Ballard Power Systems Inc.

Notice of Annual Meeting,

Management Proxy Circular and

2010 Annual Report

TABLE OF CONTENTS

| 2010 ANNUAL REPORT | ||

| LETTER FROM IAN A. BOURNE CHAIR OF THE BOARD | 1 | |

| LETTER FROM JOHN W. SHERIDAN PRESIDENT AND CHIEF EXECUTIVE OFFICER | 2 | |

| BALLARD EMPLOYEE AWARDS OF EXCELLENCE FOR 2010 | 6 | |

| NOTICE OF ANNUAL MEETING | 7 | |

| MANAGEMENT PROXY CIRCULAR | 8 | |

| DEFINED TERMS | 8 | |

| MATTERS TO BE VOTED UPON | 8 | |

| ELECTION OF DIRECTORS | 9 | |

| APPOINTMENT OF AUDITORS | 12 | |

| ADVISORY VOTE ON APPROACH TO EXECUTIVE COMPENSATION | 12 | |

| VOTING | 13 | |

| Solicitation of Proxies | 13 | |

| How to Vote | 13 | |

| Execution and Revocation of Proxies | 13 | |

| Voting of Shares and Exercise of Discretion by Proxies | 14 | |

| Voting Shares and Principal Shareholders | 14 | |

| Interest of Certain Persons or Companies in Matters to be Acted Upon | 14 | |

| BOARD AND COMMITTEES | 15 | |

| Board Composition and Nomination Process | 15 | |

| Majority Voting Policy | 15 | |

| Board Meetings | 15 | |

| Committees of the Board | 15 | |

| Audit Committee | 16 | |

| Management Development, Nominating & Compensation Committee | 16 | |

| Corporate Governance Committee | 16 | |

| CORPORATE GOVERNANCE | 16 | |

| EXECUTIVE COMPENSATION | 17 | |

| Compensation Discussion and Analysis | 17 | |

| Objectives of Our Executive Compensation Program | 17 | |

| Philosophy and Objectives | 18 | |

| How Executive Compensation is Determined | 18 | |

| Executive Pay Mix and the Emphasis on "At Risk" Pay | 18 | |

| The Use of Benchmarking | 18 | |

| Current Executive Compensation Elements | 19 | |

| Annual Salary | 19 | |

| Annual Bonus for Executive Officers | 20 | |

| Long Term Incentives | 21 | |

| Chief Executive Officer Compensation | 23 | |

| Termination and Change of Control Benefits | 24 | |

| Perquisites | 24 | |

| Retirement Benefits | 25 | |

| Total Executive Officer Compensation | 25 | |

| Minimum Share Ownership Guidelines | 25 | |

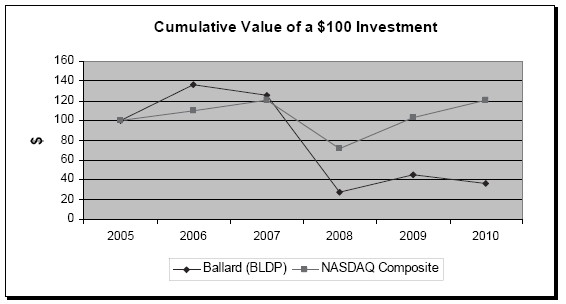

| Performance Graph | 26 | |

| Executive Compensation Tables | 27 | |

| Incentive Plan Awards | 30 | |

| Pension Plan Benefits | 32 | |

| Termination and Change of Control Benefits | 32 | |

| Employment Contracts | 32 | |

| Equity-Based Compensation Plans | 33 | |

| DIRECTOR COMPENSATION | 35 | |

| Incentive Plan Awards | 37 | |

| EQUITY BASED COMPENSATION PLANS | 38 | |

| SECURITIES AUTHORIZED FOR ISSUANCE UNDER EQUITY COMPENSATION PLANS | 38 | |

| INTEREST OF INFORMED PERSONS IN MATERIAL TRANSACTIONS | 38 | |

| INDEBTEDNESS OF DIRECTORS AND EXECUTIVE OFFICERS | 39 | |

| DIRECTORS’ AND OFFICERS’ LIABILITY INSURANCE | 39 | |

| ADDITIONAL INFORMATION | 39 | |

| PROPOSALS | 39 | |

| APPROVAL BY BOARD | 40 |

i

| APPENDIX "A" DESCRIPTION OF OPTION PLAN | A-1 | |

| APPENDIX "B" DESCRIPTION OF SDP | B-1 | |

| FINANCIAL INFORMATION | F-1 | |

| MANAGEMENT’S DISCUSSION AND ANALYSIS | F-1 | |

| CONSOLIDATED FINANCIAL STATEMENTS | F-2 | |

| Corporate Information | F-3 |

This document contains forward-looking statements, including: revenue estimates; market growth projections; cash operating costs; gross margins; adjusted EBIDTA; and product cost reductions. These forward-looking statements reflect Ballard’s current expectations as contemplated under section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Any such forward-looking statements are based on Ballard’s assumptions relating to its financial forecasts and expectations regarding its product development efforts, manufacturing capacity, and market demand.

These statements involve risks and uncertainties that may cause Ballard's actual results to be materially different, including general economic and regulatory changes, detrimental reliance on third parties, successfully achieving our business plans and achieving and sustaining profitability. For a detailed discussion of these and other risk factors that could affect Ballard's future performance, please refer to Ballard's most recent Annual Information Form. Readers should not place undue reliance on Ballard's forward-looking statements and Ballard assumes no obligation to update or release any revisions to these forward-looking statements, other than as required under applicable legislation.

ii

Letter from IAN A. BOURNE

Chair of the Board

Chair of the Board

Fellow Shareholders:

Ballard on a Positive Trajectory

The past three years have been key to re-setting Ballard’s course and ensuring an “up and to the right” trajectory for revenue growth and overall financial results. As John Sheridan discusses in his President and CEO Letter, 2010 was a turning point along the Company’s path to profitability – particularly with respect to sales and product shipment momentum across the Company’s target markets. We are now seeing the early stage of what promises to be an exciting next chapter for Ballard fuel cell products.

During the past three years Management has, with the full support of your Board of Directors, successfully closed a number of key transactions that have raised over C$100 million in cash – the last of these transactions was the sale-leaseback agreement for the head office building site in Burnaby, completed in early-2010. Collectively, these transactions have established a strong liquidity position that will facilitate execution of Ballard’s multi-market growth strategy.

Committed People …. Building Momentum

Your Board of Directors congratulates Management, under John’s leadership, for the strong corporate results in 2010 – this is a testament to the good judgment and sound business practices of Ballard’s Management team. The Board, comprised of a seasoned group of business leaders with a variety of complementary skill sets, has naturally gained a deeper understanding of the fuel cell sector over time – as a result, I believe we are contributing measurably to the planning effort for Ballard’s future and to prudent governance of the business.

The employees of Ballard Power Systems certainly deserve recognition for their hard work, spirit of innovation and passionate desire to make a real difference for the environment. I encourage you to look at the “Employee Awards of Excellence for 2010” in the following pages, which acknowledge the outstanding contributions made by our people.

Finally, I would like to thank shareholders for your commitment and support of Ballard. The Company is focused on consistent execution of its business strategy, and the early results are offering a glimpse to a promising future.

"Ian A. Bourne"

Ian A. Bourne

Chair of the Board of Directors

1

Letter from JOHN W. SHERIDAN

President and Chief Executive Officer

President and Chief Executive Officer

2010 – A Turning Point for Our Company

2010 was a turning point for Ballard. With our corporate transformation completed – after 3 years of re-positioning and foundation building – we posted significant progress in growth and profitability in 2010.

This transformation began in 2007, with the shift away from high-cost, long-term automotive fuel cell technology development. At that time, Ballard embarked on a new vision: to leverage our technology and intellectual property, to become a global leader in clean energy, fuel cell products in commercial markets. We committed to this fundamental change in strategic direction to enable Ballard’s movement towards profitability – after decades of high cash burn and large losses. And, as part of this transformation, we re-set our cost base to enable near-term profitability and we built a solid liquidity position.

This commercial market focus has been all about replacing legacy diesel engines, diesel generators and lead-acid batteries, with cost-effective zero-emission fuel cell solutions. To maximize revenue potential and to minimize risk, we have pursued a multi-market growth strategy, addressing opportunities in:

- Backup power;

- Distributed generation;

- Buses; and

- Material handling.

