Weatherford International Ltd./Switzerland (WFT) Inactive

Filed: 17 Apr 14, 12:00am

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

SCHEDULE 14A

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the Securities

Exchange Act of 1934

| Filed by the Registrant |  | Filed by a Party other than the Registrant |

| Check the appropriate box: | |

| Preliminary Proxy Statement |

| Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| Definitive Proxy Statement |

| Definitive Additional Materials |

| Soliciting Material Under §240.14a-12 |

WEATHERFORD INTERNATIONAL LTD.

(Name of Registrant as Specified In Its Charter)

NOT APPLICABLE

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

| Payment of Filing Fee (Check the appropriate box): | ||

| No fee required. | |

| Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |

| (1) | Title of each class of securities to which transaction applies: | |

| (2) | Aggregate number of securities to which transaction applies: | |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): | |

| (4) | Proposed maximum aggregate value of transaction: | |

| (5) | Total fee paid: | |

| Fee paid previously with preliminary materials. | |

| Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |

| (1) | Amount Previously Paid: | |

| (2) | Form, Schedule or Registration Statement No.: | |

| (3) | Filing Party: | |

| (4) | Date Filed: | |

Dear Fellow Weatherford Shareholder,

In last year’s Proxy Statement, we discussed board actions and changes, and outlined our mission to ensure that Weatherford’s business and affairs are managed in a manner that is effective and accountable, and serves your long-term interests. Mindful of these objectives, over the past year, we have worked alongside Weatherford’s management and employees in a manner we believe position the company to build and pursue a foundation of sustainable long-term returns and margins. Our industrial core is built upon exceptional competence around a distinctive group of specialized business segments. Our industrial mission is well-defined. We will relentlessly pursue the highest possible shareholder returns with the same drive and dedication our owners should expect from a management team that also views itself, above all, as owners. In the past year we have achieved fundamental progress.

Our Foundational Accomplishments

During 2013, we successfully remediated our material weakness in income tax accounting, negotiated a settlement of our FCPA and trade sanctions matters, and renewed our focus on cash generation and returns. We believe these foundational accomplishments position Weatherford on a path towards a culture of efficiency, operational excellence, and capital and administrative quality. We are now moving forward with a focus on growing our core businesses and divesting non-core assets. In March, we announced the signing of an agreement for the first of these planned divestitures.

Weatherford’s Future

A successful business requires a supportive and stable pro-business and regulatory environment in which to operate and grow and which will allow us to manage our business in a predictable manner over time. As such, we have closely monitored proposed and recently implemented changes to Swiss law that would limit Weatherford’s ability as a multinational company to retain and attract key executive talent and directors, today and into the future. In addition, this new legislation will significantly increase administrative costs and result in more complex corporate functions, all of which could have long-term adverse effects on the company.

Swiss law provides that changes to corporate and other laws can be put to a national referendum of voters at the request of Swiss citizens who obtain a requisite number of signatures. If a referendum is approved by voters, it is adopted into the Swiss constitution without a legislative process. Irish law provides that corporate and other laws, including those which may be put to a national referendum of voters and adopted into the Irish constitution, can only be initiated through the legislative process. There is no analogous procedure whereby Irish citizens, by obtaining a requisite number of signatures, can initiate such laws or put them to a national referendum outside the legislative process. Thus we believe the legal and regulatory environment in Ireland is more predictable and stable.

As a result, we are recommending that Weatherford change its place of incorporation from Switzerland to Ireland.

Why Incorporate in Ireland?

We anticipate a NYSE-traded parent company incorporated in Ireland will provide us the following benefits:

| • | Our Strategy: Weatherford has implemented initiatives and measures needed to reengineer and turnaround the company on what we expect will be a long-term financially rewarding path. Our present focus is to grow our four core businesses, Well Construction, Formation Evaluation, Completion and Artificial Lift, lower our cost structure and generate cash. Our planned divestiture of non-core assets is essential and imperative to the company’s future success. We believe an Irish incorporation will provide us additional flexibility required to execute and quickly move forward. Incorporating in Ireland will best enable the execution of these goals and solidly move Weatherford along its transformational path. |

| • | Our People: Our employees and executives are essential to our success. As a multinational company in the oil and gas industry competing with other multinational companies, we need the flexibility to attract and retain talented executives and directors. In order to best address future shareholder interests, we need to continue to preserve our ability to recruit and select highly qualified directors with diverse skills, expertise and experience to serve on our Board. Over the last year, we have been in the advantageous position to be able to add two outstanding new members whose specific skills have supported the company’s efforts and foundational progress. We further need the ability to properly and competitively incentivize candidates in their roles. Recent changes in Swiss law limit our ability to attract and retain top talent. This could have an adverse impact on us, thus hindering our efforts to achieve our objectives. Today, our legacy issues are behind us. Our ability to retain and attract talent is a primary component driving our future progress and growth. We believe Ireland would provide us the best corporate environment as a multinational company to achieve our goals. |

| • | Irish Legal System: Ireland is a common law jurisdiction, which is more consistent with the legal system in the United States. We believe our shareholders are most accustomed to this system, combined with the rules and regulations of the SEC and NYSE. We also believe a common law system is more flexible than civil law jurisdictions such as Switzerland. We believe this flexibility will be beneficial to us in paying future dividends (including facilitating a potential spin-off of our land rig business via a stock dividend), administering corporate functions and, in conjunction with, other corporate governance matters. We believe that Irish corporate and common law combined with our shares being listed on the NYSE as well as continued compliance with SEC rules and regulations will achieve an ideal balance between robust external governance oversight and shareholder rights. |

Weatherford International Ltd. - 2014 Extraordinary General Meeting i

| • | Shareholder Rights: Ireland has a stable and well-developed legal system that includes an established and predictable corporate governance regime, which provides shareholders with substantial rights. As an Irish company subject to the rules of the SEC and the NYSE, our shareholders will continue to have the annual right to elect directors and hold an advisory vote on executive compensation, as well as to vote on any amendment to our Articles of Incorporation and Memorandum of Association or the creation of any preferred shares. A detailed comparison of shareholder rights is included on page 41. |

| • | Cost Effectiveness: The new regulatory and governance requirements of Switzerland are complex. This would result in increased general and administrative costs which could be significant. Conversely, the Irish common law system enables greater cost-effectiveness and a more flexible business environment. In addition to further reducing our cost structure, we plan to delist from the SIX Swiss Exchange and the NYSE Euronext-Paris. The reduction in legal and other administrative costs from delisting will benefit the company. In addition, the delisting will relieve our shareholders of the administrative costs of complying with the multiple filing and other requirements of the SIX and Euronext exchanges. We reiterate that our shares will continue to be listed on the NYSE and we will continue to be regulated by the SEC. |

| • | Ireland: The country is an attractive proposition from an economic and business perspective. Ireland represents a stable, cost-effective corporate environment which will serve us well, and be an essential component to Weatherford’s turnaround success. An Irish incorporation will ensure a business-friendly base for Weatherford’s global operations. This proposed redomiciliation will bring us closer to our U.K. operations, which includes approximately 1,500 employees, our regional office in Aberdeen, Scotland, and numerous operational and manufacturing facilities which contribute several hundred million of US dollars in annual revenue. In addition, we believe that the perception of an Irish company among regulatory authorities, investors, creditors, and customers is highly favorable. |

We are asking you to approve a corporate reorganization which will merge the current company (“Weatherford Switzerland”) into its newly formed subsidiary, Weatherford International Limited (“Weatherford Ireland”). After the merger, Weatherford Ireland will be the parent company of the Weatherford group of companies.

Your Weatherford share ownership-what changes?

After the merger, your registered shares in Weatherford Switzerland will become ordinary shares in Weatherford Ireland. While Swiss and Irish corporate law differ in some respects, we believe our new charter documents will preserve key features and rights you currently have such that Weatherford Ireland ordinary shares will be substantially similar to those of the Weatherford Switzerland registered shares that you currently own. Examples of these rights, before and after the merger, can be found on page v. A detailed summary is included herein under the section titled “Comparison of Shareholder Rights” starting on page 41.

Your Weatherford share ownership-what stays the same?

