UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

xANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2013

or

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES ACT OF 1934

For the transition period from _____________ to _____________

Commission file number: 000-53559

GEPCO, LTD.

(Exact name of registrant as specified in its charter)

| Nevada | 80-0212045 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

| 9025 Carlton Hills Blvd. Ste. B, Santee, CA | 92071 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code

909-708-4303

Securities registered pursuant to Section 12(b) of the Act: None.

Securities registered pursuant to Section 12(g) of the Act: Common stock, $0.001 par value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. o Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. o Yes x No

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes o No

Indicate by checkmark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). x Yes o No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulations S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer o | Accelerated Filer o | |

Non-accelerated Filer¨ (Do not check if a smaller reporting company) | Smaller Reporting Company x |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). o Yes x No

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter of June 30, 2013 was $429,642.

On March 26, 2014, the Company had 221,252,555 outstanding shares of Common Stock, $.001 par value per share.

TABLE OF CONTENTS

Page

| PART I | 2 | |

| Item 1. | BUSINESS | 2 |

| Item 1A. | RISK FACTORS | 11 |

| Item 1B. | UNRESOLVED STAFF COMMENTS. | 15 |

| Item 2. | PROPERTIES | 15 |

| Item 3. | LEGAL PROCEEDINGS | 15 |

| Item 4. | MINE SAFETY DISCLOSURES | 15 |

| PART II | 16 | |

| Item 5. | MARKET FOR THE REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES | 16 |

| Item 6. | SELECTED FINANCIAL DATA | 16 |

| Item 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 17 |

| Item 7A. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 19 |

| Item 8. | FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA | 19 |

| Item 9. | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE | 19 |

| Item 9A. | CONTROLS AND PROCEDURES | 20 |

| Item 9B. | OTHER INFORMATION | 21 |

| PART III | 22 | |

| Item 10. | DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE | 22 |

| Item 11. | EXECUTIVE COMPENSATION | 24 |

| Item 12. | SECURITIES OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS | 25 |

| Item 13. | CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE | 27 |

| Item 14. | PRINCIPAL ACCOUNTING FEES AND SERVICES | 28 |

| Item 15. | EXHIBITS, FINANCIAL STATEMENTS SCHEDULES | 29 |

| i |

Introductory Comment

Throughout this Annual Report on Form 10-K, the terms “we,” “us,” “our” and the “Company” refer to Gepco, Ltd. and our subsidiary, Gemvest Ltd.

“Safe Harbor” Statement

From time to time, we make oral and written statements that may constitute “forward-looking statements” (rather than historical facts) as defined by the Securities and Exchange Commission (the “SEC”) in its rules, regulations and releases, including Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”).

All statements in this Annual Report, including under the captions “Business” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” other than statements of historical fact, are forward-looking statements for purposes of these provisions, including statements of our current views with respect to our business strategy, business plan and research and development activities, our future financial results, and other future events. These statements include forward-looking statements both with respect to us, specifically, and the technology industry, in general. In some cases, forward-looking statements can be identified by the use of terminology such as “may,” “will,” “expects,” “plans,” “anticipates,” “estimates,” “potential” or “could” or the negative thereof or other comparable terminology. Although we believe that the expectations reflected in the forward-looking statements contained herein are reasonable, there can be no assurance that such expectations or any of the forward-looking statements will prove to be correct, and actual results could differ materially from those projected or assumed in the forward-looking statements.

All forward-looking statements involve inherent risks and uncertainties, and there are or will be important factors that could cause actual results to differ materially from those indicated in these statements. Such risk factors include, among others: whether the Company can successfully execute its operating plan, including the Company’s ability to integrate acquired companies and technology; the Company’s ability to retain key employees; general market conditions; and other factors discussed under the captions “Business” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” all of which you should review carefully. If one or more of these or other risks or uncertainties materialize, or if our underlying assumptions prove to be incorrect, actual results may vary materially from what we anticipate. Please consider our forward-looking statements in light of those risks as you read this Annual Report. Actual results may differ materially from those contained in the forward-looking statements in this Annual Report. The Company does not undertake any obligation to update or revise forward-looking statements to reflect changed assumptions, the occurrence of unanticipated events or changes to future operating results. We undertake no obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise.

| 1 |

PART I

| Item 1. | BUSINESS |

History

Gepco, Ltd. (“Gepco, Ltd.” or the “Company”) was incorporated on June 27, 2008 in the State of Nevada as Kensington Leasing, Ltd.

The Company’s initial business plan was to specialize in leasing equipment to a select clientele. Because it took longer than anticipated to launch the Company’s leasing business, the Company elected to investigate additional lines of business. The leasing business generated minimal revenues since inception and has been discontinued.

On June 4, 2010, the Company, through its newly formed wholly-owned subsidiary Allianex Corp., purchased substantially all of the assets of Allianex, LLC (the “Allianex acquisition”). The Company’s primary business after the Allianex acquisition until the acquisition of Wikifamilies SA, as discussed below, was the production, marketing and distribution of a retail line of prepaid stored value cards for the purchase of technology support and security services for electronic devices. Allianex Corp. generated nominal revenues since the acquisition and the assets were disposed of on December 22, 2011.

On May 20, 2011, the Company acquired all of the outstanding equity securities of Wikifamilies SA (the “Wikifamilies acquisition”), making Wikifamilies SA a wholly owned subsidiary of Kensington Leasing, Ltd. For accounting purposes, the Wikifamilies acquisition was treated as a reverse acquisition with Wikifamilies SA treated as the acquirer and Kensington Leasing, Ltd. as the acquired party. As a result, the business and financial information included in previous reports was the business and financial information of Wikifamilies SA prior to May 20, 2011 and the combined entity after May 20, 2011.

On October 27, 2011, the Company changed its name to Wikifamilies, Inc. through a short-form merger with its newly formed wholly owned subsidiary of the same name.

As of May 20, 2011, the Company’s business plan as Wikifamilies was to design, develop and operate an Internet-based social media website, Wikifamilies.com, with a unique emphasis on families and new technologies which web-based platform was intended to enhance the ability of families to communicate and share family history and events while providing a secure location to transact family-related business matters. Then, on September 7, 2012, our business plan changed to the development and marketing of an Internet search engine through the licensing from Clairnet, Ltd. of their process enabling online and mobile viewers to search, index, watch and personalize web-based videos while facilitating the monetizing of investments by video content providers, advertisers and marketers.

On September 7, 2012, Wikifamilies, Inc. entered into a Share Exchange Agreement with ClairNET Ltd., a Hong Kong entity and their shareholders by which all of the issued and outstanding shares of ClairNET were to be exchanged for 36,504,056 shares in Wikifamilies Inc, representing 75% of the company’s common stock. Additionally, ClairNET Ltd was to receive 2,500,000 shares of Voting Only Preferred Stock in Wikifamilies, with 100:1 voting rights. On the same date, the parties also signed a License Agreement by which Wikifamilies was to acquire exclusive global licensing rights to ClairNET’s products, with an end goal of ClairNET becoming a subsidiary of Wikifamilies, Inc.