Our strong revenue growth in 2010 is clear evidence of our progress in penetrating these markets, and is also an early barometer of the future potential. Customers, suppliers and industry experts are now recognizing this potential. As an example, Deloitte – a global business consulting service – recently issued its 2011 technology predictions, which includes the striking headline “Hydrogen comes out of hiding: the alternative alternative energy source”. “Deloitte predicts that hydrogen will enjoy tremendous success in 2011” precisely in the application areas that Ballard is focusing on. And, Deloitte goes on to say that “HFCs (hydrogen fuel cells) … could easily create a billion-dollar market by 2015.”

2010 Operating Results – “Putting Fuel Cells to Work”

In 2010, we drove significant improvement in our top-line revenue, which grew 39% to $65 million on fuel cell product shipment growth of 104%. This growth in revenue met the guidance we had provided to the investment community.

Gross margin improved significantly in the 4th quarter, and was up 3 points for the full year, to 16% — moving towards our longer term target of 30-35%.

2

In addition, we improved cash flow from operations by 30%, excluding the impacts of Dantherm Power and foreign exchange, ending the year at $(29.3) million. We also drove an improvement in Adjusted EBITDA of 33%, moving Ballard closer to overall profitability.

Finally, we ended the year with substantial cash reserves of $74.4 million, which puts the company on a strong financial footing for continued execution of our multi-market growth strategy.

Looking back on our ‘growth story’ for 2010, I am very pleased to report solid achievements that helped build momentum throughout the year –

- We secured orders for a number of fuel cell modules to be used in transit buses - including 3 additional buses for Transport for London in the U.K., 2 for SunLine Transit Agency in Palm Springs, CA and 4 that will be utilized in various locations under a U.S. FTA program. In addition, we secured an order from Tuttotrasporti in December for 3 modules that will be integrated into buses in Brazil, the world’s largest transit bus market.

- A 1-megawatt CLEARgenTM distributed generation system was delivered to FirstEnergy Generation Corp. in Ohio.

- A CLEARgenTM system was sold to K2 Pure Solutions, which will utilize by-product hydrogen from its bleach plant in California as fuel.

- 1.25-megawatts of fuel cell stacks were sold to Real Time Engineering for creation of a utility-scale distributed power generator in Singapore.

- We extended our supply agreement with Plug Power through 2014 under a mutually exclusive arrangement for the North American material handling market and Plug Power announced commercial orders with such customers as Coca-Cola, BMW, FedEx, Sysco and United Natural Foods.

- Ballard launched FuelWorksTM, a center of excellence for the advancement of fuel processing technology that will be important in the development of backup / supplemental power markets, together with founding partners University of Maryland and the U.S. Department of Defense.

- In February of 2011 we announced a conditional award of up to C$7 million from Sustainable Development Technology Canada to fund activities that will contribute to product cost reduction for the FCgen®-1300 fuel cell product platform, which powers the CLEARgen™ distributed generation system.

Unfortunately, despite this momentum and solid overall operating performance, our share price declined over the year – about 21% on NASDAQ and about 25% on the TSX. While Ballard’s share price outperformed our fuel cell company comparators, this share price performance is not acceptable. However, we remain convinced that we are on the right path to grow shareholder value, with a commitment to continue to build growth momentum on the ‘top line’ and drive the company to profitability, on the bottom line, after decades of losses. And progress on these fundamental goals was clearly evident in 2010.

Looking Forward – “Smarter Solutions for a Clean Energy Future”

We will continue aggressively driving forward on growth and profitability fronts in 2011.

In terms of growth, we expect revenue to be up in 2011, in excess of 30%, through our multi-market fuel cell product strategy:

- We expect the strongest growth to be in the bus and backup power markets;

- We will continue to work closely with Plug Power, to drive continued growth in the material handling market; and

- We expect to forge key progress with major customers, continuing to create a solid foundation in the fuel cell distributed generation market.

3

In terms of progressing to profitability, we expect an improvement in Adjusted EBITDA in 2011 in excess of 40%, through:

- Strong growth, with a shift to higher margin products;

- Further reductions in product costs;

- Improvements in gross margin toward a 30-35% target; and

- Maintenance of the operating cost base at the current run-rate.

Behind these numbers are enthusiastic Ballard employees who are committed to playing an important role in the clean energy sector. We are all working hard to deliver smarter solutions for a clean energy future, and remain focused on:

- Maintaining our leadership position in the fuel cell sector;

- Expanding our channels into global markets for target applications;

- Continuing to build equity in Ballard’s brand; and

- Becoming a profitable, sustainable business.

I look forward to reporting our progress as we move through 2011. Thank you for your continued support of Ballard.

"John Sheridan"

John Sheridan

President & CEO

Ballard Power Systems

President & CEO

Ballard Power Systems

4

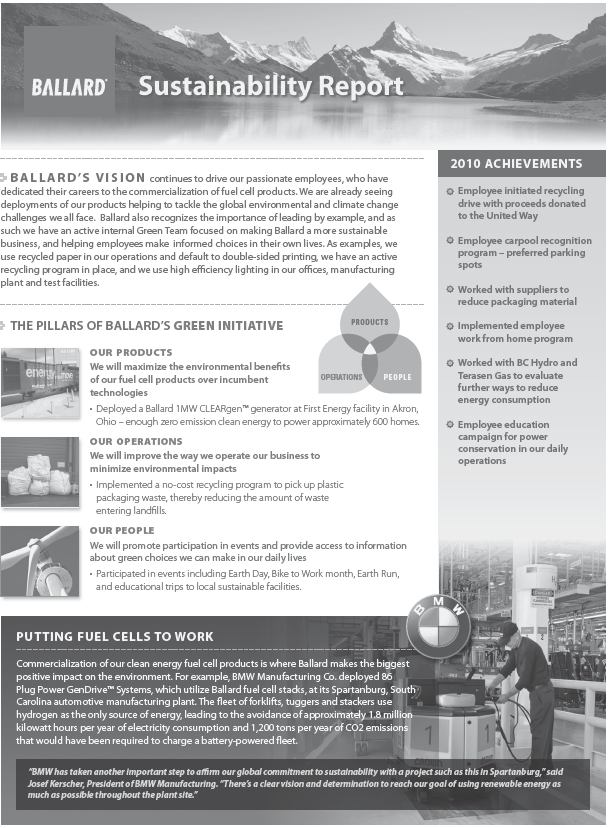

Sustainability Report

5

Ballard Employee Awards of Excellence for 2010

6

BALLARD POWER SYSTEMS INC.

9000 Glenlyon Parkway

Burnaby, British Columbia, Canada V5J 5J8

Burnaby, British Columbia, Canada V5J 5J8

NOTICE OF ANNUAL MEETING

TO OUR SHAREHOLDERS:

Our 2011 Annual Meeting (the "Meeting") will be held at 9000 Glenlyon Parkway, Burnaby, British Columbia, on Tuesday, May 31, 2011 at 1:00 p.m. (Pacific Daylight Time) for the following purposes:

| 1. | To receive our audited financial statements for the financial year ended December 31, 2010 and the report of our auditors thereon; | ||

| 2. | To elect our directors for the ensuing year; | ||

| 3. | To appoint our auditors for the ensuing year and to authorize our Audit Committee to fix the remuneration of the auditors; and | ||

| 4. | To consider and, if thought appropriate, to approve a resolution, on an advisory basis, accepting the Corporation’s approach to executive compensation. | ||

In addition, shareholders will be asked to consider any amendment to or variation of a matter identified in this Notice and to transact such other business as may properly come before the Meeting or any adjournment thereof.

A detailed description of the matters to be dealt with at the Meeting, our 2010 Annual Report, our consolidated financial statements for the year ended December 31, 2010 and the report of our auditors thereon, and our 2010 Management’s Discussion and Analysis, are included with this Notice.

If you are unable to attend the Meeting in person and wish to ensure that your shares will be voted at the Meeting, you must complete, date and execute the enclosed form of proxy and deliver it in accordance with the instructions set out in the form of proxy and in the Management Proxy Circular accompanying this Notice, so that it is received by Computershare Investor Services Inc. no later than 1:00 p.m. (Pacific Daylight Time) on Friday, May 27, 2011.

If you plan to attend the Meeting you must follow the instructions set out in the form of proxy and in the Management Proxy Circular to ensure that your shares will be voted at the Meeting.

DATED at Burnaby, British Columbia, April 15, 2011.

| BY ORDER OF THE BOARD |

| "Kerry Hillier" |

| Kerry Hillier |

| Corporate Secretary |

| Ballard Power Systems |

7

MANAGEMENT PROXY CIRCULAR

dated as of April 15, 2011

dated as of April 15, 2011

DEFINED TERMS

In this Management Proxy Circular:

"Ballard", "Corporation", "we", "us" and "our" refer to Ballard Power Systems Inc.