The merger will not affect the number of shares you own or your economic ownership. As a result of the merger, all of the assets and liabilities of Weatherford Switzerland will be transferred to Weatherford Ireland. Weatherford will continue to conduct its day-to-day business as we do now and, as noted above, we expect the ordinary shares of Weatherford Ireland to be listed on the NYSE. We will remain subject to SEC reporting requirements, the mandates of the Sarbanes-Oxley Act, the Dodd-Frank Wall Street Reform and Consumer Protection Act and the corporate governance rules of the NYSE. We will continue to report our consolidated financial results in U.S. dollars and under U.S. GAAP. Also, Weatherford will continue to hold an Annual General Meeting at which our shareholders will vote to elect directors, and to approve other matters including an advisory vote on executive compensation. Finally, we intend for Weatherford Ireland to maintain Swiss tax residency, the current tax residency of Weatherford Switzerland.

With Weatherford Ireland as our parent company, we believe that the equity and rights of our shareholders will continue to be best safeguarded. As such, we encourage you to carefully read this proxy statement/prospectus and ask that you vote FOR the proposals described in this proxy statement/prospectus.

Thank you for your investment

Weatherford has an outstanding industrial core which is backed by the quality of our management and employees. We are firm in our strategy, culture and unshakeable intent to grow shareholder value for the benefit of our clients, owners and employees. Weatherford has a well-defined industrial mission built upon distinctive cutting-edge proprietary technologies and exceptional collective expertise. We are finally free to focus on strategic, tactical and shareholder value issues without any legacy accounting or legal distractions. The company has been redirected and is set on a focused path of core, cost and cash. This is the next chapter in our history, and we are proud to serve as your directors. We take this opportunity to thank you for your determined and steadfast trust and support. We are confident that Weatherford’s entrepreneurial spirit combined with a disciplined and focused path will drive great future opportunities.

Weatherford International Ltd. - 2014 Extraordinary General Meeting ii

April 17, 2014

Dear Fellow Shareholder:

I am pleased to invite you to participate in an Extraordinary General Meeting of Shareholders, which will be held at 12:00 P.M. (Central European Time) on Monday, June 16, 2014, at the Theater Casino Zug located at Artherstrasse 2-4, 6300 Zug, Switzerland.

Please vote right away

We are asking you to approve a proposal that would change Weatherford’s jurisdiction of incorporation from Switzerland to Ireland. Ireland’s established pro-business framework has attracted many of the world’s leading corporations, creating a successful and competitive business environment which we expect will serve Weatherford well. If the proposal is approved by the shareholders, your relative economic interest in our company will remain unchanged. The number of Weatherford Ireland ordinary shares you will own will be the same as the number of common shares you held in Weatherford Switzerland. The redomiciliation will provide the company with the ability to quickly and efficiently execute and move forward on our transformational path. This step would ensure that we reach our goals in the best way possible as we embark on this new chapter in our history.

Weatherford Ireland will remain subject to U.S. SEC reporting requirements (including mandatory votes on executive compensation), the Sarbanes-Oxley Act, the Dodd-Frank Wall Street Reform and Consumer Protection Act as well as the applicable rules of the NYSE. In addition, Weatherford Ireland will continue to report consolidated financial results in U.S. dollars and under U.S. GAAP. We are also asking our shareholders to approve a proposal relating to the creation of “distributable reserves” which are required under Irish law to, among other things, be able to pay future dividends or repurchase ordinary shares.

These proposals will promote Weatherford’s future success, and therefore, the Board recommends that you give your support by voting FOR the proposed agenda items.

Your vote is very important. Whether or not you plan to attend the meeting, we strongly encourage you to carefully read this proxy statement/prospectus and provide your proxy by telephone, the internet or by completing, signing and returning the enclosed proxy card at your earliest convenience.

Our Direction: Core, Cost and Cash

Growth around a specific industrial focus enabled Weatherford to develop into a multinational integrated oilfield service provider in only a quarter of a century. We did this from very humble beginnings with essentially nothing at the start. This course has been rewarding to shareholders, clients and employees through this period of time. Over the 27 years since inception in 1987, Weatherford, and our predecessor company EVI, have delivered a compound annual growth rate of share price appreciation of approximately 19% per annum. This was in spite of difficult years in 2009-2012. These were truly challenging times. After a constructive year of problem resolution in 2013, Weatherford’s financial and operational performance is turning around here and now.

Weatherford’s board of directors and executive leadership understand that our earlier strategy of aggressive growth created organizational inefficiencies, leading to issues that distracted the company and tested shareholder resolve. Today, these legacy issues are behind us. We are focused now on the industrial development of your company for shareholder wealth generation.At Weatherford, when we focus on something, we do it well. It is a fundamental trait and character of your organization.

Weatherford has implemented the initiatives and measures needed to leverage and further develop our industrial strength and turnaround the company onto a long-term financially rewarding path. These initiatives are here, in progress and designed to last. Our steadfast commitment is to deliver sustainable high returns to shareholders through direction and relentless focus on three simple actions:Core, Cost and Cash.

| • | Core: We will grow our core. We are focusing on four product lines: Well Construction, Formation Evaluation, Completion and Artificial Lift. This includes also concentrating on people, technology, sales and quality. Our non-core businesses have already been identified as land drilling rigs, pipeline and specialty services, drilling fluids, testing and production services as well as wellheads. These are part of an aggressive and ongoing divestiture program, the successful completion of which is essential for management at all levels to refocus on the remaining core businesses. We have already started this process, and recently announced the successful signing of a definitive agreement to sell the pipeline and specialty services business. After years of investing and building, Weatherford is where its clients need it to be in every sense: strategically, technologically, operationally and geographically. In 2014, we will see a disciplined growth around our core businesses. We will not steer away from our core. |

Weatherford International Ltd. - 2014 Extraordinary General Meeting iii

| • | Cost: Efficiency will be a way of life. While maintaining quality of execution, running support functions and operations with a lower cost structure is a key management metric. We are currently engaged in an aggressive cost reduction program, involving a lower support headcount and eliminating unprofitable operations. Going forward, as we further grow our core business we are committed to keep our support cost base efficient, driving better margins. |

| • | Cash: The culture of cash is embedded in the DNA of the company, and is here to stay. We will generate free cash flow, efficient working capital, and lower capital intensity compatible with growing our core. Our objective is to reduce our net debt to total capitalization ratio from 52% to 25% over the next few years through a combination of higher, sustainable and growing free cash flow augmented by divestiture proceeds. The sooner, the better. |

Exceptional women and men are leading Weatherford’s turnaround

Our employees are the future of Weatherford and a compelling reason for optimism. We are concentrating on our people: not only their training, development and retention, but also to allow a constant stream of hiring of the industry’s best talents. In a vibrant oilfield services labor market, recruiting and retaining strong performers is a constant challenge. Our transformational program is heavily dependent on our ability to attract and retain top talent. Acting as responsible stewards of your capital and moving forward in 2013 and beyond, it is in our shareholders’ best interest that we preserve our ability to recruit and select new highly qualified directors whose significant experience and depth of knowledge can continue to provide us with input and sound direction as we continue to pursue and build the highest possible shareholder returns. Over the last year, two of our directors have retired. We were fortunate to be able to quickly attract top talent whose specific skills have supported the company’s efforts and foundational progress. Legislative changes in Switzerland (particularly in reference to the Minder Initiative) will make it extremely difficult to recruit the best that the industry has to offer. Our incorporation under Irish law would maintain Weatherford’s steady transformational course, allow us to operate at the lowest possible cost and strengthen the company’s ability to retain, as well as further attract, the best talent in the industry. Weatherford’s future success depends on talented employees, managers, executives and directors. Our incorporation under Irish law would provide Weatherford the best environment to achieve these objectives. This is not a small issue.