On September 8, 2012 the Company and the founders of Wikifamilies SA entered into a Rescission Agreement, whereby the share consideration originally tendered by the corporation for the acquisition of the Wikifamilies SA assets, was rescinded by mutual agreement. This Rescission unwound the March 23, 2011, Exchange Agreement between Wikifamilies Inc. and Wikifamilies SA, and Wikifamilies SA agreed to return the remaining 26,925,000 shares to Wikifamilies treasury, being the full balance of the original 31,500,000 shares tendered as part of the original Exchange Agreement and the Company returned its interest in Wikifamilies SA to the Wikifamilies SA founders. The Wikifamilies SA founders retained all assets and liabilities of Wikifamilies SA. Additionally, Wikifamilies, Inc forgave the intercompany loans from Wikifamilies Inc. to Wikifamilies SA in full compensation for non-payment of salaries, fees and expenses to the founders.

On September 10, 2012 the full Board of Directors of the Company elected John Karlsson, Dan Clayton and Vincent Qi as Members of the Board of Directors.

On September 10, 2012, following the appointment of the new Board Members, Robert Coleridge, Chris Dengler, Steve Brown, William Hogan and Thomas Hudson resigned from their positions on the Board. Trisha Malone resigned her position as Board Member and Chief Financial Officer effective September 13, 2012, and Malcolm Hutchinson resigned his position as Board Member and Chief Executive Officer effective September 13, 2012.

| 2 |

The three members of the Board of Directors elected on September 10, 2012 changed the Company’s name in the State of Nevada to ClairNET, Ltd. but failed to complete the ClairNET, Ltd. merger, which left the Company with no operating entity, and failed to file any and all required filings with the Securities and Exchange Commission (the “SEC”), in effect abandoning the Company. After repeated attempts at contact with the Board of Directors with no response, certain creditors of the Company petitioned the Eighth Judicial District Court in Clark County Nevada to receive custodianship of the Company.

On April 8, 2013, the Eighth District Court of the State of Nevada appointed Trisha Malone as Custodian of Wikifamilies, Inc. pursuant to section 78.347 of the Nevada Revised Statutes, and authorized her to appoint a new Board of Directors, to continue the business of the Company, and to bring current the Company’s filings with the SEC. The appointment was made pursuant to a petition filed by Trisha Malone with the Court on February 27, 2013, to become Custodian of the Company due to former management’s malfeasance and nonfeasance in allowing the filings with the SEC to become delinquent, exposing the Company to potential revocation of registration proceedings under Section 12j of the Securities Exchange Act of 1934 and a potential trading suspension under Section 12k of the Securities Exchange Act, and in failing to maintain the business of the Company.

The Court also nullified the issuance of shares of Company Common Stock issued as a result of the Exchange Agreement entered into between the Company and Clairnet, Ltd., a Hong Kong corporation, dated September 7, 2012 and the Technology License Agreement between the Company and Clairnet, Ltd., a Hong Kong corporation. Among the nonfeasance of the prior management was the failure to effect the change of the Company's name from Wikifamilies, Inc. to Clairnet, Ltd. in the marketplace, by notification to FINRA. Prior to being known as Clairnet, Ltd., the Company was known as Wikifamilies, Inc., to reflect the business plan of operations of its foreign subsidiary, Wikifamilies, S.A. However, Wikifamilies, S.A. was returned to its founders by reason of a Rescission Agreement executed between the founders and the Company on September 8, 2012.

The Court further ordered that all stocks issued as a result of the September 7, 2012 Share Exchange Agreement between the Company and ClairNET Ltd., a Hong Kong entity and their shareholders, are declared null and void and ordered to be returned to the Company or its transfer agent for cancellation. The Court further ordered that the License Agreement between the Company and ClairNET, Ltd. a Hong Kong entity, is declared null and void.

Finally, the Court ordered the cancellation of an aggregate of 26,925,000 shares of Common Stock to effectuate the Company's September 8, 2012 Rescission agreement with the founders of Wikifamilies SA.

On April 9, 2013 the duly appointed Custodian of the Company appointed Trisha Malone and Larry A. Zielke as Members of the Board of Directors. Ms. Malone was also appointed as Chief Executive Officer, Chief Financial Officer and Secretary of the Company and Mr. Zielke was appointed Vice President and Corporate Counsel.

On August 27, 2013, the Company held a Special Meeting of Shareholders. At the Special Meeting, the Shareholders of the Company approved the change in the Corporation’s name from Wikifamilies, Inc. to Gepco, Ltd. On September 11, 2013, the Company filed an amendment to its Articles of Incorporation to, inter alia, change its name to Gepco, Ltd. from Clairnet, Ltd. (Wikifamilies, Inc.) In conjunction with the amendment, the Company filed with FINRA to change its name and ticker symbol. Effective October 8, 2013, the Company’s common stock, which was previously traded under the ticker symbol “WFAM” on the OTCQB market, began trading under the new ticker symbol “GEPC”.

| 3 |

On October 15, 2013, Gepco, Ltd. (the “Company”) entered into a Stock Purchase Agreement (the “Stock Purchase Agreement”) with GemVest, Ltd. pursuant to which the Company shall purchase (the “Acquisition”)100% of the issued and outstanding capital stock (“GemVest Shares”) of GemVest, Ltd., a Nevada corporation (“GemVest”). The purchase price for the Shares set forth therein is 150,000,000 shares of the Company’s restricted Common Stock.

The parties arrived at the purchase price as follows:The 10 day average closing price from September 30, 2013 through October 14, 2013 (the 10 trading days prior to signing the agreement) was $0.0326 which attaches a value of the 150,000,000 shares at $4,890,000.

Immediately prior to Closing (as defined below), the parties to the Stock Purchase Agreement and the stockholders of GemVest entered into an amendment to the Stock Purchase Agreement whereby the stockholders of GemVest affirmed all of the obligations and representations of GemVest under the Stock Purchase Agreement and agreed to convey 100% of the issued and outstanding GemVest Shares to the Company in consideration for the Purchased Company Shares in a transaction exempt from registration under Section 4(2) of the Securities Act of 1933.

The Acquisition was consummated (the “Closing”) on December 6, 2013, in a transaction exempt from registration under Section 4(2) of the Securities Act of 1933, as amended. Pursuant to the Stock Purchase Agreement, GemVest and the Company agreed to the following covenants regarding management of the Company for a period of five years from the date of Closing:

| · | Angelique de Maison shall serve as Executive Chairman of the Company and of GemVest, Peter Voutsas shall serve as Chief Executive Officer and Chief Investment Officer of the Company and of GemVest, Trisha Malone shall serve as President, Chief Financial Officer and Secretary of the Company and Chief Financial Officer, Chief Operating Officer and Secretary of GemVest, Nicholas Marlin shall serve as Chief Marketing Officer the Company and President and Chief Marketing Officer of GemVest and Ronald Loshin shall serve as Chief Creative Officer of the Company and of GemVest. |

| · | The Board of the Company shall consist of six directors: Angelique de Maison, Peter Voutsas, Trisha Malone, Larry Zielke, Ronald Loshin and Nicholas Marlin. The Board of GemVest shall consist of five directors: Angelique de Maison, Peter Voutsas, Trisha Malone, Ronald Loshin and Nicholas Marlin. |

| · | If the Company’s EBITDA (as defined in GAAP) is not at least $750,000 for the fiscal year ended December 31, 2014, then on a pro rata basis, based on percentage of ownership of Gepco immediately prior to Closing, the shareholders of Gepco shall return to the Company one million shares of the Company’s Common Stock for each $10,000 increment by which EBITDA is less than $750,000. |

Subsequent to closing of the Acquisition, GemVest became a wholly owned subsidiary of Gepco. For accounting purposes, GemVest is deemed the accounting acquirer.