"Beneficial Shareholders" means holders of our Shares that do not hold our Shares in their own name, but instead, whose Shares are held on the Record Date by a bank, trust company, securities broker or other nominee.

"Board" means the board of directors of Ballard.

"C$" refers to Canadian currency.

"DSU" means deferred share unit.

"$" or "dollars" refer to United States currency unless specifically stated otherwise.

"Meeting" means the 2011 annual meeting of our Registered Shareholders and includes any adjournment thereof, unless otherwise indicated.

"NASDAQ" means the NASDAQ Global Market.

“Option Plan” means the Corporation’s consolidated share option plan, the principal terms of which are set out in Appendix "A".

"Record Date" means 5:00 p.m. Pacific Daylight Time on April 15, 2011.

"Registered Shareholders" means registered holders of our Shares on the Record Date.

"RSU" means restricted share unit.

“SDP” means the Corporation’s consolidated share distribution plan, the principal terms of which are set out in Appendix "B".

“SEC” means the U.S. Securities and Exchange Commission

"Shares" means common shares without par value in the capital of Ballard.

"TSX" means the Toronto Stock Exchange.

"US$" refers to United States currency.

MATTERS TO BE VOTED UPON

Registered Shareholders or their duly appointed proxyholders will be voting on:

- the election of directors to our Board;

- the re-appointment of our auditors and authorization for our Audit Committee to fix the remuneration of the auditors; and

- on an advisory basis, the Corporation’s approach to executive compensation.

As of the date of this Management Proxy Circular, we know of no amendment, variation or other matter that may come before the Meeting other than the matters referred to in the Notice of Annual Meeting. If any other matter is properly brought before the Meeting, it is the intention of the persons named in the enclosed proxy to vote the proxy on that matter in accordance with their best judgment.

With respect to resolutions to be voted on at the Meeting, a simple majority of the votes (greater than 50%) cast in favour by Registered Shareholders, by proxy or in person, will constitute approval.

8

ELECTION OF DIRECTORS

At the Meeting you will be asked to elect eight directors. All of our eight nominees are currently members of the Board. Each elected director will hold office until the end of our next annual shareholders’ meeting (or if no director is then elected, until a successor is elected) unless the director resigns or is otherwise removed from office earlier. If any nominee for election as a director advises us that he or she is unable to serve as a director, the persons named in the enclosed proxy will vote to elect a substitute director at their discretion.

The following information pertains to our nominees for election as directors at the Meeting, as of April 15, 2011. The number of Shares shown as being held by each nominee constitute the number beneficially owned, or controlled or directed, directly or indirectly, by that nominee and such information has been provided to us by that nominee.

Ian A. Bourne Age: 63 Alberta, Canada Director since: 2003 Independent | Mr. Bourne’s principal occupation is corporate director, and he has been the Chair of the Board of Ballard since February 2006. Mr. Bourne was also our lead director from October 2005 to February 2006. Previously, Mr. Bourne was the Executive Vice President and the Chief Financial Officer of TransAlta Corporation (electricity generation and marketing) from January 1998 to December 2006 and from January 1998 to December 2005, respectively. He has completed the Directors Education Program of the Institute of Corporate Directors and has received his ICD.D designation. | ||||

| Board and Committee Membership | Attendance | Board Memberships | |||

| Board (Chair) Audit Corporate Governance Management Development, Nominating & Compensation | 5 5 4 4 | 100% 100% 100% 100% | Current: SNC-Lavalin Group; Canadian Public Accountability Board; Wajax Corporation (formerly Wajax Income Fund); Canada Pension Plan Investment Board; Canadian Oil Sands Limited; The Calgary Foundation Previous: TransAlta Power LP; TransAlta CoGen LP; Glenbow Museum; Calgary Philharmonic Orchestra | ||

| Securities Held(1) | |||||

| Year | Shares | DSUs | Total of Shares and DSUs | Total Value of Shares and DSUs (C$)(2) | |

| 2011 | 26,824 | 77,706 | 104,530 | $211,151 | |

| 2010 | 26,824 | 77,706 | 104,530 | $266,552 | |

Edwin J. Kilroy Age: 51 Ontario, Canada Director since: 2002 Independent | Mr. Kilroy’s principal occupation is corporate director. Previously, Mr. Kilroy was the Chief Executive Officer of Symcor Inc. (business process outsourcing services), from January 2005 to November 2010. Prior to that, Mr. Kilroy was the Chief Executive Officer of IBM Canada Ltd. (information technology) from April 2001 to January 2005. | ||||

| Board and Committee Membership | Attendance | Board Memberships | |||

Board Audit (Chair) Management Development, Nominating & Compensation | 5 5 3 | 100% 100% 100%(3) | Current: not applicable Previous: Symcor Inc.; The Conference Board of Canada | ||

| Securities Held(1) | |||||

| Year | Shares | DSUs | Total of Shares and DSUs | Total Value of Shares and DSUs (C$)(2) | |

| 2011 | 2,752 | 42,844 | 45,596 | $92,104 | |

| 2010 | 2,752(4) | 42,844 | 45,596 | $116,270 | |

9

Dr. Chong Sup (C.S.) Park Age: 63 California, U.S.A. Director since: 2007 Independent | Dr. Park’s principal occupation is corporate director. Previously, Dr. Park was the Chief Executive Officer and Chairman of the Board of Maxtor Corporation (storage solutions and hard disk drives) from November 2004 to May 2006. Dr. Park was also the Managing Director, Investment Partner and Senior Advisor of H&Q Asia Pacific (private equity investment) from November 2002 to September 2004. | ||||

| Board and Committee Membership | Attendance | Board Memberships | |||

Board Corporate Governance Management Development, Nominating & Compensation | 5 4 4 | 100% 100% 100% | Current: Brooks Automation, Inc.; Seagate Technology; Computer Sciences Corp.; Sand Force Inc.; American Leadership Forum (Silicon Valley); Silicon Valley Community Foundation Previous: Smart Modular Technologies, Inc. | ||

| Securities Held(1) | |||||

| Year | Shares | DSUs | Total of Shares and DSUs | Total Value of Shares and DSUs (C$)(2) | |

| 2011 | 17,091 | 0 | 17,091 | $34,524 | |

| 2010 | 17,091 | 0 | 17,091 | $43,582 | |

John W. Sheridan Age: 56 B.C., Canada Director since: 2001 Non-Independent | Mr. Sheridan is President and Chief Executive Officer of Ballard, a position he has held since February 2006. Mr. Sheridan was also Chair of our Board from June 2004 to February 2006. | ||||

| Board and Committee Membership | Attendance | Board Memberships | |||

| Board | 5 | 100% | Current: AFCC Automotive Fuel Cell Cooperation Corp.; Dantherm Power; Premier’s Technology Council; Canadian Hydrogen Fuel Cells Association Previous: Aliant Inc.; Bell Canada, Bell Actimedia, Bell Distribution, Bell Express Vu, Bell Mobility, Bell West, Bell Sygma UK Ltd; Encom Cable TV & Telecommunications, plc; Manitoba Telecom Services Inc.; MTS Communications Inc.; Photowatt Technologies; Sun Media Corp. Ltd.; NewPage Corporation; BC Hydrogen Highway | ||

| Securities Held(1) | |||||

| Year | Shares | DSUs | Total of Shares and DSUs | Total Value of Shares and DSUs (C$)(2) | |

| 2011 | 269,913 | 57,943 | 327,856 | $662,269 | |

| 2010 | 261,710 | 57,943 | 319,653 | $815,115 | |

David J. Smith Age: 76 B.C., Canada Director since: 2006 Independent | Mr. Smith is a part-time Commissioner of the British Columbia Securities Commission (provincial securities regulator), a position he has held since July 2006. Mr. Smith was counsel with Lawson Lundell LLP (law firm) from May 2005 until April 2006, and prior to that, he was a partner at Lawson Lundell LLP and predecessor firms practicing corporate, commercial and securities law. He has completed the Directors Education Program of the Institute of Corporate Directors and has received his ICD.D designation. | ||||

| Board and Committee Membership | Attendance | Board Memberships | |||

Board Corporate Governance (Chair) | 5 4 | 100% 100% | Previous: Member of Executive Committee, British Columbia Chapter, Institute of Corporate Directors | ||

| Securities Held(1) | |||||

| Year | Shares | DSUs | Total of Shares and DSUs | Total Value of Shares and DSUs (C$)(2) | |