The Weatherford Board appreciates your support and involvement

The joint effect of divesting non-core assets and lowering our cost structure is powerful. The successful completion of our cost reduction and divestment initiatives are of immediate priority to the entire management team. These essential steps will position Weatherford to deliver sustainable long-term performance driven by high margins and high cash returns. Weatherford is steadfast in delivering its product and service portfolio which is a result of our long-term industrial vision. Weatherford is strategically well positioned for the future, and its core should experience some of the industry’s strongest and long-lasting growth. We are immeasurably grateful to our shareholders, first, for their patience, and now, for their continued commitment towards our progress and transformational path. Weatherford’s industrial might will again reemerge to the greater benefit of our clients, shareholders and employees. We are ready to shine on an organized and disciplined course forward. Please help us make this happen.

The Weatherford Board and its senior management is very grateful for your support and involvement.

| Sincerely, | ||

| ||

| Bernard J. Duroc-Danner | ||

| Chairman of the Board, | ||

| President and Chief Executive Officer |

Weatherford International Ltd. - 2014 Extraordinary General Meeting iv

Due to the complex nature of Swiss and Irish corporate law, we have provided some examples to help you understand your rights as a shareholder before and after the Merger, including as they relate to SEC and NYSE rules and requirements, as Weatherford remains subject to these rules and requirements both before and after the Merger.

These examples are for illustrative purposes only. Please refer to “Comparison of Shareholder Rights” on page 41 for a detailed summary of your current rights as holder of Weatherford Switzerland shares and as holder of Weatherford Ireland shares following the Merger.

| Example shareholder rights | Before Merger | After Merger | ||

| Shareholders election of directors |  May only serve on Board if elected by majority of votes cast May only serve on Board if elected by majority of votes castFrequency of Vote: Annually | May only serve on Board if elected by majority of votes cast Frequency of Vote: Annually | ||

| Number of directors | Minimum 3; Maximum 18 | Minimum 3; Maximum 14 | ||

| Shareholders vote to approveexecutive compensation at annual general meeting | Non-binding until 2015 Frequency of Vote: Annually | Non-binding Frequency of Vote: Annually | ||

| Shareholder may submitproposals at annual general meeting |  60 - 90 days prior to the annual general meeting by shareholders holding no less than CHF 1 million in nominal value (e.g. 862,068 shares) 60 - 90 days prior to the annual general meeting by shareholders holding no less than CHF 1 million in nominal value (e.g. 862,068 shares) | 60 - 90 days prior to the anniversary of prior annual general meeting by shareholders holding no less than 860,000 ordinary shares | ||

| Shareholder right to call specialmeetings | Upon request by shareholders holding at least 10% of shares | Upon request by shareholders holding at least 10% of shares | ||

| Shareholder right to removedirectors | Requires approval of two-thirds of votes represented at a shareholders meeting (plus an absolute majority of the par value of shares) | Requires approval by a majority of votes actually cast at a shareholders meeting | ||

| Shareholder right to fill directorvacancies | Vacancy filled only by approval of shareholders at general meeting | Vacancy filled by approval of shareholders at general meeting. Board of directors also has power to fill vacancies in the board | ||

| Payment of dividends | Requires shareholder resolution | Directors may approve without shareholder resolution | ||

| Merger vote requirement | At least two-thirds of the votes represented at a shareholders meeting (plus the majority of the par value of shares) | Generally, at least a majority in number of shareholders, representing at least 75% of the votes cast at shareholders meeting. If a takeover offer, requires acquisition of more than 50% of voting rights; may squeeze out others if buyer acquires at least 80% of shares to which the offer relates | ||

| Mandatory takeover bid | Upon acquisition of 33.33% of voting rights | Upon acquisition of 30% of voting rights | ||

| Voting rights – One vote per share | | | ||

| Preferred shares | Not authorized; shareholder approval by at least two-thirds of the votes represented at shareholders meeting (plus the majority of the par value of shares) | Not authorized; shareholder approval by at least 75% of the votes cast | ||

| Quorum (generally) | One-third of shares in share register and entitled to vote | 50% of total issued voting rights | ||

| Preemptive rights | Shareholders have preemptive rights, however, Weatherford Switzerland has opted for them to be limited or withdrawn by the board in many circumstances | Shareholders have preemptive rights, however, Weatherford Ireland has opted out of them, but the opt-out requires renewal every 5 years | ||

| Amendment to Articles ofAssociation (Switzerland) / Memorandum and Articles of Association (Ireland) | Except in limited circumstances, only by resolution of shareholders at general meeting; requires for certain changes at least two-thirds of the votes represented at shareholders meeting (plus the majority of the par value of shares) | Only by resolution of shareholders at general meeting; requires at least 75% of the votes cast | ||

| No transfer restrictions on shares (subject to applicable securities laws) | | |

Weatherford International Ltd. - 2014 Extraordinary General Meeting v

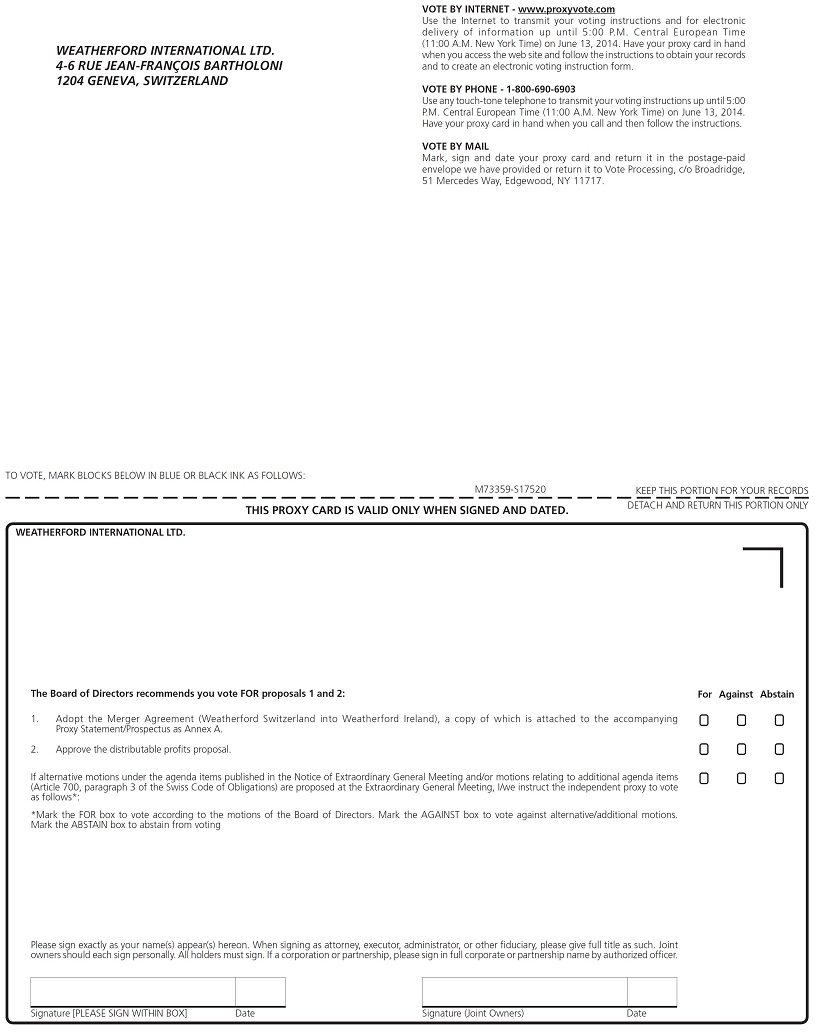

Vote before our Extraordinary General Meeting

Every vote matters to the future of Weatherford. Even if you plan to attend the meeting, please take the time to vote in advance using one of the following methods.