Unless the context otherwise requires, references to the “Company” mean the Company and its subsidiary GemVest, Ltd. In the context of Common Stock, notes and other securities, references to the “Company” mean Gepco, Ltd. unless otherwise stated.

Business of Gepco, Ltd.

The Company’s business is now the business of GemVest. GemVest, Ltd. was incorporated on October 2, 2013 in the State of Nevada. GemVest is a start-up development stage company that has had no revenue or expenses since its inception. As the Company was a shell company prior to the acquisition of GemVest, GemVest is the acquirer for accounting purposes, and future financial reporting shall be set forth as if GemVest acquired the Company.

| 4 |

The Company intends to sell and broker high end rare investment grade diamonds that are obtained from wholesale diamond cutters all over the world with which our Chief Executive Officer, Peter Voutsas, has long, outstanding relationships and from individuals and estates seeking liquidity who possess investment grade diamonds and heirloom quality jewelry.

GemVest Business Description:

Peter Voutsas (“Peter”) has also established a worldwide reputation as a purveyor of exquisite, extraordinary fine quality precious stones and jewelry pieces that are retailed in an elegant but friendly environment and sold at competitively reasonable prices. Peter has an international clientele that includes individuals from every continent who are known to be seekers of investment grade stones and exquisite rare heirloom jewelry items. The placing of such exquisite jewelry and gemstones is one of Peter’s most noted talents and helps enable Peter to gain top dollar and quick turnover for virtually each such item.

Through Peter’s reputation and long standing close business ties to the diamond wholesale market, the Company will have direct access to acquiring an unsurpassed collection of the highest investment grade diamonds that are released each year on a wholesale basis. This enables the Company to wholesale these gems to investors, other jewelry retailers throughout the country, and to other wholesalers who need to supplement their own inventory at attractive margins with high turnover. Management anticipates that each wholesale diamond order will carry a ticket value of $300,000 to $5,000,000 and gross margins of approximately 30%-40% that can be expected from their sales with an average sales turn rate of 90-120 days.

Increasingly, Peter has taken advantage of his retail store’s location and his reputation for integrity, fairness, and expertise by becoming “the place to go” to dispose of precious diamonds and other investment grade stones and heirloom jewelry for those desiring to convert highly valued holdings into cash. Because of the high worth of some of these items, some valued in excess of $35 million, Peter has, until now, relied on taking such goods on a consignment basis and earning a modest consignment fee. This has restricted his earnings while impairing his serving his customers to the fullest extent because of their preference for immediate cash. GemVest plans to purchase such items outright, often at very discounted prices, providing the seller immediate cash and providing the Company with gross margins typically anywhere between 30%-70%.

Rare and highly valued precious stones and jewelry are normally sold within 90-120 days giving the Company 3-4 turns of inventory per year. The Company will hire certified gemologists to ensure that each diamond and gemstone is precisely categorized, given a proper serial number, and provided a proper documentation trail.

Overview of Investment Grade Diamonds

The allure of diamonds is, like gold, they are easily authenticated, eternal lasting and an excellent store of value and safe haven from inflation. Unlike gold or oil, diamonds have exhibited stable pricing and avoided the high price volatility and instability seen in other commodity based stores of value. To date, diamonds have not been touched very much by large inflows and outflows of speculative money. This could change if the new efforts succeed and large speculative inflows materialize into precious “investment grade” diamonds, as may well be underway. Gold investments, rather than jewelry, have long been the primary choice of investors looking for a commodity based asset that preserves value. Gold investments have become the primary driver of the price increase and corresponding growth in the gold industry, pushing annual production to record levels of around $205 billion in 2011 according to the World Gold Council. By comparison, the annual production of polished diamonds has remained modest is still only about $18 billion (source: Bain & Co.).

Furthermore, the sometimes need to sell high-end jewelry and precious stones for cash is an all but universal one. Once GemVest and Peter Voutsas demonstrate the “proof of concept” in the Beverly Hills store and extend the GemVest brand to the acquisition of landmark jewelry and precious stones for cash, we envision a roll out of this business into other major markets in the US and cities throughout the world that are known for their strong jewelry heritage. Those areas plagued by current economic hardships and instability that have a strong jewelry heritage are particularly attractive target markets for our growth.

| 5 |

GemVest has entered into an exclusive and perpetual agreement with Peter Voutsas for his services to develop and manage this business. All purchase and resale business by Peter Marco Jewelers will now be done under the GemVest name. We expect that the proof of concept and a corresponding codification of operating procedures and business practices will have been accomplished within the first six months of operations. Several highly visible appearances of Peter Marco jewelry in conjunction with the entertainment industry will be utilized as well to further enhance the branding and establish Peter as a celebrity to facilitate our rollout into other world center cities.

In addition to securing inventory for resale by purchasing investment grade estate items from individuals and estates, Peter Voutsas also has direct access to diamonds directly from diamond cutters located around the world. This direct source of mined diamonds is available to Peter and GemVest at deep wholesale prices which then enables GemVest to distribute the diamonds and gemstones to other jewelers and investors of investment grade diamonds and gemstones at competitive prices while still earning significant returns. This business too has vast opportunities for international expansion given the availability of sizeable capital that the GemVest venture will provide.

Primary Objectives

| · | To establish GemVest as an international branded investment diamond jewelry merchant business under the well-established Peter Marco Extraordinary Jewels of Beverly Hills, Rodeo Drive store front for the acquisitions of exclusive high end jewelry and investment grade precious stones that are acquired from individuals and estates and sold through private transactions to investors and consumers interested in obtaining such rare jewelry and precious stones. |

| · | To complete a proof of concept in demonstrating that the income and profit margins now present in the consignment based acquisition of merchandise and resale structure would be very significantly increased by a multitude of many times by converting to outright purchase and resale of “treasure chest” collector jewelry and other merchandise. To codify all procedures, risk management controls, advertising and merchandising, inventory controls, promotion, valuation and assessment, purchase and sales techniques, etc. so as to enable prudent but timely expansion into other primary domestic and international targeted cities that are noted for populations having exclusive luxury jewelry collections an appreciation for investment grade stones, and an ample number of estates and people seeking to liquidate such exclusive holdings and others who wish to purchase such treasure goods.* |

| · | To prepare a master national and international target city list, perform site reviews and selections and prepare for such future expansion inclusive of operating manuals, plans for executive recruitment and training, and an initial promotional and public relations campaign that would be used as we enter new markets. Expansion could then take place under GemVest’s direct ownership of satellite stores or, depending on the particular circumstances, through franchising with the “best in class” independent jewelers in selected cites who would operate under a franchise arrangement, inclusive of capital being provided for purchase of conforming merchandise. |

| · | To provide investors with a rare opportunity to participate in this extremely attractive high end of the jewelry and rare precious stone sectors with the prospects of high returns, relatively low risks, and exclusive entertainment event opportunities where Peter Marco jewelry is featured. |

| · | To establish the first international brand for the liquidation and purchase of rare and timeless treasured heirloom jewelry and precious stones. |

| · | Instill the highest level of cordiality and friendliness in customer service in what is an exclusive and elegant setting. |