| 2011 | 8,411 | 14,841 | 23,252 | $46,969 | |

| 2010 | 7,911 | 14,841 | 22,752 | $58,018 | |

10

David B. Sutcliffe Age: 51 B.C., Canada Director since: 2005 Independent | Mr. Sutcliffe’s principal occupation is corporate director. Previously, Mr. Sutcliffe was the Chief Executive Officer of Sierra Wireless, Inc. (electrical and electronic industrial products) from May 1995 to October 2005. From May 2001 to April 2005, he was also the Chair of the Board of Sierra Wireless, Inc. He has completed the Directors Education Program of the Institute of Corporate Directors and has received his ICD.D designation. | ||||

| Board and Committee Membership | Attendance | Board Memberships | |||

Board Management Development, Nominating & Compensation (Chair) | 5 4 | 100% 100% | Current: Sierra Wireless, Inc. Previous: BC Technology Social Venture Partners; E-Comm 911 | ||

| Securities Held(1) | |||||

| Year | Shares | DSUs | Total of Shares and DSUs | Total Value of Shares and DSUs (C$) (2) | |

| 2011 | 3,600 | 25,528 | 29,128 | $58,839 | |

| 2010 | 3,600 | 25,528 | 29,128 | $74,276 | |

Mark A. Suwyn Age: 68 Florida, U.S.A. Director since: 2003 Independent | Mr. Suwyn’s principal occupation is corporate director. Previously, Mr. Suwyn was Executive Chairman of the Board of NewPage Corporation (coated papers) from March 2009 to June 2010; Acting Chief Executive Officer and Chairman of the Board from March 2009 to January 2010; and Chief Executive Officer and Chairman of the Board, positions he held from April 2006 and May 2005, respectively. Mr. Suwyn was the President of MARSUW LLC (consulting) from November 2004 to April 2005. He was the Chief Executive Officer and Chairman of the Board of Louisiana-Pacific Corporation (building products) from January 1996 to October 2004. | ||||

| Board and Committee Membership | Attendance | Board Memberships | |||

| Board Audit | 5 5 | 100% 100% | Current: BlueLinx Corporation Previous: NewPage Corporation; Hope College Board of Trustees; Louisiana Pacific Corporation; International Paper Company; Junior Achievement Inc.; Junior Achievement International; Kelly Cabinets; The Nature Conservancy of Oregon; United Rentals Inc. | ||

| Securities Held(1) | |||||

| Year | Shares | DSUs | Total of Shares and DSUs | Total Value of Shares and DSUs (C$) (2) | |

| 2011 | 7,237 | 35,019 | 42,256 | $85,357 | |

| 2010 | 7,237 | 35,019 | 42,256 | $107,753 | |

Douglas W.G. Whitehead Age: 64 B.C., Canada Director since: 1998 Independent | Mr. Whitehead is the Chairman of Finning International Inc. (heavy equipment reseller). Previously, Mr. Whitehead was the President and Chief Executive Officer of Finning International Inc. from 1999 to May 2008. | ||||

| Board and Committee Membership | Attendance | Board Memberships | |||

| Board Audit | 5 5 | 100% 100% | Current: International Forest Products Inc.; INMET Mining Corporation; Belkorp Industries Inc.; Finning International Inc.; Vancouver General Hospital/University of British Columbia Hospital Foundation | ||

| Securities Held(1) | |||||

| Year | Shares | DSUs | Total of Shares and DSUs | Total Value of Shares and DSUs (C$) (2) | |

| 2011 | 5,383 | 36,916 | 42,299 | $85,444 | |

| 2010 | 4,383 | 36,916 | 41,299 | $105,312 | |

| (1) | As of April 13, 2010 and April 15, 2011, respectively. | |

| (2) | Based on a C$2.02 and C$2.55 closing Share price on the TSX as of April 15, 2011 and April 13, 2010, respectively. | |

11

| (3) | Mr. Kilroy was appointed to the Management Development, Nominating & Compensation Committee on June 1, 2010 and attended all meetings scheduled from that time. | |

| (4) | Mr. Kilroy’s shareholdings were reported as 2,424 shares in 2010 due to error, which has been corrected. Mr. Kilroy’s actual shareholdings have not increased since that time. | |

APPOINTMENT OF AUDITORS

Our Audit Committee has recommended that KPMG LLP, Chartered Accountants, of 777 Dunsmuir Street, Vancouver, British Columbia, be nominated at the Meeting for re-appointment as our external auditors. Our Audit Committee will fix the remuneration of our external auditors if authorized to do so by shareholders at the Meeting. It is expected that representatives of KPMG LLP will be present at the Meeting. KPMG LLP were appointed as our external auditors in 1999. Total fees paid to KPMG in 2010 and 2009 are set forth in the table below. We comply with the requirement regarding the rotation of our audit engagement partner every five years. The current audit engagement partner at KPMG LLP may continue in his role until the end of 2016.

The following table shows the fees we incurred with KPMG LLP in 2010 and 2009:

| Type of Audit Fees | 2010 | 2009 | ||

| (C$) | (C$) | |||

| Audit Fees | $353,302 | $340,089 | ||

| Audit-Related Fees(1) | Nil | $9,587 | ||

| Tax Fees(2) | $19,265 | $6,115 | ||

| All Other Fees | Nil | Nil | ||

| (1) | The Audit-Related Fees for 2009 relate primarily to accounting advice for International Financial Reporting Standards. | |

| (2) | The Tax Fees for 2010 and 2009 related to tax advisory services. | |

For a more detailed description of the Audit Committee or to see the Audit Committee’s mandate, a copy of which is posted on our website, see the section entitled "Board Committees – Audit Committee" in our Annual Information Form dated March 9, 2011, which section is incorporated by reference into this Management Proxy Circular.

ADVISORY VOTE ON APPROACH TO EXECUTIVE COMPENSATION

The adoption of advisory votes on executive compensation, commonly known as “say-on-pay”, is a recent and still evolving corporate governance practice in Canada and elsewhere. The Corporate Governance Committee has monitored developments and trends relating to say-on-pay and reviewed the guidelines provided by various advisory bodies on this subject, including in particular the Canadian Coalition for Good Governance’s Model Shareholder Engagement and “Say on Pay” Policy for Boards of Directors.

The Corporate Governance Committee also noted that, in the United States, the SEC has established say-on-pay advisory shareholder vote requirements. The Corporation’s shares are traded on NASDAQ and it is a reporting company with the SEC. However, Ballard is a “foreign private issuer” with the SEC and accordingly these requirements do not apply to it.

In Canada, the Ontario Securities Commission has commenced a study of a number of “shareholder democracy issues” including say-on-pay. There is a possibility that say-on-pay shareholder voting requirements may be mandated in Canada and the Corporate Governance Committee will continue to monitor the situation.

In light of these developments, the Corporate Governance Committee recommended to the Board that Ballard shareholders be provided the opportunity, on an advisory basis, to vote at the Meeting in respect of the Corporation’s approach to executive compensation. The Corporate Governance Committee also recommended that adoption of a formal say-on-pay policy by the Board should be deferred until Canadian regulatory requirements applicable to the Corporation are known.

12

Accordingly, the shareholders of the Corporation are being given the opportunity to vote at this Meeting, on an advisory and non-binding basis, “FOR” or “AGAINST” the Corporation’s approach to executive compensation through the following resolution:

“RESOLVED, on an advisory basis and not to diminish the role and responsibilities of the Board of Directors of the Corporation, that the shareholders accept the approach to executive compensation disclosed in the Corporation’s management information circular delivered in advance of the Corporation’s 2011 annual meeting of shareholders.”

The Board believes that shareholders should be well informed as to, and fully understand, the objectives, philosophy and principles that it has used to make executive compensation decisions. For information regarding Ballard’s approach to executive compensation, shareholders should review the section entitled "Compensation – Compensation Discussion and Analysis" appearing below in this Management Information Circular.

The Board recommends that shareholders vote “FOR” the foregoing resolution. The representatives of management named in the enclosed form of proxy, if named as proxyholders, intend to vote for the resolution, unless the shareholder has specified in the form of proxy that his or her shares are to be voted against the resolution.

Approval of the above resolution will require an affirmative vote of a majority of the votes cast on the matter at the Meeting. As the vote on this resolution is advisory, the results will not be binding on the Board or the Management Development, Nominating & Compensation Committee ("MDNCC"). However, the Board and the MDNCC will take the results of the advisory vote into account, as appropriate, as part of their ongoing review of executive compensation philosophy, policies and programs.