In all cases, have your proxy card or voting instruction form in hand and follow the instructions.

| Agenda items that require your vote | Board recommendation | |

| ITEM 1 | Adopt the Merger Agreement (Weatherford Switzerland into Weatherford Ireland), a copy of which is attached to the accompanying proxy statement/prospectus as Annex A. | FOR |

| ITEM 2 | Approve the distributable profits proposal. | FOR |

| You are a shareholder of record |

If you hold Weatherford shares directly in your name, please complete,sign and return your proxy cardas follows:

| Vote by mail |

| When— Complete and send your proxy card immediately to allow time for our receipt of your completed proxy card on or before June 13, 2014 | |

| How— Follow these instructions to mark, sign and date your proxy card |

| You are a beneficial shareholder |

If you hold your Weatherford shares through a broker, bank or other nominee,you can vote by Internet, by telephone or by mail.

| Visit our Extraordinary General Meeting of Shareholders Website |  |

We have centralized all of our Extraordinary General Meeting materials in one place atwww.wftproxy.com

There, you can download electronic copies of our Proxy Statement/ Prospectus, and use the link to vote

| www.proxyvote.com |

| When— 24h/7 until 5:00 P.M. Central European Time (11:00 A.M. New York Time) on June 13, 2014 | |

| How— Use the Internet to transmit your voting instructions |

| 1-800-690-6903 |

| When— 24h/7 until 5:00 P.M. Central European Time (11:00 A.M. New York Time) on June 13, 2014 | |

| How— Use any touch-tone telephone to transmit your voting instructions |

Weatherford International Ltd. - 2014 Extraordinary General Meeting vi

April 17, 2014

Dear fellow shareholder:

I am pleased to invite you to participate in an Extraordinary General Meeting of Shareholders, which will be held at 12:00 p.m. (Central European Time) on Monday, June 16, 2014, at the Theater Casino Zug located at Artherstrasse 2-4, 6300 Zug, Switzerland.

We will be asking you to approve a proposal that would result in a corporate reorganization of Weatherford International Ltd., our current Swiss public holding company (“Weatherford Switzerland”), and the group of companies it controls. If the proposal is approved by our shareholders, we will merge Weatherford Switzerland into Weatherford International Limited, a newly formed private limited company incorporated under Irish law, which will be re-registered as an Irish public limited company and renamed “Weatherford International plc” or a similar name prior to the effective time of the merger (“Weatherford Ireland”). Weatherford Ireland would become our new public holding company and would serve as the parent of the Weatherford group of companies. The merger would also result in your holding ordinary shares in Weatherford Ireland rather than registered shares in Weatherford Switzerland.

The merger will not affect the number of shares you hold or your economic ownership. We will continue to conduct our business as we do now, and we expect the ordinary shares of Weatherford Ireland to be listed on the New York Stock Exchange under the symbol “WFT,” the same symbol under which your registered shares of Weatherford Switzerland are currently listed. We will remain subject to the U.S. Securities and Exchange Commission (“SEC”) reporting requirements, the mandates of the Sarbanes-Oxley Act, the Dodd-Frank Wall Street Reform and Consumer Protection Act and applicable corporate governance rules of the New York Stock Exchange, and we will continue to report our consolidated financial results in U.S. dollars and in accordance with U.S. generally accepted accounting principles. We will also continue to have annual meetings of shareholders for the election of directors and annual shareholder advisory votes on executive compensation as required by SEC rules. Furthermore, we will comply with any additional reporting and governance requirements of Irish law. We intend for Weatherford Ireland to maintain Swiss tax residency, the current tax residency of Weatherford Switzerland.

If the merger agreement is adopted by our shareholders, we will ask you at the meeting to approve a proposal to create “distributable profits.” Under Irish law, Weatherford Ireland requires distributable profits in order to make distributions to shareholders (including dividends) and, generally, to undertake share repurchases and share redemptions. While the board of directors recommends that shareholders vote for both proposals, approval of the distributable profits proposal is not a condition to proceeding with the merger, and adoption of the merger agreement is not conditional upon the approval of the distributable profits proposal.

Under U.S. federal income tax law and Swiss tax law, the holders of registered shares of Weatherford Switzerland generally are not expected to recognize any gain or loss on the cancellation of their Weatherford Switzerland registered shares as consideration for the allotment of ordinary shares of Weatherford Ireland in the merger.We urge you to consult your own tax advisor regarding your particular tax consequences.

This proxy statement/prospectus provides you with detailed information regarding the transactions. We encourage you to read this entire proxy statement/prospectus carefully.In particular, you should carefully consider “Risk Factors” beginning on page 16 for a discussion of risks related to the transactions before voting.

Weatherford International Ltd. - 2014 Extraordinary General Meeting vii

Your vote is important. Whether or not you plan to attend the meeting, we strongly encourage you to provide your proxy by telephone, the internet or by completing, signing and returning the enclosed proxy card at your earliest convenience.

Your Board of Directors has unanimously approved the transactions and recommends that you vote “FOR” the proposals described in this proxy statement/prospectus.

Thank you for your cooperation and support.

| Sincerely, | ||

| ||

| Bernard J. Duroc-Danner | ||

| Chairman of the Board, | ||

| President and Chief Executive Officer |

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities to be issued in the transaction described in this proxy statement/prospectus or determined if this proxy statement/prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This proxy statement/prospectus is dated April 17, 2014 and it is first being mailed to shareholders on or about April 24, 2014.

Weatherford International Ltd. - 2014 Extraordinary General Meeting viii

![]()

| Notice of Extraordinary General Meeting of Shareholders |

June 16, 2014

12:00 P.M. (Central European Time)

Theater Casino Zug, Artherstrasse 2-4, 6300 Zug, Switzerland

AGENDA ITEMS

| 1. | Adopt the merger agreement (the “Merger Agreement”), a copy of which is attached to the accompanying proxy statement/ prospectus as Annex A, by and between Weatherford International Ltd., our current Swiss public holding company (“Weatherford Switzerland”), and Weatherford International Limited, a newly formed private limited company incorporated under Irish law and a wholly-owned subsidiary of Weatherford Switzerland (“Weatherford Ireland”), pursuant to which Weatherford Switzerland will be merged into Weatherford Ireland and each registered share of Weatherford Switzerland will be cancelled as consideration for the allotment of one ordinary share of Weatherford Ireland (except for registered shares held by, or for the benefit of, Weatherford Switzerland or any of its subsidiaries, which will also be cancelled, but for which no ordinary shares of Weatherford Ireland will be allotted). Weatherford Ireland will be re-registered as an Irish public limited company and renamed “Weatherford International plc” or a similar name prior to the effective time of the merger. | |

| 2. | If the Merger Agreement is adopted, approve the creation of distributable profits of Weatherford Ireland under Irish law by reducing the entire share premium of Weatherford Ireland (or such lesser amount as may be determined by the Board of Directors of Weatherford Ireland) resulting from the allotment and issue of Weatherford Ireland ordinary shares pursuant to the Merger Agreement. We refer to this proposal as the “distributable profits proposal.” |

Your Board of Directors has unanimously approved the transactions and recommends that you vote “FOR” the proposals described in this proxy statement/prospectus.

ORGANIZATIONAL MATTERS

We have established the close of business on May 19, 2014, as the record date for determining the shareholders listed in our share register (registered shareholders) entitled to attend, vote or grant proxies to vote at the meeting or any adjournments or postponements of the meeting.

A copy of this proxy statement/prospectus and enclosed proxy card are also being sent to each shareholder registered in our share register as of March 27, 2014. Any additional shareholders who are registered in our share register on our record date of May 19, 2014, will receive a copy of these materials after the record date.

Only shareholders who are registered in our share register as of May 19, 2014, will be entitled to attend, vote or grant proxies to vote at the meeting.

April 17, 2014

By Order of the Board of Directors

Alejandro Cestero

Corporate Secretary

Weatherford International Ltd. - 2014 Extraordinary General Meeting ix

This proxy statement/prospectus incorporates documents by reference which contain important business and financial information about us that is not included in this proxy statement/prospectus and which documents are described under “Where You Can Find More Information.” These documents are available to any shareholder, including any beneficial owner, free of charge upon request directed to Investor Relations, Weatherford International Ltd., 2000 St. James Place, Houston, Texas 77056, telephone (713) 836-4000. To ensure timely delivery of these documents, any request should be made no later than five business days prior to the meeting. The exhibits to these documents will generally not be made available unless they are specifically incorporated by reference in this proxy statement/prospectus.

You should rely only on the information contained or incorporated by reference in this proxy statement/prospectus. We have not authorized anyone else to provide you with different information. The information contained or incorporated by reference in this proxy statement/prospectus is accurate only as of the date thereof (unless the information specifically indicates that another date applies), or in the case of information incorporated by reference, only as of the date of such information, regardless of the time of delivery of this proxy statement/prospectus. Our business, financial condition, results of operations and prospects may have changed since such dates. Therefore, you should not rely upon any information that differs from or is in addition to the information contained in this proxy statement/prospectus or in the documents incorporated by reference.