_______________

* With the reach of the Peter Marco’s brand across the world, it is not essential that local markets have an active core of buyers. Such merchandise can be sold on the international market

| 6 |

Mission

| · | Make GemVest the most trusted, esteemed, and successful trader of pre-owned rare jewelry and precious stones in the international market. |

| · | Establish and implement an international highly recognizable brand known by the international elite for heirloom jewelry and high-end investment grade precious stones. |

| · | To identify additional business opportunities where access to capital, expert knowledge of rare jewelry and precious stones, and reputation are paramount to success. |

| · | Establish GemVest as the preferred place to purchase, sell and exchange investment grade precious stones and fine jewelry. |

| · | Establish a wholesale marketplace for investment grade diamonds that can be sold directly to jewelers, wholesalers, and pre-approved investors over the Internet. |

| · | To select an esteemed investment bank partner interested in pursuing the regulatory filing and sale of bundled $100MM investment grade diamonds to high net worth investors |

| · | To link with expert local jewelers through an Internet supported distribution system such that affiliate jewelers will be able to retail precious diamonds and other investment grade stones on their premises through Internet enabled displays and advanced secured distribution system. |

Keys to Success

Some of the key factors that will help GemVest expand its operations include:

| · | Timely access to capital and debt financing sufficient to support increasing capital requirements in order for GemVest to avail itself of expansion opportunities and respond to new business opportunities.† |

| · | Creating a world-class brand supported by retail storefronts for the acquisition and sale of legacy holdings. |

| · | Establishing proper risk and internal controls to assure that all assets are assessed correctly, properly secured and safeguarded to assure and protect inventory. |

| · | Establishing a high volume “Diamond Exchange” wholesale marketplace for investment grade diamonds. |

| · | Securing adequate umbrella insurance coverage to cover the purchase, sale, transportation of all high valued inventory. |

| · | Developing a customized website for promoting the Company’s business and evaluate whether it is desirable to make it transactional, such that sellers could submit detailed information about what they wish to sell to the Company (or, if we so choose to other prospect buyers as well) and buyers, be they limited to affiliate jewelers or to the public could submit offers on listed merchandise.‡ |

| · | Maintaining the highest business integrity such that all sellers and buyers can have comfort that they are being treated fairly and with the utmost of respect, that there is transparency, and that there is a consistency in practices across transactions. |

| · | Expanding our visibility and access to sellers of rare jewelry and precious stones such that we will be able to secure a sufficient volume of high worth artifacts to support the buyer base and business overhead. |

| · | Becoming more visible to diamond investors and speculators across the U.S. and globally and to the international investment banking community when we are ready for such relationships. |

| · | Identifying attractive locations in other US cities and worldwide for setting expansion priorities. |

| · | Improving our logistic/supply chain to enable quicker, secured deliveries and returns. |

| · | Developing a state of the art information system, inclusive of inventory data base, historical purchase and sale prices, number of days in inventory by item and category, any item specific special circumstances, seller and buyer and respective locations, demographics, product interests, etc. that will give us an added competitive advantage and improve our internal controls and IT. |

| · | Implementing a public relations and marketing program that will introduce and reinforce our branding. |

_______________

[†] We anticipate linking with an international investment bank that wishes to help develop a securitized asset backed portfolio of precious stones.

[‡] This could be restricted to invited parties, e.g., past clients.

| 7 |

Company Startup Summary

GemVest is now poised to purchase and resell investment grade diamonds, precious stones and heirloom top of the line jewelry on a volume basis from both the world’s top diamond mining companies and from individuals and estates seeking timely access to liquidity. Included in the company’s attributes are:

| · | A world-class acclaimed (prestigious) retail jewelry nameplate with an aura that connotes exclusivity and exquisiteness. We enter this field with an already very meaningful presence in Peter Voutsas, our CEO and Chief Investment Officer, and an experience and expertise that any new entrant could only wish for. |

| · | The CEO and Chief Investment Officer, Peter Voutsas, is an internationally renowned jeweler with a reputation for integrity, honesty, and high customer satisfaction. We will have the benefit of Peter’s experience, expertise and leadership from the very beginning of our enterprise. There is no need for a learning curve. We are expanding on proven business practices, principles and activities that have made Peter one of the most respected and successful independent jewelers in the world. Few businesses can ever start with such advantages out of the gate. |

| · | The Company is layering strong financial resources on top of proven business practices so that the present and past success can be magnified and most all the risks are very much minimized. |

| · | The access to rare gems including diamonds paves the way for an international expansion at an accelerated pace. |

| · | Few products, even other luxury goods makers, are so dependent on reputation as purveyors of luxury jewelry. This is perhaps even more important in the retail arena by our being able to attract owners of rare jewelry and precious stones by the feel of an absolute comfortable and cordial environment that customers experience inside a Peter Marcos store. |

| · | Start-up expenses are relatively modest since the first store front, the buying and selling infrastructure and business relationships to the world wholesale markets are already in place. In addition, the brand is already well established. Nor will there be need to expand current sales staffing until we start adding an Internet based sales channel and expanded beyond the Beverly Hills store. |

Products and Services

GemVest seeks to become a world-wide destination for the purchase and resale of rare investment grade precious stones and jewelry by focusing on becoming:

| · | An international wholesale of high end investment grade precious stones including featured diamonds that would be marketed directly to collectors, investors, other wholesalers who are looking to supplement their own inventory and that of individual jewelry stores operating in high end of local markets. |

| · | Heirloom and keepsake “collector and investor” grade diamond and other precious stone jewelry through the highest grade museum and collector pieces that will be marketed to an international clientele, high net worth shoppers, collectors, and investors. |

Market Segmentation

The diamond and jewelry distribution and sales industry is one of the United States’ most concentrated and exclusive industries characterized by a relatively small number of suppliers supplying diamonds to the entire market. As of the last economic census, there were approximately only 9,000 businesses that deal specifically with the sale of diamonds and jewelry on both a wholesale and retail level. Presumably, some of these did so in volumes that were virtually inconsequential. For each of the last five years, the industry has generated more than $54 billion dollars a year of revenue and has provided jobs to more than 70,000 people. Each year, approximately $7 billion dollars of payrolls are disbursed to these employees. Approximately half of the diamond distribution firms in the country are located in New York, California, and Texas.

| 8 |

Size of U.S. Diamond Market

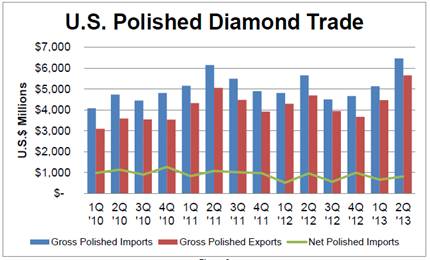

Reflecting its scarcity, by world trade standards, diamond trade is still a modest niche market. Polished diamond imports to the U.S. has risen from $4 billion in Q1 of 2010 to about $6.4 billion in Q1 of 2013 (see U.S. Polished Diamond Export - Import Volume, 2010Q1- 2013Q1 graph below). During this same period, U.S. exports rose from $3.1 billion to $5.6 billion, making us a net imported by about $0.75 billion a quarter.