VOTING

SOLICITATION OF PROXIES

This Management Proxy Circular is furnished in connection with the solicitation of proxies by our management in connection with the Meeting to be held on Tuesday, May 31, 2011 at 1:00 p.m. Pacific Daylight Time in Vancouver, British Columbia, Canada, or the date and place of any adjournment thereof. We are soliciting proxies primarily by mail, but our directors, officers and employees may solicit proxies personally, by telephone, by facsimile transmission or by other means of electronic communication. The cost of the solicitation will be borne by us. The approximate date on which this Management Proxy Circular and the related materials are first being sent to Registered Shareholders is May 6, 2011.

HOW TO VOTE

Only Registered Shareholders or their duly appointed proxyholders are permitted to vote at the Meeting. Beneficial Shareholders are not permitted to vote at the Meeting as only proxies from Registered Shareholders can be recognized and voted at the Meeting. You may vote as follows:

Registered Shareholders: If you are a Registered Shareholder you may vote by attending the Meeting in person, or if you do not plan to attend the Meeting, by completing the proxy and delivering it according to the instructions contained in the form of proxy and this Management Proxy Circular.

Beneficial Shareholders: If you are a Beneficial Shareholder you may only vote by carefully following the instructions on the voting instruction form or proxy form provided to you by your stockbroker or financial intermediary. If you do not follow the special procedures described by your stockbroker or financial intermediary, you will not be entitled to vote.

EXECUTION AND REVOCATION OF PROXIES

A Registered Shareholder or the Registered Shareholder’s attorney authorized in writing or, where the Registered Shareholder is a company, a duly authorized officer or attorney of that company, must execute

13

the proxy. In order to be effective, completed proxies must be deposited at the office of the registrar and transfer agent for the Shares, being Computershare Investor Services Inc. ("Computershare"), Proxy Dept., 100 University Avenue, 9th Floor, Toronto Ontario, M5J 2Y1 (Fax: within North America: 1-866-249-7775; outside North America: 1-416-263-9524), not less than 48 hours (excluding Saturdays and holidays) before the time of the Meeting. The individuals named as proxyholders in the accompanying form of proxy are directors and officers of Ballard. A Registered Shareholder desiring to appoint a person or company (who need not be a shareholder) to represent him or her at the Meeting, other than the persons or companies named in the enclosed proxy, may do so by inserting the name of such other person or company in the blank space provided in the proxy.

A proxy may be revoked by written notice executed by the Registered Shareholder or by his or her attorney authorized in writing or, where the Registered Shareholder is a company, by a duly authorized officer or attorney of that company, and delivered to:

- Computershare, at the address or fax number set out above, at any time up to and including the last business day preceding the day of the Meeting at which the proxy is to be used;

- the registered office of the Corporation at any time up to and including the last business day preceding the day of the Meeting at which the proxy is to be used; or

- the chair of the Meeting on the day of the Meeting and before any vote in respect of which the proxy is to be used is taken.

A proxy may also be revoked in any other manner provided by law. Any revocation of a proxy will not affect a matter on which a vote is taken before such revocation.

VOTING OF SHARES AND EXERCISE OF DISCRETION BY PROXIES

If you complete and deposit your proxy properly, then the proxyholder named in the accompanying form of proxy will vote or withhold from voting the Shares represented by the proxy in accordance with your instructions. If you do not specify a choice on any given matter to be voted upon, your Shares will be voted in favour of such matter. The proxy grants the proxyholder the discretion to vote on amendments to or variations of matters identified in the Notice of Annual Meeting and with respect to other matters that may properly come before the Meeting.

VOTING SHARES AND PRINCIPAL SHAREHOLDERS

As of the Record Date of April 15, 2011 we had 84,345,192 Shares issued and outstanding, each carrying the right to one vote. On a show of hands, every individual who is present as a Registered Shareholder or as a representative of one or more corporate Registered Shareholders, or who is holding a proxy on behalf of a Registered Shareholder who is not present at the Meeting, will have one vote, and on a poll, every Registered Shareholder present in person or represented by proxy and every person who is a representative of one or more corporate Registered Shareholders, will have one vote for each Share recorded in the Registered Shareholder’s name on the register of shareholders, which is available for inspection during normal business hours at Computershare and will be available at the Meeting.

As of the Record Date, to the knowledge of our directors and executive officers, no person beneficially owns, controls or directs, directly or indirectly, Shares carrying more than 10% of the voting rights attached to all issued and outstanding Shares carrying the right to vote in all circumstances.

INTEREST OF CERTAIN PERSONS OR COMPANIES IN MATTERS TO BE ACTED UPON

No one who has been a director or executive officer of ours at any time since January 1, 2010, or any of his or her associates or affiliates, has any material interest, direct or indirect, by way of beneficial ownership of Shares or otherwise, in any matter to be acted on at the Meeting other than the election of directors.

14

BOARD AND COMMITTEES

BOARD COMPOSITION AND NOMINATION PROCESS

Our Management Development, Nominating & Compensation Committee ("MDNCC") conducts an annual process under which an assessment is made of the skills, expertise and competencies of the directors and is compared to our needs and the needs of the Board. This process culminates in a recommendation to the Board of individual nominee directors for election at our annual shareholders’ meeting.

Directors are elected yearly at our annual shareholders’ meeting and serve on the Board until the following annual shareholders’ meeting, at which time they either stand for re-election or leave the Board. If no meeting is held, each director serves until his or her successor is elected or appointed, unless the director resigns earlier. The Board has established director resignation guidelines, which set out the circumstances under which a director would be compelled to submit a resignation or be asked to resign.

MAJORITY VOTING POLICY

The Board has adopted a policy which requires that any nominee for director who receives a greater number of votes "withheld" than "for" his or her election shall tender his or her resignation to the Board following our annual shareholders’ meeting, to take effect immediately upon acceptance by the Board. Upon receipt of such conditional resignation, the Corporate Governance Committee will consider the matter and, as soon as possible, make a recommendation to the full Board regarding whether or not such resignation should be accepted. After considering the recommendation of the Corporate Governance Committee, the Board will decide whether or not to accept the tendered resignation and will, not later than 90 days after the annual shareholders’ meeting, issue a press release which either confirms that it has accepted the resignation or provides an explanation for why it has refused to accept the resignation. The director tendering his or her resignation will not participate in any meeting of the Board or the Corporate Governance Committee at which the resignation is considered. Subject to any restrictions or requirements contained in applicable corporate law or Ballard’s constating documents, the Board may: (a) leave a resulting vacancy unfilled until the next annual shareholders’ meeting; (b) appoint a replacement director whom the Board considers merits the confidence of the shareholders; or (c) call a special meeting of shareholders to elect a replacement director who may be a person nominated by management. The policy does not apply in respect of any contested shareholders’ meeting, which is any meeting of shareholders where the number of nominees for director is greater than the number of directors to be elected.

BOARD MEETINGS

The Board meets on a regularly scheduled basis and directors are kept informed of our operations at meetings of the Board and its committees, and through reports by and discussions with management. In 2010, in-camera sessions were held after each regularly scheduled Board meeting. The in-camera sessions consisted of all of the independent directors without the presence of management. The Chair of the Board chairs the in-camera session. In 2010, there were 5 regularly scheduled meetings of the Board. In addition, communications between the directors and management occur apart from regularly scheduled Board and committee meetings. The Board has set a minimum meeting attendance guideline of 70%. Non-compliance with this guideline by a director is one of the factors considered in his or her individual performance evaluation at the end of the year.

COMMITTEES OF THE BOARD

The Board has established three standing committees: (1) the Audit Committee; (2) the MDNCC; and (3) the Corporate Governance Committee. Each committee has been delegated certain responsibilities, performs certain advisory functions and either makes certain decisions or makes recommendations to the Board. Each committee chair reports on the activities of the committee to the Board following each committee meeting. None of the members of these committees are current or former officers or employees of ours, or any of our subsidiaries.

15

In July 2009, in support of the Corporation's cost reduction initiatives, the Board decided to reduce the size of the standing committees. This was accomplished by providing that committee chairs no longer maintain membership on multiple committees. In order to maintain an adequate quorum on the Corporate Governance Committee following the departure of Mr. Kilroy from that Committee, Dr. Park joined the Committee at that time.

Following Dr. Sinclair’s resignation in June 2010, the Board determined that another director should replace her on the Management Development, Nominating & Compensation Committee in order to maintain adequate quorum. Given Mr. Kilroy’s previous experience serving on this committee, the Board approved his appointment as an exception to the requirement that committee chairs no longer maintain membership on multiple committees.

The information below sets out the members of each of our standing committees and indicates the number of meetings that each committee held in 2010. After the Meeting, we will reconstitute all of the committees to reflect the newly elected Board.