Weatherford International Ltd. - 2014 Extraordinary General Meeting x

Weatherford International Ltd. - 2014 Extraordinary General Meeting xi

Weatherford International Ltd. - 2014 Extraordinary General Meeting xii

Weatherford International Ltd. - 2014 Extraordinary General Meeting xiii

This page intentionally left blank.

Information about the Meeting and Voting

Date and Time

Monday, June 16, 2014, at 12:00 p.m. (Central European Time).

Place

Theater Casino Zug, Artherstrasse 2-4, 6300 Zug, Switzerland.

General

We are furnishing this proxy statement/prospectus to our shareholders in connection with the solicitation of proxies by the board of directors of Weatherford International Ltd., a Swiss joint-stock corporation (“Weatherford Switzerland”), for use at the Extraordinary General Meeting of Shareholders of Weatherford Switzerland.

This proxy statement/prospectus and the enclosed proxy card are being mailed on behalf of Weatherford Switzerland’s board of directors to all shareholders beginning on or about April 24, 2014.

Weatherford Switzerland’s principal executive offices in Switzerland are located at 4-6 Rue Jean-François Bartholoni, 1204 Geneva, Switzerland and our telephone number at that location is +41.22.816.1500.

Agenda

At the Extraordinary General Meeting, shareholders will be asked to vote on the following agenda items:

| • | Item 1: Adopt the merger agreement (the “Merger Agreement”), a copy of which is attached to this proxy statement/prospectus as Annex A, by and between Weatherford Switzerland and Weatherford International Limited, a newly formed private limited company incorporated under Irish law and a wholly-owned subsidiary of Weatherford Switzerland (“Weatherford Ireland”). |

| • | Item 2: Approve the distributable profits proposal. |

Who Can Vote

All shareholders registered in our share register (registered shareholders) at the close of business on the record date of May 19, 2014 have the right to attend the Extraordinary General Meeting and vote their shares. Such shareholders are entitled to one vote per registered share at the Extraordinary General Meeting.

Proxies Solicited By

Your vote and proxy are being solicited by our board of directors in favor of Buis Bürgi AG, acting as independent proxy, for use at the Extraordinary General Meeting.

How to Vote

All registered shareholders at the close of business on the record date of May 19, 2014 have the right to attend the Extraordinary General Meeting and vote their shares. However, to ensure your representation at the Extraordinary General Meeting, we request that you grant your proxy to vote on each of the proposals in this notice and any other matters that may properly come before the meeting to the person named in the enclosed

Weatherford International Ltd. - 2014 Extraordinary General Meeting 1

proxy card by completing, signing, dating and returning the enclosed proxy card for receipt by us no later than June 13, 2014, whether or not you plan to attend the meeting.

Most of our individual owners hold their shares through a brokerage account and therefore are not listed in our share registry. Shareholders who hold their shares through a bank, broker or other nominee (in “street name”) must vote their shares in the manner prescribed by their bank, broker or other nominee. We generally refer to these shareholders as holding their shares “beneficially” and to these banks, brokers or other nominees as “brokers.” Shareholders who hold their shares in this manner and wish to vote in person at the meeting must obtain a valid proxy from the broker that holds their shares. This may be very difficult for an individual shareholder to do, so individual shareholders holding their shares in street name are strongly encouraged to submit their proxy to their broker, who in turn will vote in accordance with their directions. See “— Quorum/Voting” as to the effect of broker non-votes.

Proxies

A copy of this proxy statement/prospectus and enclosed proxy card are being sent to each shareholder registered in our share register as of March 27, 2014. Any additional shareholders who are registered in our share register on our record date of May 19, 2014 will receive a copy of these proxy materials after May 19, 2014. Shareholders not registered in our share register as of May 19, 2014 will not be entitled to attend, vote or grant proxies to vote at the Extraordinary General Meeting. No shareholder will be entered in our share register as a shareholder with voting rights between the close of business (Eastern Standard Time) on May 19, 2014 and the opening of business on the day following the Extraordinary General Meeting. American Stock Transfer & Trust Company LLC (“AST”), which maintains our share register, will, however, continue to register transfers of our registered shares in the share register in its capacity as transfer agent during this period.

In accordance with recently-enacted Swiss regulations, shareholders may no longer appoint company officers as proxies. We therefore request that you grant your proxy to vote on each of the proposals described in this proxy statement/prospectus and any other matters that may properly come before the meeting to Buis Bürgi AG, acting as independent proxy, by completing, signing, dating and returning the enclosed proxy card for receipt by us no later than June 13, 2014, whether or not you plan to attend.

Shares of registered shareholders who have timely submitted a properly executed proxy card by mail and specifically indicated their votes will be voted as indicated. If you are a registered shareholder and you properly give a proxy, but do not indicate how you wish to vote, your proxy will vote your shares in accordance with the recommendations of our board of directors.

We may accept a proxy by any form of communication permitted by Swiss law and Weatherford Switzerland’s articles of association.

Revoking Your Proxy

If you are a registered shareholder, you may revoke your proxy by:

| • | writing to the Secretary at 4-6 Rue Jean-François Bartholoni, 1204 Geneva, Switzerland for arrival by June 13, 2014; |

| • | submitting a later-dated proxy via mail for receipt by us no later than June 13, 2014; or |

| • | (i) presenting yourself in person to our Secretary at the entrance of the meeting no later than one hour prior to the start of the Extraordinary General Meeting, (ii) declaring your intent to revoke your proxy and cast your vote in person at the Extraordinary General Meeting and (iii) applying with the Secretary for the remittance of the necessary voting documentation upon presentation of documents evidencing your position as shareholder as of the record date of May 19, 2014. |

You may not revoke a proxy simply by attending the Extraordinary General Meeting. To revoke a proxy, you must take one of the actions described above.

If you are a beneficial shareholder who holds your shares through a broker, you must follow the instructions provided by your broker if you wish to revoke a previously granted proxy.

Outstanding Shares

As of April 4, 2014, the most recent practicable date before the date of this proxy statement/prospectus, there were approximately 772,618,358 registered shares issued and entitled to vote. We do not expect the number of such shares to be materially different on the record date.

Quorum/Voting

The presence in person or by proxy of at least one-third of the registered shares entitled to vote will form a quorum. Under Swiss law, treasury shares are not counted for purposes of determining whether a quorum is present and are not entitled to vote. If you have properly given a proxy by mail, your shares will count toward the quorum, and the person named on the proxy card will vote your shares as you have instructed. See “— Proxies.”

Pursuant to Swiss law and Weatherford Switzerland’s articles of association, the following are counted for quorum purposes: (i) registered shares represented at the Extraordinary General Meeting for which votes are withdrawn or withheld on any matter; (ii) registered shares that are represented by “broker non-votes” (i.e., registered shares held by brokers that are represented at the Extraordinary General Meeting, but with respect to which the broker is not empowered to vote on a particular proposal); and (iii) registered shares for which the holder abstains from voting or submits blank or invalid ballots on any matter.

If you are a beneficial shareholder and your broker holds your shares in “street name,” the broker is permitted to vote your shares with respect to “routine” proposals, even if the broker does not receive voting instructions

Weatherford International Ltd. - 2014 Extraordinary General Meeting 2

from you. However, your broker may not vote your shares with respect to “non-routine” proposals. Proxies submitted by brokers without instructions from customers for non-routine matters are referred to as “broker non-votes.” Under the rules of the New York Stock Exchange (“NYSE”), we believe that all of the proposals in this proxy statement/prospectus are non-routine proposals. Accordingly, if you hold your shares in “street name,” your broker will not be able to vote your shares in these matters unless your broker receives voting instructions from you.