* Source: U.S. Polished Diamond Export - Import Volume, 2010Q1-2013Q1:

Target Market Segment Strategy

As the Company does not intend to market its investment diamond inventories directly to the general public, the marketing campaign required to support this business is quite limited. Foremost, the Company must immediately expand its relationships with other i). diamond distributors, ii). jewelry retailers, and iii). jewelry manufacturers that will continuously supply the business with purchase orders. At the onset of operations, Mr. Voutsas intends to directly approach regional premium jewelry stores to become an ongoing major supplier of such premium stock diamonds. Additionally, the Company will implement an interactive online website for the wholesale sector so that the Company’s target market can easily locate the Company’s contact information and easily find information related to making bulk purchases. Once registered and approved (verified as a qualified customer or business (jeweler)), registered users will be given access to all current inventories of investor diamonds in inventory and available for immediate delivery. All such affiliate jewelers will also be given a special code whereby they can quickly access any diamond that have interest in and show it on their own WEB site through an Internet Link. All such displays by the affiliate jewelers will show their logo and name above such “reserved” diamonds, which makes for an impressive presentation to their customers. Planning for the Internet capability described above is already in the planning and development stage. The Company also plans to hire a specialist marketing firm to place the Company’s inventory in trade directories serving the jewelry industry. In addition, the Management of GemVest, will regularly attend industry events that will allow them to network among potential clients that will regularly purchase diamonds from the business. Mr. Voutsas will also attend selected Christies and Sotheby’s auctions to showcase the Company’s higher-end diamonds.

| 9 |

Currently, total annual diamond sales in the U.S. have reached $5.5 billion, out of total jewelry sales of an estimated $40 billion, which represents approximately 18% of total jewelry sales. This includes everything from engagement rings, anniversary jewelry, ornamental items, watches, etc. The Company’s opportunity is establishing itself as a source of exquisite investment grade diamonds that are desired for speculation and asset protection in addition to demand from consumers seeking exquisite, eye catching beauty.

The diamond market itself is fragmented and characterized mostly by vendors targeting "mass" market demand with ordinary diamonds. It is also highly seasonal with year-end gifts and purchases accounting for a very significant portion of annual sales. The market is divided into three echelons: premium end, middle end, and low end. Online diamond retail also has different categories, parallel to the brick-and-mortar stores. BlueNile is typical of the upper-echelon vendors for high-end online diamonds, while Best Gem targets mostly middle end customers.

GemVest will target only in the upper echelon of high quality diamonds, with an average sale expected to be in the hundreds of thousands of dollars. The Company’s initial target is the top 25% of the diamond market, including the top ten percent of upper-echelon buyers. First year sales volume is targeted at $15-45 million.

Technology

GemVest intends to build a state of the art custom website that enables the Company to conduct e-commerce throughout the world. We will utilize existing technology solutions when appropriate and efficient and, when necessary, invest in developing proprietary software to support our business. GemVest will invest in the creation of an Internet platform for attracting both collectors and investors in fine jewelry and investment grade stones for purchase. We wish to establish a platform that offers fair prices, immediate cash, and great convenience and confidentiality. The website will emphasize these features and allow sellers to receive a binding quote subject to all descriptions and ratings of gems being verified at time of receipt. In addition to supporting this commerce, the site will also promote our brand.

In addition, the business will seek or build an overall CRM solution for overseeing and managing satellite locations, available inventories, evaluating performances on a live basis, and live consolidation of results.

Competitive Edge

GemVest shall utilize its Management who are highly skilled at purchasing diamonds and have longstanding relationships with wholesale sources for investment grade diamonds at between 40% and 70% discounts to Rapaport Prices through its well established trade connections. Discount levels for select qualities of diamonds vary rather significantly and are based on a broad range of factors including the specific physical and technical characteristics of a particular diamond, type of market, location, state of market liquidity, and terms of sale. GemVest will have the benefit of robust funding which will enable the Company to become a repeat buyer of the highest grade precious diamonds and sustain a comprehensive and diverse inventory, sell, through the Rapaport Exchange supplemented by sales to trade sources in the wholesale exchange. With normal turnover, we expect to be able to turnover inventory at 3 to 4 times per year.

Marketing Strategy

GemVest’s Management has extensive, pre-existing relationships with jewelers and industry participants and will extend those relationships electronically through networks like RapNet. The BUY-SIDE will focus on finding distressed sales of estate jewelry and pawnshop situations. The SELL-SIDE will attempt to attain full prices or near full prices as quoted on the Rapaport Price List. Spreads of 30% and higher are quite common under this strategy.

Employees

The Company has five part-time consultants. Our employees consist of Mr. Voutsas who serves as the Chief Executive Officer and Chief Investment Officer of Gepco, Ltd. and GemVest, Ltd.; Ms. Malone who serves as President, Chief Financial Officer and Secretary of Gepco, Ltd. and as the Chief Operating Officer, Chief Financial Officer and Secretary of GemVest, Ltd.; Mr. Marlin who serves as the Chief Marketing Officer of Gepco, Ltd. and the President and Chief Marketing Officer of GemVest, Ltd., Mr. Loshin who serves as Chief Creative Officer of Gepco, Ltd. and GemVest, Ltd. and Mr. Zielke who serves as Vice President and Corporate Counsel of Gepco Ltd., all of whom provide services to us on a part-time basis.

To the best of its knowledge, the Company is compliant with local prevailing wage, contractor licensing and insurance regulations, and has good relations with its employees.

| 10 |

| Item1A. | RISK FACTORS |

An investment in the Company’s common stock involves a high degree of risk. In determining whether to purchase the Company’s common stock, an investor should carefully consider all of the material risks described below, together with the other information contained in this report before making a decision to purchase the Company’s securities. An investor should only purchase the Company’s securities if he or she can afford to suffer the loss of his or her entire investment.

Risks Related to our Business

A decline in the price of diamonds could adversely affect the market price of our stocks, and our financial results and condition, may in the future be materially adversely affected by declines in the price of rough and polished diamonds.

As prices decline, this may prove to be a less attractive commodity to our investors thus decreasing demand and lowering the market price for our diamonds. If we have diamonds for which we have paid a higher price, and the market declines, we may be forced to sell at a lower price than expected, thus decreasing our profit margin or forcing us to less at a price less than the price which we paid for inventory.

Due to the international nature of the diamond industry, we bear significant foreign currency risk.

The diamond market is international with pricing generally determined by large participants in the global diamond trading centers and exchanges, which prices may be denominated in foreign currency. Thus if purchases are denominated in foreign currency, thus we will become exposed to foreign currency fluctuations relative to the U.S. dollar which may affect our financial results.

Because our auditors have issued a going concern opinion, there is substantial uncertainty we will continue operations in which case you could lose your investment.

Our auditors have issued a going concern opinion. This means that there is substantial doubt that we can continue as an ongoing business for the next twelve months. The financial statements do not include any adjustments that might result from the uncertainty about our ability to continue in business. As such we may have to cease operations and you could lose your investment. Further, we have not considered and will not consider any activity beyond our current exploration program until we have completed our exploration program.

Because we may still not have sufficient capital to fund our business plan, we may have to sell additional securities and raise additional capital which could dilute your investment.

We may not have the capital to fund our business plan. As a result we may have to raise additional capital to maintain operations. There is no assurance that we will be able to secure enough capital to maintain operations and if we cannot raise the capital needed we may have to suspend operations.

We have no operating history upon which an evaluation of our prospects can be made.

We have had no operations in the diamond industry since our inception upon which to evaluate our business prospects. As a result, investors do not have access to the same type of information in assessing their proposed investment as would be available to purchasers in a company with a history of prior substantial operations. We face all the risks inherent in an early stage business, including the expenses, lack of adequate capital and other resources, difficulties, complications and delays frequently encountered in connection with conducting operations, including capital requirements and management’s potential underestimation of initial and ongoing costs. We also face the risk that we may not be able to effectively implement our business plan. If we are not effective in addressing these risks, we will not operate profitably and we may not have adequate working capital to meet our obligations as they become due.

| 11 |

We may be unable to successfully execute any of our identified business opportunities or other business opportunities that we determine to pursue.