Audit Committee

The Audit Committee met 6 times during the financial year ended December 31, 2010. The members in 2010 were Ian A. Bourne, Edwin J. Kilroy (Chair), Mark A. Suwyn and Douglas W.G. Whitehead. All of the members of the Audit Committee are independent of our management in accordance with the applicable Canadian and United States securities laws and exchange requirements.

For a more detailed description of the Audit Committee or to see the Audit Committee’s mandate, a copy of which is posted on our website, see the section entitled "Board Committees – Audit Committee" in our Annual Information Form dated March 9, 2011, which section is incorporated by reference into this Management Proxy Circular.

Management Development, Nominating & Compensation Committee

The MDNCC met 4 times during the financial year ended December 31, 2010. The members in 2010 were Ian A. Bourne, Edwin J. Kilroy, Dr. C.S. Park and David B. Sutcliffe (Chair). All of the members of the MDNCC are independent of our management in accordance with the applicable Canadian and United States securities laws and exchange requirements.

For a more detailed description of the MDNCC or to see the MDNCC’s mandate, a copy of which is posted on our website, see the section entitled "Board Committees – Management Development, Nominating & Compensation Committee" in our Annual Information Form dated March 9, 2011, which section is incorporated by reference into this Management Proxy Circular.

Corporate Governance Committee

The Corporate Governance Committee met 4 times during the financial year ended December 31, 2010. The members in 2010 were Ian A. Bourne, Dr. C.S. Park and David J. Smith (Chair). All of the members of the Corporate Governance Committee are independent of our management in accordance with the applicable Canadian and United States securities laws and exchange requirements.

For a more detailed description of the Corporate Governance Committee or to see the Corporate Governance Committee’s mandate, a copy of which is posted on our website, see the section entitled "Board Committees – Corporate Governance Committee" in our Annual Information Form dated March 9, 2011, which section is incorporated by reference into this Management Proxy Circular.

CORPORATE GOVERNANCE

Our Board and senior management consider good corporate governance to be central to our effective and efficient operation. We monitor corporate governance initiatives as they develop and benchmark industry practices to ensure that we are in compliance with corporate governance rules.

16

Our corporate governance practices are reflected in our Corporate Governance Guidelines, which provide for director qualification standards, director responsibilities, the form and amount of director compensation, director orientation and continuing education, management succession planning and performance evaluation of the Board. A copy of the Corporate Governance Guidelines can be found on our website. We have also reviewed our internal control and disclosure procedures, and are satisfied that they are sufficient to enable our Chief Executive Officer and Chief Financial Officer to certify our interim and annual reports filed with Canadian securities regulatory authorities, and to certify our annual reports filed with or submitted to the SEC.

In addition, we have set up a process for shareholders to communicate to the Board, the details of which can be found on our website. A summary of shareholder feedback is provided to the Board through a semi-annual report.

For a more detailed description of our corporate governance policies and practices, see the section entitled "Corporate Governance" in our Annual Information Form dated March 9, 2011, which section is incorporated by reference into this Management Proxy Circular.

EXECUTIVE COMPENSATION

COMPENSATION DISCUSSION AND ANALYSIS

This section of this Management Proxy Circular contains a discussion of the elements of compensation earned by our "Named Executive Officers", who are listed in the Summary Compensation Table below: John W. Sheridan (President and Chief Executive Officer), Bruce Cousins(1) (former Vice President and Chief Financial Officer), Tony Guglielmin(2) (Vice President and Chief Financial Officer), Christopher J. Guzy (Vice President and Chief Technical Officer), Michael Goldstein (Vice President and Chief Commercial Officer) and William Foulds (Vice President and President, Ballard Material Products).

Objectives of Our Executive Compensation Program

The structure of our executive compensation program is designed to compensate and reward executives appropriately for driving superior performance. For our Named Executive Officers, a significant portion of their total direct compensation is "at risk" and tied closely to the success of the Corporation’s short and long-term objectives. "At risk" means that the executive will not realize value unless specified goals, many of which are directly tied to the Corporation’s performance, are achieved or the price at which our common shares are traded on the TSX or NASDAQ appreciates. In 2010, these performance goals, and resulting compensation awards, were largely focused on the Corporation’s key business drivers including growing revenue and building the long term order book, EBITDA(3) performance, reducing costs, customer deliveries and the delivery of key strategic business enablers to position the Corporation for long term success. This compensation philosophy puts a strong emphasis on pay for performance, and uses equity awards as a significant component in order to correlate the long-term growth of shareholder value with management’s most significant compensation opportunities. The strategic goals of the Corporation are reflected in the incentive-based executive compensation programs so that executives’ interests are aligned with shareholders interests.

| (1) | Mr. Cousins resigned as Chief Financial Officer on June 14, 2010.and provided transition support to Mr. Guglielmin until June 30, 2010 when he departed the company. | |

| (2) | Mr. Guglielmin was appointed Vice President and Chief Financial Officer on June 14, 2010. | |

| (3) | For a discussion of EBITDA and Adjusted EBITDA , please refer to Ballard’s Management’s Discussion & Analysis. | |

17

Philosophy and Objectives

Our philosophy and objectives regarding compensation are to:

| (a) | attract and retain experienced, qualified, capable executive officers by paying salaries which are competitive in the markets in which we compete for executive talent; | ||

| (b) | motivate short and long-term performance by directly linking annual bonuses to performance; and | ||

| (c) | link our executive officers' interests with those of our shareholders by providing our executive officers with equity-based compensation, requiring them to comply with minimum share ownership guidelines and build a sustained ownership position. | ||

How Executive Compensation is Determined

The MDNCC is charged, on behalf of our Board, with reviewing and approving executive officers’ benefit policies and compensation plans, including our annual bonus plan and our long-term equity-based compensation plans. As part of its mandate, the committee approves and recommends to the Board the appointment of our executive officers. The committee also reviews and approves the amount and form of their compensation, their development and succession plans, and any significant organizational or management changes. The committee retains independent compensation consultants for professional advice and as a source of competitive market information. In 2010, the committee directly retained Towers Watson (formerly Towers Perrin), on an as-needed basis, to provide independent advice related to Ballard executive compensation items. The committee also seeks the advice and recommendations of our President and Chief Executive Officer with respect to the compensation of our other executive officers. The President and Chief Executive Officer does not participate in the portions of the committee discussions that relate directly to his personal compensation.

Executive Pay Mix and the Emphasis on "At Risk" Pay

We place emphasis on performance by having a significant proportion of our executive officers’ total annual compensation linked to corporate and individual performance. For 2010, an average of 63% of the annual compensation earned by each of our Named Executive Officers came from "at risk", variable, performance-related compensation containing inherent market performance risk, where annual compensation includes base salary, annual bonus and equity-based long-term incentives (including share options and RSUs).

The Use of Benchmarking

Our overall compensation objective is to pay executives on average at the 50th percentile of the comparator group for full achievement of performance goals. Over-achievement or under-achievement will result in being over or under the average.

In late 2008, the MDNCC, working with Towers Watson, updated the comparator companies contained within the Corporation’s compensation comparator group to better reflect the Corporation’s business size and market focus following the divestment of the automotive business in January 2008. A new list of comparator companies was reviewed and accepted by the committee, which selected the group of comparators ensuring a suitable mix of Canadian and United States companies exhibiting a growth oriented mix of revenues, employee base, asset base, market capitalization and market focus. This comparator group comprises the primary source of compensation data for review of the Corporation’s market competitiveness. The committee reviews the composition of the comparator company list on an annual basis.

The committee compares each executive officer’s annual salary, target annual incentive bonus and long-term incentive compensation value, both separately and in the aggregate, to amounts paid for similar positions at comparator group companies. As noted above, the committee’s practice is to target annual total

18

direct compensation for each executive at approximately the 50th percentile among the comparator group companies.

The Corporation’s current comparator group is:

| Canadian Companies(4) | United States Companies | |

| Gennum Corporation | American Superconductor Corp. | |

| MacDonald Dettwiler and Associates Ltd. | Clean Energy Fuels Corp. | |

| QLT Inc. | Comverge Inc. | |

| Sierra Wireless Inc. | Energy Conversion Devices Inc. | |

| Westport Innovations Inc. | Evergreen Solar Inc. | |

| FuelCell Energy Inc. | ||

| Maxwell Technologies Inc. | ||

| PMC-Sierra Inc. | ||

| Plug Power Inc. | ||

| Power Integrations Inc. |

Current Executive Compensation Elements

Our compensation program for our executive officers has three primary components:

| (a) | annual salary; | ||

| (b) | annual incentives (bonus); and | ||

| (c) | equity-based long-term incentives comprised of awards that may be issued under our Option Plan or under the Market Purchase RSU Plan(5). | ||

Annual Salary

The MDNCC approves the annual salary of our executive officers. Salary guidelines and salary adjustments for our executive officers are considered with reference to:

| (a) | comparative market assessments performed by external compensation consultants; | ||

| (b) | the experience and qualifications of each executive officer; | ||

| (c) | the individual performance of each executive officer; and | ||

| (d) | the roles and responsibilities of each executive officer. | ||

The Corporation chooses to pay this element of compensation, because the Corporation’s view is that a competitive base salary is a necessary element for attracting and retaining qualified and experienced executive talent.