Approval of the proposal to adopt the Merger Agreement in Agenda Item 1 to be presented at the Extraordinary General Meeting requires the affirmative vote of at least two-thirds of the voting rights of the shareholders voting on this proposal at the Extraordinary General Meeting (which must also represent an absolute majority of the par value of the shares represented at the meeting). Abstentions, “broker non-votes,” blank or invalid and withdrawn votes will be counted as a vote against the proposals. Although the board of directors recommends that shareholders vote for both proposals, the adoption of the Merger Agreement in Agenda Item 1 is not conditional upon the approval of the distributable profits proposal in Agenda Item 2. However, please see “Risk Factors — If the distributable profits proposal is not approved by our shareholders and the High Court of Ireland, Weatherford Ireland will not be able to make distributions or, generally, undertake share purchases or share redemptions until such time as it has created sufficient distributable profits from its trading activities following the Merger” for a discussion of ways in which the Merger would be affected if the distributable profits proposal is not approved.

Approval of the distributable profits proposal in Agenda Item 2 to be presented at the Extraordinary General Meeting requires the affirmative vote of a relative majority of the shareholders voting on this proposal at the Extraordinary General Meeting. A “relative majority” means a majority of the votes actually cast for or against the matter being determined, disregarding abstentions, “broker non-votes,” blank or invalid ballots and withdrawn votes. In addition, while approval of the distributable profits proposal by the relative majority of the votes cast is sufficient for approval of the proposal under Swiss law (which governs the Extraordinary General Meeting at which the vote is taking place), we are seeking the approval of not less than 75% of the votes cast, in person or by proxy, at the meeting to increase the likelihood of obtaining Irish High Court approval with respect to the creation of distributable profits in Weatherford Ireland because such higher approval threshold would be required if the vote on the distributable profits proposal was being conducted under Irish law.

Multiple Proxy Cards

If you receive multiple proxy cards, this indicates that your shares are held in more than one account, such as two brokerage accounts, and are registered in different names. You should complete and return each of the proxy cards to ensure that all of your shares are voted.

Cost of Proxy Solicitation

We have retained AST Phoenix Advisors to solicit proxies from our shareholders at an estimated fee of $15,000, plus expenses. Some of our directors, officers and employees may solicit proxies personally, without any additional compensation, by telephone or mail. Proxy materials also will be furnished without cost to brokers and other nominees to forward to the beneficial owners of shares held in their names. All costs of proxy solicitation will be borne by us.

Proxy Holders Of Deposited Shares

Institutions subject to the Swiss Federal Law on Banks and Savings Banks as well as professional asset managers who hold proxies for beneficial owners who did not grant proxies to the person named on the proxy card are requested to inform us of the number and par value of the registered shares they represent as soon as possible, but no later than 12:00 p.m. (Central European Time) on the day of the Extraordinary General Meeting at the admission office for the Extraordinary General Meeting.

Inspection Rights

In accordance with Swiss law, Weatherford Switzerland and Weatherford Ireland will allow their shareholders, during a 30-day period prior to the Extraordinary General Meeting, to inspect at the registered office of Weatherford Switzerland at Alpenstrasse 15, 6300 Zug, Switzerland, and the registered office of Weatherford Ireland at 70 Sir John Rogerson’s Quay, Dublin 2, Ireland, the following documents: (i) the Merger Agreement; (ii) the joint merger report of the board of directors of Weatherford Switzerland and the board of directors of Weatherford Ireland; (iii) the auditors report on the Merger; and (iv) the annual accounts and annual reports of the preceding three business years of the merging companies, as applicable. Copies of these materials may also be obtained without charge by contacting Investor Relations at +1 (713) 836-4000 or emailing us atinvestor.relations@weatherford.com.

Questions

You may call our proxy solicitor, AST Phoenix Advisors, at 1-800-252-7164 (toll-free) or +1 (201) 806-2222 (International), or our U.S. Investor Relations Department at +1 (713) 836-4000 or email us atinvestor.relations@weatherford.com if you have any questions or need directions to be able to attend the meeting and vote in person.

PLEASE VOTE – YOUR VOTE IS IMPORTANT

Weatherford International Ltd. - 2014 Extraordinary General Meeting 3

We are seeking your approval of a proposal that would result in a corporate reorganization of Weatherford Switzerland, our current Swiss public holding company, and the group of companies it controls. If the proposal is approved by our shareholders, we would effect a merger (the “Merger”) whereby Weatherford Switzerland will be merged into Weatherford Ireland. Weatherford Ireland has only nominal assets and has not engaged in any business or other activities other than in connection with its formation and transactions contemplated hereby. The Merger would be effected pursuant to the Merger Agreement, dated as of April 2, 2014, between Weatherford Switzerland and Weatherford Ireland, as it may be amended, a copy of which is attached to this proxy statement/prospectus as Annex A, by way of an international (cross border) merger without liquidation of Weatherford Switzerland in compliance with, inter alia, Art. 3 et seq. Swiss Act on Merger, Demerger, Transformation and Transfer of Assets and Art. 163b, 163c and 164 Swiss Private International Law Act and applicable laws of Ireland. Weatherford Ireland will be re-registered as an Irish public limited company and renamed “Weatherford International plc” or a similar name prior to the effective time of the Merger.

As a result of the Merger:

| • | Weatherford Ireland will be the surviving company and will become our new public holding company and the parent of the Weatherford group of companies; |

| • | each registered share of Weatherford Switzerland you hold immediately prior to the effective time of the Merger will be cancelled as consideration for the allotment to you of one ordinary share of Weatherford Ireland; |

| • | you will receive shares of Weatherford Ireland and your rights as a shareholder will be governed by Irish law and by Weatherford Ireland’s memorandum and articles of association, which will be amended and restated prior to the effective date of the Merger in substantially the form attached to this proxy statement/prospectus as Annex B; |

| • | the assets and liabilities of Weatherford Switzerland will be transferred to Weatherford Ireland by operation of law; and |

| • | Weatherford Ireland will assume certain employee benefit plans that had previously been sponsored by Weatherford Switzerland and we will amend such plans in order to permit the issuance or delivery of Weatherford Ireland ordinary shares thereunder, instead of Weatherford Switzerland registered shares. |

The Merger will not affect the number of shares you hold or your economic ownership. We will continue to conduct our business as we do now, and we expect the ordinary shares of Weatherford Ireland will be listed on the NYSE under the symbol “WFT,” the same symbol under which your registered shares of Weatherford Switzerland are currently listed. Currently, there is no established public trading market for the ordinary shares of Weatherford Ireland. In connection with the Merger, we plan to delist the Weatherford Switzerland registered shares from the SIX Swiss Exchange and the NYSE Euronext-Paris. We do not plan for Weatherford Ireland’s ordinary shares to be listed on the SIX Swiss Exchange, the NYSE Euronext-Paris or the Irish Stock Exchange.

We will remain subject to the U.S. Securities and Exchange Commission (the “SEC”) reporting requirements, the mandates of the Sarbanes-Oxley Act, the Dodd-Frank Wall Street Reform and Consumer Protection Act and applicable corporate governance rules of the NYSE, and we will continue to report our consolidated financial results in U.S. dollars and in accordance with U.S. generally accepted accounting principles (“U.S. GAAP”). We will also continue to have annual meetings of shareholders for the election of directors and annual shareholder advisory votes on executive compensation as required by SEC rules. Furthermore, we will comply with any additional reporting and governance requirements of Irish law. We intend for Weatherford Ireland to maintain Swiss tax residency, the current tax residency of Weatherford Switzerland.

The following diagram depicts our organizational structure immediately before and after the Merger. The diagram does not depict any other legal entities in the Weatherford group owned by Weatherford Switzerland before the Merger or Weatherford Ireland after the Merger.

If the Merger Agreement is adopted by the requisite vote of our shareholders and the other conditions to completing the Merger are satisfied, we will file an application to effect the Merger with the commercial register of the Canton of Zug, Switzerland (the “Commercial Register”) as soon as practicable following the approval. We expect that the application will be approved and the Merger effected approximately two-weeks after such filing subject to approval by the Swiss Federal Commercial Register. We currently expect to complete the Merger in the second quarter of 2014, although we may postpone or abandon the Merger at any time prior to the effective time of the Merger, even after the shareholders have adopted the Merger Agreement at the Extraordinary General Meeting.