We currently have a limited corporate infrastructure. In order to pursue business opportunities, we will need to continue to build our infrastructure and operational capabilities. Our ability to do any of these successfully could be affected by any one or more of the following factors:

| · | our ability to raise substantial additional capital to fund the implementation of our business plan; |

| · | our ability to execute our business strategy; |

| · | the ability of our products to achieve market acceptance; |

| · | our ability to manage the expansion of our operations and any acquisitions we may make, which could result in increased costs; |

| · | our ability to attract and retain qualified personnel; |

| · | our ability to manage our third party relationships effectively; and |

| · | our ability to accurately predict and respond to the rapid changes in our industry and the evolving demands of the markets we serve. |

Our failure to adequately address any one or more of the above factors could have a significant impact on our ability to implement our business plan with respect to marketing and selling our nutritional supplement products and our ability to pursue any related opportunities that arise.

We have a history since inception of losses, and we may not be able to cover our costs of operation or achieve profitability in the future.

For the year ended December 31, 2013, Gepco, Ltd. incurred net losses of $23,107. There can be no assurances that we will generate sufficient revenues in the future to cover our costs of operation or that we will be profitable. If we cannot cover our costs of operation, either through profits or otherwise securing sufficient capital to fund our costs of operation, it would be very unlikely that we would achieve profitability, and we may be required to cease our operations.

We may not be able to effectively control and manage our proposed business plan, which would negatively impact our operations.

If our business and markets grow and develop (and there are there are no assurances what growth and development will occur, if any), it will be necessary for us to finance and manage expansion in an orderly fashion. We may face challenges in managing expanding product offerings and in integrating any acquired businesses with our own. Such occurrences will increase demands on our existing management, workforce and facilities. Failure to satisfy increased demands could interrupt or adversely affect our operations and cause administrative inefficiencies.

Economic declines may have a material adverse effect on our sales, and a slow recovery could prevent us from achieving our financial goals.

We cannot predict the extent to which economic conditions will change and many economists predict that the economic decline will be prolonged, that any recovery may be weak, and that conditions may deteriorate further before there is any improvement or even after some improvement has occurred. Continuing weak economic conditions in the United States or abroad as a result of the current global economic downturn, lower consumer spending (especially discretionary items), lower consumer confidence, continued high or higher levels of unemployment, higher inflation or even deflation, higher commodity prices, such as the price of oil, political conditions, natural disaster, labor strikes or other factors could negatively impact our sales or ability to achieve profitability.

| 12 |

Natural disasters, armed hostilities, terrorism, labor strikes or public health issues could have a material adverse effect on our business.

Armed hostilities, terrorism, natural disasters, or public health issues, whether in the United States or abroad could cause damage and disruption to our company, our suppliers, our manufacturers, or our customers or could create political or economic instability, any of which could have a material adverse impact on our business. Although it is impossible to predict the consequences of any such events, they could result in a decrease in demand for our product or create delay or inefficiencies in our supply chain by making it difficult or impossible for us to deliver products to our customers, or for our manufacturers to deliver products to us, or suppliers to provide component parts.

We rely on key personnel and, if we are unable to retain or motivate key personnel or hire qualified personnel, we may not be able to grow effectively.

Our success depends in large part upon the abilities and continued service of Peter Voutsas, our chief executive officer. There can be no assurance that we will be able to retain the services of Peter Voutsas. Our failure to retain the services of our key personnel could have a material adverse effect on the Company. In order to support our projected growth, we will be required to effectively recruit, hire, train and retain additional qualified management personnel. Our inability to attract and retain the necessary personnel could have a material adverse effect on the Company.

Risks Related to the Company’s Common Stock

There is not an active liquid trading market for the Company’s common stock.

The Company files reports under the Securities Exchange Act of 1934, as amended, and its common stock is eligible for quotation on the OTCQB. However, there is no regular active trading market in the Company’s common stock, and we cannot give an assurance that an active trading market will develop. If an active market for the Company’s common stock develops, there is a significant risk that the Company’s stock price may fluctuate dramatically in the future in response to any of the following factors, some of which are beyond our control:

| · | variations in our quarterly operating results; |

| · | announcements that our revenue or income are below analysts’ expectations; |

| · | general economic slowdowns; |

| · | sales of large blocks of the Company’s common stock; |

| · | announcements by us or our competitors of significant contracts, acquisitions, strategic partnerships, joint ventures or capital commitments; and |

| · | fluctuations in stock market prices and volumes, which are particularly common among highly volatile securities of early stage technology companies. |

The ownership of our common stock is highly concentrated among a few shareholders.

Our executive officers and directors currently beneficially own approximately 151,319,548 shares of our outstanding common stock (68.39%). As a result, they have the ability to exercise control over our business by, among other items, their voting power with respect to the election of directors and all other matters requiring action by stockholders. Such concentration of share ownership may have the effect of discouraging, delaying or preventing, among other items, a change in control of the Company.

| 13 |

The Company’s common stock will be subject to the “penny stock” rules of the SEC, which may make it more difficult for stockholders to sell the Company’s common stock.

The Securities and Exchange Commission has adopted Rule 15g-9 which establishes the definition of a "penny stock," for the purposes relevant to us, as any equity security that has a market price of less than $5.00 per share or with an exercise price of less than $5.00 per share, subject to certain exceptions. For any transaction involving a penny stock, unless exempt, the rules require:

| · | that a broker or dealer approve a person's account for transactions in penny stocks; and |

| · | the broker or dealer receive from the investor a written agreement to the transaction, setting forth the identity and quantity of the penny stock to be purchased. |

In order to approve a person's account for transactions in penny stocks, the broker or dealer must:

| · | obtain financial information and investment experience objectives of the person; and |

| · | make a reasonable determination that the transactions in penny stocks are suitable for that person and the person has sufficient knowledge and experience in financial matters to be capable of evaluating the risks of transactions in penny stocks. |

The broker or dealer must also deliver, prior to any transaction in a penny stock, a disclosure schedule prescribed by the Commission relating to the penny stock market, which, in highlight form:

| · | sets forth the basis on which the broker or dealer made the suitability determination; and |

| · | that the broker or dealer received a signed, written agreement from the investor prior to the transaction. |

Disclosure also has to be made about the risks of investing in penny stocks in both public offerings and in secondary trading and about the commissions payable to both the broker-dealer and the registered representative, current quotations for the securities and the rights and remedies available to an investor in cases of fraud in penny stock transactions. Finally, monthly statements have to be sent disclosing recent price information for the penny stock held in the account and information on the limited market in penny stocks.

The regulations applicable to penny stocks may severely affect the market liquidity for the Company’s common stock and could limit an investor’s ability to sell the Company’s common stock in the secondary market.

As an issuer of “penny stock,” the protection provided by the federal securities laws relating to forward-looking statements does not apply to the Company.

Although federal securities laws provide a safe harbor for forward-looking statements made by a public company that files reports under the federal securities laws, this safe harbor is not available to issuers of penny stocks. As a result, the Company will not have the benefit of this safe harbor protection in the event of any legal action based upon a claim that the material provided by the Company contained a material misstatement of fact or was misleading in any material respect because of the Company’s failure to include any statements necessary to make the statements not misleading. Such an action could hurt our financial condition.