The Corporation’s decisions about this element of compensation and its annual level impacts decisions about the level of target annual incentive an executive might receive, but only in the sense that the incentive bonus target is set as a percentage of annual salary.

In 2010, there were no annual salary increases for the Named Executive Officers (with the exception of Mr. Foulds, who received an increase to $230,000 as a result of his elevation to a job level consistent with the other Senior Executives). However, in 2010 base salary levels for Named Executive Officers (with the

| (4) | Xantrex Technology was removed from the Canadian comparator group in 2009 following its acquisition by Schneider Electric. | |

| (5) | For a detailed description of our equity-based compensation plans, see “Equity Based Compensation Plans” and Appendix "A" and "B" of this Management Proxy Circular. | |

19

previously noted exception of Mr. Foulds) were restored to previous levels, following an action in 2009, where the full-time Named Executive Officers voluntarily accepted a temporary 10% reduction in base salary, consistent with the Corporation's overall cost reduction efforts and austerity measures.

Annual Bonus for Executive Officers

The MDNCC reviews and approves the annual bonus for each executive officer based on the recommendations of our President and Chief Executive Officer in accordance with the factors described in the foregoing section. Ballard had historically paid the annual bonus in Shares or in DSUs. Starting in 2010, the Corporation commenced the payment of annual bonuses for our Named Executive Officers in cash. This change was consistent with the overall move away from the use of treasury shares for compensation purposes and the changes approved by shareholders in 2009 related to the consolidation and funding of the Corporation's share and option based plans.

The annual target bonus for executive officers (excluding the President and Chief Executive Officer) was set at 70% of base salary in 2010. This bonus target had been reduced in 2008 to 70% from 75% in 2007 (this reduction followed a similar reduction in the target bonus level of 5% from 2006 levels to better align annual incentive levels to market levels relative to the Corporation’s comparator group). Each executive officer’s actual 2010 bonus was based on a combination of his individual performance and our corporate performance relative to goals, as discussed below under the section entitled "Methodology for Determining Annual Incentives".

The Corporation maintains an annual bonus program in order to motivate short and long-term performance by directly linking annual bonuses to the performance and progress of the Corporation.

The Corporation’s decisions about this element of compensation do not directly affect decisions about any other element of the Corporation’s compensation program.

For a full discussion of annual incentive compensation for our President and Chief Executive Officer, see the section entitled "Chief Executive Officer Compensation". The section below entitled "Methodology for Determining Annual Incentives" applies equally to the President and Chief Executive Officer as it does to the other executives.

Methodology for Determining Annual Incentives

The actual annual bonus for each executive officer is determined by the MDNCC on the basis of the following formula:

annual base salary x target bonus percentage x individual performance multiplier x corporate multiplier

The corporate multiplier is determined by the MDNCC and approved by the Board with reference to achievement against the corporate goals set out in a Corporate Performance Scorecard approved by the MDNCC and the Board prior to the commencement of the year. Each corporate performance goal on the scorecard is assigned a relative weighting in terms of importance to annual performance and growth of the Corporation, as well as a range of targeted outcomes, such that below a certain performance level the contribution of that goal to the overall corporate multiplier is zero. For 2010, the Corporate Performance Scorecard reflected a balance of Quantitative annual goals focussed on delivery of the 2010 operating plan (60% of the scorecard) and Qualitative goals focussed on key strategic outcomes during 2010 to position the Corporation for longer term success (40% of the scorecard). The Quantitative portion of the scorecard had 3 financial elements (Revenue from fuel cell products, Revenue from supporting business segments and EBITDA performance) and 3 operational elements (Cost of Goods Sold target improvements, on-time delivery of customer orders and building an order book for 2011). The Qualitative portion of the scorecard had 4 elements (successful execution of the sales/lease back agreement for the Burnaby location, demonstrating an EBITDA inflection point toward corporate profitability in Q4 2010, booking a major Distributed Generation sale in hydrogen by-product or wind application, and establishing key strategic systems and fuel processing capabilities for supplemental power).

20

Goals related to Revenue from the supporting business segments, Cost of Goods Sold target improvements and order book build for 2011 targets were all exceeded and received between 100% to 150% scoring in the overall corporate multiplier.

Targets related to on-time delivery of manufacturing orders, the sales leaseback transaction, DG sale in by-product hydrogen and strategic systems and fuel processing capability in supplemental power were all met, and received 100% scoring, while the EBITDA inflection point target was partially met and received a 50% score in the overall corporate multiplier.

While significant progress was made in 2010 in overall revenue growth and EBITDA performance, aggressive stretch targets related to Revenue from fuel cell products and EBITDA were not met and received 0% scoring in the overall corporate multiplier.

The overall corporate multiplier for 2010, as reviewed and agreed to by the MDNCC and the Board, based on achievement relative to these corporate goals, was 90%.

Given the nature of the corporate performance multiplier, for any particular year the corporate performance multiplier is not determined until our annual financial statements for that particular financial year are complete. However, notwithstanding that the corporate performance multiplier is not determined, and the annual bonus based thereon is not paid until the end of the first quarter following each particular financial year, in our summary compensation table we report the annual bonus for each particular financial year as if it had been determined and paid in the particular financial year.

A discussion of the annual base salary, target bonus percentage and corporate multiplier components of this annual incentive formula for each executive officer is set out above. The individual performance multiplier is determined with reference to achievement against the individual goals set for each executive officer, with an individual performance multiplier greater than 100% being awarded for superior performance against these goals, and an individual performance multiplier of less than 100% being awarded for substandard performance against these goals. Individual goals are set for individual executive officers by the Chief Executive Officer and are based on agreed-upon objective/identifiable measures relative to their respective functional accountabilities, which are aligned to the corporate performance goals. Our Named Executive Officers’ individual performance multipliers for 2010 ranged from 90% to 140%.

Mr. Guglielmin was appointed Chief Financial Officer on June 14, 2010. Although only a partial year, Mr. Guglielmin has met his overall performance goals for his CFO role, related to financial operations, administration, investor relations and information technology since the date of his appointment.

Mr. Guzy’s primary responsibilities for 2010, in his role of Vice President and Chief Technology Officer, were in research programs, product development and project implementation. Mr. Guzy met his goals in his fundamental accountabilities for product cost reduction goals, key technology development programs and the establishment of FuelWorks--the Fuel Processing Solutions Center of Excellence at the University of Maryland.

Mr. Goldstein continued key programs in 2010 to build stronger organizational capabilities in sales and marketing through the recruitment of external talent, sales training, improving the funnel management processes, etc. He also played a key leadership role in heightening the business focus on distributed generation business opportunities.

Mr. Foulds had a strong performance year in 2010. Under his leadership the Ballard Material Products division exceeded its goals, producing strong revenue growth and positive bottom line results.

Mr. Cousins resigned effective June 30, 2010 and did not receive an annual bonus for 2010, nor did he receive any severance payment.

Long Term Incentives

We provide our executive officers with equity-based long-term incentives through the Option Plan, Market Purchase RSU Plan and the SDP. These plans are designed to reinforce the connection between executive officer remuneration and our performance by motivating and rewarding participants for improving our long-term financial strength and enhancing shareholder value, and also providing retention value to

21

executives. With respect to equity-based long-term compensation awards for our executive officers, individual performance and future contribution expectations are taken into account in determining the award. In 2010, the President and Chief Executive Officer recommended to the MDNCC a value amount in dollars for each Named Executive Officer which considered the previous comparator company study by Towers Perrin (now Towers Watson), which was approved for each executive: see the amounts set out under “Share-Based Awards” and “Option-Based Awards” in our Summary Compensation Table. 50% of this value amount was then converted to RSUs at the then current market price by dividing the dollar value by the closing share price on either the TSX or NASDAQ on the award date. 50% of this value amount was converted to options by dividing the dollar value by the Black-Scholes value of a Ballard option on the award date. These options were then priced at the closing share price on the day prior to the award date.

A new hire Long Term Incentive award consisting of both options and RSUs was given to Mr. Guglielmin upon his appointment as executive to the Corporation on June 14, 2010.