In this proxy statement/prospectus, “we,” “us” and “our” refer to, as the context requires, Weatherford Switzerland, together with its subsidiaries, prior to the Merger and Weatherford Ireland, together with its subsidiaries, following the Merger. References in this proxy statement/prospectus to Weatherford Switzerland shares and Weatherford Ireland shares means the registered shares of Weatherford Switzerland, having a par value of 1.16 Swiss francs each, and the ordinary shares of Weatherford Ireland, nominal value of $0.001 per share, respectively.

Weatherford International Ltd. - 2014 Extraordinary General Meeting 4

QUESTIONS AND ANSWERS ABOUT THE MERGER

The following questions and answers are intended to address briefly what we expect to be commonly asked questions regarding the proposed Merger. These questions and answers do not address all questions that may be important to you. Please refer to the more detailed information contained elsewhere in this proxy statement/prospectus, its annexes and exhibits and the documents referred to or incorporated by reference in this proxy statement/ prospectus. For instructions on obtaining the documents incorporated by reference, see “Where You Can Find More Information.”

| Q: | What is the Merger? |

| A: | Pursuant to the Merger Agreement, a copy of which is attached to this proxy statement/prospectus as Annex A, and by way of an international (cross border) merger without liquidation of Weatherford Switzerland in compliance with, inter alia, Art. 3 et seq. Swiss Act on Merger, Demerger, Transformation and Transfer of Assets and Art. 163b, 163c and 164 Swiss Private International Law Act and applicable laws of Ireland, Weatherford Switzerland will merge into Weatherford Ireland, which will become our new public holding company and the parent of the Weatherford group of companies. The assets and liabilities of Weatherford Switzerland will be transferred to Weatherford Ireland by operation of law. In the Merger, each Weatherford Switzerland share will be cancelled as consideration for the allotment of one Weatherford Ireland share (except for Weatherford Switzerland shares held by, or for the benefit of, Weatherford Switzerland or any of its subsidiaries, which will also be cancelled, but for which no Weatherford Ireland shares will be allotted). As a result, your rights as a shareholder will be governed by Irish law and by Weatherford Ireland’s memorandum and articles of association, which will be amended and restated prior to the effective date of the Merger in substantially the form attached to this proxy statement/prospectus as Annex B. |

| The Merger will not affect the number of shares you hold or your economic ownership. We will continue to conduct our business as we do now, and we expect that the Weatherford Ireland shares will be listed on the NYSE under the symbol “WFT,” the same symbol under which your Weatherford Switzerland shares are currently listed. Currently, there is no established public trading market for the Weatherford Ireland shares. In connection with the Merger, we plan to delist the Weatherford Switzerland shares from the SIX Swiss Exchange and the NYSE Euronext-Paris. We do not plan for Weatherford Ireland’s shares to be listed on the SIX Swiss Exchange, the NYSE Euronext-Paris or the Irish Stock Exchange. | |

| We will remain subject to SEC reporting requirements, the mandates of the Sarbanes-Oxley Act and applicable corporate governance rules of the NYSE, and we will continue to report our consolidated financial results in U.S. dollars and in accordance with U.S. GAAP. We will also continue to have annual meetings of shareholders for the election of directors and annual shareholder advisory votes on executive compensation as required by SEC rules. Furthermore, we will comply with any additional reporting and governance requirements of Irish law. We intend for Weatherford Ireland to maintain Swiss tax residency, the current tax residency of Weatherford Switzerland. | |

| Q: | What vote does the Weatherford Switzerland board of directors recommend? |

| A: | Your board of directors has unanimously approved the Merger Agreement and recommends that you vote “FOR” the proposals described in this proxy statement/prospectus. |

| Q: | Who are the parties to the Merger? |

| A: | The parties to the Merger are Weatherford Switzerland and Weatherford Ireland. Weatherford Ireland is a newly formed, wholly-owned subsidiary of Weatherford Switzerland, has only nominal assets and has not engaged in any business or other activities other than in connection with its formation and transactions contemplated hereby. |

| Q: | What are the major actions that have been performed or will be performed to effect the Merger? |

| A: | We have taken or will take (or cause to be taken) the actions listed below to effect the Merger: |

| • | Weatherford Ireland was formed as a wholly-owned subsidiary of Weatherford Switzerland; | |

| • | the Merger Agreement was signed by Weatherford Switzerland and Weatherford Ireland; | |

| • | shareholders will vote on the adoption of the Merger Agreement at the Extraordinary General Meeting; and | |

| • | if the Merger Agreement is adopted by the requisite vote of our shareholders and the other conditions to completion of the Merger are satisfied, we will file an application to effect the Merger with the Commercial Register as soon as practicable following the approval. We expect that the application will be approved and the Merger effected approximately two-weeks after such filing subject to approval by the Swiss Federal Commercial Register. | |

| Q: | What are the conditions to completing the Merger? |

| A: | The Merger cannot be completed without satisfying certain conditions, the most important of which is that shareholders must adopt the Merger Agreement. In addition, there are other conditions such as the requirement to obtain authorization for listing Weatherford Ireland’s shares on the NYSE, receipt of any consents required to complete the Merger and receipt of certain legal opinions. Please see “Agenda Item 1 Adoption of the Merger Agreement — Conditions to Completion of the Merger.” |

| Q: | What will I receive in the Merger? |

| A: | In the Merger, you will receive one Weatherford Ireland share for each Weatherford Switzerland share you hold immediately prior to the effective time of the Merger. |

| Q: | If the Merger Agreement is adopted, am I required to take any action with respect to my new holding of Weatherford Ireland shares? |

| A: | This depends on how you currently hold your Weatherford Switzerland shares. In the Merger, each Weatherford Switzerland share will be cancelled as consideration for the allotment and issue of one Weatherford Ireland share (except for Weatherford Switzerland shares held by, or for the benefit of, Weatherford Switzerland or any of its subsidiaries, which will also be cancelled, but for which no Weatherford Ireland shares will be allotted). |

Weatherford International Ltd. - 2014 Extraordinary General Meeting 5

All Weatherford Ireland shares allotted to, or for the benefit of, the former holders of Weatherford Switzerland shares in connection with the Merger will be promptly issued at the effective time of the Merger to a bank or trust company selected by Weatherford Switzerland to act as exchange agent in connection with the Merger (including its successors, affiliates or designees, the “Exchange Agent”) or, in the case of former holders of Weatherford Switzerland shares deposited with the Depository Trust Company (“DTC”), to DTC.

| • | Beneficial holders. Beneficial holders of our shares held in “street name” through a bank, broker, trustees, custodians or other nominee within the facilities of DTC will not be required to take any further action. We generally refer to these shareholders as holding their shares “beneficially” and to these banks, brokers, trustees, custodians or other nominees as “brokers.” Your ownership of new Weatherford Ireland shares will be recorded in book-entry form by your broker without the need for any additional action on your part. | |

| • | Registered holders. If you hold Weatherford Switzerland share certificates or you are a registered holder of Weatherford Switzerland shares recorded in book-entry form, the Exchange Agent will hold your Weatherford Ireland shares, and all entitlements (including dividend entitlements) arising therefrom, as nominee on your behalf pending formal delivery of such shares to you. Such share delivery shall be subject to customary exchange procedures established by the Exchange Agent to implement the delivery. In this regard, as soon as reasonably practicable after the effective time of the Merger, the Exchange Agent will mail a letter of transmittal to you, which will, among other matters, contain instructions as to how you may: (i) register your new Weatherford Ireland shares directly in your own name or that of your designee and have a new share certificate or certificates issued to you (if you hold shares in certificated form); (ii) register your new Weatherford Ireland shares directly in your own name or that of your designee in book-entry form; or (iii) deposit your Weatherford Ireland shares in the facilities of DTC.YOU SHOULD NOT RETURN SHARE CERTIFICATES WITH THE ENCLOSED PROXY CARD. |

As of April 4, 2014, the most recent practicable date before the date of this proxy statement/prospectus, approximately 99% of our shares (other than treasury shares) were held in “street name” through a broker. However, each shareholder should independently confirm how they hold shares.