The Company has not paid dividends in the past and does not expect to pay dividends in the foreseeable future. Any return on investment may be limited to the value of the Company’s common stock.

No cash dividends have been paid on the Company’s common stock. We expect that any income received from operations will be devoted to our future operations and growth. The Company does not expect to pay cash dividends in the near future. Payment of dividends would depend upon our profitability at the time, cash available for those dividends, and other factors as the Company’s board of directors may consider relevant. If the Company does not pay dividends, the Company’s common stock may be less valuable because a return on an investor’s investment will only occur if the Company’s stock price appreciates.

| 14 |

| Item 1B. | UNRESOLVED STAFF COMMENTS |

Not Applicable.

| Item2. | PROPERTIES |

Gepco, Ltd. has use of an administrative office in San Diego, CA, that is provided to us without charge by our President, Chief Financial Officer and Secretary.

GemVest has use of retail space in Beverly Hills, CA that is provided without charge by our Chief Executive Officer and Chief Investment Officer.

| Item 3. | LEGAL PROCEEDINGS |

On April 8, 2013, former Chief Financial Officer and Director and present shareholder Trisha Malone was appointed as Custodian of the Company, by the Eighth Judicial District Court of Clark County, Nevada, pursuant to Nevada Revised Statutes 78.347. The Court further ordered that Ms. Malone is authorized to appoint new officers and directors of the Company, to send notice to all stockholders of record noticing a meeting of shareholders, to pay all fees owed to the SEC and to bring current all the Company's SEC filings.

The Court further ordered that all stocks issued as a result of the September 7, 2012 Share Exchange Agreement between the Company and ClairNET Ltd., a Hong Kong entity and their shareholders, are declared null and void and ordered to be returned to the Company or its transfer agent for cancellation. The Court further ordered that the License Agreement between the Company and ClairNET, Ltd. a Hong Kong entity, is declared null and void.

Finally, the Court ordered the cancellation of an aggregate of 26,925,000 shares of Common Stock to effectuate the Company's September 8, 2012 Rescission agreement with the founders of Wikifamilies SA.

| Item4. | Mining and Safety Disclosures. |

Not applicable.

| 15 |

PART II

| Item5. | MARKET FOR THE REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Our common stock has traded on the OTCQB under the symbol “KNSL”sinceAugust 17, 2009, under the ticker symbol “WFAM” since December 20, 2011 and under the symbol “GEPC” since October 8, 2013. The OTCQB is a regulated quotation service that displays real-time quotes, last-sale prices and volume information in over-the-counter equity securities. The OTCQB securities are traded by a community of market makers that enter quotes and trade reports. Over-the-counter market quotations reflect inter-dealer prices, without retail mark-up, mark-down or commission and may not necessarily represent actual transactions. This market is extremely limited and any prices quoted may not be a reliable indication of the value of our common stock. Furthermore, the trading volume of our securities fluctuates and may be limited during certain periods. As a result of these volume fluctuations, the liquidity of an investment in our securities may be adversely affected. The following table sets forth the high and low sale prices per share of our common stock for the periods indicated as reported on the OTCQB. As of March 26, 2014, the closing-sale price for our common stock was $0.238per share.

| Common Stock | |||

| High | Low | ||

| 2014: | |||

| First Quarter (through March 26, 2014) | $0.29 | $0.07 | |

| 2013: | |||

| Fourth Quarter | $0.09 | $0.02 | |

| Third Quarter | $0.042 | $0.01 | |

| Second Quarter | $0.0675 | $0.005 | |

| First Quarter | $0.0289 | $0.012 | |

| 2012: | |||

| Fourth Quarter | $0.084 | $0.01 | |

| Third Quarter | $0.105 | $0.02 | |

| Second Quarter | $0.26 | $0.08 | |

| First Quarter | $0.59 | $0.1281 | |

| 2011: | |||

| Fourth Quarter | $0.99 | $0.11 | |

| Third Quarter | $2.40 | $0.51 | |

| Second Quarter | $3.24 | $1.05 | |

| First Quarter | $4.00 | $2.50 | |

Holders

As of March 26, 2014, there were 221,252,555 shares of common stock outstanding held by approximately 205 holders of record.

Dividends

Our Board of Directors has not declared a dividend on our Common Stock since inception and we do not anticipate the payments of dividends in the near future, as we intend to reinvest our profits to grow our business.

Equity Compensation Plans

We have no equity compensation plans as defined under Item 402 of Regulation S-K.

Recent Sales of Unregistered Securities

On October 15, 2013, the Company entered into a Stock Purchase Agreement with GemVest, Ltd. which was consummated on December 6, 2013 pursuant to which the Company purchased 100% of the issued and outstanding capital stock of GemVest, Ltd., for 150,000,000 shares of the Company’s restricted Common Stock.

These issuances were effected without registration under the Securities Act of 1933, as amended, in reliance on the exemption from registration contained in Section 4(2) of the Securities Act of 1933, as amended, and/or Regulation D there under. The shareholders of GemVest, Ltd. are accredited investors, no general solicitation or advertising was used in connection with the sale of the shares, and the Company has imposed appropriate limitations on resales. There was no underwriter involved in these sales.

| Item6. | SELECTED FINANCIAL DATA |

Not Applicable.

| 16 |

| Item 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

The following discussion of our financial condition and results of operations should be read in conjunction with the financial statements and related notes to the financial statements included elsewhere in this Annual Report on Form 10-K.

For a discussion of our financial statements prior to the Acquisition, see our financial statements and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” contained in our Annual Report on Form 10-K for the year ended December 31, 2012 and our Quarterly Reports on Form 10-Q for the quarters ended March 31, 2013, June 30, 2013, and September 30, 2013. Until the Acquisition, we had conducted only nominal business operations.

Forward Looking Statements

This discussion and the accompanying financial statements (including the notes thereto) may contain “forward-looking statements” that relate to future events or our future financial performance, which are made pursuant to the safe harbor provisions of the Exchange Act. The forward-looking statements are based on the Company’s current expectations and beliefs concerning future developments and their potential effects on the Company. These statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements. These risks and other factors include, among others, those contained elsewhere in this Annual Report on Form 10-K. The Company undertakes no obligation to publicly update any forward-looking statements.

Overview

GemVest, Ltd. was incorporated on October 2, 2013 in the State of Nevada. GemVest is a start-up development stage company that has had no revenue and limited expenses from its inception through December 31, 2013.

The Company intends to sell and broker high end rare investment grade diamonds that are obtained from wholesale diamond cutters all over the world with which our Chief Executive Officer, Peter Voutsas, has long, outstanding relationships and from individuals and estates seeking liquidity who possess investment grade diamonds and heirloom quality jewelry.

As the Company was a shell company prior to the acquisition of GemVest, GemVest is the acquiror for accounting purposes, and future financial reporting shall be set forth as if GemVest acquired the Company.

Critical Accounting Policies and Estimates.

Basis of Presentation

The accompanying financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America.

Revenue Recognition

Revenue is recognized net of indirect taxes, rebates and trade discounts and consists primarily of the sale of products, and services rendered.