This element of compensation and the Corporation’s decisions about this element fit into the Corporation’s overall compensation objectives in that they link our shareholders’ interests with those of our executive officers by providing our executive officers with equity-based compensation, and requiring them to comply with minimum share ownership guidelines.

The Corporation’s decisions about this element of compensation do not affect decisions about any other element of the Corporation’s compensation.

Share Options

Share options are granted annually in respect of approximately 50% of the long-term incentive compensation to be provided to an executive. As a result, previous grants of Share options are not generally taken into account when making new grants. The actual number of Share options granted is determined by dividing the dollar value of the portion of the long-term incentive to be satisfied though an option grant by the Black-Scholes value of a Ballard option on the award date.

Under our Option Plan:

| (a) | the exercise price of each option is determined by the Board, but must not be less than the closing price per Share on the TSX on the last trading day before the date the option is granted; and | ||

| (b) | each option may be exercised by the holder in respect of up to one-third of the Shares subject to the option on or after the first, second and third anniversary of the effective date of the option on a cumulative basis. | ||

Share options are typically granted for a term of seven years.

Restricted Share Units

Employees and executive officers are eligible to receive new RSU awards under the Market Purchase RSU Plan, which provides for vesting over periods of up to three years and awards may be subject to certain performance criteria, as determined by the Board upon the recommendation of the MDNCC. Redemption of these RSUs is satisfied with Shares bought under the Market Purchase RSU Plan.

The amount of the long-term incentive that is awarded to each executive officer is typically determined in the first quarter of each financial year, in conjunction with the determination of that executive officer’s annual bonus for the prior financial year. Since the long-term incentive is tied to future (as opposed to past) corporate performance, in our summary compensation table we report the grant of the long-term incentive in the "Share-Based Awards" column and the "Option-Based Awards" column for the particular year in which they were actually granted. The year-end values of unexercised or unvested Share options and RSUs, and the vesting during the year of Share options and RSUs are reported in the tables under the heading "Incentive Plan Awards".

New Issuances

On March 11, 2010, 254,587 RSUs were issued to the Named Executive Officers, including the President and Chief Executive Officer (this amount of RSUs does not include 50,000 units which were issued

22

to Mr. Cousins, but subsequently expired upon his departure). For all our executive officers who received an award on that date, the RSU awards included a performance criteria achievement goal of a minimum corporate multiplier of 75% in each of the 3 years of the award. With redemption of each 1/3 of the award subject to a minimum corporate performance of 75% in 2010, 2011 and 2012. Failure to meet this minimum corporate performance threshold in any one year results in that year’s award portion expiring and not being redeemed (see the section above entitled "Methodology for Determining Annual Incentives" for a description of the determination of the corporate multiplier).

Mr. Guglielmin received a grant of RSUs as part of his new hire award. These RSU awards were subject to time vesting only over 3 years. He received 75,676 RSUs on June 14, 2010.

Redemptions

On February 22 2010, 23,055 RSUs reached the end of their restriction period and after statutory withholdings, 13,167 RSUs were redeemed into Shares, representing one-third of the 2007 annual RSU long-term incentive award granted to Mr. Sheridan, Mr. Guzy and Mr. Foulds on February 22, 2007. These RSUs were redeemed into Shares following the Board’s previous confirmation that the performance criteria (>75% achievement of the corporate multiplier in 2007) was met.

On February 22 2010, 33,191 RSUs reached the end of their restriction period and after statutory withholdings, 18,993 RSUs were redeemed into Shares, representing one-third of the 2008 annual RSU long-term incentive award granted to Mr. Sheridan on May 12, 2008 and to Mr. Guzy and Mr. Foulds on February 21, 2008. These RSUs were redeemed into Shares following the Board’s confirmation that the performance criteria (>75% achievement of the corporate multiplier in 2008) was met. The remaining one-third of the RSU award will be issued to each executive officer in 2011, provided they remain employed by the Corporation on the respective redemption dates.

On May 4, 2010, 19,943 RSUs reached the end of their restriction period and after statutory withholdings, 11,228 RSUs were redeemed into Shares for Mr. Goldstein. This award was the first 1/3 of his new hire award, granted on May 5, 2009 and subject to time vesting only.

On April 30, 2010, 19,047 RSUs reached the end of their restriction period and after statutory withholdings, 10,724 RSUs were redeemed into Shares for Mr. Cousins. This award was the first 1/3 of his new hire award, granted on April 30, 2009 and subject to time vesting only. The remaining 2/3’s of this award was cancelled upon his departure, and no further RSUs were redeemed for shares to Mr. Cousins.

Chief Executive Officer Compensation

Mr. Sheridan was appointed President and CEO by the Board on February 22, 2006. When appointed, his base salary at that time was fixed at $530,000 Cdn per year. The CEO base salary has been frozen since that time, other than a 10% voluntary temporary reduction during the 2nd half of 2009. This base salary reduction from August until year end 2009, was volunteered as an austerity measure in support of cost reduction initiatives that were being implemented across the Corporation. In January 2010, Mr. Sheridan’s base salary returned to its original level of $530,000 Cdn per year.

Mr. Sheridan is entitled to receive an RRSP contribution (US$11,060 (6) in 2010). Due to changes in the corporate RRSP program in 2010 this benefit was reduced by 50% relative to 2009, and is now subject to an equivalent matching contribution from Mr. Sheridan. Mr. Sheridan is also entitled to receive company paid insurance premiums (US$1,826 (7) in 2010).

Mr. Sheridan’s target bonus for 2010, as detailed below was equal to 90% of his annual base salary. This level of target bonus has been reduced from 100% in 2007. Mr. Sheridan’s bonus for 2010 was determined by the MDNCC on the basis of corporate financial and operational performance reflected in the

____________________

| (6) | RRSP contribution was paid in Canadian dollars (C$11,000) and was converted into United States dollars for the purpose of the disclosure above using the Bank of Canada noon rate of exchange on December 31, 2010. | |

| (7) | Insurance premiums were paid in Canadian dollars (C$1,816) and were converted into United States dollars for the purpose of the disclosure above using the Bank of Canada noon rate of exchange on December 31, 2010. |

23

Corporate Performance Scorecard rating, plus performance relative to the CEO’s individual goals for 2010, as approved by the Board.

The MDNCC assessed Mr. Sheridan's financial and operational performance as being strong overall, as evidenced by strong operating results:

- Revenue: $65m (39% growth versus 2009)

- Adjusted EBITDA: - $26m (33% improvement versus 2009)

- Cash Flow from Operations: -$29.3m (30% improvement, excluding foreign exchange adjustments and Dantherm Power)

- Product Shipments: 3,014 Units (104% growth versus 2009)

- Gross Margin: 16% (3 point improvement versus 2009)

- Yearend Cash Reserves: $74.4m

In addition, the MDNCC recognized strong achievements relative to Mr. Sheridan’s individual goals, as approved by the Board of Directors, including the development of an effective operating model with Dantherm Power, effective strategic planning to position the Company to move to the ‘next level’ of growth and profitability, and the re-energization of the organization after the downsizing & cost-cutting in 2009.

These individual goals were purposely not weighted in advance so that the Board could retain the flexibility to assess the overall individual performance of Mr. Sheridan after reviewing all aspects of performance for the full year, without the constraint of a pre-set weighting on any particular goal.

After assessing the above achievements relative to the goals, the Board approved an individual performance multiplier of 125%. Applying this individual multiplier and the corporate multiplier of 90% (determined in accordance with the corporate multiplier methodology set forth in the section entitled "Methodology for Determining Annual Incentives"), to Mr. Sheridan’s target bonus for 2010 of 90% of base salary, resulted in a bonus payment to Mr. Sheridan of US$539,539(8) for the fiscal year ended December 31, 2010.

The total value of Mr. Sheridan's compensation in 2010 was US$1,612,180.

On March 11, 2010, the Board approved the recommendation by the MDNCC and Mr. Sheridan was granted a long-term incentive award, equivalent at the time of grant to a total value of US$502,894; with US$251,852 converted to options in respect of 185,185 Shares (at an exercise price of CDN$2.40 per Share) and a RSU award of US$251,042 (104,167 RSUs at a price of CDN$2.40 per Share). These awards formed Mr. Sheridan’s 2010 long-term incentive package, and the overall value and equity mix was approved by the MDNCC and the Board following consultations with Towers Watson. Consistent with other Named Executive Officers, the RSU award has performance criteria and time vesting as described above in the Restricted Share Units – New Issuances section, and the share options were granted with a 7-year term, with one-third of the options vesting at the end of each of the first three years.