If you wish to have your Weatherford Ireland shares registered directly in your own name (and to be issued a share certificate, if requested), you will not be charged any fees to do so by the Exchange Agent or Weatherford Ireland.

Until persons holding certificates representing previous Weatherford Switzerland shares or who were registered holders of Weatherford Switzerland shares elect, in accordance with the procedures set forth in the letter of transmittal, as to how they desire to hold their new Weatherford Ireland shares, those persons will not be able to transfer their new Weatherford Ireland shares. Such persons will, however, be able to vote their new Weatherford Ireland shares through the Exchange Agent acting as their proxy pending formal delivery of legal title thereto.

Any Weatherford Ireland shares issued to the Exchange Agent that remain undelivered to the former holders of Weatherford Switzerland shares as of the 12 month anniversary of the effective time of the Merger (or the termination of the Exchange Agent’s engagement, if later) will be delivered to Weatherford Ireland or its designee, together with all entitlements (including dividend entitlements) arising therefrom, upon demand, and Weatherford Ireland or its designee will thereafter continue to hold such shares and entitlements, as nominee for, and on behalf of, the former holders of Weatherford Switzerland shares, on substantially similar terms as the Exchange Agent, pending formal delivery of legal title thereto, but subject to applicable abandoned property, escheat or similar laws. No interest shall be payable on any dividend entitlements or other amounts held, from time to time, by Weatherford Ireland, the Exchange Agent or any of their respective affiliates or designees as nominee for any former holder of Weatherford Switzerland shares, and none of Weatherford Ireland, the Exchange Agent or any of their respective affiliates or designees shall be required to account to any former holder of Weatherford Switzerland shares for same.

If you elect to register your new Weatherford Ireland shares directly in your own name or that of your designee, you should particularly note that subsequent transfers of Weatherford Ireland shares may be subject to Irish stamp duty. Please see “Material Tax Considerations — Irish Tax Considerations — Stamp Duty” for a more detailed description of the Irish stamp duty. As a result, persons holding certificates representing Weatherford Switzerland shares or who are a registered holder of Weatherford Switzerland shares are strongly encouraged to deposit and maintain their holdings within the facilities of DTC going forward.

| Q: | Will the Merger result in any changes to my rights as a shareholder? |

| A: | Your rights as a shareholder of Weatherford Switzerland are governed by Swiss law and Weatherford Switzerland’s articles of association. After the Merger, you will become a shareholder of Weatherford Ireland and your rights will be governed by Irish law and Weatherford Ireland’s memorandum and articles of association as they will be in effect after the Merger. The legal system governing corporations organized under Irish law differs from the legal system governing corporations organized under Swiss law. As a result, while many of the principal attributes of Weatherford Switzerland’s shares and Weatherford Ireland’s shares will be similar under Swiss and Irish corporate law, differences will exist. In addition, the provisions of Weatherford Ireland’s proposed memorandum and articles of association will be substantially similar to the provisions of Weatherford Switzerland’s articles of association, except for changes (i) required by Irish law, or (ii) necessary in order to preserve the current rights of shareholders and powers of the board of directors of Weatherford Ireland following the Merger. We summarize your rights as a shareholder under Swiss law and under Irish law following the Merger and the material differences between the governing documents for Weatherford Switzerland and Weatherford Ireland under “Comparison of Shareholders Rights.” A copy of Weatherford Ireland’s memorandum and articles of association in substantially the form to be amended and restated prior to the effective date is attached to this proxy statement/prospectus as Annex B. |

| Q: | Will the Merger dilute my economic interest? |

| A: | No. Immediately after the effective time of the Merger, your relative economic ownership in Weatherford Ireland will remain the same as your relative economic ownership in Weatherford Switzerland immediately prior to the effective time of the Merger. |

| Q: | Are Weatherford Switzerland shareholders able to exercise appraisal rights? |

| A: | Yes. Weatherford Switzerland shareholders whose shares are registered in their name can exercise appraisal rights under Article 105 of the Swiss Merger Act by filing suit against Weatherford Ireland for the examination of equity and membership interests. The suit must be filed within two months after the publication of the Merger resolution. An appraisal suit can be filed by shareholders who vote against the Merger Agreement, who abstain from voting or who do not participate in the shareholders meeting approving the Merger Agreement. A shareholder who votes in favor of the adoption of the Merger Agreement proposal |

Weatherford International Ltd. - 2014 Extraordinary General Meeting 6

may also be able to file a suit. If a suit is filed, the court will determine the compensation, if any, that it considers adequate. Because shareholders will receive, as consideration in the Merger, Weatherford Ireland shares on a one-for-one basis and the assets and liabilities of Weatherford Switzerland will be transferred to Weatherford Ireland in the Merger, we believe that the equity and membership interests of Weatherford Switzerland shareholders are adequately safeguarded. If a claim by one or more Weatherford Switzerland shareholders is successful, all of the Weatherford Switzerland shareholders who held Weatherford Switzerland shares at the effective time of the Merger would receive the same compensation. The filing of an appraisal suit will not prevent the completion of the Merger. If you are a beneficial owner and your Weatherford Switzerland shares are held in “street name” by a broker, you should consult with your broker. For more information about appraisal rights, please see “Agenda Item 1 Adoption of the Merger Agreement — Appraisal Rights.” | |

| Q: | What is the distributable profits proposal and how does it relate to the Merger? |

| A: | Under Irish law, distributions to shareholders (including dividends) and, generally, share repurchases and share redemptions may only be made from “distributable profits” of Weatherford Ireland. These profits are determined by reference to an unconsolidated balance sheet prepared in accordance with the Companies Acts 1963-2013 of Ireland (the “Irish Companies Acts”). Immediately following the Merger, Weatherford Ireland will not have any distributable profits. If the Merger Agreement is adopted, our shareholders will also be asked at the meeting to approve the creation of distributable profits of Weatherford Ireland by reducing the entire share premium of Weatherford Ireland (or such lesser amount as may be determined by the board of directors of Weatherford Ireland) resulting from the allotment and issue of Weatherford Ireland shares pursuant to the Merger. |

| In addition, the distributable profits proposal requires the approval of the High Court of Ireland. If our shareholders approve the distributable profits proposal and the Merger is completed, Weatherford Ireland intends to seek the approval of the High Court of Ireland for the distributable profits proposal as soon as practicable following the completion of the Merger. The approval of the High Court of Ireland is expected to be obtained within 15 weeks of the completion of the Merger. Although we are not aware of any reason why the High Court of Ireland would not approve the distributable profits proposal, it is a matter of judicial discretion and there is no guarantee that such approval will be forthcoming. | |

| While the board of directors recommends that shareholders vote for the distributable profits proposal, approval of the distributable profits proposal is not a condition to the Merger. We currently do not plan to make any distributions, other than the potential spin-off of our rigs business. If the distributable profits proposal is not approved by our shareholders and the High Court of Ireland, Weatherford Ireland will not be able to make distributions and, generally, undertake share purchases or share redemptions until such time as it has otherwise created sufficient distributable profits from its trading activities following the Merger. See “Risk Factors” and “Agenda Item 2 Approval of the Distributable Profits Proposal.” | |

| Q: | When do you expect to complete the Merger? |

| A: | If the Merger Agreement is adopted by our shareholders, and the other conditions to completing the Merger are satisfied, we currently expect to complete the Merger in the second quarter of 2014. We may postpone or abandon the Merger at any time prior to the effective time of the Merger, even after the shareholders have adopted the Merger Agreement at the Extraordinary General Meeting. Although the board of directors recommends that shareholders vote for both proposals, the adoption of the Merger Agreement in Agenda Item 1 is not conditional upon the approval of the distributable profits proposal in Agenda Item 2. |

| However, please see “Risk Factors — If the distributable profits proposal is not approved by our shareholders and the High Court of Ireland, Weatherford Ireland will not be able to make distributions or, generally, undertake share purchases or share redemptions until such time as it has created sufficient distributable profits from its trading activities following the Merger” for a discussion of ways in which the Merger would be affected if the distributable profits proposal is not approved. | |

| Q: | Why do you want to change the place of incorporation of the Weatherford group’s publicly traded parent from Switzerland to Ireland? |