Revenue is recognized in accordance with Accounting Standards Codification Topic No. 605-10-S99 “Revenue Recognition” (ASC 605-10-S99) when the following criteria are met:

| · | evidence of an arrangement exists; |

| · | delivery has occurred or services have been rendered and the significant risks and rewards of ownership have been transferred to the purchaser; |

| · | transaction costs can be reliably measured; |

| · | the selling price is fixed or determinable; and |

| · | collectability is reasonably assured. |

| 17 |

Estimates

The presentation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from these estimates.

Fair Value of Financial Instruments

The carrying amounts for the Company’s cash, investments, accounts payable, accrued liabilities and current portion of long term debt approximate fair value due to the short-term maturity of these instruments.

Results of Operations

GemVest is a development stage company that has had no revenue or expenses since its inception. Gepco has incurred expenses required to operate as a publicly reporting company. There is no comparative financial information available due to the fact the company was organized in October 2013 and had not yet commenced significant operations as of December 31, 2013.

Revenues

There were no revenues from October 2, 2013 (inception) through December 31, 2013. We expect revenues for 2014 to grow as we begin to implement our business plan. The rate at which our revenues will increase will depend on how quickly we can begin sales and the amount of sales generated.

Operating Expenses

Sales, General and Administrative expenses from October 2, 2013 (inception) through December 31, 2013 were $1,772. Legal and accounting expenses from October 2, 2013 (inception) through December 31, 2013 were $13,523. We expect selling, general and administrative and legal and accounting expenses for 2014 to trend significantly upward as we begin to bring in additional sales and marketing personnel necessary to grow our business and to service the significant demand we expect for our products and services.

Other Income/(Expense)

Other expense from October 2, 2013 (inception) through December 31, 2013 was $7,812 which consisted of interest expense on convertible notes payable and amortization of debt discount related to these convertible notes. We expect interest expense for 2014 to increase as the expenses from October 2, 2013 (inception) through December 31, 2013 reflected only the period post Closing of the Acquisition. We will continue to incur interest expense and debt discount amortization until the convertible notes payable are paid or converted in full.

Net Income (Loss)

We are a development stage company that has had no revenue and limited expenses since its inception and therefore a minimal net loss of $23,107.

Financial Condition, Liquidity and Capital Resources

We are a development stage company that has had no revenue and limited expenses since its inception.

Future Financing

We plan to rely on equity sales of our common shares and the sale of secured notes in order to fund our business operations. Issuances of additional shares will result in dilution to existing stockholders. There is no assurance that we will achieve any additional sales of the equity securities or arrange for debt or other financing to fund planned acquisitions, expansions and exploration activities or if we are able to secure additional financing, whether such financing shall be on favorable terms.

| 18 |

Off-Balance Sheet Arrangements

As of December 31, 2013, the Company did not have any off-balance sheet debt nor did it have any transactions, arrangements, obligations (including contingent obligations) or other relationships with any unconsolidated entities or other persons that have or are reasonably likely to have a material current or future effect on financial condition, changes in financial condition, results of operations, liquidity, capital expenditures, capital resources, or significant components of revenue or expenses material to investors.

| Item 7A. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK |

Not Applicable.

| Item8. | FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA |

Our financial statements, notes thereto and related reports are included in this Annual Report on Form 10K beginning on page F-1 and are included herein by reference.

| Item 9. | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE |

(a) Previous independent auditor

On March 3, 2014, we dismissed M&K CPAS, PLLC (“M&K”) as our independent auditor. This dismissal of M&K was approved by our board of directors (we do not have an audit committee).

M&K's reports on our consolidated financial statements for each of our fiscal years ended December 31, 2011 and December 31, 2012 did not contain an adverse opinion or disclaimer of opinion, nor were they qualified or modified as to uncertainty, audit scope or accounting principles, except that each of such reports contained a going concern qualification.

In connection with the audits of our financial statements for the years ended December 31, 2011 and December 31, 2012 and the subsequent interim period through March 3, 2014: (i) there were no disagreements between our company and M&K on any matter of accounting principles or practices, financial statement disclosure, or auditing scope or procedure, which disagreements, if not resolved to M&K’s satisfaction, would have caused M&K to make reference to the subject matter of the disagreement in connection with its report for such years; and (ii) M&K did not advise us of any of the events requiring reporting in this Current Report on Form 8-K under Item 304(a)(1)(v) of Regulation S-K.

We provided M&K with a copy of the disclosures made in this report before this report was filed with the Securities and Exchange Commission. We requested that M&K furnish a letter addressed to the Securities and Exchange Commission stating whether or not it agrees with the above statements that are related to M&K. Their letter is attached to this filing as Exhibit 16.

(b) New independent auditor

As of February 24, 2014 we have engaged De Joya Griffith & Company, LLC (“De Joya Griffith”) to serve as our independent auditors for the fiscal years ending December 31, 2013 and December 31, 2014. The engagement of De Joya Griffith was approved by our board of directors on March 3, 2014.

For the years ended December 31, 2012 and December 31, 2013 and the subsequent interim period through February 24, 2014 neither we nor anyone acting on our behalf consulted De Joya Griffith regarding either (i) the application of accounting principles to a specific, completed or proposed transaction, or the type of audit opinion that might be rendered on our financial statements, or (ii) any matter that was either the subject of a disagreement (as defined in Item 304(a)(1)(iv) of Regulation S-K and the related instructions to Item 304 of Regulation S-K) or a reportable event (as defined in Item 304(a)(1)(v) of Regulation S-K).

| 19 |

| Item9A. | CONTROLS AND PROCEDURES |

Evaluation of Disclosure Controls and Procedures

As required by Rule 13a-15 under the Exchange Act, the Company carried out an evaluation under the supervision and with the participation of the Company’s management, including the Chief Executive Officer and Chief Financial Officer, of the effectiveness of the Company’s disclosure controls and procedures as of December 31, 2013. In designing and evaluating the Company’s disclosure controls and procedures, the Company recognizes that there are inherent limitations to the effectiveness of any system of disclosure controls and procedures, including the possibility of human error and the circumvention or overriding of the controls and procedures. Accordingly, even effective disclosure controls and procedures can only provide reasonable assurance of achieving their desired control objectives. Additionally, in evaluating and implementing possible controls and procedures, the Company’s management was required to apply its reasonable judgment. Based upon the required evaluation, the Chief Executive Officer and Chief Financial Officer concluded that as of December 31, 2013, the Company has determined that its system of controls and procedures are not effective to ensure that information required to be disclosed by the Company in the reports it files or submits under the Exchange Act is recorded, processed, summarized and reported within the time periods specified in the SEC’s rules and forms. The Company’s management intends to address the material weaknesses in its disclosure controls and procedures as soon as possible.

Management’s Annual Report on Internal Control Over Financial Reporting

Our management is responsible for establishing and maintaining adequate internal control over financial reporting, as defined in Rule 15d-15(f) under the Exchange Act, and for assessing the effectiveness of internal control over financial reporting.

Internal control over financial reporting is intended to provide reasonable assurance regarding the reliability of our financial reporting and the preparation of financial statements for external purposes in accordance with accounting principles generally accepted in the United States. Internal control over financial reporting includes those policies and procedures that (1) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of our assets, (2) provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with accounting principles generally accepted in the United States and that our receipts and expenditures are being made only in accordance with authorizations of our management and directors, and (3) provide reasonable assurance regarding prevention or timely detection of unauthorized acquisitions, use, or disposition of our assets that could have a material effect on our financial statements.