majority-owned subsidiaries, in the business of purchasing or otherwise acquiring mortgages and other interests in real estate. Although the SEC staff has issued little interpretive guidance with respect to Section 3(c)(6), we believe that we and our Operating Partnership may rely on Section 3(c)(6) if 55% of the assets of our Operating Partnership consist of, and at least 55% of the income of our Operating Partnership is derived from, majority-owned subsidiaries that rely on Section 3(c)(5)(C).

Regardless of whether we and our Operating Partnership must rely on Section 3(c)(6) to avoid registration as an investment company, we expect to limit the investments that we make, directly or indirectly, in assets that are not Qualifying Assets and in assets that are not Real Estate-Related Assets. To the extent that the SEC staff provides more specific guidance regarding any of the matters bearing upon the exceptions we and our subsidiaries rely on from registration as an investment company, we may be required to adjust our strategy accordingly. Any additional guidance from the SEC staff could further inhibit our ability to pursue the strategies we have chosen.

How will you use the proceeds raised in this offering?

We expect to use substantially all of the net proceeds from our primary offering of 100,000,000 shares to invest in and manage a diverse portfolio of real estate-related loans, real estate-related debt securities and other real estate-related investments. Depending primarily upon the number of shares we sell in our primary offering and assuming a $10.00 purchase price for shares sold in the primary offering, we estimate that we will use 83.17% to 87.21% of the gross proceeds from the primary offering, or between $8.32 and $8.72 per share, for investments, assuming we raise the minimum and maximum offering amounts, respectively. We will use the remainder of the gross proceeds from the primary offering to pay offering expenses, including selling commissions and the dealer manager fee, to maintain a working capital reserve and to pay a fee to our advisor for its services in connection with the selection and acquisition or origination of our investments. Until we invest the proceeds of this offering in real estate-related loans, real estate-related debt securities and other real estate-related investments, we may invest in short-term, highly liquid or other authorized investments. Such short-term investments will not earn as high of a return as we expect to earn on our real estate-related investments, and we may be not be able to invest the proceeds in real estate-related investments promptly.

16

We expect to use substantially all of the net proceeds from the sale of shares under our dividend reinvestment plan for general corporate purposes, including, but not limited to, the repurchase of shares under our share redemption program; reserves required by any financings of our investments; future funding obligations under any real estate loan receivable we acquire; the acquisition or origination of assets, which would include payment of acquisition and origination fees to our advisor; the repayment of debt; and expenses relating to our investments, such as purchasing a loan senior to ours to protect our junior position in the event of a default by the borrower on the senior loan, making protective advances to preserve collateral securing a loan, or making capital and tenant improvements or paying leasing costs and commissions related to real property.

| 250,000 Shares | 140,000,000 Shares | |||||||||||||||||||||||

| Minimum Offering ($10.00/share) | Primary Offering (100,000,000 shares) ($10.00/share) | Div. Reinv. Plan (40,000,000 shares) ($9.50/share) | ||||||||||||||||||||||

| $ | % | $ | % | $ | % | |||||||||||||||||||

Gross Offering Proceeds | 2,500,000 | 100.00% | 1,000,000,000 | 100.00% | 380,000,000 | 100.00% | ||||||||||||||||||

Selling Commissions | 162,500 | 6.50% | 65,000,000 | 6.50% | 0 | 0.00% | ||||||||||||||||||

Dealer Manager Fee | 75,000 | 3.00% | 30,000,000 | 3.00% | 0 | 0.00% | ||||||||||||||||||

Other Organization and Offering Expenses | 137,500 | 5.50% | 14,166,833 | 1.42% | 660,000 | 0.17% | ||||||||||||||||||

Acquisition and Origination Fees | 20,792 | 0.83% | 8,721,120 | (1) | 0.87% | 0 | 0.00% | |||||||||||||||||

Initial Working Capital Reserve | 25,000 | 1.00% | 10,000,000 | 1.00% | 0 | 0.00% | ||||||||||||||||||

Amount Available for Investment | 2,079,208 | 83.17% | 872,112,047 | 87.21% | 379,340,000 | 99.83% | ||||||||||||||||||

(1) If we raise the maximum offering amount and our debt financing is equal to 30% of the cost of our investments, then acquisition and origination fees would be $12,458,744. We expect that once we have fully invested the proceeds of this offering, our debt financing will be 30% or less of the cost of our investments, although it may exceed this level during our offering stage. Our charter limits our borrowings to 75% of the cost of our tangible assets; however, we may exceed that limit if a majority of the conflicts committee approves each borrowing in excess of our charter limitation and we disclose such borrowing to our stockholders in our next quarterly report with an explanation from the conflicts committee of the justification for the excess borrowing. If we raise the maximum offering amount and our debt financing is equal to 75% of the cost of our investments, then acquisition and origination fees would be $34,884,482.

What kind of offering is this?